SSE Financial Results 6 months to 30 September 2015

Richard Gillingwater

2

Chairman

The SSE team

3

Safety comes first

4

SSE Total Recordable Injury Rate*

0.04

0.08

0.12

0.16

HY15 HY16

0.12 0.12

0

20

40

60

80

HY15 HY16

65 52

Total SSE and Contractor Recordable Injuries

*TRIR – per 100,000 hours worked

Strategy for long-term success

5

− Operating and investing in a balanced range of energy assets and businesses

− Range of opportunities to develop new assets and new customer propositions

− Annual dividend increases of at least RPI inflation

Working for a long-term framework

6

SSE view is that policy making should:

− Be clear and transparent

− Respect committed investments

− Include effective transitional arrangements

SSE strongly believes in constructive engagement with policy-makers and regulators

£757m invested

Industry leadership in Service

Dividend at least keeps pace with RPI

At least 115p EPS targeted

Delivering solid financial results

7

Gregor Alexander

8

Finance Director

₋ Financial Overview ₋ Networks

Focusing on the key financial results HY15 £m HY16 £m % change

Adjusted profit before tax 370.3 548.8 +48.2%

Fair value re-measurements (IAS 39) (17.3) (284.5)

Exceptional items - (2.2)

Interest on net pension liabilities (IAS 19R) (14.3) (11.3)

Tax on JCEs and associates (22.1) (20.0)

Reported profit before tax 316.6 230.8

Adjusted earnings per share 31.1p 45.9p +47.6%

Adjusted effective tax rate 15.0% 14.6%

Interim dividend 26.6p 26.9p +1.1%

9

10

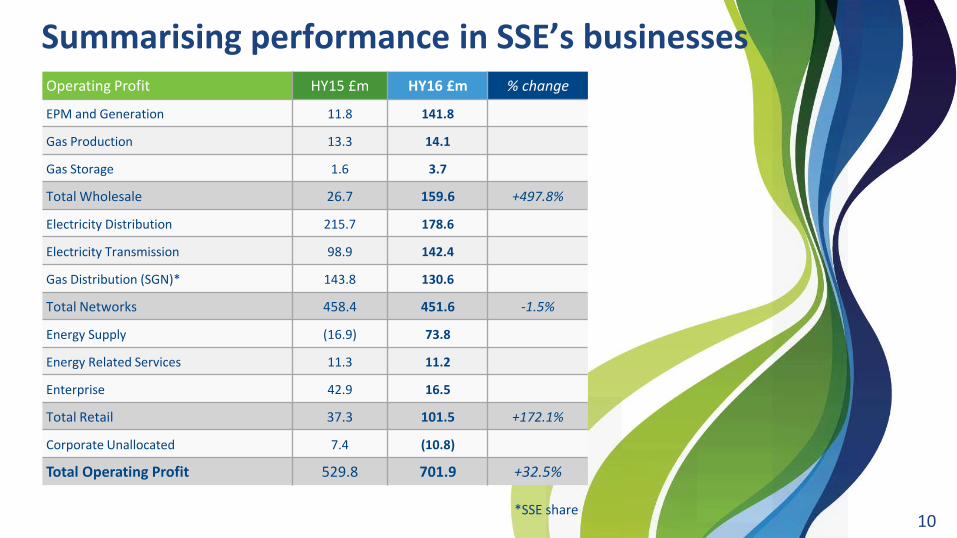

Summarising performance in SSE’s businesses Operating Profit HY15 £m HY16 £m % change

EPM and Generation 11.8 141.8

Gas Production 13.3 14.1

Gas Storage 1.6 3.7

Total Wholesale 26.7 159.6 +497.8%

Electricity Distribution 215.7 178.6

Electricity Transmission 98.9 142.4

Gas Distribution (SGN)* 143.8 130.6

Total Networks 458.4 451.6 -1.5%

Energy Supply (16.9) 73.8

Energy Related Services 11.3 11.2

Enterprise 42.9 16.5

Total Retail 37.3 101.5 +172.1%

Corporate Unallocated 7.4 (10.8)

Total Operating Profit 529.8 701.9 +32.5%

*SSE share

Focusing on adjusted earnings per share

11

- SSE is continuing to target FY16 adjusted EPS of at least 115p

- Adjusted dividend cover range from around 1.2x to around 1.4x in the 3 years to March 2018

- Long-term target closer to 1.5x - based on a dividend that at least keeps pace with RPI

Adjusted EPS HY and FY (p)

0

50

100

150

FY12 FY13 FY14 FY15 FY16

25.3 35.6 29.4 31.1

45.9

112.9 118.5 123.4 124.1 At least 115p

Making the right investment decisions (1)

12

HY15 FY15 HY16

Capital expenditure and investment (£m) 679 1,475 757

Adjusted net debt and hybrid capital (£m) 7,907 7,568 7,937

Average interest rate 4.50% 4.21% 3.96%

SSE benefited from:

- Good working capital management

- Reduced cash dividend through Scrip

- Low funding costs

- Commitment to maintaining strong balance sheet

Lawers Dam

Making the right investment decisions (2)

13

Up to 2018 and beyond

50%

30%

10%

10%

Networks

Wholesale

Retail (incl.Enterprise)Other

FY16 c. £1.75bn capex forecast

− Capex programme of around £5.5bn net across four years to March 2018

− Expected to be able to outline investment priorities beyond 2018 in the course of 2016

− Wide range of options post-2018

Focusing on value

14

Disposals and capital ‘recycling’ programme

SSE windfarm 0

1,000Remaining disposalprogramme

Wind assets sold or with saleagreements reached

Non-core assets sold or withsale agreements reached

£m

HY99 HY00 HY01 HY02 HY03 HY04 HY05 HY06 HY07 HY08 HY09 HY10 HY11 HY12 HY13 HY14 HY15 HY16

7.7 8.3 9.0

9.7 10.5

11.3 12.2

13.8 15.1

18.1

19.8 21.0

22.4 24.0

25.2 26.0 26.6 26.9

Maintaining a platform for dividend growth

15

Dividend Per Share HY (p)

Targeting dividend increases at least equal to RPI in future

Networks central to SSE’s strategy

16

0

2

4

6

8

FY10 FY11 FY12 FY13 FY14 FY15 HY16

Transmission Electricity Distribution SGN

Total Networks RAV, £bn (net)

Operating Profit HY15 HY16 % change

Electricity Distribution 215.7 178.6 -17.2%

Transmission 98.9 142.4 +44.0%

Gas Distribution (SGN) 143.8 130.6 -9.2%

Networks Operating Profit 458.4 451.6 -1.5%

Networks RAV increased by over 50% since April 2010 to £7.6bn; and is well placed to reach £10bn by 2020

Beauly-Denny

Keeping the lights on for Distribution customers

17

0

50

100

150

HY12 HY13 HY14 HY15 HY16

112 118 128 128

113

Distribution capex (£m)

0

50

100

150

200

250

HY15 HY16

216 179

Operating profit (£m) Distribution RAV (£bn)

0

1

2

3

4

FY10 HY15

2.56 3.13

Live Line Harvesting

Working for customers in ED-1

New Distribution price control

- Delivering an underlying reduction in household distribution costs

Stable and transparent regulatory framework

- Allowed revenues now set to 2023

SSE is focused on:

- Achieving efficiencies and innovation

- Ensuring investors receive fair return

18

0

20

40

HY12 HY13 HY14 HY15 HY16

30 33 33 29

24 30 33 32 32

21

SHEPD SEPD

Customer Minutes Lost (CML)

0

20

40

HY12 HY13 HY14 HY15 HY16

30 33

37 31 31

36 31

36 32

24

Customer Interruptions (CI)

Increasing the asset base in Transmission

0

50

100

150

200

HY15 HY16

99

142

Operating Profit (£m) Transmission RAV (£bn)

0

0.5

1

1.5

2

2.5

FY10 HY16

0.41

2.01

0

100

200

300

HY12 HY13 HY14 HY15 HY16

68

168 195 213

289

Transmission capex (£m)

19

Projects nearing completion:

− Beauly-Denny - £680m

− Foyers-Knocknagael - £26m

− Beauly-Blackhillock-Kintore - £94m

− Kintyre-Hunterston - £210m

− Beauly-Mossford - £68m

£1.1bn Caithness-Moray project now also underway

Securing value from Gas Distribution

20

Operating Profit* (£m)

0

50

100

150

200

HY15 HY16

144 131

0

1

2

3

FY10 HY16

1.95 2.48

SGN RAV* (£bn)

0

200

400

600

800

1000

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 RAVadditions

Cash returns Equity investment

Investment in SGN

Alistair Phillips-Davies

21

Chief Executive

₋ Business and Political Environment ₋ Wholesale ₋ Retail ₋ Outlook

Working within the emerging policy and regulatory framework

22 2015/16 – an important year for energy businesses in GB & Ireland

Key developments since May 2015

- Outcome of RIIO-ED1 appeal

- Implementation of the new government’s energy policies

- Provisional findings and potential remedies from the CMA market investigation

Emerging framework should enable SSE

- Deliver good operational performance for customers

- Deliver solid financial results for investors

- Be well-positioned to succeed in a changing sector

Working in the interest of customers and investors alike

23

Prudent decision to take more time

Pragmatic approach to closing RO in 2016

Progressive Price Control process

Managing Wholesale business in response to long-term trends

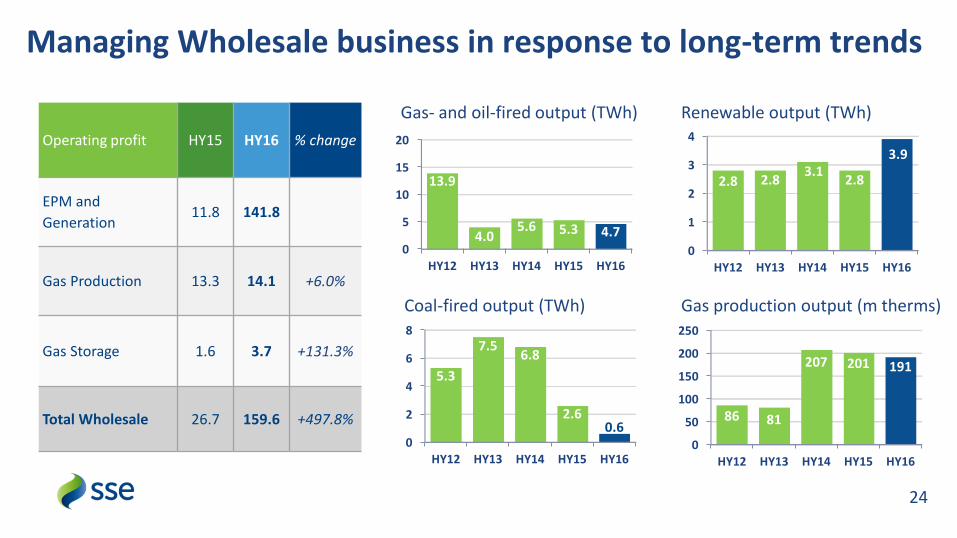

24

Operating profit HY15 HY16 % change

EPM and

Generation 11.8 141.8

Gas Production 13.3 14.1 +6.0%

Gas Storage 1.6 3.7 +131.3%

Total Wholesale 26.7 159.6 +497.8%

0

2

4

6

8

HY12 HY13 HY14 HY15 HY16

5.3

7.5 6.8

2.6 0.6

Coal-fired output (TWh)

0

1

2

3

4

HY12 HY13 HY14 HY15 HY16

2.8 2.8 3.1

2.8

3.9

Renewable output (TWh)

0

50

100

150

200

250

HY12 HY13 HY14 HY15 HY16

86 81

207 201 191

Gas production output (m therms)

0

5

10

15

20

HY12 HY13 HY14 HY15 HY16

13.9

4.0 5.6 5.3 4.7

Gas- and oil-fired output (TWh)

Playing our part in contributing to security of supply with gas-fired power stations

25

- Peterhead secured one-year SBR contract for 2015/16

- Medway continued good performance in response to market requirements

- Keadby expected to return to full commercial operation mid-December

- Great Island CCGT completed six months of full commercial operation

Great Island CCGT

Keadby CCGT

Wholly owned gas-fired power stations

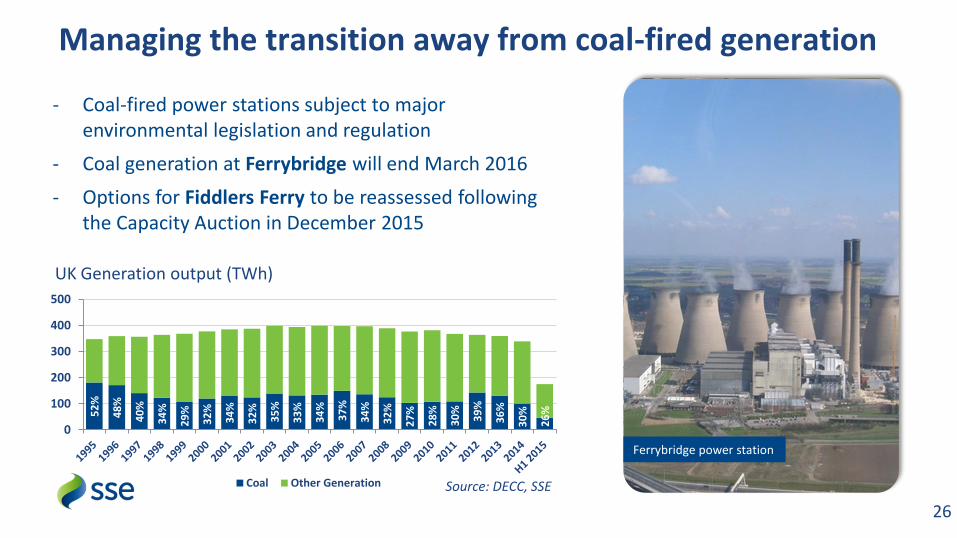

Managing the transition away from coal-fired generation

26

UK Generation output (TWh)

- Coal-fired power stations subject to major environmental legislation and regulation

- Coal generation at Ferrybridge will end March 2016

- Options for Fiddlers Ferry to be reassessed following the Capacity Auction in December 2015

Source: DECC, SSE

52

%

48

%

40

%

34

%

29

%

32

%

34

%

32

%

35

%

33

%

34

%

37

%

34

%

32

%

27

%

28

%

30

%

39

%

36

%

30

%

26

%

0

100

200

300

400

500

Coal Other Generation

Ferrybridge power station

Modernising electricity generation

− £300m/69MW multi-fuel plant at Ferrybridge fully commissioned, with another 90MW consented

27

Peterhead CCGT Ferrybridge Multifuel

− Developing world’s first full-scale carbon capture and storage project at Peterhead

Taking the right decisions in Generation – renewables (1)

28

Total Renewable Capacity (GW)

2.4 2.9 3.2 3.3 3.4 3.4

0

1

2

3

4

FY11 FY12 FY13 FY14 FY15 HY16

Hydro Onshore wind Offshore wind

• Since 2010 SSE developed:

- Just under 800MW* of new onshore wind

- 350MW** of new offshore wind

• c. 600MW of onshore wind in construction

• Beatrice FID due in 2016

Beatrice demonstrator

*83MW sold **SSE share

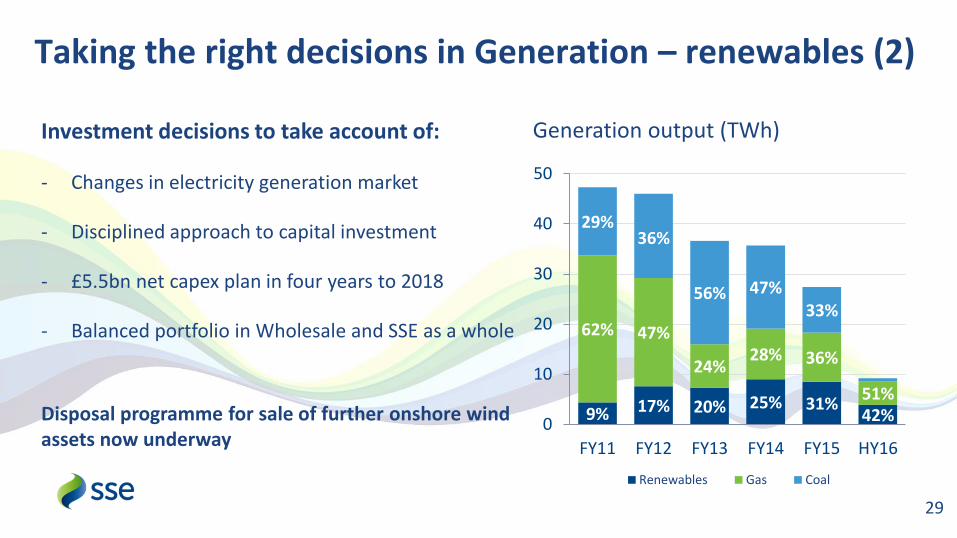

Taking the right decisions in Generation – renewables (2)

29

Investment decisions to take account of:

- Changes in electricity generation market

- Disciplined approach to capital investment

- £5.5bn net capex plan in four years to 2018

- Balanced portfolio in Wholesale and SSE as a whole

Disposal programme for sale of further onshore wind assets now underway

Generation output (TWh)

9% 17% 20% 25% 31% 42%

62% 47%

24% 28% 36%

51%

29% 36%

56% 47% 33%

0

10

20

30

40

50

FY11 FY12 FY13 FY14 FY15 HY16

Renewables Gas Coal

Maintaining Gas Production assets

30

Greater Laggan asset acquisition

− Natural complement to existing gas production assets

− Shetland Gas Plant

− Long-term assets

− Further diversity to SSE investment programme

− 3 - 4p EPS enhancement in 2016/17

Long term asset with medium-term UK tax benefits Shetland Gas Plant

Managing issues in Energy Supply

31

Operating profit (£m) HY15 HY16 % change

Energy Supply -16.9 73.8

Energy Related Services 11.3 11.2 -0.9%

Enterprise 42.9 16.5 -61.5%

Total Retail 37.3 101.5 +172.1%

Energy Customer Accounts (m) 8.89 8.41

Aged Debt (£m) 134.5 128.3

Source: Citizen Advice Bureau

944 770

645 577

518 421

170 141

123 119 116 97 91 89 83

70 64 48

18. Scottish Power17. Extra Energy16. Co-Operative Energy15. nPower14. Spark Energy13. First Utility12. Flow Energy11. Economy Energy10. Ovo Energy9. Utility Warehouse8. Utilita7. Green Star Energy6. Good Energy5. E.ON4. British Gas3. Ecotricity2. EDF Energy1. SSE

Ratio of complaints per 100,000 customers April – June 2015

Putting customers first for the long term

32

New systems to help customers

Price Freeze until July 2016

Brand building Industry-leading broadband offer

‘Treating Customers

Fairly’ principles

Customer service

improvement

Digital channels overhaul

£70m Investment in Energy Supply

Building a new business - Enterprise

33

- Potential to attract significant and sustainable growth

- Further integration of products and services

- SSE Enterprise Contracting named top contractor

Operating profit (£m)

42.9*

16.5 0

20

40

60

HY15 HY16

*includes £15.3m gas pipelines disposal gain

Meeting the needs of customers and investors

34

SSE priorities

− Develop our business for growth in emerging political and regulatory framework

− Ensure we are positioned well for the long term

− Meet our dividend commitments

Doing the right things for the long term

35

Wholesale Networks Retail

− Completed Ferrybridge multi-fuel plant

− Enhanced roles of Peterhead & Keadby

− Acquired new gas production assets

− Started onshore wind disposal process

− RIIO-ED1 Price Control

− Enhanced customer focus in Distribution

− Strong Transmission investment programme delivery

− Best-in-class customer service

− Smart meter installation delivery

− Successfully extended product range

SSE Group − Dynamic and opportunistic approach to financing

− Actively manage asset base with targeted disposals

− Measured approach to changes in technology affecting energy sector

− Constructive approach to policy and regulation

Delivering dividend growth for the long-term

36

FY99 FY00 FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

25.7 27.5 30.0 32.4 35.0 37.7 42.5

46.5

55.0 60.5

66.0 70.0

75.0 80.1

84.2 86.7 88.4 RPI*

Dividend Per Share FY (p)

*forecast, at least RPI

Value for customers and value for investors Q and A

37