economic and social overview of latin america and caribbean · latin america (18 countries): ......

TRANSCRIPT

Economic and social overview of Latin America and Caribbean

Meeting of the Regional Coordination Mechanism for Latin America and the Caribbean - Santiago, 24 January 2013 Antonio Prado, Deputy Executive Secretary

Contents

• The region in the context of the global crisis:

recent trends in economic and social

development

• Long-run challenges to achieve structural

change for equality

Crises have traditionally cut deep into the social fabric in the region

LATIN AMERICA AND THE CARIBBEAN: COMPARISON OF PER CAPITA GDP AND POVERTY RATES, 1980-2011

Source: ECLAC, on the basis of specia tabulations of household surveys

Poverty GDP per capita

Source: Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of special tabulations of household surveys

conducted in the respective countries.

a Data for urban areas in Argentina, Ecuador and Uruguay. Data for 2002 are from 2002 except for Brazil, El Salvador, Nicaragua, Paraguay

and Peru (2001), Argentina (2004) and Chile (2000). Data for 2011 are from 2011 except for Costa Rica, Nicaragua and the Plurinational State

of Bolivia (2009), El Salvador, Honduras and Mexico (2010) and Guatemala (2006). b Data for urban areas in Argentina. Data for 2010 refer to figures for 2009 in Brazil and Chile.

LATIN AMERICA (18 COUNTRIES): GINI COEFFICIENT, 2002-2011 AND 2010-2011

There has been a clear reduction in inequality since 2002, and this continued in 2011

This crisis current is different: a recession caused by a financial crisis arising from

private over indebtedness

• Recessions of this sort are longer and impact more heavily on output and employment.

• Recoveries are precarious and highly vulnerable to economic or financial volatility.

• Necessary private debt reduction takes place in periods of slack economic activity and asset value slippage.

• Deleveraging and recomposition of private savings make monetary stimulus measures less effective.

• Emerging economies and South-South trade have been key in global growth

Since the beginning of this crisis, Latin America and the Caribbean showed a certain resilience

Downside

Trade contraction, especially towards Europe and China

Adverse climate factors (soy)

Insufficient investment limited the growth capacity (supply)

Some exchange rate volatility (Brazil and Mexico)

Lower financial inflows to the region

Upside

GDP growth of 3.1% (above the global average of 2.2%) in 2012

Fall in unemployment (to 6.4%) and an increase in average wages

Accommodative monetary policy and continued reserve accumulation

Increased investment and consumption

Fiscal prudence

External context 2012

• Financial, fiscal and competiveness imbalances in the Euro area were associated with:

– A recession in the majority of the countries of the EZ, with economic growth of -0.5%

– A slow process of joint problem solving, although with the decision of the ECB to intervene under certain conditions

– Financial instability, though with improvements in the risk premiums in the EZ during the second half

• Slowdown in China, from 9.2% in 2011 to 7.7% in 2012

• Modest growth in the USA, between 1.8% and 2.1%

• Absence of shocks in the oil market

Global economic growth decelerated

GLOBAL GDP GROWTH BY REGION, 2010 – 2013 (in percentage)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on UN/DESA. a/ Estimate. b/ Projection.

4.0

2.7

2.2 2.4

2.1

1.5

-0.5

0.3

2.4

1.8 2.1

1.7

6.0

4.3

3.1

3.8

7.7

5.7

4.7 5.1

10.3

9.2

7.7 7.9

4.5

-0.7

1.5

0.6

-2

0

2

4

6

8

10

12

2010 2011 2012 a/ 2013 b/

World Euro area United States Latin America and the Caribbean Developing economies China Japan

LATIN AMERICA AND THE CARIBBEAN: CONTRIBUTION TO REGIONAL GDP GROWTH BY COUNTRY, 2004 – 2012a

Regional GDP grew by 3.1% in 2012, above the global average (2.2%)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Figures for 2012 correspond to estimations.

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7% 2

00

4

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Brazil

Argentina

The Caribbean

Mexico

Central America

Rest of South America

Latin America and the Caribbean

LATIN AMERICA AND THE CARIBBEAN: GDP GROWTH RATES, 2012a (Percentages)

The majority of Latin America countries posted growth above 3.1% in 2012

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Estimate

-1.8

1.1

1.2

1.2

2.2

2.5

2.7

3.0

3.1

3.1

3.3

3.5

3.8

3.8

3.8

4.0

4.2

4.5

4.8

5.0

5.0

5.3

5.5

6.2

10.5

-4 -2 0 2 4 6 8 10 12

Paraguay

The Caribbean

Brazil

El Salvador

Argentina

Haiti

South America (10 countries)

Cuba

Latin America and the Caribbean

Latin America

Guatemala

Honduras

Dominican Republic

Mexico

Uruguay

Nicaragua

Central America (9 countries)

Colombia

Ecuador

Bolivia (Plur. St. of)

Costa Rica

Venezuela (Bol. Rep. of)

Chile

Peru

Panama

THE CARIBBEAN: GDP GROWTH RATES, 2012a (Percentages)

Growth in the Caribbean increased from 0.4% in 2011 to 1.1% in 2012

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Estimate

-0.8

-0.2

0.2

0.2

0.9

0.9

1.0

1.1

1.5

1.6

2.5

3.1

3.6

3.8

4.2

-2 -1 0 1 2 3 4 5

Saint Kitts and Nevis

Jamaica

Granada

Barbados

Saint Lucia

Antigua and Barbuda

Trinidad and Tobago

The Caribbean

Saint Vincent and the Grenadines

Dominica

Bahamas

Latin America and the Caribbean

Suriname

Guyana

Belize

Consumption continued to be the most important driver of growth

LATIN AMERICA: CONTRIBUTION TO GDP GROWTH, 2008 – 2012a

(As a percentage of GDP)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Figures for 2012 correspond to estimations.

-4%

-2%

0%

2%

4%

6%

8%

10%

20

08

20

09

20

10

20

11

20

12

Private Consumption General Government Consumption Investment Net Exports GDP

The region’s investment coefficient has continued to grow persistently

LATIN AMERICA: GROSS FIXED CAPITAL FORMATION AS A PERCENTAGE OF GDP, 1980 – 2012a

(2005 constant dollars)

0%

5%

10%

15%

20%

25%

30% 1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Figures for 2012 correspond to estimations.

FDI inflows remained above 120 billion dollars

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2008 2009 2010 2011 2012

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Figures for 2012 correspond to estimations.

LATIN AMERICA AND THE CARIBBEAN: FOREIGN DIRECT INVESTMENT INFLOWS, 2008 – 2012a (In millions of dollars)

Inflation slowed, with some exceptions

LATIN AMERICA AND THE CARIBBEAN: CONSUMER PRICE INDEX, Jan 2008 – Oct 2012 (Rate of change over twelve months)

0%

2%

4%

6%

8%

10%

12%

14%

16% Ja

nu

ary

Feb

ruar

y M

arch

A

pri

l M

ay

Jun

e Ju

ly

Au

gust

Se

pte

mb

er

Oct

ob

er

No

vem

be

r D

ecem

be

r Ja

nu

ary

Feb

ruar

y M

arch

A

pri

l M

ay

Jun

e Ju

ly

Au

gust

Se

pte

mb

er

Oct

ob

er

No

vem

be

r D

ecem

be

r Ja

nu

ary

Feb

ruar

y M

arch

A

pri

l M

ay

Jun

e Ju

ly

Au

gust

Se

pte

mb

er

Oct

ob

er

No

vem

be

r D

ecem

be

r Ja

nu

ary

Feb

ruar

y M

arch

A

pri

l M

ay

Jun

e Ju

ly

Au

gust

Se

pte

mb

er

Oct

ob

er

2009 2010 2011 2012

CPI Food Core

International reserves accumulation continued throughout the region, though at a slower rate than in 2011

GROSS INTERNATIONAL RESERVES, 2001 - 2012 (Millions of dollars and as a percentage of GDP)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures.

45,274

751

13,772

377,753

38,943

36,402

5,366 6,804

1,400

2,524

1,990

165,590

1,856 4,838

62,212

3,347

9,326

13,120

25,864

0%

10%

20%

30%

40%

50%

60%

October 2011 October 2012

INTERNATIONAL PRICE INDICES OF COMMODITIES AND MANUFACTURES, 2008-2012 (2005=100, three month moving average)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on figures from the United Nations Conference on Trade and Development (UNCTAD) and the Netherlands Bureau for Economic Analysis (CPB).

Some decline in commodity prices, but with increased volatility

80

100

120

140

160

180

200

220

240

260

280

300

320

340

360

Ja

n-0

8

Ap

r-0

8

Ju

l-0

8

Oct-

08

Ja

n-0

9

Ap

r-0

9

Ju

l-0

9

Oct-

09

Ja

n-1

0

Ap

r-1

0

Ju

l-1

0

Oct-

10

Ja

n-1

1

Ap

r-11

Ju

l-11

Oct-

11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oct-

12

Food Tropical beverages

Oils and oilseeds Forestry and agricultural raw materials

Minerals and metals Energy

Manufactured goods

Exchange rate volatility increased in Brazil and Mexico, with a greater diversity in exchange-rate trajectories

NOMINAL EXCHANGE RATE, Jan 2008 – Nov 2012 (National currency per dollar, index 01/01/2008=100)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures.

80

90

100

110

120

130

140

150

01-0

1-2

008

01-0

3-2

008

01-0

5-2

008

01-0

7-2

008

01-0

9-2

008

01-1

1-2

008

01-0

1-2

009

01-0

3-2

009

01-0

5-2

009

01-0

7-2

009

01-0

9-2

009

01-1

1-2

009

01-0

1-2

010

01-0

3-2

010

01-0

5-2

010

01-0

7-2

010

01-0

9-2

010

01-1

1-2

010

01-0

1-2

011

01-0

3-2

011

01-0

5-2

011

01-0

7-2

011

01-0

9-2

011

01-1

1-2

011

01-0

1-2

012

01-0

3-2

012

01-0

5-2

012

01-0

7-2

012

01-0

9-2

012

01-1

1-2

012

Brazil Chile Colombia Mexico Peru

-200,000

-150,000

-100,000

-50,000

0

50,000

100,000

150,000

200,000

250,000

2008 2009 2010 2011 2012

Portfolio investment outflows Portfolio investment inflows

Other investment outflows Other investment inflows

Net financial flows (excl. net FDI and errors)

Although the trade channel was most affected, net financial flows to the region also declined

LATIN AMERICA AND THE CARIBBEAN: GROSS CAPITAL FLOWS, 2008 – 2012a

(In millions of dollars)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a Figures for 2012 correspond to estimations.

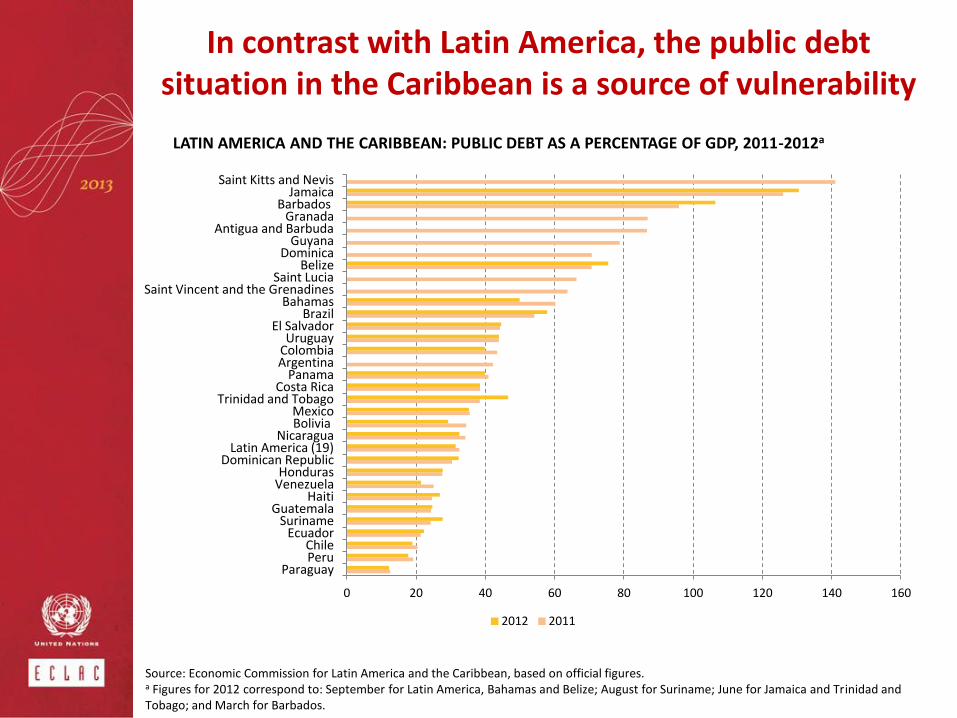

In contrast with Latin America, the public debt situation in the Caribbean is a source of vulnerability

LATIN AMERICA AND THE CARIBBEAN: PUBLIC DEBT AS A PERCENTAGE OF GDP, 2011-2012a

Source: Economic Commission for Latin America and the Caribbean, based on official figures. a Figures for 2012 correspond to: September for Latin America, Bahamas and Belize; August for Suriname; June for Jamaica and Trinidad and Tobago; and March for Barbados.

0 20 40 60 80 100 120 140 160

Paraguay Peru Chile

Ecuador Suriname

Guatemala Haiti

Venezuela Honduras

Dominican Republic Latin America (19)

Nicaragua Bolivia Mexico

Trinidad and Tobago Costa Rica

Panama Argentina Colombia Uruguay

El Salvador Brazil

Bahamas Saint Vincent and the Grenadines

Saint Lucia Belize

Dominica Guyana

Antigua and Barbuda Granada

Barbados Jamaica

Saint Kitts and Nevis

2012 2011

The rise in consumption reflected improved labour market conditions: unemployment fell (to 6.4%) and

wages increased

LATIN AMERICA AND THE CARIBBEAN: ECONOMIC GROWTH, INCREASE IN REAL AVERAGE WAGE AND VARIATION IN THE UNEMPLOYMENT RATE

Source: Economic Commission for Latin America and the Caribbean, (ECLAC), based on official figures.

e/ Estimate.

80.00

85.00

90.00

95.00

100.00

105.00

110.00

115.00

120.00

-4.00

-2.00

.00

2.00

4.00

6.00

8.00

10.00

12.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 e/ Re

al A

vera

ge S

alar

y (I

nd

ex

20

00

= 1

00

)

Rat

es

(pe

rce

nta

ges)

Economic Growth Unemployment Rate (left axis) Real Average Wages (right axis)

CENTRAL AMERICA

MEXICO

CARIBBEAN

BRAZIL

4

5

6

7

8

9

10

2008 2009 2010 2011 2012 e/

Brazil Rest of South America (7 countries) Mexico Central America (3 countries) The Caribbean (3 countries)

REST OF SOUTH AMERICA

Evolution of unemployment by sub-region

URBAN UNEMPLOYMENT RATE, 2008 - 2012 (Percentage)

Source: Economic Commission for Latin America and the Caribbean, (ECLAC), based on official figures. e/ Estimate. For the Caribbean: First half of the year.

Salaried employment grew more than own-account work, although at a lower rate than in 2011

LATIN AMERICA: ECONOMIC GROWTH AND EMPLOYMENT DYNAMICS, 2000 - 2012 (Percentage)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a/ January-September

-2

-1

0

1

2

3

4

5

6

Salaried Employment Own Account Workers GDP

Formal employment increased, but in various countries at a slower pace

LATIN AMERICA: YEAR-ON-YEAR CHANGE OF FORMAL, SALARIED EMPLOYMENT (Percentage)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a/ January-September, except Argentina and Panama, whose data correspond to the period January-June; and Uruguay, January-August.

-5

-3

-1

1

3

5

7

9

Argentina Brazil Chile Costa Rica Mexico Nicaragua Panama Peru Uruguay

2009 2010 2011 2012 a/

LATIN AMERICA: POVERTY AND INDIGENCE, 1980-2012 a

(Percentages and millions of people)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of special tabulations of household surveys conducted

in the respective countries. a Estimate for 18 countries of the region plus Haiti. The figures above the bars refer to the percentage of total poor (indigents and non-indigent

poor). The figures for 2012 are projections.

Both poverty and indigence posted a fresh decline in 2011

LATIN AMERICA (7 COUNTRIES): ANNUAL VARIATION IN TOTAL INCOME PER CAPITA

AND INCOME SOURCE IN POOR HOUSEHOLDS,a 2010-2011 b

(Percentages)

Source: Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of special tabulations of household

surveys conducted in the respective countries. a The percentage of the population analysed is the same for both periods and corresponds to the poverty rate for 2008 or nearest

previous year. b Corresponds to the period 2009-2011 in Brazil and Chile. c Urban areas.

Wages were the main driver of higher income in poor groups...

Source: Economic Commission for Latin America and the Caribbean (ECLAC), on the basis of special tabulations of household

surveys conducted in the respective countries.

a Urban areas.

LATIN AMERICA (18 COUNTRIES): FEMININITY INDEX OF POVERTY, 2011

… but gaps between women and men have been widening, leading to greater feminization

of poverty

Social public spending has kept rising as precentage of GDP

Fuente: Comisión Económica para América Latina y el Caribe (CEPAL), sobre la base de cifras oficiales.

11.3

3.1 2.7

4.4

1.2

17.9

4.9

3.7

7.9

1.6

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Gasto social total Gasto en educación Gasto en salud Gasto en seguridad y asistencia social

Gasto en vivienda y otros

AMÉRICA LATINA Y EL CARIBE (21 PAÍSES): EVOLUTION OF SOCIAL SPENDING IN DIFFERENT ECTORS, 1990-1991 A 2008-2009.

(in percentage of GDP)

1990-1991 1994-1995 1998-1999

6.6 a/

1.8 a/

1.0 a/

3.5 a/

0.4 a/

Total social spending

Spending in education

Spending in health

Spending in social protection

Spending in housing and other

Balance, perspectives and challenges

In 2013, external demand will not be a source of dynamism

• European Union

– Solvency problems persist both in terms of public debt and in the financial system, as well as insufficient external adjustment

– Low growth and a possible recession in 2013

– Institutional changes (fiscal union and a unified banking supervisor) will take time

• United States:

– Liquidity will continue to expand

– Labour, housing and banking solvency indicators suggest possibilities of increased growth in 2013

– There remains a risk of the fiscal cliff

• China

– Indicators suggest growth similar to or greater than that of 2012: 7.9% in 2013 compared to 7.7% in 2012

But a slight uptick in growth is predicted for the region (3.8%) in 2013

LATIN AMERICA AND THE CARIBBEAN: CONTRIBUTION TO REGIONAL GDP GROWTH BY COUNTRY , 2004 - 2013

Source: Economic Commission for Latin America and the Caribbean (ECLAC), based on official figures. a/ Estimate b/ Projection

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7% 2

00

4

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

/a

20

13

/b

Brazil

Argentina

The Caribbean

Mexico

Central America

Rest of South America

Latin America and the Caribbean

LATIN AMERICA AND THE CARIBBEAN: GDP GROWTH RATES, 2013a (Percentages)

With a recovery in some countries and a small slowdown in others

Source: Economic Commission for Latin America and the Caribbean (ECLAC). a Projection

2.0

2.0

2.0

3.0

3.5

3.5

3.5

3.5

3.5

3.5

3.5

3.8

3.9

4.0

4.0

4.0

4.0

4.5

4.5

4.8

5.0

6.0

6.0

7.5

8.5

00 01 02 03 04 05 06 07 08 09

Venezuela (Bol. Rep. of) The Caribbean

El Salvador Dominican Republic

Argentina Guatemala Costa Rica

Cuba Ecuador

Honduras Mexico

Latin America and the Caribbean Central America (9 countries) South America (10 countries)

Brazil Uruguay

Latin America Colombia Nicaragua

Chile Bolivia (Plur. St. of)

Haiti Peru

Panama Paraguay

THE CARIBBEAN: GDP GROWTH RATES, 2013a (Percentage)

The Caribbean will also grow, at 2.0%, but vulnerabilities remain

Source: Economic Commission for Latin America and the Caribbean (ECLAC) a Projection

0.1

1.0

1.2

1.5

1.7

1.8

1.9

2.0

2.3

2.4

2.5

3.0

3.8

4.7

4.9

.0 1.0 2.0 3.0 4.0 5.0 6.0

Jamaica

Barbados

Granada

Saint Vincent and the Grenadines

Dominica

Saint Kitts and Nevis

Saint Lucia

The Caribbean

Belize

Antigua and Barbuda

Trinidad and Tobago

Bahamas

Latin America and the Caribbean

Suriname

Guyana

In the short term

The role of domestic demand (national and intra- regional) should be strengthened and expanded, in order to:

• Grow to achieve equality (through employment and wages)

• Enhance investment dynamics

• Avoid internal macroeconomic disequilibria (inflation or financial bubbles)

• And external disequilibria (increasing current account deficits)

• In the Caribbean: ensure fiscal consolidation, but with social protection

• Strengthen regional demand through intra-regional trade

Longer-term challenges: structural gaps to be closed

Inequality For the first time in

recent history there have been

advances in combating inequality

Investment Investment, at 23% of GDP, is insufficient for development

Productivity Closing the external

gap (with the technological

frontier) and the internal gap

(between sectors and actors)

Taxation Regressive tax systems; weak non-

contributory pillar

International linkages

Risk of “lock-in” of the export structure, with low value added and little investment

in technology

Environ-mental

sustainabi-lity

Move towards sustainable

production and consumption

patterns

• In order to move towards productive convergence, policymakers must look beyond the price boom: economic policies based on a relevant, long-term, sustainable vision at the macroeconomic, productive and territorial levels.

• To take advantage of the opportunities provided by the international context, exports must have a higher value added and knowledge content, with the focus on diversification of production, integration of sustainable production processes, re-evaluation of global and regional partnerships and strengthening open regionalism.

• Consensus on priorities and respective financing: a fiscal covenant with a redistributive impact – with access to innovation, job security and internalization of externalities.

• New equation: State-market-society.

AMÉRICA LATINA Y EL CARIBE: ESTRUCTURA DE LAS EXPORTACIONES POR NIVEL DE INTENSIDAD TECNOLÓGICA, 1981-2010 a

(En porcentajes del total)

Risk of lock-in based on static comparative advantages

LATIN AMERICA (18 COUNTRIES): STRUCTURAL HETEROGENEITY INDICATORS, AROUND 2009 (Percentages)

Productive structure and employment: concentrated in low-productivity sectors

Source: ECLAC, on the basis of R. Infante, “América Latina en el ‘umbral del desarrollo’. Un ejercicio de convergencia productiva”, Working Paper, No. 14, Santiago, Chile, June 2011, unpublished.

Access to financing for development for middle-income countries

• The focus on per capita income does not reflect the broad and multi-faceted nature of the development process

• ECLAC proposes an alternative approach based on structural gaps must be adopted

• This implies: • Focusing cooperation and financing towards

development, not only poverty reduction • Re-thinking the role and integration of middle

income countries in the system of regional cooperation

• New political dialogue at the global and regional levels

Strengthening the regional integration agenda

• Intraregional trade, development of value chains, investment and infrastructure

• Harnessing strategic opportunities with Asia, especially China

• Enhancing the regional financial architecture • Closer regional cooperation to tackle global

challenges (global governance, financing for development, Rio+20, development agenda beyond 2015).

ECLAC’s proposal: structural change for equality

Close economic and social gaps, both internal and external • Progress towards more knowledge-intensive activities • Reduction of production and territorial heterogeneity

Spread throughout the economic and social structure:

• Production and technology capabilities • Ample job opportunities and quality employment

• Social protection with universal access

• Environmental sustainability in the context of the technology revolution

Strengthen the role of the State as a guarantor of rights and driver of policies for sustainable economic and social development