e-commerce: the emergence of a new asset class?

TRANSCRIPT

The shape of the futureE-commerce: The emergence of a new asset class?

Alexandra Tornow

Head of EMEA Logistics

& Industrial Research

Why logistics real estate: The retail factor

1

Improving quality of logistics assets …

but large parts of the existing stock

will remain competitive

High and increasing diversity

of space requirements drive

opportunities for all lot sizesNew distribution patterns drive

incremental demand for

logistics space

The inexorable shift to ‘everywhere

consumption’ is pushing the

importance of the asset class

Logistics network

alignment has only just begun

Source: JLL

Incremental logistics demand

2

10 millionsq m p/a

13.2 millionsq m p/a

Further globalization of supply chains

Source: JLL

The boom era2004 - 2008

Economic woes2009 - 2013

New retail patterns

30%

… and a variety of different delivery options

Increased supply chain complexity

3

Today, the path of a parcel

involves up to four warehouses …

LOCAL COLLECTION

DEPOT

HUB

LOCAL DELIVERY

DEPOT

E-FULFILLMENT CENTRE CLICK &

COLLECT

SAME-DAY

DELIVERY

CAR DROP-OFFPackage repository

through secure access

PRIVATE

PARCEL BOX

SAME-HOUR

DELIVERYBased on predictive

analytics

SHIP

FROM STORE

LOCKER

STATIONSAt major transport

interlinks

NEW

CONCEPTSYet to be designed

+

Source: JLL

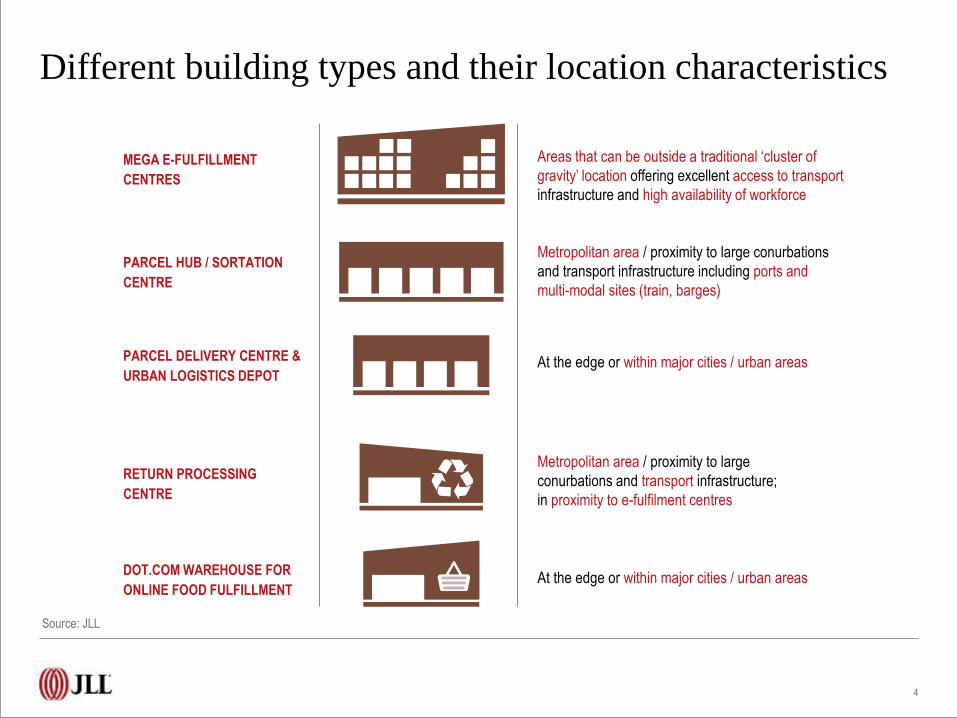

Different building types and their location characteristics

4

Areas that can be outside a traditional ‘cluster of

gravity’ location offering excellent access to transport

infrastructure and high availability of workforce

Metropolitan area / proximity to large conurbations

and transport infrastructure including ports and

multi-modal sites (train, barges)

At the edge or within major cities / urban areas

At the edge or within major cities / urban areas

Metropolitan area / proximity to large

conurbations and transport infrastructure;

in proximity to e-fulfilment centres

MEGA E-FULFILLMENT

CENTRES

PARCEL HUB / SORTATION

CENTRE

PARCEL DELIVERY CENTRE &

URBAN LOGISTICS DEPOT

RETURN PROCESSING

CENTRE

DOT.COM WAREHOUSE FOR

ONLINE FOOD FULFILLMENT

Source: JLL

5

JLL occupier survey: % of respondents indicating their floorspace requirements (multiple responses possible)

No size fits all …

38% Very large

(30,000 - 50,000 sq m)

32%Medium sized

(10,000 - 30,000 sq m)

30% Small

(below 10,000 sq m)

25% Mega-sheds

(above 50,000 sq m)

Source: JLL logistics and industrial occupier survey Europe in cooperation with CoreNet Global

… but big is beautiful

The ‘emergence’ of mega sheds…

6

6.5 million sq mCompleted

2009 – H1 2014

~ 1.1 million sq m Under construction

Source: JLL

… and their tenant base

7

25%3 PL

23%Online

23%Multi-channel

21%General retail

6%Manufacturing

2%Other

Source: JLL

Single unit assets >50,000 sq m

394

8

The geography of mega sheds

Source: JLL

190*

276

910

2,490

282

540512

584

225

160

100

1,340

n/a

,000 sq m

*planned

Improving quality of logistics assets

9

More than of new facilities built since 2009 30 million sq mFeaturing:

Mezzanine floorspace

Power supply

Loading doors

Employee rooms

Car parking

Port location

Rail access

Multi-modal

Sustainability

`

P

Source: JLL

Month 00, 2014 10

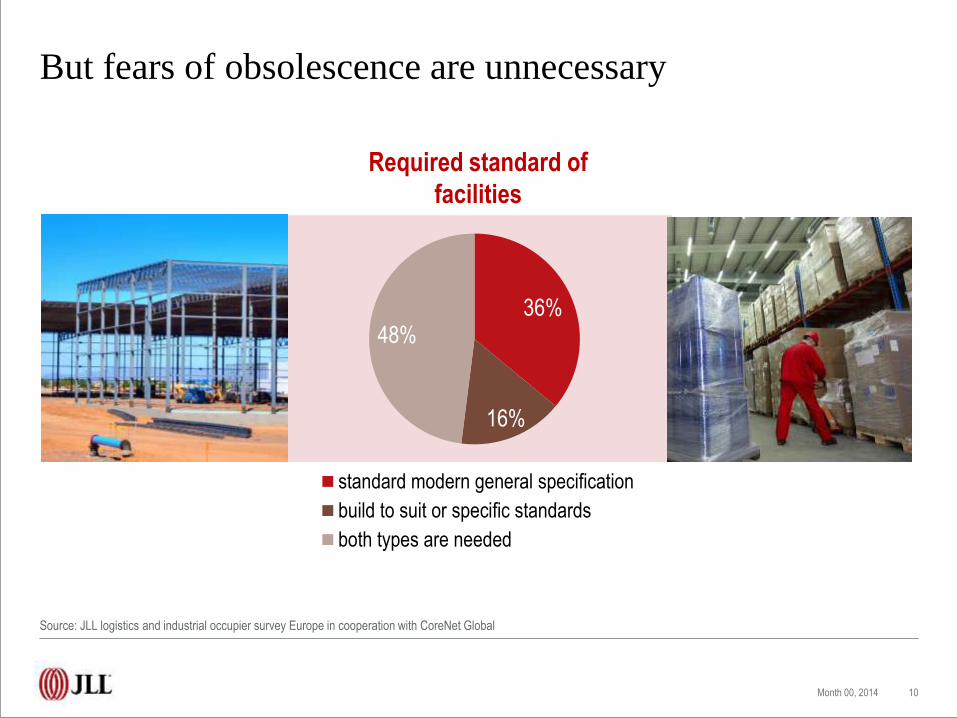

36%

16%

48%

standard modern general specification

build to suit or specific standards

both types are needed

Required standard of

facilities

Source: JLL logistics and industrial occupier survey Europe in cooperation with CoreNet Global

But fears of obsolescence are unnecessary

Logistics network not fit for the futureLive-poll results of 70+ seminar attendees

11

Source: JLL, Corenet Global

3%Yes, current network

alignment is fit for

purpose

67%No, current network

alignment will need

significant future

restructuring.

30%

Minor adjustments

required

The opportunities

Why logistics real estate?

12

Growing geographic spread: rising appeal of smaller markets

Widespread demand offers opportunities for all lot sizes

Large-size single assets: continued development

Further potential for portfolio and JV deals

Moving up the risk curve: value-add and opportunistic

Further yield compression as asset class matures

Growing liquidity: further stock expansion

Source: JLL

13

Logistics real estate networks will continue to

evolve, sustaining ongoing healthy market fundamentals

and therefore further opportunities for landlords,

developers and investors

For successful ‘everywhere consumption’

logistics and supply chain managementare critical

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without

the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no

representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang

LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Contact

14

Alexandra Tornow

Head of EMEA Logistics & Industrial Research

Frankfurt

+49 (0)69 2003 1352

de.linkedin.com/pub/alexandra.tornow

@aletornow