The Philippine’s Socio-economic

Performance, Outlook, Challenges, and Vision

National Economic and Development Authority

ILO Trade on Employment Workshop6-7 October 2016

Socio-economic Performance

-10

-8

-6

-4

-2

0

2

4

6

8

10

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

The Philippines’ growth trajectory has been improving, with

17 years of uninterrupted expansion

2.01980-1989

2.81990-1999

4.52000-2009

6.22010-2015

GDP growth rates (in %, at constant prices)

Source: Philippine Statistics Authority (PSA)3

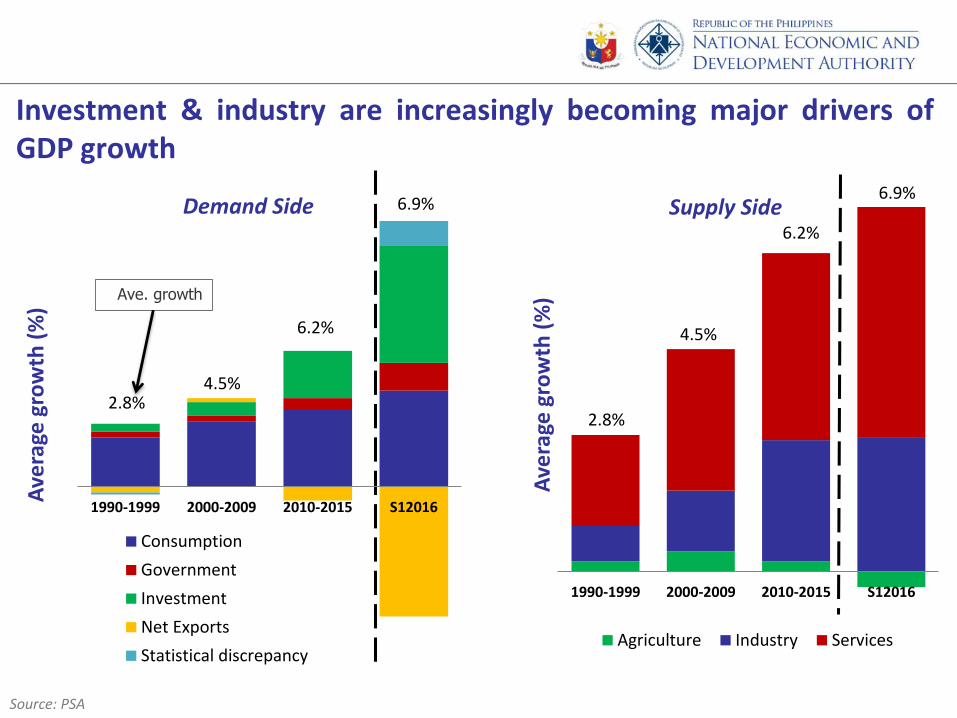

Investment & industry are increasingly becoming major drivers ofGDP growth

Supply SideDemand Side

1990-1999 2000-2009 2010-2015 S12016

Ave

rage

gro

wth

(%

)

Agriculture Industry Services

2.8%

4.5%

6.2%

6.9%

1990-1999 2000-2009 2010-2015 S12016

Ave

rage

gro

wth

(%

)

Consumption

Government

Investment

Net Exports

Statistical discrepancy

2.8%4.5%

6.2%

6.9%

Ave. growth

Source: PSA

PARTICULARS

First

QuarterSecond Quarter

First

Semester

2016 2015 2016 2016

GROSS NATIONAL INCOME 7.4 5.4 6.8 7.1

Net Primary Income 9.9 2.5 6.2 8.0

GROSS DOMESTIC PRODUCT 6.8 5.9 7.0 6.9

By Industrial Origin

Agri, Fishery and Forestry (4.4) (0.1) (2.1) (3.3)

Industry 9.0 6.1 6.9 7.9

o.w. Manufacturing 8.0 4.7 6.3 7.2

Services 7.6 6.7 8.4 8.0

By Expenditure

Household Final Consumption

Expenditure7.0 6.4 7.3 7.2

Gov’t Final Consumption Expenditure 11.8 2.4 13.5 12.7

Capital Formation 26.6 21.4 27.6 27.1

o.w. Fixed Capital Formation 28.2 12.7 27.2 27.7

Exports 7.3 5.1 6.6 7.0

Imports 19.0 12.6 20.9 19.9

Growth accelerated in first half of 2016

Source: PSA

• as of Aug ’16 ** as of Jul’16

Headline and Core Inflation, 2005- 2016*

Inflation has been tame, while financial sector is stable…

Real Interest Rate and Non-performing Loans, 2005- 2016

* Average of Jan - Aug 2016

Source: PSA and Bangko Sentral ng Pilipinas (BSP)

1.7

3.7

15.8

0

2

4

6

8

10

12

14

16

18

20

NPL Ratio*

Real interest rates**

CAR

1.7

1.5

0

1

2

3

4

5

6

7

8

9

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Core Inflation

Headline Inflation

Source: BSP

The country’s external position remains robust

26.2

0.50

20

40

60

80

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 1H 2016

Positive Current Acct. & Declining External Debt

External Debt to GDP ratio - LHS Current Account to GDP Ratio - RHS

85.8

10.0 9

10

11

12

0

20

40

60

80

100

2010 2011 2012 2013 2014 2015 end-Aug 2016

Healthy International Reserves

Gross International Reserves (US$ bn) - LHS Months of import cover - RHS

2.5 3.0

3.8 4.4

4.8 5.0

2.7 3.5

3.9 4.3 4.7 4.8

5.4

3.0

2010 2011 2012 2013 2014 2015 Jan-Jun 2016

Buoyant International Tourism Receipts

Receipts Arrivals

Source: Department of Tourism, IT and Business Process Association of the Philippines

12.8 14.4 16.4 17.3 18.8 20.1 21.4 23.0 24.6 25.8

3.4 4.5 6.1 7.1 8.9

11.0 13.2

16.1 18.9

22.0 25.0

28.9

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 F 2017 F

IT-BPO Revenues is Set to Overtake Remittances

Cash Remittances (US$ bn) IT-BPO Revenues (US$ bn)

Supported by major drivers…

Our stronger fiscal position has been recognized as evidenced by ourinvestment-grade sovereign credit rating

• Modest fiscal deficit; Declining Public debt & interest payments; Increasing reliance on domestic financing • Result: resilient fiscal sector

Fiscal side:

Fiscal Position

National Government Borrowing Program (%)

Share of expenditures allocated to interest payments

National gov’t outstanding debt (% of GDP)

29.7

13.9 12.6

15.5

0

5

10

15

20

0

5

10

15

20

25

30

35

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 S12016

Int. Payments to Disbursement Primary Exp to GDP (rhs)

74.4

41.2

*Using the program 2016 GDP

11.813.6

Fiscal Position Revenue Effort Tax Effort

64.6 65.6 65.283.6

93.972.1

57.671.1

84.0

35.4 34.4 34.816.4

6.127.9

42.428.9

16.0

2009 2010 2011 2012 2013 2014 2015 as of Jul2016

2016Proposed

Domestic Foreign

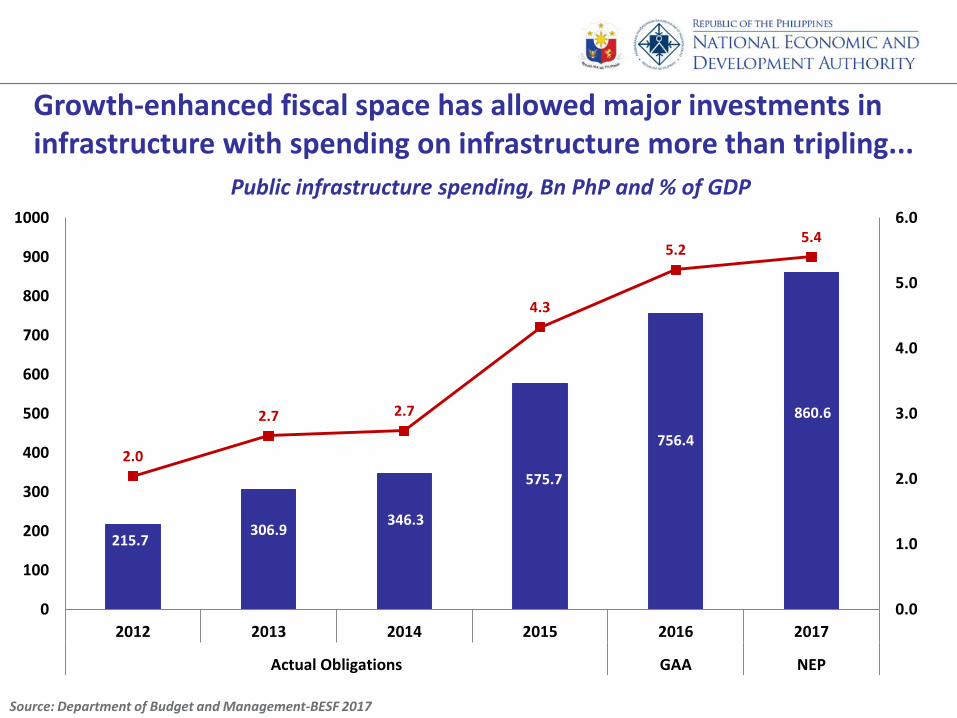

Growth-enhanced fiscal space has allowed major investments in infrastructure with spending on infrastructure more than tripling...

Source: Department of Budget and Management-BESF 2017

Public infrastructure spending, Bn PhP and % of GDP

215.7306.9

346.3

575.7

756.4

860.6

2.0

2.7 2.7

4.3

5.25.4

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

100

200

300

400

500

600

700

800

900

1000

2012 2013 2014 2015 2016 2017

Actual Obligations GAA NEP

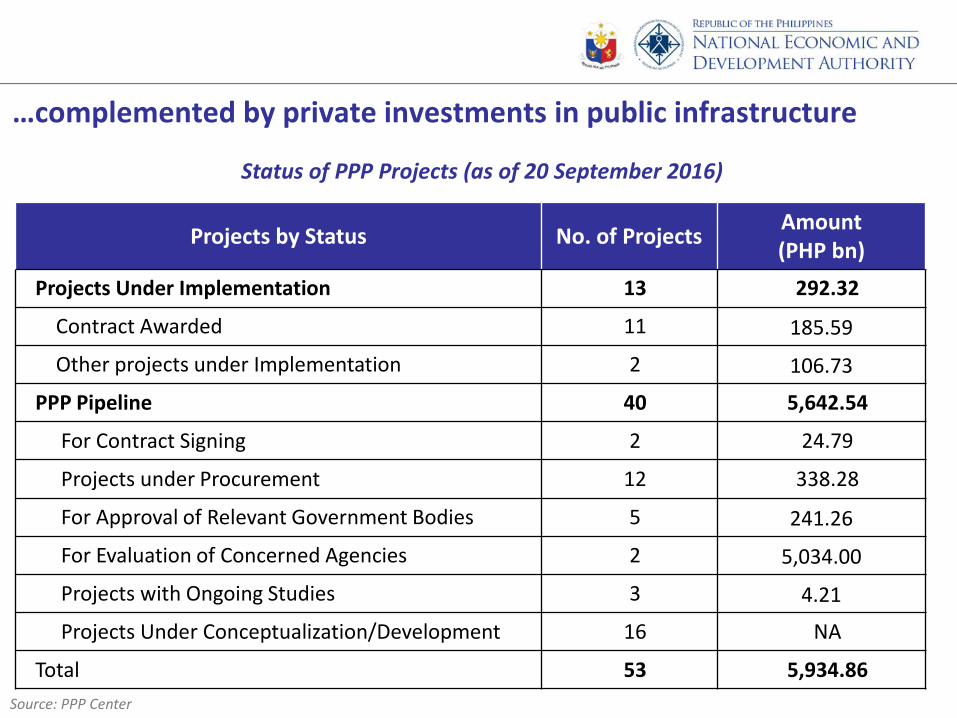

…complemented by private investments in public infrastructure

Source: PPP Center

Status of PPP Projects (as of 20 September 2016)

Projects by Status No. of ProjectsAmount(PHP bn)

Projects Under Implementation 13 292.32

Contract Awarded 11 185.59

Other projects under Implementation 2 106.73

PPP Pipeline 40 5,642.54

For Contract Signing 2 24.79

Projects under Procurement 12 338.28

For Approval of Relevant Government Bodies 5 241.26

For Evaluation of Concerned Agencies 2 5,034.00

Projects with Ongoing Studies 3 4.21

Projects Under Conceptualization/Development 16 NA

Total 53 5,934.86

Source: DBM, PSA-NSCB

Increased fiscal resources have also allowed greater public investments in social services…

1,426 1,372

1,764

2,843

3,519

160 148

359

685762

417 482

888

1,247

1,484

38 56 126 17377

2,644 2,679

3,842

5,777

6,761

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2000-2004 2005-2009 2010-2015 2016 GAA 2017 Proposed

Spending on Social Services Per Capita, Constant Prices

Education Health Social Security (incl. CCT) Housing Total Social Services (rhs)

Our vibrant economy is producing more and better jobs...Unemployment and Underemployment rates (%) Employment Generated 2000- 2015 (‘000)

21.0

22.6

20.1

19.319.118.8

19.3

20.0

19.3

18.418.5

17.9

7.88.0

7.3 7.4 7.5 7.47.0 7.0 7.1

6.66.3

5.7

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

15.0

16.0

17.0

18.0

19.0

20.0

21.0

22.0

23.0

Un

emp

loym

ent

Rat

e

Un

der

emp

loym

ent

Rat

e

Underemployment Rate (%) Unemployment Rate (%)

37823448

4493

50.351.9

57.2

61.9

45

50

55

60

65

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2000-2004/a 2005-2009 2010-2015/c,d Apr-July 2016/e Wag

e an

d s

alar

y w

ork

er (

% in

to

tal e

mp

loym

ent)

Emp

loym

ent

Gen

erat

ed ('

00

0)

Employment Generated ('000) Wage and salary worker (% in total employment)

Wage and salary worker (% in total employment)

a/ Starting 2006, population projection benchmark is based on the 2000 Population Census, hence 2006 employment generation can not be computed due to break in the seriesb/ Starting January 2012 Labor Force Survey (LFS), the codes for industry adopted the 2009 PSIC. Prior to this, codes for industry used the 1994 PSIC.c/ Annualized data for 2014 refer to the average estimates for April, July and October survey rounds that exclude Leyte.d/ Annualized data for 2015 refer to the average estimates of all 4 quarter rounds of LFS 2015 results, excluding Leyte. Employment generation refers to the average of estimates for April, July and October survey rounds. e/Not comparable with previous rounds of LFS; break in the data series due to change sin the Master Sample Design. Starting April 2016, the LFS used the 2013 MS Design, the 2010 Census of Population and Housing(CPH)-based population projections and the 2012 Philippine Standard Occupation Classification (PSOC).

Notes:

Source: PSA

Services and industry sectors remain to be the main contributor in employment generation...

32.2 31.1 30.529.2

25.9

15.3 15.6 16.0 16.218.1

52.6 53.4 53.5 54.756.0

36

37

37

38

38

39

39

40

40

41

41

0

10

20

30

40

50

60

2012 2013 2014a/ 2015b/ Apr-Jul 2016c/

To

tal P

hilip

pin

e E

mp

loym

en

t (i

n m

illio

ns)

Sh

are

in

To

tal E

mp

loym

en

t (%

)

AGRICULTURE INDUSTRY SERVICES TOTAL EMPLOYMENT

a/ Annualized data for 2014 refer to the average estimates for April, July and October survey rounds that exclude Leyte.b/ Annualized data for 2015 refer to the average estimates of all 4 quarter rounds of LFS 2015 results, excluding Leyte. Employment generation refers to the average of estimates for April, July and October survey rounds. c/Not comparable with previous rounds of LFS; break in the data series due to change sin the Master Sample Design. Starting April 2016, the LFS used the 2013 MS Design, the 2010 Census of Population and Housing(CPH)-based population projections and the 2012 Philippine Standard Occupation Classification (PSOC). d/ Starting January 2012 Labor Force Survey (LFS), the codes for industry adopted the 2009 PSIC. Prior to this, codes for industry used the 1994 PSIC.

Notes:

Source: PSA

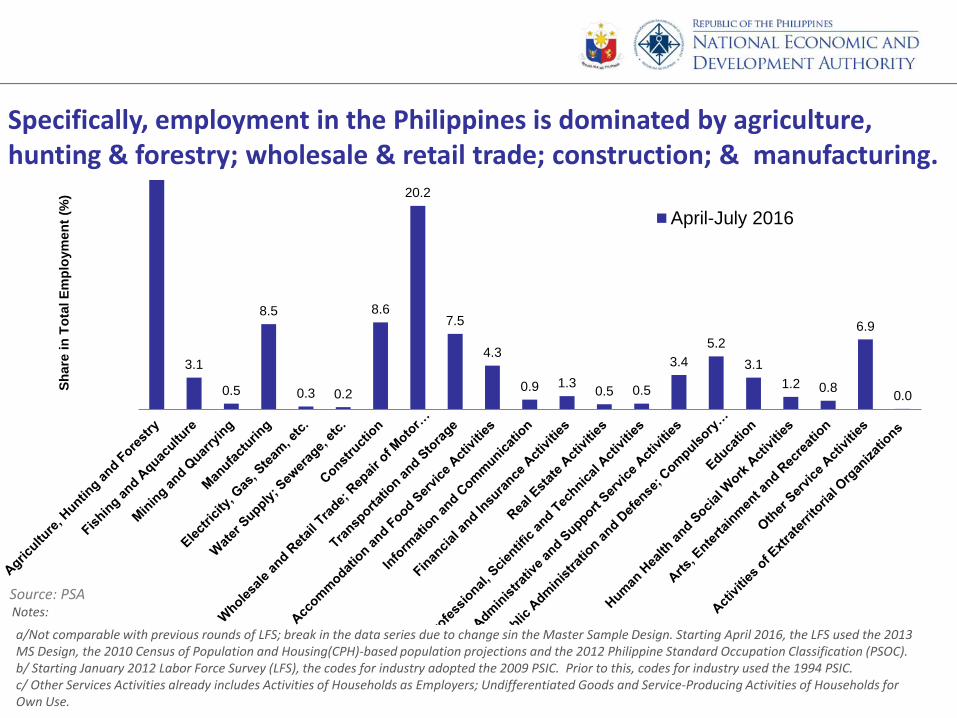

22.8

3.1

0.5

8.5

0.3 0.2

8.6

20.2

7.5

4.3

0.9 1.30.5 0.5

3.4

5.2

3.1

1.2 0.8

6.9

0.0

Sh

are

in

To

tal E

mp

loym

en

t (%

)

April-July 2016

Specifically, employment in the Philippines is dominated by agriculture, hunting & forestry; wholesale & retail trade; construction; & manufacturing.

Notes:

a/Not comparable with previous rounds of LFS; break in the data series due to change sin the Master Sample Design. Starting April 2016, the LFS used the 2013 MS Design, the 2010 Census of Population and Housing(CPH)-based population projections and the 2012 Philippine Standard Occupation Classification (PSOC). b/ Starting January 2012 Labor Force Survey (LFS), the codes for industry adopted the 2009 PSIC. Prior to this, codes for industry used the 1994 PSIC.c/ Other Services Activities already includes Activities of Households as Employers; Undifferentiated Goods and Service-Producing Activities of Households for Own Use.

Source: PSA

Beginning April 2016, the PSA adopted the 2013 Master Sample for household surveys in the sampling design of the LFS. Thus, April 2016 LFS figures are not comparable with previous data.Source: PSA

Target unemployment rateTarget underemployment rate

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0Unemployment rateUnderemployment rate

PH NCR CAR I II III IV-A IV-B V VI VII VIII IX X XI XII Caraga ARMM NIR

Unemployment rate 5.4 6.5 5.0 5.4 3.5 6.2 7.6 4.3 4.0 5.3 5.1 4.5 4.8 6.1 4.3 3.5 4.5 2.9 4.0

Underemployment rate 17.3 9.3 24.6 17.2 8.9 13.9 10.7 26.6 25.4 17.6 14.3 31.0 20.3 32.2 15.4 29.0 26.2 7.7 18.6

Unemployment and Underemployment Rates, by Region: July 2016

Gains in unemployment were broad-based geographically as most ofthe regions had unemployment rates lower than the national unemployment rate

Poverty reduction has improved but needs to accelerate further

14.2

13.3 13.4

12.1

28.8 28.627.9

26.3

25.0

26.0

27.0

28.0

29.0

10.0

11.0

12.0

13.0

14.0

15.0

2006S1 2009S1 2012S1 2015S1

Pove

rty

(% o

f p

op

ula

tio

n)

Sub

sist

ence

(%

of

po

pu

lati

on

)

Subsistence (% of population) Poverty (% of population)

Poverty Statistics, First Semester (%)

Poverty Statistics, Full Year (%)

12.0

10.9

10.4

26.526.3

25.2

24.5

25.0

25.5

26.0

26.5

27.0

9.5

10.0

10.5

11.0

11.5

12.0

12.5

2006 2009 2012

Pove

rty

(% o

f p

op

ula

tio

n)

Sub

sist

ence

(%

of

po

pu

lati

on

)

Subsistence (% of population) Poverty (% of population)Source: PSA

Growth Outlook and Risks

The Philippines is expected to remain one of the fastest growing economies in Asia

GDP growth of selected Asian economies (%)

Source: IMF-WEO April 2016, July 2016 Update, Article IV consultations for forecast values, and various government websites for actual values

7.3

5.9

6.96.7

4.85.0

2.8

2.0

7.5

6.96.7

5.55.1

4.1

3.4

2.1

7.4

6.46.6

6.1

4.9

4.4

3.0

1.8

7.4

6.7

6.2 6.2

5.3

4.8

3.2

2.2

India Philippines China Vietnam Indonesia Malaysia Thailand Singapore

2015 1H 2016 2016F 2017F

The vibrant view on the Philippine economy is also shared by the private sector

Source: Various sources, as of 17 August 2016

Consensus Forecast (in %)

Institution 2016 2017 2018ADB 6.0 6.1 -

Barclays 6.2 5.8 -

Citi 6.3 6.5 -

Fitch rating 5.9 6.0 -

Goldman Sachs 6.4 6.1 -

HSBC 6.3 6.3 -

IMF 6.0 6.2 6.3

Metrobank Research 6.3 - -

Moody’s 6.0 6.0 -

Nomura 6.3 6.0 -

Standard and Poor’s 6.1 6.3 6.2

Standard Chartered Bank 6.4 6.0 5.8

UNESCAP 6.4 - -

WB 6.4 6.2 6.2

Median 6.3 6.1 6.2

Mean 6.3 6.1 6.1

Indicators2014

Actual2015

Actual

Projections1/

2016 2017 2018 2019 2020 2021 2022

Real GDP Growth Rate 6.2 5.9 6.0-7.0 6.5-7.5 7.0-8.0 7.0-8.0 7.0-8.0 7.0-8.0 7.0-8.0

Outlook and targets for 2016-2022

1/ Assumptions adopted by the Development Budget Coordination Committee (DBCC) on July 2016

2,1092,257

2,482

2,990

3,327

2,231

2,6462,960

3,5173,907

122

389 478 527 581

15.8 15.515.6

17.0 17.216.8

18.2 18.6

20.020.2

0.9

2.7 3.0 3.0 3.0

0

5

10

15

20

25

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2015Actual

2016Outlook

2017Proposed

2018Proposed

2019Proposed

Revenue Disbursement Deficit Revenue-to-GDP Disbursement-to-GDP Deficit-to-GDP

Medium-term fiscal outlook 2015 - 2019

Source: BESF 2017

Expected Drivers of Growth

Demand side

Household consumption: remittance inflows, better employment prospects, strong

consumer confidence, low inflation, low interest rates

Government spending: expansion of human development and social protection

programs (i.e. CCT, K-12, health, etc)

Investment: public construction, including infrastructure and reconstruction; private

construction

Exports of services: good prospects for Business Process Management (BPM) and

tourism

Supply side

Lower petroleum prices

Construction and infrastructure development

Manufacturing resurgence

Real estate, renting, and business activities in response to demand from the BPM

sector

Tourism-related services

Wholesale and retail trade

Fragile growth in Japan and European Union

Slowdown in large emerging economies, particularly China

Asynchronous monetary policies in major developed economies

Uncertainties over “Brexit”

Geopolitical tensions in the Middle East, extended period of low

oil prices

Maritime dispute in the West Philippine Sea

Risks to Growth

External

Domestic

Logistics bottlenecks

Delays in government infrastructure and reconstruction projects

Weather shocks, potential La Nina

Closure of mines

We remain vigilant and well- positioned against the downside risks to

growth

Opportunities

Closer economic integration in the ASEAN region which would open up new

sources of capital and markets

Peaceful and smooth transfer of power

Commitment of new Administration to continue current policies and

programs, sustain reform momentum

Resumption of peace talks with NDF, MILF, MNLF

Challenges

• High growth relatively recent

phenomenon

• Growth has not been broadly shared

across socioeconomic classes and

regions

• Agriculture, Fishery and Forestry grew

by only 1.4% annually in 2010-2015; -

3.3% in S1 2016.

• Food price, in particular rice, rose;

poverty line increased by almost 30%

during the period 2009-2015.

• High pop’n growth, resulting in 10M+

more Filipinos in 6 years.

The nagging PUZZLE: fast GDP growth but slow reduction in poverty incidence. Why?

Source: World Bank’s World Development Indicators

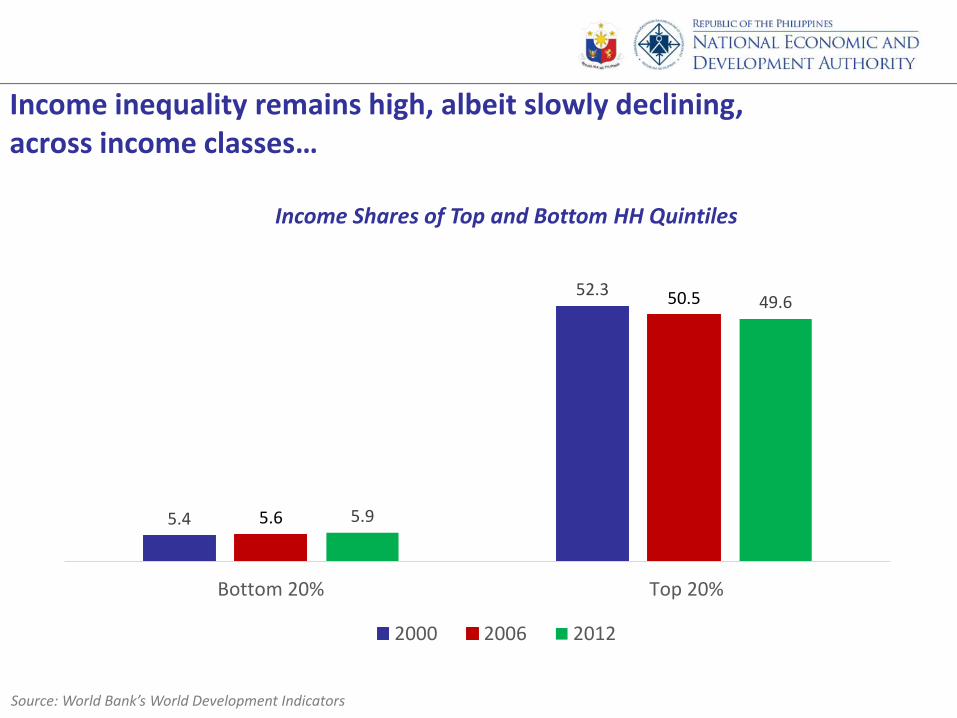

Income inequality remains high, albeit slowly declining, across income classes…

5.4

52.3

5.6

50.5

5.9

49.6

Bottom 20% Top 20%

Income Shares of Top and Bottom HH Quintiles

2000 2006 2012

0

50,000

100,000

150,000

200,000

250,000

in P

hP

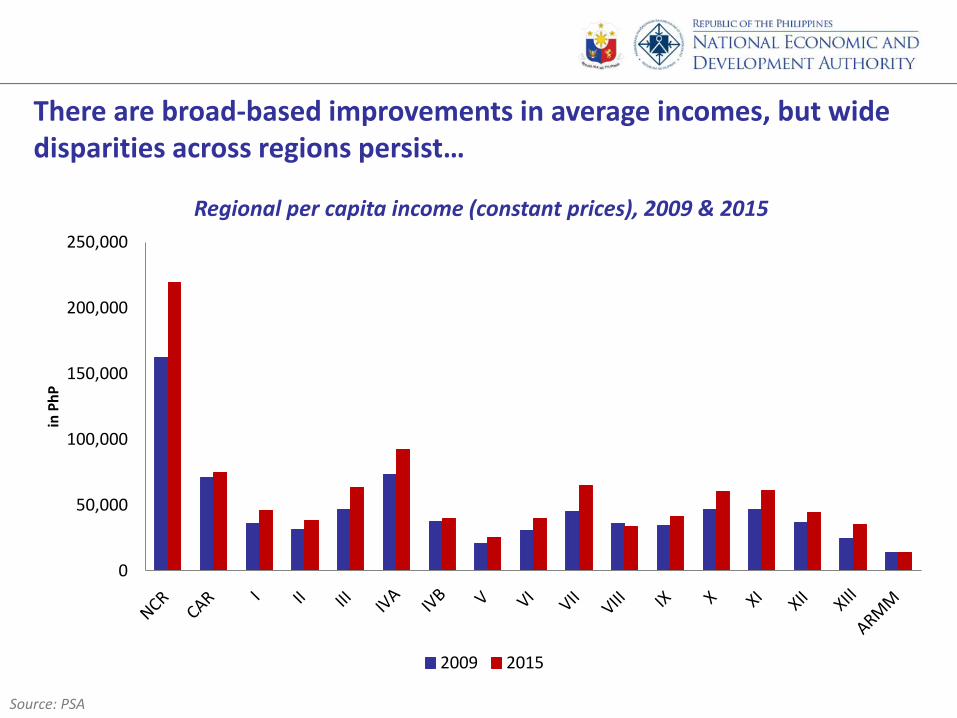

Regional per capita income (constant prices), 2009 & 2015

2009 2015

There are broad-based improvements in average incomes, but wide disparities across regions persist…

Source: PSA

0 10 20 30 40 50 60

NCR

CAR

Region I

Region II

Region III

Region IV-A

Region IV-B

Region V

Region VI

Region VII

Region VIII

Region IX

Region X

Region XI

Region XII

Caraga

ARMM

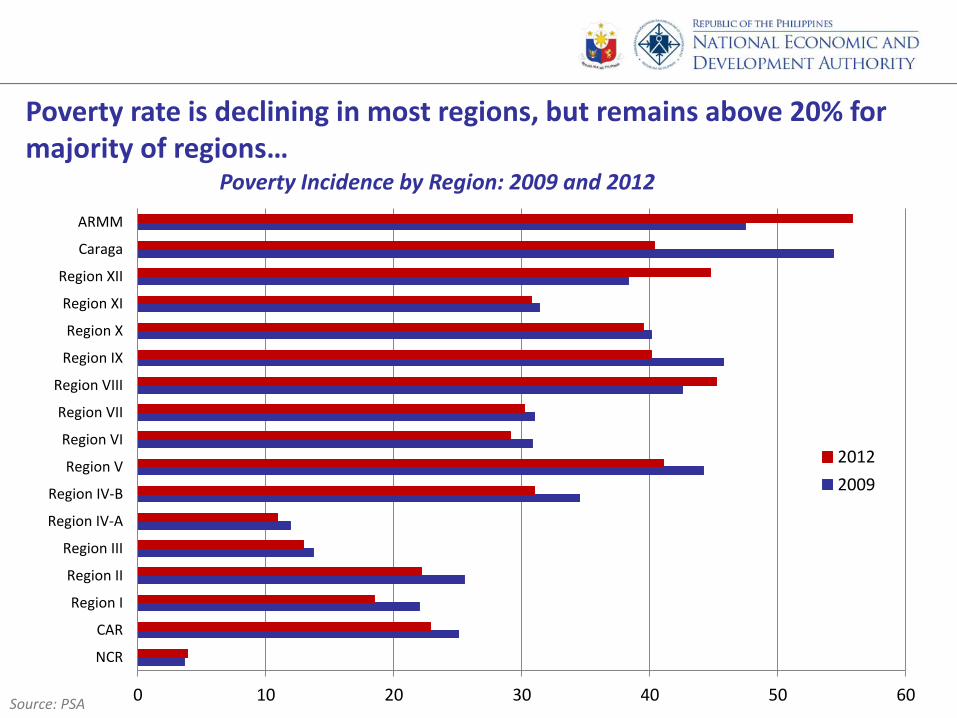

Poverty Incidence by Region: 2009 and 2012

2012

2009

Poverty rate is declining in most regions, but remains above 20% for majority of regions…

Source: PSA

We need to sustain the gains to catch up with our ASEAN neighbors in terms of poverty reduction

Source: World Development Indicators; government statistical agencies

Notes: No poverty data available for the Philippines on 2013 and 2014

25.2

12.012.6

1.7

Philippines Indonesia Thailand Malaysia

Poverty headcount ratio at national poverty lines, 2012 (% of population)

Philippines

Indonesia

Thailand

Malaysia

Challenge Agenda

Adverse investment climate Peace and order; massive infrastructure upgrade; cut red tape; ease constitutional restrictions on FDI ...

Uneven growth Regional and rural development; pro-poor economic growth ...

Contraction in Agriculture and Fishery sector

Agricultural development; land administration and asset reform; technology and innovation; moving up the value chain and agri-business ...

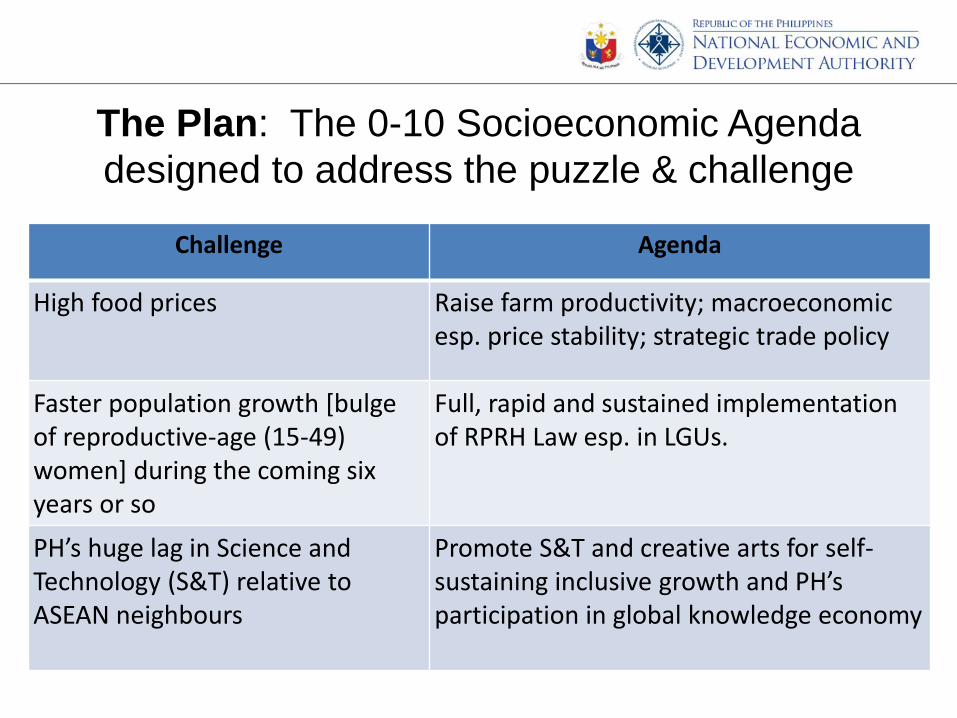

The Plan: The 0-10 Socioeconomic Agenda

designed to address the puzzle & challengeFor instance….

Challenge Agenda

High food prices Raise farm productivity; macroeconomic esp. price stability; strategic trade policy

Faster population growth [bulge of reproductive-age (15-49) women] during the coming six years or so

Full, rapid and sustained implementation of RPRH Law esp. in LGUs.

PH’s huge lag in Science and Technology (S&T) relative to ASEAN neighbours

Promote S&T and creative arts for self-sustaining inclusive growth and PH’s participation in global knowledge economy

The Plan: The 0-10 Socioeconomic Agenda

designed to address the puzzle & challenge

The Philippine’s Socio-economic

Performance, Outlook, Challenges, and Vision

National Economic and Development Authority

ILO Trade on Employment Workshop6-7 October 2016