eaton residences to defy market forces - amazon s3s3-ap-southeast-1.amazonaws.com/...see our cover...

TRANSCRIPT

Market InsightsInvestors look beyond

core assetsEP4

Property PicksGood deals to be had in

the northeast regionEP6&7

OffshoreIs Yangon’s market ready

for retail investors?EP12

Done Deals TwentyOne Angullia Park

unit sold for $2,995 psfEP14&15

A PULLOUT WITH

MCI (P) 043/03/2016 PPS 1519/09/2012 (022805)

Visit TheEdgeProperty.com to find properties, research market trends and read the latest news THE WEEK OF NOVEMBER 28, 2016 | ISSUE 756

M A K E B E T T E R D E C I S I O N S

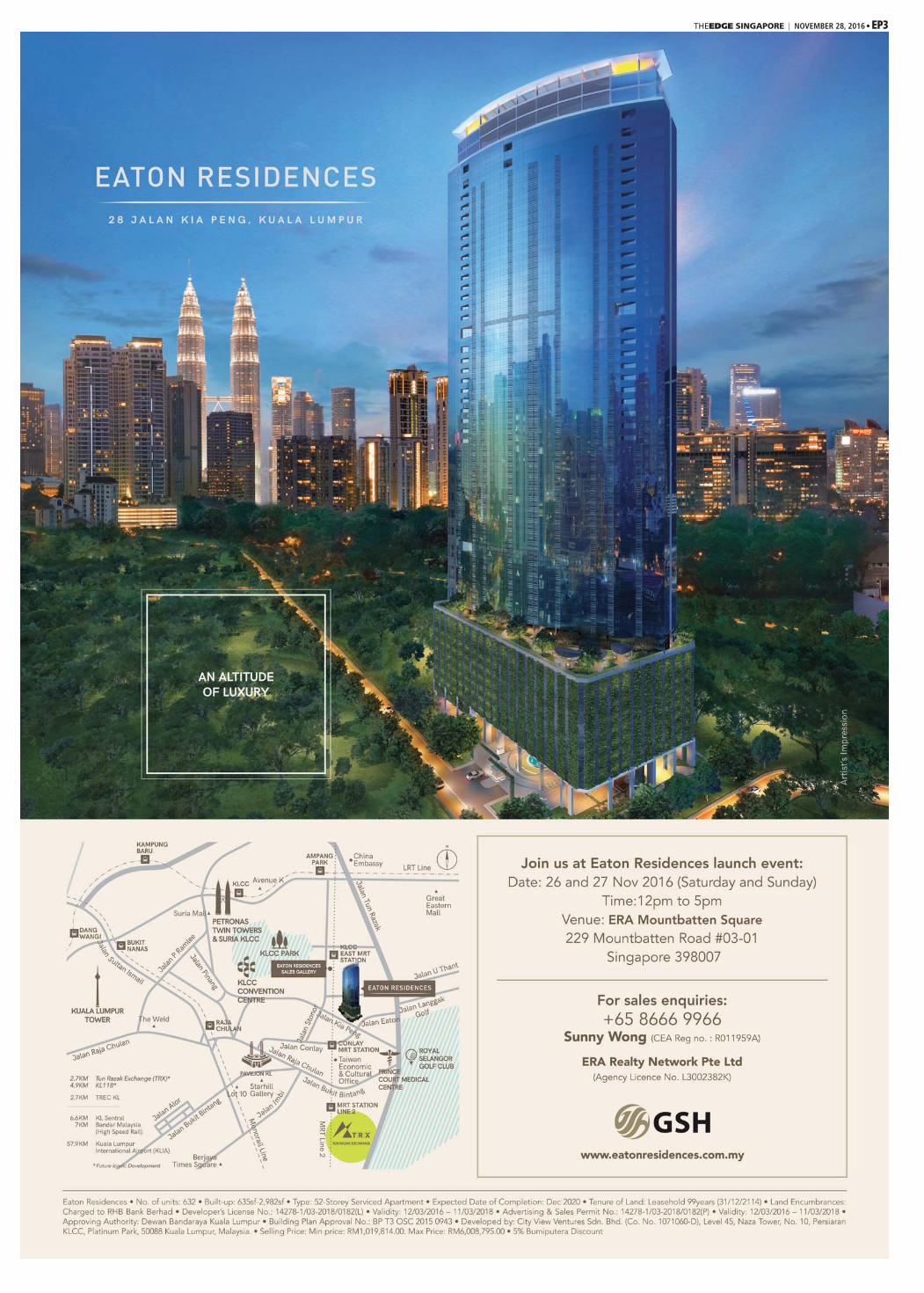

Eaton Residences to defy market forces

The sinking Malaysian ringgit is certainly a boon to holidaymakers, but investors are wondering whether it is time to enter the property market. GSH Corp believes the

quality of its project, prime location in KLCC and skyline views will help it overcome the challenges.

See our Cover Story on Pages 8 and 9.

KEN

NY

YAP/

THE

EDG

E M

ALAY

SIA

EP2 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

HDB launches 10,118 BTO flats for saleHDB has launched 10,118 flats for sale

under its November 2016 Build-To-Order

(BTO) and Sale of Balance Flats (SBF)

exercise. This will be its largest joint

BTO-SBF exercise this year, comprising

5,110 BTO units and 5,008 SBF units

across 25 towns or estates.

This latest launch brings the total BTO

supply in 2016 to 17,891 units. Together

with the 10,178 balance flats offered in the

May and November SBF exercises, a total

of 28,069 flats were launched in 2016, to

meet Singaporeans’ housing needs.

The BTO flats on offer are distrib-

uted across nine projects. Three are in

the non-mature town of Punggol and

the other six are in the mature towns/

estates of Bedok, Bidadari (Toa Payoh)

and Kallang/Whampoa.

Sale of balance flats will be in 11

non-mature towns and 14 mature towns/

estates under the November 2016 SBF ex-

ercise. Applications for the flats launched

in the November 2016 BTO and SBF ex-

ercise can be submitted online on the

HDB InfoWEB from Nov 22 to 28.

HDB says it will offer about 4,100

flats in Clementi, Punggol, Tampines

and Woodlands under the February 2017

BTO exercise.

Stanhope releases new units at TV Centre to Singapore buyersUK developer Stanhope has released

20 park-facing two- and three-bedroom

units at Television Centre (above, cen-

tre) for sale to Singaporeans. Accord-

ing to Stanhope’s sales and marketing

director Peter Allen, these new units

are priced from £1 million ($1.77 mil-

lion) for a 900 sq ft two-bedroom unit,

and from £1.5 million for a 1,400 sq ft

three-bedroom unit.

“We are releasing these new west-

facing Crescent apartments for the first

time,” says Allen.

This new apartment building forms a

crescent around the inner Helios build-

ing and has views of Hammersmith Park

and Japanese Garden.

“The new units are priced 10% high-

er than non-park-facing units. On the

whole, we have not raised prices from

a year ago,” adds Allen.

According to Stanhope, they have

sold 250 units to 25 nationalities from

around the world. Of the 250 units, 14

one- and two-bedroom units were bought

by Singaporean buyers.

The scheme is also planned to in-

clude cafés and restaurants, an inde-

pendent cinema, 400,000 sq ft of pre-

mium office space and a new outpost

of private members’ club Soho House,

complete with a 47-room hotel.

The first phase of the project — cost-

ing around £795 million — comprises

432 homes due for completion in 2018,

with prices ranging from £700,000 for

a one-bedroom apartment to £7 mil-

lion for a penthouse. Stanhope says 250

units will be ready by December 2017,

with the remaining units to be complet-

ed over the first three quarters of 2018.

Apartments at Television Centre were

designed by Stirling Prize-winning AHMM

Architects, with interiors by London de-

signer Suzy Hoodless. BBC Worldwide,

which relocated to new headquarters in

April 2015, retains space at the scheme,

with three TV studios, including the fa-

mous Studio 1, set to reopen in early 2017.

Greenland Group launches Spire London apartments for saleChinese developer Greenland Group will

be launching its latest development Spire

London (above, right) in London Docklands

for sale in Singapore on Nov 26 and 27.

Spire London is a 67-storey residen-

tial tower with a gross development value

of more than £800 million. The 999-year

leasehold development is also the tall-

est in the UK and Western Europe, with

concierge, retailing, residents’ gardens

and five-star lifestyle amenities, includ-

ing a Spa and Club Bar on the 35th floor.

The tower will provide 861 apart-

ments, of which 765 are for private sale.

The apartments are located on the eighth

to 66th floors of the tower and measure

538 sq ft for a one-bedroom apartment

to 1,615 sq ft for a three-bedroom du-

plex. The units are priced from £685,000.

Located in Hertsmere Road, adjacent

to Canary Wharf and directly fronting 30

acres of waterfront in West India Quay,

Spire London is designed by architects

Larry Malcic and Christopher Colosimo of

multi-award-winning architectural prac-

tice HoK, as well as leading interior de-

signer Nicola Fontanella of Argent Design.

JLL has been appointed the sole mar-

keting agent for Spire London. — Com-

piled by Michael Lim

EDITORIALEDITOR | Ben PaulTHE EDGE PROPERTY

SECTION EDITOR | Cecilia ChowHEAD OF RESEARCH | Feily Sofi anDEPUTY SECTION EDITOR |Michael LimSENIOR ANALYSTS | Esther Hoon, Lin ZhiqinANALYST | Tan Chee Yuen

COPY-EDITING DESK | Elaine Lim, Evelyn Tung, Chew Ru Ju, Tan Gim Ean,Geraldine TanPHOTO EDITOR | Samuel Isaac ChuaPHOTOGRAPHER | Albert ChuaEDITORIAL COORDINATOR | Rahayu MohamadDESIGN DESK | Tan Siew Ching, Christine Ong, Monica Lim, Mohd Yusry, Tun Mohd Zafi an Mohd Za’abah

ADVERTISING + MARKETING ADVERTISING SALES

DIRECTOR, ADVERTISING & SALES | Cowie TanASSOCIATE ACCOUNT DIRECTOR | Diana LimACCOUNT MANAGERS | Priscilla Wong, James Chua

THE EDGE SINGAPORE

ADVERTISING + MARKETING

ADVERTISING SALES

CHIEF MARKETING OFFICER |Cecilia KaySENIOR MANAGER | Windy Tan, Garry LoMANAGER | Elaine TanEVENTS

SENIOR MANAGER | Sivam KumarMARKETING

EXECUTIVES | Tim Jacobs, Sam Ridzam

COORDINATOR | Nor Aisah Bte Asmain

CIRCULATIONBUSINESS DEVELOPMENT DIRECTOR | Victor TheASSISTANT MANAGER | Sandrine GerberEXECUTIVES | Malliga Muthusamy, Ashikin Kader

CORPORATE CHIEF EXECUTIVE OFFICER | Ben PaulDIRECTOR | Anne Tong CORPORATE AFFAIRS DIRECTOR | Ng Say Guan

PUBLISHERThe Edge Publishing Pte Ltd150 Cecil Street #08-01Singapore 069543Tel: (65) 6232 8622Fax: (65) 6232 8620

PRINTERKHL Printing Co Pte Ltd57 Loyang DriveSingapore 508968Tel: (65) 6543 2222Fax: (65) 6545 3333

We welcome your commentsand criticism: [email protected]

Pseudonyms are allowed but please state your full name, address and contact number for us to verify.

PROPERTY BRIEFS

| BY OLIVIA ZALESKI & LULU YILUN CHEN |

Airbnb is in talks to acquire China’s

Xiaozhu.com to expand in the nation’s

home rental sharing market, according

to a person familiar with the matter.

The companies have held multiple meet-

ings and the discussions are advanced in na-

ture, the person says, asking not to be identi-

fied, as the talks are private. A deal is likely,

the person adds.

While Airbnb is the biggest platform for

people to rent their homes to travellers global-

ly, it is grappling with more established local

rivals Xiaozhu and Tujia.com in China. The

San Francisco-based company already has

about 75,000 properties listed in the world’s

most populous nation and plans to increase

staffing 10-fold to 300 full-time workers.

Airbnb and Xiaozhu declined to comment on wheth-

er the companies were in talks about a deal.

China’s online holiday rental market could reach

RMB10.3 billion ($2.1 billion) in transaction volume by

2017, up from an estimated RMB6.78 billion this year,

according to IResearch. Before the deal surfaced, the

US start-up had been anticipating two million “room

nights” in China, the person says. The company had

also recently inked a partnership agreement with Ten-

cent Holdings, whose messaging service WeChat has

more than 800 million active monthly users and pro-

vided 60% to 70% of Airbnb China’s logins.

Xiaozhu would give Airbnb an instant boost in the

world’s second-largest economy. The Chinese start-

up, which was founded in 2012, this month said

it raised US$65 million ($92.8 million) in new

funding. The company says it has 10 million

active users and more than 100,000 listings in

301 cities across the country. CEO Kelvin Chen

Chi said at the time of the funding announce-

ment that Xiaozhu expected to deliver 500%

organic growth in 2016.

A deal for Xiaozhu would also help Airbnb

reduce the risk of a costly battle for market share.

Uber Technologies lost more than US$1 billion

in China in a battle with Didi Chuxing before

selling its business in the country to its rival.

In September, Airbnb said it raised US$555.5

million in new funds as it expands around the

world. The funding round, which valued the

company at US$30 billion, could eventually reach

US$850 million, a person familiar with the mat-

ter said at the time.

Tujia was valued at more than US$1 billion

after a US$300 million funding round last year from

investors including All-Stars Investment. The compa-

ny is also backed by HomeAway, Ctrip.com Interna-

tional, LightSpeed Venture Partners and GGV Capital.

The company says it has listings for 450,000 homes in

total, including 335 destinations in China and 1,018

overseas. — Bloomberg LP

Airbnb in talks to buy China rival Xiaozhu

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

STAN

HOPE

GRE

ENLA

ND

GRO

UP

E

E

Airbnb is in talks to acquire China’s Xiaozhu.com to expand in the nation’s home rental sharing market

BLO

OM

BERG

Singapore 77 Bencoolen St | Kuala Lumpur Level 3 The Intermark Jalan Tun Razak | Sydney, Melbourne, Brisbanespacefurniture.asia | Instagram @spacefurnitureasia

THEEDGE SINGAPORE | NOVEMBER 28, 2016 • EP3

EP4 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

MARKET INSIGHTS

Investors seek alternative to core assets | BY FEILY SOFIAN |

Real estate investors are considering

emerging markets for higher returns,

as they face a shortage of core assets

and increasingly compressed yields in

safe-haven cities. Two Indian cities,

Bangalore and Mumbai, took the top spots in

Asia-Pacific for investment prospects in 2017,

according to the latest annual survey by PwC

and the Urban Land Institute.

Singapore tumbled to 21st position from 11th

in the previous survey. John Fitzgerald, Chief

Executive of Urban Land Institute, Asia-Pacif-

ic, describes the city-state as being in a per-

fect storm of a weak economy, excess supply

and declining demand. While office occupan-

cy rates have been hit by the downsizing of

the financial sector, another 4.05 million sq ft

of office space is expected to come onstream

next year, going by the latest statistics by URA.

The “Emerging Trends in Real Estate Asia

Pacific” survey polled about 600 industry lead-

ers on the outlook of real estate investment,

trends and other issues. A majority of respond-

ents are based in Singapore, Australia, China,

Hong Kong and Japan.

The survey found a dramatic turn in senti-

ment. Bangalore jumped to the first position,

up from 12th in the last survey. Domestic and

international companies are said to be flock-

ing to the city to open call-in and R&D centres,

driving demand for new spaces.

Mumbai rose to second position from 13th

in the last survey as major road and rail in-

frastructure programmes boosted investment

sentiments.

The swing in votes was also testament to

how fast economic conditions in several emerg-

ing markets have improved, the survey report

says. Manila, Ho Chi Minh City, Shenzhen,

Shanghai, Jakarta and Bangkok occupied the

third to eighth positions.

Tokyo and Sydney, which had been investors’

top picks in recent years, slipped to 12th and

ninth placing respectively. Residential assets

have remained popular, underpinned by high

occupancy rates and stable rental income. The

office market, on the other hand, is bracing for

a large supply in 2018. Investors might also be

jaded with the shortage of available assets as

owners choose to refinance their properties

rather than sell in the current negative inter-

est-rate environment.

The shift in investment preference towards

emerging markets may not necessarily translate

into a surge in transaction volume, according

to the report. These markets are said to lack

the critical mass of investable assets, and a

majority of investors do not have the connec-

tions, experience and risk appetite to exploit

the opportunities.

In addition, investors who continue to fa-

vour core assets have the option to develop one.

“Development has become more popular. One

way to get around the shortage of core prod-

ucts is simply to buy land and build one,” says

Fitzgerald. Development entails higher risks,

however, and core investors usually avoid the

option, he notes.

Recently, Malaysia’s IOI Properties Group

won a white site at Central Boulevard in Marina

Bay. The group had put in a bid of $2.57 bil-

lion, or $1,689 psf per plot ratio, 16% high-

er than the next highest bid. A total of seven

deve lopers contested for the site, including

Chinese developer Nanshan Group as well as

the Hongkong Land and Cheung Kong Prop-

erty Holdings partnership.

By property type, logistics facilities have

become the most favoured asset class among

institutional investors on the back of struc-

tural undersupply in the region, driven by the

boom in e-commerce, according to Fitzgerald.

Geographically, Shenzhen ranked first in

the industrial/distribution property sector. A

total of 83% of respondents recommended

buying and the rest advised holding. The on-

going infrastructure development in the Pearl

River Delta is expected to enhance transport

network and boost demand for these facilities.

Mumbai and Bangalore took second and

third spots, with 80% of respondents taking

a buy stance. India is said to be a chronical-

ly undersupplied market. Meanwhile, compa-

nies are expected to consolidate their opera-

tions from a single large warehouse with the

implementation of the goods and services tax.

This move will enhance efficiency and allow

e-commerce players to serve more locations.

Under the existing regime, tax rates vary across

regions and companies would operate from

multiple locations to save on taxes.

Bangalore also ranked top in the apartment

Investment prospects ranking

EMER

GIN

G T

REN

DS

IN R

EAL

ESTA

TE A

SIA

PA

CIF

IC S

URV

EY

2017 2016

Bangalore 1 12

Mumbai 2 13

Manila 3 8

Ho Chi Minh City 4 5

Shenzhen 5 18

Shanghai 6 9

Jakarta 7 6

Bangkok 8 19

Sydney 9 2

Guangzhou 10 20

Beijing 11 14

Tokyo 12 1

New Delhi 13 16

Auckland 14 10

Osaka 15 4

Melbourne 16 3

Seoul 17 7

Hong Kong 18 15

Kuala Lumpur 19 21

China – secondary cities 20 22

Singapore 21 11

Taipei 22 17

rental sector. One respondent commented that

the market was driven by the inflow of engi-

neers into India’s top IT destination. He cau-

tioned, however, that a potential oversupply

might hamper capital appreciation.

Ho Chi Minh City came in second. Local

purchasers are expected to dominate the mar-

ket, with smaller and affordable homes like-

ly to fare better than those in the higher-end

segment.

Emerging markets also topped the chart

for office properties. Manila and Bangalore

ranked highest on the back of robust demand

from business process outsourcing companies.

Yields in Bangalore are said to be around 9%.

In Manila, there is plenty of domestic capital

competing for these properties.

Separately, niche assets such as affordable

housing, senior housing and self-storage fea-

tured strongly among investors, in line with

their quest for higher returns.

CHAR

TS: E

MER

GIN

G T

REN

DS IN

REA

L ES

TATE

ASI

A PA

CIFI

C 20

17 S

URVE

Y

E

By property type, logistics facilities have become the most favoured asset class among institutionalinvestors driven by the boom in e-commerce

BLO

OM

BERG

Industrial/distribution properties

% of total

Taipei

New Delhi

Singapore

Auckland

Melbourne

Osaka

Kuala Lumpur

Bangkok

Sydney

Tokyo

Hong Kong

Manila

Shanghai

Seoul

Guangzhou

China – secondary cities

Ho Chi Minh City

Beijing

Jakarta

Bangalore

Mumbai

Shenzhen

0 100

83.3 16.7

80.0 20.0

80.0 20.0

76.9 23.1

75.0 4.2 20.8

71.4 28.6

66.7 33.3

66.7

63.6 9.1 27.3

57.1

39.1

38.2

33.3 66.7

55.6

54.5

29.4 11.8 58.8

54.8

33.3 66.7

100

Buy Hold Sell

20 40 60 80

17.4 43.5

44.117.6

14.3 28.6

51.913.534.6

25.819.4

16.716.7

13.6 31.8

33.3 11.1

20.0 80.0

37.03.759.3

Apartment rental properties

% of total

Guangzhou

Hong Kong

Melbourne

Beijing

Seoul

Singapore

Mumbai

Shanghai

New Delhi

China – secondary cities

Manila

Bangkok

Sydney

Osaka

Tokyo

Shenzhen

Jakarta

Ho Chi Minh City

Bangalore

Kuala Lumpur

Auckland

Taipei

100

71.4

54.5 18.2

50.0 25.0

35.0 10.0

33.3

33.3

28.6

27.3

25.0

23.1 7.7 69.2

20.0 60.0

18.8 53.1

14.3 14.3 71.4

13.6 13.6 72.7

8.3 45.8

5.6 66.7

50.0 50.0

33.3

25.0

10.0

Buy Hold Sell

0 10020 40 60

21.236.4

80

66.7

75.0

90.0

75.0

45.5

71.4

43.8

66.7

55.0

42.4

28.6

27.3

25.0

22.9

27.3

20.0

28.1

45.8

27.8

Office properties

% of totalBuy Hold Sell

Bangkok

Kuala Lumpur

China – secondary cities

Guangzhou

Taipei

Auckland

New Delhi

Singapore

Seoul

Hong Kong

Shenzhen

Tokyo

Beijing

Sydney

Osaka

Melbourne

Ho Chi Minh City

Shanghai

Bangalore

Jakarta

Mumbai

Manila 85.7 14.3

83.3 16.7

80.0 20.0

80.0 20.0

57.8 8.9

50.0 50.0

43.5

40.5

40.0

36.4

33.3 55.6

32.3 51.6

31.6 47.4

31.4 47.1

25.0 75.0

16.7 66.7

16.7 83.3

14.3 14.3 71.4

12.5 37.5

10.5 57.9

25.0 75.0

0 10020 40 60 80

36.020.044.0

43.2

40.0

37.8

39.1

33.3

17.4

21.6

20.0

20.5

11.1

16.1

21.1

21.6

16.7

50.0

31.6

THEEDGE SINGAPORE | NOVEMBER 28, 2016 • EP5

EP6 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

PROPERTY PICKS

Good deals to be had in the Northeast| BY MICHAEL LIM |

Homebuyers are spoilt for choice in the

northeast region of Upper Serangoon

Road and Buangkok Drive. If they are

not prepared to cough up more than

$1,200 psf at a new launch, however,

and want a unit they can move into immedi-

ately, there is a mix of private condominiums

and privatised executive condos (ECs) — those

that have crossed their 10th year of completion

— that are still available.

Those who want a value-for-money pur-

chase could look at the older privatised ECs

and even private condos in the area that are

priced at $600 to $770 psf. “These are real-

ly great buys,” says Alan Cheong, head of re-

search at Savills Singapore.

For instance, the oldest private condo in

the area is the 716-unit Rio Vista. The 99-

year leasehold condo, developed by MCL Land

and completed in 2004, comprises a mix of

two- to four-bedroom units measuring 1,367

to 1,851 sq ft.

This year, there were 12 resales in the pro-

ject and they averaged $760 psf. In the latest

transaction, a 1,378 sq ft, four-bedroom unit

on the third level was sold for $1.05 million

($762 psf) in October, according to a caveat

lodged with URA Realis.

The first EC in the area, The Florida, was

developed by City Developments. The 496-

unit development, completed in 2000 and pri-

vatised in 2010, has three- and four-bedroom

units sized from 1,216 to 2,034 sq ft.

This year, 12 units changed hands at The

Florida at an average price of $650 psf. Most

recently, a 1,302 sq ft, three-bedroom unit on

the fourth floor was sold for $780,000 ($599

psf). A 1,324 sq ft, three-bedroom unit on the

14th floor of another block changed hands for

$878,000 ($663 psf) in September, according

to caveats lodged.

“If you were to compare the oldest private

condo in the area, which is Rio Vista, and

the oldest privatised EC in the area, which

is The Florida, there is still a 15% price gap

based on recent transactions,” says Fred Teo,

executive head of business unit at KF Prop-

erty Network.

The Florida is not the only privatised EC

in the area: Park Green and The Rivervale are

The Florida is the first EC in the area and was developed by City Developments

The 716-unit Rio Vista is the oldest private condo in the area

Developed by NTUC Choice Homes, the 368-unit Park Green was completed in 2005 and privatised last year

PICT

URES

: SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

THEEDGE SINGAPORE | NOVEMBER 28, 2016 • EP7

PROPERTY PICKS

adjacent to each other on Rivervale Link. “Be-

tween the two, Park Green has proven to be

a better development in terms of design and

maintenance of the project,” says Teo.

Developed by NTUC Choice Homes, the

368-unit Park Green was completed in 2005

and privatised last year. The development

comprises five 17-storey blocks with predom-

inantly three- and four-bedroom units measur-

ing 1,162 to 1,926 sq ft. There are also three-

and four-bedroom maisonettes ranging from

1,937 to 2,163 sq ft.

This year, seven units at Park Green were

sold at an average of $722 psf. In the latest

transaction, a 1,356 sq ft, three-bedroom unit

fetched $980,000 ($723 psf) in July.

One street away from Park Green is The

Rivervale, an EC developed by CapitaLand

and completed in 2001 and privatised in 2011.

The 671-unit project comprises four 16-storey

blocks of three-bedroom units measuring

1,238 to 1,873 sq ft. There are also three- and

four-bedroom maisonettes measuring 2,691

to 2,723 sq ft.

So far this year, 20 units at The Rivervale

changed hands at an average price of $677 psf.

Most recently, a 1,313 sq ft, three-bedroom

unit on the fifth floor was sold for $905,000

($689 psf) in October, according to a cave-

at lodged then.

Adjacent to Park Green is a new EC, Austville

Residences developed by UE E&C. The 540-unit

EC project was completed in 2014. The latest

transaction was the resale of a 1,023 sq ft unit

that fetched $805,000 ($787 psf) in March 2016.

The unit was first sold for $709,000 ($693 psf)

in February 2012.

Two units changed hands at Austville Res-

idences. One was a 1,249 sq ft unit that was

sold for $825,000 ($661 psf) in August last

year. The seller had bought the unit during the

launch in May 2011 for $750,000 ($601 psf).

The other was a 1,023 sq ft unit on the

13th floor that was sold in April last year for

$834,000 ($815 psf). It also achieved the high-

est price psf for Austville Residences. When the

project was launched in 2011, the unit fetched

$758,000 ($741 psf).

Adjacent to Austville Residences is 99-year

leasehold private condo Riversound Residenc-

es. The 590-unit project, developed by Qingjian

Realty and completed in 2015, has six 18-sto-

rey blocks comprising 452 sq ft, one-bedroom

units to 1,421 sq ft, four-bedroom units.

Since Riversound Residences was completed

last year, about 10 units have changed hands

at an average of $998 psf. This month, a 1,066

sq ft, three-bedroom unit fetched $1.06 mil-

lion ($990 psf).

“Even when comparing a newly complet-

ed EC with a newly completed private condo

that are adjacent to each other, as in the case

of Austville Residences and Riversound, there

is a 20% price gap based on recent transacted

prices,” points out KF’s Teo.

Located across the river from Riversounds

is Riversails, a 928-unit private condo by All-

green Properties. The 99-year leasehold con-

do was completed in 2015 and comprises 12

blocks of 18 storeys each. It offers 505 sq ft,

one-bedroom units to 1,367 sq ft, four-bedroom

units. Penthouses measure 1,819 to 2,970 sq ft.

Of the total of 17 units sold this year, five

were developer sales and averaged $990 psf.

The most recent secondary market transactions

were that of a 506 sq ft, one-bedroom unit that

fetched $600,000 ($1,186 psf); and a 1,184 sq

ft, three-bedroom unit that was sold for $1.25

million ($1,056 psf) in October.

Rio Vista and The Florida — the oldest pri-

vate condo and oldest EC respectively — are

now joined by two new private condos. One

is the 493-unit Boathouse Residences, joint-

ly developed by Far East Organization, Frasers

Centrepoint and Sekisui House and complet-

ed last year.

The project has a mix of 624 sq ft, one-bed-

room units to 1,722 sq ft penthouses. Units at

Boathouse Residences have been trading at an

average of $1,021 psf, according to caveats lodged

this year. A 732 sq ft, two-bedroom unit was sold

for $780,000 ($1,066 psf) in August.

On Upper Serangoon View Road, across

the road from Boathouse Residences, stands

the 1,165-unit Kingsford Waterbay, a private

condo by Kingsford Development. The project

has nine 16-storey blocks fronting the Seran-

goon River. As at end-October, 546 units had

been sold at a median price of $1,204 psf, ac-

cording to URA data.

Kingsford Waterbay was unveiled last year,

the latest such launch in the area.

The Rivervale, an EC developed by CapitaLand, was completed in 2001 and privatised in 2011 Austville Residences is a 540-unit EC project developed by UE E&C and was completed in 2014

Riversound Residences is a 590-unit project, developed by Qingjian Realty and completed in 2015 The 1,165-unit Kingsford Waterbay was unveiled last year, the latest such launch in the area

Riversails is a 928-unit private condo by Allgreen PropertiesThe 493-unit Boathouse Residences was jointly developed by Far East Organiza-tion, Frasers Centrepoint and Sekisui House and completed last year

E

EP8 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

COVER STORY

| BY CECILIA CHOW |

On the weekend of Nov 19 and 20,

GSH Corp launched in Singapore

its maiden residential development,

Eaton Residences, a high-end condo-

minium on Jalan Kia Peng in Kuala

Lumpur City Centre (KLCC). The property exhi-

bition was held at Fairmont Singapore in Raffles

City. So far, 180 units have been booked, says

GSH. The figure includes the 150 units tak-

en up when the first phase of 280 units was

launched in KL on Sept 20, and the units sold

subsequently.

“These days, it’s hard to achieve double-digit

sales in any overseas property launch,” observes

Donald Han, managing director of Chester-

ton Singapore. “With the Singapore econo-

my in the doldrums, people are conserving

cash. Meanwhile, companies are trying to cut

costs. So, in the current environment, if you

can achieve such sales at an overseas project

launch, that’s excellent.”

Over the weekend, more than 20 groups

were said to have visited the exhibition. “For

a standalone overseas project exhibition, it’s

quite a good turnout,” says Sunny Wong, divi-

sion director at ERA Realty, the exclusive mar-

keting agent for the project. “These are serious

buyers. Some are interested in buying a unit

as a second home and others are looking at

an investment opportunity.”

Riding on the momentum, Eaton Residences

will be showcased for a second consecutive

weekend in Singapore at ERA’s office and

sales gallery in Mountbatten Square on Nov 26

and 27.

Palatable absolute pricesWith the Malaysian ringgit tumbling to a new

low of 3.1 against the Singapore dollar, “the

exchange rate is looking favourable for Singa-

poreans, and in terms of absolute prices, it’s

equivalent to a 30% to 40% discount”, says

Gilbert Ee, CEO of GSH.

To make absolute prices palatable to price-

sensitive buyers, one-bedroom and one-bed-

room-plus-study units make up 394 (62%) of

a total of 632 units at Eaton Residences. These

are sized from 635 to 872 sq ft. Two-bedroom-

plus-study units measuring 1,098 to 1,464 sq

ft and three- and four-bedroom-plus-study

units measuring 1,550 to 2,874 sq ft account

for 36% of the units. There are also 12 pent-

houses of 2,271 to 2,982 sq ft.

The one-bedroom units at Eaton Residences

are priced from RM1.14 million ($365,000)

and one-bedroom-plus-study units start from

RM1.45 million ($465,000). Therefore, these

units have been the most appealing to inves-

tors because of the affordability of their ab-

solute prices. For $365,000 to $465,000, you

cannot even buy a shoebox apartment in Sin-

gapore today, says a property agent.

At that price range, you can probably buy a

brand-new BMW 6 Series convertible, a Jaguar

F-Type, a Mercedes CLS-Class or a Porsche Box-

ster in Singapore. “But if you buy a property,

you can rent it out and earn a return,” says Ee.

Rental yieldsContrary to popular belief, it is easier to find

tenants in KL than in Singapore, says Bruce

Lye, managing partner of realtor SRI. Lye, a

Singaporean, has been marketing projects in

KL and investing there for the past six years.

Today, he and his wife jointly own seven condo

units in KL — three in the Mont’Kiara area, a

popular suburb with expatriates; two at Sen-

tral Residences near the KL Sentral train sta-

tion, which is due for completion within the

next few months; one in KLCC; and one in

Bukit Bintang.

“Based on my experience with the properties

that I own there, I realise that the big units in

the KLCC area do not perform as well in terms

of rentability compared with those in Mont’Ki-

ara,” says Lye. “The big units in Mont’Kiara

tend to be rented out quickly because they are

popular with families, as there are internation-

al schools in the neighbourhood.”

In the KLCC area, one- and two-bedroom

units are sought after because of the profile of

Eaton Residences to defy market forces

The sinking Malaysian ringgit is certainly a boon to holidaymakers, but investors are wonderingwhether it is time to enter the property market. GSH Corp believes the quality of its project,

prime location in KLCC and skyline views will help it overcome the challenges.

Petronas Twin Towers — the landmark of Kuala Lumpur City Centre

Ee: The [SGD/RM] exchange rate at this point is looking favourable for Singaporeans, and in terms of absolute prices, it’s equivalent to a 30% to 40% discount

PICT

URES

: MO

HD S

HAHR

IN Y

AHYA

/THE

EDG

E M

ALAY

SIA

THEEDGE SINGAPORE | NOVEMBER 28, 2016 • EP9

COVER STORY

the tenants, says Lye. “They tend to be young

singles or couples with no children. In fact,

rents of the larger units are quite close to the

one- and two-bedroom units in the KLCC area.”

According to Lye, gross rental yields in the

Mont’Kiara and KLCC area are about 6%. If

one were to take financing cost into consider-

ation, however, then net yield would be 2%

to 3%, which is on a par with yields in Singa-

pore, he says. “Without a mortgage, however,

yields will be around 6%.”

Reinvesting, dollar cost averagingWhile Lye’s portfolio of properties have seen

capital gains, he will incur a loss based on the

current exchange rate. This is because many

of his purchases were made five to six years

ago when the ringgit was 2.2 against the Singa-

pore dollar, says Lye.

One way to avoid a currency exchange loss

is to reinvest his gains in Malaysia, he says.

Thus, he intends to buy another small one- or

two-bedroom unit in the KLCC area within the

next six months.

Another bonus of having multiple proper-

ties in KL is that it can also be a second or

holiday home. “I travel up to KL at least once

a month,” says Lye. “If one of my properties

is available between tenants, I will stay in it.”

While Singaporeans account for about 20%

of buyers at Eaton Residences, mainland Chinese

form the majority. Other international buyers

include those from Hong Kong, Indonesia and

Taiwan, says GSH’s Ee.

In early November, the Hong Kong govern-

ment doubled stamp duty for foreign buyers

from 15% to 30%, and for second and subse-

quent Hong Kong resident buyers from 8.5%

to 15%. Anticipating that property investors

will now look elsewhere, Singapore develop-

ers have been quick to seize the opportunity

by bringing their projects to Hong Kong on

roadshows.

Like the other Singapore developers, GSH is

also launching Eaton Residences at a weekend

roadshow in Hong Kong on Nov 26 and 27.

“If the overseas and local investors in

Hong Kong are deterred by the higher

stamp duty, money will flow out and

look to invest elsewhere,” says Ee. “KL

may be at the receiving end of some

of that outflow.”

The downward trend of the ring-

git is a double-edged sword for many

overseas investors. “I remember 25

years ago when the exchange rate be-

tween the ringgit and Singapore dollar

was 1.5 to 1,” recounts Chesterton’s

Han. “And now it’s hovering at 3.1 to

1. So, it’s been on a downward trend.

And in the short term and even the

medium term, it’s hard to foresee the

ringgit strengthening, especially with

oil prices still depressed and the cur-

rent political uncertainty in Malaysia.”

Priced at RM1,550 to RM1,800 psf,

Eaton Residences looks particularly com-

pelling, especially in the face of a falling

ringgit, concedes Han. “In the KLCC area,

ultra luxury condos priced at RM2,500

to RM3,000 psf are finding it difficult to

move units, especially if they are large

and the absolute prices are high.”

He reckons that GSH’s Eaton Resi-

dences could have hit the sweet spot

with foreign buyers with the exclusiv-

ity of the project, and by capitalising

on its location and the views.

Capitalising on views, locationEaton Residences is located within KL’s Em-

bassy Row and near the Petronas Twin Tow-

ers and Jalan Bukit Bintang shopping belt. It

is within walking distance of the KLCC LRT

station and within 150m of a future MRT sta-

tion at Jalan Conlay. The project is also near

the Prince Court Medical Centre.

The 51-storey tower offers unobstructed

panoramic views of the Petronas Twin Towers

on one side and the Royal Selangor Golf Club

on the other. GSH had purchased the prime

62,726.4 sq ft site from Tropicana Kia Peng for

RM132.4 million in December 2013.

The 99-year lease on the project is not a

concern, says Ee. Unlike in Singapore, owners

of private property in Malaysia are able to

renew their 99-year lease at a prescribed

amount. And buyers only need to pay to re-

new the lease when there are only 30 years

left, he says.

GSH has appointed Singapore’s most estab-

lished architectural firm, Swan & Maclaren, to

design Eaton Residences in collaboration with

Patty Mak (formerly of Suying Metropolitan

Studio) as interior design consultant.

Eaton Residences will have an entrance

driveway and lobby designed with the “gran-

deur of a luxury hotel”, says Lim Chai Boon,

Swan & Maclaren’s group director. There are

three levels of basement parking below an

eight-storey car-park podium. Ample parking is

provided, as the one-bedroom units are desig-

nated one parking space each, but most of the

other units have two parking spaces each and

the penthouses have up to four.

On the rooftop of the car-park podium, there

is a facilities deck with a children’s playground,

barbeque pods, fitness stations and multi-use

spaces. The 33rd level has a sky garden and

lounge. The 51st level has a 40m cantilevered

infinity swimming pool that allows residents

to enjoy the view, says Lim. There are also spa

pools and a leisure pool on this level.

“The view from the 51st floor will be as

spectacular as being at the SkyPark of Marina

Bay Sands,” says GSH’s Ee. “This is what’s

going to set the project apart from the rest.”

And there are many upcoming develop-

ments in the vicinity. According to Property

Talk & Lifestyle Malaysia’s PTML Research in

a September 2015 report, more than 120 sites

in the KL city area are under construction, be-

ing proposed for development or being planned

for future development.

“KL is a city of skyscrapers, and that’s no

different from other cities such as Shanghai

or Manhattan,” notes interior design doyenne

Mak. “I felt it was important to create an iden-

tity for Eaton Residences. We wanted to cre-

ate city living, and that means embracing the

skyline — so, every room in every unit must

have a view.”

All units have an open-concept kitchen,

says Mak. “This allows residents to inter-

act with other members of the family even

while cooking, and enjoy the view at the

same time.”

At Eaton Residences, Mak also chose a muted

palette for the units, with the same white

marble carried throughout the unit and in the

bathrooms, and white timber flooring for the

bedrooms. Kitchen cabinets and wardrobes,

which are custom-designed, are also in white

or grey tones. “The idea is to create a canvas

for the owner to fill in the colours to complete

their dream home against the backdrop of a

blue sky,” she says.

Luxury quality for a stealThe quality of the materials used at Eaton Resi-

dences is equivalent to those of luxury condos

in the prime districts of Singapore. Mak has

designed the interiors of many high-end con-

dos in Singapore, including the 462-unit OUE

Twin Peaks on Leonie Hill Road, where she

even handpicked the furniture for each unit;

Allgreen Properties’ 360-unit SkySuites

@ Anson on Enggor Street; Sing Hold-

ings’ 134-unit Robin Residences; and

the 97-unit Centennia Suites, where

action star Jackie Chan is said to have

purchased three units.

With Swan & Maclaren and Mak be-

hind the design of Eaton Residences,

“the response to our project has been

very good”, says Ee. “Despite the chal-

lenging environment, we swung quite

a few buyers from neighbouring pro-

jects because of our price point, prod-

uct quality and uniqueness.”

The construction cost of Eaton Res-

idences is estimated at RM450 million,

and the condo is expected to be com-

pleted in 2020. “I don’t think I can

construct a 51-storey condoproject of

this quality in Singapore for $150 mil-

lion,” says Ee.

“Even if the ringgit collapses fur-

ther, property prices in Malaysia will

have to go up because developers can

no longer build properties at these pric-

es,” he adds.

“The cost of labour and construc-

tion materials will only go up, and

that means property prices will also

rise. So, if you’re buying a unit at be-

low RM2,000 psf in KLCC today, there

will be upside potential.”

Every unit at Eaton Residences comes with an open-kitchen concept with a view of the city skyline

Every room in every unit — from the kitchen and living area to the master bedroom — has a view

Model of the 632-unit Eaton Residences on Jalan Kia Peng in KLCC E

PICT

URES

: KEN

NY

YAP/

THE

EDG

E M

ALAY

SIA

EP10 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

PROPERTY TAKE

Stamp duty: Common mistakes to avoid| BY INLAND REVENUE AUTHORITY OF SINGAPORE |

For the past three years, more

than 90% of taxpayers have

complied with the requirements

for stamp duty, which is paid on

documents or agreements relat-

ed to properties in Singapore as well

as stocks and shares. These include

tenancy or lease agreements, accept-

ance of options to purchase as well as

sale and purchase (S&P) agreements.

The minority who did not com-

ply were mostly those who failed to

stamp their documents, were late

in stamping their documents or did

not pay the correct amount of stamp

duty due to incorrect computation,

such as stamp duty being comput-

ed based on purchase price, which

is far below the market value of the

property.

The Inland Revenue Authority

of Singapore takes a strong stance

against the non-compliant taxpay-

ers to ensure fairness of the tax sys-

tem. IRAS recovered $21 million in

taxes and penalties from stamp duty

audits between FY2013 and FY2015.

Some non-compliance scenarios

that arose from taxpayers’ lack of un-

derstanding of stamp duty require-

ments include:

Transfer of property by way of gift For transfer of property by way of

gift, stamp duty should be based on

the market value of the property. In

an actual case, a homeowner who

transferred his property by way of

gift to his son stamped the document

based on the consideration amount

of $1 instead of the market value.

The recipient of the gifted proper-

ty, who is liable to pay stamp duty,

should ensure that the document is

adequately stamped based on the rea-

sonable market value of the property.

Misconception that stamp duty is not required for rental of rooms, sublet and lease renewalsThere have also been cases where

tenancy agreements were not duly

stamped for rental of rooms, rental

of whole property units and renew-

al of leases. Stamp duty is payable

on signed documents for subletting

and/or renewal of lease. Usually, ten-

ants are responsible for paying the

stamp duty, unless otherwise stated

in the tenancy or lease agreements.

Tenants should ensure that ten-

ancy agreements for rental of rooms,

rental of whole property units and

renewal of leases are duly stamped.

Additional buyer’s stamp dutyABSD, introduced in December 2011,

is to be paid on top of the existing

buyer’s stamp duty. The ABSD rate

depends on whether the buyer is a

Singapore citizen, Singapore perma-

nent resident, foreigner or corporate

entity, as well as the number of resi-

dential properties owned by the buyer.

As the ABSD rate depends on

the number of residential proper-

ties owned, a buyer should consid-

er all such properties in the property

count, including those that are com-

pleted or under construction; owned

wholly by the buyer or jointly with

others; transferred to the buyer by

way of gift or inheritance; and held

in trust where the buyer is a benefi-

ciary stated in the trust instruments.

Close to 40 out of 437 stamp duty

audit cases uncovered in FY2013-

FY2015 involved non-compliance with

ABSD. Several common non-compli-

ance scenarios arose from negligence

or lack of understanding of ABSD.

An example of non-compliance is

a buyer who did not pay ABSD on

the purchase of his third residential

property. His claim was that he was

not aware of his joint ownership in

two other residential properties that

were transferred to him from his late

parents.

Another example is someone who

did not pay ABSD on his second prop-

erty as he thought that ABSD was not

applicable to him as he had already

discharged his loan for his first prop-

erty, an HDB flat. However, ABSD is

not dependent on the number of out-

standing loans but the number of res-

idential properties owned.

A third example is someone who

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

ZONING APPLICATION OF ABSD

Residential Yes, 100% of land/building value

Residential with commercial at first storey Yes, on residential property component

Commercial and residential Yes, on residential property component

White Yes, 100% of land/building value

Residential/institution Yes, 100% of land/building value

Non-residential, for example, hotel, commercial and business park No

As the ABSD rate depends on the number of residential properties owned, a buyer should consider all such properties in the property count, including those that are completed or under construction

APPLICATION OF ABSD

Yes, 100% of land/building value

Yes, on residential property component

Yes, on residential property component

Yes, 100% of land/building value

Yes, 100% of land/building value

No

THEEDGE SINGAPORE | NOVEMBER 28, 2016 • EP11

PROPERTY TAKE

did not pay ABSD on the purchase

of a second residential property that

was under construction, under the

impression that ABSD was only pay-

able at the point of completion, or

upon the development’s obtaining

Temporary Occupation Permit.

The penalties imposed for the

cases above were up to two times

the amount of ABSD that the buyer

failed to pay.

Buyers should therefore seek ad-

vice from their lawyers or IRAS if

they require assistance in determin-

ing their total property count.

Misconceptions on property and land useThere were instances where mixed-

use properties had been regarded by

buyers as commercial properties, and

the buyers mistakenly thought that

ABSD would not apply. For mixed-

use properties, such as HDB shops

with living quarters, ABSD applies

to the portion where the permitted

use is residential.

Buyers need to pay ABSD on the

purchase of the following:

• Building units (including those

under construction), where the

permanent permitted use at the

point of purchase is residential;

• Vacant land or entire building with

land, depending on the Master

Plan zoning.

For example, a Singapore citizen

who owned two residential proper-

ties bought an HDB shop with living

quarters on the second storey. IRAS’s

audit found that he paid only the 3%

buyer’s stamp duty only. He claimed

that the HDB shop with living quar-

ters was a commercial property and

would not attract ABSD.

However, ABSD applied to the

living quarters on the second sto-

rey. The buyer therefore had to pay

additional stamp duty of 10% and

a penalty of two times the amount

of ABSD that he had failed to pay.

Inaccurate advice given by intermediariesIRAS also found that some interme-

diaries such as property agents and

lawyers had given inaccurate advice

on ABSD to their clients. For exam-

ple, a Singapore citizen purchased

his second residential property and

signed the S&P agreement on June

11, 2013. ABSD payable was there-

fore 7%. However, his lawyer had

referred to the outdated ABSD rules

and failed to advise him that ABSD

was payable.

After an audit review, the buyer

was asked to pay ABSD of 7%. The

lawyer agreed to pay the penalty of

two times the amount of ABSD un-

dercharged due to his negligence.

Intermediaries who handle con-

veyance matters for their clients have

to be familiar with prevailing stamp

duty policies and rates. They are

responsible for ensuring that they

provide correct advice on ABSD li-

ability based on the date of docu-

ment, permitted use/zoning, count

of residential properties owned and

the residency status of their clients.

Stamp duty fraudIRAS takes a serious view of any in-

dividual or business that deliberate-

ly forges stamp duty certificates and

knowingly misrepresents counterfeit

“certificates” as genuine. IRAS will

ensure that these individuals or busi-

nesses are dealt with appropriately in

accordance with the law. The maxi-

mum punishment on someone who

has been convicted of such a crime

would be an imprisonment term of

up to three years or a fine of up to

$10,000 or both.

Since 2010, IRAS has prosecuted

eight persons who forged or used

counterfeit stamp certificates. The

latest case pertained to a former pa-

ralegal who was convicted in Febru-

ary 2016 of forging and using coun-

terfeit stamp certificates for property

transactions. He was sentenced to 12

weeks’ jail.

Potential property buyers and ten-

ants can check the authenticity of

the stamp certificates in their pos-

session by visiting the e-stamping

website at https://estamping.iras.

gov.sg. An authentic stamp certifi-

cate should bear the full details of

the stamp duty payment, descrip-

tion of the document, address of

the property, stamp duty amount

and date of document. All these de-

tails, including the stamp certificate

reference number, should match the

information shown on the e-stamp-

ing website.

Although stamp duty is usually

paid by property buyers and tenants,

sellers and landlords should also re-

quest copies of stamp certificates and

verify them online to protect their in-

terests. For instance, in the event of

legal disputes, the document has to

be duly stamped before it can be ad-

mitted as evidence in court. E

Stamp duty assessed

INSTRUMENTS FY2013/14 FY2014/15 FY2015/16

NUMBER $ MIL NUMBER $ MIL NUMBER $ MIL

Sale & purchase agreement 57,190 3,181 44,101 2,152 48,393 2,115

Lease agreement 203,764 840 210,252 580 221,615 711

Mortgage agreement 70,213 34 70,534 34 71,677 35

Share transfer 27,391 56 28,429 84 29,145 93

Others 1,034 4 965 1 861 2

Total 359,592 4,116 354,281 2,851 371,691 2,956

Stamp duty assessed for private residential properties

CY2013 CY2014 CY2015

NUMBER $ MIL NUMBER $ MIL NUMBER $ MIL

Buyer’s stamp duty 29,966 1,156 15,633 620 18,234 693

Additional buyer’s stamp duty 12,530 1,502 7,521 920 7,130 788

Seller’s stamp duty 844 49 519 30 550 26

Buyer’s stamp duty and additional buyer’s stamp duty rates and computation

ABSD RATES FROM ABSD RATES FROM PROFILE OF BUYER BSD RATES DEC 8, 2011 TO JAN 11, 2013 JAN 12, 2013

Singapore citizens* buying first 1% on first $180,000 Not applicable Not applicableresidential property 2% on next $180,000 3% for the remainder

Singapore citizens buying second Not applicable 7%residential property

Singapore citizens buying third 3% 10%residential property

Singapore permanent residents buying Not applicable 5%first residential property

Singapore permanent residents buying 3% 10%second and subsequent residential property

Foreigners and entities buying any 10% 15%residential property

Vietnam builder for younger buyers sells US$120 mil stake| BY MAI NGOC CHAU |

A Vietnamese developer of

high-rise apartments target-

ing younger buyers sold a

stake to investors for about US$120

million ($171.2 million), the most

raised by a real estate company in

the country in 3½ years.

No Va Land Investment Group

Corp, whose high-rise residential

towers make up 30% of the hous-

ing market in Ho Chi Minh City,

Vietnam’s business centre, says it

has raised the funds selling a 10th

of the company to 18 institution-

al investors. That is the most since

a group led by private-equity firm

Warburg Pincus invested US$200

million in Vingroup JSC’s Vincom

Retail unit in May 2013, according

to data compiled by Bloomberg.

“We received more than twice

as many bids as our offering vol-

ume,” Novaland CEO Phan Thanh

Huy says, ahead of plans to list as

many as 600 million shares on the

Vietnamese stock exchange next

month. “About 70% of our inves-

tors are overseas financial institu-

tions, from Hong Kong, Singapore

and Thailand.”

The company is riding on increas-

ing home sales fuelled by South-

east Asia’s fastest-growing econo-

my after the Philippines. Vietnam’s

economy expanded 6.4% in 3Q, up

from 5.78% in the previous three

months, according to the General

Statistics Office. Novaland’s stake

sale, which is bigger than any IPO

in Vietnam this year, also comes as

the benchmark VN Index climbed

18% this year, making it the re-

gion’s top performer.

Novaland, which targets younger

middle-class buyers, plans to price

its shares at about VND50,000 each,

giving it an estimated market val-

ue of VND30 trillion ($1.9 billion),

Huy says. As much as 20% of No-

valand’s shares will be available for

trading, he says.

The company, which started ex-

panding into other Vietnamese cit-

ies and provinces, is targeting to

sell as many as 9,000 homes next

year, up from an estimated 8,000

in 2016, Huy says.

Property transactions in Ho Chi

Minh City jumped 44% in the first

nine months of the year to 20,801,

while sales in the capital Hanoi

added 2% to 17,264, says Savills

Vietnam, a real estate brokerage

and consulting firm. The momen-

tum may continue for the next few

years even as prices remain stable,

according to CBRE Vietnam, anoth-

er property brokerage and research

company.

“The residential market will con-

tinue to go strong from next year

through 2020, but may slow down

and stabilise itself to avoid a bub-

ble,” says Marc Townsend, man-

aging director of CBRE Vietnam.

“There have been concerns about

a bubble in the residential market,

yet we believe this to be unlikely.”

Before the share sale, Novaland

raised US$60 million in converti-

ble loans earlier this year, follow-

ing US$50 million in 2015 through

convertible preferred shares, the

company says.

Other Vietnamese developers have

also turned to the bond market. FLC

Group JSC, Vietnam’s fourth-larg-

est developer by market value, is in

talks with foreign banks to sell its

first overseas bonds worth as much

as US$200 million next year for its

real estate projects. Sai Gon Thuong

Tin Real Estate JSC, another listed

property company, says it plans to

issue as much as US$53.2 million

worth of bonds next year.

CapitaLand, Southeast Asia’s big-

gest developer, says it is setting up

a US$500 million commercial fund

by 2017 as it expands in Vietnam,

where it plans to buy as many as

2,500 units of residential develop-

ment next year.

Property stocks on the VN Index

have risen 21% this year, driven by

the 27% surge in shares of Vingroup,

Vietnam’s biggest publicly traded de-

veloper. FLC has fallen 14%.

Novaland posted profit of VND1.5

trillion in the first nine months this

year, with the company projecting

earnings of VND1.6 trillion for the

year. Net income is expected to

almost triple to VND5 trillion on

revenue of VND24 trillion in 2018,

Huy says.

“Novaland’s revenue was ranked

No 2 among listed real estate compa-

nies last year, only after Vingroup,”

says Saigon Securities’ senior analyst

Dinh Thi Mai Anh, who estimates

that Novaland has a 30% share of

the Ho Chi Minh City housing mar-

ket. “We think the company will

maintain this position for the next

two years.” — Bloomberg LP

CY2013

NUMBER $ MIL

29,966 1,156

12,530 1,502

844 49

CY2015

NUMBER $ MIL

18,234 693

7,130 788

550 26

BSD RATES

1% on first $180,000 2% on next $180,000 3% for the remainder

ABSD RATES FROMJAN 12, 2013

Not applicable

7%

10%

5%

10%

15%

* Whether owned wholly, partially or jointly with others

E

Property transactions in Ho Chi Minh City jumped 44% in the first nine months of this year to 20,801

BLO

OM

BERG

EP12 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

OFFSHORE

Investors searching for the next real estate

that could offer extraordinary returns have

been asking REMS Advisors for our views

on investing in the Myanmar real estate

market, especially after the US abolished all

sanctions against Myanmar on Oct 7.

We started exploring the market in 2012,

during the initial frenzy over the last untapped

real estate market in Southeast Asia. In 2015,

the peaceful election and subsequent transition

to a civilian government further raised expec-

tations of a country’s being finally unleashed

from its shackles to realise its potential.

Expectations not matched by realityA year on, it has become apparent that a lot

of work remains to be done. Participants in

the real estate market have been spooked by

the government’s decision to cancel the five

large projects that had been pre-approved

and already in various stages of construc-

tion; the stop-work orders issued to almost

200 high-rise construction projects; and the

continuing lack of clarity on the implemen-

tation of the Condominium Law. The lack

of financing for developers and end-users

is also inhibiting the growth of the market.

These have resulted in weaknesses in the

Yangon real estate market.

High-end residential: Foreign purchasers

needed to stimulate the market

The residential sector in Yangon almost ground

to a halt in 2015 and only sporadic sale activi-

ties resumed in 2016. The much hyped-about

Condominium Law was finally passed in Jan-

uary 2016. The law allows foreigners to pur-

chase and own condos subject to certain types

of underlying land title. The units should be

above the sixth floor and total foreign owner-

ship is capped at 40%.

As the associated by-laws or regulations were

not put in place, however, foreigners remain

locked out of the market. In addition, there is

der more pressure in the next

few years, with the imminent

completion of various large of-

fice developments such as Sule

Square and Junction City. Old-

er buildings and poorly man-

aged office buildings are likely

to bear the brunt of the easing

of rents.

Serviced apartment: Resilience

due to lack of supply

The serviced apartment sector

has been the most resilient in

Yangon. Average rents eased

7% in 3Q2016 from its peak in 1Q2015 (see

Chart 2). The key reason for its resilience is

the general lack of new completions over the

last two years.

Despite easing rents, overall occupancy rates

have remained above 90%. Newer serviced

apartments are still operating at near full oc-

cupancy and have long waiting lists. The larg-

er three- and four-bedroom apartments seem

to be enjoying an increase in demand in re-

cent quarters.

Ingredients for growth of real estate market are in placeAll the theoretical factors that could drive de-

mand for real estate in Myanmar are falling

into place. The economy enjoyed its fastest

pace of growth over the last three years and is

expected to be the star performer in the com-

ing three years, according to The Internation-

al Monetary Fund’s forecast. Foreign direct in-

vestments are climbing after a hiatus in 2015.

Effectively, the country is now free of sanctions

and that could further boost its FDIs.

An increase in new investments is like-

ly to bring in more foreigners, who will need

hotel rooms, serviced apartments, offices and

retail options. More economic activity is like-

ly to increase the pace of urbanisation. Taken

together, continued economic growth will fuel

the virtuous circle of attracting more people to

the city and increasing demand for real estate.

The slowdown in new construction starts

provides some breathing space for the market

to absorb the large projects that are due for

completion in the next two years.

Investors should be looking at ser-

viced apartments operated by rep-

utable operators, high-end residen-

tial developments and warehouse

or logistics property investments

in Yangon.

Are you ready to investin Myanmar? Without a doubt, we should be

seeing investment schemes or pro-

jects that will be brought by de-

velopers or real estate agencies to

market in Singapore in the com-

ing months or years.

Singaporeans’ insatiable appetite for small

quantum investments in property is apparent

from the positive sales of newly launched res-

idential projects in Singapore and the good

sales momentum for Cambodian residential

projects in recent months.

Thus, Myanmar property might fit into

the low quantum investment space. Investors

should consider five important factors when

investing in Yangon:

• Is there a resale market for the location or

sector they are in?

• Are they getting clear, unencumbered own-

ership of the property they buy?

• Does the developer have the resources, dis-

cipline and capability to complete the pro-

ject as promised?

• Are there people or entities that can help

with absentee management? and

• Can they withstand the risks and policy

shocks that can happen?

Invest a little, diversify a lotIn general, we would like to advocate that inves-

tors consider their appetite for risk when invest-

ing in emerging markets and not invest because

it is cheap. Alternatively, investors should con-

sider taking part in shared investment schemes

(which have clearly defined investment terms)

and allocate small amounts to each investment

and diversify their risks.

Tan Kok Keong is CEO of REMS Advisors and

co-founder of FundPlaces

BLO

OM

BERG

| BY TAN KOK KEONG |

Is Yangon’s real estate market ready for retail investors?

Yangon serviced apartment rental index

Base = 3Q2013

1Q20

13

2Q20

13

3Q20

13

4Q20

13

1Q20

14

2Q20

14

3Q20

14

4Q20

14

1Q20

15

2Q20

15

3Q20

15

4Q20

15

1Q20

16

2Q20

16

3Q20

16

140

130

120

110

100

90

80

70

60

Yangon office rental index

Base = 3Q2012140

130

120

110

100

90

80

70

60

3Q20

12

4Q20

12

1Q20

13

2Q20

13

3Q20

13

4Q20

13

1Q20

14

2Q20

14

3Q20

14

4Q20

14

1Q20

15

2Q20

15

3Q20

15

4Q20

15

1Q20

16

2Q20

16

3Q20

12

a large number of units under construction,

which could put the market under some price

and rent pressure in the coming years.

Office: Flight to quality

The prime office segment in Yangon continues

to underwhelm, as the lack of new inbound in-

vestments means that new demand for offices

remains low. The market is also struggling to

absorb the large supply from the completion

of about 874,000 sq ft of the Myanmar Centre

Phase 1. As at 3Q2016, prime office rents con-

tinued to decline, marking the ninth quarter

of decline (see Chart 1).

We expect overall office rent to come un-

The lack of financing for developers and end-users is also inhibiting the growth of the market, resulting in weaknesses in Yangon’s real estate market

E

CHAR

TS: R

ESM

RES

EARC

H

Chart 1

Chart 2

THEEDGE SINGAPORE | NOVEMBER 28, 2016 • EP13

GAINS AND LOSSES

Residential transactions with contracts dated Nov 8 to 15

URA

, THE

EDG

E PR

OPE

RTY

Most profi table deals

Non-profi table deals

PROJECT DISTRICT AREA (SQ FT) SOLD ON SALE PRICE ($ PSF) BOUGHT ON PURCHASE PRICE ($ PSF) PROFIT ($) PROFIT (%) ANNUALISED PROFIT (%) HOLDING PERIOD (YEARS)

NON-LANDED

1 Woollerton Park 10 2,357 11-Nov-16 1,591 22-Apr-03 759 1,960,000 109 6 13.6

2 Southbank 7 969 9-Nov-16 1,493 27-Jul-06 546 917,000 173 10 10.3

3 Monterey Park Condominium 5 2,056 11-Nov-16 851 19-Aug-05 471 782,000 81 5 11.2

4 Southaven II 21 1,841 14-Nov-16 951 7-Jul-09 527 780,000 80 8 7.4

5 Watten Estate Condominium 11 2,465 11-Nov-16 1,002 23-Nov-06 702 740,000 43 4 10.0

6 Costa Del Sol 16 1,475 15-Nov-16 1,268 5-Jan-07 794 698,680 60 5 9.9

7 Varsity Park Condominium 5 2,013 9-Nov-16 944 7-Aug-07 636 620,000 48 4 9.3

8 Cairnhill Crest 9 1,733 11-Nov-16 1,691 1-Jun-05 1,339 610,000 26 2 11.5

9 The Verte 15 2,314 11-Nov-16 886 6-Apr-09 640 569,040 38 4 7.6

10 8@Woodleigh 13 1,098 13-Nov-16 1,288 15-Jul-09 787 550,120 64 7 7.3

LANDED

1 Terrace / Jalan Sahabat 19 2,551 11-Nov-16 1,117 20-Apr-07 394 1,845,000 184 12 9.6

2 Terrace / Gerald Crescent 28 4,187 10-Nov-16 712 15-May-06 339 1,560,000 110 7 10.5

3 Semi-Detached / Poole Road 15 3,520 8-Nov-16 1,136 18-Jan-08 852 1,000,000 33 3 8.8

4 Terrace / Pavilion View 23 2,260 9-Nov-16 1,349 2-Oct-09 950 902,000 42 5 7.1

5 Terrace / Jalan Selamat 14 3,531 9-Nov-16 1,087 14-Mar-11 857 813,000 27 4 5.7

PROJECT DISTRICT AREA (SQ FT) SOLD ON SALE PRICE ($ PSF) BOUGHT ON PURCHASE PRICE ($ PSF) LOSS ($) LOSS (%) ANNUALISED LOSS (%) HOLDING PERIOD (YEARS)

1 Marina Bay Residences 1 1,227 11-Nov-16 2,445 30-Aug-10 3,120 828,000 22 4.0 6.2

2 Kovan Residences 19 1,798 11-Nov-16 1,029 30-Oct-12 1,229 360,000 16 4.0 4.0

3 The Sound 15 1,518 10-Nov-16 1,272 17-Jun-10 1,405 202,400 9 2.0 6.4

4 The Boutiq 9 506 8-Nov-16 1,977 18-May-11 2,247 136,780 12 2.0 5.5

5 Caribbean At Keppel Bay 4 1,281 15-Nov-16 1,312 4-Jun-10 1,415 132,615 7 1.0 6.5

6 The Tropica 18 1,496 10-Nov-16 795 20-May-11 872 115,000 9 2.0 5.5

7 Icon 2 969 10-Nov-16 1,806 18-Nov-09 1,921 111,000 6 1.0 7.0

8 The Marbella 10 1,755 9-Nov-16 1,539 2-May-12 1,596 100,000 4 1.0 4.5

9 West Bay Condominium 5 893 10-Nov-16 824 15-Jun-12 895 64,000 8 2.0 4.4

10 Hillington Green 23 1,755 11-Nov-16 1,003 2-May-12 1,026 40,000 2 0.5 4.5

Note: The profit and loss computation excludes transaction costs such as stamp dutiesURA caveat record downloaded on Nov 8 and 22

Seller incurs $111,000 loss despitebuying near bottom of market| BY FEILY SOFIAN |

Properties sold near the bottom of the

market are not necessarily a value buy.

A 969 sq ft apartment at Icon, a residen-

tial project located a short walk from

the Tanjong Pagar MRT station, was re-

cently sold at a loss of $111,000. The seller had

purchased the unit in November 2009, shortly

after the market picked up from the Lehman

Brothers crisis.

He had paid $1.86 million, or $1,921 psf,

for the unit, which is located above the 40th

floor. Comparable units in the development

went for an average price of $1,725 psf in 2009.

On Nov 10 this year, the unit was resold

at $1.75 million, or $1,806 psf, 6% below the

purchase price. This works out to a 1% loss

annually over seven years.

Another 969 sq ft unit located directly above

it was also sold at a loss amounting to $179,000,

or 9%. The seller had also paid a toppish price

of $1.96 million, or $2,022 psf, on the same day

as the first seller in November 2009.

He incurred losses, despite selling the unit

near the peak of the market in 2013. The unit

fetched $1.78 million, or $1,837 psf, in a re-

sale transaction on July 19, 2013.

So far, there have been 60 resale transac-

tions involving units bought in 2009. Of these,

57 were sold at a profit and three at a loss.

The 57 units were previously purchased at an

average price of $1,386 psf. The three units

sold at a loss were previously bought at an

average price of $1,958 psf.

The 646-unit Icon was one of the best-sell-

ing residential projects when it was launched

in 2003, right after the Severe Acute Respiratory

Syndrome outbreak. Many units were snapped

up at an average price of $650 psf. The 99-year

leasehold condominium was completed in 2007.

The development saw a total of 611 sub-sale

transactions between 2003 and 2010. Sub-sale,

which refers to secondary market transactions

before the issuance of the Certificate of Statu-

tory Completion, is often seen as a barometer

of speculative activities.

The biggest loss in the week of Nov 8 to 15

amounted to $828,000. It accrued to a 1,227

sq ft unit in Marina Bay Residences. The sell-

er had purchased the unit in August 2010 in a

sub-sale at $3.83 million, or $3,120 psf.

On Nov 11, the unit was resold for $3 mil-

lion, or $2,445 psf — a loss of 22% over a six-

year holding period.

Interestingly, the unit has been flipped three

times. The first seller, who bought the unit from

the developer in December 2006 at $1,701 psf,

made a profit of $612,300 when he flipped the

unit in June 2009 at $2,200 psf.

The second seller, who flipped the unit in

August 2010 at $3,120 psf, reaped a profit of

$1.13 million. Unfortunately, the musical chairs

stopped and the third seller, who sold the unit

this month, sustained a hefty loss. The unit

is located above the 30th floor. Marina Bay

Residences is a 428-unit, 99-year leasehold

development completed in 2010.

A 1,227 sq ft unit at Marina Bay Residences was flipped three times. The third seller took in a loss of $828,000.E

SAM

UEL

ISAA

C CH

UA/T

HE E

DGE

SIN

GAP

ORE

EP14 • THEEDGE SINGAPORE | NOVEMBER 28, 2016

| BY TAN CHEE YUEN |

At Twentyone Angullia Park, a

2,314 sq ft, three-bedroom unit

on the 11th floor of the 36-sto-

rey tower was sold for $6.93

million, according to a caveat

lodged on Nov 10. The sale price trans-

lated to $2,995 psf, marking the second

lowest price in the project in per sq ft

terms. The last transaction and the lowest

in terms of price psf was that of a 2,777

sq ft, four-bedroom unit on the second

floor; it changed hands for $8.3 million

($2,989 psf) in July.

John Fong, deputy head of business unit

at KF Property Network, says the unit on the

second level is the only one on that level,

with the other units located from the ninth

floor. Therefore, the pricing is “realistic”

and presents “a buying opportunity”.

The recently sold unit on the 11th floor

is also considered to be on a relatively low

floor, says Samuel Eyo, managing direc-

tor of Singapore Christie’s International

Real Estate.

The developer, CS Land (formerly known

as China Sonangol Land), is still pricing

the remaining units on the lower floors in

the range of $3,300 to $3,500 psf, and the

upper floors from $4,000 psf, says Eyo.

TwentyOne Angullia Park was designed

by Chan Soo Khian of SCDA Architects, the

same architect for The Marq on Pater son

Hill, located farther down Paterson Road.

The 66-unit The Marq on Paterson Hill was

developed by Simon Cheong of SC Global

Developments, known for its luxury pro-

jects. Completed in 2011, The Marq is still

the only condominium in Singa pore where

prices surpassed $6,000 psf.

Meanwhile, on Tomlinson Road just off

Orchard Boulevard is Tomlinson Heights.

The freehold 70-unit luxury condo devel-

oped by Hotel Properties was complet-

ed in August 2014. The project contains

exclusively large units, with three-bed-

room apartments from 2,734 to 2,745 sq

ft, five-bedroom units from 4,004 to 4,047

sq ft and two five-bedroom penthouses

of 4,941 sq ft.

A 4,047 sq ft, five-bedroom unit on the

32nd floor of the 36-storey tower was re-

cently sold for $12 million ($2,965 psf),

according to a caveat lodged on Nov 9.

In September, a similar unit on the 30th

floor was also sold for $12 million.

Like most luxury condo developers that

are listed or have foreign shareholders, the

developers of these two projects are subject

to extension charges for unsold units two

years after Temporary Occupation Permit

(TOP) under the conditions of the Qual-

ifying Certificate. “These developers are

therefore motivated to offer attractive pric-

es to move their units,” says Christie’s Eyo.

OUE has achieved success in offloading

its units with an innovative deferred pay-