e-sign lessons learned

TRANSCRIPT

www.brodeconsulting.com Page 1

E-Sign Lessons Learned

June 24, 2021

P O Box 1072

Ravenna, Ohio 44266

Presented By: Molly Stull

Email: [email protected]

www.brodeconsulting.com

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided

with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or

other expert assistance is required, the services of a competent professional should be sought.

www.brodeconsulting.com Page 2

About Brode Consulting Services, Inc.

Brode Consulting Services has been in business since 1998 and our mission statement has been our mantra from day one... to provide exceptional consulting services and to be your partner in this ever-changing banking environment. Our clients are business partners as well as friends... it's always been that way. We understand your needs and challenges because all of our consultants have "been there / done that"! We are committed to serving community financial institutions and always will be. And although banking can be frustrating, we truly love it! Thanks for the honor and opportunity to work with you today. We invite you to visit our website at https://www.brodeconsulting.com/ to sign up for our weekly Brode Bulletin (Free) and our quarterly newsletter NewsFlash, and to learn more about Brode Consulting Services, Inc. Contact us for a free consultation on how we can assist you with your Compliance Risk Management program, including audits and reviews, risk assessments, and more.

OVERVIEW

We were asked to social distance and shelter-in-place which has caused us to utilize alternative delivery methods, but are we really “delivering” the required documents? With a “click” of a button documents can be instantaneously sent, but is the process in compliance with the E-Sign Act? It’s a hot topic so let’s make sure your process is compliant.

Background

The Electronic Signatures in Global and National Commerce Act (E-Sign Act) was signed into law on June 30, 2000, and the consumer consent provisions became effective on October 1st of the same year. The E-Sign Act, available here, allows the use of electronic records to satisfy any statute, regulation, or rule of law requiring that such information be provided in writing. The consumer must receive notice and must affirmatively consent prior to the electronic delivery of the disclosure or document.

When Does the E-Sign Act Become Relevant?

The E-Sign Act becomes relevant when a federal law or regulation REQUIRES the Institution to send or deliver a document and that law or regulations states that it has to be IN WRITING. When these

www.brodeconsulting.com Page 3

two conditions are present, then either the document must be delivered in paper format or delivered electronically in compliance with the E-Sign Act.

Fundamental Information

Many acts are implemented by a final rule such as the Truth in Lending Act, which is implemented by Regulation Z, with oversight provided by the Consumer Financial Protection Bureau (CFPB). The E-Sign Act does not have an implementing regulation. Typically, an implementing regulation provides additional details designed to assist with carrying out the requirements of an act. The E-Sign Act does not provide for any civil money penalties (CMPs), but don’t assume that there will be no consequences for your institution if the Act is not followed during electronic delivery. The E-Sign Act is a beneficial act, which means that it grants additional opportunities, such as providing the option to deliver documents through an electronic process. There is no requirement to utilize electronic delivery as many other delivery options exist such as hand delivering loan documents or using the U.S. mail. However, if the electronic delivery method is the chosen method, then compliance with the E-Sign Act is required. The E-Sign Act is not limited to financial institutions. It is a universal Act which allows all types of entities to utilize an electronic delivery option unless an exception exists.

The Act is located in Title 15-Commerce and Trade, Chapter 96, Electronic Signatures in Global and National Commerce, (15 U.S.C. §7001 et seq.) and consists of the following sections: Subchapter I – Electronic Records and Signatures in Commerce

• 7001. General rule of validity • 7002. Exemption to preemption • 7003. Specific exceptions • 7004. Applicability to Federal and State governments • 7005. Studies • 7006. Definitions

Subchapter II – Transferable Records

www.brodeconsulting.com Page 4

• 7021. Transferable Records

Subchapter III – Promotion of International Electronic Commerce

• 7031. Principles governing the use of electronic signatures in international transactions.

Definitions

As always when one is reviewing and researching, it is critical that one utilizes the definitions under the corresponding act or regulation. The following definitions are critical to understanding the E-Sign Act:

• Consumer: Means an individual who obtains, through a transaction, products or services which are used primarily for personal, family, or household purposes, and also means the legal representative of such an individual.

• Electronic Record: A contract or other record, created, generated, sent, communicated, received, or stored by electronic means.

• Electronic Signature: An electronic sound, symbol, or process, attached to or logically associated with a contract or other record and executed or adopted by a person with the intent to sign the record.

• Person: An individual, corporation, business trust, estate, trust, partnership, limited liability company, association, joint venture, governmental agency, public corporation, or any other legal or commercial entity.

• Record: Information that is inscribed on a tangible medium or that is stored in an electronic or other medium and is retrievable in perceivable form.

Internal Procedure vs Regulatory Requirement

When checking to determine if a document must be delivered through an E-Sign Act compliant method, be sure to understand if the document’s delivery is required due to your institution’s internal processes or is a regulatory requirement. A very helpful resource

www.brodeconsulting.com Page 5

for reviewing numerous regulations is the CFPB’s Interactive Bureau Regulations, which is located at: https://www.consumerfinance.gov/policy-compliance/rulemaking/regulations/. Also ensure that one takes into consideration if the document is delivered utilizing more than one delivery method, as an electronic delivery followed by an in-person delivery might satisfy the regulatory delivery requirements. It is recommended that the institution develop a flowchart or map that details the timing and delivery methods utilized in providing loan documentation to applicants and borrowers.

Notice

Essentially, there are two main conditions that must be satisfied, the delivery of a notice and the consumer must affirmatively consent to receiving the document(s) electronically. These steps must be completed prior to sending required written documents electronically. The following are more details applicable to each condition:

1) Consumer must be provided with a Notice prior to consent that includes:

a. Any right or option to receive a disclosure in paper form;

b. Whether the consent applies only to a particular transaction or to categories that may be provided during the course of the parties’ relationship;

c. The right to withdraw consent to have records provided electronically, including any conditions, consequences, or fees associated with doing so;

d. The institution must describe the procedures for withdrawing consent;

e. Procedures for updating information needed to contact the consumer electronically;

www.brodeconsulting.com Page 6

f. How the consumer may obtain a paper copy of the record upon request; and

g. The hardware and software requirements for access to and retention of the electronic information.

The notice must detail the types of transactions in which the consumer is providing consent. Therefore, it is important to read the E-Sign Act notice that is being provided to the consumer. Does the notice limit the consent to just one account, such as the following sample? This E-Sign Disclosure and Consent (the "Consent") provides the person(s) giving his/her consent below ("you" and "your") with information relating to your electronic receipt of disclosures and notices (collectively, the "Disclosures") in connection with your residential mortgage loan application (the "Loan") pending with the Lender identified in the Disclosures. By providing your consent, you agree that the Lender may send you any and all Disclosures (which are described below) relating to the Loan in an electronic form so that you may view, download, upload, approve, sign (if requested) and return documents electronically. The notice language may be limited to deposit products, loan products, products and services requested online or it may entail all future account relationships with the institution. The language is unique to your institution, so be sure that the E-Sign Act notice includes the product or service for which the institution desires to fulfill written delivery requirements electronically.

2) Consumer must affirmatively consent:

• If the consumer consents electronically, or confirms his or her consent electronically, it must be in a manner that reasonably demonstrates the consumer can access information in the electronic form that will be used to provide the information that is the subject of the consent.

The consumer must also affirmatively consent to receiving documents via electronic delivery. Just providing the written E-Sign Act notice during an in-person meeting does not fulfill this

www.brodeconsulting.com Page 7

obligation. Typically, the consumer will consent electronically in a manner that reasonably demonstrates that the consumer can access information in the electronic form that will be used to provide the information that is the subject of the consent. This consent must be retained. Are you able to prove that your institution obtained affirmative consent prior to sending required written disclosures electronically? A common practice is to bundle the E-Sign Act notice and the affirmative consent process with the initial electronic delivery of required disclosures, such as with the delivery of the Loan Estimate. While this practice is acceptable there is one thing to keep in mind. If your consumer does not affirmatively consent to receiving documents electronically prior to the end of the third business day, technically the Loan Estimate has not been delivered timely. Why? The consumer has not agreed to receiving documents electronically. So be sure that if your institution sends required written disclosures with the E-Sign Act notice and consent process that someone is checking to ensure that the consumer electronically affirms consent within the required delivery timeframe. If no consent is received, then the institution must provide written notice via a non-electronic method, such as placing the Loan Estimate in the mail within the required time frame. In the case of a Loan Estimate, this would be within three business days. Does the institution need to confirm that an email containing a Loan Estimate or other required disclosure was opened? It is not necessary to monitor the email to ensure that it was read by the consumer provided that the institution has record that the consumer affirmatively agreed to receive written disclosures for the identified product or service. Think of this in the same way as an envelope physically mailed to the consumer. We have no way of knowing that the consumer actually opened and read the contents, but by placing the envelope in the mail within the required time period we have satisfied the delivery requirements. The same is true for electronic delivery of documents. The use of electronic delivery is quick and easy. Just make sure to identify the documents that are being provided electronically, determine if these documents must be provided in writing as outlined by their governing regulation and that the institution has received affirmative consent as outlined in the E-Sign Act that includes these products and services from the consumer for their

www.brodeconsulting.com Page 8

electronic delivery. Then, if all of these conditions are satisfied, delivery is as easy as clicking a button!

E-Sign Act Considerations TRID

Loan Estimate (LE) Only one applicant needs to receive the Loan Estimate. Closing Disclosure (CD) At least one copy of the CD must be provided in connection with each loan subject to Regulation Z. When providing the CD, one must also determine who is entitled to the right of rescission. Right of Rescission If the loan transaction is subject to the right of rescission, then all persons with the right to rescind need to receive a copy of the CD (and two (2) copies of the RoR). The CD contains the material TILA disclosures which are a trigger for ROR timing. 1026.17(d)-2. Multiple consumers.

• When two consumers are joint obligors with primary liability on an obligation, the disclosures may be given to either one of them.

o [2 applicants, disclosures to either applicant]

• If one consumer is merely a surety or guarantor, the disclosures must be given to the principal debtor.

o [1 applicant & guarantor, disclosures to applicant only]

• In rescindable transactions, however, separate disclosures

must be given to each consumer who has the right to rescind under § 1026.23, although the disclosures required under § 1026.19(b) need only be provided to the consumer who expresses an interest in a variable-rate loan program.

o 1026.23: Right of Rescission section o 1026.19(b): Certain variable-rate transactions

CHARM booklet Loan program disclosure

• When two consumers are joint obligors with primary

liability on an obligation, the early disclosures required by

www.brodeconsulting.com Page 9

§ 1026.19(a), (e), or (g), as applicable, may be provided to any one of them.

o 1026.19: Closed-End Credit o (a) Mortgage transactions subject to RESPA (LE) o (e) Mortgage loans – early disclosures o (g) Special information booklet at time of application

• In rescindable transactions, the disclosures required by

§ 1026.19(f) must be given separately to each consumer who has the right to rescind under § 1026.23.

o 1026.19(f) Mortgage loans – final disclosures (CD) o 1026.23: Right of rescission

• In transactions that are not rescindable, the disclosures

required by § 1026.19(f) may be provided to any consumer with primary liability on the obligation. See §§ 1026.2(a)(11), 1026.17(b), 1026.19(a), 1026.19(f), and 1026.23(b).

• If the transaction is not subject to the right of rescission,

then the CD must be given to any consumer who is primarily liable on the obligation.

In summary, each person that has the right to rescind shall receive:

• One (1) copy of the Closing Disclosure • Two (2) copies of the RoR notice (One copy if delivered

electronically) • Timing requirements for delivery of the CD apply. (3 Business

Days prior to consummation) Separately

• Note, the regulation says that the disclosures must be provided “separately.” How does your institution handle this?

• Mailing – Two separate envelopes…one to the borrower and one to the non-borrowing spouse.

Electronic delivery

• If there is a non-borrowing spouse involved, ensure that the disclosure is delivered in writing. Check to ensure compliance with the E-Sign Act if delivered electronically. Sending the disclosures to the borrower would not fulfill the requirement if the non-borrowing spouse has not authorized electronic delivery.

www.brodeconsulting.com Page 10

Signatures on the CD

• Technically not required by Regulation Z • Recommended as this provides evidence that they have

received the disclosure. • Investor guidelines may require a signature.

No Automatic E-Sign System

Without the use of an E-Sign Act software product, it is possible for an institution to utilize electronic delivery utilizing the following steps:

1. Develop a notice that contains all of the required information.

2. Email this notice to the applicant in the same file format in which the institution will be sending required compliance documents, such as a PDF file.

3. Either include on the notice or in a separate file, a code that

the applicant would need to obtain.

4. Request that the applicant sign the notice affirmatively stating that they have consented to electronic delivery and return the notice.

5. Request that the applicant state the “code” in their return

email and that they wish to receive documents electronically. 6. The institution will need to retain proof of the electronic

consent (the return email).

This process will demonstrate that the consumer has the ability to retrieve the document electronically and also has consented to receive delivery electronically. The institution will also need to have a process to update email changes or when a consumer wishes to return to paper deliver.

Changes to Hardware or Software Requirements

www.brodeconsulting.com Page 11

If you or your third-party vendor make a change to the hardware or software requirements needed to access or retain electronic records that creates a material risk that the consumer will not be able to access or retain subsequent electronic records subject to the consent, you must:

• Provide the consumer with a statement of: o The revised hardware and software requirements for

access to and retention of electronic records, and o The right to withdraw consent without the

imposition of any condition, consequence, or fee for such a withdrawal; and

• Obtain confirmation of consent as detailed above. Uniform Electronic Transaction Act (UETA)

The Uniform Electronic Transaction Act (UETA) was published by the Uniform Law Commission in 1999 to ensure that electronic signatures, electronic records, and contracts based or memorialized in electronic formats would not be rejected merely because of their electronic nature. The UETA only applies in certain types of transactions and only when the parties have agreed to conduct the transactions electronically. The scope of this Act is inherently limited by the fact that the Act defines “transaction” as “an action or set of actions occurring between two or more persons relating to the conduct of business, commercial or governmental affairs.” The E-Sign Act was implemented in 2000 and addressed consumer consent provisions. As of June 2021, forty-eight states, the District of Columbia, and the U.S. Virgin Islands have adopted the UETA. Washington adopted the UETA on June 11, 2020. Illinois has introduced the Act through HB 3205 and SB 2176 during 2021 which currently has passed both houses. New York has not adopted UETA. Both states have existing laws recognizing electronic signatures. The Uniform Law Commission (ULC) is a nonprofit formed in 1892 to create nonpartisan state legislation. Over 350 volunteer commissioners – lawyers, judges, law professors, legislative staff, and others – work together to draft laws where uniformity of state law is desirable.

www.brodeconsulting.com Page 12

Record Retention

The E-Sign Act requires a financial institution to maintain electronic records accurately reflecting the information contained in applicable contracts, notices or disclosures and that they remain accessible to all persons who are legally entitled to access for the period required by law in a form that is capable of being accurately reproduced for later reference.

You will satisfy the requirement to provide electronic disclosures in a form that the consumer can retain if the disclosures are provided in a standard electronic format that can be downloaded and saved or printed on a typical home personal computer.

What Examiners Will Be Looking For

Determine if and to what extent your institution electronically delivers compliance-related notices or disclosures subject to the consumer consent provisions of the E-Sign Act.

Determine if your institution has established procedures to ensure compliance with the provisions of the Act.

Determine that the consumer, prior to consenting, is provided appropriate notice with each of the requirements outlined above.

Determine that the consumer provides affirmative consent electronically, or confirms their consent electronically, in a manner that reasonably demonstrates they can access the electronic records (statements, disclosures, notices) subject to the consent.

If your institution made changes to the hardware or software requirements needed to access or retain the electronic records, examiners will verify you provided the consumer with a statement of the changes as detailed above, and obtained a new affirmative consent.

Determine if your institution maintains a single “authoritative” copy of any transferable record relating to a loan secured by real property. This record shall be “unique”, “identifiable”, and “unalterable.” (Examples include, deeds, titles, and mortgages)

www.brodeconsulting.com Page 13

Determine whether your institution maintains electronic records accurately reflecting the information contained in applicable contracts, notices, or disclosures and that they remain accessible to all persons who are legally entitled to access for the period required by law in a form that is capable of being accurately reproduced for later reference.

We have provided a sample E-Sign Compliance Exam Checklist in your Toolkit you may utilize in reviewing and auditing your policies and procedures.

Consequences of Non-Compliance

As we stated earlier, there is no provision in the Act for fines or penalties. However, if documents are not provided through a process which satisfies the requirement for the document to be delivered in writing, then the document will be deemed never to have been provided. Fines and penalties could then be assessed under the specific act or regulation which required the delivery of the document. In the case of Regulation Z, if the CD or Right of Rescission was not properly delivered, the rescission period remains open for three years!

E-Sign Act Exceptions (7003)

The provisions of Section 7001 shall not apply to a contract or other record to the extent it is governed by-

1) A statute, regulation, or other rule of law governing the creation and execution of wills, codicils, or testamentary trust;

2) State statute, regulation, or other rule of law governing adoption, divorce, or other matters of family law; or

3) The Uniform Commercial Code, as in effect in any State, other than sections 1-107 and 1-206 and Articles 2 and 2A.

Additional exceptions:

1) Court orders or notices, or official court documents (including briefs, pleadings, and other writings) required to be executed in connection with court proceedings;

2) Any notice of-

www.brodeconsulting.com Page 14

a. The cancellation or termination of utility services (including water, heat, and power);

b. Default, acceleration, repossession, foreclosure, or eviction, or the right to cure, under a credit agreement secured by, or a rental agreement for, a primary residence of an individual;

c. The cancellation or termination of health insurance or benefits or life insurance benefits (excluding annuities); or

d. Recall of a product or material failure of a product, that risks endangering health or safety; or

3) Any document required to accompany any transportation or handling of hazardous materials, pesticides, or other toxic or dangerous materials.

Financial institutions should review applicable state law for any additional restrictions.

Best Practices

E-Sign violations most often result from changes to a financial institution’s electronic products, services and delivery. How can you avoid these errors?

• Involve compliance personnel when relying on electronic delivery of products and services.

• Establish a regular audit or review that independently identifies institution products and services (e.g., deposit accounts), activities and information consumers can access electronically.

• Focus on how changes in vendors or other third parties

affect E-Sign compliance. Vendors often assist institutions in complying with the act.

• Complete the Six-Step Consumer Consent Process:

1. Availability of Paper Delivery or Paper Copies 2. Consent Choices 3. Consumer Actions 4. Hardware/Software Requirements 5. Affirmatively Consent 6. After Consent Disclosure

www.brodeconsulting.com Page 15

TOOLKIT

ELECTRONIC NOTICE CHECKLIST

Disclosure Item Yes No

Prior Consent, Notice of Availability of Paper Records

1. Consumer right/option to have records provided in paper/non-electronic form

2. Right to withdraw consent, including any conditions and fees

3. Whether consent applies to the particular transaction or to identified categories of records that may be provided during the course of the consumer’s relationship with the institution.

4. Procedures the consumer must use to withdraw consent.

5. Procedures the consumer must use to update the information needed to contact the consumer electronically.

6. Information on how the consumer may request a paper copy of their statement/disclosures and if any additional fees apply.

Hardware & Software Requirements; Notices of Changes

7. Statement of the hardware and software requirements for access to and retention of electronic records.

8. Consumer electronic confirmation of consent reasonably demonstrates the consumer can access information in the electronic form that will be used to provide the information

9. TIMING: If the consumer opened an account or enrolled for a service electronically, the disclosures were provided before the account was opened or service was requested.

10. Disclosures are maintained on the institution’s website for a “reasonable amount of time” for consumers to access, view and retain the disclosures.

Post-Consent Changes by the Institution

11. Have any changes to the hardware/software requirements to access electronic statements and/or disclosures occurred in the last twelve (12) months? If yes, continue below.

a. Was the consumer provided a statement of the revised requirements?

b. Was the consumer given the right to withdraw consent without the imposition of fees or consequences?

c. Did the consumer provide a new affirmative consent?

www.brodeconsulting.com Page 16

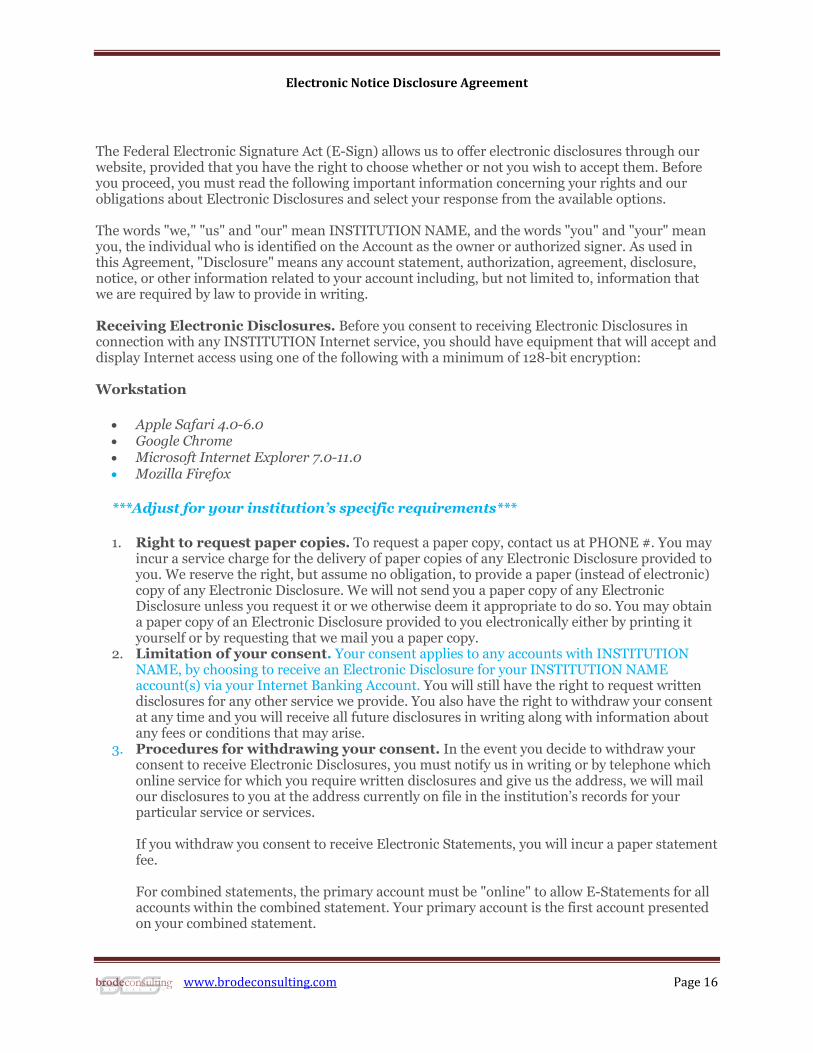

Electronic Notice Disclosure Agreement

The Federal Electronic Signature Act (E-Sign) allows us to offer electronic disclosures through our website, provided that you have the right to choose whether or not you wish to accept them. Before you proceed, you must read the following important information concerning your rights and our obligations about Electronic Disclosures and select your response from the available options. The words "we," "us" and "our" mean INSTITUTION NAME, and the words "you" and "your" mean you, the individual who is identified on the Account as the owner or authorized signer. As used in this Agreement, "Disclosure" means any account statement, authorization, agreement, disclosure, notice, or other information related to your account including, but not limited to, information that we are required by law to provide in writing. Receiving Electronic Disclosures. Before you consent to receiving Electronic Disclosures in connection with any INSTITUTION Internet service, you should have equipment that will accept and display Internet access using one of the following with a minimum of 128-bit encryption: Workstation

• Apple Safari 4.0-6.0 • Google Chrome • Microsoft Internet Explorer 7.0-11.0 • Mozilla Firefox

***Adjust for your institution’s specific requirements***

1. Right to request paper copies. To request a paper copy, contact us at PHONE #. You may incur a service charge for the delivery of paper copies of any Electronic Disclosure provided to you. We reserve the right, but assume no obligation, to provide a paper (instead of electronic) copy of any Electronic Disclosure. We will not send you a paper copy of any Electronic Disclosure unless you request it or we otherwise deem it appropriate to do so. You may obtain a paper copy of an Electronic Disclosure provided to you electronically either by printing it yourself or by requesting that we mail you a paper copy.

2. Limitation of your consent. Your consent applies to any accounts with INSTITUTION NAME, by choosing to receive an Electronic Disclosure for your INSTITUTION NAME account(s) via your Internet Banking Account. You will still have the right to request written disclosures for any other service we provide. You also have the right to withdraw your consent at any time and you will receive all future disclosures in writing along with information about any fees or conditions that may arise.

3. Procedures for withdrawing your consent. In the event you decide to withdraw your consent to receive Electronic Disclosures, you must notify us in writing or by telephone which online service for which you require written disclosures and give us the address, we will mail our disclosures to you at the address currently on file in the institution’s records for your particular service or services. If you withdraw you consent to receive Electronic Statements, you will incur a paper statement fee. For combined statements, the primary account must be "online" to allow E-Statements for all accounts within the combined statement. Your primary account is the first account presented on your combined statement.

www.brodeconsulting.com Page 17

We may treat an invalid email address or the subsequent malfunction of a previously valid address as a withdrawal of your consent to receive Electronic Disclosures. We will not charge you a fee to process the withdrawal of your consent. If you withdraw your consent to receive Electronic Disclosures, the withdrawal will become effective after your request is processed. How to contact us. If you decide to withdraw your consent to receive Electronic Disclosures, or wish to update personal information including your email address, or if you would like to receive a printed copy of any disclosure, contact us at: INSTITUTION NAME AND ADDRESS

4. Affirmative consent. By proceeding to the following message, you acknowledge that you are able to read and retain all of the disclosures available on this site. You also confirm that you have carefully reviewed this Electronic Disclosure Agreement. By clicking "I Agree" or "I Do Not Agree" below , you are agreeing to the following:

• Indicating that you agree to receive electronic disclosures. • Indicating that you do not wish to accept electronic disclosures.

5. Enrollment. Enrolling for Electronic Disclosures will allow you to receive your institution statement through the convenience and security of Internet Banking. You will receive a notice by email when your Electronic Disclosure is available to retrieve. To be eligible to receive Electronic Disclosures, you must:

• Have an Access ID and Password for Internet Banking • Agree that you will no longer receive a paper copy of your statement delivered through

the U.S. Mail. • Notify the institution if your email address changes.

Cancellation. You have the right to cancel this Electronic Disclosure Enrollment at any time by notifying the institution in person, via telephone at PHONE NUMBER or mail at INSTITUTION NAME, ADDRESS.

Click one of the following options:

I Agree to accept the E-Statement disclosures online. I would like to sign up for E-Statement now.

I Do Not Agree to accept the E-Statement disclosures online. I would like to request that written

disclosures be sent to me.

I Agree Cancel

www.brodeconsulting.com Page 18

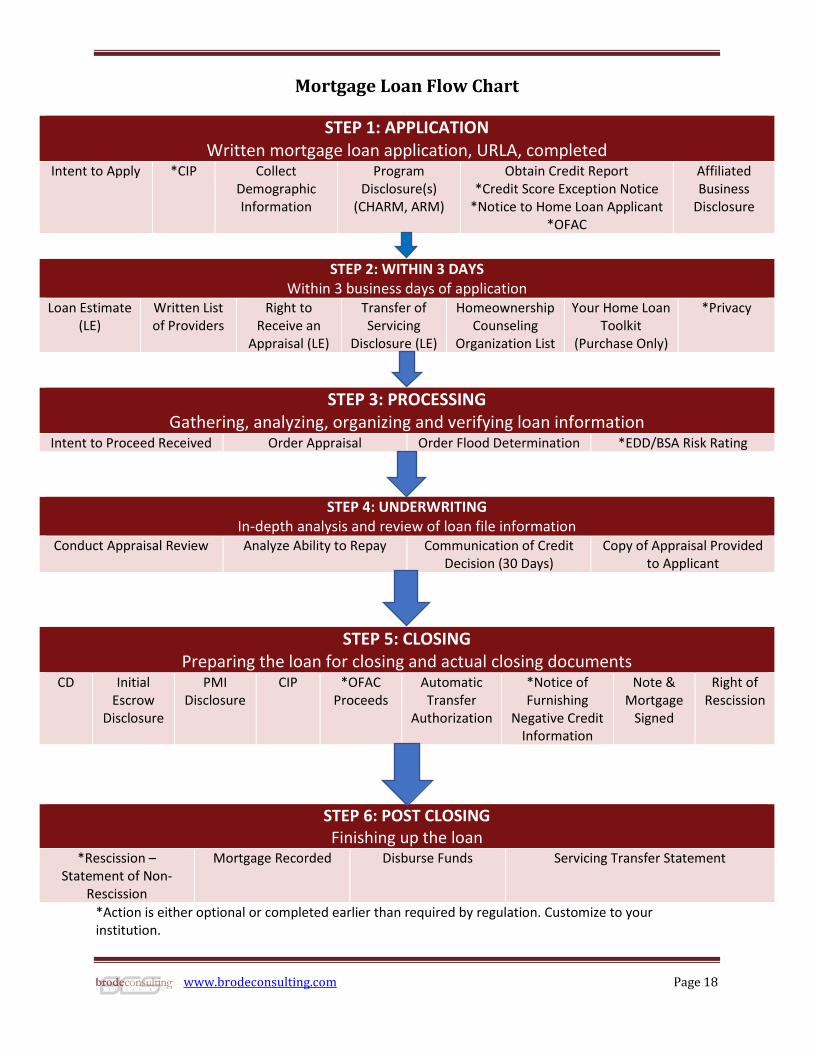

Mortgage Loan Flow Chart

STEP 1: APPLICATION Written mortgage loan application, URLA, completed

Intent to Apply *CIP Collect Demographic Information

Program Disclosure(s)

(CHARM, ARM)

Obtain Credit Report *Credit Score Exception Notice

*Notice to Home Loan Applicant *OFAC

Affiliated Business

Disclosure

STEP 2: WITHIN 3 DAYS Within 3 business days of application

Loan Estimate (LE)

Written List of Providers

Right to Receive an

Appraisal (LE)

Transfer of Servicing

Disclosure (LE)

Homeownership Counseling

Organization List

Your Home Loan Toolkit

(Purchase Only)

*Privacy

STEP 3: PROCESSING Gathering, analyzing, organizing and verifying loan information

Intent to Proceed Received Order Appraisal Order Flood Determination *EDD/BSA Risk Rating

STEP 4: UNDERWRITING In-depth analysis and review of loan file information

Conduct Appraisal Review Analyze Ability to Repay Communication of Credit Decision (30 Days)

Copy of Appraisal Provided to Applicant

STEP 5: CLOSING Preparing the loan for closing and actual closing documents

CD Initial Escrow

Disclosure

PMI Disclosure

CIP *OFAC Proceeds

Automatic Transfer

Authorization

*Notice of Furnishing

Negative Credit Information

Note & Mortgage

Signed

Right of Rescission

STEP 6: POST CLOSING Finishing up the loan

*Rescission – Statement of Non-

Rescission

Mortgage Recorded Disburse Funds Servicing Transfer Statement

*Action is either optional or completed earlier than required by regulation. Customize to your institution.

www.brodeconsulting.com Page 19

Resources

• E-Sign Act: 15 U.S.C. §7001 et seq.

• Federal Reserve, Board Announces Amendments to Five Regulations to Clarify Requirements

for Providing Consumer Disclosure in Electronic Form, November 1, 2007. https://www.federalreserve.gov/newsevents/pressreleases/bcreg20071101a.htm

• Federal Reserve System: Consumer Affairs Electronic Banking Examination Checklist

https://www.federalreserve.gov/boarddocs/caletters/2003/0310/caltr0310.htm

• Federal Reserve System: Consumer Compliance Outlook, Moving from Paper to Electronics: Consumer Compliance Under the E-Sign Act. Jeffrey Paul and Gary Louis. Fourth Quarter 2009. https://consumercomplianceoutlook.org/2009/fourth-quarter/q4_02/

• Federal Reserve System: Consumer Compliance Outlook, Compliance Spotlight: E-Sign Act

and the COVID-19 Pandemic. Second Issue 2020. https://consumercomplianceoutlook.org/2020/second-issue/compliance-spotlight-e-sign-act-and-the-covid-19-pandemic/

• Uniform Electronic Transactions Act (UETA):

https://www.uniformlaws.org/committees/community-home?CommunityKey=2c04b76c-2b7d-4399-977e-d5876ba7e034

www.brodeconsulting.com Page 20

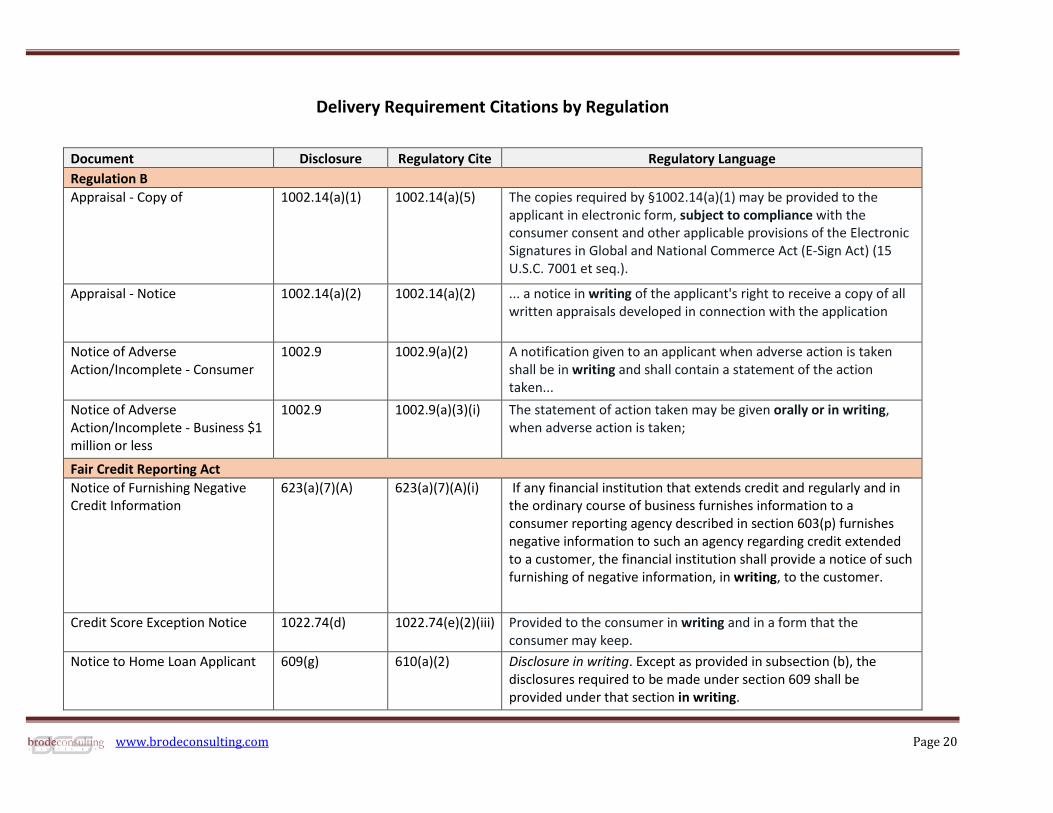

Delivery Requirement Citations by Regulation

Document Disclosure Regulatory Cite Regulatory Language Regulation B Appraisal - Copy of 1002.14(a)(1) 1002.14(a)(5) The copies required by §1002.14(a)(1) may be provided to the

applicant in electronic form, subject to compliance with the consumer consent and other applicable provisions of the Electronic Signatures in Global and National Commerce Act (E-Sign Act) (15 U.S.C. 7001 et seq.).

Appraisal - Notice 1002.14(a)(2) 1002.14(a)(2) ... a notice in writing of the applicant's right to receive a copy of all written appraisals developed in connection with the application

Notice of Adverse Action/Incomplete - Consumer

1002.9 1002.9(a)(2) A notification given to an applicant when adverse action is taken shall be in writing and shall contain a statement of the action taken...

Notice of Adverse Action/Incomplete - Business $1 million or less

1002.9 1002.9(a)(3)(i) The statement of action taken may be given orally or in writing, when adverse action is taken;

Fair Credit Reporting Act Notice of Furnishing Negative Credit Information

623(a)(7)(A) 623(a)(7)(A)(i) If any financial institution that extends credit and regularly and in the ordinary course of business furnishes information to a consumer reporting agency described in section 603(p) furnishes negative information to such an agency regarding credit extended to a customer, the financial institution shall provide a notice of such furnishing of negative information, in writing, to the customer.

Credit Score Exception Notice 1022.74(d) 1022.74(e)(2)(iii) Provided to the consumer in writing and in a form that the consumer may keep.

Notice to Home Loan Applicant 609(g) 610(a)(2) Disclosure in writing. Except as provided in subsection (b), the disclosures required to be made under section 609 shall be provided under that section in writing.

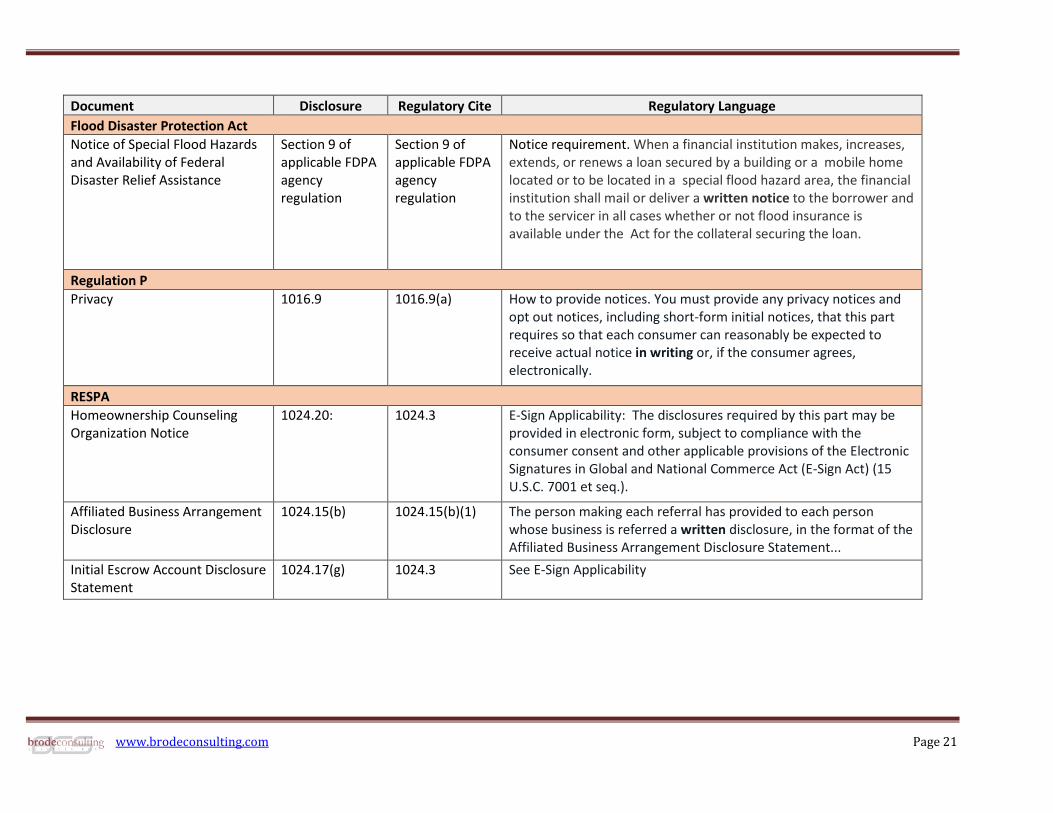

www.brodeconsulting.com Page 21

Document Disclosure Regulatory Cite Regulatory Language Flood Disaster Protection Act Notice of Special Flood Hazards and Availability of Federal Disaster Relief Assistance

Section 9 of applicable FDPA agency regulation

Section 9 of applicable FDPA agency regulation

Notice requirement. When a financial institution makes, increases, extends, or renews a loan secured by a building or a mobile home located or to be located in a special flood hazard area, the financial institution shall mail or deliver a written notice to the borrower and to the servicer in all cases whether or not flood insurance is available under the Act for the collateral securing the loan.

Regulation P Privacy 1016.9 1016.9(a) How to provide notices. You must provide any privacy notices and

opt out notices, including short-form initial notices, that this part requires so that each consumer can reasonably be expected to receive actual notice in writing or, if the consumer agrees, electronically.

RESPA Homeownership Counseling Organization Notice

1024.20: 1024.3 E-Sign Applicability: The disclosures required by this part may be provided in electronic form, subject to compliance with the consumer consent and other applicable provisions of the Electronic Signatures in Global and National Commerce Act (E-Sign Act) (15 U.S.C. 7001 et seq.).

Affiliated Business Arrangement Disclosure

1024.15(b) 1024.15(b)(1) The person making each referral has provided to each person whose business is referred a written disclosure, in the format of the Affiliated Business Arrangement Disclosure Statement...

Initial Escrow Account Disclosure Statement

1024.17(g) 1024.3 See E-Sign Applicability

www.brodeconsulting.com Page 22

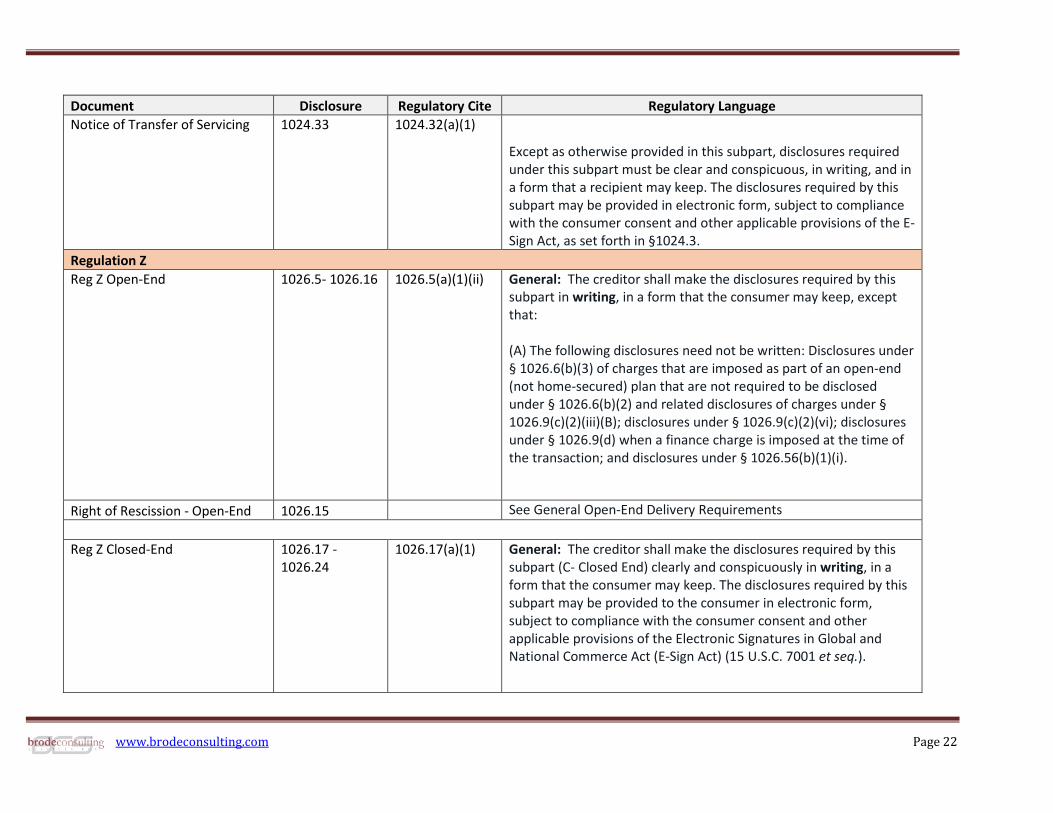

Document Disclosure Regulatory Cite Regulatory Language Notice of Transfer of Servicing 1024.33 1024.32(a)(1)

Except as otherwise provided in this subpart, disclosures required under this subpart must be clear and conspicuous, in writing, and in a form that a recipient may keep. The disclosures required by this subpart may be provided in electronic form, subject to compliance with the consumer consent and other applicable provisions of the E-Sign Act, as set forth in §1024.3.

Regulation Z Reg Z Open-End 1026.5- 1026.16 1026.5(a)(1)(ii) General: The creditor shall make the disclosures required by this

subpart in writing, in a form that the consumer may keep, except that: (A) The following disclosures need not be written: Disclosures under § 1026.6(b)(3) of charges that are imposed as part of an open-end (not home-secured) plan that are not required to be disclosed under § 1026.6(b)(2) and related disclosures of charges under § 1026.9(c)(2)(iii)(B); disclosures under § 1026.9(c)(2)(vi); disclosures under § 1026.9(d) when a finance charge is imposed at the time of the transaction; and disclosures under § 1026.56(b)(1)(i).

Right of Rescission - Open-End 1026.15 See General Open-End Delivery Requirements

Reg Z Closed-End 1026.17 - 1026.24

1026.17(a)(1) General: The creditor shall make the disclosures required by this subpart (C- Closed End) clearly and conspicuously in writing, in a form that the consumer may keep. The disclosures required by this subpart may be provided to the consumer in electronic form, subject to compliance with the consumer consent and other applicable provisions of the Electronic Signatures in Global and National Commerce Act (E-Sign Act) (15 U.S.C. 7001 et seq.).

www.brodeconsulting.com Page 23

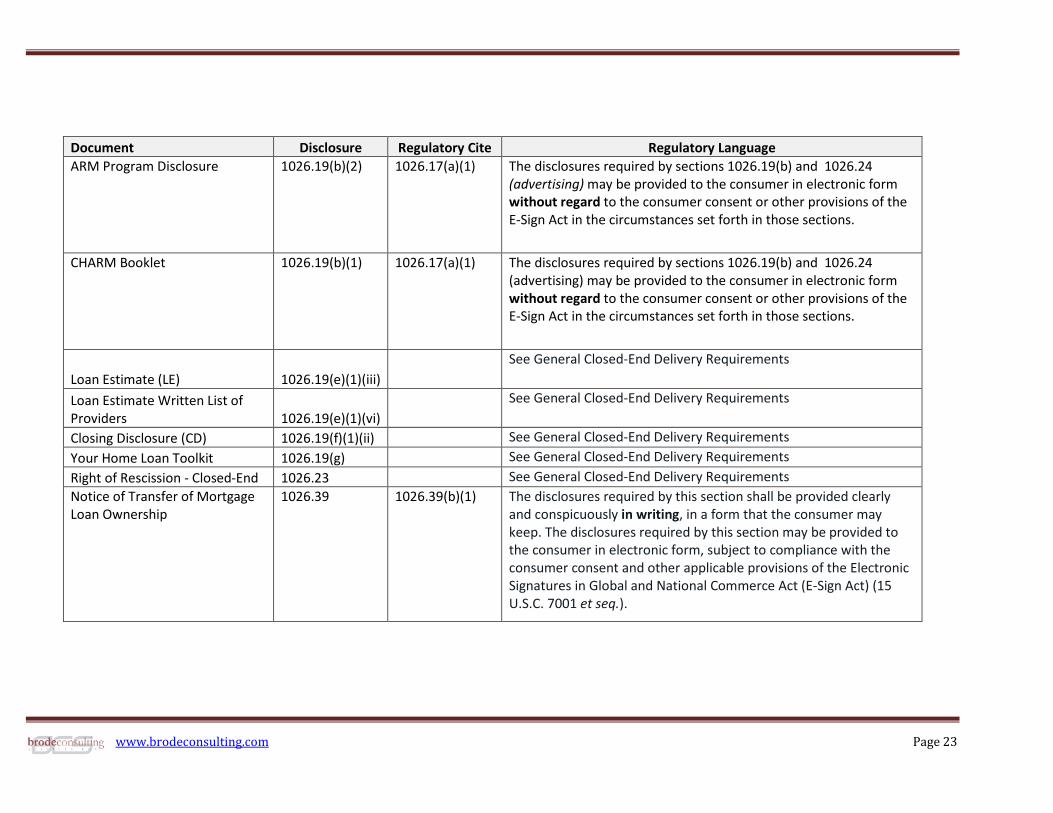

Document Disclosure Regulatory Cite Regulatory Language ARM Program Disclosure 1026.19(b)(2) 1026.17(a)(1) The disclosures required by sections 1026.19(b) and 1026.24

(advertising) may be provided to the consumer in electronic form without regard to the consumer consent or other provisions of the E-Sign Act in the circumstances set forth in those sections.

CHARM Booklet 1026.19(b)(1) 1026.17(a)(1) The disclosures required by sections 1026.19(b) and 1026.24 (advertising) may be provided to the consumer in electronic form without regard to the consumer consent or other provisions of the E-Sign Act in the circumstances set forth in those sections.

Loan Estimate (LE) 1026.19(e)(1)(iii) See General Closed-End Delivery Requirements

Loan Estimate Written List of Providers 1026.19(e)(1)(vi)

See General Closed-End Delivery Requirements

Closing Disclosure (CD) 1026.19(f)(1)(ii) See General Closed-End Delivery Requirements Your Home Loan Toolkit 1026.19(g) See General Closed-End Delivery Requirements Right of Rescission - Closed-End 1026.23 See General Closed-End Delivery Requirements Notice of Transfer of Mortgage Loan Ownership

1026.39 1026.39(b)(1) The disclosures required by this section shall be provided clearly and conspicuously in writing, in a form that the consumer may keep. The disclosures required by this section may be provided to the consumer in electronic form, subject to compliance with the consumer consent and other applicable provisions of the Electronic Signatures in Global and National Commerce Act (E-Sign Act) (15 U.S.C. 7001 et seq.).

www.brodeconsulting.com Page 24

Document Disclosure Regulatory Cite Regulatory Language Periodic Statement - Delinquency Information

1026.41 1026.41(c) The servicer must make the disclosures required by this section clearly and conspicuously in writing, or electronically if the consumer agrees, and in a form that the consumer may keep.

IRS IRS Form 1098 - Mortgage Interest Statement

IRS. General Instructions for Certain Informational Returns(2021), Section M. If you are required to furnish a written statement (Copy B or an acceptable substitute) to a recipient, then you may generally furnish the statement electronically instead of on paper, but only if you meet the requirements discussed later in this section.