Underwriting Guideline Matrix

Subject to Change Without Notice – Valid as of: 1/16/2018

Copyright © 2017 Skyline Financial Corp. dba NewLeaf Wholesale, Nationwide Mortgage Licensing System (NMLS) Company ID# 12072. Arizona Mortgage

Banker License #927740, Licensed by the Department of Business Oversight under the California Residential Mortgage Lending Act File No: 4130296, Colorado

Registered with Colorado Division of Real Estate, Florida Mortgage Lender/Servicer License No. MLD947 issued by the Florida Office of Financial Regulation,

Georgia Mortgage Lender License #42980, Hawaii Licensed by the Hawaii Division of Financial Institutions No. HI-12072, Idaho Licensed by the Idaho

Department of Finance MBL-7422, Illinois Residential Mortgage License # MB.6761108, Louisiana Residential Mortgage Lending License, Nebraska Mortgage

Bank License, New Jersey Residential Mortgage Lender License, New Mexico Financial Institutions Division, Registered Mortgage Company License # 01653,

Oregon Mortgage Lender License ML-2797, South Carolina Mortgage Lender / Servicer License MLS #12072, Tennessee Mortgage License #108815, Texas

NewLeaf 1: DU-LP Conforming & High Balance Fixed Rate

Program / Product Codes:

Conforming: NewLeaf 1 – 30 Year Fixed (W101) NewLeaf 1 – 20 Year Fixed (W102) NewLeaf 1 – 15 Year Fixed (W113) NewLeaf 1 – 10 Year Fixed (W114) NewLeaf 1 – 30 Year Fixed LPMI (W143) NewLeaf 1 – 20 Year Fixed LPMI (W144) NewLeaf 1 – 15 Year Fixed LPMI (W145) NewLeaf 1 – 10 Year Fixed LPMI (W146) High Balance NewLeaf 1 HB – 30 Year Fixed (W109) NewLeaf 1 HB – 20 Year Fixed (W110) NewLeaf 1 HB – 15 Year Fixed (W121) NewLeaf 1 HB – 10 Year Fixed (W122) NewLeaf 1 HB LPMI – 30 Year Fixed (W125) NewLeaf 1 HB LPMI – 20 Year Fixed (W126) NewLeaf 1 HB LPMI – 15 Year Fixed (W127) NewLeaf 1 HB LPMI – 10 Year Fixed (W128)

www.NewLeafWholesale.com

(V5-17) Page 1 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Registered with Texas Department of Savings and Mortgage Lending, Utah Licensed by the Division of Real Estate License # 5318719, Virginia Lender License

MC-5861, Washington Consumer Loan Company License CL-12072. This is a business to business communication intended for Real Estate and Lending

Professionals only. Refer to www.nmlsconsumer.org and input NMLS #12072 to see where Skyline Financial Corp. is a licensed lender.

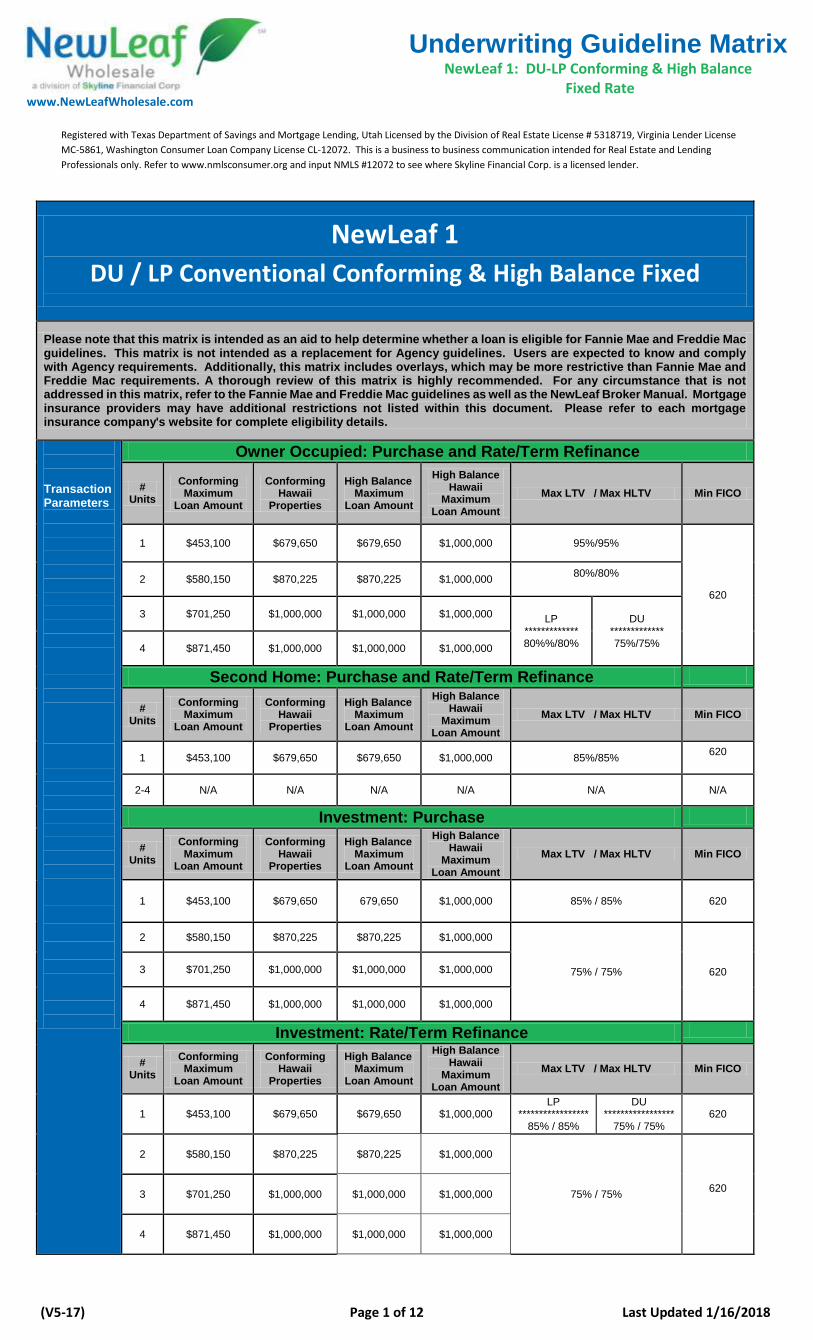

NewLeaf 1

DU / LP Conventional Conforming & High Balance Fixed

Please note that this matrix is intended as an aid to help determine whether a loan is eligible for Fannie Mae and Freddie Mac guidelines. This matrix is not intended as a replacement for Agency guidelines. Users are expected to know and comply with Agency requirements. Additionally, this matrix includes overlays, which may be more restrictive than Fannie Mae and Freddie Mac requirements. A thorough review of this matrix is highly recommended. For any circumstance that is not addressed in this matrix, refer to the Fannie Mae and Freddie Mac guidelines as well as the NewLeaf Broker Manual. Mortgage insurance providers may have additional restrictions not listed within this document. Please refer to each mortgage insurance company's website for complete eligibility details.

Transaction Parameters

Owner Occupied: Purchase and Rate/Term Refinance

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 $679,650 $1,000,000 95%/95%

620

2 $580,150 $870,225 $870,225 $1,000,000 80%/80%

3 $701,250 $1,000,000 $1,000,000 $1,000,000 LP ************* 80%%/80%

DU ************* 75%/75% 4 $871,450 $1,000,000 $1,000,000 $1,000,000

Second Home: Purchase and Rate/Term Refinance 1,202,925 1,804,375

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 $679,650 $1,000,000 85%/85% 620

2-4 N/A N/A N/A N/A N/A N/A

Investment: Purchase

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 679,650 $1,000,000 85% / 85%

620

2 $580,150 $870,225 $870,225 $1,000,000

75% / 75%

620

3 $701,250 $1,000,000 $1,000,000 $1,000,000

4 $871,450 $1,000,000 $1,000,000 $1,000,000

Investment: Rate/Term Refinance

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 $679,650 $1,000,000 LP

*****************85% / 85%

DU *****************

75% / 75%

620

2 $580,150 $870,225 $870,225 $1,000,000

75% / 75% 620

3 $701,250 $1,000,000 $1,000,000 $1,000,000

4 $871,450 $1,000,000 $1,000,000 $1,000,000

www.NewLeafWholesale.com

(V5-17) Page 2 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

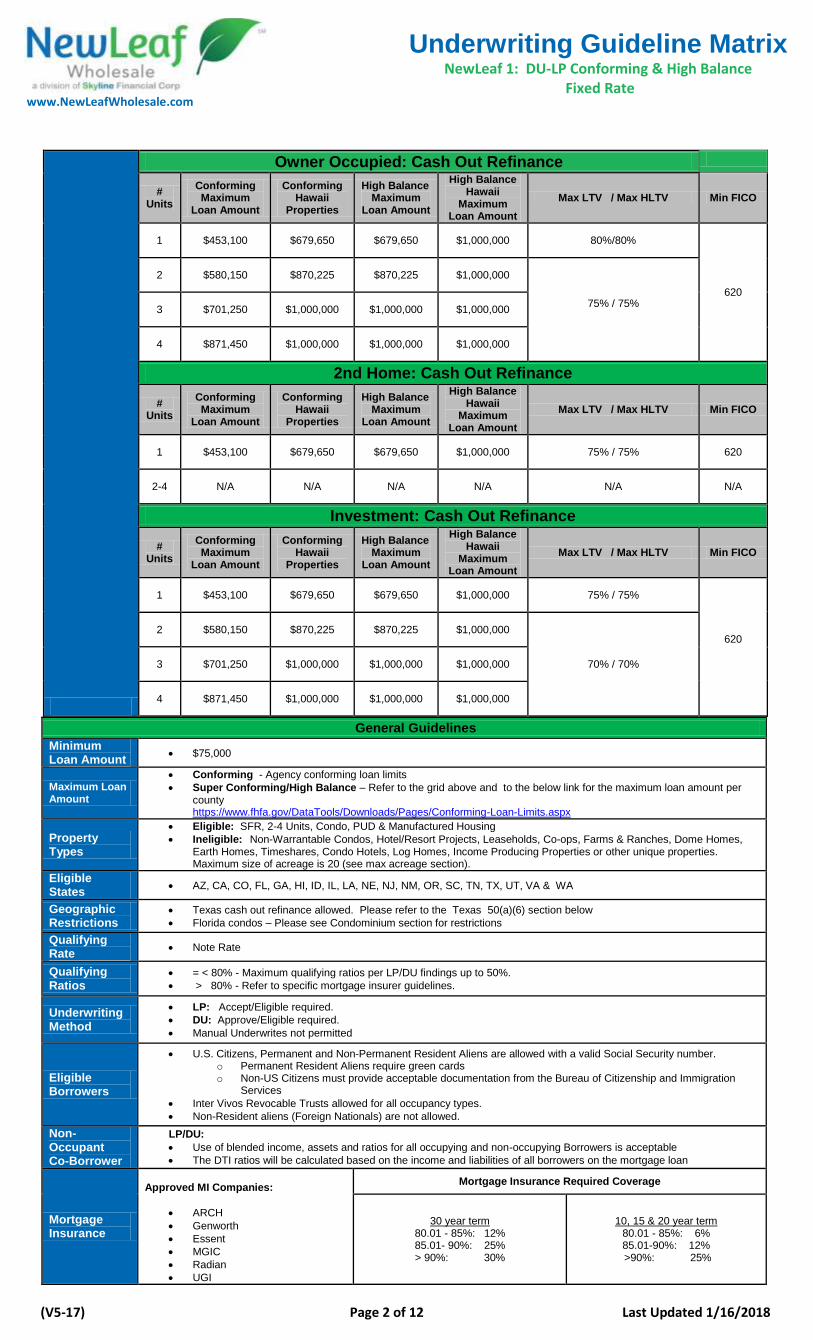

General Guidelines

Minimum Loan Amount

$75,000

Maximum Loan Amount

Conforming - Agency conforming loan limits

Super Conforming/High Balance – Refer to the grid above and to the below link for the maximum loan amount per county https://www.fhfa.gov/DataTools/Downloads/Pages/Conforming-Loan-Limits.aspx

Property Types

Eligible: SFR, 2-4 Units, Condo, PUD & Manufactured Housing

Ineligible: Non-Warrantable Condos, Hotel/Resort Projects, Leaseholds, Co-ops, Farms & Ranches, Dome Homes, Earth Homes, Timeshares, Condo Hotels, Log Homes, Income Producing Properties or other unique properties. Maximum size of acreage is 20 (see max acreage section).

Eligible States

AZ, CA, CO, FL, GA, HI, ID, IL, LA, NE, NJ, NM, OR, SC, TN, TX, UT, VA & WA

Geographic Restrictions

Texas cash out refinance allowed. Please refer to the Texas 50(a)(6) section below

Florida condos – Please see Condominium section for restrictions

Qualifying Rate

Note Rate

Qualifying Ratios

= < 80% - Maximum qualifying ratios per LP/DU findings up to 50%.

> 80% - Refer to specific mortgage insurer guidelines.

Underwriting Method

LP: Accept/Eligible required.

DU: Approve/Eligible required.

Manual Underwrites not permitted

Eligible Borrowers

U.S. Citizens, Permanent and Non-Permanent Resident Aliens are allowed with a valid Social Security number. o Permanent Resident Aliens require green cards o Non-US Citizens must provide acceptable documentation from the Bureau of Citizenship and Immigration

Services

Inter Vivos Revocable Trusts allowed for all occupancy types.

Non-Resident aliens (Foreign Nationals) are not allowed.

Non-Occupant Co-Borrower

LP/DU:

Use of blended income, assets and ratios for all occupying and non-occupying Borrowers is acceptable

The DTI ratios will be calculated based on the income and liabilities of all borrowers on the mortgage loan

Mortgage Insurance

Approved MI Companies:

ARCH

Genworth

Essent

MGIC

Radian

UGI

Mortgage Insurance Required Coverage

30 year term 80.01 - 85%: 12% 85.01- 90%: 25% > 90%: 30%

10, 15 & 20 year term 80.01 - 85%: 6% 85.01-90%: 12% >90%: 25%

Owner Occupied: Cash Out Refinance

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 $679,650 $1,000,000 80%/80%

620

2 $580,150 $870,225 $870,225 $1,000,000

75% / 75%

3 $701,250 $1,000,000 $1,000,000 $1,000,000

4 $871,450 $1,000,000 $1,000,000 $1,000,000

2nd Home: Cash Out Refinance

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 $679,650 $1,000,000 75% / 75% 620

2-4 N/A N/A N/A N/A N/A N/A

Investment: Cash Out Refinance

# Units

Conforming Maximum

Loan Amount

Conforming Hawaii

Properties

High Balance Maximum

Loan Amount

High Balance Hawaii

Maximum Loan Amount

Max LTV / Max HLTV Min FICO

1 $453,100 $679,650 $679,650 $1,000,000 75% / 75%

620

2 $580,150 $870,225 $870,225 $1,000,000

70% / 70% 3 $701,250 $1,000,000 $1,000,000 $1,000,000

4 $871,450 $1,000,000 $1,000,000 $1,000,000

www.NewLeafWholesale.com

(V5-17) Page 3 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

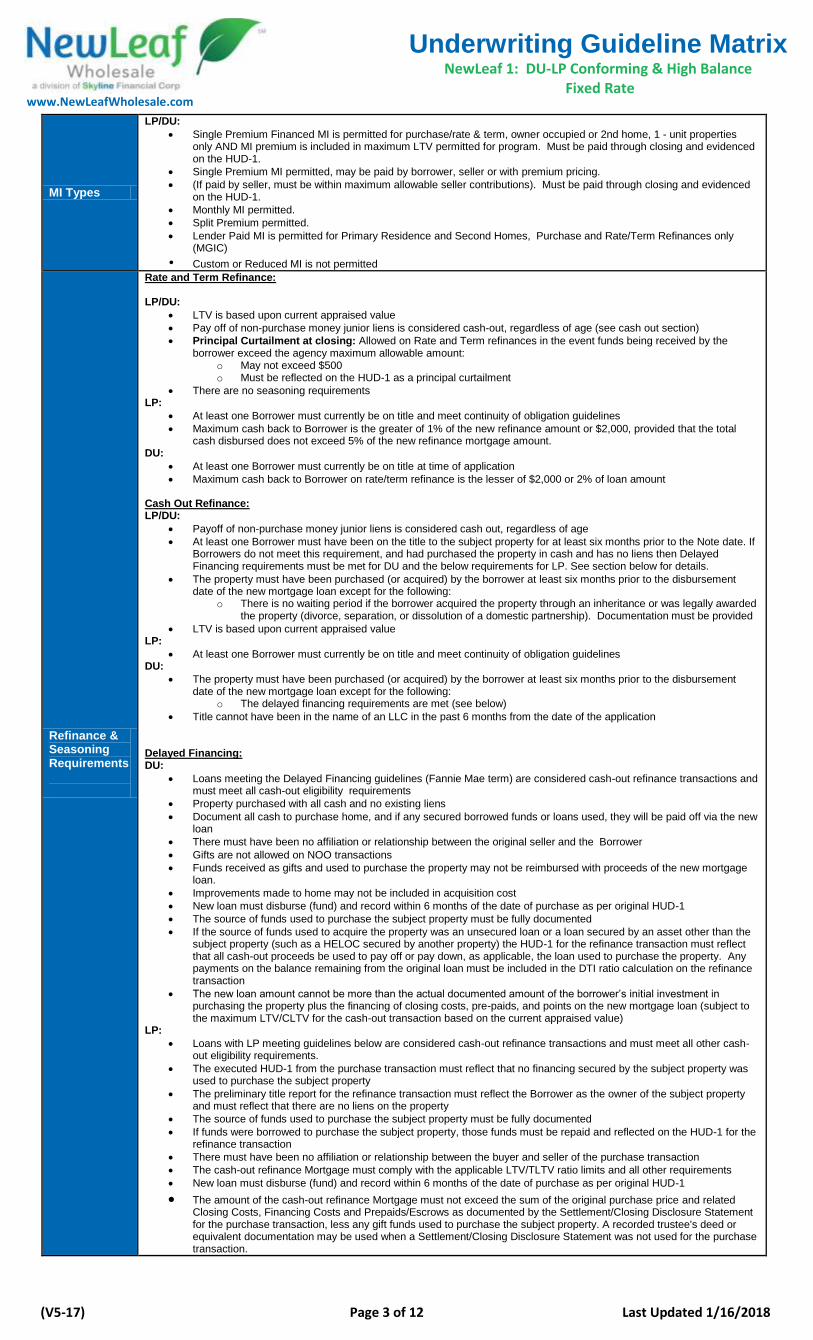

MI Types

LP/DU:

Single Premium Financed MI is permitted for purchase/rate & term, owner occupied or 2nd home, 1 - unit properties only AND MI premium is included in maximum LTV permitted for program. Must be paid through closing and evidenced on the HUD-1.

Single Premium MI permitted, may be paid by borrower, seller or with premium pricing.

(If paid by seller, must be within maximum allowable seller contributions). Must be paid through closing and evidenced on the HUD-1.

Monthly MI permitted.

Split Premium permitted.

Lender Paid MI is permitted for Primary Residence and Second Homes, Purchase and Rate/Term Refinances only (MGIC)

• Custom or Reduced MI is not permitted

Refinance & Seasoning Requirements

Rate and Term Refinance: LP/DU:

LTV is based upon current appraised value

Pay off of non-purchase money junior liens is considered cash-out, regardless of age (see cash out section)

Principal Curtailment at closing: Allowed on Rate and Term refinances in the event funds being received by the borrower exceed the agency maximum allowable amount:

o May not exceed $500 o Must be reflected on the HUD-1 as a principal curtailment

There are no seasoning requirements LP:

At least one Borrower must currently be on title and meet continuity of obligation guidelines

Maximum cash back to Borrower is the greater of 1% of the new refinance amount or $2,000, provided that the total cash disbursed does not exceed 5% of the new refinance mortgage amount.

DU:

At least one Borrower must currently be on title at time of application

Maximum cash back to Borrower on rate/term refinance is the lesser of $2,000 or 2% of loan amount

Cash Out Refinance: LP/DU:

Payoff of non-purchase money junior liens is considered cash out, regardless of age

At least one Borrower must have been on the title to the subject property for at least six months prior to the Note date. If Borrowers do not meet this requirement, and had purchased the property in cash and has no liens then Delayed Financing requirements must be met for DU and the below requirements for LP. See section below for details.

The property must have been purchased (or acquired) by the borrower at least six months prior to the disbursement date of the new mortgage loan except for the following:

o There is no waiting period if the borrower acquired the property through an inheritance or was legally awarded the property (divorce, separation, or dissolution of a domestic partnership). Documentation must be provided

LTV is based upon current appraised value LP:

At least one Borrower must currently be on title and meet continuity of obligation guidelines DU:

The property must have been purchased (or acquired) by the borrower at least six months prior to the disbursement date of the new mortgage loan except for the following:

o The delayed financing requirements are met (see below)

Title cannot have been in the name of an LLC in the past 6 months from the date of the application

Delayed Financing: DU:

Loans meeting the Delayed Financing guidelines (Fannie Mae term) are considered cash-out refinance transactions and must meet all cash-out eligibility requirements

Property purchased with all cash and no existing liens

Document all cash to purchase home, and if any secured borrowed funds or loans used, they will be paid off via the new loan

There must have been no affiliation or relationship between the original seller and the Borrower

Gifts are not allowed on NOO transactions

Funds received as gifts and used to purchase the property may not be reimbursed with proceeds of the new mortgage loan.

Improvements made to home may not be included in acquisition cost

New loan must disburse (fund) and record within 6 months of the date of purchase as per original HUD-1

The source of funds used to purchase the subject property must be fully documented

If the source of funds used to acquire the property was an unsecured loan or a loan secured by an asset other than the subject property (such as a HELOC secured by another property) the HUD-1 for the refinance transaction must reflect that all cash-out proceeds be used to pay off or pay down, as applicable, the loan used to purchase the property. Any payments on the balance remaining from the original loan must be included in the DTI ratio calculation on the refinance transaction

The new loan amount cannot be more than the actual documented amount of the borrower’s initial investment in purchasing the property plus the financing of closing costs, pre-paids, and points on the new mortgage loan (subject to the maximum LTV/CLTV for the cash-out transaction based on the current appraised value)

LP:

Loans with LP meeting guidelines below are considered cash-out refinance transactions and must meet all other cash-out eligibility requirements.

The executed HUD-1 from the purchase transaction must reflect that no financing secured by the subject property was used to purchase the subject property

The preliminary title report for the refinance transaction must reflect the Borrower as the owner of the subject property and must reflect that there are no liens on the property

The source of funds used to purchase the subject property must be fully documented

If funds were borrowed to purchase the subject property, those funds must be repaid and reflected on the HUD-1 for the refinance transaction

There must have been no affiliation or relationship between the buyer and seller of the purchase transaction

The cash-out refinance Mortgage must comply with the applicable LTV/TLTV ratio limits and all other requirements

New loan must disburse (fund) and record within 6 months of the date of purchase as per original HUD-1

The amount of the cash-out refinance Mortgage must not exceed the sum of the original purchase price and related Closing Costs, Financing Costs and Prepaids/Escrows as documented by the Settlement/Closing Disclosure Statement for the purchase transaction, less any gift funds used to purchase the subject property. A recorded trustee's deed or equivalent documentation may be used when a Settlement/Closing Disclosure Statement was not used for the purchase transaction.

www.NewLeafWholesale.com

(V5-17) Page 4 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Buying out an owner’s interest

LP: Special Purpose Cash-Out Refinance:

Special Purpose Cash-Out Refinance is a cash-out refinance where the owner of a property uses the proceeds of the refinance transaction to buy out the equity of a co-owner. The loan amount is limited to amounts used to buy out the equity and must meet the cash-out LTV/CLTV and the following requirements:

o The Borrower and co-owner must have jointly owned the property for a minimum of 12 months prior to the loan application (parties who inherited an interest in the property are exempt from this requirement)

o The Borrower and co-owner must provide evidence that they occupied the subject property as their Primary Residence (parties who inherited an interest in the property are exempt from this requirement)

o The Borrower and co-owner must provide a written agreement, signed by all parties, stating the terms of the property transfer and the disposition of the proceeds from the refinancing transaction

o The Borrower who retains sole ownership may not receive any of the proceeds from the refinance transaction DU: Refinance to Buy Out An Owner’s Interest:

A transaction that requires one owner to buy out the interest of another owner (for example, as a result of a divorce settlement or dissolution of a domestic partnership) is considered a limited cash-out refinance if the secured property was jointly owned for at least 12 months preceding the disbursement date of the new mortgage loan and must meet the following requirements:

o All parties must sign a written agreement that states the terms of the property transfer and the proposed disposition of the proceeds from the refinance transaction.

o Except in the case of recent inheritance of the subject property, documentation must be provided to indicate that the security property was jointly owned by all parties for at least 12 months preceding the disbursement date of the new mortgage loan

o Borrowers who acquire sole ownership of the property may not receive any of the proceeds from the refinance. The party buying out the other party’s interest must be able to qualify for the mortgage pursuant to Fannie Mae’s underwriting guidelines

Continuity of Obligation

LP: When an existing Mortgage will be satisfied as a result of a refinance transaction, one of the following requirements must be met:

At least one Borrower on the refinance Mortgage was a Borrower on the Mortgage being refinanced; OR

At least one Borrower on the refinance Mortgage held title to and resided in the mortgaged premises as a Primary Residence for the most recent 12 month period and the Mortgage file contains documentation evidencing that the Borrower, either:

o Has been making timely Mortgage payments, including the payments for any secondary financing, for the most recent 12-month period; OR

o Is a Related Person to a Borrower on the Mortgage being refinanced;

At least one Borrower on the refinance Mortgage inherited or was legally awarded the Mortgaged Premises by a court in the case of divorce, separation or dissolution of a domestic partnership.

The loan being refinanced and the title to the property are in the name of a natural person. Transfer of ownership from a corporation or a LLC to an individual does not meet the continuity of obligation requirement.

The borrower acquired the property through an inheritance or was legally awarded the property through a divorce, separation, or dissolution of a domestic partnership. There is no minimum waiting period with regard to when the borrower acquired the property before completing a new refinance transaction. Documentation must be provided.

DU: There are no requirements for continuity of obligation

Texas 50(a)(6)

LP/DU:

Must be determined whether the proposed refinance of a Mortgage secured by the Borrower’s homestead is a Mortgage that must be originated pursuant to Section 50(a)(6) of Article XVI of the Texas Constitution

15, 20 & 30 year terms only

Maximum LTV is the lesser of 80% or the maximum allowed per the LTV matrix above

At the time the loan is made it must not exceed an amount that, when added to the principal balances of all other liens against the subject property, is more than 80% of the fair market value

1 unit primary residences only

2-4 unit properties, investment properties and second homes are ineligible

Properties located in the state of Texas

The property is the Borrower's homestead and is a residential property, not a farm, ranch or used for any agricultural purposes

A Living Trust may be a Borrower for a Texas 50(a)(6) Mortgage if the Living Trust meets the requirements for a “qualifying trust” under Texas law for purposes of owning residential property that qualifies for the homestead exemption

The seller and the owner of the homestead must execute a written acknowledgment of the "fair market value" of the homestead property as of the date the extension of credit is made. The appraisal report must be attached to the acknowledgment.

A full appraisal is required

Maximum 10 acres

Subordinate liens are not allowed

All liens currently on title must be paid at closing

Closing costs must not exceed 3% of the loan amount

Verification from the borrower(s) that their homestead has not been used as collateral for a Texas Home Equity loan in the preceding 12 months is required

Non-Borrowing spouse must execute all documents, regardless of ownership interest

POA is not allowed on LP loans

Number of Financed Properties

LP:

Owner Occupied - No Limit

Investment/2nd Home - Borrower individually and all Borrowers collectively that are obligated on the properties may own up to six 1-4 unit financed residential properties, including the subject property provided that all guidelines are met including 6 months PITIA for the subject property (refer to Reserve Section for guidelines). When a borrower is not obligated, those properties do not need to be considered in the maximum number and are not required to meet the additional reserves requirements

For properties in the name of an LLC, it is not counted in the maximum number if the mortgage is not reflected on the Borrower’s personal credit.

DU:

Owner Occupied - No Limit

Investment/2nd Home - Borrower individually and all Borrowers collectively may own up to six (6) 1-4 unit financed residential properties, including the subject property. (See Reserve section for requirements)

Definition of ownership is a residential 1-4 unit property with a mortgage for which the borrower is personally obligated

All financed properties, including the subject property must not exceed $2 million in loan amount exposure to New Leaf. If 7-10 properties owned, refer to DU only Programs W103, W104, W115, and W116.

Age of Credit/Apprai

Credit documents, including but not limited to, credit reports, income, assets, and title documentation cannot exceed 90 days from the Note Date

See the Collateral section for Appraisals

www.NewLeafWholesale.com

(V5-17) Page 5 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

sal Documents

Power Of Attorney

Permitted on Purchase and Rate Term Refinances

Not allowed on Cash-Out transactions

PACE

LP:

PACE loans are not allowed to be subordinated

PACE loans may be paid off through a cash-out transaction

PACE loans may be paid off through a rate term refinance for Freddie Mac owned loans only

Link to the Lookup website: https://ww3.freddiemac.com/loanlookup/

DU:

PACE loans are not allowed to be subordinated

PACE loans may be paid off through a cash-out transaction transactions only

HPML

Any loan that is determined to be HPML, the following is required: o The VA residual income calculation is required o For DTIs > 43% or First Time Homebuyers a 12 month housing history with 0X30 is required. If not available,

an AUS run with zero current housing payment is required o Impounds (tax & insurance) are required o HPML worksheet must be completed by NewLeaf Underwriter

Employment / Income

Employment Gaps

LP/DU:

Gaps in employment that are more than 60 days in length must be listed on the 1003 and an explanation from the Borrower must be provided.

Re-entering the workforce: For a Borrower who is re-entering the workforce and has less than a two-year employment and income history, the Borrower's income may be used as qualifying income if the Borrower has been at the current employer for a minimum of six months and there is evidence of a previous employment history.

Employment Documentation

LP/DU:

Follow AUS findings.

VOE only not permitted.

Overtime, Bonus, & Commissions

LP:

Borrower must have a 2 year consecutive history of receiving in order to use as qualifying income.

DU:

12-24 month history may be acceptable, depending on overall strength of the loan and compensating factors. Acceptance will be determined by the UW

Unreimbursed Employee Expenses (2106)

LP:

2106 expenses must be deducted when o any portion of the borrower’s qualifying income is derived from commission

For a borrower who is qualified using any of the following income types below, personal tax returns or record of account transcripts are not required to determine if the Borrower has unreimbursed employee business expenses (2106). In this instance, unreimbursed employee business expenses do not need to be deducted from the borrower’s qualifying income, or added to monthly liabilities even when it is typical for a specific line of work. However, if tax returns or record of account transcripts are in the file for any reason, 2106 expenses must be considered in the income analysis.

o base pay, o bonus, or o overtime

DU:

For a borrower who is qualified using any of the following income types below, unreimbursed employee business expenses (2106) are not required to be analyzed or deducted from the borrower’s qualifying income, or added to monthly liabilities. This applies regardless of whether unreimbursed employee business expenses are identified on tax returns (IRS Form 2106) or tax transcripts received from the IRS:

o base pay, o bonus, o overtime, or o commission income which is less than 25% of the borrower’s annual employment income:

A 2106 expense must be deducted from the qualifying income when: o a borrower has commission income that represents 25% or more of the borrower’s total annual

employment income, or o when an automobile allowance is included in the borrower’s monthly qualifying income

Social Security, & Disability

LP:

For existing and established sources of Social Security & Disability Income: o Document income type, source, payment frequency and pre-determined payment amount with a benefit

verification letter, award letter or equivalent, AND o Document receipt with current bank statement, current benefit verification letter, current award letter

For newly established sources of Social Security & Disability Income: o Document the finalized terms of the newly established income including, but not limited to, the source,

benefit type, effective date of income commencement, payment frequency and pre-determined payment amount with the benefit verification letter, notice of award letter or other equivalent documentation from the payor that provides and establishes these terms. The income must commence prior to or on the first Mortgage payment due date. The documentation must be dated no more than 120 days prior to the Note Date. Verification of current receipt is not required.

o Note: Pending or current re-evaluation of medical eligibility for insurance and/or benefit payments is not considered an indication that the insurance and/or benefit payment will not continue.

For existing and established sources of Survivor & Dependent Benefit Income o For existing and established: Document income type, source, payment frequency and pre-determined

payment amount with a benefit verification letter, award letter, 1099 or other equivalent documentation is required.

o Document current receipt with a bank statement, benefit verification letter, notice of award letter or other equivalent documentation. Age of documentation requirements as described in Section 37.20(d) must be met.

For new sources of Survivor & Dependent Benefit Income o Document the finalized terms of the newly established income including, but not limited to, the source,

type, effective date of income commencement, payment frequency and pre-determined payment amount with the benefit verification letter, notice of award letter or other equivalent documentation from the payor that provides and establishes these terms. The income must commence prior to or on the first Mortgage payment due date. The documentation must be dated no more than 120 days prior to the Note Date. Verification of current receipt is not required.

www.NewLeafWholesale.com

(V5-17) Page 6 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Social Security, & Disability (cont.)

DU:

Social Security & Disability Income: o Either proof of current receipt or the Social Security Administration's (SSA) award letter must be

obtained. o Supplemental Security Income (SSI) must be verified with a copy of the SSA award letter and proof of

current receipt. o If the Social Security income is for Survivor Benefits, retirement, or disability for the benefit of another;

the income must be verified with a copy of the SSA award letter, proof of current receipt, and any additional documentation required to confirm a three-year continuance.

IRA Distributions/ Pension/ Retirement

LP/DU: Borrower must be of retirement age (59.5 years or older). DU:

If the assets are in the form of stocks, bonds, or mutual funds, 70% of the value (remaining after any applicable costs for the subject transaction) must be used to determine minimum 3 year continuance.

Retirement Income: o Retirement, government annuity, or pension income requires proof of receipt and one of the following

documents: o Letters from the organization providing the income retirement award letters, o Federal tax returns, o IRS W-2 or 1099 forms, o A bank statement. o Documentation of three year continuance is not required.

If the retirement income is paid in the form of a monthly distribution from a 401(k), IRA, SEP, or Keogh retirement account (documentation of asset ownership must be in compliance with the Allowable Age of Documents policy), determine that the income will continue for at least three years after the date of the mortgage application

LP:

For existing and established sources of retirement income: o Document income type, source, payment frequency and pre-determined payment amount with a benefit

verification letter, award letter, pay statement, 1099 or other equivalent documentation. o Document current receipt with a bank statement, pay statement, benefit verification letter, award letter

or other equivalent documentation. or

For newly established sources of retirement income: o Document the finalized terms of the newly established income including, but not limited to, the source,

type, effective date of income commencement, payment frequency and pre-determined payment amount with the benefit verification letter, notice of award letter or other equivalent documentation from the payor that provides and establishes these terms. The income must commence prior to or on the first Mortgage payment due date. Verification of current receipt is not required.

Retirement account distributions as income

Most recent retirement account statement(s), documentation from financial institution holding retirement account that verifies regularly scheduled distribution arrangements, 1099(s) and/or other equivalent documentation showing income source, type, distribution frequency, distribution amounts, and history of receipt (as applicable), and

Bank statement(s) or other equivalent documentation evidencing current receipt (as applicable), and

Evidence of sufficient assets to support the qualifying income

If the retirement distributions are not scheduled monthly payments (e.g., annual, semi-annual, quarterly), the most recent distribution verified through a retirement account statement, 1099 and/or other equivalent documentation, as applicable, is sufficient in lieu of current receipt; however, verification of receipt of multiple distributions may be necessary to determine frequency of distributions, history of receipt and amount of stable monthly qualifying income.

Secondary Employment

LP:

Minimum of 2 year uninterrupted history required. DU:

12-24 months uninterrupted history may be acceptable, depending on overall strength of the loan and compensating factors. Acceptance will be determined by UW.

If a wage-earner has a self-employed secondary business and is qualifying only with W2 income, losses from that business do not need to be considered from qualifying income regardless of the size of loss

www.NewLeafWholesale.com

(V5-17) Page 7 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Future Income

LP:

Income from future primary employment may be used for qualifying with the following requirements: o The Borrower’s employment offer must be non-contingent and the non-contingent offer letter must be

included in the file o The Borrower’s written acceptance of the employment offer must be in the file o The time frame between the Mortgage Note Date and the commencement of employment (the

employment gap) must not exceed 60 days o Must be a Purchase transaction, 1 unit Primary Residence o The Borrower must have cash reserves after the Note Date to pay the monthly housing expense during

the employment gap PLUS an additional one month PITIA o A VOE must be obtained no more than 10 business days prior to the Note Date or after the note date or

prior to the delivery date DU:

Allowed per DU Findings with the below requirements when number of months and years employed is zero:

When Borrower Starts Employment at time of funding, an executed copy of offer or contract AND paystub with

sufficient information to support income used to qualify is required, per terms of the employment offer or contract.

When Borrower has not started employment at time of funding, the following requirements apply:

o 1 Unit property only

o Purchase Transactions only

o Primary Residence only

o The borrower Is not employed by a family member or by an interested party to the transaction, AND The

borrower is qualified using only fixed base income

o The borrower’ start date must be within 90 days of the note date

o The contract for future employment must:

clearly identify the employer and the borrower, be signed by the employer and be acceted and

signed by the borrower

must clearly identify the terms of employment, including position, type and rate of pay and

start date, and

must be non-contingent. If conditions of employment exist, all conditions must be satisfied

prior to closing by verbal verification or written documentation. This confirmation must be

noted in the file.

o In addition to the amount of reserves required by DU or for the transaction type, one of the following is

required:

Financial reserves sufficient to cover principal, interest, taxes, insurance, and association

dues (PITIA) for the subject property for six months; or

Financial reserves or current income sufficient to cover the monthly liabilities included in the

debt-to-income ratio, including the PITIA for the subject property, for the number of months

between the note date and the employment start date, plus one. Current income may be used

in lieu of or in addition to financial reserves. For this purpose, the amount of income the

borrower is expected to receive may be used between the note date and the employment

start date. If the current income is not being used for qualifying purposes, it can be

documented by using income documentation, such as a paystub, and no verification of

employment is required.

For calculation purposes, consider any portion of a month as a full month.

Declining Income

Income which has declined from the previous year will be evaluated to determine level of income likely to continue and confirm no further decline. Additionally, the underwriter will evaluate documentation provided to determine if declining income is now considered stable and eligible to be used for qualifying. This applies to both employed and self-employed borrowers.

Credit

Minimum Trade Lines

LP/DU:

No minimum number of trade lines required

Mortgage History

LP/DU:

Acceptability of payment history determined by LP/DU

If an open mortgage is not reported on the credit report, a 12 month rating must be obtained reflecting zero lates

Requirements of Extenuating Circumstances

LP:

Not permitted DU:

Extenuating circumstances are non-reoccurring events that are beyond the Borrower’s control such as sudden, significant and prolonged reduction in income or catastrophic increase in financial obligations. Examples of documentation that can be used to support extenuating circumstances include a divorce decree, notice of job loos/layoff or medical bills.

Bankruptcy

LP/DU:

Chapter 7 & 11: 4 years from discharge date

Chapter 13: 2 years from discharge date or 4 years from dismissal date

Multiple BK's within 7 years requires a 5 year waiting period from dismissal or discharge DU:

If a mortgage debt has been discharged through a Bankruptcy, even a Foreclosure has been subsequently completed to reclaim the property in satisfaction of the debt, the borrower is held to the Bankruptcy waiting period (above) and not the Foreclosure waiting period. Bankruptcy documents must be provided to verify that the mortgage debt was discharged as part of the Bankruptcy.

o If the mortgage was reaffirmed through the bankruptcy or a foreclosure had occurred prior to the bankruptcy follow standard foreclosure seasoning requirements

Foreclosure

LP/ DU:

7 year time period with re-established credit from foreclosure recording date DU:

If mortgage debt has been discharged through a Bankruptcy, see Bankruptcy section above for requirements. o If the mortgage was reaffirmed through the bankruptcy or a foreclosure had occurred prior to the

bankruptcy follow standard foreclosure seasoning requirements Dates are determined from recorded date to credit report date

www.NewLeafWholesale.com

(V5-17) Page 8 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Short Sale, Pre-Foreclosure, Deed-in-Lieu

LP:

Short Sales – Determined by LP

Pre-Foreclosure/Deed-in-Lieu: o 4 years

90% max LTV/TLTV or max allowed for the transaction Purchase and Rate/Term only

o 7 years eligible for max financing - all occupancies and transaction types DU:

4 year waiting period is required from the completion of the Short Sale, Pre-Foreclosure or Deed-in-Lieu as reported on the credit report or other documents provided by the borrower

Exception for Extenuating circumstances: o 2 year waiting period is required with an LOE and supporting documentation

Dates are determined from recorded date to credit report date Application date - The date on which receipt of the borrowers financial information first triggers the Federal Truth In Lending disclosure requirement

Charged Off Mortgage Debt

LP:

Determined by LP DU:

4 year waiting period is required from the completion date as reported on the credit report or other documents provided by the borrower

2 years with extenuating circumstances with an LOE and supporting documentation Application date - The date on which receipt of the borrowers financial information first triggers the Federal Truth In Lending disclosure requirement

Restructured Debt/Modified Mortgages Definition and Requirements

LP/DU:

Determined by DU or LP

Collection Accounts

LP:

Non-Medical collections must be paid off if the total exceeds $2,500 individually or aggregate

DU:

Non-Medical collections must be paid off if the total exceeds $2,500 individually or aggregate for Primary Residence 1 unit properties

Medical and Non-Medical collections must be paid off for 2-4 units, Second Homes and Investment properties as follows:

o 2-4-unit owner-occupied and second home properties, collections and charge-offs totaling more than $5,000 must be paid in full prior to or at closing

o For investment properties, individual accounts equal to or greater than $250 and accounts that total more than $1,000 must be paid in full prior to or at closing

Timeshare Accounts

LP:

Determined by LP DU:

Timeshare accounts may be identified in a borrower’s credit report as being installment debt or mortgage-related debt, depending on the individual timeshare. Timeshare may be treated as installment loans rather than mortgage debt, even if they are identified as mortgage debt on the credit report (or other documentation).

Revolving Accounts

LP:

When determining Borrower's monthly debt payment for purposes of calculating the monthly debt payment-to-income ratio, if Borrower's credit report does not indicate the required minimum monthly payment for any particular revolving or open-end account, the required monthly payment to be used is 3% percent of the outstanding balance of the account.

DU:

If a revolving debt is provided on the loan application without a monthly payment amount, use the greater of $10 or 5% of the outstanding balance as the monthly payment when calculating the total debt-to-income ratio.

Disputed Trade lines

LP:

No further action is required with LP Accept. DU:

Follow DU findings Note: Manual Underwriting is not permitted

Subordinate Financing

LP/DU:

HELOCs qualified using the minimum monthly payment per credit report for both subject and other property owned. If HELOC funds used for closing, new payment at the higher balance must be documented.

Closed ended subordinate financing qualified using credit report payment.

No Negative Amortization

Copy of Note required

When a new concurrent subordinate lien results in cash back, the first trust deed may be considered rate and term as long as cash back does not exceed the lesser of 2% or $2,000 on the first TD final HUD-1. A separate final HUD-1 is required on the concurrent second and may reflect cash back.

LP:

Closed end subordinate financing that is not fully amortized with a maturity date or balloon payment within 5 years is ineligible.

HELOC's with a maturity or call date within 5 years are eligible

DU:

All subordinate financing, including HELOCs, where the maturity or balloon payment is due less than five years of application date is ineligible

www.NewLeafWholesale.com

(V5-17) Page 9 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Paying Off Debt

LP/DU:

Gifts are permitted to pay off debt

Installment debt-allowed, payment excluded from qualifying ratios.

Revolving: o LP: Payoff of revolving debt allowed subject to underwriter review of DTI and reserves - Creditor must

confirm account paid to zero balance. o DU: Payoff of revolving Debt is allowed subject to underwriter review of DTI and reserves - Account

does not have to be closed.

Paying Down Debt

LP/DU:

Paying down revolving debt to qualify is not allowed.

Installment loans that are being paid down to 10 or fewer remaining monthly payments do not need to be included in the borrower’s long-term debt (Subject to UW review of DTI and reserves).

Installment Debt with 10 Months or Less Remaining

If an installment debt has 10 months or less remaining, it may be excluded from the ratios subject to underwriter review of DTI and reserves.

Student Loans

LP:

Student Loans in Repayment: For calculating the monthly DTI ratio, use the greater of:

The monthly payment amount reported on the credit report, or

0.5% of the original loan balance or outstanding balance as reported on the credit report, whichever is greater Student Loans in Deferment or Forbearance: Use the greater of:

The monthly payment amount reported on the credit report, or

1% of the original loan balance or outstanding balance as reported on the credit report, whichever is greater

Student loan forgiveness, cancelation, discharge and employment-contingent repayment programs:

The student loan payment may be excluded from the monthly DTI ratio provided the Mortgage file contains documentation that indicates the following:

o The student loan has ten or less monthly payments remaining until the full balance of the student loan is

forgiven, canceled, discharged or in the case of an employment-contingent repayment program, paid, or o The monthly payment on a student loan is deferred or is in forbearance and the full balance of the student

loan will be forgiven, canceled, discharged or in the case of an employment-contingent repayment program, paid at the end of the deferment or forbearance period

AND

o The Borrower currently meets the requirements for the student loan forgiveness, cancelation, discharge or

employment-contingent repayment program, as applicable DU:

If a payment amount is provided on the credit report, that amount can be used for qualifying purposes.

If the credit report does not identify a payment amount (or reflects $0), use either 1% of the outstanding student loan balance, or a calculated payment that will fully amortize the loan based on the documented loan repayment terms

If documentation is obtained to evidence the actual monthly payment is $0, qualify the borrower with the $0 payment as long as the $0 payment is associated with an income-driven repayment plan

Contingent Liabilities

LP:

Debt may be excluded if borrower provides 12 months of cancelled checks reflecting "other party" is making payments. All payments must reflect as paid as agreed

Please see “Debt Paid by Business” section for debts paid by self-employed Borrower’s business funds

DU:

Certain debts can be excluded from the borrower’s recurring monthly obligations and the DTI ratio:

o When a borrower is obligated on a non-mortgage debt –

but is not the party who is actually repaying the debt the monthly payment may be excluded from the borrower's recurring monthly obligations. This applies whether or not the other party is obligated on the debt, but is not applicable if the other party is an interested party to the subject transaction (such as the seller or realtor). Non-mortgage debts include installment loans, student loans, revolving accounts, lease payments, alimony, child support, and separate maintenance.

In order to exclude non-mortgage or mortgage debts from the borrower’s DTI ratio, the most recent 12 months' cancelled checks (or bank statements) must be obtained from the other party making the payments that document a 12-month payment history with no delinquent payments

o When a borrower is obligated on a mortgage debt –

but is not the party who is actually repaying the debt the full monthly housing expense (PITIA) may be excluded from the borrower’s recurring monthly obligations if

the party making the payments is obligated on the mortgage debt,

there are no delinquencies in the most recent 12 months, and

the borrower is not using rental income from the applicable property to qualify.

In order to exclude mortgage debts from the borrower’s DTI ratio, the most recent 12 months'

cancelled checks (or bank statements) must be obtained from the other party making the

payments that document a 12-month payment history with no delinquent payments

When a borrower is obligated on a mortgage debt, regardless of whether or not the other party is making the monthly mortgage payments, the referenced property must be included in the count of financed properties

Debt Paid by Business

LP/DU

Debts paid by self- employed Borrower’s business funds may be excluded if all the following requirements are met:

o The account in question does not have a history of delinquency, and o The business provides acceptable evidence that the obligation was paid out of company funds (such as

12 months of canceled company checks), and o The lender’s cash flow analysis of the business took payment of the obligation into consideration

www.NewLeafWholesale.com

(V5-17) Page 10 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Primary Residence Pending Sale or Converted to 2nd Home / Investment

LP/DU

Converting primary residence to 2nd home or investment property o For Primary Residence converting to Investment property - See requirements under Investment

properties in Collateral section o For Primary Residence converting to Second homes follow AUS findings

LP:

Current residence is pending sale and will not close prior to new transaction - PITIA may be excluded from DTI if one of the following requirements is met:

o An executed sales contract for the property pending sale. If the executed sales contract includes a financing contingency, the Mortgage file must also contain evidence that the financing contingency has been cleared or a lender’s commitment to the buyer of the property pending sale; or

o An executed buyout agreement that is part of an employer relocation plan where the employer/relocation company takes responsibility for the outstanding Mortgage(s)

DU:

Current residence is pending sale and will not close prior to new transaction - PITIA may be excluded from DTI if the following is provided:

o A fully executed sales contract for the current residence and confirmation that any financing contingencies have been cleared

o Reserves determined by DU

Departing Residence – Using Rental Income

LP/DU:

Rental income may be used to qualify with the following requirements: o Fully executed lease, and o A 1007 to support market rent or Verification that security deposit has been deposited in the Borrower’s

Account

Alimony/Child Support Payments

LP:

A copy of the divorce decree, separation agreement or any other written legal agreement must be provided

Child support and Alimony/Child Support must be included in the DTI unless 10 months or less remaining DU:

A copy of the divorce decree, separation agreement or any other written legal agreement must be provided

Child support must be included in the DTI unless 10 months or less remaining

If Alimony/Spousal support will continue for 10 months or more past the funding date, this obligation can be either

included in the DTI or deducted from the Borrower’s monthly qualifying income

Assets

Down Payment & Source of Funds

LP/DU:

LTV/CLTV < 80% - Entire down payment may come from gift funds

LTV/CLTV > 80%: o 1 unit Primary Residence, use of all gift funds allowed subject to MI approval o 2-4 units and 2nd homes require minimum 5% down payment from the Borrower’s own funds

Gift funds not allowed on Investment properties regardless of LTV/CLTV

For Stocks, Bonds, Mutual Funds - If there is documentation that the value of the asset is at least 20% more

than the funds needed for the borrower’s down payment and closing costs, no documentation of liquidation is

required. Otherwise, documentation of the borrower’s actual receipt of funds realized from the sale or liquidation

must be obtained.

For retirement funds – If there is documentation that the vested value of the asset is at least 20% more than the

funds needed for the borrower’s down payment and closing costs, no documentation of liquidation is required.

Otherwise, documentation of the borrower’s actual receipt of funds realized from the sale or liquidation must be

obtained.

For Vested Stock Options –eligible source of Borrower Funds and reserves with following requirements: o Copy of the statement to verify options are vested and exercisable

Unacceptable sources of funds: Cash-on-hand, unsecured personal loans and credit card advances, non-vested stock options, non-vested restricted stock options and retirement funds that are dependent upon borrower employment status to access

Reserves

LP:

Owner Occupied

1 Unit -Determined by LP

2-4 Unit - 6 months PITIA

Cash proceeds from subject loan may not be used as reserves

2nd Home

2 mos. PITI for the subject and 2 mos. PITIA for other financed 1-4 unit investment properties and 2nd homes

. Cash proceeds from subject loan may not be used as reserves

Investment

6 months PITIA reserves on subject investment property, plus 2 months reserves for other financed residential properties, excluding the primary residence or those owned free and clear.

Cash proceeds from subject loan may not be used as reserves

Gift funds are allowed for reserves on primary residences only

DU:

Owner Occupied

1 Unit - Determined by DU

2-4 Units - 6 months PITIA

Cash proceeds from subject loan may not be used as reserves

2nd Home or Investment

Subject property – Determined by DU

For Multiple Financed Properties: The other financed properties reserves amount must be determined by applying a specific percentage to the aggregate of the outstanding unpaid principal balance (UPB) for mortgages and HELOCs on the other financed properties. The percentages are based on the number of financed properties:

o 2% of the aggregate UPB if the borrower has one to four financed properties,

o 4% of the aggregate UPB if the borrower has five to six financed properties, or

o 6% of the aggregate UPB if the borrower has seven to ten financed properties

Gift funds are allowed for reserves on primary residences only

Retirement Accounts

DU/LP:

Availability of withdrawal must not be contingent upon Borrower’s retirement termination or death (i.e. PERS, STRS, etc.)

100% of the vested value of the asset is allowed when determining available reserves.

If there is documentation that the vested value of the asset is at least 20% more than the funds needed for the borrower’s down payment and closing costs, documentation of liquidation is not required. Otherwise, documentation of the borrower’s actual receipt of funds realized from the sale or liquidation must be obtained

www.NewLeafWholesale.com

(V5-17) Page 11 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Stocks, Bonds, & Mutual Funds for Reserves

LP: Allows 100% of balance (minus any funds required to close) as reserves. DU: Allows 100% of balance (minus any funds required to close) as reserves.

Stock Options as Reserves

LP/DU:

Stock Options are eligible source for reserves with following requirements: o Must be vested o Must verify the security is owned by the borrower and that the security is publicly traded on an

exchange, or marketplace readily verifiable through financial publications.

o Stock options must be vested and exercisable.

o The value of vested stock options can be documented by

A statement that lists the number of options and the option price, and

Using the current stock price to determine the gain that would be realized from exercise of an

option and the sale of the optioned stock.

Non-vested stock options are not an acceptable source of funds for the down payment, closing costs, or reserves.

Interested Party Contributions

LP/DU:

Owner Occupied and Second Home

LTV/TLTV > 90%: 3%

LTV/TLTV 75.01 - 90%: 6%

LTV/TLTV < 75%: 9% Investment

All LTVs: 2%

LP/DU:

Cash or items of value, such as giveaways, passed to the buyer by the seller to encourage the buyer to purchase the property and excessive interested party contributions are considered sales concessions. If there is a sales concession present, the LTV/CLTV is calculated using the lower of the reduced sales price (after the reduction for all sales concessions, including excess financing contributions) or the appraised value.

Lender Premium pricing may be used to pay for borrowers closing costs/prepaids and is not included in maximum contributions from all interested parties (Seller, Realtors, etc). However, total lender and interested party contributions may not exceed actual closing costs/prepaids.

Business Funds

DU/LP:

If the Borrower is using business funds for down payment, closing costs and/or funds to close, a minimum of 3 months business bank statements is required. NewLeaf Underwriter will complete a cash flow analysis and determine if using these funds will have any negative impact on the business. If there is no negative impact, the funds may be used

Additional bank statements/documentation may be required at the underwriter’s discretion when 3 months statements are inconclusive to determine the impact to the business

CPA letter is not required nor acceptable to determine impact to the business

If Borrower is not 100% owner of the business, a letter from the other owner(s) granting permission to use business funds is required

Large Deposits

DU/LP:

For Purchase transactions only

When bank statements, typically covering the most recent two months are used, a written explanation and documentation is required for the source of large deposits, defined as a single deposit for funds that are required for the transaction that exceeds 50% of the total monthly qualifying income for the loan

When a deposit includes both sourced and unsourced (undocumented) portions, only the unsourced portion must be used in calculating whether the deposit exceeds the 50% of the qualifying income

When reduced asset amount is used, net of the unsourced amount of a large deposit, that reduced amount must be used for underwriting purposes

If the source of a large deposit is readily identifiable on the account statement(s) such as a direct deposit from an employer (payroll), the Social Security Administration, or IRS or state tax refund, or a transfer of funds between verified accounts, and the source of the deposit is printed on the statement, there is no need to obtain further explanation or documentation

For refinance transactions the underwriter remains responsible for ensuring that any borrowed funds, including any related liability, are considered

Collateral

Age of Appraisals

LP/DU:

If the effective date of the appraisal report is more than 120 days before the Note Date, and not more than 12 months before the Note Date, an appraisal update with at least an exterior-only inspection (1004D/442) is required.

The appraisal update (recent value) must occur within the four months that precede the date of the note and mortgage.

Re-Use of an Appraisal:

o The borrower and the lender/client must be the same on the original and subsequent transaction.

o The use of an original appraisal for a subsequent transaction if the following requirements are met:

The subsequent transaction may only be a Limited Cash-Out Refinance

The Appraiser must confirm the value has not declined LP:

Re-Use of an Appraisal:

o Cannot pay off secondary financing regardless if it’s a purchase money second

Appraisal and Review Requirements

Follow DU/LP findings for appraisal requirements. A minimum of 2055 exterior only appraisal is required.

High Balance – A field review is required for property values > $1,000,000 & > 75% LTV/CLTV/HCLTV

Refer to Broker Manual and Appraisal Policy.

Properties Listed For Sale

LP: Refinances are not permitted on properties presently listed for sale. If listing was canceled prior to application and appraisal date, the following applies:

Rate/Term Refinance - No further restrictions

Cash-out Refinance - Listing agreement must be canceled 6 months prior to application date or LTV/CLTV limited to 70% or less if mandated by the specific product, occupancy or property type

DU: Refinances are not permitted on properties presently listed for sale. If listing was canceled prior to application and appraisal date, the following applies:

Rate/Term & Cash-Out Refinances - No further restrictions

www.NewLeafWholesale.com

(V5-17) Page 12 of 12 Last Updated 1/16/2018

Underwriting Guideline Matrix NewLeaf 1: DU-LP Conforming & High Balance

Fixed Rate

Investment Properties

LP/DU:

Borrower must currently own a primary residence for Purchase transactions or be able to document current rental payments with 12 months canceled checks or VOR from a property management company.

If subject is a 1 unit purchase Investment property and is not rented, Form 1007 is required

If Subject is Investment property owned in previous tax year(s): Income calculated using the prior year’s Sch E. If Subject is investment property not owned in previous tax year: Income calculated using Forms 72/1000 for LP and Form 1007 for DU and copy of current lease/rent agreement. Documentation to support receipt of current rents required.

If other investment property owned in previous tax year: Income calculated using the prior year’s Sch E

If other investment property not reported on the previous tax year Sch E: Income calculated using current lease / rental agreement (75% gross rents minus PITI). Documentation to support receipt of current rents required.

Gift funds are not permitted.

Landlord experience not required in order to use rental income from subject

LP:

Reserve requirement: 6 months PITI reserves on subject investment property, plus 2 months reserves for each other residential property owned, excluding the primary residence or those owned free and clear.

DU:

If subject is an investment property and is currently rented, a copy of the current rental/lease agreement is required even if no rents are used to qualify.

6 mos. rent loss insurance if rental income from subject is used to qualify.

Refer to the Reserves section for requirements

Conversion of

Primary Residence

to Investment

Property

LP/DU:

Follow the standard rental income and financial reserve requirements when the borrower converts his or her current principal residence to an investment property.

Landlord History Landlord history not required

Maximum Acreage Site size must be typical for the area and supported by comps. Maximum 20 acres.

Income producing properties are ineligible.

Property Inspection Waivers

PIWs not allowed - minimum inspection is 2055 exterior only. (Refer to Program W102 & W108 for utilization of PIW)

Condominiums

Projects must be warrantable per FHLMC/FNMA guidelines; applicable condo documentation to be submitted. See Broker Manual for details.

DU: o New and Newly Converted condo projects with a PERS or CPM approval o Established condos with Limited Review – All states except Florida:

Owner Occupied – 80% LTV/CLTV ( > 80% LTVs, refer to NewLeaf 2) Second Homes – 75% LTV/CLTV Investment Properties – Not Allowed

o Established condos with Limited Review - Florida: Owner Occupied - 75%/90% LTV/CLTV Second Homes – 70%/75% LTV/CLTV Investment Properties – Not Allowed

LP: o New and Newly Converted condo projects with a PERS only (CPM not allowed) o Established condos with Streamline Review – All states except Florida:

Owner Occupied – 90% LTV/CLTV Second Homes – 75% LTV/CLTV Investment Properties – Not Allowed

o Established condos with Streamline Review - Florida: Owner Occupied - 75% LTV/CLTV Second Homes – 70% LTV/CLTV Investment Properties – Not Allowed

Manufactured Housing

Refer to NewLeaf 1 Manufactured Housing matrix

Not allowed for High Balance

Deed Restrictions

Must be the borrower’s principal residence, 1 to 2 units only.

Original Transaction must have been an arms-length transaction.

Full title policy required.

Appraisal to include 2 comps and 1 listing with the same restriction.

For a refinance transaction must use lower of purchase price or appraised value.

Cash out refinance requires 12 seasoning from date of purchase