dpp: nepal: improving access to finance sector ... report project number: 40558-012 july 2012...

TRANSCRIPT

Workshop Report

Project Number: 40558-012 July 2012

Improving Access to Finance Sector Development Program Workshop Seminar on Access to Finance

a

ASIAN DEVELOPMENT BANK

Improving Access to Finance Sector Development Program Workshop Seminar on Access to Finance

July 17, 2012

Workshop Seminar Report

Organized by Ministry of Finance

Asian Development Bank In Association with

National Banking Training Institute August, 2012

b

ASIAN DEVELOPMENT BANK: TA 7777 Improving Access to Finance Sector Development Program

Workshop Seminar on Access to Finance July 17, 2012

ADB/TA Team

1. Ms. Mayumi Ozaki, Finance Specialist,

2. Mr. David Lucock, Team Leader

3. Dr. Purushottam Shrestha, National Team leader

Microfinance Development Specialist.

4. Mr. Normand Arsenault, Microfinance MIS Specialist

5. Mr. Ramesh Nath Gongal, Mapping and Survey Coordinator

6. Ms. Pramila Shrestha, Gender and Social Development Specialist.

c

ABBREVIATIONS ADB : Asian Development Bank

CIB : Credit Information Bureau

CMF : Center for Microfinance

DEPROSC/N : Development Project Service Center/Nepal

DSLP : Deprived Sector Lending Program

EAFS : Enhancing Access to Financial Services

FINGO : Financial Intermediary Non government Organization

IAFSDP : Improving Access to Finance Sector Development Program

IME : International Money Express

IPO : Initial Public Offering

MF : Microfinance

MFDB : Microfinance Development Bank

MFIs : Microfinance Institutions

MIFAN : Microfinance Association of Nepal

MIS : Management Information

MoF : Ministry of Finance

NACCFL : Nepal Agriculture Cooperative Central Federation Limited

NBTI : National Banking Training Institute

NEAT : Nepal Economic Agriculture and Trade Activity

NEFSCUN : Nepal Federation of Savings and Credit Co‐operative Unions

NGOs : Non Government Organizations

NRB : Nepal Rastra Bank

NRM : Nepal Resident Mission

PDAs : Personal Digital Assistants

RFSDCP : Rural Finance Sector Development Cluster Program

RMDC : Rural Microfinance Development Centre

SACCOs : Saving and Credit Cooperative Societies

SFDB : Small Farmers Development Bank

SHG : Self‐Help Group

SRG : Self Reliant Group

UNCDF : United Nations Capital Development Fund

d

Contents

1. INTRODUCTION..............................................................................................................................1

1.1 Background .........................................................................................................................1

1.2 Objectives ...........................................................................................................................1

1.3 Expected Outcomes............................................................................................................1

1.4 Participants .........................................................................................................................2

1.5 Venue..................................................................................................................................2

2. OPENING SESSION........................................................................................................................2

2.1 Key note Address by Mr. Gopal Prasad Kaphle, Deputy Governor, Nepal Rastra Bank ...2

2.2 ADB Policy on Access to Finance by Mr. K. Yokoyama, Country Director of Nepal Resident Mission, Asian Development Bank ......................................................................3

2.3 Welcome Speech by Mr. Baikuntha Aryal, Joint Secretary of Ministry of Finance.............3

3. PAPER PRESNTATION SESSION.................................................................................................4

3.1 First Session: Survey Report on Access to Finance Mr. Ramesh Nath Gongal ................4

3.2 (a) Second Session: Access to Financial Services in the Hills and Mountain Areas .........7

3.3 (b) Role of Microfinance Institutions in Mobile and Branchless Banking in the Hill and

Mountain Areas ...................................................................................................................8

3.4 Third Session: Outline of Supervision System for MFIs ...................................................11

3.5 Wrap up of the Workshop Seminar...................................................................................15

3.6 Outcomes ..........................................................................................................................17

3.7 Conclusion ........................................................................................................................17

Annexes

Photos

1

ASIAN DEVELOPMENT BANK: TA 7777

Improving Access to Finance Sector Development Program Workshop Seminar on Access to Finance

July 17, 2012 1. INTRODUCTION

1.1 Background

The Government of Nepal recognizes that access to finance is critical to the development of the country’s economy. Nepal Rastra Bank has introduced deprived sector directed lending programs, mandated banks to open branches outside of the Kathmandu valley, and has created specialized wholesale and retail financial institutions in an effort to expand the outreach of financial services. Although the number of financial institutions has grown rapidly, a significant proportion of the country’s population is still constrained in accessing financial services. The Three Year Plan Approach Paper (2010/11 – 2012/13) of Government of Nepal is committed to a major reform program in financial sector. Therefore a study on Access to Finance was conducted under PPTA No. 7777-NEP through the financial assistance of Asian Development Bank (Annex-1) and agency support of Ministry of Finance and Nepal Rastra Bank.

1.2 Objectives

The objectives of the workshop were to disseminate major findings of the technical assistance consultancy including the access to finance survey conducted through the consultancy and seek feedback, comments and suggestions concerning financial services in the hill and mountain areas and the policy and regulatory environment needed to facilitate the expansion of microfinancial services. Accordingly the workshop discussed:

Findings of the access to finance survey

Ways to improve access to financial services in hill regions

Regulation and supervision of microfinancial services (annex 2) 1.3 Expected Outcomes

The workshop seminar is expected to have following outcomes at the end.

Better understanding of how to improve access to financial services in hill and mountain areas, and

Better understanding of the regulation and supervision needs and provide enabling policy environment for access to finance.

2

1.4 Participants

The participants included representatives of the Government, Nepal Rastra Bank, Commercial Banks, Development Banks, Microfinance Development Banks, Saving and Credit Cooperative Societies, Financial Intermediary Nongovernmental Organizations, Financial Associations, Nepal Federation of Savings and Credit Cooperative Unions Limited, representatives from Asian Development Bank, World Bank, Enhancing Access to Financial Services, International Finance Corporation, National and International Non-governmental Organizations and other related stakeholders. Altogether 63 representatives participated in the workshop seminar (Annex-3).

1.5 Venue

The workshop Seminar was held on July 17, 2012, in Hotel Shangrila Lazimpat Kathmandu between 8:30 am and 1:30 p.m. in association with National Banking Training Institute (NBTI).

2. OPENING SESSION 2.1 Key note Address by Mr. Gopal Prasad Kaphle, Deputy Governor, Nepal Rastra

Bank

Mr. Gopal Prasad Kaphle in his key note address expressed the matter of satisfaction to be able to continue the cooperation between Nepal and Asian Development Bank. Over a period of more than four decades, the cooperation between Nepal and the ADB has expanded to many important areas of Nepal’s development needs, including important policy reforms, development of infrastructure facilities, agriculture and rural development, and development of the social sectors. As such the ADB has evolved as a key development partner of Nepal since 1968 and continues to support reforms and provide policy advice, technical assistance, and development financing.

Besides these areas of cooperation, the ADB has recently opened up its avenues to support the inclusive development needs of Nepal through projects such as improving access to finance sector development program. The efforts of ADB through its various aids and grants programs targeted towards reducing poverty and improving rural and agricultural financing are really commendable and the recent areas of cooperation on improving access of financial services in Nepal, particularly in rural areas would further enhance our areas of cooperation.

We all know that micro financing is basically a pro-poor program. The institutions and the human resource involved in micro-financing are required to be service oriented and fully committed to their jobs. Lack of fund is another concern for micro-financing institutions as they face paucity of owned funds so as to move in their growth path. In our context, poverty and deprivation are basically found in rural and remote areas. While remoteness and absence of physical infrastructure make it very difficult to operate micro-financing programs in such areas and it is a real challenge to microfinance operators as well as policy making and implementing agencies, the operational and financial viability of these institutions for the long run sustainability of those institutions is another challenge. As such, along with many credit plus activities, proper and continued development of human resource conducive to the micro-financing jobs is mostly warranted.

As today’s workshop is focused on access to finance in Nepal, I am confident that the workshop would highlight on many fields of our endeavors pertaining to access of our rural and poor people

3

to finance, status of microfinance, its expansion and scope; and regulatory and supervisory issues on microfinance.

The speaker expressed confidence that the present workshop would contribute to enhance our knowledge and provide suggestions and policy inputs regarding improving access of finance and needs for a prudent and sustainable micro-financial framework that would help achieve inclusive development of the country (Annex-4).

2.2 ADB Policy on Access to Finance by Mr. K. Yokoyama, Country Director of Nepal

Resident Mission, Asian Development Bank

Mr. Yokoyama presented the ADB Policy on Access to Finance and stated that access to financial services is an essential social infrastructure to channel resources to productive sectors to support the sustainable economic growth. Access to reliable financial services is crucial for the poor to capture economic opportunities, and make sustainable improvements in their social and economic wellbeing. Increased financial intermediation will enable resources to flow to the rural sector, giving better opportunities for rural development. Experiences in microfinance in many countries including Nepal show that improved access to finance is effective for empowerment of women.

ADB has a long partnership with the Government of Nepal in assisting the financial sector development. ADB has provided a loan and grant assistances for the establishment of a microfinance wholesale apex organization, institutional reform and strengthening of key rural finance institutions, enhancement of supervision and regulation of microfinance institutions and improved access to financial services to the disadvantaged hills and mountain areas. ADB initiated a technical assistance project on improving access to finance in October 2011 to review the current status of access to finance in Nepal, and develop practical strategies to further enhance access to reliable institutional financial services especially in the hills and mountain areas with the use of technologies. For this purpose, the project conducted a comprehensive access to finance survey. The findings of the survey will be presented later today.

Nepal’s financial sector reached to a certain maturity and it may be the right time to review the current status of the sector and visualize the future course of actions to enhance quality, outreach, and diversity of financial services especially to poor and vulnerable people.

Mr. Yokoyama mentioned that today’s workshop is to discuss with the policy makers and practitioners of the financial sector strategies to develop a sound access to finance sector for greater financial outreach and stronger private sector participation. Finally, he requested the participants actively participate in the workshop and expresses wishes for fruitful discussions. (Annex-5)

2.3 Welcome Speech by Mr. Baikuntha Aryal, Joint Secretary of Ministry of Finance

Mr. Aryal welcomed all distinguished guests and participants present at the workshop seminar on behalf of the organizer and host institution.

Addressing the function Mr. Aryal stated that the Government of Nepal is taking microfinance institutions as a tool for reaching to the poorest of the poor section of the country. Financial services are more or less concentrated in the city areas and in the more accessible and facilitated areas and microfinance institutions in some way or the other can reach to very remote areas and reach to the poorest of the poor section in the country. But again there are some kinds of problems within the microfinance institutions and within access to services. They need to

4

enhance corporate governance, reporting systems, and capacity development to reach the poor and disadvantaged people.

Even though we have some kind of financial access there is still a high risk that at some time deposit and all the financial services could collapse. So, the findings of the survey report and findings of this consulting team would be beneficial for discussion and finding the gaps how we can intervene and how we can inject some of the policy issues so that financing to the rural people would be more strengthened and lending and deposits and all those financial services would run appropriately in the local level: this is one issue, and strengthening of microfinance institutions is another key issue Although the Nepal Rastra Bank is the lead regulator for microfinance institutions, given the capacity of Nepal Rastra bank and given the number of large and huge number of financial institutions in the country, Nepal Rastra Bank alone might not be able to monitor and regulate all the microfinance institutions in the country. So the Government is thinking to promulgate a separate Act which is in the draft stage. Mr. Aryal expected that, the finding of the study conducted on “Access to Finance” would be beneficial to inject new policy issues to improve the microfinance sector in Nepal (Annex-6).

3. PAPER PRESNTATION SESSION 3.1 First Session: Survey Report on Access to Finance

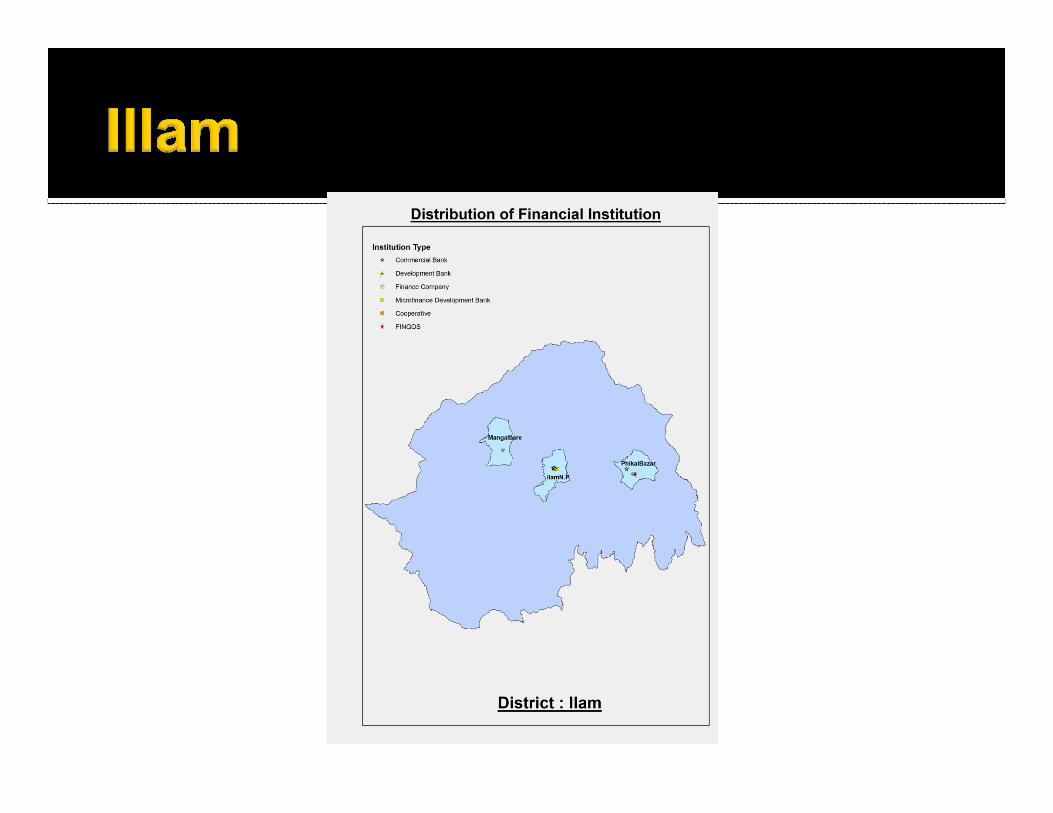

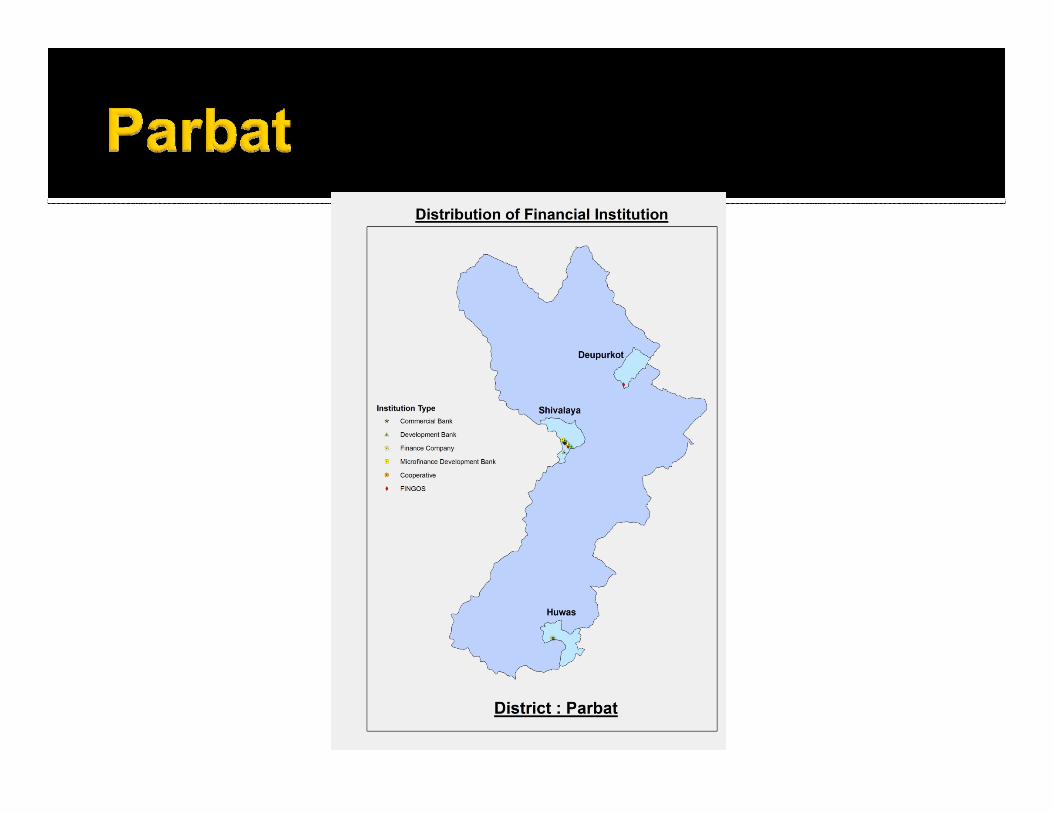

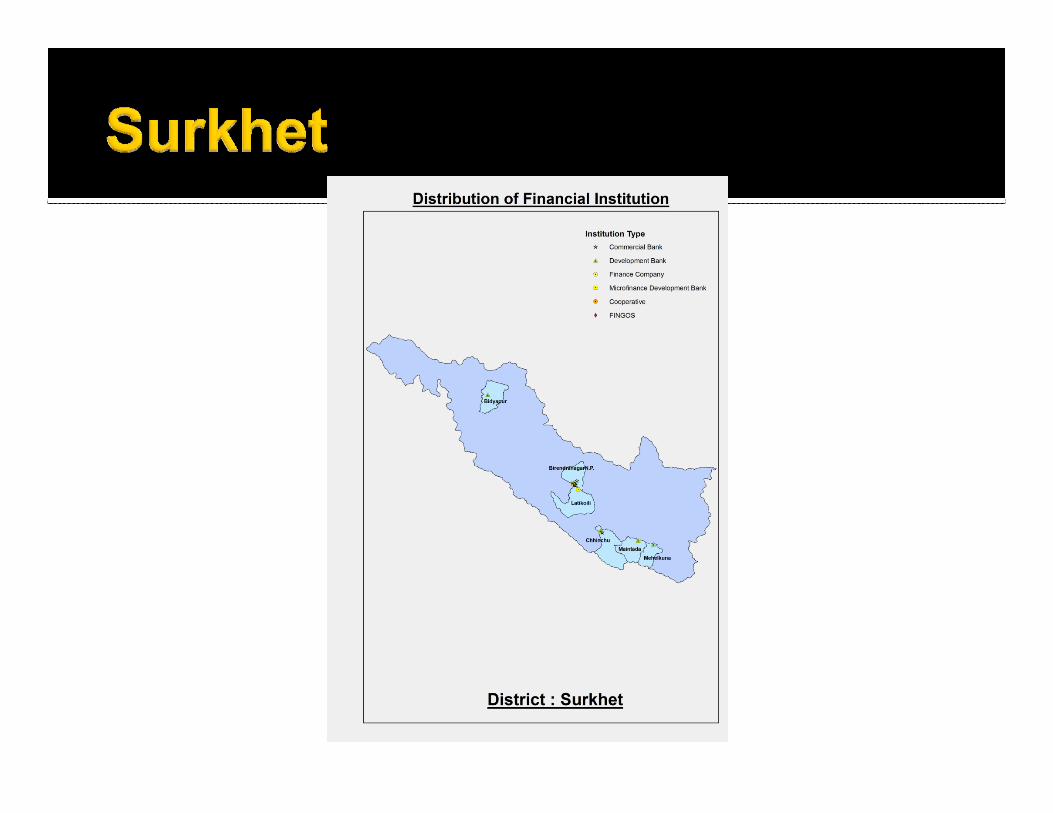

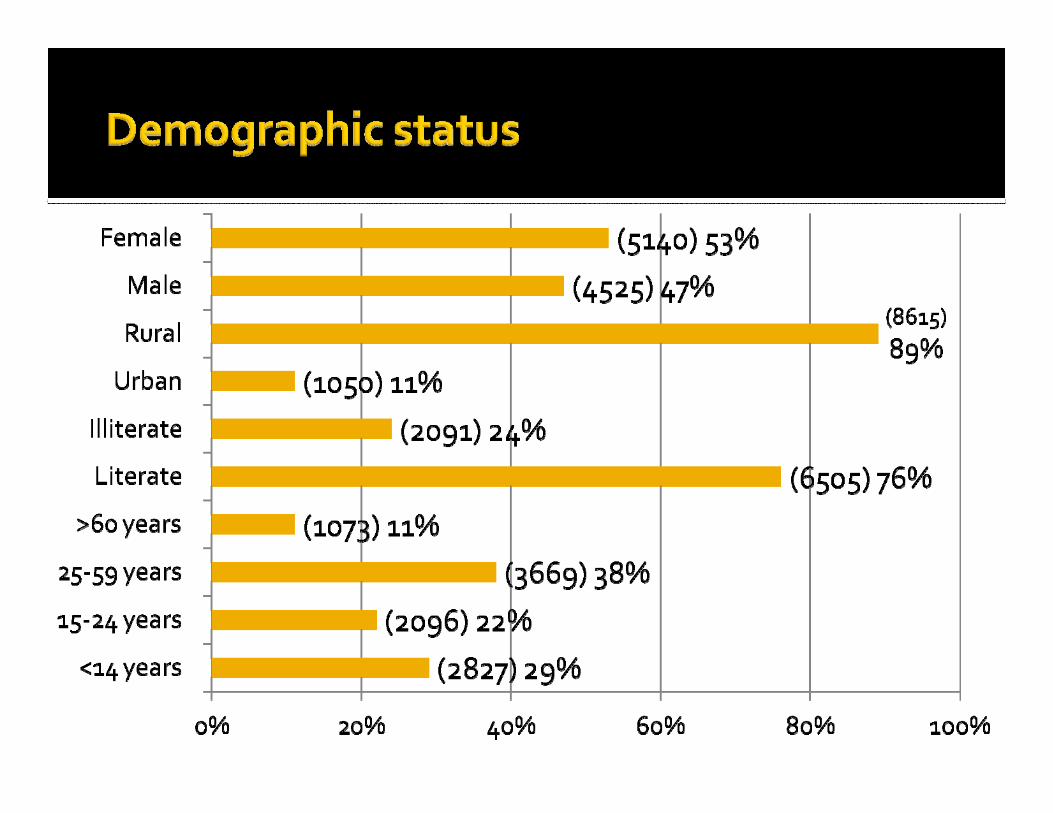

Mr. Ramesh Nath Gongal , Mapping Survey Coordinator presented the findings of the Survey on Access to Finance. The session was chaired by Mr. Gopal Prasad Kaphle, Deputy Governor of Nepal Rastra Bank. Mr. Gongal mentioned that the survey was conducted in 8 districts covering 8 domains hill/mountains and terai from four development regions of Nepal. The presentation covered the objectives, sampling methodology, survey administration, data analysis of the survey. Maps were presented showing the districts covered in the survey and also the location of financial institutions in the surveyed districts. The presentation covered the major financial service providers, such as, formal, semi-formal and informal sectors. The 397 branches of the financial institutions were located in 73 VDCs focused mostly in urban areas. The presentation covered the demographic status of the surveyed households. Fifty-three percent of the respondents are female, 89 percent of the respondents are from rural areas, 76 percent of the respondents are literate and 38 of the respondents are between 25 to 59 Years of age. With regards to average household income of the poorest 20 percent of the households, it had an average monthly household income of Rs. 4,263 and the richest 20 percent of the households reported an average monthly income of Rs.39,369. Access to financial services by rural and urban areas indicated that about 67 percent of the households have deposit accounts (66 percent rural, 71 percent urban). About 35 percent borrow (35 percent rural and 31 percent urban). About 33 percent have access to remittance services (35 percent rural and 18 percent urban). Only 16 percent of the households have access to insurance services (30 percent urban and 14 percent rural). Savings are the most used financial services and insurance services the least used financial services.

Access to financial services by income quintile group, shows that there is a big gap in access to financial services between poor quintile groups and rich quintile groups in accessing financial services. Rich quintile groups enjoy higher access to financial services. Only 47 percent of poor quintile group have savings, 27 percent have loans, 20 percent have remittances and 6 percent have insurance services.

5

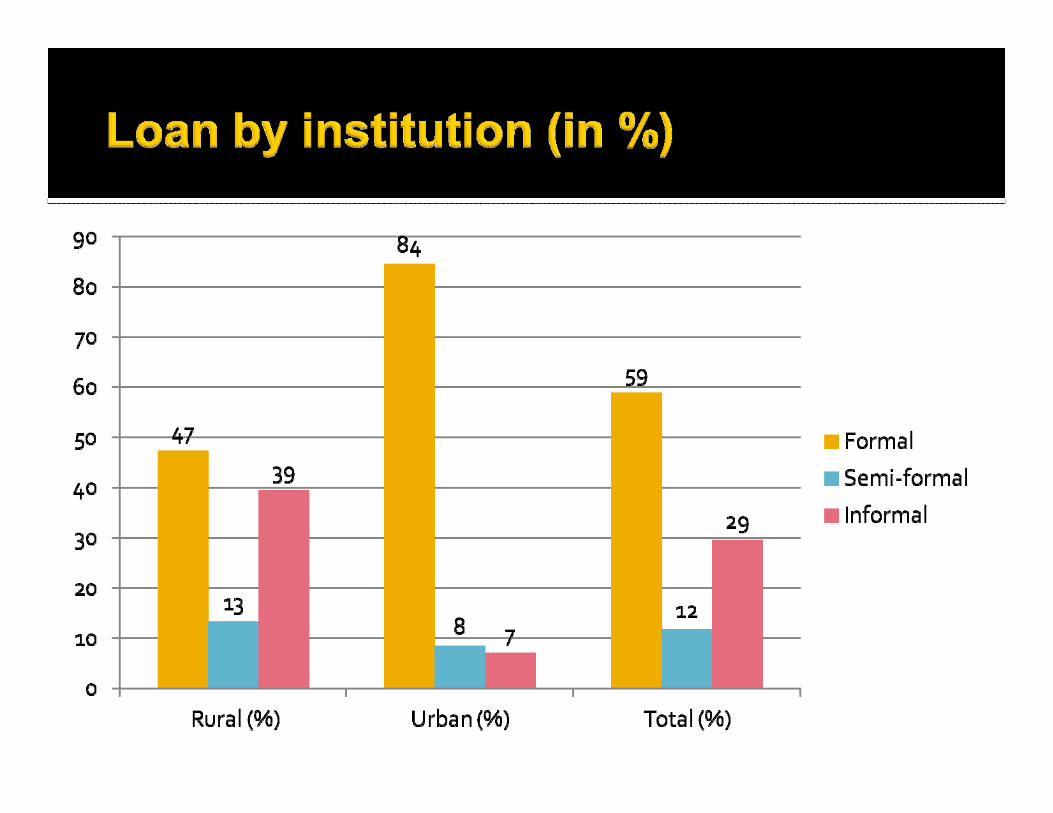

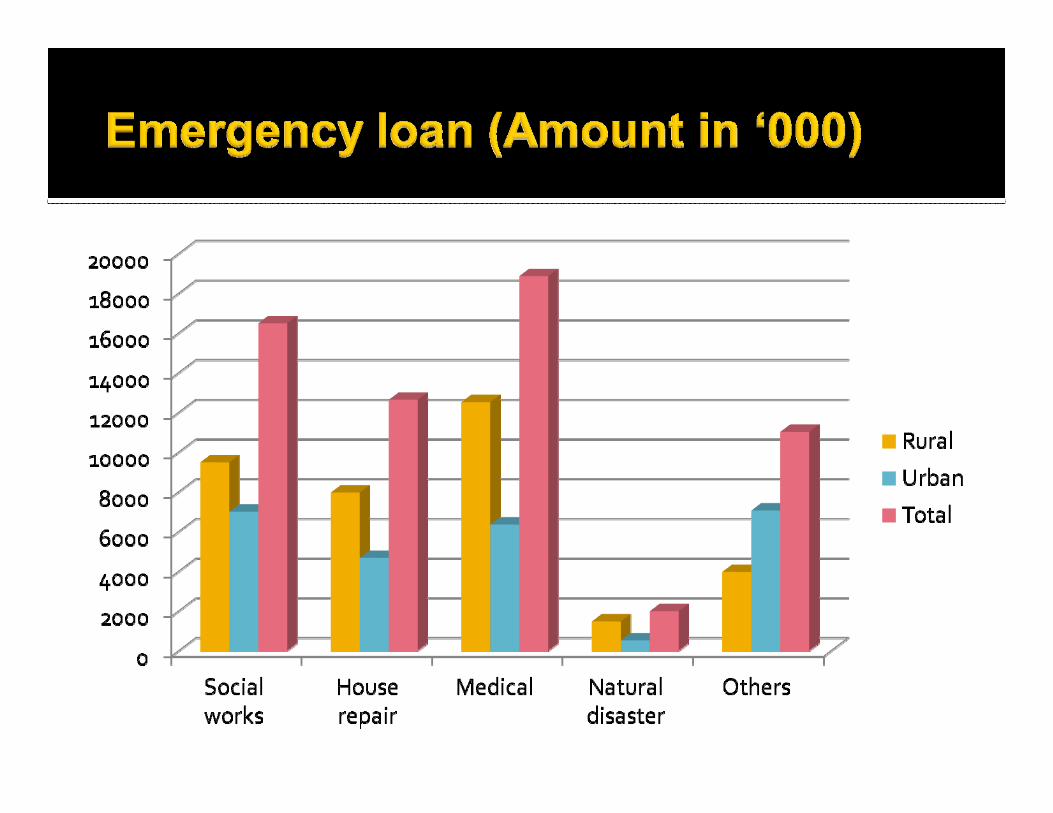

Size of deposit by institution shows that 1,266 household have savings. It shows that 69 percent in formal, 89 percent in semi-formal and 95 percent in informal institutions is for less than Rs.25,000. The survey result shows that the informal and semi-formal sectors are playing a major role in providing saving deposit services to its clients. People generally save at home, save in banks and in SHGs. They also invest in businesses. Access to lending by institution shows that 654 household have a loan from various sources. Urban respondents have more access to loans from formal sources. Rural respondents have access to loans from both formal and informal sources. The informal sector also plays a major role in providing loan services in rural areas. Major reasons for taking a loan are for investment purposes. The other reason is to meet basic needs such as education, food and medicine. Some respondents also borrow to pay off loans. A total 545 households incurred emergency expenses during past 12 months. Overall medical expense was the major emergency expenses followed by social expenses and house repair. Major source of meeting emergency expenses is the use of saving followed by informal sources such as friends and relatives and money lenders. Borrowing from formal and semi-formal sources is limited. Multiple borrowing occur when one household has more than one loan. In this category there were 888 households with an average of 1.2 loans per household. Multiple borrowing from the semi-formal sector is 1.3 loans per household.

A total 132 households transferred money during the past 12 months. The average amount of money transfer is almost double in urban compared to rural areas. The main mode of money transfer is carrying cash followed by bank account transfers. For rural households foreign remittances comprised 25% of monthly household income compared to 9% for urban households with a total 630 households with access to remittance services. The survey result shows that the main player in foreign remittance services is remittance companies followed by carrying cash. Remittances are used mostly for basic needs such as food, education, medicine followed by loan repayment. Insurance services were used by 299 households. Life insurance is the most popular insurance product both in rural and urban area. Overall 82 percent of respondents have mobile phones. The survey revealed that about 40% of respondents were interested in mobile phones for banking transactions.

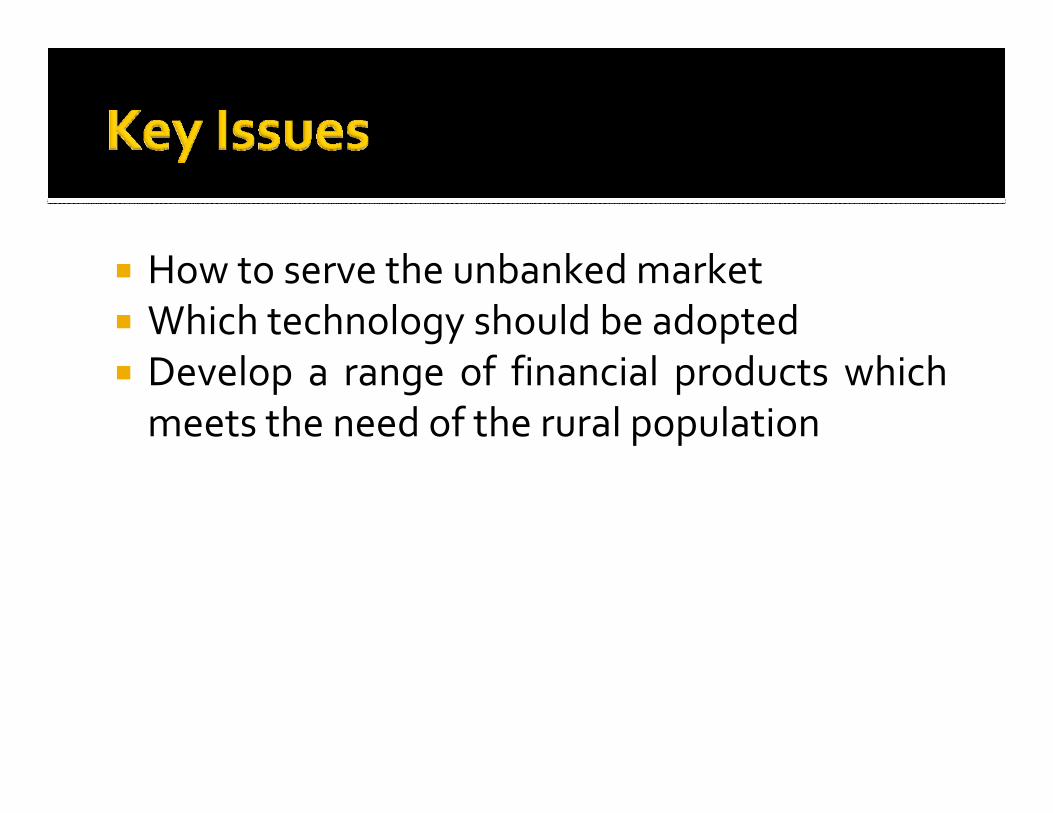

Key Issues Identified These were how to serve the unbanked market, which technology should be adopted, and the need to develop a range of financial products that meet the needs of the rural population. The Way Ahead Is to extend banking services through agent banking, use of technology such as mobile phones, and develop innovative financial products extending financial services to the rural population (Annex-7) Issues raised and Suggestions given by the Participants After the presentation the floor was open for discussion. Issues raised and suggestions provided by the participants are as follows.

1. In the study repayment rate of the financial institutions was found missing.

6

2. Mobile phone is easy for transferring the funds and checking the balance. There are many facilities in mobile phone.

3. Report needs to include the reasons of multiple borrowing. It is mainly due to no intension to repay loans of other institutions or to run small business properly.

4. Report did not mention about the sample unit taken from the hilly areas because the report is talking about access to finance in the hills and mountain areas and mentioned the reason for selecting the urban based cooperative in the sample. What is the price of the product to deliver in the market in the urban and rural areas? What were the products delivered in the rural area specifically related to access to finance?

5. A lot of cost is involved in delivering the product, what was the monitoring cost to deliver the product?

6. What were the disaggregated data served by MFDBs. commercial banks, other banks and finance companies in rural areas that rational decision can be made in policy making and program designing?

7. What was the level of risk for the financial institutions to deliver services? If the report mentions something about this then we can discuss on the strategy.

8. What is the cost of demand side and supply side and what is the charging rate of mobile?

9. In the report highest income of household is Rs. 39,000 which needs to be verified with the result of Nepal Living Standard Survey report.

10. Sample size taken for the study and the coverage is found small.

11. There is need of creating enterprises rather than increasing the outreach. Because remittances are being used for housing, food and other activities which are not directly income-generative and also used in paying debt servicing. So, It needs to concentrate on creating business, helping members with complementary services such as keeping their accounts, making business plan, supporting to establish market and market linkages

12. The report should have brought up how important is the cost from the users’ point of view. Do they understand the interest rate of 18% or 20% they have to pay? That would have been come out from the report.

13. More important is the access to finance rather than cost.

14. In the survey commercial banks have a lot of presence, concentrated more in the urban areas than in the rural areas. Are commercial banks ready to fit to manage this sort of loan in terms of the cost to give their product and in terms of their understanding to be able to deliver? It is not like opening branch and giving the loan. It is going in to the poor and understanding their needs. Therefore, access to finance survey should have been more towards the rural area than concentrated in the urban areas.

15. Report mentioned that 29% of the respondents are below the age of 14. Was that relevant?. Why somebody from below the age of 14? Is it because below the age of 14 has no easy access to finance from banking institutions or not have access to loans?

16. There is tremendous growth of microfinance institutions and they are working well. But how to go in the high hills and remote areas? So, what could be the reasons for not going in the high hills and remote areas?

17. The report has not included the high hills and remote areas. It has covered only the NRB licensed MFIs. NRB has stopped giving license to FINGOs and cooperatives since a long time. In the mean time, the cooperatives can do their business, They are working and several cooperatives have been growing in the high hills and remote areas. So, they need to be included in the report.

18. Why are the FINGOs categorized under semi formal organizations? Since this project is being launched in collaboration with NRB. It is believed that the FINGOs are under formal organization since the FINGOs are licensed by NRB. If that is the case whole scenario has to be changed in the analysis.

7

19. In the report, the number of commercial banks and MFDBs needs to be clarified whether the figure given in the report is either the number of banks or branches.

20. In addition to the mobile banking there is a need for a delivery model itself which could be appropriate to go in the hills and mountain areas whether it is cooperatives, Grameen model or SRG model which is adopted in the country or there might require some thing new in order to go to hills and mountain areas.

21. Suggestion to ADB and NRB, this sort of workshop needs to be done at the time of designing of the survey so that whatever the suggestions are given by the professionals could be helpful for the survey to make more meaningful.

22. Even in urban areas there is no option to transfer fund from one bank to another bank account. So there is need to create a financial highway to transfer funds from one bank to another.

23. NRB suggests if commercial banks and development banks want to establish separate division or separate desk with mission and goals to develop microfinance they can do direct deprive sector lending and microfinance lending. For example Mega Bank and some other banks have started financing in microfinance sector.

24. NRB clarifies that licensing and supervision of more than 12,000 cooperatives is beyond the capacity of NRB. So, the NRB stopped giving limited banking license to FINGOs. According to BAFIA, BFIs from class A to D are formal financial institutions and the rest of the limited licensing cooperatives, other cooperatives and FINGOs which do limited savings and credits within the members are categorized as semi formal institutions.

25. Insurance penetration is very low. The insurance companies are interested to expand services but there are some problems because MFIs are providing insurance coverage by themselves and they are a little reluctant to tie-up with insurance companies. The Insurance Regulator is coming up with six new products. Hopefully, it will increase the coverage in the days to come.

After the discussion queries were clarified by the panelist and suggestions were well taken for improvement of the report.

Remarks from the Chairman The chairman expressed his views that the survey finding would be useful for policy makers and practitioners to improve financial services in the days to come. He suggested incorporating the comments and feedback given by the participants and thanked all for the active participation in the discussion and their valuable inputs.

3.2 Second Session: Access to Financial Services in the Hills and Mountain Areas:

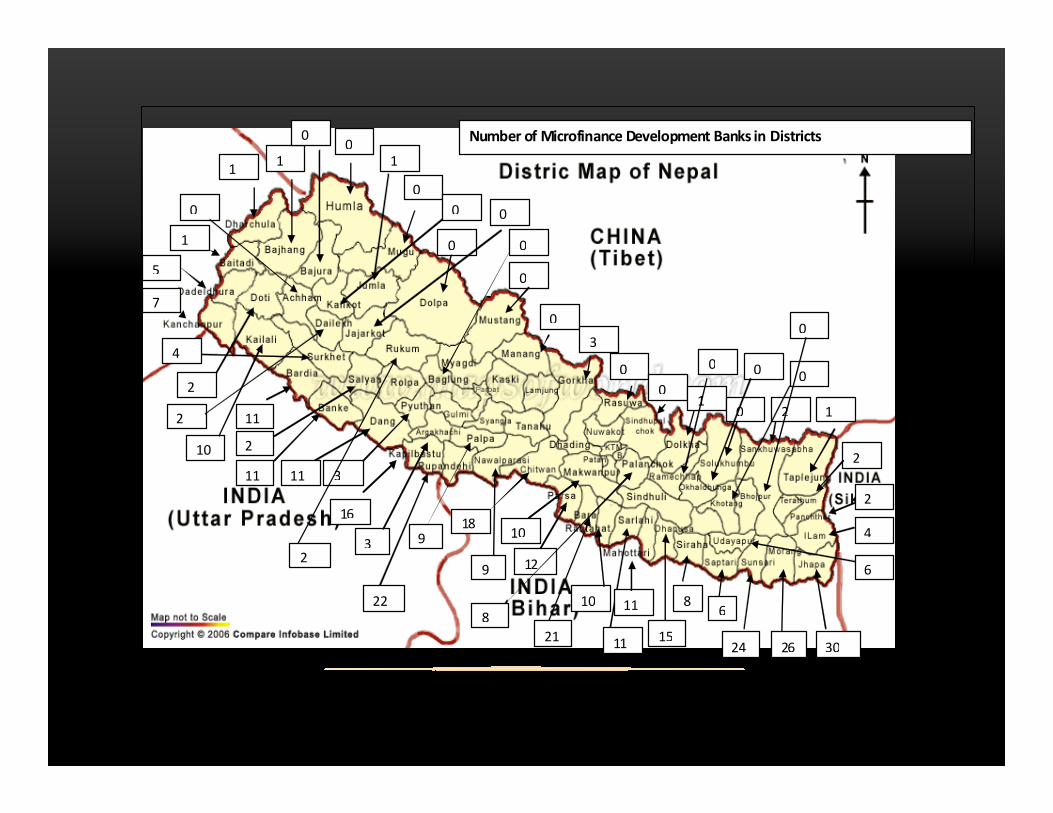

In the second session Dr. Purushottam Shrestha, National Team Leader, presented a paper on Access to Financial Services in the hills and mountain areas. The session was chaired by Mr. Baikuntha Aryal, Joint Secretary, Ministry of Finance. The presentation was divided in to four sections (a). Current situation, (b) Constraints to go in the hills and mountain areas, (c) Branchless banking and (d) Recommendations. The presentation started with the map of Nepal showing the presence of Microfinance Development Banks in the terai, hills and mountain districts. According to the map, Microfinance Development Banks are more concentrated in the plain areas rather than in the hill districts. In some districts there is even no representation. It indicates that there is strong need for Microfinance Development Banks to provide services in the hill and mountain areas to provide microfinance services to the un-served, deprived, destitute and disadvantaged groups. Regarding the current situation, half of the population lives in the hills and mountain areas with high incidence of poverty and this is present large challenges in the provision of financial services. There are four major constraints to be considered (a) lack of security, (b) lack of cash transit insurance, (c) lack of infrastructures and (d) high overhead costs.

8

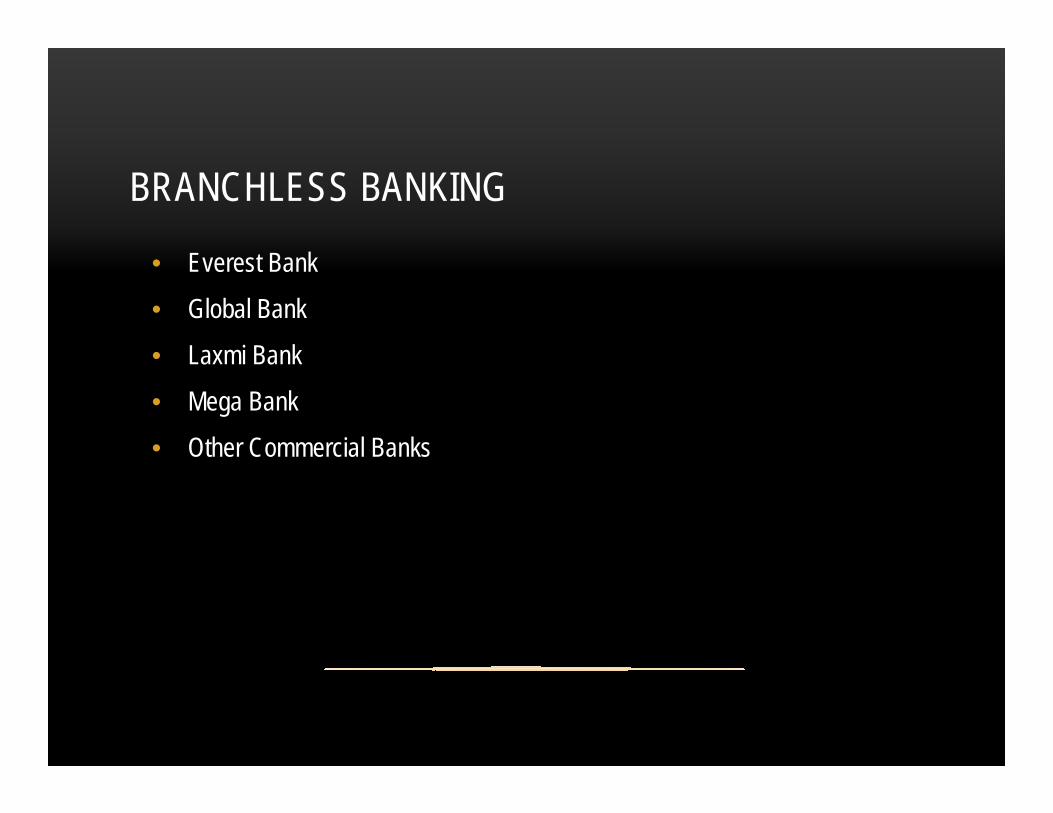

Based on the study, it is suggested that one of the options to reach the hills and mountain areas could be through branchless banking technology as some commercial banks e.g. Everest Bank, Global Bank, Laxmi Bank, Mega Bank and other commercial banks are undertaking this endeavor. However, there is a need to pilot services in the nearby hill districts of Kathmandu as frequent monitoring and follow-up will be needed for the prompt correction of mistakes. At the same time group members as well as MFI staff need to be well trained first and develop confidence. The following recommendations were made:

• There should be no distance restriction to operate branchless banking if it is feasible.

• Since operation of branchless banking is expensive, regulations should allow the bank to take the nominal home delivery service charge from the customers to meet their overhead cost.

• There is need for a mass awareness program to educate the rural community about branchless banking facilities.

• There are needs to develop policy, guidelines and directives to expand access of low income households to branchless banking (Annex-8)

3.3 Roles of Microfinance Institutions in Mobile and Branchless Banking in the Hill

and Mountain Areas

Mr. Normand Arsenault MIS Specialist presented the paper. Firstly, some definitions were presented: Under Mobile Banking and Mobile Money, there are three categories of mobile money (a) Card Payment Systems (Prepaid Cards) (b) Mobile Phone Payment Systems (Mobile Wallet) and (c) Agent Payment Systems (Branchless Banking Systems). (a) Card Payment Systems (Prepaid Cards) includes Stored-value Card and Cash Card

(b) Mobile Phone Payment Systems (Mobile Wallet) includes (a) Stored value and pre-paid mobile phone applications and (b) NFC mobile wallet

(c) Agent Payment Systems (Branchless Banking Systems) includes (a) Bank Model (b) Mobile Operator Model (M-Pesa and G-cash) This was followed by a description of models. Field Officer Model In this model banking services are offered at the customer location, door-step banking services in an agent driven mode, Designated staff regularly travel to rural communities to provide the financial services in an informal group setting and field officers use personal digital assistants (PDAs) or mobile phones. Field officers may use a smart phone that wirelessly connects to the bank server to process transactions and provide customer real-time access to their accounts. The smart phone may also encrypt and store transaction data offline and later synchronize it with the bank’s system using batch processing Banks need core banking system that include a mobile platform system. The main challenges are:

MIS systems of MFIs: no backend systems

NRB needs to increase its knowledge of mobile and branchless banking

Interoperability between mobile operators, banks, service payment providers, and microfinance institutions

9

Based consultancy findings it is suggested that:

we need to know more about existing mobile payments and mobile banking infrastructure in Nepal. There is a big difference between mobile payments and mobile banking.

a start is made by using phones for data collection and other non- cash purposes. By simply sending automatic SMS messages for repayment reminders and allowing customers to check balances via their phones. This is a very good way to start to get familiarity with these technologies.

a backend system is implemented

MFIs approach banks using mobile payments and explore possible sharing arrangements

m-banking systems are used for loan disbursements/ repayments and deposits.

MFIs act as agents on behalf of bank (Annex-9)

Issues Raised and Suggestions Given by the Participants

1. Banking is about trust. When new channels and new technology are introduced first the trust has to be accepted before doing banking. In one year full-fledged banking over mobile phone is not possible. First of all the channel has to be accepted by the customers, that the channel works, system works and the agent works. So, if it can establish this fact then mobile banking has good future.

2. Some commercial banks have started branchless banking over the last four years. Until now they do not have cost breakeven. In this case, can MFIs really want this as a business case in terms of rate of interest of about 19% or 20%. Can they pay out of this to the agent sufficiently so that agent can have more business case? Do they have interest to do this business later on? Otherwise they may start for six months and will vanish. As a result the MFIs and the clients will suffer.

3. Real challenge in mobile banking and even agent based banking is the loan disbursement. They can make the repayment through the technology but still there are challenges facing by M-Peso and G-Cash to disburse the cash to the people.

4. Regarding regulatory challenge, who regulates the technology providers? Is this Central Bank? In case of Nepal it is telecommunication authority. If there is a technical risk inside the telecommunication and service providers, then where do banks or other operators claim, where do they go for settlement. In some countries this technology is already in operation. Visa Card providers and master card are paying back to their clients $7 billion at this time. Even in developed countries the regulators could not track these things, how can our regulators and mobile technology providers track all these kinds of missing loopholes in operations?

5. The map has shown that MFDBs are more concentrated in the plain areas. Now, it has become a challenge for all: Nepal Government, Central Bank and all commercial banks. So, we have to design the project where there should be a role of Government, Central Bank and commercial banks. Some commercial banks are playing the leading role in using mobile technology. Technology is good .More than 82% people have a mobile phone. MFIs are not well equipped. We have to design the project to work comprehensively in 3 to 4 districts and in 5 development regions 2 to 3 years time as a pilot testing which will be helpful to find how the mobile users adopt and how the commercial banks adopt this technology. For this, supports from Nepal Government, Development Partners and Central Bank are inevitable.

6. From the recent experience of Mega Bank and Laxmi Bank it is realized that the customer education is one of the greatest challenge at the grass roots level. The presenters have highlighted in the institutional level about the challenges that exist regarding Nepal Rastra Bank, MIS and interoperability. So, to adopt this sort of technology, customer education must be taken into account.

10

7. Regarding constraints to go in the hill and mountain region overhead cost should be considered as the principal constraint. There are other more constraints to be added which have hindered the access to microfinance services.

8. Pertaining to the regulator, what happens if the Central Bank allows commercial banks to take partnership with the MFIs for branchless banking? It would be better that the commercial banks and MFIs both of them tie up and MFIs work as agents in some commission or fee sharing basis and go together offering same products in the rural area.

9. It is a nice news that Nepal can be a good model of mobile banking. NRB has taken steps to increase knowledge in mobile banking and branchless banking.

10. Regarding the collaboration with commercial banks and MFIs, commercial banks have huge technology regarding mobile banking. They are looking for collaboration with their subsidiary MFIs. Recently, NRB has issued the circular regarding mobile banking. However, it is not clearly mentioned. Commercial banks are not allowed to operate with MFIs. But if the commercial banks are interested to operate with MFIs, they need to send the proposal to NRB and the NRB will look into it and make necessary decision as required based on how it can be managed on behalf of client protection and risk protection.

11. Shidhartha Bank has been piloting from the extreme high hills to the terai region in 30 locations for the last two years with 4,000 plus customers. The people are keen to use the system. They want to open the account. They want to use Visa card, and ATM. The reality on the ground is the problem of infrastructure i.e. telecom network which does not work for 3 to 5 consecutive days due to lack of recharging services when the network is out of function.

12. There are more reasons for not going in the hills and mountain areas i.e. limited business. Even to attain self sufficiency and financial viability it takes 5 to 10 years,

13. Regarding access to finance more focus is given to mobile banking. It is suggested to add some other cost effective model to expand the microfinance services. Cooperatives and SRG model could be some of the options.

14. Use of mobile phone could be a good option. However, there is lack of skilled labor and investment capacity of MFDBs and cooperatives. For instance, even after the installation of software there was no trained person to operate smoothly. Right now there is no internet connection in the hills and mountains. It is possible to adopt in the plain areas.

15. Commercial banks adopt this technology only for deposit collection what about loan since MFI starts loan first then savings.

16. Remittance Company such as IME has been working for the last 10-11 years in Nepal with huge networks with 700 private agent outlets with enormous financial and technical capacity. There is a tremendous potential with their agents to do branchless banking, mobile banking and any other business. So, It is suggested to the regulators and concerned offices that commercial banks should be allowed to appoint remittance companies and money transfer companies as principal agents for branchless banking. If it is allowed and clearly specified in the policy it will be very easy and lead to immense success in branchless banking and mobile banking in Nepal.

17. How are hill MF program more expensive than that in the terai ? Is there any study undertaken?

The questions raised were answered by the concerned panelist and the comments and suggestions were well taken.

11

Remarks from the Chairman At the end of the session the Chairman concluded with the following remarks.

There are some policy issues and practical issues that have to be sorted out. There is a lot to

do about mass awareness for branchless banking technology.

Financial literacy is very poor in the country even in the urban areas. Therefore, people are not accessing financial services at the expected level. So, financial literacy is imperative to improve the financial services through MFIs.

Instead of supporting the banking services and all these things, donors and others can support in the technology which can contribute and complement services which are provided by the bank and financial institutions especially the microfinance institutions.

Regarding technology, customers should trust the technology. In addition to that, service providers should also trust it. In some cases the service providers are not trusting the technology.

About subsidiary companies and allowing remittance companies as partners with commercial banks - that can be discussed later in other forums.

There are 10 to 15 different models of branchless banking. A single model cannot be adoptable in all over the country because of difficult terrains and different development levels throughout the country.

Regarding nexus between technology and services how these two things can be taken simultaneously and side by side to the local level in hilly regions. That is very crucial. Unless and until these two things can be matched mobile banking cannot happen.

It is suggested to assess the risk before going to any model because risk is very high in any area.

It was seen in the picture that only the commercial banks are concentrated in the city areas. Based on the presentation of Dr. Shrestha MFDBs are also concentrated in the city areas and urban areas. It is an irony for the country. Government wants MFIs to go in the hills and mountain regions also. Of course, there are some policy issues and incentives are needed. Government will provide supports if they needed but they should go in the hilly and mountain region.

3.4 Third Session: Outline of Supervision System for MFIs

This session was taken by Mr. David Lucock, Team Leader. The session was chaired by Mr. Bhasker Mani Gyanwali, Executive Director of Nepal Rastra Bank. The speaker stated that since policy should set the microfinance framework, regulation and supervision of MFIs would be discussed within the context of policy. He touched upon (a) State of the MFDB/FINGO Subsector (b) Regulations and (c) Policy. The presentation was summarized as follows:

A. State of the MFDB/FINGO Subsector

About 1.4 million borrowers (subtracting multiple borrowing)

Household debt is twice lending declared by institutions - much of debt is to money lenders

MFIs lack household socio-economic information

B. Regulations

Many prudential regulations at present are either not up to international standards or are not conducive to industry development. Some examples:

12

1. Prudential requirements: 3 examples

a. CAR 8% - should be at least 12% and phased in over 3 years. Stress test shows: if 10% loan loss 12/18 MFDBs fail CAR. Only 2/18 would be able to continue borrowing in an open market. Two become insolvent. There is a high risk of contagion. Investors have not been vetted to ensure they can provide additional equity when required.

An assumption of a 10% loan loss leaves 13 MFDBs with aggregate equity of NPR 197 million and CAR 2.5%: need additional equity of NPR 467 million to recover to 8% CAR, NPR 773 million to recover to 12% CAR. Where would this money come from?

b. D:E now 30:1 should be 8:1

c. Liquidity requirements are too low –20% MFDBs had inadequate liquidity July 2011.

2. Loan classification and loss provisioning is inadequate. A category of 30-60 days is needed - 90 days overdue for short term unsecured lending is too long. Loss provisioning should start at 0 days. Classification changes are especially needed to counter rapid (and irresponsible) loan growth.

3. IPOs make no commercial or developmental sense – by attracting profit-seeking investors IPOs constrain development of services in remote areas. Two years are insufficient to provide a proper valuation of the MFDB.

4. MFDBs, in particular, are now less focused on community development issues and the status and needs of households than previously.

5. Growth restraints on branchless banking – there is as yet no evidence that public or FIs are at risk.

6. There is no enforcement of regulatory compliance among cooperatives – without enforcement, existing and proposed legislation is meaningless.

C. Supervision

It is impossible, under one umbrella, to fully supervise all financial service cooperatives, FINGOs and MFDBs: total > 23,000 MFIs. Steps to take:

1. Rationalize numbers (i) firstly obtain a better understanding of efficient financial service delivery

systems, (ii) then focus on how to encourage and supervise service delivery points: individual MFIs, federations of MFIs, MFIs partnering with banks. With e-banking, there is no need for a large number of MFIs.

2. Fully supervise +/- 30 MFDBs, license and monitor FINGOs.

3. Concerning cooperatives, Registrar of Cooperatives should fully supervise Federations of SACCOs and individual SACCOs on a spot check basis. Suggest re-license SACCOs with (i) larger number of members, (ii) stable and adequate capital, and (iii) membership of an approved federation. Ensure certification only of cooperatives under the control of a properly functioning federation. Is a new legislation needed for this?

1. Emphasize (i) improved due diligence by creditors of MFIs (ii) improved reporting by MFIs, (iii) better loan portfolio classification and management, (iv) improved governance and risk management within MFIs.

a. Since the number of MFIs are growing there should be rationalization of number of MFIs.

2. Establish an orderly process for liquidation of non-performing MFIs – do not waste resources propping them up.

3. Inform public about dangers of dealing with non-certified non-supervised MFIs. D. Policy

1. Use financial modeling to determine (i) systems that provide various financial services in a range of

locations, (ii) impact of regulations, (iii) supervision/control systems, (vi) impact of policy prescriptions. Then provide appropriate supports (not necessarily through MFIs alone).

2. With e-banking, there may be no need for more than 20 well-managed MFDBs plus a federated system such as the SFDB/SFCLs to reach more than three million rural and urban households with micro

13

financial services. Banks will cover many of these households also plus all other households with a set of financial services. This enables coverage of all households and businesses.

3. E-banking in rural areas: banks may be under-estimating the need for improved financial literacy and may not understand social development issues in rural communities. There is a risk of “cherry picking” by banks leaving poorer households un-served. Partnering with socially-aware MFIs or NGOs could be useful.

4. Review licensing requirements and procedures for all types of MFIs (i) set new requirements, (ii) reissue licenses subject to attainment of performance targets, (iii) cancel licenses for non-attainment.

5. What has DSLP done to improve the microfinance sector ?

(i) diverted funds to microcredit

(ii) increased household debt

(iii) refinanced informal debt.

(iv) increased D:E ratios of MFIs to dangerous levels

(v) encouraged formation of many weak MFIs

Suggest that DSLP be used to restructure microfinance sector and be closed January 2017.

encourage longer term lending to MFIs – to enable MIS upgrades, loan product development

allow Class A-C financial institutions to pay a levy as an alternative to deprived sector lending

use the levy as grant funding to promote rural hill financial services, rural financial literacy, training, MFI supervision, loan product development, sector surveys

ensure MFIs reach international standards < 4 years (Annex – 10) Issues Raised and Suggestions Given by the Participants

1. IPO has been made compulsory by the act for MFDBS. So the Act itself needs to be revised. However,

the MFIs cannot wait long for revising the Act because it takes at least 2 to 3 years. IPO is not right financing equipment. Until there is IPO, salary cannot be increased and distribution of dividends are not allowed by Nepal Rastra Bank

2. Since MFIs are largely concentrated in terai area or plain areas. The question is how to move to hills and mountain areas where the people are un-served. Then, how to promote new banks and emerging banks to run in Humla, Jumla, or Karnali districts. So, for this there are few suggestions (i) relicensing (ii) cut down if possible in the plain areas or terai area (iii) if they go in the hills and mountain areas they should be promoted and encouraged with some appropriate supports and incentives.

3. The termination of DSL needs to be considered very cautiously. Regarding the phase out of DSL after five years It is suggested to put 10 years as by this time MFIs will be able to make good ground since commercial banks have money that has to be taken in rural areas So, DSL should not be phased out before 10 years. Removing DSL will be a big problem for MFIs.

4. There are some conflicts of interest in recommendations, because in one technological presentations it is mentioned that we are promoting mobile banking and agent based model to commercial banks and another recommendation proposed to increase CAR for MFIs from 8% to 12 percent even limit the debt equity ratio from 30 percent to 5 percent. Is there any analysis done for the profitability of MFIs even after removing DSL policy after 5 years?. It needs to think the sustainability of MFIs. For recommending to increase the CAR from 8 to 12 percent, is it calculated how much is the cost for MFIs and if there is no interest from the promoters to increase the capital?. Because, this is not the similar context in Bangladesh and Cambodia. In Cambodia, outside investors are pushing money. So it is not proper time to limit the debt equity ratio for MFIs and removing DSL policy in Nepal’s context.

14

5. As mentioned in the presentation, DSL would be terminated after 5 years. DSL should not be contradictory with the policy of Nepal Rastra Bank since Nepal Rastra bank has directed to the commercial banks to increase the deprived sector lending by 0.5 percent for each year reaching 5 percent over the next three years.

6. There are many investors which are interested to finance MFIs but their interest rate is very high. So DSL has become very helpful for Microfinance institutions which are getting a cheap interest rate from commercial banks. So, If is removed, MFIs will have a big problem.

7. Microfinance program is different from that of the neighbouring country India. In Nepal Microfinance programs are executed as social privilege, not as business organization. There is no problem in Microfinance except multi financing. However, it will be solved after the CIB is established in near future.

8. The word cease has created some confusion and it should have better understanding. Is presenter trying to linkup with upcoming branchless banking and mobile banking? Perhaps microfinance as such and the requirement of FINGOs and MFIs is reducing or being redundant over a period of 5 years or more?

9. It is mentioned that borrowing and lending is 1:1. Perhaps that is correct in terms of lot of balance sheet of MFIs represent.

10. Just linking to the IPO, is the need for IPO and is the need for equity or share holding. But rather than allowing the MFIs to go to IPO for public equity, may the commercial banks and development banks be the only shareholders of MFIs in terms of making lending already through equity and also the risk taking capacity would be much higher with commercial banks and development banks than the general public and need would also be understood in terms of linking with dividend expectation. Of course the MFI should not be in loss and continue in this position. They also should make profit.

11. Based on some balance sheet of MFIs more than 75 percent loan is in single category which is general loan. Linking with the NRB directives to commercial banks to lend 5 percent in the deprived sector lending and 20 percent in productive sector, altogether 25 percent of lending of commercial bank is effectively directed. So, why is it not directed in the case of the MFIs? They also should have been directed with specific criteria like livestock so much rather than investing more in single loan i.e. general loan alone.

12. Does it need to reinvent the wheel since the policy is already there in place to be implemented? There is no need to bring new policy.

13. NRB’s comments and suggestions

Recommendation for increasing CAR is positive. However, considering the real situation it is very difficult for MFIs to do so. Because if the MFs have to increase the CAR they have to bear additional cost burden.

Liquidity requirement is too low: NRB will manage it according to the requirement of MFIs.

Change in loan classification and provisioning: As per the recommendation, overdue after 30 days would be better to classify as good loan, overdue between 30 and 60 days as substandard and more than 90 days as bad.

Termination of DSL after 5 years: The recommendation should be country specific, The commercial banks should have social responsibility towards the poor people or MFIs for the development in addition to gaining profit by providing big loan to large borrowers. If the DSL is removed, more than 50 percent MFIs which are providing services to the poor and deprived people will be closed down within 5 years.

IPO: It is not compulsory to go to IPO for the MFIs like commercial banks. However, according to BAFIA (Section 7) it is made compulsory for all BFIs. According to section 36 it is not allowed to distribute any types of allowances before going to the IPO. Therefore, NRB has to restrict increases in salary, allowances, remuneration and other facilities to the Board of Directors, Managing Director and CEO and those who are in key positions. NRB has realized this problem and is planning how this issue could be resolved in future.

15

Increasing Liquidity: It will increase the cost for MFIs. However, NRB will manage based on the discussion with MFIs.

Presenter has not addressed the employee’s union problem that has hassled all MFIS and banks.

As mentioned in the presentation, some MFDBs could fail within five years. NRB does not see this possibility, since there is the separate Department of Microfinance Promotion and Supervision. For the last two years NRB has been supervising regularly all MFDBs only, not other institutions. In the two years MFDBs have become more streamlined than before. NRB has focussed more intensively than previous. From the last two months NRB has issued directives for the credit information system to all MFDBs to implement within very soon. Many MFDBs will upgrade their information system and they will become more effective.

There will be more capital injection from development banks and shareholders. NRB is going to start the stress test for MFDBs from this year.

There will be separate directives to the MFDBs, and cooperatives and FINGOs having limited banking license from NRB. So, in the coming days the MFDBs will be stronger and more sustainable than before. Prudential norms are based on Basel standard and there is no question of systemic failure problem because the loan size of MFDBs is small.

Regarding loan insecurity, MFDB has group based loan. They have to lend two third in group based loan without collateral and one third loan in collateral based enterprises. Repayment rate of MFDBs are still high and in Nepalese context, poor people’s repayment rate is high because they are honest and sincere.

Remarks from the Chairman After the discussion on the presentation the Chairman has given the following remarks.

NRB is giving license for D class institutions to increase financial access. NRB has given

priority to establish D class institutions in rural areas and rural districts.

NRB also provides an industry loan if interested microfinance entrepreneurs want to establish D class institutions in high hills and mountain areas and rural areas.

Regarding the branchless and mobile banking NRB has recently issued e-banking regulation. It is open to all A,B,C,D classes. He informed all D class institutions to come with solid and specific proposal in which way and how they are interested to operate the branchless banking and mobile banking. NRB will be very pleased to give the permission to operate in those areas.

NRB has no policy to cease DSL. Instead of that, NRB has increased from this fiscal year by 50 basis point and it will be 5 percent to commercial banks, 3.5 percent for the development banks and 3 percent for finance companies.

In Nepal this is a specific need. If such types of facilities are not given to MFDBs there will be a big resource gap for them.

NRB is very keen to develop financial access in rural areas. In this regard NRB has issued regulations for directed lending and also has promised in the regulation that NRB will finance if any one goes on direct lending and no need to worry for financial support.

3.5 Wrap up of the Workshop Seminar

At the end of the workshop seminar Mr. David Lucock wrapped up with following remarks. Starting with the survey report he mentioned that we had a discussion about the repayment rate in the survey. It was not discussed because the survey was just a single time survey. It was not a time series survey. This is important because what we see is that some of the formal borrowing is being used to refinance informal borrowing. The only way to see the net benefit of a formal loan is to look at the total household debt and assets over a certain time period. That requires a much

16

more elaborate survey. So, our focus was just on access to financial services. We see a need to provide sector support to encourage microfinance services especially rural areas. Forty percent of borrowing in rural areas is coming from family money lenders and only 10 percent in urban area. So, that gives us an indicator of the potential for additional lending over the next 5 years we see something like an additional 800,000 households being reached especially in rural areas. We appreciate your point about using survey policy and we agree that there is greater need for this. It is very good that NRB is now initiating another survey concerning finance in rural locations. We need to encourage that and we need to fund these sorts of initiatives. It is difficult to provide a single cost for services as we have to determine the types of service and to determine the transaction size and determine the locations. So, there is no clear and single answer on this. That is why, a bank can make a $5 million at 12% interest and MFIs make a $50 loan at 20% interest. The overhead cost is relatively smaller for a large loan. In terms of financial services we would like to have more time with you to discuss expansion of services in the hills area and exactly how to do it. But one of the good points that came out of this workshop was the need to pilot some of the services especially mobile phones with a MFDB. We need to see how far the MFIs can take electronic banking – at least and certainly for loan repayment and money transfer and messages concerning loan overdue. Even these few steps would improve customers services through microfinance institutions We do not see all of this happen overnight. It was mentioned by several of you that we need to build up customer confidence and trust through experience with services. We would like to see NRB being more involved to the process of developing electronic banking. The Executive Director made a very good suggestion a few minutes ago that he would like the MFDBs to set out proposals for the operation of electronic banking in this services. This is a very good idea. We discussed the number of different models that are feasible. We have the wholesale development banks working with MFDB, FINGOs and some SACCOS - that is one model and this model could be used to reach more than 2 million households. We also have the model of a bank coming in with mobile banking services or branchless banking services and agencies and that model could also reach a very large number of people, maybe not so much on the micro credit side but certainly for the other financial services there are required and requested. As said earlier, in 5 years time we would expect the number of households using electronic banking services to exceed the number of microcredit borrowers. So, the market right now is poised to expand very quickly. In the area of policy and supervision the need, we think, is for the Government - Ministry of Finance and NRB - to be looking at different models that could provide financial services in the future. Then in relation to that, determine how many service points do we need and what types of service points and what types of financial institutions do we need. We need to identify this because we need to rationalize the number of MFIs especially cooperatives. On supervision, we would like to suggest that supervision may be more focussed on risk-based supervision. This is essentially a matter of determining those financial MFIs that are so large that their failure will adversely impact the market. Secondly where do the large major risks lie? We think the two major risks are (i) the lack of certainty over loan portfolio quality, and (ii) that the financial structure of the MFIs is essentially built on a very short term liability basis that has the potential to collapse once something starts to go wrong. There is a high risk of systemic failure. On regulatory enforcement, the problem is not with the class A to D banks. We think they are being well regulated by NRB. The cooperatives on the other hand are not being required to comply with regulations and that needs to rectified at some stage if we are going to protect consumers who use cooperative services. So, this is a major concern. How do we do it ?. Maybe

17

federate smaller cooperatives as done through NEFSCUN. Supervision would obviously be by NEFSCUN. But each of the SACCOS belonging to that federation would be required to show its certificate, the certificate that attests to good practice that consumers can trust. That places a liability on NEFSCUN but reduces some of the supervision requirement of the Regulator. On the DSL program, we looked at this 10 years ago. RMDC evolved as a result of this process. We are concerned that DSL program creates dependency - every baby must be weaned at some stage. The problem, furthermore is that we are only focussing on credit. There is no development of deposit services and the problem then becomes that MFIs rely on borrowing. A rating agency may come in and say your loan portfolio is not good enough for this borrowing. Many international MFIs today have raised deposits and lowered their borrowing so that the ratio between the loan portfolio and borrowing becomes quite acceptable. This means that alternative investment or borrowing opportunities are not confined just to DSL program and not confined just to short term borrowing. To support expansion of financial services and customer development, we have suggested that some of the DSL funding would go into a grant fund that would be administered by NRB, a representative of commercial banks and a representative of MFDBs who would recommend allocation of the money to the development of financial services in the hills area. This is just one example of variations to DSL that could be considered. Finally, he thanked all and expressed the wish that the final report to be circulated would provide scope for future discussion on the development process of the microfinance sector in Nepal.

3.6 Outcomes

The workshop seminar succeeded in achieving the following outcomes

Better understanding of survey findings and how to improve access to financial services in hills and mountain areas

Better understanding of the policy, regulation and supervision needs and the provision of an improved environment for access to finance.

3.7 Conclusion

The significant number of participants present in the workshop seminar participated in a lively and fruitful manner concerning suggestions, comments and viewpoints on a range of issues including. DSL, branchless banking, regulation and supervision, and financial ratios. The much appreciated presence of the Country Director of NRM/ADB, Deputy Governor of NRB and Joint Secretary of the Ministry of Finance inspired all participants to enrich and broaden their knowledge on policy and operational matters of institutions working in the microfinance sector in Nepal. The comments and suggestions provided by the participants were useful for the preparation of the final report of the technical assistance consultancy.

18

ANNEXES

19

Annex-1 ASIAN DEVELOPMENT BANK: TA 7777

Improving Access to Finance Sector Development Program Workshop Seminar on Access to Finance

July 17, 2012 Background The Government of Nepal recognizes that access to finance is critical to the development of the country’s economy. Nepal Rastra Bank has introduced deprived sector directed lending programs, mandated banks to open branches outside of the Kathmandu valley, has created specialized wholesale and retail financial institutions in an effort to expand the outreach of financial services. Although the number of financial institutions has grown rapidly, a significant proportion of the country’s population are still constrained in accessing financial services. The Three Year Plan Approach Paper (2010/11 – 2012/13) of Government of Nepal is committed to a major reform program in financial sector. The workshop will deal with the following:

- Sharing findings of the access to finance survey

- Financial access to hill regions

- Regulation and supervision of microfinancial services

Outputs

- Better understanding of how to improve access to financial services in hill areas

- Better understanding of the regulation and supervision needs and provide enabling policy environment for access to finance.

Participants The participants will include representatives of the Government, Nepal Rastra Bank, Commercial Banks, Development Banks, Microfinance Development Banks, Saving and Credit Cooperative Societies, Financial Intermediary Nongovernmental Organizations, Financial Associations, Nepal Federation of Savings and Credit Cooperative Unions Limited, representatives from Asian Development Bank, World Bank, Enhancing Access to Financial Services, International Finance Corporation, National/International Nongovernmental Organizations and other related stakeholders. Venue :Hotel Shangrila, Lazimpat, Kathmandu

Phone: 4410108, 4412999

Time: 8.30 am - 1.30 pm

20

Annex-2 ASIAN DEVELOPMENT BANK: TA 7777

Improving Access to Finance Sector Development Program Workshop Seminar on Access to Finance

July 17, 2012

8:30 AM - 9:00 AM Registration/Breakfast

9:00 AM - 9:10 AM Welcome Speech Mr. B. Aryal Joint Secretary, MoF

9:10 AM – 9:20 AM ADB Policy on Access to Finance Mr. K.Yokoyama,Country Director,NRM/ADB

9:20 AM – 9:30 AM Key note address: Mr. G. Pd. Kaphle, Deputy Governor, NRB

9:30 AM– 10:00 AM Survey Report on Access to Finance

Chairman Mr. G. Pd. Kaphle, Deputy Governor, NRB,

Presenter Mr. R. N. Gongal, M/Survey Coordinator

10:00 AM - 10:30 AM Comments and Suggestions

10:30 AM – 11:00 AM Tea Break

11:00 AM – 11:30 AM Access to Finance in Hill and Mountain Areas

Chairman Mr. B. Aryal Joint Secretary, MoF

Presenter Dr. P. Shrestha National Team Leader

Mr. N. Arsenault MIS Specialist

11:30 AM – 12:00 PM Comments and Suggestions

12:00 -12:30 PM Outline of Supervision System for MFIs

Chairman Mr. B. M. Gyanwali ED. NRB

Presenter Mr. D. Lucock Team Leader

12:30 PM –1:00 PM Comments and Suggestions

1: 00 PM – 1:30 PM Wrap up Mr. D. Lucock Team Leader

21

Annex-3

ASIAN DEVELOPMENT BANK: TA 7777 Improving Access to Finance Sector Development Program

Workshop Seminar on Access to Finance July 17, 2012

List of Invitees SN Name Designation Organization

Nepal Rastra Bank 1. Mr. Gopal Prasad Kafle Deputy Governor Nepal Rastra Bank 4412963 2. Mr. Bhasker Mani Gyanwali Executive Director “ 4411407 3. Mr. Khyam Narayan Dhakal Director “ 4412823 4. Mr. Rebati Nepal Deputy Director “4412823 5. Mr. Lekhnath Dahal Assistant Director “4412823 Ministry of Finance

1. Mr. Baikuntha Aryal Joint Secretary Ministry of Finance 4211826/4211406 Wholesale Microfinance Devt.

Bank

1. Mr. Jalan Kumar Sharma CEO SFDB 4111752/4111828 2. Mr. Numnath Poudel CEO First Microfinance Development Bank

4425358 3. Mr. Ram Dayal Rajbansi Senior Manager RMDC 4268019/4268020 NMBA/MFDB

1. Dr. Harihar Dev Panta Executive Director Nirdhan Utthan Bank Ltd. 4102665 2. Mr. Ram Chandra Joshi Executive Director/CEO Chhimek Laghu Bitta B. Bank Limited.

4490513 3. Mr. Rajendra Kumar Mainali Executive Director Naya Nepal Laghu Bitta B. Bank Ltd.

011- 490671 4.. Mr. Sharada Pd.Kattel CEO Depsosc Laghu Bitta B. Bank Limited

4288652 5. Mr. Saroj Prasad Rimal Legal Officer Shorojgar Laghu Bitta B Bank Ltd.

011-661060 NEFSCUN

1. Mr. Bishnu Pathak CEO NEFSCUN 4781963 FINGO/MIFAN

1. Mr. Pitamber P. Acharya Executive Director/Chairman

DEPROSC/ Nepal/MIFAN 4244723

2. Ms. Shova Bajracharya Senior Manager Manushi 4425228/9841248552 Cooperatives

1. Mr. Amri Prasad Kayastha CEO Women cooperative Society Ltd. 4301619 Commercial Bank and Devt.

Bank Association

1. Mr. Rajan Shingh Bhandari Vice Chairman Banker’s Association Commercial Banks

1. Mr. Prakash Raj Sharma CEO Microfinance, Laxmi Bank Ltd. 4785306/07 2. Mr. Krishna Raj Parajuli CEO Business Universal Development Bank

Ltd.4102773/4102774 3. Mr. Dilip Shah Division Chief Agricultural Devt. Bank Limited.

4462797 4. Mr. Govinda Gurung General Manager Mega Bank Nepal Ltd. 4257711 5. Mr. B.N Gharti Deputy General

Manager Kist Bank Limited. 422033/4232500

6. Mr. Bimal Daga Assistant General Manager

NIC Bank Ltd. 4262277/4222336

7. Mr. Gopal Chandra Sharma Department Chief, Credit Department

Rastriya Banijya Bank 4228031/4252595

8 Mr. Tilak Panday Department Chief, Credit Department

Nepal Bank Limited 437533

9. Mr. Yub Raj Guragain Head, Micro Banking Mega Bank Nepal Ltd. 4257711

22

SN Name Designation Organization 10. Mr. Ashish Kumar Sharma Head, Payment

Solutions Shidhartha Bank Ltd.4442919/4442920 ext. 2410

11. Mr. Suresh Raj Maharjan Head Marketing Global Bank Nepal Ltd. 4231198 12. Mr. Pramod Raj Sharma Company Secretary Everest Bank Ltd.4443377/9851146144 13. Ms. Shanta Siwakoti Senior Relationship

Manager Global Bank Nepal Ltd. 4231198

14. Mr. Badri Lall Amatya Manager Nepal SBI Bank Ltd. 4218836/9851034791. 4435516

15. Mr. Prasanna K. C. Senior Relationship Manager

Laxmi Bank Limited 4444684/4444685

16. Mr. Nikesh Ghimire Manager Laxmi Bank 4444684/4444685 17. Ms. Rukmani Maharjan Assist. Relationship

Manager NMB Bank Ltd 4246160

Training Institutions 1. Mr. Tej Hari Ghimire CEO CMF 4434041 2. Mr. Sanjib Subba CEO NBTI 4415905 3. Mr. Rudra Bhattarai General Manager NACCF 5010758 4. Mr. Avash Nirola Program Officer NBTI 4415905 5 Mr. Sabin Nepal Administration Officer NBTI 4415905 ADB and TA Team

1. Mr. Kenichi Yokoyama, Country Director, NRM/ADB 4227779/84 2. Ms. Mayumi Ozaki Finance Specialist ADB 4227779/84 3. Mr. Raju Tuladhar Senior Program Officer NRM/ADB 4227779/84 4. Mr. Siddhanta Vikram Senior Public

Management Specialist NRM/ADB 4227779/84

5. Ms. Nileena Nakarmi Associate Economics Analyst

MRM/ADB 4227779/84

6. Mr. Geisen Johannes Project Manager AFC International 7. Mr. David Lucock Team Leader IAFSDP/ADB TA 9843006785 8 Dr. Purushottam Shrestha National Team Leader IAFSDP/ADB 9851140544 9. Mr. Normand Arsenault MIS Specialist IAFSDP/ADB 10. Mr. Ramesh Nath Gongal Mapping and Survey

Coordinator IAFSDP/ADB 9841279333

11. Ms. Pramila Shrestha Gender and Social Development Specialist

IAFSDP/ADB 9841403214

12. Dr. Nara Hari Dhakal Program Coordinator RFSDCP/ADB 9851048729 Credit Information Bureau

1. Mr. Anil Chandra Adhikary CEO CIB 4222855 Insurance Company

1. Mr. Arun Basnet Manager ALICO 5555166 ex.110/9851056553 Remittance Company

1. Mr. Suman Pokharel General Manager IME 4430600 2. Mr. Dibakar Thapa General Manager Western Union 4258387/4261313/4258225

Mob. 9851019972 International Organizations

1. Mr. Jhank Narayan Shrestha Deputy Technical Advisor

EAFS/UNCDF 4010058/9813506161

2. Mr. Ramesh Kumar Gautam Microfinance Manager NEAT 5524038/9841593312 3. Mr. Sabin Shrestha Senior Financial Sector

Specialist World Bank 4226792/93

4. Mr. Hem Raj Poudyal Program Manager Plan International 5535580/5536431 5. Mr. Ganesh Bista Technical Advisor Mercy Corps Nepal 5012571 Mobile Financial Service

Solution Provider.

1. Mr. Sanjay Shah Executive Chairman Finaccess Pvt. Limited. 5000654 Total 63.

23

Annex-4 Key note Address

Mr. Gopal Prasad Kaphle Deputy Governor

Nepal Rastra bank Distinguished Delegates, Ladies and Gentlemen, It is indeed a great pleasure for me to speak of few words among this august gathering. It is really a matter of satisfaction for us to be able to continue the cooperation between Nepal and Asian Development Bank. Over a period of more than four decades, the cooperation between Nepal and the ADB has expanded to many important areas of Nepal’s development needs, including important policy reforms, development of infrastructure facilities, agriculture and rural development, and development of the social sectors. As such the ADB has evolved as a key development partner of Nepal since 1968 and continues to support reforms and provide policy advice, technical assistance, and development financing. Besides these areas of cooperation, the ADB has recently opened up its avenues to support the inclusive development needs of Nepal through projects pertaining to improving access to finance sector development program. The efforts of the ADB through its various aids and grants programs targeted towards reducing poverty and improving rural and agricultural financing are really commendable and the recent areas of cooperation on improving access of financial services in Nepal, particularly in rural areas would further enhance our cooperation between us. As today’s workshop is focused on access to finance in Nepal, I am confident that the workshop would highlight on many fields of our endeavors pertaining to access of our rural and poor people to finance, status of microfinance, its expansion and scope; and regulatory and supervisory issues on microfinance. In many countries microfinance has emerged as an important tool that help transform subsistence rural agro based economy into a vibrant commercial economy. We have also been practicing agro-financing and rural financing for a long time. During this time, we have adopted various types of micro-financing models developed as well as evolved in our region such as Grameen model, Cooperatives model, financial NGOs model, group based/collateral less lending models and other program based models. Many micro-financial products are being developed and offered to the targeted rural and deprived people. We have many local success stories to share among ourselves and we have many failures as well. We have learned from our failures and replicated many successful micro-financing models. During last two decades, our country witnessed a tremendous growth in size and structure of our financial system. The growth of banks and financial institutions in the last two decades has been primarily urban centered. Despite our sincere efforts, a large segment of rural households still do not have access to formal financing. As such, as a central bank of the country, we are now moving towards promoting inclusive financial growth by undertaking various policy and strategic actions. We all know that micro financing is basically a pro-poor program. The institutions and the human resource involved in micro-financing are required to be service oriented and fully committed to their jobs. Lack of fund is another concern for micro-financing institutions as they face paucity of owned funds so as to move in their growth path. In our context, poverty and deprivation are basically found in rural and remote areas. While remoteness and absence of physical infrastructure make it very difficult to operate micro-financing programs in such areas and it is a real challenge to microfinance operators as well as policy making and implementing agencies, the operational and financial viability of these institutions for the long run sustainability of those institutions is another challenge. As such, along with many credit plus activities, proper and continued development of human resource conducive to the micro-financing jobs is mostly warranted. I am confident that the present workshop would certainly contribute to enhance our knowledge and come out with suggestions and policy inputs regarding improving access of finance and need of prudent and sustainable micro-financial framework that would help achieve inclusive development of the country. I wish the program all success. Thank you all.

24

Annex-5 ADB Policy on Access to Finance,

Mr. K.Y. Yokoyama Country Director, NRM/ADB