The Sourcing Issues From Around the

Globe Panel

November 2010

“RMG is labor intensive industry”China

The main driver for this industry.

Surpassed Japan as the world’s second-largest economy last quarter.

Nominal gross domestic product for the second quarter totaled $1.337 trillion.

Economy grew steadily in recent years to reach 8.7% in 2009 and 10.3% in Q2 2010.

Exports dropped by 20% in year 2009.

Local Investments & Private consumption are the main two drivers of the GDP that

were mainly affected by the recession in 2009.

•

•

•

•

•

•

•

•

•

•

•

Apparel consumption decreased since Jan 08 and started rebounding in Jan 10 in terms of

Quantity & Quality.

The biggest importer for men’s woven shirt in 09 counting for 633 million USD.

The labor cost tripled in the last 10 years.

Acceleration in urbanization and income distribution reform would shift earnings from

corporate to employees leading to further labor cost growth and stronger domestic

consumption.

Active working population (15-54) which grew by 7 million per year in the past decade

would decline by 1 million a year.

The drop in China exports is bound

to be shifted to areas

in the same region.

(ex: India, Bangladesh, Indonesia, Pakistan, Vietnam, Cambodia)

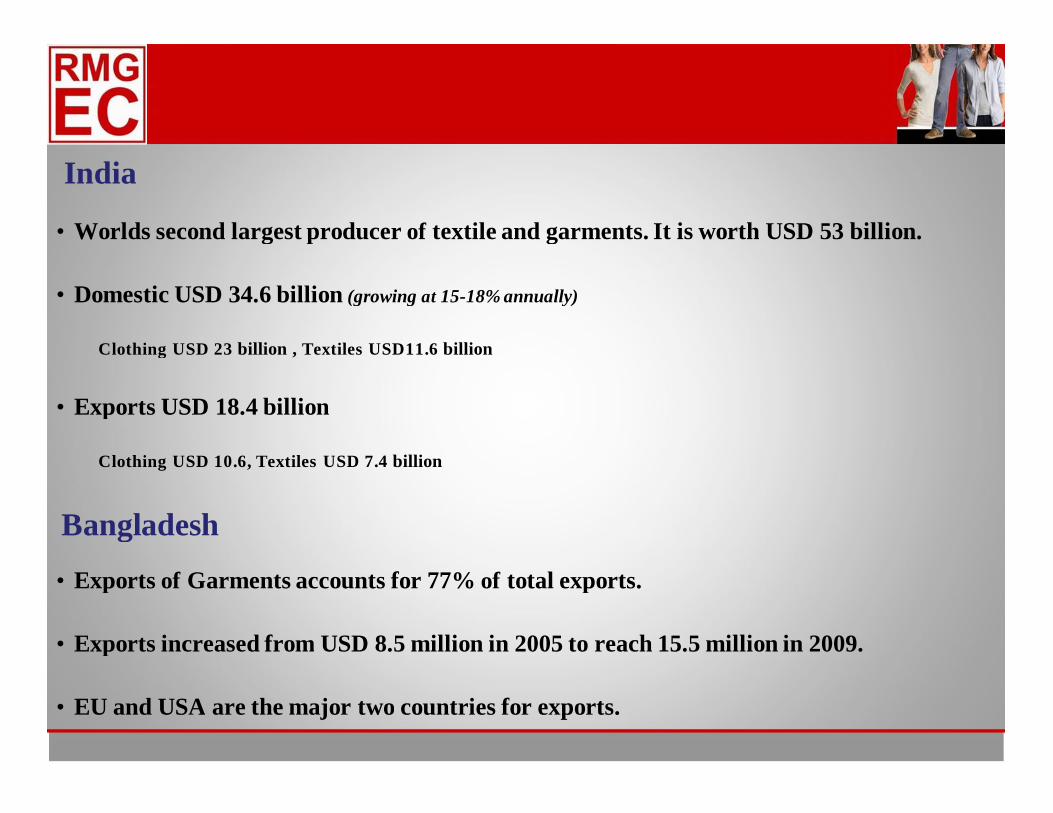

India

Worlds second largest producer of textile and garments. It is worth USD 53 billion.

Domestic USD 34.6 billion

Clothing USD 23 billion , Textiles USD11.6 billion

Exports USD 18.4 billion

Clothing USD 10.6, Textiles USD 7.4 billion

Bangladesh

Exports of Garments accounts for 77% of total exports.

Exports increased from USD 8.5 million in 2005 to reach 15.5 million in 2009.

EU and USA are the major two countries for exports.

•

•

•

•

•

•

(growing at 15-18% annually)

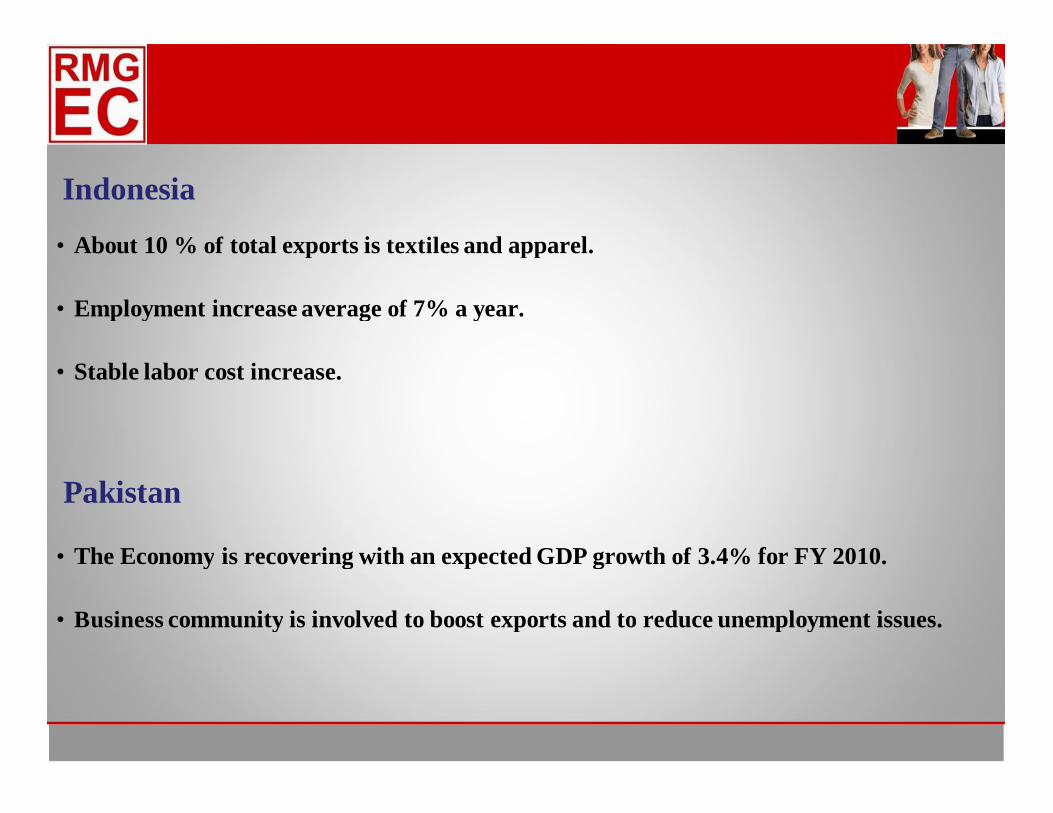

Indonesia

About 10 % of total exports is textiles and apparel.

Employment increase average of 7% a year.

Stable labor cost increase.

The Economy is recovering with an expected GDP growth of 3.4% for FY 2010.

Business community is involved to boost exports and to reduce unemployment issues.

Pakistan

•

•

•

•

•

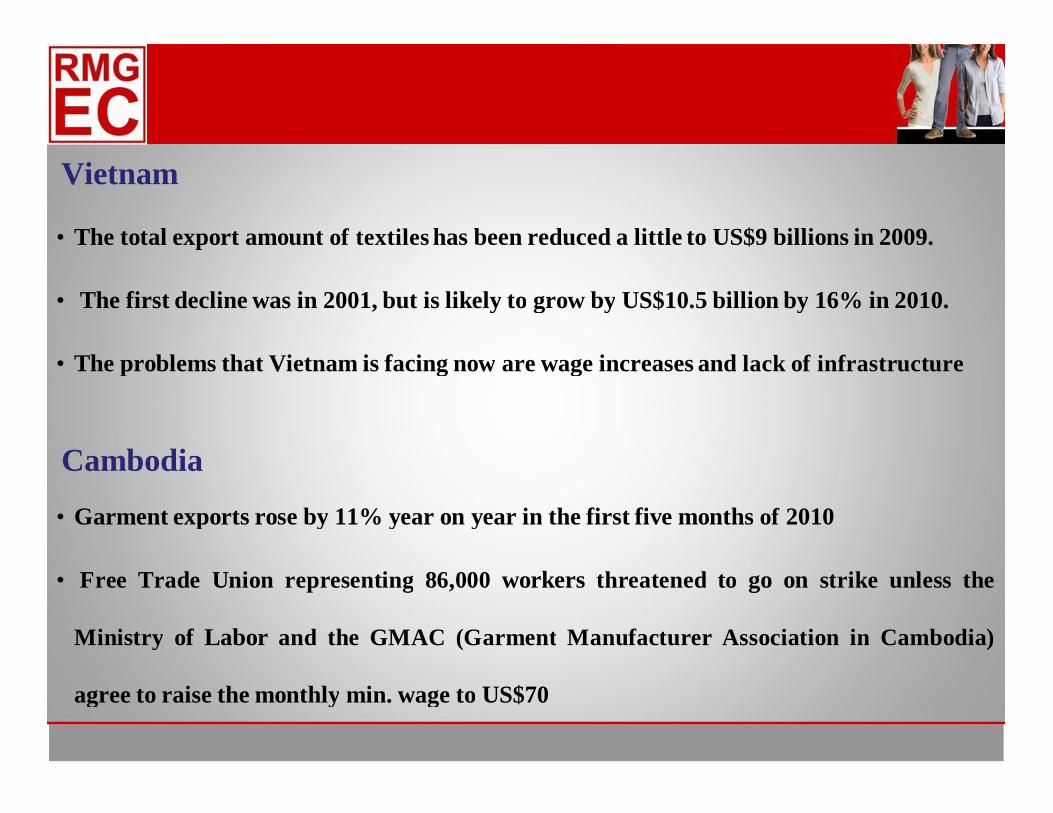

Vietnam

The total export amount of textiles has been reduced a little to US$9 billions in 2009.

The first decline was in 2001, but is likely to grow by US$10.5 billion by 16% in 2010.

The problems that Vietnam is facing now are wage increases and lack of infrastructure

Cambodia

Garment exports rose by 11% year on year in the first five months of 2010

Free Trade Union representing 86,000 workers threatened to go on strike unless the

Ministry of Labor and the GMAC (Garment Manufacturer Association in Cambodia)

agree to raise the monthly min. wage to US$70

•

•

•

•

•

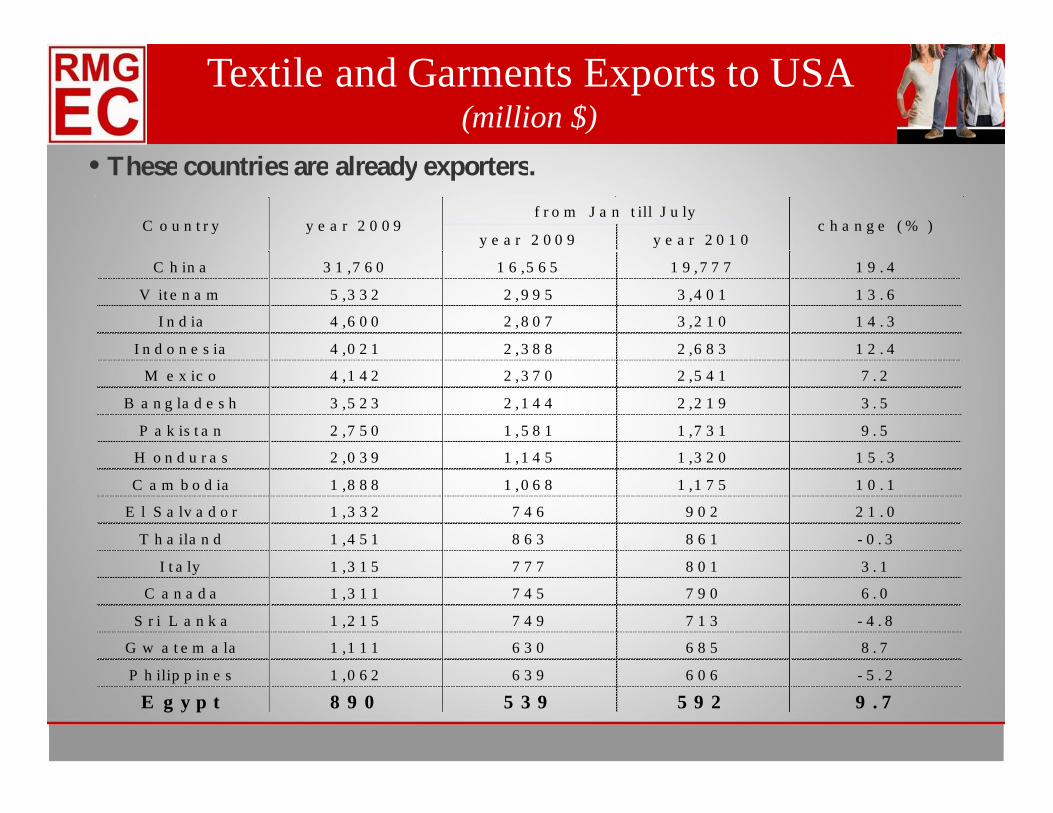

• These countries are already exporters.

y e a r 2 0 0 9 y e a r 2 0 1 0

C h in a 3 1 ,7 6 0 1 6 ,5 6 5 1 9 ,7 7 7 1 9 . 4

V it e n a m 5 ,3 3 2 2 ,9 9 5 3 ,4 0 1 1 3 . 6

I n d ia 4 ,6 0 0 2 ,8 0 7 3 ,2 1 0 1 4 . 3

I n d o n e s ia 4 ,0 2 1 2 ,3 8 8 2 ,6 8 3 1 2 . 4

M e x ic o 4 ,1 4 2 2 ,3 7 0 2 ,5 4 1 7 . 2

B a n g la d e s h 3 ,5 2 3 2 ,1 4 4 2 ,2 1 9 3 . 5

P a k is t a n 2 ,7 5 0 1 ,5 8 1 1 ,7 3 1 9 . 5

H o n d u r a s 2 ,0 3 9 1 ,1 4 5 1 ,3 2 0 1 5 . 3

C a m b o d ia 1 ,8 8 8 1 ,0 6 8 1 ,1 7 5 1 0 . 1

E l S a lv a d o r 1 ,3 3 2 7 4 6 9 0 2 2 1 . 0

T h a ila n d 1 ,4 5 1 8 6 3 8 6 1 - 0 . 3

I t a ly 1 ,3 1 5 7 7 7 8 0 1 3 . 1

C a n a d a 1 ,3 1 1 7 4 5 7 9 0 6 . 0

S r i L a n k a 1 ,2 1 5 7 4 9 7 1 3 - 4 . 8

G w a t e m a la 1 ,1 1 1 6 3 0 6 8 5 8 . 7

P h ilip p in e s 1 ,0 6 2 6 3 9 6 0 6 - 5 . 2

y e a r 2 0 0 9f r o m J a n t ill J u ly

c h a n g e ( % )C o u n t r y

Textile and Garments Exports to USA

E g y p t 8 9 0 5 3 9 5 9 2 9 . 7

(million $)

The potential growth will have to be in a place

where labor force is available

AFRICA …. WHERE?

Egypt

Why Egypt?

Growth & Stability

Access & Proximity to Markets

Diversified Economy

Large Consumer Markets

Infrastructure

Tax Structure

Reformist Investment Climate

Political Stability

Personal Security

Macroeconomic Indicators:Gross Domestic Product (PPP) (6,000 $/capita)Annual Real Growth Rate (4.7%)Total Exports (24.26 billion $)Total Imports (47.59 billion $)GINI index = 34.4Composition of Egyptian ExportsForeign Direct Investment – FDI (Inwards Stocks –Inflows)Labor Force (Age 20 – 60 of Population) (25.4 million)

Egypt at a Glance...

§

§

§

§

§

§

§

§

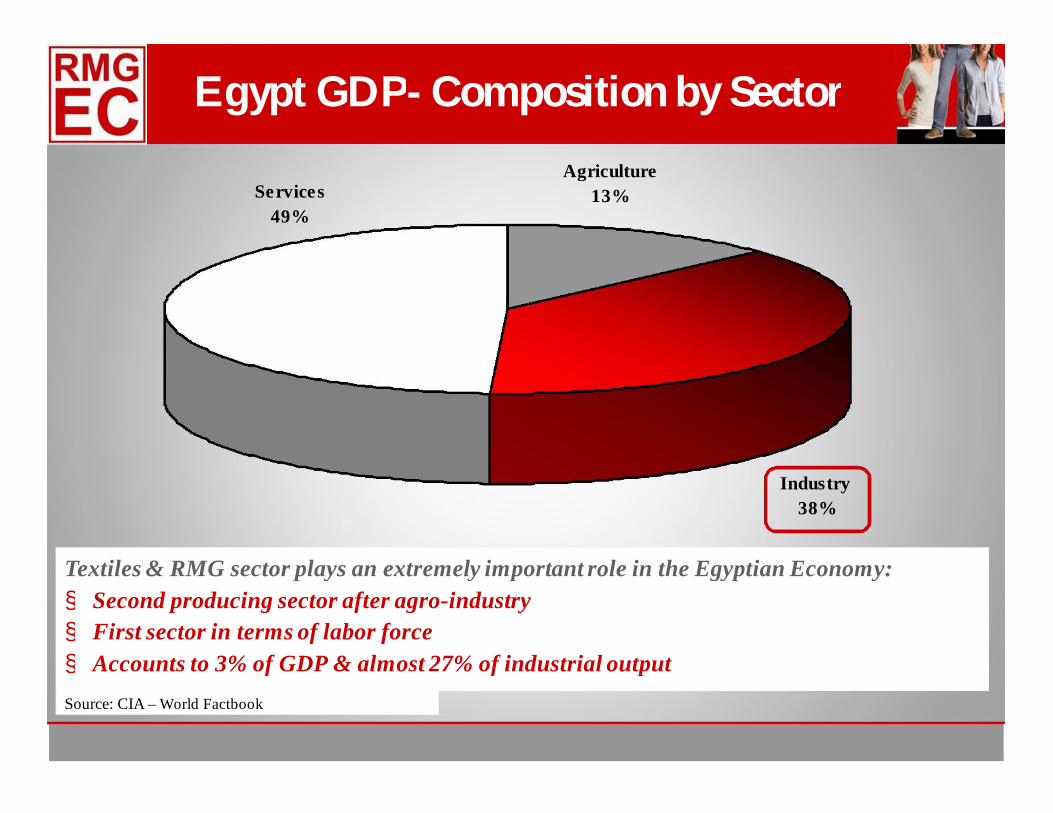

Egypt GDP- Composition by Sector

Source: CIA – World Factbook

Services49%

Industry 38%

Agriculture13%

Textiles & RMG sector plays an extremely important role in the Egyptian Economy: Second producing sector after agro-industryFirst sector in terms of labor forceAccounts to 3% of GDP & almost 27% of industrial output

§§§

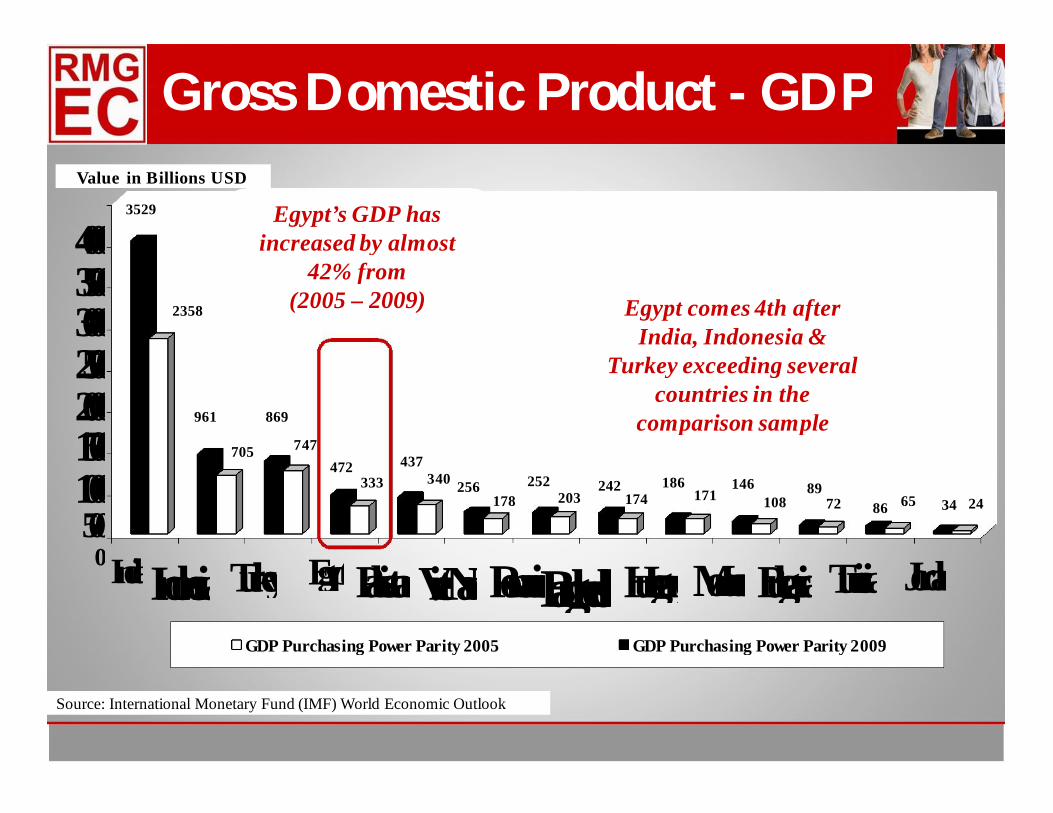

Gross Domestic Product - GDP

2358

3529

705

961

747

869

333472

340437

178256

203252

174242 171

186108

14672

896586 2434

05001000150020002500300035004000

IndiaIndonesiaTurkey EgyptPakistanViet NamRomaniaBangladeshHungaryMoroccoBulgariaTunisia JordanGDP Purchasing Power Parity 2005 GDP Purchasing Power Parity 2009

Value in Billions USD

Source: International Monetary Fund (IMF) World Economic Outlook

Egypt’s GDP has increased by almost

42% from (2005 – 2009) Egypt comes 4th after

India, Indonesia & Turkey exceeding several

countries in the comparison sample

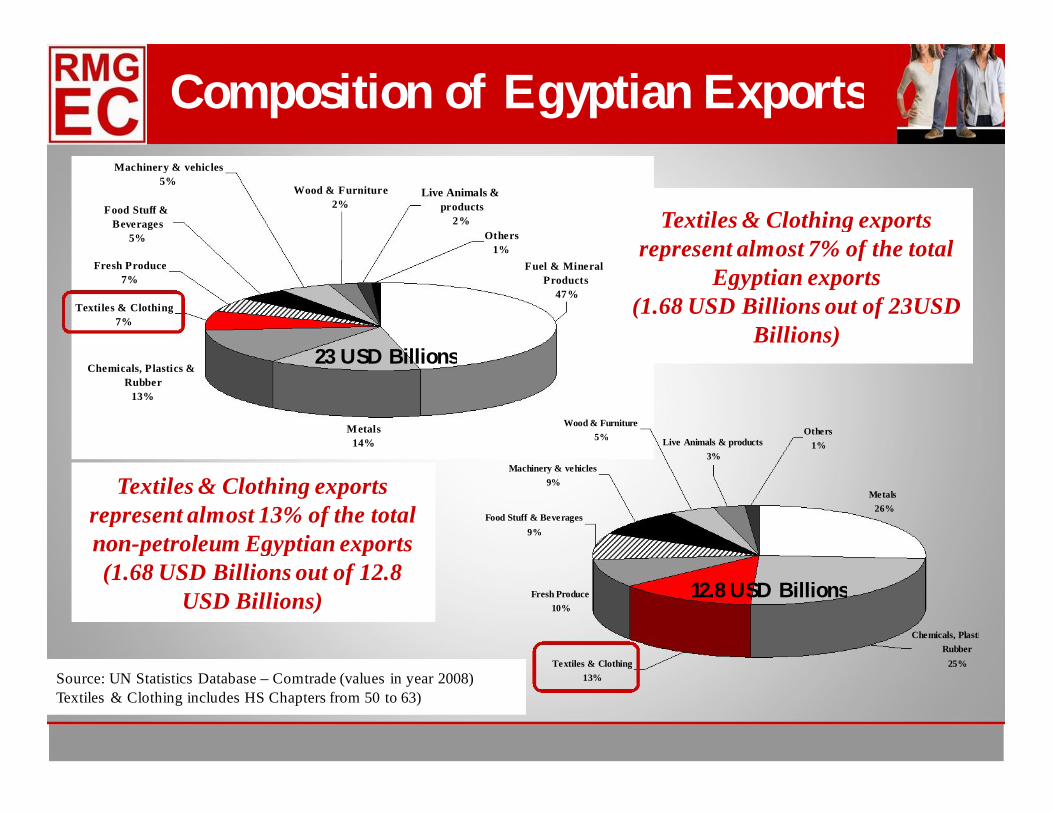

Chemicals, Plastics & Rubber

13%

Metals14%

Textiles & Clothing7%

Fresh Produce7%

Fuel & Mineral Products

47%

Others1%

Live Animals & products

2%

Wood & Furniture2%Food Stuff &

Beverages5%

Machinery & vehicles5%

Wood & Furniture5%

Machinery & vehicles9%

Live Animals & products3%

Others1%

Metals 26%

Food Stuff & Beverages9%

Fresh Produce10%

Chemicals, Plastics & Rubber

25%Textiles & Clothing13%

Textiles & Clothing exports represent almost 7% of the total

Egyptian exports (1.68 USD Billions out of 23USD

Billions)

Textiles & Clothing exports represent almost 13% of the total non-petroleum Egyptian exports (1.68 USD Billions out of 12.8

USD Billions)

23 USD Billions

12.8 USD Billions

Composition of Egyptian Exports

Source: UN Statistics Database – Comtrade (values in year 2008)Textiles & Clothing includes HS Chapters from 50 to 63)

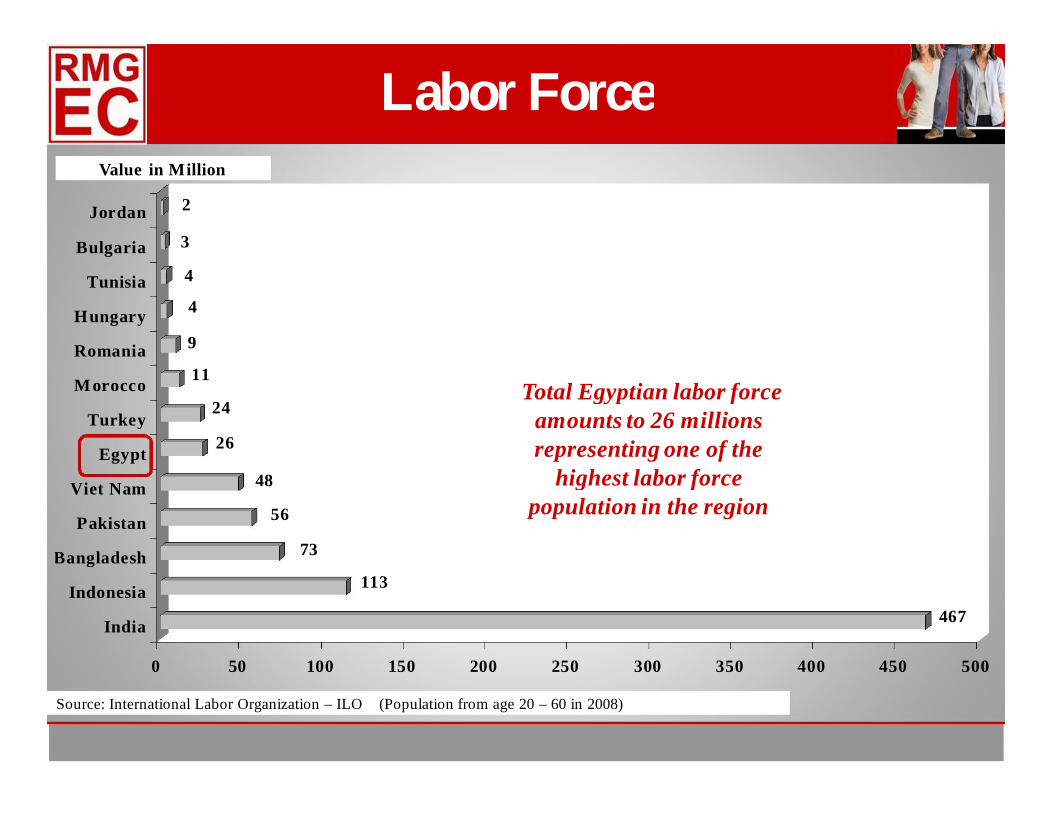

467

113

73

56

48

26

24

11

9

4

4

3

2

0 50 100 150 200 250 300 350 400 450 500

India

Indonesia

Bangladesh

Pakistan

Viet Nam

Egypt

Turkey

M orocco

Romania

Hungary

Tunisia

Bulgaria

Jordan

Value in Million

Labor Force

Source: International Labor Organization – ILO (Population from age 20 – 60 in 2008)

Total Egyptian labor force amounts to 26 millions representing one of the

highest labor force population in the region

Current & Potential Trade Partners

US + Israel (QIZ) EU 27

EFTA

COMESA

PAFTATurkey

Arab BilateralsLebanon – Syria –Iraq – Tunisia –Morocco - Libya

Agadir

MERCOSUR

Russian Federation

Syria FTA Egypt – Syria December 1991

PAFTA FTAAlgeria – Bahrain – Egypt – Iraq – Jordan – Kuwait – Lebanon – Libya –Morocco – Oman – Palestine – Qatar – Saudi Arabia – Sudan – Syria –

Tunisia – UAE – Yemen January 1998

Tunisia FTA Egypt – Tunisia March 1999

Lebanon FTA Egypt – Lebanon March 1999

Morocco FTA Egypt – Morocco April 1999

Jordan FTA Egypt – Jordan December 1999

COMESA FTABurundi – Comoros – Congo – Djibouti – Egypt – Eritrea – Ethiopia – Kenya – Libya – Madagascar – Malawi – Mauritius – Rwanda – Seychelles – Sudan

– Swaziland – Uganda – Zambia - ZimbabweOctober 2000

Iraq FTA Egypt – Iraq July 2001

EU Association Agreement

(EU 27)

FTA

Austria – Belgium – Bulgaria – Cyprus – Czech Republic – Denmark –Estonia – Finland – France – Germany – Greece, Hungary – Ireland – Italy –Latvia – Lithuania – Luxemburg – Malta – Netherlands – Poland – Portugal

– Romania – Slovakia – Slovenia – Spain – Sweden - UK

June 2004

QIZ Protocol Egypt – Israel – United States February 2005

Turkey FTA Egypt – Turkey March 2007

Agadir FTA Egypt – Morocco – Tunisia – Jordan March 2007

Libya FTA Egypt – Libya April 2007

EFTA FTA Egypt – Iceland – Liechtenstein – Norway – Switzerland August 2007

Trade Partners by Agreement

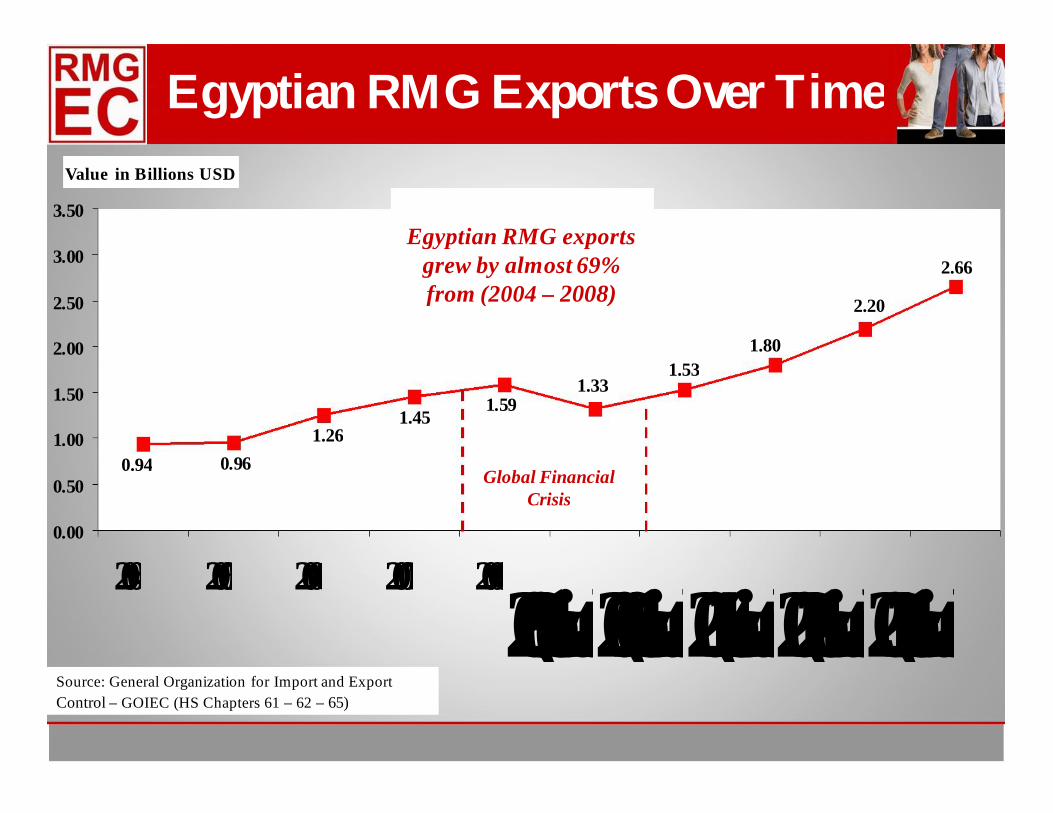

Egyptian RMG Exports Over Time

0.94 0.961.26

1.451.59

1.331.53

1.80

2.20

2.66

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2004 2005 2006 2007 20082009 (estimated)2010 (estimated)2011 (estimated)2012 (estimated)2013 (estimated)

Value in Billions USD

Source: General Organization for Import and Export Control – GOIEC (HS Chapters 61 – 62 – 65)

Global Financial Crisis

Egyptian RMG exports grew by almost 69% from (2004 – 2008)

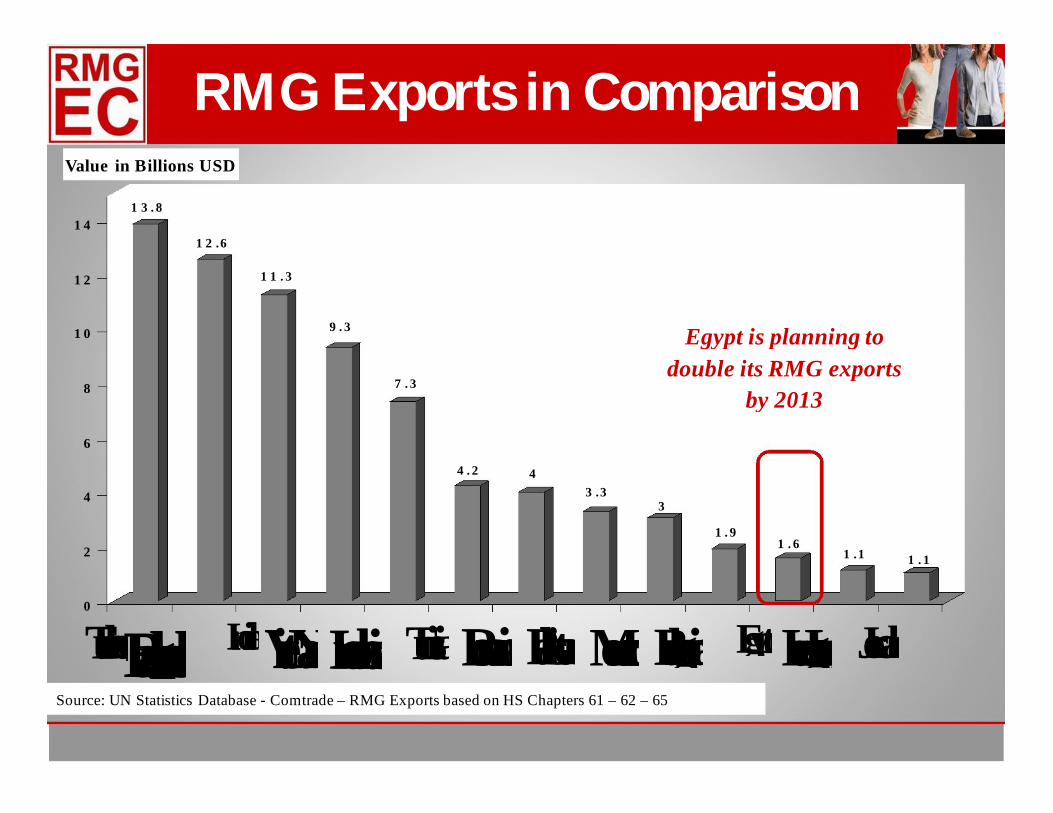

RMG Exports in ComparisonValue in Billions USD

1 3 . 8

1 2 .6

1 1 . 3

9 . 3

7 . 3

4 . 2 43 .3

3

1 . 91 . 6

1 .1 1 . 1

0

2

4

6

8

1 0

1 2

1 4

TurkeyBangladesh IndiaViet NamIndonesiaTunisiaRomaniaPakistanMoroccoBulgaria EgyptHungary JordanSource: UN Statistics Database - Comtrade – RMG Exports based on HS Chapters 61 – 62 – 65

Egypt is planning to double its RMG exports

by 2013

Egyptian RMG Exports by Trade Partners

1.59 USD Billions

Trade Partners Egypt’s Market Share 2005 Egypt’s Market Share 2008

USA 0.62% 1%

EU 27 0.38% 0.49%

EFTA 0.11% 0.15%

Turkey 0.31% 1.47%

PAFTA 0.30% 0.54%

Source: UN Statistics Database - Comtrade – RMG Exports based on HS Chapters 61 – 62 – 65 in year 2008

United States of America

49%

P AFTA1%

O thers4%

Turkey 2%

EF TA 2%

EU 27 43%

Trade Agreement

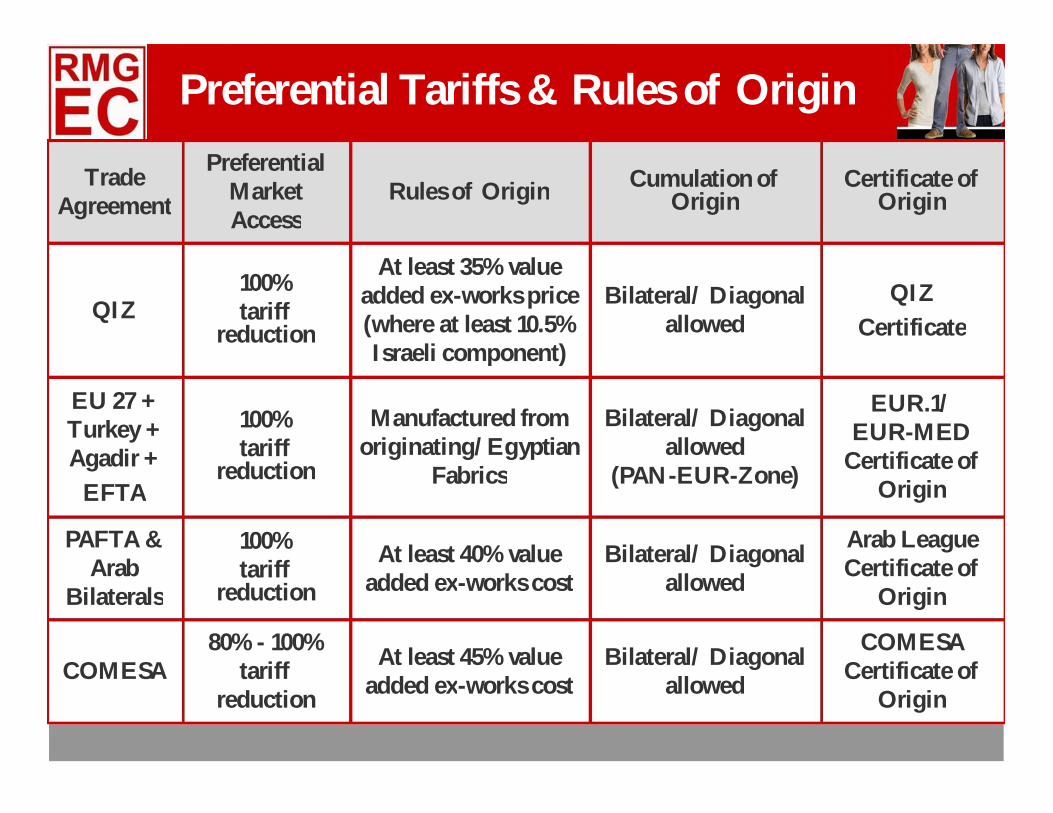

Preferential Market Access

Rules of Origin Cumulation of Origin

Certificate of Origin

QIZ100% tariff

reduction

At least 35% value added ex-works price (where at least 10.5% Israeli component)

Bilateral/ Diagonal allowed

QIZ Certificate

EU 27 + Turkey + Agadir +

EFTA

100% tariff

reduction

Manufactured from originating/Egyptian

Fabrics

Bilateral/ Diagonal allowed

(PAN-EUR-Zone)

EUR.1/ EUR-MED

Certificate of Origin

PAFTA & Arab

Bilaterals

100% tariff

reduction

At least 40% value added ex-works cost

Bilateral/ Diagonal allowed

Arab League Certificate of

Origin

COMESA 80% - 100%

tariff reduction

At least 45% value added ex-works cost

Bilateral/ Diagonal allowed

COMESA Certificate of

Origin

Preferential Tariffs & Rules of Origin

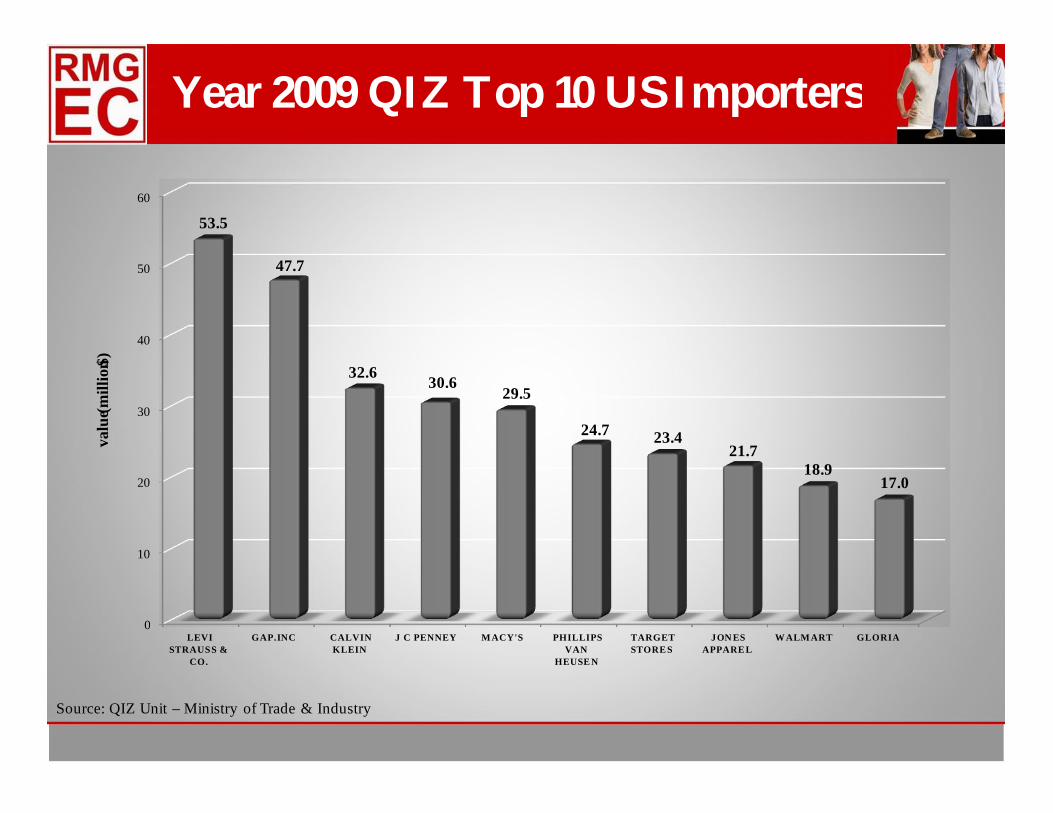

Year 2009 QIZ Top 10 US Importers

Source: QIZ Unit – Ministry of Trade & Industry

0

10

20

30

40

50

60

LEVISTRAUSS &

CO.

GAP.INC CALVINKLEIN

J C PENNEY MACY'S PHILLIPSVAN

HEUSE N

TARGETSTORE S

JON ESAPPARE L

W ALMART GLORIA

53.5

47.7

32.6 30.629.5

24.7 23.421.7

18.917.0

valu

e (mill

ion $

)

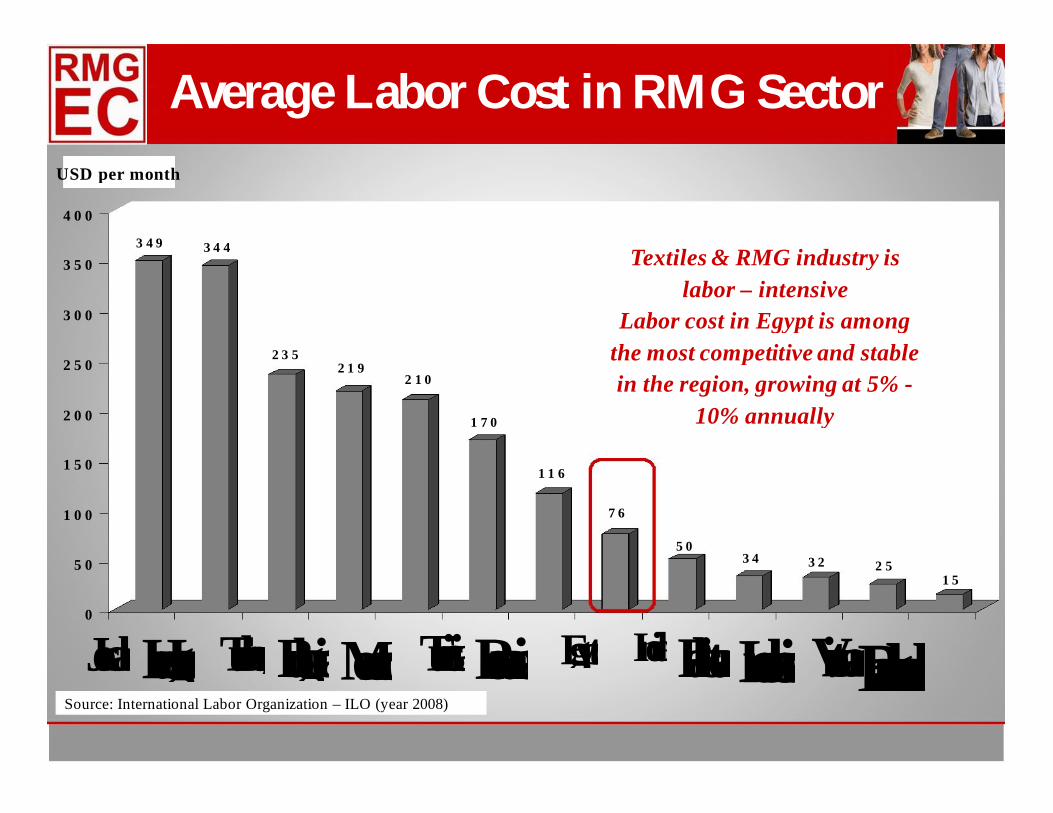

Average Labor Cost in RMG Sector USD per month

3 4 9 3 4 4

2 3 52 1 9

2 1 0

1 7 0

1 1 6

7 6

5 03 4 3 2 2 5

1 5

0

5 0

1 0 0

1 5 0

2 0 0

2 5 0

3 0 0

3 5 0

4 0 0

JordanHungary TurkeyBulgariaMorocco TunisiaRomania Egypt IndiaPakistanIndonesiaVietnamBangladeshSource: International Labor Organization – ILO (year 2008)

Textiles & RMG industry is labor – intensive

Labor cost in Egypt is among the most competitive and stable in the region, growing at 5% -

10% annually

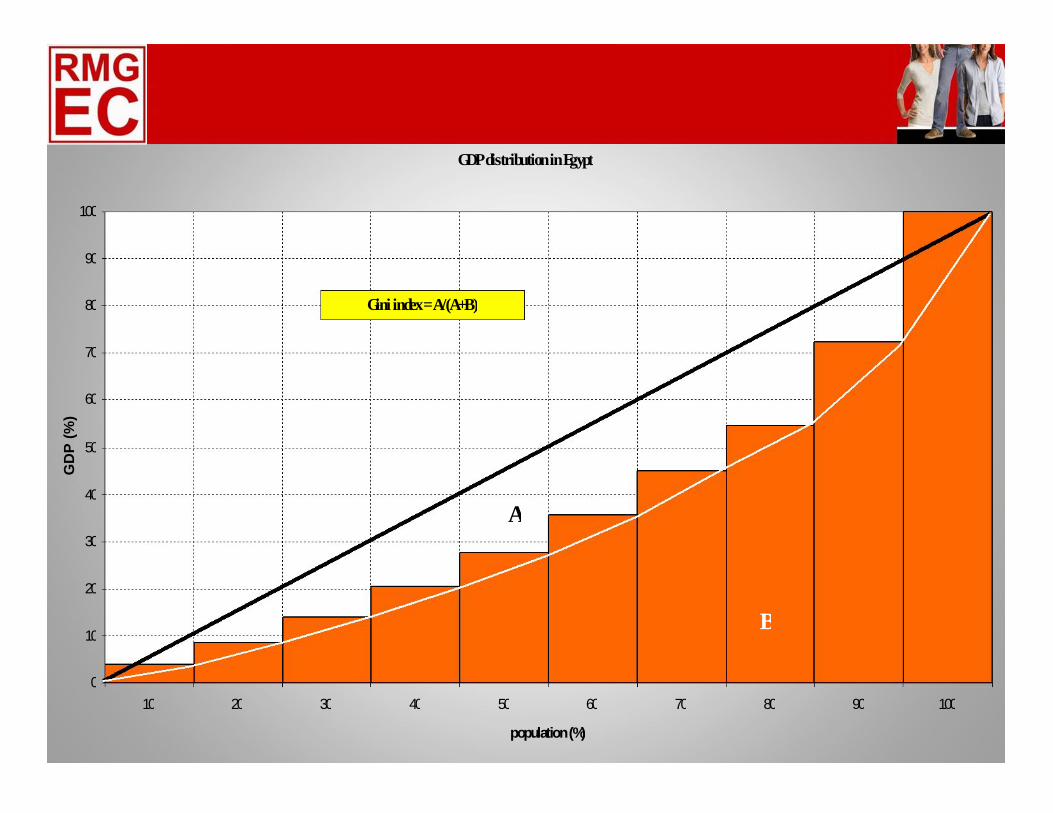

GDP distribution in Egypt

A

B

Gini index = A/(A+B)

0

10

20

30

40

50

60

70

80

90

100

10 20 30 40 50 60 70 80 90 100

population (%)

GD

P (%

)

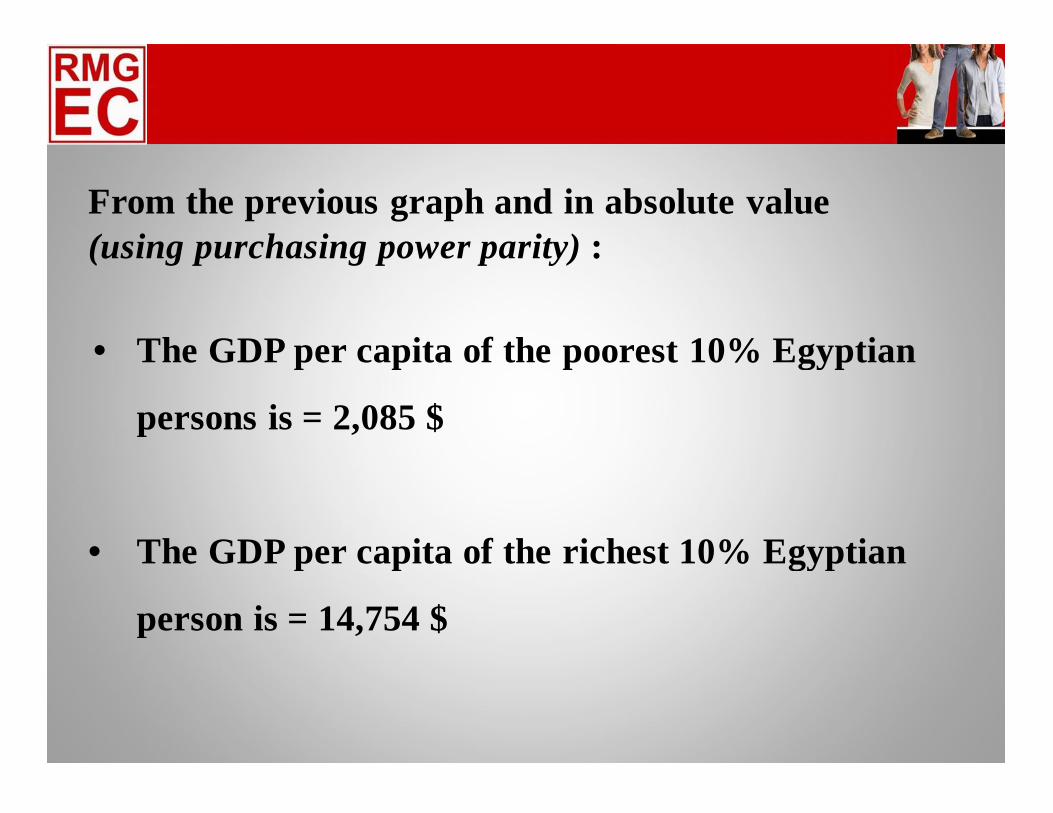

From the previous graph and in absolute value :

The GDP per capita of the poorest 10% Egyptian

persons is = 2,085 $

The GDP per capita of the richest 10% Egyptian

person is = 14,754 $

(using purchasing power parity)

•

•

§

§

Egypt is in line with the list of countries in terms of :

Age structure segmentation ( ready pool for future labor )

Unemployment rate ( ready pool for future labor )

Low wage structure

On the other hand, Egypt is in privileged by the following:

Political Stability vs. Pakistan & Cambodia

Proximity to Europe ( lead time to delivery )

Free Trade Agreement with:

USA

Europe

Turkey

Pan Arab

Conclusion

–

–

–

–

–

–

•

•

•

•

–

–

–

–

–

Supplier Council Presentations

http://web.worldbank.org/WBSITE/EXTERNAL/COUNTRIES/MENAEXT/EGYPTEXTN

/0,,menuPK:287166~pagePK:141132~piPK:141107~theSitePK:256307,00.html

http://www.businessweek.com/news/2010-08-16/china-gdp-surpasses-japan-capping-three-

decade-rise.html

https://www.cia.gov/library/publications/the-world-factbook/

https://www.cia.gov/

Sources

Thank you