© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

STOCK EXCHANGE TRENDS IN EUROPE AND THE WORLD- HOW THEY INFLUENCE BALTIC AND NORDIC MARKETS

20 May, 2011 / Lauri Rosendahl

Agenda

• Introduction

•Global / European / Nordic securities trading•Global / European / Nordic securities trading

landscape

- Financial crisis, transparency and new regulation

- Market and Competition => Fragmentation

•What & how is NASDAQ OMX Nordic doing ?

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

•What & how is NASDAQ OMX Nordic doing ?

•Conclusions for the Nordic & Baltic region

2

The changing landscape for Stock Exchanges

European Union: Competition is sharper but liquidity fragmentedliquidity fragmentedBy Jeremy Grant

Published: October 20 2009 16:57

It is hard to believe that a dry-sounding European Commission directive that came into force almost exactly two years ago could have had the effect on Europe’s equities markets that it has.

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 3

But the Markets in Financial Instruments Directive (Mifid) has resulted in some astonishing changes to the trading landscape – probably far beyond what its architects envisaged.

Almost 100 years of exchange history in Finland

Helsinki Stock

Exchange

1912 1997

HEX Tallinn

2001 2002

HEX Riga

2003

NASDAQ – OMX -merger

20081999

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

Merger of

exchange and CSD

HEX TallinnOM-HEX merger

Merger of equity

and derivative

exchanges

The Helsinki Stock Exchange

- First Green Office Exchange in the world

(Dec 2010)

History of NASDAQ

Idea was actually sparked in the

1960’s

Became first fully electronic market in

ACT and SWAT

launch to NASDAQ

NASDAQ announces BRUT integration developments

electronic market in the world

1971

1986 1994

1996

First market to launch

investor Website – NASDAQ.com

1981

NASDAQ-100, Futures and Options created

1985 1989

launch to reduce risks in trading

1999

2000

NASDAQ becomes

shareholder-owned, for-

profit company

2002

2004

developments

Google lists on NASDAQ

2007

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

Apple and Microsoft list on NASDAQ

NASDAQ surpasses the New York Stock

Exchange in yearly share volume

NASDAQ MarketSite opens in Times Square

The Market Intelligence Desk launches

NASDAQ’s INET acquisition clears and INET goes

live

5

GET TO KNOW US

We invented electronic trading 40 years ago and are now the world’s largest exchange

We power

1 in 10of the world’s securities

NASDAQ OMX

trading technology is

used to power

more than 70exchanges

in 50

NASDAQ OMX lists

3,600global companies

worth $5.4T in market cap

representing diverse world’s largest exchange company.

Electronic trading is trusted and

emulated by every electronic

equities exchange in the world,

making the world’s capital markets

move faster, more efficiently and

more transparently.

NASDAQ OMX is a public

securities transactions

in 50countries

We own and operate More than

Our global platform

can handle

more than 1M

representing diverse industries and many of the world’s most well-known and innovative brands

company and part of the S&P 500

Index.

6

operate 24 markets3 clearing houses

5 central securities depositories

More than

$500B is tied to

our global indexes

can handle

more than 1M messages/second

at sub-100 microsecond

average speeds

NASDAQ OMX– A Global Market for Global Leaders

In total some 3 700 companies from 50 countries Market capitalization some 4 200 billion dollars

Health Care

18%

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 7

Financial Crisis, Transparency and new regulation

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

Financial crisis and regulation

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 9

Financial crisis and regulation

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 10

Financial crisis and regulation

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 11

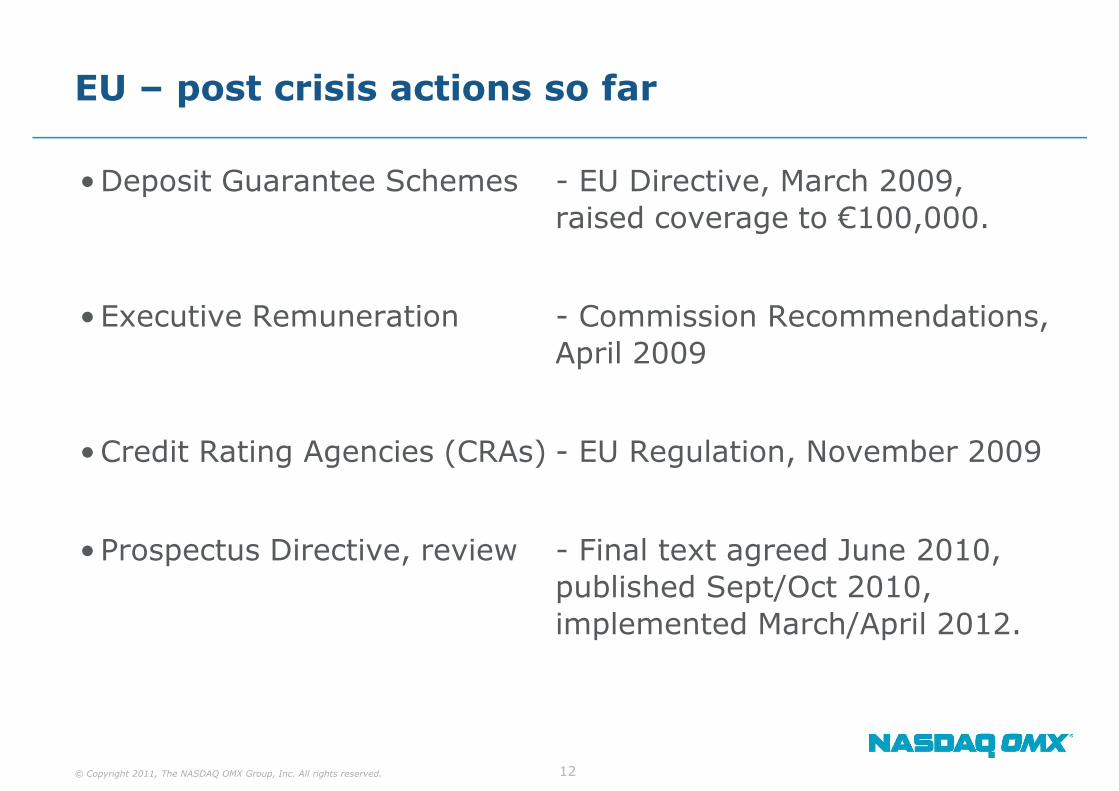

EU – post crisis actions so far

•Deposit Guarantee Schemes - EU Directive, March 2009,

raised coverage to €100,000.

•Executive Remuneration - Commission Recommendations,

April 2009

•Credit Rating Agencies (CRAs) - EU Regulation, November 2009

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

•Prospectus Directive, review - Final text agreed June 2010,

published Sept/Oct 2010,

implemented March/April 2012.

12

Market and Competition in Equity TradingMarket and Competition in Equity Trading=> Fragmentation and (less) Transparency

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

European Exchange landscape pre- and post -MiFID

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

Trading is gradually moving more apart from listing, market data and market surveillance services

Consolidation

Ownership consolidationFewer platforms

New ownersNew platforms

Fragmentation

14

Venues competing for order flow… unevenlyTrading Venues as defined by MiFID OTC

Regulated markets, i.e. stock exchanges

Multilateral trading facilities (MTF)

Systematic internalisers

Unclassified

broker dealer

“dark pools”

&

Lit Dark pools

&

crossing networks

•Athens Exchange

•BME

•Börse Berlin-Equiduct

•Bratislava SE

•Bucharest SE

•Budapest SE

•Bulgarian SE

•Cyprus SE

•Deutsche Börse

•Irish SE

•Ljubljana SE

•London SE Group

•Chi-X

•BATS Europe

•Burgundy

•Nasdaq OMX Europe

•NYSE Arca Europe

•Turquoise

•Euro TLX

•PEX

•Baikal (LSE)

•Chi-X Delta

•Euronext SmartPool

•SWX Swiss Block

•Instinet Block Match

•Liquidnet

•NYFIX Euro Millennium

•Pipeline Block Board

•Posit

•Turquoise Mid Point

•ABN Amro Bank

•BNP Paribas

•Citigroup Global

•Citigroup UK

•Credit Suisse

•Danske Bank

•Deutsche Bank

•Goldman Sachs

•Knight Equity Markets

International

•Nomura

•Nordea

CA Chevreux Alternative Crossing Engine

•Citi LIQUIFI

•Credit Suisse CrossFinder

•Goldman Sachs SIGMA X

•Knight Match

•Merrill Lynch MLNX

•Morgan Stanley Pool

•Société Général Alpha x Europe

•UBS PIN

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

•London SE Group

•Luxembourg SE

•Malta SE

•Nasdaq OMX

•NYSE Euronext

•Oslo Børs

•Plus Markets

•Prague SE

•SWX Europe

•SIX Swiss Exchange

•Warsaw SE

•Wiener Börse

•Turquoise Mid Point Cross

•Nasdaq OMX Europe

Neuro Dark

•Plus Markets Dark

•UBS

•UBS AG (London Branch)

•UBS PIN

15

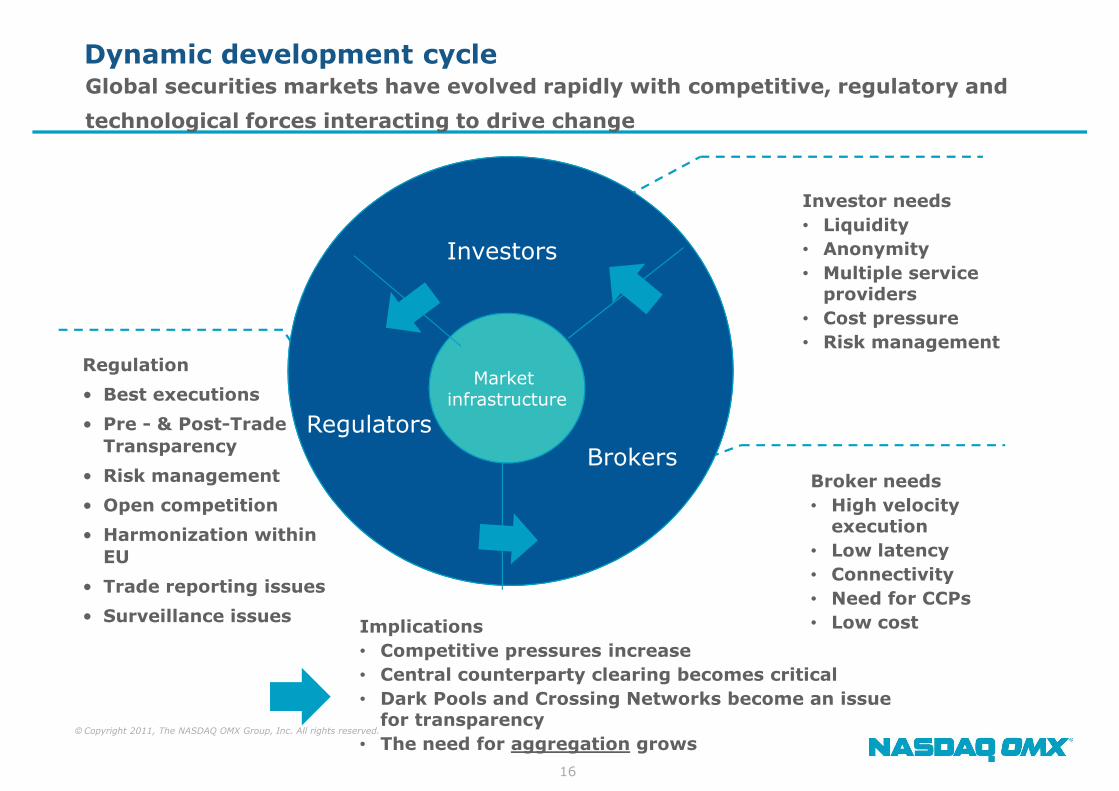

Dynamic development cycle

Investor needs

• Liquidity

• Anonymity

• Multiple service Investors

Global securities markets have evolved rapidly with competitive, regulatory and

technological forces interacting to drive change

Fragmented

securities

trading

landscape

Global

market for

blue chip

trading

Regulation

• Best executions

• Pre - & Post-Trade

Transparency

• Risk management

• Open competition

• Harmonization within

• Multiple service providers

• Cost pressure

• Risk management

Market infrastructure

Investors

Regulators

BrokersBroker needs

• High velocity execution

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

• Harmonization within

EU

• Trade reporting issues

• Surveillance issues

16

execution

• Low latency

• Connectivity

• Need for CCPs

• Low costImplications

• Competitive pressures increase

• Central counterparty clearing becomes critical

• Dark Pools and Crossing Networks become an issue for transparency

• The need for aggregation grows

European Equity Trading StatisticsDevelopment in Electronic Order Book TradingAugust 2007 – April 2011

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

Market Operator 2005 2006 2007 2008 2009 2010

1 London SE Group 1 541 2 216 3 133 2 601 1 270 2 084

European Equity Trading StatisticsElectronic Order Book Trading (EUR billion)2005 - 2010

2 Chi-X 50 658 858 1 536

3 NYSE Euronext 1 783 2 375 3 289 2 606 1 383 1 533

4 Deutsche Börse 1 125 1 593 2 443 2 192 1 084 1 237

5 Spanish Exchanges (BME) 848 1 151 1 666 1 243 898 1 031

6 SIX Swiss Exchange 543 692 1 008 957 530 595

7 NASDAQ OMX Nordic 544 776 1 037 818 499 568

8 BATS Europe 5 188 489

9 Turquoise 80 268 289

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

9 Turquoise 80 268 289

10 Oslo Børs 142 254 321 276 164 199

11 Burgundy 5 23

Domestic and Foreign figures are included. All the figures comply with the FESE Statistics Methodology.

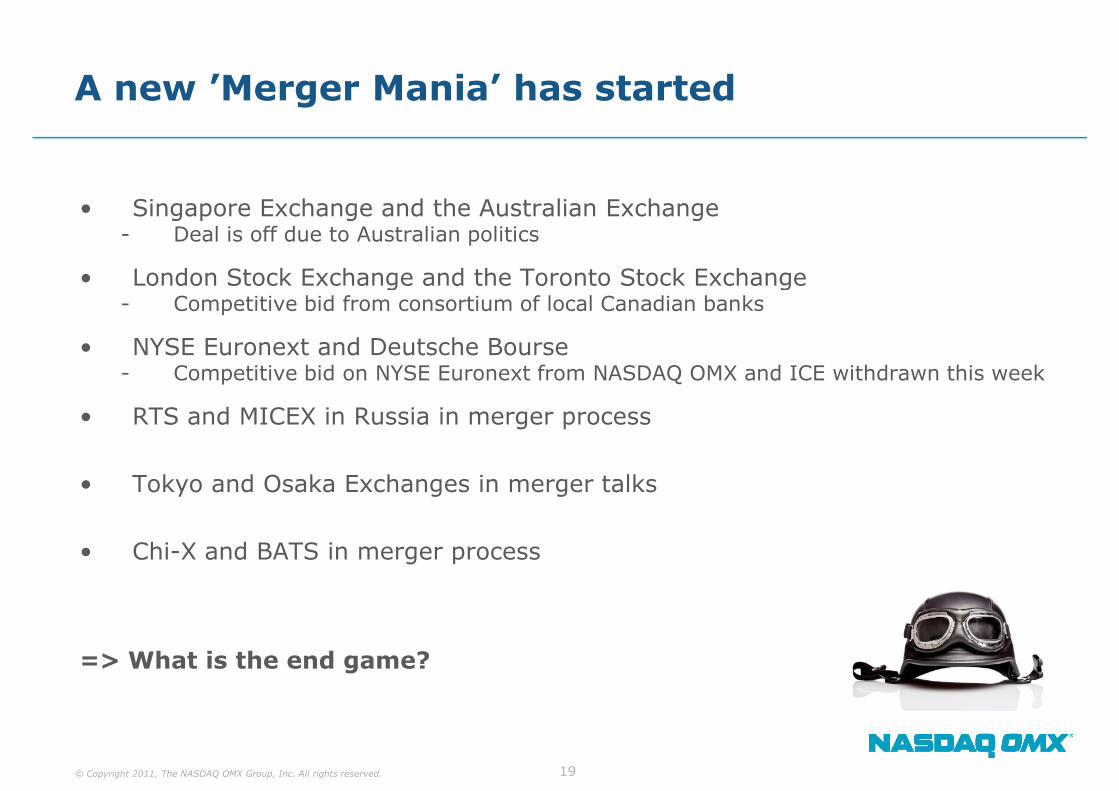

A new ’Merger Mania’ has started

• Singapore Exchange and the Australian Exchange- Deal is off due to Australian politics

• London Stock Exchange and the Toronto Stock Exchange • London Stock Exchange and the Toronto Stock Exchange - Competitive bid from consortium of local Canadian banks

• NYSE Euronext and Deutsche Bourse- Competitive bid on NYSE Euronext from NASDAQ OMX and ICE withdrawn this week

• RTS and MICEX in Russia in merger process

• Tokyo and Osaka Exchanges in merger talks

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

• Chi-X and BATS in merger process

=> What is the end game?

19

Conclusions and Long Term Vision

Regulation will cover more asset classes and will be tighter

Overall tighter

regulation

New Regulation for classes and will be tighter

We will see fewer trading venues

New Regulation for

more exotic products

like OTC derivatives

Consolidation to

continue

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

20

More instruments and asset classes will be available on trading venues

More broadly and

better organized

trading

What & How is NASDAQ OMX Nordic doing?

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

ADAPTING TO OPEN COMPETITION AND THE NEW HIGH SPEED ENVIRONMENT- CASE NORDIC MARKETS

STANDARDISATION OF THE NORDIC MARKETS TOTAL COST OF TRADING

DRAMATICALLY REDUCED

CCP LAUNCHED OCTOBER 2009

INET LAUNCHED FEBRUARY 2010

GENIUM INET FOR DERIVATIVES OCTOBER 2010

NORDIC@MID NOVEMBER 2010

REDUCED COST FOR OPERATING THE EXCHANGES = LOWER TRADING FEES

REDUCED COST FOR MARKET PARTICIPANTS = MORE VOLUMES

ENABLES ULTRA LOW LATENCY AND HIGH THROUGHPUT

SIGNIFICANT INCREASE IN INTEREST FROM ALGORITHMIC TRADERS

SIGNIFICANT INCREASE IN THE DEMAND FOR CO-LOCATION SERVICES

CCP-ONLY MEMBERSHIP

CO-LOCATION SERVICES

SPONSORED ACCESS WITH PRM TOOLS

22

Share trading value per day2005 – 2011

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

Total 3055 4197 5273 3657 2245 2528 2911

Includes both system (on book) and manual (off book) volume

NASDAQ OMX Nordic market sharesJanuary 2009 – April 2011

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

MTF MARKET SHARES IN THE NORDIC MARKET 2009 – 2011

16 %

18 %

20 %

6 %

8 %

10 %

12 %

14 %

Venues in Europe only and

auto match only

25

0 %

2 %

4 %

2009-01-02 2009-04-02 2009-07-02 2009-10-02 2010-01-02 2010-04-02 2010-07-02 2010-10-02

BATS Burgundy Chi-X Euronext Arca Turquoise XETRA

Note: Europe only and auto match only, excluding OTC.

Global Nokia market share in number of shares tradedJanuary 2001 – April 29, 2011

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

26

Continuously Declining Quoted Spreads

The introduction of CCP and INET technology, along with smaller tick sizes, have all made a meaningful contribution to lower quoted spreads.

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 27

spreads.

CCP introduced

INETintroduced

Algorithmic trading on the Helsinki Stock Exchange January 2007 – April 2011

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved. 28

HIGH FREQUENCY TRADING ON NASDAQ OMX NORDIC – BY TOTAL MARKET

”Pure” HFT is still far from US levels of roughly 2/3 of total volume.

HFT SHARE OF TOTAL TURNOVER ON

3 %

4 %

5 %

6 %

7 %

8 %

HFT SHARE OF TOTAL TURNOVER ON NASDAQ OMX NORDIC

29

0 %

1 %

2 %

3 %

70,00 %

DARK POOLSEurope 2.55% (Rosenblatt) US 15.92% (Rosenblatt)

Trading by Reuters trade classification (Finnish instruments)

63,29 %

24,75 %

20,00 %

30,00 %

40,00 %

50,00 %

60,00 %

% SHARE

0,12 %

5,01 %1,91 %

4,91 %

0,00 %

10,00 %

20,00 %

Order Book

- Lit Total

Order Book

- Hidden Total

Order Book

- Auction Total

Dark Order

Book Total

Off Order

Book Total

MiFID OTC

Total

30

Current challenges for a ”traditional” Exchange

• Behavioural and cultural change

- From a monopoly (... 97 years for the Helsinki Stock Exchange ...) to a market economy company in open competitionmarket economy company in open competition

• From a closed and product centric approach to a client centric and dynamic approach

- Moving from exchanges traditionally having heavy legacy structures to streamlined and efficient operations

• Systems, routines, processes, resources ...

• Competitive pressures

- The ’money’ is in trading (= transaction fees), hence that is where the competition is => What is left if you lose that battle?

- Alternative trading venues – both regulated (MTFs) and non-regulated- Alternative trading venues – both regulated (MTFs) and non-regulated

- Trend towards less transparent OTC markets in cash equities

• Need for level playing field, and need for tougher regulation

- Prepare for more intense competition in derivatives

• Pursuit new business opportunities in an open market

31

Strategic targets to differentiate

• NASDAQ OMX wants to be different

- We do things differently, we are not only about price, our value offering is different and unique, we are efficient, leading, local, and deliver on our different and unique, we are efficient, leading, local, and deliver on our brand perception

- Demonstrate our new-thinking and proactiveness

- Show initiatives that a ’perceived ex-monopoly’ would not typically do

• NASDAQ OMX perceived as innovator & driver of Nordic

market development

- Both in technology & trading models

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

• Business targets in the Nordic region

- Maintain & increase volume & velocity, attract new members & new trading patterns

- Support the business of members by introducing new attractive products & services and by offering sales support & customer education

32

TRADING FEE CHANGES

In total, Nordic Cash Equity trading fees have been cut by 43,8% since January 2008 !!In total, Nordic Cash Equity trading fees have been cut by 43,8% since January 2008 !!

33

We will continue to focus on our local presenceand service members and listed companies locally

Local legal

NASDAQ OMX Nordic

Listing Trading&

Marketdata

Local stakeholders

Local legalentity

Object for localsupervision

Customers

LocalSalesTeam

Local SalesTeam

LocalSalesTeam

Local management, local presence

&Clearing

data

Local public head

of exchange

Local Nordic

and Baltic

Offices

Sweden

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

of exchange

Denmark

Bjørn Sibbern

Finland

Lauri Rosendahl

Sweden

Jens Henriksson

Sweden

Denmark

Finland

Norway

Iceland

Estonia

Latvia

Lithuania

34

• Leveraging on INET and CCP - “Velocity is everything”1. Extended/improved functionalities on INET and Nordic Workstation

• Pre trade risk management tools• Volatility Guards

Focus areas for NASDAQ OMX Nordic in 2011

• Volatility Guards

2. Smart Order Routing in Nordic Equities – as the first Exchange in Europe

3. CCP Interoperability – move to open competition with 3 service providers

4. Non-displayed orders (Nordic @Mid) – large / mid / small caps

5. Market Access US & Canada to Local/Nordic members

• Improved service offering in Structured Products (ETFs, ETNs…)

• Norwegian Equities & Derivatives (full offering in 2011)

• Russian Derivatives

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

• Russian Derivatives

• Implementation of Genium INET for derivatives & fixed income

• Enhanced algorithmic service offering- Co-Location services- Sponsored Access with enhanced PRM tools- Non-regulated membership

35

The Market Access service offers NASDAQ OMX Nordic members

an efficient way to execute orders on other markets

Market Access – US & CanadaOverview

The service initially covers US and Canadian equities and certain

equity like securities like ETFs

All Market Access orders are sent to Citigroup for execution on the

relevant market

NASDAQ OMX Nordic provides network connectivity to CitigroupNASDAQ OMX Nordic provides network connectivity to Citigroup

Citigroup ensures execution according to US and Canadian rules

and regulations

36

No startup costs

No initial fee

Market Access – US & CanadaBenefits

No initial fee

No monthly fee

Competitive execution costs

Pay for executed orders only; i.e. no trade no pay

Easy implementation

Use existing network connectivity to NASDAQ OMX Nordic

Use existing INET Nordic FIX interface to NASDAQ OMXUse existing INET Nordic FIX interface to NASDAQ OMX

Flexible setup

Use as primary or backup execution tool

Choose between “Execution only” or “Execution to custody”

37

Conclusions for Nordics and (perhaps) implications for the Baltics

Intense competition will continue despite consolidation

Open competition

between many

different trading

venues is here to despite consolidation

Industry dynamics will continue to develop very quickly

venues is here to

stay

Latency race,

algorithmic trading,

HFT, sponsored

access, ...

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

38

NASDAQ OMX will continue to proactively develop new services and products at the forefront of the changing market dynamics

We are very well

positioned to drive

development to the

benefit of our

customers

TänanThank YouKiitos

© Copyright 2011, The NASDAQ OMX Group, Inc. All rights reserved.

39

KiitosTack