duval charter school at westside - flauditor.gov rpts... · duval charter school at westside a...

TRANSCRIPT

Duval Charter School at WestsideA Department of Renaissance Charter School, Inc.(A Component Unit of the DuvalCounty School Board, Florida)

Basic Financial StatementsFor the Year Ended June 30, 2016

Duval Charter School at Westside

Table of Contents

Independent Auditor’s Report 1 2

Management's Discussion and Analysis (Not Covered byIndependent Auditor’s Report) 3 6

Basic Financial Statements

Government wide Financial Statements:

Statement of Net Position (Deficit) 7

Statement of Activities 8

Fund Financial Statements:

Balance Sheet Governmental Funds 9

Reconciliation of the Balance Sheet of the GovernmentalFunds to the Statement of Net Position (Deficit) 10

Statement of Revenues, Expenditures, and Change inFund Balances Governmental Funds 11

Reconciliation of the Statement of Revenues, Expenditures,and Change in Fund Balances of the GovernmentalFunds to the Statement of Activities 12

Statement of Revenues and ExpendituresBudget and Actual General Fund 13

Statement of Revenues and ExpendituresBudget and Actual Special Revenue Fund 14

Statement of Assets and Liabilities Agency Fund 15

Notes to Basic Financial Statements 16 23

Other Independent Auditor’s Reports

Report on Internal Control over Financial Reporting and on Compliance andOther Matters Based on an Audit of Financial Statements Performed inAccordance with Government Auditing Standards 24 25

Independent Auditor’s Report to the Board of Directors 26 27

KMCcpa.com | 6550 N Federal Hwy, 4th Floor Fort Lauderdale, FL 33308 Phone: 954.771.0896 Fax: 954.938.9353

1

INDEPENDENT AUDITOR’S REPORT

To the Board of DirectorsDuval Charter School at WestsideA Department of Renaissance Charter School, Inc.Jacksonville, Florida

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each majorfund, and the aggregate remaining fund information of Duval Charter School at Westside (the“School”), a Department of Renaissance Charter School, Inc. and a component unit of the Duval CountySchool Board, Florida, as of and for the year ended June 30, 2016, and the related notes to the financialstatements, which collectively comprise the School’s basic financial statements as listed in the table ofcontents.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements inaccordance with accounting principles generally accepted in the United States of America; this includesthe design, implementation, and maintenance of internal control relevant to the preparation and fairpresentation of financial statements that are free from material misstatement, whether due to fraudor error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. Weconducted our audit in accordance with auditing standards generally accepted in the United States ofAmerica and the standards applicable to financial audits contained in Government Auditing Standards,issued by the Comptroller General of the United States. Those standards require that we plan andperform the audit to obtain reasonable assurance about whether the financial statements are freefrom material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosuresin the financial statements. The procedures selected depend on the auditor's judgment, including theassessment of the risks of material misstatement of the financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to the entity'spreparation and fair presentation of the financial statements in order to design audit procedures thatare appropriate in the circumstances, but not for the purpose of expressing an opinion on theeffectiveness of the entity's internal control. Accordingly, we express no such opinion. An audit alsoincludes evaluating the appropriateness of accounting policies used and the reasonableness ofsignificant accounting estimates made by management, as well as evaluating the overall presentationof the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basisfor our audit opinions.

2

Duval Charter School at Westside

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, each major fund, and the aggregateremaining fund information of the School, as of June 30, 2016, and the respective changes in financialposition, and respective budgetary comparison for the General Fund and Special Revenue Fund for theyear then ended in accordance with accounting principles generally accepted in the United States ofAmerica.

Emphasis of Matter

As discussed in Note 1, the financial statements of the School are intended to present the financialposition and change in financial position of only that portion of the governmental activities, each majorfund and the aggregate remaining fund information of Renaissance Charter School, Inc. that isattributable to the transactions of the School. They do not purport to, and do not, present fairly thefinancial position of Renaissance Charter School, Inc. as of June 30, 2016 and the changes in itsfinancial position or budgetary comparisons, where applicable, for the year ended, in conformity withaccounting principles generally accepted in the United States of America. Our opinion is not modifiedwith respect to this matter.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that themanagement's discussion and analysis on pages 3 through 6 be presented to supplement the basicfinancial statements. Such information, although not a part of the basic financial statements, isrequired by the Governmental Accounting Standards Board, who considers it to be an essential part offinancial reporting for placing the basic financial statements in an appropriate operational, economic,or historical context. We have applied certain limited procedures to the required supplementaryinformation in accordance with auditing standards generally accepted in the United States of America,which consisted of inquiries of management about the methods of preparing the information andcomparing the information for consistency with management's responses to our inquiries, the basicfinancial statements, and other knowledge we obtained during our audit of the basic financialstatements. We do not express an opinion or provide any assurance on the information because thelimited procedures do not provide us with sufficient evidence to express an opinion or provide anyassurance.

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated September15, 2016, on our consideration of the School’s internal control over financial reporting and on our testsof its compliance with certain provisions of laws, regulations, contracts, and grant agreements andother matters. The purpose of that report is to describe the scope of our testing of internal controlover financial reporting and compliance and the results of that testing, and not to provide an opinionon internal control over financial reporting or on compliance. That report is an integral part of an auditperformed in accordance with Government Auditing Standards in considering the School’s internalcontrol over financial reporting and compliance.

KEEFE McCULLOUGH

Fort Lauderdale, FloridaSeptember 15, 2016

MANAGEMENT’S DISCUSSIONAND ANALYSIS

3

Duval Charter School at WestsideManagement’s Discussion and AnalysisJune 30, 2016

As management of Duval Charter School at Westside (the “School”), a Department of RenaissanceCharter School, Inc. and a component unit of the Duval County School Board, Florida (the “SchoolBoard”), we offer readers of the School’s basic financial statements this narrative overview andanalysis of the financial activities of the School for the year ended June 30, 2016 and 2015.

Management’s discussion and analysis is included at the beginning of the School’s basic financialstatements to provide, in layman’s terms, the current position of the School’s financial condition.This summary should not be taken as a replacement for the audit, which consists of the basicfinancial statements.

Financial Highlights

Our basic financial statements provide these insights into the results of this year’s operations.

• As of June 30, 2016, the School’s fund balance was $ 298,296 as compared to$ 161,600 at June 30, 2015.

• As of June 30, 2016, the School had net position (deficit) of $ (1,312,767), ascompared to $ (1,087,802) at June 30, 2015.

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to the School’s basic financialstatements. The School’s basic financial statements are comprised of three components:1) government wide basic financial statements, 2) fund basic financial statements, and 3) notes tothe basic financial statements.

Government Wide Financial Statements: The government wide financial statements are designedto provide readers with a broad overview of the School’s finances, in a manner similar to a privatesector business.

The statement of net position presents information on all of the School’s assets, liabilities, anddeferred inflows/outflows of resources, with the difference between the two reported as netposition. Over time, increases or decreases in net position may serve as a useful indicator ofwhether the financial position of the School is improving or deteriorating.

The statement of activities presents information showing how the School’s net position changedduring the year. All changes in net position are reported as soon as the underlying event giving riseto the change occurs, regardless of the timing of related cash flows. Thus, revenues and expensesare reported in this Statement for some items that will only result in cash flows in future fiscalperiods (e.g. uncollected revenues and services rendered but unpaid).

The government wide financial statements include all governmental activities that are principallysupported by grants and entitlements from the state for full time equivalent funding. The Schooldoes not have any business type activities. The governmental activities of the School primarilyinclude instruction and instructional support services.

The government wide basic financial statements can be found on pages 7 and 8 of this report.

4

Duval Charter School at WestsideManagement’s Discussion and AnalysisJune 30, 2016

Fund Financial Statements: A fund is a grouping of related accounts that is used to maintaincontrol over resources that have been segregated for specific activities or objectives. The School,like other state and local governments, uses fund accounting to ensure and demonstratecompliance with finance related legal requirements.

Governmental Funds: Governmental funds are used to account for essentially the same functionsreported as governmental activities in the government wide financial statements. However, unlikethe government wide basic financial statements, governmental fund basic financial statementsfocus on near term inflows and outflows of spendable resources, as well as balances of spendableresources available at the end of the fiscal year. Such information may be useful in evaluating theSchool’s near term financing requirements.

Because the focus of governmental funds is narrower than that of the government wide financialstatements, it is useful to compare the information presented for governmental funds with similarinformation presented for governmental activities in the government wide financial statements.By doing so, readers may better understand the long term impact of the School’s near termfinancing decisions. Both the governmental fund balance sheet and the governmental fundstatement of revenues, expenditures and change in fund balances provide a reconciliation tofacilitate this comparison between governmental funds and governmental activities.

The School maintains two individual governmental funds. Information is presented in thegovernmental fund balance sheet and the governmental fund statement of revenues, expendituresand change in fund balances. The General Fund and Special Revenue Fund are considered to be theSchool’s major funds.

The School adopts an annual budget for its governmental funds. A budgetary comparisonstatement has been provided for the General Fund and Special Revenue Fund to demonstratecompliance with the budget.

The governmental fund financial statements can be found on pages 9 through 14 of this report.

Agency Fund: In addition, the School has one agency fund which is a student activity fund. Thisfund is formed for educational and school purposes.

The Agency Fund financial statement can be found on page 15 of this report. The assets andliabilities of this Fund are not included in the government wide statement of net position.

Notes to Basic Financial Statements: The notes provide additional information that is essential fora full understanding of the data provided in the government wide and fund financial statements.The notes to basic financial statements can be found on pages 16 through 23 of this report.

Government Wide Financial Analysis

This is the School’s third year of operations; therefore, comparative government wide data ispresented. The School’s net position (deficit) was $ (1,312,767) at June 30, 2016. This amountrepresents net investment in capital assets (deficit) of $ (1,597,565) and unrestricted of $ 284,798.The School’s net position (deficit) was $ (1,087,802) at June 30, 2015, which represented netinvestment in capital assets (deficit) $ (1,240,471) and unrestricted of $ 152,669.

5

Duval Charter School at WestsideManagement’s Discussion and AnalysisJune 30, 2016

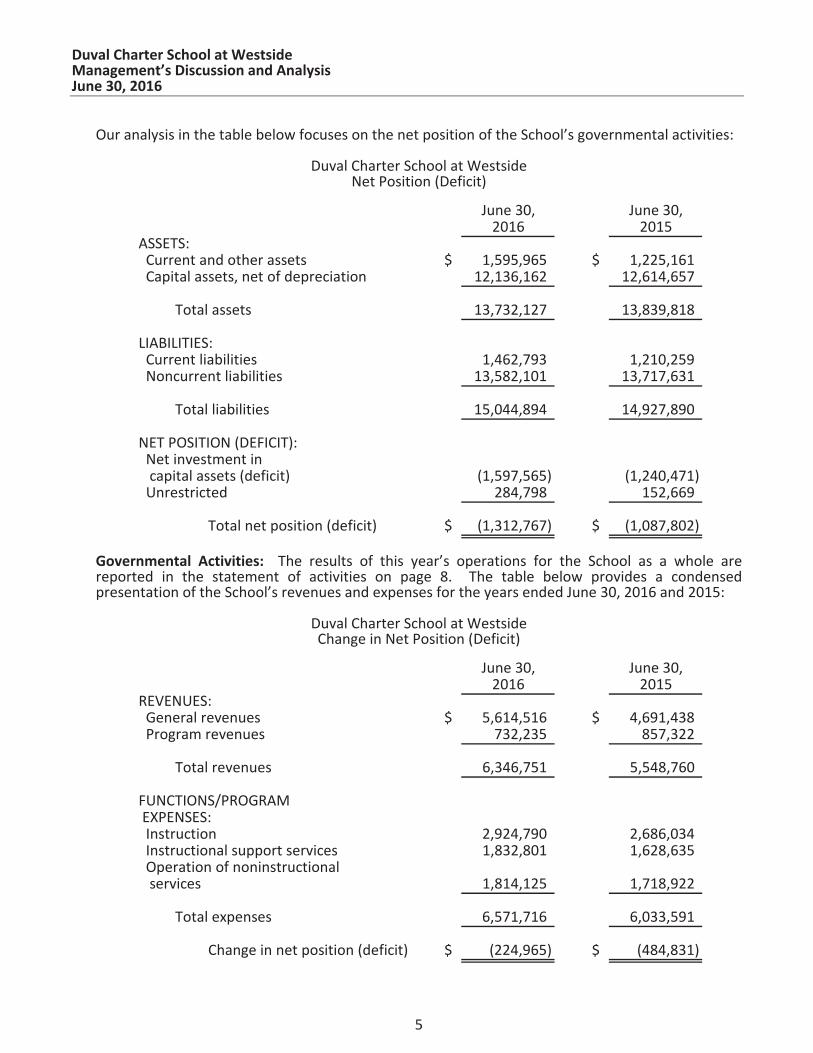

Our analysis in the table below focuses on the net position of the School’s governmental activities:

Duval Charter School at WestsideNet Position (Deficit)

June 30, June 30,2016 2015

ASSETS:Current and other assets $ 1,595,965 $ 1,225,161Capital assets, net of depreciation 12,136,162 12,614,657

Total assets 13,732,127 13,839,818

LIABILITIES:Current liabilities 1,462,793 1,210,259Noncurrent liabilities 13,582,101 13,717,631

Total liabilities 15,044,894 14,927,890

NET POSITION (DEFICIT):Net investment incapital assets (deficit) (1,597,565) (1,240,471)Unrestricted 284,798 152,669

Total net position (deficit) $ (1,312,767) $ (1,087,802)

Governmental Activities: The results of this year’s operations for the School as a whole arereported in the statement of activities on page 8. The table below provides a condensedpresentation of the School’s revenues and expenses for the years ended June 30, 2016 and 2015:

Duval Charter School at WestsideChange in Net Position (Deficit)

June 30, June 30,2016 2015

REVENUES:General revenues $ 5,614,516 $ 4,691,438Program revenues 732,235 857,322

Total revenues 6,346,751 5,548,760

FUNCTIONS/PROGRAMEXPENSES:Instruction 2,924,790 2,686,034Instructional support services 1,832,801 1,628,635Operation of noninstructionalservices 1,814,125 1,718,922

Total expenses 6,571,716 6,033,591

Change in net position (deficit) $ (224,965) $ (484,831)

6

Duval Charter School at WestsideManagement’s Discussion and AnalysisJune 30, 2016

Governmental Fund Expenditures

In the table below, we have presented the cost of the largest functions/programs as a percentageof total governmental expenditures:

Expenditures Percent Expenditures Percent

Governmental expenditures:Instructional expenditures $ 2,560,175 41.2% $ 2,396,975 40.8%Debt service 1,425,763 23.0% 1,364,004 23.2%Plant operations and maintenance 924,685 14.9% 860,460 14.6%Administrative services 352,779 5.7% 272,280 4.6%Food services 284,002 4.6% 270,647 4.6%Capital outlay 157,585 2.5% 363,221 6.2%All other functions/programs 505,066 8.1% 350,536 6.0%

Total governmentalexpenditures $ 6,210,055 100.0% $ 5,878,123 100.0%

2016 2015Functions/Programs

Capital Assets and Debt Administration

Capital assets: At June 30, 2016, the School had capital assets of $ 12,136,162, net of accumulateddepreciation, invested in buildings, computer equipment and furniture, fixtures and equipment ascompared to $ 12,614,657 at June 30, 2015.

Debt: At June 30, 2016, the School had outstanding debt of $ 13,733,727 as compared to$ 13,855,128 at June 30, 2015. Additional information on the School’s debt can be found in Notes8 and 9 on page 22.

General Fund Budgetary Highlights

Revenues were unfavorable to the budget mainly due to a shortfall in enrollment. Expenditureswere favorable to the budget as the School was able to decrease salaries for instructional staffpositions which were enrollment driven. Overall, the School ended the year with a change in fundbalance which was favorable to the budget by approximately $ 389,700.

Economic Factors and Next Year’s Budget

The State of Florida has increased its Florida Education Finance Program funding for the next yearby approximately 1%. This brings the per student funding to $ 7,178.49. In addition, the CharterSchool Capital Outlay pool, which includes all charter schools, was increased to $ 75,000,000.

Expenditures are budgeted in proportion to enrollment as well as strategic objectives at the School.

Requests for Information

If you have questions about this report or need additional information, please contact HillaryDaigle, Vice President of Finance; Charter Schools USA; 800 Corporate Drive, Suite 700; FortLauderdale, Florida 33334.

BASICFINANCIAL STATEMENTS

The accompanying notes to basic financial statements are an integral part of these statements.

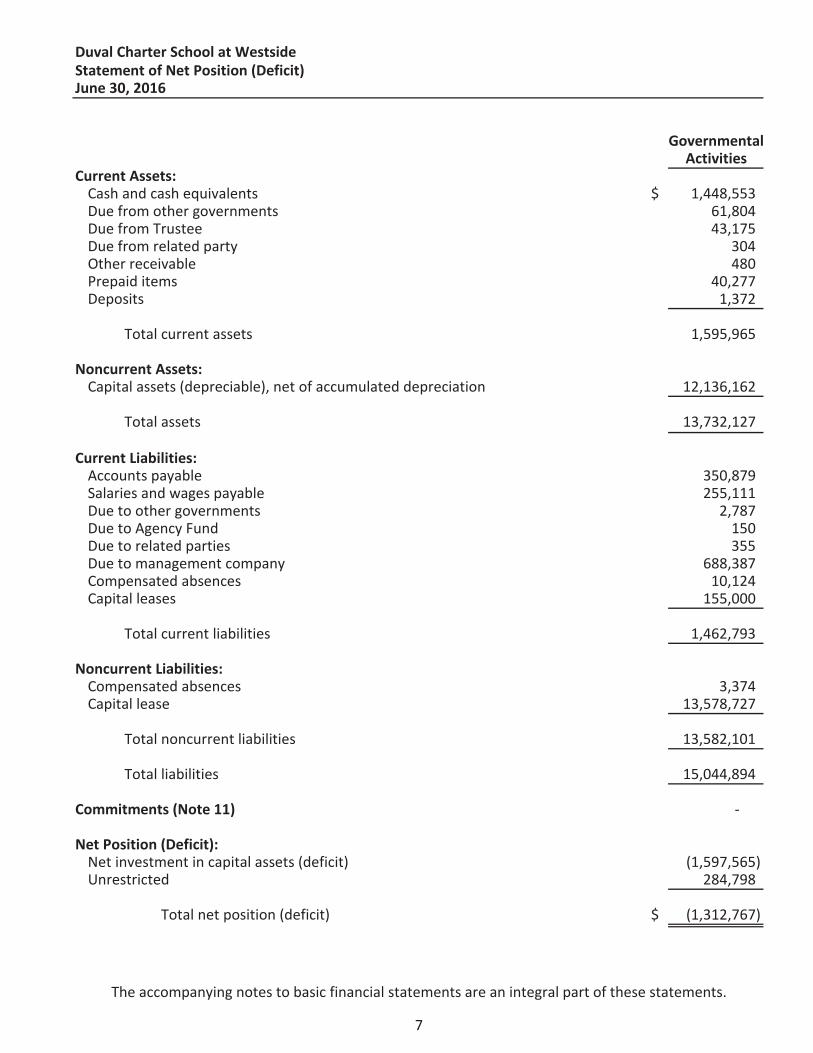

7

GovernmentalActivities

Current Assets:Cash and cash equivalents $ 1,448,553Due from other governments 61,804Due from Trustee 43,175Due from related party 304Other receivable 480Prepaid items 40,277Deposits 1,372

Total current assets 1,595,965

Noncurrent Assets:Capital assets (depreciable), net of accumulated depreciation 12,136,162

Total assets 13,732,127

Current Liabilities:Accounts payable 350,879Salaries and wages payable 255,111Due to other governments 2,787Due to Agency Fund 150Due to related parties 355Due to management company 688,387Compensated absences 10,124Capital leases 155,000

Total current liabilities 1,462,793

Noncurrent Liabilities:Compensated absences 3,374Capital lease 13,578,727

Total noncurrent liabilities 13,582,101

Total liabilities 15,044,894

Commitments (Note 11)

Net Position (Deficit):Net investment in capital assets (deficit) (1,597,565)Unrestricted 284,798

Total net position (deficit) $ (1,312,767)

Duval Charter School at WestsideStatement of Net Position (Deficit)June 30, 2016

The accompanying notes to basic financial statements are an integral part of these statements.

8

GovernmentalActivities

Net RevenueCharges Operating Capital (Expense) andfor Grants and Grants and Change in

Expenses Services Contributions Contributions Net Position

Functions/Programs:Instruction $ 2,924,790 $ $ 76,503 $ $ (2,848,287)Pupil personnel services 150,508 (150,508)Instructional and curriculumdevelopment services 2,576 (2,576)Instructional staff trainingservices 30,001 30,001Instruction related technology 96,220 (96,220)School Board 39,958 (39,958)School administration 352,779 (352,779)Fiscal services 9,433 (9,433)Food services 284,002 25,623 270,541 12,162Central services 87,405 (87,405)Operation of plant 992,683 80,400 (912,283)Maintenance of plant 208,034 (208,034)Community services 88,965 111,149 12,407 34,591Interest on long term debt 1,304,362 125,611 (1,178,751)

Total governmentalactivities $ 6,571,716 $ 136,772 $ 469,852 $ 125,611 (5,839,481)

General revenues:Grants and entitlements 5,555,027Miscellaneous 59,489

Total general revenues 5,614,516

Change in net position (deficit) (224,965)

Net position (deficit), July 1, 2015 (1,087,802)

Net position (deficit), June 30, 2016 $ (1,312,767)

Program Revenues

Statement of ActivitiesFor the Year Ended June 30, 2016

Duval Charter School at Westside

The accompanying notes to basic financial statements are an integral part of these statements.

9

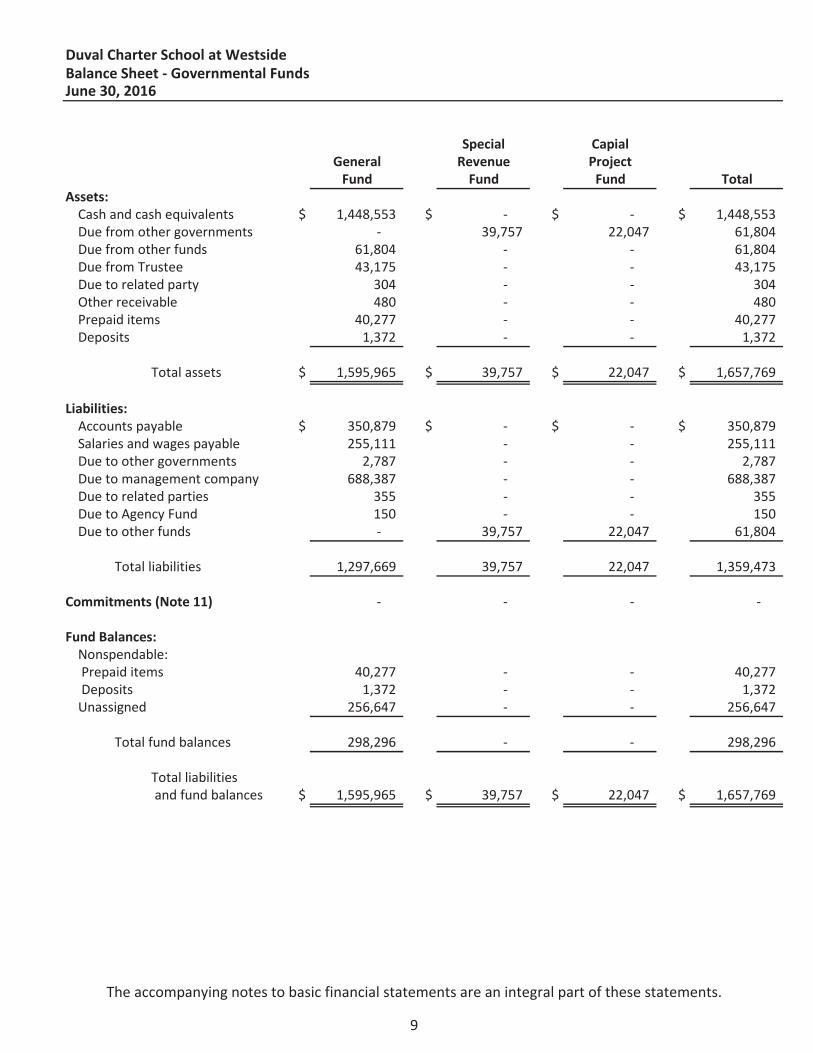

Special CapialGeneral Revenue ProjectFund Fund Fund Total

Assets:Cash and cash equivalents $ 1,448,553 $ $ $ 1,448,553Due from other governments 39,757 22,047 61,804Due from other funds 61,804 61,804Due from Trustee 43,175 43,175Due to related party 304 304Other receivable 480 480Prepaid items 40,277 40,277Deposits 1,372 1,372

Total assets $ 1,595,965 $ 39,757 $ 22,047 $ 1,657,769

Liabilities:Accounts payable $ 350,879 $ $ $ 350,879Salaries and wages payable 255,111 255,111Due to other governments 2,787 2,787Due to management company 688,387 688,387Due to related parties 355 355Due to Agency Fund 150 150Due to other funds 39,757 22,047 61,804

Total liabilities 1,297,669 39,757 22,047 1,359,473

Commitments (Note 11)

Fund Balances:Nonspendable:Prepaid items 40,277 40,277Deposits 1,372 1,372Unassigned 256,647 256,647

Total fund balances 298,296 298,296

Total liabilitiesand fund balances $ 1,595,965 $ 39,757 $ 22,047 $ 1,657,769

Duval Charter School at WestsideBalance Sheet Governmental FundsJune 30, 2016

The accompanying notes to basic financial statements are an integral part of these statements.

10

Total Fund Balances Governmental Funds, Page 9 $ 298,296

Amounts reported for governmental activities in the statementof net position (deficit) are different because:

The cost of capital assets acquired is reported as anexpenditure in the governmental funds. The statementof net position (deficit) includes those capital assets, net ofaccumulated depreciation, among the assets of theSchool as a whole.

Cost of capital assets $ 13,704,253Accumulated depreciation (1,568,091) 12,136,162

Liabilities not payable with current available resourcesare not reported as fund liabilities in the governmentalfund statements. All liabilities both current andlong term, are reported in the government widestatements.

Compensated absences (13,498)Capital leases payable (13,733,727) (13,747,225)

Net Position (Deficit) of Governmental Activities, Page 7 $ (1,312,767)

Duval Charter School at WestsideReconciliation of the Balance Sheet of the Governmental Fundsto the Statement of Net Position (Deficit)June 30, 2016

The accompanying notes to basic financial statements are an integral part of these statements.

11

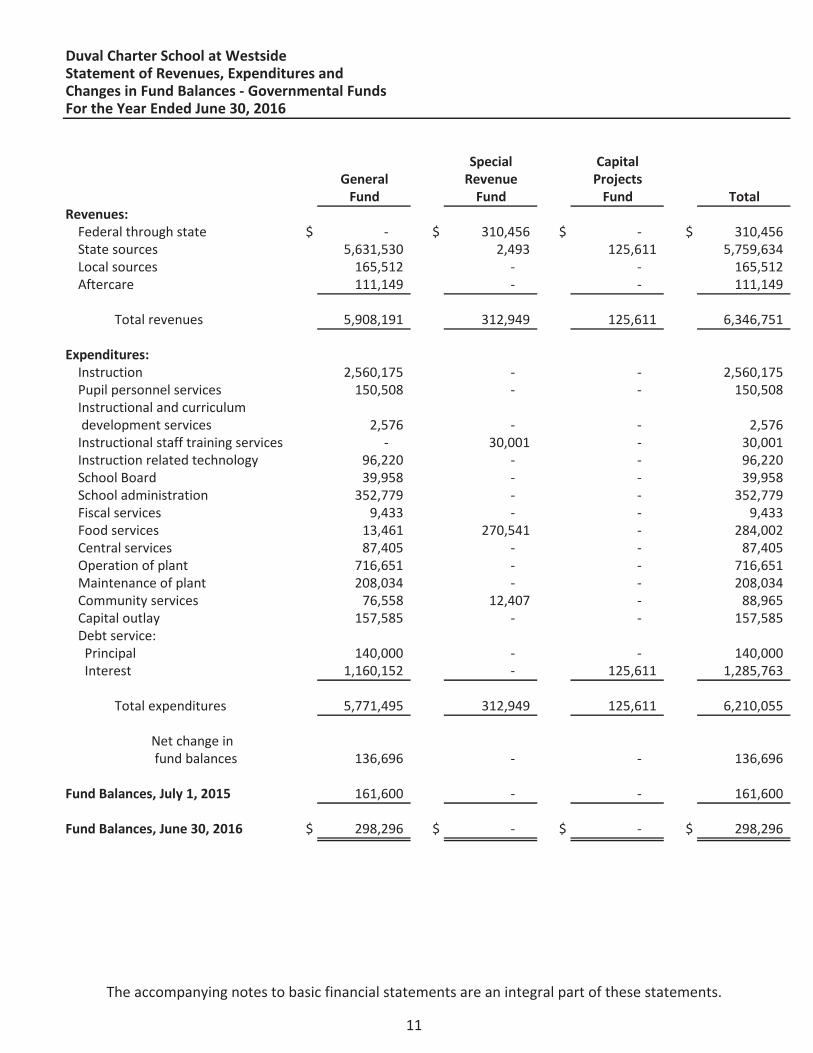

Special CapitalGeneral Revenue ProjectsFund Fund Fund Total

Revenues:Federal through state $ $ 310,456 $ $ 310,456State sources 5,631,530 2,493 125,611 5,759,634Local sources 165,512 165,512Aftercare 111,149 111,149

Total revenues 5,908,191 312,949 125,611 6,346,751

Expenditures:Instruction 2,560,175 2,560,175Pupil personnel services 150,508 150,508Instructional and curriculumdevelopment services 2,576 2,576Instructional staff training services 30,001 30,001Instruction related technology 96,220 96,220School Board 39,958 39,958School administration 352,779 352,779Fiscal services 9,433 9,433Food services 13,461 270,541 284,002Central services 87,405 87,405Operation of plant 716,651 716,651Maintenance of plant 208,034 208,034Community services 76,558 12,407 88,965Capital outlay 157,585 157,585Debt service:Principal 140,000 140,000Interest 1,160,152 125,611 1,285,763

Total expenditures 5,771,495 312,949 125,611 6,210,055

Net change infund balances 136,696 136,696

Fund Balances, July 1, 2015 161,600 161,600

Fund Balances, June 30, 2016 $ 298,296 $ $ $ 298,296

Duval Charter School at WestsideStatement of Revenues, Expenditures andChanges in Fund Balances Governmental FundsFor the Year Ended June 30, 2016

The accompanying notes to basic financial statements are an integral part of these statements.

12

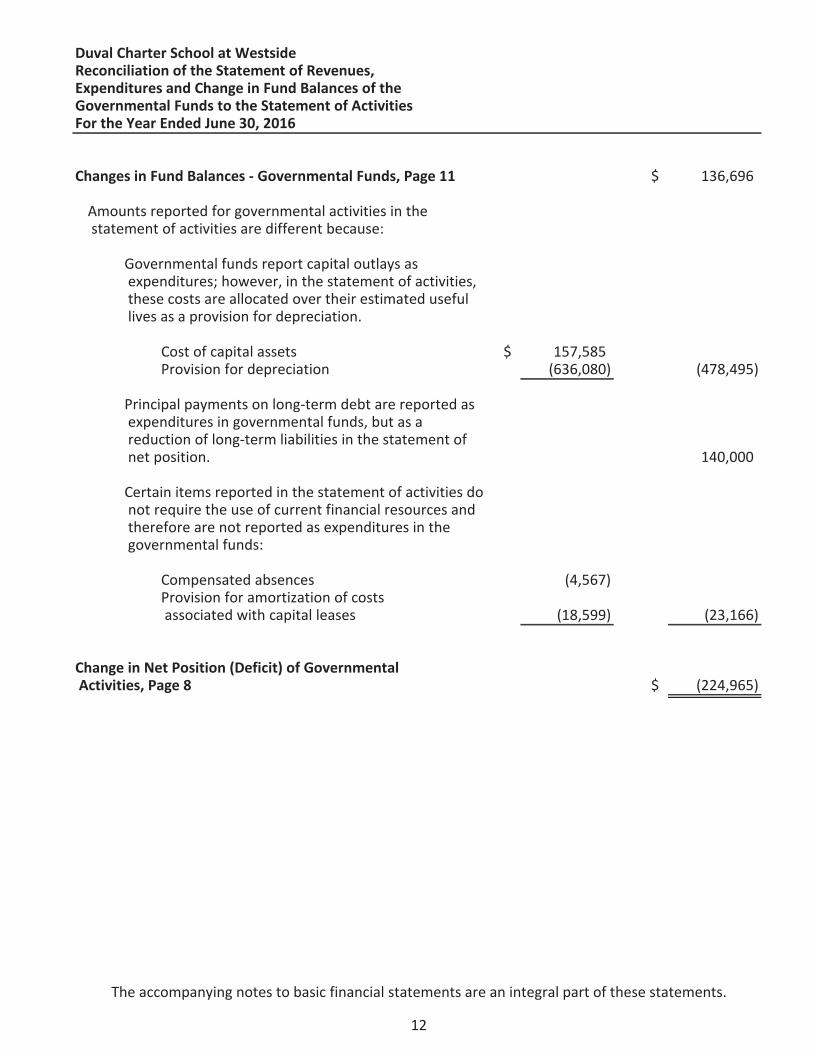

Changes in Fund Balances Governmental Funds, Page 11 $ 136,696

Amounts reported for governmental activities in thestatement of activities are different because:

Governmental funds report capital outlays asexpenditures; however, in the statement of activities,these costs are allocated over their estimated usefullives as a provision for depreciation.

Cost of capital assets $ 157,585Provision for depreciation (636,080) (478,495)

Principal payments on long term debt are reported asexpenditures in governmental funds, but as areduction of long term liabilities in the statement ofnet position. 140,000

Certain items reported in the statement of activities donot require the use of current financial resources andtherefore are not reported as expenditures in thegovernmental funds:

Compensated absences (4,567)Provision for amortization of costsassociated with capital leases (18,599) (23,166)

Change in Net Position (Deficit) of GovernmentalActivities, Page 8 $ (224,965)

For the Year Ended June 30, 2016

Duval Charter School at WestsideReconciliation of the Statement of Revenues,

Governmental Funds to the Statement of ActivitiesExpenditures and Change in Fund Balances of the

The accompanying notes to basic financial statements are an integral part of these statements.

13

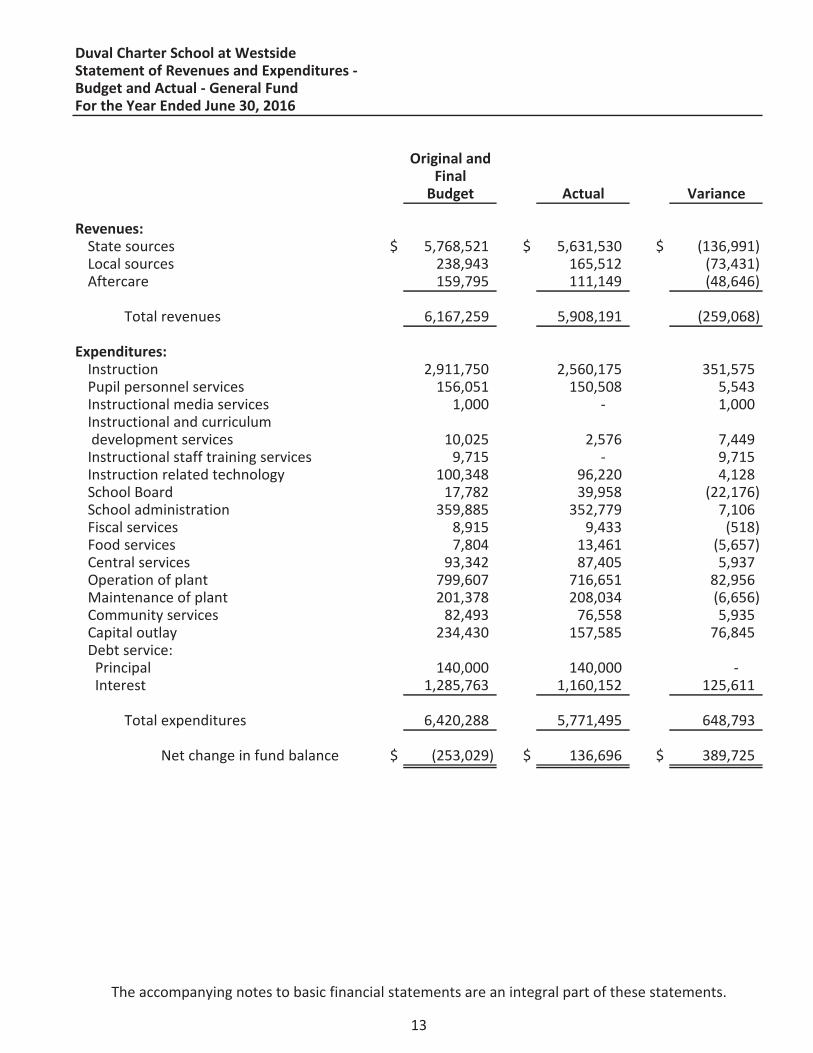

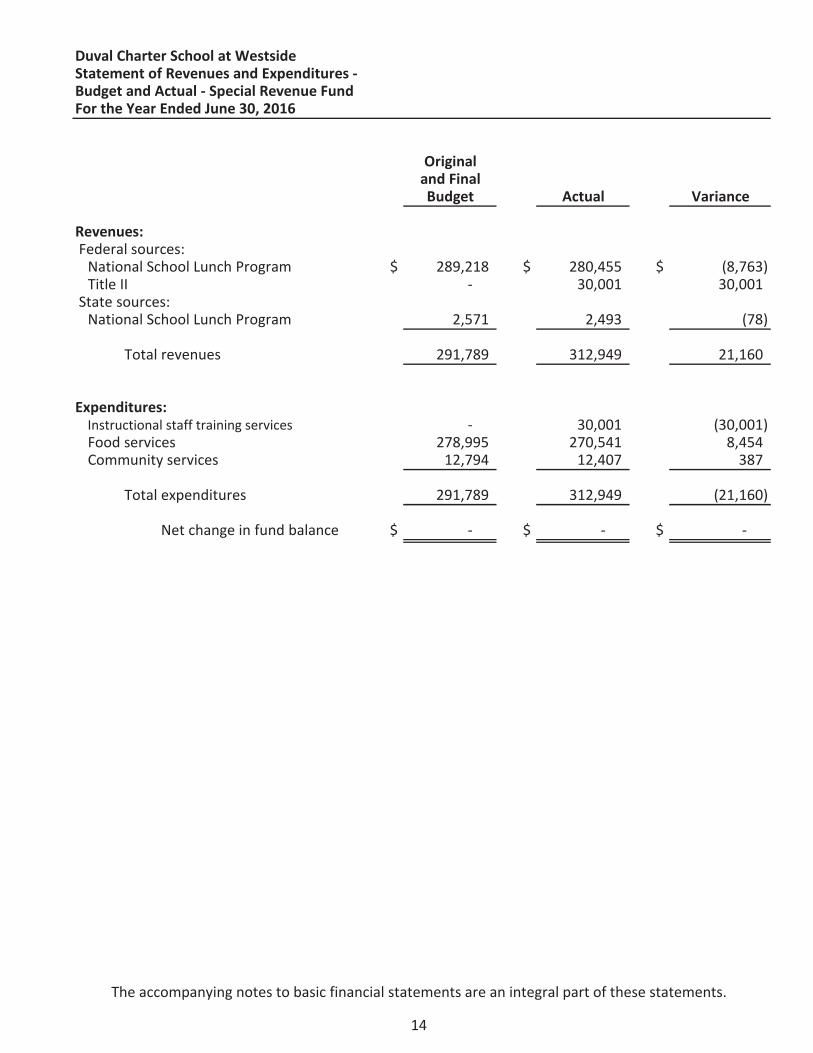

Original andFinalBudget Actual Variance

Revenues:State sources $ 5,768,521 $ 5,631,530 $ (136,991)Local sources 238,943 165,512 (73,431)Aftercare 159,795 111,149 (48,646)

Total revenues 6,167,259 5,908,191 (259,068)

Expenditures:Instruction 2,911,750 2,560,175 351,575Pupil personnel services 156,051 150,508 5,543Instructional media services 1,000 1,000Instructional and curriculumdevelopment services 10,025 2,576 7,449Instructional staff training services 9,715 9,715Instruction related technology 100,348 96,220 4,128School Board 17,782 39,958 (22,176)School administration 359,885 352,779 7,106Fiscal services 8,915 9,433 (518)Food services 7,804 13,461 (5,657)Central services 93,342 87,405 5,937Operation of plant 799,607 716,651 82,956Maintenance of plant 201,378 208,034 (6,656)Community services 82,493 76,558 5,935Capital outlay 234,430 157,585 76,845Debt service:Principal 140,000 140,000Interest 1,285,763 1,160,152 125,611

Total expenditures 6,420,288 5,771,495 648,793

Net change in fund balance $ (253,029) $ 136,696 $ 389,725

Duval Charter School at WestsideStatement of Revenues and ExpendituresBudget and Actual General FundFor the Year Ended June 30, 2016

The accompanying notes to basic financial statements are an integral part of these statements.

14

Originaland FinalBudget Actual Variance

Revenues:Federal sources:National School Lunch Program $ 289,218 $ 280,455 $ (8,763)Title II 30,001 30,001

State sources:National School Lunch Program 2,571 2,493 (78)

Total revenues 291,789 312,949 21,160

Expenditures:Instructional staff training services 30,001 (30,001)Food services 278,995 270,541 8,454Community services 12,794 12,407 387

Total expenditures 291,789 312,949 (21,160)

Net change in fund balance $ $ $

Duval Charter School at WestsideStatement of Revenues and ExpendituresBudget and Actual Special Revenue FundFor the Year Ended June 30, 2016

The accompanying notes to basic financial statements are an integral part of these statements.

15

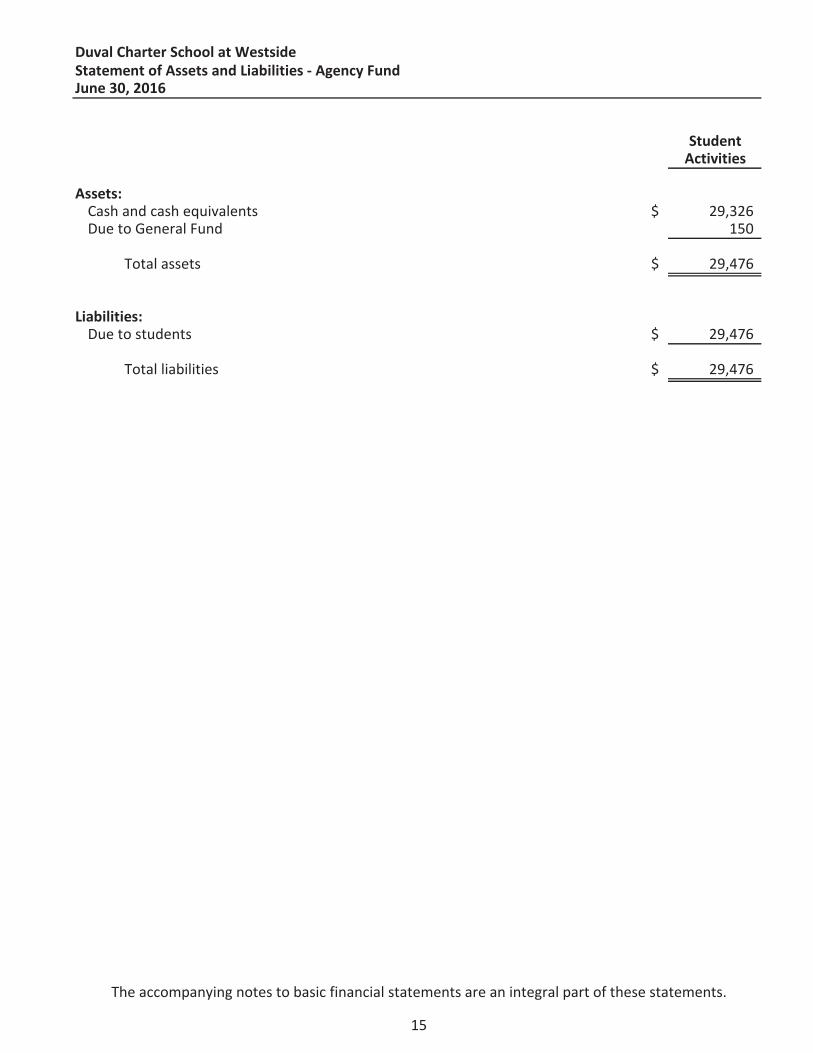

StudentActivities

Assets:Cash and cash equivalents $ 29,326Due to General Fund 150

Total assets $ 29,476

Liabilities:Due to students $ 29,476

Total liabilities $ 29,476

June 30, 2016

Duval Charter School at WestsideStatement of Assets and Liabilities Agency Fund

16

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 1 Organization and Operations

Duval Charter School at Westside (the “School”), a Department of Renaissance Charter School, Inc.and a component unit of the Duval County School Board, Florida, was established in 2013 as apublic charter school to serve students from kindergarten to eighth grade in Duval County.Renaissance Charter School, Inc. is a Florida nonprofit corporation organized in August 1998. Therewere 851 students enrolled for the 2015/2016 school year.

The basic financial statements of the School present only the balances, activity and disclosuresrelated to the School. They do not purport to, and do not, present fairly the financial position ofRenaissance Charter School, Inc. as of June 30, 2016, and the changes in its financial position orbudgetary comparisons, where applicable, for the year then ended in conformity with accountingprinciples generally accepted in the United States of America. Renaissance Charter School Inc.,(Notes 8 and 11) is an entity created to fund the purchase of the facility housing the School’soperations. Accordingly, these basic financial statements only include balances, activity anddisclosures related to the School.

Note 2 Summary of Significant Accounting Policies

Reporting entity: The School operates under a charter granted by the sponsoring Duval CountySchool Board. The current charter is effective until June 30, 2018, and may be renewed inincrements of five years by mutual written agreement between the School and the School Board.At the end of the term of the charter, the School Board may choose not to renew the charter undergrounds specified in the charter in which case the School Board is required to notify the School inwriting at least ninety days prior to the charter's expiration. During the term of the charter, theSchool Board may also terminate the charter if good cause is shown. Duval Charter School atWestside is considered a component unit of the Duval County School Board.

The School may also be financially accountable if an organization is fiscally dependent on theSchool regardless of whether the organization has a separately elected governing board, agoverning board appointed by another government, or a jointly approved board. In addition,component units can be other organizations for which the nature and significance of theirrelationship with the School are such that exclusion would cause the basic financial statements tobe misleading or incomplete.

As a result of evaluating the above criteria, management has determined that no component unitsexist for which the School is financially accountable which would require inclusion in the School'sbasic financial statements.

Basis of presentation: Based on the guidance presented in the American Institute of CertifiedPublic Accountants Audit and Accounting Guide Not for Profit Organizations and provisions ofSection 228.056(9), Florida Statutes, the School is presented as a governmental organization forfinancial statement reporting purposes.

Government wide basic financial statements: The School's basic financial statements include bothgovernment wide (reporting the School as a whole) and fund financial statements (reporting theSchool's major funds). Both the government wide and fund financial statements categorizeprimary activities as either governmental or business type. All of the School's activities areclassified as governmental activities.

17

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 2 Summary of Significant Accounting Policies (continued)

In the government wide statement of net position, the governmental activities column is presentedon a consolidated basis, if applicable, and is reported on a full accrual, economic resource basis,which recognizes all noncurrent assets and receivables as well as all noncurrent debt andobligations.

The government wide statement of activities reports both the gross and net cost of each of theSchool's functions. The net costs, by function, are also supported by general revenues(unrestricted contributions, investment earnings, miscellaneous revenue, etc.). The statement ofactivities reduces gross expenses (including provision for depreciation) by related programrevenues, operating and capital grants and contributions. Program revenues must be directlyassociated with the function. Operating grants include operating specific and discretionary (eitheroperating or capital) grants while the capital grants column reflects capital specific grants. For theyear ended June 30, 2016, the School had program revenues of $ 732,235.

This government wide focus is more on the ability to sustain the School as an entity and the changein the School's net position resulting from the current year's activities.

Fund financial statements: The accounts of the School are organized on the basis of funds. Theoperations of the funds are accounted for with a separate set of self balancing accounts thatcomprise its assets, liabilities, equity, revenues and expenditures.

The school reports the following major governmental funds:

General Fund this fund is used to account for all operating activities of theSchool except for those required to be accounted for in another fund.

Special Revenue Fund This fund is used to account for federal grants andcertain state grants that are legally restricted to expenditures for particularpurposes.

Measurement focus and basis of accounting: Basis of accounting refers to the point at whichrevenues or expenditures/expenses are recognized in the accounts and reported in the financialstatements. It relates to the timing of the measurements made regardless of the measurementfocus applied. Governmental funds use the current financial resources measurement focus and thegovernmental wide statements use the economic resources measurement focus.

Governmental activity in the government wide basic financial statements is presented on the fullaccrual basis of accounting. Revenues are recognized when earned and expenses are recognizedwhen incurred.

The governmental funds basic financial statements are presented on the modified accrual basis ofaccounting under which revenue is recognized in the accounting period in which it becomessusceptible to accrual (i.e., when they become both measurable and available). "Measurable"means the amount of the transaction can be determined and "available" means collectible withinsixty days after year end or soon enough thereafter to be used to pay liabilities of the currentperiod.

Cash and cash equivalents: The School considers all demand accounts and money market fundswhich are not subject to withdrawal restrictions to be cash and cash equivalents.

The School maintains its cash accounts at one financial institution. The School’s accounts at thisinstitution, at times, may exceed the federally insured limit. The School has not experienced anylosses in such accounts and does not believe it is exposed to any significant credit risk (Note 3).

18

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 2 Summary of Significant Accounting Policies (continued)

Prepaid items: Certain payments to vendors reflect costs applicable to future accounting periodsand are recorded as prepaid items.

Due to and due from other funds: Interfund receivables and payables arise from interfundtransactions and are recorded by all funds affected in the period in which transactions areexecuted. The balances result from the time lag between the dates that interfund goods andservices are provided or reimbursable expenditures occur, transactions are recorded in theaccounting system, and payments between funds are made.

Revenue recognition: Student funding is provided by the State of Florida through the SchoolBoard. Such funding is recorded as entitlement revenue in the government wide financialstatements and state source revenue in the fund financial statements. This funding is received on aprorata basis over the twelve month period and is adjusted for changes in full time equivalent (FTE)student population.

Income taxes: The School is a division of a nonprofit corporation. Revenue of the School is derivedprimarily from other governmental entities. The School is exempt from income taxes under Section501(c)(3) of the Internal Revenue Code. Accordingly, no provision for income taxes has been madein these financial statements.

Capital assets: Property and equipment purchased or acquired are capitalized at historical cost orestimated historical cost. Capital assets are defined by the School as assets with an initial cost of$ 750 and useful life of over one year. Donated property and equipment are valued at theestimated fair market value as of the date received. Additions, improvements and other capitaloutlays that significantly extend the useful life of an asset are capitalized and depreciated over theremaining useful lives of the related fixed assets. Other costs incurred for repairs and maintenanceare expensed as incurred.

Depreciation on all assets is provided on the straight line basis over the estimated useful lives asfollows:

Building 45 yearsFurniture, fixtures and equipment 5 yearsComputer equipment 3 years

Deferred outflows/inflows of resources: In addition to assets, the statement of financial positionwill sometimes report a separate section for deferred outflows of resources. This separatefinancial statement element, deferred outflows of resources, represents a consumption of netposition that applies to a future period(s) and so will not be recognized as an outflow of resources(expense/expenditure) until then. The School does not have any items that qualify for reporting inthis category.

In addition to liabilities, the statement of financial position will sometimes report a separatesection for deferred inflows of resources. This separate financial statement element, deferredinflows of resources, represents an acquisition of net position that applies to a future period(s) andso will not be recognized as an inflow of resources (revenue) until that time. The School does nothave any items that qualify for reporting in this category.

19

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 2 Summary of Significant Accounting Policies (continued)

Unearned revenue: Unearned revenue arises when the School receives resources before it has alegal claim to them.

Compensated absences: The School’s policy permits employees to accumulate earned but unusedpaid time off, which is eligible for payment upon separation from services. The liability for suchleave is reported as incurred in the government wide financial statements. A liability for thoseamounts is recorded in the governmental funds only if the liability has matured as a result ofemployee resignations or retirements. The liability for compensated absences includes salaryrelated benefits, where applicable. Payments for compensated absences are generally paid out ofthe General Fund.

Net position: Net position is classified in three categories. The general meaning of each is asfollows:

Net investment in capital assets represents the difference between thecost of capital assets, less accumulated depreciation reduced by theoutstanding balances of borrowings used for the acquisition, constructionor improvement of those assets.

Restricted consists of net position with constraints placed on their useeither by 1) external groups such as creditors, grantors, contributors, orlaws or regulations of other governments, or 2) law throughconstitutional provisions or enabling legislation.

Unrestricted indicated that portion of net position that is available tofund future operations.

Fund balance: The governmental fund financial statements present fund balances based on theprovisions of GASB Statement No. 54, Fund Balance Reporting and Governmental Fund TypeDefinitions. This Statement provides more clearly defined fund balance classifications and also setsa hierarchy which details how the School may spend funds based on certain constraints. Thefollowing are the fund balance classifications used in the governmental fund financial statements:

Nonspendable this classification includes amounts that cannot be spentbecause they are either not in spendable form or are legally orcontractually required to be maintained intact. The School classifiesinventories, prepaid items, long term notes receivable and deposits asnonspendable since they are not expected to be converted to cash or arenot expected to be converted to cash within the next year.

Restricted this classification includes amounts that are restricted forspecific purposes by external parties such as grantors and creditors or areimposed by law through constitutional provisions or enabling legislation.

Committed this classification includes amounts that can be used forspecific purposes voted on through formal action of the Board ofDirectors (the highest level of decision making authority). The committedamount cannot be used for any other purpose unless the Board ofDirectors removes or changes the commitment through formal action.

20

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 2 Summary of Significant Accounting Policies (continued)

Assigned this classification includes amounts that the Board of Directorsintends to use for a specific purpose but they are neither restricted norcommitted. The School classifies existing fund balance to be used in thesubsequent year’s budget for elimination of a deficit as assigned.

Unassigned this classification includes amounts that have not beenrestricted, committed or assigned for a specific purpose within theGeneral Fund.

The details of the fund balances are included in the Governmental Fund Balance Sheet on page 9.

When the School incurs expenditures for which restricted or unrestricted fund balance is available,the School would consider restricted funds to be spent first. When the School has expenditures forwhich committed, assigned or unassigned fund balance is available, the School would considercommitted funds to be spent first, then assigned funds and lastly unassigned funds.

Use of estimates: The preparation of financial statements in conformity with generally acceptedaccounting principles requires management to make estimates and assumptions that affect certainreported amounts and disclosures. Accordingly, actual results could differ from those estimates.

Budget: An operating budget is adopted and maintained by the governing board for the Schoolpursuant to the requirements of Florida Statutes. The budget is adopted using the same basis ofaccounting that is used in the preparation of the basic financial statements.

Date of management review: Subsequent events were evaluated by management throughSeptember 15, 2016, which is the date the financial statements were available to be issued.

Note 3 Cash and Cash Equivalents

At June 30, 2016, the carrying amount of the deposits and cash on hand totaled $ 1,477,879, with abank balance of $ 1,488,056.

State statutes require, and it is the School’s policy, that all deposits be made into, and be held by,financial institutions designated by the Treasurer of the State of Florida as “qualified publicdepositories” as defined by Chapter 280 of the Florida Statutes. This Statute requires that everyqualified public depository institution maintain eligible collateral to secure the public entity’s funds.The minimum collateral to be pledged by an institution, the collateral eligible for pledge, and thereporting requirements of the qualified public depositor to the Treasurer is defined by statute.Collateral is pooled in a multiple qualified public depository institution pool with the ability toassess members of the pool should the need arise. The School’s deposits are held in a qualifiedpublic depository and are covered by the collateral pool because the School has identified itself asa public entity.

Note 4 Due From/To Related Party

The School is a Department of Renaissance Charter School, Inc. (“RCS”). As of June 30, 2016, RCSowes the School $ 304 for various prepaid expenses.

21

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 4 Due From/To Related Party (continued)

Both the School and Duval Charter School at Mandarin (MAND) are related, as they areDepartments of RCS. As of June 30, 2016, the financial statements include an amount due toMAND in the General Fund of $ 236.

The School shares common board membership with various other schools, as they are allDepartments of RCS. As of June 30, 2016, the basic financial statements include amounts due toseveral of these affiliated schools of $ 119, in aggregate, for payroll related expenses.

Note 5 Due From/To Other Governments

Due from other governments at June 30, 2016 consists of amounts due from the FloridaDepartment of Education relating to capital outlay and Title II funding and an amount due from theFlorida Department of Agriculture for the National School Lunch Program.

Due to other governments at June 30, 2016 consists of an amount due to the School Board of DuvalCounty for FTE funding overpayment.

Note 6 Due From Trustee

Due from trustee at June 30, 2016 consists of amounts relating to FTE funds that have yet to betransferred to the School.

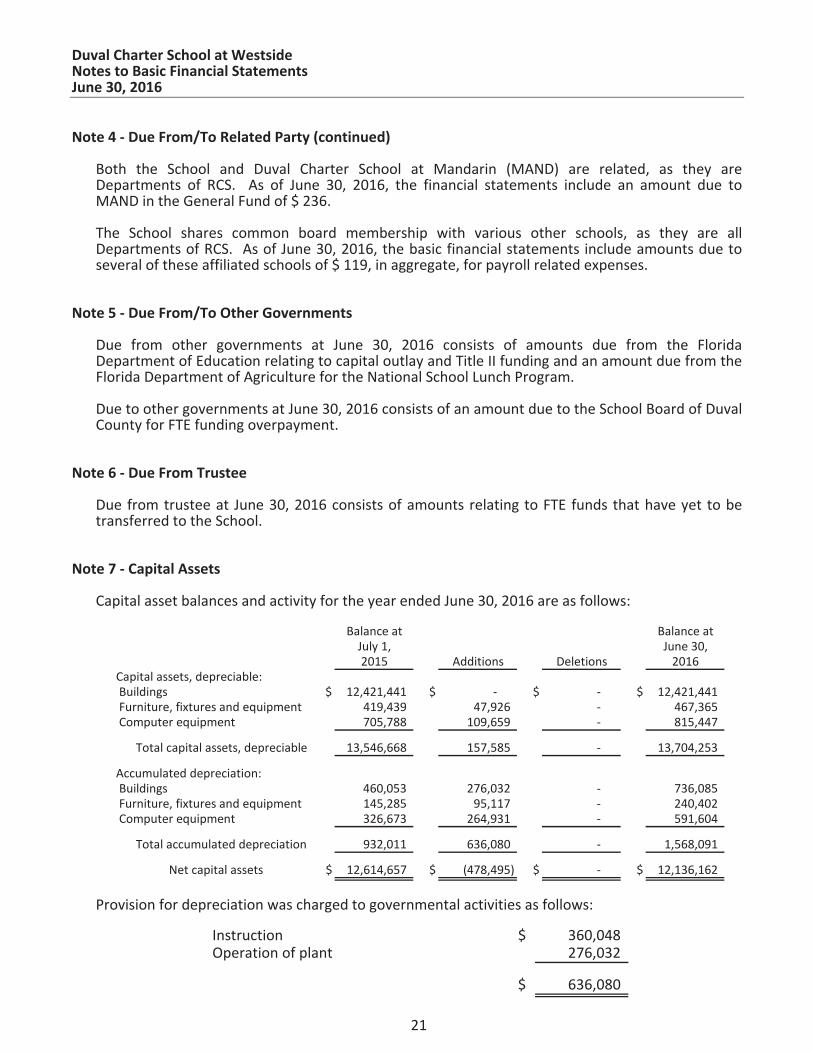

Note 7 Capital Assets

Capital asset balances and activity for the year ended June 30, 2016 are as follows:

Balance at Balance atJuly 1, June 30,2015 Additions Deletions 2016

Capital assets, depreciable:Buildings $ 12,421,441 $ $ $ 12,421,441Furniture, fixtures and equipment 419,439 47,926 467,365Computer equipment 705,788 109,659 815,447

Total capital assets, depreciable 13,546,668 157,585 13,704,253

Accumulated depreciation:Buildings 460,053 276,032 736,085Furniture, fixtures and equipment 145,285 95,117 240,402Computer equipment 326,673 264,931 591,604

Total accumulated depreciation 932,011 636,080 1,568,091

Net capital assets $ 12,614,657 $ (478,495) $ $ 12,136,162

Provision for depreciation was charged to governmental activities as follows:

Instruction $ 360,048Operation of plant 276,032

$ 636,080

22

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

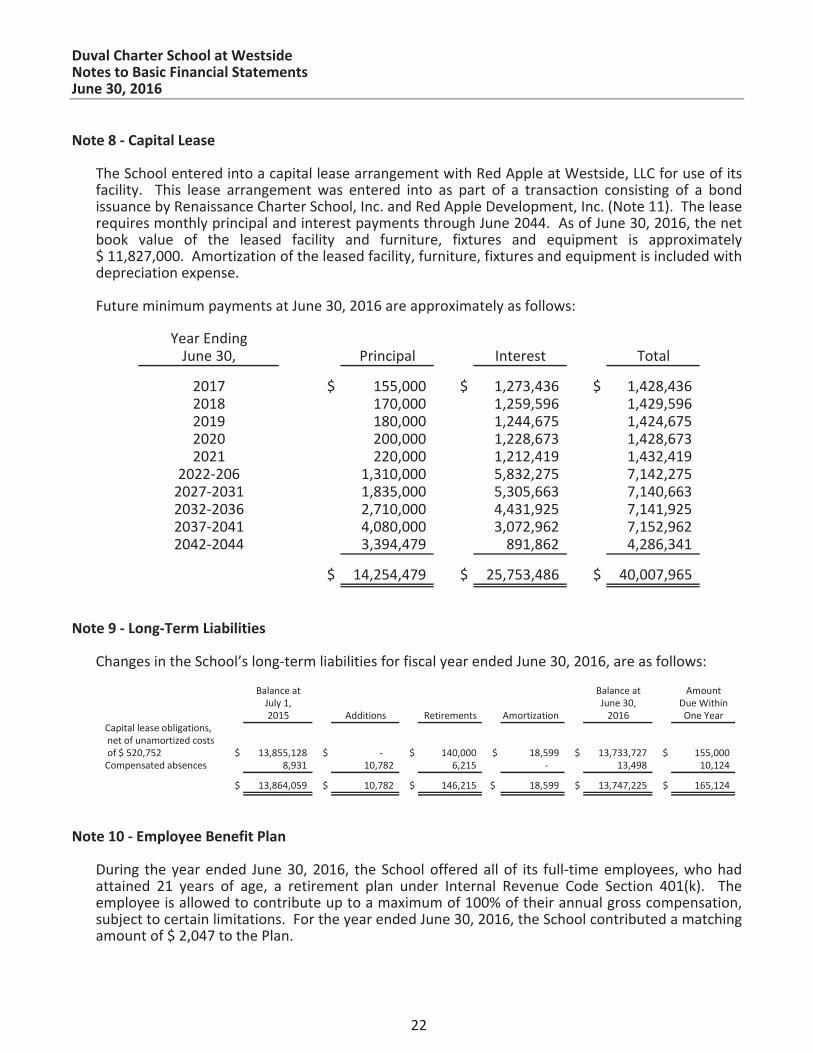

Note 8 Capital Lease

The School entered into a capital lease arrangement with Red Apple at Westside, LLC for use of itsfacility. This lease arrangement was entered into as part of a transaction consisting of a bondissuance by Renaissance Charter School, Inc. and Red Apple Development, Inc. (Note 11). The leaserequires monthly principal and interest payments through June 2044. As of June 30, 2016, the netbook value of the leased facility and furniture, fixtures and equipment is approximately$ 11,827,000. Amortization of the leased facility, furniture, fixtures and equipment is included withdepreciation expense.

Future minimum payments at June 30, 2016 are approximately as follows:

Year EndingJune 30, Principal Interest Total

2017 $ 155,000 $ 1,273,436 $ 1,428,4362018 170,000 1,259,596 1,429,5962019 180,000 1,244,675 1,424,6752020 200,000 1,228,673 1,428,6732021 220,000 1,212,419 1,432,419

2022 206 1,310,000 5,832,275 7,142,2752027 2031 1,835,000 5,305,663 7,140,6632032 2036 2,710,000 4,431,925 7,141,9252037 2041 4,080,000 3,072,962 7,152,9622042 2044 3,394,479 891,862 4,286,341

$ 14,254,479 $ 25,753,486 $ 40,007,965

Note 9 Long Term Liabilities

Changes in the School’s long term liabilities for fiscal year ended June 30, 2016, are as follows:

Balance at Balance at AmountJuly 1, June 30, Due Within2015 Additions Retirements Amortization 2016 One Year

Capital lease obligations,net of unamortized costsof $ 520,752 $ 13,855,128 $ $ 140,000 $ 18,599 $ 13,733,727 $ 155,000Compensated absences 8,931 10,782 6,215 13,498 10,124

$ 13,864,059 $ 10,782 $ 146,215 $ 18,599 $ 13,747,225 $ 165,124

Note 10 Employee Benefit Plan

During the year ended June 30, 2016, the School offered all of its full time employees, who hadattained 21 years of age, a retirement plan under Internal Revenue Code Section 401(k). Theemployee is allowed to contribute up to a maximum of 100% of their annual gross compensation,subject to certain limitations. For the year ended June 30, 2016, the School contributed a matchingamount of $ 2,047 to the Plan.

23

Duval Charter School at WestsideNotes to Basic Financial StatementsJune 30, 2016

Note 11 Commitments

Management agreement: The School has a formal agreement with Charter Schools USA, Inc.(“CSUSA”) to manage, staff and operate the School. The agreement states that CSUSA shall beentitled to cost reimbursements and management fees (the “fee”) for its services, subject toavailability of funds. The fee is subordinated to all lease payment requirements (Note 8). The feeranges from $ 608,906 for fiscal year 2017 to $ 1,132,876 for fiscal year 2043 as defined in theagreement or the budgeted amount approved by the Board of Directors based on enrollment andSchool performance. The agreement has an initial term which expires in June 2018. It willautomatically renew for five year periods unless terminated by either party. For the year endedJune 30, 2016, CSUSA did not receive a fee.

The School had an amount of $ 688,387 due to CSUSA at June 30, 2016. In addition the School’saccounts payable balance had an amount payable to CSUSA for $ 296,964, for invoiced services.

Lease agreement: In October 2013, the Florida Development Finance Corporation (the“Corporation”) issued $ 73,040,000 in Tax Exempt Educational Facilities Revenue Bonds, Series2013A and $ 7,485,000 in Taxable Educational Facilities Revenue Bonds, Series 2013B pursuant toan Indenture of Trust between the Corporation and a trustee to make a loan to RenaissanceCharter Schools, Inc. (“REN”), a division of which the School exists, and Red Apple Development,LLC and subsidiaries (“RAD”) to finance the acquisition of the facilities of five charter schoolsexisting under Renaissance Charter Schools, Inc. In order to secure the payment of the principaland interest on the bonds, the Corporation assigned all of its rights and interest in the loanagreement to the trustee. The bonds are payable from and secured by a lien upon and pledge ofpayments to be received by the trustee.

Concurrent with the preceding loan transaction, RAD, through its wholly owned subsidiaries,entered into five lease agreements with REN. The facilities which are owned by RAD are leased byREN on behalf of the schools under a 45 year lease (Note 8). The leases are deemed to be capitalleases and the capital lease payments are based on the debt service requirements of the bondswhich extend through June 2044. These payments are made from the revenues received from theDuval County School Board for the operation of the Schools. REN is obligated under the Indentureto deposit all Charter revenues received from the School Board and additional revenues, if any,directly with the trustee during the term of the lease. The payments are applied by the trustee tomake sinking fund payments and pay for operating expenses.

In addition to the capital lease payments noted in Note 8, the School is required to pay incrementalrent payments to RAD. The incremental rent payments range from approximately $ 116,045 to$ 243,980 per year over the term of the agreement which is through June 2043. For the yearending June 30, 2016, the School paid incremental rent to RAD in the amount of $ 116,465.

Post retirement benefits: The School does not provide post retired benefits to retired employees.

Note 12 Risk Management

The School is exposed to various risks of loss related to torts, thefts of, damage to, and destructionof assets and natural disasters. The School has obtained property insurance from commercialcompanies including, but not limited to, general liability and errors and omissions insurance. Therehave been no claims in excess of insurance coverage limits during the past three years.

As disclosed in Note 11, CSUSA employs all of the employees of the School. As a result, the Schoolis not exposed to medical or workers’ compensation claims for these individuals. In addition, CSUSAcarries all required insurance including, but not limited to, general liability and errors and omissionsinsurance.

OTHER INDEPENDENTAUDITOR’S REPORTS

KMCcpa.com | 6550 N Federal Hwy, 4th Floor Fort Lauderdale, FL 33308 Phone: 954.771.0896 Fax: 954.938.9353

24

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVERFINANCIAL REPORTING AND ON COMPLIANCE AND OTHER

MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMEDIN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

To the Board of DirectorsDuval Charter School at WestsideA Department of Renaissance Charter School, Inc.Jacksonville, Florida

We have audited, in accordance with the auditing standards generally accepted in the United States ofAmerica and the standards applicable to financial audits contained in Government Auditing Standardsissued by the Comptroller General of the United States, the financial statements of the governmentalactivities, each major fund, and the aggregate remaining fund information of Duval Charter School atWestside (the “School”), a Department of Renaissance Charter School, Inc. and a component unit ofthe Duval County School Board, Florida, as of and for the year ended June 30, 2016, and the relatednotes to the financial statements, which collectively comprise the School’s basic financial statements,and have issued our report thereon dated September 15, 2016.

Internal Control Over Financial Reporting

In planning and performing our audit of the financial statements, we considered the School’s internalcontrol over financial reporting (internal control) to determine the audit procedures that areappropriate in the circumstances for the purpose of expressing our opinions on the financialstatements, but not for the purpose of expressing an opinion on the effectiveness of the School’sinternal control. Accordingly, we do not express an opinion on the effectiveness of the School’s internalcontrol.

A deficiency in internal control exists when the design or operation of a control does not allowmanagement or employees, in the normal course of performing their assigned functions, to prevent, ordetect and correct, misstatements on a timely basis. A material weakness is a deficiency, or acombination of deficiencies, in internal control, such that there is a reasonable possibility that amaterial misstatement of the entity's financial statements will not be prevented, or detected andcorrected on a timely basis. A significant deficiency is a deficiency, or a combination of deficiencies, ininternal control that is less severe than a material weakness, yet important enough to merit attentionby those charged with governance.

Our consideration of internal control was for the limited purpose described in the first paragraph ofthis section and was not designed to identify all deficiencies in internal control that might be materialweaknesses or, significant deficiencies. Given these limitations, during our audit we did not identify anydeficiencies in internal control that we consider to be material weaknesses. However, materialweaknesses may exist that have not been identified.

25

Duval Charter School at Westside

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the School’s financial statements are freefrom material misstatement, we performed tests of its compliance with certain provisions of laws,regulations, contracts, and grant agreements, noncompliance with which could have a direct andmaterial effect on the determination of financial statement amounts. However, providing an opinionon compliance with those provisions was not an objective of our audit, and accordingly, we do notexpress such an opinion. The results of our tests disclosed no instances of noncompliance or othermatters that are required to be reported under Government Auditing Standards.

Purpose of this Report

The purpose of this report is solely to describe the scope of our testing of internal control andcompliance and the results of that testing, and not to provide an opinion on the effectiveness of theentity's internal control or on compliance. This report is an integral part of an audit performed inaccordance with Government Auditing Standards in considering the entity's internal control andcompliance. Accordingly, this communication is not suitable for any other purpose

KEEFE McCULLOUGH

Fort Lauderdale, FloridaSeptember 15, 2016

KMCcpa.com | 6550 N Federal Hwy, 4th Floor Fort Lauderdale, FL 33308 Phone: 954.771.0896 Fax: 954.938.9353

26

INDEPENDENT AUDITOR’S REPORT TO THE BOARD OF DIRECTORS

To the Board of DirectorsDuval Charter School at WestsideA Department of Renaissance Charter School, Inc.Jacksonville, Florida

Report on the Financial Statements

We have audited the financial statements of Duval Charter School at Westside (the “School”), aDepartment of Renaissance Charter School, Inc. and a component unit of the Duval County SchoolBoard, Florida, as of and for the year ended June 30, 2016, and have issued our report thereon datedSeptember 15, 2016.

Auditor’s Responsibility

We conducted our audit in accordance with auditing standards generally accepted in the United Statesof America and the standards applicable to financial audits contained in Government AuditingStandards, issued by the Comptroller General of the United States and Chapter 10.850, Rules of theAuditor General.

Other Report

We have issued our Independent Auditor’s Report on Internal Control over Financial Reporting andCompliance and Other Matters Based on an Audit of the Financial Statements Performed inAccordance with Government Auditing Standards. Disclosures in that report, which is datedSeptember 15, 2016, should be considered in conjunction with this management letter.

Prior Audit Findings

Section 10.854(1)(e)1., Rules of the Auditor General, requires that we determine whether or notcorrective actions have been taken to address findings and recommendations made in the precedingannual financial audit report. There were no recommendations made in the preceding audit report.

Official Title

Section 10.854(1)(e)5., Rules of the Auditor General, requires the name or official title of the entity.The official title of the entity is Duval Charter School at Westside.

Financial Condition

Section 10.854(1)(e)2., Rules of the Auditor General, require that we report the results of ourdetermination as to whether or not the School has met one or more of the conditions described inSection 218.503(1), Florida Statutes, and identification of the specific condition(s) met. In connectionwith our audit, we determined that the School did not meet any of the conditions described in Section218.503(1), Florida Statutes.

27

Duval Charter School at Westside

Pursuant to Sections 10.854(1)(e)6.a. and 10.855(12), Rules of the Auditor General, we appliedfinancial condition assessment procedures for the School. It is management’s responsibility to monitorthe School’s financial condition, and our financial condition assessment was based in part onrepresentations made by management and the review of financial information provided by same.

Transparency

Sections 10.854(1)(e)7. and 10.855(13), Rules of the Auditor General, require that we report the resultsof our determination as to whether the School maintains on its website the information specified inSection 1002.33(9)(p), Florida Statutes. In connection with our audit, we determined that the Schoolmaintained on its website the information specified in Section 1002.33(9)(p), Florida Statutes.

Other Matters

Section 10.854(1)(e)3., Rules of the Auditor General, requires that we address in the managementletter any recommendations to improve financial management. In connection with our audit, we didnot have any such recommendations.

Section 10.854(1)(e)4., Rules of the Auditor General, requires that we address noncompliance withprovisions of contracts or grant agreements, or abuse, that have occurred, or are likely to haveoccurred, that have an effect on the financial statements that is less than material but which warrantsthe attention of those charged with governance. In connection with our audit, we did not have anysuch findings.

Purpose of this Letter

Our management letter is intended solely for the information and use of the Legislative AuditingCommittee, members of the Florida Senate and the Florida House of Representatives, the FloridaAuditor General, Federal and other granting agencies, the Board of Directors and applicablemanagement and is not intended to be and should not be used by anyone other than these specifiedparties.

KEEFE McCULLOUGH

Fort Lauderdale, FloridaSeptember 15, 2016