Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

The Multilateral Convention Panel Discussion

15 June 2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Need for BEPS

215-06-2017

Income tax developed in the 19th century - an alignment between economic reality and tax rules

Globalisation resulted in the rise of multinationals (MNCs) with operations in various jurisdictions – opportunity to look at tax ‘cost’ savings

Saving = erosion of tax bases in high tax countries and shifting taxable profits to no or low tax jurisdictions

Significant revenue losses through tax leakages in many countries

G20 countries and OECD felt a need to end tax avoidance or evasion by way of Base Erosion Profit Shifting (BEPS) Project

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Changes to the international taxation landscape

BEPS Actions

315-06-2017

Action 6: Prevent treaty abuse

Action 7: Prevent the artificial avoidance of permanent establishment status

Action 8: Consider transfer pricing for intangibles

Action 9: Consider transfer pricing for risks and capital

Action 10: Consider transfer pricing for other high-risk transactions

Action 15: Development of amultilateral instrument foramending bilateral treaties

Action 11: Establishmethodologies to collect andanalyse data on BEPS andactions addressing it

Action 12: Require taxpayers todisclose their aggressive taxplanning arrangements

Action 13: Re-examine transferpricing documentation

Action 14: Making disputeresolutions more effective

Action 2: Neutralise the effectsof hybrid mismatcharrangements

Action 3: Strengthen CFC rules

Action 4: Limit base erosion viainterest deductions and otherfinancial payments

Action 5: Counter harmful taxpractices more effectively,taking into accounttransparency and substance

Action 1: Address the taxchallenges of the digitaleconomy

Action Plan on Base Erosion and

Profit Shifting (BEPS)

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

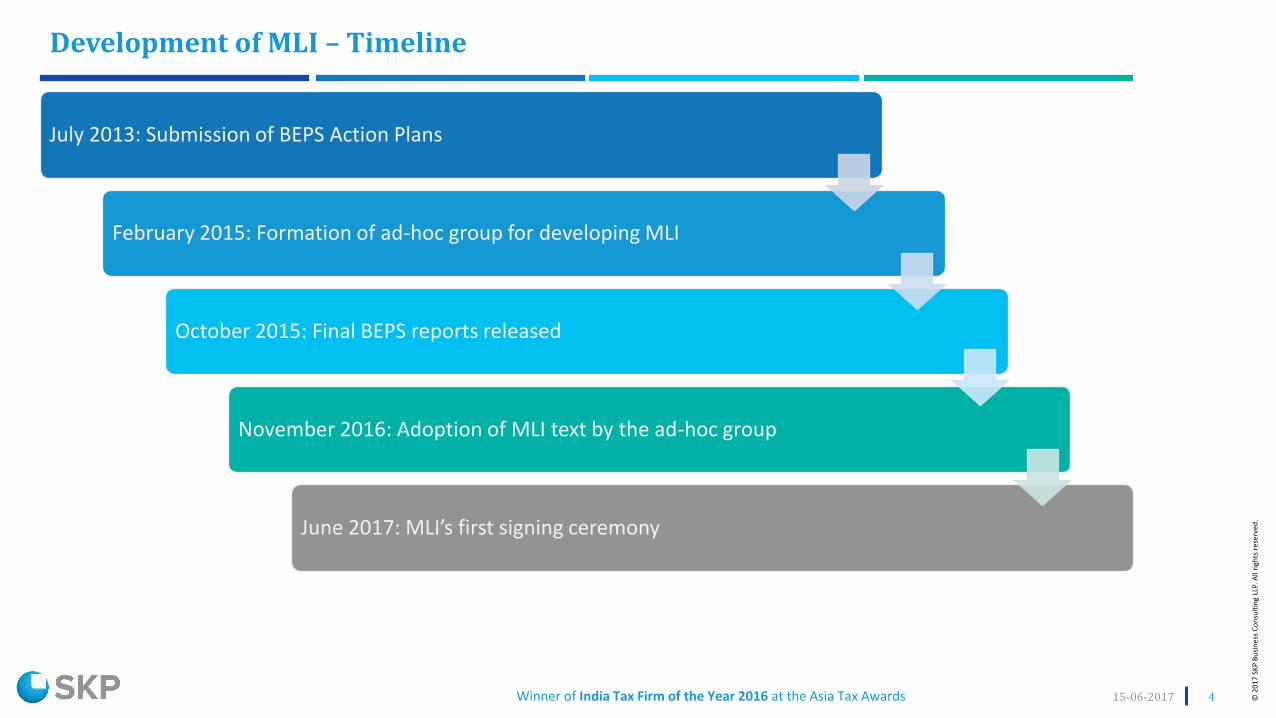

Development of MLI – Timeline

415-06-2017

July 2013: Submission of BEPS Action Plans

February 2015: Formation of ad-hoc group for developing MLI

October 2015: Final BEPS reports released

November 2016: Adoption of MLI text by the ad-hoc group

June 2017: MLI’s first signing ceremony

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

68 jurisdictions have signed the MLI on 7 June 2017

India has signed the MLI and notified tax treaties of 93 countries including Mauritius, Singapore, United States ofAmerica, Netherlands, etc.

United States of America has not signed the MLI

Mauritius has deferred signing of MLI till 30 June 2017

Notable treaty partners of India such as United Arab Emirates, Malaysia, Brazil have yet not signed the MLI

Germany and China have not notified their tax treaties with India

Totally, 1105 treaties covered under the MLI – aim is to cover most of existing 3000 tax treaties

All positions notified under the MLI are currently provisional – final positions will be notified subsequently

How does MLI Apply?

515-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

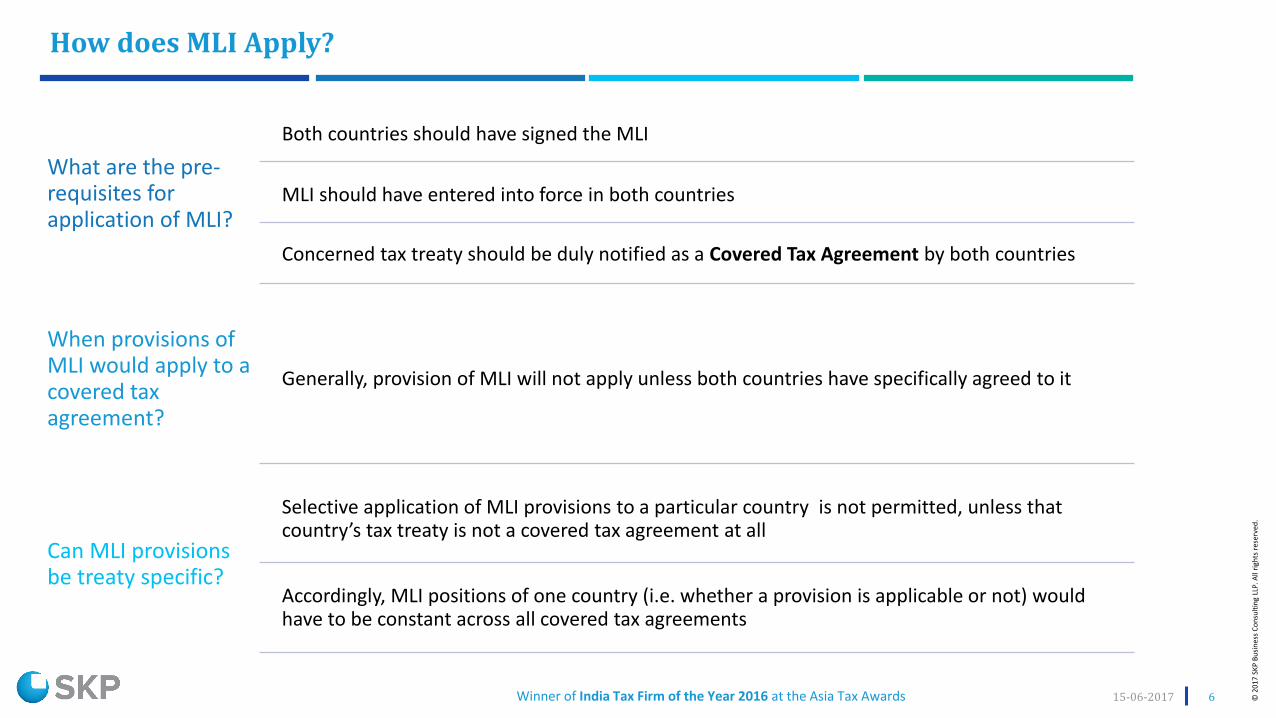

How does MLI Apply?

615-06-2017

What are the pre-requisites for application of MLI?

Both countries should have signed the MLI

MLI should have entered into force in both countries

Concerned tax treaty should be duly notified as a Covered Tax Agreement by both countries

When provisions of MLI would apply to a covered tax agreement?

Generally, provision of MLI will not apply unless both countries have specifically agreed to it

Can MLI provisions be treaty specific?

Selective application of MLI provisions to a particular country is not permitted, unless that country’s tax treaty is not a covered tax agreement at all

Accordingly, MLI positions of one country (i.e. whether a provision is applicable or not) would have to be constant across all covered tax agreements

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

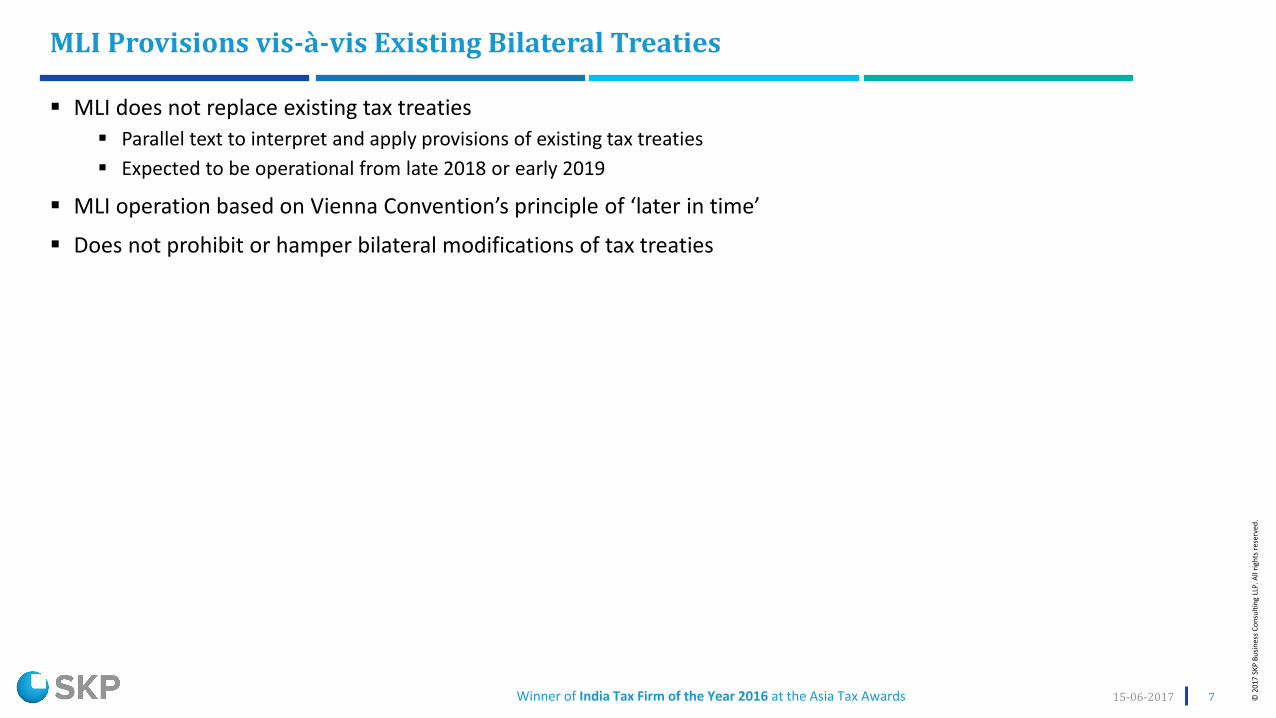

MLI does not replace existing tax treaties

Parallel text to interpret and apply provisions of existing tax treaties

Expected to be operational from late 2018 or early 2019

MLI operation based on Vienna Convention’s principle of ‘later in time’

Does not prohibit or hamper bilateral modifications of tax treaties

MLI Provisions vis-à-vis Existing Bilateral Treaties

715-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

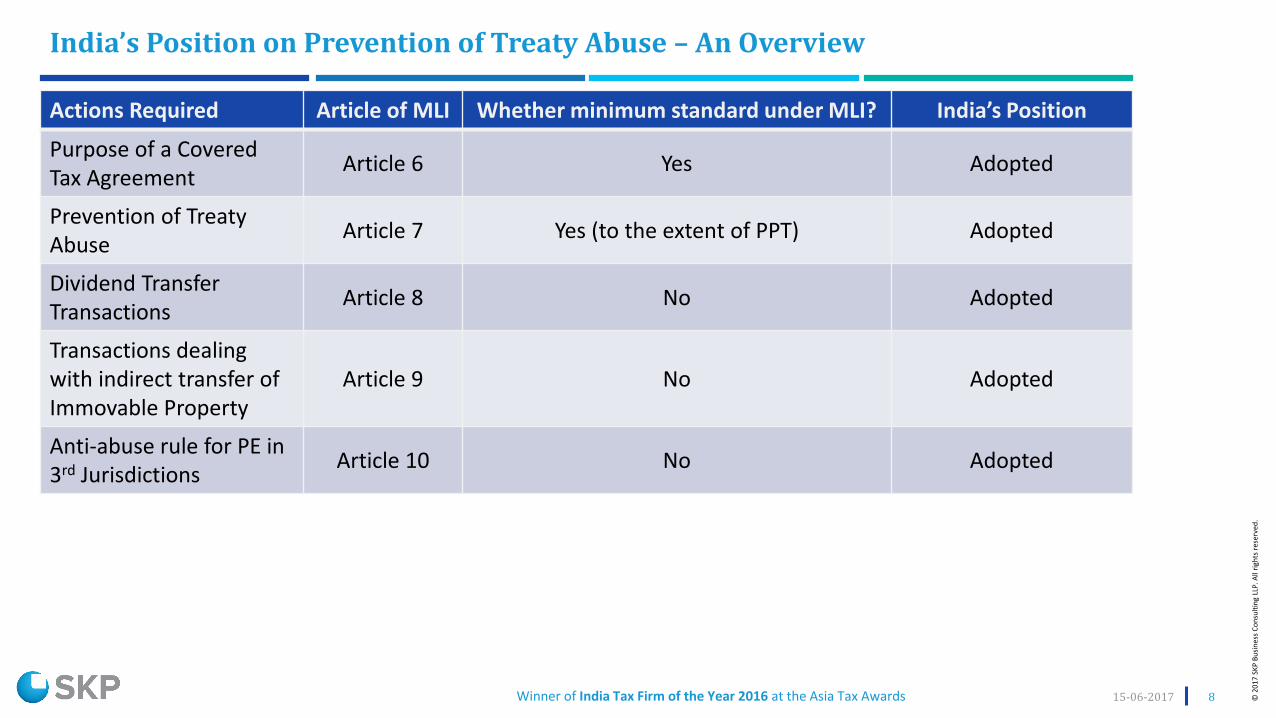

India’s Position on Prevention of Treaty Abuse – An Overview

815-06-2017

Actions Required Article of MLI Whether minimum standard under MLI? India’s Position

Purpose of a Covered Tax Agreement

Article 6 Yes Adopted

Prevention of Treaty Abuse

Article 7 Yes (to the extent of PPT) Adopted

Dividend Transfer Transactions

Article 8 No Adopted

Transactions dealing with indirect transfer of Immovable Property

Article 9 No Adopted

Anti-abuse rule for PE in 3rd Jurisdictions

Article 10 No Adopted

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Article 6 of MLI – requires every covered tax agreement to include preamble

Preamble to bring out that the purpose of the tax treaty is to:

eliminate double taxation

without creating opportunities for non-taxation or reduced taxation

through tax evasion or avoidance

including through treaty-shopping arrangements aimed at obtaining reliefs for the indirect benefit of residents of third jurisdictions

The preamble would assist in interpretation and application of tax treaty provisions in the required spirit

This article being a minimum standard will apply to all of India’s tax treaties who are signatories to the MLI

Article 6 of MLI – Preamble

915-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Article 7 of MLI requires:

implementing a Principal Purpose Test (PPT) only (minimum standard); or

a PPT along with SLOB (optional); or

a DLOB (instead of PPT or SLOB) in line with BEPS recommendations (optional)

PPT to deny treaty benefits if one of the principal purposes of an arrangement or transaction is to obtaintax treaty benefits

PPT is broad and generic whereas supplementary SLOB is more defined and clear with suitable carve outs

India has opted for PPT plus SLOB

However, Netherlands, Singapore, Cyprus, France , Luxembourg, have not opted for SLOB

Accordingly, only PPT should apply in such tax treaties

Interesting to understand interplay between PPT and GAAR

Article 6 of MLI – Prevention of Treaty Abuse

1015-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

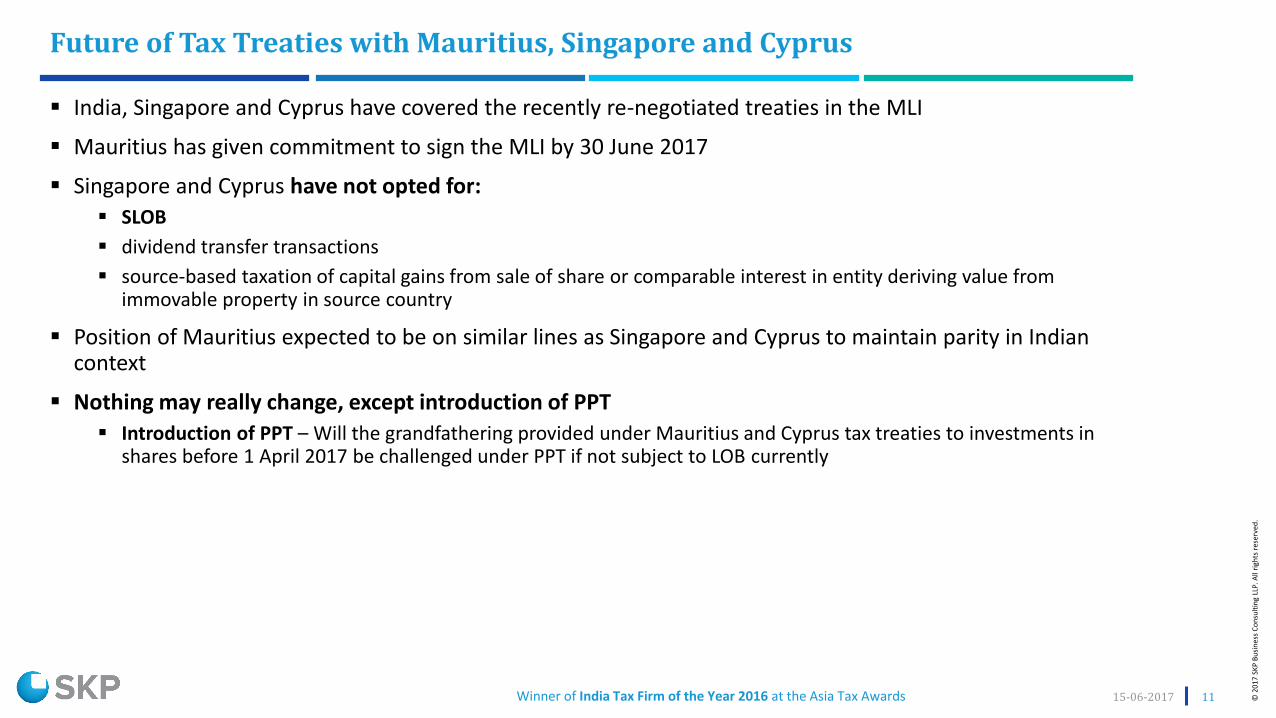

India, Singapore and Cyprus have covered the recently re-negotiated treaties in the MLI

Mauritius has given commitment to sign the MLI by 30 June 2017

Singapore and Cyprus have not opted for:

SLOB

dividend transfer transactions

source-based taxation of capital gains from sale of share or comparable interest in entity deriving value fromimmovable property in source country

Position of Mauritius expected to be on similar lines as Singapore and Cyprus to maintain parity in Indiancontext

Nothing may really change, except introduction of PPT

Introduction of PPT – Will the grandfathering provided under Mauritius and Cyprus tax treaties to investments inshares before 1 April 2017 be challenged under PPT if not subject to LOB currently

Future of Tax Treaties with Mauritius, Singapore and Cyprus

1115-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Commissionaire arrangement

Specific activity exemption – preparatory and auxiliary services

Splitting-up of contracts

Action Plan 7 – Artificial Avoidance of PE

1215-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

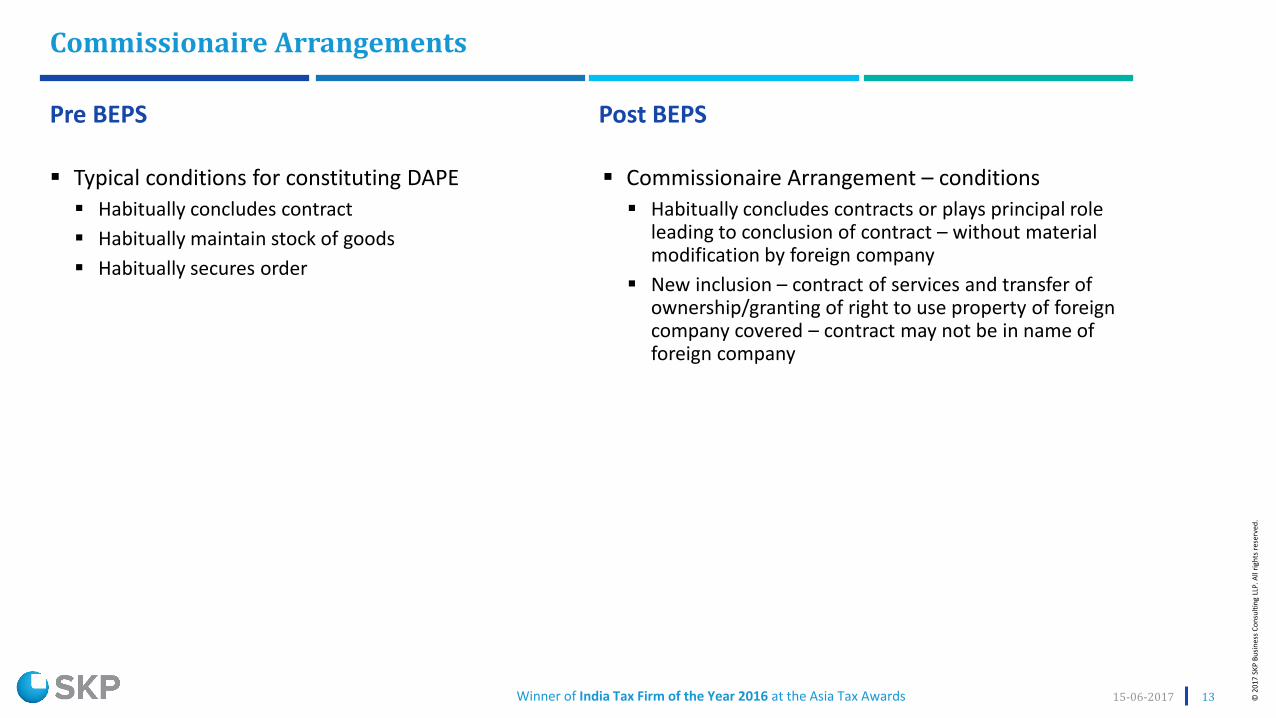

Commissionaire Arrangements

Pre BEPS

Typical conditions for constituting DAPE

Habitually concludes contract

Habitually maintain stock of goods

Habitually secures order

Post BEPS

Commissionaire Arrangement – conditions

Habitually concludes contracts or plays principal roleleading to conclusion of contract – without materialmodification by foreign company

New inclusion – contract of services and transfer ofownership/granting of right to use property of foreigncompany covered – contract may not be in name offoreign company

1315-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Commissionaire Arrangements

Impact on Liaison Office

Activities of liaison office – whether playing principal role?

Whether activities are preparatory and auxiliary?

1415-06-2017

Impact on EPC Contracts

Taxability trigger – onshore services

Impact – onshore services split between entities

Impact on Marketing Entities

DAPE conditions – wider and subjective

Operations in India – needs a relook

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Article 4 of the MLI deals with determination of residency of dual resident entities (tie-break)

Such cases to be solved only by mutual agreement of competent authorities

in absence of mutual agreement, no relief or exemption would be granted unless otherwise provided

Factor such as

POEM

place of incorporation or constitution and

other relevant factors

would be considered for tie-breaking

Countries that have opted for this article along with India

Australia, Netherlands, United Kingdom

Countries that have not opted for this article along with India

Singapore, Cyprus, Luxembourg, Denmark

Article 4 of MLI – Tie-break For Dual Resident Entities

1515-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Article 4 of MLI – Impact on Key Treaties

1615-06-2017

Treaty Partners Pre BEPS Adoption of Article 4 of MLI Post BEPS

Australia POEM Yes MAP replaces POEM

Netherlands POEM Yes MAP replaces POEM

United Kingdom POEM Yes MAP replaces POEM

Japan MAP Yes MAP provisions strengthened

Singapore POEM NoExisting article remains unchanged as Singapore has opted out of this article

Cyprus

- POEM,- If cannot be determined by

POEM, then by MAP within 2 years

NoExisting article remains unchanged as Cyprus has opted out of this article

Luxembourg

- POEM,- If cannot be determined by

POEM, then by Mutualagreement

NoExisting article remains unchanged as Luxembourghas opted out of this article

Denmark POEM NoExisting article remains unchanged as Denmark has opted out of this article

CanadaMAP, in absence of which no tax benefits available

NoExisting article remains unchanged as Canada has opted out of this article – however, similar to Article 4 of MLI

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

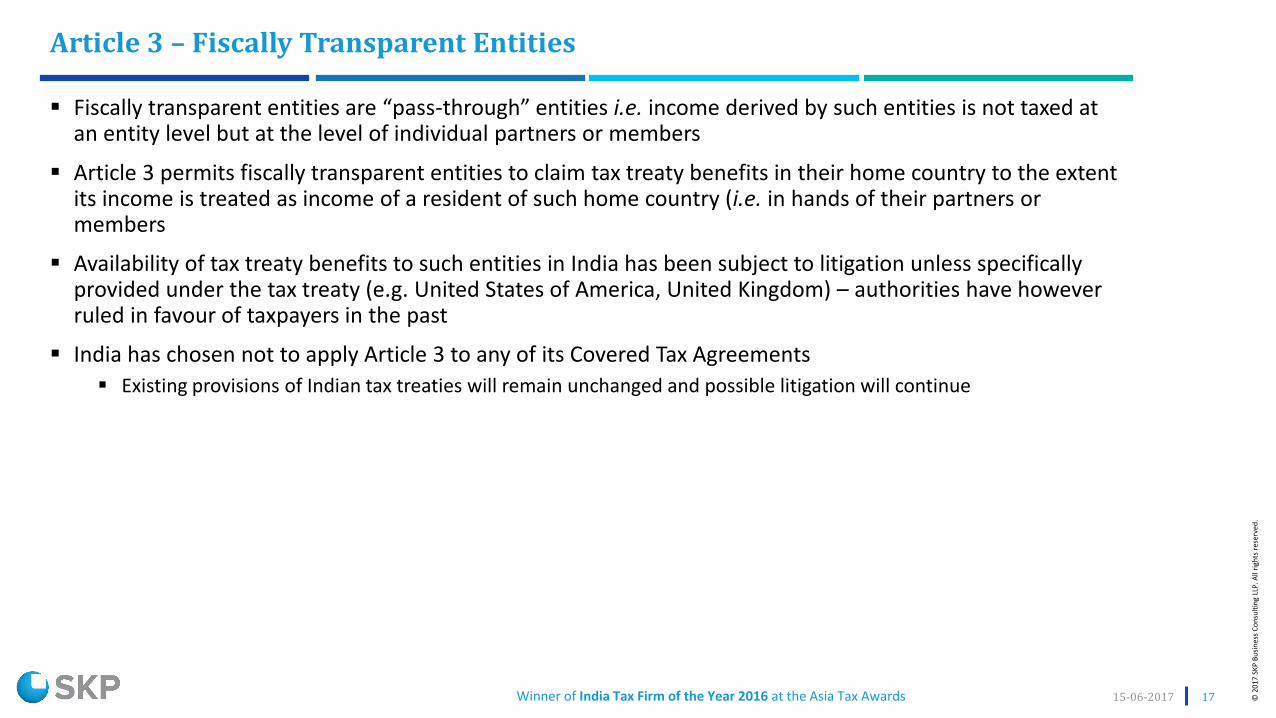

Fiscally transparent entities are “pass-through” entities i.e. income derived by such entities is not taxed at an entity level but at the level of individual partners or members

Article 3 permits fiscally transparent entities to claim tax treaty benefits in their home country to the extent its income is treated as income of a resident of such home country (i.e. in hands of their partners or members

Availability of tax treaty benefits to such entities in India has been subject to litigation unless specifically provided under the tax treaty (e.g. United States of America, United Kingdom) – authorities have however ruled in favour of taxpayers in the past

India has chosen not to apply Article 3 to any of its Covered Tax Agreements

Existing provisions of Indian tax treaties will remain unchanged and possible litigation will continue

Article 3 – Fiscally Transparent Entities

1715-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

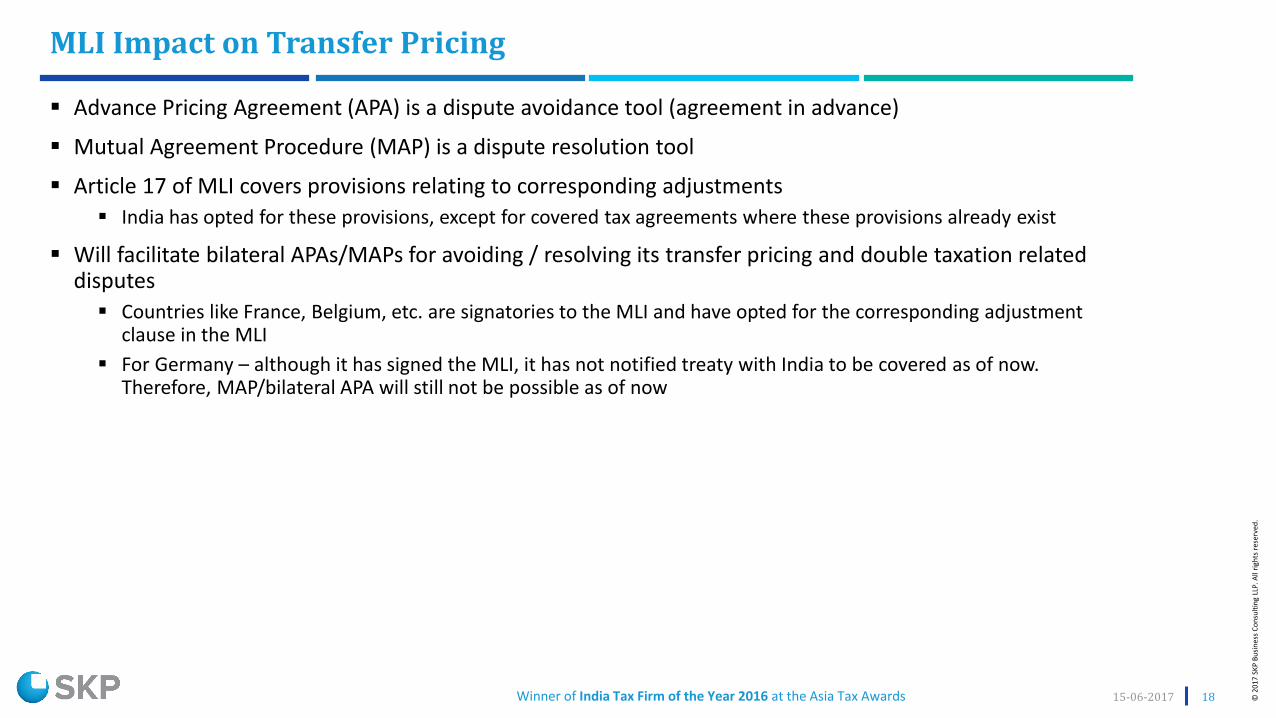

Advance Pricing Agreement (APA) is a dispute avoidance tool (agreement in advance)

Mutual Agreement Procedure (MAP) is a dispute resolution tool

Article 17 of MLI covers provisions relating to corresponding adjustments

India has opted for these provisions, except for covered tax agreements where these provisions already exist

Will facilitate bilateral APAs/MAPs for avoiding / resolving its transfer pricing and double taxation related disputes

Countries like France, Belgium, etc. are signatories to the MLI and have opted for the corresponding adjustment clause in the MLI

For Germany – although it has signed the MLI, it has not notified treaty with India to be covered as of now. Therefore, MAP/bilateral APA will still not be possible as of now

MLI Impact on Transfer Pricing

1815-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Entry into Force

For the first five countries that ratify MLI 1st day of the month after expiry of 3 calendar months after deposit of 5th instrument of ratification or acceptance or approval

For countries that ratify subsequently 1st day of the month after expiry of 3 calendar months after deposit of instrument of ratification or acceptance or approval

India’s position on entry into effect initiation date – 30 days after both countries notify completion of internal procedures

on withholding taxes – applicable to credits or payments that occur in the taxable year beginning after the initiation date

on other taxes – applicable to taxable year beginning after expiry of 6 months from the initiation date

For instance, India-Australia tax treaty, if date of notification to the OECD of completion of internal procedures by India is 1 March 2019 and by Australia is 1 January 2019, then initiation date will be 31 March 2019 i.e. 30 days after the later of the aforesaid dates

applicability for withholding taxes – credits or payments that occur in FY 2019-20 (taxable year starting after 31 March 2019)

applicability for other taxes – in FY 2020-21 i.e. taxable year starting after expiry of 6 months from initiation date of 31 March 2019

Entry into Force or Entry into Effect of MLI

1915-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Multinationals to understand whether their strategies are BEPS-ready

Multinationals to analyse their group functions in light of substance and transfer pricing policies

Multinationals to re-check financing options, treasury functions and operating model

Specifically

BEPS impact on sales and marketing operations from PE perspective

Limited Risk Distributor model

Limit on interest deduction

Carrying out a value chain analysis of the overall value chain

Employee mobility and recruitment

Action Points for Multinationals in India

2015-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

MLI is a landmark change from perspective of taxation of cross border transactions

Interpretation of tax treaty no longer straightforward or simple

Tax treaty to be read along with MLI provisions (including inclusions or exclusions or reservations)

Important for businesses and advisors to analyze and understand the potential impact of MLI on commercial operations

Conclusion

2115-06-2017

© 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

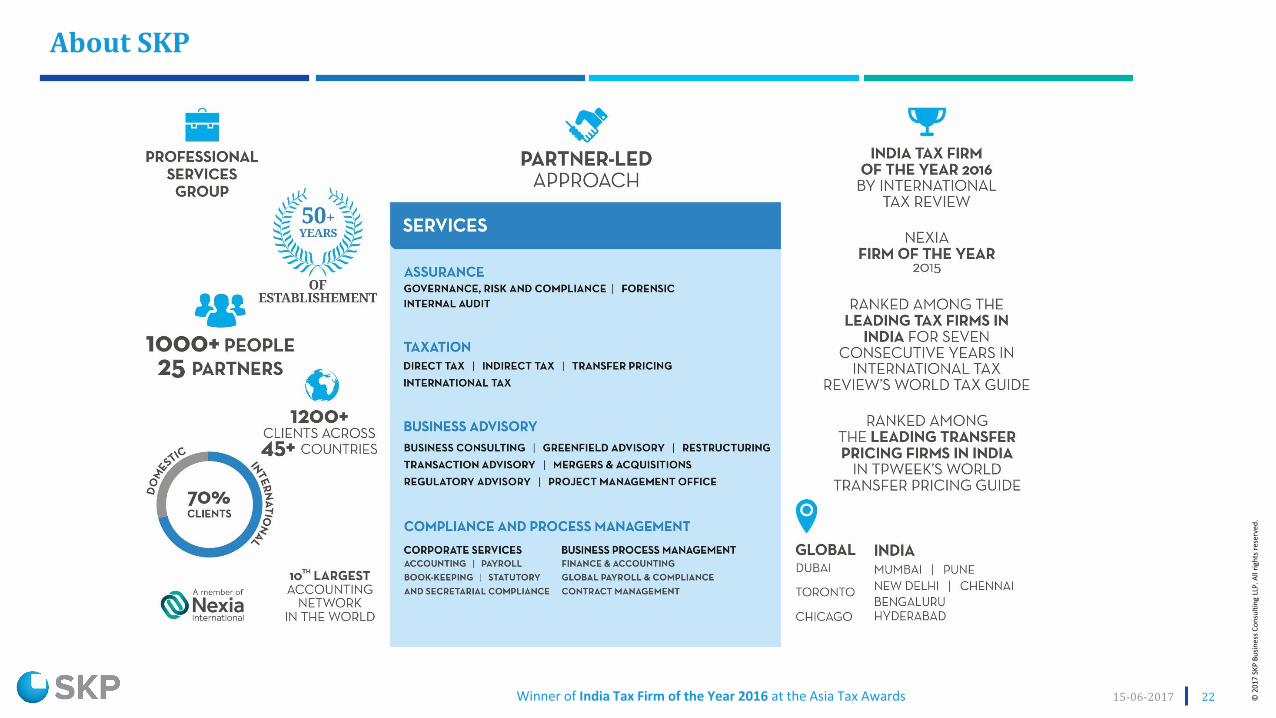

About SKP

2215-06-2017

The contents of this presentation are intended for general marketing and informative purposes only and should not be construed to becomplete. This presentation may contain information other than our services and credentials. Such information should neither beconsidered as an opinion or advice nor be relied upon as being comprehensive and accurate. We accept no liability or responsibility to anyperson for any loss or damage incurred by relying on such information. This presentation may contain proprietary, confidential or legallyprivileged information and any unauthorised reproduction, misuse or disclosure of its contents is strictly prohibited and will be unlawful.

DisclaimerMumbai

Pune

Hyderabad

New Delhi

Chennai

Bengaluru

Toronto

Chicago

Dubai

Connect with us

Subscribe to our alerts

www.skpgroup.com

SKP Business Consulting LLP is a member firm of the "Nexia International" network. Nexia International Limiteddoes not deliver services in its own name or otherwise. Nexia International Limited and the member firms of theNexia International network (including those members which trade under a name which includes the wordNEXIA) are not part of a worldwide partnership. For the full Nexia International disclaimer, please click here.

Icons designed by Freepik © 2

017

SKP

Bu

sin

ess

Co

nsu

ltin

g LL

P. A

ll ri

ghts

res

erve

d.

2315-06-2017