draft – not to be quoted measuring investment in intangible asset in the uk: results from a unique...

TRANSCRIPT

DRAFT – NOT TO BE Q

UOTEDMeasuring Investment in Intangible Asset in the UK: results from a unique survey

Presentation by Gaganan Awano, UK Office for National Statistics, to COINVEST Conference, Lisbon , 19 March 2010

This work is a component of NESTA’s innovation index project and carried out by a team at Imperial College Business School and ONS. The team are (ONS) Gaganan Awano, Mark Franklin, Andrew Thomas and (Imperial) Jonathan

Haskel, Zafeira Kastrinaki.

This work contains statistical data from ONS which is Crown copyright and reproduced with the permission of the controller of HMSO and Queen's Printer for

Scotland. The use of the ONS statistical data in this work does not imply the endorsement of the ONS in relation to the interpretation or analysis of the statistical data. This work uses research datasets which may not exactly

reproduce National Statistics aggregates.

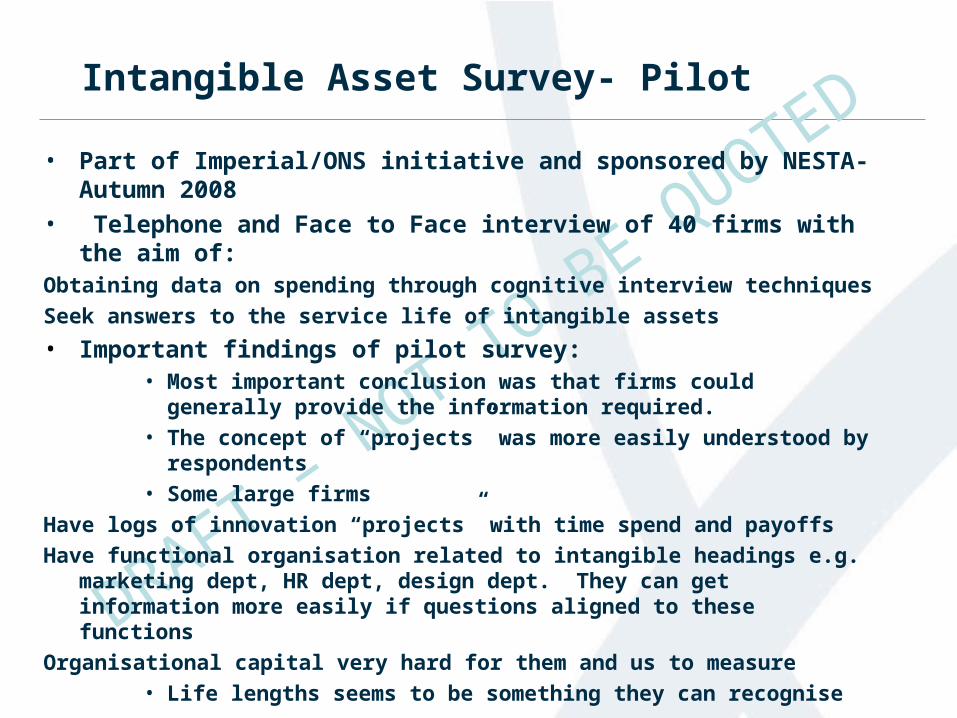

DRAFT – NOT TO BE Q

UOTEDIntangible Asset Survey- Pilot

• Part of Imperial/ONS initiative and sponsored by NESTA- Autumn 2008

• Telephone and Face to Face interview of 40 firms with the aim of:Obtaining data on spending through cognitive interview techniques

Seek answers to the service life of intangible assets

• Important findings of pilot survey:• Most important conclusion was that firms could generally provide the

information required.• The concept of “projects” was more easily understood by

respondents• Some large firms

Have logs of innovation “projects” with time spend and payoffs

Have functional organisation related to intangible headings e.g. marketing dept, HR dept, design dept. They can get information more easily if questions aligned to these functions

Organisational capital very hard for them and us to measure• Life lengths seems to be something they can recognise

DRAFT – NOT TO BE Q

UOTEDIIA Survey- Phase II

• Conducted by the ONS in October 2009• Voluntary postal survey of 2000 UK companies• Objectives are to measure:

– Firms’ spending on main intangible assets: R&D, software, training, branding, design, organisation or business process improvement

– Extra mural– Intra mural– Life lengths

• Linkable via business register• Minimum burden on respondents, i.e. short as possible

DRAFT – NOT TO BE Q

UOTEDLayout of questionnaire

Assets divided into sections

DRAFT – NOT TO BE Q

UOTEDEach section has a filter question which defines the asset with examples

DRAFT – NOT TO BE Q

UOTEDThen asks purchased and own-account

DRAFT – NOT TO BE Q

UOTEDFinally life lengths

DRAFT – NOT TO BE Q

UOTEDSampling

• Sample 2000 firms drawn from the Business Register

• Market sector - consistent with intangibles growth accounting framework

• Stratified by industry and employment

• Mild bias informed by pilot and UK Innovation Survey results:

Over-sample Under-sampleEngineering ConstructionICT UtilitiesFinancial Services Distribution

TransportAccommodation

DRAFT – NOT TO BE Q

UOTEDSurvey findings: response rates

Response Rate: by firm size

Firm Size Usable Response Rate (%) % Positive Response*

10-99 47 50

100-499 48 68

500-4999 33 80

5000+ 21 76

Total 42 58

*Percentage of usable responses reporting positive spending in one or more category of intangible asset

•More large firms answered affirmative to investing in at least one intangible asset than small firms

•Sample size: 2000•Total response: ~ 1400•Usable response: 838

DRAFT – NOT TO BE Q

UOTEDIncidence

Intangible Asset Category Firms’ Propensity

Training 35%

Software 30%

Reputation & Branding 22%

R&D 8%

Design 10%

Business Process Improvement 13%

•Most firms do not invest in intangible assets

•Of those that do, most firms invest in training and least in R&D

% of respondent firms conducting intangible investment by asset category

DRAFT – NOT TO BE Q

UOTEDIncidence: by size bands

Firm Size Incidence of Intangible Asset Spending (%)

Training Software Reputation & Branding R&D Design BPI

10-99 32 29 21 7 10 12

100-499 64 43 30 11 12 19

500-4999 70 57 38 19 19 33

5000+ 66 64 40 14 18 24

•The propensity for investing in intangible assets generally increases with firm size

•By contrast, response rates are higher for smaller firms

DRAFT – NOT TO BE Q

UOTEDAverage Expenditure

Intangible Asset Category

Mean Expenditure

(£,k)

Training 94*

Software 191

Reputation & Branding 192

R&D 579

Design 53

Business Process

Improvement48

• Data were weighted to reflect the characteristics of the population from which the sample was drawn and the pattern of responses received.

• Average of firms conducting the activity

• R&D has the highest mean expenditure

• A small number of very large firms make huge spending on R&D

*Note includes imputed value of employee time while undertaking training

DRAFT – NOT TO BE Q

UOTEDPurchased vs own-account expenditure

Mean Expenditure (£,k)

Intangible Asset Category Extra Intra

Training 32 68

Software 56 192

Reputation & Branding 143 64

R&D 325 300

Design 15 43

Business Process Improvement 27 30

•R&D has the highest extramural and intramural spending among the assets

•Average intramural spending is higher in all intangible assets except reputation & branding and R&D

DRAFT – NOT TO BE Q

UOTEDMean Expenditure by broad sector

Asset Manufacturing (£,k) Services (£,k)

Training 104 92

Software 81 215

Reputation & Branding 289 175

R&D 1280 234

Design 122 30

BPI 90 38

•Except for Software, the manufacturing sector has higher average spending for all other assets

•Average spending on R&D by the manufacturing sector is exceptionally high

DRAFT – NOT TO BE Q

UOTEDLife length

Asset Category Meal benefit life (yrs)

CHS(2006) estimates (yrs)

Training 2.7 2.5

Software 3.2 3

Reputation & Branding 2.7 2

R&D 4.6 5

Design 4.0 5

Business Process Improvement 4.2 2.5

•Using single declining balance, life length is the reciprocal of depreciation

•Our life lengths although varied are not that far off from literature estimates, and are distributed around CHS estimates

DRAFT – NOT TO BE Q

UOTEDLife lengths by broad sector

Asset Manufacturing (yr) Services (yr)

Training 2.9 2.7

Software 3.4 3.2

Reputation & Branding 4.1 2.5

R&D 5.5 4.3

Design 4.6 3.7

BPI 5.4 4.0

•Manufacturing sector has longer life lengths for investments in intangible assets than the services on all asset categories

DRAFT – NOT TO BE Q

UOTEDExpenditure Levels (£,Million)

0

2000

4000

6000

8000

10000

12000

Training Softw are Reputation & Branding R&D Design Business ProcessImprovement

DRAFT – NOT TO BE Q

UOTEDSome comparison with other sources

Software

• Chamberlin et al (2007) valued own-account software investment in the UK at £10b and contributes about 50% of total.

• IIA survey total for own-account software expenditure is £7b and contributes 70% of total

R&D

• UK Business Enterprise Research & Development (BERD) survey (2008) states the total R&D expenditure in the UK at £15.9b

• Total R&D expenditure in IIA survey stood at £8.1b

• Innovation Survey (2009) shows the manufacturing sector generally more innovative than the services sector.

• The manufacturing sector in the IIA survey has higher mean spending and life lengths than the services sector. Any links?

DRAFT – NOT TO BE Q

UOTEDConclusions

• Most firms are small and do not invest in intangible assets

• Most firms engage in staff training and fewer in R&D, albeit mean spending is highest on R&D

• Spending on 4 out of 6 assets is more on in-house than purchased

• Asset life lengths although varied are not too far from literature estimates

• A larger survey may help clarify the variations of data with other sources and provide lower confidence intervals around estimates

DRAFT – NOT TO BE Q

UOTEDNext Steps

• Present results to NESTA

• Analyse data against 2009 Innovation Survey

• Detailed analysis against software estimates

• Expanded survey- subject to funding

DRAFT – NOT TO BE Q

UOTED

Thank you!

Andrew D Thomas: [email protected]

Gaganan Awano: [email protected]

Mark Franklin: [email protected]

Jonathan Haskel: [email protected]

Zafeira Kastrinaki: [email protected]