The Case for Reasonable Estimates of General Property, Plant, and Equipment (GPP&E)

Post-Clean Opinion

American Society of Military Comptrollers (ASMC) San Diego, PDI

1 June 2017Presenters: LCDR Khris Johns, USCG and Bobby

Hart

1

• How do you address unsupported GPP&E items post clean audit opinion? – This workshop will assist you in valuing items in a post SFFAS #50

AND post clean audit opinion world, whether the items were discovered based on mission and operations or if the items were not properly valued based on a break down in policies, procedures, and/or information systems.

– A lithe and nimble CFO organization is required in the coming times of greater fiscal austerity, and the techniques discussed in this workshop will assist in addressing the valuation of items discovered after the “we don’t know what we don’t know” phase of GAAP-compliance.

Workshop 71

2

Agenda

• “Drain the Swamp and Turn the Spigot Off”• Case Study 1: Execute Alternate Valuation• Transition to Historical Cost• Case Study 2: Post-Clean Audit

3

“Drain the Swamp AND Turn the Spigot Off”

• GAAP-compliance not a “two-step,” but concurrent• Management Assertion focused

“Righty-tighty”

Presentation and Disclosure

Completeness

Existence

Rights and Obligations

Valuation

4

Management Assertions – Rights and Obligations

Rights and obligations – the legal ownership properly accounted for, including intra-entity transfers as well as complete documentation of3rd-party relationships.

5

Floor to Book / Record

Book / Record to Floor

Current Fiscal Year (FY)FY - 1 FY + 1

Management Assertions – Completeness and Cutoff

Completeness and cutoff – all necessary transactions reported, nothing unauthorized.

6

Management Assertions – Existence and Occurrence

Existence and occurrence – the items exist and transactions occurred.

7

Management Assertions, Existence and Occurrence – Key Data Elements

• Unique Identification Number (UID) (e.g., Serial Number, Aviation Identification Number (AIN), Hull Identification Number (HIN), Vehicle Identification Number (VIN), Real Property UID, etc.)

• Organization Code• Last Inventory Date• Detailed Location (e.g., GPS coordinates; Building, Floor, Room; Department Division,

Office; etc.) • Status

8

𝑓𝑓 𝑥𝑥 = 𝑎𝑎0 + �𝑛𝑛=1

∞

𝑎𝑎𝑛𝑛 cos𝑛𝑛𝑛𝑛𝑥𝑥𝐿𝐿 + 𝑏𝑏𝑛𝑛 sin

𝑛𝑛𝑛𝑛𝑥𝑥𝐿𝐿

Management Assertions – Valuation and Allocation

Valuation and allocation – the items are properly valued, documentation exists.

9

Management Assertions – Valuation and Allocation – Key Data ElementsVariable (from asset to asset)• Date Placed-in-Service (DPiS)• Estimated Useful Life (in Days, Months, etc.)• CostConstant• Today’s DateEquations (Straight-line depreciation is the norm)• Remaining Useful Life (in Days, Months, etc.)• Accumulated Depreciation• Net Book Value (NBV)

NBV = 𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶 − 𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝐴𝑎𝑎𝐶𝐶𝐴𝐴𝐴𝐴 𝐷𝐷𝐴𝐴𝐷𝐷𝐷𝐷𝐴𝐴𝐴𝐴𝐷𝐷𝑎𝑎𝐶𝐶𝐷𝐷𝐶𝐶𝑛𝑛

Accumulated Depreciation = 𝐶𝐶𝐶𝐶𝐶𝐶𝐶𝐶 ∗ 𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸 𝑈𝑈𝐸𝐸𝐸𝐸𝑈𝑈𝑈𝑈𝑈𝑈 𝐿𝐿𝐸𝐸𝑈𝑈𝐸𝐸 −𝑅𝑅𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝑛𝑛𝐸𝐸𝑛𝑛𝑅𝑅 𝑈𝑈𝐸𝐸𝐸𝐸𝑈𝑈𝑈𝑈𝑈𝑈 𝐿𝐿𝐸𝐸𝑈𝑈𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸𝐸 𝑈𝑈𝐸𝐸𝐸𝐸𝑈𝑈𝑈𝑈𝑈𝑈 𝐿𝐿𝐸𝐸𝑈𝑈𝐸𝐸

Remaining Useful Life = 𝐸𝐸𝐶𝐶𝐶𝐶𝐷𝐷𝐴𝐴𝑎𝑎𝐶𝐶𝐴𝐴𝐴𝐴 𝑈𝑈𝐶𝐶𝐴𝐴𝑓𝑓𝐴𝐴𝐴𝐴 𝐿𝐿𝐷𝐷𝑓𝑓𝐴𝐴 − (𝐷𝐷𝐷𝐷𝐷𝐷𝐷𝐷 − 𝑻𝑻𝑻𝑻𝑻𝑻𝑻𝑻𝒚𝒚′𝒔𝒔 𝑫𝑫𝑻𝑻𝑫𝑫𝑫𝑫)

10

Case Study 1: Execute Alternate Valuation

• Deemed Cost• Unreserved assertion• Valuation Methods available

11

What is Deemed Cost?

• FASAB 50 provides for alternative valuation methods, and introduces the idea of Deemed Cost for GPP&E.

• Deemed Cost - an amount used as a surrogate for initial amounts that otherwise would be required to establish opening balances.

• Available to reporting entities presenting financial statements either:1) For the first time or2) After a period during which existing systems

could not provide necessary information in accordance with GAAP without use of alternative methods

12

What is an Unreserved Assertion?

• Unreserved assertion is an – “unconditional statement”– Could be made for

• Financial statements• One or more lines • Classes of PP&E presented in Notes to Financial Statements

– “financial statements are presented fairly in accordance with GAAP”

• “Snapping the chalk line” or “unreserved assertion” is only available ONCE

• Following the unreserved assertion, reporting entity is expected to comply with GAAP going forward

13

Which Valuation Methods are available?

• Valuation Methods includei. Replacement Costii. Estimated historical cost (initial amount)

a) cost of similar assets at the time of acquisition;b) current cost of similar assets discounted for inflation since

the time of acquisition (that is, deflating current costs to costs at the time of acquisition by general price index); or

c) other reasonable methods, including latest acquisition cost and estimation methods based on information such as, but not limited to, budget, appropriations, engineering documents, contracts, or other reports reflecting amounts to be expended.

iii. Fair Value

14

Case Study 1: Execute Alternate Valuation

15

Alternate Valuation Methodology Metrics at Time Unmodified Opinion Was Earned

Priority Methodology (Real and Personal Property)

CountAverage

Acquisition Cost

Total Acquistion Cost

Total Accumulated Depreciation

Total Net Book Value

% of Total Count

% of Total Total Net

Book Value5 Third-Party Appraisal 571 $8,702,472 $4,969,111,683 $2,281,524,752 $2,687,586,930 3.67% 39.82%4 Budgetary Estimate 576 $7,717,068 $4,445,031,194 $3,016,567,450 $1,428,463,744 3.70% 21.17%1 Like-Item 297 $3,358,051 $997,341,149 $122,710,823 $874,630,326 1.91% 12.96%

SFFAS 6 Historical 3395 $446,956 $1,517,416,469 $676,380,298 $841,036,171 21.80% 12.46%3c Plant Replacement Value (PRV) 1005 $1,747,303 $1,756,039,672 $1,153,706,347 $602,333,325 6.45% 8.92%n/a No Valuation Documentation 9570 $160,405 $1,535,073,714 $1,222,238,595 $312,835,119 61.45% 4.64%2b Construction Cost Estimate 7 $965,634 $6,759,435 $5,343,387 $1,416,048 0.04% 0.02%3 OEM Price Certification 120 $169,241 $20,308,954 $19,747,742 $561,212 0.77% 0.01%

2/2a Published Price List 13 $161,324 $2,097,211 $2,073,182 $24,029 0.08% 0.00%3b Parametric Model 20 $26,680 $533,600 $532,150 $1,449 0.13% 0.00%

Grand Total 15574 $979,178 $15,249,713,081 $8,500,824,727 $6,748,888,354 100.00% 100.00%

16

Alternate Valuation Methodology Examples

• Like-item – All – Priority: 1• Tax Assessment – All RP – Priority: 2c• Parametric Model – Aids-to-Navigation – Priority: 3b• Plant Replacement Value (PRV) – All RP – Priority: 3c • Budgetary Estimate – All – Priority: 4• Third-Party Appraisal – All – Priority: 5

17

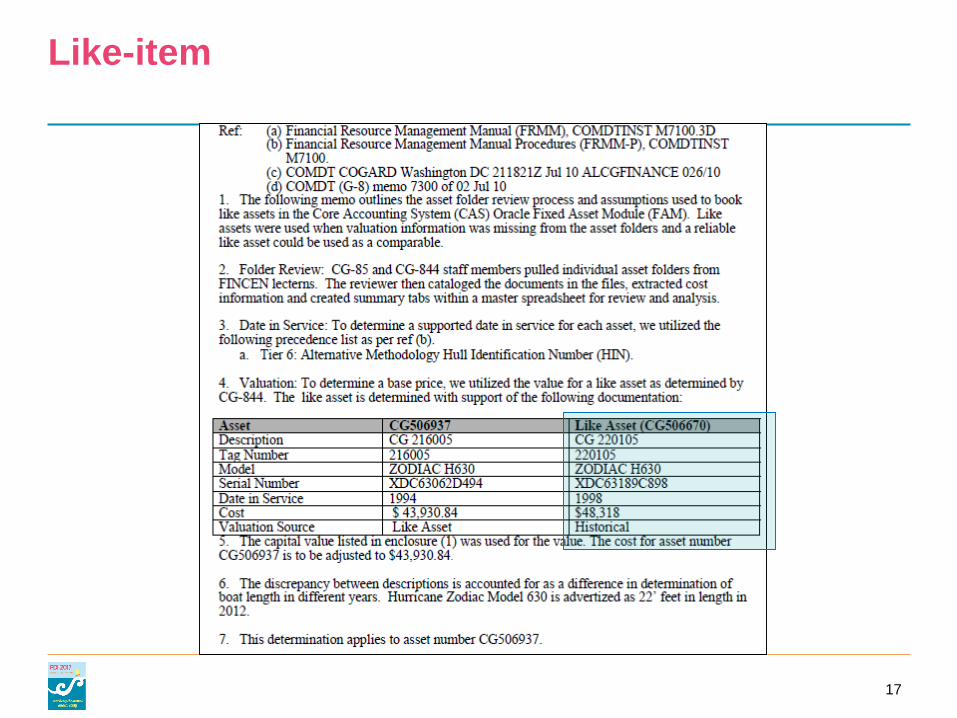

Like-item

18

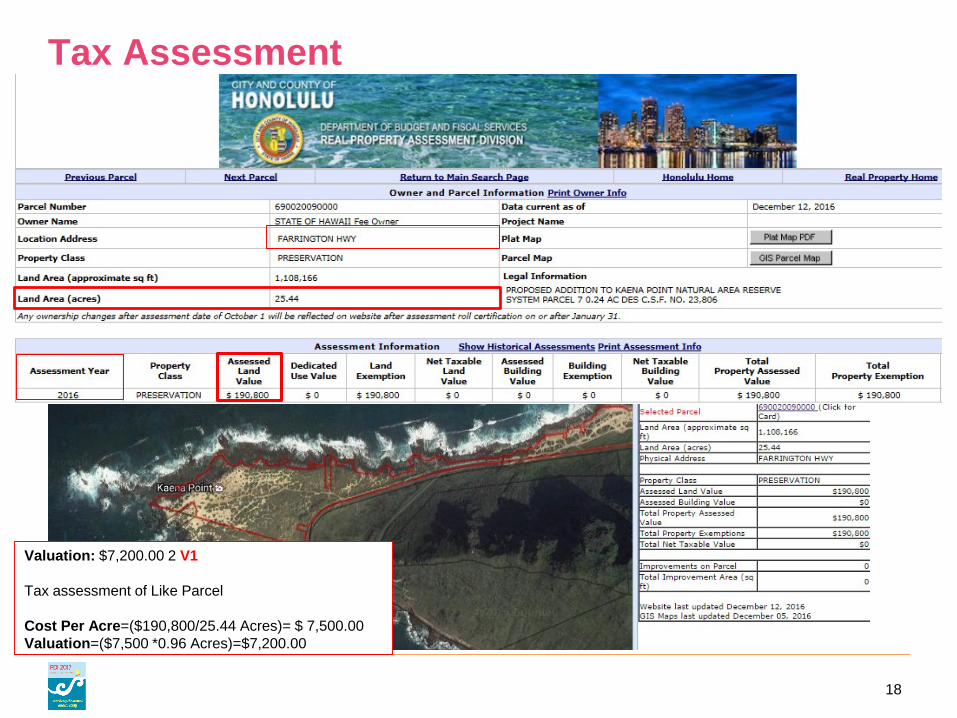

Tax Assessment

Valuation: $7,200.00 2 V1

Tax assessment of Like Parcel

Cost Per Acre=($190,800/25.44 Acres)= $ 7,500.00 Valuation=($7,500 *0.96 Acres)=$7,200.00

19

Parametric Model

20

Plant Replacement Values (PRV)

• Selected Inputs– Category Code (e.g. Building and Structure Type; not Land)– Replacement Cost Factor – per unit of measure (e.g. $/sq. foot)– Size – unit of measure

• Other Inputs– Area Cost Factor; Historical Record Adjustment; Planning & Design

Factor; Supervision; Inspection; and Overhead (SIOH); & Contingency• Indexing

– Needs to be Indexed• Land – Bureau of Labor Statistics provided Indexing Back to 1913; 2% used on

average prior to 1913• Buildings – Engineering News Record-Building Cost Index (ENR-BCI)• Structure – Engineering News Record-Construction Cost Index (ENR-CCI)

– Can be Indexed Forward (Inflated) or Backward (Deflated)

21

Asset Enrolment Template (AET)

Includes General Services Administration (GSA) Federal Real

Property Council (FRPC) Data Requirements

22

Asset Valuation Template (AVT) – PRV Calculation

** * * * * =

23

Budgetary Estimates

• Inputs– Congressional Justification (CJ) – Program Pages– Conference Reports– Appropriation Acts, Digests, etc.– Warrants from Treasury

• Uses – Specific Identification (e.g. Hull #1, Aircraft#11, etc.)– Per Asset (e.g. Boats #32 – 42, Tanks #1– 20, etc.)– Program Level (e.g. Program Costs, Administrative Costs, etc.)

EXTERNAL TO REPORTING ENTITY

24

Completeness Through Reconciliation

Appropriations Public Laws –Appropriation

Warrants -Appropriation

Congressional Justification (CJ) – PPA

Level

Conference Reports – PPA

25

Conference Reports – PPA Level

26

CJ – Specific Identification

27

CJ – Per Asset

28

CJ – Program Level

Program Costs

29

Third-Party Appraisal

• Approaches– Cost approach– Market approach– Income approach– Value-in Use

• Uses– Class-wide– Model-wide– Modification-wide– Others

30

Alternate Date-in-Service (DIS) Methodologies

31

Alternate DIS Methodologies Impact

Priority Methodology (Real and Personal Property)

CountAverage

Acquisition Cost

Total Acquistion Cost

Total Accumulated Depreciation

Total Net Book Value

% of Total Count

% of Total Total Net

Book Value5 Third-Party Appraisal 571 $8,702,472 $4,969,111,683 $2,281,524,752 $2,687,586,930 3.67% 39.82%4 Budgetary Estimate 576 $7,717,068 $4,445,031,194 $3,016,567,450 $1,428,463,744 3.70% 21.17%1 Like-Item 297 $3,358,051 $997,341,149 $122,710,823 $874,630,326 1.91% 12.96%

SFFAS 6 Historical 3395 $446,956 $1,517,416,469 $676,380,298 $841,036,171 21.80% 12.46%3c Plant Replacement Value (PRV) 1005 $1,747,303 $1,756,039,672 $1,153,706,347 $602,333,325 6.45% 8.92%n/a No Valuation Documentation 9570 $160,405 $1,535,073,714 $1,222,238,595 $312,835,119 61.45% 4.64%2b Construction Cost Estimate 7 $965,634 $6,759,435 $5,343,387 $1,416,048 0.04% 0.02%3 OEM Price Certification 120 $169,241 $20,308,954 $19,747,742 $561,212 0.77% 0.01%

2/2a Published Price List 13 $161,324 $2,097,211 $2,073,182 $24,029 0.08% 0.00%3b Parametric Model 20 $26,680 $533,600 $532,150 $1,449 0.13% 0.00%

Grand Total 15574 $979,178 $15,249,713,081 $8,500,824,727 $6,748,888,354 100.00% 100.00%

32

DIS Methodology Examples

• Midpoint• SFFAS 6: Historical• Then SFFAS 35: Alternate Valuation, Now SFFAS 50:

Deemed Cost– Ship’s Plaque – Vessels – Priority: 1– Dedication Plaque – All RP – Priority: 2– Cornerstone – All RP – Priority: 3– Earliest Site Plot or Asset Drawing – All RP – Priority: 5(a)– Earliest Maintenance Record – All RP – Priority: 5(b)– Other Third-Party – Both PP & RP – Priorities: Various (4-7)

33

Midpoint

Exhibit Date Type First Date Second Date Midpoint1943 Year 1/1/1943 12/31/1943 7/2/19431942 Year 1/1/1942 12/31/1942 7/2/19421941 Year 1/1/1941 12/31/1941 7/2/19411940 Year - Leap 1/1/1940 12/31/1940 7/1/1940

December-43 Month - 31 12/1/1943 12/31/1943 12/16/1943November-43 Month - 30 11/1/1943 11/30/1943 11/15/1943February-40 Month - 29 2/1/1940 2/29/1940 2/15/1940February-43 Month - 28 2/1/1943 2/28/1943 2/14/1943

34

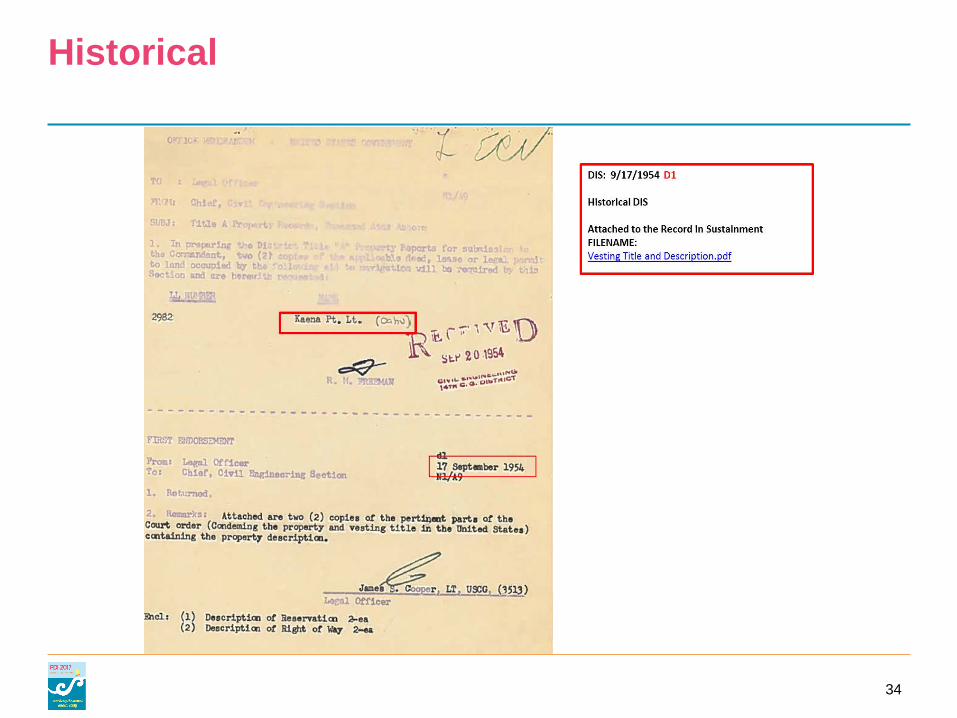

Historical

35

Ship’s Plaque

36

Dedication Plaque

37

Cornerstone

38

Earliest Site Plot or Asset Drawing

39

Earliest Maintenance Record

40

Other Third-Party

41

1720 –Construction-in-Progress

1832 –IUS-in-

Development

Software or Other?

1830 – IUS1750 –General

Equipment

1740 –Structure

1730 –Buildings

SoftwareOther

171x –Land

accountsDirect / Transfer

Constructed

Transition to Historical Cost

EXPENSES

42

Key FASAB Guidance HighlightsStatement of Federal Financial Accounting Standards (SFFAS) and Technical Releases (TR)

SFFAS 4: Managerial Cost Accounting Standards and Concepts:

• Direct tracing• Cause and

effect• Reasonable

allocation

SFFAS 50: Establishing Opening Balances for GPP&E…

• Deemed Cost• Unreserved

Assertion• Reasonable

Estimates

Implementation Guide:• Estimating the Historical Cost of General Property, Plant & Equipment (TR 13)• Accounting for the Disposal of General Property, Plant & Equipment (TR 14)• Implementation Guidance for General Property, Plant, and Equipment Cost

Accumulation, Assignment and Allocation (TR 15) • Implementation Guidance For Internal Use Software (TR 16)• Conforming Amendments to Technical Releases for SFFAS 50, Establishing

Opening Balances for General Property, Plant, and Equipment (TR17)

SFFAS 6: Accounting for Property, Plant, and Equipment (PP&E)• Accounting standards

for Federally owned PP&E

• Deferred maintenance on PP&E

• Clean up costs on PP&E

43

Capitalization vs. Expense

Ordinary Repair and Maintenance

New or Improves Capability and

Extends Capacity

• Expense in Period Performed

Cost Accumulated in the CIP AccountForm and Condition Suitable for Intended UseCapitalized at Date in Service

44

Property Continuum

x Axis Portabilityy Axis Tangibility

(x)

(y)

• Land

• Building• Structures• Linear Structures

Real Property

Intangible

Tangible

• Watercraft• Electronic Systems• Helicopters• Tanks• Servers• Manufacturing

Equipment• IT Equipment• Office Furniture

Personal Property

Mobile

Operating Materials & Consumable Supplies

• Inventory Held for Sale• Stockpile• Pre-positioned Stock• Raw Materials or work in

process• Paper Towels• Pens• Printer Toner

Immobile

• IUS

Real Property

45

Direct Costs vs. Indirect Costs

Direct Costscan be traced directly to a cost object such as a product or a department

Indirect Costsis a cost that is not directly traceable to a cost object. Rather, the cost is common to several objects and requires an allocation.

Overhead Allocations• Material OH• Labor OH• Machine OH• Admin OH

Key Direct Costs• Direct Labor• Direct Materials

46

Different Allocation Methods Between Real Property and Personal Property

Real Property Personal Property

(e. g. sidewalk concrete)

(e. g. One invoice per asset)

Reasonable Allocation PRV ratio Cost Estimate ratio

Blended Method

Overhead Blended

Invoices to actual workDirect Tracing

Ratios based off direct tracing for remainder not directly traced

47

Self-Constructed and OGA-Constructed Assets

• Self-Constructed– Direct tracing– Cause and effect– Reasonable allocation

• OGA-constructed– Economy Act – Cost Recovery– Transfer – Net Realizable

Value

48

1720 –Construction-in-Progress

1832 –IUS-in-

Development

Software or Other?

1830 – IUS1750 –General

Equipment

1740 –Structure

1730 –Buildings

SoftwareOther

171x –Land

accountsDirect / Transfer

Constructed

Transition to Historical Cost

EXPENSES

Self-Constructed

OGA-Constructed

49

New Found Property

• Property Inventories– Property Custodian

Finds– eGIS

• System Reconciliations– Property Management

Systems– Financial System of

Record

50

Case Study 2: Post-Clean Audit

• Reasonable Estimate (Third-party Appraisal) was found to be overstate value of class of aircraft

• Found during scheduled internal review of Construction-in-Progress balances prior to project closeout/asset acceptance

• Pre-SFFAS 50, but SFFAS 50-like situation/fact pattern

51

Case Study 2: Post-Clean Audit

Information Systems

Balance Sheet ASSETS (Note 2) Intragovernmental: Fund Balance with Treasury (Note 3) Investments (Note 4) Accounts Receivable (Note 5) Other Assets (Note 6) Total Intragovernmental Assets

Cash and Other Monetary Assets (Note 7) Accounts Receivable,Net (Note 5) Loans Receivable (Note 8) Inventory and Related Property,Net (Note 9) General Property, Plant and Equipment,Net (Note 10) Investments (Note 4) Other Assets (Note 6) TOTAL ASSETS STEWARDSHIP PROPERTY, PLANT & EQUIPMENT (Note 10)

LIABILITIES (Note 11) Intragovernmental: Accounts Payable (Note 12) Debt (Note 13) Other Liabilities (Note 15 & 16) Total Intragovernmental Liabilities

Accounts Payable (Note 12) Military Retirement and Other Federal Employment Benefits (Note 17) Environmental and Disposal Liabilities (Note 14) Loan Guarantee Liability (Note 8) Other Liabilities (Note 15 and Note 16) TOTAL LIABILITIES

COMMITMENTS AND CONTINGENCIES (NOTE 16) NET POSITION Unexpended Appropriations - Dedicated Collections (Note 23) Unexpended Appropriations - Other Funds Cumulative Results of Operations - Dedicated Collections (N TOTAL NET POSITION

TOTAL LIABILITIES AND NET POSITION

Policy & Procedures

52

What is Deemed Cost?

• SFFAS 50 provides for alternative valuation methods, and introduces the idea of Deemed Cost for GPP&E.

• Deemed Cost - an amount used as a surrogate for initial amounts that otherwise would be required to establish opening balances.

• Available to reporting entities presenting financial statements either:1) For the first time or2) After a period during which existing systems

could not provide necessary information in accordance with GAAP without use of alternative methods

• SFFAS 50 provides for alternative valuation methods, and introduces the idea of Deemed Cost for GPP&E.

• Deemed Cost - an amount used as a surrogate for initial amounts that otherwise would be required to establish opening balances.

• Available to reporting entities presenting financial statements either:1) For the first time or2) After a period during which existing systems

could not provide necessary information in accordance with GAAP without use of alternative methods

53

Case Study 2: Post-Clean Audit

Information Systems

Balance Sheet ASSETS (Note 2) Intragovernmental: Fund Balance with Treasury (Note 3) Investments (Note 4) Accounts Receivable (Note 5) Other Assets (Note 6) Total Intragovernmental Assets

Cash and Other Monetary Assets (Note 7) Accounts Receivable,Net (Note 5) Loans Receivable (Note 8) Inventory and Related Property,Net (Note 9) General Property, Plant and Equipment,Net (Note 10) Investments (Note 4) Other Assets (Note 6) TOTAL ASSETS STEWARDSHIP PROPERTY, PLANT & EQUIPMENT (Note 10)

LIABILITIES (Note 11) Intragovernmental: Accounts Payable (Note 12) Debt (Note 13) Other Liabilities (Note 15 & 16) Total Intragovernmental Liabilities

Accounts Payable (Note 12) Military Retirement and Other Federal Employment Benefits (Note 17) Environmental and Disposal Liabilities (Note 14) Loan Guarantee Liability (Note 8) Other Liabilities (Note 15 and Note 16) TOTAL LIABILITIES

COMMITMENTS AND CONTINGENCIES (NOTE 16) NET POSITION Unexpended Appropriations - Dedicated Collections (Note 23) Unexpended Appropriations - Other Funds Cumulative Results of Operations - Dedicated Collections (N TOTAL NET POSITION

TOTAL LIABILITIES AND NET POSITION

Policy & Procedures

54

Remember Key to Reasonable Estimates

• Maintain low-level of “swampification”• Leverage Existing Guidance• Continually strive to know what we currently don’t know –

there is always something!– Self-constructed or Other Government Agency (OGA)-constructed

assets, disconnected systems– New found property– System break down

55

Questions?

Information Systems

Balance Sheet ASSETS (Note 2) Intragovernmental: Fund Balance with Treasury (Note 3) Investments (Note 4) Accounts Receivable (Note 5) Other Assets (Note 6) Total Intragovernmental Assets

Cash and Other Monetary Assets (Note 7) Accounts Receivable,Net (Note 5) Loans Receivable (Note 8) Inventory and Related Property,Net (Note 9) General Property, Plant and Equipment,Net (Note 10) Investments (Note 4) Other Assets (Note 6) TOTAL ASSETS STEWARDSHIP PROPERTY, PLANT & EQUIPMENT (Note 10)

LIABILITIES (Note 11) Intragovernmental: Accounts Payable (Note 12) Debt (Note 13) Other Liabilities (Note 15 & 16) Total Intragovernmental Liabilities

Accounts Payable (Note 12) Military Retirement and Other Federal Employment Benefits (Note 17) Environmental and Disposal Liabilities (Note 14) Loan Guarantee Liability (Note 8) Other Liabilities (Note 15 and Note 16) TOTAL LIABILITIES

COMMITMENTS AND CONTINGENCIES (NOTE 16) NET POSITION Unexpended Appropriations - Dedicated Collections (Note 23) Unexpended Appropriations - Other Funds Cumulative Results of Operations - Dedicated Collections (N TOTAL NET POSITION

TOTAL LIABILITIES AND NET POSITION

Policy & Procedures

56

Contact Information

• LCDR Khris Johns, CPA, CGFM– [email protected]

• Bobby Hart, CPA, CMA, CFM, PMP, CGFM, CICA– [email protected]

57

Picture Sources

• Presentation and disclosure– Construction site:

https://commons.wikimedia.org/wiki/File:Construction_in_Toronto_May_2012.jpg– Finished Building: https://en.wikipedia.org/wiki/Area_codes_416,_647,_and_437

• Existence and occurrence– Clipboard: http://wheresthebenefit.blogspot.com/2012/06/guest-post-spoon-overdrafts-and-

wca.html – Geologist: http://www.thaigoodview.com/files/u84124/gt_geologist04.jpg

• Existence and occurrence– System: https://dpassupport.golearnportal.org/images/DPAS_Role_Difference.pngSlide 10 -

Valuation and allocation• Slide 10 – Valuation and allocation

– Mathematician: http://narlmathsci.wikispaces.com/ • Slide 12 – Unreserved Assertion

– http://www.buildipedia.com/