The impact of photovoltaic on power market in Italy

Rome, 27 April 2017

Ing. Dario Migali, Ing. Valerio Covicchio

Forecasting and optimisation unit

Content

1. PV systems overview

1. GSE’s energy sold and relevance in PV market

2. Installed capacity of PV systems

3. Geographical Distribution of GSE’s PV capacity

2. Impact of PV systems on Day-Ahead Market

1. System Marginal Price

2. Demand

3. Constraints

4. Wholesale energy price (PUN)

5. Zero prices

2

3

PV systems overview Gse’s energy sold and relevance in PV market

11

During 2016 GSE has sold in the Italian electricity market*, commonly called Italian Power Exchange (IPEX), around 27 TWh of electricity produced by RES power plants.

The share of solar energy is 49% (13,4 TWh) of total renewable energy sources sold on the market.

(*) Data are reffered to Day Ahead Market’s sales

0

500

1000

1500

2000

2500

3000

3500

4000

Jan Feb Mar Apr May jun jul Ago Sep Oct Nov Dec

GWh

Energy sold in Day-Ahead Market 2016

Others

Biogas

Hydro

Wind

PV

Thermal

49%

6%

15%

25%

5%

%Share of RES 2016

PV Wind Hydro Biogas Others

4

PV systems overview Installed capacity ,production

12

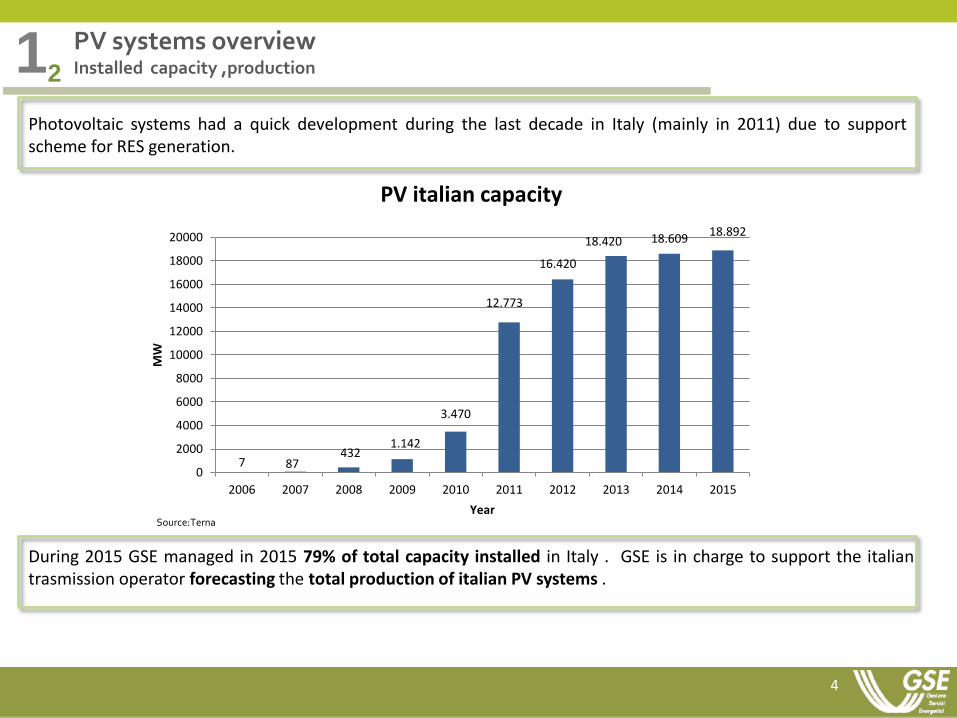

Photovoltaic systems had a quick development during the last decade in Italy (mainly in 2011) due to support scheme for RES generation.

7 87 432

1.142

3.470

12.773

16.420

18.420 18.609 18.892

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MW

Year

PV italian capacity

During 2015 GSE managed in 2015 79% of total capacity installed in Italy . GSE is in charge to support the italian trasmission operator forecasting the total production of italian PV systems .

Source:Terna

5

PV systems overview Geographical Distribution of PV power

13

The italian market is splitted in 6 market zones (NORD , CNORD, CSUD, SUD, SICI, SARD), each of these zones is considered by TSO as a delivery point of elecrtical energy. The figure represents the GSE capacity of PV systems installed* for each zone.

NORD; 7143

CNORD; 1830

CSUD; 2058

SUD; 2419

SICI; 981

SARD; 499

(*) Year 2015

Zonal Capacity in MW

6

Impact of PV systems on Day-Ahead Market Marginal price system and main actors

21

The Day-Ahead market is based on marginal price system. In this kind of system offers and bids are collected and ordered by price. The clearing price (marginal price) is the highest price offered and accepted in the market session. Each power plant that offered a lower price is paid at the same price (marginal price). Accordingly the intoduction of PV systems (with almost zero variable costs) affects the accepted offer, lowering the clearing price.

RES

2

1

3

1 2 Coal

3 Gas

PV

3

2

4

1 2 RES

3 Coal

4 Gas

1

Price

Quantity

Price

Quantity

7

Impact of PV systems on Day-Ahead Market Demand

22

The economic impact of PV production on italian energy market is strictly linked to demand. In order to have a better understanding of price’s development it is necessary to analyze evolution of energy demand in time and geographical distribution of local requirement of energy.

317.533 318.953 319.037

299.915

309.885

313.792

307.220

297.288

291.084

297.180

275000

280000

285000

290000

295000

300000

305000

310000

315000

320000

325000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Consumption

GWh

8

Impact of PV systems on Day-Ahead Market Demand

22

The consumption of electrical energy is not homogeneously distributed over the grid. The NORD market zone consumption is 57% of the national consumption*.

(*) Year 2015, SourceTerna

Zonal Consumption in GWh

NORD; 169241,3

CNORD; 31344,4

CSUD; 45030

SUD; 25804,6

SICI; 17355,9

SARD; 8403,5

9

Impact of PV systems on Day-Ahead Market Constraints

23

Terna (TSO) evaluates power flows limitations on the grid and provide this information before Day-Ahead market opening. The market’s algorithm collects all natiolan supply offers and demand bids (described in terms of quantity and price) and calculates the marginal price of accepted quantities. If equilibrium between supply and demand does not satisfy these constraints the market algorithm runs again splitting one or more market zones.

Example of market split (14/04/2017)

0

20

40

60

80

100

1 3 5 7 9 11 13 15 17 19 21 23

€/MWh

NORD CNOR CSUD SUD SARD SICI

10

Impact of PV systems on Day-Ahead Market Wholesale energy price (PUN)

24

The single national price (PUN) is the wholesale price of weighted average of zonal prices formed in each market zone. Contraction of demand, development of fuel’s cost, increase of PV installations and evolution of imports are the main factors that affect PUN’s evolution in time.

74,8 71,0

87,0

63,7 64,1

72,2 75,5

63,0

52,1 52,3

0

10

20

30

40

50

60

70

80

90

100

275000

280000

285000

290000

295000

300000

305000

310000

315000

320000

325000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Pu

n E

uro

/MW

h

De

man

d G

Wh

Demand/Pun

Demand Pun

11

Impact of PV systems on Day-Ahead Market Wholesale energy price (PUN)

24

PV production has a direct impact on hourly national price evolution over a day. This penomenon is not evident in annual average PUN’s trend. The figure below shows the average value of hourly price.

0

20

40

60

80

100

120

140

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

€/M

Wh

hour

PUN

2006

12

Impact of PV systems on Day-Ahead Market Wholesale energy price (PUN)

24

0

20

40

60

80

100

120

140

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

€/M

Wh

hour

PUN

2006

2011

2016

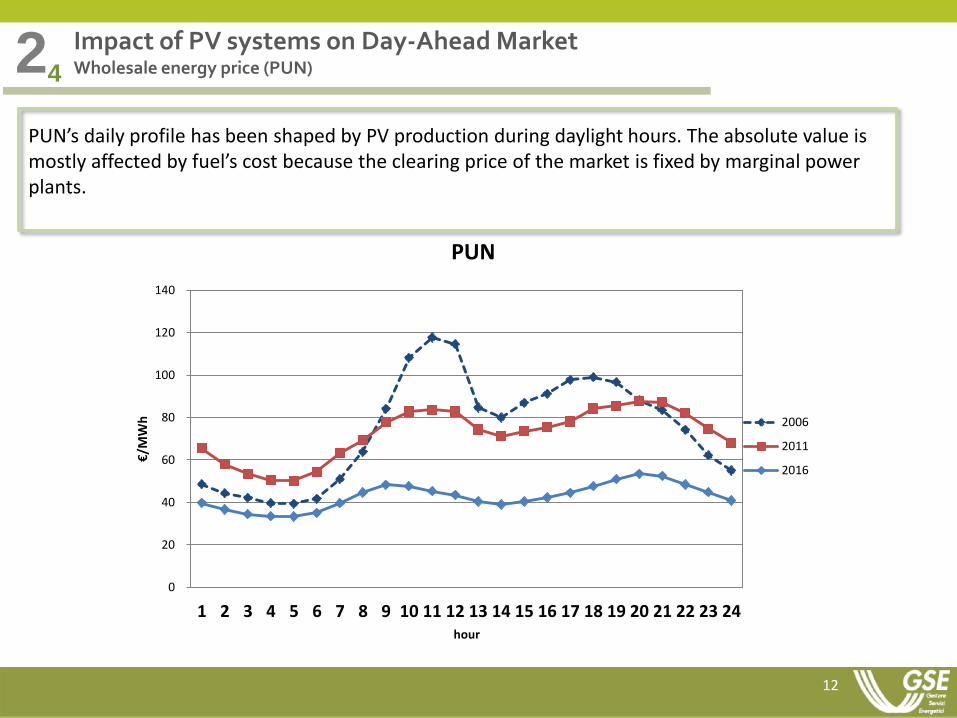

PUN’s daily profile has been shaped by PV production during daylight hours. The absolute value is mostly affected by fuel’s cost because the clearing price of the market is fixed by marginal power plants.

13

Impact of PV systems on Day-Ahead Market Wholesale energy price (PUN)

24

Peak price hours shift and increased stability of mean hourly price over the day

0

20

40

60

80

100

120

140

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

€/M

Wh

hour

PUN

2006

2016

14

Impact of PV systems on Day-Ahead Market Zero Prices

24

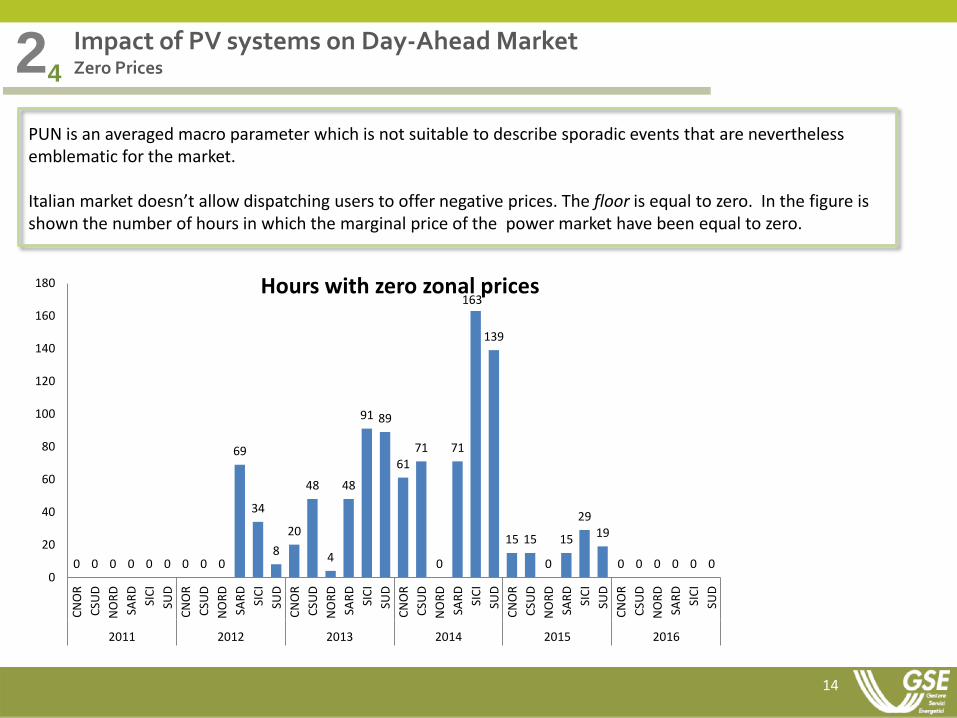

PUN is an averaged macro parameter which is not suitable to describe sporadic events that are nevertheless emblematic for the market. Italian market doesn’t allow dispatching users to offer negative prices. The floor is equal to zero. In the figure is shown the number of hours in which the marginal price of the power market have been equal to zero.

0 0 0 0 0 0 0 0 0

69

34

8

20

48

4

48

91 89

61 71

0

71

163

139

15 15

0

15

29 19

0 0 0 0 0 0 0

20

40

60

80

100

120

140

160

180

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

2011 2012 2013 2014 2015 2016

Hours with zero zonal prices

15

Impact of PV systems on Day-Ahead Market Zero Prices

24

PUN is an averaged macro parameter which is not suitable to describe sporadic events that are nevertheless emblematic for the market. Italian market doesn’t allow dispatching users to offer negative prices. The floor is equal to zero. In the figure is shown the number of hours in which the marginal price of the power market have been equal to zero.

0 0 0 0 0 0 0 0 0

69

34

8

20

48

4

48

91 89

61 71

0

71

163

139

15 15

0

15

29 19

0 0 0 0 0 0 0

20

40

60

80

100

120

140

160

180

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

CN

OR

CSU

D

NO

RD

SAR

D

SIC

I

SUD

2011 2012 2013 2014 2015 2016

Hours with zero zonal prices

275000

280000

285000

290000

295000

300000

305000

310000

315000

320000

325000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

De

man

d G

Wh

Demand

Demand

16

Next steps

3

The anomalies underlined require investments in grid development and

improvement of market rules and structure The main issues authorities and stakeholders are working on are: • Capacity Market

• Dispacthing services in MT/BT (DSO)

• Ancillary services provided by FER

17

Thanks for your attention