VALUE CHAIN ANALYSIS OF THEARTISANAL FISHERIES - MAURITIUS

June 2012

REPORT/RAPPORT : SF/2012/8

EuropeanUnion

Funded by

Photo by Yann Yvergniaux

Implementation of a Regional Fisheries Stategy For The Eastern-Southern Africa And Indian Ocean Region

10th European Development FundAgreement No: RSO/FED/2009/021-330

“This publication has been produced with the assistance of the European Union. The contents of this publication are the sole responsibility of the author and can in no way be taken to the views of the European Union.”

Implementation of a Regional Fisheries StrategyFor The Eastern-Southern Africa and India Ocean Region

Programme pour la mise en oeuvre d'une stratégie de pêche pour laregion Afrique orientale-australe et Océan indien

Value Chain Assessment of the Artisanal Fisheries - Mauritius

SF/2012/8Soobaschand Sweenarain

This report has been prepared with the technical assistance ofLe présent rapport a été réalisé par l'assistance technique de

Juin 2012

EuropeanUnion

Funded by

Implementation of a Regional Fisheries Stategy For The Eastern-Southern Africa And Indian Ocean Region

10th European Development FundAgreement No: RSO/FED/2009/021-330

“This publication has been produced with the assistance of the European Union. The contents of this publication are the sole responsibility of the author and can in no way be taken to the views of the European Union.”

Table of Content

List of Abbreviations & Acronyms …………………................................................ 5

Acknowledgements……………………………………………................................... 6

Preface……………………………………………………………………....................... 7

Layman’s Summary………………………………………………................................ 11

Résumé des Non-initiés……………………………………….................................... 11

Executive Summary……………………………………………................................... 11

Résumé Analytique…………………………………………….................................... 17

1.0 Introduction.................................................................................................................. 25 1.1 Work Plan and Implementation ........................................................................... 25 1.2 Methodology.... .................................................................................................... 26 1.3 Analysis................................................................................................................ 27

2.0 Overview of the Artisanal Fisheries Sub-sector.................................................... 28 2.1 Fisheries Policies................................................................................................... 28 2.2 Supporting Institutions ....................................................................................... 28 2.3 On-going Programmes in the Artisanal Fisheries .................................................. 29 2.4 Coastal Fisheries Infrastructure ........................................................................... 29 2.5 Fish Resources in the Lagoon and Off-lagoon..... .................................................. 30 2.6 Supply of Fresh Fish.............................................................................................. 31 2.7 Fisher Community................................................................................................. 31 2.8 Fishing Equipment................................................................................................ 31 2.9 Fishing Gears........................................................................................................ 32 2.10 Preservation of Fish on Board............................................................................... 33

3.0 VCA of Fishing Enterprises........................................................................................ 34 3.1 Case Study I – Hand Line Fishing Unit / Enterprise................................................ 35 3.2 Case Study II – Basket Trap Fishing Unit................................................................ 37 3.3 Case Study III – Large Net Fishing Cooperative / Enterprise................................... 38 3.4 Case Study IV – Non-Motorized Boat Hand Line Unit ........................................... 39 3.5 Case Study V - On-foot Hand Line & Harpoon Fishing.......................................... 40 3.6 Summary of Economic Indicators of Artisanal Fisheries........................................ 41 3.7 ProfitabilityofFishingEnterprise–Rs/Kg............................................................. 42 3.8 Cash Flow Management....................................................................................... 42 3.9 Bio-Economic Approach of the Artisanal Fisheries................................................ 43

4.0 Fresh Fish Trade in Mauritius.................................................................................... 46 4.1 Fishmongers......................................................................................................... 47 4.2 Marketing and Distribution Logistics.................................................................... 48 4.3 Pricing Mechanism............................................................................................... 49

5.0 VCA of Marketing Channels..................................................................................... 51 5.1 Case Study VI – Integrated Coastal Retailer of Hand Line Harvested Fish.............. 51 5.2 CaseStudyVII–IntegratedCoastalRetailerofBasketTrapHarvestedfish...........52

5.3. Case study VIII – Wholesaler of Large Net & Basket Trap Harvested Fish............... 53 5.4. Case study IX – Municipal Fish Retail Outlet......................................................... 54 5.5. Case Study X – Fish Stall in a Hypermarket........................................................... 55

6.0 Distribution of Value Added Between Fishing and Marketing Functions.....56 6.1 HL Integrated (Fishing and Marketing) Activities .................................................. 56 6.2 BT Integrated (Fishing and Marketing) Activities.................................................. 57 6.3 HL and Supermarket Fish Stall Integrated Activities.............................................. 57 6.4 LN Fishing and Institutional Fish Market Integrated Activities.............................. 57 6.5 Integrated Fishing and Marketing Activities – Non-Motorized HL Boats............... 58 6.6 On-foot Fishers - Integrated Fishing and Marketing Activities.............................. 58 6.7 Summary of Case Study Results............................................................................ 59

7.0 Results and Discussions ............................................................................................ 60 7.1 Management and Monitoring Measures .............................................................. 60 7.2 FLS and LFC as the Focal Point.............................................................................. 61 7.3 Handling and Preservation of Fresh Fish............................................................... 62 7.4 Processing and Value Added Activities..................................................................62 7.5 New Concept of Fish Terminal...............................................................................63

8.0 Recommendations...................................................................................................... 64

Appendix 1: Terms of Reference........................................................................................... 69

Appendix 2: Commercial Category of Fish Harvested by the Artisanal Fisheries... 71

Appendix 3: Fishing Business Model................................................................................... 73

Appendix 4: Consolidated Data – Reg. Fishers / Fishing Boats / Fishmongers........ 75

Appendix 5: Catch Composition of the Artisanal Fisheries - Year 2010................. 75

Appendix 6: Questionnaire 2 - Distribution and Marketing Channels................... 76

Appendix 7: Questionnaire 2 – Fishing Enterprise................................................ 79

Appendix 8: Fish Landing Stations (FLS) Around Mauritius.................................. 82

Appendix 9: List of Persons Met........................................................................................ 83

Appendix 10: References........................................................................................................ 84

List of Publications ................................................................................................................. 85

7SmartFish Programme Report SF/2012/8

LIST OF ABBREVIATIONS & ACRONYMSAFRC Albion Fisheries Research CentreBDS Business Development ServicesCA Competent AuthorityCOP Code of PracticeCOP Cost of ProductionCOS Cost of SalesCPBL Catch Per Boat LandingCPFD Catch Per Fisherman DayCSP Consumer Sale Price DBM Development Bank of Mauritius EEZ Exclusive Economic Zone EFAM Electronic Fish Auction Market ESA – IO East-Southern Africa - Indian Ocean EU European Union FD Fisheries Department FAD Fish Aggregating Device FGD Focus Group Discussion FIT Fishermen Investment Trust FITEC Fishermen Investment Trust Extension Centre FLS Fish Landing Station FPO FisheriesProtectionOfficer HACCP Hazard Analysis and Critical Control PointsHP Horse Power IFAD International Fund for Agricultural DevelopmentIFRS Implementation of Fisheries Regional StrategiesIOC Indian Ocean Commission L/T Long Term LFC Local Fisher Community M/T Medium term MC Marketing Cost MdP Maison des Pêcheurs MM Marketing Margin MOFR Ministry of Fisheries and Rodrigues MP MarketingProfit MSY Maximum Sustainable Yield PM ProfitMargin PSP Producer Sale Price RRA Rural Rapid Appraisal S/T Short Term SMEDA Small Medium Enterprises Development AuthoritySTE Short Term Expertise T Metric Tonne TC Total Cost VCA Value Chain Analysis WSP Wholesale Price

8 SmartFish Programme Report SF/2012/8

ACKNOWLEDGEMENTS

The consultant wishes to thank the following institutions and people for their valuable assistance in bringing up this report.

Ministry of Fisheries and Rodrigues• Mr.D.Mauree• Mr.VishnuSoondroon• Mr.MarayvenNallee• Mr.SatishKheedun

Fisheries Enumerators• Mr.Munisami• Mr.FBBholah• Mr.D.Bolaky• Mr.S.SokAppadu• Mr.S.Mohabir• Mr.SRamkisson

Ministry of Cooperatives, Small and Medium Business Enterprises• Dr.ManojNandooarsingh

Fishermen Investments Trust• Mr.AdilBunwaree

Fishermen Investments Trust Extension Centre• Mr.B.Ramcharrun

Mauritius Fishermen Cooperative Federation• Mr.PatrickFortuno

AuriflaLimited• Mr.RPermall

9SmartFish Programme Report SF/2012/8

PREFACE

Value Chain Assessment: Artisanal Fisheries of Mauritius & Rodrigues

Within the broader framework of the IOC SmartFish programme (Implementation of a Regional Fisheries Strategy for ESA-IO programme), component Result 4, Regional Trade Development, this report has been prepared to assist theMinistryofFisheries&Rodrigues inMauritiustobetterunderstandthesituation intheartisanalfisheryfromaneconomic and value perspective. This will allow for objective planning for potential interventions to assist in the move towardsamoremarketdrivenandsustainablefisherythatwillenhanceandcontributetothegrowingdemandforfishinthecountryinthelong-term,whilstmaintainingthesocio-economicvalueofthefisheryinthecountry.

Thisreportlookscloselyatthedifferenttypesoffishingmethodswithintheartisanalsub-sector,suchasthehand-line(motorizedandnon-motorized)fishery,thebaskettrapfishery,thelargenetfisheryaswellastheon-footfishery.Itprovides a detailed analysis of performance in terms of typical business models for each unit and makes assessments of performance with respect to catch potential, capacity /over-capacity vs. stocks and estimated MSY. Ultimately the impactonthelocalfishingcommunities,aswellasthebroaderissueofincreasingdemandinthecountry,isaddressedandhowtore-modelandempowertheartisanalfisherytobetterservetheeconomy,aswellasthelocalpopulation.Recommendations for short-term interventions are made to inform the many stakeholders of what works and what doesn’tworksowellandaviewtothefutureforeveryone’sbenefit.

Regionally,smallislandartisanalfisheries,aswellasregionalcoastalartisanalfisheriesarealldealingwithissuesofover-capacity and depleted stocks in coastal lagoons, as well as deciding how to ensure future productivity of the sector wherelocalfishersderiveasignificantpartoftheirlivelihoodsfromfishing.Thisreportwillcontributetotheregionalknowledge in this regard and inform other initiatives to be planned regionally under the SmartFish programme.

Thisreport isthefirststepandasimilarexerciseistobeimplementedfortheislandofRodrigues.Althoughsomesimilaritiesareexpected,thereareverydifferentaspectstoeachofthesefisheriestobeunderstood.

10 SmartFish Programme Report SF/2012/8

LAYMAN’S SUMMARY

The study has carried out an economic appraisal of the production and marketing systems in the artisanal fisheries in Mauritius. The results have shed some light on the profitability of the different enterprises involved in the supply chain and on the distribution of value added or profit between fishing and marketing. The major problems identified in the fisheries are namely; open access which is tantamount to overfishing; obsoleteness of fisheries infrastructure; over-investments in fishing operations; and, absence of a food safety and quality standard for the fresh fish on the local markets. Appropriate measures have been recommended to drive the artisanal fisheries on the path socio-economic and ecological sustainability.

RÉSUMÉ DES NON-INITIÉS

Uneétuded’analyseéconomiqueestentreprisedanslesfilièresdelapêcheetdelacommercialisationdanslesecteurde la pêche artisanale à Maurice. L’étude a apporté un éclairage sur la rentabilité des différentes entreprises dans la filièreetsurlepartagedelavaleurajoutéeentrelescomposantesdelapêcheetcellesdelacommercialisation.Lesproblèmes identifiésdans lesous-secteursontentreautres, le libreaccèscequicomporteunrisquepotentieldesurpêche,surinvestissementsdans lesoutilsdeproduction,mauvaisétatdes infrastructuresdelapêchecôtièreetl’absence des normes sanitaires et de qualité des produits de pêche sur les marchés locaux. Des actions nécessaires ont été recommandées pour que la pêche artisanale soit socio-économiquement et écologiquement soutenable.

EXECUTIVE SUMMARY

This study was commissioned by the Ministry of Fisheries and Rodrigues of Mauritius and executed by the Implementation of Regional Fisheries Strategies for the ESA-OI under the aegis of the Indian Ocean Commission funded by the EuropeanUnion. Itsprincipalobjective is tocarryout avaluechainanalysisof theartisanal fisheries sub-sector inMauritius to assess the economic performance of its production functions and marketing channels. Based on the findings,recommendationsaremadetoenhanceoverallefficienciesintheartisanalfisherieswhiletakingintoaccountthe social and ecological implications.

Actuallytheartisanalfisheriesarethemainsuppliersoffreshfishtothelocalmarketswithanannualproductionof830metrictonnes.Asof2010therewere1,620registeredfishers,1,605fishingboatsand400activefishmongersinthesub-sector.ThetargetedfishstockshaveattainedtheirMSY.TheCPFDisat6.4kgoverthepast3years.TheMOFRprovidesaplethoraofincentivestodivertfishingeffortsfromthelagoontooff-lagoondeep-seaFADanddemersalfisheriesinordertorelievefishingpressureinthelagoon. Thereare60FishLandingStations(FLS)aroundMauritiusthatserveasoperationalbasetothecoastalfishingfleet.Theyaremandatedforunloadingoffish,datacollectionandprimarysaleoffish.Intheearly70’stheywereconceivedtoprovidebasicfacilitiesforcleaning,sortingandmarketingoffish.Actuallymostofthemhaveoutlivedtheirpurposesand are out of use. The decline of the Local Fishing Community (LFS) has had a negative impact on the development andmanagementofthecoastalfisheriesandtheorganisationoftheLFC.EffortsarebeingmadebytheMinistrytorehabilitate the FLS network around the island in consultation with the LFC.

Amajorconcernfortheartisanalfisheriesistheabsenceofafoodsafetyandqualitystandardalongthesupplychain,fromcapturetoconsumption.Preservationoffishonboardisrudimentaryornon-existent.FlakeIceisnotavailablearoundtheislandparticularlyattheFLS.Traditionalboatsarenotequippedwithfishholdsandiceissimplynotused.

11SmartFish Programme Report SF/2012/8

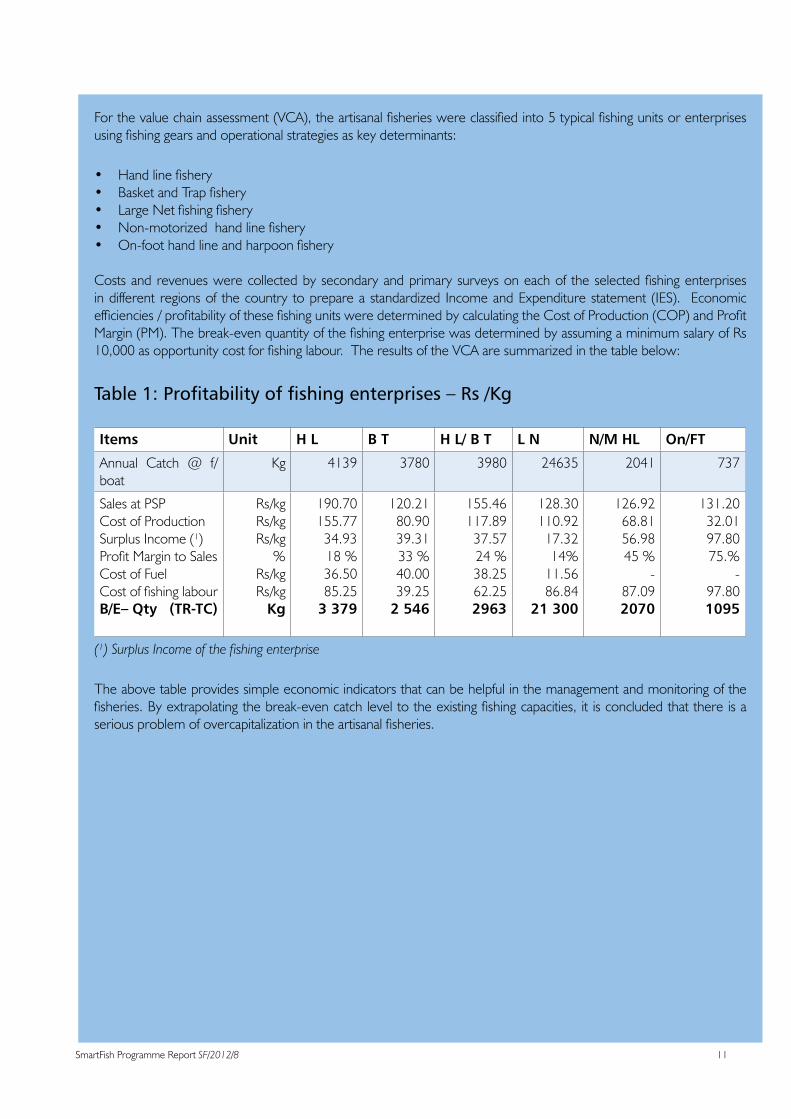

Forthevaluechainassessment(VCA),theartisanalfisherieswereclassifiedinto5typicalfishingunitsorenterprisesusingfishinggearsandoperationalstrategiesaskeydeterminants:

• Handlinefishery• BasketandTrapfishery• LargeNetfishingfishery• Non-motorizedhandlinefishery• On-foothandlineandharpoonfishery

Costs and revenueswerecollectedby secondaryandprimary surveysoneachof the selectedfishingenterprisesin different regions of the country to prepare a standardized Income and Expenditure statement (IES). Economic efficiencies/profitabilityofthesefishingunitsweredeterminedbycalculatingtheCostofProduction(COP)andProfitMargin(PM).Thebreak-evenquantityofthefishingenterprisewasdeterminedbyassumingaminimumsalaryofRs10,000asopportunitycostforfishinglabour.TheresultsoftheVCAaresummarizedinthetablebelow:

Table1:Profitabilityoffishingenterprises–Rs/Kg

Items Unit H L B T H L/ B T L N N/M HL On/FT

Annual Catch @ f/ boat

Kg 4139 3780 3980 24635 2041 737

Sales at PSPCost of Production Surplus Income (¹)ProfitMargintoSalesCost of FuelCostoffishinglabourB/E– Qty (TR-TC)

Rs/kgRs/kgRs/kg

%Rs/kgRs/kg

Kg

190.70155.7734.9318 %36.5085.25

3 379

120.2180.9039.3133%40.0039.25

2 546

155.46117.8937.5724 %38.2562.252963

128.30110.9217.3214%11.5686.84

21 300

126.9268.8156.9845%

-87.092070

131.2032.0197.8075.%

-97.801095

(¹) Surplus Income of the fishing enterprise

The above table provides simple economic indicators that can be helpful in the management and monitoring of the fisheries.Byextrapolatingthebreak-evencatchleveltotheexistingfishingcapacities, it isconcludedthatthereisaseriousproblemofovercapitalizationintheartisanalfisheries.

12 SmartFish Programme Report SF/2012/8

Table2:EstimatesofSurplusfishingcapacitiesatcurrentMSYlevel

Items HL BT BT/HL LN O/f–HL/H TOTAL

Annual Catch PercentageMean Catch @ f/ boat (kg)

22712%

4 139

26711%

3780

2836%

3960

2226%

24635

8735%737

831100%

Optimal No. f/boats (N)Optimal On-foot fishers (N)

54-

150-

7-

27-

-118

238

ActivefishingboatsActiveon-footfishers

678 761 139 27 -134

1605

Surplus fishing boats (N)Surplus On-foot fishers (N)

624-

611-

132-

0-

-16

1367

AtthecurrentMSY,theartisanalfisheriescansustain238fishingboatsand832fishersincluding118on-footfishers.Thereisasurplusof1367boatsand788registeredfishersincluding16on-footfishers.Thesituationismorealarminginrealitybecausethecoastalfisheries,withtheexceptionoftheLNfisheryareopenaccess.On the marketing side, a preliminary survey was carried out to have an in-depth understanding on the market structures andmarketingchannelsof theartisanalfisheries.Toaddress theVCA in themarketingchannels,MarketingMargin(MM),MarketingCost(MC)andMarketingProfit(MP)weredetermined.Thefreshfishmarketissupplydrivenandthemarketpricehashighvolatile.Infacttherearenearly400activefishmongerschasing830metrictonnesoffreshfishannually.Anincreasingnumberoffishmongersareownersoffishingboatsasapartofabusinessstrategytosecurearegularsupplyoffish.Someotherswouldactasindigenousbankerstofishingenterprisestogainpriorityoftheircatch.Alsoanincreasinglylargenumberoffishingenterprisesinthecoastalareashavediversifiedintoroadsidefishretailingas a household business.

Figure1:FlowchartofthemarketchannelsoffreshfishinMauritius

End Consumers Exports

Super / hyper MarketsFish Shops Hotel & Restaurants

Retailer / Wholesalers F/boat owner (N= 150)

Wholesaler/ Distributors(N= 10)

Fishers (N=1655) – F/Boats (N=1700) – Production (830 t)

Retailers FLS(N=100)

N:3

Inland Retail Outlets:Town & Large Village Markets, 340Roadside & Ambulant vendors

L

O

G

I

S

T

I

C

S

13SmartFish Programme Report SF/2012/8

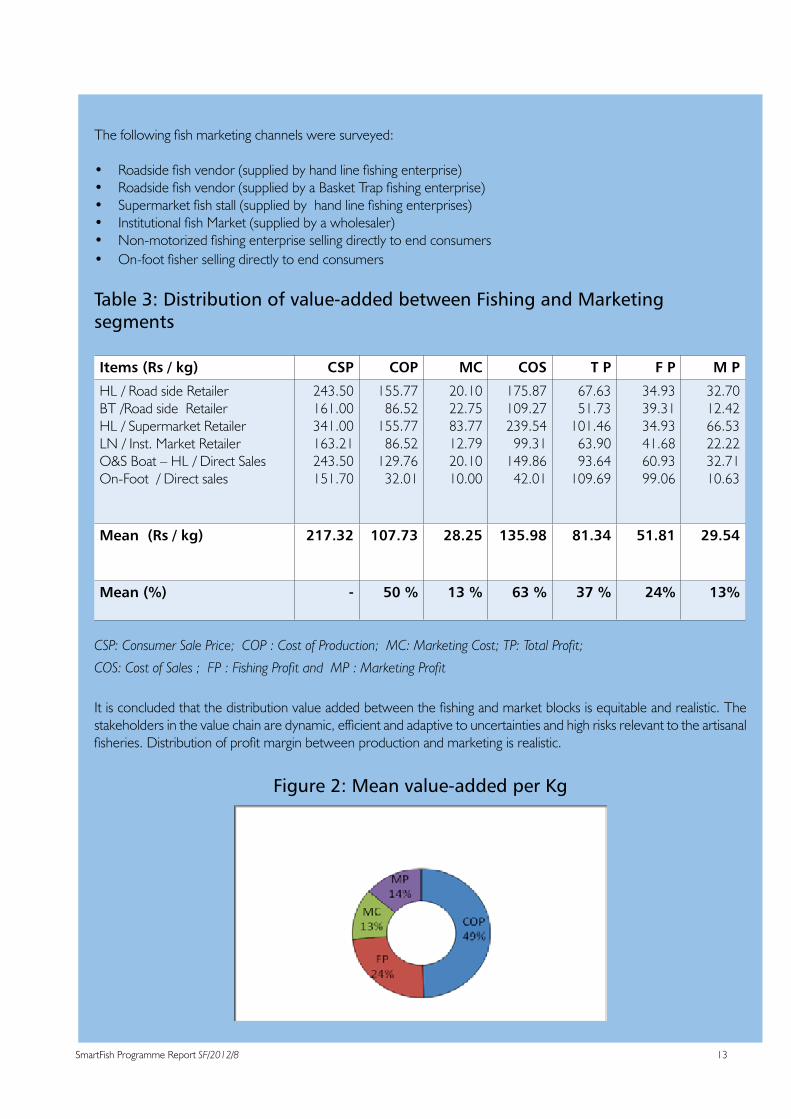

Thefollowingfishmarketingchannelsweresurveyed:

• Roadsidefishvendor(suppliedbyhandlinefishingenterprise)• Roadsidefishvendor(suppliedbyaBasketTrapfishingenterprise)• Supermarketfishstall(suppliedbyhandlinefishingenterprises)• InstitutionalfishMarket(suppliedbyawholesaler)• Non-motorizedfishingenterprisesellingdirectlytoendconsumers• On-footfishersellingdirectlytoendconsumers

Table 3: Distribution of value-added between Fishing and Marketing segments

Items (Rs / kg) CSP COP MC COS T P F P M P

HL / Road side RetailerBT /Road side RetailerHL / Supermarket RetailerLN / Inst. Market RetailerO&S Boat – HL / Direct SalesOn-Foot / Direct sales

243.50161.00341.00163.21243.50151.70

155.7786.52155.7786.52

129.7632.01

20.1022.7583.7712.7920.1010.00

175.87109.27239.5499.31

149.8642.01

67.6351.73

101.4663.9093.64

109.69

34.9339.3134.9341.6860.9399.06

32.7012.4266.5322.2232.7110.63

Mean (Rs / kg) 217.32 107.73 28.25 135.98 81.34 51.81 29.54

Mean (%) - 50 % 13 % 63 % 37 % 24% 13%

CSP: Consumer Sale Price; COP : Cost of Production; MC: Marketing Cost; TP: Total Profit;

COS: Cost of Sales ; FP : Fishing Profit and MP : Marketing Profit

Itisconcludedthatthedistributionvalueaddedbetweenthefishingandmarketblocksisequitableandrealistic.Thestakeholdersinthevaluechainaredynamic,efficientandadaptivetouncertaintiesandhighrisksrelevanttotheartisanalfisheries.Distributionofprofitmarginbetweenproductionandmarketingisrealistic.

Figure2:Meanvalue-addedperKg

14 SmartFish Programme Report SF/2012/8

MarketingCostisnegligibleoftheshortdistributionnetworkandlowcapitalinvestmentinlogistics.Itrepresents13%oftheCSP.Howevermarketingcostfordedicatedfishstallinsupermarketsishigher(25%oftheCSP)andobviouslyitisrewardedbyahigherprofitmargin(20%).Theimplementationforfoodsafetyandqualitystandardhastobeviewedas market opportunities instead of cost constraints. There should be no resistance on the part of marketing channels to comply with a food safety and quality standard. Actually the development of micro and small processing and value addedenterprisesisonstandstillmainlyduetoshortageofsupplyoffreshfishandabsenceoffoodsafetyandqualitynorms.Howeverthemarketprospectsaregood.Theculturalheritageoftheartisanalfisheriescanbepromotedasanattractionforthetourismindustry.Anewconceptoffishterminalisproposedtotapadditionalrevenueforfishercommunity from the growing number of foreign visitors in the country. Thestudyhasconcludedandrecommendedthefollowing:• There is a potential risk of overfishing in the artisanal fisheries because the active fishing capacities exceed inmanifoldthesustainablelevel.Thereisanurgentneedtoundertakeariskassessmentonfishstocksharvestedinthe lagoon and off-lagoon.

• The coastal ecosystem is under more intense pressure from an increasingly large number of (non-registered) professional,amateurandsportfishers.Todoawaywiththeprevailingopenaccessenvironment,itisrecommendedto conduct a survey on the activities of the amateur and sport fisheries leading to the implementation of anappropriateregulatoryframeworktomanageandmonitorthesefisheriesatparwiththeartisanalfisheries.

• Thepresentfisheriesstatisticalmodel includingsamplinganddatacollectionstrategieshasoutlived itspurposeand it is high time to replace it. The new system must be capable of integrating the activities of amateur and sport fisheries.

• Anappropriatebio-economicmodelfortheartisanalfisherieshastobedevelopedtoserveasamanagementtool

kit.

• AnEconomicUnitheadedbyafisherieseconomisthastobesetwithintheAFRC.Itwillberesponsibleforallsocio-economicissuesrelatedthefisheriessector,inparticulartheartisanalfisheries.

• TheFLSnetworkhastoberehabilitatedattheearliestwiththeinvolvementofthelocalfishercommunities.LFCshave to be empowered with local governance, leadership and co-management skills to bring about a shift from an externalenforcementapproachtosharedgoalsandresponsibilitiesinfisheriesmanagement.ItisindicatedthatIFAD-MARS is committed to fund a study on a comprehensive management plan for the lagoon and off-lagoon fisherieswithintheframeworkoftheupcomingFisheriesMasterPlan.

• There should be no compromise regarding safety and quality of fresh fish placed on the localmarkets. TheguidelineforadetailedactionplanfortheenforcementoftheCOP–HandlingandPreservationoffreshfishisenumeratedasfollows:

- Launch an awareness campaign at the national level using audio-visual means and FGD to sensitize consumersandproducersofthecriticalneedforfoodsafetyandqualityoffreshfishonthelocalmarketsandparticularlytheuseofice-flakesforfishpreservation.

- Conductanauditontheexistingfisheriesinfrastructurefromtheperspectiveoftheimplementationof the COP – “Handling and Preservation of Fresh Fish” as minimum food safety and quality in the artisanalfisheries.

- EnforcementoftheCOP–HandlingandPreservationof freshfishbytheMOFRasanationalfoodsafetyandqualitystandardforthemarketingoffreshfish.

15SmartFish Programme Report SF/2012/8

- Development of a human resources plan at public and private sector levels to ensure the smooth implementation of the safety and quality standard.

- Implement a pilot project on COP – Handling and Preservation of Fresh Fish based on

voluntary compliance at Tamarin or Trou d’eau Douce where an ice-plants exists, to showcase its importance.

• To develop a new concept of a Fish Terminal at strategic locations to serve equally as a tourist attraction, as a strategy tomaximise revenueof the artisanal fisheries.The cultural heritageof the fisher communities, theeveryday activities at the fishingwharf and seafoodmarketwill bemain theme of this concept. The projectwillcreatepositiveinteractions/synergiesbetweenartisanalfisheriesandthetourismsector.Itisproposedtoprepare a pre-feasibility study and business plan for the development of a pilot project to be located at “Maison des Pêcheurs” complex, Fishermen Village of Mahebourg Waterfront.

• The prospects for the development of micro and small scale processing and value addition activities will grow progressivelywithan increase inthesupplyof freshfish.FITECwillhavetoadoptapro-activeandone-stop-shop approach to assist promoters through project facilitation, training in technical and entrepreneurial skills and mentoring.

• To strengthen management and extension capacities of AFRC, by creating an Economic Observatory headed by afisherieseconomist.Itwillberesponsibleforallsocio-economicissuesrelatedtothefisheriessectorinteralias,cost-benefitanalysisofpolicy-decisions,socio-economicsurveysandtechnicalsupportstoFITEC.

• Apilotprojecttoempowerlocalfishercommunitiesinlocalgovernance,leadershipparticipatorymanagementleading shared commitment and responsibility in policy formulation and voluntary compliance; and co-management oflocalfisheriesinfrastructuresuchasFLS.

Many international and regional organisations as well as inter-governmental Co-operations are active in the artisanal fisheriessub-sector.AnewFisheriesMasterPlanisintheprocessofapprovalbytheCabinet.Aconcertedapproachwill be necessary to allocate adequate technical and financial resources for the implementation of the aboverecommendations.

16 SmartFish Programme Report SF/2012/8

RÉSUMÉ EXECUTIF

LaprésenteétudeaétécommandéeparleMinistèredelaPêcheetdeRodrigues(MOFR)deMauriceeteffectuéepar le Programme pour la Mise en oeuvre d’une Stratégie Régionale de la pêche pour la région Afrique Orientale et Australe-OcéanIndien(AOA-OI)sousl’égidedelaCommissiondel’OcéanIndien(COI)aveclefinancementdel’Union européenne (UE). L’objectif principal consistait à entreprendre une étude de la chaîne de valeur du sous-secteur de la pêche artisanale à Maurice dans le but d’évaluer la performance économique de ses fonctions de production et de sescanauxdecommercialisation.Surlabasedesconclusions,desrecommandationssontformuléesafinderenforcerl’efficacitéglobaledelapêcheartisanaletoutentenantcomptedesimplicationssocialesetécologiques.

La pêche artisanale constitue en fait la principale source d’approvisionnement des marchés locaux en poisson frais, avec uneproductionannuellede830tonnesmétriques.En2010,oncomptait1620pêcheursenregistrés,1605bateauxde pêche et 400 mareyeurs actifs dans le sous-secteur. Les stocks de poissons ciblés ont atteint leur rendement maximal durable(RMD).Lescapturesparpêcheurparjoursesontélevéesà6,4kgaucoursdestroisdernièresannées.LeMOFR fournit une pléthore de mesures incitatives pour détourner l’effort de pêche vers l’extérieur du lagon, sur les pêcherieseneauxprofondes,démersalesousurDCP,afindediminuerlapressiondepêchedanslelagon. IlexisteautourdeMaurice60stationsdedébarquementdupoisson(SDP)quiserventdebased’opérationsàlaflottedepêchecôtière.Ellessonthabilitéesàdéchargerlepoisson,recueillirlesdonnéeseteffectuerlapremièreventedupoisson. Au début des années 70, ils étaient conçus de sorte à offrir les installations élémentaires pour le nettoyage, le tri et la commercialisation du poisson. En fait, la plupart d’entre elles ont fait leur temps et sont hors d’usage. Le déclin des communautés de pêche locales (CPL) a eu un impact négatif sur le développement et la gestion des pêches côtièresetl’organisationdesSDP.LeMinistèreentreprendactuellementdeseffortsafinderéhabiliterleréseaudesitesde débarquement autour de l’île en consultation avec les CPL.

Unesourcemajeuredepréoccupationpour lapêcheartisanales’avèreêtre l’absencedenormesdequalitéetdesécurité alimentaire le long de la chaîne d’approvisionnement, de la capture à la consommation. Les mesures de préservation du poisson à bord des bateaux sont rudimentaires ou non existantes. La glace en flocons n’est pasdisponible autourde l’île, enparticulier auxdébarcadères.Lesbateaux traditionnelsne sontpasmunisde cales àpoisson et la glace n’est simplement pas utilisée.

Auxfinsdel’analysedelachaînedevaleur(ACV),lapêcheartisanaleaétéclasséeencinqtypesd’unitésoud’entreprisesdepêche,enutilisantlesenginsdepêcheetlesstratégiesopérationnellescommedéterminantsclés:

• pêche à la ligne (HL) ;• pêche au panier et au casier (BT) ; • pêcheaugrandfilet(LN);• pêche à la ligne non motorisée (NM HL) ; • pêche à la ligne à pied et pêche au harpon (On/FT).

Desdonnéessurlescoûtsetlesrevenusontétérecueilliesgrâceàdesenquêtessecondairesetprimairesauprèsdechacunedesentreprisesdepêchesélectionnéesdansdifférentesrégionsdupaysafindepréparerunétatstandardisédes revenus et des dépenses (IES). L’efficience et la profitabilité de ces unités de pêche ont été déterminées encalculantlecoûtdeproduction(CP)etlamargedeprofit(MP).Laquantitérequisepourlarentabilitédel’unitédepêche a été déterminée en supposant qu’il y ait un salaire minimal de Rs 10 000 comme coût d’opportunité pour la maind’œuvredepêche.Letableausuivantprésenteunrésumédesconclusionsdel’ACV:

17SmartFish Programme Report SF/2012/8

Tableau 1: Rentabilité des entreprises de pêche - Rs/kg

Eléments Unité HL BT HL / BT LN N/M HL On / FT

Prise annuelle par bateau Kg 4139 3780 3960 24635 2041 737

Ventes aux PSPCoûts de production Revenus en excédent (¹)Marge de profit parrapport aux ventesCoût du carburantCoût de la main d’œuvre de pêche

B/E– Qté (TR-TC)

Rs/kgRs/kgRs/kg

%

Rs/kgRs/kg

Kg

190.70155.7734.9318 %

36.5085.25

3 379

120.2180.9039.3133%

40.0039.25

2 546

155.46117.8937.5724 %

38.2562.25

2963

128.30110.9217.3214%

11.5686.84

21 300

126.9268.8156.9845%

-87.09

2070

131.2032.0197.8075.%

-97.80

1095

(¹) Revenus en excédent de l’entreprise de pêche

Le tableau ci-dessus fournit des indicateurs économiques simples qui peuvent être utiles dans la gestion et la surveillance des pêches. En extrapolant le niveau des prises nécessaires pour atteindre le seuil de rentabilité des capacités de pêche existantes (B/E–Qté), l’onconclutqu’ilexisteunsérieuxproblèmedesurcapitalisationdans lesous-secteurde lapêche artisanale.

Tableau 2 : Estimations des capacités de pêche excédentaires au niveau actuel de RMD (rendement maximal durable)

Eléments HL BT BT / HL LN O/F - HL / H TOTAL

Prise annuelle PourcentagePrise moyenne par bateau (kg)

22712%4139

26711%3780

2836%3960

2226%

24635

8735%737

831100%

Nombre de bateaux de pêche optimal (N)Nombre de pêcheurs à pied optimal (N)

54

-

150

-

7

-

27

-

-

118

238

-

Bateaux de pêche actifs Pêcheurs à pied actifs

678 761 139 27 -134

1605

Nombre de bateaux de pêche en surplus (N)Nombre de pêcheurs à pied en surplus (N)

624

-

611

-

132

-

0

-

-

16

1367

18 SmartFish Programme Report SF/2012/8

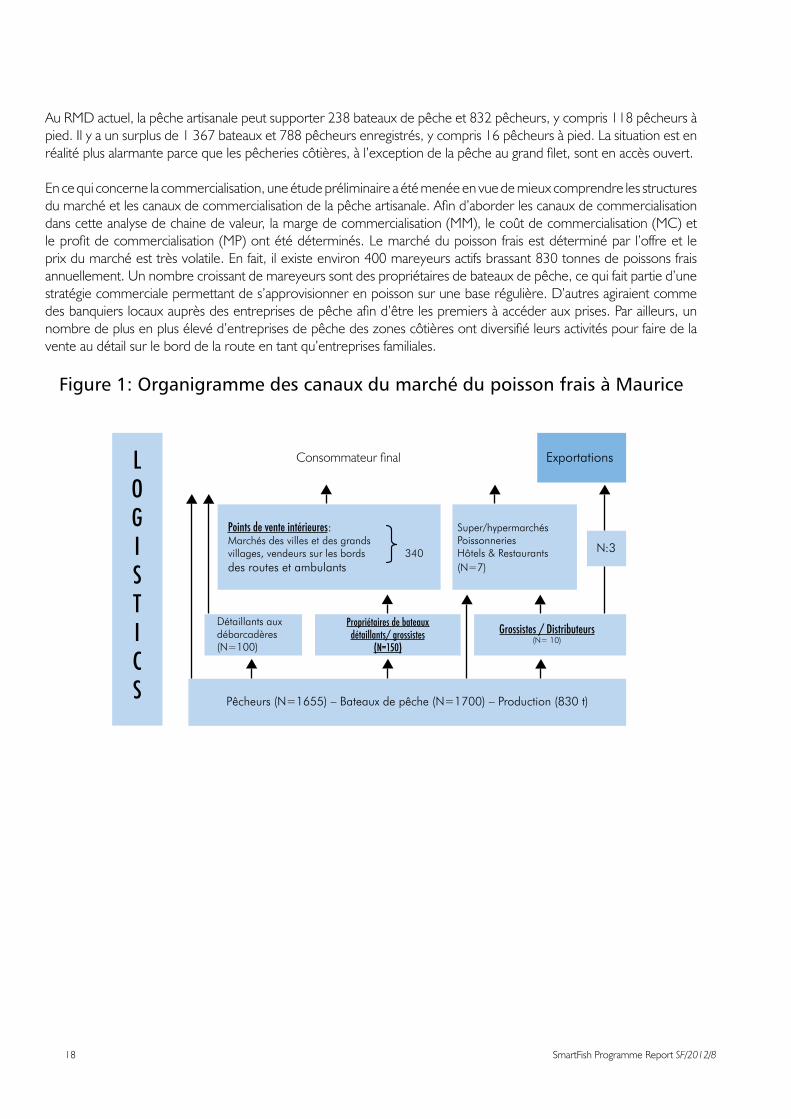

AuRMDactuel,lapêcheartisanalepeutsupporter238bateauxdepêcheet832pêcheurs,ycompris118pêcheursàpied.Ilyaunsurplusde1367bateauxet788pêcheursenregistrés,ycompris16pêcheursàpied.Lasituationestenréalitéplusalarmanteparcequelespêcheriescôtières,àl’exceptiondelapêcheaugrandfilet,sontenaccèsouvert.

En ce qui concerne la commercialisation, une étude préliminaire a été menée en vue de mieux comprendre les structures dumarchéetlescanauxdecommercialisationdelapêcheartisanale.Afind’aborderlescanauxdecommercialisationdans cette analyse de chaine de valeur, la marge de commercialisation (MM), le coût de commercialisation (MC) et leprofitdecommercialisation(MP)ontétédéterminés.Lemarchédupoisson fraisestdéterminépar l’offreet leprixdumarchéesttrèsvolatile.Enfait,ilexisteenviron400mareyeursactifsbrassant830tonnesdepoissonsfraisannuellement. Un nombre croissant de mareyeurs sont des propriétaires de bateaux de pêche, ce qui fait partie d’une stratégiecommercialepermettantdes’approvisionnerenpoissonsurunebaserégulière.D’autresagiraientcommedesbanquierslocauxauprèsdesentreprisesdepêcheafind’êtrelespremiersàaccéderauxprises.Parailleurs,unnombredeplusenplusélevéd’entreprisesdepêchedeszonescôtièresontdiversifiéleursactivitéspourfairedelavente au détail sur le bord de la route en tant qu’entreprises familiales.

Figure 1: Organigramme des canaux du marché du poisson frais à Maurice

Consommateurfinal Exportations

Super/hypermarchésPoissonneriesHôtels & Restaurants(N=7)

Propriétaires de bateauxdétaillants/ grossistes

(N=150)

Grossistes / Distributeurs(N= 10)

Pêcheurs (N=1655) – Bateaux de pêche (N=1700) – Production (830 t)

Détaillants aux débarcadères(N=100)

N:3

Points de vente intérieures:Marchés des villes et des grandsvillages, vendeurs sur les bords 340des routes et ambulants

LOGISTICS

19SmartFish Programme Report SF/2012/8

Les canaux suivants de commercialisation du poisson ont fait l’objet d’une étude :

• Vendeur de poisson sur les bords des routes (approvisionné par une entreprise de pêche à la ligne) ;• Vendeur de poisson sur les bords des routes (approvisionné par une entreprise de pêche au panier/casier) ;• Étal de poisson de supermarché (approvisionné par des entreprises de pêche à la ligne) ;• Marché au poisson institutionnel (approvisionné par un grossiste) ; • Entreprisedepêchenon-motoriséevendantdirectementauxconsommateursfinaux;• Pêcheuràpiedvendantdirectementauxconsommateursfinaux.

Tableau3:Distributiondelavaleurajoutéeentrelessegmentsdelapêcheetde la commercialisation

Eléments (Rs / Kg) CSP COP MC COS T P F P M P

HL / Détaillant sur les bords des routesBT / Détaillant sur les bords des routesHL / Détaillant au supermarchéLN / Détaillant au marché institutionnel O&S Bateau – HL /Ventes directesÀ pied/Ventes directes

243.50161.00341.00163.21243.50151.70

155.7786.52155.7786.52

129.7632.01

20.1022.7583.7712.7920.1010.00

175.87109.27239.5499.31

149.8642.01

67.6351.73

101.4663.9093.64

109.69

34.9339.3134.9341.6860.9399.06

32.7012.4266.5322.2232.7110.63

Moyenne (Rs / kg) 217.32 107.73 28.25 135.98 81.34 51.81 29.54

Moyenne (%) - 50% 13% 63% 37% 24% 13%

CSP: Prix de vente au consommateur ; COP : Coût de production; MC: Coût de commercialisation ; TP: Profit total ; COS : Coût des ventes ; FP : Profit des pêches ; MP : Profit de commercialisation

L’on conclut que la distribution de la valeur ajoutée entre la pêche et la commercialisation est équitable et réaliste. Lespartiesprenantesdelachaînedevaleursontdynamiques,efficacesets’adaptentauxincertitudesetauxrisquesélevésafférentsàlapêcheartisanale.Ladistributiondelamargedeprofitentrelaproductionetlacommercialisationest réaliste.

20 SmartFish Programme Report SF/2012/8

Figure 2 : Valeur ajoutée moyenne/kg

Les coûts de commercialisation sont négligeables pour le court réseau de distribution et le faible investissement en capitaldanslalogistique.Ilreprésente13%duCSP.Toutefois,lescoûtsdecommercialisationpourlesétalsdepoissondédiésdanslessupermarchéssontplusélevés(25%duCSP)et,manifestement,unemargedeprofitsupérieure(20%) en découle.

La mise en œuvre de normes de sécurité alimentaire et de qualité doit être perçue comme des opportunités de marché plutôt que comme des contraintes coûteuses. Les canaux de commercialisation ne devraient nullement s’opposer au respect des normes de sécurité alimentaire et de qualité. En fait, le développement de micro et petites entreprises de transformationetd’ajoutdevaleurestaupointmort,particulièrementenraisond’unepénuried’approvisionnementen poisson frais et de l’absence de normes de sécurité alimentaire et de qualité. Cependant, les perspectives de marché sont satisfaisantes. Il est possible de promouvoir l’héritage culturel de la pêche artisanale comme une attraction pour l’industrie du tourisme. Il est proposé de créer un nouveau concept de terminal de poisson pour engendrer des revenusadditionnelsenfaveurdelacommunautédespêcheursauprèsdunombrecroissantdevisiteursétrangersdans le pays.

Lesconclusionsetlesrecommandationsdel’étudesontlessuivantes:

• Ilexisteunrisquepotentieldesurpêchedanslapêcheartisanaleparcequelescapacitésactivesdepêche dépassenttrèslargementleniveaudurable.Ilestextrêmementurgentdemeneruneévaluationdesrisques en ce qui concerne les stocks de poisson ciblés à l’intérieur et hors du lagon.• L’écosystèmecôtiersubitdeplusenplusdepressiond’unnombregrandissantdepêcheursprofessionnels, amateursetsportifs(nonenregistrés).Afindesedébarrasserdecetenvironnementd’accèsouvert,ilest recommandé de mener une étude sur les activités de la pêche amateur et sportive, qui aboutira à la mise en œuvre d’un cadre réglementaire approprié pour gérer et surveiller ces pêcheries comme c’est le cas dans la pêche artisanale.• Leprésentmodèlestatistiqueenmatièredepêche,notammentl’échantillonnageetlacollectededonnées, estdevenuobsolèteetilestgrandtempsdeleremplacer.Lenouveausystèmedoitêtreenmesure d’intégrer les activités de la pêche amateur et sportive.

21SmartFish Programme Report SF/2012/8

• Ilestnécessaired’élaborerunmodèlebioéconomiqueappropriépourlapêcheartisanale,qui servirait de boîte à outils de gestion.• Ilestnécessairedemettreenplaceuneunitééconomiquedirigéeparunéconomistedespêches au sein de l’AFRC. L’unité sera chargée de toutes les questions socio-économiques relatives au secteur de la pêche, en particulier la pêche artisanale.• Ilestnécessairederéhabiliterauplustôtleréseaudestationsdedébarquementdupoissonavecla collaboration des communautés de pêcheurs locales (LFC). Les compétences des LFC devront êtrerenforcéesenmatièredegouvernancelocale,deleadershipetdeco-gestion,afindepasser d’une approche externe de la gestion des pêches à une approche où les buts et les responsabilités sont partagés. Il est indiqué que le FIDA-MARS (Fonds International de DéveloppementAgricole)s’estengagéàfinanceruneétudesurunplandegestionexhaustifdela pêche à l’intérieur et hors du lagon dans le cadre du prochain Plan directeur sur la pêche.• Aucuncompromisnedevraitêtreautoriséencequiconcernelasécuritéetlaqualitédupoisson frais mis sur le marché local. Les lignes directrices d’un plan d’action détaillé pour l’applicationduCOP–Manutentionetpréservationdupoissonfrais,sedéclinentcommesuit:

- lancer une campagne nationale de sensibilisation à l’aide de moyens audiovisuels et de FGD (groupesdediscussiondirigée)afinquelesconsommateursetlesproducteursprennent conscience de l’urgente nécessité d’assurer la sécurité alimentaire et la qualité du poisson frais sur lesmarchéslocaux,enparticulierl’utilisationdeglaceenfloconspourlapréservationdupoisson; - entreprendre un audit de l’infrastructure existante pour la pêche dans l’optique d’une mise en œuvre du COP – Manutention et préservation du poisson frais – comme un minimum de sécurité alimentaire et de qualité dans la pêche artisanale. - formulerunpland’actiondétaillécomprenantunbudgetetuncalendrierspécifiquesen consultation avec tous les intervenants de la chaîne d’approvisionnement, y compris les prestataires de services indirects dans le but de créer un environnement propice à la mise en œuvre de normes de sécurité et de qualité ; - appliquer le COP – Manutention et préservation du poisson frais – grâce aux efforts du MOFR, en tant que normes nationales de sécurité alimentaire et de qualité pour la commercialisation du poisson frais ; - développerunplanderessourceshumainesauxniveauxdessecteurspublicetprivéafind’assurer la mise en œuvre harmonieuse des normes de sécurité et de qualité ; - mettre en œuvre un projet pilote sur le COP - Manutention et préservation du poisson frais – surlabasedurespectvolontaireàTamarinouàTroud’eauDouce,oùexistentdesglacières,afin d’illustrer son importance.

• Ilestnécessaired’élaborerunnouveauconceptdeTerminaldupoissondansdessitesstratégiquesquiagirait également comme attraction touristique, en tant que stratégie visant à maximiser les revenus de la pêche artisanale. L’héritage culturel des communautés de pêcheurs, les activités quotidiennes au quai de pêche etlemarchédesproduitsdelamerconstituerontlethèmeprimordialdececoncept.Leprojetcréerades interactions/synergies positives entre les pêcheries artisanales et le secteur du tourisme. Il est proposé de préparer une étude de préfaisabilité et un business plan en vue de développer un projet pilote qui sera installé à la «Maison des Pêcheurs », sur le front de mer du village de pêcheurs de Mahébourg.• Lesperspectivesdedéveloppementd’activitésdetransformationetd’ajoutdevaleuràl’échelledemicro et petites entreprises croîtront graduellement avec l’augmentation de l’approvisionnement en poisson frais. FITECdevraadopteruneapprocheproactiveetdeguichetuniqueafind’aiderlespromoteursgrâceàla facilitation du projet, la formation en compétences techniques et d’entreprenariat et l’encadrement.• Ilestnécessairederenforcerlescapacitésdegestionetdevulgarisationdel’AFRC(Centrederecherche d’Albionenmatièredepêche)encréantunObservatoireéconomiquedirigéparunspécialistede l’économie des pêches. Cet Observatoire sera chargé de toutes les questions socioéconomiques relatives au secteur de la pêche, entre autres, de l’analyse des coûts-avantages des décisions politiques, des études socioéconomiques et de l’appui technique au FITEC (Fisheries Training and Extension Centre - Centre de

22 SmartFish Programme Report SF/2012/8

formationetdevulgarisationenmatièredepêche).• Ilestnécessairedemettreenplaceunprojetpiloteenvuederenforcerlescapacitésdescommunautés de pêcheurs locales en gouvernance locale, en leadership et gestion participative, de sorte qu’elles se partagent l’engagement et la responsabilité dans la formulation des décisions et le respect volontaire des normes ; et en co-gestion des infrastructures de pêche locales telle que les stations de débarquement.

De nombreuses organisations internationales et régionales ainsi que des initiatives de coopération intergouvernementales sont actives dans le sous-secteur de la pêche artisanale. Un nouveau Plan directeur sur la pêche est en voie d’approbation par le Conseil des ministres. Il est nécessaire d’adopter une approche concertée en vue d’allouer des ressources techniquesetfinancièressuffisantespourmettreenœuvrelesrecommandationssusmentionnées.

Introduction

23SmartFish Programme Report SF/2012/8

1.0 Introduction

TheGovernmentofMauritiusaccordshighprioritytothesustainabledevelopmentoftheartisanalfisheriessub-sectorbecause of its crucial role in providing employment opportunities and protein diets to some 4,000 households in themarginalcoastalregionsofthecountryandthuscontributingsignificantlytopovertyalleviation,foodsecurityandgender emancipation. Artisanalfisheriesarethemainsuppliersof freshfishtothedomesticmarkets inMauritius.Asmallquantityofhighgradereeffish,mainlychilledsnappers isalsoexportedtoRéunionIsland.Currentlythetotalcatch isestimatedat830tonnes,whichisclosetotheMSYofthetargetedfishstocks.Asof2010therewere2,303registeredfishersapartfromanincreasinglylargenumberofnon-registeredactiveamateursandsportfishersoperatinginthelagoonandoff-lagoon.Therewere2,525registeredfishingboatsbutaccordingtoarecentsurveyoftheAFRC,only70%oftheseregisteredfishersandfishingboatsareactive.Themarketingfunctionsareperformedbysome400licensedfishmongersatwholesaleandretaillevels.

This study is conducted under the “Implementation of Fisheries Regional Strategies for the ESA-OI” under the aegis of the IOC and funded by the EU. The overall objective of the Programme is to enhance socio-economic and environmentaldevelopmentanddeeperregionalintegrationintheESA-OIthroughsustainableexploitationoffisheriesresources.ThisassignmentfallsspecificallyundertheModuleofResult4relatedtotheimplementationofstrategicimprovementtoproductionandsupplyoffish.TheaimofthisVCA12is to gain a deeper understanding of the value chain with particular emphasis on the production functions, market structures and marketing channels of the artisanal fisheriessub-sector,soastoassessitseconomicefficiencies.Thestudywillalsoexaminetheunderlyingprospectsandweaknessestocomeupwithanactionplantoenhancesustainabledevelopmentoftheartisanalfisheriesinahighlydynamic and competitive global environment.

1.1 Work Plan and Implementation

• Toexaminethemarketstructuresandmarketingsystemsoffishproductionoftheartisanalfisheriessub-sector;

• Todeterminethemarketingcostandmarketingmarginofthefishmongersinthedistributionandmarketstructures;

• Tocollectcriticaldataonproductioncosts(fishingoperations),marketingcost(logisticcost)andproductpricesindifferent market channels (PSP, WSP and CSP);

• Toexaminethevaluechainoffreshfishandfishproductsaimingtodeterminethevalueadditiontomarketedfishat different levels of market channels;

• To investigate the key factors for improvement of preservation, quality, value addition, processing and marketing of fishproductionoftheartisanalfisheries.

1 The terms of reference of the study is given in Appendix 1

24 SmartFish Programme Report SF/2012/8

1.2 Methodology

ThisisthefirstVCA23intheartisanalfisheriesofMauritius.Itwasnotpossibletoconductaclassicalstratifiedsurveyofthe sub-sector. A preliminary survey was carried out to determine cost and revenue data which were readily available and those that had to be collected or derived to perform the study. A systemic approach was adopted to gather quantitative and qualitative data through primary and secondary surveys without compromising the consistency of the study. RRA and FGD were primarily conducted to have a deeper understanding of structural and functional features of thesupplychainthatincluded:

• Fishers’statuswithregardtoownershipoffishingassets;• Types of gears used; • Commercial grades and market prices of fresh; • Fishmonger status and marketing channels;• Verticalintegrationanddiversificationinsupplychain;• Technologicalandenvironmentalfactors–fishinggears,fishingareas…• Hardandsoftfisheriesinfrastructure:FLS,MdP,Institutionalfishmarkets...• Fisheries regulations; management and monitoring measures;• Seasonal/ regional/variation of catch and market prices;• Location of main production and market centres;• Safetyandqualityoffreshfishonlocalmarkets.• Processing and Value addition activities.

1.2.1 Primary and Secondary Sources

Data were collected both from primary and secondary sources. Fisheries Statistics, PSP and CSP time series of the MOFRwereactualizedthroughfieldworks.DiscussionswereheldwithFIT,FITECandMFFC.FocusgroupdiscussionswereorganisedwithfishersandfishmongersatlandingcentresintheNorth,EastandWest.Literatureresearchwasfocusedonthesestudyreports:

• Annual Fisheries Statistics and Fish Price data from 2009 and 2010 (unpublished) of the MOFR;• Study on Fish Handling, Preservation and Marketing in Mauritius & Rodrigues– Final Report, Volume 1 and 2,

Appavoo & Associates, 2007;• FishHandling,processingandMarketinginMauritius,FAO,2005;• Enquête socio-économique sur la pêche artisanale à Maurice, sous l’égide du Projet Thonier régional Phase II de laCOI/EU,S.Sweenarain,1995.

Following the preliminary surveys, two questionnaires3 werepreparedtocollect inputsandcostdata fromfishingunits4 and marketing enterprises. One–to–one interviews were also arranged with selected stakeholders to cross-check data / information so as to ascertain their accuracy. PSP and CSP data of the FD are limited to the FLS. Complementarypricedataweregatheredfrominstitutionalfishmarketsinmaintownsandvillages;fishpeddlersandhawkers;dedicatedfishshopsandfishstallsinsuper/hypermarkets.

2 The theory of Value Chain Analysis was developed by Micheal Porter in 1980. It is applied to determine the efficiencies of each and every component of a business enterprise so as to improve its over comparative advantages and competitiveness on the markets.

3 Given in Appendices 2 and 3 4 A fishing Unit or enterprise is considered as an economic unit and is defined in terms of ownership of fishing assets and control of fishing operations and marketing of harvested fish. This concept leads to a better understanding of the economic role of fishing labour / crew in the artisanal fisheries.

Methodology

25SmartFish Programme Report SF/2012/8

1.3 Analysis

The analytical works aim at determining the economic efficiencies and income generating capacity/profitability ofenterprisesinvolvedinthesupplychainoftheartisanalfisheries.Astandardizedbusinessmodel5 was used to prepare IncomeandExpenditureStatements for thevarious typesof fishingactivities. Economicefficiency ismeasured intermsofprofitability,costofproduction(COP),break-even(B/E)revenueandotherrelevantfinancialratios.TheB/ERevenue was assumed on the basis of a minimum monthly salary of Rs 10,000 as an opportunity cost of labour. A specificcasestudywaspreparedforeachoneofthetypicalfishingenterprises:

• HandLinefishery• Basket Trap Fishery • Large Net Fishery• Non-motorizedhandline(lagoon)fishery• On-footLine&Harpoon(lagoon)fishery

In the VCA of the marketing channels, two important variables were measured namely marketing cost and marketing margin. While marketing margin represents the difference between consumer and producer price, marketing cost consistsofmaterial andnon-material costs involved inperformingmarketing functionsby the fishmongers.Thesefunctionsincludetransportation,grading,storage,processing,financingandotherdirectservices.Themainplayersinthe marketing channels are wholesalers/distributors and different types of retailers.

Verticalintegrationorlinkagebetweenproductionandmarketstructuresanddiversificationarecommonintheartisanalfisherieswhereby:

• Anincreasingnumberoffishingunitsareinvolvedinretailmarketingeitherbydirectsaleorthroughahouseholdroadsidefishstall.Fishersdonotrequireafishmongerlicensetoselltheircatchtoendconsumers.

• About25%oflicensedfishmongersareownersofupto3fishingboats(Appavoo&Associates,2007).Itispartoftheirbusinessstrategytosecureregularandadequatesupplyoffish.Theynormallymanagethefishingoperationsbycontractingfishingcrew/labour.

5 The fishing Business Model used for the Value Chain Assessment is given in Appendix 4

26 SmartFish Programme Report SF/2012/8

2.0 Overview of the Artisanal Fisheries Sub-sector 2.1 Fisheries Policies

With an EEZ of 1.9 million km², the Government of Mauritius envisions the land based oceanic industries as a strategy for extracting more value from the ocean to spearhead sustainable economic growth. Development of the seafood hub6,1themarine fisheries and aquaculture forms part of the aforesaid strategy. Actually the fisheries sector has acontribution of about 1% of the GDP and provides some 20,000 direct and indirect jobs.

Government through its “People First” philosophy is laying special emphasis on the development of the artisanal fisheriessub-sectorandonthewelfareofcoastalfishercommunitiesthroughvarious institutionsandprogrammes.It isrecognizedthatthesocialwelfareprogrammeinfavourofprofessionalfishersinMauritius isuniqueandhighlygenerous. However, this approach may be appropriate for socio-economic and ecological sustainability of the coastal fisheries.

The Fisheries and Marine Resources Act 2007 provides a policy framework of the Government with regards to the developmentoftheartisanalfisheriessub-sectorthatfocusesonaccesstoinvestmentcapitalthroughtheEmpowermentFund,SMEDA,SMEPartnershipFundandextensionservicestoempowertraditionalfisherstoparticipateactivelyinthedevelopmentofFADanddeep-seademersalfisheries.AnambitiousFisheriesMasterPlan is in theprocessofapproval by the Cabinet.

FITECwassetup toprovide tailor-cut trainingcourses infishing technologyandfishhandlingandpreservation toenhanceoverallcapabilitiesofregisteredfishersandlicensedfishmongers.TheextensionservicesdispensedbyFITEChave to be further oriented towards effective BDS including facilitation and mentoring of new entrants in the extended artisanal fisheries. Itwillhaveakey role toplay inpromotingmicroand small scaleprocessingandvalueadditionactivitiesintheartisanalfisheries.

FITwassetupin2006toactasaninvestmentarmoftheGovernmentinfisheriessectorandmandatedbyitsparentMinistrytoinvestinfishing,processing,logisticsandmarketingactivities.RegisteredfishersareshareholdersoftheFITand are represented on the Board of Directors. It will have to take the lead in promoting investment in promoting viablecommercialprojectssuchasintegratedfishterminals,iceplantsandlogisticsservicesintheartisanalfisheries.Governmenthaspromoted“SyndicatdesPêcheurs”toencouragelocalfishercommunities(LFC)toparticipateinpolicyformulationandinjointmanagementofthefisheriesecosystemsandinfrastructure.Thisorganisationhastobeequippedwith local governance, leadership and participatory management skills through capacity building programmes. Emphasis hastobelaidonthesocialimplicationsofvoluntarycompliancetofisheriesregulations,sustainablemanagementandconservation of marine resources.

2.2 Supporting Institutions

The Fisheries Division (FD) is under the organisational structure of the MOFR and is responsible for the overall managementanddevelopmentofmarineresourcesintheEEZofMauritiusincludingfisheries,aquacultureandtheseafood hub. It is organized into various services to cater for Research & Development, Management and Protection

6 Seafood hub is defined as an efficient and attractive environment for the supply of value added processes and services related to the sourcing and market of sea food products.

Overview of the Artisanal Fisheries Sub-sector

27SmartFish Programme Report SF/2012/8

of marine resources and so on. AFRC and FITEC are also under the aegis of FD. An audit is underway at AFRC to align its organisational and functional structures to the challenges and opportunities ahead of the Mauritian seafood sector. MFFCregroupsover600registeredfishersincluding16LNfishercooperativesocietiesinMauritius.Itwasestablishedinthe1970stoemancipateandempowerthefishercommunities.ActuallytheMFFCisvettedbytheMOFRandMOC for theoperationalizationof3 integratedfish landing centres commonly knownas “MaisonsdesPêcheurs”(MdP) at Cap Malheureux, Tamarin and Mahebourg. The MdP at Cap Malheureux is inactive while the other ones at TamarinandMahebourgareunderutilized.MFFCisanimportantplayerinthedistributionandmarketingoffreshfish.Theyhaveanice-plantof500kgperdaycapacityatTamarin,whichcanbeincludedinapilotprojectforpreservationoffreshfishintheregion. TheseMdParelocatedatstrategicpointsofthecoastalfisheriesandmajortouristhubsontheisland.Itisproposedto prepare a pre-feasibility for the conversion of the MdP at Fishermen Village of Mahebourg Waterfront into an integrated Fish Terminal cum dedicated commercial complex as a pilot project to create positive synergies with the tourism industry.

TheCompetentAuthority(CA)istheapexorganisationwithregardtohealthandsanitarystandardsforfishandfishproducts. It is responsible for compliance with HACCP and EU health and sanitary standard in the seafood export industry. It also provides a one-stop-shop for export formalities to the seafood hub in Port Louis. Actually there is no foodsafetyandqualitystandardapplicabletotheartisanalfisheries.Theseworldclassstandardsmightbeanidealfortheartisanalfisheriesinthelong-run.However,thejourneymuststartwiththecreationofanadequateenvironmentfortheenforcementoftheCOPforhandlingandpreservationoffreshfishandCPCFestablishedbyFITEC.

2.3 On-going Programmes in the Artisanal Fisheries

Thereareseveralon-goingnational,regionalandinternationaltechnicalassistanceprogrammesintheartisanalfisheriesandcoastalmarineecosystems.Theseprogrammesincludeamongstothers:• The electronic fish auction market (EFAM) project at Fort William was sponsored financially by the Greek

Government and implemented by the MOFR. The project is nearing completion this year and its operationalization will be entrusted to the Private Sector. The assistance of SmartFish is sought to provide STE for the preparation of a feasibility study in view of preparing an international bidding exercise to allocate a service provider contract. The project is due to become operational next year.

• IFAD-MARSinitiativetoconductaValueChainAnalysisintheFADfisheries.Itisindicatedthatthebiddingprocessisunderway. This institution is also committed to provide technical assistance in the preparation of a comprehensive managementplanforthelagoonandoff-lagoonfisherieswithintheframeworkofthenewFisheriesMasterPlan.

• MauritiusisanactiveparticipantofSWIOFPandACP-FISHII,whicharedeliveringtechnicalandscientificassistancesinfishstockassessmentandmanagementintheartisanalfisheries.Thereisanurgentneedtoundertakeariskassessmentstudyonfishstockcommonlyexploitedby theartisanalfisheries.The technicalassistancemaybeextended to create a bio-economic model to serve as an effective tool for management and monitoring.

FDalsobenefits from the technical assistance frombilateral cooperationwith Japan,Norway andAustralia in thefisheriessector.

2.4 Coastal Fisheries Infrastructure

Thereare60FLSaroundMauritius that serveasoperationalbases tocoastal fishingactivities.Statutorily theyaremandatedforunloadingfishandforfisheriesdatacollection.Theyconsistofsmallconcretestructureswithbasicutilitiessuchaswater,electricity(atsomeplaces)thatservefordischarging,cleaning,gradingandprimarysaleoffish.Theyaremanaged by FD and maintained by the Local Authorities. These FLS have outlived their purposes and most of them

28 SmartFish Programme Report SF/2012/8

havebecomeobsoleteforthefollowingreasons:• They are not accessible during low tides (dredging works required);• They are far from the Fisheries Post and traditional landing sites;• They are in an unhygienic condition;• There is no attached washroom and toilet;• Absenceofactiveparticipationofthelocalfishercommunities.

TheMOFRhasstartedmodernizingsomeoftheseFLS.Thenewonese.g.theoneatAlbion,ismorefisher-friendly.Itprovidesforlockerstostackfishinggearsandoutboardengines.Localfishercommunitiesandfishmongersarethemain users of the FLS and therefore they have to be consulted on any rehabilitation works / development of new facilities.TheyshouldbeempoweredtoparticipateinthemanagementofthefisheriesinfrastructuretogetherwiththeFD and the local authorities.

2.5 Fish Resources in the Lagoon and Off-lagoon

Todateabout60%offishharvestedbytheartisanalfisheriesisstillfromthelagoon.Fishstocksinthelagoonandoff-lagoon are exploited to their MSY levels (Boyer & Soondron, 2009). A series of restrictions such as; a close season of sixmonthsforthenetfisheries,abanonimportsofsmallhooksandacrackdownonillegalfishing,areimplementedbytheFDtohelpthefishstockstorecover.Animpactassessmentoffishgearsusedbytheartisanalfisheriesonthemarineecosystemandnon-targetedfishspecieshastobecarriedoutsoastoimprovemanagementandconservationpolicies.

AplethoraofincentiveshavebeenintroducedbytheMOFRtodivertfishingeffortsfromthecoastalfishingzonestodeep-seaFADanddemersalfisheries.However,themobilityoftraditionalfishersisusuallyveryslowduetheiraversiontonewtechnologiesandreluctancetochange.Consumers’preferencefortraditionalreefanddemersalfishisalsoresponsibletosomeextentfortheslowdevelopmentoftheFADfisheryinMauritius.Itwasassumedthatconsumerswould readily accept tuna and tuna-like species. It is necessary to embark on a nation-wide awareness campaign tosensitizeconsumersandthepopulationat largeontheneedtomodifytheirfishconsumptionhabit infavouroflargepelagicfish.BysodoingtheywillcontributesignificantlytotheconservationoffishstocksinthelagoonandinpromotingprivateinvestmentsintheFADfishery.Thereisunlimitedscopeforprocessingandvalueaddedactivitiesof raw tuna for the local and export markets. Similar development models can be adapted from the experience of countries like Hawaii, Bangladesh, Uganda and so.

Theactualcoastalfisheriesmanagementandconservationmeasurescannotyieldtheexpectedresultsbecauseoftheprevailing open-access environment,whichistantamounttothehighriskofoverexploitationofthefishstocks.Thenumberofnon-registeredactive,amateurandsportfishersactiveincoastalfisheriessignificantlyexceedsthenumberof registered fishers7.2To attain socio-economic and ecological sustainability in the artisanal fisheries, developmentstrategiesmustfocusonselectionoffishinggears8,quality,valueadditionandefficientmarketing,asultimatemeanstomaximiseeconomicrentofthefishresourcesandrevenueofthestakeholders.

7 According to a Survey conducted by the Ministry of Fisheries and Cooperatives in 2003, there were over 25500 of amateur fishers operating regularly in the coastal fisheries. It is likely that this figure has increased significantly.

8 Selectivity of fishing gears promotes eco-friendly technologies so as to reduce negative impacts of fishing activities on the marine ecosystem. They are instrumental to avoid untargeted fish species and undersized fish with low commercial value.

Overview of the Artisanal Fisheries Sub-sector

29SmartFish Programme Report SF/2012/8

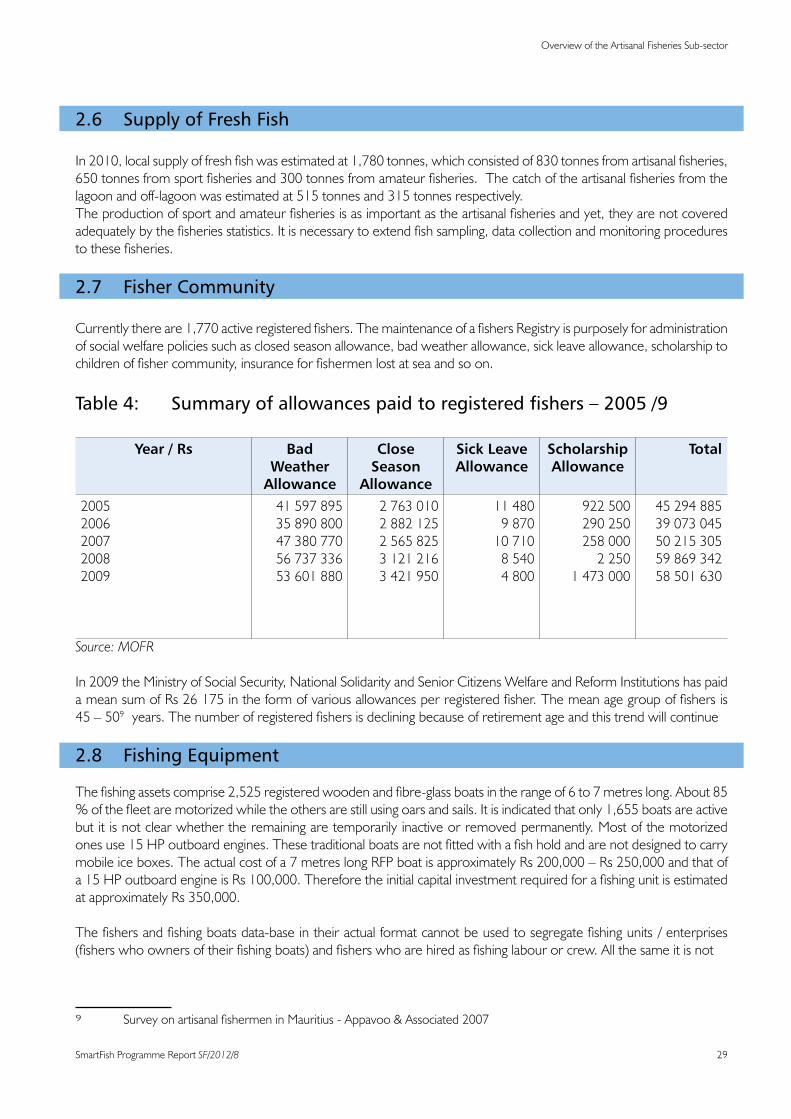

2.6 Supply of Fresh Fish

In2010,localsupplyoffreshfishwasestimatedat1,780tonnes,whichconsistedof830tonnesfromartisanalfisheries,650tonnesfromsportfisheriesand300tonnesfromamateurfisheries.Thecatchoftheartisanalfisheriesfromthelagoonandoff-lagoonwasestimatedat515tonnesand315tonnesrespectively.Theproductionofsportandamateurfisheriesisasimportantastheartisanalfisheriesandyet,theyarenotcoveredadequatelybythefisheriesstatistics.Itisnecessarytoextendfishsampling,datacollectionandmonitoringprocedurestothesefisheries.

2.7 Fisher Community

Currentlythereare1,770activeregisteredfishers.ThemaintenanceofafishersRegistryispurposelyforadministrationof social welfare policies such as closed season allowance, bad weather allowance, sick leave allowance, scholarship to childrenoffishercommunity,insuranceforfishermenlostatseaandsoon.

Table4: Summaryofallowancespaidtoregisteredfishers–2005/9

Year / Rs Bad Weather

Allowance

Close Season

Allowance

Sick Leave Allowance

Scholarship Allowance

Total

20052006200720082009

4159789535890800473807705673733653601880

27630102882125256582531212163421950

11 4809 870

10 71085404 800

9225002902502580002250

1473000

4529488539073045502153055986934258501630

Source: MOFR

In 2009 the Ministry of Social Security, National Solidarity and Senior Citizens Welfare and Reform Institutions has paid ameansumofRs26175intheformofvariousallowancesperregisteredfisher.Themeanagegroupoffishersis45–5093years.Thenumberofregisteredfishersisdecliningbecauseofretirementageandthistrendwillcontinue

2.8 Fishing Equipment

Thefishingassetscomprise2,525registeredwoodenandfibre-glassboatsintherangeof6to7metreslong.About85%ofthefleetaremotorizedwhiletheothersarestillusingoarsandsails.Itisindicatedthatonly1,655boatsareactivebut it is not clear whether the remaining are temporarily inactive or removed permanently. Most of the motorized onesuse15HPoutboardengines.Thesetraditionalboatsarenotfittedwithafishholdandarenotdesignedtocarrymobileiceboxes.Theactualcostofa7metreslongRFPboatisapproximatelyRs200,000–Rs250,000andthatofa15HPoutboardengineisRs100,000.ThereforetheinitialcapitalinvestmentrequiredforafishingunitisestimatedatapproximatelyRs350,000.

Thefishersandfishingboatsdata-baseintheiractualformatcannotbeusedtosegregatefishingunits/enterprises(fisherswhoownersoftheirfishingboats)andfisherswhoarehiredasfishinglabourorcrew.Allthesameitisnot

9 SurveyonartisanalfishermeninMauritius-Appavoo&Associated2007

30 SmartFish Programme Report SF/2012/8

possibletoidentifyfishmongerswhoarealsoownersoffishingboats.TheaboveinformationarekeptandmaintainedinhardcopyatregionalFisheriesPosts.Itisnecessarytocreateaninteractivedata-basetodealwithfishers,boatsandfishmongerinputsatthenationallevelformanagementandmonitoringpurposes.

2.9 Fishing Gears

Themaintypesofgearusedintheartisanalfisheriesaredescribedbrieflybelow:

Hand linefishing isfishingwithasinglefishing lineheld in thehandswithoneormorebaitedhooksor lures thatcontributesto20%ofthetotalcatch.Itisaselectivegearandtargetshighvaluebottomfishesinthelagoonandoff-lagoon.ThetargetedfishspeciesareVieilleRouge(RedSnapper)andCapitaine(Emperor).

Basket Trapsaremadeofgalvanizedsteelsmeshandarepassiveandclose-endgearused to trapreeffishes. It isthemostcommonfishinggearoftheartisanalfisheriesandissometimesusedalternatelywithhandlining.Themainharvested species is Licorne (82%).

Large Net Fishery consistsofusinganetof500mlongtoencirclereeffishinthelagoon.OneNetfishingoperationcomprisesaminimumof3fishingboatsand15fishers(about5fishersperboat).Thenetfisheryharvests22%ofthetotalcatch,whichcomprisesCordonnier(30%),Licorne(37%)andCapitaine(22%).Thenetfisheryisregulatedintermsofprescribedsizeofmeshandlengthofnet,renewalofwornoutnetsandacloseseasonof5monthsfromOctobertoFebruaryannually.DuringcloseseasonregisterednetfishersareentitledtoanallowanceofRs210perdayinspiteofthefactoftheexistenceofabuybackschemetoencouragenetfisherstogiveupthisfishery.

Since 1996 the Government has introduced a buy-back scheme for nets for the reduction of nets operating in the lagoon.Presentlythereare15largenetsinactivity.

On-foot, Line and Harpoon Fishery is practiced on foot during low tides and in shallow waters in the lagoon. It targets mainlyoctopusandsmallreeffish.31%offishersinthisfisherycontributetoonly15%oftheproduction.MOFRhasintroducedabanonimportsofsmallhookstoavoidthefishingofjuvenilefishinthelagoon.

Table5: Totalcatchbyfishers,byfishinggearsandfishingboats(2010)

Items HL BT BT/HL LN O/F-HL/H TOTAL

Registered Fishers (N)PercentageActive Fishers

F/Boats (N)PercentageActive fishing boats

Catch (t)Percentage

28312%212

112444%728

22727%

27911%195

114946%761

26732%

86236%638

2259%149

283%

1466%106

271%17

22228%

73335%620

---

8710%

2303100%1770

2525100%1655

831100%

Source: Annual Report 2010 - MOFR

Overview of the Artisanal Fisheries Sub-sector

31SmartFish Programme Report SF/2012/8

Withtheexceptionofthenetfishery,whichispseudoregulated,thereisnorestrictionwhatsoeverontheuseofHLor BT. HL is a more selective and more environmentally friendly gear as compared to BT and LN. During the close season,netfishersmayoptforHLand/orBTfishing.

2.10 Preservation of Fish on Board

Thereisaseriousconcernaboutsafetyandqualityoffishlandedbytheartisanalfisheries.Postcapturehandlingandpreservationproceduresarenon-existent.Consumerssuspectthefreshnessandqualityoffishpreservedonice.Themainreasonsadvancedbythefishersfornotusingiceare:

• Catch is kept only for a few hours on board and is sold immediately at FLS;

• Fishing boats are not equipped with an ice box or ice;

• IceincubesorflakesisnotavailableattheFLS;

• Consumershaveanaversionforfishpreservedinice;

• Additional operating cost.

Safetyandqualityoffreshfishismandatorytoavoidhealthhazardsandpoorqualityofrawfishonthelocalmarkets.An intensive awareness campaign through audio-visual means to sensitize producers, consumers and logistics services providersaboutfoodsafetyandqualityoffreshfishisrequired.AllstakeholderswillhavetoworktogethertoimplementtheCOP–HandlingandPreservationoffreshfishalongthesupplychain.

32 SmartFish Programme Report SF/2012/8

3.0 VCA of Fishing Enterprises

Asstatedinsection1.2above,thisstudyrepresentsanattempttoassesstheeconomicefficienciesanddistributionofthevalue-added,ofthevarioustypesoffishingunitswithintheartisanalfisheriessub-sector.Theanalysisnormallyis carried using accounting records. In the absence of the relevant accounting records and procedures, the consultant had to gather cost and revenue data so as to prepare Income and Expenditure Statements in the form of case studies foreachtypeoffishingunit.

Keyfactors/assumptionsapplicabletoallthefishingunitsareasfollows:

• Capital Investment-Actualcostofa6-7mfishingboatwhetherwoodenorfibreglassisatRs200,000andisdepreciatedattherate5%perannum(anaveragelifetimeof20years).ActualCostofa15HPoutboardengineia

atRs100,000andisdepreciatedattherate20%perannum(anaveragelifetimeof5years).

• Informal sector-Noformalaccountingproceduresarefollowedbyartisanalfishers.

• Seasonal variation - Fishing activities are more intensive and productive in the summer (6 months), than in the winter(6months)duetobadweather.Itisassumedthatafishingboatmakes2fishingtrips/weekduringwinterand5fishingtripsperweekduringsummer.Onthebasisof52weeksperyear,thetotalnumberoffishingtripsperyearisat182e.g.52fishing/daysinwinterand130fishing/daysinsummer.

• Classification of Commercial grade of fish-asestablishedbytheMOFRwasusedasitregroupsallfishspeciesinto6groupsaccordingtotheirrespectivecommercialimportance.Thesecommercialgradesreflectthemarket realities in Mauritius and were used in this study.

• Latest PSP and CSP time series data of the MOFR - used and actualized by primary surveys; e.g. catch compositionbygearandPSPatFLS.Table6onthefollowingpageshowsPSPDataforthefishingunitsforspeciesgroups.

• Cash business -Paymentreceivedfromfishmongersandprovidedtofishingcrewiscustomarilyonaweeklybasis. The transactions are mostly on a cash basis.

• A conservative approach is adopted so as to avoid under estimates of cost and/or over-estimates of revenue.

• License-Afisherdoesnotrequireafishmongerlicensetosellhiscatchdirectlytoendconsumers.

• Auto-consumption-Fishtakenhomebyfisherscommonlycalled“curry”isnotincludedinthesimulations.

• There is no Value Added Tax (VAT)onfreshfish.

• Environmental / ecological cost-(damagescausedbyaspecificgeartothemarineecosystem)isincludedin the VCA.

• The revenue estimates are before any interest paid on loans and income tax.

VCA of Fishing Enterprises

33SmartFish Programme Report SF/2012/8

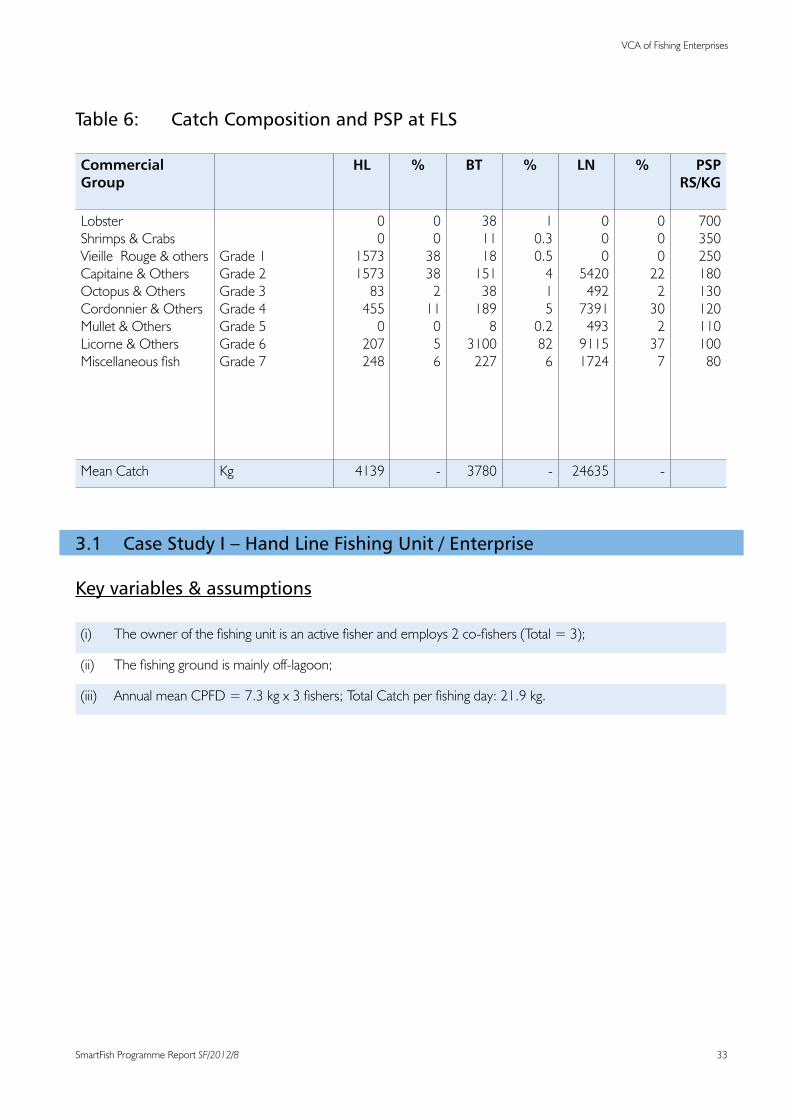

Table 6: Catch Composition and PSP at FLS

Commercial Group

HL % BT % LN % PSPRS/KG

Lobster Shrimps & Crabs Vieille Rouge & othersCapitaine & OthersOctopus & OthersCordonnier & OthersMullet & OthersLicorne & OthersMiscellaneousfish

Grade 1Grade 2Grade3Grade 4Grade5Grade 6Grade 7

00

1573157383455

0207248

003838

211

056

38111815138

1898

3100227

10.30.5

415

0.282

6

000

5420492739149391151724

000

22230

237

7

700350250180130120110100

80

Mean Catch Kg 4139 - 3780 - 24635 -

3.1 Case Study I – Hand Line Fishing Unit / Enterprise

Keyvariables&assumptions

(i) Theownerofthefishingunitisanactivefisherandemploys2co-fishers(Total=3);

(ii) Thefishinggroundismainlyoff-lagoon;

(iii) AnnualmeanCPFD=7.3kgx3fishers;TotalCatchperfishingday:21.9kg.

34 SmartFish Programme Report SF/2012/8

3.1.1 Income and Expenditure Statement

Thefollowingtableshowsanormalyearofactivityforahandlinefishingunit.

Table 7: Income and Expense for Hand Line Fishing Unit

Items (a normal year of activity) Rs Rs Rs

Sales – 4139 kg @ Rs 190.70

Less Fixed CostsDepreciation:F/Boat5%p.a;O/boardEngine20%p.aRepairandMaintenance:F/Boat&Engine–10%p.aSundryfixedcosts(Rs1000/month)Less Variable Costs (excluding Labour costs)FuelandLubes(Rs800@fishingday)Repair&Replacement–fishinggears(Rs1000p.m.)Baits(Rs200@fishingday)Sundries(Rs100@fishingday)

30 00030 00012 000

151 20012 000 37 80018 900

72 000

219900

789 307

291 900497 407

Less Labour Cost3fishersincl.boatowner-fisher([email protected])Surplus income after provision for depreciation

352 850Rs 144 557

3.1.2 Economic Analysis • Thefishingenterprise’smeanincomepermonthisRs21,848whichincludesRs9,801tofishersandRs 12,047toprofitorsurplusincomeforfishingenterprise);• Fisher(crew)meanincome:Rs9,801/month;• CostofProduction:Rs155.77perkg;• ProfitMargin:Rs34.93perkilo;• ProfitMarginonsales:18%;• Break-evenquantity(TR=TC)=3379kge.g.CPFD=6.0kg.

VCA of Fishing Enterprises

35SmartFish Programme Report SF/2012/8

3.2 Case Study II – Basket Trap Fishing Unit

3.2.1Keyvariablesandassumptions(i) Theboatownerisanactivefisherandhasnoco-fisher.Thefishingunitoperates10baskettrapsperfishing day.(ii) CPFD=20kg;Totalannualcatch:3780kg;(iii) Fishingground:Lagoon&OffLagoon.

3.2.2 Income and Expenditure StatementThefollowingtabledemonstratesanormalyearofactivityfortheBasketTrapfishingunit.

Table 8: Income and Expenses for Basket Trap Fishing Unit

Items (a normal year of activity) Rs Rs Rs

Sales – 3780 kg @ Rs120.21

Less Fixed CostsDepreciation:F/Boat5%p.a;O/boardEngine20%p.aRepairandMaintenance:F/Boat&Engine–10%p.aSundryfixedcosts(Rs1000p.m)

Less Variable Costs (excluding Labour costs)FuelandLubes(Rs800@fishingday)Repair&Replacement–fishinggears(30BT@Rs1500)Baits(Rs100@fishingday)Sundries(Rs100@fishingday)

30 00030 00012 000

151 20045 00018 90018 900

72 0000

234 000

454 394

306 000

Surplus of income after provision for depreciation 148 394

3.2.3 Economic Analysis

• Fishermeanincomepermonth:Rs12366• COP:Rs80.95perkg• ProfitMargin:Rs39.31perkilo• ProfitMargintoSales:32.7%• Break-EvenQuantity=2546kg(67.35%fishingcapacity)

36 SmartFish Programme Report SF/2012/8

3.3 Case Study III – Large Net Fishing Cooperative / Enterprise

3.3.1 Keyvariables&assumptions(i) Onefishingenterprisecomprises3fishingboatsand15fishers(e.g.eachfishingboathas5fishers).The fishingunitoperatesaseinenetof500mlong;(ii) Thefisheryisregulatedintermsofsizeofmeshandlengthofnet,asixmonthcloseseasonfromOctober to March every year;(iii) Fishingground:Lagoon;(iv) Catchperfishingdaysis259.3kg,(84.44Kg/boat)No.fishingdays:95;(v) Fishingcrewremuneration:Oneadditionalshareforboatownerafterdeductionoftripcosts.

3.3.2 Income and Expenditure Statement

ThefollowingtableshowsanormalyearofactivityforalargeNetfishingenterprise

Table 9: Income and Expense for Large Net Fishing Enterprise

Items (a normal year of activity) Rs Rs Rs

Sales – 24 635 kg @ Rs 128.30

Less Fixed CostsDepreciation: 3x (F/Boat 5 % p.a; O/board Engine 20% p.a)Repair and Maintenance: 3x(F/Boat & Engine –10 % p.a) Sundryfixedcosts3x(Rs1000p.m)

Less Variable Costs (excluding Labour costs)FuelandLubes(Rs1000@fishingday)Repair&Replacement–fishinggears(10Nets@Rs4500)Sundries(Rs500@fishingday)

90 00090 00036 000

285 00045 00047 500

216 000

377 500

3 160 690

593 5002 567 190

Less Labour Cost15 Fishers: (5/6 of net revenue after deduction of trip costs) Surplus of Income after provision for depreciation

2 139 325

427 865

3.3.3 Economic Analysis • BoatOwnerIncome=Rs47540/month(forsixmonths)• FishermeanIncome=Rs23770/month(forsixmonths)• COP:Rs110.92perkg• ProfitMargin:Rs17.38perkilo• ProfitMargintoSale:13.6%• Break-EvenQuantity(TR=TC)=21300kg(at86%ofactualcapacity)

VCA of Fishing Enterprises

37SmartFish Programme Report SF/2012/8

3.4 Case Study IV – Non-Motorized Boat Hand Line Unit

3.4.1 Keyvariablesandassumptions(i) OwnerofthefishingUnitisanactivefisherandemploys1co-fisher;

(ii) Thefishinggroundismainlylagoon;

(iii) AnnualmeanCPFD=5.4kgx2fishers;TotalCatchperfishingday:10.8kg.

3.4.2 Income and Expenditure Statement

Table 10 shows a normal year of activity for a non-motorised boat hand line unit

Table 10: Income and Expense for Non-motorised Boat Hand Line unit

Items (a normal year of activity) Rs Rs Rs

Sales – 2041 @ Rs 126.92

Less Fixed Costs

Depreciation:F/Boat5%perannunRepairandMaintenance:F/Boat–10%Sundryfixedcosts(Rs500/month)

Less Variable Costs (excluding Labour costs)

Repair&Replacement–fishinggears(Rs600/month)Baits(Rs100@fishingday)Sundries(Rs100@fishingday)

Cost of Labour – Rs 1021 Kg @ 60.21

10 00020 0006 000

7 200 18 90018 900

36 000

45 000

259 065

81 000178 06561 474

Surplus of income after provision for depreciation 116 291

3.4.3 Economic Analysis

• Meanannualincomeoffishingenterprise:Rs116292orRs9691permonth• Fishermeanincomepermonth:Rs5123

38 SmartFish Programme Report SF/2012/8

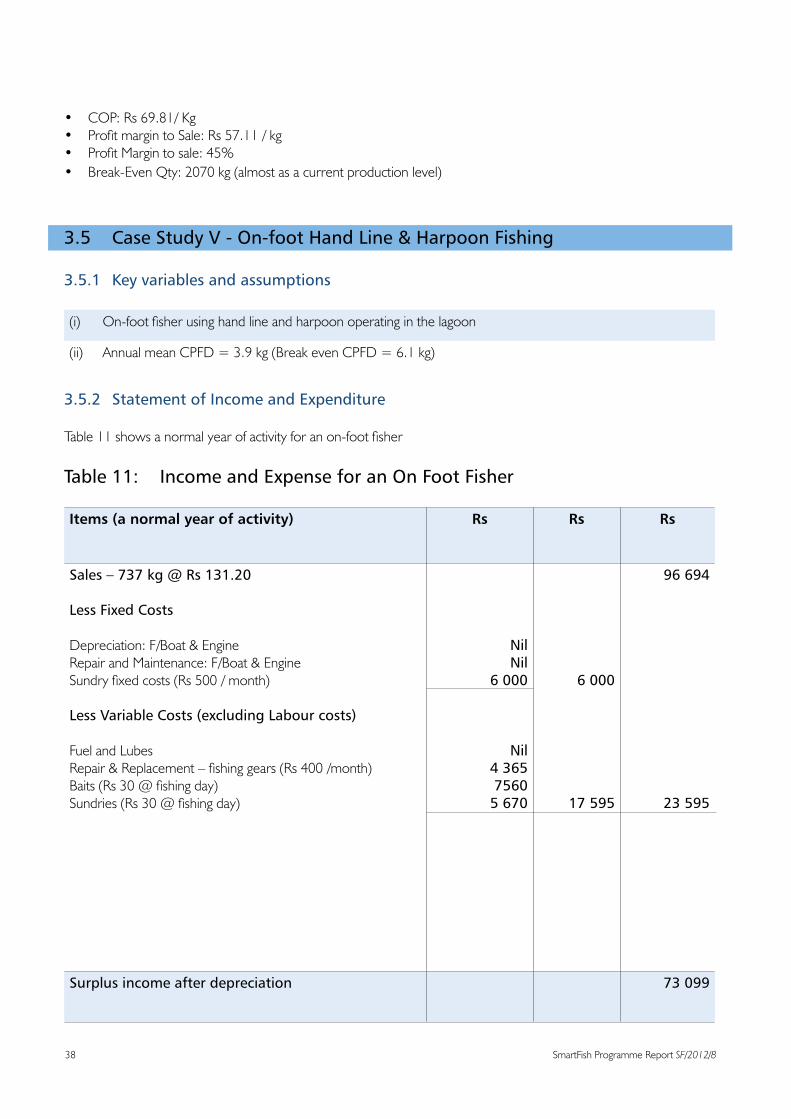

• COP:Rs69.81/Kg• ProfitmargintoSale:Rs57.11/kg• ProfitMargintosale:45%• Break-EvenQty:2070kg(almostasacurrentproductionlevel)

3.5 Case Study V - On-foot Hand Line & Harpoon Fishing

3.5.1 Keyvariablesandassumptions

(i) On-footfisherusinghandlineandharpoonoperatinginthelagoon

(ii) AnnualmeanCPFD=3.9kg(BreakevenCPFD=6.1kg)

3.5.2 Statement of Income and Expenditure