draft decisi… · web viewagl’s submission stated that there did not appear to be any logical...

TRANSCRIPT

Access Arrangement draft decisionMultinet Gas (DB No.1) Pty LtdMultinet Gas (DB No.2) Pty Ltd

2013–17

Part 2Attachments

September 2012

© Commonwealth of Australia 2012

This work is copyright. Apart from any use permitted by the Copyright Act 1968, no part may be reproduced without permission of the Australian Competition and Consumer Commission. Requests and inquiries concerning reproduction and rights should be addressed to the Director Publishing, Australian Competition and Consumer Commission, GPO Box 3131, Canberra ACT 2601.

Shortened formsShortened form Full title

2008-12 access arrangement Access arrangement for Multinet effective from 1 January 2008 to 31 December 2012 inclusive

2008-12 access arrangement period 1 January 2008 to 31 December 2012 inclusive

2013-17 access arrangement period 1 January 2013 to 31 December 2017

2018-22 access arrangement Access arrangement for Multinet effective from 1 January 2018 to 31 December 2022 inclusive

ACCC Australian Competition and Consumer Commission

AER Australian Energy Regulator

access arrangement information Multinet, Access arrangement information, 30 March 2012

access arrangement proposal Multinet, Access arrangement proposal, 30 March 2012

capex capital expenditure

CAPM capital asset pricing model

CPI consumer price index

Code National Third Party Access Code for Natural Gas Pipeline Systems

DRP debt risk premium

ESC Essential Services Commission (Victoria)

MRP market risk premium

Multinet Multinet Gas (DB No.1) Pty Ltd (ACN 086 026 986), Multinet Gas (DB No.2) Pty Ltd (ACN 086 230 122)

NGL National Gas Law

NGO National Gas Objective

NGR National Gas Rules

opex operating expenditure

PTRM post tax revenue model

RAB regulatory asset base

RFM roll forward model

RPP revenue pricing principles

WACC weighted average cost of capital

AER draft decision | Multinet 2013–17 | Attachments

Contents Shortened forms...................................................................................i

Contents...............................................................................................i

1 Pipeline Services..........................................................................1

2 Capital base.................................................................................6

3 Capital expenditure....................................................................20

4 Rate of return.............................................................................72

5 Depreciation.............................................................................115

6 Operating expenditure..............................................................128

7 Incentive mechanisms...............................................................170

8 Corporate income tax................................................................185

9 Demand....................................................................................195

10 Tariff setting.............................................................................203

11 Tariff variation mechanism........................................................213

12 Non-tariff components..............................................................247

AER draft decision | Multinet 2013–17 | Attachments

1 Pipeline ServicesThe NGR includes a number of requirements with respect to:

identifying the pipeline which the access arrangement relates to1 and

the services which Multinet proposes to offer to provide by means of that pipeline.2

1.1 AER’s draft decision

The AER considers that Multinet has met its obligations to describe the pipeline services and specify the reference services that it proposes to offer.

The AER approves Multinet's proposed ancillary reference services but does not approve Multinet's proposed reference services.

1.2 Multinet's proposal

Multinet’s access arrangement proposal describes the type and nature of pipeline services to be provided by its Victorian gas distribution network. This includes references services (services that are likely to be sought by a significant part of the market) and non reference services. Multinet’s access arrangement sets out a single reference service and four ancillary reference services.

1.3 Assessment approach

In its access arrangement proposal Multinet is required to specify all reference services.3 A reference service is a pipeline service that is likely to be sought by a significant part of the market.4 A pipeline service is a:

service provided by means of a pipeline, including a:

haulage service

service facilitating the interconnection of pipelines

a service ancillary to one of these services.5

A reference service must also be consistent with the NGO.6

The AER's approach to assessing these requirements involves first identifying the covered pipeline that will be regulated through the access arrangement. This involves identifying:

1 NGR, r. 101(1).2 NGR, r. 48(1)(b).3 NGR, r. 48(1)(c), NGR, r. 101(1).4 NGR, r. 101(2).5 NGL, s. 2.6 NGR, r. 100(a).

AER draft decision | Multinet 2013–17 | Attachments 1

the covered pipeline under the earlier access arrangement

any extensions or expansions that were completed during the earlier access arrangement and which are taken to be 'covered' under that access arrangement's extension and expansion requirements.

After identifying the covered pipeline the next step is to describe the pipeline services and reference service that will be regulated through the access arrangement. It is then possible to:

calculate the reference tariff

determine the other non-tariff terms and conditions which will form part of the access arrangement.7

1.4 Reasons for decision

Identification of the pipeline

The AER considers that Multinet has met its obligations pursuant to r. 48(1)(a) of the NGR.

Clause 1.2 of Multinet’s access arrangement proposal states that ‘the Access Arrangement as revised comprises this document together with the plans of the Distribution System lodged with the Regulator’ and that ‘A description of the Distribution System can be inspected at www.multinetgas.com.au’. The Access Arrangement Information lodged by Multinet with the access arrangement proposal contains a description of Multinet’s distribution network.8

Description of the pipeline services

The AER considers that the pipeline services that Multinet proposes to offer are adequately described.9

Multinet has described the pipeline services being offered as haulage reference services and ancillary reference services available to users and prospective users of its distribution system. These services will be offered at the reference tariffs in accordance with its reference tariff policy set out in its proposal.10

Specification of the reference service

The glossary to Multinet’s access arrangement proposal defines Haulage Reference Services as including the injection, conveyance and withdrawal of gas form transfer and distribution supply points (as applicable).

7 Such as queuing requirements, extension and expansion requirements, and capacity trading requirements.

8 Multinet, access arrangement information,30 March 2012, s.1.2.9 In accordance with NGR 48(1)(b).10 Multinet, Access arrangement proposal, Part A–Principal arrangements, 30 March 2012, clause

5.1.

AER draft decision | Multinet 2013–17 | Attachments 2

Schedule 1 of Multinet’s access arrangement proposal defines Ancillary Reference Services as meter and gas installation tests, disconnection, energisation and reconnection and special meter readings.

Multinet states that the Reference Services are likely to be sought by a significant part of the market when sought by a Retailer. The AER considers that it is unnecessary to include the qualification 'when sought by a retailer'. The AER considers that the proposed Reference Services are likely to be sought by a significant part of the market, regardless of the market activity of the access seeker.

Reference service

Multinet’s access arrangement proposal states that the reference services provided by Multinet, as described above, are likely to be sought by a significant part of the market.11

The AER considers that a service that provides for the injection, conveyance and withdrawal of gas is likely to be sought by a significant part of the market. Accordingly, the AER is satisfied that the reference services proposed by Multinet are likely to be sought by a significant part of the market. This means they must be covered by the access arrangement.

However, as discussed above, the AER does not consider it necessary to contain the qualification that the Reference Services are likely to be sought by a significant part of the market, when sought by a retailer. The AER considers that the focus of r. 101(2) is on whether a significant part of the market is likely to seek the service, not whether the person seeking the service belongs to a class that forms a significant part of the market.

The AER’s draft decision is based on the current definitions of a reference service and rebateable service. These definitions are currently the subject of a proposed rule change.12 The AEMC is presently considering whether any rule change is to take effect for the purposes of the review of the Victorian gas access arrangements for 2013-17.13 In the event that the AEMC determines in its 1 November 2012 final rule determination that the rule change is to apply to the current review, Multinet may need to take this into account when revising its proposal if the rule change affects its proposal.

11 Multinet, Access arrangement proposal: Part A–Principal arrangements, clause 5.1.1.12 On 5 August 2011 the AER submitted a rule change proposal to amend the definition of a

reference service and rebateable service in the NGR. The AEMC released its draft rule determination in March 2012. On 27 July 2012, the AEMC extended the time for the making of its final rule determination to 1 November 2012.

13 On 13 September 2012, the AEMC released a Consultation Paper on the rule change which specifically invites comments on “the operation and application of the final rule to access arrangement reviews already in progress” and the need for “transitional arrangements if the final rule was to apply to access arrangements that are currently being assessed by the AER” (pg 26). See: http://www.aemc.gov.au/gas/rule-changes/open/reference-service-and-rebateable-service-definitions.html

AER draft decision | Multinet 2013–17 | Attachments 3

Ancillary reference services

The AER considers that the proposed ancillary reference services are likely to be sought by a significant part of the market. It is possible that there are other services that may also be sought by a significant part of the market. However, the submissions the AER received did not address whether these services are services that are likely to be sought by a significant part of the market. As a result, there is insufficient evidence before the AER to find that these services are ancillary reference services.

The ancillary reference services proposed by Multinet are largely consistent with those in its current access arrangement.

The AER received submissions from AGL and Origin on ancillary reference services.14 Concerns in the submissions were general in nature. The submissions did not identify any specific services currently provided as pipeline services other than reference services that should be included as an ancillary reference service.

AGL’s submission stated that there did not appear to be any logical reason for why some services are included in the definition of ancillary reference services, while others are excluded. AGL included meter and gas installation testing as an example of what it considers is the inconsistent approach taken by the three distribution businesses. AGL did not state its view as to which category such a service should fall within.15 AGL did not state whether it believes meter and gas installation tests are accessed by a significant part of the market and whether these tests should be included in the definition of ancillary reference services.

AGL stated that its preference is to include services that can only be performed by the monopolistic service providers in the definition of ancillary reference services.16

The AER notes AGL's preference. However, AGL does not provide a list of specific ancillary services that it believes are likely to be sought by a significant part of the market.

Origin also submitted that the definitions of ancillary and excluded (negotiated) services are not consistent across the three distributors and Origin would propose that the definitions be made consistent. Origin submits that all monopoly services other than standard haulage services should be defined as ancillary.17 However, Origin’s submission does not specify exactly what services it believes are likely to be sought by a significant part of the market.

14 AGL, Submission to the AER: SP AusNet, Envestra and Multinet access arrangement proposals, 29 June 2012, Attachment A; Origin, Submission to the AER: SP AusNet, Envestra and Multinet access arrangement proposals, 28 June 2012, p. 3.

15 AGL, Submission to the AER: SP AusNet, Envestra and Multinet access arrangement proposals, 29 June 2012, p. 3.

16 AGL, Submission to the AER: SP AusNet, Envestra and Multinet access arrangement proposals, 29 June 2012, Attachment A.

17 Origin, Submission to the AER: SP AusNet, Envestra and Multinet access arrangement proposals, 28 June 2012, page 3.

AER draft decision | Multinet 2013–17 | Attachments 4

1.4.1Non reference services

Non reference services (negotiated or excluded services) are outside the scope of an access arrangement. Therefore, the AER’s decision in respect of Multinet’s access arrangement proposal does not extend to such services.

Multinet stated that it will provide pipeline services other than reference services as agreed or otherwise in accordance with Regulatory instruments.18 These services include Tariff D Connection, Tariff L Connection and Tariff V Complex Connection.19

The AER did not receive any submissions that address whether these services are likely to be sought by a significant part of the market.

An access arrangement is required to contain pipeline services that are reference services.20 If a service is unlikely to be sought by a significant part of the part market, it will not be a reference service–it will be a negotiated or excluded service.

AGL submitted that excluded or negotiated services (pipeline services other than reference services) charges are becoming less transparent and more arbitrary. It considers that the number of disputes between service providers and retailers about negotiated services has increased in recent years. AGL submitted that after it questioned the veracity and reasonableness of certain negotiated service charges with one service provider, the service provider threatened to withdraw its services unless AGL signed an excluded services agreement.

AGL claims that service providers have little incentive to perform distribution services in a timely manner (as they exclude their liability). Further, since third parties do not provide some of those services, AGL claims retailers have no option but to accept the service provider’s quoted negotiated service charges. AGL submitted that negotiated services should therefore be listed and their corresponding fees included in the access arrangement.21

AGL has not provided specific details of any negotiated or excluded services that it considers would be sought or likely to be sought by a substantial part of the market i,e. reference services or ancillary services. In the absence of any specific examples, the AER is unable to assess whether there are any such services.

In reaching its final decision, the AER will consider any submissions it receives in response to this draft decision. This includes submissions about further possible reference services or ancillary reference services. If a party making submissions considers that there are such services, it should give reasons why it considers they are likely to be sought by a significant part of the market.

18 Multinet, Access arrangement proposal, Part A - Principal arrangements, 30 March 2012, clause 5.1.3.

19 Multinet, Access arrangement proposal, Part A - Principal arrangements, 30 March 2012, clause 5.1.3.

20 NGR, r. 48(1)(c); NGR, r. 101(2); NGL s. 2. 21 AGL, Submission to the AER: SP AusNet, Envestra and Multinet access arrangement proposals,

29 June 2012, Attachment B.

AER draft decision | Multinet 2013–17 | Attachments 5

In the absence of further evidence, the AER proposes to monitor these non reference services, the associated revenues, and demand during the access arrangement period. The AER will reconsider whether such services should be part of the reference service, ancillary reference services, or additional reference services, at the next access arrangement review.

1.4.2Revisions

Revision 1.1: amend clause 5.1.1 as follows:

Delete 'when sought by a retailer' from the last line in the first paragraph.

AER draft decision | Multinet 2013–17 | Attachments 6

2 Capital baseThe capital base roll forward accounts for the value of Multinet's regulated assets over the access arrangement period. The opening capital base value for a regulatory year is rolled forward by indexing it for inflation, adding any conforming capex, and subtracting depreciation and other possible factors (for example, disposals or customer contributions). Following this process, the AER arrives at a closing value of the capital base at the end of the relevant year. The opening value of the capital base is used to determine the return of capital (regulatory depreciation) and return on capital building block allowances.

The AER is required to make a decision on Multinet's opening capital base as at 1 January 2013 for the 2013–17 access arrangement period. The AER is also required to make a decision on Multinet's projected capital base for the 2013–17 access arrangement period. This attachment presents the AER's draft decision on these matters.

2.1 Draft decision

The AER does not approve Multinet's proposed opening capital base of $1072.9 million as at 1 January 2013 because it considers that some of Multinet's inputs into the capital base roll forward model (RFM) do not comply with NGR.22 These include:

Multinet's revised estimate for capex in 2012

formulae and calculation errors in Multinet's proposed capital base models.

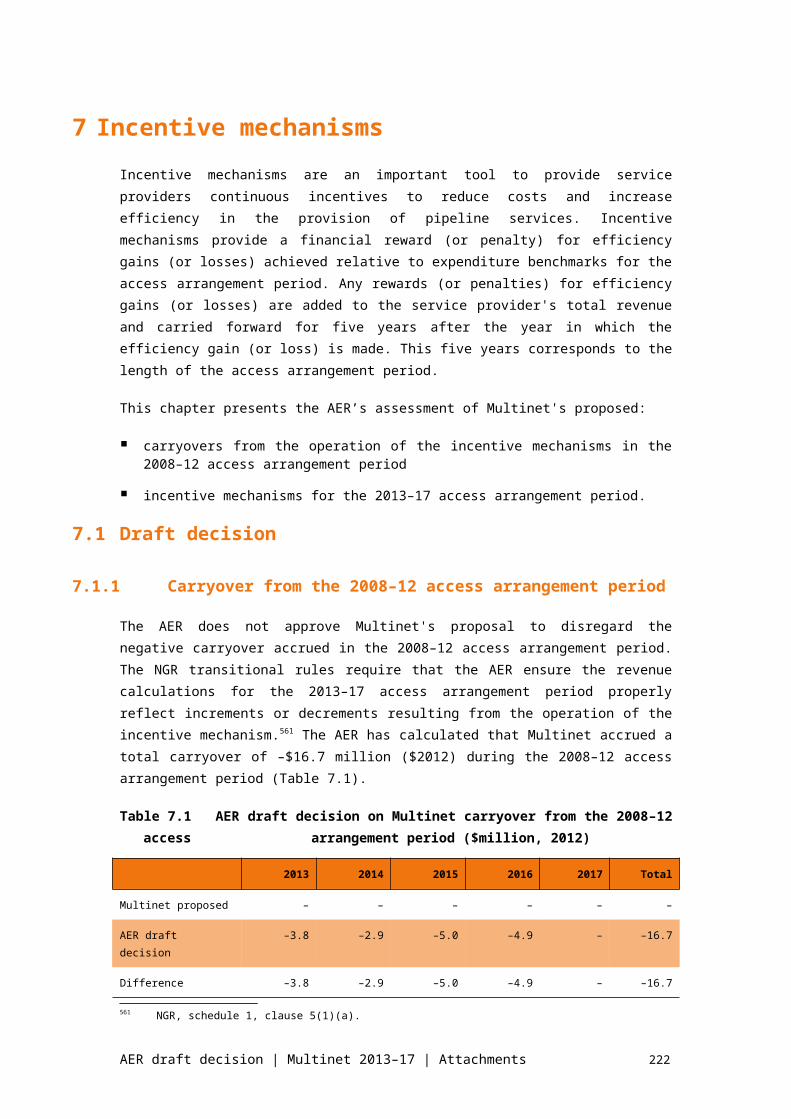

After adjusting these inputs, the AER has determined an opening capital base of $1016.5 million ($nominal) as at 1 January 2013, which is approximately $56 million less than that proposed by Multinet. Table 2.1 summarises the AER's draft decision on the roll forward of Multinet's capital base during the 2008–12 access arrangement period.

The AER approves some aspects of Multinet's proposal to determine the opening capital base as at 1 January 2013. These include:

the opening capital base at 1 January 2007, which is consistent with the value adopted in the ESC's further final decision for the 2008–12 gas access arrangement review

the use of forecast depreciation as set by the ESC.

22 NGR, r. 77(2).

AER draft decision | Multinet 2013–17 | Attachments 7

Table 2.1 AER's draft decision on Multinet's capital base roll forward for the 2008–12 access arrangement period ($million, 2012)

2008 2009 2010 2011 2012

Opening capital base 1082.1 1071.8 1033.1 1017.8 1025.8

Capex 41.2 39.1 40.7 64.5 47.6a

Less: customer contributions 2.4 25.9 2.4 2.2 2.0

Less: depreciation 49.1 51.8 53.6 54.3 54.9

Closing capital base 1071.8 1033.1 1017.8 1025.8 1016.5

Opening capital base at 1 January 2013 1016.5

Source: AER analysis.(a) The AER has approved 2012 capex values equal to the ESC's benchmark capex, adjusted for

actual growth. This is consistent with the ESC's capex incentive scheme and is discussed in section 2.4.2.

Based on the approved opening capital base and the AER's draft decisions on forecast capex and depreciation, and inflation, the AER has determined a projected closing capital base of $1097.0 million ($nominal) as at 31 December 2017. Table 2.2 sets out the projected roll forward of the capital base during the 2013–17 access arrangement period.

Table 2.2 AER's draft decision on projected capital base roll forward for the 2013–17 access arrangement period ($million, nominal)

2013 2014 2015 2016 2017

Opening capital base 1 016.5 1 052.1 1 065.9 1 079.6 1 094.2

Net capex 50.4 34.5 37.2 40.7 31.9

Less: depreciation 40.3 47.0 50.2 53.1 56.5

Indexation 25.4 26.3 26.6 27.0 27.4

Closing capital base 1 052.1 1 065.9 1 079.6 1 094.2 1 097.0

Source: AER analysis.

2.2 Multinet's proposal

Multinet proposed adopting an opening capital base as at 1 January 2008 of $1085.9 million ($2012).23 This included an increase of $0.9 million from the

23 Multinet, 2013–17 access arrangement review—Access arrangement information, March 2012, p. 165. (Multinet, Access arrangement information, March 2012).

AER draft decision | Multinet 2013–17 | Attachments 8

previous access arrangement review to reflect the difference between the ESC's approved capex for 2007 and Multinet's actual capex for 2007.

Based on the opening capital base as at 1 January 2008 and the roll forward of the capital base in the 2008–12 access arrangement period, Multinet proposed an opening capital base of $1072.9 million as at 1 January 2013. This is shown in Table 2.1.

Table 2.1 Multinet's proposed capital base roll forward during the 2008–12 access arrangement period ($million, 2012)

2008 2009 2010 2011 2012

Opening capital base 1085.9 1075.6 1037.0 1021.7 1029.7

Capex 41.2 39.1 40.7 64.5 99.0

Less: customer contributions 2.4 25.9 2.4 2.2 1.0

Less: disposals – – – – –

Less: depreciation 49.1 51.8 53.6 54.3 54.9

Closing capital base 1075.6 1037.0 1021.7 1029.7 1072.9

Opening capital base at 1 January 2013

1072.9

Source: Multinet, Access arrangement information, March 2012, p. 167.

2.2.2Capital expenditure in the 2008–12 access arrangement period

Multinet indicated it has incurred capex of $284.6 million ($2012) in the 2008–12 access arrangement period.24 This amount included actual capex from 2007–2011, and Multinet's current forecast of capex for 2012.

Multinet proposed that its capex amounts comply with the relevant NGR requirements and should be included in the opening capital base for the 2008–12 access arrangement period as set out in Table 2.1. The capex proposed under each category driver is discussed in more detail in attachment 3.

24 Multinet, Response to the AER's initial information request—Asset base and depreciation calculation model, 11 May 2012.

AER draft decision | Multinet 2013–17 | Attachments 9

Table 2.1 Multinet's proposed conforming capital expenditure for the earlier access arrangement period ($million, 2012)

2008 2009 2010 2011 2012 Total

Transmission and distribution 25.6 22.3 19.3 30.8 33.2 131.2

Services 8.7 10.1 9.8 4.1 18.5 51.1

Cathodic protection 0.1 0.2 0.1 0.2 0.8 1.3

Supply regulators/ Valve stations 2.7 1.6 1.0 2.0 4.0 11.3

Meters 3.1 3.6 4.0 3.0 3.2 16.8

Land and buildings – – – – – –

IT 0.9 1.3 6.4 23.8 39.4 71.8

SCADA 0.1 0.1 – 0.6 – 0.8

Other – – 0.2 0.1 – 0.3

Total net capex 41.2 39.1 40.7 64.5 99.0 284.6

Source: Multinet, Response to the AER's initial information request, 11 May 2012.Note: Totals may not add due to rounding.

Multinet's capital base models include its disaggregated asset classes as applied in the PTRM. These differ from the asset classes approved by the ESC and included in Multinet's access arrangement information. The AER has used the disaggregated asset classes to roll forward the capital base.

2.2.3Adjustment to the capital base for inflation in the 2008–12 access arrangement period

Multinet proposed to roll forward its capital base in real 2006 dollar terms, and then apply a CPI adjustment to determine the opening capital base as at 1 January 2013. Specifically, Multinet proposed to apply six years of actual inflation to index the opening capital base from real 2006 dollars to real 2012 dollars for insertion into the post-tax revenue model (PTRM). It determined the six years of actual inflation using September–September annual changes in CPI.25

2.2.4Depreciation in the 2008–12 access arrangement period

Multinet proposed to depreciate its capital base roll forward for the 2008–12 access arrangement using forecast straight-line depreciation, as approved by the ESC in its 2008–12 gas access arrangement review.26

25 Multinet, Opening capital base model, April 2012.26 Multinet, Access arrangement information, March 2012, p. 151.

AER draft decision | Multinet 2013–17 | Attachments 10

2.2.5Projected capital base over the 2013–17 access arrangement period

Multinet proposed a projected closing capital base as at 31 December 2017 of $1301.4 million ($nominal).27 The projected roll forward of the capital base during the 2013–17 access arrangement period is shown in Table 2.1. Multinet has included in its capital base projection:

annual forecast inflation of 2.51 per cent28

forecast straight-line depreciation, which is discussed in more detail in attachment 5. Multinet proposed to use this forecast depreciation to determine the roll forward of the opening capital base at the next access arrangement review for the 2018–22 access arrangement period.29 Multinet has also included in its forecast depreciation proposal some accelerated straight-line depreciation linked to redundant assets to be replaced before the end of their economic lives.

Table 2.1 Multinet's proposed projected capital base roll forward during the 2013–17 access arrangement period ($million, 2012)

2013 2014 2015 2016 2017

Opening capital base

1072.9 1133.0 1179.5 1218.2 1265.3

Net capex 87.0 79.1 75.2 87.2 81.0

Less: depreciation 53.8 61.1 66.1 70.7 76.7

Indexation 26.9 28.4 29.6 30.6 31.8

Closing capital base

1133.0 1179.5 1218.2 1265.3 1301.4

Source: Multinet, Post tax revenue model, March 2012.

2.3 Assessment approach

In assessing Multinet's proposal, the AER is required to consider the transitional provisions of the NGR. This is because Multinet's access arrangement for the 2008–12 access arrangement period was ongoing when the new access regime came into force.30 The NGR provides that actual or forecast capex (new facilities investment) approved by a Relevant Regulator under section 8.21 of the Code is taken to be a decision by the AER that the capex conforms with the NGR's new capex criteria.31

27 Multinet, Post tax revenue model, March 201228 Multinet, Post tax revenue model, March 2012.29 Multinet, Access arrangement information, March 2012, pp. 166–167.30 NGR, Schedule 1, clause 1(1)(a).31 NGR, Schedule 1, clause 3(2)(a).

AER draft decision | Multinet 2013–17 | Attachments 11

The AER's approach to assessing Multinet's projected capital base is consistent with that adopted by the AER in previous gas decisions made under the NGR.32 In accordance with rr. 77(2) and 78 of the NGR, the AER applied three steps to calculate the projected capital base:

First, the AER confirms the value of the opening capital base for the first year of the 2008–12 access arrangement period (in this case, 1 January 2008). Typically, this requires making an adjustment to account for any difference between actual and estimated capex in the final year of the previous access arrangement period (in this case, 2007). This adjustment is also subject to any changes made in the AER's assessment of conforming capex for that year.

Second, the opening capital base as at 1 January 2008 is rolled forward to determine the closing capital base as at 31 December 2012. This closing capital base is also used as the value of the opening capital base for the access arrangement period as at 1 January 2013. This involves:33

adding conforming actual capex for each year—this requires assessing the capex and determining that it is consistent with the provisions of the 2008–12 access arrangement and historical regulatory accounts

removing forecast depreciation for each year based on the approach approved for the 2008–12 access arrangement

removing any capital contributions during the 2008–12 access arrangement period

adding any speculative capex or redundant assets that were reused during the 2008–12 access arrangement period

removing any redundant assets and disposals during the 2008–12 access arrangement period

indexing the roll forward each year for actual inflation.

Third, the capital base is projected over the 2013–17 access arrangement period by rolling forward the opening capital base as at 1 January 2013 to 31 December 2017. This involves taking the opening capital base:34

adding forecast conforming capex for each year

removing forecast depreciation for each year

removing the forecast value of assets to be disposed of during the 2013–17 access arrangement period

32 AER, Final decision: Jemena access arrangement, June 2010; AER, Final decision: Country Energy Gas access arrangement, March 2010; AER, Final decision: ActewAGL access arrangement, March 2010; AER, Final decision: Envestra arrangement proposal Qld, June 2011; AER, Final decision: Envestra Ltd access arrangement proposal for the SA gas network 2011–2016, June 2011 (AER, Final decision: Envestra access arrangement SA, June 2011); AER, Final decision: APT Allgas access arrangement, June 2011; AER, Final decision: NT Gas access arrangement, July 2011. AER, Final decision: Roma to Brisbane Pipeline 2012–13 to 2016–17, April 2012.

33 NGR, r. 77(2).34 NGR, r. 78.

AER draft decision | Multinet 2013–17 | Attachments 12

indexing the capital base of the roll forward each year for forecast inflation.

2.4 Reasons for draft decision

The AER considers Multinet's proposed inputs into the capital base roll forward overstate the value of the opening capital base at 1 January 2013 and consequently the projected closing capital base as at 31 December 2017. In particular, the AER considers:

Multinet's separate roll forward and depreciation models contained formulae errors. The AER has corrected the errors and adjusted Multinet's two separate models into a combined RFM for determining the opening capital base (including the opening tax asset base and depreciation calculations for the 2008–12 access arrangement period). Further, Multinet's capital base models incorrectly included the benchmark adjustment to 2007 capex and therefore overstated the opening capital base as at 1 January 2008.

The ESC's capex incentive scheme should still apply to 2012 capex. The capital base roll forward over the 2008–12 access arrangement period should therefore include benchmark 2012 capex adjusted for actual growth in demand, as per the ESC's approach.

Multinet's proposed forecast capex and depreciation inputs used to roll forward the projected capital base for the 2013–17 access arrangement period need to be amended. The AER considers that these proposed inputs do not meet the requirements of the NGR (see attachments 3 and 5 respectively).

The AER has also made other minor amendments to Multinet's capital base roll forward, which are discussed in the following sections. These amendments are individually necessary for consistency with relevant NGR requirements. The AER's detailed assessment follows.

2.4.1Opening capital base in the 2008–12 access arrangement period

The AER does not approve Multinet's proposed opening capital base as at 1 January 2008 because it does not correctly account for 2007 capex. Instead, the AER approves an opening capital base of $1082.1 million ($nominal) as at 1 January 2008, which is a reduction of $3.2 million ($2006)35 from Multinet's proposal. This amount includes the AER's adjustment to account for the difference between forecast and actual capex for 2007. The AER considers that its draft decision therefore meets the requirements under the NGR.36

The AER considers that Multinet's capital base roll forward should remove the adjusted benchmark capex for 2007 from the capital base and include in its place the actual capex for 2007. This is consistent with the ESC's approach for including in the capital base the final year capex of an access arrangement period. However, Multinet's RFM:

35 Which is equal to $3.8 million ($nominal) of the opening capital base as at 1 January 2013.36 NGR, r. 77(2)(a).

AER draft decision | Multinet 2013–17 | Attachments 13

1. Subtracts from the opening capital base as at 1 January 2008 the capex amount of $54.6 million ($2006). This amount is equal to the ESC's adjusted benchmark capex for 2007 approved at the previous access arrangement review. The adjusted benchmark capex for 2007 already included $3.2 million ($2006) of adjustment for actual growth in demand.

2. Adds back into the capital base the $3.2 million adjustment to benchmark capex for 2007.

3. Adds into the capital base $306.7 million of actual capex.

The AER considers that steps 1 and 3 are correct. However, step 2 is incorrect. The amount in step 2 is the adjustment that the ESC made to the benchmark (forecast) 2007 capex included in the capital base at the previous access arrangement review. It has already been removed as part of step 1. In response to an information request from the AER, Multinet submitted that step 2 was not an error.37 It stated that the $3.2 million should be recognised in the capital base because it does not appear as actual capex for 2007 in Multinet's regulatory accounts.

The AER does not agree with Multinet's interpretation of the ESC's approach for rolling into the capital base the adjusted benchmark capex for 2007. The adjustment to the benchmark capex for 2007 was not intended to be a permanent addition to the capital base. The adjustment was instead used to update the ESC's forecast from the 2003–07 access arrangement review in 2002. Specifically, the adjustment reflected changes to the scale of Multinet's network, and Multinet's replacement of meters and low pressure pipelines over the 2003–07 access arrangement period. The resulting adjusted benchmark value was used to determine the power of the efficiency incentive for Multinet's capex in 2007. Now that actual capex is available for 2007, Multinet's capital base should only include its conforming capex for that year.

2.4.2Conforming capital expenditure in the 2008–12 access arrangement period

The AER's assessment of conforming capex is set out in attachment 3. In determining the opening capital base as at 1 January 2013, the AER assessed whether Multinet's proposed capex amounts for the 2008–12 access arrangement are properly accounted for in the capital base roll forward.

The AER accepts that Multinet's proposed capex for the 2008–12 access arrangement period is properly included in the capital base roll forward. The AER considers it is consistent with the requirements of the NGR,38 with the exception of the following:39

estimate of 2012 capex — the AER has replaced Multinet's estimate of 2012 capex with benchmark (forecast) 2012 capex adjusted for actual growth. This is consistent with the ESC's capex incentive scheme for the 2008–12 access arrangement period

37 Multinet, Response to AER information request regarding the roll forward of the RAB, 5 June 2012.

38 NGR, r. 77(2)(b).39 The AER's detailed analysis of conforming capex by project and driver is in attachment 3.

AER draft decision | Multinet 2013–17 | Attachments 14

minor reconciliation differences between Multinet's proposal and Multinet's audited regulatory accounts.

In total, these amendments result in a reduction of $51.5 million (2012) or 18 per cent of Multinet's proposed capex amounts for the 2008–12 access arrangement period. The AER's draft decision on conforming net capex amounts as used in the capital base roll forward are set out in Table 2.1.

Table 2.1 AER's approved conforming capex for the 2008–12 access arrangement period ($million, 2012)

Asset class 2007 2008 2009 2010 2011 2012 Total

Transmission and distribution 68.4 23.2 –3.6 16.9 21.6 25.1 151.4

Services 5.0 8.7 10.1 9.8 10.6 12.1 56.3

Cathodic protection 0.1 0.1 0.2 0.1 0.1 0.1 0.7

Suppy regulators/Valve stations 1.3 2.7 1.6 1.0 1.1 1.3 9.0

Meters 3.3 3.1 3.6 4.0 4.3 13.1 31.3

Land and buildings 0.0 0.0 0.0 0.0 0.0 0.0 0.0

IT 0.9 0.9 1.3 6.4 24.3 0.3 34.1

SCADA 0.2 0.1 0.1 0.0 0.1 0.3 0.8

Other 0.0 0.0 0.0 0.2 0.1 0.0 0.3

Total net capex 79.2 38.8 13.2 38.3 62.3 52.2 284.0

Source: AER analysis.Note: Totals may not add due to rounding.

Adjustments to 2012 capex

The AER does not approve Multinet's proposed capex estimate for 2012 because it does not properly reflect increments or decrements arising from the operation of the ESC’s capex incentive scheme.40 In attachment 7, the AER has addressed the application of the ESC's capex incentive scheme from 2008–11. However, the ESC's capex incentive scheme required a distinct approach to the treatment of capex in the final year of an access arrangement period. Specifically, the ESC's approach to dealing with capex in the final year of an access arrangement period as part of its capex incentive scheme requires the following for this access arrangement review:41

the 2012 capex to be included in the opening capital base as at 1 January 2013 should be set as the adjusted benchmark 2012 capex

this adjusted benchmark 2012 capex is based on the ESC's approved benchmark 2012 capex at the previous access arrangement review. The benchmark capex is then adjusted for customer growth, meter replacement and low pressure pipeline replacement.

40 NGR Schedule 5, clause 5(1)(a).41 Essential Services Commission, Gas access arrangement review 2008–12, Final decision, March

2008, pp. 431–432.

AER draft decision | Multinet 2013–17 | Attachments 15

Multinet has instead proposed revised estimates of its actual capex for 2012. This approach changes the power of the capex incentive for 2012 compared to other years in the 2008–12 access arrangement period.

The AER will roll into the capital base Multinet's actual (conforming) capex for 2012 at the next access arrangement review. The AER considers that this approach properly applies the ESC's capex incentive scheme for the full period. This will ensure Multinet fully receives any benefits or penalties for capex that diverges from the benchmark set by the ESC. The AER's adjustments to benchmark 2012 capex are set out in Table 2.2.

Table 2.2 AER's approved benchmark capex for 2012 ($million, 2012)

Asset class Allocated ESCV benchmarka

Benchmark adjustment

AER approved

2012 gross capex

Transmission and distribution 30.4 –3.3 27.1

Services 12.1 – 12.1

Cathodic protection 0.1 – 0.1

Supply regs/Valve stations 1.3 1.3

Meters 5.0 8.1 13.0

Land and buildings – – –

IT 0.3 – 0.3

SCADA 0.3 – 0.3

Other – – –

Total gross capex 49.5 4.8 54.3

Source: AER analysis.Note: Totals may not add due to rounding.(a) These values total to the ESC's benchmark capex for 2012 set in the access arrangement

review for the 2008–12 access arrangement period. However, Multinet has disaggregated its asset classes since that previous access arrangement review. The AER has therefore allocated the total values for 2012 capex to Multinet's disaggregated asset classes using the approved asset class proportions for 2011 capex.

The AER's draft decision results in a reduction to Multinet's proposed opening capital base as at 1 January 2013 of approximately $44.7 million ($nominal), or 4 per cent of Multinet's proposed opening capital base. However, this value will be updated for actual 2012 capex at the time of the next access arrangement review. Multinet will only gain or lose the return on capital associated with the difference between the approved benchmark 2012 capex and actual 2012 capex for five years, as discussed below. The following sections explain the operation of the ESC's approach for final year capex in an access arrangement period, and the AER's proposed approach to updating the capital base for actual 2012 capex at the next access arrangement review.

AER draft decision | Multinet 2013–17 | Attachments 16

Operation of the ESC's approach for final year capex

In applying its capex incentive scheme, the ESC took the following steps:42

1. At the time of the ESC's access arrangement review, actual capex for the final year (year 5) of an access arrangement period was not yet known. The ESC therefore included in the capital base roll forward an amount equal to the benchmark capex for that year, as estimated at the earlier access arrangement review. To recognise growth in the network, the ESC adjusted this benchmark capex for growth in customer numbers, meter replacement and replacement of low pressure pipelines.

2. At the next access arrangement review, the ESC included actual capex in the capital base roll forward for the final year of the earlier access arrangement period, replacing the adjusted benchmark capex for that year.

3. The ESC made no adjustment for the accumulated return on capital associated with any difference between actual capex and the adjusted benchmark capex.

The final step allowed the service provider to gain or lose the return on capital associated with the difference between actual and the adjusted benchmark capex for five years. This ensured the power of the capex incentive scheme was the same for the final year as for the other years during the access arrangement period.

AER's approach to updating the capital base for actual capex

The AER does not operate any capex incentive schemes similar to the ESC’s. Accordingly, the AER does not typically need to set an adjusted benchmark capex for the final year of an access arrangement period to preserve incentives. Instead, it requires service providers to provide their best forecast of capex for the final year of the access arrangement period. This minimises any difference between forecast and actual capex that needs to be adjusted from the capital base at the next access arrangement review. At the next access arrangement review, the AER will adjust the capital base for:

the difference between the forecast and actual capex for the final year of the earlier access arrangement period

the five year accumulated return on capital associated with the difference between the forecast and actual capex for the final year of the earlier access arrangement period.

The AER has decided not to include a capex incentive scheme for the 2013–17 access arrangement period (see attachment 7). Under the NGR,43 the AER must ensure that revenue calculations for the 2013–17 access arrangement period properly reflect increments or decrements resulting from the operation of the ESC's capex incentive mechanism. This requires the AER to approve an adjusted benchmark capex for 2012, which will be updated for actual capex at the next access arrangement review. At that time, the AER will not adjust the capital base for the five year accumulated return on capital associated with the difference between the adjusted benchmark and actual capex for 2012. This is contrary to 42 Essential Services Commission, Gas access arrangement review 2008–12, Final decision, March

2008, pp. 431–432.43 NGR Schedule 1, clause 5(1)(a).

AER draft decision | Multinet 2013–17 | Attachments 17

the AER's standard approach, as noted above, but is required to properly reflect increments or decrements resulting from the operation of ESC's capex incentive scheme. Following this, the AER will have completed the application of the ESC's capex incentive scheme.

Multinet's models

The AER has developed a consolidated model combining all aspects of Multinet’s capital base, tax asset base and economic life roll forward calculations. The AER considers that its model:

corrects the formulae errors in Multinet's models

is more transparent than Multinet’s separate models

is consistent with the approach used in the AER’s assessment of all of the Victorian gas distribution businesses.

Multinet did not include in its proposal a supporting model to demonstrate the calculations of inputs into its proposed capital base roll forward. The AER requested from Multinet a copy of its supporting calculations for the proposed capital base roll forward.44 Multinet provided two separate models, covering the roll forward of the capital base and the tax asset base, including its depreciation calculations.45 The calculations in these models are interdependent, but the models as provided to the AER were not linked. The AER also found a number of formulae errors in Multinet’s models. Due to these errors, the AER considers Multinet's proposed calculations for its capital base roll forward:

are not arrived at on a reasonable basis46

do not represent the best forecasts or estimates possible in the circumstances.47

The AER’s consolidated RFM for Multinet is broadly based on Multinet’s proposed approaches in its models, corrected for these errors.

2.4.3Indexation of the capital base

The AER approves Multinet's total proposed indexation of the capital base over the 2008–12 access arrangement period because it will sufficiently compensate Multinet for the effects of inflation. This approach applies one year of change in the September–September CPI to index the capital base for one year. This is consistent with the AER's standard approach, and with the ESC's approach to roll forward the capital base.

44 AER, Initial information request to Multinet, 26 April 2012, p. 6.45 Multinet, Response to the AER's initial information request, 11 May 2012.46 NGR, r. 74(2)(a).47 NGR, r. 74(2)(b).

AER draft decision | Multinet 2013–17 | Attachments 18

2.4.4Depreciation used in the 2008–12 access arrangement period

The AER approves Multinet's proposal to roll forward the capital base to 1 January 2013 using forecast depreciation (straight-line method) as approved in the previous access arrangement review for the 2008–12 access arrangement period. The use of forecast depreciation to determine the opening capital base is consistent with the AER's standard approach to depreciation for gas distribution service providers.48

The AER must subtract from the capital base depreciation calculated in accordance with the relevant access arrangement as required under the NGR.49 In its previous access arrangement review, the ESC calculated a benchmark depreciation allowance for Multinet, based on its forecast capex allowance over the 2008–12 access arrangement period.50 The ESC had also previously used forecast depreciation to determine the opening capital base. The AER therefore accepts that Multinet's proposed approach is consistent with the relevant provisions in the 2008–12 access arrangement and therefore with the NGR.51

2.4.5Projected capital base during the 2013–17 access arrangement period

The AER’s forecast of Multinet’s projected capital base at 31 December 2017 is $1097.0 million ($nominal), a reduction of $204.5 million or 15.7 per cent from Multinet's proposal. This is because of the AER's draft decision having amended the inputs to the determination of the projected capital base. The AER has amended the inputs as follows:

Reduced Multinet's proposed opening capital base as at 1 January 2013 to $1016.5 million or by 5 per cent to reflect the changes required in this attachment.

Reduced to zero the opening asset values in the 'Pipeworks retirement (mains)' and 'Pipeworks retirement (services)' asset classes, and moved these asset values into the 'Transmission & distribution' and 'services' asset classes respectively. This does not change the opening capital base as at 1 January 2013, but does affect the forecast depreciation allowance. This is discussed in more detail in attachment 5.

Reduced Multinet's proposed forecast capex allowance by approximately $191 million ($2012) or 52 per cent. The AER's detailed assessment of the forecast capex allowance is set out in attachment 3.

Reduced Multinet's proposed forecast depreciation allowance by approximately $67 million ($nominal) or 37 per cent. The AER's assessment of the proposed forecast depreciation allowance is set out in attachment 5.

48 For example, AER, Final decision: Jemena access arrangement proposal, June 2010, p. 92; AER, Final decision: APT Allgas access arrangement, June 2011, p. 13; AER, Final decision: Envestra access arrangement Qld, June 2011, p. 25; AER, Final decision: Envestra access arrangement SA, June 2011, p. 28.

49 NGR, r. 77(2)(d).50 ESC, Gas access arrangement review 2008–12, Final decision, March 2008, p. 439.51 NGR, r.77(2)(d).

AER draft decision | Multinet 2013–17 | Attachments 19

Updated forecast inflation to be 2.50 per cent per annum for the 2013–17 access arrangement period. While the AER accepts Multinet's proposed approach to estimating forecast inflation, the AER has updated the forecast for this draft decision. The AER's assessment of Multinet's proposed forecast inflation is set out in attachment 4.

The capital base at the commencement of the 2018–22 access arrangement period will be subject to adjustments under the NGR.52 These adjustments include, but are not limited to:

the difference between actual and forecast capex for 2012 (the final year of the 2008–12 access arrangement period)

actual inflation and approved depreciation over the 2013–17 access arrangement period.

The AER accepts Multinet's proposal to use forecast depreciation approved in the final decision for the 2013–17 access arrangement period to establish Multinet’s opening capital base as at 1 January 2018.53 The AER approved such an approach in the decisions for Jemena Gas Networks (JGN), APT Allgas, and Envestra networks.54 This approach is also consistent with the approach outlined in the AER’s Access Arrangement Guideline.55

2.5 Revisions

The AER requires the following revisions to make the access arrangement proposal acceptable:

Revision 2.1: Make all necessary amendments to reflect the AER’s draft decision on the roll forward of the opening capital base for the 2008–12 access arrangement period, as set out in 2.1.1Table 2.1.

Revision 2.2: Make all necessary amendments to reflect the AER’s draft decision on the projected opening capital base for the 2013–17 access arrangement period, as set out in 2.1.1Table 2.2.

Revision 2.3: Make all necessary amendments to reflect the AER’s draft decision on net capex by asset class during the 2008–12 access arrangement period, as set out in 2.4.2Table 2.1.

52 NGR r. 77(2).53 Multinet, Access arrangement information, March 2012, pp. 166–167.54 AER, Final decision: Jemena access arrangement proposal, June 2010, p. 92; AER, Final decision:

APT Allgas access arrangement, June 2011, p. 13; AER, Final decision: Envestra access arrangement Qld, June 2011, p. 25; AER, Final decision: Envestra access arrangement SA, June 2011, p. 28.

55 AER, Final access arrangement guideline, March 2009, pp. 65–66.

AER draft decision | Multinet 2013–17 | Attachments 20

3 Capital expenditureThis attachment outlines the AER's assessment of Multinet's proposed capital expenditure (capex) for 2007–11 and forecast capex for the 2013–17 access arrangement period.

3.1 Draft decision

Conforming capital expenditure for 2007–11

The AER approves $231.7 million ($2012, including internal direct overheads) total net capex for 2007-11 as conforming capex under r. 79(1) of the NGR.For the purpose of the capital base roll forward, the AER has adopted the ESC's benchmark capex for 2012, adjusted for actual growth.

Table 3.1 AER approved capital expenditure by category over 2007–11 ($million, 2012)

Category 2007 2008 2009 2010 2011 2012(a)

Mains replacement 22.4 7.8 4.9 4.7 4.2 21.3

Residential connections 45.9 17.8 18.8 12.6 14.0 12.7

Commercial/industrial connections 1.6 1.6 2.8 1.9 2.5 0.9

Meters 2.2 1.8 2.0 2.5 1.8 4.4

Augmentation 7.6 6.0 6.5 7.9 12.0 5.2

IT 0.9 0.8 1.1 5.8 21.9 0.3

SCADA 0.2 0.1 0.1 0.0 0.1 0.3

Other 1.8 1.2 1.3 1.4 1.6 2.6

Internal direct overheads 0.0 0.0 0.0 0.0 0.0 0.0

Indirect overheads 0.0 4.1 1.6 4.1 6.4 0.0

GROSS TOTAL 82.6 41.2 39.1 40.7 64.5 47.6

Customer contributions 3.4 2.4 2.4 2.4 2.2 2.0

Government contributions 0.0 0.0 23.6 0.0 0.0 0.0

NET TOTAL 79.2 38.8 13.2 38.3 62.3 45.6

Source: AER analysis.Notes: (a) The AER has approved 2012 capex values equal to the ESC's benchmark capex, adjusted

for actual growth. This is consistent with the ESC's capex incentive scheme and is discussed in attachement 2.

AER draft decision | Multinet 2013–17 | Attachments 21

Conforming capital expenditure for the 2013–17 access arrangement period

The AER approves $177.7 million ($2012) total net capex of Multinet's proposed $375.3 million ($2012) total net capex for 2013–17.

Table 3.2 shows approved capex for the 2013–17 access arrangement period by category.

Table 3.2 AER approved capital expenditure by category over the 2013–17 access arrangement period ($million, 2012)

Category 2013 2014 2015 2016 2017

Mains replacement 10.5 7.8 9.9 7.7 9.0

Residential connections 12.6 12.6 12.5 12.0 11.9

Commercial/industrial connections

0.9 0.8 0.8 0.8 0.8

Meters 2.2 2.2 2.2 2.2 2.2

Augmentation – 1.7 2.3 3.5 –

IT 17.8 6.4 4.5 5.3 1.6

SCADA 0.8 0.1 0.0 0.0 0.0

Other 14.9 4.7 3.1 6.1 3.6

Internal direct overheads – – – – –

Indirect overheads – – – – –

GROSS TOTAL 59.7 36.3 35.4 37.7 29.2

Customer contributions 11.6 4.3 1.6 1.6 1.6

Government contributions – – – – –

NET TOTAL 48.1 32.1 33.8 36.1 27.6

Source: AER analysis.

Table 3.3 shows Multinet's proposed capex compared with the AER's approved allowance for each category.

Table 3.3 Comparison of AER approved and Multinet's proposed capital expenditure over the 2013-17 access arrangement period ($million, 2012)

Category Multinet proposed AER approved Difference

Mains replacement 121.3 44.8 -63%

Residential connections 96.0 61.5 -36%

AER draft decision | Multinet 2013–17 | Attachments 22

Commercial/industrial connections

12.7 4.2 -67%

Meters 14.0 11.2 -20%

Augmentation 35.1 7.4 -79%

IT 46.9 35.6 -24%

SCADA 7.4 1.0 -86%

Other 46.1 32.4 -30%

Internal direct overheads 16.4 – -100%

Indirect overheads – – 0%

GROSS TOTAL 396.0 198.4 -50%

Customer contributions 20.7 20.7 0%

Government contributions – – 0%

NET TOTAL 375.3 177.7 -53%

Source: AER analysis, Multinet.

The reasons for the AER's reductions are:

The low pressure to high pressure mains replacement program volumes are reduced in line with the annual average volumes delivered over the 2008–11 period. A pass through provision is provided to allow for changes in circumstances that may encompass a change in volumes. The average unit rate is reduced due to the AER's assessment that Multinet did not forecast unit rates on a reasonable basis as required by r. 74(2)(a) of the NGR. Multinet overstated the direct overheads in its internal cost build up of unit rates. The cast iron and low pressure designated zone programs are not approved as Multinet has not justified the need for the programs, as required under r. 79(2) of the NGR.

Residential and commercial/industrial connections capex is reduced due to Multinet's estimate of volumes and unit rates not being forecast on a reasonable basis as required by r. 74(2)(a) of the NGR. The AER was unable to corroborate NIEIR's abolishment rate and Multinet did not provide the volume information for meters, services and mains which would have allowed the AER to assess the unit rates for meters, services and mains.

Residential and commercial/industrial meter replacement capex is reduced as the AER was not satisfied that Multinet's proposed unit rates were prudent and efficient and comply with r. 79(1) of the NGR. The AER considers that Multinet’s forecast volumes of meter replacement appear commensurate with its historical replacement rate. However, Multinet did not provide sufficient evidence for the AER to establish the reasonableness of Multinet's proposed unit rates. Accordingly, the AER considers that that an average of Multinet's historical expenditure over the 2008–12 period is the best forecast available in the circumstances.56

Augmentation expenditure is reduced due to:

56 Escalated to $2012.

AER draft decision | Multinet 2013–17 | Attachments 23

project estimates not being arrived at on a reasonable basis, as required under r. 74(2)(a) of the NGR, as cost elements were not justified and gas pressure information was conflicting

the project not being justified, as required under r. 79(2) of the NGR, as solutions did not show the expected improvement in gas pressures

IT expenditure is reduced, for consistency with r. 79(1)(a) of the NGR, because:

allocations for risk and contingency were above efficient levels

The AER considered several projects, including GIS Strategy, GE Smallworld Upgrade and Data Warehouse Enhancement, are necessary but the capex forecast was above an efficient level.

SCADA expenditure is reduced, for consistency with r. 79(1)(a) and (b) of the NGR, because

one IT-related project (SCADA Separation) was found to be scheduled too early for efficient use of the assets, and related projects for SCADA infrastructure upgrade were therefore found to be not necessary

accelerated replacement of RTUs was not efficient

there is insufficient evidence of the need for several other projects, including new fringe RTUs, electronic gas detectors and upgrading equipment from monitoring to control.

Certain projects within Multinet's "Other non-demand" capex program do not comply with r. 79(1)(a) of the NGR as the AER does not consider they would be undertaken by a prudent and efficient service provider. Additionally, some projects do not comply with r. 74(2) of the NGR as the AER does not consider Multinet has demonstrated that the forecast capex for these projects was arrived at on reasonable basis or is the best possible forecast in the circumstances.

Internal direct overhead expenditure was not approved by the AER on the basis that this cost reflects a shift from costs which were previously incurred by contractors to costs which are incurred internally under the new business structure, so there is no net new cost.

AER draft decision | Multinet 2013–17 | Attachments 24

Multinet's Proposal

2007–11 period

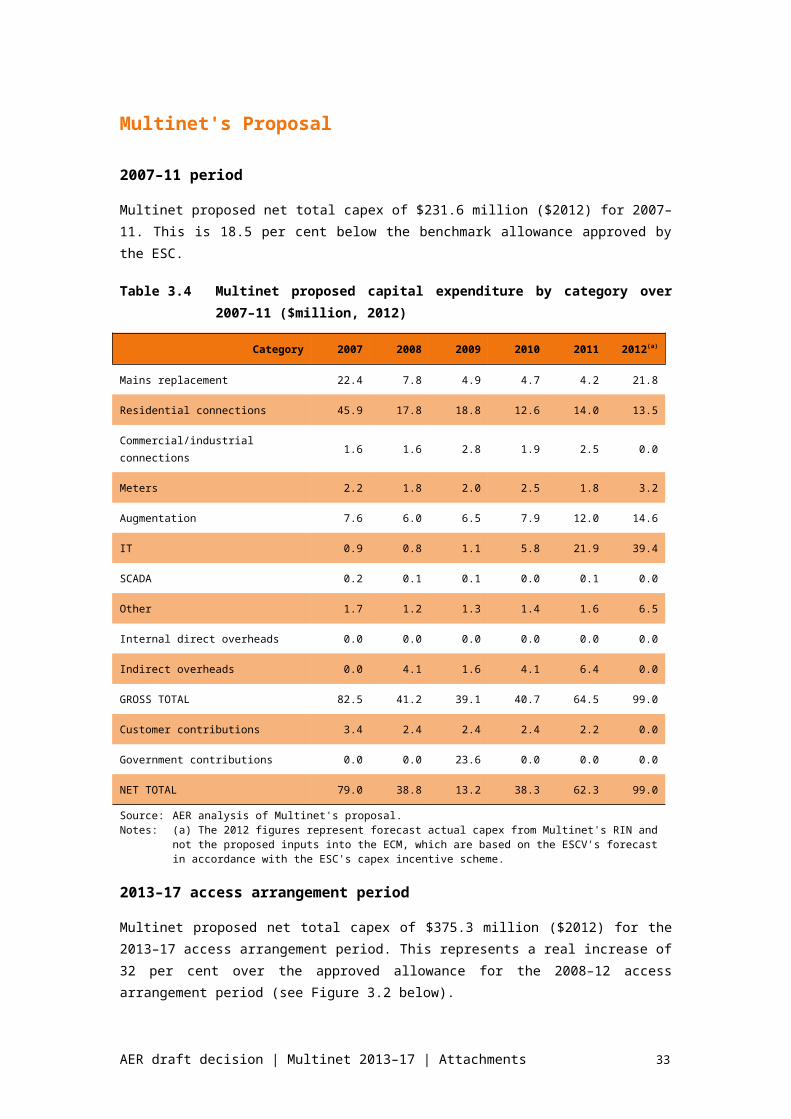

Multinet proposed net total capex of $231.6 million ($2012) for 2007–11. This is 18.5 per cent below the benchmark allowance approved by the ESC.

Table 3.4 Multinet proposed capital expenditure by category over 2007–11 ($million, 2012)

Category 2007 2008 2009 2010 2011 2012(a)

Mains replacement 22.4 7.8 4.9 4.7 4.2 21.8

Residential connections 45.9 17.8 18.8 12.6 14.0 13.5

Commercial/industrial connections 1.6 1.6 2.8 1.9 2.5 0.0

Meters 2.2 1.8 2.0 2.5 1.8 3.2

Augmentation 7.6 6.0 6.5 7.9 12.0 14.6

IT 0.9 0.8 1.1 5.8 21.9 39.4

SCADA 0.2 0.1 0.1 0.0 0.1 0.0

Other 1.7 1.2 1.3 1.4 1.6 6.5

Internal direct overheads 0.0 0.0 0.0 0.0 0.0 0.0

Indirect overheads 0.0 4.1 1.6 4.1 6.4 0.0

GROSS TOTAL 82.5 41.2 39.1 40.7 64.5 99.0

Customer contributions 3.4 2.4 2.4 2.4 2.2 0.0

Government contributions 0.0 0.0 23.6 0.0 0.0 0.0

NET TOTAL 79.0 38.8 13.2 38.3 62.3 99.0

Source: AER analysis of Multinet's proposal.Notes: (a) The 2012 figures represent forecast actual capex from Multinet's RIN and not the

proposed inputs into the ECM, which are based on the ESCV's forecast in accordance with the ESC's capex incentive scheme.

2013–17 access arrangement period

Multinet proposed net total capex of $375.3 million ($2012) for the 2013–17 access arrangement period. This represents a real increase of 32 per cent over the approved allowance for the 2008–12 access arrangement period (see Figure3.2 below).

Table 3.5 Multinet proposed capex by category over the 2013–17 access arrangement period ($million, 2012)

Category 2013 2014 2015 2016 2017

Mains replacement 24.8 26.2 22.5 22.1 25.7

AER draft decision | Multinet 2013–17 | Attachments 25

Residential connections 15.0 19.9 20.4 20.4 20.4

Commercial/industrial connections 2.2 2.6 2.5 2.7 2.6

Meters 3.6 3.3 2.4 2.3 2.4

Augmentation 8.5 6.9 6.1 6.4 7.2

IT 19.9 8.8 6.9 7.8 3.5

SCADA 1.1 0.5 0.5 5.0 0.4

Other 17.7 7.1 6.1 9.0 6.2

Internal direct overheads 1.9 3.5 3.6 3.7 3.8

Indirect overheads 0.0 0.0 0.0 0.0 0.0

GROSS TOTAL 94.6 78.8 71.0 79.4 72.2

Customer contributions 11.6 4.3 1.6 1.6 1.6

Government contributions 0.0 0.0 0.0 0.0 0.0

NET TOTAL 83.0 74.5 69.4 77.8 70.6

Source: AER analysis of Multinet's proposal.

Figure 3.2 Comparison of Multinet's past approved, actual and proposed capex ($million, 2012)

Source: Multinet, ESC.

AER draft decision | Multinet 2013–17 | Attachments 26

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

ESC approved 2007-11 Multinet actual 2007-11 Multinet proposed 2013-17

The major components of the forecast gross total expenditure are mains replacement (32 per cent), residential connections (23 per cent), IT (13 per cent), other non-demand (12 per cent) and augmentation (9 per cent), (see Figure 3.3).

Figure 3.3 Composition of Multinet's total capex for 2013–17 ($million, 2012)

Source: Multinet.

3.2 Assessment approach

NGR requirements for conforming capital expenditure

The AER must accept, as part of the opening capital base for the access arrangement period, any conforming capex made (or to be made) during the earlier access arrangement period.

The AER must also consider forecast conforming capex for the access arrangement period as part of calculating the projected capital base for the access arrangement period.57

Capex will be conforming if it:

meets the definition of capex in r. 69 of the NGR. Capex is defined as costs and expenditure of a capital nature incurred to provide, or in providing, pipeline services

is based on a forecast or estimate which is supported by a statement of the basis of the forecast or estimate as set out in r. 74(1) of the NGR. Any forecast or estimate submitted must:

be arrived at on a reasonable basis57 NGR, r. 78.

AER draft decision | Multinet 2013–17 | Attachments 27

Mains replacement31%

Residential connections24%

Commercial/industrial connections

3%

Meters3%

Augmentation9%

IT12%

SCADA2%

Other12%

Gas Extensions-NGEP0%

Overheads4%

represent the best forecast or estimate possible in the circumstances58

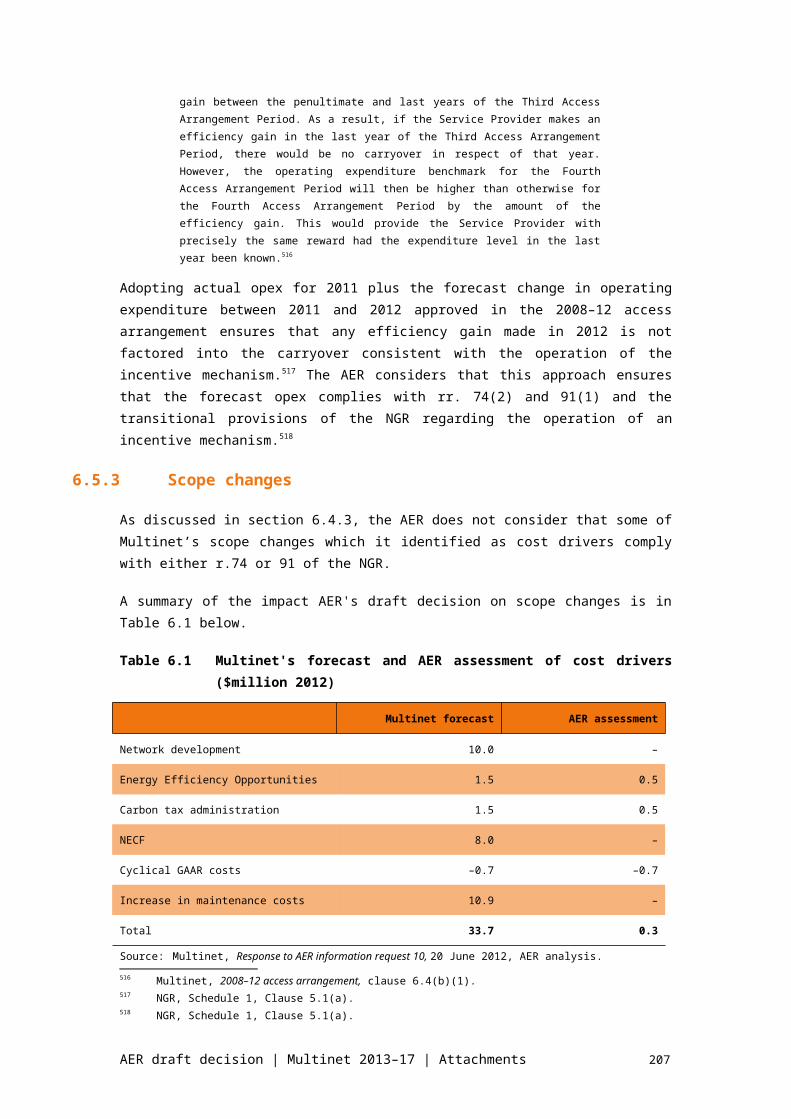

conforms with the capex criteria in r. 79 of the NGR. There are two essential criteria that must both be met under this rule:

The expenditure must be such as would be incurred by a prudent service provider acting efficiently, in accordance with good industry practice, to achieve the lowest sustainable cost of providing services; and

The expenditure must be justifiable on one of four grounds set out in r. 79(2) of the NGR.

The four grounds set out in r. 79(2) of the NGR can be summarised as follows. The capex

must either:

have an overall economic value that is positive

demonstrate an expected present value of the incremental revenue that exceeds the expenditure

be necessary to maintain and improve the safety of services, or maintain the integrity of services, or comply with a regulatory obligation or requirement, or maintain capacity to meet levels of demand existing at the time the capex is incurred, or

be justifiable as a combination of the preceding two dot points.

The AER has limited discretion when making decisions under r. 79 of the NGR.59 The AER must approve a particular element of the access arrangement proposal if that element complies with the applicable requirements of the NGR and NGL and is consistent with any criteria set out in the NGR or NGL.

Assessment of conforming capital expenditure

The AER considers the access arrangement information provided by Multinet in assessing its proposed capex. The AER will not approve certain information and forecasts provided by Multinet if the information does not meet the requirements set out in the NGR. The AER must exercise its economic regulatory functions in a manner that will or is likely to contribute to the achievement of the NGO. For instance, having regard to the NGO, the AER takes the view that a prudent service provider will seek cost efficiencies through continuous improvements, and that customers ultimately share in these benefits. This also provides the service provider with a reasonable opportunity to recover at least its efficient costs in accordance with the revenue and pricing principles.

In assessing Multinet’s proposed capex in the earlier access arrangement period, the AER reviewed Multinet's supporting material. This included information on Multinet's reasoning and, where relevant, business cases, audited regulatory accounts, and other relevant information. This information helped the AER identify the need for the capex over the earlier access arrangement period and, in turn, 58 NGR, r. 74(2).59 NGR, r. 40(2), r. 79(6).

AER draft decision | Multinet 2013–17 | Attachments 28

whether that capex should be included in the opening capital base in accordance with r. 77 (2)(b) of the NGR.

Although the capital base roll forward relates to the 2008–12 access arrangement period, the AER is also required to adjust for the difference between actual and forecast capex in the capital base60. Generally, the final year of the previous access arrangement period is based on forecast capex (in this case, 2007). Therefore, the AER’s assessment of conforming capex includes the regulatory years for 2007–11. This is because:

2007 capex—at the previous access arrangement review, the ESC did not yet have actual capex for 2007. The ESC therefore included in the capital base benchmark (forecast) capex for 2007, adjusted for actual growth. Since actual capex is now available for 2007, the AER has assessed whether Multinet’s actual capex for 2007 is conforming capex under the NGR61. This conforming capex is then included in the capital base roll forward.62

2008–11 capex—for this access arrangement review, the AER has the actual capex for 2008–11. Consistent with 2007 capex, the AER has assessed whether Multinet’s actual capex for 2008–11 is conforming under the NGR for inclusion in the capital base roll forward63

2012 capex—for this access arrangement review, the AER does not yet have actual capex for 2012. The AER is required under the NGR to properly reflect any increments or decrements arising from the operation of the ESC’s capex incentive scheme64. The AER has therefore adopted the ESC’s approach for 2012 capex. This requires the AER to include in the capital base roll forward benchmark (forecast) capex for 2012, adjusted for actual growth. At the next access arrangement review, the AER will assess whether Multinet's actual capex for 2012 is conforming capex under the NGR65.

The AER’s detailed analysis of the capex incentive scheme is set out in attachment 7, and its application to the capital base roll forward is addressed in attachment 2.

In making its assessment of whether Multinet’s proposed capex in the projected capital base complies with the capex criteria in r. 79(1) of the NGR, the AER assessed the key drivers for the capex. In making its decision on Multinet's proposed capital expenditure the AER relied upon the following information:

The access arrangement information (AAI) - this document outlines Multinet's program of capital expenditure and describes the main drivers of increased capital expenditure

The Asset Management Plan,66 Asset strategy plans and appendices which provided specific expenditure detail67

60 NGR r. 77(2)(a)61 NGR r.7962 NGR r.77(2)(a)63 NGR r. 79 and 77(2)(b)64 NGR, Schedule 1, clause 5(1)(a)65 NGR r.7966 Multinet, Access Arrangement Information: Appendix D-1: Multinet Gas Network Asset

Management Plan 2012/13-2017/18, March 2012 (CONFIDENTIAL)67 Multinet, Access Arrangement Information: Appendices D-2 – D-16, E-1 (CONFIDENTIAL).

AER draft decision | Multinet 2013–17 | Attachments 29

Vic DNSPs RIN Template

Multinet responses to AER information requests

Submissions received in the course of consulting on the access arrangement proposal68

Initially the AER assessed whether the proposed capex is justified on one of the four grounds under r. 79(2) of the NGR.

The AER then assessed the prudency and efficiency of the proposed capex. For analysis purposes the capex was broken into categories depending on whether the expenditure is driven by:

Growth in demand - extensions, connections, augmentation

Replacement on the basis of asset life, obsolescence, safety or regulatory obligations - mains, services, meters, regulators, city gates, IT, SCADA, or

Other - new regulatory or safety obligations, opex or reliability improvements.

For each category of expenditure the scope, timing and cost of the proposed expenditure was considered in order to form a view on the prudency and efficiency of the expenditure. The assessment also considered whether cost forecasts have been arrived at on a reasonable basis and represent the best forecast possible in the circumstances.

A combination of the following approaches was used by the AER to assess efficiency and prudency of Multinet's proposed capex:

Assessing competitive tender processes for outsourced activities

Outsourcing to specialist providers of a particular service is a common means by which businesses in the economy are able to gain access to economies of scale and scope and other efficiencies.

Where the gas businesses have used tendered rates as the basis of proposed unit costs, the AER relied on its conceptual approach to assessing outsourcing arrangements. This approach is outlined in its Final decision for the Victorian electricity distribution network service providers Distribution determination 2011–2015.69

The first stage of the conceptual framework is a 'presumption threshold' designed to be an initial filter to determine which contracts can be presumed to reflect efficient costs that would be incurred by a prudent operator.

In undertaking this ‘presumption threshold’ assessment, the AER considers:

Did the service provider have an incentive to agree to non-arm’s length terms at the time the contract was negotiated (or at its most recent re-negotiation)?

68 Submissions were received from Energy Users Coalition of Victoria, Origin Energy, AGL and Australian Power and Gas.

69 AER, Final decision for the Victorian electricity distribution network service providers, Distribution determination 2011-15, pp. 150–151.

AER draft decision | Multinet 2013–17 | Attachments 30

If yes, was a competitive open tender process conducted in a competitive market?

In the absence of an incentive to agree to non-arm’s length terms, the AER considers it reasonable to presume a contract price reflects efficient costs. The AER also considers this presumption to be reasonable where an incentive to agree to non-arm’s length terms exists but the contract was the outcome of a competitive open tender process in a competitive market.

Where an arrangement 'passes' the presumption threshold, the AER considers the starting point for setting future expenditure allowances should be the contract price itself, with limited further examination required. This further examination involves checking whether the contract wholly relates to the relevant services and whether the (efficient) contract price already compensates for risks or costs provided for elsewhere in the building blocks.

Revealed cost approach

The revealed cost approach considers information revealed by the past performance of a gas business. Under the ex ante regime, gas businesses are rewarded for spending less capex than allowed by the regulator. This incentive enables the AER to place some reliance on the historical costs of a gas business when reviewing its forecast capex. The AER used historical costs and volumes as an indicator of efficient costs and volumes for the Victorian gas businesses. In particular, the AER used historical total costs, unit costs and volumes in assessing connections, mains and services replacements, meter replacements, SCADA and IT.

The revealed cost approach is an accepted industry practice. Many gas businesses have used this approach as a basis to forecast expenditure proposals. This approach has also been used previously by the ESC in its assessment of access arrangement proposals for the Victorian gas businesses and the AER in its past reviews.

Benchmarking against the other businesses' proposed unit costs and volumes

The AER also conducted comparative analysis of unit costs Multinet has used to develop its capex forecast. In particular, the AER undertook a high level benchmarking of a selection of Multinet's unit costs against similar unit costs of the other Victorian gas businesses. Where required some adjustment for compositional difference was made. This comparison was used for assessing connections, mains and services replacements, SCADA and IT.

Where this benchmarking indicated that Mulitnet's capex may not be efficient, the AER undertook a detailed review of Multinet‘s proposal. The AER‘s detailed review involved consideration of relevant documentation and the impact of factors expected to differ from the past and/or from the other Victorian gas businesses.

The AER recognises that forecast efficient costs may legitimately depart from those revealed through past performance, and compared with other gas businesses. For example, gas businesses may discover more efficient processes over time. The gas businesses may propose they can best achieve their safety,

AER draft decision | Multinet 2013–17 | Attachments 31

reliability or regulatory obligations by incurring expenditure to implement new, more efficient processes, and include such expenditure in their proposed forecast capex. The AER assumed that operating processes would only be changed (from revealed, or otherwise efficient processes) if they are likely to result in efficiency gains (in the absence of any information to suggest other reasons for the change). Where the AER considered that future cost savings should result from capex investments, the AER took this into consideration in determining Multinet‘s opex allowance.

Specialist technical advice

The AER engaged Nous Group to provide technical advice on the prudency and efficiency of IT projects. The AER engaged Zincara to provide engineering technical advice on the prudency and efficiency of augmentation projects and the medium pressure and minor specific mains replacement programs.70

Cash flow analysis for equity raising costs

To determine the amount of equity raising costs, the AER has undertaken an assessment of benchmark cash flows calculated in the PTRM. Under this method, a prudent service provider, acting efficiently will first exhaust the cheapest sources of funding through the use of internal cash flows before using more expensive external sources of equity financing. The cash flow modelling approach used by the AER incorporates this assumption to determine if any external equity financing would be required based on the AER’s capex forecast for Multinet.

3.3 Reasons for decision

3.3.1Conforming capital expenditure for 2007–11

The AER considers that $231.7 million ($2012) of the net capital expenditure incurred by Multinet for 2007-11 complies with r. 79(1) of the NGR.

In reaching this view, the AER has considered the following factors:

Multinet's capex was $52.6 million (18.5 per cent) below the ESC approved amount of $284.4 million ($2012) (see Table 3.1)

Multinet spent less than the ESC allowance in five out of ten categories.

The largest underspends occurred in the mains replacement, meter replacement, IT and SCADA and "Other" categories:

The category with the largest underspend by value was mains replacement, where Multinet spent 58.4 per cent below the ESC approved amount of $105.5 million ($2012). This resulted from the length of pipeline completed being 40 per cent below the benchmark, and unit cost 28 per cent below the benchmark set by the ESC.

Meter replacement capex was 17.5 per cent under the ESC benchmark of $12.5 million ($2012).

70 The AER notes that Zincara was not requested to provide advice in relation to the assessment of the capex proposed for the Lilydale pipeline.

AER draft decision | Multinet 2013–17 | Attachments 32

IT capex was 3.9 per cent below the ESC benchmark of $31.7 million. SCADA capex was 87.1 per cent below the ESC benchmark of $ 3.7 million

In the "Other" capex category, Multinet spent 63.6 per cent below the ESC benchmark of $20.2 million ($2012). This was due to deferral of projects.

Multinet spent more than the ESC allowance in 4 out of ten categories,

The largest overspends occurred in the residential connections and augmentation categories: