downloads to date - subtelforum.com · internet to resume normal speed on may 10 ... president...

TRANSCRIPT

82

Subsea Capacity Edition

DOWNLOADS TO DATE

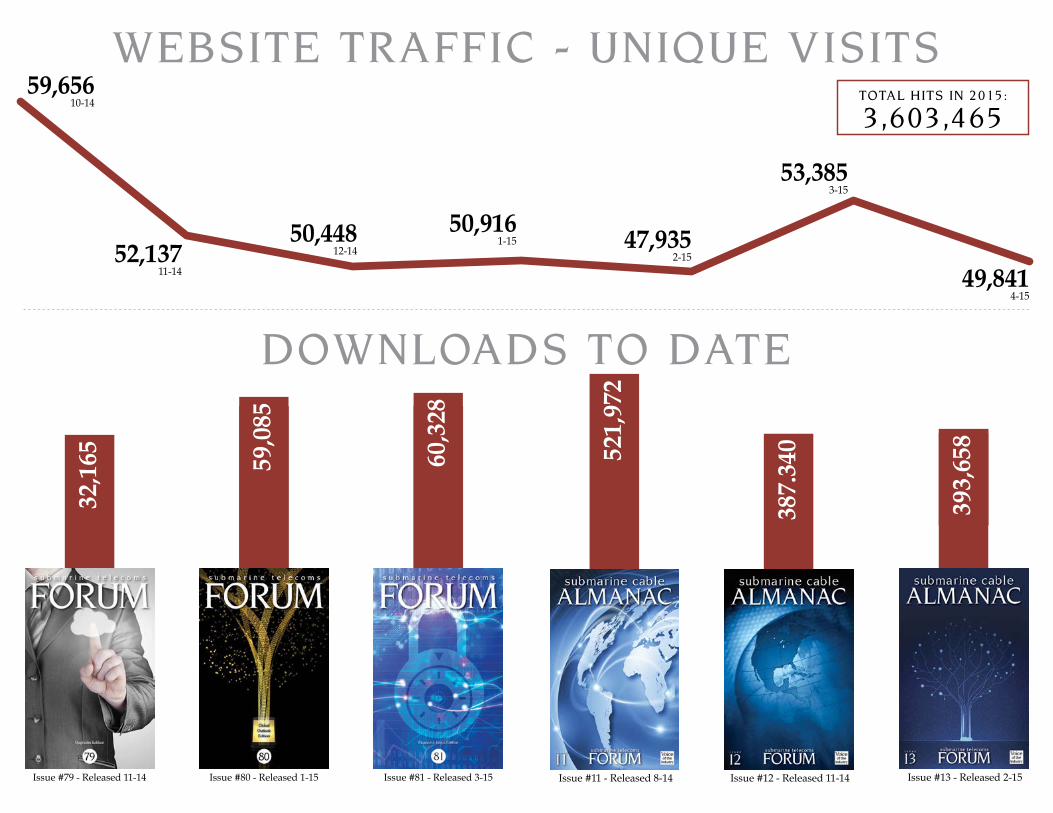

WEBSITE TRAFFIC - UNIQUE VIS ITSTOTAL HITS IN 2015 :

3 , 603 ,465

50,9161-15 47,935

2-15

59,65610-14

50,44812-1452,137

11-14

Issue #11 - Released 8-14

521,

972

Issue #12 - Released 11-1438

7.34

0

59,0

85

Issue #80 - Released 1-15

49,7

16

Issue #79 - Released 11-14

32,1

65

Issue #13 - Released 2-15

393,

658

53,3853-15

49,8414-15

60,3

28

Issue #81 - Released 3-15

Welcome to Issue 81, our Subsea Capacity edition.

When my son flew out a couple of weeks ago, I contacted an old friend, Roly, and told him that the former baby he used to play with under our dining room table left for American Samoa to join his first cableship for an inter-island submarine cable install, and that he would be the junior Owner’s Rep. for the project.

My friend brought me into this industry 30 years ago this year when he hired me to see if there was any business I could pick up here in Washington for BT’s cableships. This started a whirlwind of travel for the two of us across the US, and resulted in a major ‘win’ some six months later. Commando “Fiasco” as it came to be called

was our first effort, and we were hired to rescue the project from what had been two previous unsuccessful installations by an American competitor. Of course we could do it better we assured the client, and possibly deluded ourselves in the process; and some months later, after our two subsequent failed attempts, we admitted defeat and moved on.

Thankfully, there were p l e n t y of other ‘ g o o d ’ projects to do, w h i c h we did, and the rest, they say, is history.

Good (and bad) experience is an excellent instructor. And I appreciate that early opportunity to come into this business and learn something totally foreign and new, as well as establishing a lasting friendship over so many years.

And it is also equally fulfilling

to watch a new, fresher experience be established…

Happy reading.

Wayne Nielsen is the Founder and Publisher of Submarine Telecoms Forum, and previously in 1991, founded and published “Soundings”, a print magazine developed for then BT Marine. In 1998, he founded and published for SAIC the magazine, “Real Time”, the industry’s first electronic magazine. He has written a number of industry papers and articles over the years, and is the author of two published novels, Semblance of Balance (2002, 2014) and Snake Dancer’s Song (2004).

+1.703.444.2527

4 ExordiumWayne Nielsen

8 Advertiser Index

10 News Now

16 Subsea Capacity: An OverviewKieran Clark

26 Trans-Pacific Cables and Their Response to the Web-Scale Effect Colin Anderson

36 Open Cables: A New Business and Technical ModelMark Enright, Edwin Muth & Georg Mohs

48 Latest Developments for Unrepeatered Cable SystemsBertrand Clesca

62 A New Dawn: The Era Of High-Speed Capacity Into IrelandDerek Cassidy

In This Issue...72 Local Partners Key To Exploiting Burgeoning International

Connectivity Demands In AfricaMike Last

82 Rethinking The Submarine NetworkArnaud Leroy

90 Back ReflectionStewart Ash

96 Advertiser’s CornerKristian Nielsen

100 CodaKevin G. Summers

Advertiser IndexOFS www.ofsoptics.com 22

SubOptic www.suboptic.org 60

Terabit Consulting www.terabitconsulting.com 46

WFN Strategies www.wfnstrategies.com 88

The world’s expanding treasure

Celebrating

of SubOptic

30years

Sponsorship and Exhibition Opportunities are now available online and our Call for

Papers will be issued in June 2015

Hosted by

Emerging Subsea Networks

Alaska Communications Partners With Quintillion Holdings To Acquire North Slope Fiber Network

Alcatel Lucent And Algerian Ministry Of Post, Information Technology And Communications To build Orval Undersea Cable System

Alcatel-Lucent Achieves Submarine Cable Breakthrough

Alcatel-Lucent And GoTo Networks To build Australia West Express

Alcatel-Lucent And Ocean Networks To Build South America Pacific Link

Alcatel-Lucent Closes Transaction Streamlining Its Cable Ship Operations

Alcatel-Lucent Unveils Major Transformation For Undersea Cable Systems

America Movil Inaugurates AMX-1 System In Colombia

NewsNow

AquaComms Begins Build Of New America-Europe Connect Subsea Cable System, AEConnect

Axione Wins Gabon Fibre Backbone Contract

Bangla Boost To Tripura Internet Connectivity

Blessing Ceremony Of The RV GEO RESOLUTION, The Latest Addition To The EGS Fleet

Cable & Wireless Consolidates In The Caribbean And Targets Latin America

Cameroon To Launch Submarine Cable System

Caribbean’s Most Ambitious Submarine Fiber-optic Link Nearly Complete

Cause Of Vietnam’s Snail-like Internet Speed Identified; Repairs To Take A Month

NewsNow

Damaged AAG Undersea Cable Repaired

Four Coastal States To Get Cable Landing Points

Global Consortium, NEC Begin Construction Of $250M SEA-US Cable System

Hibernia Express Begins Cable Deployment

Huawei Marine Presents At The 2015 ICPC Plenary

Industry Supplement Issue 2

InfraCos To Connect Lagos, 60 Cities With broadband

Infracos: MainOne, IHS Set To Connect 60 Cities To Broadband

Internet Blackout In Gabon Caused By Sabotage

Internet To Resume Normal Speed On May 10

KJCN Turns To Ciena For Submarine Network Upgrade

KVH Upgrades to 100G Backbone on SJC between Tokyo, Singapore and Hong Kong

Microsoft Invests In Several Submarine Cables In Support Of Cloud Services

New Cross Pacific Has Begun Construction

NEWS Xtera Launches Flex-Rate Channel Card For Flexible, High-Performance 100G/100G+ Optical Networking

Nextgen Connects Pilbara Miner With Perth Ops Centre

Nigeria: Again, Glo Tops Winners’ Chart At Telcos Awards

Nokia Agrees To Buy Out Alcatel-Lucent

Nokia, Alcatel-Lucent Confirm Merger Talks

NewsNow

President Jokowi To Inaugurate Optical Cable System In W. Papua

Sea-floor Sensors Detect Possible Volcanic Eruption

State Ponders New Data Cable

Submarine Cable Plans To Sell Bandwidth To Italian Firm At Low Price

Submarine Cables And Deep Seabed Mining: A Successful And Foundational Workshop

SubOptic 2016: Programme And Papers Committee Now Formed

Telstra Completes Acquisition Of Pacnet

The Plan To Build An Undersea Cable Around The US—And Why We Need It

University Of Hawaii Undersea Cable Upgrade Planned

Vietnam Plans New Internet Cable To China As Problems Recur On Undersea Connection

Vietnam Suffers Second Internet Cable Cut In Less Than 4 Months

Weekly Wrap-up April 27-May 1

Weekly Wrap-Up May 11-15

Weekly Wrap-Up May 4-8

Zayo Group Selects Hibernia Express To Expand Transatlantic Network

Subsea CapacityAn Overview

Kieran Clark

Welcome to SubTel Forum’s annual Subsea Capacity

issue. Every May we aim to take the industry’s pulse by looking at the future of our corner of the telecoms market – specifically what cable owners are planning to add to the ever growing pool of capacity and what technologies are being implemented. The data used in this article is obtained from the public domain and is tracked by the ever-evolving SubTel Forum database, where products like the Almanac, Cable Map and the STF Supplement find their roots.

As new systems continue to come online and existing systems are upgraded, there is a very strong upward trend in global capacity as the world continues to demand more telecommunications services. This is mostly due to increasing demand for low latency, high bandwidth international connections, and to the almost exponential increase in demand for mobile services over the last few years. These factors show little signs of slowing down, so there is a strong expectation that demand will continue to rise at a rapid rate in the coming years.

Even with fewer systems entering service in 2014 than the

previous two years, there was a much larger increase in capacity by comparison. With upgrades more accessible than ever, and with 100 Gb/s wavelength technology being the upgrade of choice, this comes as little surprise. New systems are also making use of increasing amounts of wavelengths crammed on to a single fiber pair. Capacity that needed six or more fiber pairs in the past can now be achieved with only two or three pairs. This allows cable owners to provide more capacity than ever, while keeping fiber manufacturing costs down.

Currently, the Pacific region has the largest share of global capacity at 28 percent, followed closely by 25 percent in the

Mediterranean region. The Atlantic, Indian Ocean and Middle East regions all have about the same amount of

capacity, with the Baltic, Caribbean and Polar regions trailing by a significant margin. With the Pacific region seeing the most amount of activity in recent years and the Mediterranean region being host to several large systems connecting Europe to Africa and Asia, this explains why over half of all global capacity is found in these two regions alone. By contrast, the Atlantic region has been more or less stagnant for the last decade or so, and cable owners are increasingly looking to avoid potentially problematic areas in the Middle East region.

With more and more systems being announced, the SubTel

0 100 200 300 400 500 600 700

2012

2013

2014

Tbps

Global System Capacity By Year 2012-2014

Atlantic 14%

Pacific 28%

Indian Ocean 13%

Mediterranean 25%

Caribbean 4%

Baltic 2%

Middle East 13%

Polar 1%

Current Capacity By Region

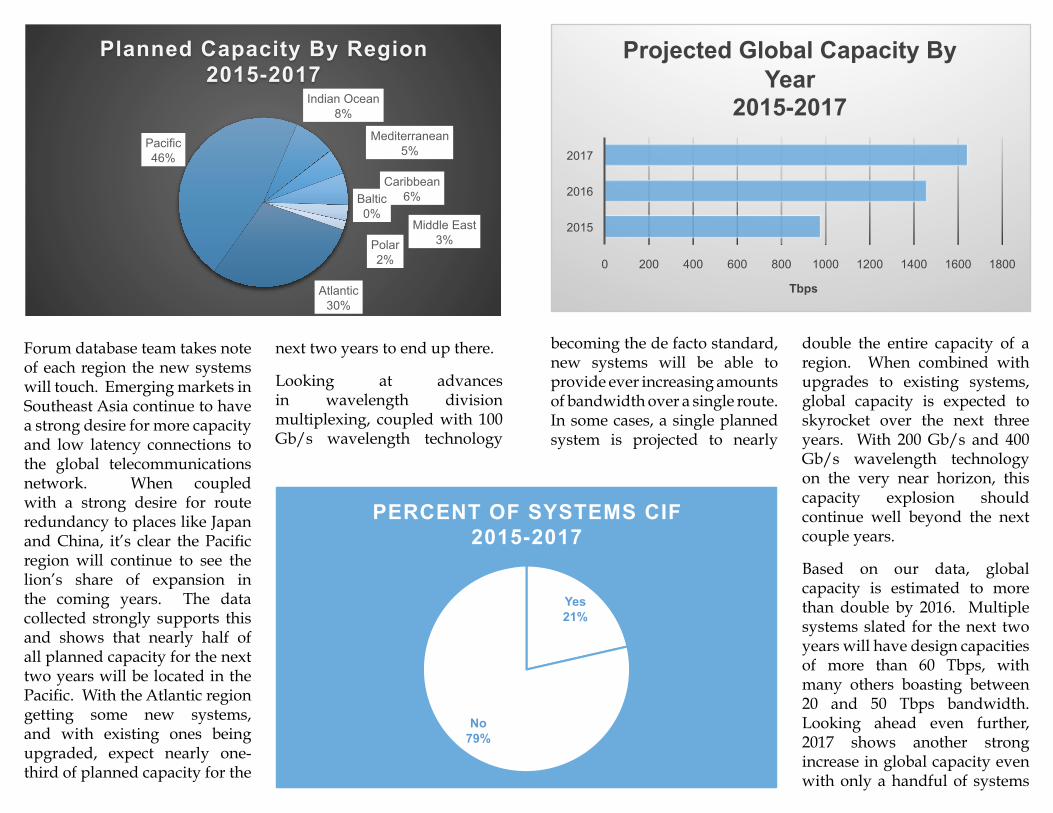

Forum database team takes note of each region the new systems will touch. Emerging markets in Southeast Asia continue to have a strong desire for more capacity and low latency connections to the global telecommunications network. When coupled with a strong desire for route redundancy to places like Japan and China, it’s clear the Pacific region will continue to see the lion’s share of expansion in the coming years. The data collected strongly supports this and shows that nearly half of all planned capacity for the next two years will be located in the Pacific. With the Atlantic region getting some new systems, and with existing ones being upgraded, expect nearly one-third of planned capacity for the

next two years to end up there.

Looking at advances in wavelength division multiplexing, coupled with 100 Gb/s wavelength technology

becoming the de facto standard, new systems will be able to provide ever increasing amounts of bandwidth over a single route. In some cases, a single planned system is projected to nearly

double the entire capacity of a region. When combined with upgrades to existing systems, global capacity is expected to skyrocket over the next three years. With 200 Gb/s and 400 Gb/s wavelength technology on the very near horizon, this capacity explosion should continue well beyond the next couple years.

Based on our data, global capacity is estimated to more than double by 2016. Multiple systems slated for the next two years will have design capacities of more than 60 Tbps, with many others boasting between 20 and 50 Tbps bandwidth. Looking ahead even further, 2017 shows another strong increase in global capacity even with only a handful of systems

Atlantic 30%

Pacific 46%

Indian Ocean 8%

Mediterranean 5%

Caribbean 6% Baltic

0% Middle East

3% Polar 2% 0 200 400 600 800 1000 1200 1400 1600 1800

2015

2016

2017

Tbps

Projected Global Capacity By Year

2015-2017

Yes 21%

No 79%

PERCENT OF SYSTEMS CIF 2015-2017

announced so far. All of the systems currently planned are being designed with 100 Gb/s technology in mind, so expect an even more drastic increase when 400 Gb/s technology enters the market.

While all of this data seems very promising, a healthy dose of reality is administered when looking at the percentage of

systems that are CIF. There are 42 systems planned globally for the next few years and only 21 percent have achieved this milestone. This is the real determination on whether or not a system will ever see the light of day, and so expectations must be adjusted when a low CIF rate is observed. The good news is that this time last year, only 11 percent of systems for

the next two years were CIF. So, while caution is advised when looking at estimated growth for the foreseeable future, the industry definitely appears to be in a stronger position than a year ago.

Overall, the submarine telecoms industry looks to be standing on solid ground from a capacity standpoint. New technologies

are making it cheaper than ever for cable owners to provide high capacity solutions to their customers. While this may mean less new systems overall moving forward, regions around the world continue to demand more capacity to feed their data needs and route redundancy to ensure communications uptime. Looking ahead, the future of the industry seems secure.

Kieran Clark is an Analyst for Submarine Telecoms Forum. He joined the company in 2013 as a Broadcast Technician to provide support for live event video streaming. In 2014, Kieran was promoted

Forum publications. He has 4+ years of live production experience and has worked alongside some of the premier organizations in video web streaming.

to Analyst and is currently responsible for the research and maintenance that supports the SubTel Forum International Submarine Cable Database; his analysis is featured in almost the entire array of SubTel

Coherent Transport

High Signal Power

Outstanding Bend Performance

Simplified Network Design

Long-term Reliability

To learn more, ask your cabler about OFS or visit www.ofsoptics.comA Furukawa Company

/ofsoptics /company/ofs/ofs_telecom /OFSoptics

TeraWave™ and Allwave® FLEX ZWP Ocean Fibers

From shore to shore . . .OFS’ fiber solution enables 100 Gb/s with high signal power & low loss performance

JAN

FEB

MAR

APR

MAY

JUN

JUL

AUG

SEP

OCT

NOV

DEC

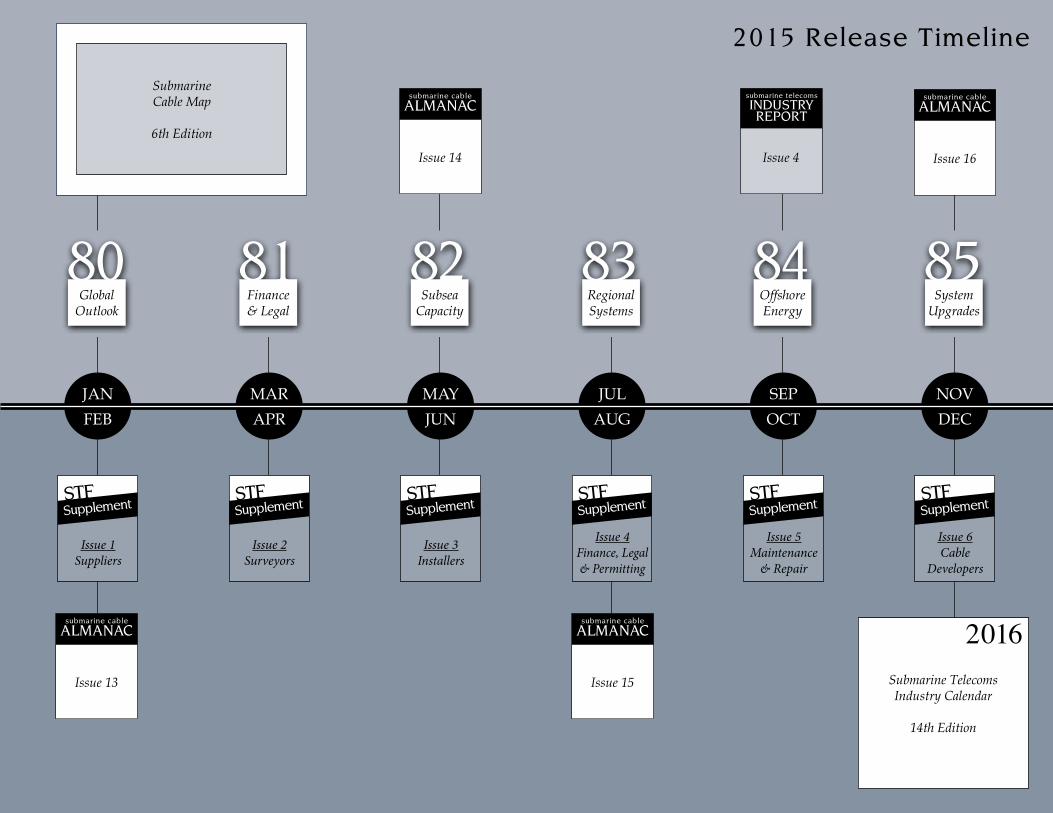

2015 Release Timel ine

SubmarineCable Map

6th Edition

80Global

Outlook

81Finance& Legal

82Subsea

Capacity

83RegionalSystems

84OffshoreEnergy

85System

Upgrades

Issue 14 Issue 16

Issue 13 Issue 15 Submarine TelecomsIndustry Calendar

14th Edition

2016

Issue 4

Issue 4Finance, Legal & Permitting

Supplement STF

Issue 3Installers

Supplement STF

Issue 2Surveyors

Supplement STF

Issue 1Suppliers

Supplement STF

Issue 5Maintenance

& Repair

Supplement STF

Issue 6Cable

Developers

Supplement STF

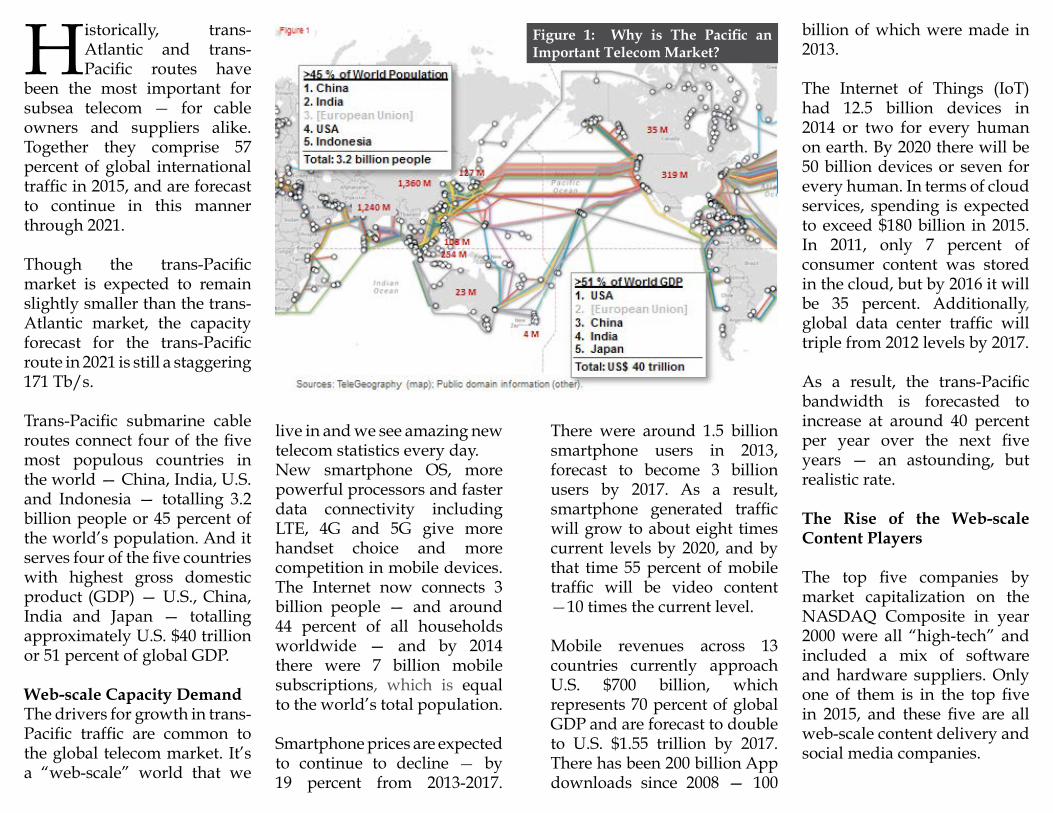

Trans-Pacific Cablesand Their Response to the Web-Scale Effect

Colin Anderson

Historically, trans-Atlantic and trans-Pacific routes have

been the most important for subsea telecom — for cable owners and suppliers alike. Together they comprise 57 percent of global international traffic in 2015, and are forecast to continue in this manner through 2021.

Though the trans-Pacific market is expected to remain slightly smaller than the trans-Atlantic market, the capacity forecast for the trans-Pacific route in 2021 is still a staggering 171 Tb/s.

Trans-Pacific submarine cable routes connect four of the five most populous countries in the world — China, India, U.S. and Indonesia — totalling 3.2 billion people or 45 percent of the world’s population. And it serves four of the five countries with highest gross domestic product (GDP) — U.S., China, India and Japan — totalling approximately U.S. $40 trillion or 51 percent of global GDP.

Web-scale Capacity DemandThe drivers for growth in trans-Pacific traffic are common to the global telecom market. It’s a “web-scale” world that we

billion of which were made in 2013.

The Internet of Things (IoT) had 12.5 billion devices in 2014 or two for every human on earth. By 2020 there will be 50 billion devices or seven for every human. In terms of cloud services, spending is expected to exceed $180 billion in 2015. In 2011, only 7 percent of consumer content was stored in the cloud, but by 2016 it will be 35 percent. Additionally, global data center traffic will triple from 2012 levels by 2017.

As a result, the trans-Pacific bandwidth is forecasted to increase at around 40 percent per year over the next five years — an astounding, but realistic rate.

The Rise of the Web-scale Content Players

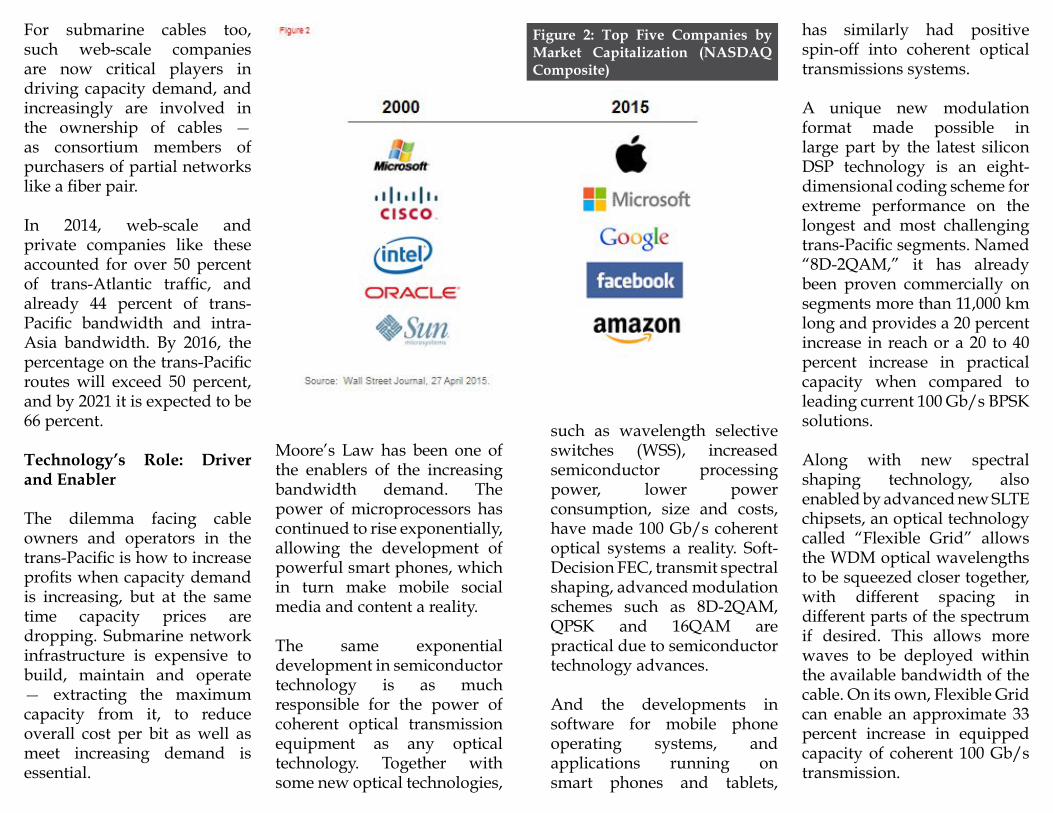

The top five companies by market capitalization on the NASDAQ Composite in year 2000 were all “high-tech” and included a mix of software and hardware suppliers. Only one of them is in the top five in 2015, and these five are all web-scale content delivery and social media companies.

live in and we see amazing new telecom statistics every day. New smartphone OS, more powerful processors and faster data connectivity including LTE, 4G and 5G give more handset choice and more competition in mobile devices. The Internet now connects 3 billion people — and around 44 percent of all households worldwide — and by 2014 there were 7 billion mobile subscriptions, which is equal to the world’s total population.

Smartphone prices are expected to continue to decline — by 19 percent from 2013-2017.

There were around 1.5 billion smartphone users in 2013, forecast to become 3 billion users by 2017. As a result, smartphone generated traffic will grow to about eight times current levels by 2020, and by that time 55 percent of mobile traffic will be video content —10 times the current level.

Mobile revenues across 13 countries currently approach U.S. $700 billion, which represents 70 percent of global GDP and are forecast to double to U.S. $1.55 trillion by 2017. There has been 200 billion App downloads since 2008 — 100

Figure 1: Why is The Pacific an Important Telecom Market?

For submarine cables too, such web-scale companies are now critical players in driving capacity demand, and increasingly are involved in the ownership of cables — as consortium members of purchasers of partial networks like a fiber pair.

In 2014, web-scale and private companies like these accounted for over 50 percent of trans-Atlantic traffic, and already 44 percent of trans-Pacific bandwidth and intra-Asia bandwidth. By 2016, the percentage on the trans-Pacific routes will exceed 50 percent, and by 2021 it is expected to be 66 percent.

Technology’s Role: Driver and Enabler

The dilemma facing cable owners and operators in the trans-Pacific is how to increase profits when capacity demand is increasing, but at the same time capacity prices are dropping. Submarine network infrastructure is expensive to build, maintain and operate — extracting the maximum capacity from it, to reduce overall cost per bit as well as meet increasing demand is essential.

Moore’s Law has been one of the enablers of the increasing bandwidth demand. The power of microprocessors has continued to rise exponentially, allowing the development of powerful smart phones, which in turn make mobile social media and content a reality.

The same exponential development in semiconductor technology is as much responsible for the power of coherent optical transmission equipment as any optical technology. Together with some new optical technologies,

such as wavelength selective switches (WSS), increased semiconductor processing power, lower power consumption, size and costs, have made 100 Gb/s coherent optical systems a reality. Soft-Decision FEC, transmit spectral shaping, advanced modulation schemes such as 8D-2QAM, QPSK and 16QAM are practical due to semiconductor technology advances.

And the developments in software for mobile phone operating systems, and applications running on smart phones and tablets,

has similarly had positive spin-off into coherent optical transmissions systems.

A unique new modulation format made possible in large part by the latest silicon DSP technology is an eight-dimensional coding scheme for extreme performance on the longest and most challenging trans-Pacific segments. Named “8D-2QAM,” it has already been proven commercially on segments more than 11,000 km long and provides a 20 percent increase in reach or a 20 to 40 percent increase in practical capacity when compared to leading current 100 Gb/s BPSK solutions.

Along with new spectral shaping technology, also enabled by advanced new SLTE chipsets, an optical technology called “Flexible Grid” allows the WDM optical wavelengths to be squeezed closer together, with different spacing in different parts of the spectrum if desired. This allows more waves to be deployed within the available bandwidth of the cable. On its own, Flexible Grid can enable an approximate 33 percent increase in equipped capacity of coherent 100 Gb/s transmission.

Figure 2: Top Five Companies by Market Capitalization (NASDAQ Composite)

The new 8D-2QAM scheme and Flexible Grid technologies complement each other. Since the 8D-2QAM modulation format is more resistant to interference between adjacent wavelengths, it allows Flexible Grid to be used to squeeze the WDM channels even closer together to utilize the available wet plant spectrum to the fullest extent.

Commercial applications in real networks have proven the strength of 8D-2QAM modulation and Flexible Grid technology. Capacity increases of up to 85 percent have been

achieved on segments over 8,000 km long.

In addition, it has enabled 100 Gb/s transmission for the first time on segments of existing systems longer than 11,000 km.

Coherent technologies for SLTE have brought enormously increased value to submerged assets, and seem likely to continue to do so. Some cables halfway through their 25-year design lifetime now have expected ultimate capacities, which are 10 to 60 times greater than at RFS date — even on the longest or most

challenging segments. Silicon technology, optical technology and software advances help to drive capacity demand up, and also help to enable coherent optical transmission systems to meet the demand, including for subsea systems.

By deploying the latest SLTE technology, cable owners and operators can monetize their assets and extract the maximum value from their investments in submerged plant infrastructure — whether new or existing. By utilizing the latest terminal equipment, they can increase ultimate capacity

and incremental revenue, and amortize the wet plant capital and O&M costs over higher capacity.

At the same time, they can also reduce equipment requirements to save on equipment cost, power consumption, space, and operation and maintenance costs, enabling increased functionality and a wider menu of services.

Planning for the Next 10 Years

“Prediction is very difficult, especially about the future” is

Figure 3: Avoiding Wasted Spectrum with Spectral Shaping and Flexible Grid

Figure 4: Trans-Pacific Example of 8D-2QAM & Flexible Grid

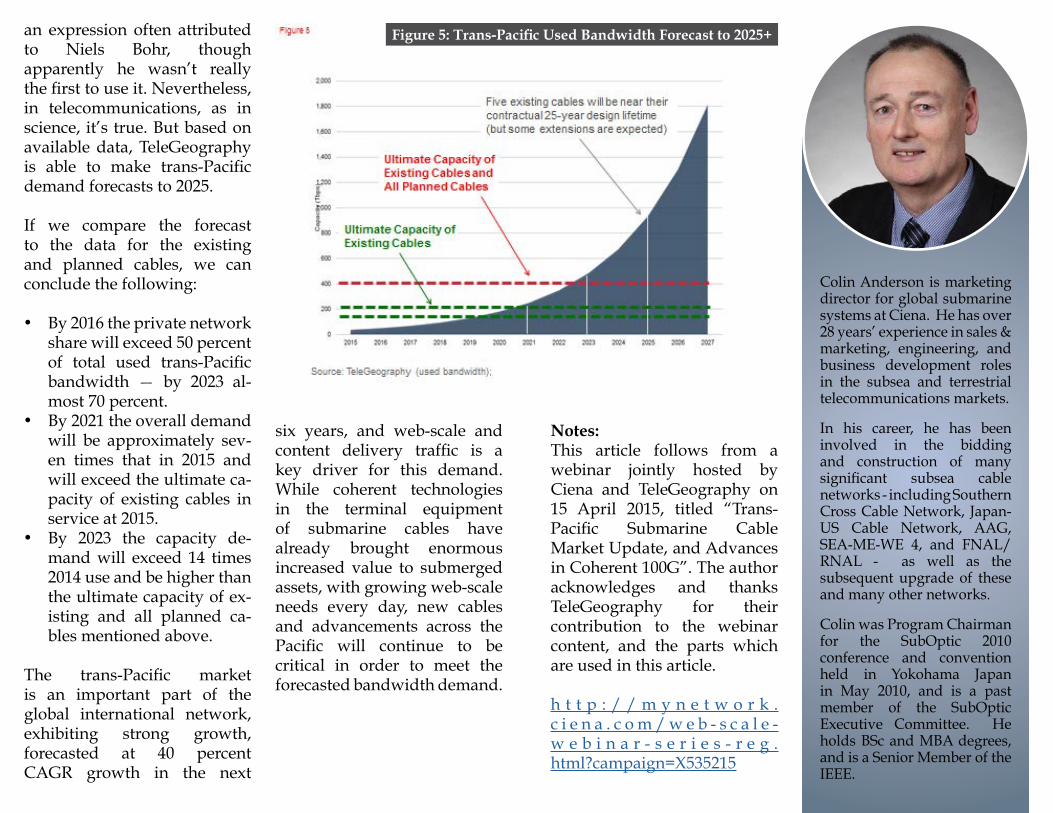

an expression often attributed to Niels Bohr, though apparently he wasn’t really the first to use it. Nevertheless, in telecommunications, as in science, it’s true. But based on available data, TeleGeography is able to make trans-Pacific demand forecasts to 2025.

If we compare the forecast to the data for the existing and planned cables, we can conclude the following:

• By 2016 the private network share will exceed 50 percent of total used trans-Pacific bandwidth — by 2023 al-most 70 percent.

• By 2021 the overall demand will be approximately sev-en times that in 2015 and will exceed the ultimate ca-pacity of existing cables in service at 2015.

• By 2023 the capacity de-mand will exceed 14 times 2014 use and be higher than the ultimate capacity of ex-isting and all planned ca-bles mentioned above.

The trans-Pacific market is an important part of the global international network, exhibiting strong growth, forecasted at 40 percent CAGR growth in the next

six years, and web-scale and content delivery traffic is a key driver for this demand. While coherent technologies in the terminal equipment of submarine cables have already brought enormous increased value to submerged assets, with growing web-scale needs every day, new cables and advancements across the Pacific will continue to be critical in order to meet the forecasted bandwidth demand.

Notes:This article follows from a webinar jointly hosted by Ciena and TeleGeography on 15 April 2015, titled “Trans-Pacific Submarine Cable Market Update, and Advances in Coherent 100G”. The author acknowledges and thanks TeleGeography for their contribution to the webinar content, and the parts which are used in this article.

h t t p : / / m y n e t w o r k .c i e n a . c o m / w e b - s c a l e -w e b i n a r - s e r i e s - r e g .html?campaign=X535215

Figure 5: Trans-Pacific Used Bandwidth Forecast to 2025+

Colin Anderson is marketing director for global submarine systems at Ciena. He has over 28 years’ experience in sales & marketing, engineering, and business development roles in the subsea and terrestrial telecommunications markets.

In his career, he has been involved in the bidding and construction of many significant subsea cable networks - including Southern Cross Cable Network, Japan-US Cable Network, AAG, SEA-ME-WE 4, and FNAL/RNAL - as well as the subsequent upgrade of these and many other networks.

Colin was Program Chairman for the SubOptic 2010 conference and convention held in Yokohama Japan in May 2010, and is a past member of the SubOptic Executive Committee. He holds BSc and MBA degrees, and is a Senior Member of the IEEE.

Open Cables:A New Business and Technical Model

Mark Enright, Edwin Muth& Georg Mohs ©2015 TE Connectivity

TE Connectivity and TE connectivity (logo) are trademarks

For many decades, the submarine cable industry provided

purchasers with complete solutions delivering capacity in increments corresponding to the best technology available at the time. As customer needs and technology evolve, the scope of undersea systems evolve as well. As recently as a few years ago, it was common for the scope of undersea systems to include Network Protection Equipment (NPE) – equipment used to aggregate and route traffic – but now most system purchasers procure this equipment separately as part of their overall network transport plan. Now this scope is evolving again via the emergence of coherent technology and performance provided by embedded high-speed digital signal processing.

This technology disruption led to some commoditization of the transponder technology, further driven by commercial merchant silicon and

module makers. In addition, it led to the possibility of converging terrestrial and submarine networks, assuming capabilities of terrestrial transponders were adequate for submarine distances. This convergence can be effective in the packet optical transport domain, as router transponders also are becoming capable of long haul transmission and bulk electronic dispersion compensation. All of these trends are leading to a strong interest in a new model of open cables.

Definition of Open Cables:

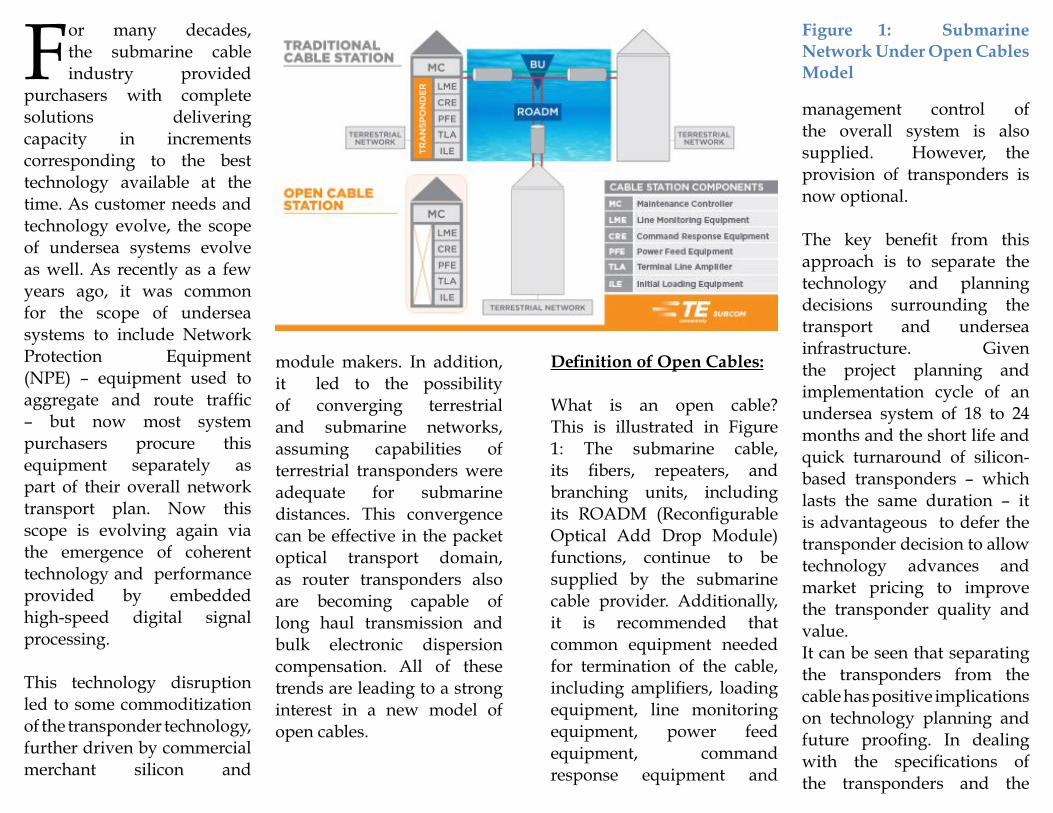

What is an open cable? This is illustrated in Figure 1: The submarine cable, its fibers, repeaters, and branching units, including its ROADM (Reconfigurable Optical Add Drop Module) functions, continue to be supplied by the submarine cable provider. Additionally, it is recommended that common equipment needed for termination of the cable, including amplifiers, loading equipment, line monitoring equipment, power feed equipment, command response equipment and

management control of the overall system is also supplied. However, the provision of transponders is now optional.

The key benefit from this approach is to separate the technology and planning decisions surrounding the transport and undersea infrastructure. Given the project planning and implementation cycle of an undersea system of 18 to 24 months and the short life and quick turnaround of silicon-based transponders – which lasts the same duration – it is advantageous to defer the transponder decision to allow technology advances and market pricing to improve the transponder quality and value.It can be seen that separating the transponders from the cable has positive implications on technology planning and future proofing. In dealing with the specifications of the transponders and the

Figure 1: Submarine Network Under Open Cables Model

aggregate of the industry’s roadmaps for these products, a purchaser can plan ahead one or two generations of transponders and ensure that consideration is given to optimize current capacity, future proofing, and cost parameters.

Modern Coherent System Characteristics

One key question to be answered is how can cables and transponders each be specified to deliver initial capacity and ensure that the

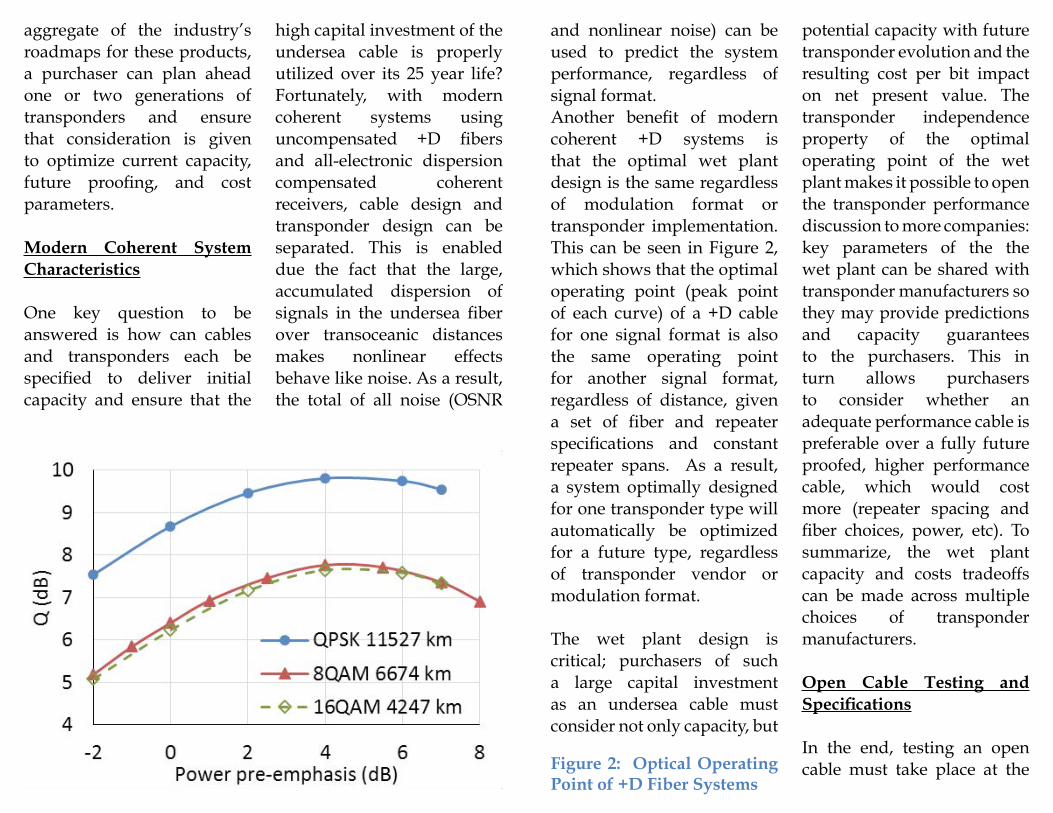

high capital investment of the undersea cable is properly utilized over its 25 year life? Fortunately, with modern coherent systems using uncompensated +D fibers and all-electronic dispersion compensated coherent receivers, cable design and transponder design can be separated. This is enabled due the fact that the large, accumulated dispersion of signals in the undersea fiber over transoceanic distances makes nonlinear effects behave like noise. As a result, the total of all noise (OSNR

and nonlinear noise) can be used to predict the system performance, regardless of signal format. Another benefit of modern coherent +D systems is that the optimal wet plant design is the same regardless of modulation format or transponder implementation. This can be seen in Figure 2, which shows that the optimal operating point (peak point of each curve) of a +D cable for one signal format is also the same operating point for another signal format, regardless of distance, given a set of fiber and repeater specifications and constant repeater spans. As a result, a system optimally designed for one transponder type will automatically be optimized for a future type, regardless of transponder vendor or modulation format. The wet plant design is critical; purchasers of such a large capital investment as an undersea cable must consider not only capacity, but

potential capacity with future transponder evolution and the resulting cost per bit impact on net present value. The transponder independence property of the optimal operating point of the wet plant makes it possible to open the transponder performance discussion to more companies: key parameters of the the wet plant can be shared with transponder manufacturers so they may provide predictions and capacity guarantees to the purchasers. This in turn allows purchasers to consider whether an adequate performance cable is preferable over a fully future proofed, higher performance cable, which would cost more (repeater spacing and fiber choices, power, etc). To summarize, the wet plant capacity and costs tradeoffs can be made across multiple choices of transponder manufacturers.

Open Cable Testing and Specifications

In the end, testing an open cable must take place at the Figure 2: Optical Operating

Point of +D Fiber Systems

time of delivery and a set of clear acceptance criteria is required for final acceptance. This Open Cable Specification must also allow transponder manufacturers, including submarine equipment incumbents, to accurately predict capacity that they are going to offer purchasers.

There are several options available to the industry.

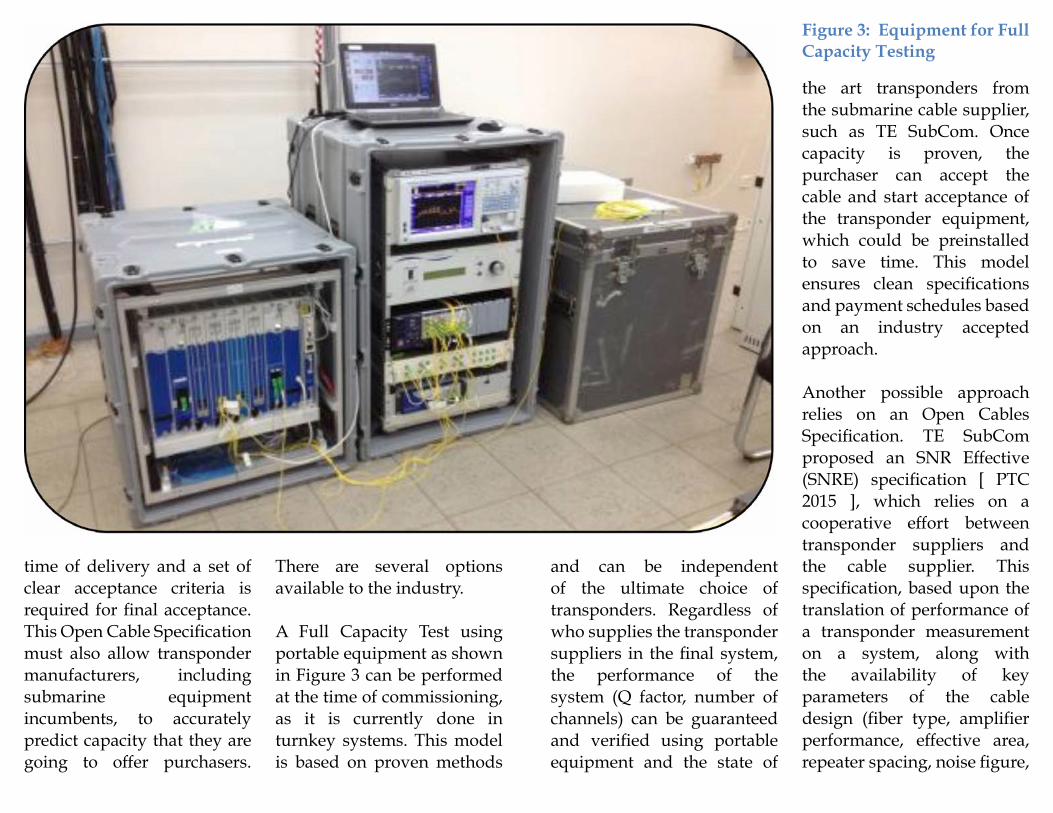

A Full Capacity Test using portable equipment as shown in Figure 3 can be performed at the time of commissioning, as it is currently done in turnkey systems. This model is based on proven methods

and can be independent of the ultimate choice of transponders. Regardless of who supplies the transponder suppliers in the final system, the performance of the system (Q factor, number of channels) can be guaranteed and verified using portable equipment and the state of

the art transponders from the submarine cable supplier, such as TE SubCom. Once capacity is proven, the purchaser can accept the cable and start acceptance of the transponder equipment, which could be preinstalled to save time. This model ensures clean specifications and payment schedules based on an industry accepted approach.

Another possible approach relies on an Open Cables Specification. TE SubCom proposed an SNR Effective (SNRE) specification [ PTC 2015 ], which relies on a cooperative effort between transponder suppliers and the cable supplier. This specification, based upon the translation of performance of a transponder measurement on a system, along with the availability of key parameters of the cable design (fiber type, amplifier performance, effective area, repeater spacing, noise figure,

Figure 3: Equipment for Full Capacity Testing

etc.) can enable a capacity projection commitment across transponder vendors and modulation types. This concept of an Open Cables Specification is in its development stage, and the effects of innovation such as nonlinear compensation will require further discussion with multiple parties. The ITU and other standards bodies would be excellent forums to advance this approach.

And finally, perhaps a solution can be developed from independent test equipment manufacturers? This test equipment could include elements of the two approaches mentioned above, including agreed upon reference transponders and SNRE, plus other measurements.

Conclusion:

In conclusion, DWDM equipment makers, test equipment makers and network owners have an opportunity to help evolve the field to further enable a wider

portfolio of options to the purchaser’s benefit. While in its fledgling state, if nurtured properly, open cables provides an opportunity for undersea networks to soar to new heights.

Mark Enright has been with TE SubCom for 27 years. During his career he has held positions in Manufacture, Project Management and R&D. Mark’s Customer Solutions team is responsible for Product Line Management, System Design and Implementation, System Testing & Training, Network Testing, Technical Customer Support Hotline and Power Feed Equipment.

Dr. Georg Mohs has been with TE SubCom since 2001. He has held various positions in the company including Transmission Testing and System Design before becoming Director Transmission Research in 2009 with responsibility for the forward looking experimental research work at SubCom. Since June 2013 Georg is Director System Design and Implementation responsible for the wet and dry engineering solutions for our Customers.

Edwin Muth is Director of Product Line Management at TE SubCom, where he manages dry and wet plant product cycles. He joined TE SubCom in 2011. Prior to this he was a Senior Director at Infineon Technologies, and held both R&D and business leadership positions at LSI, Agere Systems and Lucent, \ and as VP of engineering of SyChip, a Lucent new venture. His leadership ranges from technical and business teams in consumer wireless, integrated circuits, semiconductor fabrication technologies and satellite communications, ranging from startup size to large teams.

It is still early in the creation and adoption of this business approach, but the future looks bright for open cables..

INTELLIGENCE, ANALYSIS, AND FORECASTINGFOR THE INTERNATIONAL TELECOMMUNICATIONS INFRASTRUCTURE COMMUNITY

Terabit Consulting is a leading source of market intelligence, forecasting, and guidance for the international telecommunications infrastructure community. Its long history of accurate, innovative analysis and advisory services is in large part attributable to the trust and respect it has earned among industry leaders. Terabit Consulting has completed studies for dozens of leading telecom infrastructure projects worldwide and its analysts have traveled to research and deliver studies in more than 70 countries, giving it an unmatched level of experience in nearly every region of the globe.

Terabit’s primary clients include financial institutions, development agencies, government ministries, telecom carriers, project developers, suppliers, financiers, law offices, and industry associations, as well as other members of the international telecommunications infrastructure community.

Learn more at www.terabitconsulting.com or contact a Terabit Consulting representative today.

Terabit Consulting245 First Street, 18th FloorCambridge, Massachusetts 02142 USATel. +1 617 444 [email protected]

Latest Developments for Unrepeatered Cable Systems

Bertrand Clesca

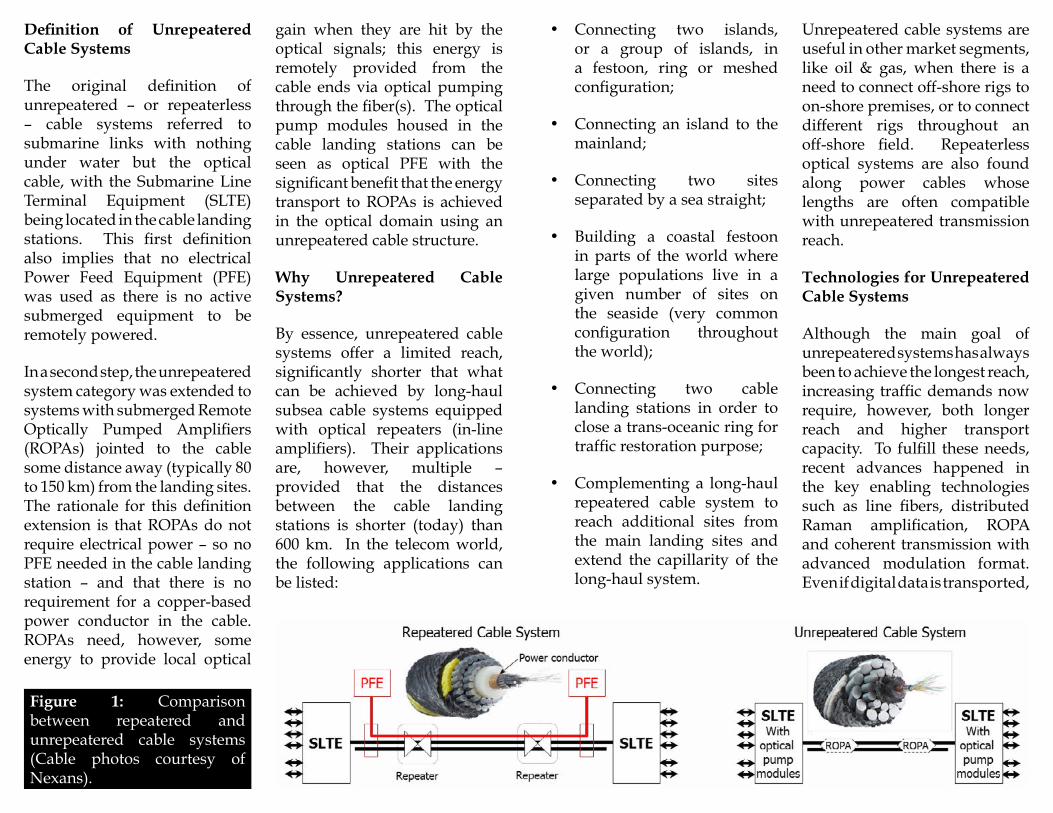

Definition of Unrepeatered Cable Systems

The original definition of unrepeatered – or repeaterless – cable systems referred to submarine links with nothing under water but the optical cable, with the Submarine Line Terminal Equipment (SLTE) being located in the cable landing stations. This first definition also implies that no electrical Power Feed Equipment (PFE) was used as there is no active submerged equipment to be remotely powered.

In a second step, the unrepeatered system category was extended to systems with submerged Remote Optically Pumped Amplifiers (ROPAs) jointed to the cable some distance away (typically 80 to 150 km) from the landing sites. The rationale for this definition extension is that ROPAs do not require electrical power – so no PFE needed in the cable landing station – and that there is no requirement for a copper-based power conductor in the cable. ROPAs need, however, some energy to provide local optical

gain when they are hit by the optical signals; this energy is remotely provided from the cable ends via optical pumping through the fiber(s). The optical pump modules housed in the cable landing stations can be seen as optical PFE with the significant benefit that the energy transport to ROPAs is achieved in the optical domain using an unrepeatered cable structure.

Why Unrepeatered Cable Systems?

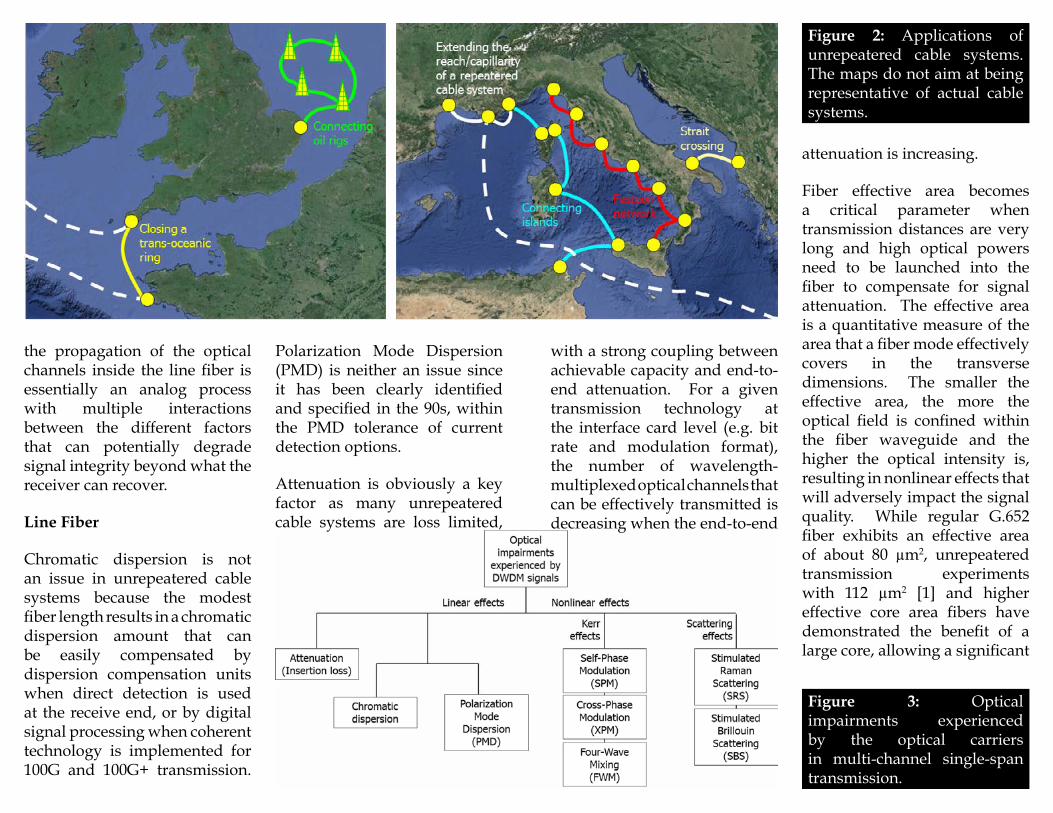

By essence, unrepeatered cable systems offer a limited reach, significantly shorter that what can be achieved by long-haul subsea cable systems equipped with optical repeaters (in-line amplifiers). Their applications are, however, multiple – provided that the distances between the cable landing stations is shorter (today) than 600 km. In the telecom world, the following applications can be listed:

• Connecting two islands, or a group of islands, in a festoon, ring or meshed configuration;

• Connecting an island to the mainland;

• Connecting two sites separated by a sea straight;

• Building a coastal festoon in parts of the world where large populations live in a given number of sites on the seaside (very common configuration throughout the world);

• Connecting two cable landing stations in order to close a trans-oceanic ring for traffic restoration purpose;

• Complementing a long-haul repeatered cable system to reach additional sites from the main landing sites and extend the capillarity of the long-haul system.

Unrepeatered cable systems are useful in other market segments, like oil & gas, when there is a need to connect off-shore rigs to on-shore premises, or to connect different rigs throughout an off-shore field. Repeaterless optical systems are also found along power cables whose lengths are often compatible with unrepeatered transmission reach.

Technologies for Unrepeatered Cable Systems

Although the main goal of unrepeatered systems has always been to achieve the longest reach, increasing traffic demands now require, however, both longer reach and higher transport capacity. To fulfill these needs, recent advances happened in the key enabling technologies such as line fibers, distributed Raman amplification, ROPA and coherent transmission with advanced modulation format. Even if digital data is transported,

Figure 1: Comparison between repeatered and unrepeatered cable systems (Cable photos courtesy of Nexans).

the propagation of the optical channels inside the line fiber is essentially an analog process with multiple interactions between the different factors that can potentially degrade signal integrity beyond what the receiver can recover.

Line Fiber

Chromatic dispersion is not an issue in unrepeatered cable systems because the modest fiber length results in a chromatic dispersion amount that can be easily compensated by dispersion compensation units when direct detection is used at the receive end, or by digital signal processing when coherent technology is implemented for 100G and 100G+ transmission.

Polarization Mode Dispersion (PMD) is neither an issue since it has been clearly identified and specified in the 90s, within the PMD tolerance of current detection options.

Attenuation is obviously a key factor as many unrepeatered cable systems are loss limited,

with a strong coupling between achievable capacity and end-to-end attenuation. For a given transmission technology at the interface card level (e.g. bit rate and modulation format), the number of wavelength-multiplexed optical channels that can be effectively transmitted is decreasing when the end-to-end

attenuation is increasing.

Fiber effective area becomes a critical parameter when transmission distances are very long and high optical powers need to be launched into the fiber to compensate for signal attenuation. The effective area is a quantitative measure of the area that a fiber mode effectively covers in the transverse dimensions. The smaller the effective area, the more the optical field is confined within the fiber waveguide and the higher the optical intensity is, resulting in nonlinear effects that will adversely impact the signal quality. While regular G.652 fiber exhibits an effective area of about 80 µm2, unrepeatered transmission experiments with 112 µm2 [1] and higher effective core area fibers have demonstrated the benefit of a large core, allowing a significant

Figure 2: Applications of unrepeatered cable systems. The maps do not aim at being representative of actual cable systems.

Figure 3: Optical impairments experienced by the optical carriers in multi-channel single-span transmission.

increase of the launched signal power with respect to standard fibers.

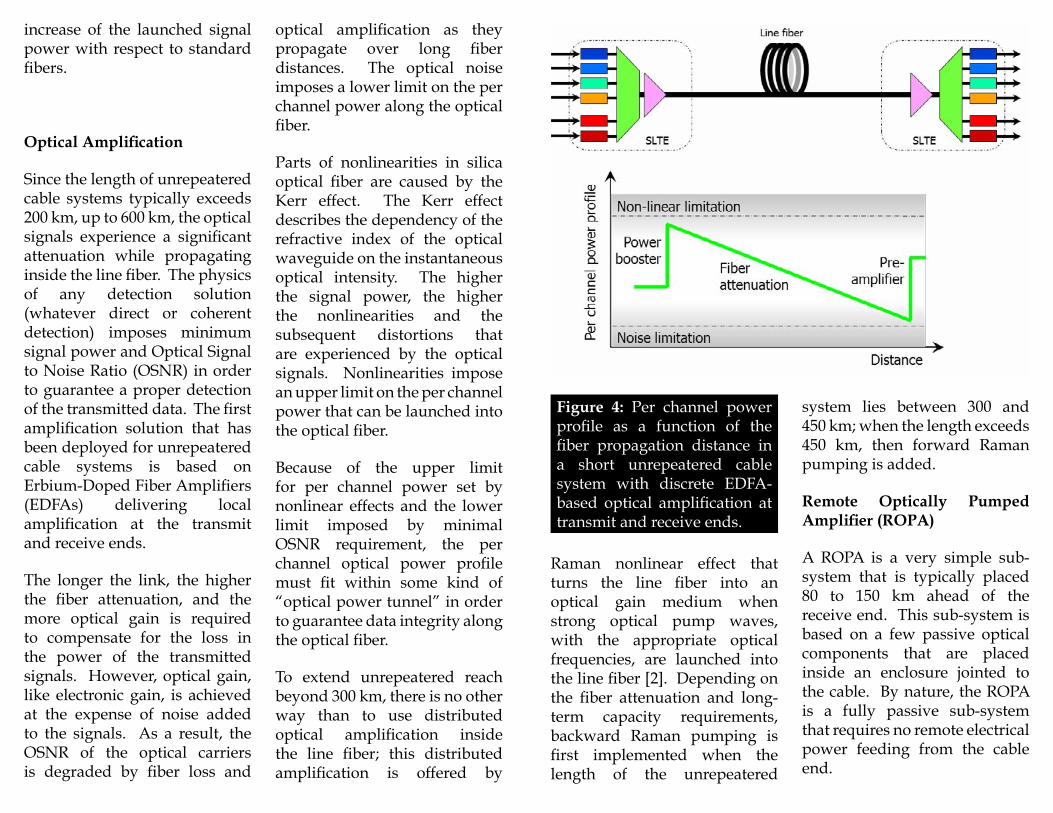

Optical Amplification

Since the length of unrepeatered cable systems typically exceeds 200 km, up to 600 km, the optical signals experience a significant attenuation while propagating inside the line fiber. The physics of any detection solution (whatever direct or coherent detection) imposes minimum signal power and Optical Signal to Noise Ratio (OSNR) in order to guarantee a proper detection of the transmitted data. The first amplification solution that has been deployed for unrepeatered cable systems is based on Erbium-Doped Fiber Amplifiers (EDFAs) delivering local amplification at the transmit and receive ends.

The longer the link, the higher the fiber attenuation, and the more optical gain is required to compensate for the loss in the power of the transmitted signals. However, optical gain, like electronic gain, is achieved at the expense of noise added to the signals. As a result, the OSNR of the optical carriers is degraded by fiber loss and

system lies between 300 and 450 km; when the length exceeds 450 km, then forward Raman pumping is added.

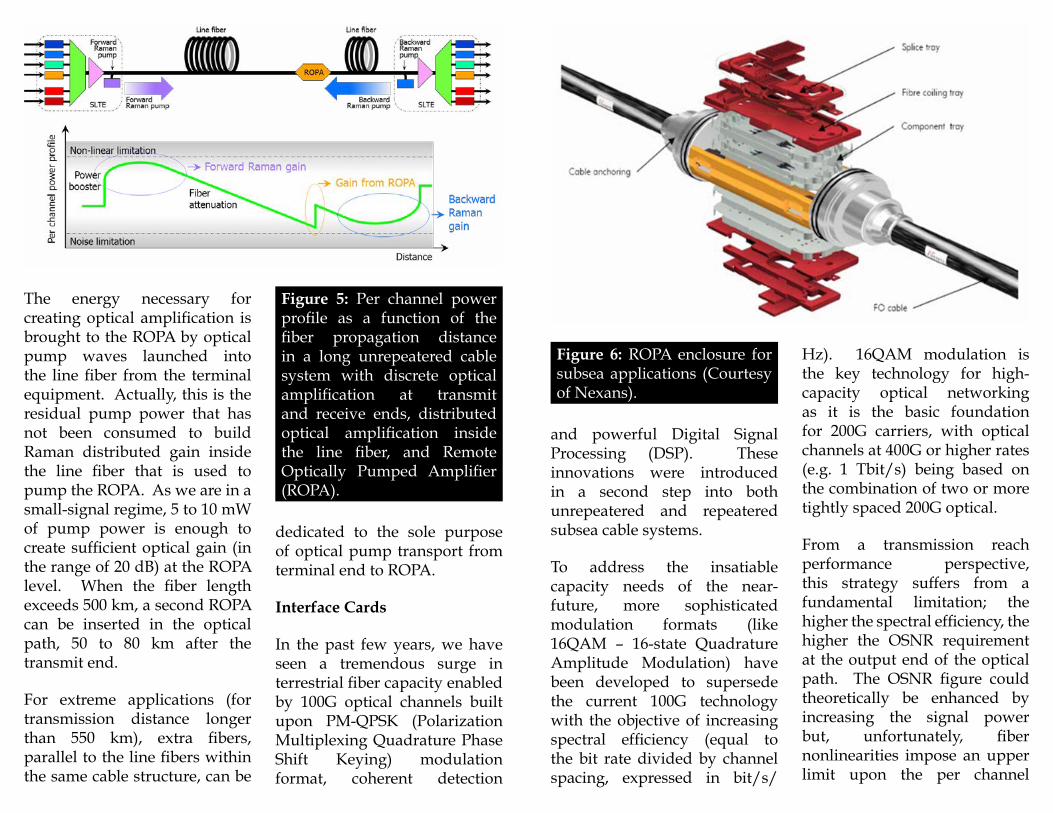

Remote Optically Pumped Amplifier (ROPA)

A ROPA is a very simple sub-system that is typically placed 80 to 150 km ahead of the receive end. This sub-system is based on a few passive optical components that are placed inside an enclosure jointed to the cable. By nature, the ROPA is a fully passive sub-system that requires no remote electrical power feeding from the cable end.

optical amplification as they propagate over long fiber distances. The optical noise imposes a lower limit on the per channel power along the optical fiber.

Parts of nonlinearities in silica optical fiber are caused by the Kerr effect. The Kerr effect describes the dependency of the refractive index of the optical waveguide on the instantaneous optical intensity. The higher the signal power, the higher the nonlinearities and the subsequent distortions that are experienced by the optical signals. Nonlinearities impose an upper limit on the per channel power that can be launched into the optical fiber.

Because of the upper limit for per channel power set by nonlinear effects and the lower limit imposed by minimal OSNR requirement, the per channel optical power profile must fit within some kind of “optical power tunnel” in order to guarantee data integrity along the optical fiber.

To extend unrepeatered reach beyond 300 km, there is no other way than to use distributed optical amplification inside the line fiber; this distributed amplification is offered by

Raman nonlinear effect that turns the line fiber into an optical gain medium when strong optical pump waves, with the appropriate optical frequencies, are launched into the line fiber [2]. Depending on the fiber attenuation and long-term capacity requirements, backward Raman pumping is first implemented when the length of the unrepeatered

Figure 4: Per channel power profile as a function of the fiber propagation distance in a short unrepeatered cable system with discrete EDFA-based optical amplification at transmit and receive ends.

The energy necessary for creating optical amplification is brought to the ROPA by optical pump waves launched into the line fiber from the terminal equipment. Actually, this is the residual pump power that has not been consumed to build Raman distributed gain inside the line fiber that is used to pump the ROPA. As we are in a small-signal regime, 5 to 10 mW of pump power is enough to create sufficient optical gain (in the range of 20 dB) at the ROPA level. When the fiber length exceeds 500 km, a second ROPA can be inserted in the optical path, 50 to 80 km after the transmit end.

For extreme applications (for transmission distance longer than 550 km), extra fibers, parallel to the line fibers within the same cable structure, can be

dedicated to the sole purpose of optical pump transport from terminal end to ROPA.

Interface Cards

In the past few years, we have seen a tremendous surge in terrestrial fiber capacity enabled by 100G optical channels built upon PM-QPSK (Polarization Multiplexing Quadrature Phase Shift Keying) modulation format, coherent detection

and powerful Digital Signal Processing (DSP). These innovations were introduced in a second step into both unrepeatered and repeatered subsea cable systems.

To address the insatiable capacity needs of the near-future, more sophisticated modulation formats (like 16QAM – 16-state Quadrature Amplitude Modulation) have been developed to supersede the current 100G technology with the objective of increasing spectral efficiency (equal to the bit rate divided by channel spacing, expressed in bit/s/

Hz). 16QAM modulation is the key technology for high-capacity optical networking as it is the basic foundation for 200G carriers, with optical channels at 400G or higher rates (e.g. 1 Tbit/s) being based on the combination of two or more tightly spaced 200G optical.

From a transmission reach performance perspective, this strategy suffers from a fundamental limitation; the higher the spectral efficiency, the higher the OSNR requirement at the output end of the optical path. The OSNR figure could theoretically be enhanced by increasing the signal power but, unfortunately, fiber nonlinearities impose an upper limit upon the per channel

Figure 5: Per channel power profile as a function of the fiber propagation distance in a long unrepeatered cable system with discrete optical amplification at transmit and receive ends, distributed optical amplification inside the line fiber, and Remote Optically Pumped Amplifier (ROPA).

Figure 6: ROPA enclosure for subsea applications (Courtesy of Nexans).

power that can be launched into the fiber span.

While the ultimate reach performance is similar between 10G and 100G channel rates (632 and 607 km, respectively, in the work described in [3]), the longest unrepeatered transmission distance reported so far for 200G channels based on 16QAM modulation format is 363 km [4].

Evolution and Conclusion

Today, unrepeatered cable systems can offer 100G transmission distance in excess of 600 km [3] and a cross-sectional capacity of 15 Tbit/s over 410 km [5]. These industry’s leading results were obtained with a 0.16 dB/km fiber offering a 112 µm2 effective area. Improved fibers with lower attenuation and larger effective area [6] are likely to further improve these reach and capacity figures. On the terminal side, Reconfigurable Optical Add Drop Multiplexers (ROADMs), implemented inside cable landing stations, in addition to the associated control plane, are becoming crucial equipment to build a global network with high resiliency against multiple faults.

Moving to network design, longer reach enables all-optical connectivity between points of presence or between datacenters with the wet unrepeatered piece in the middle, instead of the traditional connectivity between beach manholes with expensive interfacing between subsea link and terrestrial networks inside the cable landing stations.

References

[1] Do-il Chang, Philippe Perrier, Herve Fevrier, Tiejun J. Xia, Daniel L. Peterson, Glenn A. Wellbrock, Sergey Ten, Christopher Towery, and Greg Mills, “Unrepeatered 100G Transmission Over 520.6 km of G.652 Fiber and 556.7 km of G.654 Fiber With Commercial Raman DWDM System and Enhanced ROPA,” IEEE Journal of Lightwave Technology, Vol. 33, No. 3, pp. 631-638, February 2015.

[2] Wayne Pelouch, “Raman Amplification: An Enabling Technology for High-Capacity, Long-Haul Transmission,” presented at OFC 2015, Los Angeles, USA, 2015, Tutorial W1C.1.

[3] Xtera’s Press Release, “Ultra-Long Unrepeatered Transmission over 607 km at 100G and 632 km at 10G Enabled by Wise RamanTM Solution and Large Effective Area Ultra-Low Loss Fiber,” March 2015.

[4] Hans Bissessur, Christian

Bastide, Suwimol Dubost, Sophie Etienne, and Dominique Mongardien, “8 Tb/s Unrepeatered Transmission of Real-time Processed 200 Gb/s PDM 16-QAM Over 363 km,” presented at ECOC 2014, Cannes, France, 2014, Paper Tu.1.5.3.

[5] Do-il Chang, Wayne Pelouch, Philippe Perrier, Herve Fevrier, Sergey Ten, Christopher Towery, and Sergejs Makovejs, “150 x 120 Gb/s Unrepeatered Transmission Over 409.6 km of Large Effective Area Fiber with Commercial Raman DWDM System”, Optics Express, Vol. 22, No. 25, December 2014.

[6] Sergejs Makovejs, Clifton C. Roberts, Florence Palacios, Hazel B. Matthews, David A. Lewis, Dana T. Smith, Paul G. Diehl, Jeffery J. Johnson, Joan D. Patterson, Christopher R. Towery, and Sergey Y. Ten, “Record-Low (0.1460 dB/km) Attenuation Ultra-Large Aeff Optical Fiber for Submarine Applications,” presented at OFC 2015, Los Angeles, USA, 2015, PD Paper Th5A.2.

Bertrand Clesca is Head of Global Marketing for Xtera and is based in Paris, France. Bertrand has over twenty five years of experience in the optical t e l e c o m m u n i c a t i o n s industry, having held a number of research, engineering, marketing and sales positions in both small and large organizations.

Bertrand Clesca holds an MSC in Physics and Optical Engineering from Institut d’Optique Graduate School, Orsay (France), an MSC in Telecommunications from Telecom ParisTech (fka Ecole Nationale Supérieure des Télécommunications), Paris (France), and an MBA from Sciences Po (aka Institut d’Etudes Politiques), Paris (France).

The world’s expanding treasure

Celebrating

of SubOptic

30years

Sponsorship and Exhibition Opportunities are now available online and our Call for

Papers will be issued in June 2015

Hosted by

Emerging Subsea Networks

A New DawnThe Era Of High-Speed Capacity Into Ireland

Derek Cassidy

The need to feed the increase in the bandwidth usage –

supported by the increasing development of WEB 2.1 due to the use of video and communication interaction and gaming – has been a driver behind the need to provide 100Gb/s and multiple 100Gb/s DWDM optical systems. These web 2.1 utilities interact with the background service to deliver data, voice and video in both real time and download storage interaction, which has meant that the bandwidth available is being filled quicker and soon Nielsen’s Law of Internet Bandwidth usage may not be applicable anymore.

With this increase in bandwidth demand combined with the ever-increasing use of online commercial & financial services, mobile communication services and data storage has led to the increased need for Data Centres & Hosting.

Ireland, on the periphery of Europe, has become a central location for the establishment of these sites and major players

in the on-line communication sphere; such as Apple, Google, Yahoo, Microsoft and Amazon, which have already established or are establishing a presence to take advantage of the economic environment, location and available educated skilled resource. But all these services and service providers require capacity of high-speed, low latency networks and this is something that Ireland is slowly delivering.

In 2011, with the introduction of the CeltixConnect submarine cable between the UK and Ireland – which offers a Neutral Carrier network design – effectively allows Network Operators their own connection to the UK and onwards to Europe and beyond. With this Neutral Carrier model, Network Operators could run their networks at whatever speed they desire and this was a huge incentive for the

first 100Gb/s networks that connected Ireland to the UK and Europe. The capacity for 100Gb/s optical channels and the networks to carry them was now available and now operational. However, this capacity was in one direction only: eastwards to the UK. The link westwards, towards the US, does not yet have the capacity to deliver 100Gb/s systems.

Ireland has seen the growth of 100Gb/s in Metro and

National networks and has even seen the development of the 500GbE superchannel that enables universities to carry out research and connect with their European counterparts via the Dante network, which delivered this superchannel in collaboration with a major telecommunications company in Ireland. The capacity required within the terrestrial networks has had the neccesary time to build up to offer this increased bandwidth and capacity needed to connect to the outside world, but until now was only available through the neutral carrier model provided by the CeltixConnect submarine cable.

With the drive to deliver fast high capacity bandwidth between Ireland, the US and the UK financial markets, Hibernia Networks were able to meet this demand with their Hibernia Atlantic Submarine cable that directly connected Ireland to the US and the UK that had the available capacity at 40Gbs capability per optical channel within a protected DWDM network design. Hibernia Networks

also delivered the fastest trans-Atlantic interconnect between financial centres. However, they recognised the need to deliver a faster and higher 100Gb/s capacity to meet the needs of the financial markets and other commercial networks.

In 2014 Hibernia Networks announced that they have designed and started the lay the fastest trans-Atlantic cable, Hibernia Express, which will connect the UK directly with the US via Halifax but will also have a connection into Cork. This new cable will deliver high speed capacity between Ireland, the US and the UK at higher speeds and with a capability to deliver 100 x 100Gb/s optical channels or 10Tb/s so that it competes directly with the existing trans-Atlantic cables and will shorten the distance or latency by at least 6ms, something that the Financial Trading companies see as profit.

However, the need to deliver high-speed low-latency optical networks has taken even one step further into the era of superfast networks.

The Arctic Fibre network will deliver 24Tb/s made up of three fibre pairs with a capability of 80 x 100Gb/s optical channels per fibre pair. The new network will directly connect Tokyo to London with two express fibre pairs capable of delivering the design capacity of 24Tb/s and a third fibre pair that will connect the terrestrial networks across Asia, America and Europe with a design capacity of 8Tb/s. This new design will directly connect Ireland to the US, UK and Asia (Tokyo) with low latency that will enable European and Irish financial

markets to connect and trade with their US and Asian markets at a speed that will enable real time trading and will enable Cork to become a cross roads on the trans-Atlantic route.

The Arctic Fibre network will be the first cable directly connecting Europe to Asia and it will do so by having a connection directly into Cork, Ireland. This will enable the development of a fast communication link that will help feed the development of international communications and will enable companies

such as Apple, Microsoft and Facebook to directly connect to their home markets thanks to the increased high capacity that this cable will deliver.

The reality that Cork will be able to connect with Tokyo, Seattle and London via the new superfast optical highway – that is, the Arctic Fibre cable – will enable Cork to develop its international communication hub and promote the Cork Internet Exchange as an independent centre for data exchange and develop Ireland as a European Gateway.

Along with the Hibernia Express cable, the Arctic Fibre network will help create a diverse, fast, low-latency submarine network connecting the US with Ireland with a combined 34Tb/s of capacity with Arctic Fibre, providing 24Tb/s. The two submarine cable systems will provide the needed multiple 100Gb/s optical channel DWDM capacity across the Atlantic.

However, there is another cable with a design capacity of 130 x 100Gb/s or 13Tb/s.

This cable is specifically designed to meet the requirements of the financial and communication markets. The network designers Aqua Comms will bring the cable into service in December 2015. This cable will be an engineered low latency cable capable of delivering 13Tb/s directly into New York from London via Killala in Ireland. It will also be the closest cable to the east coast of the US. This new submarine cable will connect into the existing network provided by its very own CeltixConnect cable that is able to deliver 13Tb/s and, more, to directly connect into the heart of the UK financial networks and onwards into Europe, via the METRO2C Alliance. As the CeltixConnect cable is a 144 fibre cable it can deliver multiples of the design bandwidth that any Trans-Atlantic cable can deliver and is well suited to help deliver the capacity of the new America Europe Connect cable (AEC) to Europe and beyond, at very high speed.

AquaComms will enable financial services, ISPs and large bandwidth hungry

companies to design their networks and use the high-speed bandwidth along with a diverse network design that will deliver communications directly into New York, closer than most other trans-Atlantic cables that connect directly to Ireland. The AEC cable is the cable that can do this.

The bandwidth hungry companies in Ireland who demand diverse high-speed bandwidth services, will now have the AEC cable and the cables being delivered by Hibernia Networks and Arctic Fibre to provide their capacity and high-speed requirements directly to the US. These three cables along with the other existing submarine cables, CeltixConnect and Hibernia Atlantic, will enable Ireland to become a high bandwidth high capacity network capable of delivering capacity from Europe to the west coast and east coast of the US and specifically to Asia with Arctic Fibre.

However, this does not finish here. The Ireland-France Submarine cable is a new development from some of the Arctic Fibre shareholders

through a new entity, Ireland-France Subsea Cable Limited, which will build a link directly into Europe – into Europe via France. As the cable will connect Cork to Lannion, it will deliver high bandwidth with a design capacity of multiple Tb/s with low latency, directly into France, bypassing the UK. This will enable quick access to the European markets, negating the need to go via the UK. This new cable will deliver access from Paris or Berlin to Tokyo or London directly via Cork. But the ability to reach Tokyo and the Asian markets from this cable will help Cork and Ireland to become a new European hub for high bandwidth service, which will help deliver the capacity needed to feed the growing economies of Ireland, the UK and Europe by have directly connected cables to London, Lannion-Paris, Seattle and Tokyo.

Ireland is re-entering the world of international communications. Once it was the gateway to the world in the telegraphic era, now with the development

of these new international superfast submarine cables Ireland is again becoming the international gateway in the new high-speed optical communication era.

The availability of high-speed, low latency international links between Ireland and the world is here!

Derek Cassidy is from Dublin, Ireland. He has worked for 23 years in the telecommunications industry of which 21 years have been spent dealing with optical terrestrial systems and submarine networks. He works for BT in their Networks and Optical Engineering division. He is Chairman of the Irish Communications Research Group, a voluntary organisation dedicated to the promotion, protection and research of Ireland’s communication heritage. He is a Chartered Engineer with the IET and is also a member of the IEEE and Engineers Ireland, and has Degrees in Physics/Optical Engineering, Structural/Mechanical Engineering and Engineering Design and has Masters Degrees in Structural, Mechanical, Forensic Engineering and Optical Engineering. He is currently researching the Communication History of Ireland and is doing a PhD research programme in the field of Optical Engineering.

Local Partners KeyTo Exploiting Burgeoning International Connectivity Demands In Africa

Mike Last

Unlocking ‘Opportunity Africa’

Without doubt, Africa is an extremely dynamic marketplace and an attractive business opportunity for a wide variety of organisations involved in ICT. This, in turn, is driving rapid growth in demand from businesses and individuals for reliable, affordable international bandwidth and improvements in reach, capacity and quality of connectivity networks serving the continent.

In order to fully realise this potential, businesses have to overcome the myriad of challenges that exist in addressing a diverse, 54-country strong continent, where local expertise, market knowledge, understanding of the regulatory environment and local contacts are all vital. So too is the ability to establish long-term, mutually-beneficial partnerships, where both parties have the ability and mindset to work together to support each other in continuing to meet the rapidly changing needs and demands of consumers

within a young and extremely dynamic marketplace.

Home to more than 1 billion people and made up of some 54 countries, Africa is a very diverse continent. Local knowledge, contacts, experience and expertise are invaluable in ensuring the reliable and cost-effective delivery of high-quality, international connectivity. For international carriers and internet service providers (ISPs) seeking to take advantage of the growing capacity market into, out of and within Africa, the advantages of partnering with an established and trusted pan-African organisation are significant.

Transformational

The way in which businesses in Africa operate and individuals go about their daily lives has been transformed by improved international connectivity, enhanced ICT infrastructure, more affordable high-performance mobile devices and prodigious growth in mobile, internet and data services.

Africa in numbers

>1.1billion – population

4.5million – internet users in 20001

298million– internet users in 20142

X4 - Africa’s mobile phone market predicted to almost quadruple in value between 2013 and 20203

16 – submarine cables serving sub-Saharan Africa (only two at the beginning of 2009)

>30Tbps – total capacity of submarine cables4

586,707 route kilometres (km) - operational terrestrial transmission network5

981,370km – total inventory of operational, under construction, planned and proposed terrestrial fibre optic

and microwave networks at the end of 20146

>x2 - total inventory of terrestrial transmission networks has more than doubled in the last five years7

44% - of the population of Sub-Saharan Africa was within 25km of an operational fibre optic network node in June

2014 (up from 30.8% in 2010) 8

52.3% - within 25km of an operational fibre optic network node once the fibre network which is currently under construction, planned and proposed enters service9

1 Internet World Stats, 2014 2 Internet World Stats, 2014 3 Manifest Mind LLC, 20134 Many Possibilities, 20155 Africa Bandwidth Maps, 20156 Africa Bandwidth Maps, 20157 Africa Bandwidth Maps, 20158 Africa Bandwidth Maps, 20159 Africa Bandwidth Maps, 2015

These advances have helped businesses improve efficiency and productivity, opened up new markets and catalyzed the creation of many new companies. Greater access to mobile broadband is continuing to revolutionise

how individuals access information, how money is handled and transferred, and has also led to phenomenal growth in uptake of internet-enabled applications such as social networking, online gaming and the streaming of music, films and video.

Virtuous connectivity circle

To meet the burgeoning demand for reliable, high-bandwidth international connectivity, the number, capacity and reliability of submarine cable systems and terrestrial fibre networks serving Africa has grown, and continues to grow, dramatically. At the beginning of 2009, just two international cables served sub-Saharan Africa. There are now 16, including a number that have been upgraded at least once to meet the growing customer demand, providing a theoretical design capacity well in excess of 30Tbps.

Investment in Africa’s terrestrial network capacity continues to increase too, catalyzed by the continent’s improved submarine capacity and rising demand from individuals and businesses wanting to take advantage of the many products and services made possible by access to reliable, affordable international connectivity.

According to Hamilton Research, Africa’s total

inventory of terrestrial transmission networks more than doubled in the last five years – from 278,056km in 2009 to 564,091km at the end of 2014. Further investment will continue to improve connectivity significantly as the total inventory of terrestrial fibre optic and microwave networks which are operational, under construction, planned or proposed was 981,370km at the end of 2014. When all of this enters service, 52 percent of the population of Sub-Saharan Africa will be within 25km of an operational fibre optic network node – compared to just 31 percent in 2010.

Partnering with experienced, regional experts

Keeping up with the pace and scope of the ongoing changes in submarine and terrestrial connectivity supply as well as the rapidly evolving demand from end-users within these diverse African markets, is a herculean challenge.

For Telcos and ISPs, business success is dependent upon

the ability to maintain an appropriate and cost-effective balance of network capacity and quality; and this can only be determined through continual review and up-to-date local expertise and knowledge of the dynamics regarding network reach, capacity and performance.

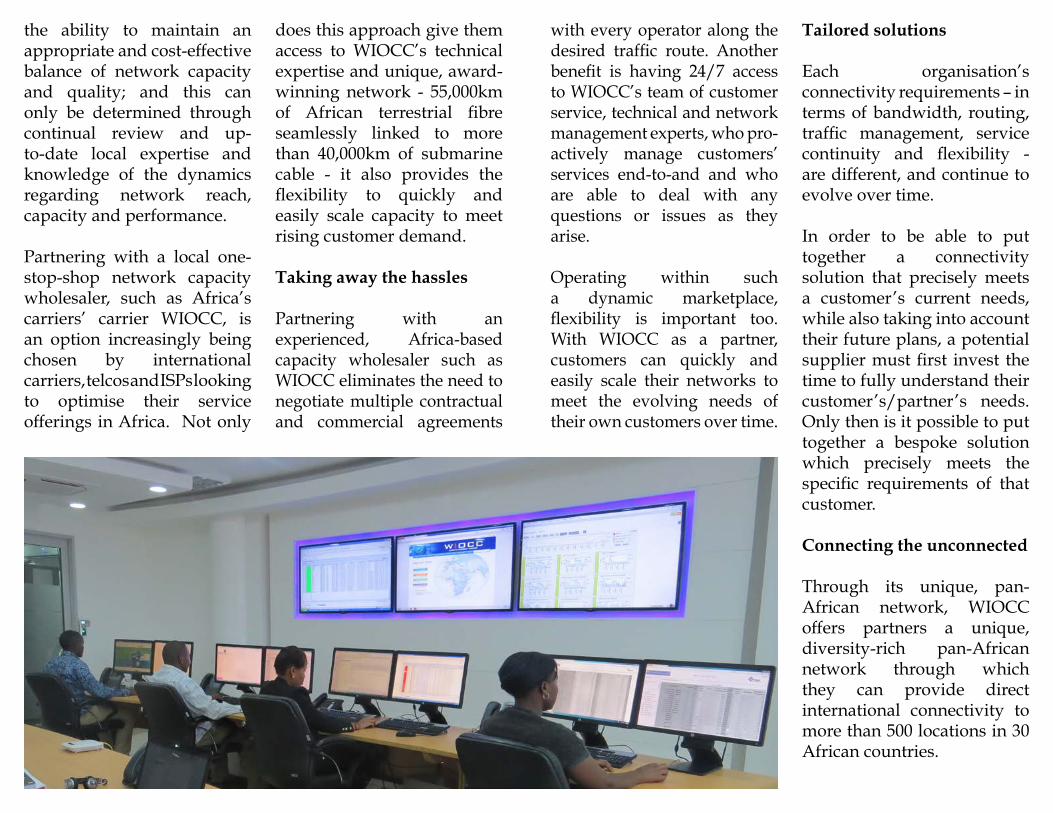

Partnering with a local one-stop-shop network capacity wholesaler, such as Africa’s carriers’ carrier WIOCC, is an option increasingly being chosen by international carriers, telcos and ISPs looking to optimise their service offerings in Africa. Not only

does this approach give them access to WIOCC’s technical expertise and unique, award-winning network - 55,000km of African terrestrial fibre seamlessly linked to more than 40,000km of submarine cable - it also provides the flexibility to quickly and easily scale capacity to meet rising customer demand.

Taking away the hassles

Partnering with an experienced, Africa-based capacity wholesaler such as WIOCC eliminates the need to negotiate multiple contractual and commercial agreements

with every operator along the desired traffic route. Another benefit is having 24/7 access to WIOCC’s team of customer service, technical and network management experts, who pro-actively manage customers’ services end-to-and and who are able to deal with any questions or issues as they arise.

Operating within such a dynamic marketplace, flexibility is important too. With WIOCC as a partner, customers can quickly and easily scale their networks to meet the evolving needs of their own customers over time.

Tailored solutions

Each organisation’s connectivity requirements – in terms of bandwidth, routing, traffic management, service continuity and flexibility - are different, and continue to evolve over time.

In order to be able to put together a connectivity solution that precisely meets a customer’s current needs, while also taking into account their future plans, a potential supplier must first invest the time to fully understand their customer’s/partner’s needs. Only then is it possible to put together a bespoke solution which precisely meets the specific requirements of that customer.

Connecting the unconnected

Through its unique, pan-African network, WIOCC offers partners a unique, diversity-rich pan-African network through which they can provide direct international connectivity to more than 500 locations in 30 African countries.

This network is helping to bring affordable, high-capacity international connectivity to landlocked countries - such as Zimbabwe, Malawi, Zambia, Botswana, Burundi and Lesotho – as well as to Somalia, which was until recently one of the last ‘corners’ of Africa without direct fibre-optic connectivity. The significance of this last achievement has been recognised by a number of recent industry awards: in November 2014 WIOCC won the Best Network Improvement and Best Connectivity Solutions for Africa awards at the seventh annual AfricaCom Awards and has been shortlisted for the Social Contribution award at the Total Telecom Africa Awards – winners will be announced at the end of May 2015.

In November 2013, after six years’ hard work in the face of extreme adversity (including piracy, shore-based unrest, etc.), WIOCC landed the >10Tbps capacity EASSy submarine cable on the coast of Somalia. The cable was connected to a brand new landing station and state-of-the-art data centre in Mogadishu, and the first

international circuits went live in February 2014.

Dalkom Somalia are now extending fibre-optic connectivity into Mogadishu, allowing an ever-increasing number of residents and businesses to access direct, high-capacity, low-latency, international fibre-optic connectivity for the first time.

Enhanced access to information is helping transform life in Somalia, encouraging renewed investment from the diaspora and the international business community, and creating a platform for sustainable economic growth.

Latency reductions of up to 80 percent dramatically af-fected end-users’ experience. According to the BBC1, the speed improvement was like “the difference between day and night”.

Other areas now benefiting include education, where previously impoverished classrooms are increasingly supplemented by online

1 BBC, 2014

libraries and digital classrooms, and improved public access to Government services - such as E-passports, E-National IDs and E-birth and death registrations.

Capacity take-up in Moga-dishu exceeded expectations and is helping drive further cost reductions and catalyse improvements in terrestrial infrastructure. Mobile uptake and internet usage are both increasing, while telecoms companies, internet service providers and IT companies are launching new services and capabilities to strengthen their customer base and in-crease revenues.

Other businesses are benefitting from more cost-effective access to the internet and the wide range of advanced service offerings facilitated by improved international connectivity. The resultant creation of new jobs is providing a very welcome boost to individuals and the Somalia economy.

Opportunity Africa

As businesses and individuals

Mike Last is the Director of Marketing & International Business Development at WIOCC.

throughout Africa become increasingly used to and dependent upon ever-more data-rich applications, demand for reliable, affordable, high-capacity international connectivity into, out of and within the continent will continue to rise.

Africa is a complex and diverse continent with the challenge of many different markets, regulatory systems and operating environments. However, with the right partner, the business opportunities are well worth the effort.

Rethinking The Submarine Network

Arnaud Leroy

The replacement of voice traffic by data distribution is driving

the need for greater capacity cable connections working at faster speeds and with more efficiency. New wet plant is emerging designed with larger spectrum and more fiber pairs to serve new data centers with ultra-high capacity. At the same time, existing wet plant designed with legacy technology needs to support increased design capacity, improved connectivity and flexibility.

Ever-rising demand brings capacity constraints

The new systems reflect the insatiable demand for increased information exchange, swifter transmission and more flexible digital traffic flow – driven by “Big Data” and enhanced user experiences. In addition, this is driving the need to upgrade inter-continental and regional cable system capacity and reach.

Data flows between these centers are growing rapidly as content providers strive to meet the demand for content

steaming and distribution, commerce, search, gaming and sharing. The next driver might be the Internet of Things, where embedded connectivity transfers data between connected devices.

All of this creates a need for longer reach and higher capacity on inter-continental and regional cable grids.

Industry-first transoceanic node of 240 Tb/s

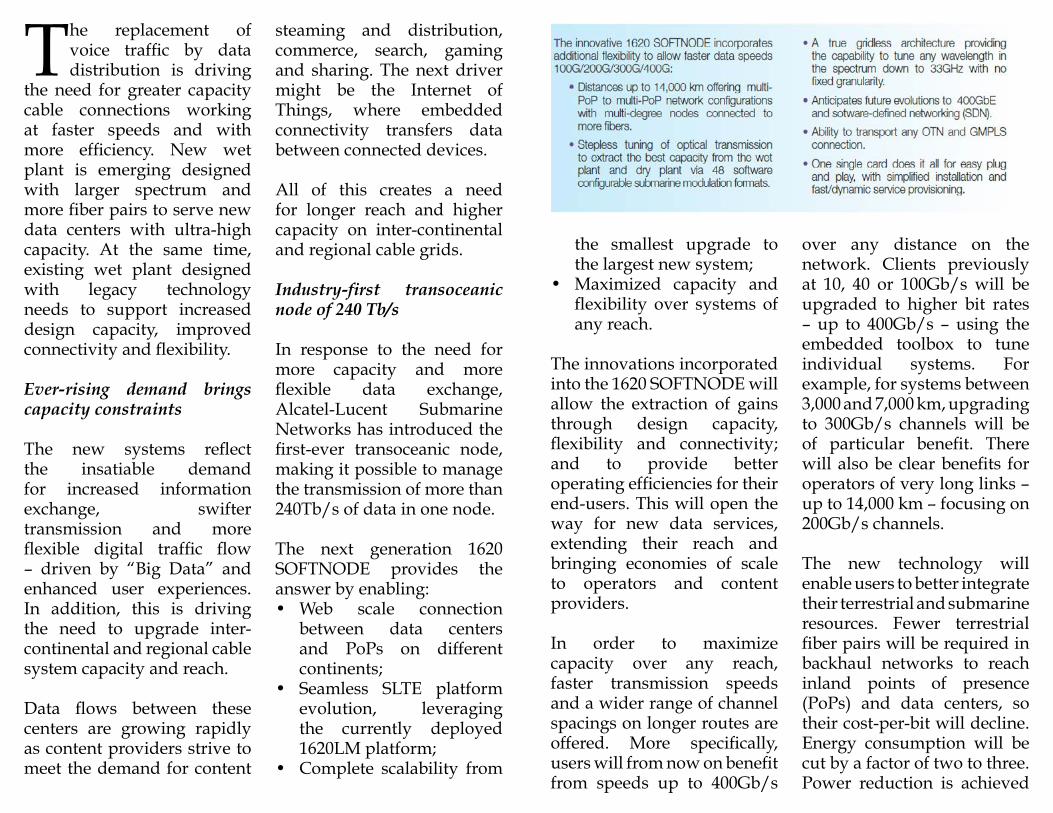

In response to the need for more capacity and more flexible data exchange, Alcatel-Lucent Submarine Networks has introduced the first-ever transoceanic node, making it possible to manage the transmission of more than 240Tb/s of data in one node.

The next generation 1620 SOFTNODE provides the answer by enabling:• Web scale connection

between data centers and PoPs on different continents;

• Seamless SLTE platform evolution, leveraging the currently deployed 1620LM platform;

• Complete scalability from

the smallest upgrade to the largest new system;

• Maximized capacity and flexibility over systems of any reach.

The innovations incorporated into the 1620 SOFTNODE will allow the extraction of gains through design capacity, flexibility and connectivity; and to provide better operating efficiencies for their end-users. This will open the way for new data services, extending their reach and bringing economies of scale to operators and content providers.

In order to maximize capacity over any reach, faster transmission speeds and a wider range of channel spacings on longer routes are offered. More specifically, users will from now on benefit from speeds up to 400Gb/s

over any distance on the network. Clients previously at 10, 40 or 100Gb/s will be upgraded to higher bit rates – up to 400Gb/s – using the embedded toolbox to tune individual systems. For example, for systems between 3,000 and 7,000 km, upgrading to 300Gb/s channels will be of particular benefit. There will also be clear benefits for operators of very long links – up to 14,000 km – focusing on 200Gb/s channels.

The new technology will enable users to better integrate their terrestrial and submarine resources. Fewer terrestrial fiber pairs will be required in backhaul networks to reach inland points of presence (PoPs) and data centers, so their cost-per-bit will decline. Energy consumption will be cut by a factor of two to three. Power reduction is achieved

through connectivity enhancements between PoPs, drawing on more efficient terminal/repeater technology and lower consumption per bit, as well as an innovative transversal ventilation system for the 1620 SOFTNODE providing faster cooling of the equipment and a greener footprint overall.

The flexibility offered by the 1620 SOFTNODE proprietary spectrum engineering allows bit rates of wavelengths to be tuned according to each specific application. For example, 400Gb/s for regional use and 300Gb/s for transoceanic transit; the variable bit rates are optimized by using a single line card. Client interfaces are provided by a selection of separate client interface modules. While the single line card provides the flexibility to use 100, 200, 300 and 400Gb/s transmission, it also provides a full set of tools to further tune the transmission performance for any given link. Transmission is truly gridless – it does not rely on any grid granularity through the entire spectrum. Existing cables will benefit from

improved spectral efficiency of the 1620 SOFTNODE by concentrating data flow into the most efficient grid down to 33GHz. This is achieved by optimizing multiple modulation formats and the use of spectrum engineering tools. SOFTNODE also enables optimization of terrestrial backhaul networks by reducing the required number of fiber pairs to extend transoceanic cap city to inland PoPs and data centers. For example, a transoceanic link may be dimensioned for N fiber pairs at Mx200G, while the terrestrial backhaul can be dimensioned at N/2 fiber pairs carrying Mx400G.