Download - Students Lecture1

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 1/67

Department of Accounting and Finance Slide 1

ACC 1000

Principles of Accounting and Finance

Lecturer John Gerrand

Topic 1

Accounting in Action

Reference: Principles of Accounting and Finance (Second edition)(Carey 2010) Chapter 1

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 2/67

Department of Accounting and Finance Slide 2

Learning ObjectivesAt the end of this topic you should be able to:

1. explain what accounting is;

2. identify the users and uses of accounting;

3. understand how accounting standards have been regulated and developed;

4. explain the nature of a reporting entity;

5. state the basic accounting equation, and define assets, liabilities and owner ’s

equity;

6. understand the two recognition criteria that must be met before an item can beincluded in the financial statements;

7 Apply to an unusual transaction

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 3/67

Department of Accounting and Finance Slide 3

Lecture Overview

• What is accounting?

• Why is accounting important?

• The accounting ‘conceptual framework’

• The elements definition and recognition criteria

• How to account for unusual transactions

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 4/67

Department of Accounting and Finance Slide 4

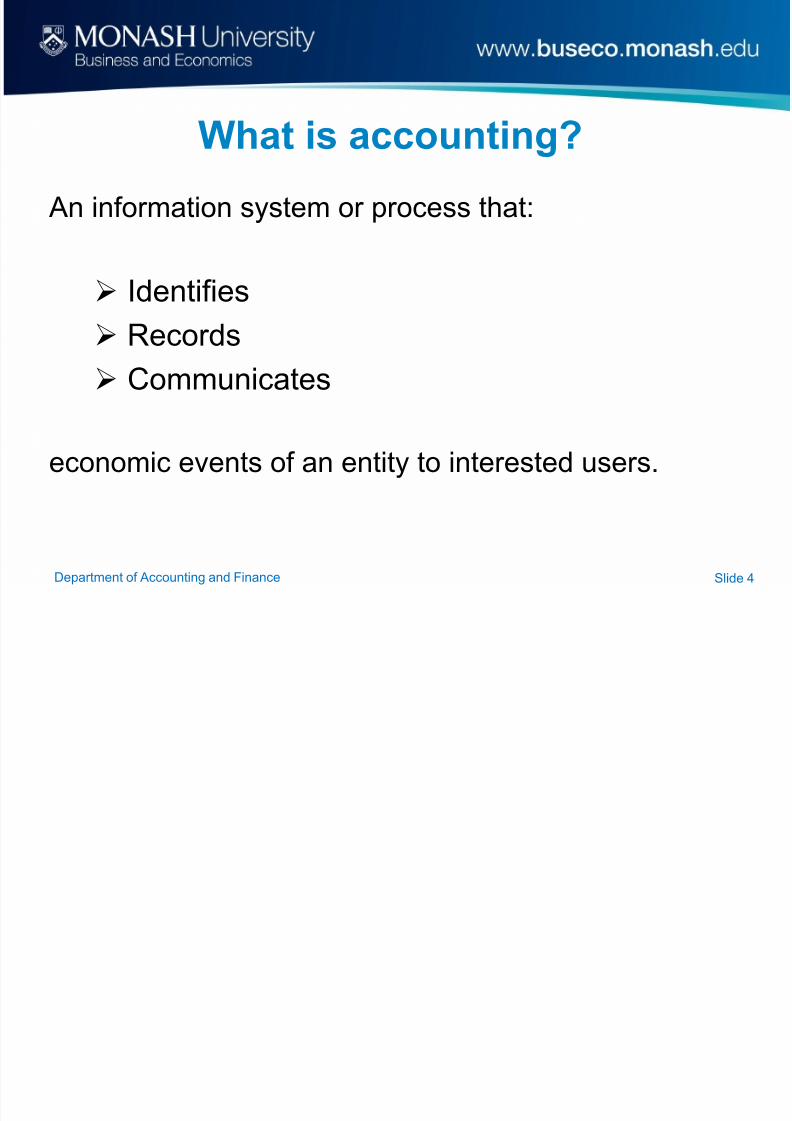

What is accounting?

An information system or process that:

Identifies

Records

Communicates

economic events of an entity to interested users.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 5/67

What is Accounting? (continued)

The Accounting Process

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 6/67

Department of Accounting and Finance Slide 6

Why is Accounting Important ?

Accounting information conveys information aboutbusiness performance to others.

Decisions are made based on the informationprovided.

Poor accounting practices by businesses canproduce information that is inaccurate or misleading.

This can lead to corporate collapses and financialruin for many people involved.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 7/67Department of Accounting and Finance Slide 7

The role of accounting

To assist people in making decisions about theallocation of scarce resources.

Accounting measures business activity, andprocesses it into reports to enable communication of

the information to users who are internal orexternal to the entity.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 8/67Department of Accounting and Finance Slide 8

Internal usersManagers who plan, organise and run the business

e.g., marketing managers, production supervisors, chieffinancial officers, other employees.

Detailed and frequent information is needed by these

managers to make business decisions on a day-by-day basis.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 9/67Department of Accounting and Finance Slide 9

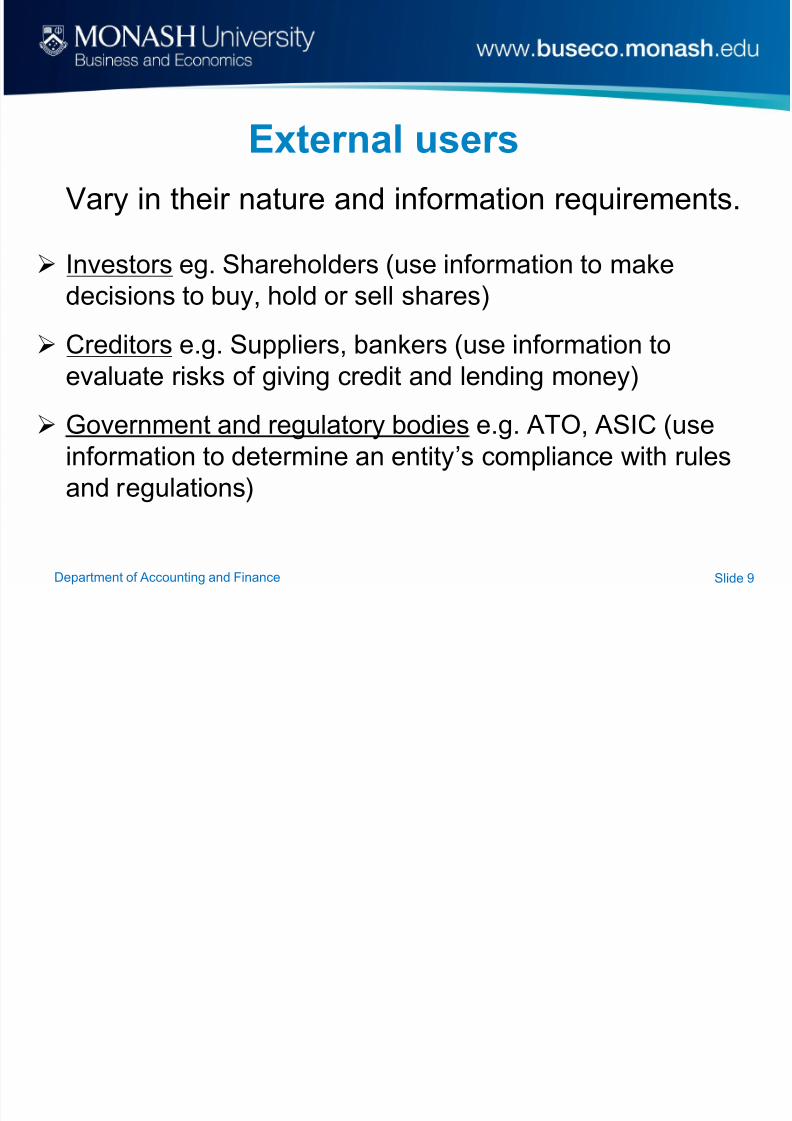

External usersVary in their nature and information requirements.

Investors eg. Shareholders (use information to makedecisions to buy, hold or sell shares)

Creditors e.g. Suppliers, bankers (use information toevaluate risks of giving credit and lending money)

Government and regulatory bodies e.g. ATO, ASIC (useinformation to determine an entity’s compliance with rulesand regulations)

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 10/67Department of Accounting and Finance Slide 10

History of regulation of accounting

Over time, Generally Accepted AccountingPrinciples (GAAP) have developed to guide the

practice of accounting.

As entities grew in size and complexity, moreformal rules for accounting were required.

Today, ‘accounting standards’ are mandatory formany entities to follow in the preparation offinancial statements.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 11/67Department of Accounting and Finance Slide 11

History of regulation of accounting(continued)

Australia has adopted standards that are consistent with thoseproduced by the International Accounting Standards Board (IASB).

The current trend in accounting standard setting is to follow globalstandards. IASB is promoting this global covergence. Australia's

accounting standards are consistent with these globaldevelopments(http://www.ifrs.org/Use+around+the+world/Use+around+the+world.htm).

While these accounting standards provide ‘rules’ for dealing withvarious accounting issues, there exists an underlying ‘conceptualframework’ upon which the standards are based.

This framework attempts to derive a theory for determining theinformation to be provided in financial statements.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 12/67Department of Accounting and Finance Slide 12

The Australian Conceptual Framework (ACF)in summary: (there are 3 components)

• SAC 1 defines a ‘reporting entity’ ie who needs toreport.

• SAC 2 provides the objective of general purposefinancial reporting.

• The Framework explains the qualitativecharacteristics of information, and the constraintson preparation, as well as defining the fiveelements of accounting and the criteria for their

recognition.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 13/67Department of Accounting and Finance Slide 13

Statement of Accounting Concepts (SAC)1(1st component of ACF)

Definition of the Reporting Entity

Defines a ‘Reporting Entity’ as any entity in which itis reasonable to expect the existence of users whodepend on general-purpose financial statements for

information to enable them to make economicdecisions.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 14/67

Process for determ ining a repo rt ing ent i ty

For each user group, ask two questions:

1. Do they need the information?

2. Do they have the power to get it?

If they need the information and do not have the

power to get it – they are a dependant usergroup

AND thus the ent i ty is a report ing ent i ty.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 15/67Department of Accounting and Finance Slide 15

SAC 1 (continued)

Factors to help determine whether dependentusers are likely to exist:

Separation of management from economicinterest

Economic or political importance /influence

Financial characteristics

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 16/67Department of Accounting and Finance Slide 16

Why is this definition important?

Entities defined as ‘reporting entities’ mustproduce general purpose financial statements in

compliance with accounting standards and makethem publicly available so the dependent userscan access the information for their decisionmaking.

Not all entities are reporting entities, even thoughthey produce annual financial statements.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 17/67

Balance Learning Exercise

The Reporting Entity

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 18/67

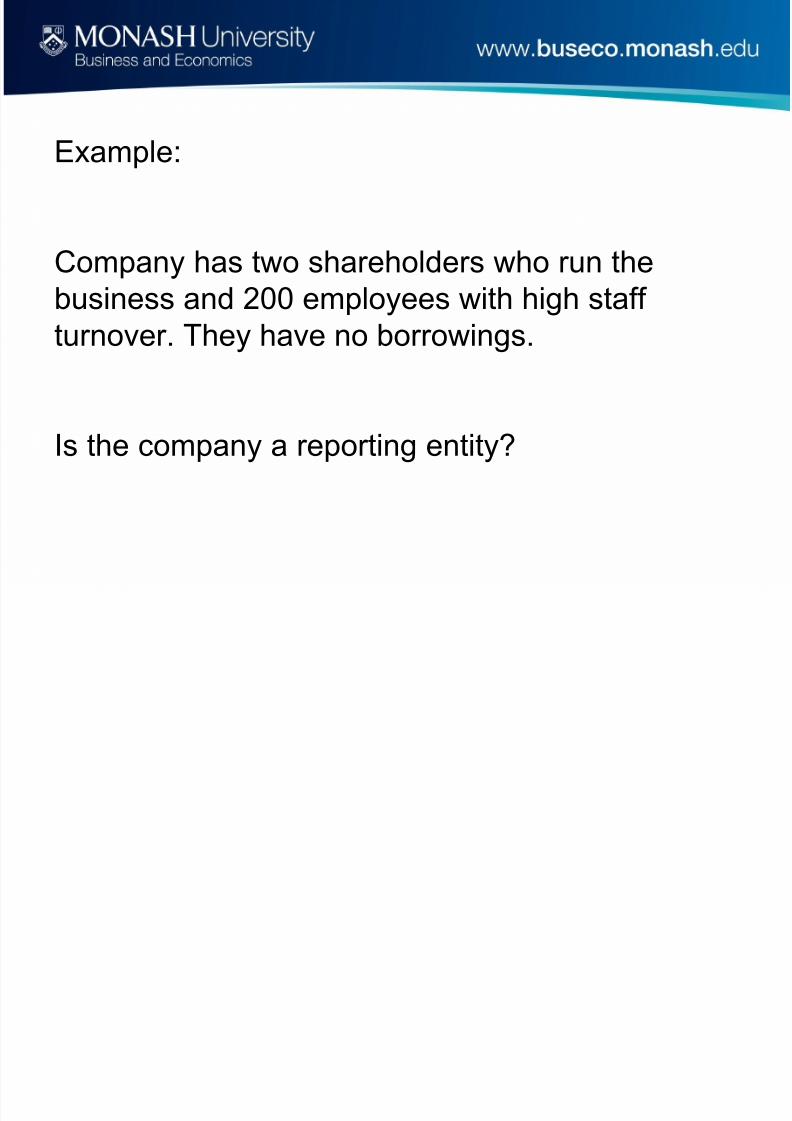

Example:

Company has two shareholders who run thebusiness and 200 employees with high staffturnover. They have no borrowings.

Is the company a reporting entity?

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 19/67

Process for determ ining a repo rt ing ent i ty

For each user group, ask two questions:

1. Do they need the information?

2. Do they have the power to get it?

If they need the information and do not have the

power to get it – they are a dependant usergroup

AND thus the ent i ty is a report ing ent i ty.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 20/67

Process

User Group Need Power

Shareholders

Employees

Conclusion: it is a reporting entity?

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 21/67

Department of Accounting and Finance Slide 21

Statement of Accounting Concepts (SAC) 2(2nd component of ACF)

Objective of General Purpose Financial Reporting

General purpose financial reporting focuses onproviding information to meet the commoninformation needs of users who are unable tocommand the preparation of reports tailored to their

particular information needs.

This highlights the fact that reports are prepared fordependent users.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 22/67

Department of Accounting and Finance Slide 22

AASB Framework(3rd component of ACF)

Adapted from the IASB Framework, it contains thefollowing:

Objective of financial reports

Assumptions underlying financial reports

Qualitative characteristics of financial reports

Elements of financial reports

Recognition criteria for the elements of financialstatements.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 23/67

Department of Accounting and Finance Slide 23

AASB Framework –

objectives offinancial reports

To provide information:

About the financial position, performance andcash flows of an entity that is useful in makingeconomic decisions.

Showing the results of accountability ofmanagement for the resources entrusted to it.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 24/67

Department of Accounting and Finance Slide 24

AASB Framework – assumptions

underlying financial reports

Accrual Basis

Going concern

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 25/67

Department of Accounting and Finance Slide 25

AASB Framework – qualitativecharacteristics of financial reports

Provide guidance for entities that need to preparefinancial statements as to the qualities of theinformation that should be contained in them.

The two fundamental characteristics are relevance and faithful representation (the latter is proposedto replace the current qualitative characteristic of‘reliability’)

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 26/67

Department of Accounting and Finance Slide 26

AASB Framework –

elements of financialstatements

There are five elements of accounting:

Assets

Liabilities

Owner ’s Equity

Income Expenses

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 27/67

Department of Accounting and Finance Slide 27

1. AssetsDefinition:

“… a resource controlled by the entity as a result of apast transaction or other past events and from which

future economic benefits are expected to flow to theentity”

Essential characteristics:

Future economic benefits

Under control of entity (rather than ‘owned’)

Result of past transaction

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 28/67

Assets - Example

‘Mike’s Inner City Cab Service’

purchased a taxi for $49,000 to carry

passengers around Melbourne.

Does the taxi meet the definition of asset?

Provides future economic benefits

Controlled by Mike Result of a past transaction

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 29/67

Department of Accounting and Finance Slide 29

2. LiabilitiesDefinition:

“… a present obligation of the entity arising from pastevents, the settlement of which is expected to result in an

outflow from the entity of resources embodying economicbenefits”

Essential characteristics:

Future sacrifice

Present obligation

Result of past transaction

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 30/67

Department of Accounting and Finance Slide 30

Liabilities - Example

‘Mike’s Inner City Cab Service’ borrowed$43,000 from the State Bank to purchase

the taxi.

Does the bank loan meet the definition ofliability?

A present obligation exists A future sacrifice will be requiredResult of a past transaction

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 31/67

Department of Accounting and Finance Slide 31

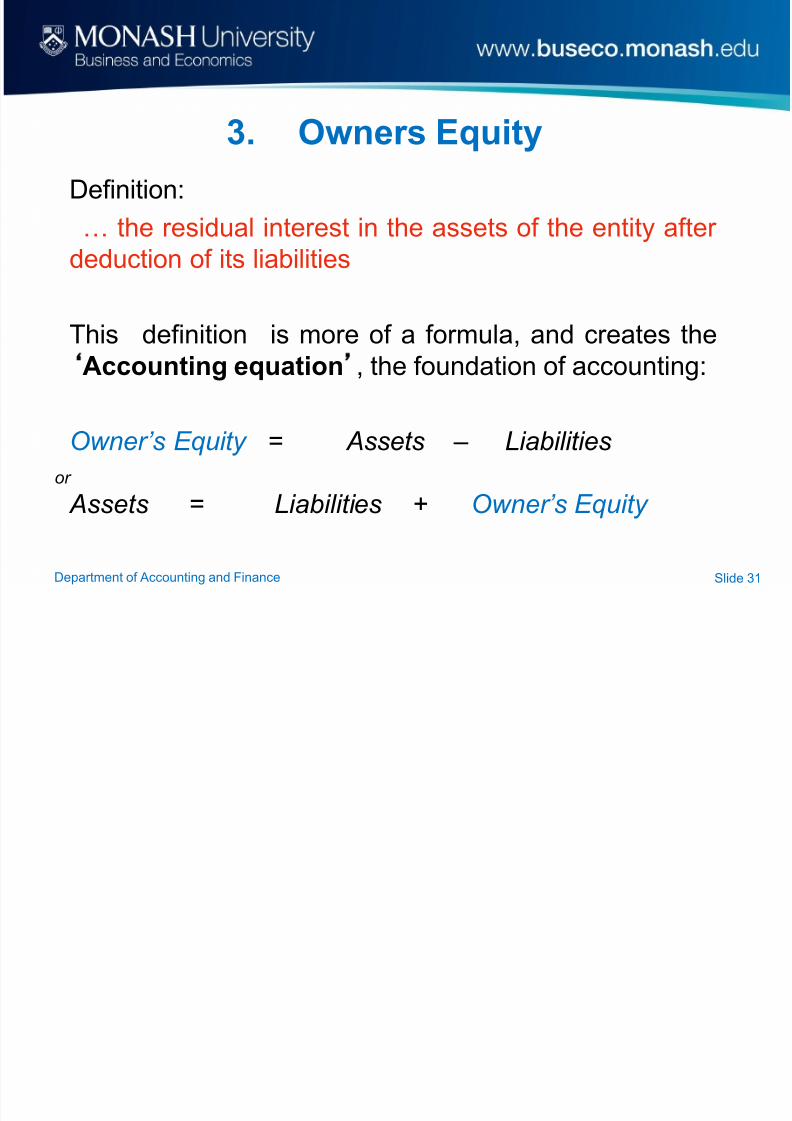

3. Owners EquityDefinition:

“… the residual interest in the assets of the entity afterdeduction of its liabilities”

This ‘definition’ is more of a formula, and creates theAccounting equation , the foundation of accounting:

Owner ’ s Equity = Assets – Liabilities

or

Assets = Liabilities + Owner ’ s Equity

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 32/67

Department of Accounting and Finance Slide 32

Owner ’s Equity - Example

‘Mike’s Inner City Cab Service’ has a taxi worth $49,000,and a bank loan of $43,000 owing to the State Bank.

What is Mike’

s owner ’

s equity?

Owner ’s Equity = Assets - Liabilities

6000 = $49,000 - $43,000

This is Mike’s personal contribution to commence hisbusiness.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 33/67

Department of Accounting and Finance Slide 33

4. Income (revenue)

Definition:

“… increases in economic benefits during the accountingperiod in the form of inflows or enhancements of assets

or decreases of liabilities that result in increases in equity,other than those relating to contributions from equityparticipants”

Essential characteristics:

An increase in economic benefits

Result in an increase in equity, but

Excludes owner ’s contributions of equity

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 34/67

Income - Example

‘Mike’s Inner City Cab Service’

charged a passenger $10 for a short

trip in Melbourne.

Does the taxi fare meet the definition of income?

Inflow of economic benefits (cash)

Contributes to an increase in equity

Was NOT contributed by Mike

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 35/67

Department of Accounting and Finance Slide 35

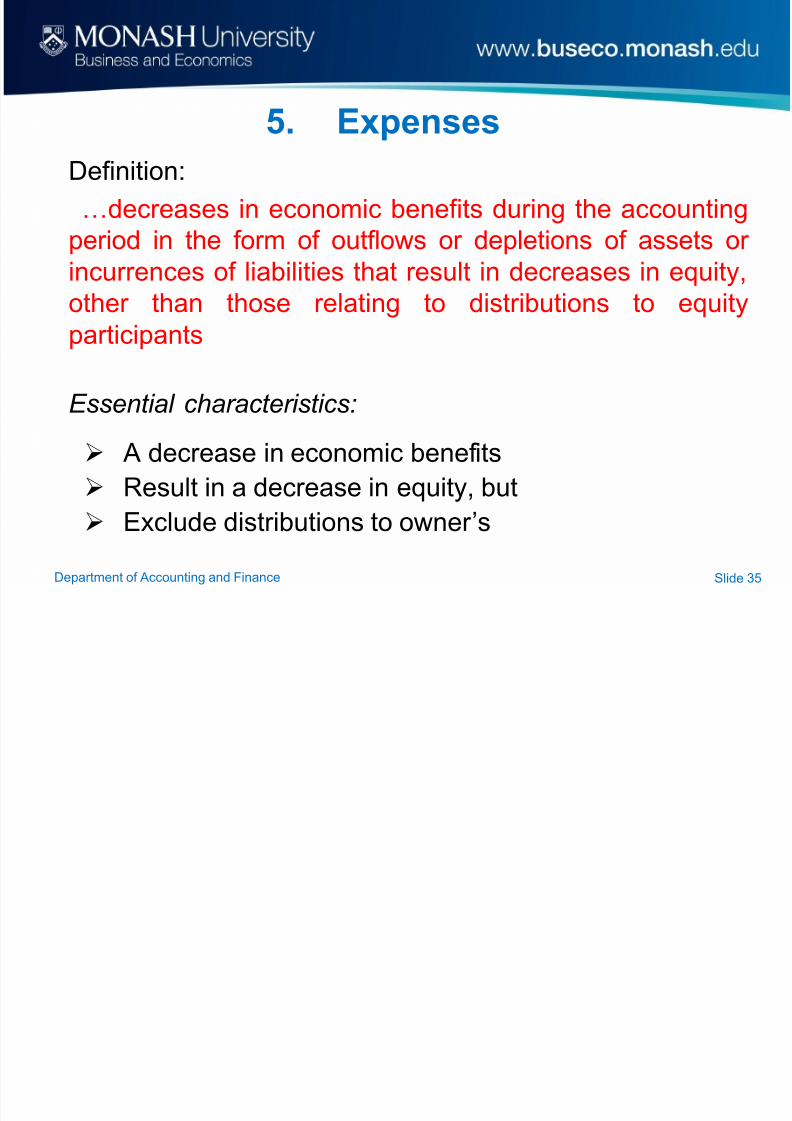

5. Expenses

Definition:

“…decreases in economic benefits during the accountingperiod in the form of outflows or depletions of assets or

incurrences of liabilities that result in decreases in equity,other than those relating to distributions to equityparticipants”

Essential characteristics:

A decrease in economic benefits

Result in a decrease in equity, but

Exclude distributions to owner ’s

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 36/67

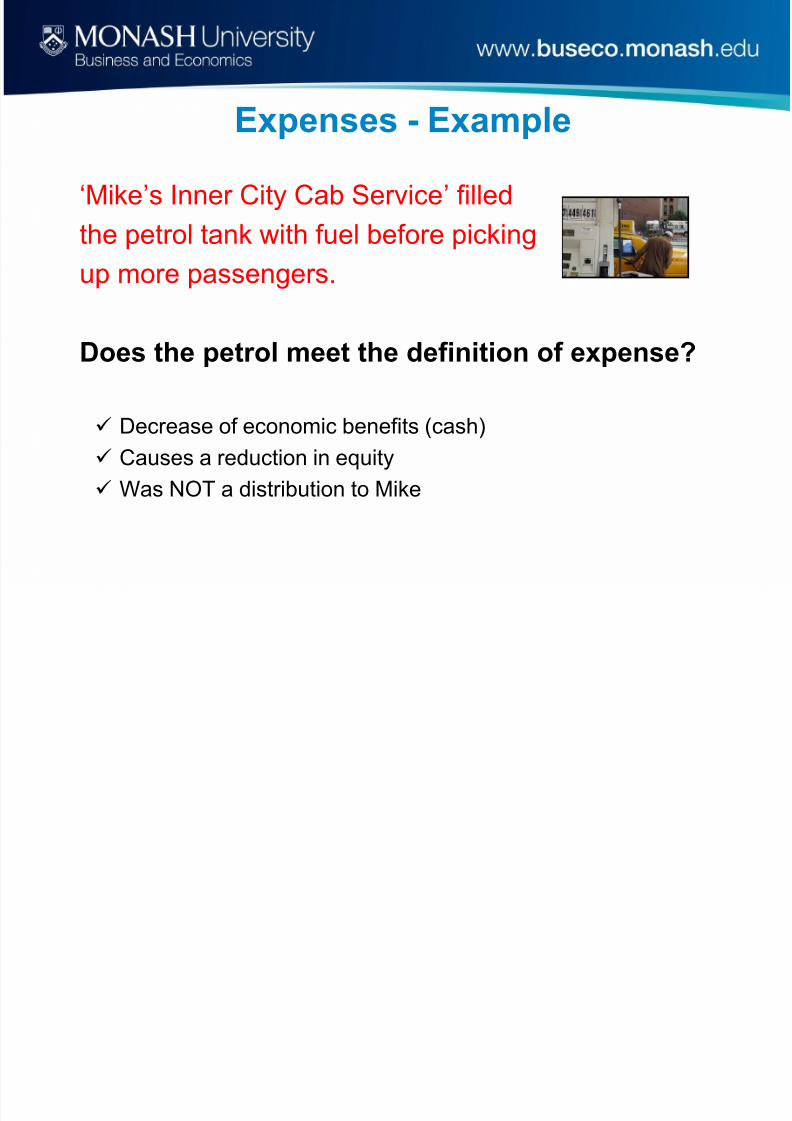

Expenses - Example

‘Mike’s Inner City Cab Service’ filled

the petrol tank with fuel before picking

up more passengers.

Does the petrol meet the definition of expense?

Decrease of economic benefits (cash)

Causes a reduction in equity

Was NOT a distribution to Mike

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 37/67

Department of Accounting and Finance Slide 37

AASB Framework – Recognition Criteria

for the elements

We have learned the definitions of the elements, butthere are two ‘recognition criteria’ for the elements as

well:

An item cannot be recorded in the entity’s accountsunless it satisfies both of these recognition criteria.

• Note that Owner ’s Equity does not have recognition criteria.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 38/67

Department of Accounting and Finance Slide 38

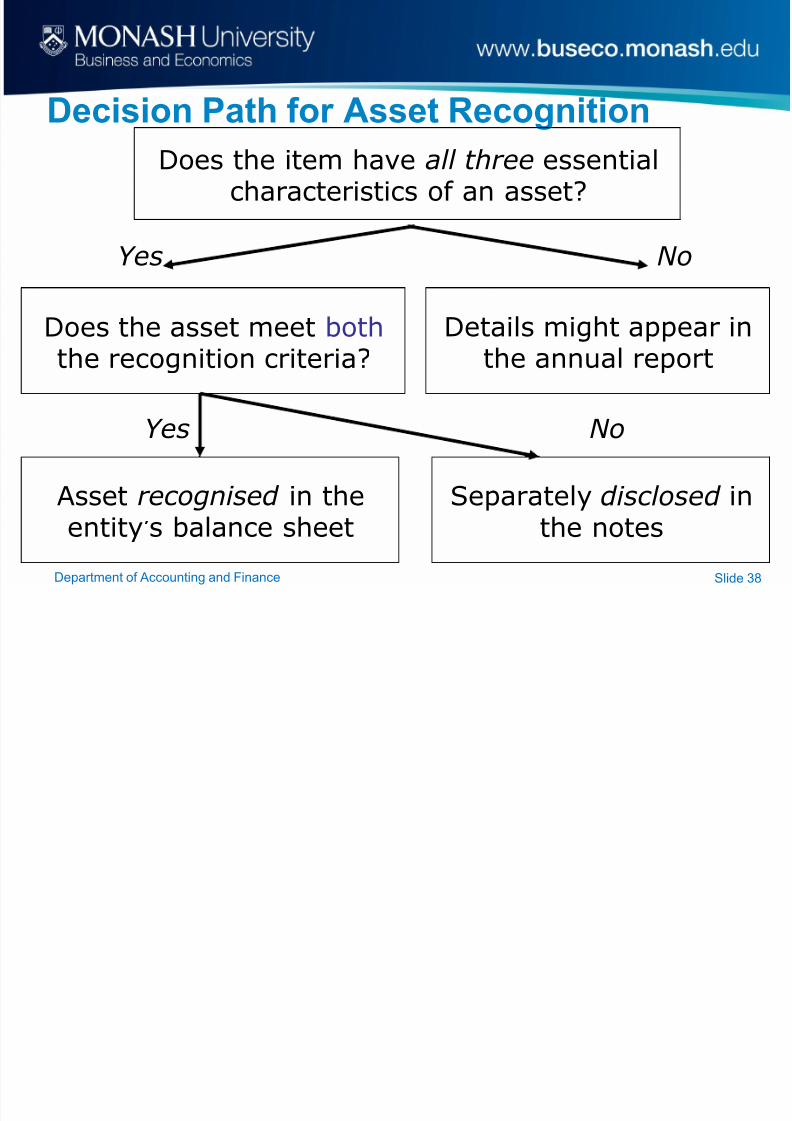

Decision Path for Asset Recognition

Does the item have all three essentialcharacteristics of an asset?

Does the asset meet both the recognition criteria?

Details might appear inthe annual report

Asset recognised in theentity’ s balance sheet

Separately disclosed inthe notes

No

No Yes

Yes

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 39/67

Department of Accounting and Finance Slide 39

Students should be able to:

• Understand the definitions and

recognition criteria of the elements

• Apply to an unusual transaction

Department of Accounting and Finance 3

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 40/67

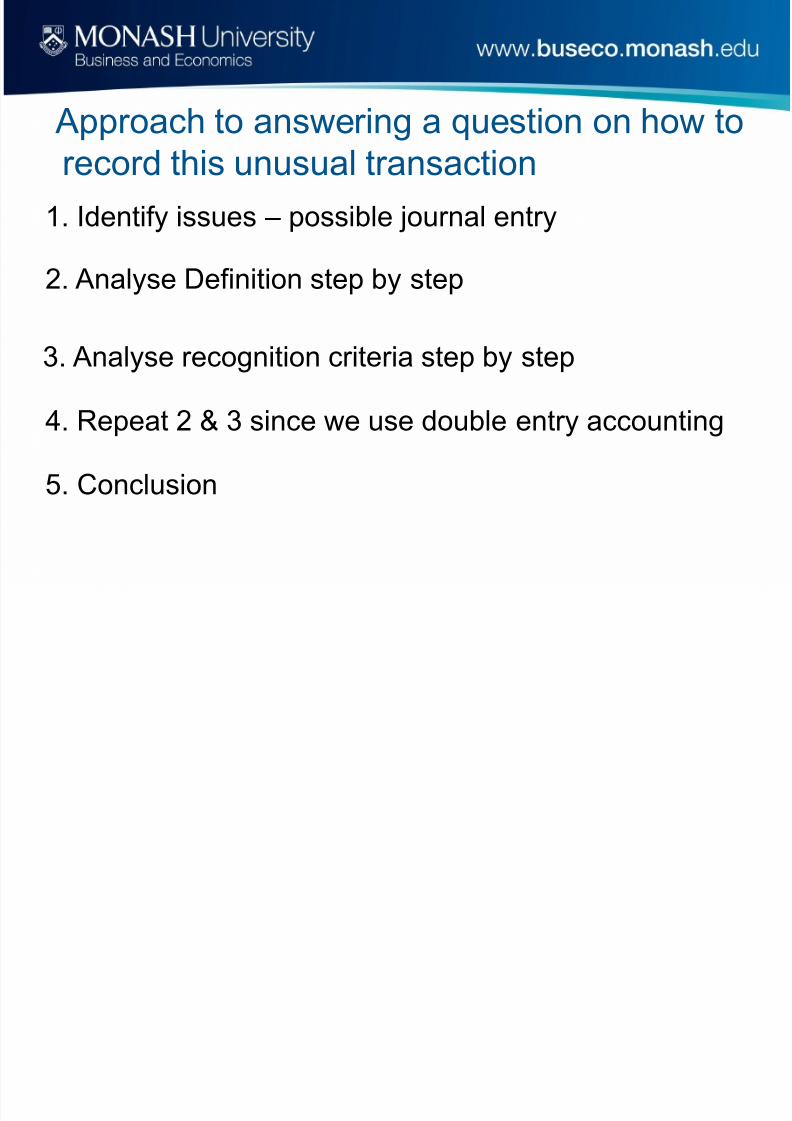

Approach to answering a question on how torecord this unusual transaction

1. Identify issues – possible journal entry

2. Analyse Definition step by step

3. Analyse recognition criteria step by step

4. Repeat 2 & 3 since we use double entry accounting

5. Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 41/67

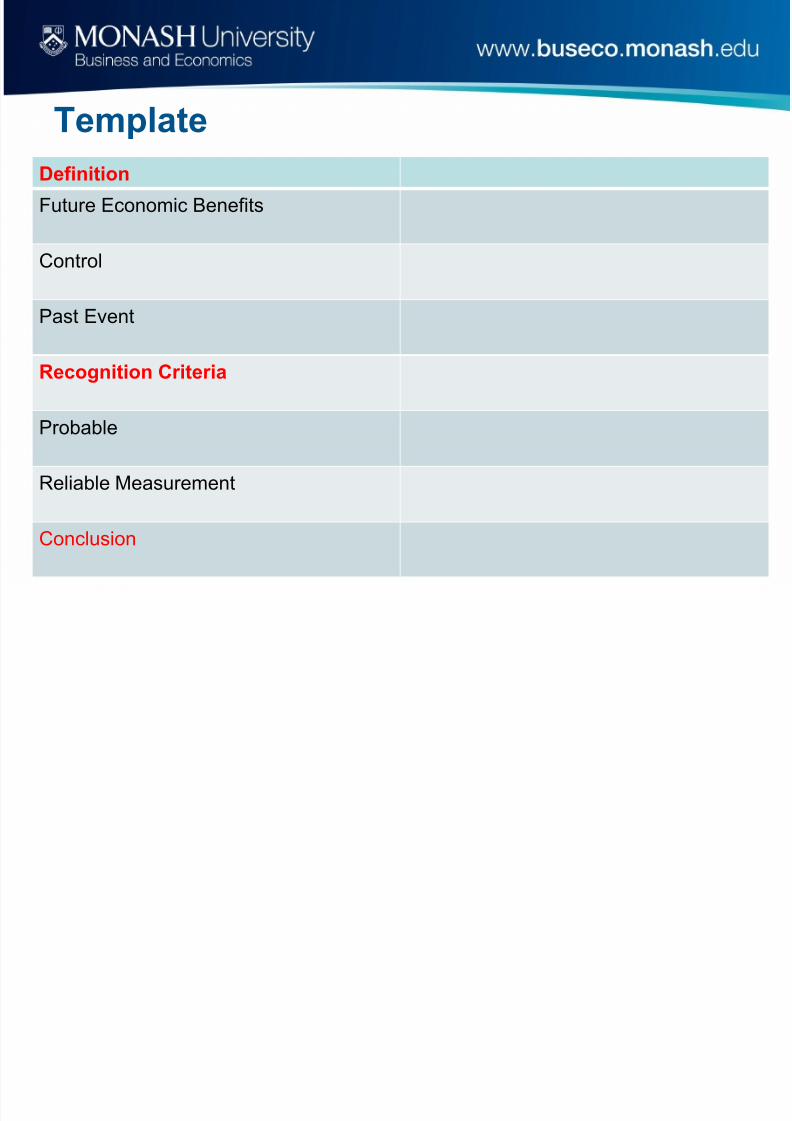

Template

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 42/67

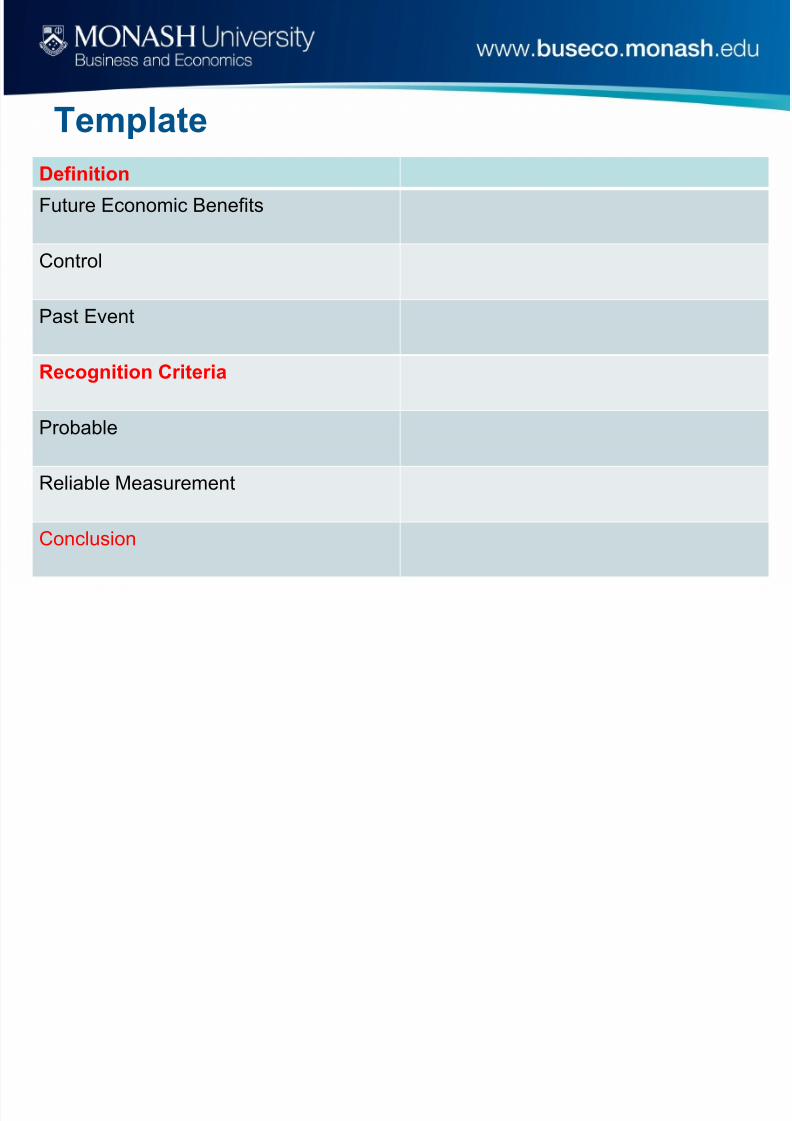

Template

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 43/67

Put it into practice

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 44/67

Department of Accounting and Finance Slide 44

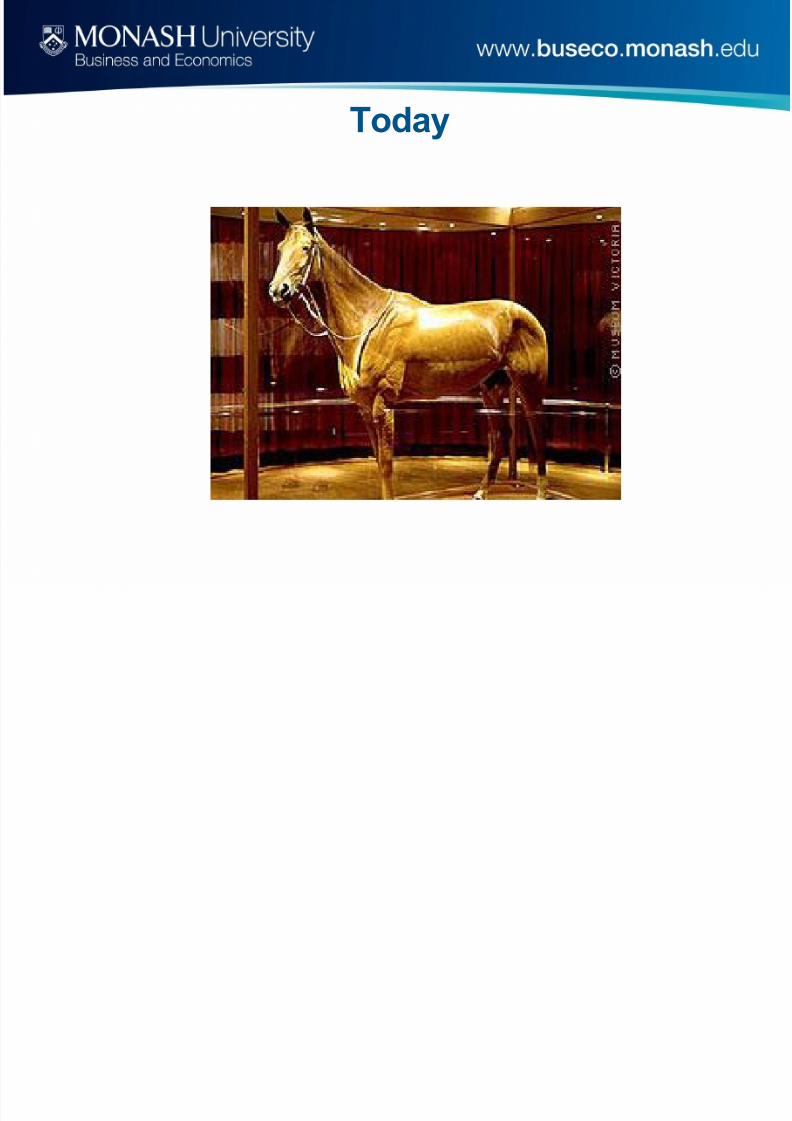

Blended Learning Question

• You own a Horse Feed Manufacturing Company.

•

The owner of Phar Lap, a good friend of yours has decided to removePhar Lap from the Museum of Victoria

• Gives Phar Lap to your company as a gift.

How do you account for this gift, using the

Conceptual Framework for guidance?

Department of Accounting and Finance 4

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 45/67

Today

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 46/67

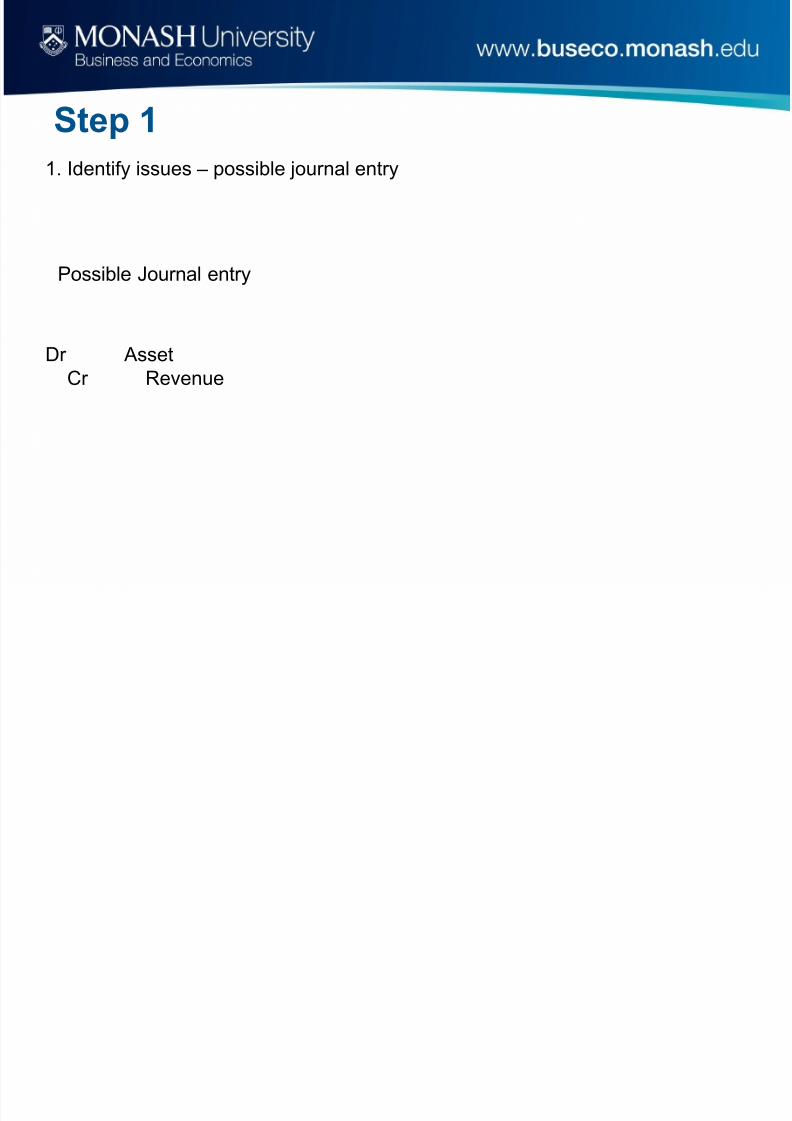

Step 1

1. Identify issues – possible journal entry

Possible Journal entry

Dr AssetCr Revenue

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 47/67

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 48/67

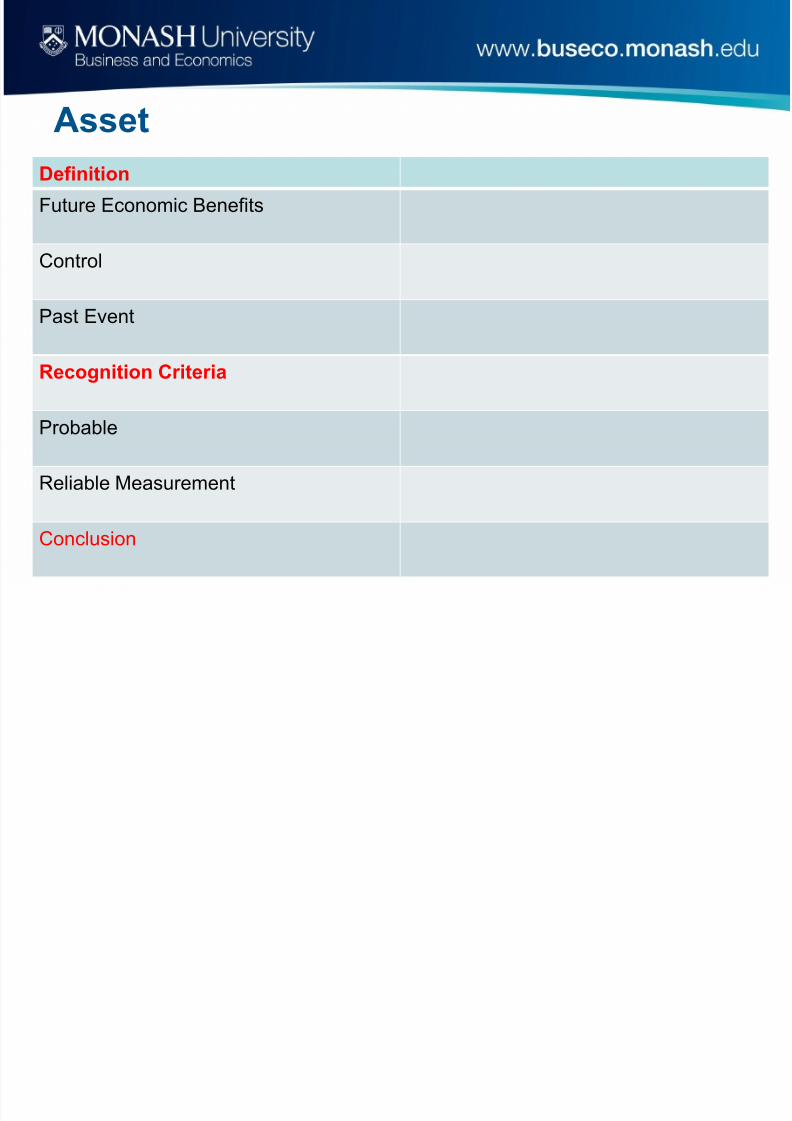

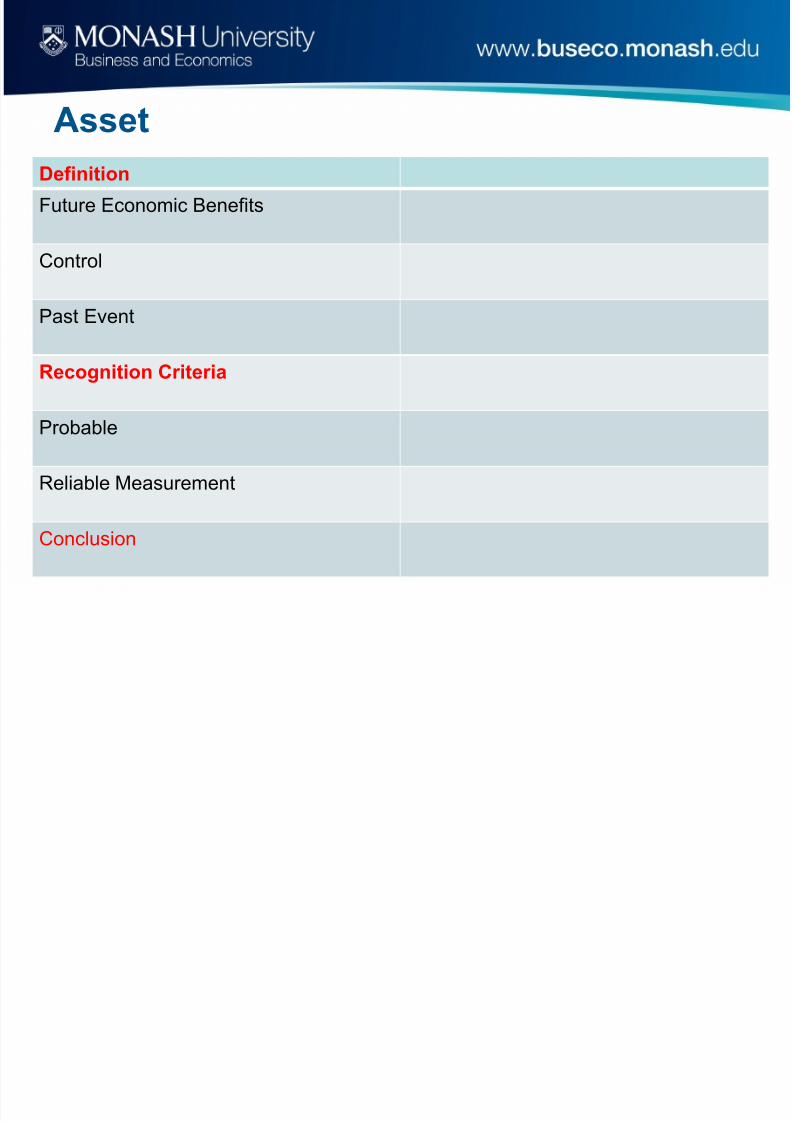

Asset

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 49/67

Asset

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 50/67

Asset

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 51/67

Asset

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 52/67

Asset

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 53/67

Asset

Definition

Future Economic Benefits

Control

Past Event

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 54/67

Revenue

Definition

Increase in economic benefits

Results in an increase in equity

Excludes owner ’s contributions of equity

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 55/67

Revenue

Definition

Increase in economic benefits

Results in an increase in equity

Excludes owner ’s contributions of equity

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 56/67

Revenue

Definition

Increase in economic benefits

Results in an increase in equity

Excludes owner ’s contributions of equity

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 57/67

Revenue

Definition

Increase in economic benefits

Results in an increase in equity

Excludes owner ’s contributions of equity

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 58/67

Revenue

Definition

Increase in economic benefits

Results in an increase in equity

Excludes owner ’s contributions of equity

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 59/67

Revenue

Definition

Increase in economic benefits

Results in an increase in equity

Excludes owner ’s contributions of equity

Recognition Criteria

Probable

Reliable Measurement

Conclusion

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 60/67

• Are brand names assets?

• Are staff development and advertising costs

assets?

• Are footballers assets?

– How do we approach such a question?

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 61/67

Where is Nicks, and Kossies etc worth

shown on the Balance Sheet?

• Why are they not

shown on theBalance Sheet as Assets?

• Economic Benefit?

• Controlled?• Past Transaction?

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 62/67

Department of Accounting and Finance Slide 62

BL Question 2

The accounting process is correctlysequenced as:

A. identification, communication, recording

B. recording, communication, identification

C. identification, recording, communication

D. communication, recording, identification

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 63/67

Department of Accounting and Finance Slide 63

BL Question 3Which of the following groups would useaccounting information to determine whetheran advertising proposal will be cost effective?

A. Investors in shares

B. Marketing managers

C. Creditors

D. Chief financial officer

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 64/67

Department of Accounting and Finance Slide 64

BL Question 4The accounting standards issues by the

Australian Accounting Standards Board areconsistent with those issued by the …

A. Financial Reporting Council.

B. Australian Taxation Office.

C. Urgent Issues Group.

D. International Accounting Standards Board.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 65/67

Department of Accounting and Finance Slide 65

BL Question 5

Which of the following is an essentialcharacteristic of income according to theConceptual Framework?

A Income arises from central, ongoingoperations.

B Income arises from providing goods and/orservices.

C Income takes the form of increases in assetsor decreases in liabilities.

D All increases in equity are income.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 66/67

Department of Accounting and Finance Slide 66

BL Question 6

The two fundamental qualities that informationshould have for it to be included in general

purpose financial reports are:

A Relevance and Faithful Representation;

B Relevance and Understandability;C Verifiability and Faithful Representation;

D Understandability and Verifiability;

E Verifiability and Relevance.

8/12/2019 Students Lecture1

http://slidepdf.com/reader/full/students-lecture1 67/67

BL Question 7

Which of the following would definitely not satisfy thedefinition of income according to the Conceptual

Framework?

A Donation to the entity from a rich old man.

B Sale of an item of inventory on credit.

C Capital contribution by an owner.D Both (a) and (c)

E None of the above