The Financial Close Process: Implications for Future

Research

The Financial Close Process: Implications for Future

Research

Diane Janvrin (Iowa State University)Maureen Mascha (University of Wisconsin – Oshkosh)

Why Financial Close Process Research?Why Financial Close Process Research?

“The economic volatility of the past few years has left businesses hungering for more timely and uniform financial information to help them react quickly to fast-changing conditions.” Emily Chasan, Wall Street Journal, 2012

“Finance organizations need to proactively manage the challenges of data quality and prepare for the upcoming regulatory requirements to avoid creating a perfect storm for their financial close and consolidation processes.” Raj Chhabra, Deliotte Consulting Director, 2010

Financial Close DefinitionFinancial Close Definition

routine process of completing the accounting cycle and preparing internal and external reports

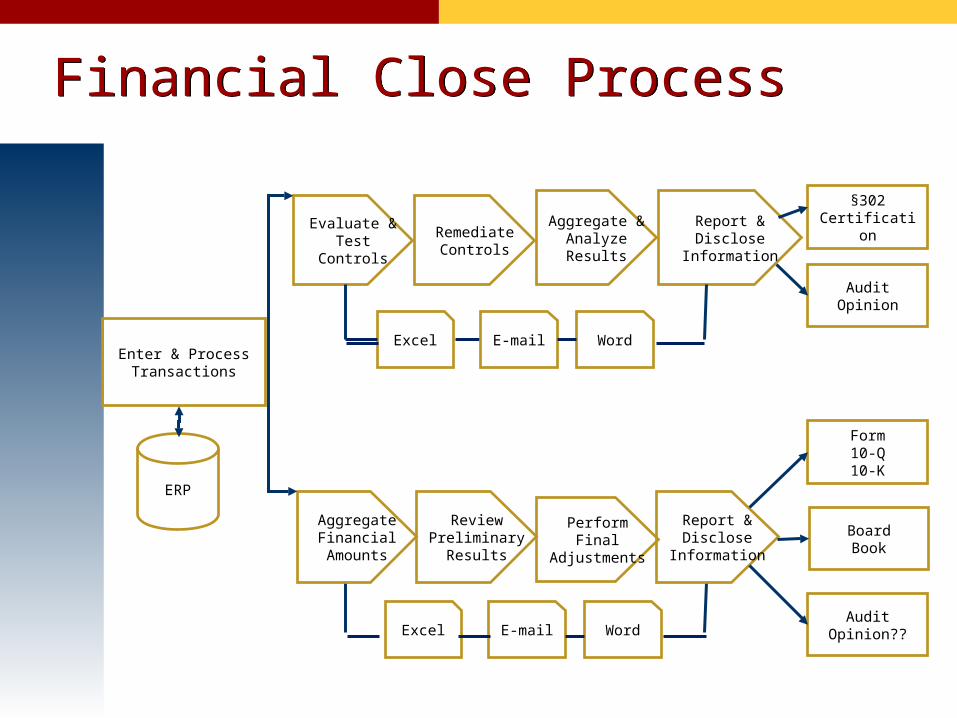

Financial Close ProcessFinancial Close Process

Enter & Process Transactions

Report & Disclose Information

Aggregate & Analyze Results

RemediateControls

Evaluate & Test Controls

§302Certification

Audit Opinion

Form10-Q10-K

BoardBook

AuditOpinion??

AggregateFinancialAmounts

ReviewPreliminary

Results

PerformFinal

Adjustments

Report &Disclose

Information

ERP

Word

Excel E-mail Word

Excel E-mail

Why is financial close process important?Why is financial close process important?

Recent economic volatility and increase in number of restatements

Regulations (i.e., Sarbanes-Oxley, fair value accounting standards, SEC’s XBRL mandate) increase period-end workload

Several recent SEC filings have significant control weaknesses related to financial close process

Time needed to complete the financial close process = internal information environment quality??

Our approachOur approach

Literature review to identify critical issues

Use results to develop field investigation questions

Conduct field investigation with various financial close participants

Analyze results

Develop future research recommendations

Four factorsFour factors

Need to meet expectations

Collaboration between multiple participants

Estimation process

Ability to incorporate new regulations into financial close process

Need to meet expectationsNeed to meet expectations

Companies often attempt to meet or beat analyst expectations during financial close process

Expectation concerns are not limited to year-end earnings

Collaboration between multiple participantsCollaboration between multiple participants

Financial close process may be hidden-profile task

In hidden-profile tasks, teams using bulletin-board computer-mediated communication tool may outperform teams using chat tool or communicating face-to-face

Before collaboration technology can be effective, participants

need to accept the technology Role ambiguity may impact participants’ willingness to

collaborate

Estimation processEstimation process

Even small changes in management’s estimates can trigger material misstatement

Estimates allow analysts to predict future year's earnings, although they are less predictive of future cash flows

Investors find ex post estimate analysis informative

Ability to incorporate new regulations into the financial close processAbility to incorporate new regulations into the financial close process

Many new regulations balance need for standardization with need for professional judgment

Technology may improve financial close process

timeliness In-house processes may increase organizational

knowledge while outsourcing options may be cheaper

Field InvestigationField Investigation

To date, 10 firms ranging from small firms to Fortune 50 companies

Director of Financial Reporting / Controller

12 questions based on literature review

30 to 45 minutes

Need to meet expectationsNeed to meet expectations

Meeting report deadline dates is critical

Meeting target bottom line numbers varies widely among firms

Companies that update forecast monthly tend to face more target bottom line pressure

Collaboration between multiple participantsCollaboration between multiple participants

Very important

Particularly for organizations with decentralized accounting functions

Estimation processEstimation process

Importance of estimation process varies significantly

Internal controls over estimation process vary widely

Some firms conduct detailed estimation reviews prior to period end

Changes in estimates is often last-minute change

Ability to incorporate new regulations into the financial close processAbility to incorporate new regulations into the financial close process

Varies widely among firms

Often can delay and/or add stress to financial close process

Firms have moved from outsourcing XBRL to internal XBRL software (bolt-on)

XBRL tagging process no long delays financial close process although several managers still question why they need to tag financial statement values

Future Research OpportunitiesFuture Research Opportunities

Need to meet expectationsNeed to meet expectations

• Research has examined to some degree who analysts and lenders form their early earnings expectations (Beaver 1979; Kim and Verrecchia 1991, 1997; Barron et al. 1998)

• Still opportunity to examine how expectations impact management’s actions and effectiveness and efficiency of financial close process

Collaboration between multiple participantsCollaboration between multiple participants

Collaboration involves performing hidden-profile task

How can hidden-profile task research improve collaboration between financial close participants?

Estimation processEstimation process

• Explore how time pressure impacts effectiveness and efficiency of estimation process

• Could ex post estimate analysis improve not only period-end estimates but potentially financial close process?

• How do improvements in technology and documentation techniques affect estimate accuracy?

Ability to incorporate new regulations into the financial close processAbility to incorporate new regulations into the financial close process

• Limited research discussing how companies incorporate new regulations into current close process

• Examine when and how existing systems need to be modified or if new systems need to be developed to meet needs of new regulations

• What impacts decision to move XBRL from outsource to in-house? Why bolt-on rather than integrated approach?

SummarySummary Financial close is important and potentially under-researched

topic

Important due to Recent economic volatility Increase in restatements New regulations Several recent SEC filings with significant financial close process control

weaknesses Time needed to complete financial close process = internal information

environment quality

• Concentrate future research on factors impacting financial close process

Meeting or beating management expectations Collaboration – hidden profile task New standards Estimation process

Questions??Questions??

Benchmarks and Key Performance Indicators (KPIs) of Financial Close Processa

Benchmarks and Key Performance Indicators (KPIs) of Financial Close Processa

Category Benchmarks KPIs

Costs Cost of non-compliance/control failure Increase in number of non-recurring transactions

FTEs for close

New account requests

Finance as percent of revenue Task re-work; supporting schedules

Audit fees as percent of revenue Journal entries containing errors or requiring re-adjustment

Quality

Number of control remediations

Changes in policies/procedures

Auditor adjustments Increase in issue escalations

Post-close adjustments Increase/decrease in expected results (returns, receivables, etc.)

Timeliness

Days to close

Increase in expected volumes (purchase orders, invoices, paychecks, etc.)

Percent tasks late Post cut-off transaction postings

Current days to close vs. previous days to close

a source: Clark 2010