skycargo.com

Ram C Menen Divisional Senior Vice President Cargo

22ND February 2011Nairobi

Air Cargo In Emerging Africa

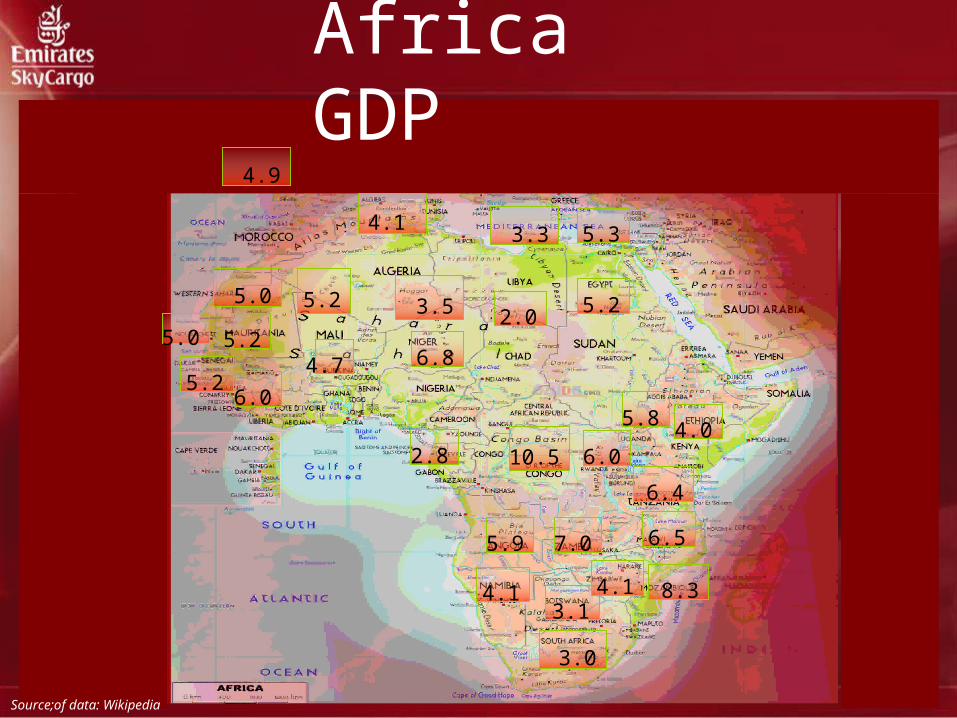

Africa TradeRepresentation of extremes –

dominated by diverse natural resources

• Agricultural products (flowers, fruits & vegetables) & seafood (fresh fish) are the trade mainstay for most developing countries

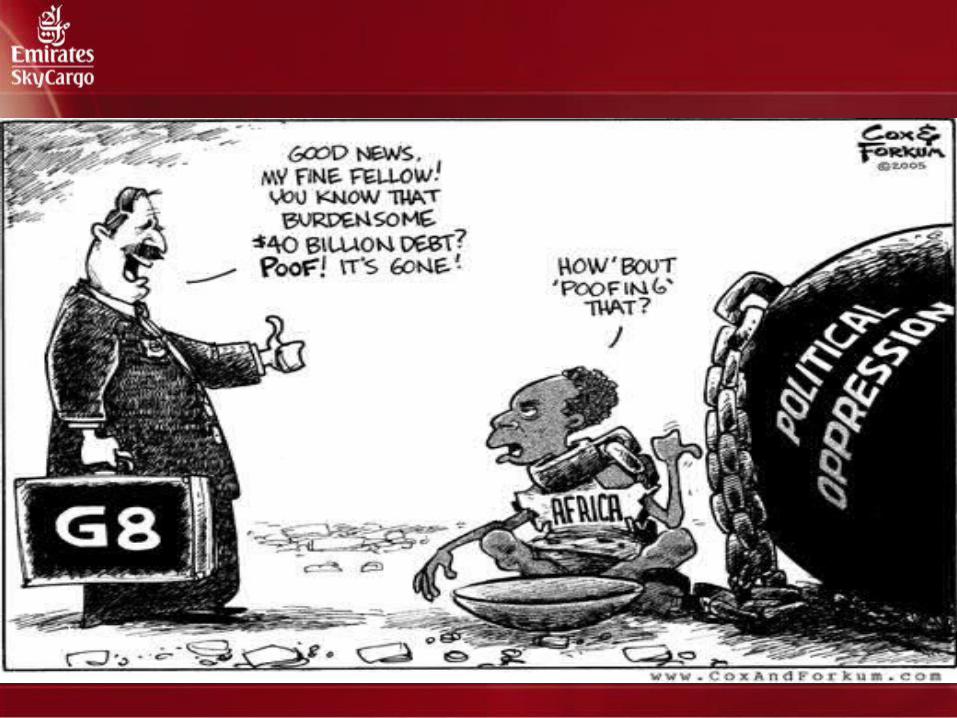

• Majority of African countries are underdeveloped and rely heavily on foreign aids to survive

• Trade varies from one country to another (Countries such as South Africa represent the higher side of the spectrum

whereas regions such as Burundi have the least trade volumes)

4.1

5.0 5.2

4.9

3.3 5.3

3.5 5.22.0

6.84.75.2

5.2

2.8 10.5

5.84.0

6.4

5.9 7.0

8.3

3.0

3.14.1 4.1

6.5

5.0

6.0

6.0

Africa GDP

Source;of data: Wikipedia

East Africa

Main Countries

• Kenya, Ethiopia, Tanzania & Uganda are the countries with tremendous air cargo potential.

Main Products• Exports of horticultural products dominate in this region. • Kenya (meat, fish, flowers, fruits), Ethiopia (flowers)

Uganda (fish, fruits & flowers).• Imports tend to be more of infrastructure development equipment

Positives

• Continued infrastructure development, especially in the field of agriculture and telecom , is providing a good growth environment

Challenges

• Poor RFS Infrastructure.

• Goods (perishables) are trucked from rural areas in open trucks exposing items to spoilage & adding delivery timing risks.

West AfricaMain Countries

• Nigeria, Ghana, Guinea, Senegal, Mauritania and Mali

predominantly all have high imports.

Main Products

• Imports - Nigeria (oil & drilling equipment), Ivory Coast (mining).

• Exports - Ghana (fruits), Senegal & Mauritania (fish).

Positives

• Investment in African resources sector covering varied mining projects along with oil & gas exploration/excavation has led to booming trade & air cargo opportunities.

Challenges

• Port inefficiency & congestion at West African ports are opportunities for air cargo.

• Poor RFS infrastructure mainly in land locked Mauritania & Mali.

• Volatile nature of West African politics/unrest in Cote d’Ivoire.

• Insecurity & pilferage at West African airports.

North AfricaMain Countries

• Egypt, Libya, Morocco, Tunisia & Algeria

predominantly all have high imports.

Main Products• Morocco / Egypt/ Tunisia have fresh produce exports and Egypt

remains the biggest exporter of fruits/vegetables.

Positives• Northern African countries, Europe’s principal trading partners,

maintain strong economic ties with EU, fueling trade demand.• Good RFS infrastructure & development.

Challenges• Security and embargo have adversely affected countries like Libya and

Algiers. • Air trade often competes with slower but price competitive surface

transport modes.• Political unrest & regulatory issues are a constraint/barrier to air cargo

growth.

Southern AfricaMain Countries

• Angola, South Africa, Namibia, Botswana and Zambia.

• South Africa functions as a manufacturing & trading hub for the entire African continent.

• Southern African trade is dominated by Botswana and South Africa, who are the two biggest exporting countries in Africa.

Main Products

• South Africa is the world’s biggest producer of gold/diamonds & has a healthy product cargo mix from machinery to perishables.

• Namibia (Fish), Mozambique & Madagascar (Fruits).

Positives

• Most of Southern Africa have a large pool of skilled labour, advanced infrastructure and developed financial resources.

• Good RFS infrastructure & development.

Challenges

• Security although improved is still an area of concern.

Central AfricaMain Countries

• Chad, Cameroon, Central African Republic (CAR).

Main Products• Limited export opportunities… imports include large volumes of

food, textiles, petroleum products, machinery, electrical equipment, motor vehicles, chemicals & pharmaceuticals via air.

Positives• Increasing demand for consumer goods and household items

Challenges• Important constraints to economic development include the

CAR's landlocked position, a poor transportation system, a largely unskilled work force & a legacy of misdirected macroeconomic policies.

• Factional fighting between the government and its opponents remains a drag on economic revitalization.

The Forecast Is Bright

Source; Boeing WACF 2010-11

Intra-Africa

• Poor road infrastructure coupled with safety and security of cargo mean that it is probably faster/cheaper to use air to inland destinations

• Air cargo is often the most secure and reliable mode in domestic Africa especially to land-locked countries.

• Physical infrastructure• Reduction of FDI due to political instability• Inadequate transportation networks• Lack of government transparency• Administrative & regulatory constraints• Lack of security• Lack of skilled labour & business knowledge• Out-dated technology

Challenges

Africa Economic Outlook

•Fertile ground for new investment and business development

•GDP Growth averaged 4.9% (2004-2009) due to:

– Strong commodity prices– Higher Asian interest (in terms of trade

and investment)– FDI - rising external inflows, both in terms

of capital and investment. – Rising fiscal spending

• These challenges can all be positives

• The legacy is going to be replaced with everything new and modern

• Africa is able to leapfrog technology

Political Situation

Thank You

And This, Ladies and Gentlemen

Is Where The Opportunities Are!!