A critical reference source for decision makers in the global Islamic � nance industry, providing strategic insights from Ernst & Young

Dear Banking & Finance Leader,

It is with great pleasure that we present to you the 8th annual edition of the World Islamic Banking Competitiveness Report 2011-12. This year’s original research project is developed in collaboration with leading global professional services and advisory fi rm, Ernst & Young. With a principal focus on “A Brave New World of Sustainable Growth”, the WIBC Competitiveness Report 2011-12 explores the key industry trends and the critical success factors guiding the global Islamic banking and fi nance industry to the next level of performance and growth.

The global Islamic fi nance industry has undergone major transformations in the last few years in its quest to boost international competitiveness and to build a sustainably profi table business model. There has been a focus on product innovation eff orts that aim to provide a more comprehensive array of Shari’ah-based products for the market. The global Islamic fi nance industry has also seen signifi cant developments in regulatory frameworks and Shari’ah standardization initiatives - making trans-jurisdictional market connectivity that much more achievable. However, both the challenge and the opportunity currently facing leading industry players is how will Islamic banks succeed in making the historical growth curve sustainable and profi table.

We would like to express our sincere gratitude to Ernst & Young and their world renowned Islamic Financial Services Team for investing their considerable talent and resources in developing the World Islamic Banking Competitiveness Report 2011-12. The Report is exclusively launched on-site at a special plenary session of the 18th Annual World Islamic Banking Conference (WIBC) where more than 1,200 industry leaders from over 50 countries gather to chart the future of Islamic fi nance.

Established as a critical reference resource for key industry players, thought leaders and policy makers in the global Islamic banking and fi nance industry, we hope that the analysis in this year’s Report will provide practical, constructive and valuable insights which will be useful in your own strategic planning activities and will assist your organization in its quest for success as the Islamic banking and fi nance industry enters the next phase of “Competing for Global Growth”. To fi nd out more on how your organization can play a part in this important research initiative in the future, please e-mail [email protected]

Yours sincerely,Yours sincerely,

David McLeanManaging DirectorThe 18th Annual World Islamic Banking ConferenceA MEGA Brand

A MEGA Brand: Shaping the Future of the Global Islamic Finance Industry Since 1993P.O. Box 72045, Dubai, UAE | t. +9714 343 1200 | f+971 4 343 6003MEGA Brands. MEGA Clients. Market Leaders.www.megaevents.net

18th Annual

World Islamic Banking Competitiveness Report 2011-12

‘A Brave New World of Sustainable Growth’

World Islamic Banking Competitiveness Report 2011-12

‘A Brave New World of Sustainable Growth’

Report Structure

Performance Analysis

Competitive Landscape

Competing to Win: The CEO

Agenda

Country Spotlight

Executive Brief

1

2 3

5 4

COMPETITIVENESS REPORT 2011-20122

A Brave New World of Sustainable Growth

Dear Executive,

The global economy, and the financial markets, are at a turning point. Fast growth economies in Asia, Middle East, Africa, Latin America and Eastern Europe now form almost half of global GDP and, in 2010, they contributed 70% to overall global growth. These trends are accelerating. The dramatic developments over the past twelve months – including Arab Spring, Eurozone crises and Occupy Wall Street movement – provide further impetus for the growth of Islamic banking.

Industry forecast suggest Islamic banking assets with commercial banks globally, will reach $1.1 trillion in 2012 (2010: $826bn). Now would be the opportune time to consider establishing Islamic sovereign wealth funds to champion the growing internationalization of the industry. The iSWF will further facilitate businesses across OIC markets seeking to transform to Shari’a compliant system and also help deepen the Islamic capital market, in our view.

As for MENA, Islamic banking assets increased to $416bn in 2010, representing a five year CAGR of 20% compared to less than 9% for leading conventional banks. As new geographies open up to Islamic banking, the MENA Islamic banking industry is expected to more than double to $990bn by 2015. However, there are significant performance variations across markets. In 2010, average ROE of leading Islamic banks declined to 10%. Also, market valuations appear to be converging to that of regional conventional peers.

Our clients agree that business models needed to shape and sustain success in this new landscape are evolving in a fundamental way. Ensuring sustainable growth will require brave, meaningful and decisive Performance Improvement initiatives. Two key themes are starting to emerge:

► Excellence in banking operations – by transforming to a customer centric, efficient and scalable operating model, driven by an enhanced risk and technology orientation; and

► Product innovation – to strengthen the Shari’a differentiation and provide greater integration with the real economy

A worrying concern though is the absence of an enabling legislative, regulatory, tax and legal environment in most OIC markets, which adds to the cost and complexity of Islamic banking operation. Where there are guidelines and standards issued by industry infrastructure institutions, their reach and enforceability remains a concern. These must be addressed as priority.

Our award-winning global Islamic Finance Center of Excellence continues to work with a diverse range of financial institutions helping them realize the true potential of their business. We trust you will find this report useful.

Ashar M. NazimIslamic Financial Services LeaderErnst and Young

Imtiaz IbrahimSenior Director, Islamic Financial ServicesErnst and Young

Islamic Banking Competitiveness Report 2011-12

Page 3

3COMPETITIVENESS REPORT 2011-2012

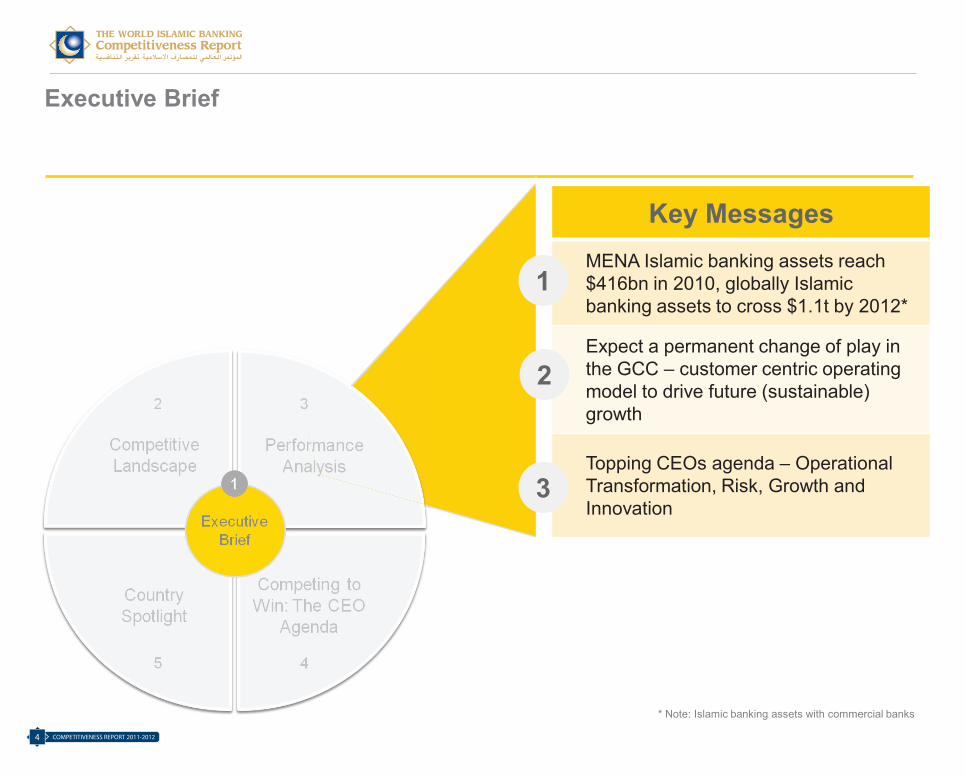

Key MessagesMENA Islamic banking assets reach $416bn in 2010, globally Islamic banking assets to cross $1.1t by 2012*

Expect a permanent change of play in the GCC – customer centric operating model to drive future (sustainable) growth

Topping CEOs agenda – Operational Transformation, Risk, Growth and Innovation

1

2

3

Executive Brief

Islamic Banking Competitiveness Report 2011-12

Page 4

* Note: Islamic banking assets with commercial banks

One potential scenario shows global Islamic banking assets with commercial banks to reach $1.1 trillion in 2012

Global Islamic Banking Assets

2010GCC MENA

(ex GCC)Malaysia Rest of the

World

Source: IMF, The Banker, Central Bank Websites, EY perspective

Islamic Banking Asset Growth (US$bn)

826

12725

38114 1,130

Global Islamic Banking Assets

2012e

Islamic Banking Competitiveness Report 2011-12

Page 5

COMPETITIVENESS REPORT 2011-20124

Key MessagesMENA Islamic banking assets reach $416bn in 2010, globally Islamic banking assets to cross $1.1t by 2012*

Expect a permanent change of play in the GCC – customer centric operating model to drive future (sustainable) growth

Topping CEOs agenda – Operational Transformation, Risk, Growth and Innovation

1

2

3

Executive Brief

Islamic Banking Competitiveness Report 2011-12

Page 4

* Note: Islamic banking assets with commercial banks

One potential scenario shows global Islamic banking assets with commercial banks to reach $1.1 trillion in 2012

Global Islamic Banking Assets

2010GCC MENA

(ex GCC)Malaysia Rest of the

World

Source: IMF, The Banker, Central Bank Websites, EY perspective

Islamic Banking Asset Growth (US$bn)

826

12725

38114 1,130

Global Islamic Banking Assets

2012e

Islamic Banking Competitiveness Report 2011-12

Page 5

5COMPETITIVENESS REPORT 2011-2012

Analysis of leading Islamic commercial banks in the MENA region shows a large variation in the average ROE between 2006-10

Total Assets 2010 Average ROE (2006-2010)

Source: Annual Reports, Zawya, EY analysis (includes sample of leading banks across Middle East and North Africa (MENA) where published information was available)

MENA Conventional AverageUS$38bn 16%

MENA Islamic AverageUS$13bn 15 %

< 9%

> 20 %

Growth(3 Yr CAGR)

Steep Slide

Long Tail

Islamic Banking Competitiveness Report 2011-12

Page 6

10.0%

0.20%

6.7%

7.4%

-1.9%

17.4%

12.6%

1.4%

-2.2%

0.1%

15.5%

12.2%

10.0%

11.6%

19.2%

8.5%

13.1%

15.2%

14.2%

26.0%

Bahrain

Bahrain

Kuwait

UAE

Kuwait

Qatar

Egypt

KSA

Bahrain

KSA

KSA

UAE

Qatar

Qatar

Bahrain

UAE

UAE

Kuwait

KSA

2,272

2,482

4,156

4,538

4,668

5,309

5,453

5,633

6,744

7,114

8,703

8,807

8,915

9,526

14,238

15,880

20,489

22,952

44,498

49,304

Kuwait

COMPETITIVENESS REPORT 2011-20126

Analysis of leading Islamic commercial banks in the MENA region shows a large variation in the average ROE between 2006-10

Total Assets 2010 Average ROE (2006-2010)

Source: Annual Reports, Zawya, EY analysis (includes sample of leading banks across Middle East and North Africa (MENA) where published information was available)

MENA Conventional AverageUS$38bn 16%

MENA Islamic AverageUS$13bn 15 %

< 9%

> 20 %

Growth(3 Yr CAGR)

Steep Slide

Long Tail

Islamic Banking Competitiveness Report 2011-12

Page 6

10.0%

0.20%

6.7%

7.4%

-1.9%

17.4%

12.6%

1.4%

-2.2%

0.1%

15.5%

12.2%

10.0%

11.6%

19.2%

8.5%

13.1%

15.2%

14.2%

26.0%

Bahrain

Bahrain

Kuwait

UAE

Kuwait

Qatar

Egypt

KSA

Bahrain

KSA

KSA

UAE

Qatar

Qatar

Bahrain

UAE

UAE

Kuwait

KSA

2,272

2,482

4,156

4,538

4,668

5,309

5,453

5,633

6,744

7,114

8,703

8,807

8,915

9,526

14,238

15,880

20,489

22,952

44,498

49,304

Kuwait

Libya

Banking industry to be made Shari’a compliant…

Oman

First two Islamic license awarded…potentially a 10% market share play by…

Tunisia

Central bank mulls Islamic banking regulations…

Egypt

Considering sovereign sukuk…

Hong Kong

HK legislating for Islamic banking…

Switzerland

Islamic Bank of Switzerland to open…

KenyaKenya to emerge as the Islamic finance gateway to East Africa…

CISFirst Islamic bank conversion…

Globally as mature markets press forward with banking reforms, many others are keen to explore an alternative Islamic finance option

Banks need US$ 106bn new tier 1 capital by 2012

Source: Published information.Image: Campaigner outside London Stock Exchange in Oct 2011 (Arab News)

by 20122012

Islamic Banking Competitiveness Report 2011-12

Page 7

7COMPETITIVENESS REPORT 2011-2012

By 2015, the MENA Islamic banking industry is projected to be worth $990bn… a significant growth story (2010: $416bn assets)

MENA Islamic Banking Assets - 2015 Forecast (US$bn)

Saudi Arabia

Oman

UAEQatar

BahrainAlgeria

LibyaEgypt

Turkey

Tunisia

MoroccoLebanon

JordanIraq

Yemen

Syria

Kuwait

156

291

13

87

140

7920

104

GCC

North Africa

The Levant

7

7

5

34

12

13

10

8

5

Projected Islamic banking assets 2015 (US$bn) - the size of the circle denotes relative size

Key

Source: 2010 Company Reports, Global Insight, EY perspective

Islamic Banking Competitiveness Report 2011-12

Page 8

COMPETITIVENESS REPORT 2011-20128

Rediscovering profits - Operational efficiency can increase Islamic banks’ profitability by approximately 25%

Current Performance

(2010)1

Growth Momentum2

Potential Combined Islamic Banking Profit Pool (2015)

Operational Improvements

$5bn – $6bn

MENA Islamic Banking - 2015 Combined Net Profit Forecast (US$bn)

$7bn- $9bn

$3bn -$4bn

$15bn - $19bn

1- Based on ROA of 1.5%, 2 – Based on asset growth projections

Emerging Islamic geographies

Affluent retail proposition

Integration with real economy

SME banking

Further Potential Growth Opportunities

► Operational Transformation

► Risk Infrastructure

► Innovation

► Growth Play

Islamic Banking Competitiveness Report 2011-12

Page 9

9COMPETITIVENESS REPORT 2011-2012

The CEO Agenda – There are four emerging trends that will permanently alter the Islamic banking play, especially in the GCC market

The CEO

Agenda

Operational Transformation

Risk & Compliance

Growth Play

Innovation

► Scalable, customer centric operating model, achieved through improved risk and technology orientation (winning back the profitability and valuation advantage)

► Economic capital, risk adjusted returns, funds transfer, pricing, regulations, and compliant products and systems to drive the change in business focus

► Shari’a compliant banking to stimulate financial access to previously unbanked – expect 100 plus new Shari’a compliant banks in MENA by 2020

► Embracing technology to deepen existing relationships and improve new customer acquisition rates

► Product research and structuring, while learning from past experiences (e.g. the sukuk market debacle)

► Having achieved 26% market share in GCC, future growth will come from mainstream customer segment; service model to be the primary proposition

Islamic Banking Competitiveness Report 2011-12

Page 10

COMPETITIVENESS REPORT 2011-201210

The CEO Agenda – There are four emerging trends that will permanently alter the Islamic banking play, especially in the GCC market

The CEO

Agenda

Operational Transformation

Risk & Compliance

Growth Play

Innovation

► Scalable, customer centric operating model, achieved through improved risk and technology orientation (winning back the profitability and valuation advantage)

► Economic capital, risk adjusted returns, funds transfer, pricing, regulations, and compliant products and systems to drive the change in business focus

► Shari’a compliant banking to stimulate financial access to previously unbanked – expect 100 plus new Shari’a compliant banks in MENA by 2020

► Embracing technology to deepen existing relationships and improve new customer acquisition rates

► Product research and structuring, while learning from past experiences (e.g. the sukuk market debacle)

► Having achieved 26% market share in GCC, future growth will come from mainstream customer segment; service model to be the primary proposition

Islamic Banking Competitiveness Report 2011-12

Page 10

Report Structure

Performance Analysis

Competitive Landscape

Competing to Win: The CEO

Agenda

Country Spotlight

Executive Brief

1

2 3

5 4

Islamic Banking Competitiveness Report 2011-12

Page 11

11COMPETITIVENESS REPORT 2011-2012

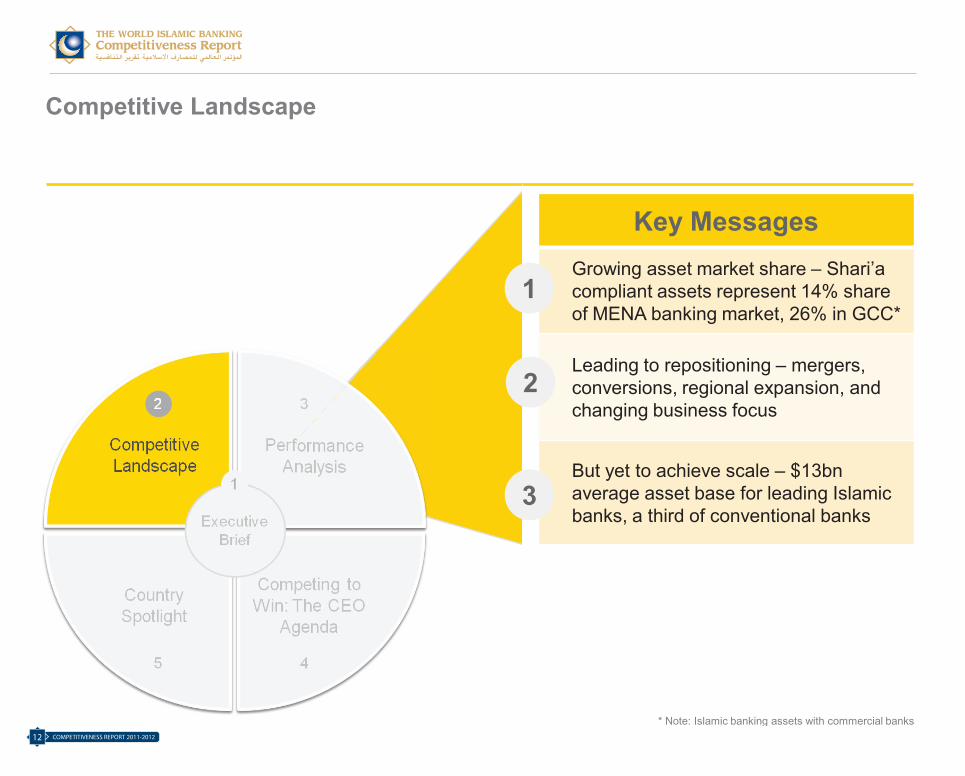

Key MessagesGrowing asset market share – Shari’a compliant assets represent 14% share of MENA banking market, 26% in GCC*

Leading to repositioning – mergers, conversions, regional expansion, and changing business focus

But yet to achieve scale – $13bnaverage asset base for leading Islamic banks, a third of conventional banks

1

2

3

Competitive Landscape

Islamic Banking Competitiveness Report 2011-12

Page 12

* Note: Islamic banking assets with commercial banks

Growth within the Muslim population throughout the emerging markets of MENA and Asia are key drivers behind increasing demand for Islamic financial services…

Source: Pew Research Center, Guardian, EY analysis

100m +

50 - 100m

10 – 50m

5 – 10m

1 – 5m

Muslim Population Density Indicator India

177mIndonesia

204m

Pakistan178m

Bangladesh148m

Turkey74m

Egypt80m

Nigeria75m

Algeria34m

Morocco32m

Iran74m

Global Estimated Muslim Populations – Selective Markets (2010)

Under 1m

China23m

Malaysia17m

Islamic Banking Competitiveness Report 2011-12

Page 13

COMPETITIVENESS REPORT 2011-201212

Growth within the Muslim population throughout the emerging markets of MENA and Asia are key drivers behind increasing demand for Islamic financial services…

Source: Pew Research Center, Guardian, EY analysis

100m +

50 - 100m

10 – 50m

5 – 10m

1 – 5m

Muslim Population Density Indicator India

177mIndonesia

204m

Pakistan178m

Bangladesh148m

Turkey74m

Egypt80m

Nigeria75m

Algeria34m

Morocco32m

Iran74m

Global Estimated Muslim Populations – Selective Markets (2010)

Under 1m

China23m

Malaysia17m

Islamic Banking Competitiveness Report 2011-12

Page 13

13COMPETITIVENESS REPORT 2011-2012

The MENA region boasts macroeconomic synergies that bode well for future GDP growth

Source: Global Insight, EY analysis (includes Turkey; excludes Palestine due to lack of data)

Key Features► Total Population 374m (2010)► CAGR Population Growth 2.1% (2007-2010) (EU = 0.4%)► 61% and 45% of world oil and gas reserves respectively ► Nominal GDP US$2.6tn► GDP CAGR 6.3% (2007-2010) (EU = 4.3%)

Hydrocarbon Reserves Population Centers

The GCC, Iraq, Algeria, Libya all have large hydrocarbon reserves and accumulated wealth

Turkey, Egypt, Saudi Arabia, Algeria and Morocco have large population centers and human capital reserves

Saudi Arabia Oman

UAE

Kuwait

Qatar

BahrainAlgeria LibyaEgypt

Turkey

Tunisia

MoroccoLebanon

Jordan

Iraq

Yemen

GCC

North Africa

The Levant

Syria

Islamic Banking Competitiveness Report 2011-12

Page 14

COMPETITIVENESS REPORT 2011-201214

Governments are utilising their hydrocarbon revenues to stimulate, develop and sustain economic activity within the region

MENA Nominal Hydrocarbon GDP (US$bn) Cost of Arab Spring (US$bn)

592

374

494

738682

2008 2009 2010 2011f 2012f

Source: Geopolicity, IIF

21

Cost to GDP Cost to Public

Finance

Total Cost

35 56

Overall growth expected to moderate in 2012, still significantly higher than

levels seen in 2009-10

Finance

Many governments have responded by (i) committing to new spending and (ii) accelerating planned large

infrastructure spending

Islamic Banking Competitiveness Report 2011-12

Page 15

15COMPETITIVENESS REPORT 2011-2012

0%

100%

200%

300%

400%

500%

600%

…but from a generally underpenetrated market position, the banking industry has considerable growth opportunities when compared to the more developed economies

Banking Asset / Nominal GDP (2010)

Average Penetration for Sample Countries1

Source: Central Bank Reports, Economist Intelligence Unit, Global Insight, EY analysis (average for EU)1 – Average Penetration for Sample Countries excludes US statistic to reduce skew.

MENA Rest of the world

1300%

Islamic Banking Competitiveness Report 2011-12

Page 16

Within MENA, the GCC markets are generally more developed with greater lending/financing assets to GDP penetration

Total Bank Lending/Financing and Penetration (2010)

Source: Central Bank Reports, Global Insight, EY analysis

273 262

92 85

28

15

268

59

37 26

6

78

43

31

11

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0

50

100

150

200

250

300

KSA UAE Kuwait Qatar Oman Bahrain Turkey Lebanon Jordan Syria Iraq Egypt Algeria Tunisia Libya

2008 2009 2010 Penetration

US$

bn

Islamic Banking Competitiveness Report 2011-12

Page 17

0%

100%

200%

300%

400%

500%

600%

…but from a generally underpenetrated market position, the banking industry has considerable growth opportunities when compared to the more developed economies

Banking Asset / Nominal GDP (2010)

Average Penetration for Sample Countries1

Source: Central Bank Reports, Economist Intelligence Unit, Global Insight, EY analysis (average for EU)1 – Average Penetration for Sample Countries excludes US statistic to reduce skew.

MENA Rest of the world

1300%

Islamic Banking Competitiveness Report 2011-12

Page 16

COMPETITIVENESS REPORT 2011-201216

Within MENA, the GCC markets are generally more developed with greater lending/financing assets to GDP penetration

Total Bank Lending/Financing and Penetration (2010)

Source: Central Bank Reports, Global Insight, EY analysis

273 262

92 85

28

15

268

59

37 26

6

78

43

31

11

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0

50

100

150

200

250

300

KSA UAE Kuwait Qatar Oman Bahrain Turkey Lebanon Jordan Syria Iraq Egypt Algeria Tunisia Libya

2008 2009 2010 Penetration

US$

bn

Islamic Banking Competitiveness Report 2011-12

Page 17

17COMPETITIVENESS REPORT 2011-2012

Shari’a compliant assets represent a significant portion of the total banking system assets of the region

Banking Assets (US$bn) and Islamic Share (%) in 2010

Total banking assets 2010 (US$bn) - the size of the circle denotes relative size

Total Islamic banking assets as a % of total assets

Saudi ArabiaOman

UAEQatar

BahrainAlgeria

LibyaEgypt

Turkey

Tunisia

MoroccoLebanon

JordanIraq

Yemen

Syria

Kuwait

17%

438

XX

X%

Key

30%

8 35%

3774%

215

2%

1%109

1%

5%

546

25%269

22%15627%46

31%155

56

117

12%

49

4%135

42

46

0%

0%

Source: Central Bank Reports, Press Releases, The Banker - Top 500 Islamic Financial Institutions, EY perspective (Note: Shari’a assets with commercial banks)

41

0%

GCC

North Africa

The Levant

Islamic Banking Competitiveness Report 2011-12

Page 18

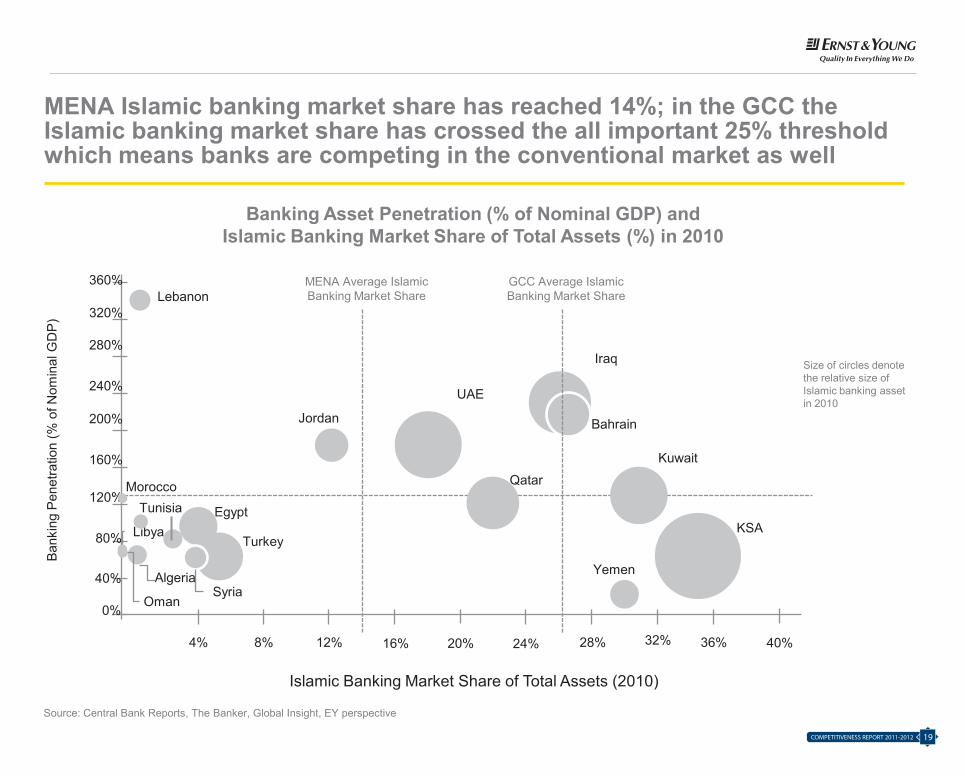

MENA Islamic banking market share has reached 14%; in the GCC the Islamic banking market share has crossed the all important 25% threshold which means banks are competing in the conventional market as well

Size of circles denote the relative size of Islamic banking asset in 2010

Banking Asset Penetration (% of Nominal GDP) and Islamic Banking Market Share of Total Assets (%) in 2010

0%

80%

120%

160%

200%

240%

280%

320%

360% MENA Average Islamic Banking Market Share

Islamic Banking Market Share of Total Assets (2010)

Bank

ing

Pene

tratio

n (%

of N

omin

al G

DP)

40%

4% 8% 12% 20% 28% 36%32%24% 40%16%

UAE

KSA

Iraq

Qatar

Kuwait

Turkey

Bahrain

Egypt

Jordan

Yemen

Lebanon

Tunisia

AlgeriaSyria

Libya

Morocco

Oman

Source: Central Bank Reports, The Banker, Global Insight, EY perspective

GCC Average Islamic Banking Market Share

Islamic Banking Competitiveness Report 2011-12

Page 19

COMPETITIVENESS REPORT 2011-201218

Shari’a compliant assets represent a significant portion of the total banking system assets of the region

Banking Assets (US$bn) and Islamic Share (%) in 2010

Total banking assets 2010 (US$bn) - the size of the circle denotes relative size

Total Islamic banking assets as a % of total assets

Saudi ArabiaOman

UAEQatar

BahrainAlgeria

LibyaEgypt

Turkey

Tunisia

MoroccoLebanon

JordanIraq

Yemen

Syria

Kuwait

17%

438

XX

X%

Key

30%

8 35%

3774%

215

2%

1%109

1%

5%

546

25%269

22%15627%46

31%155

56

117

12%

49

4%135

42

46

0%

0%

Source: Central Bank Reports, Press Releases, The Banker - Top 500 Islamic Financial Institutions, EY perspective (Note: Shari’a assets with commercial banks)

41

0%

GCC

North Africa

The Levant

Islamic Banking Competitiveness Report 2011-12

Page 18

MENA Islamic banking market share has reached 14%; in the GCC the Islamic banking market share has crossed the all important 25% threshold which means banks are competing in the conventional market as well

Size of circles denote the relative size of Islamic banking asset in 2010

Banking Asset Penetration (% of Nominal GDP) and Islamic Banking Market Share of Total Assets (%) in 2010

0%

80%

120%

160%

200%

240%

280%

320%

360% MENA Average Islamic Banking Market Share

Islamic Banking Market Share of Total Assets (2010)

Bank

ing

Pene

tratio

n (%

of N

omin

al G

DP)

40%

4% 8% 12% 20% 28% 36%32%24% 40%16%

UAE

KSA

Iraq

Qatar

Kuwait

Turkey

Bahrain

Egypt

Jordan

Yemen

Lebanon

Tunisia

AlgeriaSyria

Libya

Morocco

Oman

Source: Central Bank Reports, The Banker, Global Insight, EY perspective

GCC Average Islamic Banking Market Share

Islamic Banking Competitiveness Report 2011-12

Page 19

19COMPETITIVENESS REPORT 2011-2012

Strong historical growth, driven by core Islamic segment; going forward expect change of play as Islamic banks begin to compete for mainstream customers who are open to Islamic or conventional banking

Source: Company Reports, EY analysis (sample includes selective Islamic and conventional banks based on asset size and published information)

19%

20%

16%

22%

39%

14%

13%

26%

7%

28%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Saudi Arabia

Kuwait

UAE

Bahrain

Qatar

Islamic Banks Conventional Banks

41%

235%

-38%

52%

40%

22%

26%

2008

2010

Asset CAGR (2006-2010)

Islamic Banking Market Share

Growth Relative to Conventional Banks

Islamic Banking Competitiveness Report 2011-12

Page 20

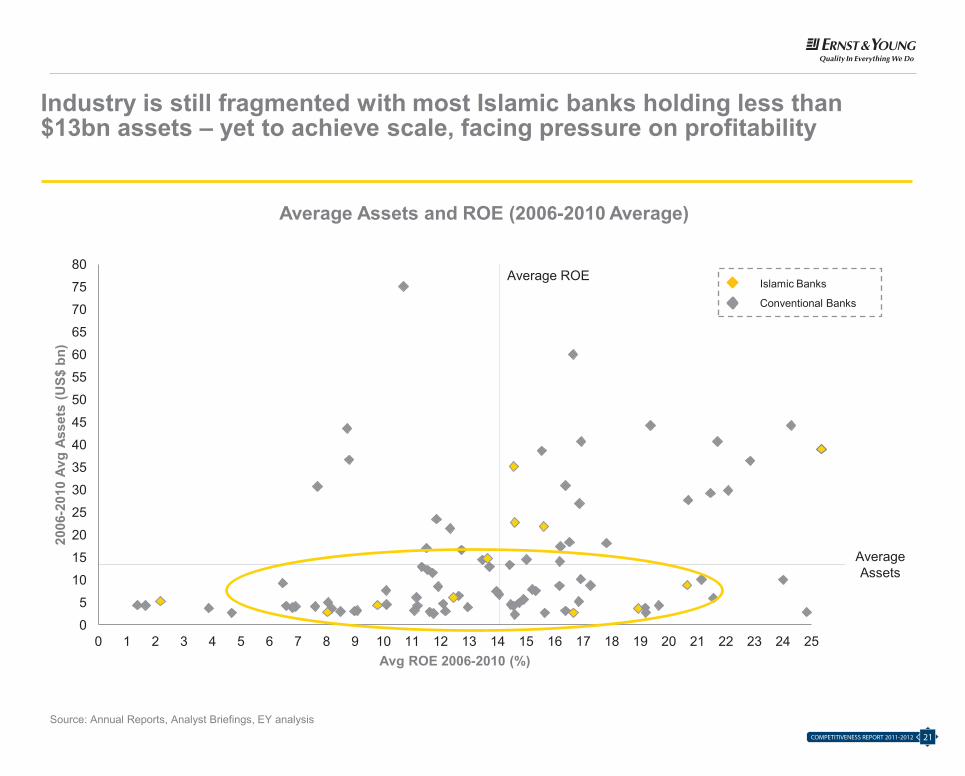

Industry is still fragmented with most Islamic banks holding less than $13bn assets – yet to achieve scale, facing pressure on profitability

Source: Annual Reports, Analyst Briefings, EY analysis

Average Assets and ROE (2006-2010 Average)

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

2006

-201

0 Av

g As

sets

(US$

bn)

Avg ROE 2006-2010 (%)

Average ROE

Average Assets

Islamic Banks

Conventional Banks

Islamic Banking Competitiveness Report 2011-12

Page 21

COMPETITIVENESS REPORT 2011-201220

Industry is still fragmented with most Islamic banks holding less than $13bn assets – yet to achieve scale, facing pressure on profitability

Source: Annual Reports, Analyst Briefings, EY analysis

Average Assets and ROE (2006-2010 Average)

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

2006

-201

0 Av

g As

sets

(US$

bn)

Avg ROE 2006-2010 (%)

Average ROE

Average Assets

Islamic Banks

Conventional Banks

Islamic Banking Competitiveness Report 2011-12

Page 21

21COMPETITIVENESS REPORT 2011-2012

The largest Islamic banks within the region are all leaders in their respective home markets and have expanded internationally to some degree

Source: Annual Reports, The Banker, EY analysis (where data was not available, calculation based on a 2 year average)

Shari’a Compliant Assets and ROA (2008-2010 Average)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0% 0.5% 1% 1.5% 2% 2.5% 3% 3.5% 4% 4.5% 5%

Regional Full Fledged Islamic Bank

Regional with Islamic Operation

Global with Islamic Window

Assets US$m

Saudi Retail Banking Leader

Saudi Islamic Windows

Qatari Islamic Banks

UAE Market Leader

UAE Islamic Banks

Islamic Banking Competitiveness Report 2011-12

Page 22

Kuwait Market Leader

COMPETITIVENESS REPORT 2011-201222

The largest Islamic banks within the region are all leaders in their respective home markets and have expanded internationally to some degree

Source: Annual Reports, The Banker, EY analysis (where data was not available, calculation based on a 2 year average)

Shari’a Compliant Assets and ROA (2008-2010 Average)

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0% 0.5% 1% 1.5% 2% 2.5% 3% 3.5% 4% 4.5% 5%

Regional Full Fledged Islamic Bank

Regional with Islamic Operation

Global with Islamic Window

Assets US$m

Saudi Retail Banking Leader

Saudi Islamic Windows

Qatari Islamic Banks

UAE Market Leader

UAE Islamic Banks

Islamic Banking Competitiveness Report 2011-12

Page 22

Kuwait Market Leader

Bank financing activity appears to be picking up, regulatory requirements may induce banks to raise higher-cost investment/ time deposits

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

GCC Banks – Growth in Advances

22%

15%

35%

1%0%

5%

10%

15%

20%

25%

30%

35%

40%

2007 2008 2009 2010

GCC Banks - Net Financing / Deposits

108%

94%

87%

92%

70%

75%

80%

85%

90%

95%

100%

105%

110%

2006 2007 2008 2009 2010

Islamic Banking Competitiveness Report 2011-12

Page 23

23COMPETITIVENESS REPORT 2011-2012

However, real estate concentration remains a concern for Islamic banks, may affect future growth

Conventional BanksIslamic Banks

Banks and FIs

Real Estate

Commercial

Others

35% 32%36%

33%

25%25%

20%

25%24%

11%18% 15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010

Source: Company Reports, Zawya, EY analysis (sample based on selective Islamic and conventional banks) (rounded numbers)

39% 41% 40%

33% 32% 33%

12%16% 16%

16%11% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010

Islamic Banking Competitiveness Report 2011-12

Page 24

COMPETITIVENESS REPORT 2011-201224

Business repositioning - (M&A, conversions, changing business focus) appear to dominate MENA Islamic banking going into 2012

Bahrain Islamic and Al Salam Bank announce they are exploring merger

Goldman Sachs registers a $2bn Islamic bond programme with the Irish Stock Exchange

Global sukuk issuance surge to $63bn YTD, GCC a primary contributor after Malaysia

Qatar Central Bank announces Islamic banking windows to be prohibited by year end

$500m sukuk issue by HSBC Middle East

Merger - Al Baraka and Emirates Global announce merger - $582m asset base, 89 branches, 40 cities (Pakistan)

International Bank of Qatar announces the sale of its Islamic banking business to Barwa Bank

DECOCTMAYFEBNOVJULY2010 AUG

Source: The Banker, IFN, Maris Strategies, Analyst Briefing

2011

ENBD acquires Dubai Bank

Conversion of AmrahBank to Islamic

Royal Decree passed to allow Islamic finance industry to commence in Oman. First banking license granted in Q2

Formation of WarbaBank in Kuwait

Several countries across Africa announce plans to introduce Islamic banking; amend regulatory and legislative regimes

Islamic Banking Competitiveness Report 2011-12

Page 25

25COMPETITIVENESS REPORT 2011-2012

Report Structure

Performance Analysis

Competitive Landscape

Competing to Win: The CEO

Agenda

Country Spotlight

Executive Brief

1

2 3

5 4

Islamic Banking Competitiveness Report 2011-12

Page 26

COMPETITIVENESS REPORT 2011-201226

Key MessagesPainful decline in profitability – industry ROE now appears to be stabilizing around the 10% range (2006: 23%)

Structural advantage – better financing margins, higher deposit growth and higher proportion of free deposits

Operating model questioned –misaligned people-processes-systems, leading to high cost to income ratio

1

2

3

Performance Analysis

Islamic Banking Competitiveness Report 2011-12

Page 27

27COMPETITIVENESS REPORT 2011-2012

ROE decomposition assists in understanding the key performance indicators of banks

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expenses

Provisions

X

Islamic Banking Competitiveness Report 2011-12

Page 28

COMPETITIVENESS REPORT 2011-201228

Islamic banks have experienced a more painful decline in profitability over recent years but this now appears to be stabilizing

Bahrain Kuwait

Qatar Saudi Arabia

United Arab Emirates

Net Income / Equity

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

23%

10%

13%

0%

5%

10%

15%

20%

25%

30%

35%

40%

2006 2007 2008 2009 2010

11%-1%

13%

9%

-20%

0%

20%

40%

2006 2007 2008 2009 2010

19%

5%

27%

12%

-20%

0%

20%

40%

2006 2007 2008 2009 2010

16% 15%

22%20%

-20%

0%

20%

40%

2006 2007 2008 2009 2010

35%

13%

29%14%

-20%

0%

20%

40%

2006 2007 2008 2009 2010

17%

8%

10%

-20%

0%

20%

40%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 29

29COMPETITIVENESS REPORT 2011-2012

2.8%

0.6%1.8%

2.2%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

Islamic banks are able to generate higher financing margins also because of their relatively stronger retail focus

Bahrain Kuwait

Qatar Saudi Arabia

United Arab Emirates

Islamic Banks Conventional Banks

Net Financing Income / Financing Assets

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

4.3%

3.7%

3.0%

2.8%

3.2%

2%

3%

4%

5%

2006 2007 2008 2009 2010

3.5%3.3%3.1%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

2.7%2.2%

3.8%

2.3%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

7.1%

4.9%3.7% 3.0%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

2.2%

3.3%2.3%

2.7%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

IB’s excluding KSA

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 30

COMPETITIVENESS REPORT 2011-201230

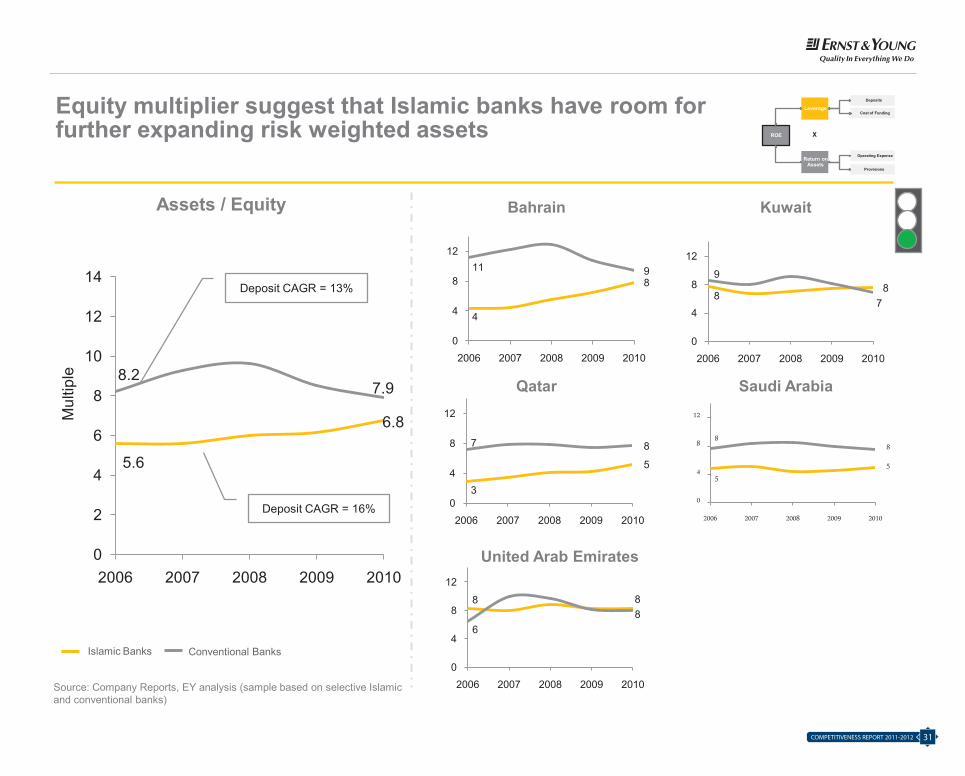

Equity multiplier suggest that Islamic banks have room for further expanding risk weighted assets

Bahrain Kuwait

Qatar Saudi Arabia

United Arab Emirates

Assets / Equity

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

5.6

6.8

8.27.9

0

2

4

6

8

10

12

14

2006 2007 2008 2009 2010

Deposit CAGR = 13%

Deposit CAGR = 16%

4

811 9

0

4

8

12

2006 2007 2008 2009 2010

88

9

7

0

4

8

12

2006 2007 2008 2009 2010

3

5

7 8

0

4

8

12

2006 2007 2008 2009 2010

5

5

88

0

4

8

12

2006 2007 2008 2009 2010

8 8

68

0

4

8

12

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Mul

tiple

Islamic Banking Competitiveness Report 2011-12

Page 31

31COMPETITIVENESS REPORT 2011-2012

Islamic banks benefit from a higher proportion of free customer deposits but there is a tendency that these are of a short term tenure

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banks Conventional Banks

Other

Investment/ Time Deposit

Saving

Current

21%

47%

29%

2.6%

0.1%

2.6%

69.7%

47.7%

65.6%

6.8% 4.9% 3.0%

UAE KSA Qatar

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

2008-2010 Average

23%

78%

45.5%15%

5%

21.7%62%

17% 10.2%

UAE KSA Qatar

Islamic Banking Competitiveness Report 2011-12

Page 32

COMPETITIVENESS REPORT 2011-201232

5.5%

3.0%3.0%

2.6%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

2.6%

-0.2%1.1%

0.9%

-2%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

After a painful decline in profitability through the financial crisis the ROA appears to be stabilizing, but now lower than conventional banks

Bahrain Kuwait

Qatar Saudi Arabia

United Arab Emirates

Net income / Assets

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

4.0%

1.5%

3.0%

1.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

2006 2007 2008 2009 2010

2.1%1.0%

2.6%1.2%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

7.2%

2.6%3.8%

1.8%0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

2.5%0.7%

3.1%1.7%

0%

2%

4%

6%

8%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 33

33COMPETITIVENESS REPORT 2011-2012

Higher provisions and operating costs have contributed to the steep decline in profitability of Islamic banks

ROA 3.2% 1.6% 1.5% 1.8% 1.6% 1.6%

Source: Company Reports, EY analysis (numbers rounded off)

Provisions

Operating Expenses

Other Income

Net Financing Income

Islamic Banks Conventional Banks

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

3.2% 3.4% 2.9%

2.5%1.5%

1.3%

-2.0% -2.0% -1.8%

-0.4%-1.4%

-1.0%

-4%

-2%

0%

2%

4%

6%

2006-2008 average

2009 2010

1.9% 2.1% 2.0%

1.1%1.1% 1.1%

-1.0% -1.0% -0.9%

-0.2%-0.6% -0.5%

-2%

-1%

0%

1%

2%

3%

4%

2006-2008 average

2009 2010

Provisions and operating expenses higher than conventional

Islamic Banking Competitiveness Report 2011-12

Page 34

COMPETITIVENESS REPORT 2011-201234

Higher provisions and operating costs have contributed to the steep decline in profitability of Islamic banks

ROA 3.2% 1.6% 1.5% 1.8% 1.6% 1.6%

Source: Company Reports, EY analysis (numbers rounded off)

Provisions

Operating Expenses

Other Income

Net Financing Income

Islamic Banks Conventional Banks

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

3.2% 3.4% 2.9%

2.5%1.5%

1.3%

-2.0% -2.0% -1.8%

-0.4%-1.4%

-1.0%

-4%

-2%

0%

2%

4%

6%

2006-2008 average

2009 2010

1.9% 2.1% 2.0%

1.1%1.1% 1.1%

-1.0% -1.0% -0.9%

-0.2%-0.6% -0.5%

-2%

-1%

0%

1%

2%

3%

4%

2006-2008 average

2009 2010

Provisions and operating expenses higher than conventional

Islamic Banking Competitiveness Report 2011-12

Page 34

Higher cost to income ratio is a combined result of modest core banking revenues and a higher cost base due to misaligned processes and systems

Operating Cost / Operating Income

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

26%

40%

29% 35%

0%

20%

40%

60%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 35

35COMPETITIVENESS REPORT 2011-2012

Performance culture – higher staff cost should translate into better performance but Islamic banks lag behind their conventional peers

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

58%

60%

57%

54%

51%

52%

53%

54%

55%

56%

57%

58%

59%

60%

2009 2010

3% 3%

0.9% 0.8%

0%

1%

1%

2%

2%

3%

3%

4%

2009 2010

Staff Cost / Operating Expenses Staff Cost / Deposits

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banks Conventional Banks

Islamic Banking Competitiveness Report 2011-12

Page 36

COMPETITIVENESS REPORT 2011-201236

2.0%1.5%

1.3%

2.2%

0%

2%

4%

6%

2006 2007 2008 2009 2010

2.1%

3.8%

1.3%1.4%

0%

2%

4%

6%

2006 2007 2008 2009 2010

Operating costs are impacting Islamic banks across the region – operating models need to be made scalable

Bahrain Kuwait

Qatar Saudi Arabia

United Arab Emirates

Operating Cost / Asset

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

2.2%2.1%

1.3% 1.5%

0%

1%

2%

3%

4%

5%

6%

2006 2007 2008 2009 2010

2.2% 2.1%

1.3%1.5%

0%

2%

4%

6%

2006 2007 2008 2009 2010

3.1%2.4%

1.6% 1.4%0%

2%

4%

6%

2006 2007 2008 2009 2010

1.6%1.6%

0.9%1.0%

0%

2%

4%

6%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 37

37COMPETITIVENESS REPORT 2011-2012

2%

18%

5% 16%

-10%

10%

30%

50%

2006 2007 2008 2009 2010

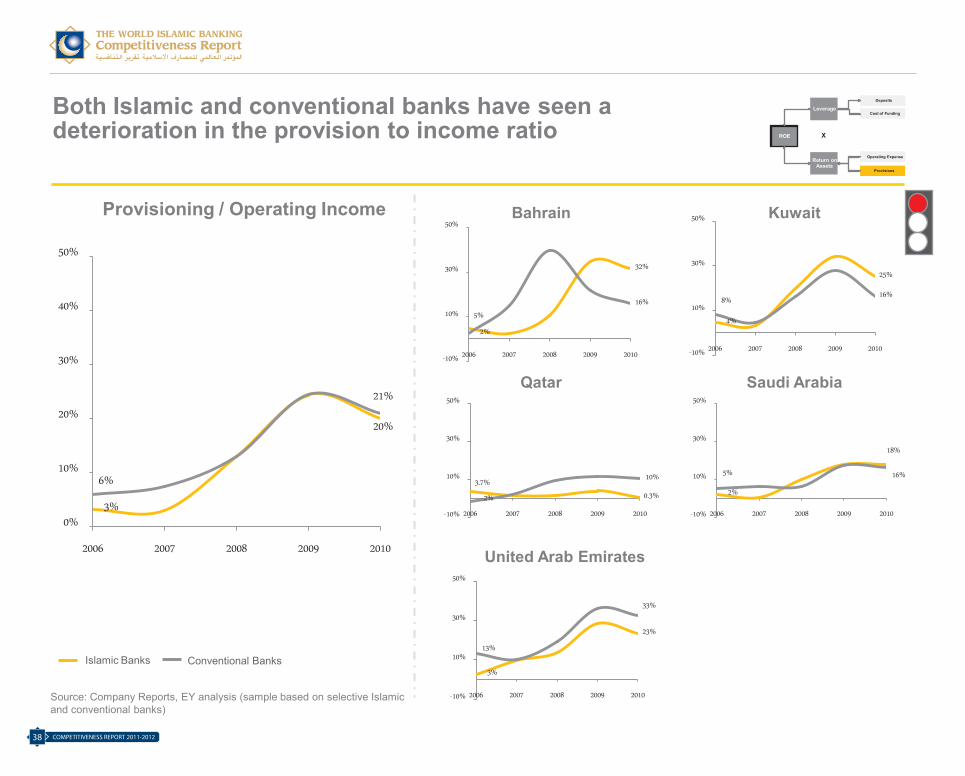

Both Islamic and conventional banks have seen a deterioration in the provision to income ratio

Bahrain Kuwait

Qatar Saudi Arabia

United Arab Emirates

Provisioning / Operating Income

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

3%

20%

6%

21%

0%

10%

20%

30%

40%

50%

2006 2007 2008 2009 2010

5%

32%

2%

16%

-10%

10%

30%

50%

2006 2007 2008 2009 2010

4%

25%

8%16%

-10%

10%

30%

50%

2006 2007 2008 2009 2010

3.7%

0.3%-2%

10%

-10%

10%

30%

50%

2006 2007 2008 2009 2010

3%

23%

13%

33%

-10%

10%

30%

50%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 38

COMPETITIVENESS REPORT 2011-201238

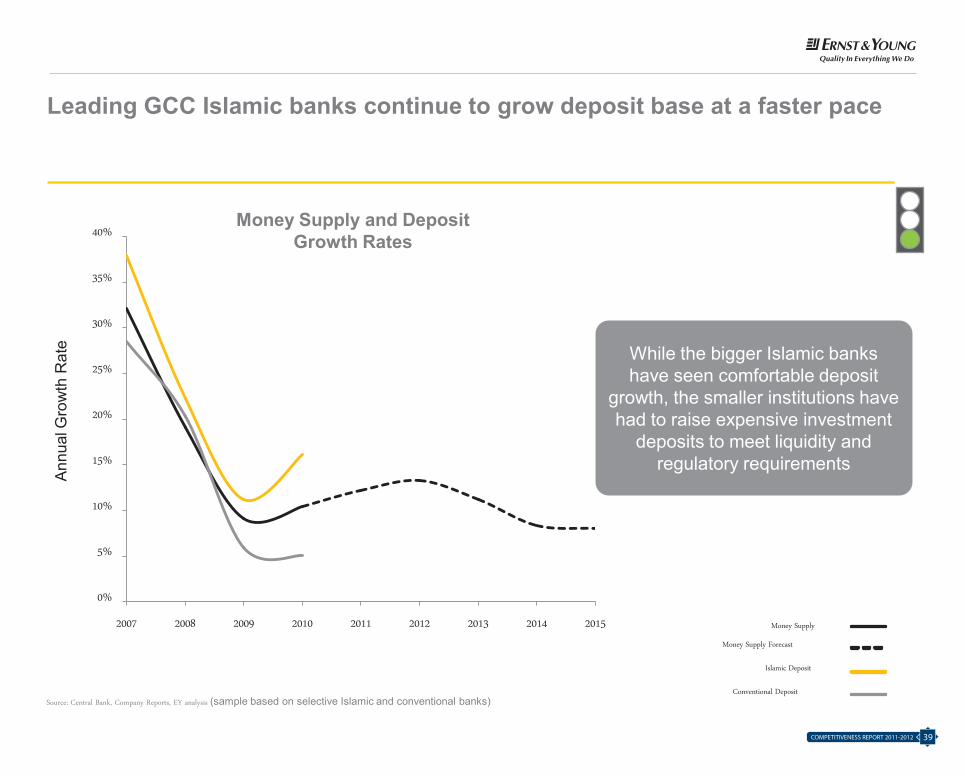

Leading GCC Islamic banks continue to grow deposit base at a faster pace

Money Supply

Islamic Deposit

Conventional Deposit

Money Supply Forecast

0%

5%

10%

15%

20%

25%

30%

35%

40%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Central Bank, Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Money Supply and Deposit Growth Rates

Ann

ual G

row

th R

ate While the bigger Islamic banks

have seen comfortable deposit growth, the smaller institutions have had to raise expensive investment

deposits to meet liquidity and regulatory requirements

Islamic Banking Competitiveness Report 2011-12

Page 39

39COMPETITIVENESS REPORT 2011-2012

Average cost of customer funds is lower for Islamic banks, primarily due to high share of free deposits in the deposit mix

Average Return on Investment Account Holders Funds/ Deposits

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

3.0%

1.3%

3.8%

1.8%

5.0%

0.4%0%

1%

2%

3%

4%

5%

6%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks), US$ LIBOR: global-rates.com

6 months US$ LIBOR (average)

However, cost of return-bearing customer deposits has been increasing relatively faster for a number of Islamic banks, compared to their conventional peers

Islamic Banking Competitiveness Report 2011-12

Page 40

COMPETITIVENESS REPORT 2011-201240

Average cost of customer funds is lower for Islamic banks, primarily due to high share of free deposits in the deposit mix

Average Return on Investment Account Holders Funds/ Deposits

ROE

Leverage

Return on Assets

Deposits

Cost of Funding

Operating Expense

Provisions

X

3.0%

1.3%

3.8%

1.8%

5.0%

0.4%0%

1%

2%

3%

4%

5%

6%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks), US$ LIBOR: global-rates.com

6 months US$ LIBOR (average)

However, cost of return-bearing customer deposits has been increasing relatively faster for a number of Islamic banks, compared to their conventional peers

Islamic Banking Competitiveness Report 2011-12

Page 40

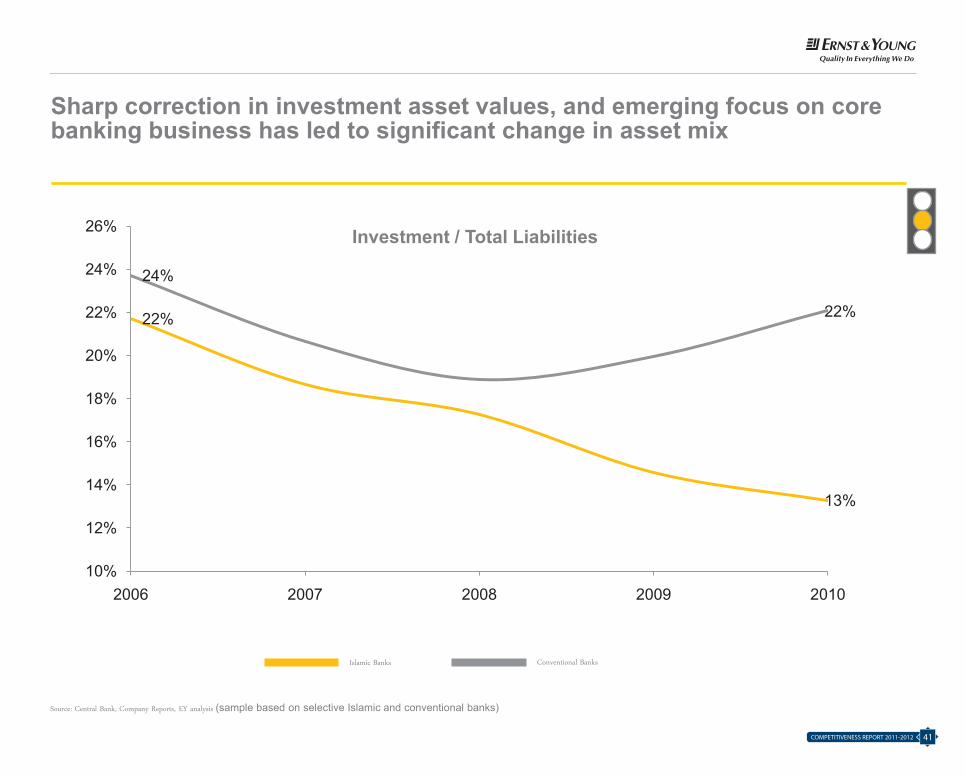

Sharp correction in investment asset values, and emerging focus on core banking business has led to significant change in asset mix

Source: Central Bank, Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banks Conventional Banks

22%

13%

24%

22%

10%

12%

14%

16%

18%

20%

22%

24%

26%

2006 2007 2008 2009 2010

Investment / Total Liabilities

Islamic Banking Competitiveness Report 2011-12

Page 41

41COMPETITIVENESS REPORT 2011-2012

Islamic banks continue to hold more liquid assets than conventional banks in most markets across the region...

Saudi Arabia

United Arab Emirates

Kuwait

Qatar

BahrainCash & Cash Equivalents / Total Liabilities

7%

16%

10%14%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010

18%

19%

15% 14%

0%

5%

10%

15%

20%

25%

2006 2007 2008 2009 2010

17%

21%

8%0%

10%

20%

30%

2006 2007 2008 2009 2010

18%

12%12%

15%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010

16%16%

14%

13%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010

33% 29%

18%22%

0%

10%

20%

30%

40%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 42

COMPETITIVENESS REPORT 2011-201242

Islamic banks continue to hold more liquid assets than conventional banks in most markets across the region...

Saudi Arabia

United Arab Emirates

Kuwait

Qatar

BahrainCash & Cash Equivalents / Total Liabilities

7%

16%

10%14%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010

18%

19%

15% 14%

0%

5%

10%

15%

20%

25%

2006 2007 2008 2009 2010

17%

21%

8%0%

10%

20%

30%

2006 2007 2008 2009 2010

18%

12%12%

15%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010

16%16%

14%

13%

0%

5%

10%

15%

20%

2006 2007 2008 2009 2010

33% 29%

18%22%

0%

10%

20%

30%

40%

2006 2007 2008 2009 2010

Islamic Banks Conventional Banks

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 42

Islamic Banks Conventional Banks

... but as noted earlier, Islamic banks have limited long term liabilities

Long Term Liabilities

Short term Liabilities

Equity

Deposits

59%63% 66% 68% 69%

27% 22% 18% 17% 15%

13% 14% 14% 14% 14%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010

66% 62% 63% 63% 64%

13%12% 12% 13% 14%

16%20% 23% 19% 17%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 2007 2008 2009 2010

Source: Central Bank, Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

As % of Total Liabilities & Equity

1% 1% 2% 1% 2% 5% 6% 2% 5% 5%

Islamic Banking Competitiveness Report 2011-12

Page 43

43COMPETITIVENESS REPORT 2011-2012

Both Islamic and conventional banks have a negative liquidity gap for short term maturity band

-44%

72%

-36%

55%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Less than one year Over 1 year

Net Liquidity Gap / Total Asset (selected maturity band)

Islamic Banks Conventional Banks

Source: Central Bank, Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 44

COMPETITIVENESS REPORT 2011-201244

Both Islamic and conventional banks have a negative liquidity gap for short term maturity band

-44%

72%

-36%

55%

-60%

-40%

-20%

0%

20%

40%

60%

80%

Less than one year Over 1 year

Net Liquidity Gap / Total Asset (selected maturity band)

Islamic Banks Conventional Banks

Source: Central Bank, Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 44

Report Structure

Performance Analysis

Competitive Landscape

Competing to Win: The CEO

Agenda

Country Spotlight

Executive Brief

1

2 3

5 4

Islamic Banking Competitiveness Report 2011-12

Page 45

45COMPETITIVENESS REPORT 2011-2012

Key MessagesRebuild to last – operating model to be transformed for quality growth and to create sustainable shareholder value

Service driven culture – investing more in customer centric activities, with better use of technology and risk tools

Shari’a differentiation – acquire and build specialist product skills, ensure better integration with real economy

1

2

3

Competing to Win – The CEO Agenda

Islamic Banking Competitiveness Report 2011-12

Page 46

COMPETITIVENESS REPORT 2011-201246

Key MessagesRebuild to last – operating model to be transformed for quality growth and to create sustainable shareholder value

Service driven culture – investing more in customer centric activities, with better use of technology and risk tools

Shari’a differentiation – acquire and build specialist product skills, ensure better integration with real economy

1

2

3

Competing to Win – The CEO Agenda

Islamic Banking Competitiveness Report 2011-12

Page 46

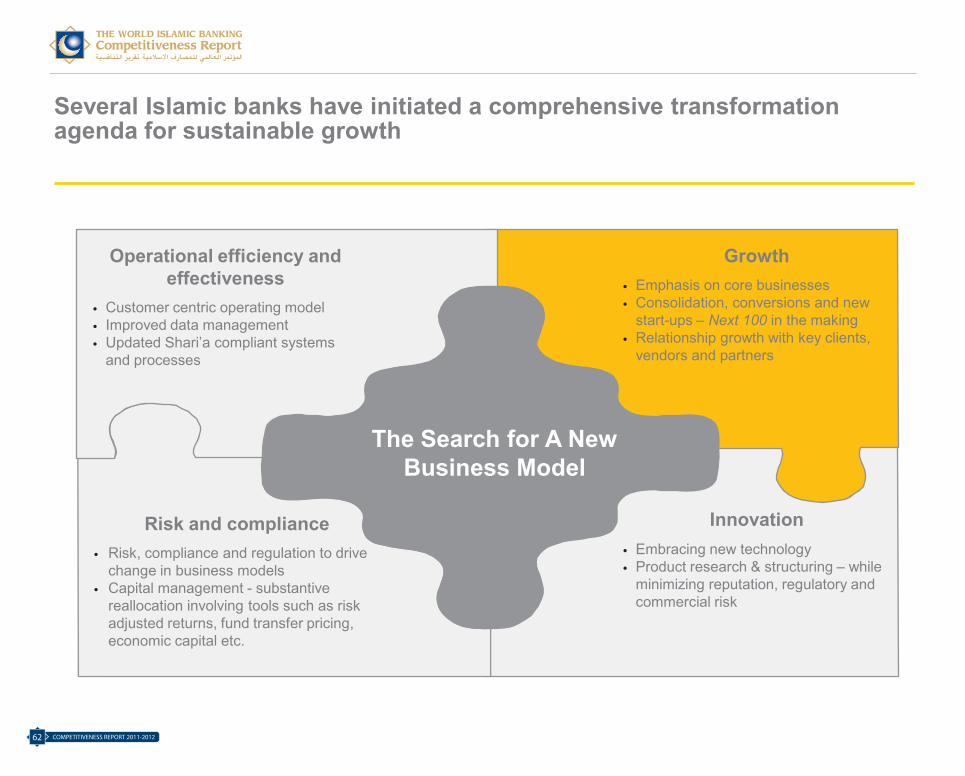

Several Islamic banks have initiated a comprehensive transformation agenda for sustainable growth

Risk and compliance • Risk, compliance and regulation to drive

change in business models• Capital management - substantive

reallocation involving tools such as risk adjusted returns, fund transfer pricing, economic capital etc.

The Search for A New Business Model

Operational efficiency and effectiveness

• Customer centric operating model• Improved data management • Updated Shari’a compliant systems

and processes

Innovation• Embracing new technology• Product research & structuring – while

minimizing reputation, regulatory and commercial risk

Growth• Emphasis on core businesses• Consolidation, conversions and new

start-ups – Next 100 in the making• Relationship growth with key clients,

vendors and partners

Islamic Banking Competitiveness Report 2011-12

Page 47

47COMPETITIVENESS REPORT 2011-2012

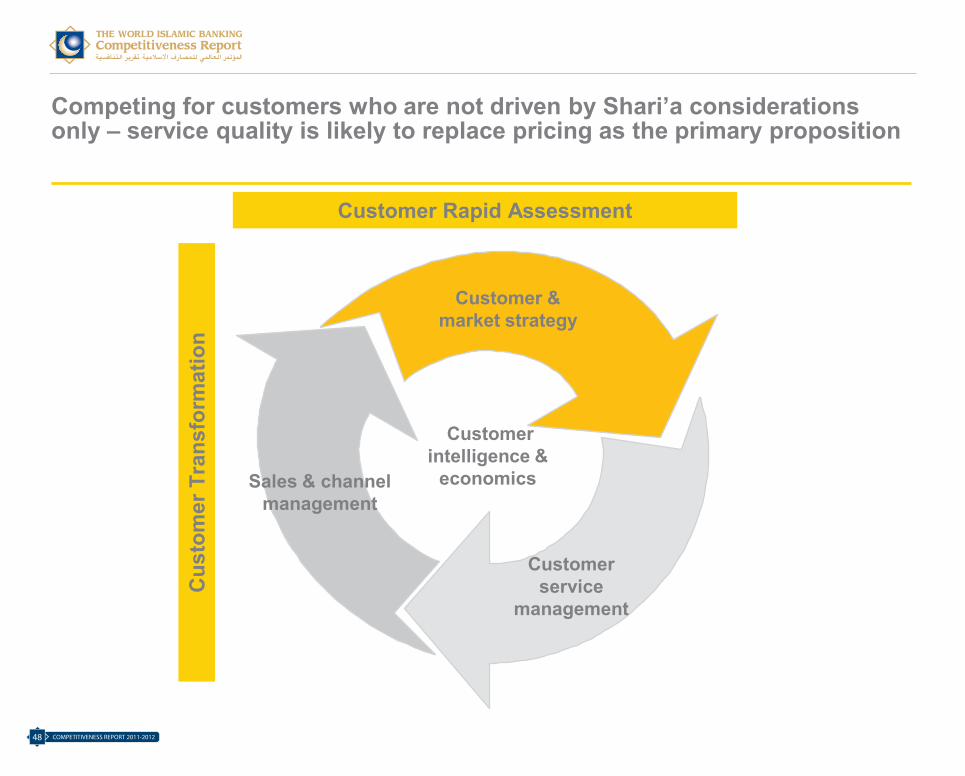

Competing for customers who are not driven by Shari’a considerations only – service quality is likely to replace pricing as the primary proposition

Sales & channel management

Customer & market strategy

Customer service

management

Customer intelligence &

economics

Customer Rapid AssessmentC

usto

mer

Tra

nsfo

rmat

ion

Islamic Banking Competitiveness Report 2011-12

Page 48

COMPETITIVENESS REPORT 2011-201248

Competing for customers who are not driven by Shari’a considerations only – service quality is likely to replace pricing as the primary proposition

Sales & channel management

Customer & market strategy

Customer service

management

Customer intelligence &

economics

Customer Rapid Assessment

Cus

tom

er T

rans

form

atio

n

Islamic Banking Competitiveness Report 2011-12

Page 48

New market strategy

►Understand the competitive landscape and assess customer trends

►Analysis of regulation, Shari’a, tax and legal requirements

Customer and market strategy (“the double compliant customer”)

Customer segmentation

►Specially designed tools to develop deep understanding of segment requirements

►Data analysis and modelling to develop logical segmentation models

Customer service improvement

►As-is and to-be analysis of customer experience to enhance customer engagement

►Develop the most important Customer moments of truth and develop service

Customer operating model review

►Development of organizational design and spans of control

►Shared service analysis

►Provide the linkage between employee, Shari’a & customer engagement

Customer service improvement

Bank’s need to review their customer and market strategies to help understand customer requirements and engagement tactics in the new competitive landscape

Islamic Banking Competitiveness Report 2011-12

Page 49

49COMPETITIVENESS REPORT 2011-2012

Single customer view

Customer analytics and economics

Single customer view

►Developing an analytical single customer view to drive marketing activity

►Developing an operational single customer view to drive service experience

Customer data architecture

►Assist in the selection and implementation of CRM technology

►Assist in designing a customer data database

Customer retention

►Customer profitability and lifetime value analysis

►Cross sales and incentive schemes to assist in both retention and customer value management

Customer economics

►Development of actionable plans for improving margin or optimizing cost

►Diagnosis of key improvement initiatives to help sustain revenues, & reduce costs whilst improving customer service

Note: CRM (Customer Relationship Management)

Customer analytics – banks can identify trends in customer behavior and spending to provide suitable products in line with the customers needs –successful rollout has delivered increases in retention and profitability

Islamic Banking Competitiveness Report 2011-12

Page 50

COMPETITIVENESS REPORT 2011-201250

Customer loyalty management

Sales and channel management

Customer loyalty management

►Assess customer data to determine position in the customer lifecycle

►Analysis of customer needs and internal practices to help match customer expectations with service

Sales force effectiveness

►Planning sales activities/ deploying resources to develop an effective sales strategy

►Overhauling the sales process including pipeline management, tender management, risk & regulation

Channel strategy

►Use of data models for channel optimisation and defining incentive compensation for channel advocacy

►Smooth transition of customers between channels, efficient complaints handling process and effective use of channels

Product development

►Developing a product strategy based on Shari’a contracts to assist in revenue growth

►Product mix optimisation, margin improvement, consumer promotional effectiveness and competitor positioning

Effective and compelling marketing tactics can increase the customer’s consideration to buy. The region is already saturated with loyalty schemes so another new one needs to be carefully thought through

Islamic Banking Competitiveness Report 2011-12

Page 51

51COMPETITIVENESS REPORT 2011-2012

Customer service management

Contact centre transformation

►Contact centre diagnostic and performance benchmarking

►Developing a detailed understanding of how contact centre fits into the overall service proposition

Service quality management

►Assess the impact of the move to self-service on the overall customer profitability

► Identify hot-spots and instigate process changes

Customer service effectiveness

►Assess service capabilities vs. competitors to identify gaps in the service proposition

►Map the high level processes and identify the key issues from a customer’s perspective

Service channel transformation

►Developing an integrated approach to servicing via multiple channels

►Determining the impact of service failures on customer experience

Contact centre transformation

Banks in the region often use costly incentives to attract customers but then spend little on service to retain them – this is unsustainable

Islamic Banking Competitiveness Report 2011-12

Page 52

COMPETITIVENESS REPORT 2011-201252

60%

30%

19%

11%

11%

8%

8%7%

5%

100%

Benefits

Typically three levers deliver the majority of the benefits

Structural Rationalisation

Process & Productivity

Improvement

Off shoring / Outsourcing

Business Portfolio

Rationalisation

Purchasing Compliance / Governance

Supplier Rationalisation

Demand Challenge

Infrastructure Rationalisation

& Efficiency

Total

In our experience, a customer-centric operating model which has processes built around the customer are the biggest drivers of benefits, as illustrated below

Islamic Banking Competitiveness Report 2011-12

Page 53

53COMPETITIVENESS REPORT 2011-2012

Several Islamic banks have initiated a comprehensive transformation agenda for sustainable growth

Risk and compliance • Risk, compliance and regulation to drive

change in business models• Capital management - substantive

reallocation involving tools such as risk adjusted returns, fund transfer pricing, economic capital etc.

The Search for A New Business Model

Operational efficiency and effectiveness

• Customer centric operating model• Improved data management • Updated Shari’a compliant systems

and processes

Innovation• Embracing new technology• Product research & structuring – while

minimizing reputation, regulatory and commercial risk

Growth• Emphasis on core businesses• Consolidation, conversions and new

start-ups – Next 100 in the making• Relationship growth with key clients,

vendors and partners

Islamic Banking Competitiveness Report 2011-12

Page 54

Reduced profits and valuations are amongst the biggest business risks facing Islamic banks

Top Risks for Islamic BanksManaging the transformation, to customer

centric business model

Reduced profits and valuations

Geopolitical, macroeconomic shocks

Human capital, including misaligned compensation structures

Product risk, balancing innovation, law of the land and Shari’a compliance

Technology risk, including absence of fully compliant/ certified systems

Liquidity and associated cost

Financial Compliance

Strategic Operational

5

Technology risk, incl. absence of fully compliant/ certified systems

Liquidity and cost

3

2

1

7

6

4

Product risk, balancing innovation, law of the land

and Shari’a compliance

Human capital, including misaligned compensation

structures

Reduced profits and valuations

Managing the transformation, to customer

centric business model

Geopolitical, macroeconomic shocks

Islamic Banking Competitiveness Report 2011-12

Page 55

COMPETITIVENESS REPORT 2011-201254

Reduced profits and valuations are amongst the biggest business risks facing Islamic banks

Top Risks for Islamic BanksManaging the transformation, to customer

centric business model

Reduced profits and valuations

Geopolitical, macroeconomic shocks

Human capital, including misaligned compensation structures

Product risk, balancing innovation, law of the land and Shari’a compliance

Technology risk, including absence of fully compliant/ certified systems

Liquidity and associated cost

Financial Compliance

Strategic Operational

5

Technology risk, incl. absence of fully compliant/ certified systems

Liquidity and cost

3

2

1

7

6

4

Product risk, balancing innovation, law of the land

and Shari’a compliance

Human capital, including misaligned compensation

structures

Reduced profits and valuations

Managing the transformation, to customer

centric business model

Geopolitical, macroeconomic shocks

Islamic Banking Competitiveness Report 2011-12

Page 55

55COMPETITIVENESS REPORT 2011-2012

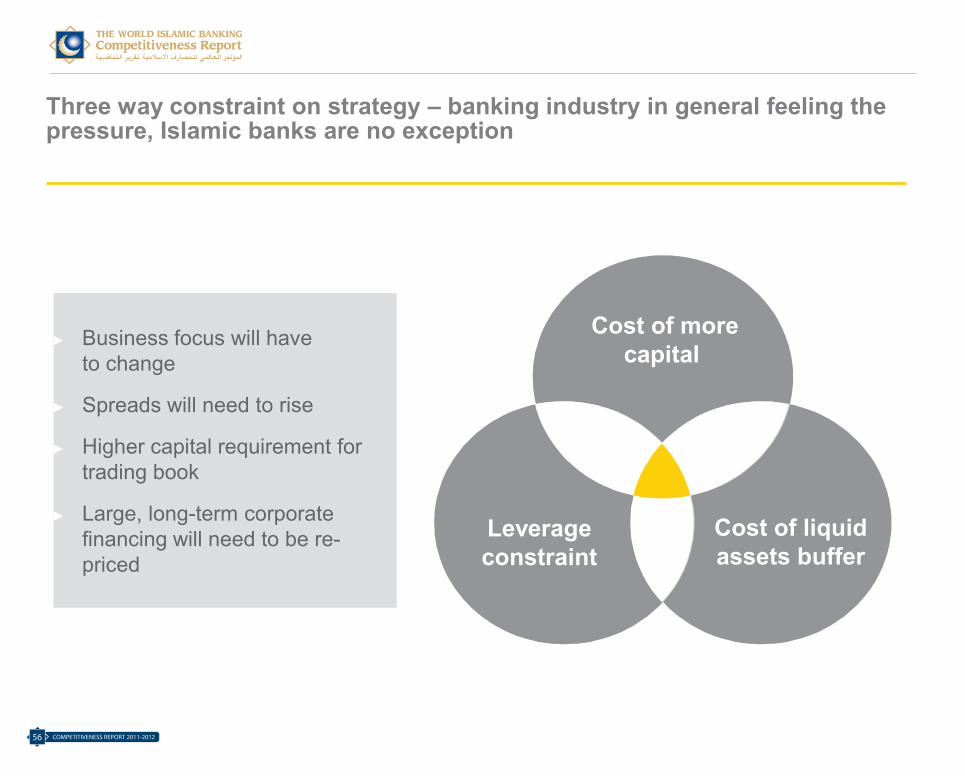

Three way constraint on strategy – banking industry in general feeling the pressure, Islamic banks are no exception

Cost of more capital

Cost of liquid assets buffer

Leverageconstraint

► Business focus will have to change

► Spreads will need to rise

► Higher capital requirement for trading book

► Large, long-term corporate financing will need to be re-priced

Islamic Banking Competitiveness Report 2011-12

Page 56

COMPETITIVENESS REPORT 2011-201256

Three way constraint on strategy – banking industry in general feeling the pressure, Islamic banks are no exception

Cost of more capital

Cost of liquid assets buffer

Leverageconstraint

► Business focus will have to change

► Spreads will need to rise

► Higher capital requirement for trading book

► Large, long-term corporate financing will need to be re-priced

Islamic Banking Competitiveness Report 2011-12

Page 56

Liquidity – challenges and needed improvements

Systems Process

Governance

Product innovation (e.g. credible, compliant

alternatives to Commodity Murabaha)

Contingent commitments

Funds transfer pricing

Enhanced analytic

capability

Collateral tracking systems

Better consolidated/ group wide

data

New data hubs needed

Islamic Banking Competitiveness Report 2011-12

Page 57

57COMPETITIVENESS REPORT 2011-2012

As with conventional institutions, Islamic banks will find it challenging to return to pre 2007 profitability levels – question is how big will the cuts be?

Pre-crisis, 15 - 25%

Estimates of cut pre-mitigating actions –reduction around 5-9 percentage points

Components of the reduction

Capital quality 0.8 Capital increase 1.3Leverage ratio 0.1Liquid assets 0.6

Strategic issue for the banks – how much disclosure is needed to convince equity investors they are safer

Rate of return on

equity

ILLUSTRATION ONLY

Islamic Banking Competitiveness Report 2011-12

Page 58

COMPETITIVENESS REPORT 2011-201258

As with conventional institutions, Islamic banks will find it challenging to return to pre 2007 profitability levels – question is how big will the cuts be?

Pre-crisis, 15 - 25%

Estimates of cut pre-mitigating actions –reduction around 5-9 percentage points

Components of the reduction

Capital quality 0.8 Capital increase 1.3Leverage ratio 0.1Liquid assets 0.6

Strategic issue for the banks – how much disclosure is needed to convince equity investors they are safer

Rate of return on

equity

ILLUSTRATION ONLY

Islamic Banking Competitiveness Report 2011-12

Page 58

It is now even more important to link remuneration code with institutions’ performance, and to retain scarce talent

Key challenges

► Talent retention► Corporate culture► Shares vs. cash/ deferrals► Data availability and quality

Current practices► Reviewing new rules and

guidance on remuneration► Revising compensation

policies, processes and systems

► Update balanced scorecards and new incentive plans

Remuneration Committee – Bank wide remuneration policy (NEDs + External Advisors)

Oversight of reward protocols + Reward framework

Bonus decision (form and amount)

“Golden handshakes” “parachute” payments

Payout decision (timing and amount)

► Human capital

► Risk► Tax

CRO

Board level executives Line Mgmnt/

HR Risk

“High end” employees

Individuals with significant influence on direction and risk profile

All other employees

Assessment

► Human capital

► Risk► Tax

Balanced Score Card

Salary

Short term incentive plans

Long term incentive plans

► Human capital

► Risk► Tax

People

Quality

Customer

Risk

Performance measurement framework

Salary / Bonus

Short term incentive plans

Long term incentive plans

Islamic Banking Competitiveness Report 2011-12

Page 59

59COMPETITIVENESS REPORT 2011-2012

MI framework with risk adjusted performance tools will be central to directing quality growth

ValueDrivers

PerformanceMeasures

OperatingMeasures Action Plans

Business Strategy

ImproveEconomic Profit

Finance Income

Operating

Bad & Doubtful Debts

Cost of Risk Capital

Income per Account

Volume

Write -Offs

Recovery Revenue

Hurdle Rate

Risk Capital

Bad Debt Provision

Credit Risk Capital

Operational Risk Capital

Other Risks

Risk free rate

Beta

Market premium

Sales (# of New Accounts)

Number of Existing Account

Number of Closed Account

Net Profit Incomeper Account

Cost of Funding

Cure Rate

Value of Delinquency

Provision Estimate Probability of Default

Loss Given Default

Exposure at Default

Portfolio Diversification

# Fraudulent Accounts

# of Delinquent Account

# of Deceased Account

Expenses

InvestmentIncome

Long Term Embedded Value

Investment Return

Cost of Funding

Investment Impairment

Value Deterioration

FX Volatility

ILLUSTRATION ONLY

Islamic Banking Competitiveness Report 2011-12

Page 60

COMPETITIVENESS REPORT 2011-201260

One potential scenario shows that risk practices at Islamic banks need to evolve significantly to achieve sustainable growth

Business Strategy

Policies, Standards, People & C

ultureR

isk Organisation &

Governance

Data &

IT Infrastructure

Risk Appetite

Risk Universe

Liquidity Risk

Op’s Risk StrategicRisk

Credit Risk

MarketRisk

Profit Rate Risk

Catastro-phe

Risks

Risk Based Pricing

Active Portfolio

Management

Capital Planning and Management

Risk Adjusted Performance Measurement

Risk Monitoring & MI

Risk Control & Limit Setting

Scenario Analysis & Stress Testing

Risk Aggregation & Economic Capital

Risk Measurement

Risk Identification

Comparable to conventional

Need Enhancement

Weak

ERM FRAMEWORK

Islamic Banking Competitiveness Report 2011-12

Page 61

61COMPETITIVENESS REPORT 2011-2012

Several Islamic banks have initiated a comprehensive transformation agenda for sustainable growth

Risk and compliance • Risk, compliance and regulation to drive

change in business models• Capital management - substantive

reallocation involving tools such as risk adjusted returns, fund transfer pricing, economic capital etc.

The Search for A New Business Model

Operational efficiency and effectiveness

• Customer centric operating model• Improved data management • Updated Shari’a compliant systems

and processes

Innovation• Embracing new technology• Product research & structuring – while

minimizing reputation, regulatory and commercial risk

Growth• Emphasis on core businesses• Consolidation, conversions and new

start-ups – Next 100 in the making• Relationship growth with key clients,

vendors and partners

Islamic Banking Competitiveness Report 2011-12

Page 62

COMPETITIVENESS REPORT 2011-201262

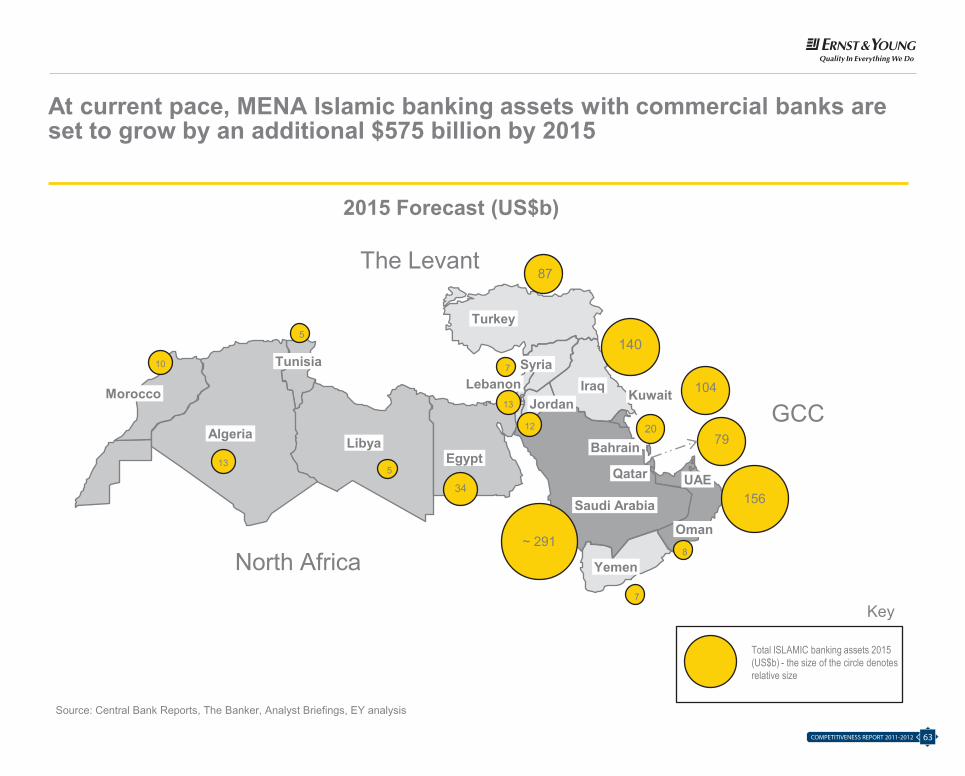

At current pace, MENA Islamic banking assets with commercial banks are set to grow by an additional $575 billion by 2015

2015 Forecast (US$b)

Source: Central Bank Reports, The Banker, Analyst Briefings, EY analysis

Saudi Arabia

Oman

UAEQatar

BahrainAlgeria

LibyaEgypt

Turkey

Tunisia

MoroccoLebanon

JordanIraq

Yemen

Syria

Kuwait

156

~ 291

13

87

140

7920

104

GCC

North Africa

The Levant

7

7

5

34

12

13

10

8

5

Total ISLAMIC banking assets 2015 (US$b) - the size of the circle denotes relative size

Key

Islamic Banking Competitiveness Report 2011-12

Page 63

63COMPETITIVENESS REPORT 2011-2012

While most Islamic banks remain localized to their GCC base, there is potential demand for an estimated 100 new Islamic financial institutions across MENA by 2020

GCC Islamic Banks GCC Conventional Banks

America

1%

America

2%

Europe

8%

Europe

5%

Asia

1%

Asia

3%MENA

85%

MENA

87%

Source: Company Reports, EY analysis (sample based on selective Islamic and conventional banks)

Islamic Banking Competitiveness Report 2011-12

Page 64

COMPETITIVENESS REPORT 2011-201264

However, a major impediment to growth is the weak Islamic finance enabling infrastructure in several OIC markets

Relatively Developed Infrastructure

Some Infrastructure

Weak or No Infrastructure OIC (Organization of Islamic Countries)

Enabling infrastructure would include legislative, regulatory, legal, accounting,

tax, human capital, and Shari’a business framework

Further, Islamic finance standard setting institutions have limited

geographic reach / enforceability remains a challenge

Bahrain, Malaysia and UAEare amongst the major Islamic finance centers

Islamic Banking Competitiveness Report 2011-12

Page 65

65COMPETITIVENESS REPORT 2011-2012

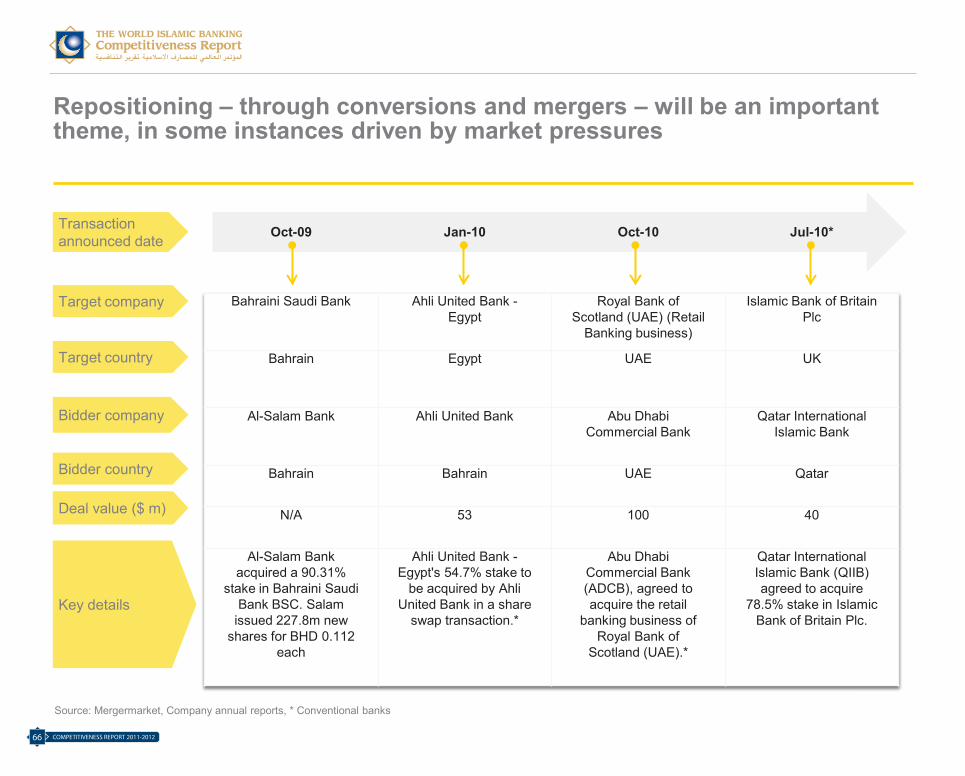

Repositioning – through conversions and mergers – will be an important theme, in some instances driven by market pressures

Bahraini Saudi Bank Ahli United Bank -Egypt

Royal Bank of Scotland (UAE) (Retail

Banking business)

Islamic Bank of Britain Plc

Bahrain Egypt UAE UK

Al-Salam Bank Ahli United Bank Abu Dhabi Commercial Bank

Qatar International Islamic Bank

Bahrain Bahrain UAE Qatar

N/A 53 100 40

Al-Salam Bank acquired a 90.31%

stake in Bahraini Saudi Bank BSC. Salam

issued 227.8m new shares for BHD 0.112

each

Ahli United Bank -Egypt's 54.7% stake to

be acquired by Ahli United Bank in a share

swap transaction.*

Abu Dhabi Commercial Bank (ADCB), agreed to acquire the retail

banking business of Royal Bank of

Scotland (UAE).*

Qatar International Islamic Bank (QIIB) agreed to acquire

78.5% stake in Islamic Bank of Britain Plc.

Oct-09 Jan-10 Oct-10 Jul-10*Transaction announced date

Target company

Target country

Bidder company

Bidder country

Deal value ($ m)