REPORT OF THE TOWN OF RUSSELL

TAX INCREMENT FINANCING (TIF) AGREEMENT

FOR THE 50 MEGAWATT RUSSELL BIOMASS PROJECT

April 2010

1

Executive Summary

Following receipt of a 20-year tax agreement proposal by Russell Biomass in January

2008 the Selectmen appointed a 5-person TIF Committee to review and negotiate

terms acceptable to the Town.1 Negotiations were held periodically to March 2010.

Under state law a Tax Increment Financing agreement (TIF) is a joint partnership

agreement among the Town, state and project applicant that guarantees the Town an

immediate and fixed tax payment stream and specified number of jobs while providing

the applicant with a predicable payment stream with lower payments in the early

years that facilitates his project loan agreement. This compares to a non-TIF tax

payment stream that does not immediately provide significant payments to the Town

until construction is complete and does not guarantee the Town jobs or tax payments

over any period of time. The TIF must be approved by Town residents through a Town

Meeting vote.

The Committee proceeded on the basis that the Town would make any agreement

conditional on the project demonstrating safe operation through the receipt of its

roughly two dozen environmental and health permit approvals. With this as a given

the Committee pursued two objectives:

1 Consider the Town’s financial situation. In summary, Russell had the lowest

tax rate in the hilltowns 25 years ago when three paper companies were

operating four mills, but Russell now has the highest tax rate with the loss

of industrial tax revenues over the last two decades. There is the prospect of

severe state revenue limitations in the foreseeable future with a steadily

increasing school system budget taking 2/3 of the Town tax revenues.

2 Negotiate the best possible agreement to lower the Town’s financial risk and

limit tax rate increases while allowing for a viable project. Specifically, the

Committee would strive to negotiate immediate financial relief for the Town,

a long-term payment guarantee and special benefits for important Town

resident needs.

In 2007 Russell Biomass initially proposed a minimum annual payment of $300,000

and a 20-year average of $600,000. At the DPU hearing in 2007 the Selectmen

testified that the increasing plant capital cost (the basis for the tax valuation) called

for higher tax payments. The full report (available on the Town web site) describes the

evolution of the negotiations and special benefits.

1The Committee members were Selectman and TIF Committee Chairman Dennis Moran, Finance Committee

Chairman Phil Winterson, Assessor Ted Gloss, ZBA Alternate and Town Moderator Illtyd Fernandez-Sierra, and

Planning Board member Jim Unger. Jim was a valuable contributor until increasing job responsibilities prompted

his resignation.

2

A summary of the final benefits negotiated is:

1 A $700,000 minimum annual payment, starting at the beginning of

construction

2 $28 million over 20 years for an average of over $1.3 million per year

3 In addition to the above payments significant non-tax financial and quality of

life benefits during construction and each operating year during the 20-year

agreement

Given the expected 50-year lifetime of the plant the Town Assessor estimates that total

tax payments will exceed $100 million over that period. The full report contains a

table comparing the 20-year TIF tax revenue stream to a non-TIF tax revenue stream

and it also contains a table showing the additional special benefits negotiated by the

TIF Committee.

During the negotiations the Committee checked the tax payments of other power

plants and other TIF agreements in Massachusetts. The final proposed Russell TIF

payment terms compare extremely favorably to other power plants and other TIFs in

the state. Comparison tables are provided in the full report.

In summary, in comparison to the benefits without a TIF, the proposed TIF agreement

provides the following:

1 Over $2 million higher payments in the first 4 years

2 Certainty of payment for 20 years with no right of Russell Biomass to contest

the payments. This will allow for higher tax relief planning because of that

certainty.

3 A predictable, increasing stream for better Town budget planning, as opposed to

a variable and sometimes decreasing stream that could occur without a TIF

4 Fairness compared to other towns and power plants

5 An additional $1 million during construction and $125,000 per operating year

for 20 years for non-tax benefits for Town recreation improvements, electric

power system reliability, Gateway School teacher conferences and after-

school busing, Main Street beautification, stove replacements to support

wintertime air quality improvements, and other community support

activities

In the final analysis no benefits will occur without the plant being built. The tax

payments will be 10 percent of the total plant operating costs. While the plant can

ultimately be financed without the TIF the fixed TIF payment stream will provide the

Town badly needed immediate payments, guaranteed payments over 20 years, special

benefits the Town would not otherwise receive and would better support the plant’s

financing plan. We believe a proper partnership balance has been struck between the

Town’s financial and residents’ needs and those of the proposed biomass plant.

3

Full Report

Following receipt of a 20-year tax agreement proposal by Russell Biomass in January 2008 the

Selectmen appointed a 5-person TIF Committee to review and negotiate terms acceptable to the

Town.2 Negotiations were held periodically to March 2010. Under state law a Tax Increment

Financing agreement (TIF) is a joint partnership agreement among the Town, state and project

applicant that guarantees the Town an immediate and fixed tax payment stream and specified

number of jobs while providing the applicant with a predicable payment stream with lower

payments in the early years that facilitates his project loan agreement. This compares to a

non-TIF tax payment stream that does not immediately provide significant payments to the

Town until construction is complete and does not guarantee the Town jobs or tax payments

over any period of time. The TIF Agreement must be approved by Town residents through a

Town Meeting vote.

The Committee proceeded on the basis that the Town would make any Town Meeting vote to

approve the TIF agreement conditional on the project demonstrating safe operation through the

receipt of its more than two dozen environmental and health permit approvals (see attached list

of permits). It was not part of the charter of this Committee to determine whether this would

occur, and with this report the Committee is not making any representation about the plant

design and safety. That is up to the several permitting agencies to decide and also the courts

with respect to any permit appeals. Rather, the Committee’s job was to negotiate the best

possible agreement for the Town if the environmental and health impacts of the biomass plant

were ultimately deemed acceptable.

With the safe design and permit receipts as a firm and absolute condition given the Committee

pursued two objectives:

1 Consider the Town’s financial situation. 25 years ago Russell had the lowest tax rate in

the hilltowns at a time when three paper companies were operating four mills. Russell

now has the highest tax mil rate in the hilltowns (see attached table of tax mil rates in

the hilltowns) because of the loss of industrial tax revenues over the last two decades.

And importantly for the Town, there is the prospect of severe state revenue limitations

in the foreseeable future with a steadily increasing school system budget taking 2/3 of

the Town tax revenues.

2 Negotiate the best possible agreement to lower the Town’s financial risk and limit tax

rate increases while allowing for a viable project. Specifically, the Committee would

strive to negotiate immediate financial relief for the Town, a long-term payment

guarantee and special benefits for important Town resident needs. Because of the

severe pressure on the Town revenues and budget there would be particular value to

substantial immediate financial relief for the Town.

2The Committee was composed of five members – Selectman and TIF Committee Chairman Dennis Moran, Town

Finance Committee Chairman Phil Winterson, Town Assessor Ted Gloss, ZBA Alternate and Town Moderator Illtyd

Fernandez –Sierra and Planning Board member Jim Unger. Jim was a valuable contributor to the process until

increasing job responsibilities prompted his resignation.

4

We first describe the history and outcome of the TIF negotiations. In 2007, prior to their formal

TIF proposal, Russell Biomass initially proposed a minimum annual payment of $300,000 and

a 20-year average of $600,000. At the DPU hearing in 2007 the Selectmen testified that the

increasing plant capital cost (the basis for the tax valuation) called for higher tax payments. In

January 2008 Russell Biomass submitted a revised proposal with increased payment

guarantees – a minimum of $400,000 in the early years, with a 20-year total of $20 million, or

an annual average of $1.0 million. Negotiations then took place over the following 2 years with

a particular focus on (a) the up-front payment amount for the Town and (b) the special resident

benefits for social services, recreation and other Town priorities.

A summary of the final benefits negotiated and proposed to the Town is outlined below:

1 A $700,000 minimum annual payment, starting immediately at the beginning of

construction

2 $28 million over 20 years for an average of over $1.3 million per year. This compares to

current property tax revenues of $2.5 million.

3 In addition to the above payments special non-tax benefits of $1 million during

construction and $125,000 per year during the 20-year agreement

Given the expected 50-year lifetime of the biomass plant the Town Assessor estimates total tax

payments of more than $100 million over that period.

Under the TIF the value of the real property taxable assessment is estimated at $72 million of

the $165 million estimated plant capital costs, against which a percentage exemption averaging

28 percent is applied over 20 years. For comparison a table is attached showing the assessed

value of the twelve largest taxpayers in Russell.

Attached to this report are three summary tables: (1) a table showing a summary of TIF tax

benefits and the value of these benefits on a per-household basis, (2) a table showing a 20-year

comparison of TIF versus non-TIF tax payments and (3) a table showing the special additional

non-tax financial and other benefits negotiated by the Committee.

To provide a basis for Town residents to judge the proposed TIF agreement we comment further

in the rest of this report on how the agreement compares to tax payments without a TIF, the

value of the certain, guaranteed stream of increasing payments, how the TIF compares to other

state power plants and other Town TIFs (i.e., its fairness) and what non-financial benefits the

TIF would provide.

To provide a perspective for the final benefits outlined above the key points of comparison of

the proposed TIF agreement that would not occur without a TIF are:

1 An immediate tax payment of $700,000 upon construction start

2 Over $2 million higher tax payments in the first 4 years

3 Certainty of payment for 20 years with no right of Russell Biomass to contest the

payments. This will allow for higher tax relief planning because of that certainty.

5

4 A predictable, increasing stream for better Town budget planning, as opposed to a

variable and sometimes decreasing stream that could occur without a TIF

5 Fairness compared to other towns and power plants

6 An additional $1 million during construction and $125,000 per operating year for 20

years for non-tax benefits for Town recreation improvements, electric power system

reliability, Gateway School teacher conferences and after-school busing, Main Street

beautification, stove replacements to support wintertime air quality improvements, and

other community support activities

Beyond the absolute amount of the tax payments there will be special value to the Town from

the guaranteed certainty and the guaranteed annual increases in the 20-year payment stream.

First, this will allow for higher tax relief planning because of that certainty – i.e., any tax relief

decision must assume the minimum assured tax payment so that the budget will be covered

for certain. Second, a predictable, increasing stream will allow better planning for the

inevitable increases in the Town budget, as opposed to a variable and sometimes decreasing

stream that could occur without a TIF. Also, with fixed, guaranteed payments there will no

right of Russell Biomass to contest the payments during the 20-year agreement period.

Regardless of the amount or guaranteed nature of the TIF payments there is the need for the

agreement to be fair to the Town compared to tax agreements for other power plants in the

state and other TIF agreements in the state.

The proposed Russell TIF payment terms compare extremely favorably to other power plants

and other TIFs in the state. The attached table showing comparable power plant tax

assessments on a per-megawatt shows that the negotiated Russell Biomass plant tax payments

would be 2 to 4 times higher per megawatt than other Massachusetts power plants. As an

historic comparison within Russell the former Westfield River Paper Company paid $50,000 per

year in taxes, or less than 1/20th of the proposed Russell Biomass plant tax payments.

Currently, the Texon plant pays $15,000 per year in taxes.

For a comparison to other TIFs see the attached list of over 20 Westfield TIFs, 90 percent of

which provide greater tax exemptions to the applicant than the proposed Russell TIF. Under

the state TIF property tax program there is a percentage exemption of the taxes applicable to

real property. For reference the proposed percentage exemption for the Russell Biomass plant

is a maximum of 62 percent in four of the early years and averages 28 percent for the 20-year

period. You will note in the table showing the Westfield TIFs that, for 90 percent of the

agreements (ranging from 5 to 12 years) the percentage exemption averages much more than

28 percent. The most current project in Westfield is the proposed 400 MW gas-fired plant,

which has recently had a tax agreement approved that reduces the taxes the plant would pay

by $100 million over 15 years, or more than half of what they would otherwise pay. See the

attached Boston Globe article on the Westfield plant.

Another instructive comparison to Westfield is the tax revenues per capita. Adjusting for the

population of Westfield and Russell the proposed Russell Biomass tax revenues per resident of

Russell are 15 times those of Westfield gas-fired plant for Westfield residents.

6

Then there are other important factors to consider - the qualitative benefits to the Town that

cannot be measured in dollar terms alone. The Committee paid particular attention to a

number of Town needs that currently suffer from lack of funding. Referring to the attached

table of special additional non-tax benefits several of these benefits support:

Improved quality of Town services across the board from a stronger financial position

Improvements along Main Street from (a) the relocation of the RMLD maintenance

building and the highway department to land near the Town transfer station at the end of

Frog Hollow Road, and (b) Main Street beautification improvements. This will create a

more appealing Town Center.

Town recreation and community activities support as shown in the attached special

additional non-tax benefits table

After-school athletic team busing and special teacher development programs not covered

in the normal budget

An annual college scholarship for one or more Russell students

Improved electric power system reliability

Reduced electric power costs by 2 cents per kWh for the first 400 kWh for all RMLD

customers

School activities not covered under the normal school budget

Reduced wintertime air pollution from the free replacement of older wood stoves with

clean-burning pellet wood stoves, as well as reduced pellet costs from wholesale

purchases and redistribution to all pellet wood stove owners.

Job and family income for Russell residents who obtain jobs from the biomass plant.

Under the TIF agreement the 50 construction and 22 permanent operating jobs and job

training would be preferential for Russell residents and a legal obligation of Russell

Biomass.

The above quality of life and air quality health improvements offer a value that each resident

must judge for himself or herself. In addition, there was a special localized issue that was

brought to the attention of the Committee in later 2009 – the concern over property value

impacts from the plant trucking traffic on residences on Frog Hollow Road, River Street and the

corners of the intersection of Frog Hollow Road and Main Street. The Committee directed

Russell Biomass to respond to this concern, and a provision was put into the TIF Agreement

requiring Russell Biomass to fund any shortfall in property sale proceeds within 4 years after

construction start for any of these residences that sold for less than its highest assessed value.

At some point after the Russell special permit and site plan review permitting processes are

completed later this year there will be a public information meeting in which the TIF will be

presented and resident questions answered. Following this a Town Meeting will be held to

obtain a public vote on whether or not to approve the agreement.

The full TIF agreement is available for inspection in the Town Hall.

7

In the final analysis no benefits will occur without the plant being built. Because the tax

payments will be 10 percent of the total plant operating costs the plant may ultimately be

financed without the TIF, but the fixed TIF payment stream will better support the plant’s

financing plan and will provide payment certainty and special benefits the Town would not

otherwise receive. We believe a proper partnership balance has been struck between the

Town’s financial needs and those of the proposed biomass plant.

Submitted to the Town residents of Russell by:

Dennis Moran – Selectman and TIF Committee Chairman

Phil Winterson – Russell Finance Committee Chairman

Ted Gloss – Town Assessor

Illtyd Fernandez-Sierra – ZBA Alternate and Town Moderator

8

Required Permits and Approvals for the Russell Biomass Project

PermitRegulatory

Agency

Permits Required Prior to Construction Financing

1 Major Comprehensive Plan Approval

Generation Facility – Air and Noise

Massachusetts

Department of

Environmental

Protection (MADEP)

2 Environmental Impact Review

Generation Facility and Transmission

Facilities

Massachusetts

Environmental Policy

Act (MEPA)

3 Special Permit

Generation Facility

Town of Russell

Zoning Board of

Appeals/ Planning

Board

4 Water Management Act (WMA)

WMA Order to Complete

Generation Facility

MADEP

5 Chapter 91 - Request for Determination of

Applicability

Generation Facility

MADEP

6 National Pollution Discharge Elimination

System (NPDES) Individual Permit

Generation Facility

MADEP/ United

States Environmental

Protection Agency

(USEPA)

7 Request for Interconnection for a Large

Generating Facility

Transmission Facilities

Independent System

Operator – New

England (ISO-NE)

8 Petition for Approval of Construction/ Section

72 Petition/ Petition for Zoning Exemption

Transmission Facilities

Energy Facility Siting

Board (EFSB)

9 Petition for Zoning Exemption

Generation Facility

Dept. of Public

Utilities (DPU)

10 Authorization to Access

Transmission Facilities

Massachusetts

Turnpike Authority

11 Water Quality Certification

Section 401 Clean Water Act

Generation Facility and Transmission

Facilities and Frog Hollow Road Extension

(FHX)

MADEP

12 Programmatic General Permit/Individual

Permit

Section 404 Clean Water Act

Generation Facility and Transmission

Facilities and FHX

Army Corps of

Engineers (ACOE)

13 Orders of Resource Area Delineation

Generation Facility and Transmission

Facilities

Russell, Montgomery,

Westfield

Conservation

Commissions and

MADEP

9

PermitRegulatory

Agency

4A Orders of Conditions

Generation Facility

Russell Conservation

Commission and

MADEP

14B Orders of Conditions

Transmission Facilities

Russell Conservation

Commission and

MADEP

14C Orders of Conditions

FHX

Russell Conservation

Commission and

MADEP

15 Orders of Conditions

Transmission Facilities

Westfield

Conservation

Commission and

MADEP

16A Determination of No Adverse Impact / Take

Generation Facility and Transmission

Facilities

NHESP/Massachuset

ts Division of

Fisheries and Wildlife

(DFW)

16B Determination of No Adverse Impact / Take

including FHX

NHESP/Massachuset

ts Division of

Fisheries and Wildlife

(DFW)

17 Conservation and Management Permit

Generation Facility and Transmission

Facilities and FHX

NHESP/DFW

18 Permit to Access State Highway at Main

Street/Route 20

Generation Facility and FHX

Massachusetts

Highway Department

19 Determination of No Adverse Impact

Generation Facility and Transmission

Facilities and FHX

MHC

20 Article 97

Transmission Facilities

MA Legislature

21 Russell Special Permit - Amendment

Generation Facility to include FHX as access

Russell Zoning Board

of Appeals

22 Russell Site Plan Review

Generation Facility to include FHX as access

Russell Planning

Board

23 Russell Special Permit for Earth Removal

Generation Facility

Russell Zoning Board

of Appeals

24 Russell Site Plan Review

Transmission Facilities

Russell Planning

Board

25 Russell Special Permit for Earth Removal

Transmission Facilities

Russell Zoning Board

of Appeals

26 Westfield Zoning Permit

Transmission Facilities

Zoning Enforcement

Officer

27 Westfield Building/Structure Height and

Stormwater Management Special Permit

Westfield Planning

Board

10

Required Permits and Approvals for the Russell Biomass Project

Permit Regulatory Agency

Permits to be Submitted Post Construction Financing

and Design

28 NPDES Notice of Intent (NOI) to be

covered under the General Permit for

Stormwater Discharges from

Construction Activities, Storm Water

Pollution Prevention Plan (SWPPP)

Generation Facility and Transmission

Facilities

USEPA

29 Subsurface Sewage Disposal Works

Permits

Generation Facility and Transmission

Facilities

Russell and Westfield Boards of

Health

30 Stack Registration

Generation Facility

Federal Aviation Administration

(FAA)

31 Transmission Line Structure

Registration

Transmission Facilities

Federal Aviation Administration

(FAA)

32 Fuel Oil Tank Permits (requires final

design)

Generation Facility

State Fire Marshal/Local Fire

Department

33 Use Permit Under 502 (requires final

design)

Generation Facility

State Fire Marshal/Local Fire

Department for ammonia and fuel

oil storage tanks

34 Permit for Construction Related

Activities and Traffic Management

Transmission Facilities

Massachusetts Turnpike

Authority

35 Building Permits

Generation Facility, Transmission

Facilities and FHX

Russell, Montgomery, Westfield

Building Inspectors

State Building Code

36 Beneficial Use Determination (BUD)

(ash reuse)

Generation Facility

MADEP

11

Single Family Assessed Value/Single Family Parcels)* Residential Tax Rate/1000

* Average single family tax bills are calculated by dividing the (single family assessed value by

the single family parcels) for each community and then multiplying the average value by the

residential tax rate and dividing by one thousand.

Massachusetts Department of Revenue

Division of Local Services

Municipal Databank/Local Aid Section

Fiscal Year 2009 Average Single Family Tax Bill

DORCode Municipality

AssessedValue Parcels

AverageValue

TaxRate

SingleFamilyTax Bill

256 RUSSELL 105,876,020 527 200,903 17.16 3,447

059 CHESTER 85,679,000 489 175,213 16.33 2,861

183 MIDDLEFIELD 37,272,500 195 191,141 15.59 2,980

331 WESTHAMPTON 194,420,000 643 302,364 13.98 4,227

329 WESTFIELD 2,230,402,000 9,281 240,319 13.94 3,350

194 MONTGOMERY 76,590,800 314 243,920 13.20 3,220

143 HUNTINGTON 147,766,500 734 201,317 13.17 2,651

033 BLANDFORD 115,887,600 521 222,433 12.92 2,874

313 WASHINGTON 47,668,900 248 192,213 12.86 2,472

279 SOUTHWICK 775,154,300 2,988 259,422 12.55 3,256

112 GRANVILLE 146,910,800 566 259,560 11.00 2,855

260 SANDISFIELD 162,469,700 583 278,679 8.96 2,497

022 BECKET 415,310,100 1,676 247,798 7.98 1,977

225 OTIS 477,843,200 1,512 316,034 6.39 2,019

297 TOLLAND 154,682,400 488 316,972 4.64 1,471

Total 5,173,933,820 20,765 249,166

Largest Taxpayers in the Town of Russell - 2010

Name Assessment

1. Westfield Paper Lands, LLC $2,555,5002. Thomas O’Brien 1,130,2003. Texon 953,8004. Littleville Power 950,8005. Woronoco Power 806,3006. Lucier Family Trust 787,4007. Oleksak Trust 780,1208. Russell Land Company 706,4009. John Kurtz 586,70010.Howard Noe 540,70011.Howard Freedman 522,70012.B&N Lands, LLC 467,715

12

13

Additional TIF Benefits beyond Tax Payments (1)

14

Additional TIF Benefits beyond Tax Payments (2)

15

Property and Taxes – Other Massachusetts Power Plants - 2007

16

WESTFIELD TIF AGREEMENTS (1)

Shaded numbers are percent of real property tax exemptions by year

Old Colony Envelope, Inc. (MFG/paper, allied products) (12/96)

TIF (10 years, 100-75-50-25-25-25-20-15-10-5)

18 new jobs; 400 jobs retained; $6 million in investment

Angy's Food Products, Inc. (MFG/food and kindred products) (12/96)

TIF (5 years, 80-75-50-50-40)

8 new jobs; 32 jobs retained; $2.6 million in investment

Advance Mfg Co., Inc. (MFG/machinery, except electrical) (3/97)

TIF Tax Increment Financing, (5 years, 80-75-50-50-40)

10 new jobs; 176 jobs retained; $2.6 million in private investment

Jen-Coat, Inc. (2 Projects) (MFG/paper, allied products) (12/97)

TIF Two 10 year TIFs (50% per year)35 new jobs; 202 jobs retained; $4.5 million in private investment

Toys “R” Us Mass., Inc. (SERVICES/retail) (12/97)

TIF (12 yrs, 60-50-50-40-40-40-40-40-40-40-40-40)

28 new jobs; 172 jobs retained; $30 million in private investment

The Caldor Corporation (SERVICES/retail) (1/98)

TIF (10 years, 5-5-5-5-5-2-2-2-2-2)

30 new jobs; 290 jobs retained; $212,000 in private investment

Lawry Freight System, Inc. (SERVICES/transportation) (8/98)

TIF (5 yrs, 80-75-50-50-40)

new jobs; 18 jobs retained; $1 million in private investment

Finishing Solutions (SERVICES/commercial) (6/99)

10-year TIF (80-75-50-50-40-40-30-30-20-10)

20 new jobs; 3 jobs retained; $400,000 in private investment

Westek Architectural Woodworking Co Inc. (MFG/lumber/wood products) (6/99)

10-year TIF (80-75-50-50-40-40-30-30-20-10)

5 new jobs; 10 jobs retained; $920,000 in private investment

DBLS Realty, LLC/Millrite Machine (11/01)

5 year STA ()

8 jobs created, 35 jobs retained, $2,240,000 in private investment

94 North Elm Street/Ronald E. Schortmann (12/02)

STA (To be determined)

30 jobs created, $5,000,000 in private investment

Electric Motor Service & Sales, Inc (11/03)

5 year TIF (80- 75- 50- 50- 40)

2 jobs created, 9 jobs retained, $750,000 in private investment

17

WESTFIELD TIF AGREEMENTS (2)

Shaded numbers are percent of real property tax exemptions by year

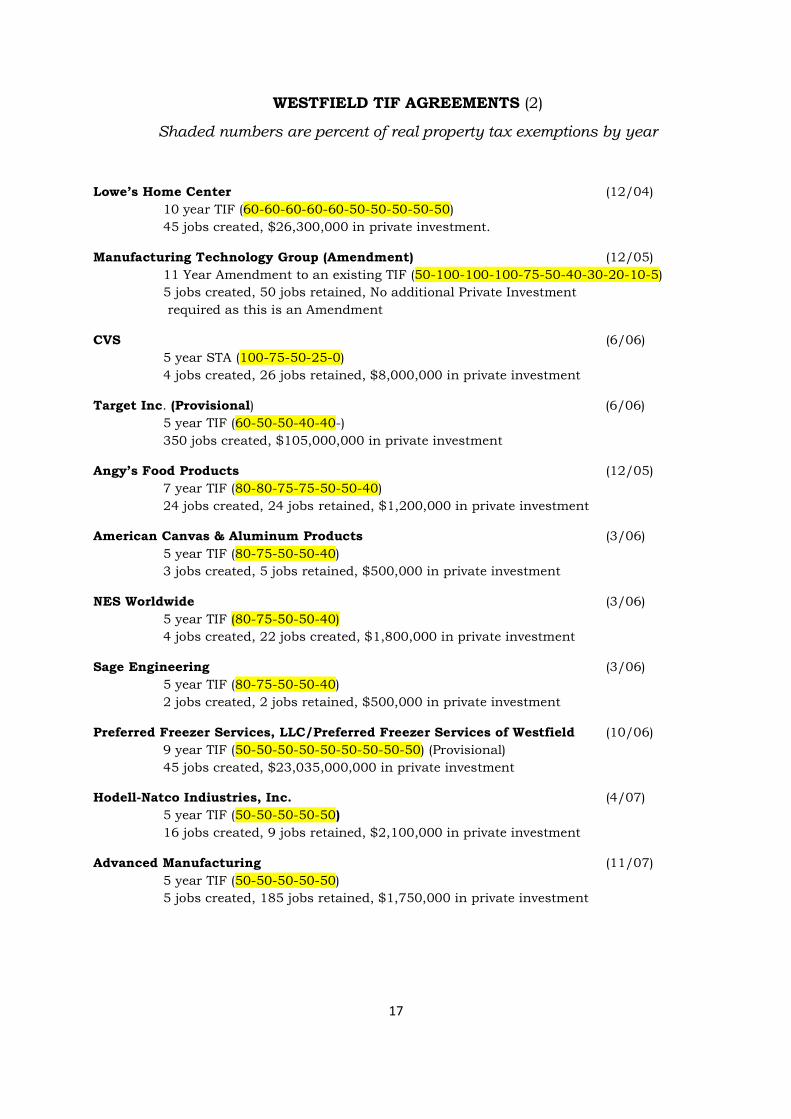

Lowe’s Home Center (12/04)

10 year TIF (60-60-60-60-60-50-50-50-50-50)

45 jobs created, $26,300,000 in private investment.

Manufacturing Technology Group (Amendment) (12/05)

11 Year Amendment to an existing TIF (50-100-100-100-75-50-40-30-20-10-5)

5 jobs created, 50 jobs retained, No additional Private Investment

required as this is an Amendment

CVS (6/06)

5 year STA (100-75-50-25-0)

4 jobs created, 26 jobs retained, $8,000,000 in private investment

Target Inc. (Provisional) (6/06)

5 year TIF (60-50-50-40-40-)

350 jobs created, $105,000,000 in private investment

Angy’s Food Products (12/05)

7 year TIF (80-80-75-75-50-50-40)

24 jobs created, 24 jobs retained, $1,200,000 in private investment

American Canvas & Aluminum Products (3/06)

5 year TIF (80-75-50-50-40)

3 jobs created, 5 jobs retained, $500,000 in private investment

NES Worldwide (3/06)

5 year TIF (80-75-50-50-40)

4 jobs created, 22 jobs created, $1,800,000 in private investment

Sage Engineering (3/06)

5 year TIF (80-75-50-50-40)

2 jobs created, 2 jobs retained, $500,000 in private investment

Preferred Freezer Services, LLC/Preferred Freezer Services of Westfield (10/06)

9 year TIF (50-50-50-50-50-50-50-50-50) (Provisional)

45 jobs created, $23,035,000,000 in private investment

Hodell-Natco Indiustries, Inc. (4/07)

5 year TIF (50-50-50-50-50)

16 jobs created, 9 jobs retained, $2,100,000 in private investment

Advanced Manufacturing (11/07)

5 year TIF (50-50-50-50-50)

5 jobs created, 185 jobs retained, $1,750,000 in private investment

18

Power plant gets $100m breakWestfield shaves property taxesBy Todd Wallack, Globe Staff | April 2, 2010

It turns out Liberty Mutual Insurance Co.’s $38.5 million tax break wasn’t the largest one approved by astate economic development board on Wednesday after all.

According to documents released after the board meeting, the Economic Assistance CoordinatingCouncil also ratified a $100 million tax break for a new power plant in Westfield — bigger than the taxbreaks given to Bristol-Myers Squibb Co., Liberty Mutual, and some other major employers that arebuilding large facilities in Massachusetts.

But unlike the Liberty Mutual and Bristol-Myers deals, only a sliver of the subsidy is coming from statetaxpayers.

As previously reported, the state gave the Pioneer Valley Energy Center $320,000 in state tax credits tobuild the $426 million plant, which will use natural gas to generate up to 400 megawatts of electricity.But Westfield also offered the company a 15-year deal that would shave the plant owner’s local propertytaxes by more than half. The net worth of that reduction is $99.5 million, documents show.

The company behind the Westfield plant is a subsidiary of Energy Management Inc., the Boston powercompany that is trying to build Cape Wind, the wind-turbine farm in Nantucket Sound.

Larry Smith, the city’s director of community development, said Westfield hired a consultant to figure outhow large an incentive it needed to offer to entice the developer to build there. Smith said it is commonfor power plants to receive large incentives, because the plants require huge amounts of investmentand generally face steep taxes on their equipment.

Even with the large tax incentive, Westfield said it will still come out ahead. The city will net nearly $2.5million in additional revenue, a substantial amount for a community its size. The site location is currentlyempty and generates little tax revenue.

“Something is better than nothing,’’ said State Representative Donald F. Humason, a Republican fromWestfield. “This was a fairly competitive siting process, and the principals had several other options.’’

Matt Palmer, the project manager for the Westfield plant, said the company would have been forced tofind an alternate site in another city without the aid.

“The project simply wouldn’t have been viable,’’ Palmer said. “When you add that kind of tax burden, theproject makes no sense.’’

The company plans to begin construction late this year and open in late 2013, creating 200 constructionjobs and 16 permanent full-time jobs. Palmer said it will be the city’s largest taxpayer, even with thediscount.

The power plant would have received an even larger tax break under the old rules for the EconomicDevelopment Incentive Program, which offers incentives to companies that promise to expand in targetareas.

Under the old system, when the state approved a local tax break, it automatically chipped in a state taxbreak worth 5 percent of the company’s investment. In the case of the Westfield plant, that would workout to $21 million, or $1.3 million per job.

But a new law gave state officials more discretion over the size of the award starting this year. In thiscase, the council offered state tax breaks worth $20,000 per job.

Overall on Wednesday, the council approved tax breaks to eight companies potentially worth $27million off their state taxes, and an estimated $124 million off their local property taxes.

Todd Wallack can be reached at [email protected].