115

4 Value-added tax

Introduction Value-added tax (VAT) is levied at a standard rate of 14 percent by registered vendors on most goods and services subject to certain exemptions, exceptions and zero-ratings provided for in the Value-Added Tax Act (1991). VAT is also levied on the importation of goods and services into South Africa.

This chapter gives an overview of:

• Number of registered VAT vendors • Domestic VAT: Payments and refunds • Turnover • The debate around current VAT concessions.

Number of registered VAT vendors The number of vendors registered for VAT shows a steady increase of 8 percent per year over the past five years. (See table 4.1.)

Table 4.1: Number of registered VAT vendors, 2002/03 – 2007/08

NumberRegistered1 Active

vendorsPercentage of

registered2002/03 506 098 487 736 96.4%

2003/04 536 281 507 203 94.6%

2004/05 578 138 530 865 91.8%

2005/06 633 703 618 417 97.6%

2006/07 677 153

2007/08 745 487

1. As per register as at 31 March of each year. Excludes coded cases where status is in suspense, estate and address unknown.

Domestic VAT: Payments and refunds Table 4.1.11 and table 4.1.2 show the number of vendors, payments and refunds per sector. The largest number of VAT vendors in 2005/06 was in the financing, insurance, real estate and business services sector (32.5 percent), followed by the agriculture, forestry and fishing (12.9 percent) and the retail trade (10.4 percent) sectors.

1 Tables numbered in italics are included at the end of the chapter.

2008 TAX STATISTICS

116

Companies in the mining and quarrying sector constitute 0.5 percent of the number of vendors and 3.8 percent of the total gross VAT payments for 2005/06, but are a negative contributor to net VAT (after refunds). The financing, insurance, real estate and business services sector made the largest gross domestic VAT payments in 2005/06, totalling R37.9 billion (29.1 percent).

By payment category

The requirement for monthly VAT payments applies primarily to larger vendors with taxable supplies (turnover) in excess of R30 million per year.

Around 90 percent of vendors submit returns on a bi-monthly basis (see table 4.2.1). Tables 4.2.2 to 4.2.5 provide a breakdown of the various sectors’ payments and refunds for the different payment periods.

By type of enterprise

Corporations (companies and close corporations) formed the bulk of VAT vendors in 2005/06 (66.3 percent in 2005/06), followed by individuals – sole proprietors (23.9 percent). Corporations accounted for 89.3 percent of gross domestic VAT collections. (See table 4.3.1.)

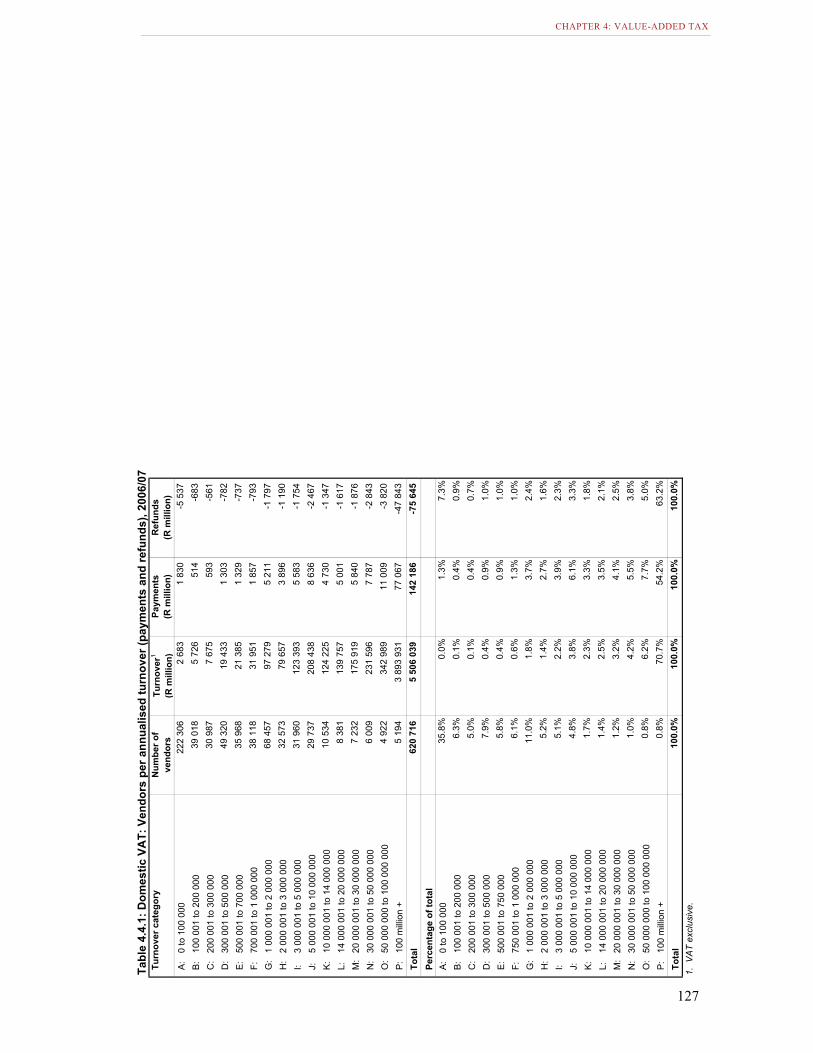

Turnover For 2006/07, 47.1 percent of VAT vendors registered voluntarily; this means they had an annual turnover of less than R300 000. About 67 percent of VAT vendors had a turnover of R1 million or less, accounting for 1.6 percent of net domestic VAT collections. The top 5 percent of VAT vendors had an annual turnover in excess of R14 million and accounted for 73 percent of the total net domestic VAT collections. It should be noted that less than 1 percent of vendors had an annual turnover greater than R100 million and this category accounted for 44 percent of the net domestic VAT collections. (See table 4.4.1.)

Current VAT concessions Based on the 2005/06 Income and Expenditure Survey (IES)2 the poorest 10 percent of households spend on average 34.9 percent of their income on food, beverages and tobacco as opposed to 8 percent for the top 10 percent of high-income households. (See table 4.5.1.) The zero-rating of 19 basic foodstuffs and illuminating paraffin was intended to alleviate the impact of VAT on the poor. The basic food items are: brown bread, maize meal, samp, mealie rice, dried mealies, dried beans, lentils, pilchards, milk powder, dairy powder blend, rice, fresh vegetables, fresh fruit, vegetable oil, milk, cultured milk, brown wheaten meal, eggs, legumes and pulses3.

• Bread and cereals account for 27.8 percent of the poorest 10 percent of household expenditure on food, beverages and tobacco. The corresponding figure for the top 10 percent of households is 10 percent and 18.9 percent for all households. (See table 4.5.2.)

• Meat accounts for 19.8 percent of the poorest 10 percent of household expenditure on food, beverages and tobacco. The corresponding figure for the top 10 percent of households is 21.3 percent and 22.8 percent for all households.

• Vegetables account for 11.7 percent of the poorest 10 percent of household expenditure on food, beverages and tobacco. The corresponding figure for the top 10 percent of households is 7.5 percent and 9 percent for all households.

• Milk, cheese and eggs account for 8 percent of the poorest 10 percent of household expenditure on food, beverages and tobacco. The corresponding figure for the top 10 percent of households is 10 percent and 9 percent for all households.

2. Statistics South Africa. 3. Value-Added Tax Act (1991), Schedule 2, Part B.

CHAPTER 4: VALUE-ADDED TAX

117

While the VAT zero-rating of basic foodstuffs (and paraffin) is targeted to assist the poor, higher income households also benefit from these concessions. As the non-poor spend significantly more on food, high income households receive greater VAT relief in rand terms. The Katz Commission found that the highest income households benefit approximately six times more in monetary terms than the poorest households. The zero-rating reduces the VAT burden of the poorest households by about 18 percent, compared to a 6 percent reduction for the highest income groups. However, of the total estimated revenue forgone due to the zero-rating, only about a third benefits households in the bottom half of the income distribution4.

Impact of VAT zero-ratings Further, empirical evidence based on household spending patterns suggests that existing VAT zero-ratings and exemptions, almost in all cases, confer substantially more benefits on higher income than on lower income groups. There are very few concessionary items where the absolute spending by lower income expenditure groups exceeds that of higher income expenditure groups. This is particularly true of some “basic foodstuff” items where the share of expenditure by the low income expenditure quintiles is relatively low, given the pattern of income inequality in South Africa5.

Table 4.5.3 indicates that the bottom 50 percent of households based on income, account for only 31.9 percent of the total expenditure on food, beverages and tobacco. The top 20 percent of households based on income, account for 37.8 percent of total expenditure on food, beverages and tobacco.

With the exception of maize meal, bread flour and maize rice, the savings derived by higher income groups from current zero-ratings are generally substantially higher than those enjoyed by lower income groups. In absolute terms the total savings from current VAT concessions enjoyed by the high and very high expenditure groups are estimated to have exceeded that accruing to the very low and low expenditure groups by almost R2 825 million in 20066. It should be noted that suppliers of maize meal and fresh milk benefit more from the current zero-rating than consumers, whereas the bulk of the zero-rating benefits in respect of rice and brown bread accrue to consumers.

Efficacy of VAT zero-ratings It needs to be noted, however, that revenue lost through zero-rating has to be made up elsewhere, most probably through a higher VAT standard rate or higher personal income taxes.

Arguments in favour of VAT zero-rating are based on the assumption that it results in lower absolute and relative prices of zero-rated goods than would have been obtained otherwise. But it is unrealistic to assume that the full benefit of zero-rating will accrue to the consumer in the form of lower prices. The extent of the price change will depend on the market structure and the relevant price elasticities of supply and demand. Even when the differential tax treatment of goods has significant immediate effects on relative prices, these effects normally diminish over time as shifts in demand from taxed goods to non-taxed substitutes tend to raise the prices of non-taxed goods. Also, a significant number of poor consumers purchase their basic necessities from informal businesses that are not VAT vendors or businesses that are subject to limited competition. This is true especially in rural areas, but also applies to urban informal settlements where consumers effectively have limited alternative sources of supply. In such cases the benefits of a VAT zero-rating are unlikely to be passed on to consumers. A prime example is paraffin, where very little of the VAT zero-rating benefit has been passed on to the poor despite the subsequent price regulation measures - the nationally prescribed maximum retail price.

Implications for tax compliance and administration Differentiated VAT rates involve an increase in compliance costs for businesses, particularly small businesses. A firm that deals in products with different rates, for example, a grocer that sells zero-rated milk along with standard rated soft drinks, has to keep separate accounts for the different rated items. International experience indicates that firms with multiple-rate outputs have up to double the compliance costs of firms with single-rate outputs7.

4. Katz Commission: Interim Report of the Commission of Inquiry into certain aspects of the Tax Structure of South

Africa (1994) pg 113 5. National Treasury: The VAT Treatment of Merit Goods and Services (2007) pg 115. 6. Ibid. 7. Cnossen S.: VAT in South Africa: Single, Dual or Multiple Rate Structure? (1999) pg. 8.

2008 TAX STATISTICS

118

It is apparent that relief through VAT zero-rating assists the poor modestly in absolute rand terms, while benefiting the non-poor by substantially greater amounts. There are compelling arguments against further VAT zero-rating of goods in a context where expenditure programmes can provide effective relief from poverty and where such programmes are under-funded or not appropriately targeted.

The impact of VAT on the poor should be considered alongside other components of public expenditure and other forms of tax, most notably the income tax system which is in its design infinitely more suited to address the distributional objectives of government. Further attempts to provide relief to the poor through VAT exemptions and zero-ratings are likely to be both unsound in terms of tax policy and ineffective in terms of social policy. Instead of trying to amend and distort the VAT system, its strengths should be used to generate revenue that will enable the government to help the poor in more effective ways, such as targeted expenditure programmes in the form of social grants. This would be a more positive approach than manipulating VAT to the point where its merits as a revenue-productive, neutral tax instrument are eroded8. 8. Tait A.: Value-Added Tax: International Practice and Problems, IMF (1991) pg. 44

•

Tables

Table 4.1.1 Domestic VAT: Payments and refunds by sector, 2002/03 – 2005/06 ............... 119 Table 4.1.2 Domestic VAT: Payments and refunds by sector, 2002/03 – 2005/06 [percentage of

total]............................................................................................................................. 120

Table 4.2.1 Domestic VAT: Payments and refunds by payment category, 2002/03 – 2005/06.................................................................................................................... 121

Table 4.2.2 Domestic VAT: Payments and refunds by sector (for vendors that submit monthly returns), 2002/03 – 2005/06......................................................................................... 122

Table 4.2.3 Domestic VAT: Payments and refunds by sector (for vendors that submit bi-monthly returns in January), 2002/03 – 2005/06........................................................................ 123

Table 4.2.4 Domestic VAT: Payments and refunds by sector (for vendors that submit bi-monthly returns in February), 2002/03 – 2005/06...................................................................... 124

Table 4.2.5 Domestic VAT: Payments and refunds by sector (for vendors that submit quarterly, bi-annually, annually returns), 2002/03 – 2005/06 ...................................................... 125

Table 4.3.1 Domestic VAT: Payments and refunds by type of enterprise, 2002/03 – 2005/06.................................................................................................................... 126

Table 4.4.1 Domestic VAT: Vendors per annualised turnover (payments and refunds), 2006/07.................................................................................................................... 127

Table 4.5.1 Household consumption expenditure by main expenditure group and income deciles, 2005/06 ...................................................................................................... 128

Table 4.5.2 Household consumption expenditure by third expenditure group and income deciles for Food, beverages and tobacco, 2005/06................................................................... 129

Table 4.5.3 Household consumption expenditure by third expenditure group and income deciles for Food, beverages and tobacco, 2005/06 [percentage across deciles]....................... 130

Tabl

e 4.

1.1:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by s

ecto

r, 20

02/0

3 –

2005

/06

Sect

or20

02/0

320

03/0

420

04/0

520

05/0

6N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)A

genc

ies

and

othe

r ser

vice

s33

727

6

025

-4 4

7035

994

7

306

-4 2

8337

316

8

161

-4 5

7943

040

10

652

-5

378

Agr

icul

ture

, for

estry

and

fish

ing

75 2

53

4 14

3

-4

236

75 9

57

3 89

1

-4

436

76 3

89

4 15

5

-4

768

80 0

28

5 41

2

-6

113

Bric

ks, c

eram

ic, g

lass

, cem

ent a

nd s

imila

r pro

duct

s1

772

409

-1

191

785

488

-1

291

936

548

-2

292

448

723

-3

45

Cat

erin

g an

d ac

com

mod

atio

n15

853

1

235

-202

16 4

16

1 37

1

-2

9717

267

1

555

-356

20 5

45

2 00

1

-4

62

Che

mic

als

and

chem

ical

, rub

ber a

nd p

last

ic p

rodu

cts

4 34

9

2

337

-1 3

644

443

2 50

3

-1

351

4 53

8

2

599

-1 2

584

885

2 78

7

-1

237

Clo

thin

g an

d fo

otw

ear

2 31

9

49

5

-193

2 30

2

61

5

-143

2 29

3

63

6

-140

2 36

0

61

9

-80

Coa

l and

pet

role

um p

rodu

cts

568

54

7

-831

573

1

071

-1 2

7360

3

1 71

3

-2

033

761

2

870

-2 7

67

Con

stru

ctio

n32

535

3

224

-1 0

3735

349

3

797

-1 0

6037

664

4

574

-1 3

7947

785

6

901

-1 9

30

Edu

catio

nal s

ervi

ces

1 86

3

16

5

-93

2 03

5

22

1

-193

2 12

2

26

9

-170

2 47

4

30

9

-139

Ele

ctric

ity, g

as a

nd w

ater

818

2

608

-182

885

2

502

-150

925

2

395

-110

1 11

7

2

123

-546

Fina

ncin

g, in

sura

nce,

real

est

ate

and

busi

ness

ser

vice

s13

4 60

5

21 6

26

-7 0

9714

4 61

6

25 1

01

-7 7

1915

8 25

0

29 4

56

-8 9

5920

1 01

2

37 9

09

-13

125

Food

, drin

k an

d to

bacc

o4

090

4 19

3

-1

720

4 09

1

4

419

-1 5

164

237

5 44

3

-1

435

4 80

5

5

884

-1 4

55

Leat

her,

leat

her g

oods

and

fur (

excl

. foo

twea

r and

clo

thin

g)37

4

105

-9

736

9

108

-6

638

4

114

-8

839

6

96

-5

9

Long

term

insu

ranc

e50

8

1 59

9

-4

1842

7

1 57

8

-4

6242

8

1 43

2

-7

4162

5

883

-1

372

Mac

hine

ry a

nd re

late

d ite

ms

9 41

4

2

571

-1 0

129

559

2 82

4

-8

489

835

3 05

4

-8

7410

749

3

438

-1 1

72

Med

ical

, den

tal a

nd o

ther

hea

lth a

nd v

eter

inar

y se

rvic

es16

585

2

135

-261

16 8

08

2 45

2

-1

6016

973

2

800

-138

17 9

08

3 33

6

-1

98

Met

al8

159

2 62

6

-2

148

8 16

6

2

643

-2 5

878

316

3 54

6

-2

624

8 94

5

3

558

-4 2

72

Min

ing

and

quar

ryin

g2

341

2 27

6

-8

869

2 42

7

2

430

-10

012

2 57

2

2

686

-9 7

573

113

5 00

5

-1

4 16

8

Oth

er m

anuf

actu

ring

indu

strie

s3

505

703

-1

174

3 57

6

83

2

-989

3 71

1

94

5

-1 0

344

164

1 07

4

-1

384

Pap

er, p

rintin

g an

d pu

blis

hing

4 59

7

1

445

-410

4 64

6

1

561

-406

4 84

1

1

706

-467

5 25

8

2

011

-494

Per

sona

l and

hou

seho

ld s

ervi

ces

3 90

0

26

5

-24

4 04

1

28

7

-29

4 31

3

34

4

-32

5 23

6

40

3

-48

Rec

reat

ion

and

cultu

ral s

ervi

ces

3 83

9

82

9

-215

3 93

8

89

5

-225

4 09

1

93

4

-284

4 57

9

1

237

-243

Res

earc

h an

d sc

ient

ific

inst

itute

s53

6

131

-1

0655

7

176

-1

0459

6

149

-1

2770

9

301

-7

4

Ret

ail t

rade

57 8

74

5 26

3

-2

343

58 3

14

6 18

3

-2

104

58 9

76

6 94

7

-2

470

64 5

81

8 54

8

-2

758

Sci

entif

ic, o

ptic

al a

nd s

imila

r equ

ipm

ent

768

15

3

-120

773

20

9

-89

798

18

7

-106

870

23

7

-91

Soc

ial a

nd re

late

d co

mm

unity

ser

vice

s2

436

174

-1

762

476

180

-2

172

549

212

-2

242

776

260

-2

11

Spe

cial

ised

repa

ir se

rvic

es10

783

70

7

-504

10 8

58

739

-2

1510

940

87

1

-172

11 6

06

1 05

0

-1

41

Text

iles

1 53

2

52

2

-282

1 57

4

59

0

-185

1 59

4

59

8

-181

1 68

7

56

8

-231

Tran

spor

t equ

ipm

ent

1 06

5

21

3

-274

1 10

7

22

8

-276

1 20

3

26

2

-289

1 44

4

36

4

-291

Tran

spor

t, st

orag

e an

d co

mm

unic

atio

ns14

973

5

977

-3 9

0715

299

7

200

-3 8

6016

270

8

011

-4 0

8119

126

9

195

-4 0

08

Veh

icle

s, p

arts

and

acc

esso

ries

5 04

7

1

852

-4 5

055

178

2 07

9

-4

009

5 31

4

2

568

-4 0

185

987

2 70

0

-5

987

Who

lesa

le tr

ade

28 6

27

4 64

4

-3

425

29 4

44

5 36

0

-2

882

30 2

85

5 80

7

-2

886

33 5

14

6 82

4

-3

650

Woo

d, w

ood

prod

ucts

and

furn

iture

3 08

9

42

7

-246

3 18

7

46

6

-245

3 31

4

60

4

-262

3 86

2

77

4

-195

Oth

er1

32

6

-633

16

-6

22

13

-422

10

-1

0

Tota

l48

7 73

6

81 6

31

-52

067

507

203

92

319

-5

2 52

853

0 86

5

105

294

-5

6 27

661

8 41

7

130

061

-7

4 63

61.

Inc

lude

s w

here

the

sect

or w

as in

dica

ted

as O

ther

or w

here

the

sect

or w

as le

ft bl

ank

on th

e re

turn

.

CHAPTER 4: VALUE-ADDED TAX

119

Tabl

e 4.

1.2:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by s

ecto

r, 20

02/0

3 –

2005

/06

[per

cent

age

of to

tal]

Sect

or20

02/0

320

03/0

420

04/0

520

05/0

6N

umbe

r of

vend

ors

Paym

ents

Ref

unds

Num

ber o

f ve

ndor

sPa

ymen

tsR

efun

dsN

umbe

r of

vend

ors

Paym

ents

Ref

unds

Num

ber o

f ve

ndor

sPa

ymen

tsR

efun

ds

Age

ncie

s an

d ot

her s

ervi

ces

6.9%

7.4%

8.6%

7.1%

7.9%

8.2%

7.0%

7.8%

8.1%

7.0%

8.2%

7.2%

Agr

icul

ture

, for

estry

and

fish

ing

15.4

%5.

1%8.

1%15

.0%

4.2%

8.4%

14.4

%3.

9%8.

5%12

.9%

4.2%

8.2%

Bric

ks, c

eram

ic, g

lass

, cem

ent a

nd s

imila

r pro

duct

s0.

4%0.

5%0.

2%0.

4%0.

5%0.

2%0.

4%0.

5%0.

4%0.

4%0.

6%0.

5%

Cat

erin

g an

d ac

com

mod

atio

n3.

3%1.

5%0.

4%3.

2%1.

5%0.

6%3.

3%1.

5%0.

6%3.

3%1.

5%0.

6%

Che

mic

als

and

chem

ical

, rub

ber a

nd p

last

ic p

rodu

cts

0.9%

2.9%

2.6%

0.9%

2.7%

2.6%

0.9%

2.5%

2.2%

0.8%

2.1%

1.7%

Clo

thin

g an

d fo

otw

ear

0.5%

0.6%

0.4%

0.5%

0.7%

0.3%

0.4%

0.6%

0.2%

0.4%

0.5%

0.1%

Coa

l and

pet

role

um p

rodu

cts

0.1%

0.7%

1.6%

0.1%

1.2%

2.4%

0.1%

1.6%

3.6%

0.1%

2.2%

3.7%

Con

stru

ctio

n6.

7%3.

9%2.

0%7.

0%4.

1%2.

0%7.

1%4.

3%2.

5%7.

7%5.

3%2.

6%

Edu

catio

nal s

ervi

ces

0.4%

0.2%

0.2%

0.4%

0.2%

0.4%

0.4%

0.3%

0.3%

0.4%

0.2%

0.2%

Ele

ctric

ity, g

as a

nd w

ater

0.2%

3.2%

0.3%

0.2%

2.7%

0.3%

0.2%

2.3%

0.2%

0.2%

1.6%

0.7%

Fina

ncin

g, in

sura

nce,

real

est

ate

and

busi

ness

ser

vice

s27

.6%

26.5

%13

.6%

28.5

%27

.2%

14.7

%29

.8%

28.0

%15

.9%

32.5

%29

.1%

17.6

%

Food

, drin

k an

d to

bacc

o0.

8%5.

1%3.

3%0.

8%4.

8%2.

9%0.

8%5.

2%2.

6%0.

8%4.

5%2.

0%

Leat

her,

leat

her g

oods

and

fur (

excl

. foo

twea

r and

clo

thin

g)0.

1%0.

1%0.

2%0.

1%0.

1%0.

1%0.

1%0.

1%0.

2%0.

1%0.

1%0.

1%

Long

term

insu

ranc

e0.

1%2.

0%0.

8%0.

1%1.

7%0.

9%0.

1%1.

4%1.

3%0.

1%0.

7%1.

8%

Mac

hine

ry a

nd re

late

d ite

ms

1.9%

3.2%

1.9%

1.9%

3.1%

1.6%

1.9%

2.9%

1.6%

1.7%

2.6%

1.6%

Med

ical

, den

tal a

nd o

ther

hea

lth a

nd v

eter

inar

y se

rvic

es3.

4%2.

6%0.

5%3.

3%2.

7%0.

3%3.

2%2.

7%0.

2%2.

9%2.

6%0.

3%

Met

al1.

7%3.

2%4.

1%1.

6%2.

9%4.

9%1.

6%3.

4%4.

7%1.

4%2.

7%5.

7%

Min

ing

and

quar

ryin

g0.

5%2.

8%17

.0%

0.5%

2.6%

19.1

%0.

5%2.

6%17

.3%

0.5%

3.8%

19.0

%

Oth

er m

anuf

actu

ring

indu

strie

s0.

7%0.

9%2.

3%0.

7%0.

9%1.

9%0.

7%0.

9%1.

8%0.

7%0.

8%1.

9%

Pap

er, p

rintin

g an

d pu

blis

hing

0.9%

1.8%

0.8%

0.9%

1.7%

0.8%

0.9%

1.6%

0.8%

0.9%

1.5%

0.7%

Per

sona

l and

hou

seho

ld s

ervi

ces

0.8%

0.3%

0.0%

0.8%

0.3%

0.1%

0.8%

0.3%

0.1%

0.8%

0.3%

0.1%

Rec

reat

ion

and

cultu

ral s

ervi

ces

0.8%

1.0%

0.4%

0.8%

1.0%

0.4%

0.8%

0.9%

0.5%

0.7%

1.0%

0.3%

Res

earc

h an

d sc

ient

ific

inst

itute

s0.

1%0.

2%0.

2%0.

1%0.

2%0.

2%0.

1%0.

1%0.

2%0.

1%0.

2%0.

1%

Ret

ail t

rade

11.9

%6.

4%4.

5%11

.5%

6.7%

4.0%

11.1

%6.

6%4.

4%10

.4%

6.6%

3.7%

Sci

entif

ic, o

ptic

al a

nd s

imila

r equ

ipm

ent

0.2%

0.2%

0.2%

0.2%

0.2%

0.2%

0.2%

0.2%

0.2%

0.1%

0.2%

0.1%

Soc

ial a

nd re

late

d co

mm

unity

ser

vice

s0.

5%0.

2%0.

3%0.

5%0.

2%0.

4%0.

5%0.

2%0.

4%0.

4%0.

2%0.

3%

Spe

cial

ised

repa

ir se

rvic

es2.

2%0.

9%1.

0%2.

1%0.

8%0.

4%2.

1%0.

8%0.

3%1.

9%0.

8%0.

2%

Text

iles

0.3%

0.6%

0.5%

0.3%

0.6%

0.4%

0.3%

0.6%

0.3%

0.3%

0.4%

0.3%

Tran

spor

t equ

ipm

ent

0.2%

0.3%

0.5%

0.2%

0.2%

0.5%

0.2%

0.2%

0.5%

0.2%

0.3%

0.4%

Tran

spor

t, st

orag

e an

d co

mm

unic

atio

ns3.

1%7.

3%7.

5%3.

0%7.

8%7.

3%3.

1%7.

6%7.

3%3.

1%7.

1%5.

4%

Veh

icle

s, p

arts

and

acc

esso

ries

1.0%

2.3%

8.7%

1.0%

2.3%

7.6%

1.0%

2.4%

7.1%

1.0%

2.1%

8.0%

Who

lesa

le tr

ade

5.9%

5.7%

6.6%

5.8%

5.8%

5.5%

5.7%

5.5%

5.1%

5.4%

5.2%

4.9%

Woo

d, w

ood

prod

ucts

and

furn

iture

0.6%

0.5%

0.5%

0.6%

0.5%

0.5%

0.6%

0.6%

0.5%

0.6%

0.6%

0.3%

Oth

er0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%

Tota

l10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%

Perc

enta

ge o

f tot

al

2008 TAX STATISTICS

120

Tabl

e 4.

2.1:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by p

aym

ent c

ateg

ory,

200

2/03

– 2

005/

06Pa

ymen

t cat

egor

y20

02/0

320

03/0

420

04/0

520

05/0

6N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)A

: M

onth

ly24

159

56 6

75

-4

2 57

124

524

64 8

00

-4

2 25

025

035

74 3

28

-4

4 34

931

016

89 7

03

-5

7 85

0

B:

Bi-M

onth

ly (J

an)

185

556

10

601

-3 6

1019

2 63

7

11 7

46

-3

895

203

721

13

370

-4 7

9123

8 49

7

17 3

32

-6

736

C:

Bi-M

onth

ly (F

eb)

245

799

13

896

-5 5

9025

8 62

1

15 4

15

-6

091

271

438

17

295

-6 8

6931

8 17

7

22 5

99

-9

716

D:

4 M

onth

ly–

–

–

–

–

–

–

–

–

1

063

24

-12

E:

6 M

onth

ly31

196

444

-289

30 5

05

33

9

-2

8729

776

284

-263

28 4

56

38

2

-3

18

F:A

nnua

lly1

026

15

-791

6

20

-589

5

18

-41

208

21

-5

Tota

l48

7 73

6

81 6

31

-5

2 06

750

7 20

3

92 3

19

-5

2 52

853

0 86

5

105

294

-5

6 27

661

8 41

7

130

061

-7

4 63

6

A:

Mon

thly

5.0%

69.4

%81

.8%

4.8%

70.2

%80

.4%

4.7%

70.6

%78

.8%

5.0%

69.0

%77

.5%

B:

Bi-M

onth

ly (J

an)

38.0

%13

.0%

6.9%

38.0

%12

.7%

7.4%

38.4

%12

.7%

8.5%

38.6

%13

.3%

9.0%

C:

Bi-M

onth

ly (F

eb)

50.4

%17

.0%

10.7

%51

.0%

16.7

%11

.6%

51.1

%16

.4%

12.2

%51

.5%

17.4

%13

.0%

D:

4 M

onth

ly0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

0%0.

2%0.

0%0.

0%

E:

6 M

onth

ly6.

4%0.

5%0.

6%6.

0%0.

4%0.

5%5.

6%0.

3%0.

5%4.

6%0.

3%0.

4%

F:A

nnua

lly0.

2%0.

0%0.

0%0.

2%0.

0%0.

0%0.

2%0.

0%0.

0%0.

2%0.

0%0.

0%

Tota

l10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%10

0.0%

100.

0%

Perc

enta

ge o

f tot

al

CHAPTER 4: VALUE-ADDED TAX

121

Tabl

e 4.

2.2:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by s

ecto

r (fo

r ven

dors

that

sub

mit

mon

thly

retu

rns)

, 200

2/03

– 2

005/

06Se

ctor

2002

/03

2003

/04

2004

/05

2005

/06

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Age

ncie

s an

d ot

her s

ervi

ces

2 21

6

4

035

-3 7

882

284

5 00

5

-3

544

2 27

4

5

592

-3 7

632

645

7 42

6

-4

399

Agr

icul

ture

, for

estry

and

fish

ing

1 11

6

1

778

-1 5

901

140

1 67

5

-1

588

1 14

5

1

988

-1 7

911

338

2 47

7

-2

330

Bric

ks, c

eram

ic, g

lass

, cem

ent a

nd s

imila

r pro

duct

s14

1

291

-9

513

0

349

-1

0713

9

378

-1

8718

6

516

-2

89

Cat

erin

g an

d ac

com

mod

atio

n48

5

608

-4

047

7

651

-8

746

9

722

-9

353

2

869

-8

8

Che

mic

als

and

chem

ical

, rub

ber a

nd p

last

ic p

rodu

cts

618

1

969

-1 2

5062

4

2 09

5

-1

251

612

2

155

-1 1

5970

3

2 29

9

-1

122

Clo

thin

g an

d fo

otw

ear

165

29

9

-157

161

41

1

-117

162

43

0

-111

169

42

0

-55

Coa

l and

pet

role

um p

rodu

cts

105

52

3

-815

105

1

043

-1 2

5111

4

1 68

1

-2

012

143

2

826

-2 7

41

Con

stru

ctio

n1

390

1 56

1

-6

351

368

1 89

9

-5

481

393

2 32

9

-7

181

888

3 64

1

-1

002

Edu

catio

nal s

ervi

ces

67

69

-60

67

83

-140

70

10

7

-117

74

12

5

-94

Ele

ctric

ity, g

as a

nd w

ater

64

2

554

-158

65

2

441

-129

69

2

335

-74

93

2

039

-522

Fina

ncin

g, in

sura

nce,

real

est

ate

and

busi

ness

ser

vice

s5

044

13 8

42

-4 6

975

385

16 2

29

-4 9

625

731

18 9

78

-5 2

347

756

23 2

20

-6 7

69

Food

, drin

k an

d to

bacc

o59

1

3 98

3

-1

591

566

4

185

-1 3

7855

7

5 18

6

-1

289

635

5

590

-1 2

90

Leat

her,

leat

her g

oods

and

fur (

excl

. foo

twea

r and

clo

thin

g)41

70

-9

140

72

-5

840

78

-7

842

63

-5

1

Long

term

insu

ranc

e20

7

1 55

6

-3

5518

9

1 53

7

-3

7318

9

1 40

1

-6

0540

1

851

-1

204

Mac

hine

ry a

nd re

late

d ite

ms

671

1

808

-843

676

1

989

-708

664

2

154

-732

777

2

381

-999

Med

ical

, den

tal a

nd o

ther

hea

lth a

nd v

eter

inar

y se

rvic

es41

4

1 03

5

-1

9540

7

1 26

8

-8

440

1

1 49

6

-6

345

4

1 68

3

-9

5

Met

al77

3

1 85

1

-2

055

770

1

815

-2 4

9976

2

2 66

0

-2

524

901

2

517

-4 1

13

Min

ing

and

quar

ryin

g47

2

1 99

2

-8

702

498

2

147

-9 8

5451

9

2 37

4

-9

583

656

4

607

-13

867

Oth

er m

anuf

actu

ring

indu

strie

s29

8

486

-1

116

309

58

9

-932

308

67

9

-965

347

75

4

-1 3

13

Pap

er, p

rintin

g an

d pu

blis

hing

344

1

089

-340

337

1

162

-342

337

1

271

-375

399

1

536

-424

Per

sona

l and

hou

seho

ld s

ervi

ces

94

84

-391

99

-1

91

12

3

-397

127

-5

Rec

reat

ion

and

cultu

ral s

ervi

ces

195

58

4

-108

192

60

0

-111

192

63

1

-176

229

86

4

-132

Res

earc

h an

d sc

ient

ific

inst

itute

s41

81

-9

043

119

-8

340

86

-1

0247

232

-4

6

Ret

ail t

rade

3 08

4

3

470

-1 7

343

100

4 18

2

-1

509

3 22

7

4

717

-1 7

854

059

5 88

3

-1

929

Sci

entif

ic, o

ptic

al a

nd s

imila

r equ

ipm

ent

55

94

-110

54

14

1

-77

54

11

7

-95

68

15

4

-74

Soc

ial a

nd re

late

d co

mm

unity

ser

vice

s21

7

41

-8

821

7

50

-1

1522

1

62

-1

1322

2

78

-8

0

Spe

cial

ised

repa

ir se

rvic

es26

3

203

-4

5525

2

188

-1

6824

3

254

-1

1527

5

302

-6

3

Text

iles

202

39

3

-249

198

45

5

-160

190

46

1

-158

220

43

1

-197

Tran

spor

t equ

ipm

ent

84

15

0

-231

84

16

5

-218

85

19

1

-234

112

26

3

-230

Tran

spor

t, st

orag

e an

d co

mm

unic

atio

ns1

170

5 07

6

-3

391

1 12

6

6

275

-3 3

121

169

6 94

3

-3

534

1 32

2

7

853

-3 2

88

Veh

icle

s, p

arts

and

acc

esso

ries

597

1

567

-4 4

4960

1

1 77

0

-3

962

605

2

226

-3 9

6374

5

2 32

9

-5

912

Who

lesa

le tr

ade

2 72

5

3

308

-2 8

882

751

3 85

5

-2

377

2 74

5

4

177

-2 3

753

246

4 89

4

-2

979

Woo

d, w

ood

prod

ucts

and

furn

iture

207

22

3

-199

214

24

2

-197

215

33

6

-220

232

44

6

-139

Oth

er1

3

3

-53

13

-6

3

9

-43

6

-1

0

Tota

l24

159

56

675

-4

2 57

124

524

64

800

-4

2 25

025

035

74

328

-4

4 34

931

016

89

703

-5

7 85

01.

Inc

lude

s w

here

the

sect

or w

as in

dica

ted

as O

ther

or w

here

the

sect

or w

as le

ft bl

ank

on th

e re

turn

.

2008 TAX STATISTICS

122

Tabl

e 4.

2.3:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by s

ecto

r (fo

r ven

dors

that

sub

mit

bi-m

onth

ly re

turn

s in

Jan

uary

), 20

02/0

3 –

2005

/06

Sect

or20

02/0

320

03/0

420

04/0

520

05/0

6N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)A

genc

ies

and

othe

r ser

vice

s13

863

87

0

-317

14 6

99

1 02

7

-3

3015

410

1

158

-360

17 8

30

1 43

8

-4

40

Agr

icul

ture

, for

estry

and

fish

ing

13 9

60

554

-7

0314

359

53

5

-766

14 8

05

555

-8

5016

096

70

7

-980

Bric

ks, c

eram

ic, g

lass

, cem

ent a

nd s

imila

r pro

duct

s72

9

47

-9

738

54

-881

2

69

-1

897

9

85

-2

3

Cat

erin

g an

d ac

com

mod

atio

n6

598

265

-7

06

801

304

-8

77

107

356

-1

128

454

475

-1

51

Che

mic

als

and

chem

ical

, rub

ber a

nd p

last

ic p

rodu

cts

1 64

8

16

2

-47

1 65

7

17

9

-40

1 70

2

19

2

-45

1 81

2

22

0

-52

Clo

thin

g an

d fo

otw

ear

946

90

-15

926

94

-10

921

96

-11

962

92

-12

Coa

l and

pet

role

um p

rodu

cts

204

11

-819

7

12

-1

021

8

17

-9

269

21

-8

Con

stru

ctio

n13

597

72

8

-151

14 7

80

833

-2

1515

764

98

3

-267

19 9

38

1 46

3

-3

95

Edu

catio

nal s

ervi

ces

774

44

-18

857

62

-27

902

64

-31

1 06

3

68

-27

Ele

ctric

ity, g

as a

nd w

ater

303

22

-12

355

28

-837

1

25

-1

246

4

34

-1

1

Fina

ncin

g, in

sura

nce,

real

est

ate

and

busi

ness

ser

vice

s56

133

3

466

-970

59 9

52

3 88

2

-1

127

66 3

07

4 62

8

-1

650

84 0

54

6 52

7

-2

868

Food

, drin

k an

d to

bacc

o1

502

93

-5

31

468

99

-5

41

573

110

-5

91

743

121

-8

8

Leat

her,

leat

her g

oods

and

fur (

excl

. foo

twea

r and

clo

thin

g)13

9

14

-2

135

13

-214

1

16

-3

141

14

-5

Long

term

insu

ranc

e14

4

13

-3

611

0

16

-5

710

4

11

-7

199

13

-8

0

Mac

hine

ry a

nd re

late

d ite

ms

3 97

4

35

4

-74

4 02

1

39

8

-63

4 22

1

42

7

-61

4 55

8

50

7

-74

Med

ical

, den

tal a

nd o

ther

hea

lth a

nd v

eter

inar

y se

rvic

es7

386

510

-3

07

456

550

-3

57

543

607

-3

87

877

741

-4

4

Met

al3

382

349

-3

63

344

372

-3

63

422

404

-4

23

572

475

-6

4

Min

ing

and

quar

ryin

g75

2

116

-5

279

0

118

-4

884

6

128

-8

11

000

159

-1

27

Oth

er m

anuf

actu

ring

indu

strie

s1

469

98

-2

61

424

111

-2

51

533

118

-3

11

675

145

-3

2

Pap

er, p

rintin

g an

d pu

blis

hing

2 01

0

16

1

-33

2 01

0

18

3

-34

2 09

8

20

4

-56

2 25

9

22

8

-35

Per

sona

l and

hou

seho

ld s

ervi

ces

1 66

0

91

-91

742

85

-1

21

868

105

-1

22

233

123

-1

6

Rec

reat

ion

and

cultu

ral s

ervi

ces

1 59

7

11

3

-49

1 63

6

14

0

-50

1 73

9

13

7

-52

1 89

4

15

7

-57

Res

earc

h an

d sc

ient

ific

inst

itute

s22

4

22

-1

123

4

27

-1

526

0

31

-1

430

3

31

-9

Ret

ail t

rade

24 2

86

784

-2

5424

211

87

2

-249

24 3

32

988

-2

8926

316

1

157

-360

Sci

entif

ic, o

ptic

al a

nd s

imila

r equ

ipm

ent

331

30

-632

1

33

-6

327

31

-535

7

37

-7

Soc

ial a

nd re

late

d co

mm

unity

ser

vice

s1

137

57

-4

31

153

60

-5

31

181

73

-6

21

291

83

-7

1

Spe

cial

ised

repa

ir se

rvic

es4

712

228

-2

34

668

251

-2

04

742

278

-2

55

009

333

-3

1

Text

iles

621

58

-12

619

61

-10

618

59

-10

662

63

-14

Tran

spor

t equ

ipm

ent

434

30

-21

441

27

-27

492

31

-26

574

45

-26

Tran

spor

t, st

orag

e an

d co

mm

unic

atio

ns6

080

414

-2

346

210

417

-2

066

581

479

-2

097

709

593

-3

04

Veh

icle

s, p

arts

and

acc

esso

ries

2 03

6

12

5

-23

2 11

4

14

0

-22

2 13

1

15

3

-25

2 33

7

16

8

-30

Who

lesa

le tr

ade

11 6

73

596

-2

3811

905

66

6

-221

12 2

89

722

-2

3313

393

87

0

-271

Woo

d, w

ood

prod

ucts

and

furn

iture

1 23

4

86

-24

1 28

4

95

-22

1 35

1

11

6

-19

1 56

4

14

0

-24

Oth

er1

18

0

-020

1

-0

10

0

-010

0

-0

Tota

l18

5 55

6

10 6

01

-3 6

1019

2 63

7

11 7

46

-3 8

9520

3 72

1

13 3

70

-4 7

9123

8 49

7

17 3

32

-6 7

361.

Inc

lude

s w

here

the

sect

or w

as in

dica

ted

as O

ther

or w

here

the

sect

or w

as le

ft bl

ank

on th

e re

turn

.

CHAPTER 4: VALUE-ADDED TAX

123

Tabl

e 4.

2.4:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by s

ecto

r (fo

r ven

dors

that

sub

mit

bi-m

onth

ly re

turn

s in

Feb

ruar

y), 2

002/

03 –

200

5/06

Sect

or20

02/0

320

03/0

420

04/0

520

05/0

6N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)A

genc

ies

and

othe

r ser

vice

s17

641

1

119

-364

19 0

00

1 27

2

-4

0919

618

1

409

-455

22 4

77

1 78

6

-5

38

Agr

icul

ture

, for

estry

and

fish

ing

28 7

41

1 36

3

-1

651

29 7

13

1 33

7

-1

795

30 4

29

1 32

5

-1

864

33 7

79

1 84

0

-2

481

Bric

ks, c

eram

ic, g

lass

, cem

ent a

nd s

imila

r pro

duct

s90

2

71

-1

691

7

85

-1

398

5

101

-2

41

280

122

-3

3

Cat

erin

g an

d ac

com

mod

atio

n8

767

361

-9

29

134

414

-1

239

685

474

-1

5011

509

65

4

-223

Che

mic

als

and

chem

ical

, rub

ber a

nd p

last

ic p

rodu

cts

2 08

3

20

7

-67

2 16

2

22

8

-59

2 22

4

25

1

-55

2 36

8

26

9

-63

Clo

thin

g an

d fo

otw

ear

1 20

8

10

6

-21

1 21

5

11

0

-15

1 21

0

11

1

-17

1 22

6

10

7

-13

Coa

l and

pet

role

um p

rodu

cts

259

13

-927

1

15

-1

227

0

16

-1

234

9

23

-1

7

Con

stru

ctio

n17

547

93

4

-251

19 2

00

1 06

5

-2

9720

505

1

263

-393

25 9

09

1 79

6

-5

33

Edu

catio

nal s

ervi

ces

1 02

1

51

-15

1 11

1

77

-26

1 15

0

98

-22

1 32

9

11

6

-18

Ele

ctric

ity, g

as a

nd w

ater

451

32

-12

465

32

-13

485

36

-24

559

50

-14

Fina

ncin

g, in

sura

nce,

real

est

ate

and

busi

ness

ser

vice

s72

778

4

310

-1 4

2778

643

4

979

-1 6

2785

596

5

839

-2 0

7210

7 87

6

8 13

5

-3

479

Food

, drin

k an

d to

bacc

o1

995

117

-7

62

055

134

-8

32

105

147

-8

72

421

173

-7

8

Leat

her,

leat

her g

oods

and

fur (

excl

. foo

twea

r and

clo

thin

g)19

4

21

-4

194

23

-520

3

20

-7

213

20

-4

Long

term

insu

ranc

e15

6

30

-2

712

7

25

-3

213

4

19

-6

612

5

19

-8

7

Mac

hine

ry a

nd re

late

d ite

ms

4 76

9

40

9

-95

4 86

2

43

8

-77

4 95

0

47

3

-81

5 40

0

55

0

-100

Med

ical

, den

tal a

nd o

ther

hea

lth a

nd v

eter

inar

y se

rvic

es8

784

591

-3

58

944

634

-4

19

029

696

-3

89

543

912

-5

8

Met

al4

004

427

-5

64

052

455

-5

24

132

482

-5

84

466

566

-9

5

Min

ing

and

quar

ryin

g1

117

168

-1

151

138

166

-1

101

206

184

-9

31

455

238

-1

74

Oth

er m

anuf

actu

ring

indu

strie

s1

737

119

-3

21

842

132

-3

31

869

148

-3

82

134

175

-3

9

Pap

er, p

rintin

g an

d pu

blis

hing

2 24

3

19

6

-36

2 29

9

21

5

-30

2 40

6

23

1

-35

2 59

2

24

7

-34

Per

sona

l and

hou

seho

ld s

ervi

ces

2 14

6

90

-12

2 20

8

10

3

-15

2 35

4

11

7

-17

2 89

5

15

3

-27

Rec

reat

ion

and

cultu

ral s

ervi

ces

2 04

7

13

2

-58

2 11

0

15

4

-63

2 16

0

16

7

-56

2 44

0

21

5

-54

Res

earc

h an

d sc

ient

ific

inst

itute

s27

1

27

-5

280

29

-629

6

32

-1

135

1

38

-1

9

Ret

ail t

rade

30 5

02

1 01

0

-3

5530

998

1

128

-346

31 4

15

1 24

2

-3

9734

115

1

506

-468

Sci

entif

ic, o

ptic

al a

nd s

imila

r equ

ipm

ent

382

29

-539

8

35

-6

417

39

-644

4

47

-1

0

Soc

ial a

nd re

late

d co

mm

unity

ser

vice

s1

081

76

-4

61

105

69

-4

91

146

77

-4

91

257

100

-6

0

Spe

cial

ised

repa

ir se

rvic

es5

807

276

-2

65

936

300

-2

75

954

339

-3

26

301

414

-4

7

Text

iles

709

70

-21

757

74

-15

786

79

-13

805

74

-21

Tran

spor

t equ

ipm

ent

545

33

-22

580

36

-31

624

40

-28

755

56

-35

Tran

spor

t, st

orag

e an

d co

mm

unic

atio

ns7

611

486

-2

807

955

508

-3

428

511

588

-3

3810

016

74

8

-416

Veh

icle

s, p

arts

and

acc

esso

ries

2 41

4

15

9

-33

2 46

3

17

0

-25

2 57

8

18

9

-30

2 90

0

20

2

-44

Who

lesa

le tr

ade

14 2

29

740

-3

0014

788

83

9

-284

15 2

50

908

-2

7716

821

1

059

-400

Woo

d, w

ood

prod

ucts

and

furn

iture

1 64

7

11

8

-23

1 68

9

13

0

-27

1 74

7

15

2

-24

2 05

8

18

7

-32

Oth

er1

11

3

-010

2

-0

9

3

-09

3

–

Tota

l24

5 79

9

13 8

96

-5 5

9025

8 62

1

15 4

15

-6 0

9127

1 43

8

17 2

95

-6 8

6931

8 17

7

22 5

99

-9 7

161.

Inc

lude

s w

here

the

sect

or w

as in

dica

ted

as O

ther

or w

here

the

sect

or w

as le

ft bl

ank

on th

e re

turn

.

2008 TAX STATISTICS

124

Tabl

e 4.

2.5:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by s

ecto

r (fo

r ven

dors

that

sub

mit

quar

terly

, bi-a

nnua

lly, a

nnua

lly re

turn

s), 2

002/

03 –

200

5/06

Sect

or20

02/0

320

03/0

420

04/0

520

05/0

6N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)N

umbe

r of

vend

ors

Paym

ents

(R

mill

ion)

Ref

unds

(R m

illio

n)A

genc

ies

and

othe

r ser

vice

s7

0

-0

11

2

-014

1

-0

88

2

-0

Agr

icul

ture

, for

estry

and

fish

ing

31 4

36

448

-2

9230

745

34

4

-288

30 0

10

286

-2

6428

815

38

8

-321

Bric

ks, c

eram

ic, g

lass

, cem

ent a

nd s

imila

r pro

duct

s–

–

–

–

–

–

–

–

–

3

0

-0

Cat

erin

g an

d ac

com

mod

atio

n3

2

-0

4

2

-16

2

-0

50

4

-1

Che

mic

als

and

chem

ical

, rub

ber a

nd p

last

ic p

rodu

cts

–

–

–

–

–

–

–

–

–

2

0

–

Clo

thin

g an

d fo

otw

ear

–

–

–

–

–

–

–

–

–

3

0

-0

Coa

l and

pet

role

um p

rodu

cts

–

–

–

–

–

–

1

–

-0–

–

–

Con

stru

ctio

n1

0

–

1

0

–

2

0

-0

50

1

-1

Edu

catio

nal s

ervi

ces

1

0

–

–

–

–

–

–

–

8

0

-0

Ele

ctric

ity, g

as a

nd w

ater

–

–

–

–

–

–

–

–

–

1

0

-0

Fina

ncin

g, in

sura

nce,

real

est

ate

and

busi

ness

ser

vice

s65

0

9

-3

636

11

-361

6

11

-3

1 32

6

27

-8

Food

, drin

k an

d to

bacc

o2

0

-0

2

0

-02

0

–

6

0

-0

Leat

her,

leat

her g

oods

and

fur (

excl

. foo

twea

r and

clo

thin

g)–

–

–

–

–

–

–

–

–

–

–

–

Long

term

insu

ranc

e1

0

-0

1

0

–

1

0

–

–

–

–

Mac

hine

ry a

nd re

late

d ite

ms

–

–

–

–

–

–

–

–

–

14

0

-0

Med

ical

, den

tal a

nd o

ther

hea

lth a

nd v

eter

inar

y se

rvic

es1

0

-0

1

–

-0–

–

–

34

1

-0

Met

al–

–

–

–

–

–

–

–

–

6

0

-0

Min

ing

and

quar

ryin

g–

–

–

1

0

–

1

0

–

2

0

–

Oth

er m

anuf

actu

ring

indu

strie

s1

–

-0

1

0

–

1

0

–

8

0

-0

Pap

er, p

rintin

g an

d pu

blis

hing

–

–

–

–

–

–

–

–

–

8

0

-0

Per

sona

l and

hou

seho

ld s

ervi

ces

–

–

–

–

–

–

–

–

–

11

0

-0

Rec

reat

ion

and

cultu

ral s

ervi

ces

–

–

–

–

–

–

–

–

–

16

0

-1

Res

earc

h an

d sc

ient

ific

inst

itute

s–

–

–

–

–

–

–

–

–

8

0

-0

Ret

ail t

rade

2

0

-05

0

-0

2

0

–

91

1

-1

Sci

entif

ic, o

ptic

al a

nd s

imila

r equ

ipm

ent

–

–

–

–

–

–

–

–

–

1

0

–

Soc

ial a

nd re

late

d co

mm

unity

ser

vice

s1

0

–

1

0

-01

0

–

6

0

-0

Spe

cial

ised

repa

ir se

rvic

es1

0

–

2

0

–

1

0

–

21

0

-0

Text

iles

–

–

–

–

–

–

–

–

–

–

–

–

Tran

spor

t equ

ipm

ent

2

0

–

2

0

–

2

0

–

3

0

-0

Tran

spor

t, st

orag

e an

d co

mm

unic

atio

ns11

2

0

-1

8

0

-09

1

-0

79

1

-0

Veh

icle

s, p

arts

and

acc

esso

ries

–

–

–

–

–

–

–

–

–

5

0

-0

Who

lesa

le tr

ade

–

–

–

–

–

–

1

0

–

54

1

-0

Woo

d, w

ood

prod

ucts

and

furn

iture

1

0

–

–

–

–

1

0

–

8

1

-0

Oth

er1

–

–

–

–

–

–

–

–

–

–

–

–

Tota

l32

222

45

9

-297

31 4

21

359

-2

9230

671

30

1

-267

30 7

27

427

-3

341.

Inc

lude

s w

here

the

sect

or w

as in

dica

ted

as O

ther

or w

here

the

sect

or w

as le

ft bl

ank

on th

e re

turn

.

CHAPTER 4: VALUE-ADDED TAX

125

Tabl

e 4.

3.1:

Dom

estic

VA

T: P

aym

ents

and

refu

nds

by ty

pe o

f ent

erpr

ise,

200

2/03

– 2

005/

06Ty

pe o

f ent

erpr

ise

2002

/03

2003

/04

2004

/05

2005

/06

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

Num

ber o

f ve

ndor

sPa

ymen

ts

(R m

illio

n)R

efun

ds(R

mill

ion)

A :

Indi

vidu

al14

2 58

1

3 82

8

-1

949

142

505

3

965

-2 1

1614

1 43

5

4 30

4

-2

129

147

566

5

384

-2 5

92

B :

Par

tner

ship

17 9

42

2

083

-1 2

6917

622

2 13

3

-1

419

17 4