economic and revenue review - home | vermont general ... briefings/december 2015... · economic and...

TRANSCRIPT

Economic and Revenue Review

for the Vermont State Legislature

Montpelier, Vermont December 1, 2015

Thomas E. Kavet, President

Dr. Nicolas O. Rockler, CEO

State Economist and Principal Economic Advisor to the Vermont State Legislature Since 1996

Kavet, Rockler & Associates, LLC

Economic and Public Policy Consulting

985 Grandview Road Williamstown, Vermont 05679-9003 USA Telephone: 802-433-1360 Facsimile: 866-433-1360 Cellular: 802-433-1111 Website: www.kavetrockler.com E-Mail: [email protected]

$- $50.0 $100.0 $150.0 $200.0 $250.0 $300.0 $350.0 $400.0 $450.0 $500.0

Education Fund (Partial)

Transportation Fund

General Fund

$64.3

$89.9

$451.9

$63.7

$90.4

$456.4

FY16 Revenues by Fund Through October 2015 Actual Revenues (Green) vs. Targets (Red), Percent Variance by Fund in Box, Source: VT Joint Fiscal Office

Actual

Target

+1.0%

+0.6%

-1.0%

Vermont Year-To-Date FY16 Revenues Have

Been Close to Expectations

• Total Revenues through October (General, Transportation and derived Education Funds) are about $4.4M above targets on a base of about $610M - a variance of about +0.7%, with characteristic volatility in Corporate receipts a plus, and in Estate tax revenues, a minus

• Consumption taxes (Sales & Use, Meals & Rooms and Motor Vehicle Purchase & Use) were very close to estimates (+0.1%) at about $166.7M through October vs. a target of $166.5M. Personal income tax revenues were $1.1M above targets, a variance of +0.5%

• The Education Fund components from the General and Transportation Funds were about $0.7M below targets (-1.5%), due to year-to-date weakness in highly variable Lottery receipts

• Corporate Income tax revenues continued to be strong through the first 4 months of the fiscal year, but mounting refunds and lower profits reported by some firms still represent a substantial risk to revenues over the balance of this year and next

• Total Transportation Fund revenues were about $0.6M above targets through October, a minor variance of about 0.6%

• Preliminary November revenues may take a few extra days to process and analyze due to the Phase 2 expansion of the VTax system in November. This may also result in some November revenue accruing in December

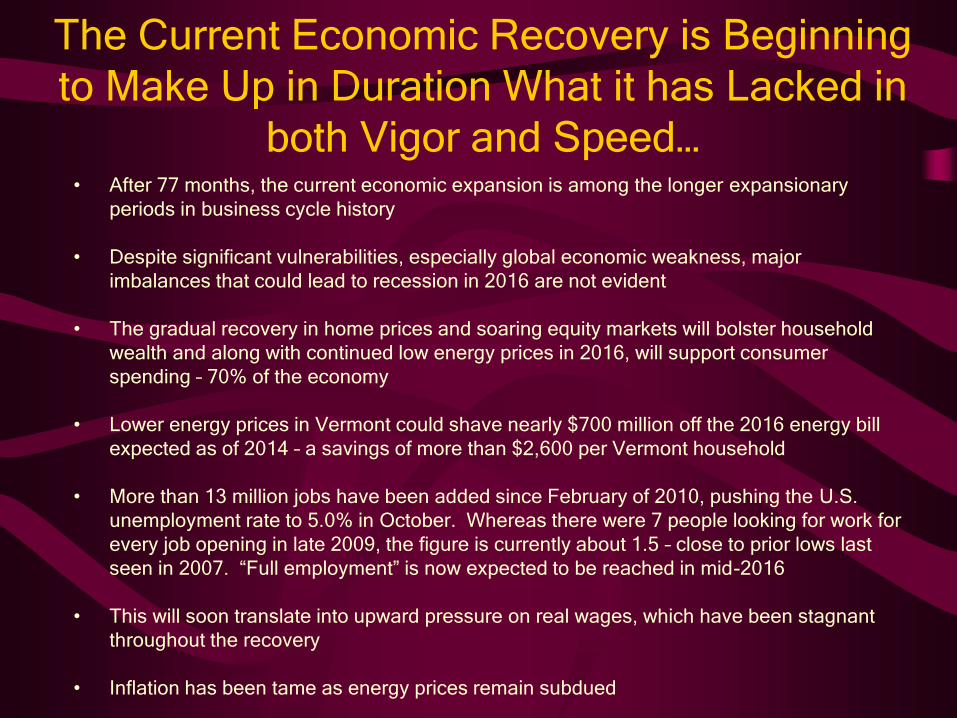

The Current Economic Recovery is Beginning

to Make Up in Duration What it has Lacked in

both Vigor and Speed…

• After 77 months, the current economic expansion is among the longer expansionary

periods in business cycle history

• Despite significant vulnerabilities, especially global economic weakness, major

imbalances that could lead to recession in 2016 are not evident

• The gradual recovery in home prices and soaring equity markets will bolster household

wealth and along with continued low energy prices in 2016, will support consumer

spending – 70% of the economy

• Lower energy prices in Vermont could shave nearly $700 million off the 2016 energy bill

expected as of 2014 – a savings of more than $2,600 per Vermont household

• More than 13 million jobs have been added since February of 2010, pushing the U.S.

unemployment rate to 5.0% in October. Whereas there were 7 people looking for work for

every job opening in late 2009, the figure is currently about 1.5 – close to prior lows last

seen in 2007. “Full employment” is now expected to be reached in mid-2016

• This will soon translate into upward pressure on real wages, which have been stagnant

throughout the recovery

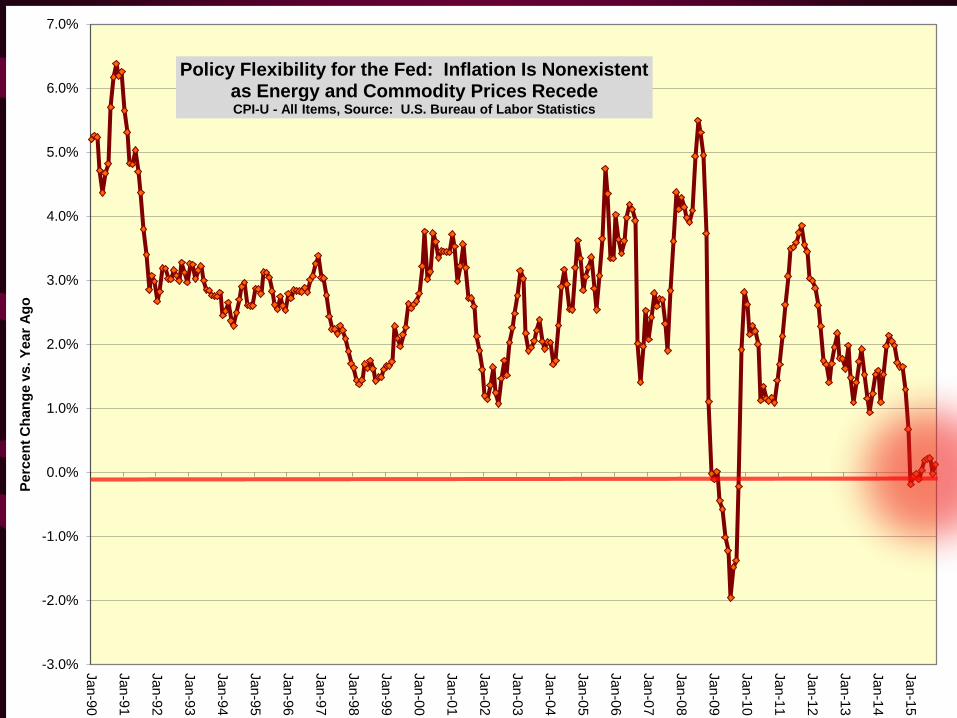

• Inflation has been tame as energy prices remain subdued

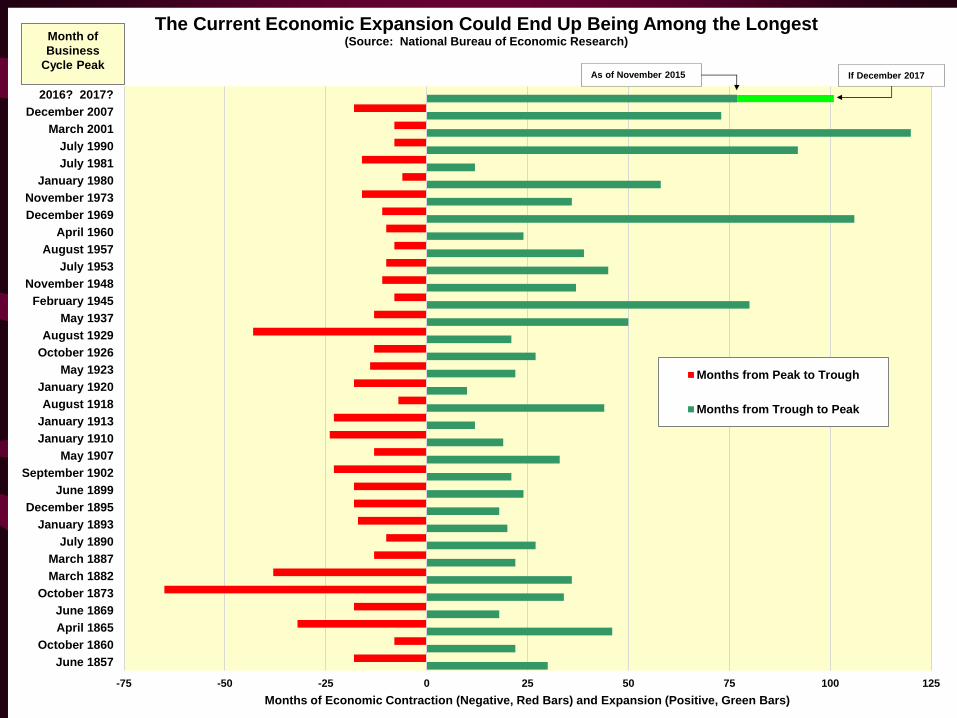

-75 -50 -25 0 25 50 75 100 125

June 1857

October 1860

April 1865

June 1869

October 1873

March 1882

March 1887

July 1890

January 1893

December 1895

June 1899

September 1902

May 1907

January 1910

January 1913

August 1918

January 1920

May 1923

October 1926

August 1929

May 1937

February 1945

November 1948

July 1953

August 1957

April 1960

December 1969

November 1973

January 1980

July 1981

July 1990

March 2001

December 2007

2016? 2017?

Months of Economic Contraction (Negative, Red Bars) and Expansion (Positive, Green Bars)

The Current Economic Expansion Could End Up Being Among the Longest (Source: National Bureau of Economic Research)

Months from Peak to Trough

Months from Trough to Peak

If December 2017 As of November 2015

Month of

Business

Cycle Peak

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

20

05Q

1

20

05Q

2

20

05Q

3

20

05Q

4

20

06Q

1

20

06Q

2

20

06Q

3

20

06Q

4

20

07Q

1

20

07Q

2

20

07Q

3

20

07Q

4

20

08Q

1

20

08Q

2

20

08Q

3

20

08Q

4

20

09Q

1

20

09Q

2

20

09Q

3

20

09Q

4

20

10Q

1

20

10Q

2

20

10Q

3

20

10Q

4

20

11Q

1

20

11Q

2

20

11Q

3

20

11Q

4

20

12Q

1

20

12Q

2

20

12Q

3

20

12Q

4

20

13Q

1

20

13Q

2

20

13Q

3

20

13Q

4

20

14Q

1

20

14Q

2

20

14Q

3

20

14Q

4

20

15Q

1

20

15Q

2

20

15Q

3

Pe

rce

nt

Ch

an

ge

Vs

. Y

ea

r A

go

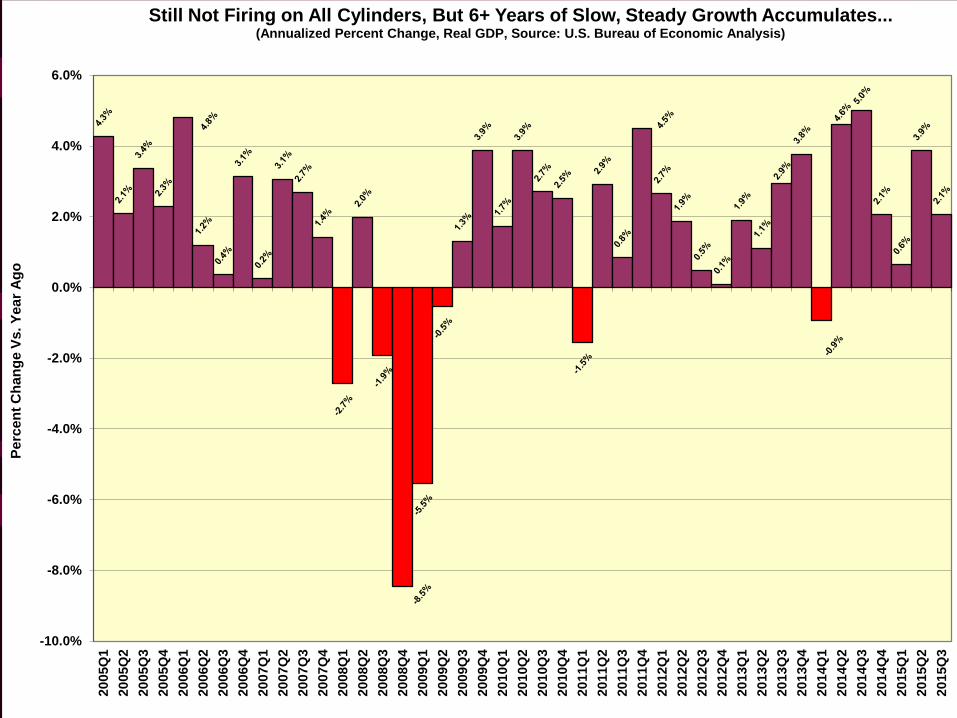

Still Not Firing on All Cylinders, But 6+ Years of Slow, Steady Growth Accumulates...

(Annualized Percent Change, Real GDP, Source: U.S. Bureau of Economic Analysis)

-900

-600

-300

0

300

600

Ju

n-0

7

Se

p-0

7

Dec

-07

Ma

r-08

Ju

n-0

8

Se

p-0

8

Dec

-08

Ma

r-09

Ju

n-0

9

Se

p-0

9

Dec

-09

Ma

r-10

Ju

n-1

0

Se

p-1

0

Dec

-10

Ma

r-11

Ju

n-1

1

Se

p-1

1

Dec

-11

Ma

r-12

Ju

n-1

2

Se

p-1

2

Dec

-12

Ma

r-13

Ju

n-1

3

Se

p-1

3

Dec

-13

Ma

r-14

Ju

n-1

4

Se

p-1

4

Dec

-14

Ma

r-15

Ju

n-1

5

Se

p-1

5

Mo

nth

to

Mo

nth

Ch

an

ge

in

To

tal N

on

ag

ric

ult

ura

l E

mp

loym

en

t (T

ho

us

an

ds

, S

AA

R)

13 Million New Jobs Over 64 Months Finally Results in Firming Labor Markets (Monthly Change in Total Payroll Employment, Seasonally-Adjusted, Source: U.S. Bureau of Labor Statistics)

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

Jan

-47

Jan-4

9

Jan

-51

Jan

-53

Jan

-55

Jan

-57

Jan

-59

Jan

-61

Jan

-63

Jan

-65

Jan

-67

Jan

-69

Jan-7

1

Jan

-73

Jan

-75

Jan

-77

Jan

-79

Jan

-81

Jan

-83

Jan

-85

Jan

-87

Jan

-89

Jan

-91

Jan-9

3

Jan

-95

Jan

-97

Jan

-99

Jan

-01

Jan

-03

Jan

-05

Jan

-07

Jan

-09

Jan

-11

Jan

-13

Jan

-15

Pri

ce

Pe

r B

arr

el -

Oc

tob

er

20

15

Co

ns

tan

t U

.S. D

olla

rs

Sources: Wall Street Journal, Moody's Analytics, KRA

Transformative Oil Price Declines Now Expected to Persist Into 2016 (West Texas Intermediate Crude Oil, PPB in October 2015 Constant Dollars)

(June 2008 - $145 per Barrel)

(April 2011 - $116 per Barrel)

(February 2009 - $44 per

(August 2015 - $43 per Barrel)

[CATEGORY NAME] $[VALUE]

[PERCENTAGE]

[CATEGORY NAME] $[VALUE]

[PERCENTAGE]

[CATEGORY NAME] $[VALUE]

[PERCENTAGE]

[CATEGORY NAME] $[VALUE]

[PERCENTAGE]

Petroleum-Based Energy Expenditures in Vermont, 2013 Millions of Dollars by Consumption Sector, Source: U.S. Energy Information Administration

Total All Sectors = $2,271.4 Million

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

Jan

-78

No

v-7

8

Se

p-7

9

Jul-8

0

Ma

y-8

1

Ma

r-82

Jan

-83

No

v-8

3

Se

p-8

4

Jul-8

5

Ma

y-8

6

Ma

r-87

Jan

-88

No

v-8

8

Se

p-8

9

Jul-9

0

Ma

y-9

1

Ma

r-92

Jan

-93

No

v-9

3

Se

p-9

4

Jul-9

5

Ma

y-9

6

Ma

r-97

Jan

-98

No

v-9

8

Se

p-9

9

Jul-0

0

Ma

y-0

1

Ma

r-02

Jan

-03

No

v-0

3

Se

p-0

4

Jul-0

5

Ma

y-0

6

Ma

r-07

Jan

-08

No

v-0

8

Se

p-0

9

Jul-1

0

Ma

y-1

1

Ma

r-12

Jan

-13

No

v-1

3

Se

p-1

4

Jul-1

5

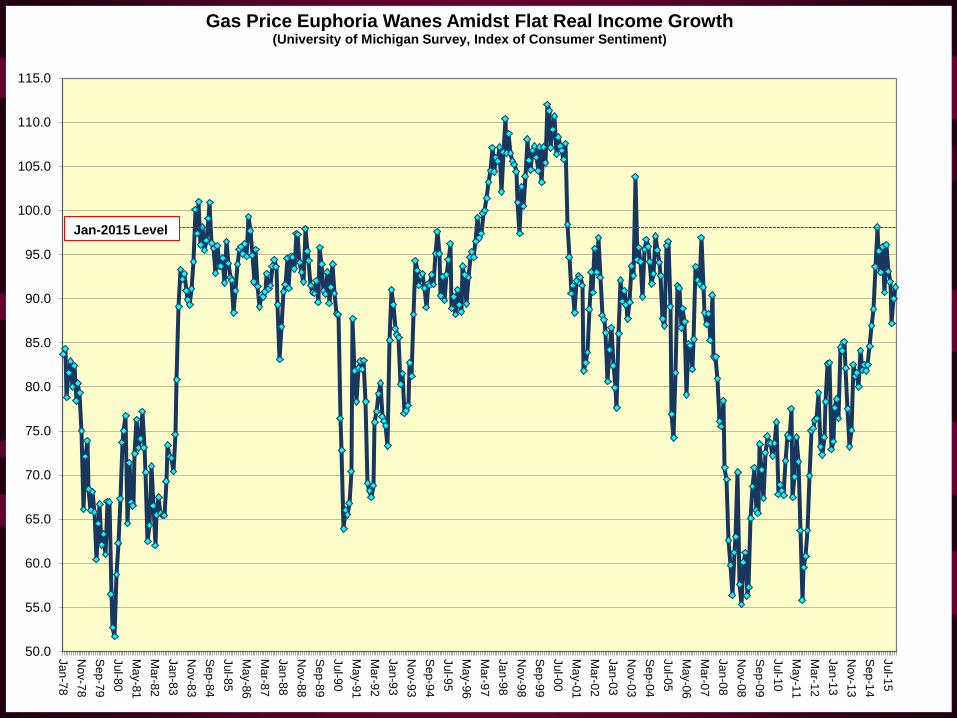

Gas Price Euphoria Wanes Amidst Flat Real Income Growth (University of Michigan Survey, Index of Consumer Sentiment)

Jan-2015 Level

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Pe

rce

nt

Ch

an

ge

Source: U.S. Census Bureau

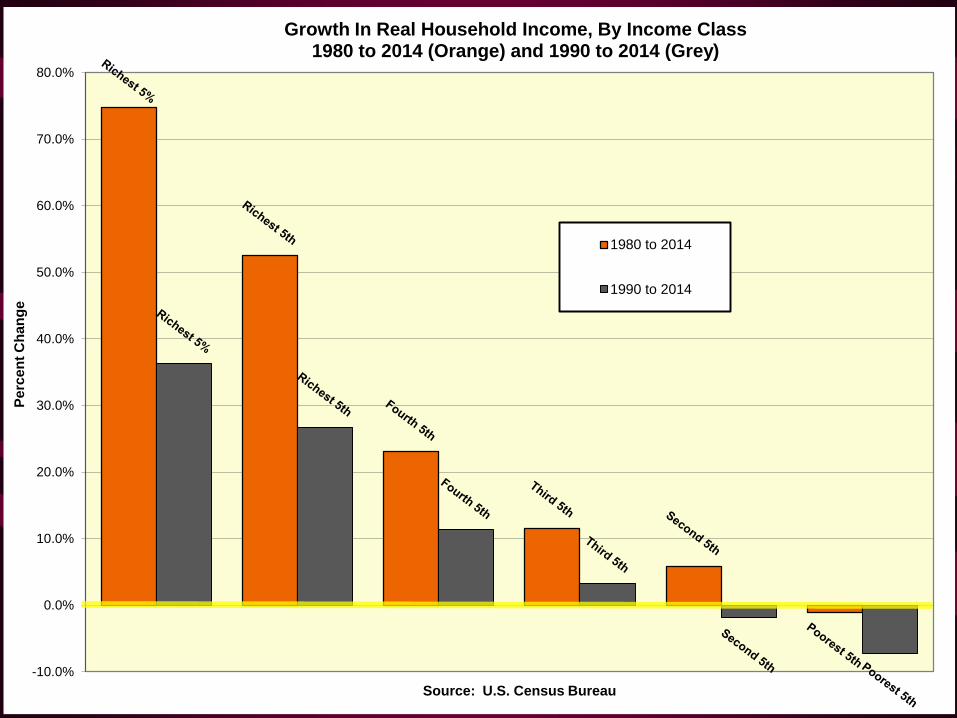

Growth In Real Household Income, By Income Class 1980 to 2014 (Orange) and 1990 to 2014 (Grey)

1980 to 2014

1990 to 2014

15.00

16.00

17.00

18.00

19.00

20.00

21.00

22.00

23.00

24.00

25.00

26.00

27.00

28.00

29.001

96

7

196

8

196

9

1970

197

1

197

2

197

3

197

4

197

5

197

6

1977

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

2003

200

4

200

5

200

6

200

7

200

8

200

9

2010

201

1

201

2

201

3

201

4

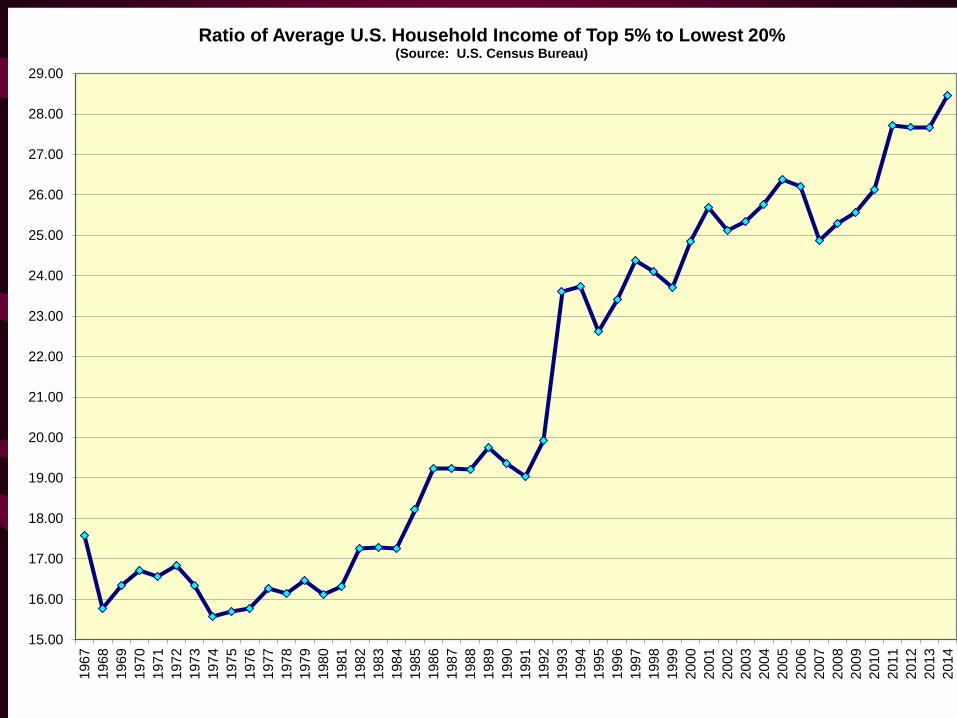

Ratio of Average U.S. Household Income of Top 5% to Lowest 20% (Source: U.S. Census Bureau)

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Ja

n-6

6

Ja

n-6

7

Ja

n-6

8

Ja

n-6

9

Ja

n-7

0

Ja

n-7

1

Ja

n-7

2

Ja

n-7

3

Ja

n-7

4

Ja

n-7

5

Ja

n-7

6

Ja

n-7

7

Ja

n-7

8

Ja

n-7

9

Ja

n-8

0

Ja

n-8

1

Ja

n-8

2

Ja

n-8

3

Ja

n-8

4

Ja

n-8

5

Ja

n-8

6

Ja

n-8

7

Ja

n-8

8

Ja

n-8

9

Ja

n-9

0

Ja

n-9

1

Ja

n-9

2

Ja

n-9

3

Ja

n-9

4

Ja

n-9

5

Ja

n-9

6

Ja

n-9

7

Ja

n-9

8

Ja

n-9

9

Ja

n-0

0

Ja

n-0

1

Ja

n-0

2

Ja

n-0

3

Ja

n-0

4

Ja

n-0

5

Ja

n-0

6

Ja

n-0

7

Ja

n-0

8

Ja

n-0

9

Ja

n-1

0

Ja

n-1

1

Ja

n-1

2

Ja

n-1

3

Ja

n-1

4

Ja

n-1

5

Pe

rce

nt

Ch

an

ge

vs

. Y

ea

r A

go

Oil Price Declines and Wage Growth Will Eventually Benefit Consumer Spending

Total Constant Dollar U.S. Retail Sales - Percent Change from Year Ago, Source: U.S. Census Bureau

Series1 6 Month Moving Average (Real U.S. Retail Sales)

Recession

RECESSION

Recession

Recession Recession

Recession

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

1600.0

1800.0

2000.0

2200.0D

ec-6

9

Dec-7

0

Dec-7

1

Dec-7

2

Dec-7

3

Dec-7

4

Dec-7

5

Dec-7

6

Dec-7

7

Dec-7

8

Dec-7

9

Dec-8

0

Dec-8

1

Dec-8

2

Dec-8

3

Dec-8

4

Dec-8

5

Dec-8

6

Dec-8

7

Dec-8

8

Dec-8

9

Dec-9

0

Dec-9

1

Dec-9

2

Dec-9

3

Dec-9

4

Dec-9

5

Dec-9

6

Dec-9

7

Dec-9

8

Dec-9

9

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Dec-1

4

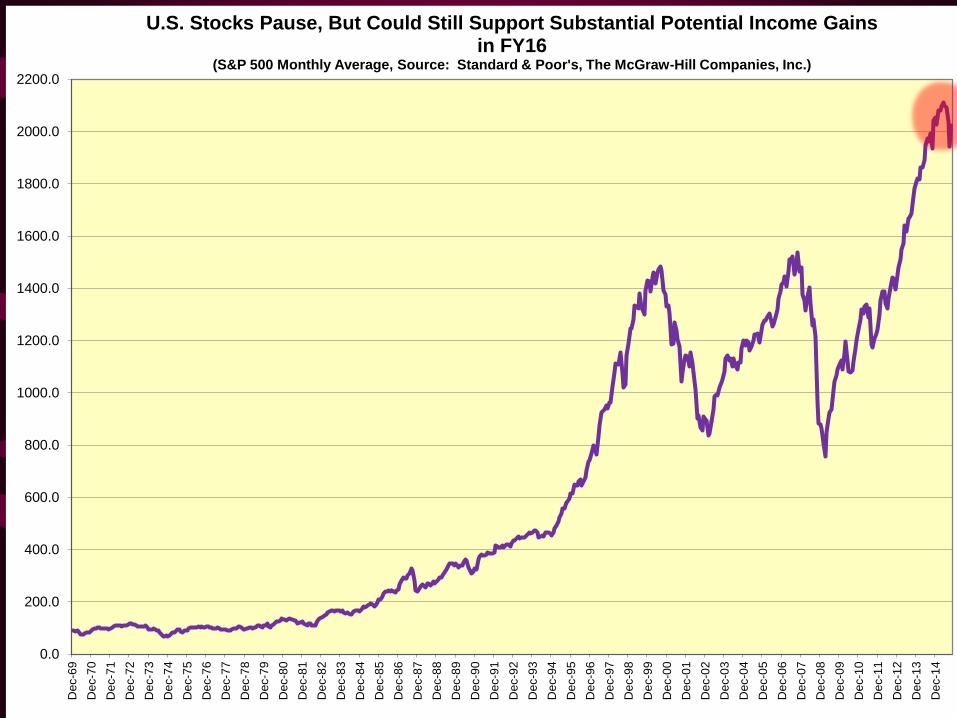

U.S. Stocks Pause, But Could Still Support Substantial Potential Income Gains in FY16

(S&P 500 Monthly Average, Source: Standard & Poor's, The McGraw-Hill Companies, Inc.)

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan-9

7

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan-0

4

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan-1

1

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Pe

rce

nt

Ch

an

ge

vs

. Y

ea

r A

go

Policy Flexibility for the Fed: Inflation Is Nonexistent as Energy and Commodity Prices Recede CPI-U - All Items, Source: U.S. Bureau of Labor Statistics

Labor Markets Are Approaching Full

Employment • Total U.S. nonagricultural employment has increased for 61

consecutive months and after losing 8.7M jobs between January 2008 and February 2010, the U.S. economy has now regained more than 13M jobs, averaging more than 230,000 jobs per month during the past 12 months

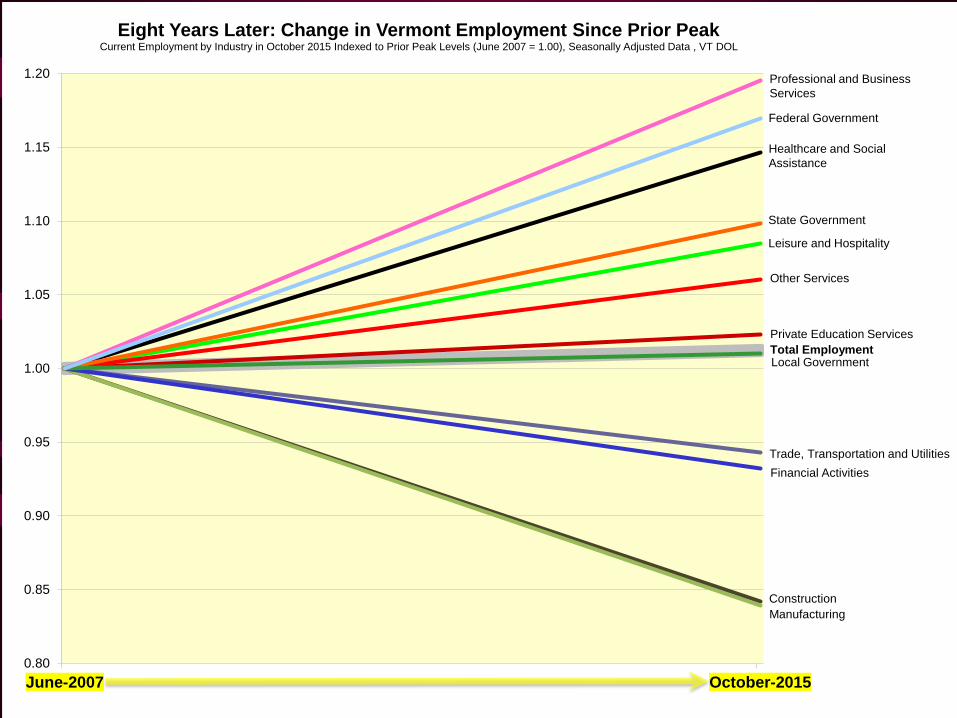

• Vermont payroll employment finally topped its pre-recession peak in June of 2014 and is currently about 18,500 jobs above its recessionary trough, reached in July of 2009

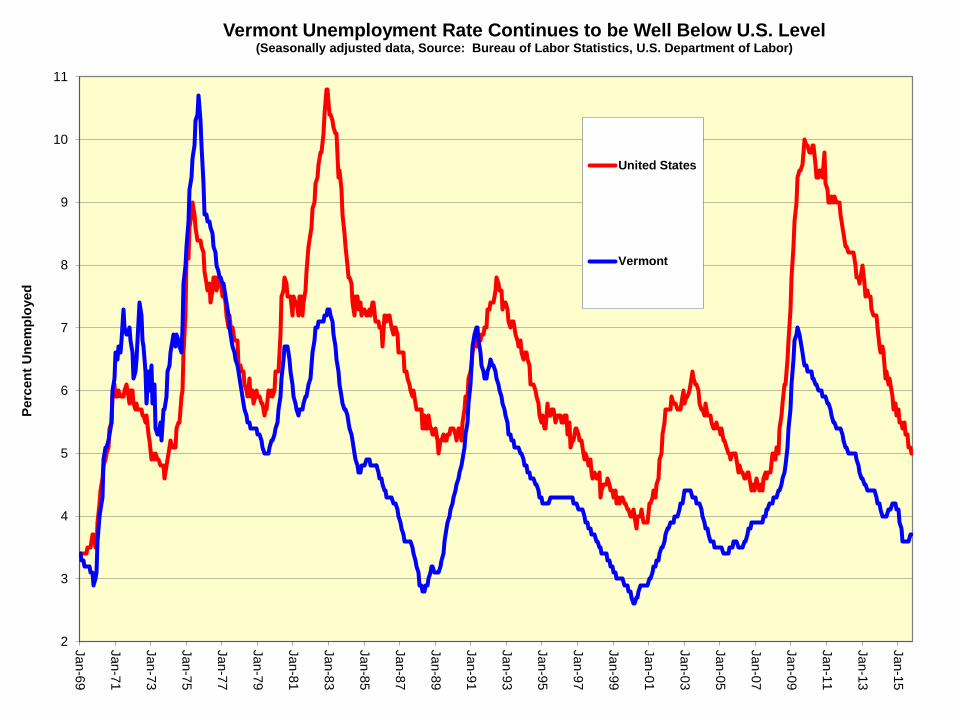

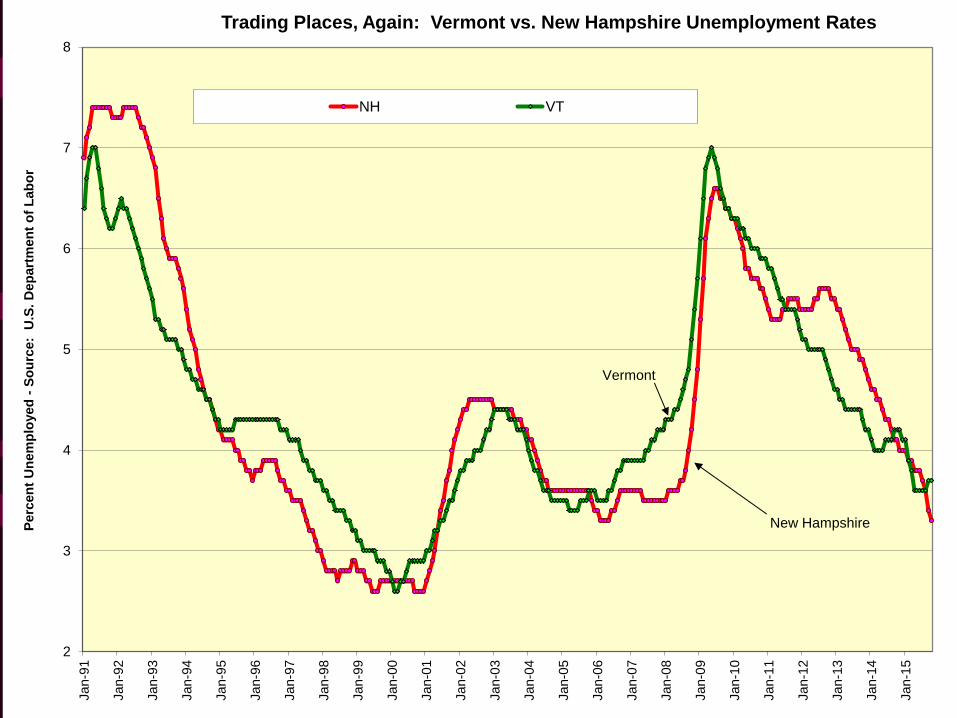

• Vermont’s unemployment rate is still among the top ten U.S. states, at 3.7%, however, it has been surpassed in the last two months in New England by New Hampshire, currently at 3.3%

• Initial Claims for Unemployment Insurance in Vermont dropped to their lowest levels in more than 25 years in September and portend continued improvement in the State labor market

• Real wage and income growth has remained flat or negative for lower income groups, with virtually all recent gains in income accruing to the highest income quintile

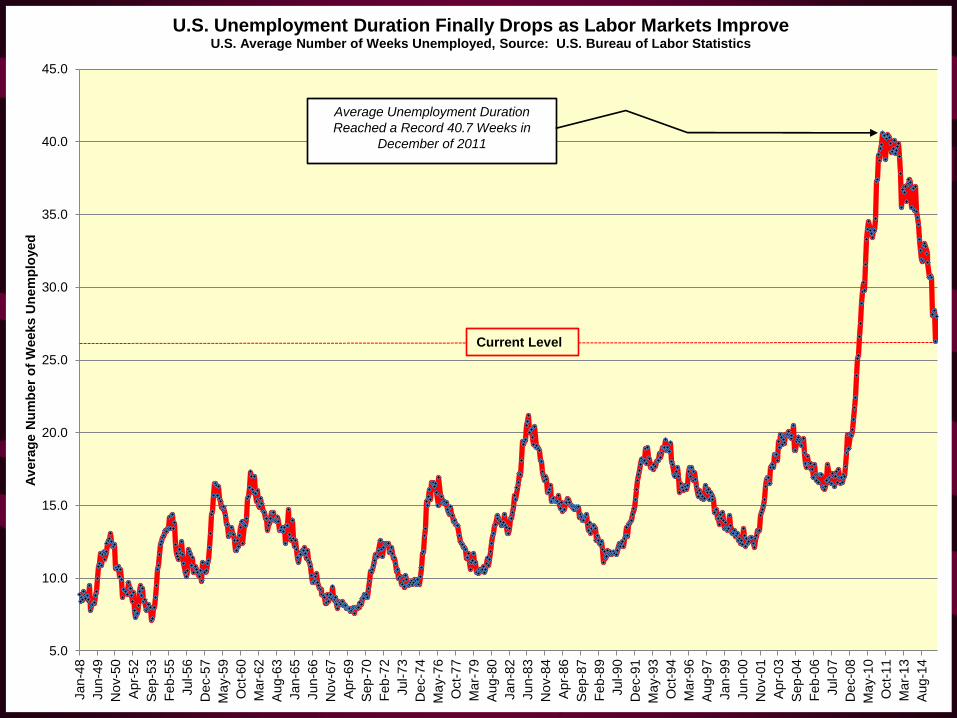

• Although chronic unemployment is reflected in a still elevated share of long-term unemployed workers, almost every measure of unemployment has improved in the last year

2

3

4

5

6

7

8

9

10

11

Jan-6

9

Jan-7

1

Jan-7

3

Jan-7

5

Jan-7

7

Jan-7

9

Jan-8

1

Jan-8

3

Jan-8

5

Jan-8

7

Jan-8

9

Jan-9

1

Jan-9

3

Jan-9

5

Jan-9

7

Jan-9

9

Jan-0

1

Jan-0

3

Jan-0

5

Jan-0

7

Jan-0

9

Jan-1

1

Jan-1

3

Jan-1

5

Perc

en

t U

nem

plo

yed

Vermont Unemployment Rate Continues to be Well Below U.S. Level

(Seasonally adjusted data, Source: Bureau of Labor Statistics, U.S. Department of Labor)

United States

Vermont

6.9%

6.8%

6.6%

6.6%

6.4%

6.2%

6.1%

6.0%

5.9%

5.9%

5.8%

5.7%

5.7%

5.6%

5.6%

5.4%

5.4%

5.3%

5.2%

5.1%

5.1%

5.1%

5.1%

5.1%

5.1%

5.0%

5.0%

4.9%

4.8%

4.6%

4.4%

4.4%

4.4%

4.3%

4.3%

4.3%

4.2%

4.1%

4.1%

4.0%

4.0%

3.8%

3.7%

3.7%

3.6%

3.5%

3.3%

3.3%

3.2%

2.9%

2.8%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

West Virginia

New Mexico

District of Columbia

Nevada

Alaska

Louisiana

Arizona

Oregon

Alabama

Mississippi

California

Georgia

North Carolina

South Carolina

Tennessee

Illinois

New Jersey

Rhode Island

Washington

Arkansas

Connecticut

Delaware

Florida

Maryland

Pennsylvania

Michigan

Missouri

Kentucky

New York

Massachusetts

Indiana

Ohio

Texas

Maine

Oklahoma

Wisconsin

Virginia

Kansas

Montana

Idaho

Wyoming

Colorado

Minnesota

Vermont

Utah

Iowa

Hawaii

New Hampshire

South Dakota

Nebraska

North Dakota

Unemployment Rate by State - October 2015 Seasonally Adjusted Data, Source: U.S. Bureau of Labor Statistics

2

3

4

5

6

7

8

Jan-9

1

Jan-9

2

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Jan-1

5

Perc

en

t U

nem

plo

yed

- S

ou

rce:

U.S

. D

ep

art

men

t o

f L

ab

or

Trading Places, Again: Vermont vs. New Hampshire Unemployment Rates

NH VT

Vermont

New Hampshire

500

550

600

650

700

750

800

850

900

950

1000

1050

1100

1150

1200

1250

1300

1350

1400

1450

1500

1550

1600Jan

-87

Jan

-88

Jan

-89

Jan

-90

Jan

-91

Jan-9

2

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan-0

2

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan-1

2

Jan

-13

Jan

-14

Jan

-15

Ave

rag

e W

ee

kly

Nu

mb

er

of

Cla

ims

Vermont Unemployment Insurance Claims Recede to a 25 Year Low,

Portending Tighter Labor Market Ahead (Average Weekly Initial Claims for Unemployment in Vermont, Seasonally Adjusted, Source: BLS and Boston Fed)

Tropical

Storm

Irene

0

2

4

6

8

10

12

14

16

18Jan-9

4

Jul-

94

Jan-9

5

Jul-

95

Jan-9

6

Jul-

96

Jan-9

7

Jul-

97

Jan-9

8

Jul-

98

Jan-9

9

Ju

l-9

9

Jan-0

0

Jul-

00

Jan-0

1

Jul-

01

Jan-0

2

Jul-

02

Jan-0

3

Jul-

03

Jan-0

4

Jul-

04

Jan-0

5

Jul-

05

Jan-0

6

Jul-

06

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Ju

l-1

2

Jan-1

3

Jul-

13

Jan-1

4

Jul-

14

Jan-1

5

Jul-

15

Perc

en

t U

nem

plo

yed

More Inclusive U.S. Unemployment Measures Depict Improvement,

as Steady Job Growth Firms Labor Markets Source: U.S. Bureau of Labor Statistics

Most Commonly Cited

"Official" Unemployment

Measure: U3

More Broadly Defined

Unemployment Measure,

Including Underemployed and

Discouraged Workers: U6

Long Term Unemployed: Out of

Work for More Than 6 Months

(and still looking for work)

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0Jan-4

8

Jun-4

9

No

v-5

0

Apr-

52

Sep-5

3

Fe

b-5

5

Jul-5

6

De

c-5

7

Ma

y-5

9

Oct-

60

Ma

r-6

2

Aug-6

3

Jan-6

5

Jun-6

6

No

v-6

7

Apr-

69

Sep-7

0

Feb

-72

Jul-7

3

De

c-7

4

Ma

y-7

6

Oct-

77

Ma

r-7

9

Aug-8

0

Jan-8

2

Jun-8

3

No

v-8

4

Apr-

86

Sep-8

7

Feb

-89

Jul-9

0

De

c-9

1

Ma

y-9

3

Oct-

94

Ma

r-9

6

Aug-9

7

Jan-9

9

Jun-0

0

No

v-0

1

Apr-

03

Sep-0

4

Feb

-06

Jul-0

7

De

c-0

8

Ma

y-1

0

Oct-

11

Ma

r-1

3

Aug-1

4

Av

era

ge N

um

ber

of

Weeks U

nem

plo

yed

U.S. Unemployment Duration Finally Drops as Labor Markets Improve

U.S. Average Number of Weeks Unemployed, Source: U.S. Bureau of Labor Statistics

Average Unemployment Duration

Reached a Record 40.7 Weeks in

December of 2011

Current Level

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

June-2007 October-2015

Eight Years Later: Change in Vermont Employment Since Prior Peak Current Employment by Industry in October 2015 Indexed to Prior Peak Levels (June 2007 = 1.00), Seasonally Adjusted Data , VT DOL

Trade,,Transportation and Utilities

Financial Activities

Construction

Manufacturing

Private Education Services

Other Services

Leisure and Hospitality

Federal Government

Healthcare and Social

Assistance

Professional and Business

Services

State Government

Local Government Total Employment

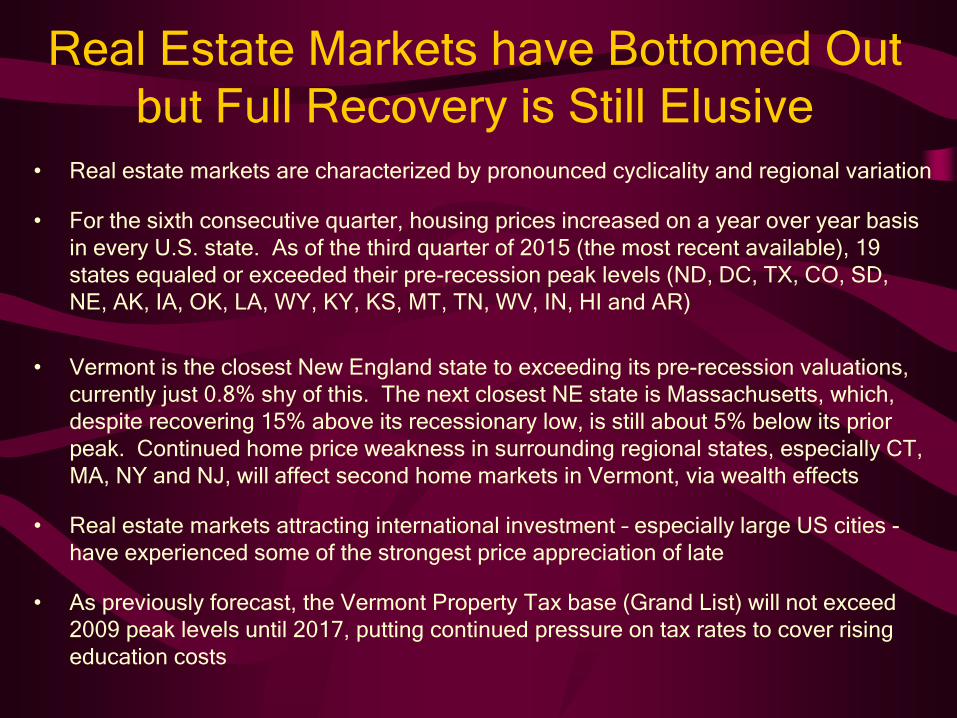

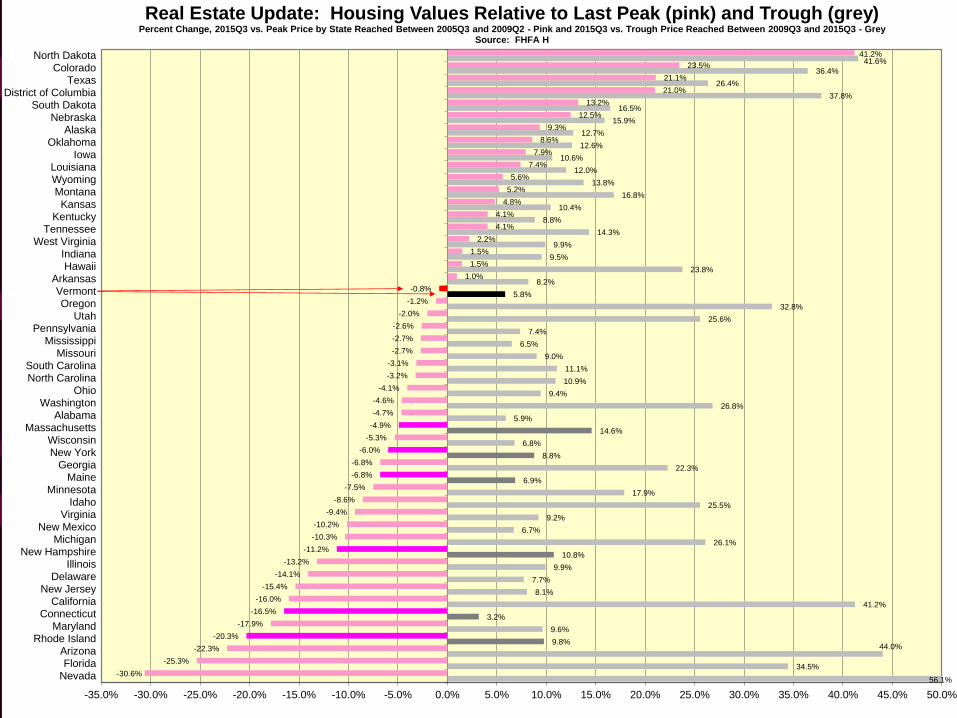

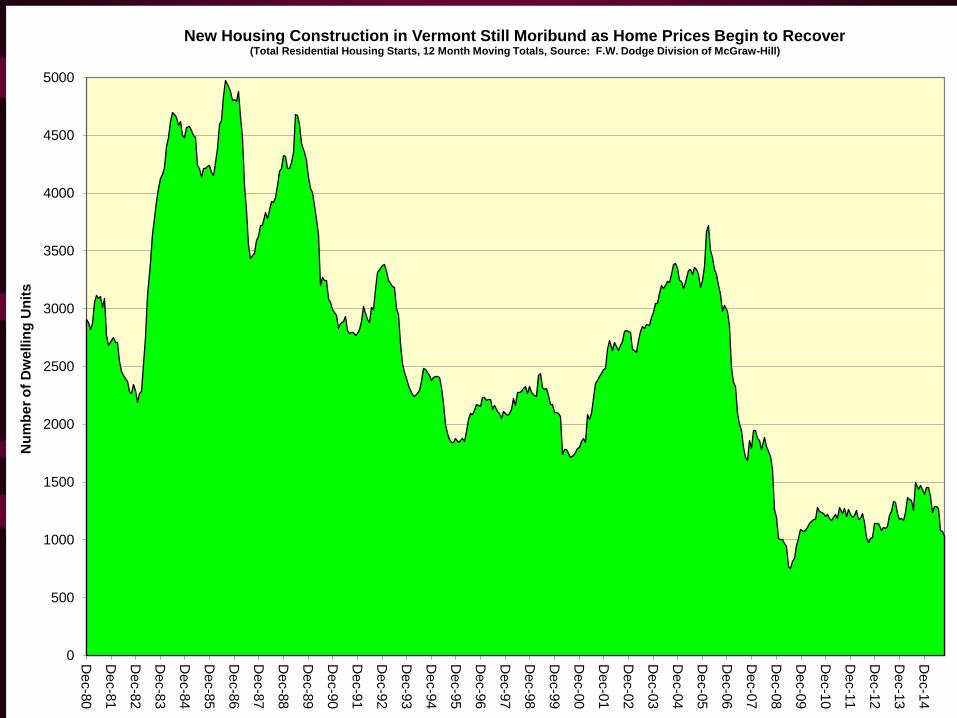

Real Estate Markets have Bottomed Out

but Full Recovery is Still Elusive • Real estate markets are characterized by pronounced cyclicality and regional variation

• For the sixth consecutive quarter, housing prices increased on a year over year basis

in every U.S. state. As of the third quarter of 2015 (the most recent available), 19

states equaled or exceeded their pre-recession peak levels (ND, DC, TX, CO, SD,

NE, AK, IA, OK, LA, WY, KY, KS, MT, TN, WV, IN, HI and AR)

• Vermont is the closest New England state to exceeding its pre-recession valuations,

currently just 0.8% shy of this. The next closest NE state is Massachusetts, which,

despite recovering 15% above its recessionary low, is still about 5% below its prior

peak. Continued home price weakness in surrounding regional states, especially CT,

MA, NY and NJ, will affect second home markets in Vermont, via wealth effects

• Real estate markets attracting international investment – especially large US cities -

have experienced some of the strongest price appreciation of late

• As previously forecast, the Vermont Property Tax base (Grand List) will not exceed

2009 peak levels until 2017, putting continued pressure on tax rates to cover rising

education costs

34.5%

44.0% 9.8%

9.6%

3.2%

41.2%

8.1%

7.7%

9.9%

10.8%

26.1%

6.7%

9.2%

25.5%

17.9%

6.9%

22.3%

8.8%

6.8%

14.6%

5.9%

26.8%

9.4%

10.9%

11.1%

9.0%

6.5%

7.4%

25.6%

32.8%

5.8%

8.2%

23.8%

9.5%

9.9%

14.3%

8.8%

10.4%

16.8%

13.8%

12.0%

10.6%

12.6%

12.7%

15.9%

16.5%

37.8%

26.4%

36.4%

41.6%

-30.6%

-25.3%

-22.3%

-20.3%

-17.9%

-16.5%

-16.0%

-15.4%

-14.1%

-13.2%

-11.2%

-10.3%

-10.2%

-9.4%

-8.6%

-7.5%

-6.8%

-6.8%

-6.0%

-5.3%

-4.9%

-4.7%

-4.6%

-4.1%

-3.2%

-3.1%

-2.7%

-2.7%

-2.6%

-2.0%

-1.2%

-0.8%

1.0%

1.5%

1.5%

2.2%

4.1%

4.1%

4.8%

5.2%

5.6%

7.4%

7.9%

8.6%

9.3%

12.5%

13.2%

21.0%

21.1%

23.5%

41.2%

-35.0% -30.0% -25.0% -20.0% -15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0%

NevadaFlorida

ArizonaRhode Island

MarylandConnecticut

CaliforniaNew Jersey

DelawareIllinois

New HampshireMichigan

New MexicoVirginia

IdahoMinnesota

MaineGeorgia

New YorkWisconsin

MassachusettsAlabama

WashingtonOhio

North CarolinaSouth Carolina

MissouriMississippi

PennsylvaniaUtah

OregonVermont

ArkansasHawaii

IndianaWest Virginia

TennesseeKentucky

KansasMontanaWyomingLouisiana

IowaOklahoma

AlaskaNebraska

South DakotaDistrict of Columbia

TexasColorado

North Dakota

Real Estate Update: Housing Values Relative to Last Peak (pink) and Trough (grey) Percent Change, 2015Q3 vs. Peak Price by State Reached Between 2005Q3 and 2009Q2 - Pink and 2015Q3 vs. Trough Price Reached Between 2009Q3 and 2015Q3 - Grey

Source: FHFA H

56.1%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%1

98

4Q

3

198

5Q

3

198

6Q

3

198

7Q

3

198

8Q

3

198

9Q

3

199

0Q

3

199

1Q

3

199

2Q

3

199

3Q

3

199

4Q

3

199

5Q

3

199

6Q

3

199

7Q

3

199

8Q

3

199

9Q

3

200

0Q

3

200

1Q

3

200

2Q

3

200

3Q

3

200

4Q

3

200

5Q

3

200

6Q

3

200

7Q

3

200

8Q

3

200

9Q

3

201

0Q

3

201

1Q

3

201

2Q

3

201

3Q

3

201

4Q

3

201

5Q

3

201

6Q

3

201

7Q

3

201

8Q

3

201

9Q

3

202

0Q

3

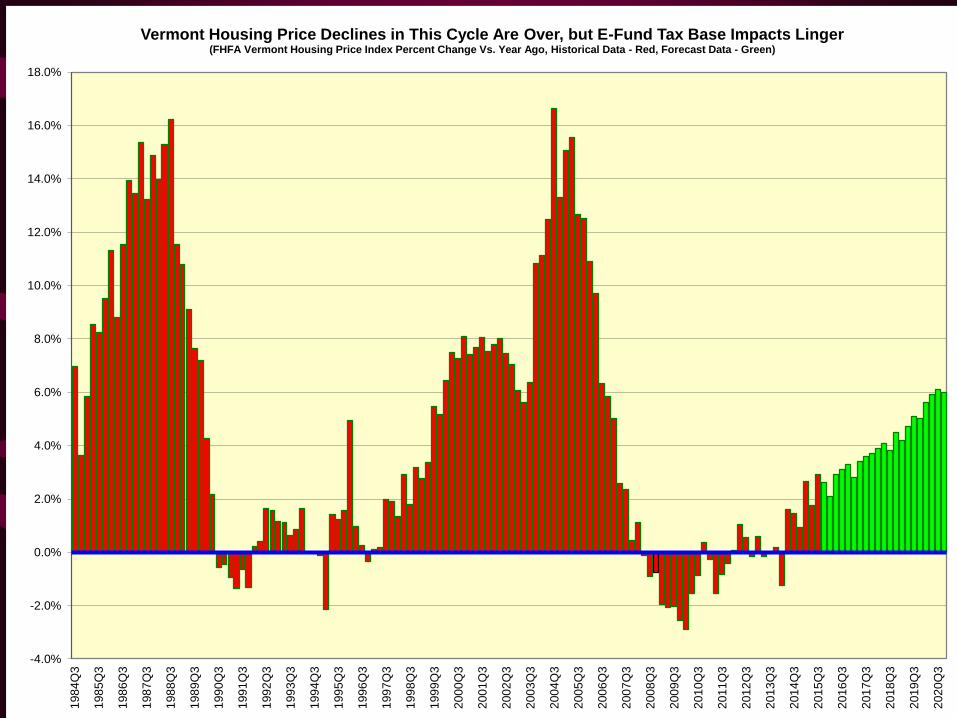

Vermont Housing Price Declines in This Cycle Are Over, but E-Fund Tax Base Impacts Linger (FHFA Vermont Housing Price Index Percent Change Vs. Year Ago, Historical Data - Red, Forecast Data - Green)

66.7

118.1

169.4

220.7

272.1

323.4

374.7

426.1

477.4

528.7

580.1

5.0

15.0

25.0

35.0

45.0

55.0

65.0

75.0

85.0

95.0

105.0

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Ho

me

Pri

ce

In

de

x, 1

98

0Q

1=

10

0

Eq

ua

lize

d E

du

ca

tio

n G

ran

d L

ist

- B

illi

on

s o

f D

oll

ars

Sources: Vermont PVR; U.S. FHFA; Prepared for the Joint Fiscal Office by Kavet, Rockler & Associates, October 2014

Vermont Adjusted Equalized Education Grand List (thick red line, left scale) Vs. FHFA Vermont Home Price Index, (Index 1980Q1 = 100)

Lagged Five Quarters (thin green line, right scale)

FORECAST

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

De

c-8

0

De

c-8

1

De

c-8

2

De

c-8

3

Dec-8

4

Dec-8

5

De

c-8

6

De

c-8

7

De

c-8

8

De

c-8

9

De

c-9

0

De

c-9

1

De

c-9

2

De

c-9

3

De

c-9

4

Dec-9

5

De

c-9

6

De

c-9

7

De

c-9

8

De

c-9

9

De

c-0

0

De

c-0

1

De

c-0

2

De

c-0

3

De

c-0

4

De

c-0

5

Dec-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

De

c-1

4N

um

be

r o

f D

we

llin

g U

nit

s

New Housing Construction in Vermont Still Moribund as Home Prices Begin to Recover (Total Residential Housing Starts, 12 Month Moving Totals, Source: F.W. Dodge Division of McGraw-Hill)

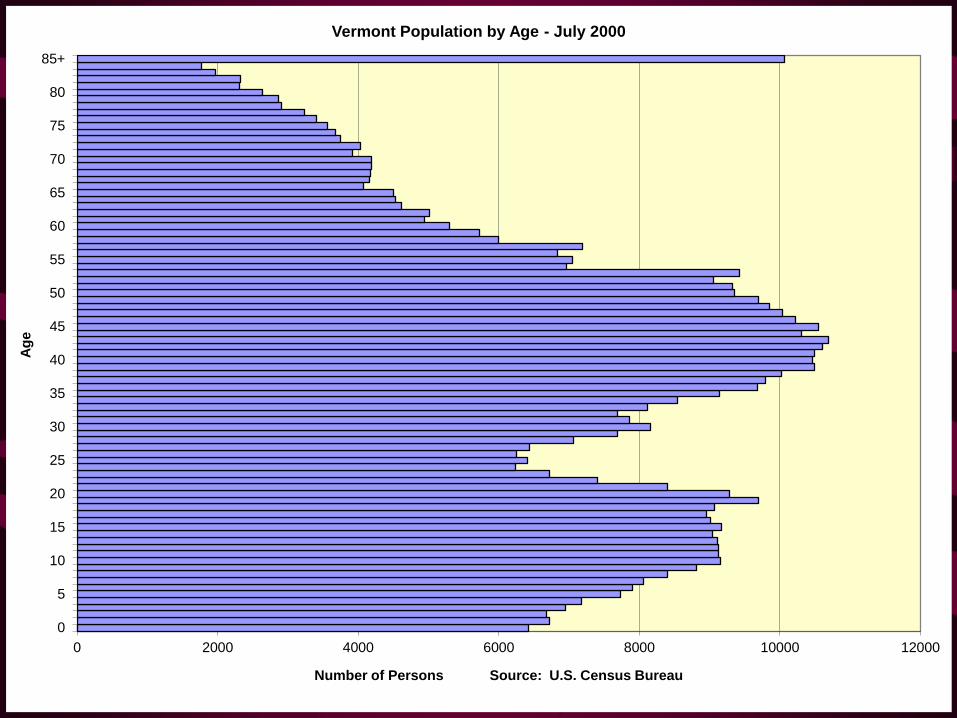

The Economy is About People:

Vermont Demographics

• A major new State demographic analysis is currently being undertaken by JFO and Administration economists, using detailed, and previously unavailable, Health Department data at the Town level. Output from this analysis should be available within the next year

• The movement over time of the “baby-boom” population bulge continues to dominate VT and U.S. demographics, and is responsible for the aging profile of both. The children of this large cohort, referred to as the “baby-boom echo,” represents a much more diffuse wave, as families have fewer children and at older ages

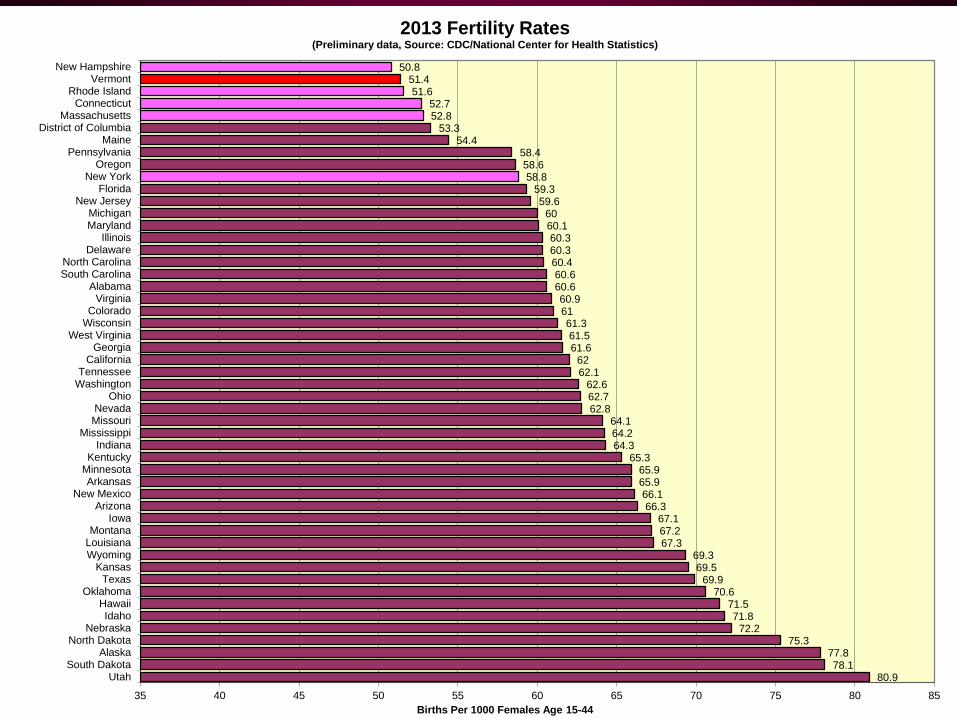

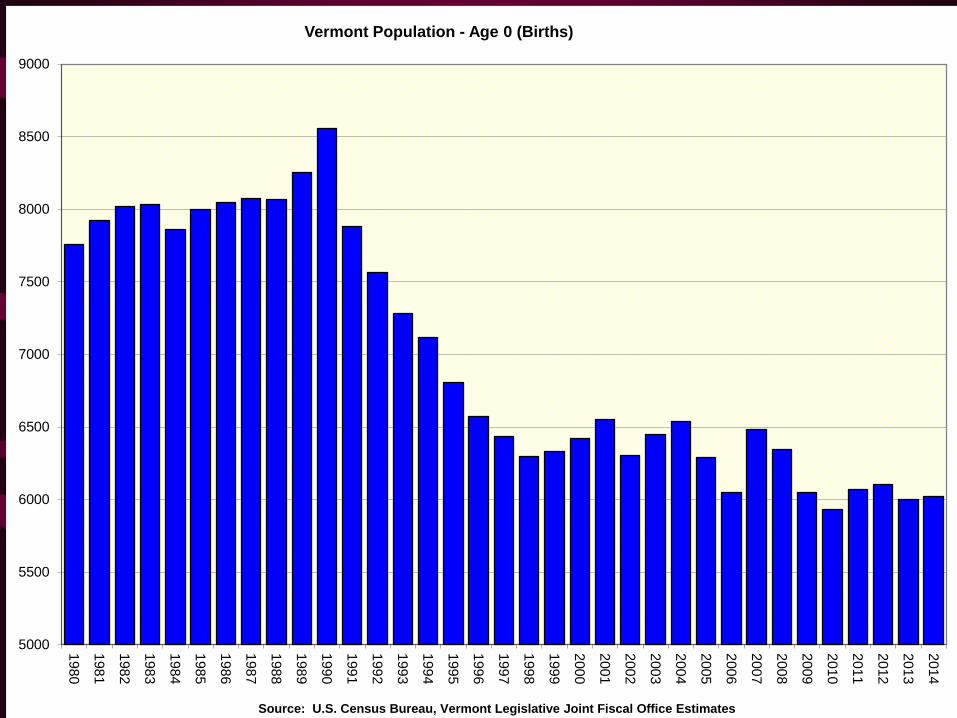

• Significant declines in fertility rates in the past 20 years have dropped Vermont births from about 8,000 per year in the early 1990’s to about 6,000 per year at present

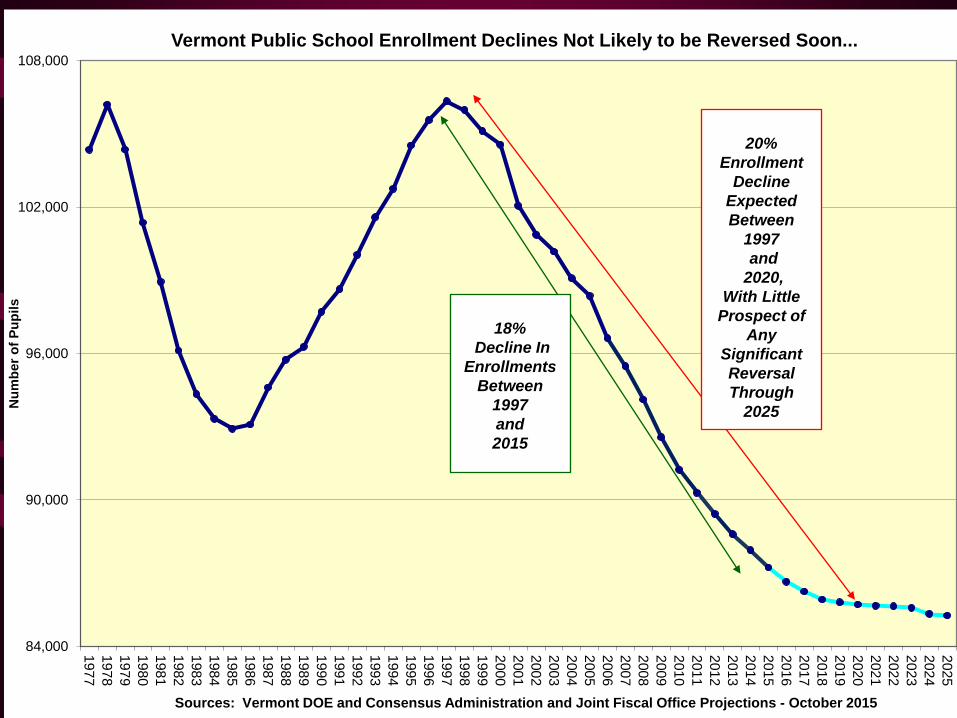

• In addition to the large declines in enrollments experienced in the State over the past 20 years, these two demographic events have (since 2011) and will combine to create declines in the prime working age population, ages 25-64 over the next 20 years. This, in turn, will affect employment, earned income and selected tax revenues in the State

80.9 78.1

77.8 75.3

72.2 71.8

71.5 70.6

69.9 69.5

69.3 67.3 67.2 67.1

66.3 66.1

65.9 65.9

65.3 64.3 64.2 64.1

62.8 62.7 62.6

62.1 62

61.6 61.5

61.3 61 60.9

60.6 60.6

60.4 60.3 60.3

60.1 60

59.6 59.3

58.8 58.6

58.4 54.4

53.3 52.8 52.7

51.6 51.4

50.8

35 40 45 50 55 60 65 70 75 80 85

UtahSouth Dakota

AlaskaNorth Dakota

NebraskaIdaho

HawaiiOklahoma

TexasKansas

WyomingLouisianaMontana

IowaArizona

New MexicoArkansas

MinnesotaKentucky

IndianaMississippi

MissouriNevada

OhioWashingtonTennessee

CaliforniaGeorgia

West VirginiaWisconsinColorado

VirginiaAlabama

South CarolinaNorth Carolina

DelawareIllinois

MarylandMichigan

New JerseyFlorida

New YorkOregon

PennsylvaniaMaine

District of ColumbiaMassachusetts

ConnecticutRhode Island

VermontNew Hampshire

Births Per 1000 Females Age 15-44

2013 Fertility Rates (Preliminary data, Source: CDC/National Center for Health Statistics)

5000

5500

6000

6500

7000

7500

8000

8500

9000

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

Source: U.S. Census Bureau, Vermont Legislative Joint Fiscal Office Estimates

Vermont Population - Age 0 (Births)

21

22

23

24

25

26

27

28

29

3019

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Ag

e o

f M

oth

er

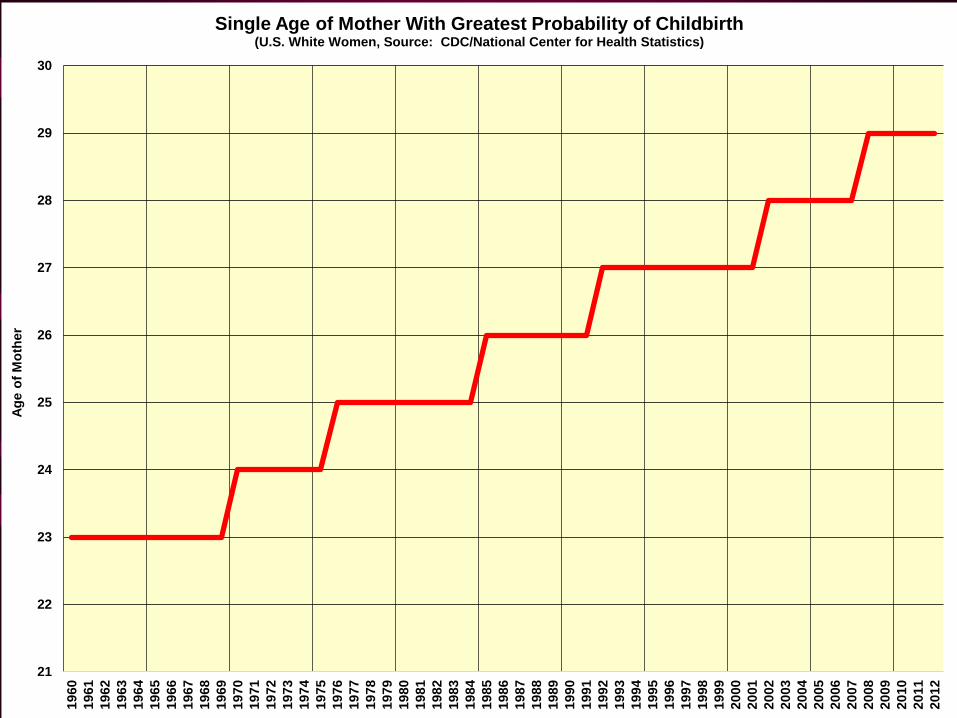

Single Age of Mother With Greatest Probability of Childbirth (U.S. White Women, Source: CDC/National Center for Health Statistics)

84,000

90,000

96,000

102,000

108,000

197

7

197

8

197

9

198

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

2023

2024

2025

Nu

mb

er

of

Pu

pils

Sources: Vermont DOE and Consensus Administration and Joint Fiscal Office Projections - October 2015

Vermont Public School Enrollment Declines Not Likely to be Reversed Soon...

18%

Decline In

Enrollments

Between

1997

and

2015

20%

Enrollment

Decline

Expected

Between

1997

and

2020,

With Little

Prospect of

Any

Significant

Reversal

Through

2025

0 2000 4000 6000 8000 10000 12000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Number of Persons Source: U.S. Census Bureau

Ag

e

Vermont Population by Age - July 1980

0 2000 4000 6000 8000 10000 12000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Number of Persons Source: U.S. Census Bureau

Ag

e

Vermont Population by Age - July 1990

0 2000 4000 6000 8000 10000 12000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Number of Persons Source: U.S. Census Bureau

Ag

e

Vermont Population by Age - July 2000

0 2000 4000 6000 8000 10000 12000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Number of Persons Source: U.S. Census Bureau

Ag

e

Vermont Population by Age - July 2010

Age 85+ = 12,874

0 2000 4000 6000 8000 10000 12000

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85+

Number of Persons Source: U.S. Census Bureau

Ag

e

Vermont Population by Age - July 2020

Age 85+ = 16,320

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Perc

en

t C

han

ge v

s. Y

ear-

Ag

o

Prime Working Age Population Growth vs. Total Population Growth in Vermont

Total Population

Ages 25 to 64

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51 53 55 57 59 61 63 65 67 69 71 73 75 77 79 81 83 85

Ad

jus

ted

Gro

ss

In

co

me

Age

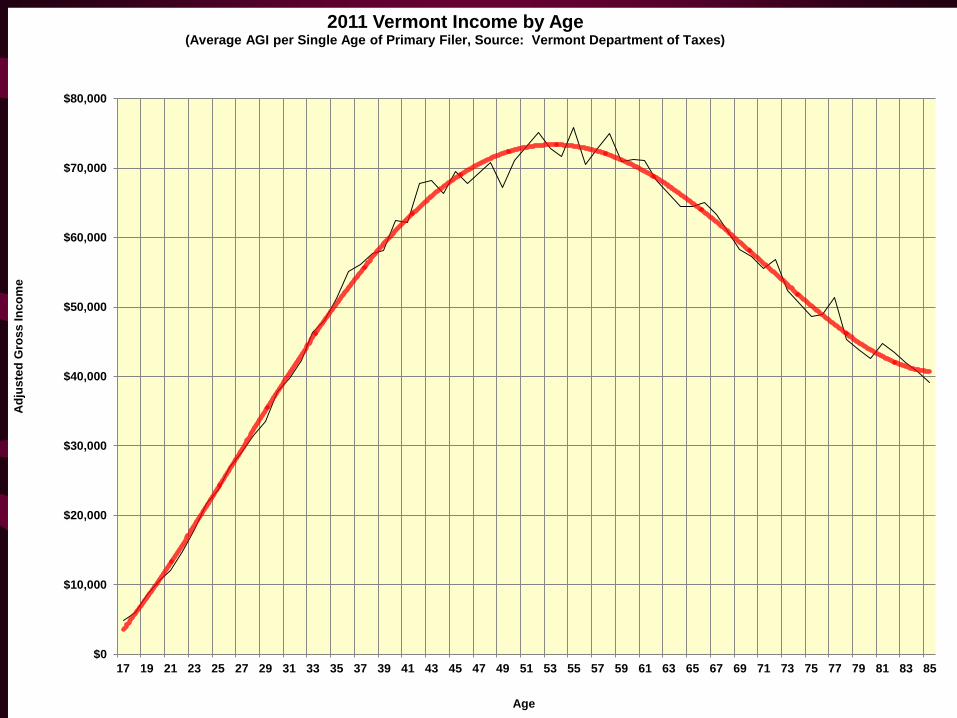

2011 Vermont Income by Age (Average AGI per Single Age of Primary Filer, Source: Vermont Department of Taxes)

Forecast Risks Remain

• The age and tenuity of the recovery makes the current expansion more susceptible to external shocks, such as severe weather, Fed miscalculation and other policy mistakes, and external global economic crises (especially emanating from China and other emerging countries), including military conflict

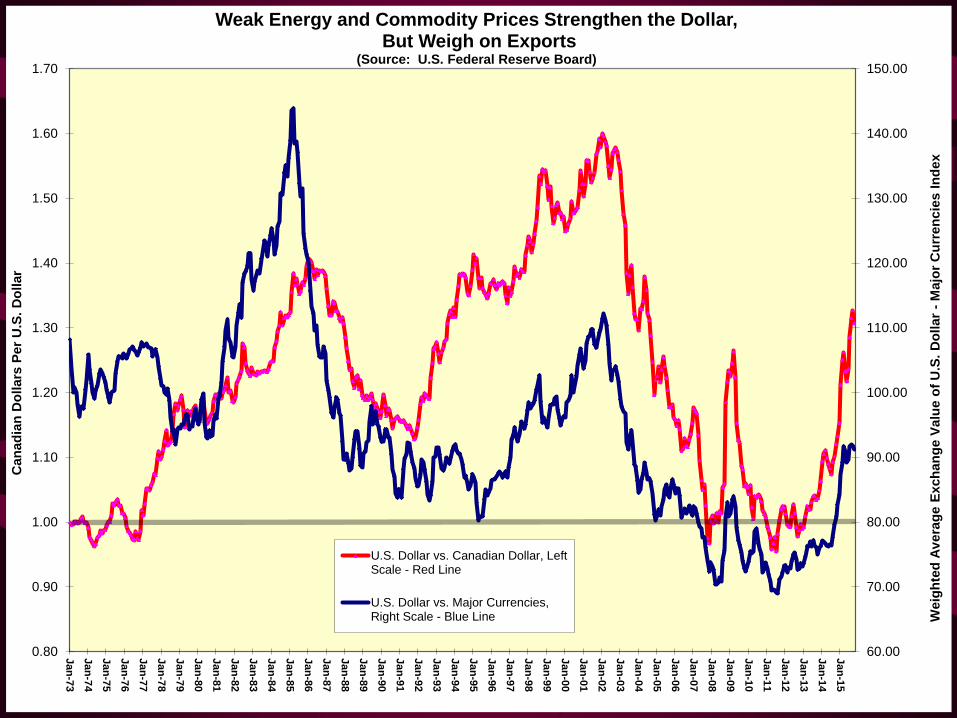

• Prominent near-term hazards include continued strengthening of the U.S. dollar and attendant export weakness and domestic industrial stress. Vermont has already experienced a 24% decline in exports over the past three years, during this period of rising exchange rates. The exchange rate with Canada, our largest trading partner, has been particularly impacted, rising more than 35%

• Slumping productivity growth of late threatens to limit non-inflationary potential economic growth to under 1%. New business formations, despite ample credit, are also abnormally low – only slightly above recessionary lows. Unless these important components of economic health recover, it could cripple future growth

• Widening income distribution inequality in the U.S. will dampen demand and slow growth relative to “normal” demographic-based indicators

• The rapid recent rise in equity markets could make them vulnerable to correction and amplify impacts from other negative events affecting market valuations and/or psychology

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

196

0Q

1

196

1Q

3

196

3Q

1

196

4Q

3

196

6Q

1

196

7Q

3

196

9Q

1

197

0Q

3

1972Q

1

1973Q

3

1975Q

1

197

6Q

3

197

8Q

1

197

9Q

3

198

1Q

1

198

2Q

3

198

4Q

1

198

5Q

3

198

7Q

1

198

8Q

3

199

0Q

1

199

1Q

3

199

3Q

1

199

4Q

3

199

6Q

1

1997Q

3

1999Q

1

200

0Q

3

200

2Q

1

200

3Q

3

200

5Q

1

200

6Q

3

200

8Q

1

200

9Q

3

201

1Q

1

201

2Q

3

201

4Q

1

Pe

rce

nt

Ch

an

ge

Vs

. Y

ea

r A

go

(T

rou

gh

to

Pe

ak

Pe

rce

nt

Ch

an

ge

in

Bu

bb

les

)

Running Out of Steam? Corporate Profit Growth Slows as Recovery Ages U.S. corporate profits with inventory valuation and capital consumption adjustment; Source: US BEA;

Data in bubbles indicate number of consecutive quarters of growth and trough to peak p

20 Q

+118% 12 Q

+63%

12 Q

+66% 18 Q

+111%

22 Q

+91%

10 Q

+32% 29 Q

+115%

17Q

+111%

60.00

70.00

80.00

90.00

100.00

110.00

120.00

130.00

140.00

150.00

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

1.70

Jan

-73

Jan

-74

Jan

-75

Jan

-76

Jan

-77

Jan

-78

Jan

-79

Jan

-80

Jan

-81

Jan

-82

Jan

-83

Jan

-84

Jan

-85

Jan

-86

Jan

-87

Jan

-88

Jan

-89

Jan

-90

Jan

-91

Jan

-92

Jan

-93

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Weig

hte

d A

vera

ge E

xch

an

ge V

alu

e o

f U

.S.

Do

llar

- M

ajo

r C

urr

en

cie

s I

nd

ex

Can

ad

ian

Do

llars

Per

U.S

. D

ollar

Weak Energy and Commodity Prices Strengthen the Dollar, But Weigh on Exports

(Source: U.S. Federal Reserve Board)

U.S. Dollar vs. Canadian Dollar, LeftScale - Red Line

U.S. Dollar vs. Major Currencies,Right Scale - Blue Line

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

18.0%

21.0%

24.0%

27.0%

30.0%

33.0%

36.0%

39.0%

42.0%

45.0%

48.0%

51.0%

54.0%

57.0%

60.0%

63.0%

66.0%

69.0%

72.0%

2250

2500

2750

3000

3250

3500

3750

4000

4250

4500

4750

199

7Q

4

199

8Q

2

199

8Q

4

199

9Q

2

199

9Q

4

200

0Q

2

200

0Q

4

200

1Q

2

200

1Q

4

200

2Q

2

200

2Q

4

200

3Q

2

200

3Q

4

200

4Q

2

200

4Q

4

200

5Q

2

200

5Q

4

200

6Q

2

200

6Q

4

200

7Q

2

200

7Q

4

200

8Q

2

200

8Q

4

200

9Q

2

200

9Q

4

201

0Q

2

201

0Q

4

201

1Q

2

201

1Q

4

201

2Q

2

201

2Q

4

201

3Q

2

201

3Q

4

201

4Q

2

Sh

are

of

Verm

on

t E

xp

ort

s t

o C

an

ad

a a

nd

Ch

ina -

4 Q

uart

er

Mo

vin

g T

ota

ls

To

tal V

T E

xp

ort

s -

Millio

ns o

f D

ollars

- 4

Qu

art

er

Mo

vin

g T

ota

ls

Canada and China Account for About 65% of All Vermont Exports (Source: World Institute of Strategic Economic Research, Federal Reseve Bank of Boston)

Total Vermont Exports - Left Scale

Canadian Share of VT Exports - Right Scale

China Share of Vermont Exports - Right Scale

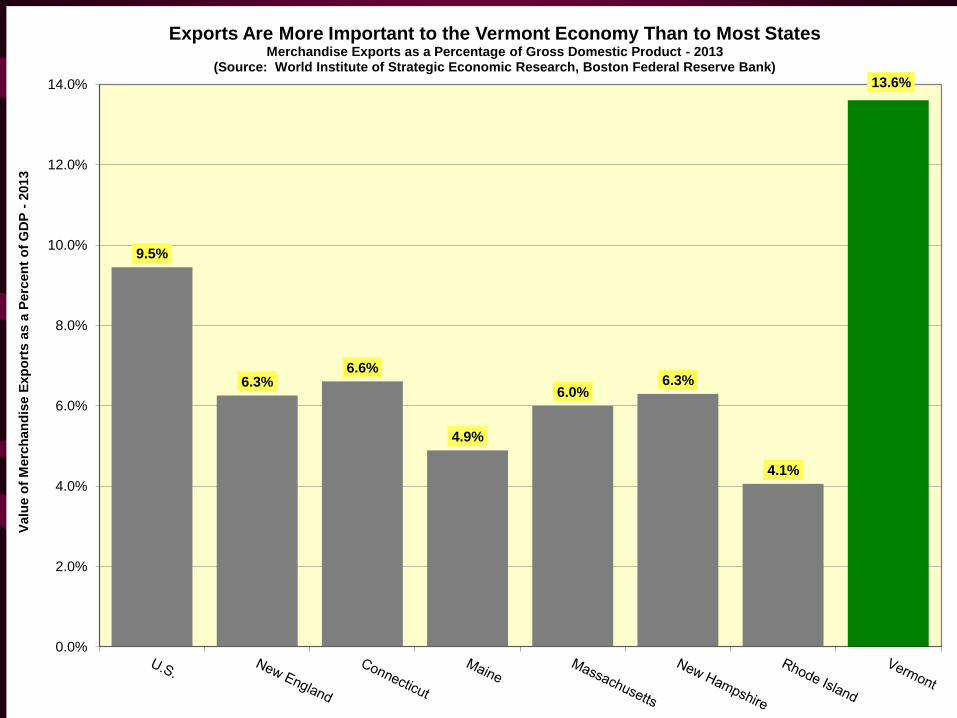

9.5%

6.3% 6.6%

4.9%

6.0% 6.3%

4.1%

13.6%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

Valu

e o

f M

erc

han

dis

e E

xp

ort

s a

s a

Perc

en

t o

f G

DP

- 2

013

Exports Are More Important to the Vermont Economy Than to Most States Merchandise Exports as a Percentage of Gross Domestic Product - 2013

(Source: World Institute of Strategic Economic Research, Boston Federal Reserve Bank)

For Further Information, Contact

The Vermont Joint Fiscal Office or:

Thomas E. Kavet, President

Dr. Nicolas O. Rockler, CEO

State Economist and Principal Economic Advisor to the Vermont State Legislature Since 1996

Kavet, Rockler & Associates, LLC

Economic and Public Policy Consulting

985 Grandview Road Williamstown, Vermont 05679-9003 USA Telephone: 802-433-1360 Facsimile: 866-433-1360 Cellular: 802-433-1111 Website: www.kavetrockler.com E-Mail: [email protected]