The top 10 things every fund manager needs to know about Solvency II

31 January 2016

1

Why should I read this?

Solvency II, implemented on 1 January 2016, requires some rethinking of the way asset managers and (re)insurers interact.

(Re)insurers will increasingly need to demonstrate why they have chosen to use a particular asset manager and show that they

understand and control their asset management arrangements. The regulators are making this clear. Under Solvency II, a

(re)insurer must have in place effective risk management systems for their third party arrangements such as asset management.

Over the past few years, this publication has become popular amongst a number of leading (re)insurers and asset managers.

While it should not be relied on as legal advice, we hope that it is a useful introduction to the complex topic of how Solvency II

affects existing asset management arrangements. However, it does not contain all of the information that asset managers or

(re)insurers require to identify and manage their material risks arising out of the impact of Solvency II on asset management

arrangements. These details can be found in our S2 Services Agreement and accompanying analyses (please see below for

further details).

Warning

As mentioned above, Solvency II and its effect on asset management arrangements is a complex topic, not least because new

Solvency II legislation and regulatory guidance will continue to emerge over the next few years (even though Solvency II is now

already in force). We are aware that a large number of asset managers believe that a “Solvency II” NDA is all that both they and

their client (re)insurer will need to cover the disclosure of data to (re)insurers. This is a dangerous misconception, the

consequences of which could include serious regulatory and risk management issues for both (re)insurers and asset managers.

Recognising the above, and the urgent need for an alternative solution to an NDA, we set up a working group for 6 months

during 2015 to produce the S2 Services Agreement (S2SA). The working group was comprised of a number of leading members

of the insurance and asset management industries (including the Investment Association). We would strongly advise referring to

the advice and provisions contained in the S2SA for a more comprehensive analysis of the issues referred to in this publication.

Please do contact Pollyanna Deane and/or Jennifer Yao if you would like to find out more information about the S2SA template

and/or the Solvency II asset risks training that we provide.

Contents

Top ten things every fund manager needs to know about Solvency II ................................................................. 2-10

Contact details ..................................................................................................................................................................................... 11

Appendix 1: Collated ITS instructions for template S.06.02 list of assets – individual and group undertakings (differences noted) ............................................................................................................. 12-21

Part 1 – information on positions held, Part 2 – information on assets

Appendix 2: Collated ITS instructions for templates S.08.01 & S.08.02 list of open derivatives and derivatives transactions – individual and group undertakings (differences noted) .................................................................................................................................................................... 22-31

Part 1 – information on positions held, Part 2 – information on derivatives

Appendix 3: Table collating the ITS Regulation annexes relating to asset and CIC categories .............. 32-37

Appendix 4: Tripartite Template for Solvency II reporting – version 3 (dated 13 October 2015) ........ 38-48

Appendix 5: UK firms with full/partial internal model PRA approval ........................................................................... 49

2

1. What is Solvency II?

Solvency II is the new set of prudential regulatory requirements for almost all insurers and reinsurers established in the EU. There are only very limited exemptions for (re)insurers which are below a certain size. Note that non-EU subsidiaries of EU headquartered groups are also affected by Solvency II.

Solvency II has replaced Solvency I which, starting from 1973, has provided a basic harmonised framework for insurance business in the EU. Solvency II introduces much more comprehensive and sophisticated rules.

As you can see from the above timeline, Solvency II came into force on 1 January 2016.

Transitional measures provide that (re)insurers will have until 31 December 2017 to comply with the new Solvency Capital Requirements (“SCR”) (see section 5 below). However, EIOPA is requiring early practice reports to be filed in connection with the new Solvency II reporting requirements. In addition, the 2014 EIOPA EU-wide stress test, the results of which were released on 28 November 2014, required (re)insurers to apply the draft Solvency II rules (including those relating to the calculation of the capital requirements) when data was collected by National Supervisory Authorities.

As Solvency II was originally due to be implemented from November 2012, in practice in the UK many (re)insurers were already substantially complying with Solvency II (in the form of an enhanced version of the FCA’s Individual Capital Adequacy Standards (ICAS +)) for some time before the implementation deadline and all (re)insurers at Lloyd's were required to comply with the Solvency II capital requirements ahead of the deadline. In reality, the first returns on a Solvency II basis will generally be due from (re)insurers in May 2016.

Set out below is the timetable* for submitting Solvency II returns for firms with a 31 December year end date:

All firms

First Solvency II returns due Solos – 20 May 2016, Day 1 submission

Groups – 1 July 2016, Day 1 submission

Q1 returns Solos – 26 May 2016

Groups – 7 July 2016

Q2 returns Solos – 25 August 2016

Groups – 6 October 2016

Q3 returns Solos – 25 November 2016

Groups – 6 January 2017

Q4 returns Solos – 25 February 2017

Groups – 8 April 2017

First annual Solvency II reporting Solos – 20 May 2017

Groups – 1 July 2017

* As set out in the PRA’s “Solvency II reporting schedule – 31 December year end” (dated 9 December 2015)

SII Directive (consolidated)

finalised

Implementing Technical Standards,

Guidelines and taxonomy issued

and finalised

Delegated Regulation finalised

Transposition date

Implementation date

May 2014 Summer 2014 to Winter 2015

31 March 2015

1 January 2016

January 2015

3

Different dates will apply to firms with a non-31 December year end date. Such firms should speak with their supervisors to confirm the dates applicable to them.

2. How will Solvency II affect fund managers?

(Re)insurers own around $25 trillion of assets under management worldwide and about 30% of the world's conventional assets under management.

To fund managers, Solvency II’s key features are: (i) it potentially alters what assets in their funds will be attractive to (re)insurers; and (ii) that Solvency II requires asset managers to provide a much greater amount, and more granular, asset data to their (re)insurer clients.

Important topics which are frequently overlooked include how insurers’ governance (and in particular outsourcing) obligations under Solvency II to date necessitate changing the legal terms between the parties; that investments in funds by insurers while often technically “direct investments” are likely to be subject to Solvency II outsourcing requirements; asset managers themselves are regulated entities and need to identify how having Solvency II clients could affect their own regulatory obligations; and the potential risk/liability issues arising out of all third parties’ involvement in the asset management arrangements. These are all topics which our S2SA working group considered and discussed in some depth, the essential points of which have been captured in the S2SA appended analyses and footnotes.

Asset managers have been surprised by (re)insurers relative lack of engagement with them on Solvency II, e.g. there have been very few requests to update investment management agreements so that they comply with at least the express Solvency II outsourcing requirements. However, now that Solvency II is in force, asset managers should be prepared for insurers taking a greater interest in updating their asset management arrangements in a manner which meets their Solvency II obligations. It is therefore important that asset managers should understand how to satisfy both their clients’ regulatory needs as well as their own in the simplest possible manner.

One possible solution is the S2SA (which is supported by the Investment Association). Using the S2SA means you can:

Minimise your liability/regulatory exposures

Have confidence that all asset information (not just the data to be incorporated in Solvency II QRTs) can be provided in a manner which meets the regulatory and other needs of (re)insurers and asset managers

Identify the potential risk areas arising from the impact of Solvency II, including where there is an indirect relationship between an asset manager and the (re)insurer

Confidently address the scope of outsourcing and use of third parties and understand Solvency II outsourcing contractual requirements, while still achieving contractual certainty for all parties

Use NDA’s efficiently and wisely

Minimise the need to review all documentation for “Solvency II compliance” – instead you can use the S2SA.

3. How will Solvency II impact (re)insurers' investment decisions?

Before the implementation of Solvency II, (re)insurers’ investments which were permitted to count towards their regulatory capital were constrained by categories of “admissible assets” and “permitted links” (which would include, for example, units in a UCITS and certain “recognised schemes”).

Under Solvency II, there are no restrictions on asset classes permitted (except for linked life policies) which opens up the possibility for (re)insurers to invest in hedge funds or private equity for the first time. It is likely of course that (re)insurers will continue to maintain internal quantitative limits for each type of asset. The permitted links rules (as amended) will also continue to apply in certain circumstances, namely for linked long-term contracts of insurance where the investment risk is borne by a policyholder/beneficiary who is a natural person.

4

(Re)insurers’ investment decisions under Solvency II will be led by two main concepts. Firstly, the (re)insurer must comply with the “prudent person principle” (see section 4 below). Secondly, if the (re)insurer does not hold the requisite risk capital against the assets it has invested in (see section 6 below), then these assets will not count towards the (re)insurer's regulatory capital.

4. What is the “prudent person principle”?

5. What capital requirements are imposed on (re)insurers under Solvency II?

(Re)insurers may choose to calculate their SCR, either on the basis of:

Standard Formulae; or

(re)insurers can develop their own “Internal Models”, although these will need to be approved by their national financial services regulator.

On 5 December 2015, the PRA published a list of the first 19 (re)insurers to have their internal models approved, noting that a number of (re)insurers were continuing to develop their internal models for later approval. The list is attached at Appendix 5.

The Market Risk Module of the Standard Formulae or the Internal Model will set out the capital required to be held in respect of (re)insurers’ investments (see section 6 below).

Interestingly, if EIOPA deems that “exceptional adverse situations” have occurred affecting (re)insurers representing a significant share of the market or the affected lines of business, firms may be permitted to breach the SCR requirements for a period of up to seven years. “Exceptional adverse situations” occur when there is: (i) a fall in financial markets that is unforeseen, sharp and steep; (ii) a persistent low interest rate environment; or (iii) a high impact catastrophic event. (Further detail can be found in EIOPA’s “Guidelines on the extension of the recovery period in exceptional adverse situations” (EIOPA-BoS-15/108 EN).)

EIOPA also has the power to adopt new Regulatory Technical Standards setting out asset eligibility criteria and quantitative limits in respect of risks not covered by the existing rules, for example this could be used to change the capital requirements of gilts of distressed EEA countries which currently all carry a 0% capital charge (see section 6 below).

Own funds Investment freedom

SCR (Solvency Capital Requirement)

Capital to cover risk of adverse events that may occur in the next 12 months

MCR (Minimum Capital Requirement)

This is the minimum capital amount which needs to be held to avoid mandatory supervisory action

Technical Provisions Provisions for liabilities sufficient to allow run-off or transfer to another firm

£

£

£

A prudent person would invest so that:

The risks of assets are able to be properly identified, measured, monitored, controlled and reported on

Assets are invested to ensure security, quality, liquidity and profitability of the portfolio overall The availability of assets is ensured Assets are invested in the “best interests of policyholders” The portfolio is diversified to avoid risk concentration

5

6. What are the capital requirements for different asset classes under Solvency II?

Pre-Solvency II, (re)insurers needed to hold regulatory capital against their investments on a linear basis, not differentiated by asset class.

Under Solvency II, there are granular capital requirements obliging (re)insurers to hold capital on an “asset by asset” basis as part of the acquisition cost. A handy thumbnail sketch of the capital requirements for different asset classes of direct investment under the Solvency II Standard Formulae are set out below. Note that the capital requirements of indirect exposure are covered in section 7.

Please note that the table below takes into account the 30 September 2015 proposed amendment to the Delegated Regulation, although this is not expected to take effect until April 2016. For clarity, we have italicised those amendments based on the proposed Delegated Regulation.

Asset

Risk capital requirement for Standard Formulae

Example

Equities∗ (listed on regulated markets in EEA countries or OECD countries or traded on multilateral trading facilities headquartered in the EU) and units or shares of : (i) collective investment undertakings which are qualifying European Social Entrepreneurship Funds; (ii) collective investment undertakings which are qualifying European Venture Capital Funds; (iii) closed-ended and unleveraged alternative investment funds which are established or marketed in the EU under the Alternative Investment Fund Managers Directive; and (iv) collective investment undertakings which are authorised as European long-term investment funds pursuant to Regulation (EU) 2015/760 on European long-term investment funds (in each case, other than qualifying infrastructure equities).

39% (+/- 10% counter-cyclical buffer) The acquisition of a listed EEA/OECD equity would require the (re)insurer to hold capital of 39% of the value of the equity The European Insurance and Occupational Pensions Authority (“ElOPA”) may vary this capital charge by +/- 10% depending on economic conditions

Other equities (all private investment, unlisted equities/private equity, equities listed outside EEA or OECD, commodities, alternative investments and any other investments not covered by the other categories of this table, such as equity derivatives and fixed income derivatives)

49% (+/- 10% counter-cyclical buffer) The acquisition of any other equity would require the (re)insurer to hold capital of 49% of the value of the equity ElOPA may vary this capital charge by +/- 10% depending on economic conditions

Qualifying infrastructure equities (equity investments in infrastructure project entities meeting certain criteria, including generating predictable cash flows and the revenues of the project meeting various detailed conditions)

30% (plus 77% of the +/- 10% counter-cyclical buffer)

The acquisition of a qualifying infrastructure equity would require the (re)insurer to hold capital of 30% of the value of the equity and 77% of the counter-cyclical buffer.

The counter-cyclical buffer refers to the fact that EIOPA may vary the capital charge by +/- 10% depending on economic conditions.

Government bonds (includes exposures to the ECB, multilateral development banks and international organisations)

Charge based on credit rating and duration: 0% to 46.5% +

For example, a government bond with an AAA or AA credit rating and a duration of 20+ years would have a capital charge of 0% of the value of the gilt

∗ Note that transitional provisions will apply to “type 1” equities not subject to duration based equity risk which were acquired on or before 1 January 2016. Additional requirements apply to equities held within a collective investment undertaking or other investments packaged as funds where the “look through” approach is not possible.

6

Asset

Risk capital requirement for Standard Formulae

Example

Bonds and loans where the exposure relates to a “qualifying infrastructure investment” that meets certain criteria, including that a credit assessment by a nominated ECAI is available for the exposure and it has been assigned a credit quality step between 0 and 3.

Charge based on credit rating and duration: 0.64% to 20.05%+

For example, a bond where the exposure relates to a qualifying infrastructure investment with a AAA credit rating and a duration of 5 years would have a capital charge of 0.64% of the value of the bond.

Corporate bonds and loans∗∗ Charge based on credit rating and duration: 0.9% to 63.5% + For unrated exposures, charge based on duration: 3% to 35.5% + For qualifying collateralised unrated bonds and loans, an adjustment to the risk capital requirement can be made calculated on the difference between the value of the bond/loan and the value of the collateral

For example, a 5 year AAA rated corporate bond would have a capital charge of 0.9% of the value of the bond

Covered bonds Charge based on credit rating and duration: 0.7% to 4.50% +

For example, a 5 year AAA rated covered bond would have a capital charge of 0.7% of the value of the bond

Credit derivatives (a derivative whose value is derived from the credit risk on an underlying bond, loan or any other financial asset)

The higher of the amount of the loss of own basic funds resulting from:

a 1.3 to 16.2+ percentage points absolute increase; and

a 75% relative decrease

of the credit spread of instruments underlying the credit derivatives (except certain risk mitigation instruments)

The acquisition of a credit derivative would require the (re)insurer to hold risk capital of 75% of the value of the derivative in most circumstances

Tradable securities/financial instruments based on repackaged loans (not resecuritised)∗∗∗

Charge based on credit rating and duration and divided into either ‘Type 1’ or ‘Type 2’ positions depending on, inter alia, the structure and terms of the securitisation, the quality of the underlying assets, the underwriting process and the transparency for investors

2.1% to 100%

For example, a Type A, AAA rated tradable security based on a repackaged loan (but not resecuritised) would attract a capital charge of 2.1% of the value of the security if it fulfilled the criteria for a ‘Type 1’ position, but if the security were an unrated ‘Type 2’ position then the charge would be 100% of the value of the security

Tradable securities/financial instruments based on repackaged loans (resecuritised) ***

Charge based on credit rating and duration: 33% to 100%

For example, a 1 year AAA rated tradable security based on repackaged loans (resecuritised) would attract a 33% capital charge of the value of the security, but if the security were unrated the charge would be 100% of the value of the security

Real estate (being land, buildings and immovable-property rights and property for the use of the (re)insurer)

25% The acquisition of a real estate asset would require a (re)insurer to hold 25% of the value of the real estate as the capital charge

Consistent asset valuation is very important under Solvency II. Valuations under Solvency II are either on a “mark to market” or best estimate basis.

Risk mitigation techniques can be taken into account when estimating the Solvency Capital Requirement, provided that credit risk and other risks arising from the use of such techniques are properly reflected in the SCR.

In making its investment decisions, the (re)insurer should, acting as a “prudent person” (see section 4 above) take into account the risks associated with the investments without relying only on the risk being adequately captured by the capital requirements. As a result (re)insurers have to take more responsibility for the investment decisions they make and will need to put more detailed information gathering and reporting procedures in place to understand the market risks inherent in its investments.

∗∗ Note that this includes commercial real estate loans but excludes retail loans secured by mortgages on residential property which are dealt with under the counterparty risk module rather than the market risk module and which is not covered by this table. ∗∗∗ Note that Solvency II prescribes that originators of such assets must retain a net economic interest of at least 5%. In relation to such assets which were issued before January 2011, this requirement only applies where new underlying exposures were added or substituted after December 2014.

7

7. What information on asset holdings do I need to provide to (re)insurers under Solvency II?

In order for (re)insurers to properly assess the market risk inherent in collective investment funds (UCITS or alternative investment funds - AIFs) or other investments packaged as funds it will be necessary for (re)insurers to examine the “economic substance” of the investments. Wherever possible, this should be achieved by (re)insurers applying a “look through” approach in order to assess the risks applying to the assets underlying the investment vehicle. The capital required to be held against each asset would then be calculated on the underlying asset as set out in section 6 above.

Look through also applies for other indirect exposures to underwriting, counterparty and/or market risk. It looks likely that look through applies to indirect exposures such as equity derivatives or fixed income derivatives. Look through applies to both passively and actively managed funds.

Look through should not be applied to investments in a related undertaking (i.e. a subsidiary).

The draft of the Technical Specifications of December 2012 explicitly stated that look through should also not be applied to investments in listed equity, tradable securities/financial instruments based on repackaged loans. However, this exception does not appear in the Delegated Act or in EIOPA’s “Guidelines on look-through approach” (EIOPA – BoS – 14/171 EN). It would therefore seem to be intended that look through should be applied to these investments to the extent that this is possible.

Where a number of iterations of the look through approach are required (for example, in relation to a fund of funds), the number of iterations should be sufficient to ensure that all material market risk is captured. Some firms have succeeded in achieving complete look through. EIOPA’s Q&A on reporting template S.06.03 (Collective Investment Undertakings) explained that, by default, all collective investment undertakings or investments packaged as funds are subject to look through. However, specific situations might be discussed with a firm’s National Supervisory Authority. The PRA expanded on this in a paper of 18 December 2015, noting that it anticipated that firms may contact supervisors on the scope of look through on a case by case basis. The PRA did, however, expect firms approaching it to first have considered factors including: (i) whether their investments qualify as collective investment undertakings; (ii) materiality under Article 305 of the Delegated Regulation (that is, whether the information’s omission or misstatement could influence the decision making or judgment of the authorities); and (iii) best available data and approximations. Firms who are finding that complete look through is not achievable (with/without the assistance of third party data managers) should aim for as great a degree of look through as possible and to provide explanations as to why a greater degree of look through was not possible. (See also section 8.)

The Commission Implementing Regulation (EU) 2015/2450 states that look through reporting on investment funds will only be required on a quarterly basis for (re)insurers that hold more than 30% of their portfolio in investment funds. For (re)insurers with 30% or less of their portfolio in investment funds, annual reporting will suffice.

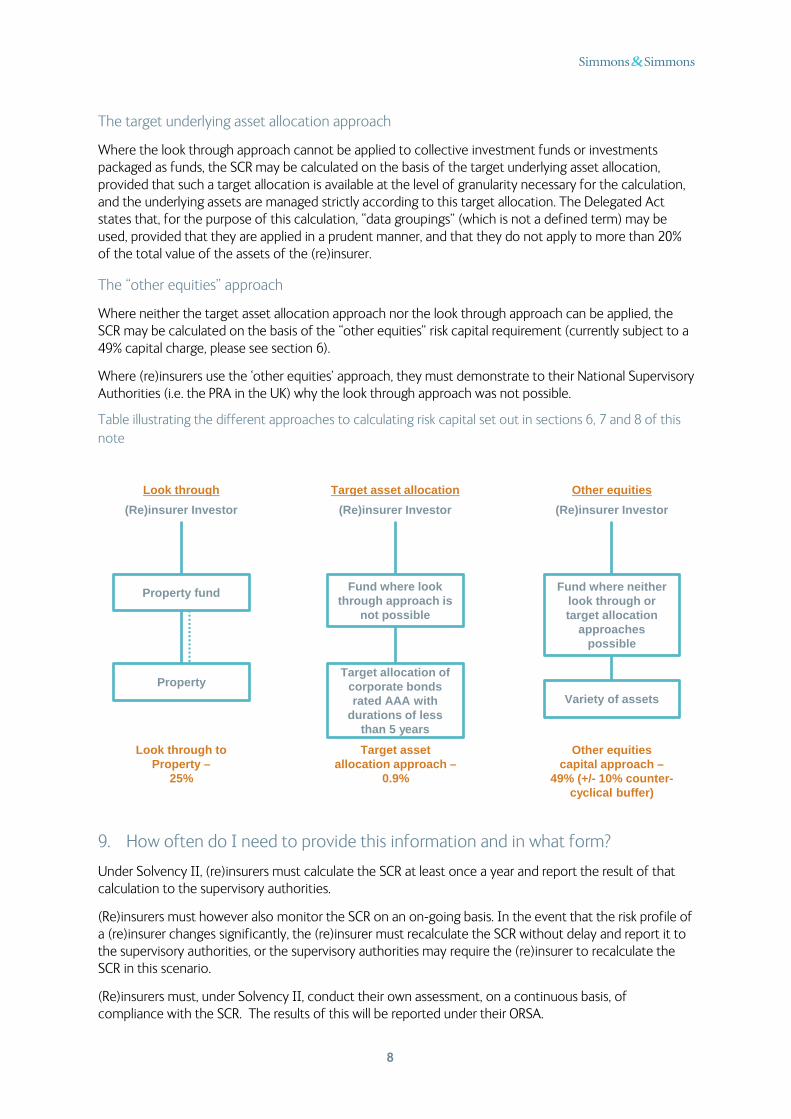

8. What if it is not possible to “look through” to the underlying assets?

The alternatives to using the look through approach to calculate a (re)insurers’ risk capital requirements are the target underlying asset allocation approach and the “other equities” approach.

8

The target underlying asset allocation approach

Where the look through approach cannot be applied to collective investment funds or investments packaged as funds, the SCR may be calculated on the basis of the target underlying asset allocation, provided that such a target allocation is available at the level of granularity necessary for the calculation, and the underlying assets are managed strictly according to this target allocation. The Delegated Act states that, for the purpose of this calculation, “data groupings” (which is not a defined term) may be used, provided that they are applied in a prudent manner, and that they do not apply to more than 20% of the total value of the assets of the (re)insurer.

The “other equities” approach

Where neither the target asset allocation approach nor the look through approach can be applied, the SCR may be calculated on the basis of the “other equities” risk capital requirement (currently subject to a 49% capital charge, please see section 6).

Where (re)insurers use the ‘other equities’ approach, they must demonstrate to their National Supervisory Authorities (i.e. the PRA in the UK) why the look through approach was not possible.

Table illustrating the different approaches to calculating risk capital set out in sections 6, 7 and 8 of this note

9. How often do I need to provide this information and in what form?

Under Solvency II, (re)insurers must calculate the SCR at least once a year and report the result of that calculation to the supervisory authorities.

(Re)insurers must however also monitor the SCR on an on-going basis. In the event that the risk profile of a (re)insurer changes significantly, the (re)insurer must recalculate the SCR without delay and report it to the supervisory authorities, or the supervisory authorities may require the (re)insurer to recalculate the SCR in this scenario.

(Re)insurers must, under Solvency II, conduct their own assessment, on a continuous basis, of compliance with the SCR. The results of this will be reported under their ORSA.

Look through Target asset allocation Other equities(Re)insurer Investor (Re)insurer Investor (Re)insurer Investor

Fund where look through approach is

not possible

Property fund Fund where neither look through or target allocation

approaches possible

PropertyVariety of assets

Look through to Property –

25%

Target asset allocation approach –

0.9%

Other equitiescapital approach –

49% (+/- 10% counter-cyclical buffer)

Target allocation of corporate bonds rated AAA with

durations of less than 5 years

9

It is very important under Solvency II that the data is accurate, consistent and of good quality, as this data forms the foundation for the risk assessment and capital requirements.

(Re)insurers will therefore be requesting full information on the up-to-date portfolio composition (including “look through”) on a regular basis (in some cases daily but more likely, quarterly) and may need to request this at any time at short notice.

The regulators will require detailed information on an item-by-item basis of the risks in the investment portfolio of (re)insurers, including a list of assets (proposed templates S.06.02.01 (individual undertakings) and S.06.02.04 (groups)), a list of open derivatives (proposed templates S.08.01.01 (individual undertakings) and S.08.01.04 (groups)) and a list of derivative transactions (proposed templates S.08.02.01 (individual undertakings) and S.08.02.04 (groups)) (see Appendices 1 and 2 for additional information in connection with completing these templates). This information will need to be submitted by (re)insurers as part of the quantitative information reporting requirements under Solvency II. Commission Implementing Regulation 2015/2450 sets out the details of the quantitative information reporting required for those using Standard Formulae. (Re)insurers with Internal Models may however use slightly different reporting templates. Fund managers will need to assist their (re)insurer clients with completing the quantitative reporting templates to enable them to make their Solvency II quantitative information submissions on an annual and quarterly basis.

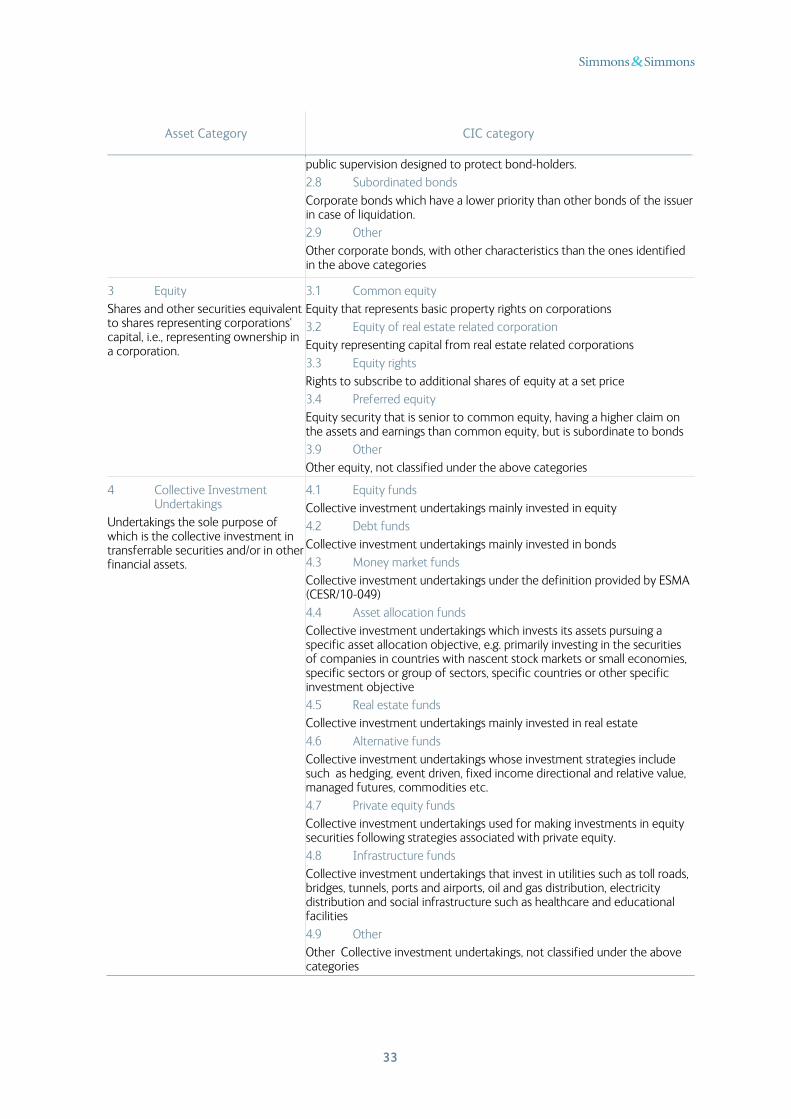

The templates require asset managers to use the Asset Categories and the Complementary Identification Codes (“CIC”) (see Appendix 3). No further guidance has been issued to aid asset managers in categorising the assets they manage, without which there is a risk of inconsistent asset classification. The Investment Management Association (now the Investment Association, “IA”) has highlighted that because the boundaries of the CIC categories are not clearly defined, there is a risk that the same asset may be categorised differently across the market. More generally, there is a lack of appropriate asset codes. This will make it difficult for fund managers to know how to classify assets and could cause problems if different (re)insurers wish for the same asset to be classified in different categories. In the absence of clear guidance on this matter, it is of utmost importance that fund managers liaise with each of their (re)insurer clients as soon as possible to understand how they wish to classify their assets. If it is not possible to use substantively the same asset categorisation for each (re)insurer client, fund managers may require a greater amount of resources to produce Solvency II compliant data to their entire client base than would otherwise have been the case.

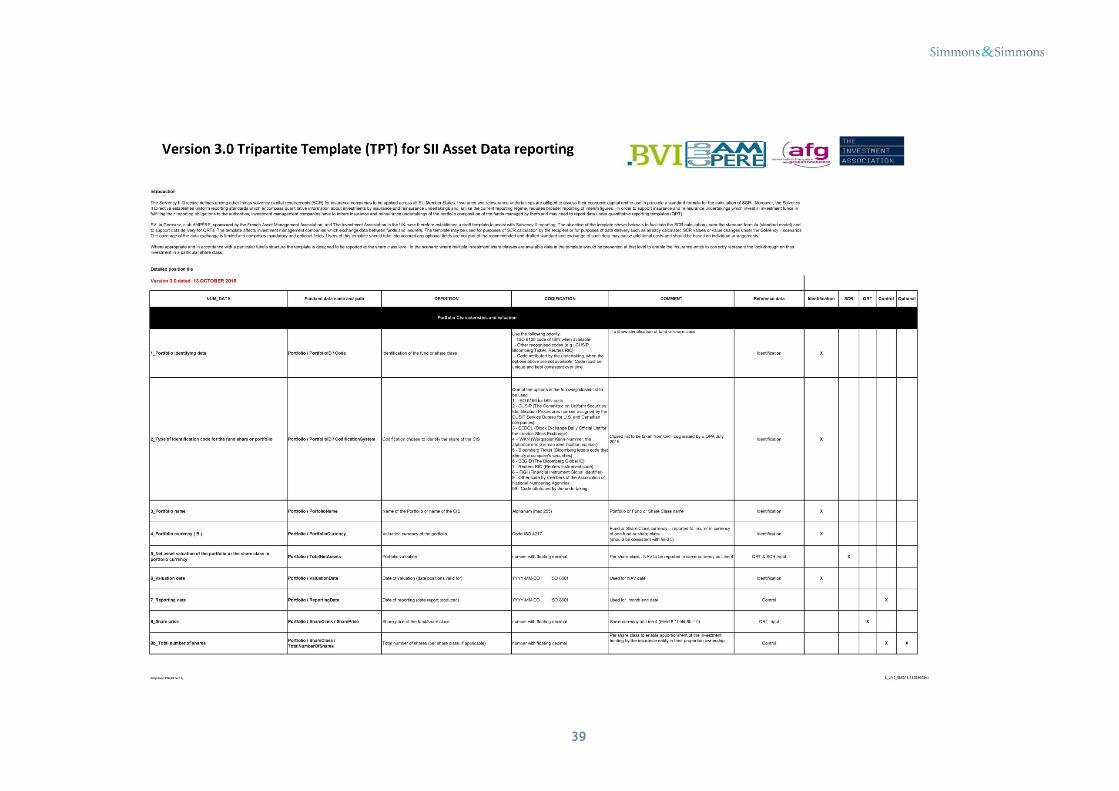

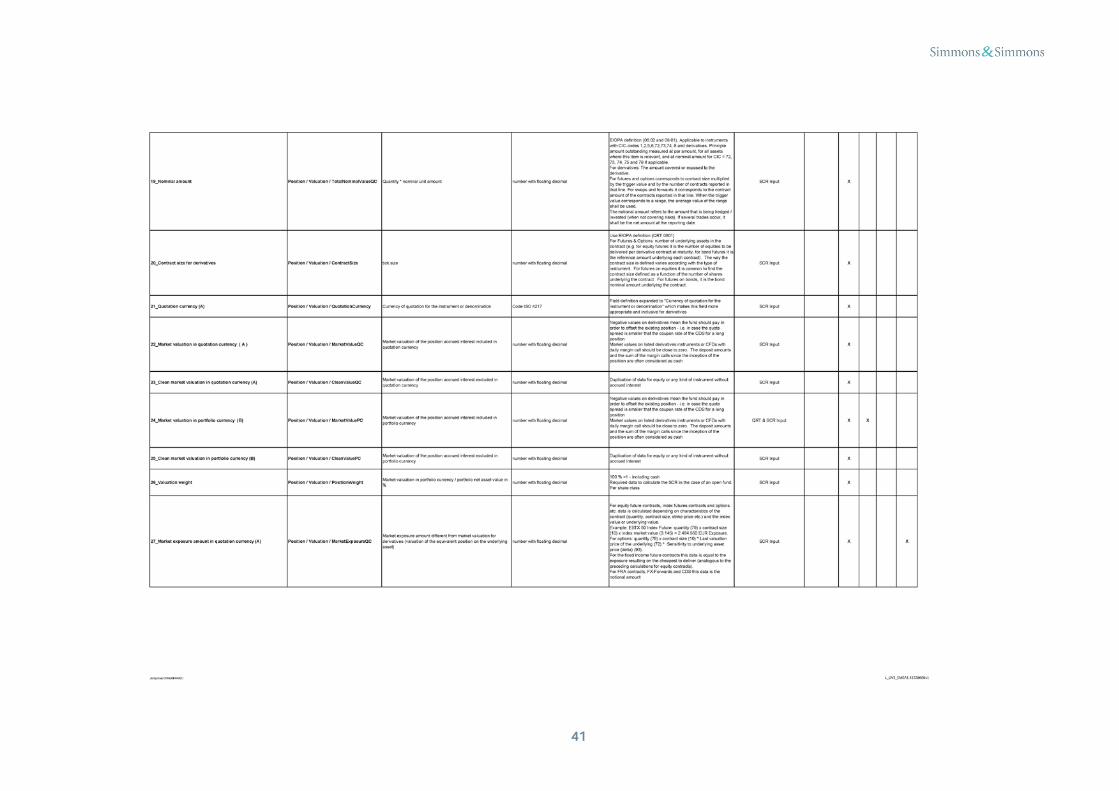

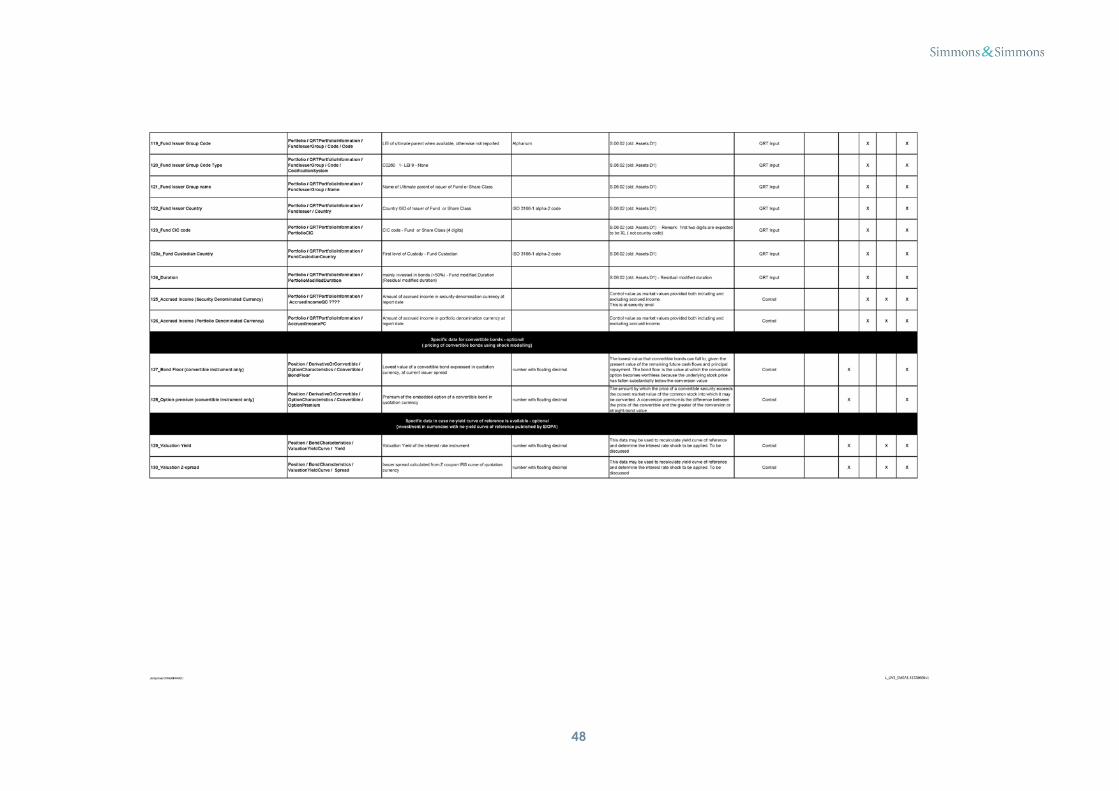

To assist data transfer between fund managers and (re)insurers, the IA, the BVI in Germany and Club AMPÈRE (sponsored by the French Asset Management Association) have developed a standard “Tripartite Template” for Solvency II reporting (see Appendix 4). (Please note that Appendix 4 needs to be printed on A3 paper to be readable, alternatively the soft copy of the document can be accessed via the link: http://www.theinvestmentassociation.org/investment-industry-information/current-initiatives/solvency-ii.html ). This Tripartite Template is a valuable resource as a starting point for dialogue between fund managers and (re)insurers regarding clients’ Solvency II data requirements, particularly where clients have not yet provided a detailed list of the information they require from their fund managers.

As a result of the potential difficulties of reporting to (re)insurers, many third party data managers are offering their reporting services to fund managers. Using the Tripartite Template, the data managers may provide a consolidated reporting service to (re)insurers taking into account (re)insurers’ investments with numerous fund managers. It is of note that some data managers have been able to achieve complete look through for their clients.

If fund managers elect to provide information to (re)insurers via third party data managers, attention must be paid to the terms of the arrangements being put in place, in particular in respect of data accuracy, ownership and confidentiality (see section 10 below).

10

10. How do I protect the confidentiality of the data?

The disclosure of up-to-date investment positions is understandably a concern for fund managers. It should be ensured that robust confidentiality provisions are in place with the (re)insurer or third party data manager(s) before such disclosure is made, in particular to ensure that such data cannot be shared with the (re)insurer’s own investment management arm.

It should also be borne in mind that managers of collective investment funds are required to treat all of their investors fairly.

This point 10 touches on the subject of both the use of NDAs, as well as the important issue of asset managers complying with their own regulatory duties. Each of these are the subject of two separate appendices to the S2SA, in response to the issues we recognised which were of particular interest to our working group participants.

We would strongly advise referring to the S2SA for a more comprehensive analysis of the issues referred to in this publication. Please do contact Pollyanna Deane and Jennifer Yao if you would like to find out more information about the S2SA template and/or the Solvency II asset risks training that we provide.

11

The information provided in this note is based on the Solvency II provisions as at 31 January 2016. This note is for information only and should not be considered as advice. Please note that not all of the Solvency II provisions have been finalised and may change.

The explanation in this note of (re)insurers' capital requirements has been simplified for ease of understanding and only covers the Standard Formulae proposals. If a (re)insurer has an Internal Model, this will alter its capital requirements.

If you require any further information about the application of Solvency II, the S2SA or Solvency II training, please contact:

Pollyanna Deane

Partner

T +44 20 7825 4303

Katherine Lamb

Supervising Associate

T +44 20 7825 4581

Jennifer Yao

Supervising Associate

T +44 20 7825 4186

Sophie Hiley

Associate

T +44 20 7825 4097

Please note that you may also submit questions to the PRA’s Working Group on Solvency II by contacting the Firm Enquiries Function ([email protected] or 020 3461 7000), and we can help with this.

12

Appendix 1 Collated ITS instructions for template S.06.02 list of assets – individual and group undertakings (differences noted)

Annex I of Commission Implementing Regulation 2015/2450 laying down the Implementing Technical Standards with regard to the templates for the submission of information to the supervisory authorities (the “ITS Regulation”, for the purposes of these appendices) contains templates for (re)insurers to complete and regularly submit to the supervisory authorities.

The table below (being derived from Annexes II and III of the ITS Regulation) sets out additional instructions in relation to completing proposed templates S.06.02.01 (individual undertakings) and S.06.02.04 (groups) – list of assets – of Annex I of the ITS Regulation. Where there are differences between the instructions for individual undertakings (Annex II of the ITS Regulation) and group undertakings (Annex III of the ITS Regulation), these are noted below.

The table is split into two parts: (i) information on positions held; and (ii) information on assets.

Part 1 – Information on positions held

Item Instructions

Groups only

C0010 (A50)

Legal name of the undertaking

Identify the legal name of the undertaking within the group that holds the asset.

This item shall be filled in only when it relates to assets held by participating undertakings, insurance holding companies, mixed-financial holding companies and subsidiaries under deduction and aggregation method.

Groups only

C0020 Identification code of the undertaking

Identification code by this order of priority if existent: Legal Entity Identifier (LEI);

Specific code

Specific code: For EEA insurance and reinsurance undertakings and other EEA regulated

undertakings within the group: identification code used in the local market, attributed by the undertaking's competent supervisory authority;

For non-EEA undertakings and non-regulated undertakings within the group, identification code will be provided by the group. When allocating an identification code to each non-EEA or non-regulated undertaking, the group shall comply with the following format in a consistent manner:

• identification code of the parent undertaking + ISO 3166-1 alpha-2 code of the country of the undertaking + 5 digits

Groups only

C0030 Type of code of the ID of the undertaking

Type of ID Code used for the “Identification code of the undertaking” item. One of the options in the following closed list shall be used:

1 - LEI

2 - Specific code

C0040 (A4)

Asset ID Code Asset ID code using the following priority:

ISO 6166 code of ISIN when available

Other recognised codes (e.g.: CUSIP, Bloomberg Ticker, Reuters RIC)

13

Item Instructions

Code attributed by the undertaking, when the options above are not available. This code must be unique and kept consistent over time.

When the same Asset ID Code needs to be reported for one asset that is issued in 2 or more different currencies, it is necessary to specify the Asset ID code and the ISO 4217 alphabetic code of the currency, as in the following example: “code+EUR”

C0050

(A5)

Asset ID Code Type Type of ID Code used for the “Asset ID Code” item. One of the options in the following closed list shall be used:

1. ISO 6166 for ISIN code

2. CUSIP (The Committee on Uniform Securities Identification Procedures number assigned by the CUSIP Service Bureau for U.S. and Canadian companies)

3. SEDOL (Stock Exchange Daily Official List for the London Stock Exchange)

4. WKN (Wertpapier Kenn-Nummer, the alphanumeric German identification number)

5. Bloomberg Ticker (Bloomberg letters code that identify a company's securities)

6. BBGID (The Bloomberg Global ID)

7. Reuters RIC (Reuters instrument code)

8. FIGI (Financial Instrument Global Identifier)

9. Other code by members of the Association of National Numbering Agencies

99. Code attributed by the undertaking

When the same Asset ID Code needs to be reported for one asset that is issued in 2 or more different currencies and the code in C0040 is defined by Asset ID code and the ISO 4217 alphabetic code of the currency, the Asset ID Code Type shall refer to option 9 and the option of the original Asset ID Code, as in the following example for which the code reported was ISIN code+currency: “9/1”.

C0060 (Al)

Portfolio Distinction between life, non-life, shareholder’s funds, general (no split) and ring fenced funds.

One of the options in the following closed list shall be used:

1. Life

2. Non-life

3. Ring fenced funds

4. Other internal funds

5. Shareholders' funds

6. General

The split is not mandatory, except for identifying ring fenced funds, but shall be reported if the undertaking uses it internally. When an undertaking does not apply a split “general” shall be used.

C0070 (A2)

Fund number Applicable to assets held in ring fenced funds or other internal funds (defined according to national markets).

Number which is attributed by the undertaking, corresponding to the unique number assigned to each fund. This number has to be consistent over time and should be used to identify the funds in other templates. It shall not be re-used for a different fund.

C0080 Matching portfolio Number which is attributed by the undertaking, corresponding to the unique

14

Item Instructions

number number assigned to each matching adjustment portfolio as prescribed in Article 77b(1)(a) of Directive 2009/138/EC. This number has to be consistent over time and should be used to identify the matching adjustment portfolio in other templates. It shall not be re-used for a different matching adjustment portfolio.

C0090 A3

Asset held in unit linked and index linked contracts

Identify the assets that are held by unit linked and index linked contracts. One of the options in the following closed list shall be used:

1. Unit-linked or index-linked

2. Neither unit-linked nor index-linked

C0100 (A6)

Asset pledged as collateral

Identify assets kept in the undertaking’s balance-sheet that are pledged as collateral. For partially pledged assets two lines for each asset shall be reported, one for the pledged amount and another for the remaining part. One of the options in the following closed list shall be used for the pledged part of the asset:

1. Assets in the balance sheet that are collateral pledged

2. Collateral for reinsurance accepted

3. Collateral for securities borrowed

4. Repos

9. Not collateral

C0110 (A12)

Country of custody ISO 3166-1 alpha-2 code of the country where undertaking assets are held in custody. For identifying international custodians, such as Euroclear, the country of custody will be the one corresponding to the legal establishment where the custody service was contractually defined.

In case of the same asset being held in custody in more than one country, each asset shall be reported separately in as many lines as needed in order to properly identify all countries of custody.

This item is not applicable for CIC category 8 – Mortgages and Loans (for mortgages and loans to natural persons, as those assets are not required to be individualised), CIC 71, CIC 75 and for CIC 95 – Plant and equipment (for own use) for the same reason.

Regarding CIC Category 9, excluding CIC 95 – Plant and equipment (for own use), the issuer country is assessed by the address of the property.

C0120 (A33)

Custodian Name of the financial institution that is the custodian.

In case of the same asset being held in custody in more than one custodian, each asset shall be reported separately in as many lines as needed in order to properly identify all custodians.

When available, this item corresponds to the entity name in the LEI database. When this is not available corresponds to the legal name.

This item is not applicable for CIC category 8 – Mortgages and Loans (for mortgages and loans to natural persons, as those assets are not required to be individualised), CIC 71, CIC 75 and for CIC category 9 – Property.

C0130 (A22)

Quantity Number of assets, for relevant assets

This item shall not be reported if item Par amount (C0140) is reported.

C0140 (A22A)

Par amount Amount outstanding measured at par amount, for all assets where this item is relevant, and at nominal amount for CIC = 72, 73, 74, 75 and 79 if applicable. This item shall not be reported if item Quantity (C0130) is reported.

C0150 (A24)

Valuation method Identify the valuation method used when valuing assets. One of the options in the following closed list shall be used:

1. quoted market price in active markets for the same assets

2. quoted market price in active markets for similar assets

3. alternative valuation methods

15

Item Instructions

4. adjusted equity methods (applicable for the valuation of participations)

5. IFRS equity methods (applicable for the valuation of participations)

6. Market valuation according to article 9(4) of Delegated Regulation 2015/35

C0160 (A25)

Acquisition value Total acquisition value for assets held, clean value without accrued interest.

Not applicable to CIC categories 7 and 8

C0170 (A26)

Total Solvency II amount Value calculated as defined by article 75 of the Directive 2009/138/EC.

The following shall be considered:

Corresponds to the multiplication of “Par amount” by “Unit percentage of par amount Solvency II price” plus “Accrued interest”, for assets where these items are relevant;

Corresponds to the multiplication of “Quantity” by “Unit Solvency II price” for assets where these two items are relevant;

For assets classifiable under asset categories 7, 8 and 9, this shall indicate the Solvency II value of the asset.

C0180 (A30)

Accrued interest Quantify the amount of accrued interest after the last coupon date for interest bearing securities. Note that this value is also part of item Total Solvency II amount.

16

Part 2 – Information on assets

Item Instruction

C0040 (A4)

Asset ID Code Asset ID code using the following priority:

ISO 6166 code of ISIN when available

Other recognised codes (e.g.: CUSIP, Bloomberg Ticker, Reuters RIC)

Code attributed by the undertaking, when the options above are not available. This code must be unique and kept consistent over time.

When the same Asset ID Code needs to be reported for one asset that is issued in 2 or more different currencies, it is necessary to specify the Asset ID code and the ISO 4217 alphabetic code of the currency, as in the following example: “code+EUR”

C0050 (A5)

Asset ID Code Type Type of ID Code used for the “Asset ID Code” item. One of the options in the following closed list shall be used:

1. ISO 6166 for ISIN code

2. CUSIP (The Committee on Uniform Securities Identification Procedures number assigned by the CUSIP Service Bureau for U.S. and Canadian companies)

3. SEDOL (Stock Exchange Daily Official List for the London Stock Exchange)

4. WKN (Wertpapier Kenn-Nummer, the alphanumeric German identification number)

5. Bloomberg Ticker (Bloomberg letters code that identify a company's securities)

6. BBGID (The Bloomberg Global ID)

7. Reuters RIC (Reuters instrument code)

8. FIGI (Financial Instrument Global Identifier)

9. Other code by members of the Association of National Numbering Agencies

99. Code attributed by the undertaking

When the same Asset ID Code needs to be reported for one asset that is issued in 2 or more different currencies and the code in C0040 is defined by Asset ID code and the ISO 4217 alphabetic code of the currency, the Asset ID Code Type shall refer to option 9 and the option of the original Asset ID Code, as in the following example for which the code reported was ISIN code+currency: “9/1”.

C0190 (A7)

Item Title Identify the reported item by filling the name of the asset (or the address in case of property), with the detail settled by the undertaking.

The following shall be considered:

Regarding CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons, this item shall contain “Loans to AMSB members” or “Loans to other natural persons”, according to its nature, as those assets are not required to be individualised. Loans to other than natural persons shall be reported line-by-line.

This item is not applicable for CIC 95 – Plant and equipment (for own use) as those assets are not required to be individualised, CIC 71 and CIC 75.

17

Item Instruction

C0200 (A8)

Issuer Name Name of the issuer, defined as the entity that issues assets to investors.

When available, this item corresponds to the entity name in the LEI database. When this is not available corresponds to the legal name.

The following shall be considered:

Regarding CIC category 4 – Collective Investments Undertakings, the issuer name is the name of the fund manager;

Regarding CIC category 7 – Cash and deposits (excluding CIC 71 and CIC 75), the issuer name is the name of the depositary entity;

Regarding CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons, this item shall contain “Loans to AMSB members” or “Loans to other natural persons”, according to its nature, as those assets are not required to be individualised;

Regarding CIC 8 – Mortgages and Loans, other than mortgage and loans to natural persons the information shall relate to the borrower;

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property.

C0210 (A31)

Issuer Code Identification of the issuer code using the Legal Entity Identifier (LEI) if available. If none is available this item shall not be reported.

The following shall be considered:

Regarding CIC category 4 – Collective Investments Undertakings, the issuer code is the code of the fund manager;

Regarding CIC category 7 – Cash and deposits (excluding CIC 71 and CIC 75), the issuer code is the code of the depositary entity

Regarding CIC 8 – Mortgages and Loans, other than mortgage and loans to natural persons the information shall relate to the borrower;

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property;

This item is not applicable to CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons.

C0220 (A33)

Type of issuer code Identification of the type of code used for the “Issuer Code” item. One of the options in the following closed list shall be used:

1 - LEI

9 – None

This item is not applicable to CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons.

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property.

C0230 (A9)

Issuer Sector Identify the economic sector of issuer based on the latest version of NACE code (as published in an EC Regulation). The letter reference of the NACE code identifying the Section shall be used as a minimum for identifying sectors (e.g. ‘A’ or ‘A0111’ would be acceptable) except for the NACE relating to Financial and Insurance activities, for which the letter identifying the Section followed by the 4 digits code for the class shall be used (e.g. ‘K6411’).

The following shall be considered:

Regarding CIC category 4 – Collective Investments Undertakings, the issuer sector is the sector of the fund manager;

18

Item Instruction

Regarding CIC category 7 – Cash and deposits (excluding CIC 71 and CIC 75), the issuer sector is the sector of the depositary entity

Regarding CIC 8 – Mortgages and Loans, other than mortgage and loans to natural persons the information shall relate to the borrower;

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property;

This item is not applicable to CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons.

C0240 (A10)

Issuer Group Name of issuer’s ultimate parent entity. For collective investment undertakings the group relation relates to the fund manager.

When available, this item corresponds to the entity name in the LEI database. When this is not available corresponds to the legal name.

The following shall be considered:

Regarding CIC category 4 – Collective Investments Undertakings, the group relation relates to the fund manager;

Regarding CIC category 7 – Cash and deposits (excluding CIC 71 and CIC 75), the group relation relates to the depositary entity

Regarding CIC 8 – Mortgages and Loans, other than mortgage and loans to natural persons the group relation relates to the borrower;

This item is not applicable for CIC category 8 – Mortgages and Loans (for mortgages and loans to natural persons)

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property.

C0250 (A32)

Issuer Group Code Issuer group’s identification using the Legal Entity Identifier (LEI) if available.

If none is available, this item shall not be reported.

The following shall be considered:

Regarding CIC category 4 – Collective Investments Undertakings, the group relation relates to the fund manager;

Regarding CIC category 7 – Cash and deposits (excluding CIC 71 and CIC 75), the group relation relates to the depositary entity

Regarding CIC 8 – Mortgages and Loans, other than mortgage and loans to natural persons the group relation relates to the borrower;

This item is not applicable for CIC category 8 – Mortgages and Loans (for mortgages and loans to natural persons)

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property.

C0260 (A33)

Type of issuer group code Identification of the code used for the “Issuer Group Code” item. One of the options in the following closed list shall be used:

1 - LEI

9 - None

This item is not applicable to CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons.

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property.

C0270 (A11)

Issuer Country ISO 3166-1 alpha-2 code of the country of localisation of the issuer.

The localisation of the issuer is assessed by the address of the entity issuing the asset.

The following shall be considered:

19

Item Instruction

Regarding CIC category 4 – Collective Investments Undertakings, the issuer country is the country is relative to the fund manager;

Regarding CIC category 7 – Cash and deposits (excluding CIC 71 and CIC 75), the issuer country is the country of the depositary entity

Regarding CIC 8 – Mortgages and Loans, other than mortgage and loans to natural persons the information shall relate to the borrower;

This item is not applicable for CIC 71, CIC 75 and CIC category 9 – Property;

This item is not applicable to CIC category 8 – Mortgages and Loans, when relating to mortgage and loans to natural persons.

One of the options shall be used:

ISO 3166-1 alpha-2 code

XA: Supranational issuers

EU: European Union Institutions

C0280 (A13)

Currency Identify the ISO 4217 alphabetic code of the currency of the issue.

The following shall be considered:

This item is not applicable for CIC category 8 – Mortgages and Loans (for mortgages and to natural persons, as those assets are not required to be individualised), CIC 75 and for CIC = 95 – Plant and equipment (for own use) for the same reason;

Regarding CIC Category 9, excluding CIC 95 – Plant and equipment (for own use), the currency corresponds to the currency in which the investment was made.

C0290 (A15)

CIC Complementary Identification Code used to classify assets, as set out in Annex V - CIC Table of the ITS Regulation. When classifying an asset using the CIC table, undertakings shall take into consideration the most representative risk to which the asset is exposed to.

In addition, for groups only:

The parent undertaking shall check and ensure that the CIC code used for the same security from different undertakings is the same in the group reporting.

C0300 Infrastructure investment Identify if the asset is an infrastructure investment.

Infrastructure investment is defined as investments in or loans to utilities such as toll roads, bridges, tunnels, ports and airports, oil and gas distribution, electricity distribution and social infrastructure such as healthcare and educational facilities.

One of the options in the following closed list shall be used:

1. Not an infrastructure investment

2. Government Guarantee: where there is an explicit government guarantee

3. Government Supported including Public Finance initiative: where there is a government policy or public finance initiatives to promote or support the sector

4. Supranational Guarantee/Supported: where there is an explicit supranational guarantee or support

9. Other: Other infrastructure loans or investments, not classified under the above categories

C0310 (A16)

Holdings in related undertakings, including

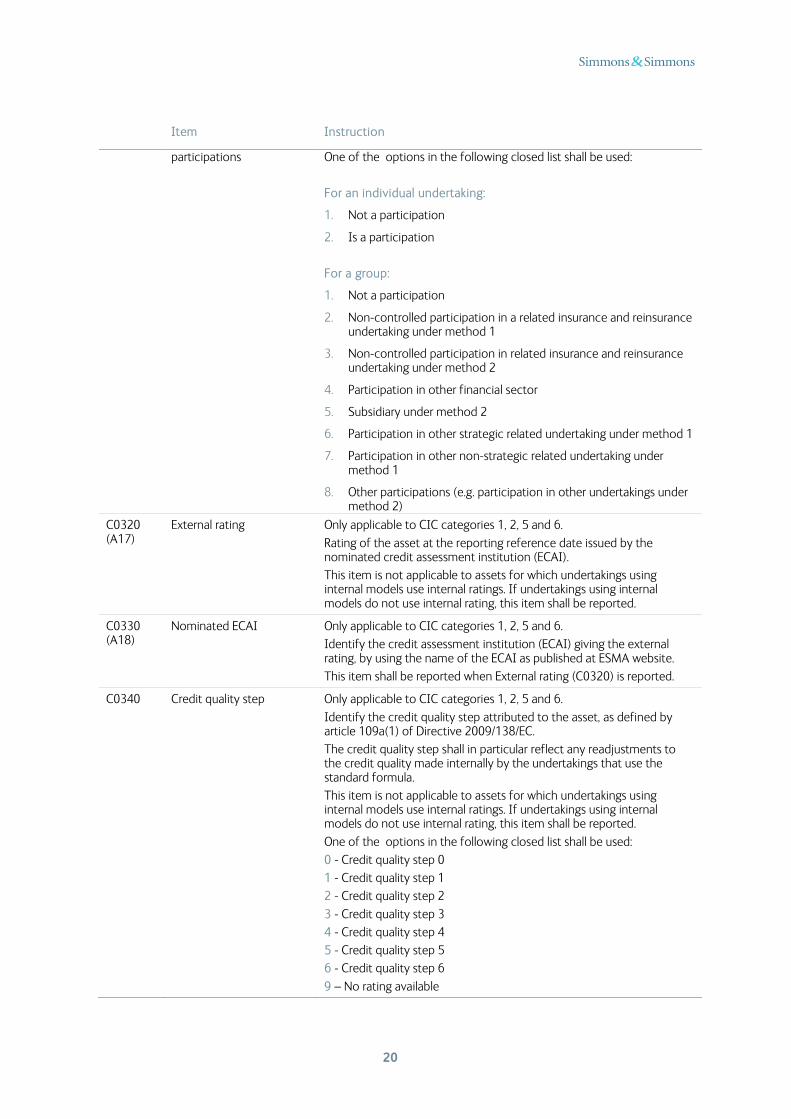

Only applicable to asset categories 3 and 4.

Identify if an equity and other share is a participation.

20

Item Instruction

participations One of the options in the following closed list shall be used:

For an individual undertaking:

1. Not a participation

2. Is a participation

For a group:

1. Not a participation

2. Non-controlled participation in a related insurance and reinsurance undertaking under method 1

3. Non-controlled participation in related insurance and reinsurance undertaking under method 2

4. Participation in other financial sector

5. Subsidiary under method 2

6. Participation in other strategic related undertaking under method 1

7. Participation in other non-strategic related undertaking under method 1

8. Other participations (e.g. participation in other undertakings under method 2)

C0320 (A17)

External rating Only applicable to CIC categories 1, 2, 5 and 6.

Rating of the asset at the reporting reference date issued by the nominated credit assessment institution (ECAI).

This item is not applicable to assets for which undertakings using internal models use internal ratings. If undertakings using internal models do not use internal rating, this item shall be reported.

C0330 (A18)

Nominated ECAI Only applicable to CIC categories 1, 2, 5 and 6.

Identify the credit assessment institution (ECAI) giving the external rating, by using the name of the ECAI as published at ESMA website.

This item shall be reported when External rating (C0320) is reported.

C0340 Credit quality step Only applicable to CIC categories 1, 2, 5 and 6.

Identify the credit quality step attributed to the asset, as defined by article 109a(1) of Directive 2009/138/EC.

The credit quality step shall in particular reflect any readjustments to the credit quality made internally by the undertakings that use the standard formula.

This item is not applicable to assets for which undertakings using internal models use internal ratings. If undertakings using internal models do not use internal rating, this item shall be reported.

One of the options in the following closed list shall be used:

0 - Credit quality step 0

1 - Credit quality step 1

2 - Credit quality step 2

3 - Credit quality step 3

4 - Credit quality step 4

5 - Credit quality step 5

6 - Credit quality step 6

9 – No rating available

21

Item Instruction

C0350 Internal rating Only applicable to CIC categories 1, 2, 5 and 6.

Internal rating of assets for undertakings using an internal model to the extent that the internal ratings are used in their internal modelling. If an internal model undertaking is using solely external ratings this item shall not be reported.

C0360 (A20)

Duration Only applies to CIC categories 1, 2, 4 (when applicable, e.g. for collective investment undertaking mainly invested in bonds), 5 and 6.

Asset duration, defined as the ’residual modified duration’ (modified duration calculated based on the remaining time for maturity of the security, counted from the reporting reference date). For assets without fixed maturity the first call date shall be used. The duration shall be calculated based on economic value.

C0370 (A23)

Unit Solvency II price Amount in reporting currency for the asset, if relevant.

This item shall be reported if a "quantity" (C0130) has been provided in the first part of the template ("Information on positions held").

This item shall not be reported if item Unit percentage of par amount Solvency II price (C0380) is reported.

C0380 (A23A)

Unit percentage of par amount Solvency II price

Amount in percentage of par value, clean price without accrued interest, for the asset, if relevant.

This item shall be reported if a "par amount" information (C0140) has been provided in the first part of the template ("Information on positions held").

This item shall not be reported if item Unit Solvency II price (C0370) is reported.

C0390 (A28)

Maturity date Only applicable for CIC categories 1, 2, 5, 6, and 8, CIC 74 and CIC 79.

Identify the ISO 8601 (yyyy-mm-dd) code of the maturity date.

It corresponds always to the maturity date, even for callable securities.

The following shall be considered:

For perpetual securities use “9999-12-31”

For CIC category 8, regarding loans and mortgages to individuals, the weighted (based on the loan amount) remaining maturity is to be reported.

22

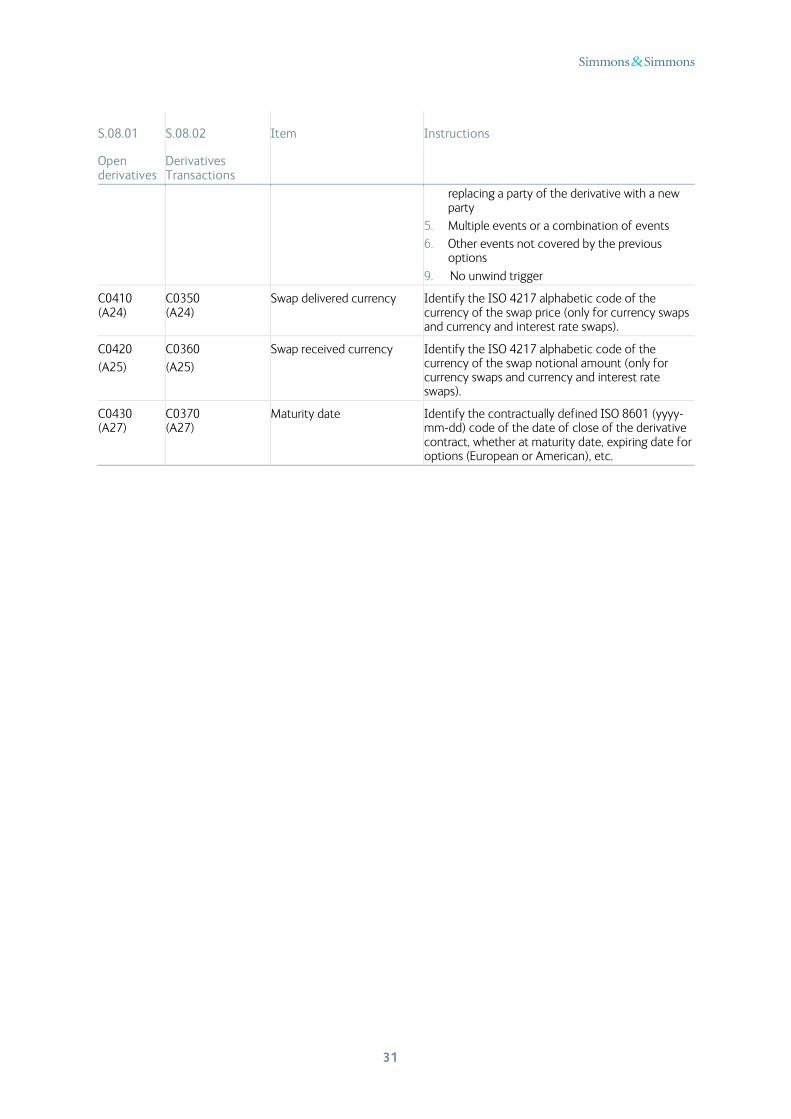

Appendix 2 Collated ITS instructions for templates S.08.01 & S.08.02 list of open derivatives and derivatives transactions – individual and group undertakings (differences noted)

The table below sets out additional instructions in relation to completing the following templates as set out in Annex I of the ITS Regulation: S.08.01.01 (individual undertakings) and S.08.01.04 (groups) – Open derivatives (old Derivatives D2O) and S.08.02.01 (individual undertakings) and S.08.02.04 (groups) - Derivatives Transactions (old Derivatives D2T). The relevant instructions can be found in Annexes II and III of the ITS Regulation. Where there are differences between the instructions for individual undertakings (Annex II of the ITS Regulation) and group undertakings (Annex III of the ITS Regulation), these are noted below.

Part 1: Information on positions held S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

Groups only

C0010 (A50)

C0010 (A50)

Legal name of the undertaking

Identify the legal name of the undertaking within the group that holds the derivative.

This item shall be filled in only when it relates to derivatives held by participating undertakings, insurance holding companies, mixed-financial holding companies and subsidiaries under deduction and aggregation method.

Groups only

C0020 C0020 Identification code of the undertaking

Identification code by this order of priority if existent:

Legal Entity Identifier (LEI);

Specific code

Specific code:

For EEA insurance and reinsurance undertakings and other EEA regulated undertakings within the group: identification code used in the local market, attributed by the undertaking's competent supervisory authority;

For non-EEA undertakings and non-regulated undertakings within the group, identification code will be provided by the group. When allocating an identification code to each non-EEA or non-regulated undertaking, the group shall comply with the following format in a consistent manner:

• identification code of the parent undertaking + ISO 3166-1 alpha-2 code of the country of the undertaking + 5 digits

Groups only

C0030 C0030 Type of code of the ID of the undertaking

Type of ID Code used for the “Identification code of the undertaking” item. One of the options in the following closed list shall be used:

1. LEI

2. Specific code

23

S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

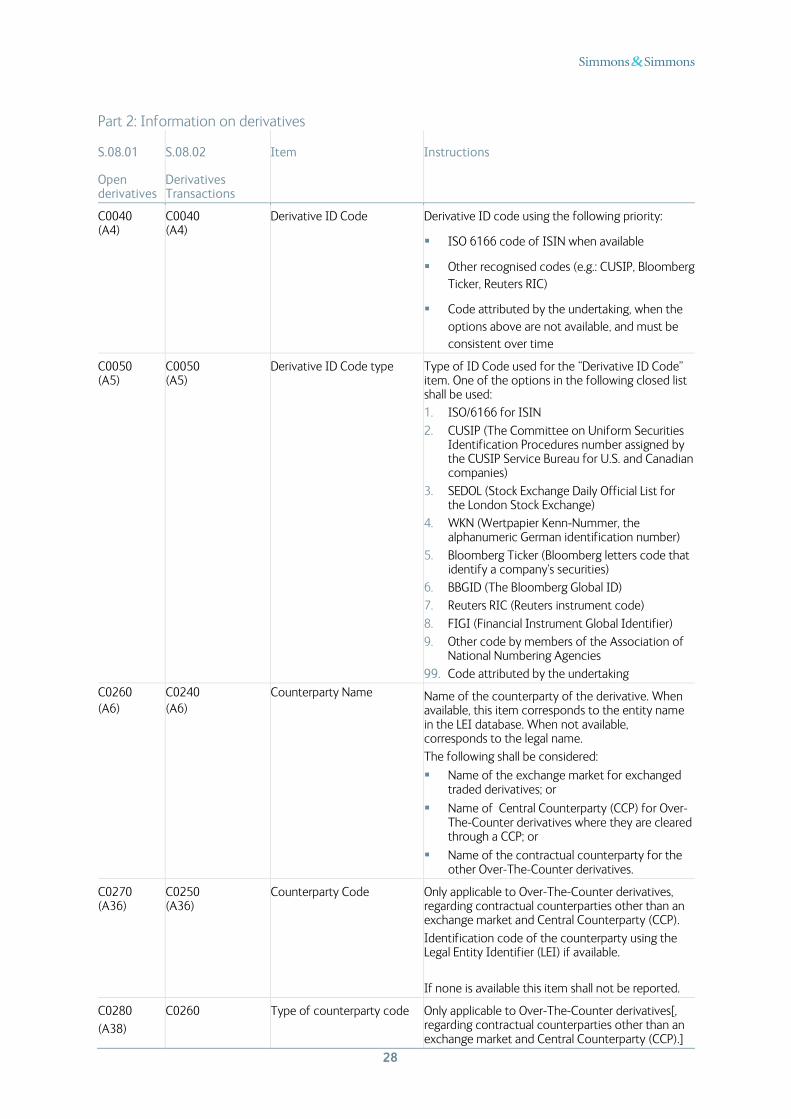

C0040 (A4)

C0040 (A4)

Derivative ID Code Derivative ID code using the following priority:

ISO 6166 code of ISIN when available

Other recognised codes (e.g.: CUSIP, Bloomberg Ticker, Reuters RIC)

Code attributed by the undertaking, when the options above are not available, and must be consistent over time

C0050 (A5)

C0050 (A5)

Derivative ID Code type Type of ID Code used for the “Derivative ID Code” item. One of the options in the following closed list shall be used:

1. ISO/6166 for ISIN

2. CUSIP (The Committee on Uniform Securities Identification Procedures number assigned by the CUSIP Service Bureau for U.S. and Canadian companies)

3. SEDOL (Stock Exchange Daily Official List for the London Stock Exchange)

4. WKN (Wertpapier Kenn-Nummer, the alphanumeric German identification number)

5. Bloomberg Ticker (Bloomberg letters code that identify a company's securities)

6. BBGID (The Bloomberg Global ID)

7. Reuters RIC (Reuters instrument code)

8. FIGI (Financial Instrument Global Identifier)

9. Other code by members of the Association of National Numbering Agencies

99. Code attributed by the undertaking

C0060 (A1)

C0060 (A1)

Portfolio Distinction between life, non-life, shareholder's funds, general (no split) and ring fenced funds. One of the options in the following closed list shall be used:

1. Life

2. Non-life

3. Ring fenced funds

4. Other internal fund

5. Shareholders' funds

6. General

The split is not mandatory, except for identifying ring fenced funds, but shall be reported if the undertaking uses it internally. When an undertaking does not apply a split “general” shall be used.

C0070

(A2)

C0070

(A2)

Fund number Applicable to derivatives held in ring fenced funds or other internal funds (defined according to national markets).

Number which is attributed by the undertaking, corresponding to the unique number assigned to each fund. This number has to be consistent over time and should be used to identify the funds in other templates. It shall not be re-used for a different fund.

24

S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

C0080 (A3)

C0080

(A3)

Derivatives held in unit linked and index linked contracts

Identify the derivatives that are held by unit linked and index linked contracts. One of the options in the following closed list shall be used:

1. Unit-linked or index-linked

2. Neither unit-linked nor index-linked

C0090 (A9)

C0090

(A9)

Instrument underlying the derivative

ID Code of the instrument (asset or liability) underlying the derivative contract. This item is to be provided only for derivatives that have a single or multiple underlying instruments in the undertakings’ portfolio. An index is considered a single instrument and shall be reported.

Identification code of the instrument underlying the derivative using the following priority:

ISO 6166 code of ISIN when available

Other recognised codes (e.g.: CUSIP, Bloomberg Ticker, Reuters RIC)

Code attributed by the undertaking, when the options above are not available, and must be consistent over time

“Multiple assets/liabilities”, if the underlying assets or liabilities are more than one

If the underlying is an index then the code of the index shall be reported.

C0100 C0100 Type of code of asset or liability underlying the derivative

Type of ID Code used for the “Instrument underlying the derivative” item. One of the options in the following closed list shall be used:

1. ISO/6166 for ISIN

2. CUSIP (The Committee on Uniform Securities Identification Procedures number assigned by the CUSIP Service Bureau for U.S. and Canadian companies)

3. SEDOL (Stock Exchange Daily Official List for the London Stock Exchange)

4. WKN (Wertpapier Kenn-Nummer, the alphanumeric German identification number)

5. Bloomberg Ticker (Bloomberg letters code that identify a company's securities)

6. BBGID (The Bloomberg Global ID)

7. Reuters RIC (Reuters instrument code)

8. FIGI (Financial Instrument Global Identifier)

9. Other code by members of the Association of National Numbering Agencies

99. Code attributed by the undertaking

This item is not reported for derivatives which have as underlying more than one asset or liability.

C0110 (A13)

C0110 (A13)

Use of derivative Describe the use of the derivative (micro / macro hedge, efficient portfolio management).

Micro hedge refers to derivatives covering a single financial instrument (asset or liability), forecasted transaction or other liability.

Macro hedge refers to derivatives covering a set of financial instruments (assets or liabilities), forecasted

25

S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

transactions or other liabilities.

Efficient portfolio management refers usually to operations where the manager wishes to improve a portfolio’s income by exchanging a (lower) cash-flow pattern by another with a higher value, using a derivative or set of derivatives, without changing the asset’s portfolio composition, having a lower investment amount and less transaction costs.

One of the options in the following closed list shall be used:

1. Micro hedge

2. Macro hedge

3. Matching assets and liabilities cash-flows used in the context of matching adjustment portfolios

4. Efficient portfolio management, other than “Matching assets and liabilities cash-flows used in the context of matching adjustment portfolios”

C0120 (A14)

N/A Delta Only applicable to CIC categories B and C (Call and put options), with reference to the reporting date.

Measures the rate of change of option value with respect to changes in the underlying asset's price.

This shall be reported as a decimal.

C0130 (A15)

C0120

(A15)

Notional amount of the derivative

The amount covered or exposed to the derivative.

For futures and options corresponds to contract size multiplied by the trigger value and by the number of contracts reported in that line. For swaps and forwards it corresponds to the contract amount of the contracts reported in that line.

(Only applicable to S.08.01: When the trigger value corresponds to a range, the average value of the range shall be used.)

The notional amount refers to the amount that is being hedged / invested (when not covering risks). If several trades occur, it shall be the net amount at the reporting date.

C0140 (A16)

C0130 (A16)

Buyer/Seller Only for futures and options, swaps and credit derivatives contracts (currency, credit and securities swaps).

Identify whether the derivative contract was bought or sold.

The buyer and seller position for swaps is defined relatively to the security or notional amount and the swap flows.

A seller of a swap owns the security or notional amount at the contract inception and agrees to deliver during the contract term that security or notional amount, including any other outflows related to the contract, when applicable.

A buyer of a swap will own the security or the notional amount at the end of the derivatives contract and will receive during the contract term that security or notional amount, including any other inflows related to the contract, when applicable.

26

S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

One of the options in the following closed list shall be used, with the exception of Interest Rate Swaps:

1. Buyer

2. Seller

For interest rate swaps one of the options in the following closed list shall be use:

3. FX-FL: Deliver fixed-for-floating

4. FX-FX: Deliver fixed-for-fixed

5. FL-FX: Deliver floating-for-fixed

6. FL-FL: Deliver floating-for-floating

C0150 (A17)

C0140 (A17)

Premium paid to date The payment made (if bought), for options and also up-front and periodical premium amounts paid for swaps, since inception.

C0160 C0150

Premium received to date The payment received (if sold), for options and also up-front and periodical premium amounts received for swaps, since inception.

N/A C0160 (A18)

Profit and loss to date

Amount of profit and loss arising from the derivative since inception, realised at the closing/maturing date. Corresponds to the difference between the value (price) at sale date and the value (price) at acquisition date.

This amount could be positive (profit) or negative (loss).

C0170 (A19)

C0170 (A19)

Number of contracts Number of similar derivative contracts reported in the line. (For S.08.01 only: It shall be the number of contracts entered into.)

For Over-The-Counter derivatives, e.g., one swap contract, “1” shall be reported, if ten swaps with the same characteristics, “10” shall be reported.

For S.08.01: The number of contracts shall be the ones outstanding at the reporting date.

For S.08.02: The number of contracts shall be the ones entered into and that were closed at the reporting date.

C0180 (A20)

C0180 (A20)

Contract size Number of underlying assets in the contract (e.g. for equity futures it is the number of equities to be delivered per derivative contract at maturity, for bond futures it is the reference amount underlying each contract). The way the contract size is defined varies according with the type of instrument. For futures on equities it is common to find the contract size defined as a function of the number of shares underlying the contract.

For futures on bonds, it is the bond nominal amount underlying the contract.

Only applicable for futures and options.

C0190 (A32)

C0190 (A32)

Maximum loss under unwinding event

Applicable to both S.08.01 and S.08.02:

Maximum amount of loss if an unwinding event occurs. Applicable to CIC category F.

Only applicable to S.08.01:

Where a credit derivative is 100% collateralised, the maximum loss under an unwinding event is zero.

27

S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

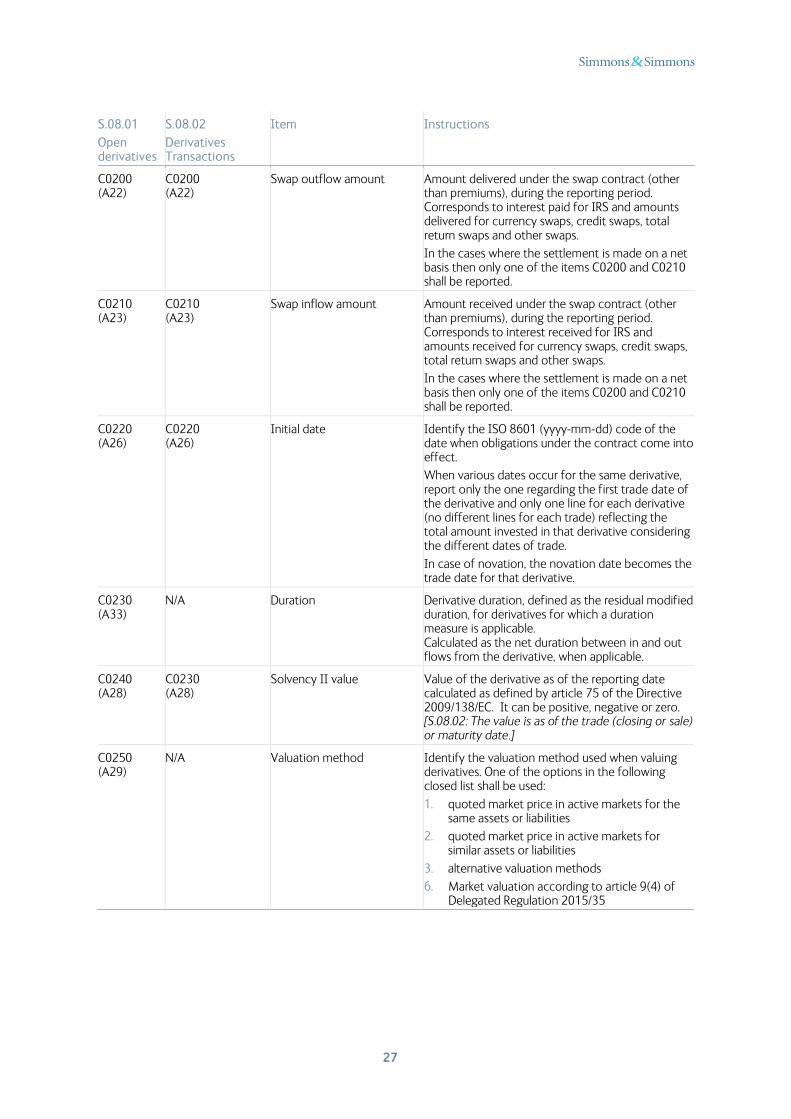

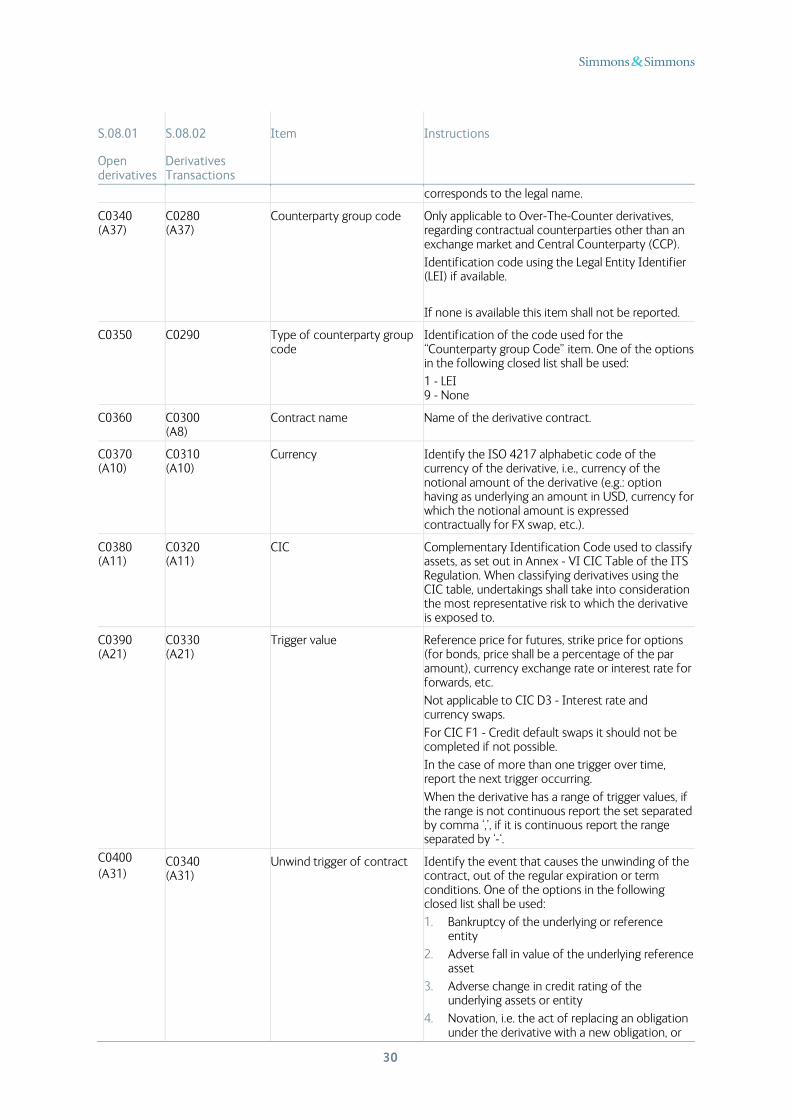

C0200 (A22)

C0200 (A22)

Swap outflow amount Amount delivered under the swap contract (other than premiums), during the reporting period. Corresponds to interest paid for IRS and amounts delivered for currency swaps, credit swaps, total return swaps and other swaps.

In the cases where the settlement is made on a net basis then only one of the items C0200 and C0210 shall be reported.

C0210 (A23)

C0210 (A23)

Swap inflow amount Amount received under the swap contract (other than premiums), during the reporting period. Corresponds to interest received for IRS and amounts received for currency swaps, credit swaps, total return swaps and other swaps.

In the cases where the settlement is made on a net basis then only one of the items C0200 and C0210 shall be reported.

C0220 (A26)

C0220 (A26)

Initial date Identify the ISO 8601 (yyyy-mm-dd) code of the date when obligations under the contract come into effect.

When various dates occur for the same derivative, report only the one regarding the first trade date of the derivative and only one line for each derivative (no different lines for each trade) reflecting the total amount invested in that derivative considering the different dates of trade.

In case of novation, the novation date becomes the trade date for that derivative.

C0230 (A33)

N/A Duration Derivative duration, defined as the residual modified duration, for derivatives for which a duration measure is applicable. Calculated as the net duration between in and out flows from the derivative, when applicable.

C0240 (A28)

C0230 (A28)

Solvency II value Value of the derivative as of the reporting date calculated as defined by article 75 of the Directive 2009/138/EC. It can be positive, negative or zero. [S.08.02: The value is as of the trade (closing or sale) or maturity date.]

C0250 (A29)

N/A Valuation method Identify the valuation method used when valuing derivatives. One of the options in the following closed list shall be used:

1. quoted market price in active markets for the same assets or liabilities

2. quoted market price in active markets for similar assets or liabilities

3. alternative valuation methods

6. Market valuation according to article 9(4) of Delegated Regulation 2015/35

28

Part 2: Information on derivatives

S.08.01

Open derivatives

S.08.02

Derivatives Transactions

Item Instructions

C0040 (A4)

C0040 (A4)

Derivative ID Code Derivative ID code using the following priority:

ISO 6166 code of ISIN when available

Other recognised codes (e.g.: CUSIP, Bloomberg Ticker, Reuters RIC)

Code attributed by the undertaking, when the options above are not available, and must be consistent over time

C0050 (A5)

C0050 (A5)

Derivative ID Code type Type of ID Code used for the “Derivative ID Code” item. One of the options in the following closed list shall be used:

1. ISO/6166 for ISIN

2. CUSIP (The Committee on Uniform Securities Identification Procedures number assigned by the CUSIP Service Bureau for U.S. and Canadian companies)

3. SEDOL (Stock Exchange Daily Official List for the London Stock Exchange)

4. WKN (Wertpapier Kenn-Nummer, the alphanumeric German identification number)

5. Bloomberg Ticker (Bloomberg letters code that identify a company's securities)

6. BBGID (The Bloomberg Global ID)

7. Reuters RIC (Reuters instrument code)

8. FIGI (Financial Instrument Global Identifier)

9. Other code by members of the Association of National Numbering Agencies

99. Code attributed by the undertaking

C0260 (A6)

C0240 (A6)

Counterparty Name Name of the counterparty of the derivative. When available, this item corresponds to the entity name in the LEI database. When not available, corresponds to the legal name.

The following shall be considered:

Name of the exchange market for exchanged traded derivatives; or

Name of Central Counterparty (CCP) for Over-The-Counter derivatives where they are cleared through a CCP; or