Strictly Private and Confidential

May 2009

Pension Fund Infrastructure Investments in Nigeria

Alternative, Impact and Growth

2Table of contents

1. Overview of Project Financing

2. Public Private Partnerships (PPPs)

3. Case study – Shuaibah IWPP, Saudi Arabia

Appendices

A. Introduction to Stanbic IBTC Bank

Section 1:

Overview of Project Financing

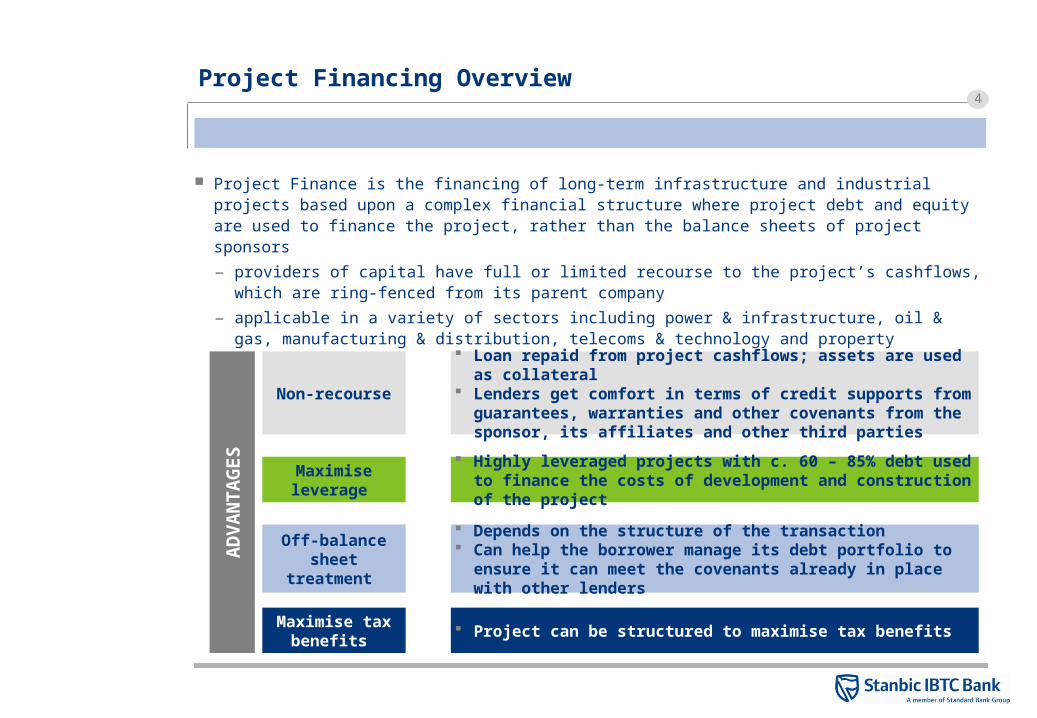

4Project Financing Overview

Project Finance is the financing of long-term infrastructure and industrial projects based upon a complex financial structure where project debt and equity are used to finance the project, rather than the balance sheets of project sponsors

– providers of capital have full or limited recourse to the project’s cashflows, which are ring-fenced from its parent company

– applicable in a variety of sectors including power & infrastructure, oil & gas, manufacturing & distribution, telecoms & technology and property

Non-recourse

Maximise leverage

Off-balance sheet treatment

Maximise tax benefits

Loan repaid from project cashflows; assets are used as collateral Lenders get comfort in terms of credit supports from guarantees,

warranties and other covenants from the sponsor, its affiliates and other third parties

Highly leveraged projects with c. 60 – 85% debt used to finance the costs of development and construction of the project

Depends on the structure of the transaction Can help the borrower manage its debt portfolio to ensure it can

meet the covenants already in place with other lenders

Project can be structured to maximise tax benefits

AD

VA

NT

AG

ES

5

Multi-currency

Multi-source

High Leverage

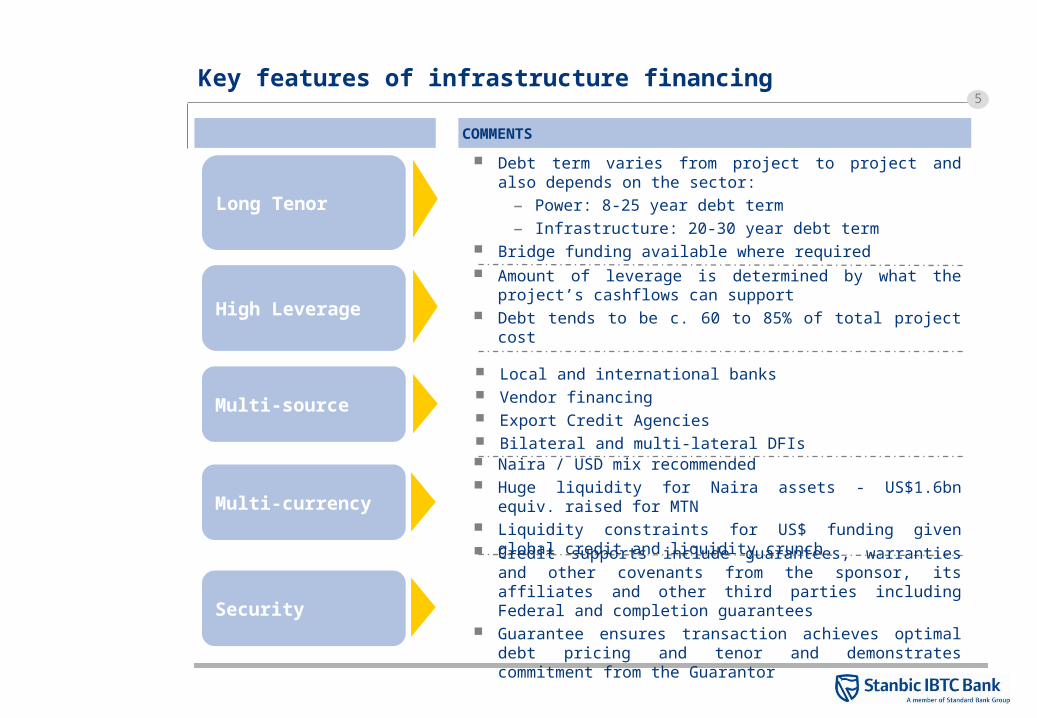

Key features of infrastructure financing

Amount of leverage is determined by what the project’s cashflows can support

Debt tends to be c. 60 to 85% of total project cost

Local and international banks Vendor financing Export Credit Agencies Bilateral and multi-lateral DFIs

Naira / USD mix recommended Huge liquidity for Naira assets - US$1.6bn equiv. raised for MTN Liquidity constraints for US$ funding given global credit and

liquidity crunch

COMMENTS

Long Tenor

Debt term varies from project to project and also depends on the sector:

– Power: 8-25 year debt term

– Infrastructure: 20-30 year debt term Bridge funding available where required

Security

Credit supports include guarantees, warranties and other covenants from the sponsor, its affiliates and other third parties including Federal and completion guarantees

Guarantee ensures transaction achieves optimal debt pricing and tenor and demonstrates commitment from the Guarantor

6Funding Sources

DEBT

EQUITY

Local Banks

International Banks

Regional Banks

ECAs

Capital Markets

Islamic Finance

Government

Foreign Partners

Local Private Sector

Pension funds

Recent entries = Infrastructure Funds, Sovereign Wealth Funds, Private Equity…

Up to 90% for strong PPPs and 80% max for typical Project financings…

Pension funds

Local Stock Market

7

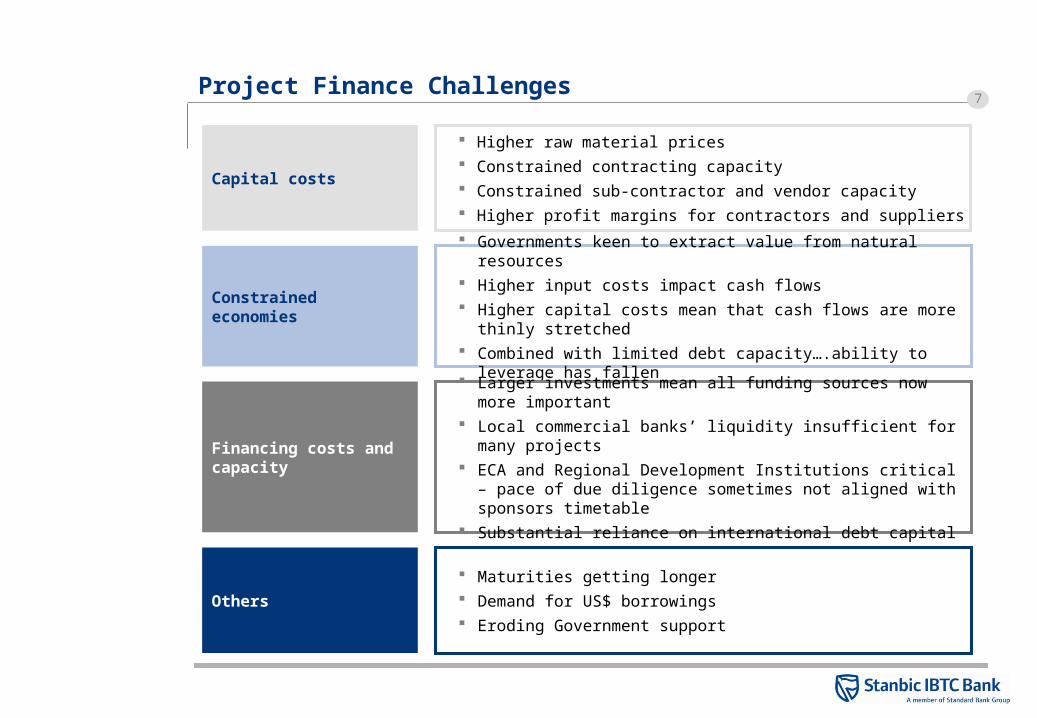

Higher raw material prices Constrained contracting capacity Constrained sub-contractor and vendor capacity Higher profit margins for contractors and suppliers

Project Finance Challenges

Capital costs

Governments keen to extract value from natural resources Higher input costs impact cash flows Higher capital costs mean that cash flows are more thinly stretched Combined with limited debt capacity….ability to leverage has fallen

Constrained economies

Larger investments mean all funding sources now more important Local commercial banks’ liquidity insufficient for many projects ECA and Regional Development Institutions critical – pace of due

diligence sometimes not aligned with sponsors timetable Substantial reliance on international debt capital

Financing costs and capacity

Maturities getting longer Demand for US$ borrowings Eroding Government support

Others

8Lessons learned

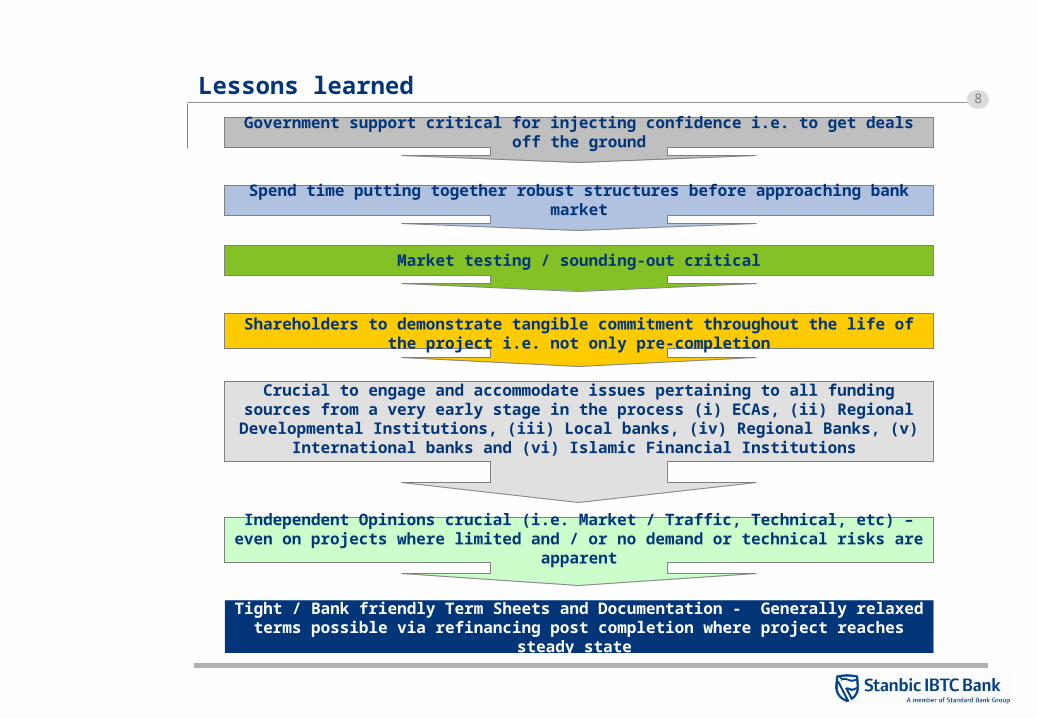

Spend time putting together robust structures before approaching bank market

Government support critical for injecting confidence i.e. to get deals off the ground

Market testing / sounding-out critical

Shareholders to demonstrate tangible commitment throughout the life of the project i.e. not only pre-completion

Tight / Bank friendly Term Sheets and Documentation - Generally relaxed terms possible via refinancing post completion where project reaches steady state

Crucial to engage and accommodate issues pertaining to all funding sources from a very early stage in the process (i) ECAs, (ii) Regional Developmental Institutions, (iii) Local

banks, (iv) Regional Banks, (v) International banks and (vi) Islamic Financial Institutions

Independent Opinions crucial (i.e. Market / Traffic, Technical, etc) – even on projects where limited and / or no demand or technical risks are apparent

9

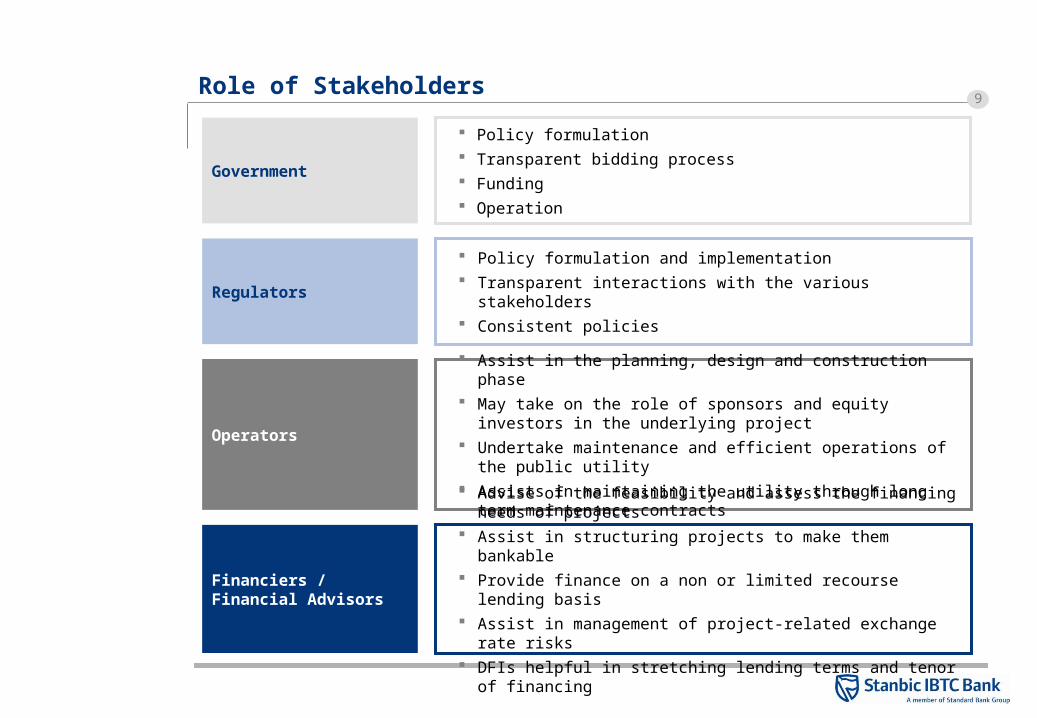

Policy formulation Transparent bidding process Funding Operation

Role of Stakeholders

Government

Policy formulation and implementation Transparent interactions with the various stakeholders Consistent policies

Regulators

Assist in the planning, design and construction phase May take on the role of sponsors and equity investors in the

underlying project Undertake maintenance and efficient operations of the public utility Assists in maintaining the utility through long term maintenance

contracts

Operators

Advise of the feasibility and assess the financing needs of projects Assist in structuring projects to make them bankable Provide finance on a non or limited recourse lending basis Assist in management of project-related exchange rate risks DFIs helpful in stretching lending terms and tenor of financing

Financiers / Financial Advisors

10

Section 2:

Public Private Partnerships (PPPs)

11Definition and Rationale for PPPs

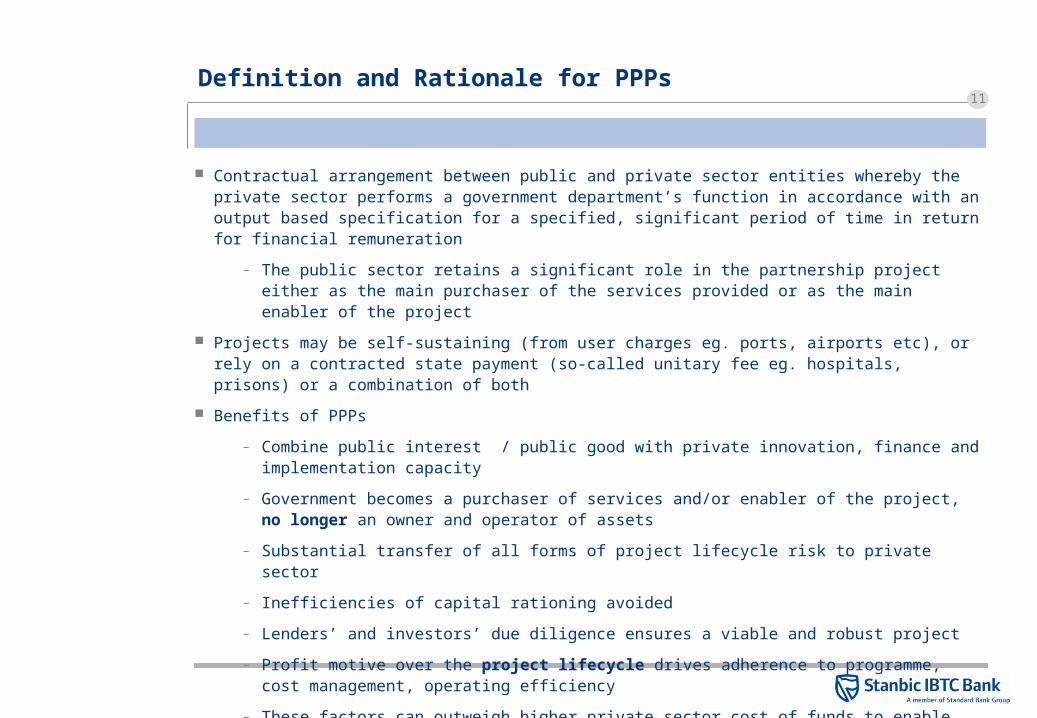

Contractual arrangement between public and private sector entities whereby the private sector performs a government department’s function in accordance with an output based specification for a specified, significant period of time in return for financial remuneration

– The public sector retains a significant role in the partnership project either as the main purchaser of the services provided or as the main enabler of the project

Projects may be self-sustaining (from user charges eg. ports, airports etc), or rely on a contracted state payment (so-called unitary fee eg. hospitals, prisons) or a combination of both

Benefits of PPPs

– Combine public interest / public good with private innovation, finance and implementation capacity

– Government becomes a purchaser of services and/or enabler of the project, no longer an owner and operator of assets

– Substantial transfer of all forms of project lifecycle risk to private sector

– Inefficiencies of capital rationing avoided

– Lenders’ and investors’ due diligence ensures a viable and robust project

– Profit motive over the project lifecycle drives adherence to programme, cost management, operating efficiency

– These factors can outweigh higher private sector cost of funds to enable value for money

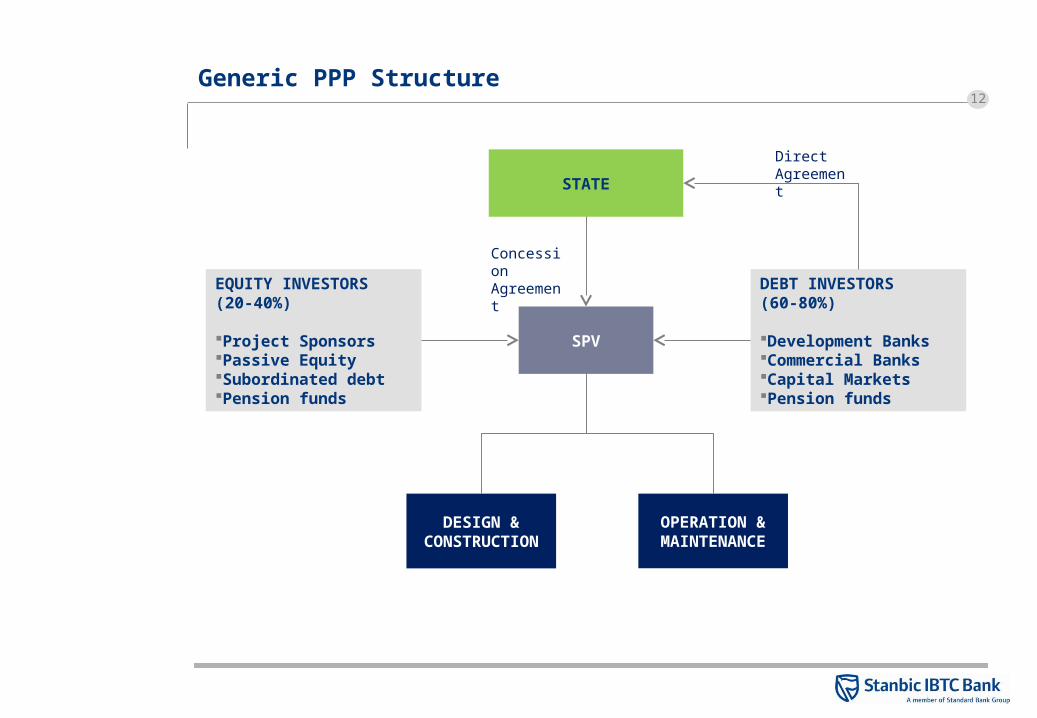

12Generic PPP Structure

EQUITY INVESTORS (20-40%) Project Sponsors Passive EquitySubordinated debt Pension funds

DEBT INVESTORS (60-80%) Development Banks Commercial Banks Capital MarketsPension funds

SPV

DESIGN & CONSTRUCTION

OPERATION & MAINTENANCE

STATE

Direct Agreement

Concession

Agreement

13

Notion of “the private sector providing a public service” must be understood and accepted at both national and local government levels, as well as traditional leadership

Willingness to overcome vested interests for the change in delivery mode, and, in some cases, motivate a new charging regime

Committed project champions in the concession granting authority to obtain support and approvals across the range of public stakeholders

State capital contributions and/or revenue support

Success Factors

Political Support

Legal and Institutional Capacity

Need developers and contractors who respond to tenders with adequate resources and commitment – to get value for money and delivery

Too many tenders attract too few bidders – why? A global boom in power and infrastructure – supply side constraints Quality and efficiency of tender process critical

Willing and Able Developers

Legal capacity to grant concessions Necessary ownership of existing asset to confer a concession over it Financial capacity to meet any financial liabilities under the concession (or

else bind the State) Institutional capacity to negotiate and manage concession agreements

14

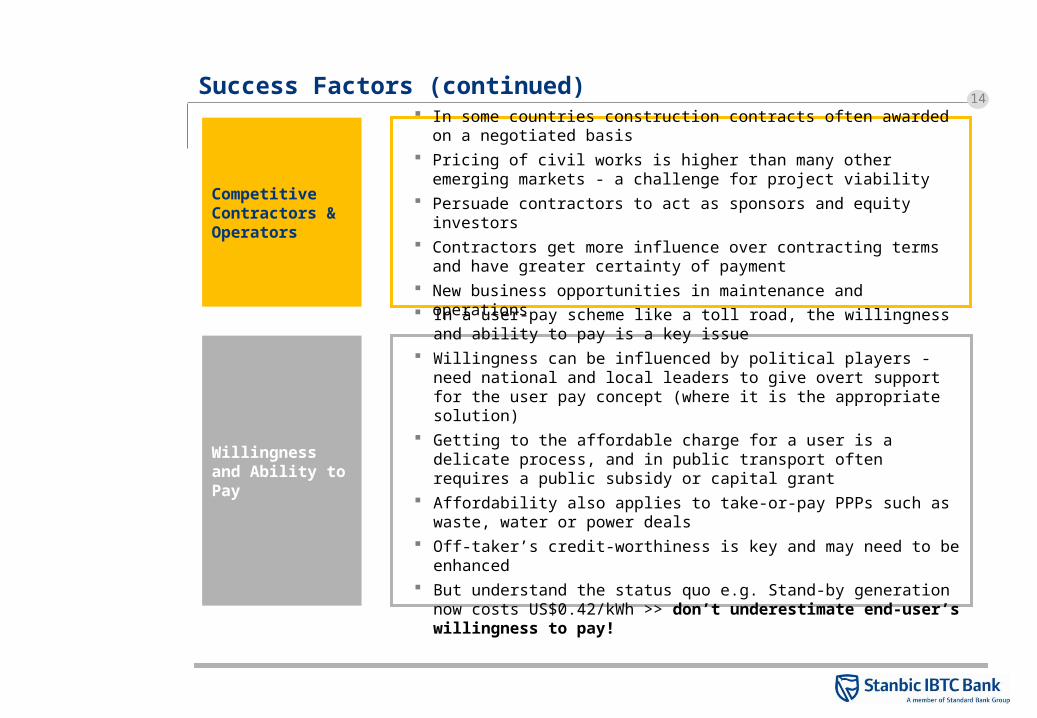

In some countries construction contracts often awarded on a negotiated basis

Pricing of civil works is higher than many other emerging markets - a challenge for project viability

Persuade contractors to act as sponsors and equity investors Contractors get more influence over contracting terms and have greater

certainty of payment New business opportunities in maintenance and operations

Success Factors (continued)

Competitive Contractors & Operators

Willingness and Ability to Pay

In a user-pay scheme like a toll road, the willingness and ability to pay is a key issue

Willingness can be influenced by political players - need national and local leaders to give overt support for the user pay concept (where it is the appropriate solution)

Getting to the affordable charge for a user is a delicate process, and in public transport often requires a public subsidy or capital grant

Affordability also applies to take-or-pay PPPs such as waste, water or power deals

Off-taker’s credit-worthiness is key and may need to be enhanced But understand the status quo e.g. Stand-by generation now costs

US$0.42/kWh >> don’t underestimate end-user’s willingness to pay!

15

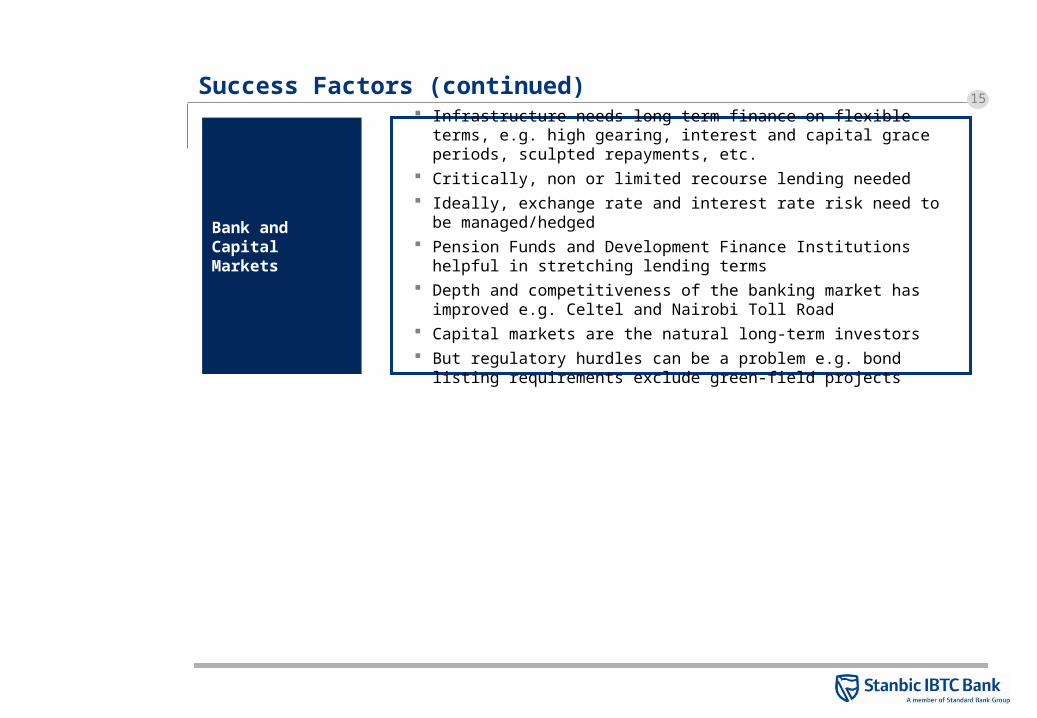

Infrastructure needs long term finance on flexible terms, e.g. high gearing, interest and capital grace periods, sculpted repayments, etc.

Critically, non or limited recourse lending needed Ideally, exchange rate and interest rate risk need to be managed/hedged Pension Funds and Development Finance Institutions helpful in stretching

lending terms Depth and competitiveness of the banking market has improved e.g. Celtel

and Nairobi Toll Road Capital markets are the natural long-term investors But regulatory hurdles can be a problem e.g. bond listing requirements

exclude green-field projects

Success Factors (continued)

Bank and Capital Markets

16Lessons Learned – Let’s move on!

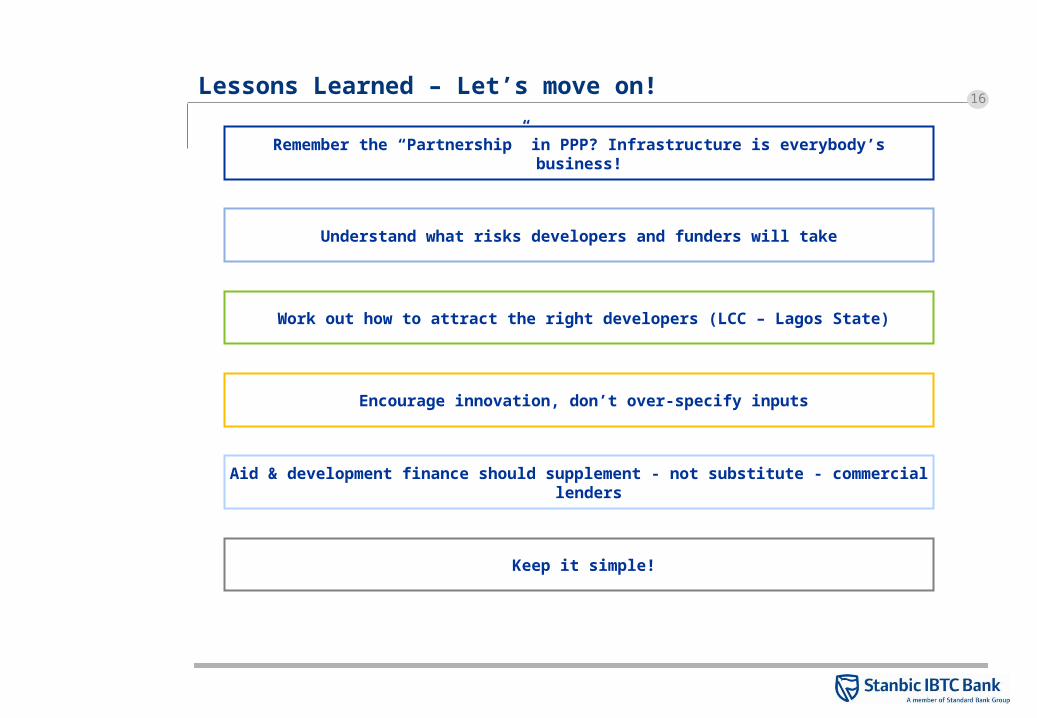

Remember the “Partnership” in PPP? Infrastructure is everybody’s business!

Understand what risks developers and funders will take

Work out how to attract the right developers (LCC – Lagos State)

Encourage innovation, don’t over-specify inputs

Aid & development finance should supplement - not substitute - commercial lenders

Keep it simple!

17

Section 3:

Case study – Shuaibah IWPP, Saudi Arabia

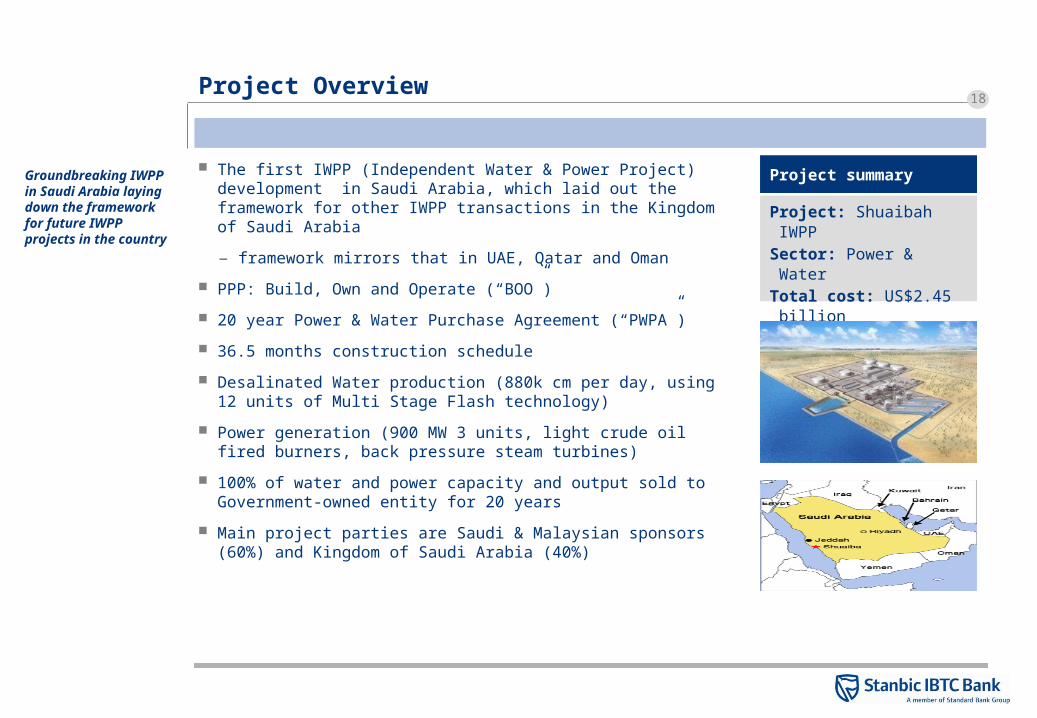

18Project Overview

The first IWPP (Independent Water & Power Project) development in Saudi Arabia, which laid out the framework for other IWPP transactions in the Kingdom of Saudi Arabia

– framework mirrors that in UAE, Qatar and Oman

PPP: Build, Own and Operate (“BOO”)

20 year Power & Water Purchase Agreement (“PWPA”)

36.5 months construction schedule

Desalinated Water production (880k cm per day, using 12 units of Multi Stage Flash technology)

Power generation (900 MW 3 units, light crude oil fired burners, back pressure steam turbines)

100% of water and power capacity and output sold to Government-owned entity for 20 years

Main project parties are Saudi & Malaysian sponsors (60%) and Kingdom of Saudi Arabia (40%)

Groundbreaking IWPP in Saudi Arabia laying down the framework for future IWPP projects in the country

Project summary

Project: Shuaibah IWPP Sector: Power & WaterTotal cost: US$2.45 billionDebt term: 20 years

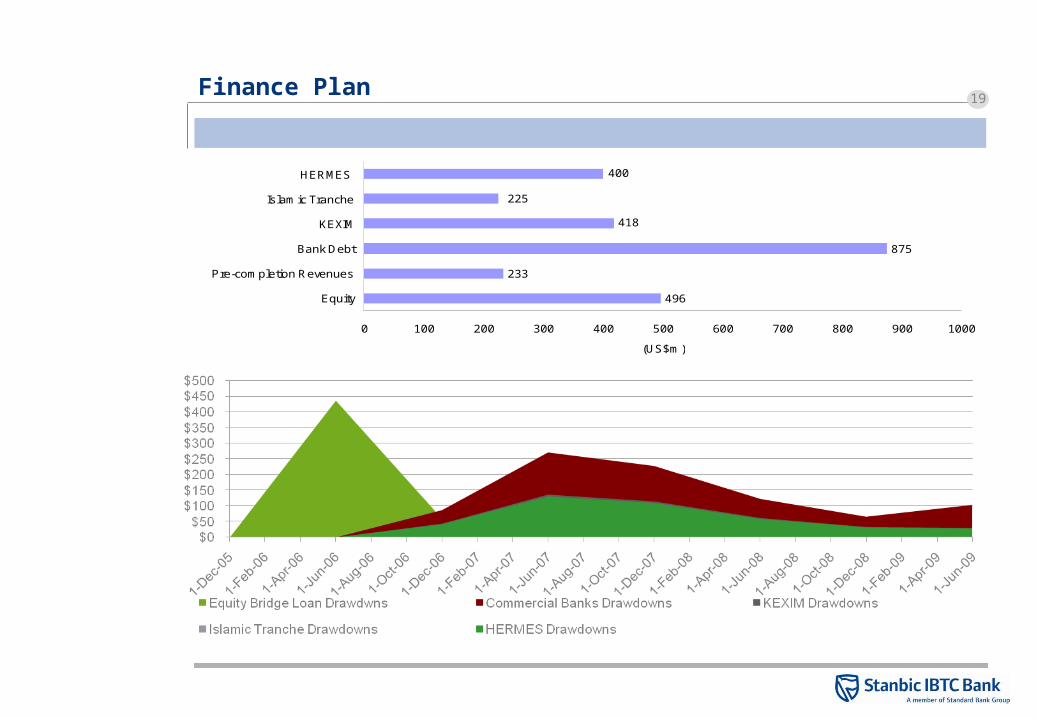

19Finance Plan

496

233

875

418

225

400

0 100 200 300 400 500 600 700 800 900 1000

Equity

Pre-completion Revenues

Bank Debt

KEXIM

Islamic Tranche

HERMES

(US$m)

20Ownership Structure

Combination of public and private sector ownership

SHUAIBAH Water & Electricity Company(Project Company / Borrower)

PRIVATE SECTOR ENTITIES GOVERNMENT OWNED ENTITIES

Public Investment Fund

Saudi Electricity Company

Saudi Sponsors

Malaysia

Sponsors

Saudi Malaysia Water & Electricity Co Ltd (Project developer / Bidder)

60%

50%32% 8%

32%

30%

12%

12%

8%6% PIF

ACWA Power Projects

Khazanah

Malakoff

SEC

Tenega Nasional Berhad

21

Patrick Okey Mgbenwelu – Head, Project Finance – Stanbic IBTC Bank [email protected]

Nigeria:Stanbic IBTC Bank Plc,

IBTC Place, Walter Carrington Crescent, P. O. Box 71707, Victoria Island, Lagos State

Tel: 01 – 448 – 8900

Fax: 01 – 448 – 8902

Mob: 0703 – 413 – 6835

www.stanbicibtcbank.com

THANK YOU

22

Appendix A

Introduction to Stanbic IBTC Bank

23Stanbic IBTC Bank

Stanbic IBTC Bank, a product of the merger between IBTC Chartered Bank Plc and Stanbic Bank Nigeria Limited, is Nigeria’s premier investment bank with a wealth of experience in advisory, privatisations and capital markets

The bank also has excellent corporate and retail banking capabilities and a network of over 60 branches in all the major cities and commercials centres spread across the geo-political zones of Nigeria

Being a member of the Standard Bank Group means that Stanbic IBTC is part of a strong global banking network

Fitch recently upgraded Stanbic IBTC’s National Long and Short-term ratings to 'AAA(nga)' from 'A(nga)' and to 'F1+(nga)' from 'F1(nga)', respectively – only local bank with a Fitch AAA rating

Stanbic IBTC Bank is the parent of Stanbic IBTC Pension Managers, Nigeria’s largest PFA and Stanbic IBTC Asset management Limited, Nigeria’s largest non-pension asset managers

Stanbic IBTC is among the 15 Primary Dealers / Market Makers recently appointed by the Debt Management Office to trade in government securities and appointed along with 13 other banks to manage Nigeria’s foreign reserves

Stanbic IBTC Bank is the parent of Stanbic IBTC Pension Managers, Nigeria’s largest PFA and Stanbic IBTC Asset management Limited, Nigeria’s largest non-pension asset managers

Overview

Selected Accolades

Stanbic IBTC is the only local bank with a Fitch AAA rating

Best Debt House: Euromoney Excellence Award 2008

Best Issuing House: Thisday Awards 2008

Best Issuing House in Africa: African Banker Awards 2007

Best Fund Manager, Nigeria: ThisDay 2005

Euromoney Project Finance Magazine ‘Deal of the Year’ Awards:

– African PPP: Lekki-Epe Expressway (2008)

– African Telecoms / Mobile: MTN Nigeria US$2bn Fund raising (2007)

Local knowledge supported by a global network and expertise

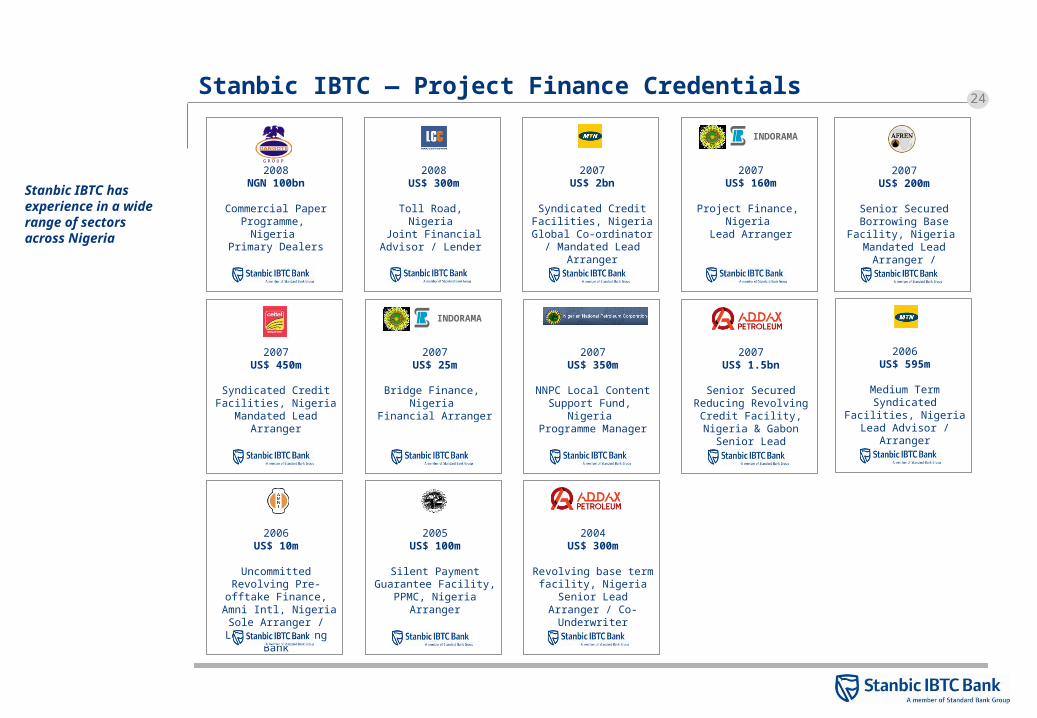

24Stanbic IBTC ― Project Finance Credentials

2008US$ 300m

Toll Road, Nigeria

Joint Financial Advisor / Lender

2007US$ 2bn

Syndicated Credit Facilities, Nigeria

Global Co-ordinator / Mandated Lead Arranger

2007US$ 160m

Project Finance, Nigeria

Lead Arranger

INDORAMA

2006US$ 595m

Medium Term Syndicated Facilities,

NigeriaLead Advisor / Arranger

2004US$ 300m

Revolving base term facility, Nigeria

Senior Lead Arranger / Co-Underwriter

2007US$ 350m

NNPC Local Content Support Fund,

Nigeria Programme Manager

2007US$ 25m

Bridge Finance, Nigeria

Financial Arranger

INDORAMA

2007US$ 450m

Syndicated Credit Facilities, Nigeria

Mandated Lead Arranger

2007US$ 1.5bn

Senior Secured Reducing Revolving

Credit Facility, Nigeria & Gabon

Senior Lead Arranger

2006US$ 10m

Uncommitted Revolving Pre-offtake Finance, Amni Intl, Nigeria

Sole Arranger / Lender / Hedging Bank

2005US$ 100m

Silent Payment Guarantee Facility,

PPMC, NigeriaArranger

2008NGN 100bn

Commercial Paper Programme,

Nigeria Primary Dealers

GROUP

Stanbic IBTC has experience in a wide range of sectors across Nigeria

2007US$ 200m

Senior Secured Borrowing Base Facility,

Nigeria Mandated Lead Arranger

/ Underwriter

25Disclaimer

Confidentiality and disclaimer

This document is provided on the express understanding that the information contained herein will be regarded and treated as strictly confidential and proprietary to Stanbic IBTC Bank Plc (“Stanbic IBTC”), its holding company Standard Bank of South Africa, and the subsidiaries of its holding company (“the Standard Bank Group”). By retaining it the recipient undertakes that it is not to be delivered and nor shall its contents be disclosed to anyone other than the intended recipient, and nor shall it be reproduced or used, in whole or in part, for any purpose other than for the purpose described herein, without the prior written consent of Standard Bank.Whilst every effort has been made to ensure the accuracy and completeness of the information contained in this document, no responsibility is accepted by the Standard Bank group for the treatment by any court of law, tax, banking or other authorities in any jurisdiction of any transaction based on the information contained herein. There may be tax implications to consider in any transaction and these should be identified and understood before investing. Separate tax advice should therefore be sought when appropriate. Should anything contained herein contribute to the acquisition of a financial product the following must be noted: there are intrinsic risks involved in transacting in any products; no guarantee is provided for the investment value in a product; any forecasts based on hypothetical data are not guaranteed and are for illustrative purposes only; returns may vary as a result of their dependence on the performance of underlying assets and other variable market factors and past performances are not necessarily indicative of future performances. Any client that is not a merchant banking client as defined in the Financial Advisory and Intermediary Services Act must note that unless a financial needs analysis has been conducted to assess the appropriateness of any product, investment or structure to its circumstances, there may be limitations on the appropriateness of any information provided by a member of the Standard Bank group and careful consideration must be given to the implications of entering into any transaction, with or without the assistance of an investment professional.