dubai real estate market overview - q3...

TRANSCRIPT

Dubai Real Estate Market Overview

Q3 2013

Dubai

Macroeconomic overview

2

Indicator 2011 2012 2013 (f)

United Arab Emirates

Population (millions) 8.9 9.2 9.3

Real GDP Growth (Y-o-Y) 3.9% 4.4% 3.7%

Consumer Price Index (% change) 0.9% 0.7% 1.5%

Real Estate Mortgage Loans (millions AED) 161,500 159,800 n/a

Dubai

Population (millions) 2.0 2.1 2.2

Real GDP Growth (Y-o-Y) 3.7% 4.4% 4.1%

Inflation (% Change) 0.5% -1.7% n/a

Sources: IHS Global Insights (August 2013); UAE Central Bank; Dubai Statistics Center 2013

e: estimated f:forecasted

Market highlights – Q3 2013

• The Dubai economy is expected to maintain its strong growth rate and expand at more than 4% in 2013. The strong economic performance remains supported by the growth of sectors such as hospitality, trade, transportation and logistics, in addition to the recovery of the construction and real estate segments.

• The business outlook remains optimistic with the Department of Economic Development‟s Business Confidence Index (BCI), reaching 120.7 points in the second quarter of 2013, an increase of 14.6 points over the same period in 2012. According to the survey, more than 83% of firms expect either stability or increased sales volumes while an increasing number of companies are planning to invest in expansion, recruitment and technology upgrades.

• The only significant commercial transaction in Q3 was an office building in TECOM. There remains however an active residential investment market across Dubai. We have also noted growing interest from Kuwaiti investment firms in all asset classes of the Dubai real estate market.

• The office leasing market witnessed slower activity in Q3 due to the summer period and the month of Ramadan. While demand continues to improve in the prime locations and some new areas, the high level of supply remains the main obstacle to a healthy broad-based recovery.

• The residential market continues to experience a broad-based recovery,

with prices and rental values picking up in the secondary and more

affordable locations, while the primary areas are now seeing slower paces

of growth.

• Activity in the retail market was quiet in Q3 due to the summer period.

However, as demand remains strong and retailers are upbeat, the sector is

expected to end the year on a strong note in both its primary and

secondary segments.

• The hotel sector has continued its strong performance, on the back of the

booming tourism and aviation industries. Year-to-date (YTD) occupancy

rates have risen to 79% while YTD Average Daily Rates (ADRs) are also

higher at USD 235. A number of hotels are due to open in the short run but

the sector is expected to maintain its positive performance

• The industrial market continues to perform well overall. Demand has

started to shift to the newer areas in the south of Dubai, which are

witnessing strong growth and are benefiting from well developed

infrastructure, good connectivity, proximity to major infrastructure projects,

as well as better quality products.

3

All sectors of the Dubai real estate market maintained their positive performance during the seasonally quieter

summer months. The retail, hotel and industrial segments continue to experience solid growth. The recovery of

the office sector remains more selective and concentrated in the prime segment with the large level of supply

and high overall vacancy rates depressing rental pressure elsewhere. The broad based recovery in the

residential sector is seeing prices and rents increase across most areas, but there are signs that the rate of

increase is slowing in some high end locations.

Talking points – Q3 2013

4

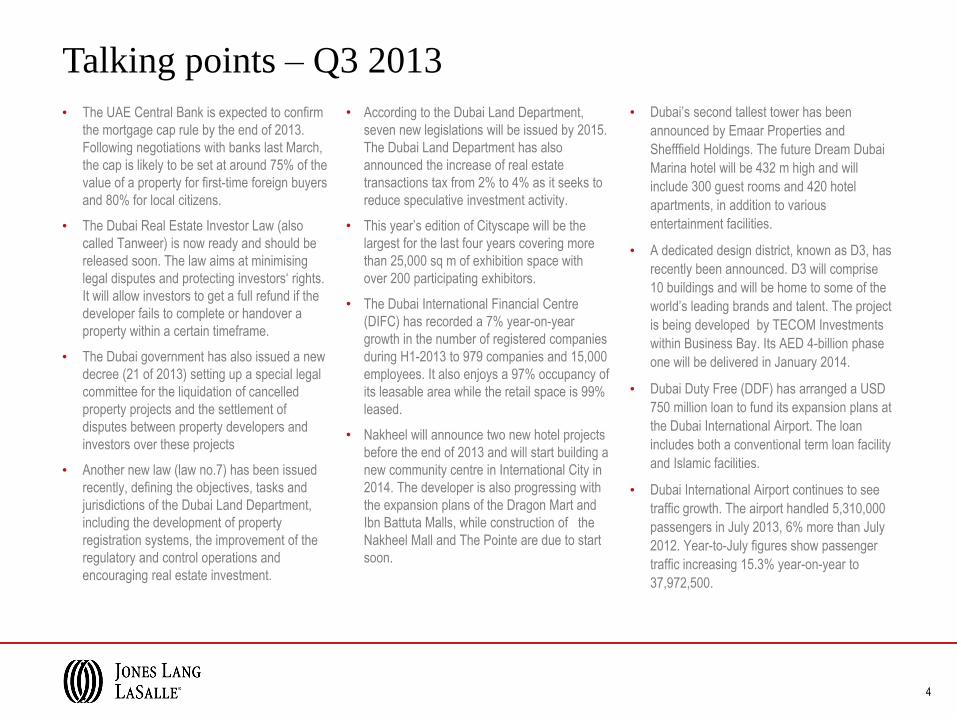

• The UAE Central Bank is expected to confirm

the mortgage cap rule by the end of 2013.

Following negotiations with banks last March,

the cap is likely to be set at around 75% of the

value of a property for first-time foreign buyers

and 80% for local citizens.

• The Dubai Real Estate Investor Law (also

called Tanweer) is now ready and should be

released soon. The law aims at minimising

legal disputes and protecting investors„ rights.

It will allow investors to get a full refund if the

developer fails to complete or handover a

property within a certain timeframe.

• The Dubai government has also issued a new

decree (21 of 2013) setting up a special legal

committee for the liquidation of cancelled

property projects and the settlement of

disputes between property developers and

investors over these projects

• Another new law (law no.7) has been issued

recently, defining the objectives, tasks and

jurisdictions of the Dubai Land Department,

including the development of property

registration systems, the improvement of the

regulatory and control operations and

encouraging real estate investment.

• Dubai‟s second tallest tower has been

announced by Emaar Properties and

Shefffield Holdings. The future Dream Dubai

Marina hotel will be 432 m high and will

include 300 guest rooms and 420 hotel

apartments, in addition to various

entertainment facilities.

• A dedicated design district, known as D3, has

recently been announced. D3 will comprise

10 buildings and will be home to some of the

world‟s leading brands and talent. The project

is being developed by TECOM Investments

within Business Bay. Its AED 4-billion phase

one will be delivered in January 2014.

• Dubai Duty Free (DDF) has arranged a USD

750 million loan to fund its expansion plans at

the Dubai International Airport. The loan

includes both a conventional term loan facility

and Islamic facilities.

• Dubai International Airport continues to see

traffic growth. The airport handled 5,310,000

passengers in July 2013, 6% more than July

2012. Year-to-July figures show passenger

traffic increasing 15.3% year-on-year to

37,972,500.

• According to the Dubai Land Department,

seven new legislations will be issued by 2015.

The Dubai Land Department has also

announced the increase of real estate

transactions tax from 2% to 4% as it seeks to

reduce speculative investment activity.

• This year‟s edition of Cityscape will be the

largest for the last four years covering more

than 25,000 sq m of exhibition space with

over 200 participating exhibitors.

• The Dubai International Financial Centre

(DIFC) has recorded a 7% year-on-year

growth in the number of registered companies

during H1-2013 to 979 companies and 15,000

employees. It also enjoys a 97% occupancy of

its leasable area while the retail space is 99%

leased.

• Nakheel will announce two new hotel projects

before the end of 2013 and will start building a

new community centre in International City in

2014. The developer is also progressing with

the expansion plans of the Dragon Mart and

Ibn Battuta Malls, while construction of the

Nakheel Mall and The Pointe are due to start

soon.

5

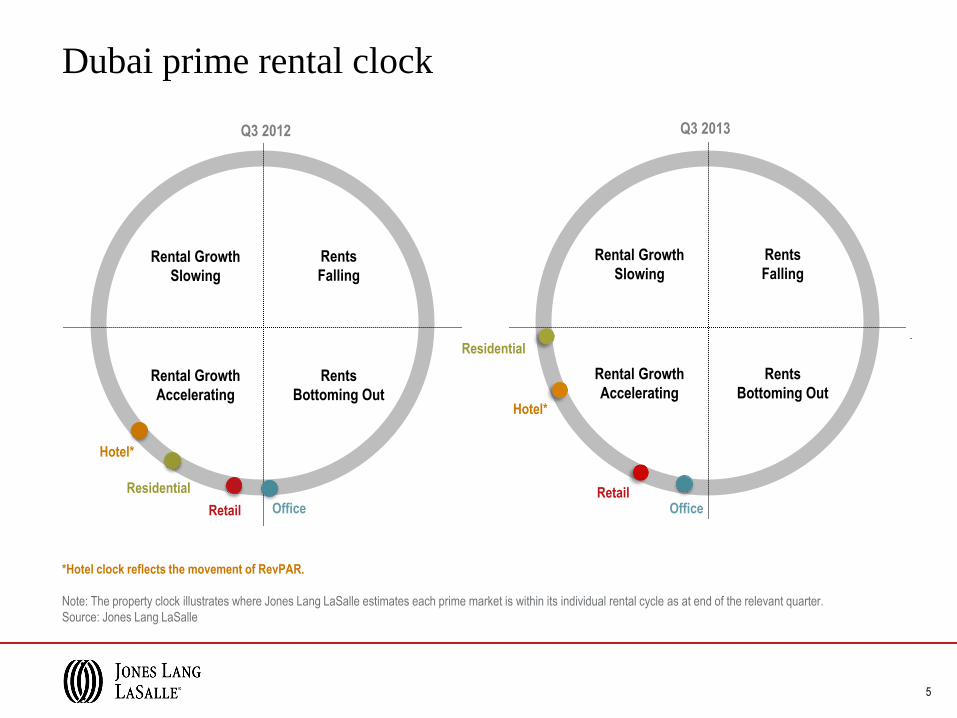

Dubai prime rental clock

*Hotel clock reflects the movement of RevPAR.

Note: The property clock illustrates where Jones Lang LaSalle estimates each prime market is within its individual rental cycle as at end of the relevant quarter.

Source: Jones Lang LaSalle

Q3 2012 Q3 2013

Rental Growth

Slowing

Rents

Falling

Rental Growth

Accelerating

Rents

Bottoming Out

Office Retail

Hotel*

Residential

Rental Growth

Slowing

Rents

Falling

Rental Growth

Accelerating

Rents

Bottoming Out

Office Retail

Hotel*

Residential

Dubai office market overview

Office supply

• The total office stock within areas monitored by JLL is estimated at 7.2

million sq m at the end of Q3 2013. Around 45,000 sq m of office space

entered the market in the last quarter, with the major completions being

“48 Burj Gate” on Sheikh Zayed Road and the API Trio Tower in Al

Barsha.

• According to developers, around 245,000 sq m will be delivered in the

last quarter of the year. However, much of the announced new supply

might be postponed to 2014 and beyond.

• As of Q3 2013, the CBD (ie DIFC, Burj Downtown and SZR) represents

less than 20% of the existing stock while areas such as Business Bay

(14%) and JLT (13.5%) are accounting for larger proportions of the

current office space.

Source: Jones Lang LaSalle, Q3 2013

• Around 1.2 million sq m of office space is expected to enter the market

by 2016, reflecting the strong supply pipeline. However, as the delivery

of this extra space may further exacerbate the current supply-demand

imbalance, some of the proposed projects might be delayed.

• Business Bay accounts for the majority of the future supply. The area is

expected to see an additional 713,000 sq m of office space by 2016

(equivalent to 58% of the total upcoming supply) including towers such

as The Burlington, Bay View, Bay Gate and Tamani Art offices. Other

locations that will see new office supply are JLT (10%), Dubai World

Central (7%), Dubai Investment Park (6%), the Greens (5%) and DTCD

(4%).

7

Breakdown of Expected Completions (2013-2016)

by Sub Market

Source: Jones Lang LaSalle, Q3 2013

Dubai Office Stock (2011 – 2016)

6.3 6.9 7.2 7.5 8.1 8.4

0.2 0.6

0.3 0.1

0

1

2

3

4

5

6

7

8

9

2011 2012 2013 2014 2015 2016

Tot

al S

tock

(m

illio

n sq

m)

Completed Stock Future Supply

CBD

8

Business Bay

The Burlington,

Bay Gate

DIFC

Burj

Daman

JLT

JBC 4

Major office completions - 2013/2014

Under Construction

Completed

JLT

Amesco Tower

Barsha

API Trio Tower

SZR

48 Burj Gate

Business Bay

Blue Bay, Oberoi

Centre

Office demand • The improvement in the Dubai

economy has resulted in an increased

demand for office space. However, the

recovery in demand remains counter -

balanced by the high level of supply

entering the market.

• Demand remains focused on high

quality space in prime locations such

as SZR, Downtown and TECOM A & B

• “Flight to quality” continues to be

noticeable with further relocations

taking place from the older and

secondary areas towards the prime

and newer locations.

• The market continues to suffer from a

shortage of large units of high quality

office space suitable for global

occupiers

• “Built-to-suit” options are therefore still

being considered, especially by large

occupiers in search of 5,000 sq m of

office space or more.

• Large companies are also becoming

increasingly sensitive to sustainability

issues and there has been an

increasing demand for LEED certified

buildings with some corporates

mandating this for all future office

space.

• Other factors influencing occupiers‟

choice include:

- Congestion and traffic

- Availability of parking space

- Proximity to a metro station

• Single ownership buildings continue to

account for the majority of the existing

supply and most of the current

demand; while strata projects remain

less popular, especially amongst large

global companies. Despite being

growing commercial locations, many

buildings in Business Bay and JLT will

not appeal to some occupiers due to

their strata status.

• Landlords are becoming more bullish in

the most prime locations, being less

flexible on rents and reducing rent-free

periods. Landlords in secondary

locations remain flexible in order to

attract tenants and to fill their buildings.

• Vacancy rates within the CBD

remained high at around 30% as the

take up remains counterbalanced by

the new supply entering the market.

Source: Jones Lang LaSalle, Q3 2013

9

Examples of recent deals

Industry Area Acquired

Location Comment

(sq m)

Banking 10,000 Bur Dubai Renewal

Oil & Gas 6,000 DIFC Acquisition

Hotelier 3,000 Dubai Renewal

IT 1,200 Downtown Acquisition

Digital Imaging 500 Barsha Acquisition

IT 300 Media City Acquisition

Finance 200 DIFC Acquisition

Rental performance

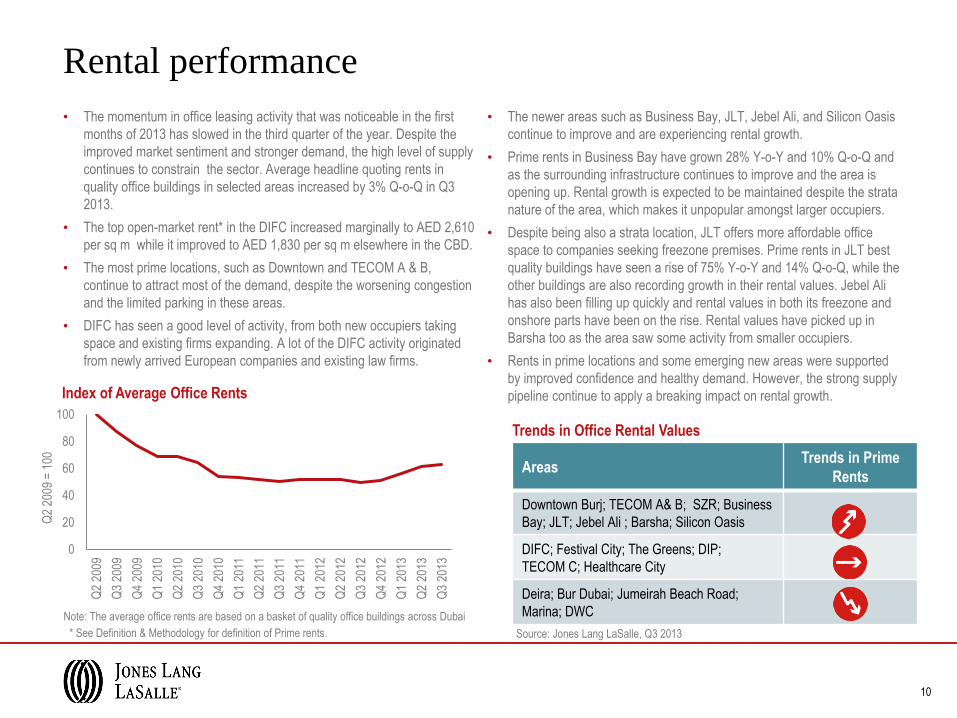

• The momentum in office leasing activity that was noticeable in the first

months of 2013 has slowed in the third quarter of the year. Despite the

improved market sentiment and stronger demand, the high level of supply

continues to constrain the sector. Average headline quoting rents in

quality office buildings in selected areas increased by 3% Q-o-Q in Q3

2013.

• The top open-market rent* in the DIFC increased marginally to AED 2,610

per sq m while it improved to AED 1,830 per sq m elsewhere in the CBD.

• The most prime locations, such as Downtown and TECOM A & B,

continue to attract most of the demand, despite the worsening congestion

and the limited parking in these areas.

• DIFC has seen a good level of activity, from both new occupiers taking

space and existing firms expanding. A lot of the DIFC activity originated

from newly arrived European companies and existing law firms.

• The newer areas such as Business Bay, JLT, Jebel Ali, and Silicon Oasis

continue to improve and are experiencing rental growth.

• Prime rents in Business Bay have grown 28% Y-o-Y and 10% Q-o-Q and

as the surrounding infrastructure continues to improve and the area is

opening up. Rental growth is expected to be maintained despite the strata

nature of the area, which makes it unpopular amongst larger occupiers.

• Despite being also a strata location, JLT offers more affordable office

space to companies seeking freezone premises. Prime rents in JLT best

quality buildings have seen a rise of 75% Y-o-Y and 14% Q-o-Q, while the

other buildings are also recording growth in their rental values. Jebel Ali

has also been filling up quickly and rental values in both its freezone and

onshore parts have been on the rise. Rental values have picked up in

Barsha too as the area saw some activity from smaller occupiers.

• Rents in prime locations and some emerging new areas were supported

by improved confidence and healthy demand. However, the strong supply

pipeline continue to apply a breaking impact on rental growth.

* See Definition & Methodology for definition of Prime rents. Source: Jones Lang LaSalle, Q3 2013

10

Note: The average office rents are based on a basket of quality office buildings across Dubai

Index of Average Office Rents

Trends in Office Rental Values

Areas Trends in Prime

Rents

Downtown Burj; TECOM A& B; SZR; Business

Bay; JLT; Jebel Ali ; Barsha; Silicon Oasis

DIFC; Festival City; The Greens; DIP;

TECOM C; Healthcare City

Deira; Bur Dubai; Jumeirah Beach Road;

Marina; DWC

0

20

40

60

80

100

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q2

2009

= 1

00

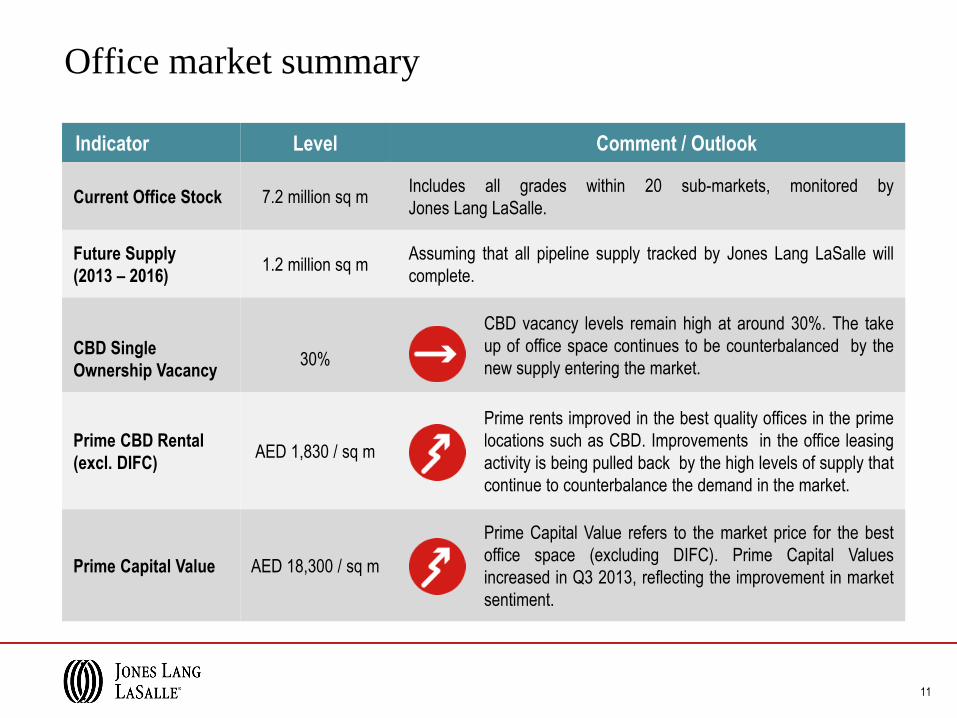

Indicator Level Comment / Outlook

Current Office Stock 7.2 million sq m Includes all grades within 20 sub-markets, monitored by

Jones Lang LaSalle.

Future Supply

(2013 – 2016) 1.2 million sq m

Assuming that all pipeline supply tracked by Jones Lang LaSalle will

complete.

CBD Single

Ownership Vacancy

30%

CBD vacancy levels remain high at around 30%. The take

up of office space continues to be counterbalanced by the

new supply entering the market.

Prime CBD Rental

(excl. DIFC) AED 1,830 / sq m

Prime rents improved in the best quality offices in the prime

locations such as CBD. Improvements in the office leasing

activity is being pulled back by the high levels of supply that

continue to counterbalance the demand in the market.

Prime Capital Value AED 18,300 / sq m

Prime Capital Value refers to the market price for the best

office space (excluding DIFC). Prime Capital Values

increased in Q3 2013, reflecting the improvement in market

sentiment.

Office market summary

11

Dubai residential market overview

341 355 364 373 394

9 21 15

0

100

200

300

400

500

2011 2012 2013 2014 2015

Completed Stock Future Supply

Residential supply

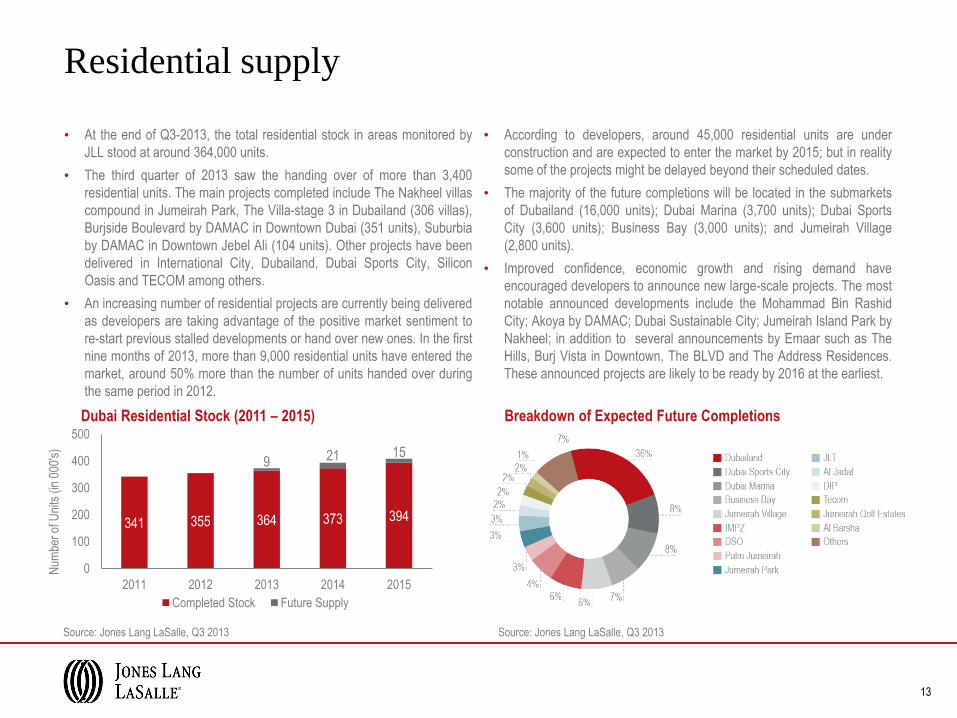

• At the end of Q3-2013, the total residential stock in areas monitored by

JLL stood at around 364,000 units.

• The third quarter of 2013 saw the handing over of more than 3,400

residential units. The main projects completed include The Nakheel villas

compound in Jumeirah Park, The Villa-stage 3 in Dubailand (306 villas),

Burjside Boulevard by DAMAC in Downtown Dubai (351 units), Suburbia

by DAMAC in Downtown Jebel Ali (104 units). Other projects have been

delivered in International City, Dubailand, Dubai Sports City, Silicon

Oasis and TECOM among others.

• An increasing number of residential projects are currently being delivered

as developers are taking advantage of the positive market sentiment to

re-start previous stalled developments or hand over new ones. In the first

nine months of 2013, more than 9,000 residential units have entered the

market, around 50% more than the number of units handed over during

the same period in 2012.

• According to developers, around 45,000 residential units are under

construction and are expected to enter the market by 2015; but in reality

some of the projects might be delayed beyond their scheduled dates.

• The majority of the future completions will be located in the submarkets

of Dubailand (16,000 units); Dubai Marina (3,700 units); Dubai Sports

City (3,600 units); Business Bay (3,000 units); and Jumeirah Village

(2,800 units).

• Improved confidence, economic growth and rising demand have

encouraged developers to announce new large-scale projects. The most

notable announced developments include the Mohammad Bin Rashid

City; Akoya by DAMAC; Dubai Sustainable City; Jumeirah Island Park by

Nakheel; in addition to several announcements by Emaar such as The

Hills, Burj Vista in Downtown, The BLVD and The Address Residences.

These announced projects are likely to be ready by 2016 at the earliest.

Source: Jones Lang LaSalle, Q3 2013 Source: Jones Lang LaSalle, Q3 2013

13

Breakdown of Expected Future Completions Dubai Residential Stock (2011 – 2015)

Num

ber

of U

nits

(in

000

's)

14

Silicon Oasis

Silicon Gate 1,

City Oasis

Major residential completions - 2013/2014

Under Construction

Completed

Dubailand

Platinum 1 & 2

Downtown Dubai

Burjside Boulevard

Jumeirah Village

Knightsbridge Courts

Jumeirah Park

Villas

Dubai Sports City

Elite 6, Mediterranean

Building

0

20

40

60

80

100

120

Feb

200

9

Apr

200

9

Jun

2009

Aug

200

9

Oct

200

9

Dec

200

9

Feb

201

0

Apr

201

0

Jun

2010

Aug

201

0

Oct

201

0

Dec

201

0

Feb

201

1

Apr

201

1

Jun

2011

Aug

201

1

Oct

201

1

Dec

201

1

Feb

201

2

Apr

201

2

Jun

2012

Aug

201

2

Oct

201

2

Dec

201

2

Feb

201

3

Apr

201

3

Jun

2013

Aug

201

3

Residential General Residential Apartment Residential Villa

0

100

200

300

400

500

600

Feb

200

8

Apr

200

8

Jun

2008

Aug

200

8

Oct

200

8

Dec

200

8

Feb

200

9

Apr

200

9

Jun

2009

Aug

200

9

Oct

200

9

Dec

200

9

Feb

201

0

Apr

201

0

Jun

2010

Aug

201

0

Oct

201

0

Dec

201

0

Feb

201

1

Apr

201

1

Jun

2011

Aug

201

1

Oct

201

1

Dec

201

1

Feb

201

2

Apr

201

2

Jun

2012

Aug

201

2

Oct

201

2

Dec

201

2

Feb

201

3

Apr

201

3

Jun

2013

Aug

201

3

Residential General Residential Apartment Residential Villa

Residential performance

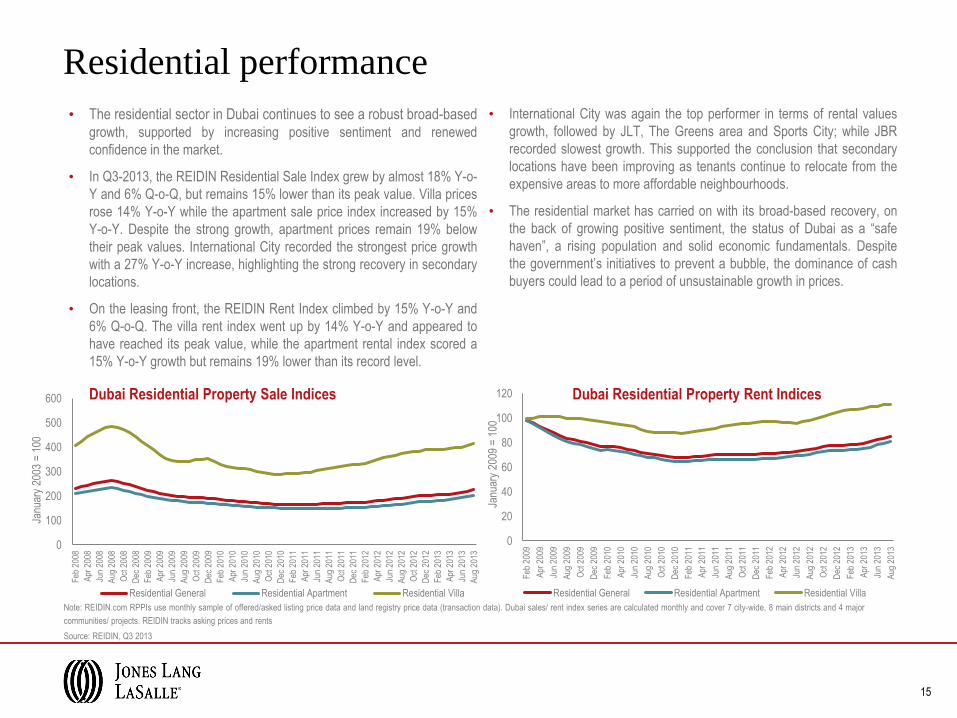

• The residential sector in Dubai continues to see a robust broad-based growth, supported by increasing positive sentiment and renewed

confidence in the market.

• In Q3-2013, the REIDIN Residential Sale Index grew by almost 18% Y-o-

Y and 6% Q-o-Q, but remains 15% lower than its peak value. Villa prices

rose 14% Y-o-Y while the apartment sale price index increased by 15%

Y-o-Y. Despite the strong growth, apartment prices remain 19% below

their peak values. International City recorded the strongest price growth

with a 27% Y-o-Y increase, highlighting the strong recovery in secondary

locations.

• On the leasing front, the REIDIN Rent Index climbed by 15% Y-o-Y and

6% Q-o-Q. The villa rent index went up by 14% Y-o-Y and appeared to

have reached its peak value, while the apartment rental index scored a

15% Y-o-Y growth but remains 19% lower than its record level.

• International City was again the top performer in terms of rental values

growth, followed by JLT, The Greens area and Sports City; while JBR

recorded slowest growth. This supported the conclusion that secondary

locations have been improving as tenants continue to relocate from the

expensive areas to more affordable neighbourhoods.

• The residential market has carried on with its broad-based recovery, on

the back of growing positive sentiment, the status of Dubai as a “safe

haven”, a rising population and solid economic fundamentals. Despite

the government‟s initiatives to prevent a bubble, the dominance of cash

buyers could lead to a period of unsustainable growth in prices.

Note: REIDIN.com RPPIs use monthly sample of offered/asked listing price data and land registry price data (transaction data). Dubai sales/ rent index series are calculated monthly and cover 7 city-wide, 8 main districts and 4 major

communities/ projects. REIDIN tracks asking prices and rents

Source: REIDIN, Q3 2013

15

Dubai Residential Property Sale Indices Dubai Residential Property Rent Indices

Janu

ary

2003

= 1

00

Janu

ary

2009

= 1

00

Residential market summary

Indicator Level Comment/Outlook

Current Residential Stock 364,000 Around 3,400 units were added to Dubai‟s residential stock inventory

in Q3 2013.

Future Supply (2013 – 2015) 45,000

Assuming that all supply tracked by Jones Lang LaSalle will

complete. In reality, some of the proposed projects may be delayed

beyond their scheduled date.

Apartment Rent

Asking rents went up by 15% Y-o-Y. The recovery is being more

broad-based with the secondary and more affordable areas growing

at faster pace than the prime locations

Apartment Sale Price

Asking apartment sale prices went up by 20% Y-o-Y. Sale prices in

the well established areas are growing at a slower pace but

accelerating in the secondary areas.

Villa Rent

Villa rents have increased by 14% Y-o-Y. Asking rents for villas in the

secondary and more affordable locations have been increasing,

sometimes at a faster rate than in the well established areas.

Villa Sale Price Asking prices for villas have increased by 11% Y-o-Y but overall

prices are growing at a decelerating rate.

Note: Direction arrows are based on the performance of the REIDIN monthly index.

16

Dubai retail market overview

Retail mall supply

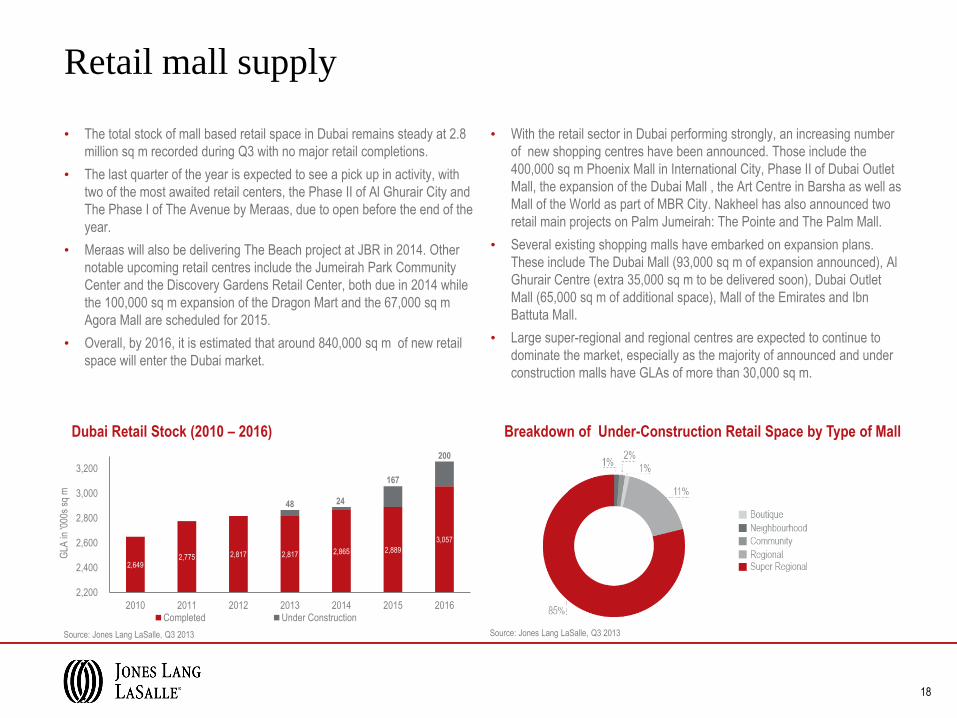

• The total stock of mall based retail space in Dubai remains steady at 2.8

million sq m recorded during Q3 with no major retail completions.

• The last quarter of the year is expected to see a pick up in activity, with

two of the most awaited retail centers, the Phase II of Al Ghurair City and

The Phase I of The Avenue by Meraas, due to open before the end of the

year.

• Meraas will also be delivering The Beach project at JBR in 2014. Other

notable upcoming retail centres include the Jumeirah Park Community

Center and the Discovery Gardens Retail Center, both due in 2014 while

the 100,000 sq m expansion of the Dragon Mart and the 67,000 sq m

Agora Mall are scheduled for 2015.

• Overall, by 2016, it is estimated that around 840,000 sq m of new retail

space will enter the Dubai market.

• With the retail sector in Dubai performing strongly, an increasing number

of new shopping centres have been announced. Those include the

400,000 sq m Phoenix Mall in International City, Phase II of Dubai Outlet

Mall, the expansion of the Dubai Mall , the Art Centre in Barsha as well as

Mall of the World as part of MBR City. Nakheel has also announced two

retail main projects on Palm Jumeirah: The Pointe and The Palm Mall.

• Several existing shopping malls have embarked on expansion plans.

These include The Dubai Mall (93,000 sq m of expansion announced), Al

Ghurair Centre (extra 35,000 sq m to be delivered soon), Dubai Outlet

Mall (65,000 sq m of additional space), Mall of the Emirates and Ibn

Battuta Mall.

• Large super-regional and regional centres are expected to continue to

dominate the market, especially as the majority of announced and under

construction malls have GLAs of more than 30,000 sq m.

Source: Jones Lang LaSalle, Q3 2013 Source: Jones Lang LaSalle, Q3 2013

18

Dubai Retail Stock (2010 – 2016) Breakdown of Under-Construction Retail Space by Type of Mall

2,649 2,775 2,817 2,817 2,865 2,889

3,057

48 24

167

200

2,200

2,400

2,600

2,800

3,000

3,200

2010 2011 2012 2013 2014 2015 2016

GLA

in '0

00s

sq m

Completed Under Construction

19

Downtown Dubai

Dubai Mall - Phase 2

Al Wasl

The Avenue

Al Barsha

Outlet Village

JBR

The Beach

International City

Dragon Mart -

Phase 2

Expected major retail projects

Deira

Al Ghurair Centre -

Phase 2

Under Construction

Rental performance – Estimated Rental Value (ERV)

• The retail market in Dubai has witnessed a slow third quarter due to the

Eid break and summer holidays. However, activity is expected to pick up

in the last months of 2013 as demand continues to be buoyant and

retailers remain quite upbeat.

• Due to the quiet summer months, the top open market net rent for a

notional standard shop in prime super regional centres has remained

unchanged in Q3 2013 at around AED 5,700 per sq m.

• The Primary Super Regional Malls continue to be very popular amongst

both residents and tourists; while the smaller community and

neighbourhood centres have been performing better, supported by

stronger demand from a growing resident population.

• The rising confidence and purchasing power in Dubai have also resulted

in more demand for premium brands, a segment that was severely hit

during the previous crisis.

• With retailers struggling to find quality locations and the large primary

malls largely full, there has been a growing demand for “street shops”. A

clear example is the increasing number of F&B units opening on the

Sheikh Mohammed Bin Rashid Boulevard in Downtown.

• The overall retail market in Dubai continues to perform well, supported

by positive sentiment, solid economic fundamentals, a growing tourism

industry and a rising number of residents. We expect leasing activity to

accelerate over the next 6 months.

Note: Chart shows mid-point ERV for an in-line store in a basket of Primary and Secondary Super Regional shopping

malls. The rent quoted reflects a notional “standard” line store unit of 100 sq m.

Source: Jones Lang LaSalle, Q3 2013

AED / sq m Q3 2013

Primary Secondary

Super Regional 4,300-5,700 1,000-2,400

Regional 1,350-2,700 970-1,900

Community 1,300-2,400 1,100-1,350

Neighbourhood 2,450-2,700 1,100

Convenience 1,500-1,900 1,300-1,400

20

Note: Based on a basket of malls of different size. (See definitions for further details)

0

1,000

2,000

3,000

4,000

5,000

6,000

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Dubai Retail Rents (Q1 2009 – Q3 2013)

Primary Secondary

AE

D /

sq m

Retail sector summary

Indicator Level Comment / Outlook

Current Retail Space (GLA) 2,817,000 sq m No major additions to the mall based retail space in Q3 2013.

Future Supply (2013 – 2016) 839, 500 sq m

The main upcoming retail completions for the last quarter of

2013 will be Phase I of the Avenue by Meraas and Phase II of

Al Ghurair Center. Other large-scale retail projects to be

delivered thereafter include The Beach Mall, The Dragon Mart

expansion and the Agora Mall.

Average Retail Rents in

Primary Malls

Average Retail Rents in

Secondary Malls

AED 5,000 / sq m

AED 1,725 / sq m

Rents of prime units in better performing centers have

remained unchanged in Q3 2013. Primary as well as

the newest secondary malls are expected to see rental

growth in 2014.

Average Regional Mall

Vacancy 13%

Citywide retail vacancy has remained unchanged at

13% in Q3 2013. Vacancy rates are expected to drop

in the coming months as leasing activity increases.

21

Dubai hotel market overview

23

Hotel supply

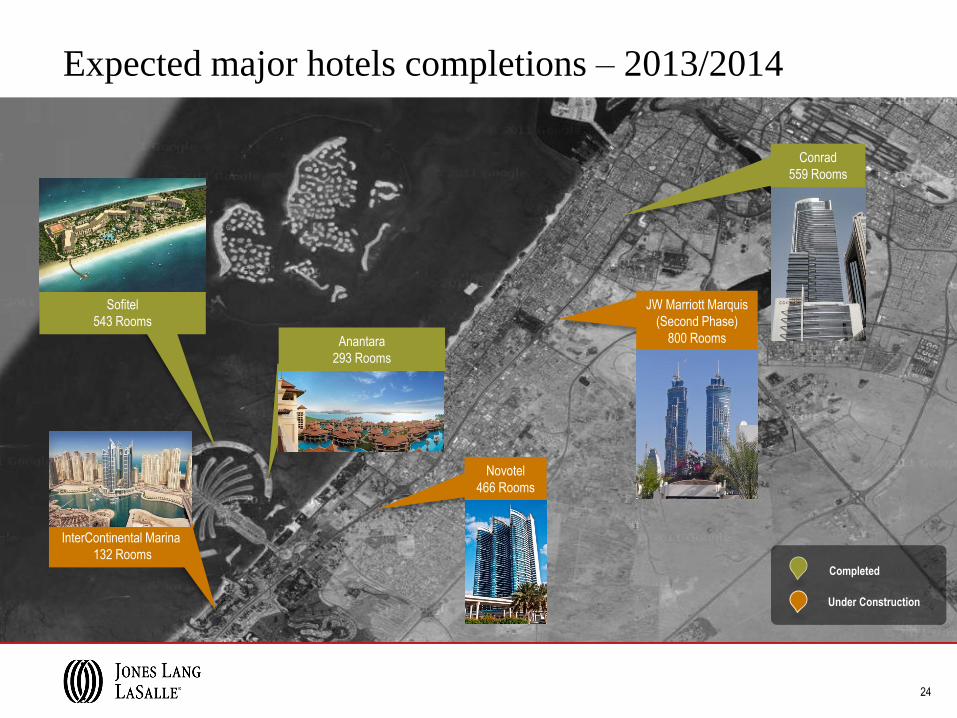

• The third quarter of 2013 saw some notable openings on Palm

Jumeirah, such as the Sofitel and the Anantara. The Conrad Dubai,

located on Sheikh Zayed Road, was also another new entrant to the

market.

• The main openings scheduled for the end of 2013 include the Novotel

Al Barsha and the expansion of the Millennium Airport.

• During the third quarter of 2013, several new hotel developments

were announced such as an hotel on JBR, two hotels by MAF

attached to their malls – Deira City Centre and Mall of Emirates, the

Dream Hotel in Marina and TRYP by Wyndham in TECOM. Some of

these new projects represent the entry of new brands and operators

into the Dubai hospitality market.

• A number of existing hotels are undergoing renovation and

refurbishment plans. The Sheraton on the Creek, has closed for a

complete renovation while the Ritz Carlton on JBR has shut down its

old wing. Habtoor Grand has recently reopened 320 refurbished

rooms in its two towers. Many hotels are also revamping specific

areas, particularly the food and beverage facilities.

• Dubai Department of Tourism and Commerce Marketing (DTCM)

have announced the Vision 2020 for the tourism sector with an

ambitious objective of achieving 20 million tourists by 2020. The

hospitality supply and tourism projects planned for the next 7 – 8

years are expected to be aligned to this goal.

Source: Jones Lang LaSalle, Q3 2013

Dubai Hotel Stock (2012 – 2015)

No.

of R

oom

s

57,345 59,380 60,900

65,600

1,520

4,700

3,600

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

2012 2013F 2014F 2015F

Current Supply Future Additions

23

24

Sofitel

543 Rooms

JW Marriott Marquis

(Second Phase)

800 Rooms

Expected major hotels completions – 2013/2014

Under Construction

Completed

InterContinental Marina

132 Rooms

Conrad

559 Rooms

Anantara

293 Rooms

Novotel

466 Rooms

25

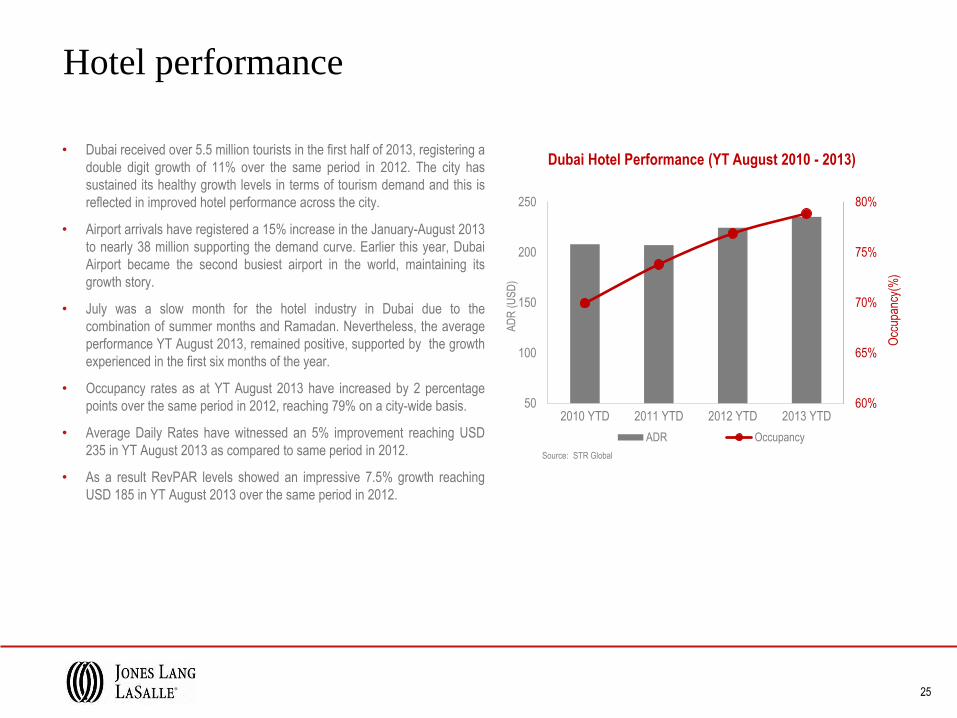

Source: STR Global

Dubai Hotel Performance (YT August 2010 - 2013) • Dubai received over 5.5 million tourists in the first half of 2013, registering a

double digit growth of 11% over the same period in 2012. The city has

sustained its healthy growth levels in terms of tourism demand and this is

reflected in improved hotel performance across the city.

• Airport arrivals have registered a 15% increase in the January-August 2013

to nearly 38 million supporting the demand curve. Earlier this year, Dubai

Airport became the second busiest airport in the world, maintaining its

growth story.

• July was a slow month for the hotel industry in Dubai due to the

combination of summer months and Ramadan. Nevertheless, the average

performance YT August 2013, remained positive, supported by the growth

experienced in the first six months of the year.

• Occupancy rates as at YT August 2013 have increased by 2 percentage

points over the same period in 2012, reaching 79% on a city-wide basis.

• Average Daily Rates have witnessed an 5% improvement reaching USD

235 in YT August 2013 as compared to same period in 2012.

• As a result RevPAR levels showed an impressive 7.5% growth reaching

USD 185 in YT August 2013 over the same period in 2012.

Hotel performance

60%

65%

70%

75%

80%

50

100

150

200

250

2010 YTD 2011 YTD 2012 YTD 2013 YTD

Occ

upan

cy(%

)

AD

R (

US

D)

ADR Occupancy

25

26

Hotel market summary

Indicator Level Comment / Outlook

Current Hotel Supply 59,380 rooms

The third quarter of 2013 witnessed the addition of two resorts on

Palm Jumeirah – Sofitel and Anantara as well as the Conrad

Dubai on Sheikh Zayed Road.

Future Supply (2013 - 2015) 9,800 rooms

Major openings scheduled for 2014 include the Four Seasons,

InterContinental Marina, second tower of J W Marriott Marquis

and Marriott Al Jadaf amongst others.

2013 YTD Occupancy 79% Increase in YTD levels of occupancy with resurgence witnessed

across all sub-markets.

2013 YTD ADR USD 235 As a result of resurgence in occupancy and ADRs; RevPAR levels

have a notable increase by 7.5% on a city-wide average basis.

26

Dubai industrial market overview

Industrial supply & demand

28

• The industrial sector in Dubai has maintained its healthy growth and

strong performance in Q3 2013.

• The growth of the industrial sector is mainly supported by the economic

growth of Dubai, the “safe haven” status of the Emirate and the positive

atmosphere surrounding the Expo 2020 bid.

• The industrial sector in Dubai is also benefiting from the well-developed

infrastructure in the Emirate and the rising aviation industry.

• The strength of the aviation sector can be highlighted by the following

facts:

• Dubai International Airport is now the world‟s second busiest airport

by passenger traffic. Year to July passenger traffic reached

37,972,500, 15.3% more than the same period in 2012. Dubai

International is also working to increase its capacity

• The new Al Maktoum International Airport is anticipated to be the

largest in the world. It will have capacity for 160 million passengers

and 12 million tons of cargo per year. The airport will start

passenger flights by the end of October.

• Emirates Airlines continues to prove itself as a world leading airline.

In 2012, the airline carried around 39 million passengers and 1.8

million tonnes of cargo.

• The Dubai ports have also been contributing strongly to the growth of the

industrial sector:

• Jebel Ali sea port opened its third terminal that will increase its

capacity to 19 million TEU* a year. By 2014 Jebel Ali is expected to

be the biggest port in the Middle East

• DP World handled 26.6 million TEU across its global portfolio in the

first half of 2013.

• On the back of the growth in the aviation sector and the position of Dubai

as a trading hub, DAFZA announced a 44% increase in demand for space

in H1 2013. DAFZA noted an 11% y-o-y growth in expansion applications

from existing tenants. European and American companies constitute 40%

of DAFZA‟s tenants.

• DAFZA has been named the Middle East Free Zone of the Future 2013/14

by FDI magazine

*TEU - Twenty-foot equivalent units

Industrial supply & demand

29

Overview of some of the main industrial areas in Dubai

Area Age Land Area (sq m) Regulatory Status Selected tenants

Traditional

Areas

Al Quoz 1973 18,500,000 Onshore Fedex, Mercedes-Benz

Al Qusais 5,450,000 Onshore Maxell, Sabco

Umm Ramool 3,900,000

Onshore

Al Futtaim, Al Ghurair Group, Al Habtoor

Leighton

Ras Al Khor 1976 12,000,000

Onshore

Aramex, Total, Unilever, Easa Saleh

Al Gurg Group

Free Zone

Areas

JAFZA 1985 JAFZA North - 45,000,000

JAFZA South- 35,000,000 Offshore

DHL, Danube, LG, Kenwood, Heinz, Kraft,

Mars, P&G

DAFZA 1996 2,000,000 Offshore Clarins, Rolls-Royce, National Foods

Products Company

Dubai World Central 2009 105,000,000

Free Zone Areas –

Logistics and

Aviation City only

Dnata, RSA, Caliper

New

Onshore

Areas

Jebel Ali Industrial

Area

21,240,000

Onshore Landmark Group, Jumbo, Bridgestone,

Dubai Investment Park 1997 16,500,000

Onshore Paris Group, Drake & Scull

Dubai Industrial City 2004 52,000,000 Onshore Nestle, Baker Hugues

Industrial supply & demand

30

• Activity in the industrial market appeared to be on the rise in Q3 2013 with

a number of transactions recorded mostly in the new and modern

industrial zones.

• The market has observed an increase in demand in the last few months,

with enquiries from both new entrants to the market as well as existing

occupiers looking to expand their operations

• With the traditional onshore areas such as Al Quoz or Ras Al Khor being

saturated and ageing, the trend is increasingly shifting towards the newer

areas such as Dubai Industrial City (DIC) and Dubai Investment Park

(DIP) and the freezone locations such as the Jebel Ali Free Zone Authority

(JAFZA) and Dubai Airport Free Zone Authority (DAFZA).

• The newly developed areas such as DIC, DIP or Dubai World Central

(DWC) offer large plots of land, suitable for the global occupiers who

prefer to build their own units.

• The old areas such Ras Al Khor or Al Qusais do not have large plots as

land availability is scarce.

• The new areas also offer the following advantages:

• Easy access and connectivity

• Proximity to major infrastructure projects.

• Modern facilities and better quality products

• A large number of enquiries for industrial space continues to emanate

from food & beverage (F&B) companies.

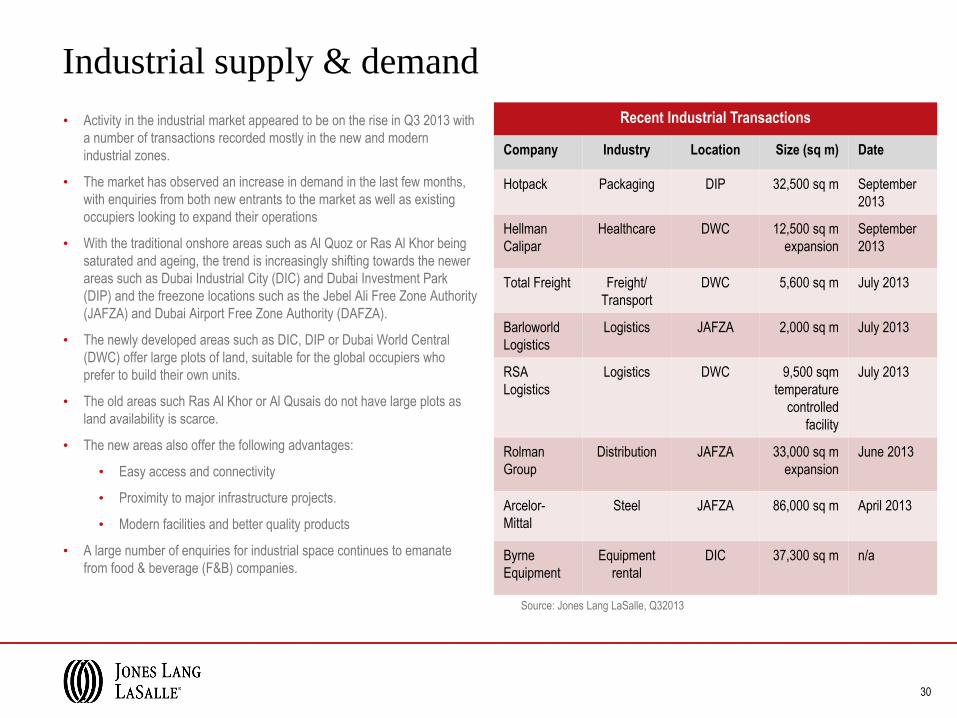

Recent Industrial Transactions

Company Industry Location Size (sq m) Date

Hotpack Packaging DIP 32,500 sq m September

2013

Hellman

Calipar

Healthcare DWC 12,500 sq m

expansion

September

2013

Total Freight Freight/

Transport

DWC 5,600 sq m July 2013

Barloworld

Logistics

Logistics JAFZA 2,000 sq m July 2013

RSA

Logistics

Logistics DWC 9,500 sqm

temperature

controlled

facility

July 2013

Rolman

Group

Distribution JAFZA 33,000 sq m

expansion

June 2013

Arcelor-

Mittal

Steel JAFZA 86,000 sq m April 2013

Byrne

Equipment

Equipment

rental

DIC 37,300 sq m n/a

Source: Jones Lang LaSalle, Q32013

30

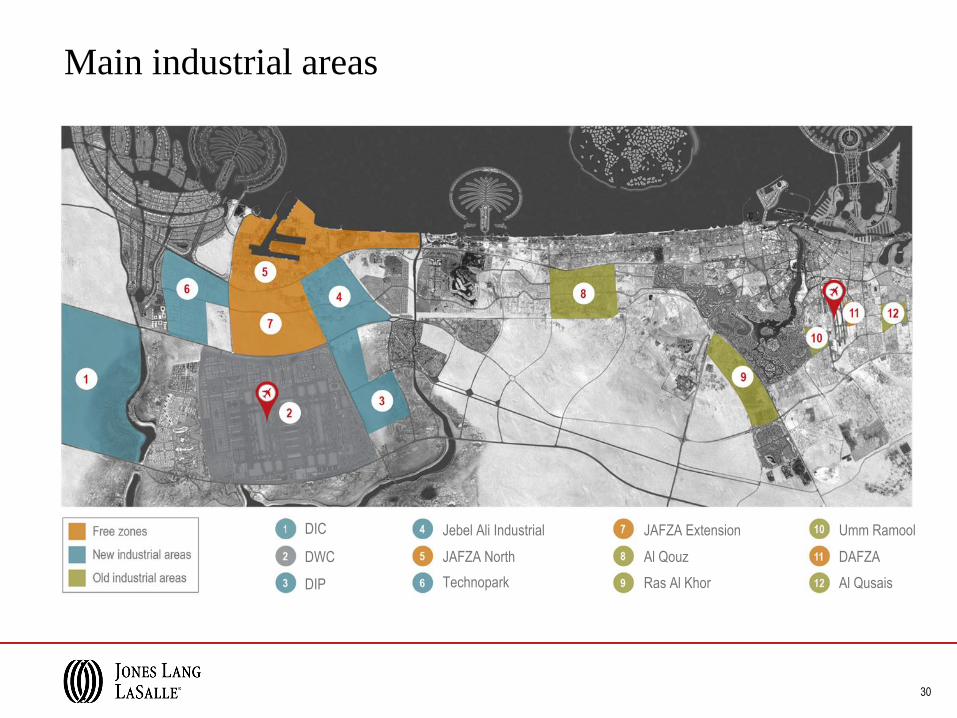

Main industrial areas

DIC

DWC

DIP Technopark

JAFZA North

Jebel Ali Industrial JAFZA Extension Umm Ramool

Al Qouz DAFZA

Ras Al Khor Al Qusais

32

Industrial performance

• The industrial sector is considered one of Dubai‟s most resilient real

estate markets, with rates remaining stable due to the lack of speculation

in the market.

• Rental rates in completed industrial units in Dubai currently vary

significantly from one area to another, with no real standardization of

logistics facilities.

• The older areas have maintained their average rents of AED 300 – 550

per sq m, due to their proximity to local markets, despite the poor quality

of their stock and the relatively underdeveloped infrastructure systems.

Completed units in newer but more peripheral locations (such as DIC

and DIP) have started to offer higher average rents as they are seeing

increasing demand.

• The free zone areas of Jebel Ali and Dubai Airport command a higher

average of between AED 350 – 800 per sq m for completed

warehousing units

• Demand is starting to shift towards those areas offering better quality

products, well developed infrastructure and access to ports and/or

airports (e.g. DIC, DIP, JAFZA). Al Maktoum International Airport will

start transforming into an integrated logistics platform over time,

increasing the attraction of industrial areas to the south of Dubai.

• The industrial market has been much less cyclical than other sectors

over recent years and continues to be dominated by long term

commitments to single tenants.

Area Unit Lease

AED / sq m / p.a.

Lease term

Older Onshore Areas 300-550 Annual

Newer Onshore areas (excl.

Freezone areas)

200-400 3-5-10 years (DIC)

1 year (DIP)

Freezone areas 350-800

(DAFZA rates 600-800)

1- 2 years

Area Land Lease

AED / sq m / p.a

Older Onshore Areas 50-80

Newer Onshore areas (excl.

Free Zone areas) 40-80

Free Zone areas 20-80 (JAFZA)

40-100 (DAFZA)

Warehouse rents

Land lease sales

Source: Jones Lang LaSalle, Q32013

Definitions and methodology

Office:

• The supply data is based on our quarterly survey of 20

sub-markets, starting from 2009.

• Completed building refers to a building that is handed over for

immediate occupation.

• Central Business District includes DIFC, DTCD, Sheikh Zayed

Road, Burj Khalifa Downtown. Free Zone areas include Jumeirah

Lake Towers, DIFC, TECOM, Dubai Silicon Oasis, DWC, Dubai

Outsource Zone and IMPZ.

• Prime Office Rent represents the top open-market rent (open

market refers to a new leasing – not to a sitting tenant) that could be

expected for a notional office unit of the highest quality and

specification in the best location in a market, as at the survey date.

Data relates to headline rents, exclusive of incentives.

• Prime Capital Value represents the top open-market capital value

that could be expected for a notional office building of the highest

quality and specification in the best location on the survey date.

• Prime capital values are a calculation, derived from prime rents and

yields:

Capital Value = (Prime Annual Rent / Prime Yield From) * 100

Residential:

• The supply and stock data is based on our quarterly survey of 37

sub markets, starting from 2009. This data excludes labour

accommodation and local Emirati housing supply.

• Completed building refers to a building that is handed over for

immediate occupation.

• Residential performance data is based on the REIDIN monthly

index. REIDIN.com Dubai Residential Property Price Indices

(RPPIs) use monthly sample of offered/asked listing price data and

land registry price data (transaction data). Index series are set at

100 starting at the beginning of each data set.

33

Retail:

• Classification of Retail Centres is based upon the ULI definition and

based on their GLA:

• Super Regional Malls have a GLA of above 90,000 sq m

• Regional Malls have a GLA of 30,000 - 90,000 sq m

• Community Malls have a GLA of 10,000 - 30,000 sq m

• Neighbourhood Malls have a GLA of 3,000 - 10,000 sq m

• Convenience Malls have a GLA of less than 3,000 sq m

• Primary Malls are the good performing malls with high levels of

turnover. Secondary Malls are the average performing malls with

lower levels of turnover.

• Prime Rent Shopping Centre represents the top open market net

rent that could be expected for a notional standard in line unit shop

of 100 sq m situated in a specified shopping centre as at the survey

date.

Hotels:

• Hotel room supply is based on existing supply figures provided by

DTCM as well as future hotel development data tracked by

Jones Lang LaSalle Hotels. Room supply includes all graded supply

and excludes serviced apartments.

• STR performance data is based on monthly survey conducted by

STR Global on a sample of more than 32,000 rooms across Dubai.

Industrial:

• Industrial Stock is calculated on the basis of applying a site

coverage to the total developed industrial land.

• Industrial rental values are based on average asking rents across

14 major industrial areas in Dubai.

34

Definitions and methodology

Dana Williamson

Head of Agency

MENA

Chiheb Ben-Mahmoud

Head of Hotels & Hospitality

MENA

Andrew Williamson

Head of Retail

MENA

Michael Heitmann

National Director, Industrial

MENA

Craig Plumb

Head of Research

MENA

Cynthia Nasseh

Senior Research Analyst

MENA

www.jll–mena.com

COPYRIGHT © JONES LANG LASALLE IP, INC. 2013

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior

written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is

made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept

any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Contacts:

twitter.com/

JLLNews

youtube.com/

joneslanglasalle

linkedin.com/company/

jones-lang-lasalle

joneslanglasalleblog.com/

EMEAResearch