US Outbound Investment

Denise MagyerSenior Vice President

Allied Irish Bank

3

AGENDAAgenda

U.S.Outbound Investment

U.S. Outbound Investment: Why Choose Ireland?

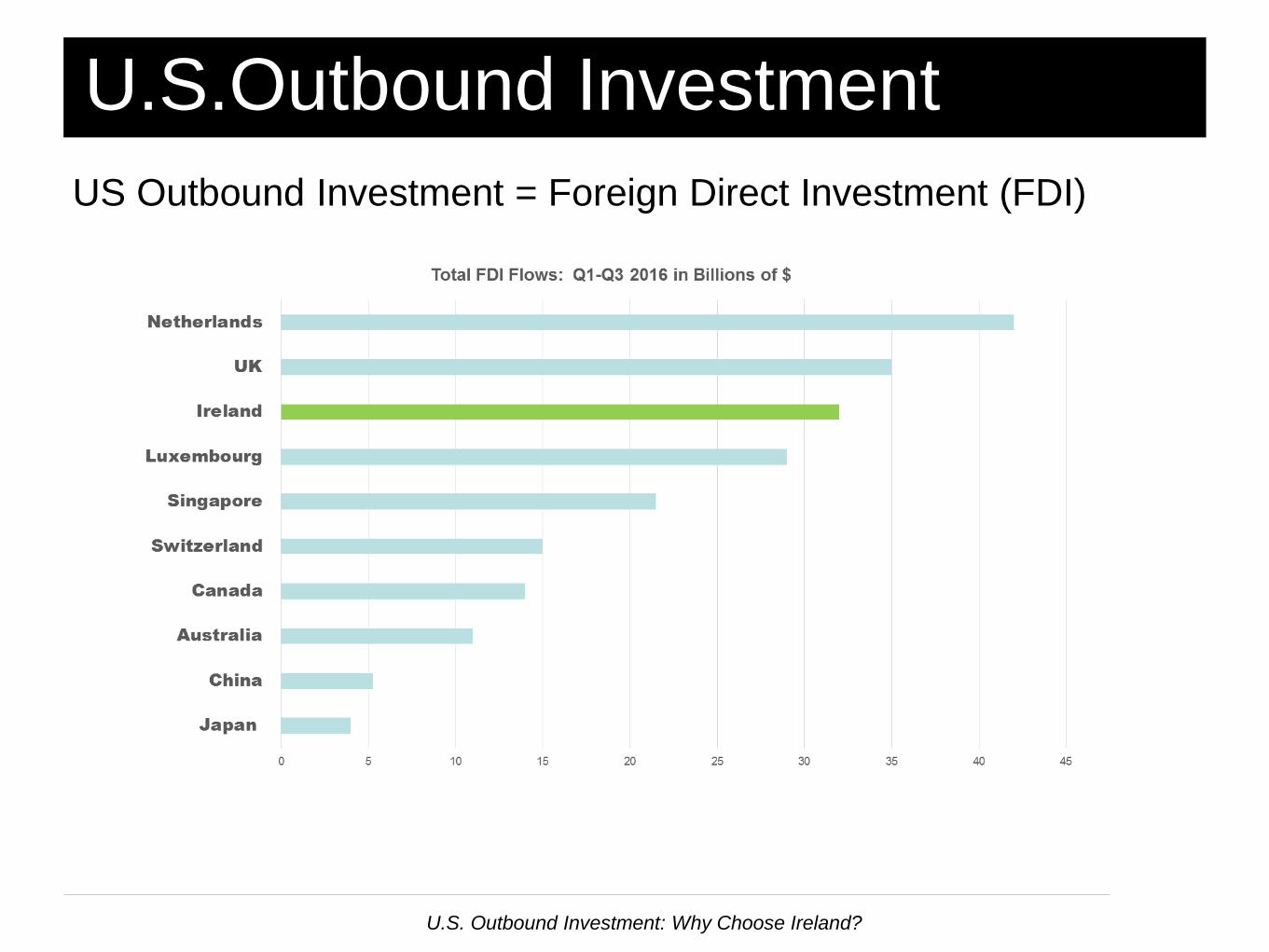

US Outbound Investment = Foreign Direct Investment (FDI)

U.S. Ireland

Source: America Ireland Chamber of Commerce “US-Ireland Business 2017”

U.S. Outbound Investment: Why Choose Ireland?

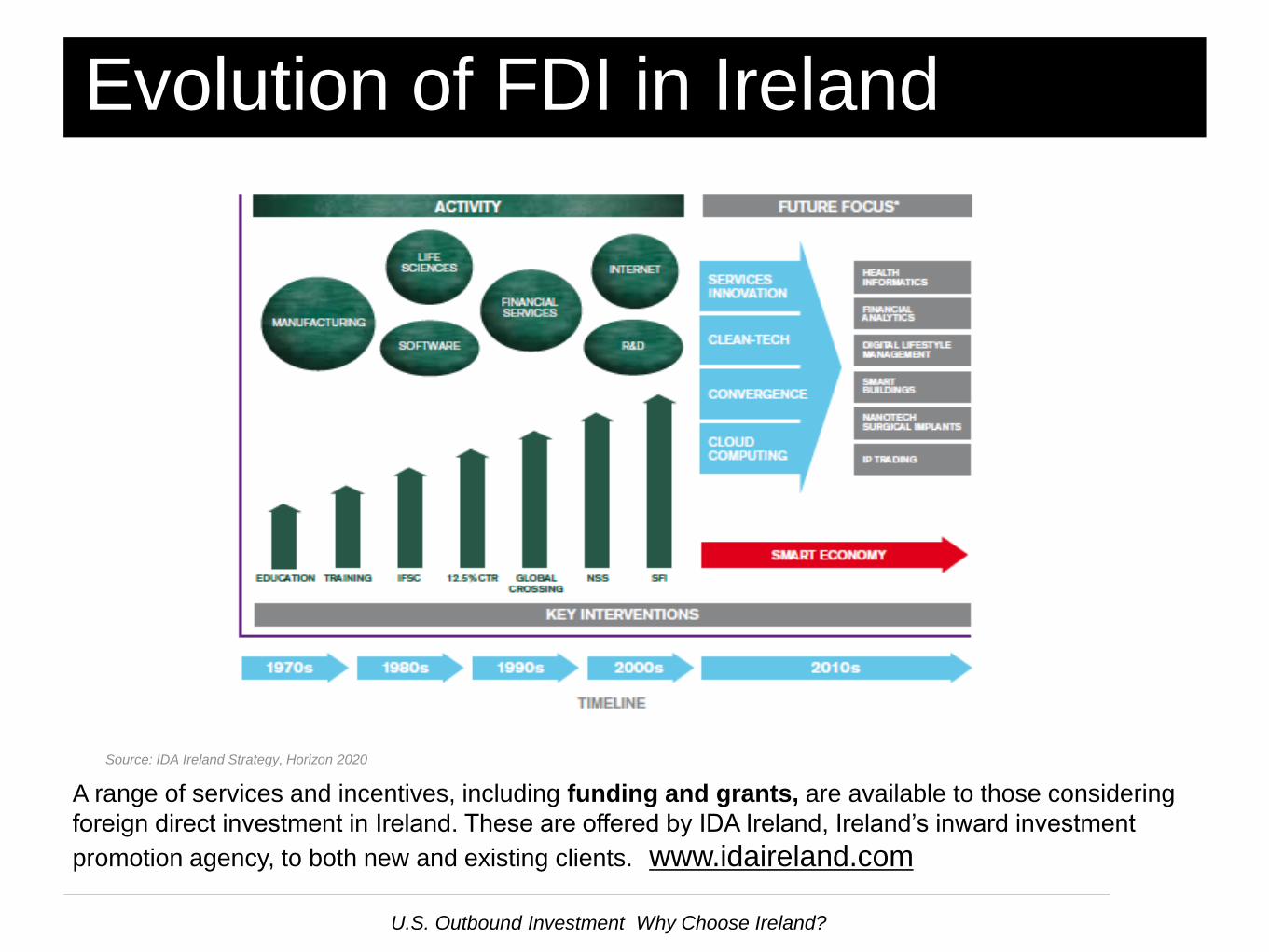

Evolution of FDI in Ireland

U.S. Outbound Investment Why Choose Ireland?

Source: IDA Ireland Strategy, Horizon 2020

A range of services and incentives, including funding and grants, are available to those considering

foreign direct investment in Ireland. These are offered by IDA Ireland, Ireland’s inward investment

promotion agency, to both new and existing clients. www.idaireland.com

Survey Results

Source: Ipsos MRBI AIB Foreign Direct Investment Research February 2014

86% of companies stated that access to Europe was critical or important

REASONS FOR SETTING UP IN IRELAND

U.S. Outbound Investment: Why Choose Ireland?

See our Sector Report, "Why Choose Ireland?" at www.aibcorporate.ie

China $11,000

EU $35,000

Access to the European market

ECONOMIC

SIZE

PER CAPITA

WEALTH

LARGE MARKET FOR

US GOODS/SERVICES

CHINA $21.3 trillion

EU $19.2

US $18.6

INDIA $8.7

JAPAN

$ 4.9

Source: Cia WORLD FACT BOOK

U.S. Outbound Investment: Why Choose Ireland?

Export Propensity

Access to the 500m people in Europe

US affiliate sales of

goods and services in

Ireland totaled $343

billion in 2015

Greater than US

affiliate sales in

China ($165bn) and

Japan ($108bn).

The reason: Export-Propensity.

Ireland ranks the number one export platform in the world for U.S. affiliates

underscoring the importance of Ireland in the global value chains

>

Source: Bureau of Economic Analysis 2016 based on most recent data

U.S. Outbound Investment: Why Choose Ireland?.

Ease of Doing Business

Source: Ipsos MRBI AIB Foreign Direct Investment Research February 2014

1

U.S. Outbound Investment: Why Choose Ireland?

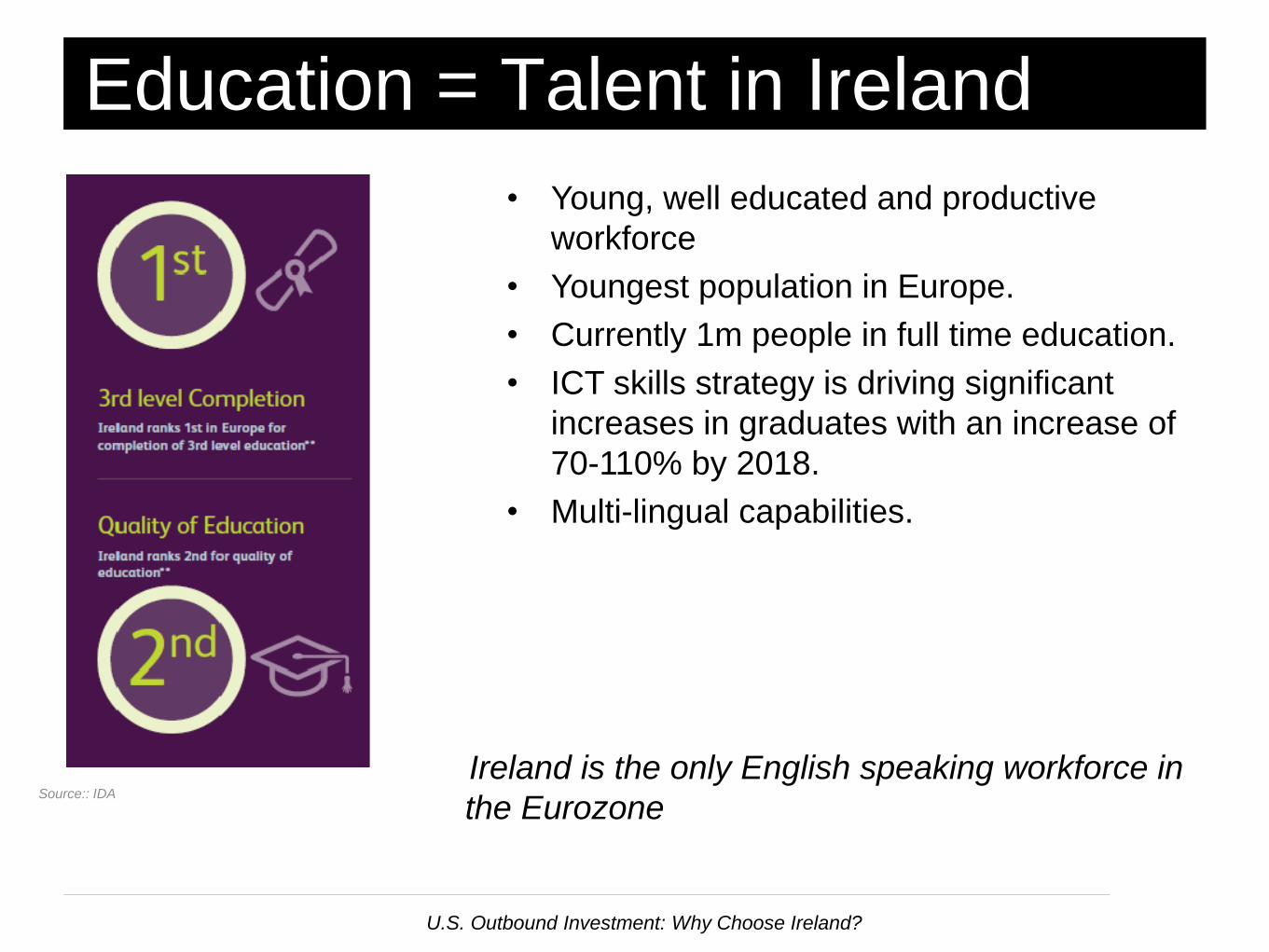

Education = Talent in Ireland

• Young, well educated and productive

workforce

• Youngest population in Europe.

• Currently 1m people in full time education.

• ICT skills strategy is driving significant

increases in graduates with an increase of

70-110% by 2018.

• Multi-lingual capabilities.

Ireland is the only English speaking workforce in

the EurozoneSource:: IDA

U.S. Outbound Investment: Why Choose Ireland?

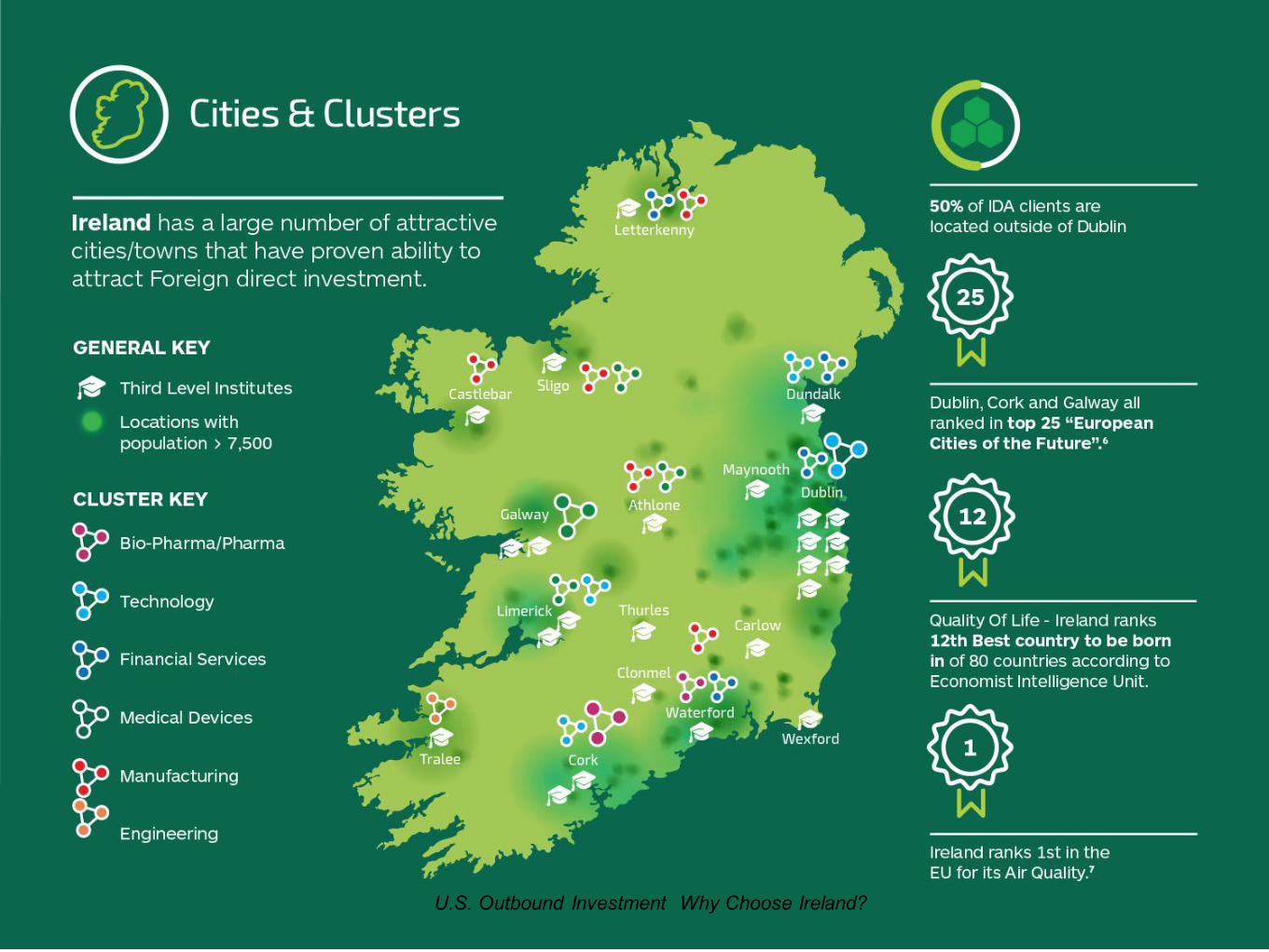

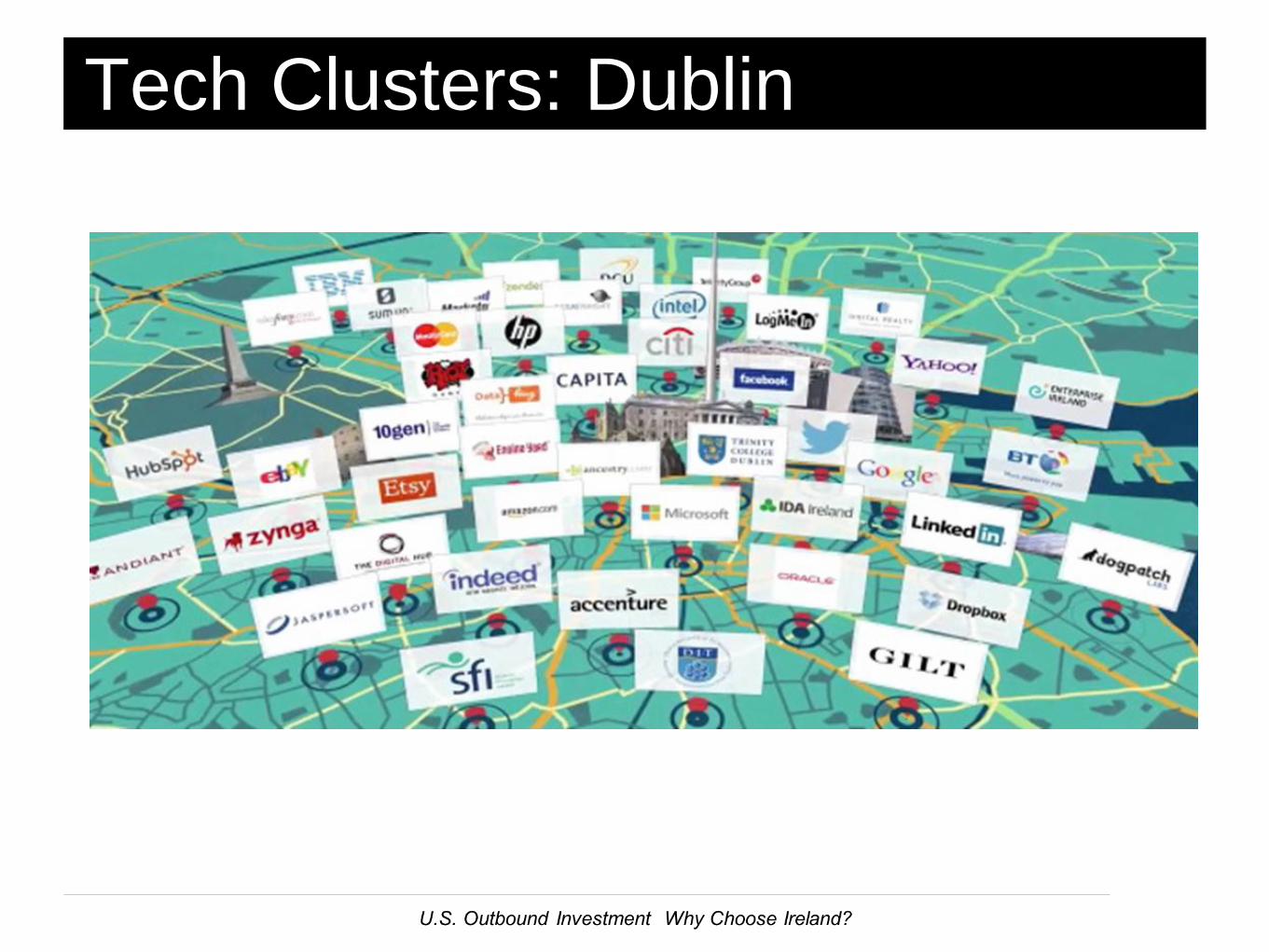

Tech Clusters: Dublin

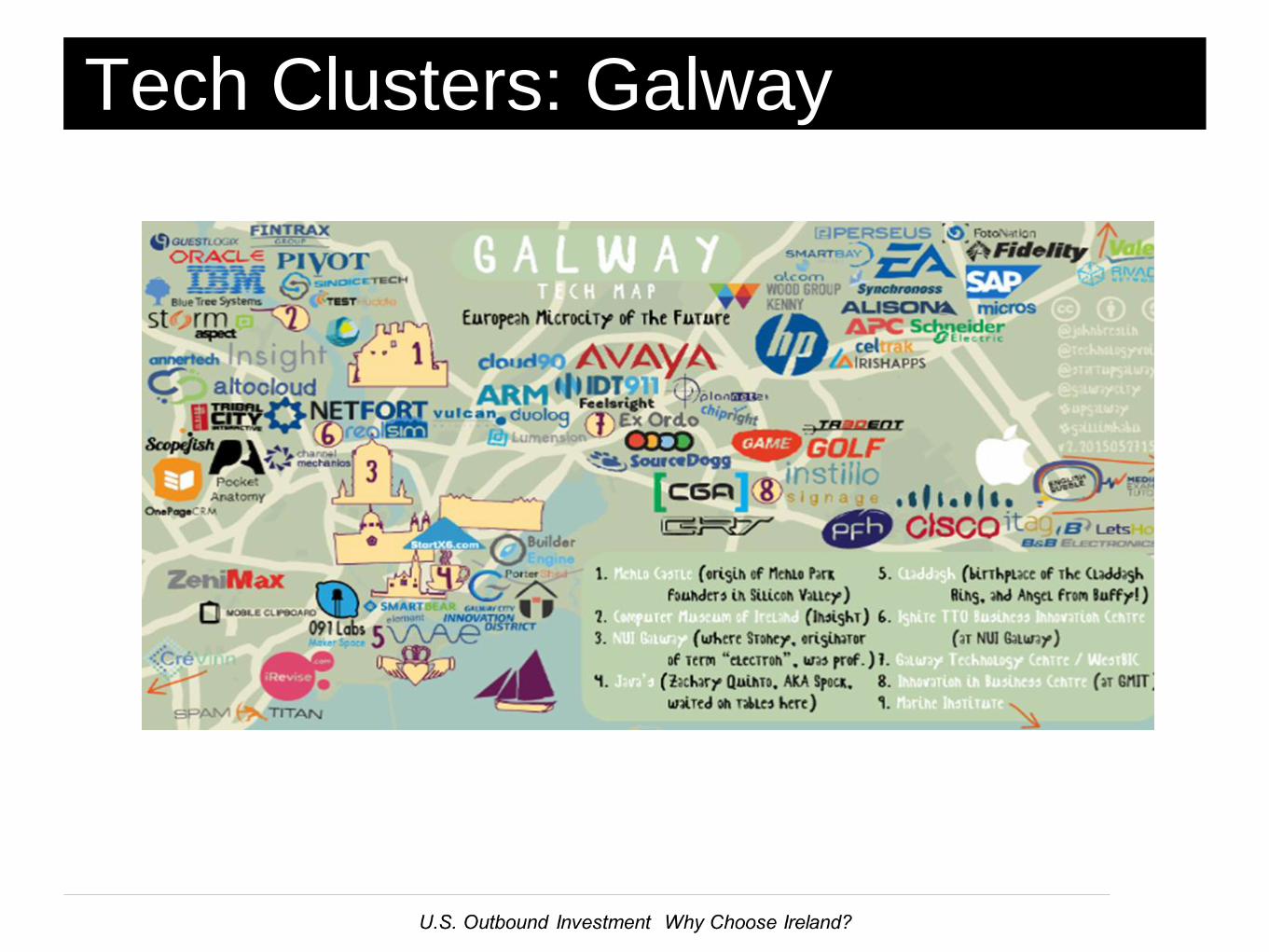

Tech Clusters: Galway

Track Record

Time Zone

Tax Regime

Corporate tax rate of 12.5% for active business.

25% Research & Development (R&D) Tax Credit

An Intellectual Property (IP) regime which

provides a tax write-off for broadly defined IP

acquisitions. Attractive relief for staff assigned from abroad,

key staff working in R&D.

“Our core offering is a competitive, business-

friendly regime with a rock solid commitment to

the 12.5% corporation tax rate”Update on Ireland’s International Tax Strategy 2016

Minister of Finance, Michael Noonan, TD

Why are Companies using Ireland?

Supply Chain Management

Headquarters & IP Management

High Value Manufacturing

Global Business Service Centers

Research, Development & Innovation

Expansion into EMEA Markets

Tax efficient supply chain management

Arm’s length pricing and transfer pricing

Operational substance in Ireland

Corporate restructuring and inversions into

Ireland

21

IRELAND AS A TREASURY LOCATION

Source: EY

12.5% on

treasury

trading profit

Transparent

tax regime

aligned to

BEPS

WHT

exemption on

interest &

dividends

No CFC or thin

capitalization

rules

OECD – based

transfer pricing

regime

No capital

duty on

shares / loan

issuances

Extensive tax

treaty

network &

EU

Directives Dedicated

securitization

regime

Unilateral

credit for

foreign

withholding

taxes

Published

guidance on

treasury

activities

Ireland also represents a very

attractive and sustainable solution

as a corporate treasury center/

group “bank”.

The taxation of interest / treasury

income at 12.5% is not targeted by

BEPS.

Ireland is not a “hybrid haven”.

The taxation of interest / treasury

income at 12.5% rate should meet

minimum taxation level of unilateral

interest base erosion measures.

IRELAND as a Treasury Location

U.S. Outbound Investment: Why Choose Ireland?

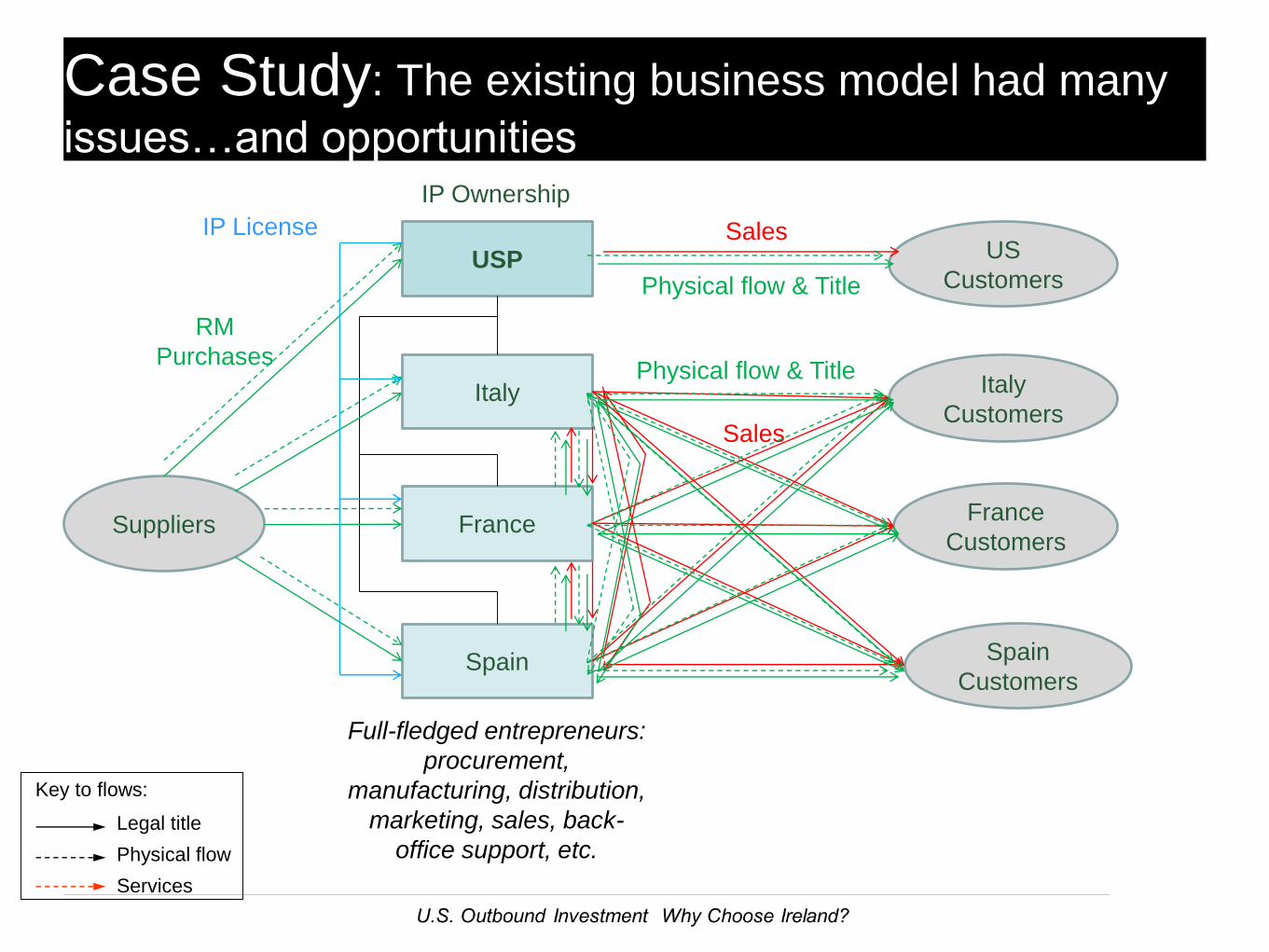

Case Study: The existing business model had many

issues…and opportunities

USP

Spain

France

Italy

Suppliers

Italy

Customers

France

Customers

Spain

Customers

IP Ownership

RM

Purchases

US

Customers

Full-fledged entrepreneurs:

procurement,

manufacturing, distribution,

marketing, sales, back-

office support, etc.

IP License

Key to flows:

Legal title

Physical flow

Services

Sales

Sales

Physical flow & Title

Physical flow & Title

Real Life Case Study: Centralized model

USP

Suppliers

FG Sale - Mkt

price less

commission

RM

Title

IP Ownership

Cost-sharing

for ROW IP

rights

IrishCo

Italy

France

Spain

RM Physical flow

US

Customers

ROW

Customers

Finished good shipped

FG Sale –

mkt price

FG Sale - mkt price

CM fee

Key to flows:

Legal title

Physical flow

Services

24Ireland: A Platform for Expansion into Europe

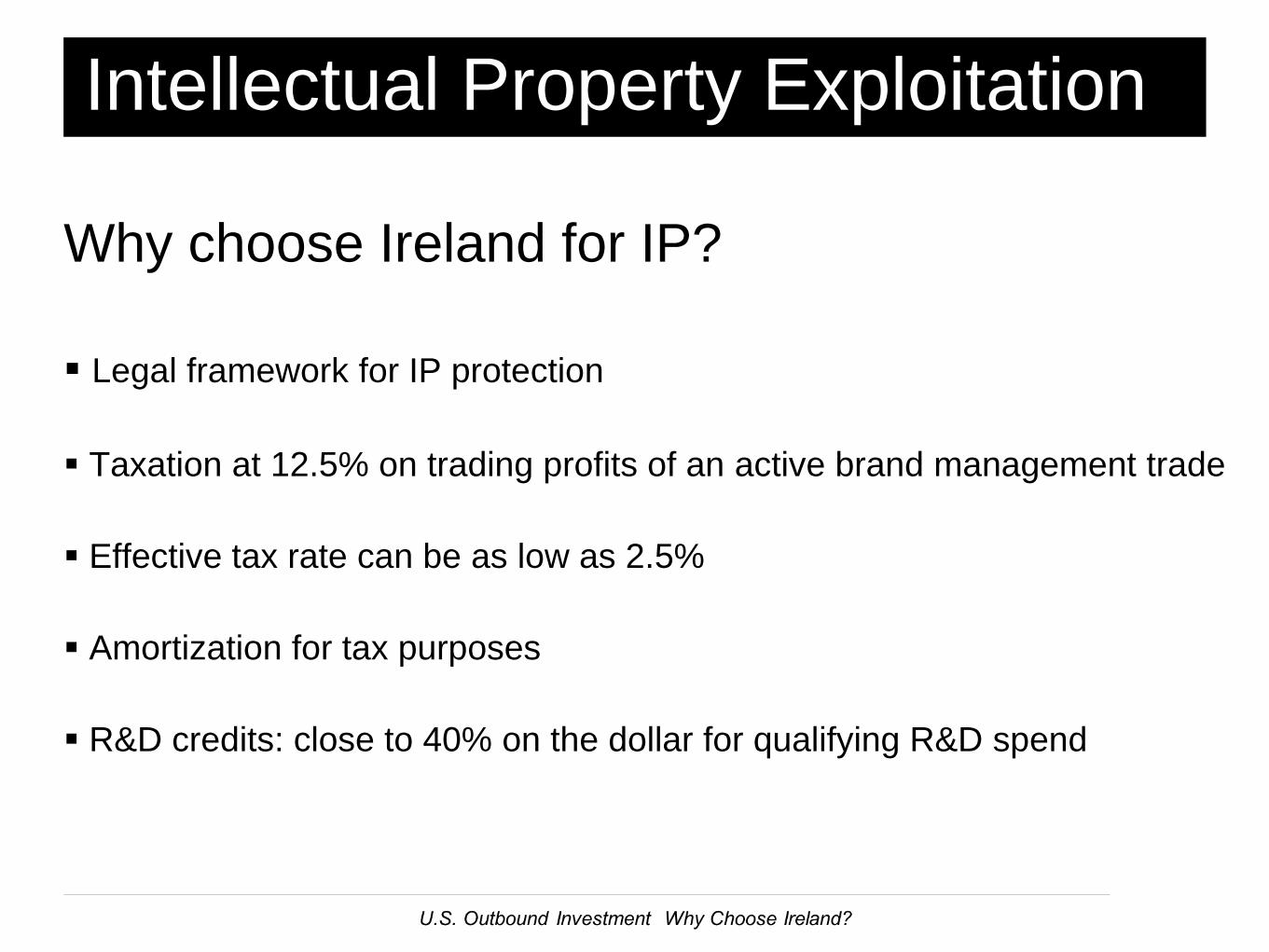

Intellectual Property Exploitation

Why choose Ireland for IP?

Legal framework for IP protection

Taxation at 12.5% on trading profits of an active brand management trade

Effective tax rate can be as low as 2.5%

Amortization for tax purposes

R&D credits: close to 40% on the dollar for qualifying R&D spend

25

Source: EY

12.5% on IP

trading profit

Tax

amortization

available for

acquired IP

WHT

exemption

on outbound

royalties

payments

Tax free

exit

available

on

migrationCredit

available for

WHT on

inbound

royalties

Interest

deduction on

borrowings

used to

acquire IP

Extensive tax

treaty network &

EU Directives25%

“refundable”

R&D tax

credit

New OECD

compliant

patent box

No stamp

duty on the

acquisition of

IP

Ireland has a very favorable IPregime with a number of largeMNE’s already choosing to locatetheir non-US IP in Ireland.

The royalty income receivedshould be taxable at the 12.5%provided the company has“substance” in Ireland is activelycarrying on an IP type trade.

A deduction for tax amortization onacquired IP and interest onborrowings also available whichcan reduce the company’s cashtax rate below the standard 12.5%rate and 0% rate is possible.

Currently seeing a huge amount ofinterest in Ireland as an IPlocation.

IRELAND as an IP Location

U.S. Outbound Investment: Why Choose Ireland?

Ireland is NOT a Tax Haven….

1. No or nominal taxes Ireland’s corporate tax rate is 12.5%

2 Lack of transparency Ireland’s tax regime is fully transparent based on

legislation

3. Unwilling to exchange Ireland exchanges information through Tax information Treaties, Information Exchange Agreements, EU

Savings Tax Directive and (proposed) FATCA);

4 No substance requirement The 12.5% tax rate applies to trading activities

only which require substance

The OECD has identified four key indicators of a

tax haven

None of which apply to Ireland

27

BASE EROSION & PROFIT SHIFTING (BEPS)

Source: OECD

What Is BEPS?

.

“Stated simply, BEPS arises because under existing rules, it is possible for companies to artificially separate taxable profits from economic activities and value creation”

Raffaele Russo, Head of BEPS project

Base Erosion Profit Shifting

U.S. Outbound Investment: Why Choose Ireland?

Tax planning strategies that exploit

gaps and mismatches in tax rules that

artificially shift profits to low or no-tax

locations where there is little or no

economic activity, resulting in little or no

overall corporate tax being paid

28

Source: EY

What is BEPS All About?

U.S. Outbound Investment: Why Choose Ireland?

29Source: Address by Minister Michael Noonan TD to Irish Times International Tax Event 1/24/17

A Message From Ireland’s Finance Minister:

Ireland is committed to the BEPS project

Country by Country reporting has been implemented

Transparency: Committed to the highest international standards

Review of Ireland’s tax code in 2017 budget

U.S. Outbound Investment: Why Choose Ireland?

30

Source: AIB, EY

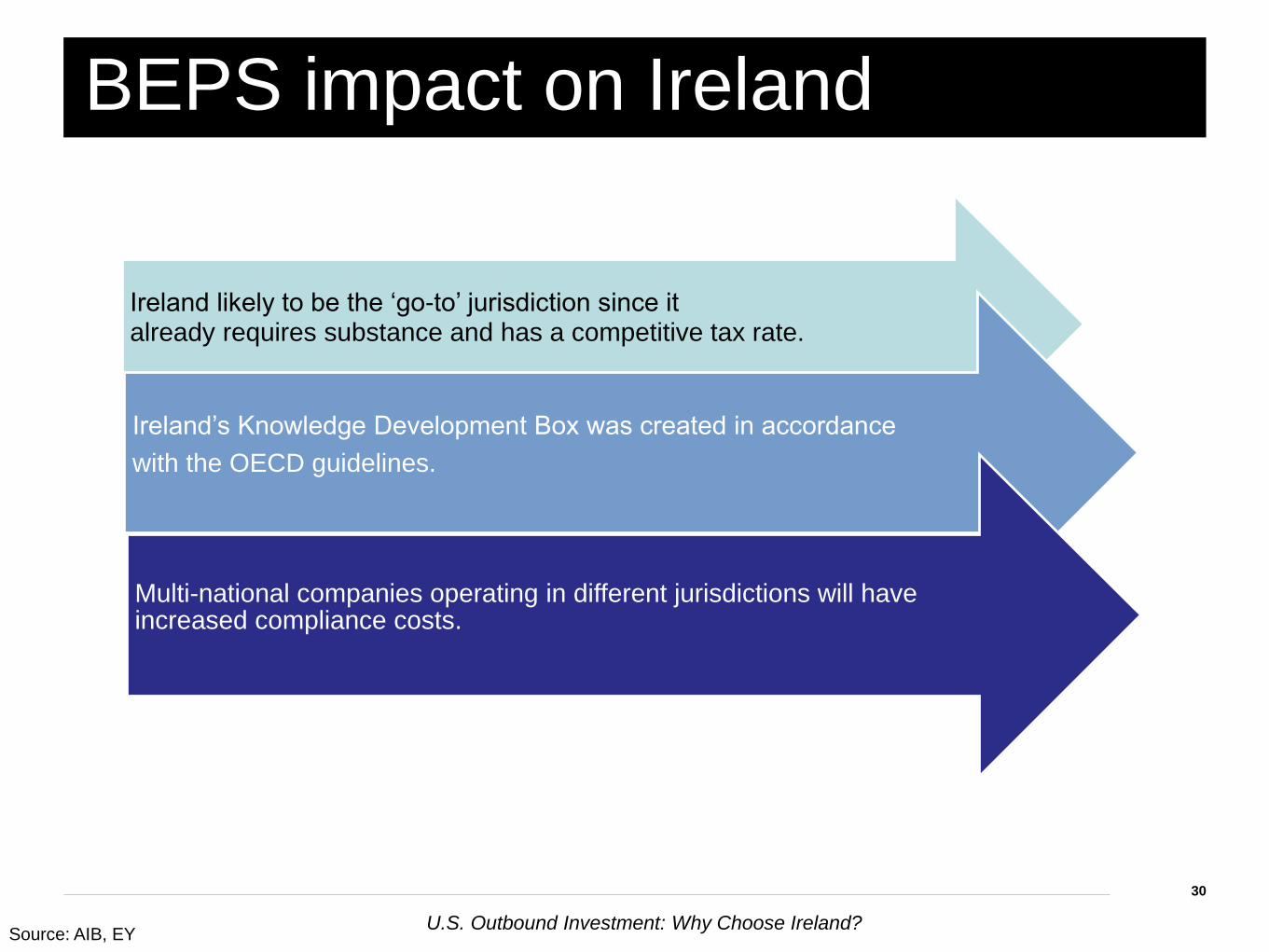

Ireland likely to be the ‘go-to’ jurisdiction since it already requires substance and has a competitive tax rate.

Ireland’s Knowledge Development Box was created in accordance

with the OECD guidelines.

Multi-national companies operating in different jurisdictions will have increased compliance costs.

BEPS impact on Ireland

U.S. Outbound Investment: Why Choose Ireland?

31

Source: EY

► Action 1: Address the tax

challenges of the digital economy

► Action 2: Neutralise the effects of

hybrid mismatch arrangements

► Action 3: Strengthen CFC rules

► Action 4: Limit base erosion via

interest deductions and other

financial payments

► Action 5: Counter harmful tax

practices more effectively, taking

into account transparency and

substance

► Action 6: Prevent treaty abuse

► Action 7: Prevent the artificial

avoidance of permanent

establishment status

Action plan

on Base

Erosion and

Profit Shifting

(BEPS)

► Action 8: Consider transfer pricing for

intangibles

► Action 9: Consider transfer pricing for

risks and capital

► Action 10: Consider transfer pricing for

other high-risk transactions

► Action 11: Establish

methodologies to collect and

analyse data on BEPS and

actions addressing it

► Action 12: Require taxpayers to

disclose their aggressive tax

planning arrangements

► Action 13: Re-examine transfer

pricing documentation

► Action 14: Making dispute

resolution mechanisms more

effective

► Action 15: Develop of a

multilateral instrument for

amending bilateral tax treaties

BEPS impact on Treasury

U.S. Outbound Investment: Why Choose Ireland?

32

Source: EY

► Action 1: Address the tax

challenges of the digital economy

► Action 2: Neutralise the effects of

hybrid mismatch arrangements

► Action 3: Strengthen CFC rules

► Action 4: Limit base erosion via

interest deductions and other

financial payments

► Action 5: Counter harmful tax

practices more effectively, taking

into account transparency and

substance

► Action 6: Prevent treaty abuse

► Action 7: Prevent the artificial

avoidance of permanent

establishment status

Action plan

on Base

Erosion and

Profit Shifting

(BEPS)

► Action 8: Consider transfer pricing for

intangibles

► Action 9: Consider transfer pricing for

risks and capital

► Action 10: Consider transfer pricing for

other high-risk transactions

► Action 11: Establish

methodologies to collect and

analyse data on BEPS and

actions addressing it

► Action 12: Require taxpayers to

disclose their aggressive tax

planning arrangements

► Action 13: Re-examine transfer

pricing documentation

► Action 14: Making dispute

resolution mechanisms more

effective

► Action 15: Develop of a

multilateral instrument for

amending bilateral tax treaties

Impact sales tax

payments- where

collected and paid

Increased reporting

requirements

& auditsTransfer pricing

calculations; impact

on intercompany

financings

Interest deductions

& Withholding tax

calcs;

Req. for substance

and shift of trading

activity

Double taxation

due to conflicting

jurisdictions?

BEPS impact on Treasury

U.S. Outbound Investment: Why Choose Ireland?

33

Ireland: Other considerations

Brexit

US Tax Reform

The Apple Case

U.S. Outbound Investment: Why Choose Ireland?

It’s Important to Have a Vision for Your BusinessInitial expansion planning decisions can have long-term impacts

Each “business” decision drives “tax” consequences and opportunities

Global Business

Model

How will I

mange foreign

currency issues

What do I do

with cash built-

up off-shore

What are my

income/indirect

tax obligationsWhat are my

financial &

regulatory

requirements

How/where will I

bill and collect

from clients

How will I sell &

conclude sales

outside the US

How will I

distribute

finished goods

How do I exploit

my Intellectual

property

How do I fund

ongoing R&D

What location(s)

should I be inWhat should my

legal structure

be

ProcSales

Acctg

ITMfg

Fin

Treas

Risk Legal

AP

Cash

AR

Anticipating and planning for each decision may help avoid unfavorable “default” decisions

which may negate benefits on an after-tax basis

If/where/how should

I manufacture

products

U.S. Outbound Investment: Why Choose Ireland?

Some thoughts…

Be aware of OECD work in progress/areas of focus

Choose a structure that best fits your company’s risk profile.

Hire the appropriate team of consultants and advisors

Questions

The Irish Advantage

It is the combination of factors

The Irish

Advantage

12.5% CT &

extensive

tax treaty

network

Stable

political

environment

& Respected

regulatory

regime

Highly

skilled,

knowledge

based

economy

Flexibility,

responsive-

ness &

innovation

Experience

delivering

Global

Business

Services

Experienced

& Innovative

Leaders

Excellent

Research

facilities &

capabilities

Irish

Government

partnering

Unique mix

of

components

Source: IDA Ireland

FUN FACTSFun Facts…

Ireland produces:

___% of the world’s contact lenses

__%of ventilators used in acute hospitals worldwide

___% of the world’s stents

___% of the world’s Botox

# of Jelly Beans daily

___% of the world’s Tic Tacs

1 in __ burgers served in European McDonalds is made with Irish beef

Driver vision systems technology is manufactured in Galway

which can park your car without you being in it.

Contacts

Denise Magyer

Senior Vice President

Allied Irish Bank

1345 Avenue of the Americas

10th Floor

New York

NY 10105

212-339-8170