17/11/2015

1

Smart Grids & Demand ResponseDevelopment in a European

Perspective

Pavla Mandatova, EURELECTRIC

iPower, Copenhagen, 4th November 2015

EURELECTRIC represents the EU electricityindustry –

all across the electricity value chain

ENERGY POLICY& GENERATION

ENVIRONMENT& SUSTAINABLEDEVELOPMENT

MARKETS RETAILCUSTOMERS

DISTRIBUTIONNETWORKS

17/11/2015

2

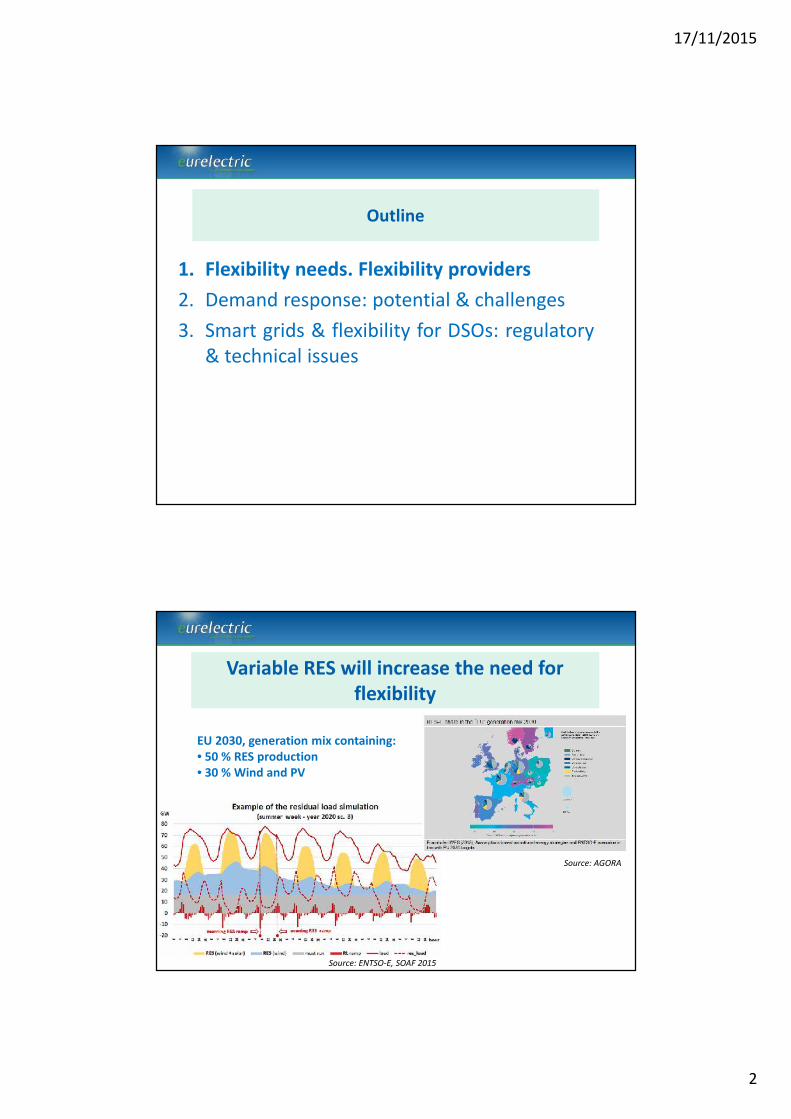

Outline

1. Flexibility needs. Flexibility providers2. Demand response: potential & challenges3. Smart grids & flexibility for DSOs: regulatory

& technical issues

Source: ENTSO-E, SOAF 2015

Variable RES will increase the need forflexibility

EU 2030, generation mix containing:• 50 % RES production• 30 % Wind and PV

Source: AGORA

17/11/2015

3

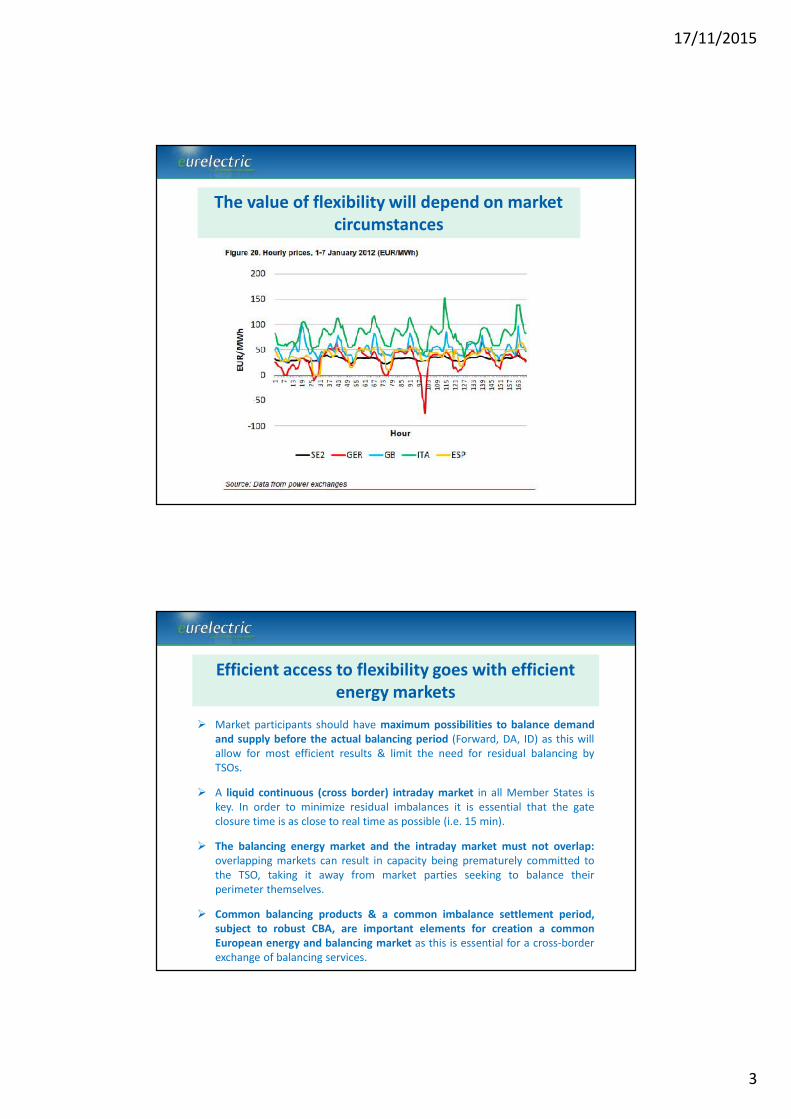

The value of flexibility will depend on marketcircumstances

Efficient access to flexibility goes with efficientenergy markets

Market participants should have maximum possibilities to balance demandand supply before the actual balancing period (Forward, DA, ID) as this willallow for most efficient results & limit the need for residual balancing byTSOs.

A liquid continuous (cross border) intraday market in all Member States iskey. In order to minimize residual imbalances it is essential that the gateclosure time is as close to real time as possible (i.e. 15 min).

The balancing energy market and the intraday market must not overlap:overlapping markets can result in capacity being prematurely committed tothe TSO, taking it away from market parties seeking to balance theirperimeter themselves.

Common balancing products & a common imbalance settlement period,subject to robust CBA, are important elements for creation a commonEuropean energy and balancing market as this is essential for a cross-borderexchange of balancing services.

17/11/2015

4

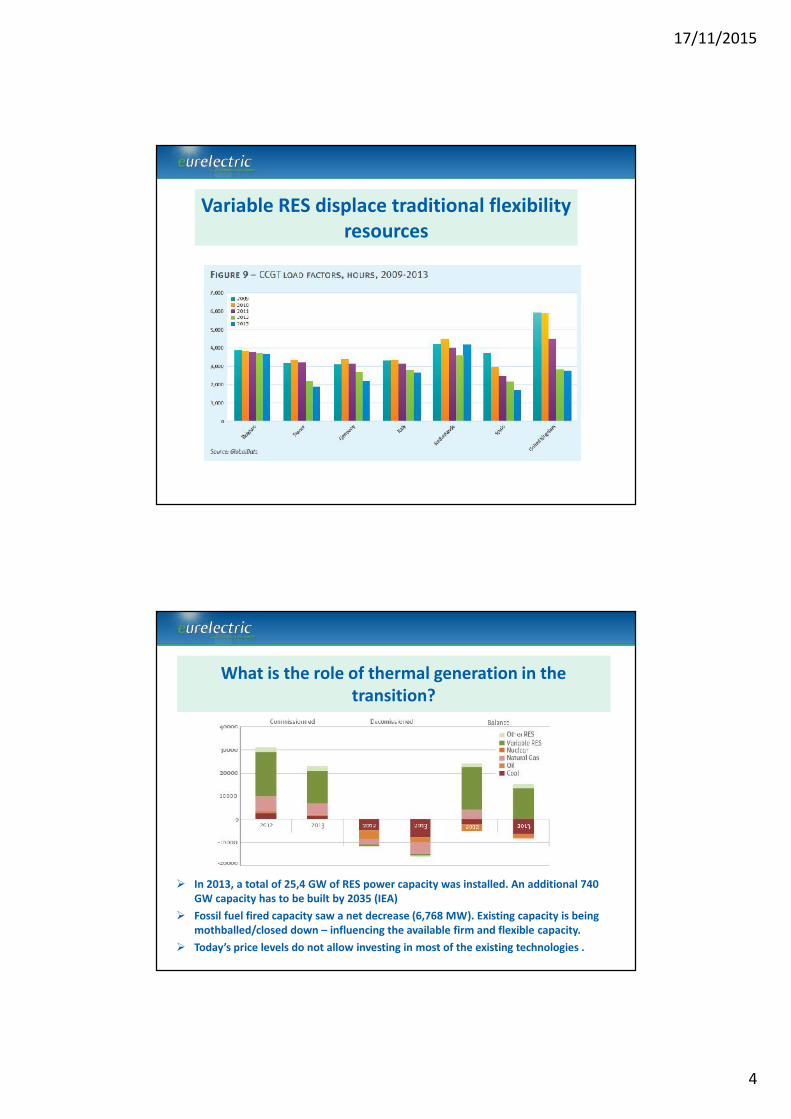

Variable RES displace traditional flexibilityresources

What is the role of thermal generation in thetransition?

In 2013, a total of 25,4 GW of RES power capacity was installed. An additional 740GW capacity has to be built by 2035 (IEA)

Fossil fuel fired capacity saw a net decrease (6,768 MW). Existing capacity is beingmothballed/closed down – influencing the available firm and flexible capacity.

Today’s price levels do not allow investing in most of the existing technologies .

17/11/2015

5

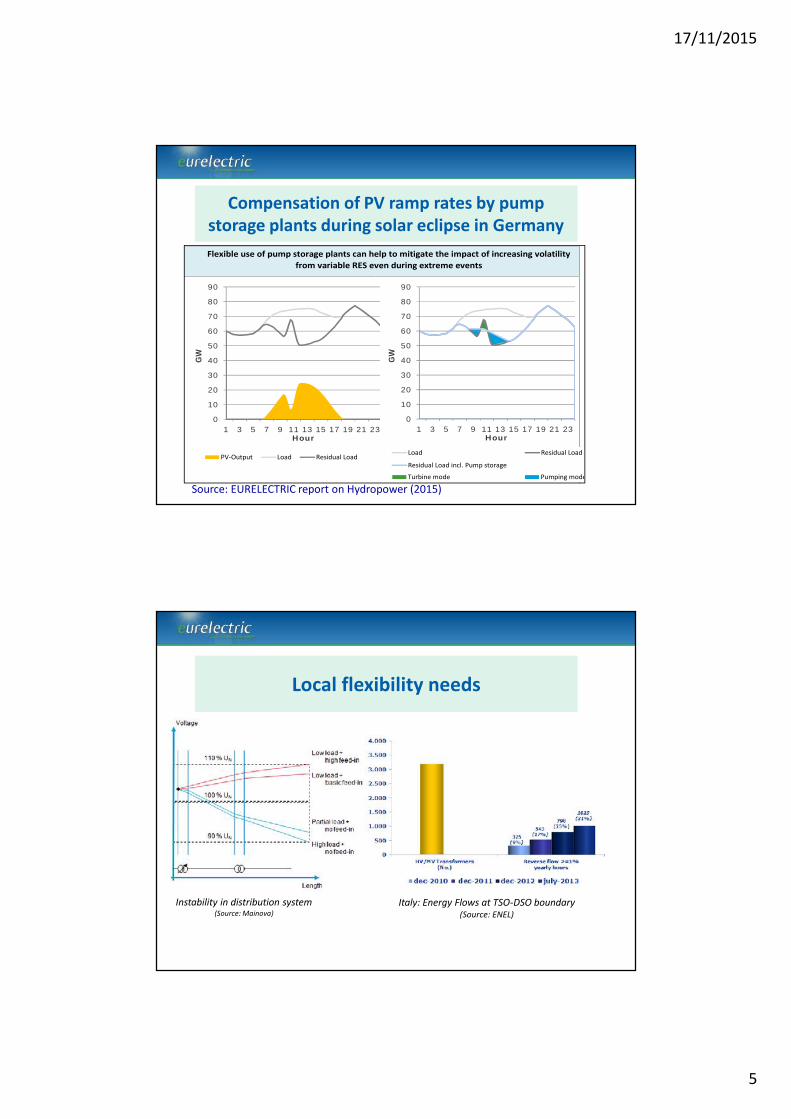

Flexible use of pump storage plants can help to mitigate the impact of increasing volatilityfrom variable RES even during extreme events

0

10

20

30

40

50

60

70

80

90

1 3 5 7 9 11 13 15 17 19 21 23

GW

Hour0

10

20

30

40

50

60

70

80

90

1 3 5 7 9 11 13 15 17 19 21 23

GW

Hour

PV-Output Load Residual Load

0

10

20

30

40

50

60

70

80

90

1 3 5 7 9 11 13 15 17 19 21 23

GW

Hour

0102030405060708090

1 3 5 7 9 11 13 15 17 19 21 23

GW

Hour

Turbine mode Pumping mode

Load Residual Load

Residual Load incl. Pump storage

0102030405060708090

1 3 5 7 9 11 13 15 17 19 21 23

GW

Hour

Turbine mode Pumping mode

Load Residual Load

Residual Load incl. Pump storage

Compensation of PV ramp rates by pumpstorage plants during solar eclipse in Germany

Source: EURELECTRIC report on Hydropower (2015)

Local flexibility needs

Instability in distribution system(Source: Mainova)

Italy: Energy Flows at TSO-DSO boundary(Source: ENEL)

17/11/2015

6

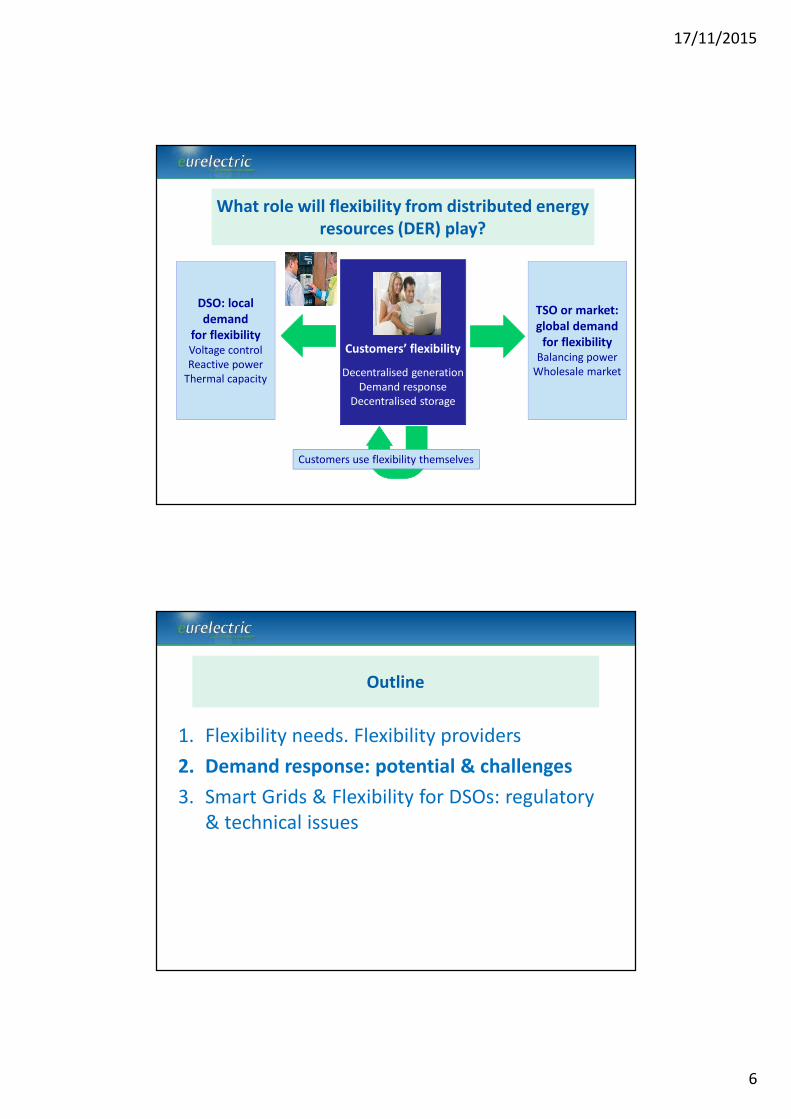

Customers use flexibility themselvesCustomers use flexibility themselves

DSO: localdemand

for flexibilityVoltage controlReactive power

Thermal capacity

DSO: localdemand

for flexibilityVoltage controlReactive power

Thermal capacity

TSO or market:global demand

for flexibilityBalancing power

Wholesale market

TSO or market:global demand

for flexibilityBalancing power

Wholesale market

Customers’ flexibility

Decentralised generationDemand response

Decentralised storage

Customers’ flexibility

Decentralised generationDemand response

Decentralised storage

What role will flexibility from distributed energyresources (DER) play?

Outline

1. Flexibility needs. Flexibility providers2. Demand response: potential & challenges3. Smart Grids & Flexibility for DSOs: regulatory

& technical issues

17/11/2015

7

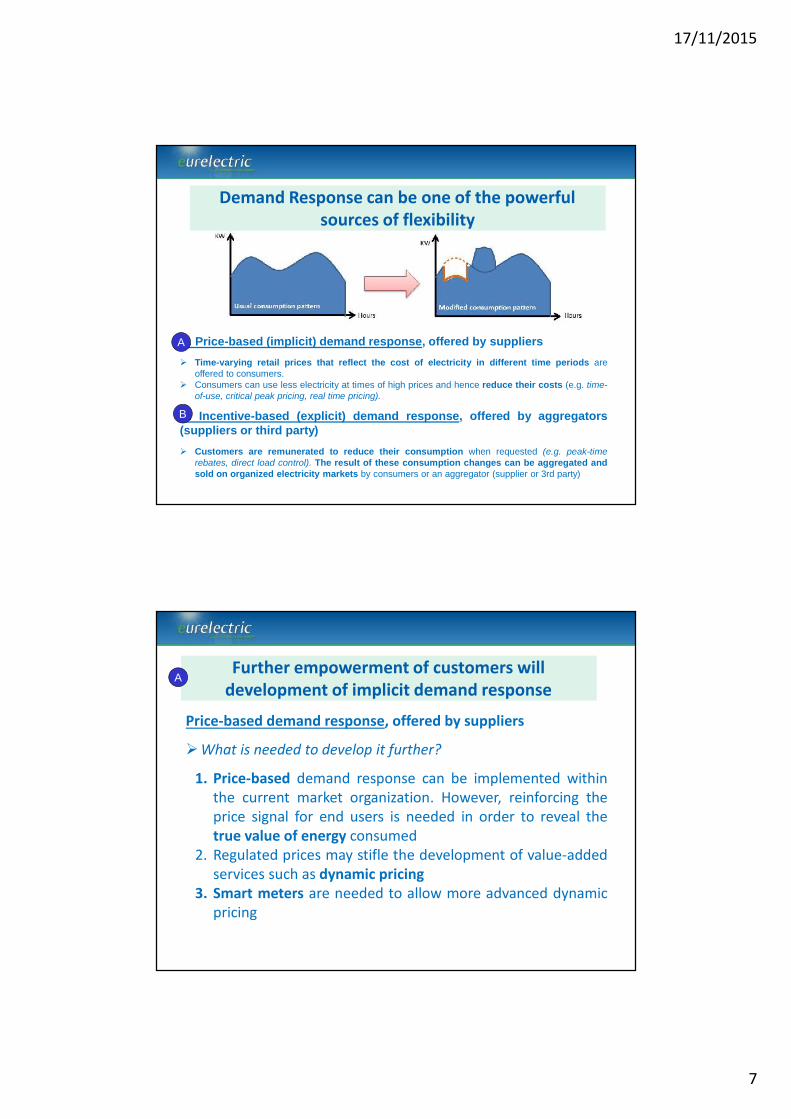

Demand Response can be one of the powerfulsources of flexibility

A. Price-based (implicit) demand response, offered by suppliers Time-varying retail prices that reflect the cost of electricity in different time periods are

offered to consumers. Consumers can use less electricity at times of high prices and hence reduce their costs (e.g. time-

of-use, critical peak pricing, real time pricing).

B. Incentive-based (explicit) demand response, offered by aggregators(suppliers or third party) Customers are remunerated to reduce their consumption when requested (e.g. peak-time

rebates, direct load control). The result of these consumption changes can be aggregated andsold on organized electricity markets by consumers or an aggregator (supplier or 3rd party)

A

B

Further empowerment of customers willdevelopment of implicit demand response

Price-based demand response, offered by suppliers

What is needed to develop it further?

1. Price-based demand response can be implemented withinthe current market organization. However, reinforcing theprice signal for end users is needed in order to reveal thetrue value of energy consumed

2. Regulated prices may stifle the development of value-addedservices such as dynamic pricing

3. Smart meters are needed to allow more advanced dynamicpricing

A

17/11/2015

8

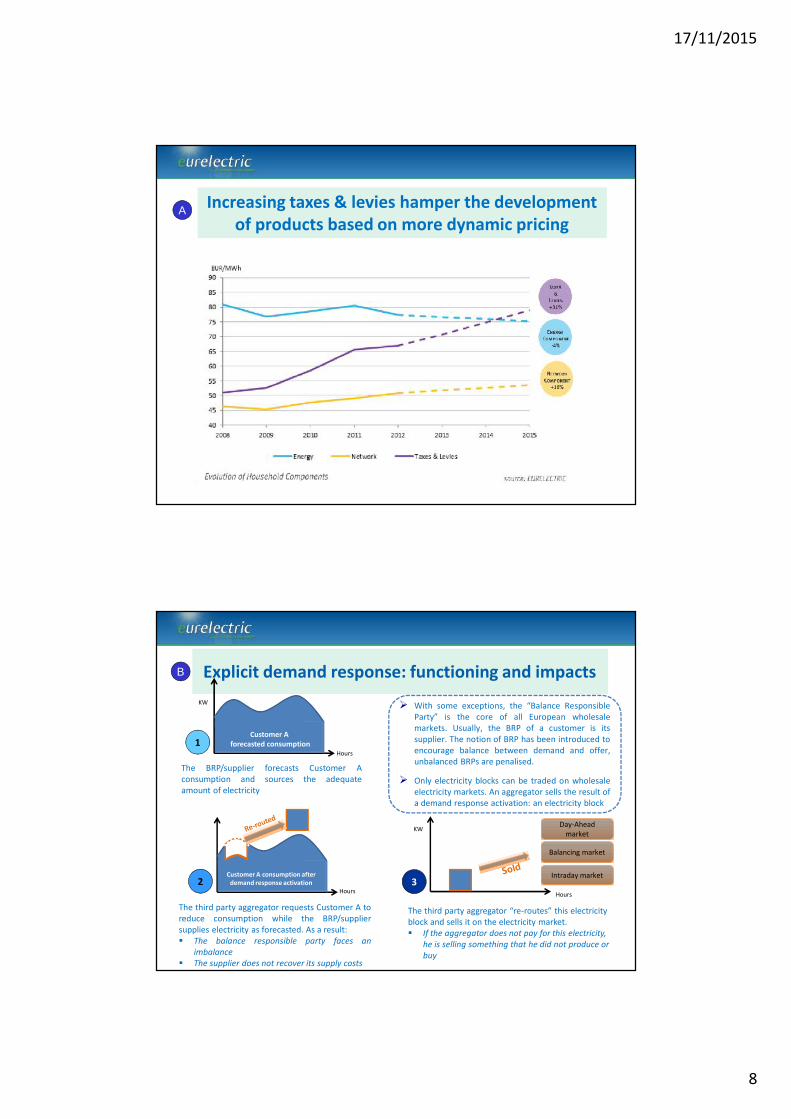

Increasing taxes & levies hamper the developmentof products based on more dynamic pricing

A

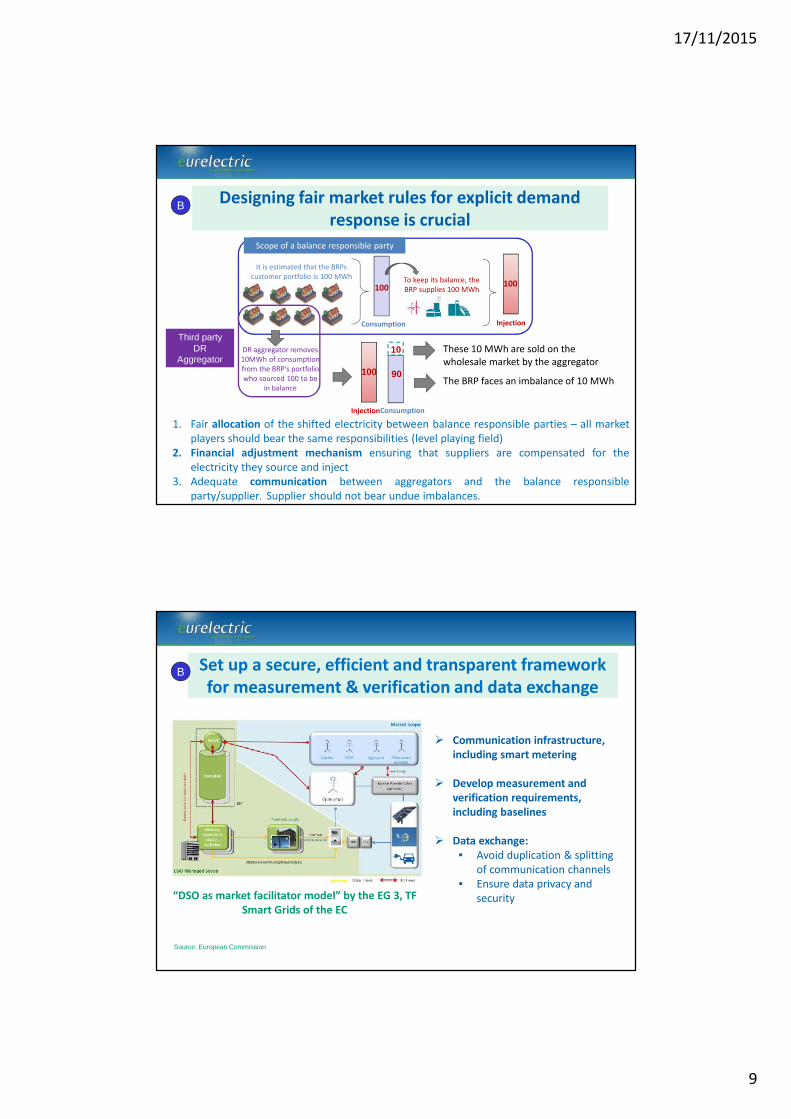

Explicit demand response: functioning and impacts

Day-Aheadmarket

Day-Aheadmarket

Balancing marketBalancing market

Intraday marketIntraday market

The BRP/supplier forecasts Customer Aconsumption and sources the adequateamount of electricity

The third party aggregator requests Customer A toreduce consumption while the BRP/suppliersupplies electricity as forecasted. As a result: The balance responsible party faces an

imbalance The supplier does not recover its supply costs

The third party aggregator “re-routes” this electricityblock and sells it on the electricity market. If the aggregator does not pay for this electricity,

he is selling something that he did not produce orbuy

Hours

KW

Hours Hours

KW

1

2 3

Customer Aforecasted consumption

Customer A consumption afterdemand response activation

With some exceptions, the “Balance ResponsibleParty” is the core of all European wholesalemarkets. Usually, the BRP of a customer is itssupplier. The notion of BRP has been introduced toencourage balance between demand and offer,unbalanced BRPs are penalised.

Only electricity blocks can be traded on wholesaleelectricity markets. An aggregator sells the result ofa demand response activation: an electricity block

B

17/11/2015

9

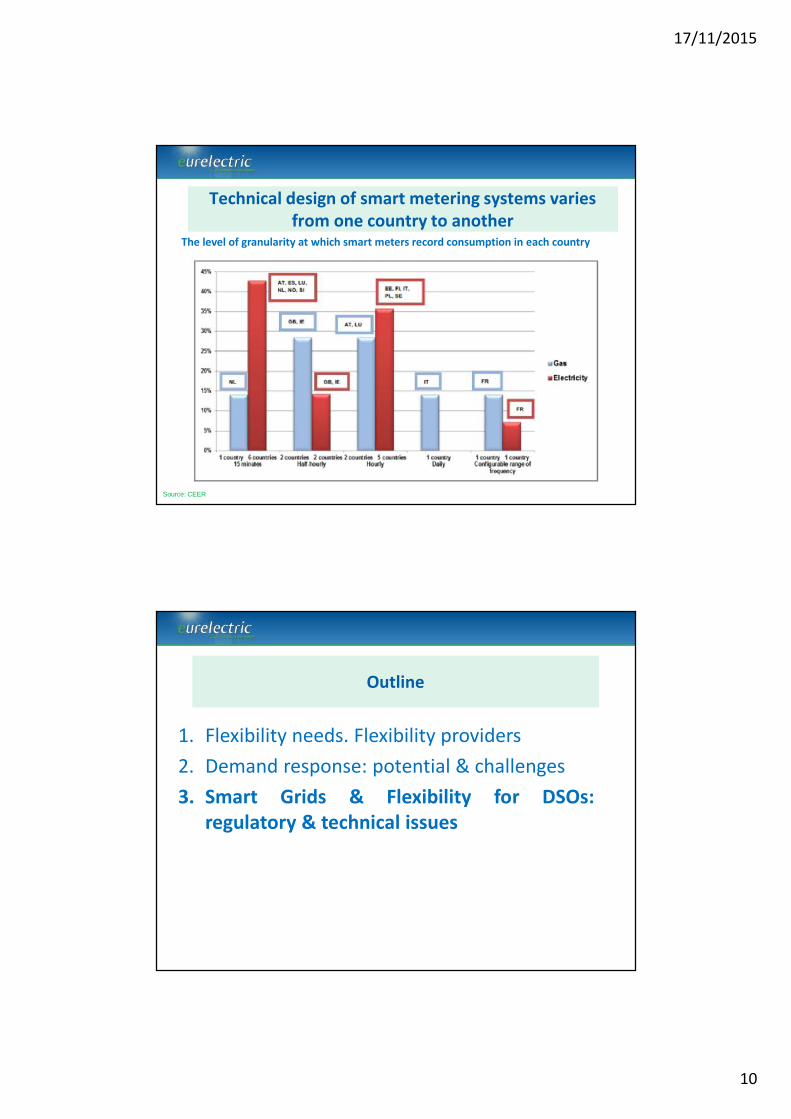

Scope of a balance responsible party

To keep its balance, theBRP supplies 100 MWh100

It is estimated that the BRPscustomer portfolio is 100 MWh

Consumption

100

Injection

ConsumptionInjection

DR aggregator removes10MWh of consumptionfrom the BRP’s portfoliowho sourced 100 to be

in balance

Third partyDR

Aggregator90100

10 These 10 MWh are sold on thewholesale market by the aggregator

The BRP faces an imbalance of 10 MWh

1. Fair allocation of the shifted electricity between balance responsible parties – all marketplayers should bear the same responsibilities (level playing field)

2. Financial adjustment mechanism ensuring that suppliers are compensated for theelectricity they source and inject

3. Adequate communication between aggregators and the balance responsibleparty/supplier. Supplier should not bear undue imbalances.

Designing fair market rules for explicit demandresponse is crucial

B

Source: European Commission

“DSO as market facilitator model” by the EG 3, TFSmart Grids of the EC

Communication infrastructure,including smart metering

Develop measurement andverification requirements,including baselines

Data exchange:• Avoid duplication & splitting

of communication channels• Ensure data privacy and

security

Set up a secure, efficient and transparent frameworkfor measurement & verification and data exchange

B

17/11/2015

10

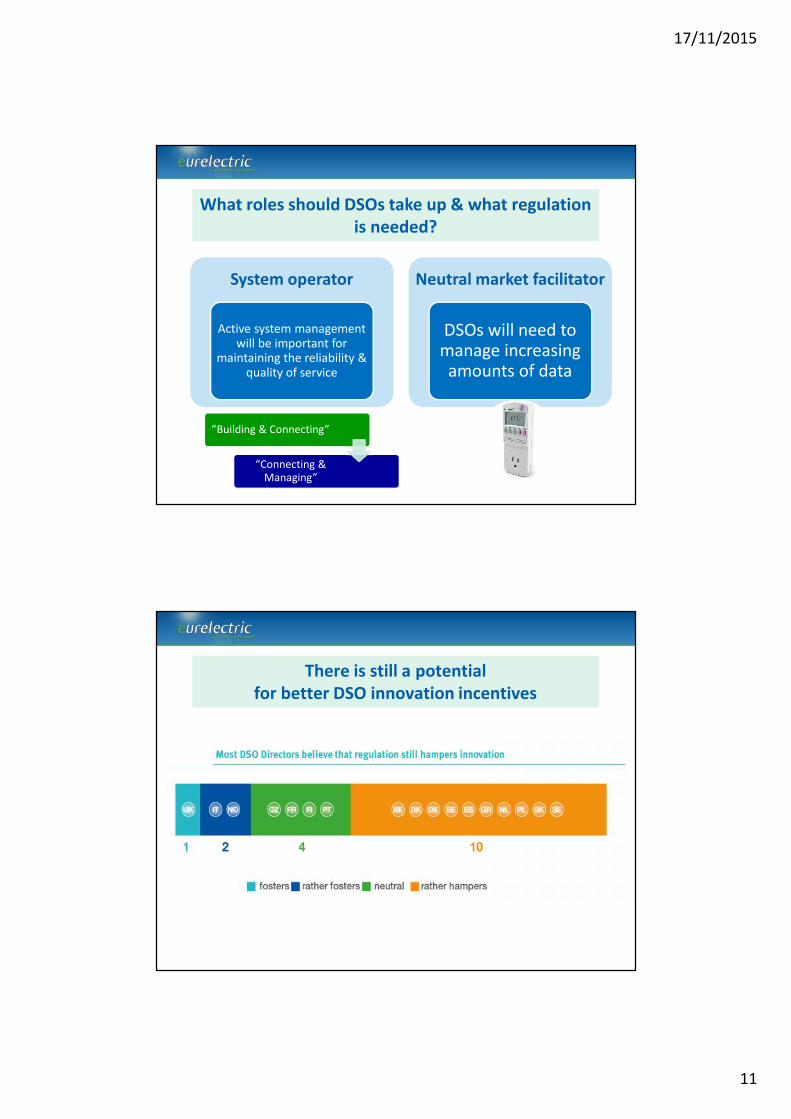

Source: CEER

The level of granularity at which smart meters record consumption in each country

Technical design of smart metering systems variesfrom one country to another

Outline

1. Flexibility needs. Flexibility providers2. Demand response: potential & challenges3. Smart Grids & Flexibility for DSOs:

regulatory & technical issues

17/11/2015

11

System operator

Active system managementwill be important for

maintaining the reliability &quality of service

Neutral market facilitator

DSOs will need tomanage increasing

amounts of data

”Building & Connecting”

“Connecting &Managing”

What roles should DSOs take up & what regulationis needed?

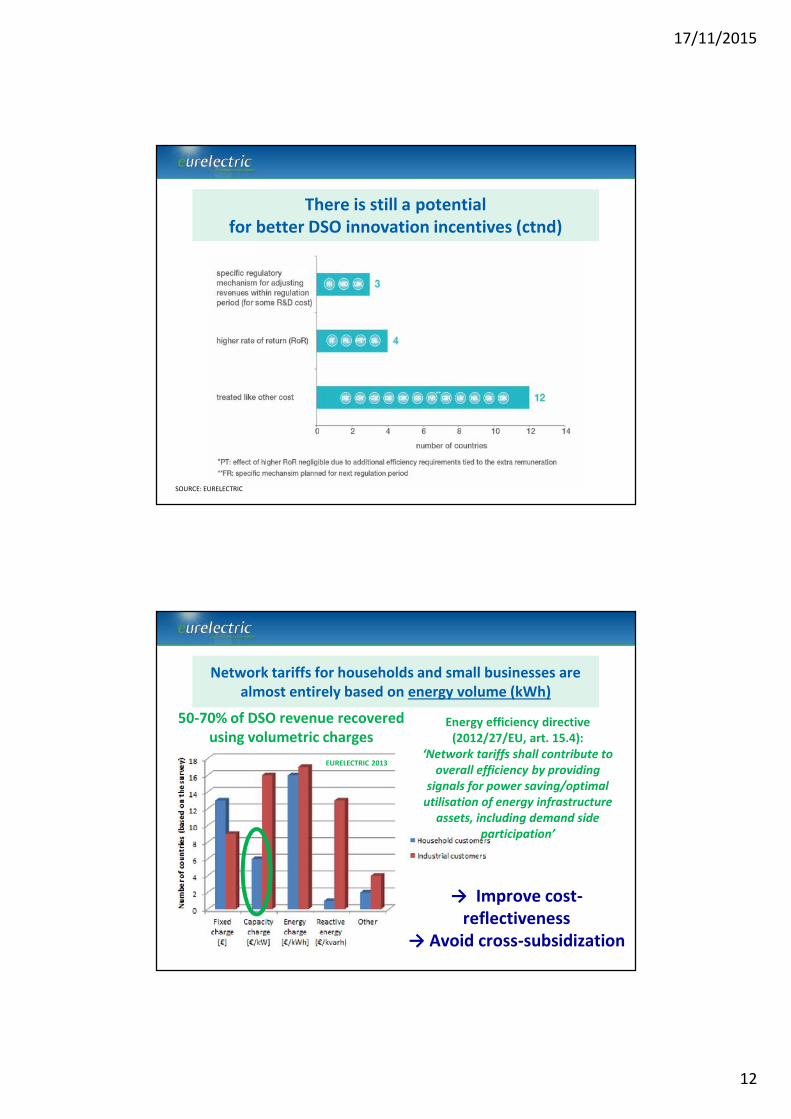

There is still a potentialfor better DSO innovation incentives

17/11/2015

12

SOURCE: EURELECTRIC

There is still a potentialfor better DSO innovation incentives (ctnd)

→ Improve cost-reflectiveness

→ Avoid cross-subsidization

Energy efficiency directive(2012/27/EU, art. 15.4):

‘Network tariffs shall contribute tooverall efficiency by providing

signals for power saving/optimalutilisation of energy infrastructure

assets, including demand sideparticipation’

EURELECTRIC 2013

50-70% of DSO revenue recoveredusing volumetric charges

Network tariffs for households and small businesses arealmost entirely based on energy volume (kWh)

17/11/2015

13

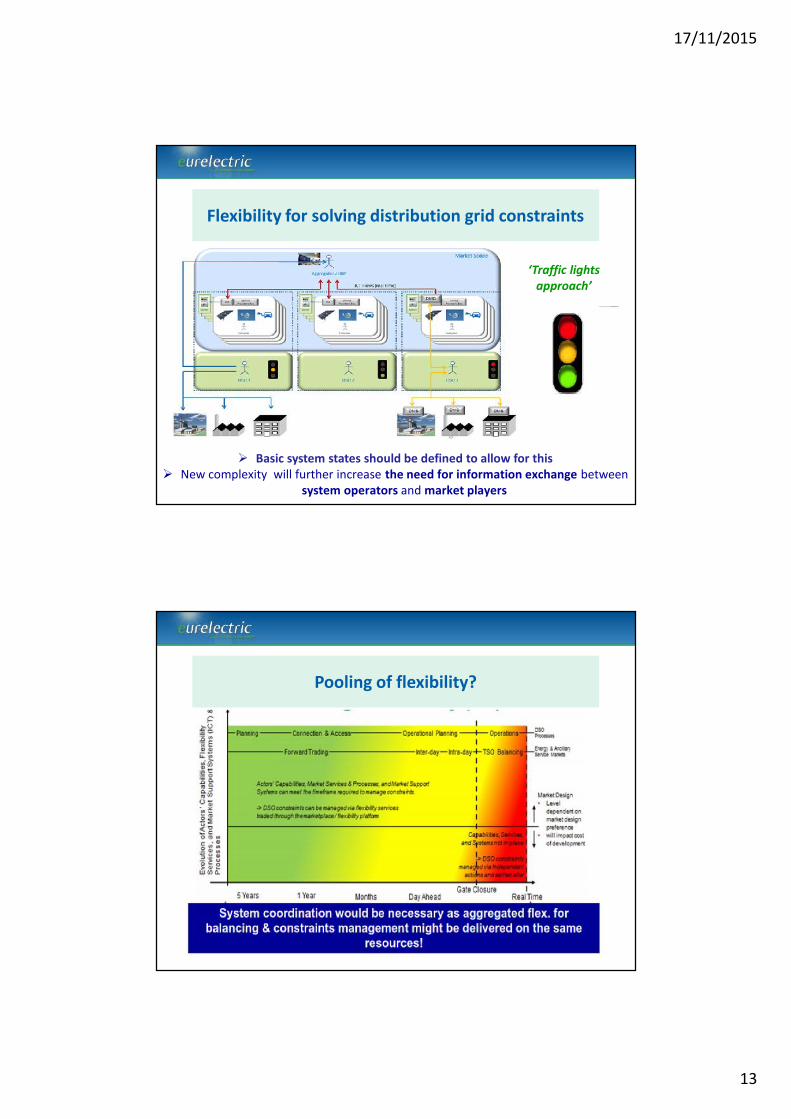

Basic system states should be defined to allow for this New complexity will further increase the need for information exchange between

system operators and market players

‘Traffic lightsapproach’

Flexibility for solving distribution grid constraints

Pooling of flexibility?

17/11/2015

14

To summarize…

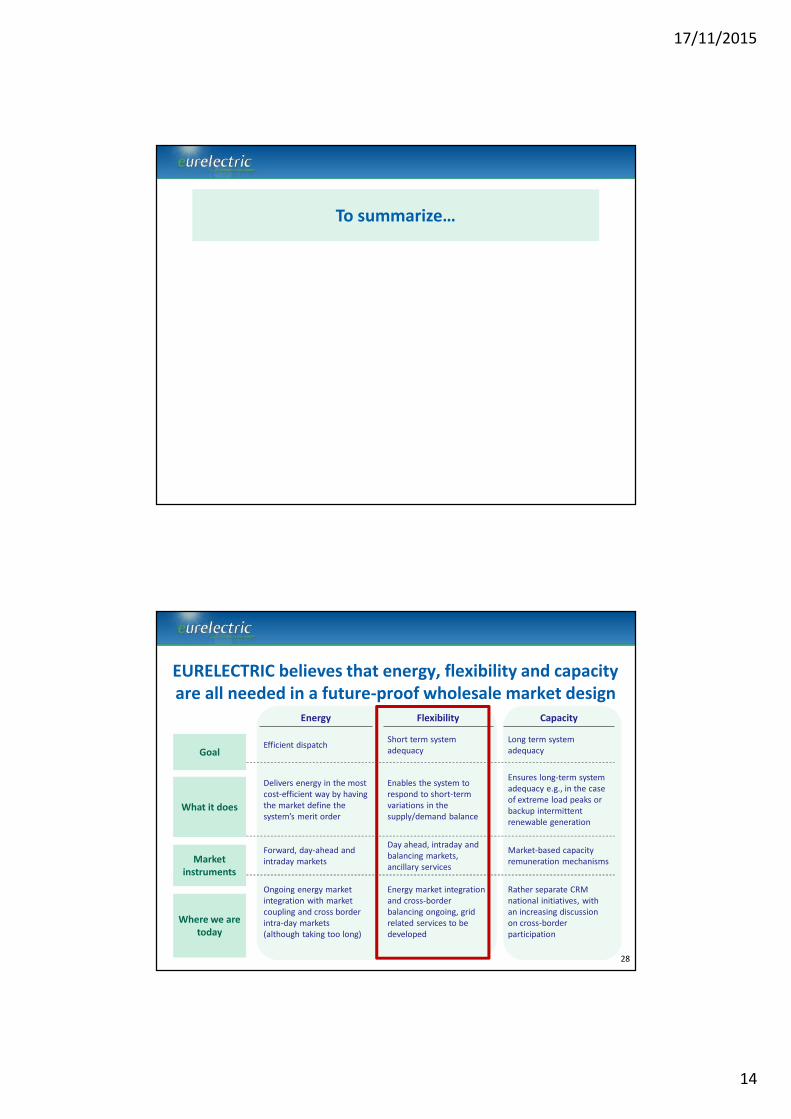

EURELECTRIC believes that energy, flexibility and capacityare all needed in a future-proof wholesale market design

Energy Flexibility Capacity

Efficient dispatch Short term systemadequacy

Long term systemadequacy

Delivers energy in the mostcost-efficient way by havingthe market define thesystem’s merit order

Enables the system torespond to short-termvariations in thesupply/demand balance

Ensures long-term systemadequacy e.g., in the caseof extreme load peaks orbackup intermittentrenewable generation

Forward, day-ahead andintraday markets

Day ahead, intraday andbalancing markets,ancillary services

Market-based capacityremuneration mechanisms

Ongoing energy marketintegration with marketcoupling and cross borderintra-day markets(although taking too long)

Energy market integrationand cross-borderbalancing ongoing, gridrelated services to bedeveloped

Rather separate CRMnational initiatives, withan increasing discussionon cross-borderparticipation

Goal

What it does

Marketinstruments

28

Where we aretoday

17/11/2015

15

Flexible and back-up generation

capacity

Integratedwholesalemarkets

Demand sidemanagement andDemand Response

Centralised anddecentralised storage

systems

Extensive newinfrastructure attransmission anddistribution level

Need for a level playing field with otherflexibility sources

A level playing field for all actors• Providers of aggregated demand response should be subject to the same market rules, the

same standards of service, and the same participation rules as other market players.• The costs created by the additional operational and contractual actions have to be clearly and

fairly allocated to the relevant market actors.

A market design suitable for all markets with full competition• When the same principles apply to all markets, flexibility providers can better optimize the

value of flexibility across timeframes. In this way, flexibility is made available for all electricitymarkets

• System Operators needs should be tendered in the market and accessible to all market parties(suppliers and third party aggregators) – market fragmentation should be avoided

Scalability for large-scale implementation• A good market design should be based on processes that can be automated, contracts that can

be standardised and allocations that can be objectified in order to allow for large-scaleimplementation.

EURELECTRIC supports general EC guidelines

Key principles to implement a good market designfor DR aggregation