dr pepper snapple group overview - s3.amazonaws.com · total bottler case sales dr pepper bottler...

TRANSCRIPT

Dr Pepper Snapple Group Overview

Investor RelationsHeather Catelotti(972) [email protected]

Media RelationsChris Barnes(972) [email protected]

Contact Information:

2

Safe Harbor Statement

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, including, in particular, statements

about future events, future financial performance including earnings estimates, plans, strategies, expectations,

prospects, competitive environment, regulation, and cost and availability of raw materials. Forward-looking statements

include all statements that are not historical facts and can be identified by the use of forward-looking terminology such

as the words “may,” “will,” “expect,” “anticipate,” “believe,” “estimate,” “plan,” “intend” or the negative of these terms

or similar expressions. These forward-looking statements have been based on our current views with respect to future

events and financial performance. Our actual financial performance could differ materially from those projected in the

forward-looking statements due to the inherent uncertainty of estimates, forecasts and projections, and our financial

performance may be better or worse than anticipated. Given these uncertainties, you should not put undue reliance on

any forward-looking statements. All of the forward-looking statements are qualified in their entirety by reference to the

factors discussed under “Risk Factors” in Part I, Item 1A of our Annual Report on Form 10-K for the year ended

December 31, 2014 and our other filings with the Securities and Exchange Commission. Forward-looking statements

represent our estimates and assumptions only as of the date that they were made. We do not undertake any duty to

update the forward-looking statements, and the estimates and assumptions associated with them, after the date of this

presentation, except to the extent required by applicable securities laws.

Non-GAAP Information

These materials include certain non-GAAP financial measures. Please refer to the “Investors” section of our website at

www.drpeppersnapplegroup.com to find a reconciliation of such non-GAAP financial measures to their most direct

GAAP counterpart.

Definitions

Please refer to the Definitions and attachments to our October 22, 2015 earnings release for the definitions of core

financial measures and certain other terms used herein.

Important Disclosures

Deliver Shareholder Returns

3

Strategic Vision and Priorities

Strategic

Priorities

• Build Our Brands

• Execute with Excellence

• Rapid Continuous

Improvement

Vision Be the Best Beverage Business

in the Americas

4

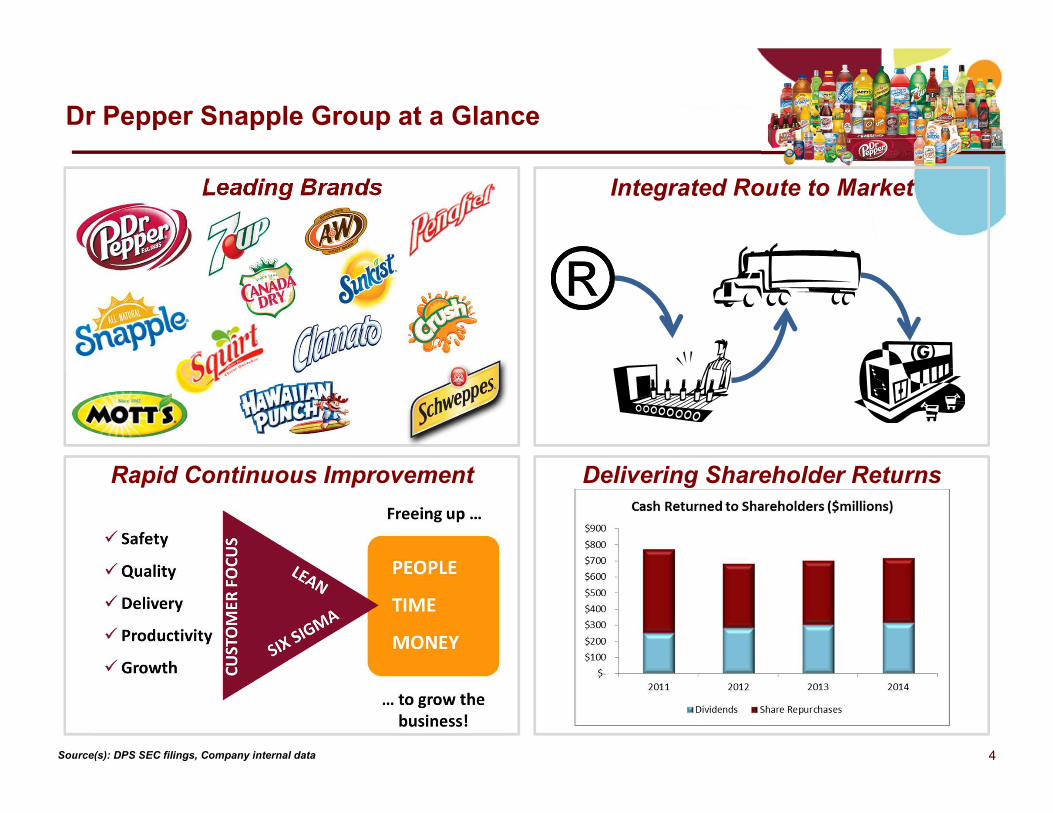

Dr Pepper Snapple Group at a Glance

Rapid Continuous Improvement

Leading Brands

Source(s): DPS SEC filings, Company internal data

Delivering Shareholder Returns

Integrated Route to Market

5

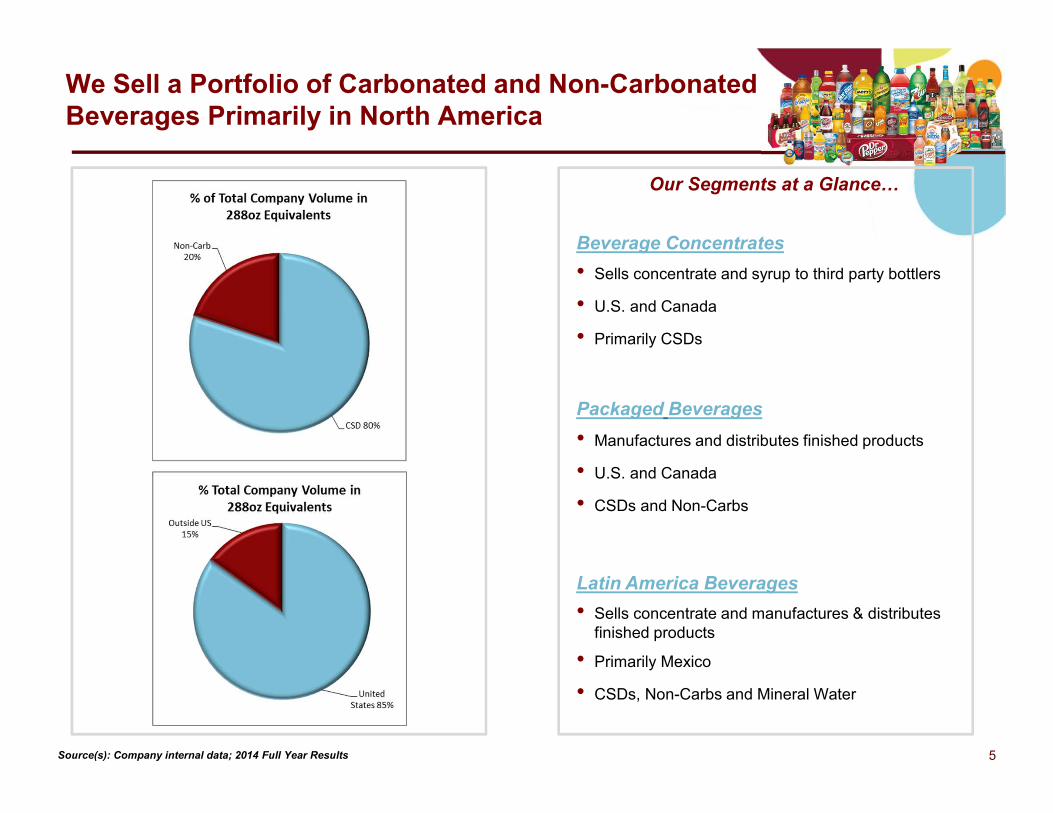

We Sell a Portfolio of Carbonated and Non-Carbonated

Beverages Primarily in North America

Our Segments at a Glance&

Beverage Concentrates

Packaged Beverages

Latin America Beverages

• Sells concentrate and syrup to third party bottlers

• U.S. and Canada

• Primarily CSDs

• Manufactures and distributes finished products

• U.S. and Canada

• CSDs and Non-Carbs

• Sells concentrate and manufactures & distributes finished products

• Primarily Mexico

• CSDs, Non-Carbs and Mineral Water

Source(s): Company internal data; 2014 Full Year Results

6

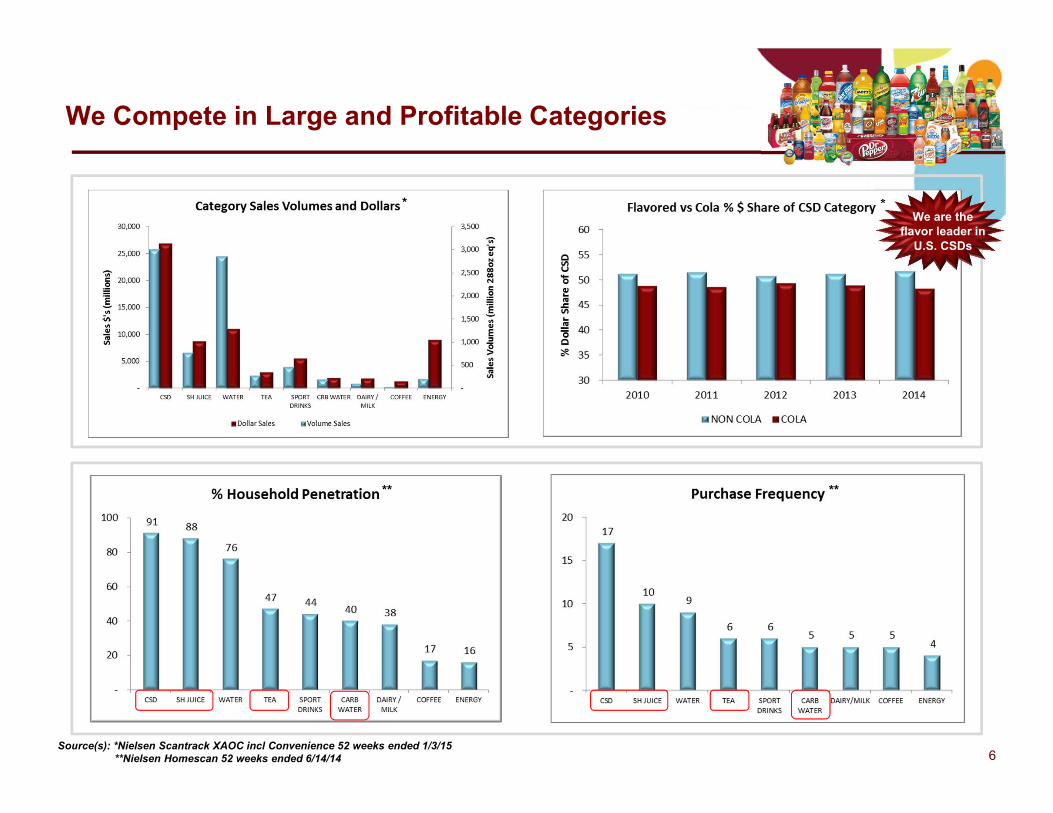

We Compete in Large and Profitable Categories

Source(s): *Nielsen Scantrack XAOC incl Convenience 52 weeks ended 1/3/15

**Nielsen Homescan 52 weeks ended 6/14/14

* *

** **

We are the

flavor leader in

U.S. CSDs

7

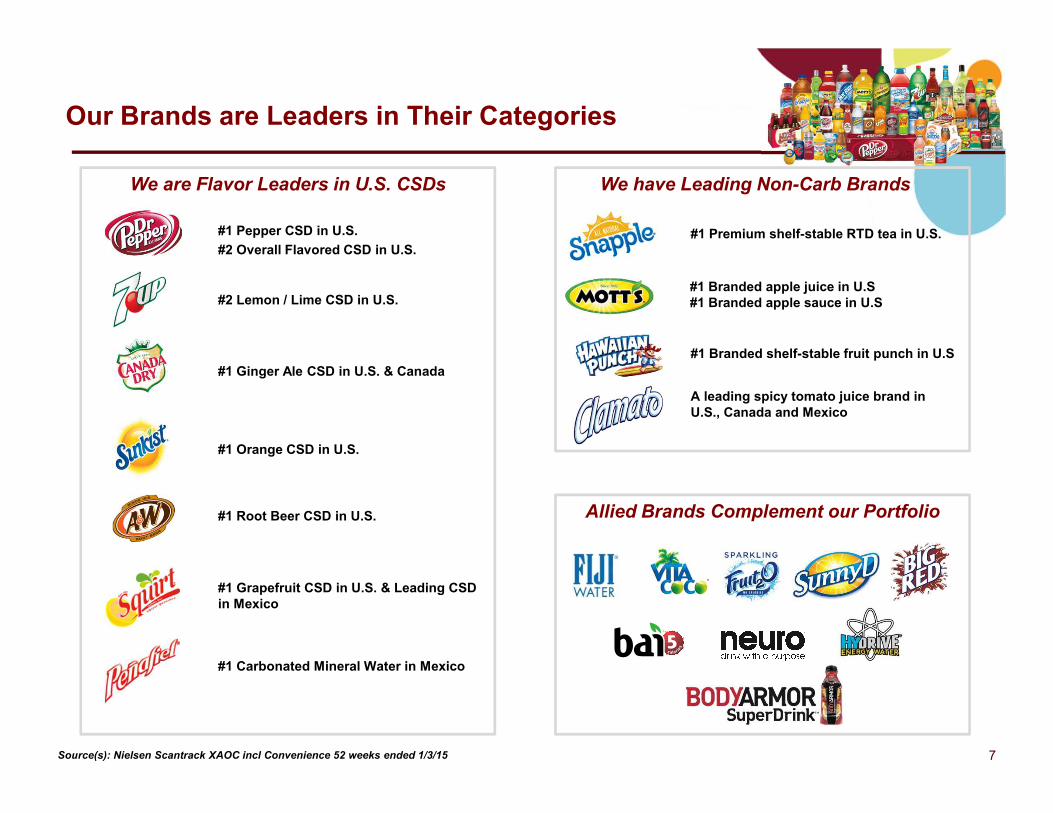

Our Brands are Leaders in Their Categories

#1 Pepper CSD in U.S.

#2 Overall Flavored CSD in U.S.

#2 Lemon / Lime CSD in U.S.

#1 Ginger Ale CSD in U.S. & Canada

#1 Orange CSD in U.S.

#1 Root Beer CSD in U.S.

#1 Grapefruit CSD in U.S. & Leading CSD

in Mexico

#1 Carbonated Mineral Water in Mexico

#1 Premium shelf-stable RTD tea in U.S.

#1 Branded apple juice in U.S

#1 Branded apple sauce in U.S

We are Flavor Leaders in U.S. CSDs

Allied Brands Complement our Portfolio

We have Leading Non-Carb Brands

Source(s): Nielsen Scantrack XAOC incl Convenience 52 weeks ended 1/3/15

#1 Branded shelf-stable fruit punch in U.S

A leading spicy tomato juice brand in

U.S., Canada and Mexico

8

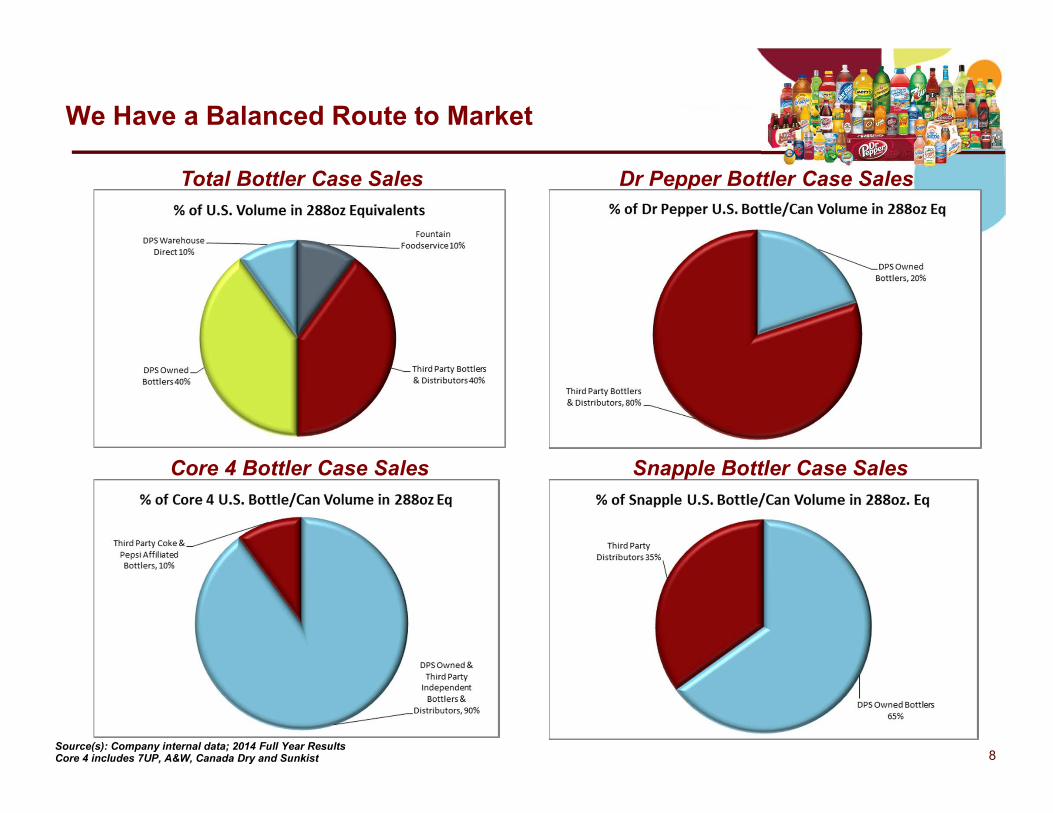

We Have a Balanced Route to Market

Total Bottler Case Sales Dr Pepper Bottler Case Sales

Core 4 Bottler Case Sales Snapple Bottler Case Sales

Source(s): Company internal data; 2014 Full Year ResultsCore 4 includes 7UP, A&W, Canada Dry and Sunkist

Build Our Brands

Execute With Excellence

Rapid Continuous Improvement

9

Strategic Priorities

10

We Focus on Building Our Brands

Investing in Marketing and Focusing on Marketing Return on Investment

Consumer Relevant Programming

Source(s): DPS SEC filings

Brand Innovation

11

We Focus on Consumer-Driven Innovation

World Class R&D Team and Facilities

Packaging Innovation

12

We Promote Balance and Encourage Active Lifestyles

We Encourage Fit and Active Lifestyles

We’re Working Together as an Industry

Build Our Brands

Execute With Excellence

Rapid Continuous Improvement

13

Strategic Priorities

14

We Focus on Execution Excellence

Priority Brand Execution through Coke & Pepsi Affiliated Bottling Networks

Driving Distribution & Availability in DSD

Accelerating Growth of Allied BrandsWinning with Hispanics

15

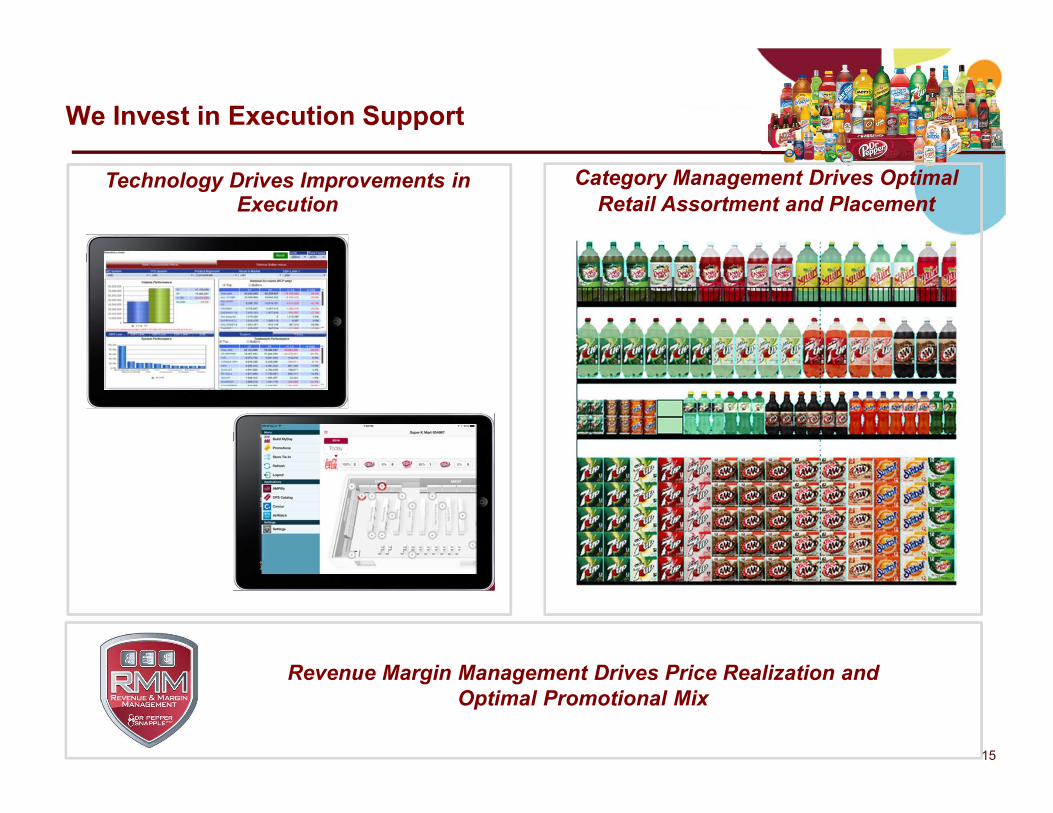

We Invest in Execution Support

Technology Drives Improvements in Execution

Revenue Margin Management Drives Price Realization and

Optimal Promotional Mix

Category Management Drives Optimal

Retail Assortment and Placement

Build Our Brands

Execute With Excellence

Rapid Continuous Improvement

16

Strategic Priorities

17

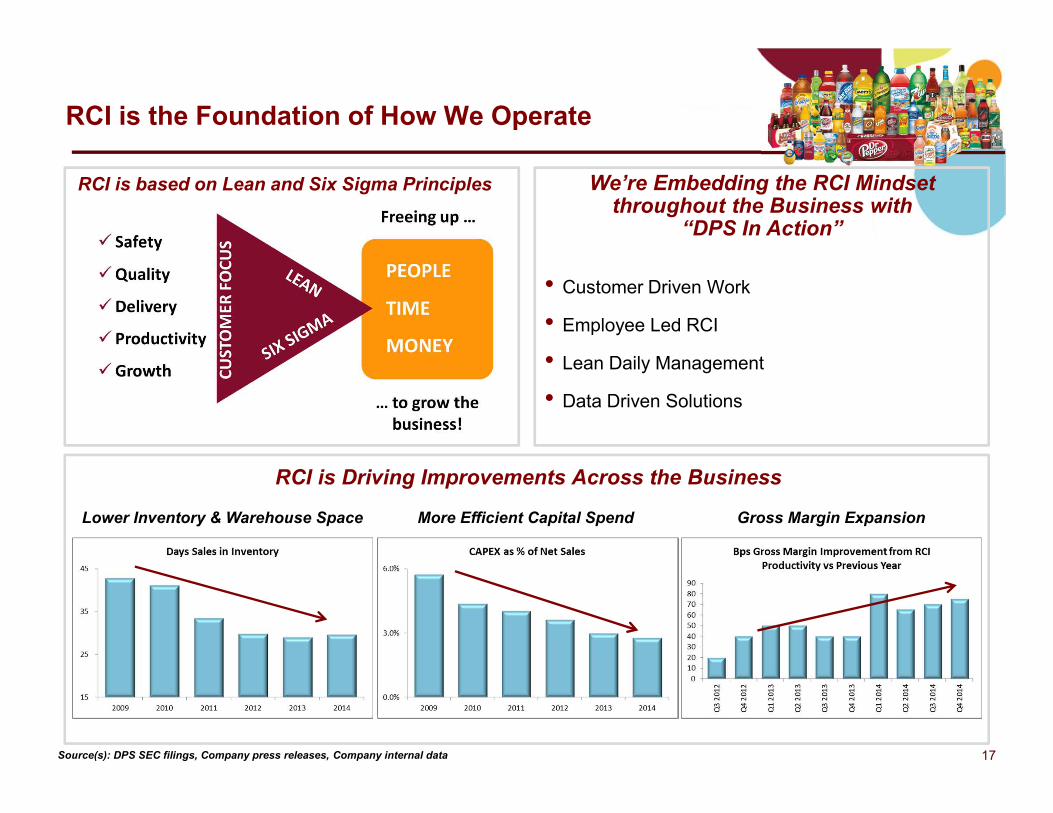

RCI is the Foundation of How We Operate

RCI is based on Lean and Six Sigma Principles

RCI is Driving Improvements Across the Business

We’re Embedding the RCI Mindset throughout the Business with

“DPS In Action”

• Customer Driven Work

• Employee Led RCI

• Lean Daily Management

• Data Driven Solutions

Lower Inventory & Warehouse Space More Efficient Capital Spend Gross Margin Expansion

Source(s): DPS SEC filings, Company press releases, Company internal data

18

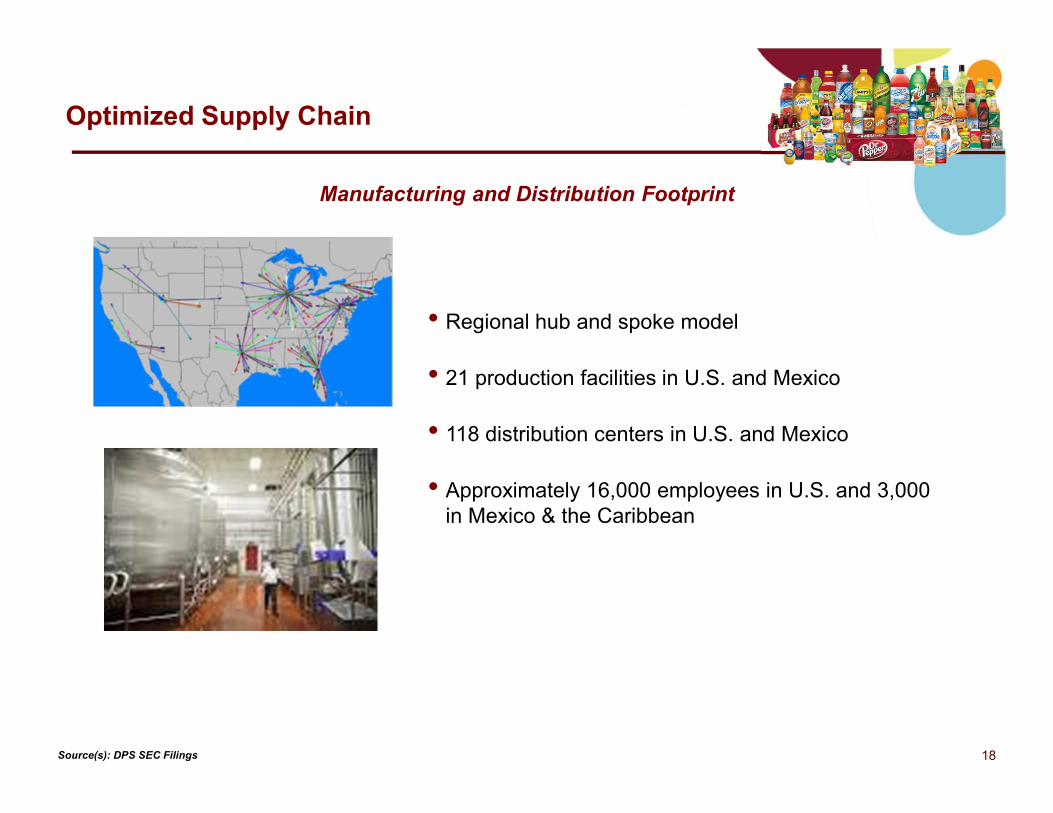

Optimized Supply Chain

Manufacturing and Distribution Footprint

• Regional hub and spoke model

• 21 production facilities in U.S. and Mexico

• 118 distribution centers in U.S. and Mexico

• Approximately 16,000 employees in U.S. and 3,000 in Mexico & the Caribbean

Source(s): DPS SEC Filings

19

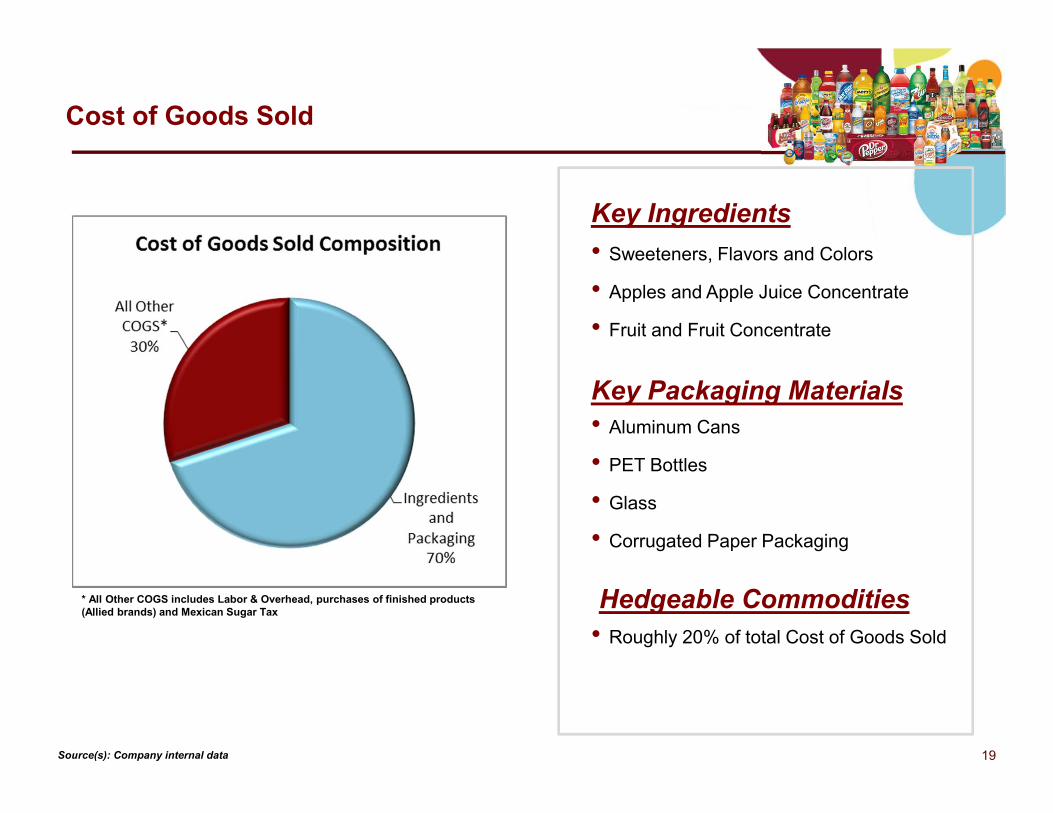

Cost of Goods Sold

Key Ingredients

Key Packaging Materials

• Sweeteners, Flavors and Colors

• Apples and Apple Juice Concentrate

• Fruit and Fruit Concentrate

• Aluminum Cans

• PET Bottles

• Glass

• Corrugated Paper Packaging

Hedgeable Commodities

• Roughly 20% of total Cost of Goods Sold

Source(s): Company internal data

* All Other COGS includes Labor & Overhead, purchases of finished products

(Allied brands) and Mexican Sugar Tax

20

International Expansion

Developing International Markets Organically

• Slow development over time with Non-carbs

• Bought back Snapple Asia Pacific rights in 2013

• Western Europe license agreement starting in 2015

• Distributor model

CSD Expansion limited to North America

• Dr Pepper owned by Coke system outside North America

• 7UP owned by Pepsi system outside United States

• Both rights sold while under previous ownership

Source(s): Company internal data

21

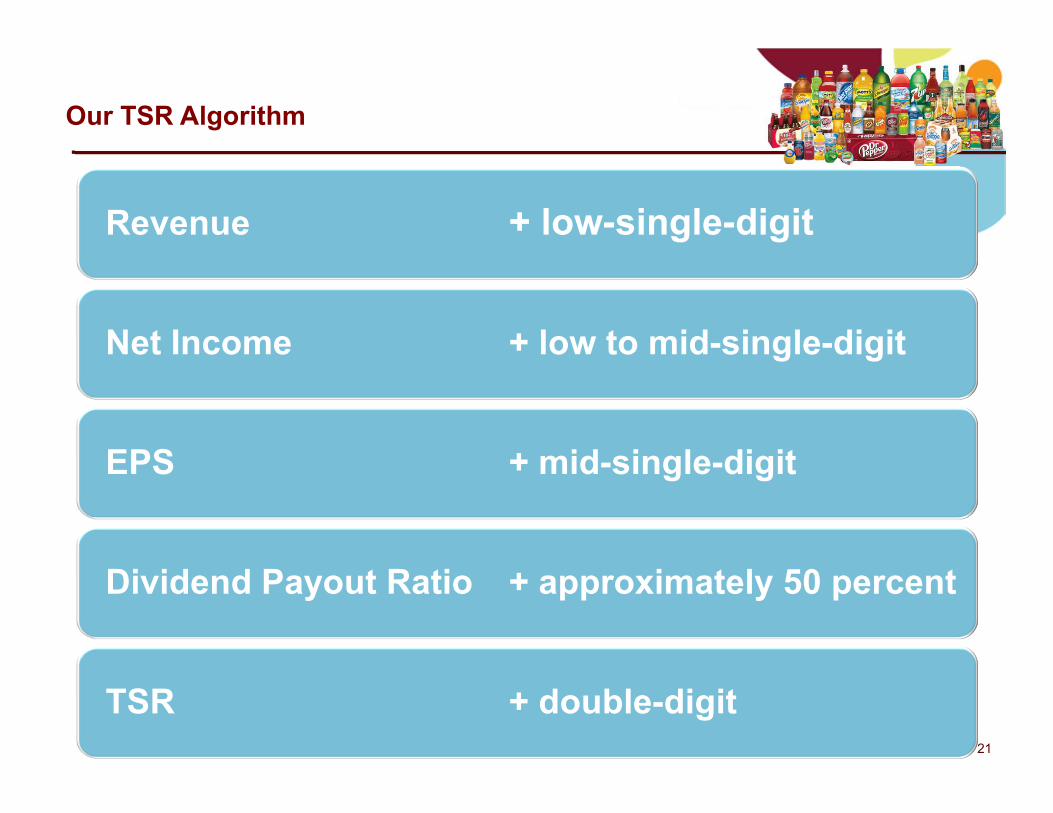

Our TSR Algorithm

Revenue

Net Income

EPS

Dividend Payout Ratio

TSR

+ low-single-digit

+ low to mid-single-digit

+ mid-single-digit

+ approximately 50 percent

+ double-digit

22

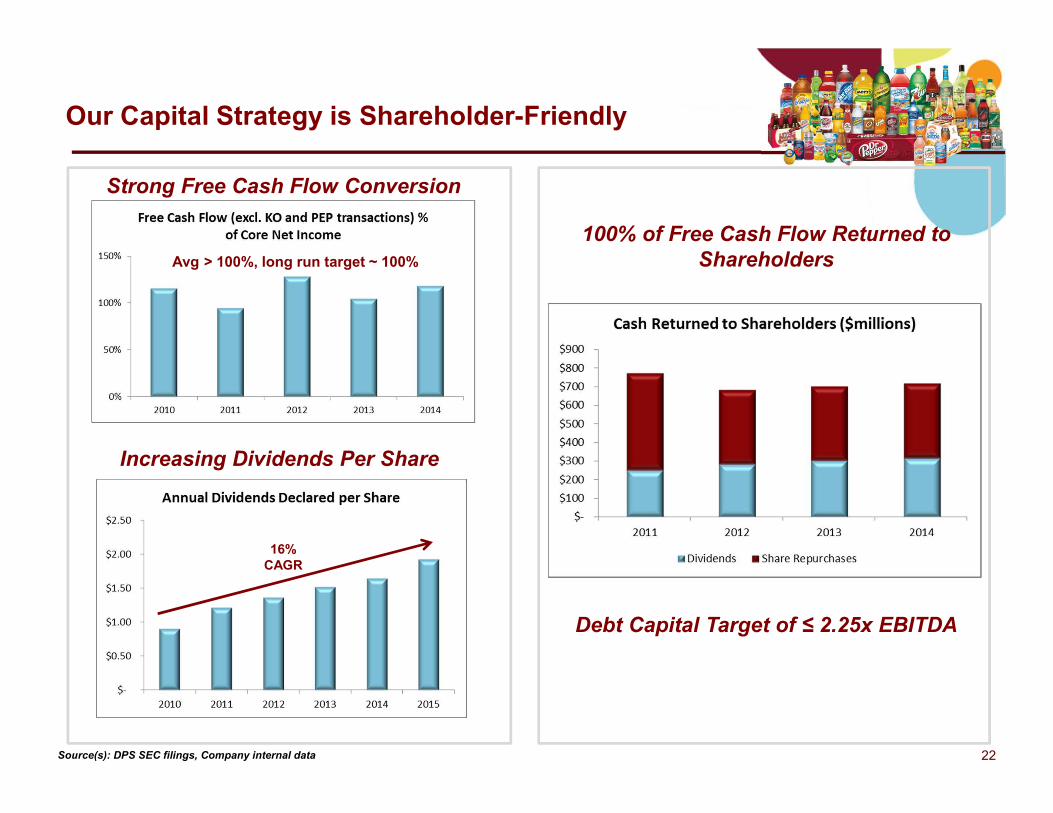

Our Capital Strategy is Shareholder-Friendly

Debt Capital Target of ≤ 2.25x EBITDA

100% of Free Cash Flow Returned to

Shareholders

Increasing Dividends Per Share

Source(s): DPS SEC filings, Company internal data

16%

CAGR

Strong Free Cash Flow Conversion

Avg > 100%, long run target ~ 100%

23

Experienced Commercial Leadership

Larry Young, President and CEO

Over 30 years of experience including the Pepsi system and DPS

Marty Ellen, CFO

Over 25 years of experience including the Pepsi system and DPS

Jim Johnston, President – Beverage Concentrates and Latin America

Beverages

Over 30 years of experience in Sales, Marketing and Strategy in the industry

Rodger Collins, President – Packaged Beverages

Over 35 years experience with the company in Sales Leadership and Marketing

Jim Trebilcock, EVP Marketing

Over 25 years of experience with the company in Marketing Leadership

Source(s): Company internal data