duties, risk and rewards of serving on a nonprofit board · ... baird holm llp: jonathan breuning...

TRANSCRIPT

Duties, Risk and Rewards of Serving on a Nonprofit Board

November 8, 2017 Scott Conference Center, Omaha, NE

Faculty Bios

Brett C. Stohs, University of Nebraska College of Law: Professor Brett Stohs directs the Weibling

Entrepreneurship Clinic at the University of Nebraska College of Law. In the Clinic, Brett supervises third-

year law students who provide free legal services to startup businesses and social enterprises

throughout the State of Nebraska. He received his J.D. from Duke University School of Law and a Master

of Public Policy from the Sanford Institute of Public Policy. Prior to joining the faculty, Brett practiced in

mergers, acquisitions, and other corporate and transactional matters at Sutherland Asbill & Brennan LLP

in Washington, DC, and at Rembolt Ludtke LLP in Lincoln.

Terrence J. Ferguson, Fraser Stryker PC LLO: Mr. Ferguson received a Bachelor of Science degree from

Creighton University in 1964 and a Juris Doctor degree from the Georgetown University Law Center in

1967. He has been Of Counsel with the Fraser Stryker Law Firm since February 1, 1999. Prior to that, he

was Senior Vice President, General Counsel and Secretary of both Level 3 Communications, Inc. from

August 1997 to January 31, 1999 and MFS Communications Company, Inc. from November 1991

through February 1997. He was a senior attorney at the Kiewit Companies from 1980 through 1991, and

a member of the Kutak Rock law firm from 1976-1980. Mr. Ferguson served as an adjunct clinical

professor (1970-1975) and an adjunct professor (1999-2007) at the Creighton Law School.

Mr. Ferguson serves on the boards of the Nebraska Appleseed Center for Law in the Public Interest, the

Nebraska Cultural Endowment and Opera Omaha. He is also a member of the Creighton University

College of Arts and Sciences Advisory Council. He served on the boards of the Joslyn Art Museum, Mid-

America Arts Alliance, Glimmerglass Opera Theatre, Lauritzen Gardens and the Sheldon Art Association.

Emily Blomstedt, Fraser Stryker PC LLO: Emily Blomstedt is an associate attorney at Fraser Stryker PC

LLO in Omaha, Nebraska. Ms. Blomstedt focuses her practice on business and corporate law and

provides services to the firm's clients in nonprofit and charitable organizations, real estate law, and

labor and employment law. She earned her Juris Doctor from the University of Nebraska College of Law

in 2014, highest distinction. Emily was admitted to the Nebraska State Bar Association in 2014 and the

Iowa Bar in 2016.

Jonathan R. Breuning, Baird Holm LLP: Jonathan Breuning is a 1979 graduate of the University of

Michigan Law School, and is currently General Counsel at Baird Holm, LLP. In that role, he advises the

firm and its attorneys on matters of legal ethics, professional responsibility and risk management. Mr.

Breuning represents external business clients on a wide range of legal issues, with particular focus on

labor and employment law. Jon previously served as Executive Vice President and General Counsel for a

technology company headquartered in Omaha, Nebraska, where his responsibilities included all legal,

human resource and facilities operations, and serving as the company's chief ethics officer. He has been

active in the Omaha business community for more than 35 years and has served on the Boards of

Directors of Community Alliance, Inc., Community Alliance Housing Corporation, Heartland Family

Service, the American Lung Association of Nebraska, the Combined Health Agencies Drive, Creighton

University Medical Center, and Omaha Morning Rotary.

Daniel Russell, Nebraska Attorney General’s Office: Daniel Russell is an Assistant Attorney General in

the Consumer Protection Division of the Nebraska Attorney General’s Office. Daniel focuses primarily on

matters involving nonprofit corporations, charitable trusts, endowment funds, and consumer protection

issues. He received his Juris Doctor from the University of Nebraska College of Law in 2013.

Krystal L. Siebrandt, HBE, LLP: Krystal Siebrandt is a partner at HBE, LLP, a CPA firm founded in Lincoln,

NE. She has been with the firm for over 14 years. In addition to being a Certified Public Accountant, she

has obtained designations as a Certified Fraud Examiner and a Chartered Global Management

Accountant. Her primary area of focus is on servicing nonprofits. In addition, Ms. Siebrandt leads HBE’s

outsourced accounting services department, where in her role she serves as the outsourced CFO for

many nonprofit clients. She also has served on the board of directors for several nonprofit

organizations, including current service to the Friendship Home and Seniors Foundation of Lincoln and

Lancaster County.

Stephanie A. Mattoon, Baird Holm LLP: represents nonprofit and for-profit organizations at all stages

of their life cycle with respect to corporate formation, mergers and acquisitions, and corporate

governance matters. She regularly assists new organizations in obtaining 501(c)(3) or other tax-exempt

status and advises existing public charities regarding compliance with federal tax law, including private

benefit issues, unrelated business income tax, lobbying and political activity restrictions, fiscal

sponsorship arrangements, and public charity support determinations. Ms. Mattoon received her Juris

Doctor, with high distinction, from the University of Nebraska College of Law in 2005, where she was

inducted into the Order of the Coif and the Order of the Barristers. While in law school, she was a

member of the Nebraska Law Review and the National Moot Court Team. Ms. Mattoon is a 2013 TOYO

Award recipient (Ten Outstanding Young Omahans), demonstrating a commitment to community

service and personal and professional development.

Legal Fundamentals of Starting & Operating a Nonprofit

Brett C. StohsUniversity of Nebraska College of Law

November 8, 2017 Scott Conference Center, Omaha, NE

1

Legal Fundamentals of

Starting and Operating a Nonprofit Corporation

Brett C. Stohs, Assistant Professor of LawCLE Sponsored by the Nebraska State Bar Association

November 8, 2017

Agenda • Forming a Nonprofit Corporation• Obtaining Tax‐Exemption • Ongoing Governance and Maintenance

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Preliminary Matters

• Remarks and slides are not legal advice!

• This presentation will focus on:• Charitable operating companies• Nebraska law

• Always ask: Is a nonprofit corporation right for me?

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Preliminary Matters

2

What is a nonprofit corporation?• Formed the Nebraska Nonprofit Corporation Act §§ 21‐1901 et seq.• ≠ tax‐exempt• ≠ corporation• ≠ B Corp, benefit corporation, L3C, etc.

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

How do I form a nonprofit corporation?1. File Articles of Incorporation2. Incorporator action appointing Board3. Board actions (adopt Bylaws, et. al.)4. Publish notice5. Obtain federal and state taxpayer IDs

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Articles of Incorporation• Required terms (§ 21‐1921)• Name (§ 21‐1931)• Type• Public benefit•Mutual benefit• Religious

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

3

Articles of Incorporation• Required terms (§ 21‐1921)• Name of registered agent• Street address of registered office• Name and street address of incorporator(s)•Whether to authorize “members”• Distribution of assets on dissolution

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Articles of Incorporation• “Required” terms for 501(c) tax exemption• Activity limitations (“Organizational Test”)• The corporation is organized exclusively for [its exempt purpose]• No political candidate activity [(c)(3)]• No substantial legislative lobbying [(c)(3)]

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Articles of Incorporation• “Required” terms for 501(c) tax exemption• Asset limitations• No part of the net earnings of the corporation shall inure to the benefit of, or be distributable to its members, trustees, officers, or other private persons…• Reasonable compensation permitted• In dissolution, assets other exempt orgs

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

4

Articles of Incorporation• Permissive terms (§ 21‐1921)• Corporate purpose(s)• Names and addresses of initial directors•Modifications to statutory default rules (e.g., indemnification limits)• Other “hard wired” rules

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Articles of Incorporation• Executed by incorporator(s) (or all initial directors named in Articles)• Filed with Nebraska Secretary of State• Fees: $10 + $5/page ($2 for eDelivery)

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Incorporator Action• Appoint initial board of directors (if not named in the Articles of Incorporation)

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

5

Board Action• Ratify Articles of Incorporation• Adopt Bylaws• Appoint Officers and vest authority• Adopt banking resolutions

Document with meeting minutes or action by written consent

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Bylaws• Subordinate to Articles• Board Governance• Composition (size > 3; terms < 5 yrs) • “Designated” – ex officio• “Appointed”– appointed by a specific person

• Term length• Staggered terms

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Bylaws•Meetings (quorum, voting, written action)• Officers; committees• Amendment• Indemnification•Members (if applicable)

Keep simple – conform to actual practices

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

6

Publish Notice (§ 21‐19,173(a))• 3 successive weeks in a legal newspaper of general circulation in county of the principal office•Must include most of the information required in the Articles of Incorporation• File proof of publication with NE SOS

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Taxpayer ID Numbers• Internal Revenue Service: Form SS‐4• Nebraska Department of Revenue: Form 20

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Forming a Nonprofit Corporation

Types of Permitted Entities• Nonprofit Corporations• Trusts• Unincorporated associations• Limited liability companies

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

7

Common 501(c) Exemptions• (c)(3): charitable, religious, educational, and scientific• (c)(4): social welfare• (c)(6): business leagues• (c)(7): social clubs

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

Benefits of Exemption• Exempt orgs: No federal income tax• EXCEPT on “unrelated business income”

• 501(c)(3) only: Donor may write‐off donations as itemized deductions

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

Obtaining Federal Exemption (501(c)(3))• No filing required if annual gross receipts are normally < $5,000•May file Form 1023‐EZ if eligible• Actual annual gross receipts for the past 3 years and projected annual gross receipts for the next 3 years must be < $50,000)•Must complete 1023‐EZ Eligibility Worksheet

• Otherwise, Form 1023 is required

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

8

Filing Details• 1023: 12 page form + schedules + attachments; $400/$850 fee; 180 day response time

• 1023‐EZ: online form (with attestations); $275; 90 day response time

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

Obtaining Federal Exemption (other orgs)•May self‐declare (via annual Form 990s)• Form 1024 ‐ optional• 6 page form + schedules + attachments; $400/$850 fee; 180 day response time• Obtain a Determination Letter from the IRS

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

Obtaining State Exemptions• NE Income Taxes• Exempt from federal exempt from state• Unrelated business income subject to tax•Must withhold income tax on employee wages

• NE Sales and Use Tax• Exemption limited to certain nonprofits•Must collect sales tax on sales

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Obtaining Tax‐Exempt Status

9

Overview•Maintaining tax exemption• Fundraising issues• State reporting• Corporate governance

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

Maintaining Tax Exemption• Operate “exclusively” for exempt purposes• Avoid private benefit and inurement• Follow political activity rules If a 501(c)(3), avoid campaigns and lobbying

• File annual reports (Form 990, et. al)

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

Maintaining Tax Exemption• Annual Reporting • 990: Gross receipts ≥ $200K OR assets ≥ $500K• 990‐EZ: Gross receipts < $200K and assets < $500K• 990‐N “Postcard”: Gross receipts normally ≤ $50K (some exceptions)• 990‐PF: ALL private foundations

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

10

Maintaining Tax Exemption• Unrelated Business Income (“UBI”)1. Income from any activity conducted to produce income

from selling goods or performing services;2. Regularly carried on; and 3. Not substantially related to the organization’s exempt

purpose (other than its need for money)

• If gross income > $1,000, file Form 990‐T with IRS and Form 1120N with NE Department of Revenue

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

Fundraising Issues• Limit unrelated business income• Demonstrate public charity status•Must show broad base of public support• Reclassified as private foundation if not shown during first 5 years or subsequent 2 year period

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

Fundraising Issues• IRS substantiation requirements•Written acknowledgment for > $250• See IRS Publication 1771 for details

• NE gaming regulations• http://www.revenue.nebraska.gov/gaming/lottraff.html

• Charitable solicitation regulations • Permit not required in NE

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

11

State Reporting• Biennial reports• Due: April 1 of odd numbered years• Fee: $20 (+ $3 for eDelivery)

• Publish notice of amendments to Articles of Incorporation, mergers, or dissolution

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

Corporate Governance• Follow corporate formalities• Apprise directors and officers of fiduciary duties• Adopt and adhere to corporate policies

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Ongoing Governance and Maintenance

Weibling Entrepreneurship ClinicUniversity of Nebraska College of Law

Schmid Clinic BuildingP.O. Box 830902

Lincoln, NE 68583‐0902(402) 472‐[email protected]

https://law.unl.edu/eclinic/Facebook@NELawEClinic

Brett C. [email protected]

Twitter @LawProfStohs

LEGAL FUNDAMENTALS OF STARTING AND OPERATING A NONPROFIT CORPORATION

Wrap‐Up

CONNECT WITH US

twitter.com/NELawEClinic@NELawEClinic

facebook.com/NELawEClinic

CONTACT USSchmid Clinic BuildingUniversity of NebraskaCollege of LawP.O. Box 830902Lincoln, NE 68583-0902

(402) [email protected] online: law.unl.edu/eclinic

Legal Services Provided

UNL does not discriminate based upon any protected status. Please see unl.edu/nondiscrimination.

The Weibling Entrepreneurship Clinic at the University of Nebraska College of Law

provides free legal services to early-stage startup business clients throughout the State of Nebraska. Under supervision of Professor Brett C. Stohs, Clinic students interact directly with clients to provide

legal counseling on a wide range of business law issues.

Serving as a capstone experience for third year law students, the Weibling

Entrepreneurship Clinic provides students with the opportunity to practice as attorneys

within a small law firm. Responsibilities include legal research, writing and analysis,

client communication and relationship building, law practice management, and

community outreach.

WEIBLING ENTREPRENEURSHIP CLINIC

Entity Formation

Regulatory Counseling

Intellectual Property Protection (excluding patents)

Contract Drafting

Employee & Independent Contractor Classification

Founder Agreement Preparation (vesting, buy/sell)

Legal, Ethical and Practical Responsibilities of Lawyers

Serving on Nonprofit Boards Terrence J. Ferguson

Of Counsel Fraser Stryker PC LLO

November 8, 2017 Scott Conference Center, Omaha, NE

Emily A. BlomstedtFraser Stryker PC LLO

1 W1742810.01

LEGAL, ETHICAL AND PRACTICAL RESPONSIBILITIES OF LAWYERS SERVING ON

NONPROFIT BOARDS

Prepared by:

Emily A. Blomstedt, Fraser Stryker PC LLO Terrence J. Ferguson, Of Counsel, Fraser Stryker PC LLO

2 W1742810.01

1. Selecting or Evaluating a Nonprofit for Potential Board Service

a. Nonprofit organizations have a wide variety of missions or activities thatmight appeal to you.

b. Pick the organization you are passionate about or one that you areencouraged to join by a boss, mentor or client and willing to learn toappreciate the organization.

c. Opportunities exist at those organizations to provide pro bonorepresentation or volunteer in some other capacity.

d. There are a myriad of nonprofits: Nebraska Appleseed Center for Law inthe Public Interest, Opera Omaha, Lauritzen Gardens, Bemis Center forContemporary Arts, Nebraska Cultural Endowment, are just a few.

2. Reasons for Becoming a Board Member

a. You have legal skills and practical experience, which can help a board'sdecision-making and oversight responsibilities.

b. You are passionate about the organization's activities.

c. You can help draft governance documents and see that the board fulfills itsduties.

d. You can think strategically with like-minded directors.

e. You get to serve alongside interesting people.

f. There is the satisfaction of supporting a meaningful organization.

g. Contacts may lead to new clients, or even better, new friends.

3. Potential Red Flags to be Aware of in Joining a Board - Do Your Diligence

a. An overactive executive committee in which a few board members make allthe key decisions.

b. Being asked to be on the board solely for your monetary contribution orfundraising capabilities.

i. There may be other structures, such as an advisory board orfundraising committee, that could fulfill this purpose without the timeand liability of board service.

ii. There should be strategic ways that you can contribute to thenonprofit other than solely through personal financial donations andfundraising.

3 W1742810.01

c. Oftentimes there are too many legacy board members. Are there termlimits?

d. Board meetings are boring. No strategic thinking is solicited or wanted.

e. There are too many board or committee meetings.

f. Only a few board members participate in getting things planned andaccomplished. The rest of the board members are just there for the ride.

g. The board fails to balance the annual budget for the organization, which canlead to real financial trouble.

h. The Executive Director does not have a good reputation in the community,or there is dissention among the staff, or factions on the board disagree withthe leadership of the Executive Director.

i. The public perception of the organization is negative.

j. There are one or two super donors. What is the risk that they will go away?

k. There is significant staff turnover, which indicates possible managementtroubles.

l. Do you like the board and staff members who interview you? Are theyforthright?

m. Look over the organization's website and social media accounts of theorganization:

i. The website should feature many of the documents listed below foryou to review, including the mission statement, a link directly to orinstructions on how to request organization's most recent Form 990return, and other financial data.

ii. Useful websites often provide such essential information as the listof board and staff members, code of ethics, and policies on conflictsof interest, document retention and destruction, and whistleblowerprotection.

4. Questions to Ask Before Joining a Board

a. How often does the board meet?

b. How much time will be necessary to spend on matters involving thenonprofit and do you have the time to be a fully engaged board member?

c. Will you need to make or get a financial contribution?

4 W1742810.01

i. If you are expected to make a financial contribution directly (a"contributing board"), how large of a contribution and how often?

ii. If you are expected to get a financial contribution, are youcomfortable asking for money from individuals and corporationswithin your circle of acquaintances?

d. What are the responsibilities of the board? Is it focused mainly on strategicplanning, policy-making, and program evaluation, or is it primarily engagedin fundraising activities or rubber-stamping the Executive Director's ideasand leadership?

e. What liability protections are available to directors, such as Director &Officer Insurance and indemnification arrangements?

f. Are there orientation or board development activities for new members?

i. Ideally, there is a formal onboarding process that will introduce youto both the other directors and the nonprofit staff.

ii. You will want to be fully informed so that you can be a strategicpartner from the beginning rather than merely showing up for yourfirst meeting and having to piece together everything that ishappening around you without proper guidance from the memberswith whom you will be working throughout your board tenure.

5. Documents to Review

a. Mission statement

i. The mission statement should be a focused exposition that statesthe purpose of the nonprofit.

ii. If you do not understand the mission clearly or do not feel a strongcommitment to what the organization does, it is unlikely that you andthe board are a good fit.

b. Basic governance materials

i. Are you able to clearly understand what is written and do the internalgovernance policies make sense?

ii. What, if any, term limits are in place?

c. Conflict of Interest Policy

i. Gives you an opportunity to consider and report any actual orpotential conflicts of interest.

5 W1742810.01

d. Audited financial statements and auditor comments for the last two years todetermine if the nonprofit is in a good financial condition

e. Financial reports for the most recent two quarters

f. The current budget and next year's proposed budget.

g. Most recent IRS Form 990

i. The 990 is a primary source of information about the nonprofit'sfinances, governance, operations and programs for federalregulators, the public and many state charity officials.

ii. The 990 can demonstrate the nonprofit's commitment toaccountability and transparency by offering additional informationabout what they do and how they operate.

h. Strategic plan

i. Names and contact information of the board members.

i. Do you know and respect any current members?

ii. Are there any potential conflicts of interest or personality issues toconsider?

iii. You may also want to contact current board members and inquireabout their experiences to determine whether joining the board issomething you really want to do.

j. Press releases about the organization over the past year

6. Responsibilities of Board Service

a. Directors have a duty of care and a duty of loyalty.

i. Duty of Care: directors must be reasonably informed, participate indiscussions, and to do so in good faith and with the care an ordinaryprudent person in similar circumstances would exercise.

ii. Duty of Loyalty: directors must act in good faith and in a manner thatyou reasonably believe to be in the best interests of the organization,not in your own best interest or in the best interest of some otherperson.

b. To fulfill your duty of care, you must:

i. Attend board and committee meetings;

6 W1742810.01

ii. Read and understand financial and other reports;

iii. Ask questions if you don't understand something; and

iv. Participate in discussions.

c. To fulfill your duty of loyalty, you must remain independent or recuseyourself from discussing and/or voting on matters in which you have apersonal interest. The independent and non-managerial board membersare an organizational resource that should be used to assure the exerciseof independent judgment in board decision-making.

i. A conflict of interest arises when a board member or staff person'sduty of loyalty to the charitable organization comes into conflict witha competing financial or personal interest that he or she (or a relative)may have in a proposed transactions.

ii. The fact of any conflict and the action taken in response, includingabstention, should be recorded in the minutes.

iii. A substantial majority of the board of a public charity, usuallymeaning at least 2/3 of the members, should be independent.

d. An attorney who is serving as a board member is increasingly expected tohave more extensive knowledge and to conduct more extensiveinvestigation into the facts than other outside directors. Nonprofitmanagement and the Board may look to you for legal guidance on a widerange of issues even when you are only acting as a board member.

i. ABA Model Rule 1.1 requires a lawyer to provide "competentrepresentation." Thus, an attorney on the board must be careful notto stray into areas of law he or she does not practice or has notbecome knowledgeable. The attorney-director must exerciseindependent professional judgment at all times.

ii. The duty of care may be heightened for an attorney serving on theboard. Action (or inaction) that may be held to be mere negligenceon the part of an outside director may be held to be gross negligenceby an attorney-director.

iii. You must clarify when you are serving in your capacity as a lawyerand avoid giving advice on areas outside of your expertise orcompetence.

e. Hold in confidence all internal matters that are not in the public domain.

7 W1742810.01

f. Participate in fundraising by supporting the organization's developmentprocess: identify potential donors, arrange meetings, and explain why youare passionate about the organization.

g. Advocate for the nonprofit.

7. Potential Liabilities of Board Service

a. Potential Liabilities of Nonprofit Organizations.

i. Nonprofits can be the subject of investigations, public scrutiny, andeven possible lawsuits, which are not limited to the actions of thecharities themselves but also can involve alleged wrongdoing bytheir directors and officers.

ii. Currently, most suits against nonprofit organizations are primarily fordiscrimination, sexual harassment, and wrongful termination. A smallpercentage of claims against these entities also involve financialmismanagement issues.

iii. A director or officer does not have to be sued to incur liability.Investigations can be burdensome in terms of time and money, sincedirectors and officers of nonprofit organizations must not only rebutallegations and absolve themselves of potential liability but must alsoensure the charitable organization's long-term reputation, which isessential to its fundraising activities.

iv. Even when a director or officer is not directly accused of misconduct,he or she may be subject to scrutiny for not doing enough to stop analleged violation. This is worrisome because most nonprofit directorsare outsiders who agree to serve on a board without compensationand with little direct knowledge of a nonprofit's day-to-day affairs.

b. Failure to Recognize Potential Personal Liability

i. Many directors pay too little attention to the individual risks facingdirectors of nonprofit organizations:

° Directors often assume that nonprofit entities enjoy a certain judicial immunity from claims against their directors and officers, since by definition such entities are not subject to shareholder actions.

° Directors also assume that the nonprofits they serve are unlikely to be sued, reasoning that some, mostly small, nonprofit organizations are known to have relatively few valuable assets, or that prospective litigants will suppress the

8 W1742810.01

urge to seek pecuniary relief from a nonprofit entity if it appears that its beneficiaries will suffer.

° Some directors assume that their existing statutory protection and indemnification arrangements set forth in the nonprofit entity's charter document are sufficient to avoid liability or to fund a defense adequately, even when they themselves have been grossly negligent or have exercised poor judgment, or when the nonprofit entity is experiencing financial difficulty.

ii. However, although the vast majority of claims are made directlyagainst the entity, some claimants do seek to sue individuals withinthe organization in addition to, or instead, of the organization itself.Those individuals are often prominent citizens who may sometimesrepresent another deep pocket.

c. Potential Sources of Personal Liability for Board Members

i. Board members may have personal liability for fines and otherpenalties as a result of certain legal violations, such as failure to payrequired payroll and other taxes or approval of excess benefit or self-dealing transactions.

° For example, Individuals engaging in prohibited private benefits or benefiting from private inurement are subject to "intermediate sanctions" under IRC § 4958. This section imposes a 25% excise tax on prohibited "excess benefit transactions" by "disqualified persons." The term "disqualified person" is broadly defined to include "any person who was, at any time during the 5-year period ending on the date of such transaction, in a position to exercise substantial influence over the affairs" of an applicable charitable organization, as well as a member of the family of such an individual or an entity at least 35% controlled by such individual. A second tier tax equal to 200% of the excess benefit involved is imposed if the disqualified person does not correct the violation within the taxable year. IRC § 4598(b). In addition, "organization managers" (defined to include a director) who participate in an excess benefit transaction, are subject to an excise tax equal to 10% of the excess benefit up to a maximum penalty of $20,000 per excess benefit transaction. However, the excise tax will not apply if the manager's participation was not willful and was due to reasonable cause. IRC § 4958(a)(2).

° An excess benefit transaction is "any transaction in which an economic benefit is provided by an applicable tax-exempt organization directly or indirectly to or for the use of any

9 W1742810.01

disqualified person if the value of the economic benefit provided exceeds the value of the consideration received for providing the benefit. IRC 4958(c)(1)(A). In general, this arises when the nonprofit pays greater than fair market value or receipt of unreasonable or excessive compensation for services is rendered.

° May unknowingly engage in an excess benefit transaction in designating compensation for key officers and employees.

ii. Nonprofits can be the subject of investigations, public scrutiny, andeven possible lawsuits, which are not limited to the actions of thecharities themselves but also can involve alleged wrongdoing bytheir directors and officers.

8. Legal Protections for Board Service

a. Statutory Protections

i. Federal statutes as well as statutes in nearly every state have beenenacted to "shield" uncompensated directors, officers, and other"volunteers" from certain claims and/or damages (commonly called"shield laws"). However, the scope of the protections is often limited.

ii. Nebraska does have a "shield law" in Neb. Rev. Stat. § 25-21,191,which provides that any person who serves as a director of anonprofit organization and who is not compensated for his or herservices on a salary or a prorated equivalent basis shall be immunefrom civil liability for any act or omission which results in damage orinjury if such person was acting within the scope of his or her officialfunctions and duties as a director unless such damage or injury wascaused by the willful or wonton act or omission of such director.

° Note that this shields only civil liability upon certain terms and conditions. In addition, Neb. Rev. Stat. § 25-21,192 provides additional limitations, such as when a director causes damage or injury while operating a vehicle or while impaired by alcohol or any controlled substance.

° Also, the statute provides that "nothing in this section shall be construed to establish, diminish, or abrogate any duties that a director, officer, or trustee of a not-for-profit organization has to the not-for-profit organization for which the director, officer, or trustee services." Neb. Rev. Stat. § 25-21,191(1).

° This statute is not a "get out of jail free card." While there are no reported decisions interpreting this statutory immunity, it appears a volunteer director can still be held liable for

10 W1742810.01

breaching his or her duties to the organization despite this statute.

iii. Nebraska law also mandates, permits, and prohibits indemnificationof directors in certain circumstances.

° Neb. Rev. Stat. § 21-1998 mandates that unless limited by the organization's articles of incorporation, a nonprofit must indemnify a director who was wholly successful, on the merits or otherwise, in the defense of any proceeding to which the director was a party because he or she was a director against reasonable expenses actually incurred by the director.

° Neb. Rev. Stat. § 21-1997 permits a nonprofit to indemnify a director if the individual satisfies certain requirements, such as acting in good faith, reasonably believing that the his or her conduct was in the nonprofit's best interest or at least not opposed to the nonprofit's best interest, and in the case of a criminal proceeding, had no reasonable cause to believe his or her conduct was unlawful.

° Neb. Rev. Stat. § 21-1997 prohibits a corporation from indemnifying a director in certain circumstances, such as in connection with a proceeding by or in the right of the nonprofit in which the director was adjudged liable to the nonprofit, or in connection with any other proceeding charging improper personal benefit to the director, in which the director was adjudged liable.

iv. There are some obscure federal statutes such as the FederalVolunteer Protection Act of 1997, which generally protects nonprofitvolunteers against liability for harm caused by ordinary negligence.See 42 U.S.C. §§ 14501-14505. There are, however, manyexceptions, including, but not limited to, acts that constitute grossnegligence or recklessness, acts of violent crime, hate crimes, andany violations of civil rights laws. Also, it does not cover claims thataffect nonprofit directors most frequently, such as claims relating towrongful termination or discrimination.

b. Courts apply the Business Judgment Rule

i. Even where a nonprofit action has proven to be unwise orunsuccessful, a director will generally be protected from liabilityarising therefrom if he or she acted in good faith and in a mannerreasonably believed to be in the organization's best interest, and withindependent and informed judgment.

11 W1742810.01

ii. The doctrine is basically a statement by the courts that it isinappropriate for them to second-guess corporate managementdecisions.

iii. For example, in a Nebraska Court of Appeals decision from 2004,certain members of a nonprofit homeowners association disagreedwith the association's decision as to how budgeted funds are appliedtoward the maintenance and common areas of the development.Stoller v. NWE Homeowners Ass'n, 2004 Neb. App. LEXIS 115, at*27 (Ct. App. May 18, 2004). The Court refused to second-guess thedecisions of the homeowner's association, stating that in the absence of usurpation, fraud, gross negligence, transgression of statutory limitations, courts will not interfere at the suit of dissatisfied stockholders merely to overrule the discretion of directors on questions of corporate management, policy, or business. This principle is also applicable to suits by dissatisfied members of a nonprofit association.

iv. There are numerous exceptions:

° Basic breaches of duty by the director (criminal activity, fraud, bad faith, willful and wonton misconduct);

° For public charities, business decisions that would result in significant reduction or cessation of operations (such as the decision of a nonprofit health system to close down a money-losing hospital) may be challenged by the state attorney general on grounds that such action would violate the directors' duties to maintain the functions of a charitable trust.

c. Nonprofit Agreements to Indemnify. Generally consists of an obligation ofthe nonprofit to cover the legal fees a board member might incur indefending an action made by the individual on behalf of the agency, as wellpaying settlements or judgments related to serving on the board.

i. Policy in Governing Documents: Often, the nonprofit places policiesin its articles of incorporation, bylaws, resolutions, or otherdocuments providing that the nonprofit will indemnity the director ifcertain conditions are satisfied.

ii. Separate Agreement: This agreement should be at least equal inscope to what is provided in the bylaws. Unlike an indemnificationpolicy in the governing documents, these protections cannot beeliminated or amended unilaterally by the board or members of thenonprofit. In addition, if the protection provided by the articles ofincorporation, bylaws, or the statutory provisions does not offer thebroadest coverage available, the agreement should include such

12 W1742810.01

additional contractual provisions as are advisable to further protect the director or officer

iii. Potential Issues:

° The extent to which a charity may indemnify its directors and officers is limited. Neb. Rev. Stat. § 21-19,104 provides that any indemnification provisions in the articles of incorporation, bylaws, a resolution of its members, or in a contract or otherwise, is valid only to the extent that it is consistent with the Nebraska laws discussed above.

° Even when indemnification is legally available, the charity may not be in a financial position to indemnify. This is especially true for smaller, local charities whose budgets are inadequate in the fact of high costs of litigation, potential litigation, investigation, or settlement.

° Even when indemnification is financially possible, the nonprofit organization does not always have the will to advance legal defense costs to defend its directors and officers.

d. Directors and Officers Insurance Policies

i. The board should assess periodically the organization's need forinsurance coverage based on its program activities and financialcapacity.

ii. Benefits the nonprofit by:

° Covering the liability of the entity for wrongful acts committed by the director or officer or acts otherwise attributable to the entity itself;

° Shifting the burden of defense payments from the entity to the insurance company;

° Limiting the adverse impact of potential D&O liability on qualified individuals' decision to work for, or become associated with, the nonprofit entity; and

° Facilitating coverage when the entity's public, financial or political standing would otherwise make direct indemnification of various individuals unfeasible or unpalatable.

13 W1742810.01

iii. With adequate D&O coverage, directors and officers do not have toworry about the financial health of the indemnifying nonprofit entity(as long as D&O insurance premiums are paid).

iv. Pay careful attention to whether employment practices liabilityclaims, such as claims involving wrongful termination, discrimination,or sexual harassment, which are often specifically excluded fromsuch policies.

e. Other financial strategies can reduce risk of loss

i. Nonprofit may establish reserve funds to absorb minor losses;

ii. Nonprofit may negotiate with third parties, such as key donors, toabsorb certain losses;

iii. Implement policies and procedures designed to reduce the risk ofvarious occurrences, or limit the exposure of the organization tocertain identified risks.

iv. A director who is also employed by an entity other than the nonprofitshould ascertain whether the other employer will agree to cover thatservice to the nonprofit under the employer's policy. If the director isemployed by a law firm, the law firm's malpractice policy coversclaims arising solely in the capacity as an attorney. Therefore, thepolicy may provide coverage if the role of the attorney-director is veryclear. If it is not, the carrier may have an argument that its coveragedoes not apply.

v. A director should have a personal umbrella policy, which may providecoverage for service as a director of a nonprofit. It may be necessaryunder the relevant policy to notify the umbrella insurer of a change inthe covered individual's status when he or she accepts a newposition as a director or officer of a nonprofit.

9. Corporate documentation is an area where attorneys can be very helpful bydrafting and explaining their purposes to other board members. Some examplesof basic nonprofit documents are the following.

a. Mission Statement

b. Bylaws

c. Conflict of Interest Policy:

i. Written policy for officers, directors, employees, and, in some cases,volunteers that should cover "self-dealing" transactions with theorganization (i.e., when the officer, director, employee, a family

14 W1742810.01

member, or affiliated corporation is "on the other side" of a transaction with the corporation), as well as prohibition against personal use of corporate assets, such as appropriating empty office space to run a personal business without payment to the organization, use of or disclosure of confidential information, or taking advantage of opportunities that rightly belong to the organization.

ii. Directors and officers should be required to disclose at least annuallytheir material business and financial relationship that create or mayresult in a conflict between their personal interest and the bestinterests of the organization.

iii. Directors and officers also should annually affirm that they have read,understood, and adhered to the organization's conflict of interestpolicies.

d. Code of Ethics:

i. The Code should be applicable to directors, senior management andkey employees and reflect a commitment to operating in the bestinterests of the organization and in compliance with applicable law,ethical business standards and the organization's governingdocuments.

ii. The Code should address duties of directors, corporateopportunities, confidentiality, fair dealing, protection, and the properuse of company assets; compliance with laws, rules, and regulations;nondiscrimination; sexual harassment; gifts, gratuities, and otherentertainment; and, along with the Whistleblower Policy,encouragement of reporting any illegal or unethical behavior.

e. Document Retention and Destruction Policy:

i. The Sarbanes-Oxley Act prohibits the destruction of documents thatmay be material to a federal investigation (applies to a nonprofit aswell as for-profit organizations). Other statutes require certain typesof records to be kept for a stated period.

ii. For the most part, however, the periods for which documents are tobe retained are based on the statute of limitations for a lawsuit. Forexample, because the IRS has six years after the filing of a return tobring a claim for taxes if there has been an underreporting of incomeby 25% or more, most policies require retention of tax returns for 7years. The policies also state that no documents may be destroyedor altered where there is pending, threatened or reasonablyforeseeable governmental investigation.

15 W1742810.01

iii. The Sarbanes-Oxley Act clarified and increased certain criminalpenalties for obstruction of justice caused by destruction ofdocuments that are, or are anticipated to become, subject to anofficial proceeding or federal agency investigation. Conviction forsuch crimes is punishable by fines and imprisonment up to 20 years.The increased penalties for obstruction of justice by destruction ofdocuments apply to all persons and entities, not just publicly tradedcompanies.

f. Whistleblower Policy:

i. The Sarbanes-Oxley Act creates penalties for retaliating againstwhistleblowers during a federal investigation.

ii. Every nonprofit, regardless of size, should have clear policies andprocedures that allow staff, volunteers, or clients of the organizationto report suspected wrongdoing within the organization without fearof retribution. Information on these policies should be widelydistributed to staff, volunteers and clients, and should beincorporated both in new employee orientations and ongoing trainingprograms for employees and volunteers. Such policies can helpboards and senior managers become aware of and addressproblems before serious harm is done to the organization. Thepolicies can also assist in complying with legal provisions that protectindividuals working in charitable organizations for engaging in certainwhistle-blowing activities. Violation of such provisions may subjectorganizations and the individuals responsible for such violations tocivil and criminal sanctions.

iii. These policies generally cover suspected incidents of theft; financialreporting that is intentionally misleading; improper or undocumentedfinancial transactions; improper destruction of records; improper useof assets; violations of the organization's conflict-of-interest policy;and any other improper occurrences regarding cash, financialprocedures, or reporting.

g. Charters for Committees: The board of a nonprofit should adopt a charterfor each of its committees. A charter should set out the who, what, when,why and how of the committee. The charter helps the committee from goingoutside of the scope of its tasks and minimizes disagreements by settingforth who is tasked with certain issues. I

h. Gift Acceptance Policy:

i. The policy can provide guidance when a prospective donor offers togift the board an interest of any kind.

16 W1742810.01

ii. The policy can be as simple as a statement that gifts other than cashand publicly traded stock are subject to an acceptance procedure.

iii. A policy may help the organization avoid offending potential donorsby making it clear that the extra level of review is something that is ageneral practice and not directed at the specific situation.

i. Investment Policy: Every organization with investment assets should havean investment policy. The existence of the policy and procedures for itsreview provide the board or investment committee the opportunity foraddressing how assets are invested and for thinking about what allocationsshould serve the organization best.

j. Investment Distribution Policy:

i. The policy specifies the procedure for settling the distributionamount, the frequency of the distribution and the purpose for whichthe funds are distributed. For example, funds might be distributedfor operating expenses of a certain endowment, pursuant to thedirection of the donor. Private foundations are required to spendannually for charitable purposes an amount equal to 5% of the valueof their net investment assets. See IRC § 4942. Charitablenonprofits generally set the distribution amount at less than 5% ofthe principal amount of the fund, and allow an additional distributionfor the management costs of the investment.

ii. The nonprofit may choose to spend more, for example, in times whenthe value of their assets have fallen. Changes in the state lawsgoverning true endowments (funds restricted by the donor to theexpenditure of income only), permit flexibility in the amount that maybe spent. This leaves the organization's governing board withchoices to make about what the level of spending from theendowment will be. Even if the organization's funds are not donorrestricted, the board needs to balance the current needs of theorganization with anticipated future needs, and setting a spendingpolicy gives the board an opportunity to consider these competingneeds.

k. Engagement letters with the Auditor and the Investment Advisor

l. Employment Agreement or contract with the Executive Director

m. Personnel Policy

n. Explain the purpose of these documents

10. Committees

17 W1742810.01

a. Standing committees. At a minimum, a nonprofit should have certainstanding committees, many of which call for independent directors underthe Sarbanes-Oxley Act.

i. Executive Committee

ii. Audit Committee. Under the Sarbanes-Oxley Act, the auditcommittee should assure the independence of the nonprofit'sfinancial auditors, review the organization's critical accountingpolicies and decisions and the adequacy of its internal controlsystems, and oversee the accuracy of its financial statements andreports.

iii. Finance and Investment Committee for smaller nonprofits

iv. Development Committee

v. Nomination and Governance Committee: Under the Sarbanes-OxleyAct, this committee should focus on core governance and boardcomposition issues, including: (1) the governing documents of theorganization and the board; (2) the criteria, evaluation , andnomination of directors; (3) the appropriateness of board size,leadership, composition, and committee structure; and (4) codes ofethical conduct.

vi. Compensation Committee: Under the Sarbanes Oxley Act, thiscommittee should determine the compensation of the chief executiveofficer and determine or review the compensation of other executiveofficers, and assures the compensation decisions are tied to theexecutives' actual performance in meeting predetermined goals andobjectives.

b. You may also want to have special project groups: subcommittees, ad hoccommittees or task forces.

Lawyers as Nonprofit Board Members – Legal Ethics

Considerations Jonathan R. Breuning

Baird Holm, LLP

November 8, 2017 Scott Conference Center, Omaha, NE

© 2017 Baird Holm LLP 1

Lawyers as Nonprofit Board Members

Legal Ethics Considerations

Jonathan R. Breuning

Introduction

• Serving a Nonprofit Corporation – Roles> Lawyer Only> Volunteer/Director Only> Dual Roles – the Lawyer/Director

• Issues Unique to Lawyers – Legal Ethics

Rules Which Promote Public Service

• Preamble comment [1] (also [6])• Rule 6.1, especially (a)(2) and (b)(1)• Rule 6.3• Rule 6.4• Rule 6.5

© 2017 Baird Holm LLP 2

Ethics Considerations When Serving Only as a Volunteer

• Can you do it?• Conflicts and Rule 1.7• Rule 1.10• Confidentiality• What if you’re on two different

nonprofit boards?

Scenario #1You chair a church committee that promotes legacy giving from its parishioners. As chair, you explain the program to parishioners. To help both the church and the parishioners who choose to give through this program, you wish to volunteer your services to prepare estate planning documents for unrepresented parishioners. You would receive no compensation for such services from either the church or its parishioners. May you do so?

Maryland State Bar Association Committee on Ethics, Docket No. 2003-08

You chair a church committee that promotes legacy giving from itsparishioners. As chair, you explain the program to parishioners. To helpboth the church and the parishioners who choose to give through thisprogram, you wish to volunteer your services to prepare estate planningdocuments for unrepresented parishioners. You would receive nocompensation for such services from either the church or its parishioners.May you do so?

A. YesB. No

© 2017 Baird Holm LLP 3

Ethics Considerations When Serving as

Both Lawyer and Volunteer

• Start with the basics – if you’re their lawyer, you’re their lawyer, and all of the Rules apply

• When are you wearing which hat? Does it matter?

Independence

• Rule 2.1> Independent professional judgment> Other (extra-legal) considerations> Comments [1] through [5]

• Rule 1.13 comment [3]

The Dual Role and Conflicts

• Rules 1.7 and 1.10• IRS Conflict of Interest Guidelines• Board decisions to hire outside counsel• Fee disputes with the client• Advice-of-counsel defense

© 2017 Baird Holm LLP 4

Scenario #2From 1989 to 1992, Clark served on the Board of Governors of a county hospital. In that role, along with other Board members, he had access to confidential information about the hospital's quality assurance and medical staff peer review activities. He was never the hospital's lawyer, and the hospital was never his client. Shortly after his term on the hospital board ended, a hospital patient died following emergency surgery. Shortly thereafter, one of Clark's law partners filed two actions against the hospital on behalf of the estate of the deceased patient, one alleging malpractice, and one seeking quality assurance and peer review records under the state Freedom of Information Act. The hospital moved to disqualify the firm based on Clark's service as a member of the hospital Board during the preceding three years. Should the firm be disqualified?

Click A to vote Yes or B to Vote No

Berry v. Saline Memorial Hospital, 907 S.W. 2d 736 (Ark. Sup. 1995)

From 1989 to 1992, Clark served on the Board of Governors of a county hospital. In that role,along with other Board members, he had access to confidential information about thehospital's quality assurance and medical staff peer review activities. He was never thehospital's lawyer, and the hospital was never his client. Shortly after his term on the hospitalboard ended, a hospital patient died following emergency surgery. Shortly thereafter, one ofClark's law partners filed two actions against the hospital on behalf of the estate of thedeceased patient, one alleging malpractice, and one seeking quality assurance and peerreview records under the state Freedom of Information Act. The hospital moved to disqualifythe firm based on Clark's service as a member of the hospital Board during the precedingthree years. Should the firm be disqualified?

A. YesB. No

The Dual Role and Confidentiality & Privilege

• Rule 1.6

• Attorney Client Privilege

© 2017 Baird Holm LLP 5

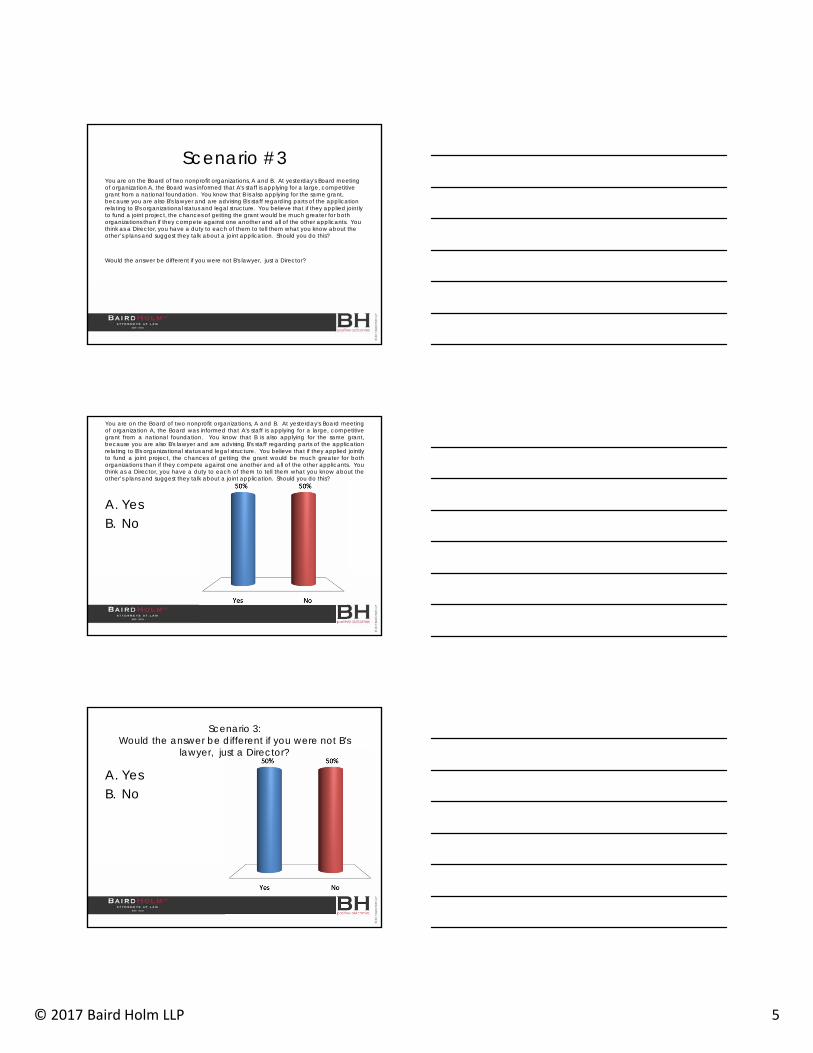

Scenario #3 You are on the Board of two nonprofit organizations, A and B. At yesterday's Board meeting of organization A, the Board was informed that A's staff is applying for a large, competitive grant from a national foundation. You know that B is also applying for the same grant, because you are also B's lawyer and are advising B's staff regarding parts of the application relating to B's organizational status and legal structure. You believe that if they applied jointly to fund a joint project, the chances of getting the grant would be much greater for both organizations than if they compete against one another and all of the other applicants. You think as a Director, you have a duty to each of them to tell them what you know about the other’s plans and suggest they talk about a joint application. Should you do this?

Would the answer be different if you were not B's lawyer, just a Director?

You are on the Board of two nonprofit organizations, A and B. At yesterday's Board meetingof organization A, the Board was informed that A's staff is applying for a large, competitivegrant from a national foundation. You know that B is also applying for the same grant,because you are also B's lawyer and are advising B's staff regarding parts of the applicationrelating to B's organizational status and legal structure. You believe that if they applied jointlyto fund a joint project, the chances of getting the grant would be much greater for bothorganizations than if they compete against one another and all of the other applicants. Youthink as a Director, you have a duty to each of them to tell them what you know about theother’s plans and suggest they talk about a joint application. Should you do this?

A. YesB. No

Scenario 3: Would the answer be different if you were not B's

lawyer, just a Director?

A. YesB. No

© 2017 Baird Holm LLP 6

The Dual Role and Business & Liability Risks

• Competence• Response to Auditors’ Inquiries• Increased Liability Risks• Insurance Coverage• Statutory Immunities

Practical ConsiderationsWhen Serving Only as a Volunteer Director

• Requests for Legal Advice• Conflicts of Interest• Duty of Competence• Need for Formal Legal Counsel

Practical ConsiderationsWhen Serving as Both Lawyer and Director

• Be Sure You Know Why• Clarity of Role• Recusing When Appropriate• Liability Coverage• Independence and Diligence• Attorney Client Privilege

© 2017 Baird Holm LLP 7

QuestionsAnd

Discussion

Top Reasons Why Nonprofits Get Investigated

Daniel Russell Nebraska Attorney General’s Office

November 8, 2017 Scott Conference Center, Omaha, NE

1

Top Reasons Why Nonprofits Get InvestigatedDaniel Russell, Assistant Attorney General

Nebraska Attorney General’s Office

The information provided in this presentation is for educational purposes only and is not intended to be complete and comprehensive. I highly recommend that you seek legal, tax, and financial advice from professionals. The Nebraska Attorney General’s Office cannot provide legal, tax, or financial advice regarding new or existing nonprofit entities.

The privileges provided by law to public benefit corporations, and other charitable

institutions, carry a corresponding obligation to be accountable to the public

for the actions such institutions undertake.

Gilbert M. & Martha H. Hitchcock Found. v. Kountze, 272 Neb. 251, 259, 720 N.W.2d 31, 37(2006).

2

…statutory authority has been given to the AG to act inthe public good in enforcing the requirements applicable to nonprofit corporations, particularly public benefit corporations. In other words, the AG has standing to protect the public interest…Gilbert M. & Martha H. Hitchcock Found. v. Kountze, 272 Neb. 251, 259, 720 N.W.2d 31, 37(2006).

The Attorney General’s Mission & The Public’s Interest

An efficient and successful nonprofit sector is absolutelyessential to Nebraska’s well-being

What we do supports that goal

We believe the nonprofit sector represents some of thebest people and ideas in Nebraska

Nebraska nonprofit corporations do an incredible job—does not get said enough

Attorney General’s Mission

Nonprofits & the law

Nebraska Attorney General’s Office

Internal Revenue Service

Nebraska Secretary of State

3

Top 10 Ways to Get Investigated

#1 Failure to Follow Mission “asleep at the wheel”

Have a duty to actively work towards fulfilling your mission.Can you say what your organization does?

Should have tangible, critical assessments of efficiency and program successes.

Bad excuse #1 “Technically, it's legal.”(but what will your donors and constituents say)

#2 Conflicts of Interest

A nonprofit corporation should be above reproach.

• If any transaction gives even the appearance of a conflict ofinterest, think hard about avoiding it.

Would the media and your Mom understand?

IRS, donors, media, and the general public all havedifferent views of conflicts.

None are good.

4

Director’s Conflict of InterestNeb. Rev. Stat. §21-1987

A conflict of interest transaction is a transaction with thecorporation in which a director of the corporation has adirect or indirect interest.

A conflict of interest transaction is not voidable or thebasis for imposing liability on a director if the transactionwas fair at the time it was entered into or approved bycertain parties.

Director’s Conflict of InterestNeb. Rev. Stat. §21-1987

A conflict matter may be approved either before or afterthe transaction if it is approved by the Attorney Generalor the district court.

A conflict matter may be approved before the transactionby the board of directors or a committee of the boardunder certain circumstances.

#3 Fraud and Embezzlement, Failing to Respond and Prevent

Nonprofit corporations, and theirdirectors, have a fiduciary duty toprotect their assets.

Why important?• They’re stealing from you!

• One sixth of major embezzlements occurs at nonprofits and religious organizations, second only to the financial industry. (Washington Post)

Many, many organizations are victims and do not know it.

5

#3 Fraud and Embezzlement, Failing to Respond and Prevent

Must take all reasonable steps to prevent.

1. Depends on organizational size.

• Even the smallest organizations MUST take steps

2. No substitute for constant vigilance!

• Culture and small steps go a long way

• Discuss and create polices

3. Remember, audits are generally not designed to catch fraud.

• Only test accuracy of internal financial statements

#3 Fraud and Embezzlement, Failing to Respond and Prevent

Fraud or Embezzlement will happen to an organizationrepresented here.

Must take all reasonable steps in response.• Punish offender

• Report to law enforcement (and cooperate!)

• Get your money back

Close whatever hole was exploited.• Opportunity to strengthen your organization

#3 Fraud and Embezzlement, Failing to Respond and Prevent

Bad excuse #2: “We completely trusted_____.”

Bad excuse #2A: “We didn’t want our donations to suffer, so we didn’t tell anyone.”

Bad excuse #2B: “We thought our auditor would catch that.”

6

#4 Paying Excess Compensation

All of your assets must go to your charitable purposes,and you must pay reasonable compensation.

Everything should be reasonable and justified.

Avoid paying substantially more than similar organizationsand lavish expense accounts.

• Remember IRS excess compensation rules

• Expense accounts matter

Bad excuse #3 “We had left over money so figured we would go to Vegas, buy a BMW, etc.”

#5 Failing to Operate with the Needed Transparency

Top complaint generator

• Easy for Attorney General to follow up

Law:

• Law: Nebraska statues list required corporate records and inspection rights for members, Neb. Rev. Stat. §21-19,165

• Law: Directors get everything

Goal: A nonprofit should seek to operate withglass pockets

Bad excuse #4: “Only our Treasurer gets to see the financial records.”

#6 Directors & Senior Leadership Failing to be Sufficiently Active

Directors have a fiduciary duty to be active and obtain sufficient information to make informed decisions.

Directors must understand the organization’s financial health.

There must be regular reporting to the Board.

• The directors must know all of the nonprofit’s activities.

• Directors must actively seek the information they need.

• The Executive Director works for the board.

Bad excuse #5 “We're a volunteer board and don't have the time to ________.”

7

#7 Not Filing What You Should with Government Agencies

What Needs to be Filed

• Internal Revenue Service: Form990 or other annual form

• After 1/1/2009 everyone MUST file something

• Automatic loss of exemption

• Secretary of State: Biennial Report

• Administrative dissolution if fail to file

#7 Not Filing What You Should with Government Agencies

Attorney General: Tax Returns• 990 PF

• Requirement of the IRS

#7 Not Filing What You Should with Government Agencies

Attorney General: Nebraska Nonprofit Corporation Act

Dissolution and transfer of assets upon dissolutionNeb. Rev. Stat. § 21-19,131 (See Attorney General handout for guidance)

Nonprofit selling/transferring all or substantially all of itsassets not within the regular course of businessNeb. Rev. Stat. § 21-19,126

Notice of the commencement of any proceeding that theNonprofit Act authorizes the AG to bring but that hasbeen commenced by another personNeb. Rev. Stat. § 21-1918

Others

8

#7 Not Filing What You Should with Government Agencies

Why important?• Severe sanctions from agency

• Public will misinterpret

• Donors, potential donors, clients, and everyone else all see lack of filing

• All information is just a click away

• Pay attention to digital footprint

• Rating sites: give.org, Charity Navigator

• 990 sites: Guidestar, Foundation Center

#8 Misusing Your Endowmentand Restricted Assets

Nebraska Uniform Trust Code (Neb. Rev. Stat. § 30-3801 to 30,110)

Nebraska Uniform Prudent Management ofInstitutional Funds Act (Neb. Rev. Stat. §§ 58-610 to 58-619)

A charitable trust may be created for the relief of poverty, the advancement of education or religion, the promotion of health, governmental or municipal purposes, or other purposes the achievement of which is beneficial to the community. (Neb. Rev.Stat. § 30-3831(a))

"Charitable trust" means a trust, or portion of a trust, created for a charitable purpose (Neb. Rev. Stat. § 30-3803(4))

Charitable Trusts

9

“In the case of a charitable trust, the Attorney General has long been recognized as having the right to maintain an action for enforcement of the trust or to prevent a misuse of the property.” Gilbert M. & Martha H. Hitchcock Found. v. Kountze, 272 Neb. 251, 259, 720 N.W.2d 31, 37(2006) citing In re Estate of Grblny, 147 Neb. 117, 22 N.W.2d 488 (1946)

Attorney General's Role

The Attorney General has the rights of a Qualified Beneficiary with regard to charitable trusts whose principal place of administration is in Nebraska

– Neb. Rev. Stat. § 30-3810(d)

What does this mean?

– The AG is required to receive notice in certain circumstances

– The AG has statutory authority to enforce the trust and bring a petition to remedy a breach of trust

Attorney General's Role

All qualified beneficiaries, including the Attorney General, must be kept reasonably informed about the administration of the trust and of the material facts necessary for them to protect their interests (Neb. Rev. Stat. § 30-3878)

– shall notify the qualified beneficiaries in advance of any change in the method or rate of the trustee's compensation.

– A trustee shall send to the distributees or permissible distributees, and to other qualified or nonqualified beneficiaries who request it, at least annually and at the termination of the trust, a report of the trust property, liabilities, receipts, and disbursements, including the source and amount of the trustee's compensation, a listing of the trust assets and, if feasible, their respective market values.

Notice Provisions

10

All qualified beneficiaries, including the Attorney General, must be kept reasonably informed about the administration of the trust and of the material facts necessary for them to protect their interests (Neb. Rev. Stat. § 30-3878)

– Furnish a copy of the trust instrument upon request

– Within 60 days of accepting a trusteeship shall notify the AG of the acceptance and of the trustee's name, address, and telephone number

– Within sixty days after the date the trustee acquires knowledge of the creation of an irrevocable trust shall notify the qualified beneficiaries of the trust's existence, of the identity of the settlor or settlors, of the right to request a copy of the trust instrument, and of the right to a trustee's report

Notice Provisions

The Attorney General must also be informed regarding changes to a trust

– Neb. Rev. Stat. § 30-3838 – changes to the administrative terms of a trust (impracticable, wasteful or impair the trust's administration)

– Neb. Rev. Stat. § 30-3839 – Cy Pres (charitable purpose becomes impracticable, impossible to achieve or wasteful)

– Neb. Rev. Stat § 30-3840 – Termination of an uneconomic trust(less than $100,000, cannot justify the costs of administration)

– Neb. Rev. Stat § 30-3843 – Combination and division of trusts.

Changes in a trust

KEEP OUR OFFICE INFORMED

Duty to Administer Trust (Neb. Rev. Stat. § 30-3866)

– Good faith

Duty of Loyalty (Neb. Rev. Stat. § 30-3867)

– Administer the trust soley in the interests of the benficiaries

Duty of Impartiality (Neb. Rev. Stat § 30-3868)

Duty of Prudent Administration (Neb. Rev. Stat. § 30-3869)

Duties of a Trustee

11

Remedies of a Breach of Trust (Neb. Rev. Stat. § 30-3890)

– Compel the trustee to perform the trustee's duties

– Enjoin the trustee from committing a breach of trust

– Compel the trustee to redress a breach of trust by paying money, restoring property, or other means

– Reduce or deny compensation to a trustee

Removal of Trustee (Neb. Rev. Stat. § 30-3862)

Powers of the AG

Uniform Prudent Management of Institutional Funds Act

– Neb. Rev. Stat. §§ 58-610 to 58-619

What is an institutional fund?

– (5) Institutional fund means a fund held by an institution exclusively for charitable purposes. The term does not include:

– (A) program-related assets;

– (B) a fund held for an institution by a trustee that is not an institution; or

– (C) a fund in which a beneficiary that is not an institution has an interest, other than an interest that could arise upon violation or failure of the purposes of the fund.

UPMIFA

Generally, institutional funds are endowment funds

– Endowment fund means an institutional fund or part thereof that, under the terms of a gift instrument, is not wholly expendable by the institution on a current basis. The term does not include assets that an institution designates as an endowment fund for its own use.

These types of funds are similar to trust funds, and face similar restrictions on their use and governance

UPMIFA

12

Neb. Rev. Stat. § 58-612 - Standard of conduct in managing and investing an institutional fund

– “Manage and invest the fund in good faith and with the care an ordinarily prudent person in a like position would exercise under similar circumstances”

– general economic conditions; the possible effect of inflation or deflation; the expected tax consequences, if any, of investment decisions or strategies; the role that each investment or course of action plays within the overall investment portfolio of the fund; the expected total return from income and the appreciation of investments; other resources of the institution; the needs of the institution and the fund to make distributions and to preserve capital; and an asset's special relationship or special value, if any, to the charitable purposes of the institution.

UPMIFA

Neb. Rev. Stat. § 58-615

– Release or modification of restrictions on management, investment, or purpose

– “unlawful, impracticable, impossible to achieve, or wasteful”

– The Attorney General MUST be notified

UPMIFA

#9 Convert from Nonprofit to For-Profit

Assets committed to nonprofit causes must remain so

• Generally, cannot convert from nonprofit to for-profit; Neb. Rev.Stat. §21-19,118

Must notify the Attorney General of fundamental changes20 days in advance

• Dissolution

When dissolving all assets must go to other nonprofits

• Merger

• Sale or transfer of “substantially all” assets

13

#10 Ignore the Attorney General’s Office

Need I say more?

(also applies to the IRS and Nebraska Secretary of State)

Daniel J. RussellAssistant Attorney General

Consumer Protection Division

2115 State Capitol

Lincoln, NE 68509

402-471-1279

402-471-4725 (fax)

Contact Information

Nebraska Attorney GeneralConsumer Protection and Anti-Trust Division

Phone: (402) 471-2682(800) 727-6432

Senior Hotline: (888) 287-0778

En Español: (402) 471-3891(888) 850-7555

protectthegoodlife.nebraska.gov

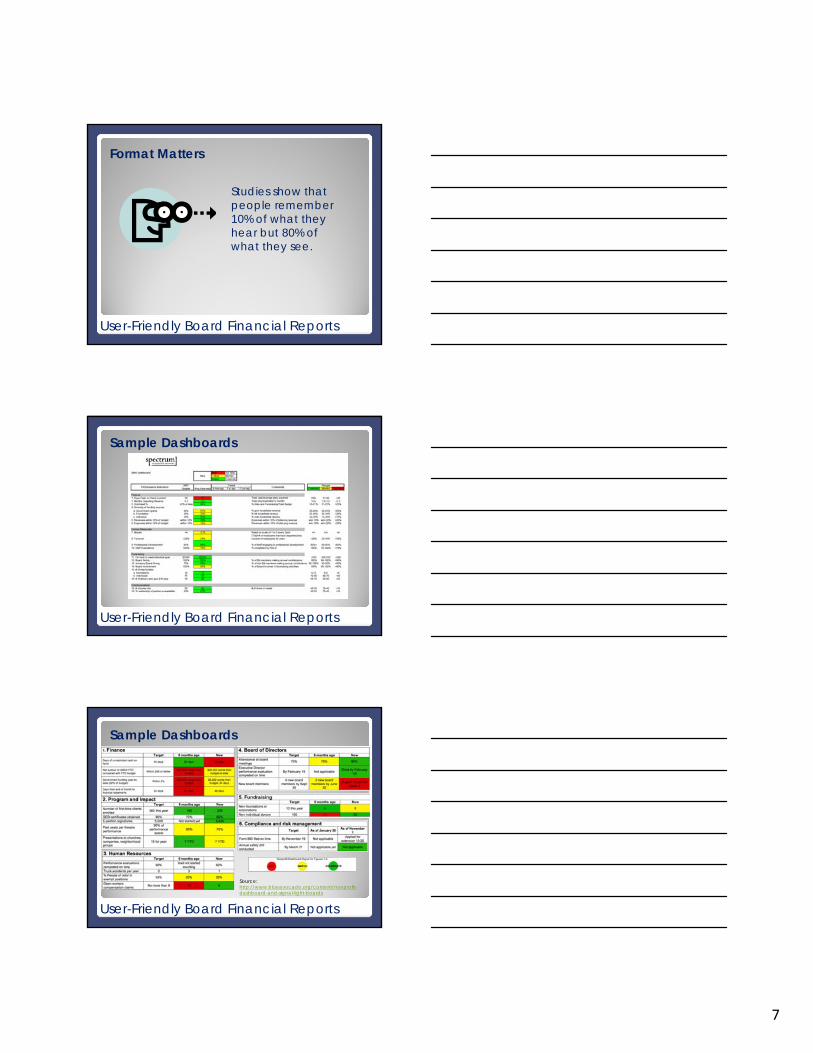

What Board Members Need to Know About Nonprofit Finance

& Accounting Krystal L. Siebrandt

HBE, LLP

November 8, 2017 Scott Conference Center, Omaha, NE

1

What Board Members Need to Know about Not-for-Profit

Finance & Accounting

November 8, 2017

What Board Members Need to Know About Not-for-Profit Finance & AccountingKrystal Siebrandt, CPA, CFE, CGMA, Partner

Agenda

• The Big Picture

• Understanding Financial Statements

• User-Friendly Board Financial Reports

• IRS Requirements

What is a nonprofit organization’s most

important asset?

2

The Big Picture

Board Members: What is your responsibility from a financial perspective?

• Set financial goals to achieve the organization’s vision and mission and monitor progress thereof.

• Financial Goals = Budget

• Monitor Progress = Read the Financial Statements

• Safeguard the organization’s assets.

Understanding Financial Statements

Statement of Financial Position

• What board members should know:

• This Statement summarizes the organization’s assets and liabilities at a point in time, similar to a for-profit Balance Sheet

• Three classes of net assets:

• Unrestricted – No donor imposed restrictions; could include board designations

• Temporarily Restricted – Purpose restrictions or time restrictions (pledges) stipulated by a donor

• Permanently Restricted – Amount is maintained in perpetuity with income being unrestricted or to be used for a specific purpose based on donor stipulations

• What board members should look for:

• Trends

• Liquidity

• Debt

• Unrestricted net assets

3

Understanding Financial Statements

2015 2014CURRENT ASSETS

Cash and cash equivalents 2,182,527$ 1,891,623$ Certificates of deposit 807,799 803,770 Accounts receivable, less allowance for doubtful

accounts of $6,241 (2015) and $11,341 (2014) 18,432 16,915 Grants receivable 634,791 620,018 Promises to give 82,500 182,500 Prepaid expenses 4,145 24,509

Total current assets 3,730,194 3,539,335

PROPERTY AND EQUIPMENT, net 796,845 869,583

Total assets 4,527,039$ 4,408,918$

CURRENT LIABILITIESAccounts payable 421,539$ 455,377$ Accrued expenses 365,393 418,442 Unearned grant revenue 185,623 195,123

Total current liabilities 972,555 1,068,942

NET ASSETS Unrestricted 3,471,984 3,157,476 Temporarily restricted 82,500 182,500

Total net assets 3,554,484 3,339,976

Total liabilities and net assets 4,527,039$ 4,408,918$

ABC ORGANIZATIONSTATEMENTS OF FINANCIAL POSITION

December 31,

ASSETS

LIABILITIES AND NET ASSETS

Understanding Financial Statements

Statement of Activities

• What board members should know:

• This Statement shows the results of operations for a period of time, similar to a for-profit Income Statement or Profit & Loss

• Non-profit revenue can include contributions, grants, program service fees, investment income, and in-kind donations

• Statements prepared on the accrual basis, will show contributions when pledged

• What board members should look for:

• Budget vs. Actual

• Dependency on major donor or funding source

• Trends

• Change in net assets

Understanding Financial Statements

2015 2014CHANGES IN NET ASSETS

Revenue and other supportGovernment grants 7,138,114$ 7,393,517$ Other agency grants 527,820 584,313 Contributions 171,873 180,036 Program fees 3,503,229 3,504,345 Interest income 6,332 5,117 Miscellaneous 4,734 10,617

Total revenue and other support 11,352,102 11,677,945

ExpensesSalaries 5,370,855 5,302,523 Pass through grants 5,572,385 5,853,237 Insurance 110,382 106,050 Supplies 40,631 52,112 Printing 15,440 12,645 Depreciation 27,901 33,529

Total expenses 11,137,594 11,360,096

INCREASE IN NET ASSETS 214,508 317,849

Net assets, beginning of year 3,339,976 3,022,127

Net assets, end of year 3,554,484$ 3,339,976$

ABC ORGANIZATIONSTATEMENTS OF ACTIVITIES

Years ended December 31,

4

Understanding Financial Statements

Statement of Cash Flows

• What board members should know: