Tax Cuts for Whom?Heterogeneous Effects of Income Tax Changes on

Growth & Employment

Owen Zidar

University of California, Berkeley

All UC Group - Huntington Library Conference

April 6, 2013

1

Variation in Tax Policy & Structure of Income Tax Changes

−2

02

−2

02

0 50 100 0 50 100

1982 1991

1993 2003

Avera

ge C

hange in T

ax L

iabili

ty a

s S

hare

of A

GI

AGI PercentileGraphs by Year

2

Research Questions

How does the composition of income tax changes affect subsequent output& employment?

Do tax cuts for high income taxpayers generate more employment &output growth than equivalently sized tax cuts for low and moderateincome taxpayers?

If so, why?

3

Overview

1 Theoretical Framework: Redistribution from savers toconstrained/less patient borrowers

2 Empirical Approach:National: Romer & Romer AER 2010 disaggregated by income groupRegional: Bartik approach

3 Data: Historical returns & counterfactuals from NBER TAXSIM

4 Results: Tax cuts for those with high incomes lead to substantiallyless employment growth and economic activity than similarly sized taxcuts for those with low and moderate incomes

Aggregate consumption, particularly durable consumption, andinvestment tend to increase more strongly after bottom 90% gets taxcutsWeak to nonexistent relationship between tax cuts for the top 10% andemployment growth

4

Motivation

Why study the impacts of these tax changes and how they varyover the income distribution?

Empirical importance of heterogeneity in effects of fiscal policy [e.g.Mertens & Ravn AER forthcoming]

Optimal stimulus design

Effects of ending the Bush tax cuts for certain income groups

Effects of mass refinancing1

But Little direct evidence. Likely due to empirical issues: endogeneity,simultaneity, and observability

1Or any other modestly sized redistributive policies at a business cyclefrequency

5

Motivation

Why study the impacts of these tax changes and how they varyover the income distribution?

Empirical importance of heterogeneity in effects of fiscal policy [e.g.Mertens & Ravn AER forthcoming]

Optimal stimulus design

Effects of ending the Bush tax cuts for certain income groups

Effects of mass refinancing1

But Little direct evidence. Likely due to empirical issues: endogeneity,simultaneity, and observability

1Or any other modestly sized redistributive policies at a business cyclefrequency

5

Motivation

Why study the impacts of these tax changes and how they varyover the income distribution?

Empirical importance of heterogeneity in effects of fiscal policy [e.g.Mertens & Ravn AER forthcoming]

Optimal stimulus design

Effects of ending the Bush tax cuts for certain income groups

Effects of mass refinancing1

But Little direct evidence. Likely due to empirical issues: endogeneity,simultaneity, and observability

1Or any other modestly sized redistributive policies at a business cyclefrequency

5

Motivation

Why study the impacts of these tax changes and how they varyover the income distribution?

Empirical importance of heterogeneity in effects of fiscal policy [e.g.Mertens & Ravn AER forthcoming]

Optimal stimulus design

Effects of ending the Bush tax cuts for certain income groups

Effects of mass refinancing1

But Little direct evidence. Likely due to empirical issues: endogeneity,simultaneity, and observability

1Or any other modestly sized redistributive policies at a business cyclefrequency

5

Motivation

Why study the impacts of these tax changes and how they varyover the income distribution?

Empirical importance of heterogeneity in effects of fiscal policy [e.g.Mertens & Ravn AER forthcoming]

Optimal stimulus design

Effects of ending the Bush tax cuts for certain income groups

Effects of mass refinancing1

But Little direct evidence. Likely due to empirical issues: endogeneity,simultaneity, and observability

1Or any other modestly sized redistributive policies at a business cyclefrequency

5

II. Empirical Framework: Background

Romer & Romer (AER 2010)

∆Yt = α + β∆Taxt + εt (1)

Types of Tax Changes

1 Counteract economic forces

2 Spending offsets

3 Address inherited deficit

4 Promote long run growth

6

II. Empirical Framework: Background

Romer & Romer (AER 2010)

∆Yt = α + β∆Taxt + εt (1)

Types of Tax Changes

1 Counteract economic forces

2 Spending offsets

3 Address inherited deficit

4 Promote long run growth

6

II. Empirical Framework: Background

Romer & Romer (AER 2010)

∆Yt = α + β∆Taxt + εt (1)

Types of Tax Changes

1 Counteract economic forces

2 Spending offsets

3 Address inherited deficit

4 Promote long run growth

6

Empirical Framework: (1) Narrative Approach

Output growth & exogenous tax changes for different income groups

GrowthY ,t =β0

+ βB90,0(∆TaxB90,t) + βT 10,0(∆TaxT 10,t) + βNON,0(∆TaxNON,t)︸ ︷︷ ︸=b0∆Taxt

+...

+ βB90,m(∆TaxB90,m) + βT 10,m(∆TaxT 10,m) + βNON,m(∆TaxNON,m)︸ ︷︷ ︸=bm∆Taxt−m

+ Xtλ+ εt

∆TaxB90 and ∆TaxT 10 are changes in income and payroll taxes as a share ofGDP for the bottom 90% and top 10% respectively

Xt is a vector of controls such as lagged GDP growth, government transfers,etc.

Assume Cov(∆Taxg ,t , εt) = 0 ∀g ∈ (BOT90,TOP10,NONINCOME )following Romer & Romer AER 2010

Frisch Waugh

7

Empirical Framework: (1) Narrative Approach

Output growth & exogenous tax changes for different income groups

GrowthY ,t =β0

+ βB90,0(∆TaxB90,t) + βT 10,0(∆TaxT 10,t) + βNON,0(∆TaxNON,t)︸ ︷︷ ︸=b0∆Taxt

+...

+ βB90,m(∆TaxB90,m) + βT 10,m(∆TaxT 10,m) + βNON,m(∆TaxNON,m)︸ ︷︷ ︸=bm∆Taxt−m

+ Xtλ+ εt

∆TaxB90 and ∆TaxT 10 are changes in income and payroll taxes as a share ofGDP for the bottom 90% and top 10% respectively

Xt is a vector of controls such as lagged GDP growth, government transfers,etc.

Assume Cov(∆Taxg ,t , εt) = 0 ∀g ∈ (BOT90,TOP10,NONINCOME )following Romer & Romer AER 2010

Frisch Waugh

7

Empirical Framework: (2) Bartik Approach

Overview of Bartik approach

Idea: Auto shock on employment in Detroit vs. Denver

Labor literature: Bartik (1991), Card (1992), Katz & Murphy(1992), Moretti (2004)

Implementation: When national tax policy affects high incometaxpayers, states with large shares of high income taxpayers will facelarger shocks

Test: If high income tax cuts have substantial effects, CT and NJshould grow faster following national high income tax cuts

Value: Provides additional identifying variation2

2Within & across state variation. Avoids national concerns: fed & trends8

Data: Constructing tax changes

Tax Change Measure is a function of three things:

1 Income and deductions from year prior to an exogenous tax change3

2 Old tax schedule

3 New tax schedule

3Preliminary tests suggest that results are robust to using two year lags andvarious inflation adjustments

9

Data: Constructing tax changes

Example: 1993 Omnibus Budget Reconciliation Act

10

Data: Constructing tax changes

I do this calculation for entire sample of NBER returns−

1000

01000

2000

Change in T

ax L

iabili

ty

0 50000 100000 150000 200000 250000Adjusted Gross Income

11

Historical Income & Payoll Tax Changes by AGI Quintile

−.6

−.4

−.2

0.2

.4P

erc

ent of G

DP

1960 1970 1980 1990 2000 2010Year

Tax Change: Bottom 20% Tax Change: 21−40%

Tax Change: 41−60% Tax Change: 61−80%

Tax Change: Top 20%

12

Results Overview

National Data:

1 Output and Employment growth

2 Mechanisms: Consumption and Investment

State Data:

1 Similar specification at state-level

2 Effects across the income distribution

13

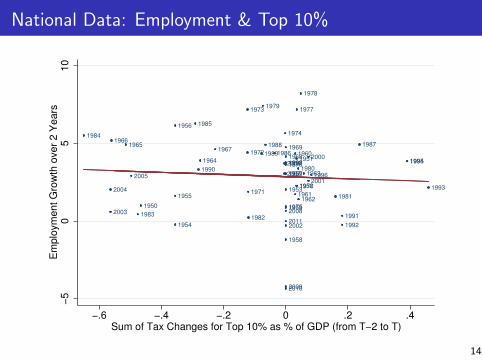

National Data: Employment & Top 10%

1950

1951

19521953

1954

1955

1956

1957

1958

1959

1960

19611962

1963

1964

19651966

19671968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

19821983

1984

1985

1986

19871988

1989

1990

1991

1992

1993

19941995

1996

19971998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

20092010

2011

−5

05

10

Em

plo

ym

ent G

row

th o

ver

2 Y

ears

−.6 −.4 −.2 0 .2 .4Sum of Tax Changes for Top 10% as % of GDP (from T−2 to T)

14

National Data: Employment & Bottom 90%

1950

1951

19521953

1954

1955

1956

1957

1958

1959

1960

19611962

1963

1964

19651966

19671968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

19821983

1984

1985

1986

1987 1988

1989

1990

1991

1992

1993

19941995

1996

19971998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

20092010

2011

−5

05

10

Em

plo

ym

ent G

row

th o

ver

2 Y

ears

−1 −.5 0 .5Sum of Tax Changes for Bottom 90% as % of GDP (from T−2 to T)

15

16

State Data: Employment & Top 10%

−10

−5

05

10

Sta

te E

mplo

ym

ent G

row

th

−1 −.5 0 .5 1Sum of Tax Changes for Residents in Top 10% as % of GDP (from T−2 to T)

17

State Data: Employment & Bottom 90%

−10

−5

05

10

Sta

te E

mplo

ym

ent G

row

th

−1.5 −1 −.5 0 .5Sum of Tax Changes for Residents in Bot. 90% as % of GDP (from T−2 to T)

18

Dependent Variable GrowthE,s(1) (2) (3) (4) (5)

∆TaxBot90,s,t 1.1 0.5 -1.1 -0.9 -0.8(1.2) (0.9) (1.0) (0.8) (0.7)

∆TaxBot90,s,t−1 -2.7* -3.2** -1.6** -2.2*** -1.4**(1.5) (1.2) (0.7) (0.7) (0.6)

∆TaxBot90,s,t−2 -1.7 -2.1** 0.5 0.1 -0.3(1.5) (0.9) (0.6) (0.7) (0.6)

∆TaxTop10,s,t 0.2 0.0 -0.1 -0.2 -0.3(0.4) (0.4) (0.2) (0.2) (0.3)

∆TaxTop10,s,t−1 -0.1 -0.2 -0.4 -0.2 -0.2(0.4) (0.3) (0.2) (0.2) (0.3)

∆TaxTop10,s,t−2 -0.2 -0.2 -0.1 0.0 -0.0(0.3) (0.2) (0.2) (0.2) (0.2)

Constant -0.1 -0.3 0.4 -0.2 -2.6**(0.6) (0.6) (0.3) (0.9) (1.2)

State & Year Fixed Effects N Y Y Y YControl for GrowthE lags N N Y Y YControl for GovTransPERCAP,s,t & lags N N N Y YControl for EPOPs,t N N N N YControl for TotalTaxPERCAP,s,t & growth N N N N YControl for squared and cubic lags N N N N YObservations 1,297 1,297 1,247 1,297 1,297R-squared 0.551 0.691 0.810 0.830 0.872Bottom90 Tax Change: βt + βt−1 + βt−2 -3.318 -4.746* -2.189 -2.937* -2.592**t-stat -0.854 -1.873 -1.378 -1.959 -2.433p-val 0.397 0.0670 0.175 0.0558 0.0187Top10 Tax Change: βt + βt−1 + βt−2 -0.164 -0.443 -0.633* -0.416 -0.481*t-stat -0.184 -0.589 -1.792 -1.176 -1.720p-val 0.855 0.558 0.0793 0.245 0.0917

Notes: All results are weighted by state population. Robust standard errors clustered by state are in parentheses. *** p<0.01,** p<0.05, * p<0.1.

19

Effects for more income groups than Bottom 90 & Top 10

How does effect β vary over the income groups?

A second order approximation of the β(g) function

β(g) = θ0 + θ1g + θ2g2

Plug into estimating equation

GrowthY ,t = α + β1∆τ1,t + β2∆τ2,t + ...+ β10∆τ10,t + X̃t λ̃+ ε̃t

GrowthY ,t = α + (θ0 + θ1 + θ2)∆τ1,t + (θ0 + θ12 + θ222)∆τ2,t + ...+ X̃t λ̃+ ε̃t

GrowthY ,t = α + θ0

(10∑

g=1

∆τg ,t

)+ θ1

(10∑

g=1

g ×∆τg ,t

)+ θ2

(10∑

g=1

g2 ×∆τg ,t

)+ X̃t λ̃+ ε̃t

20

Aggregate Effects Across the Income Distribution

1 2 3 4 5 6 7 8 9 10−8

−6

−4

−2

0

AGI Decile

Em

plo

ym

ent

Gro

wth

This figure shows the third order approximation of the β(g) function, i.e., θ̂1g + θ̂2g2 + θ̂3g3

21

Conclusion

Summary

1 Construct a new measure of income tax changes

2 Show substantial heterogeneity in effects of fiscal policy

3 Find stimulative effect of income tax cuts are largely from bottom90% and empirical link between employment growth and tax changesfor upper income earners seems weak to negligible

4 Suggest letting Bush tax cuts expire for $250K won’t have substantialemployment consequences over the business cycle

22