economic consulting associates limited 41 lonsdale road london nw6 6ra uk tel +44 (0)20 7604 4545 /...

TRANSCRIPT

ECONOMIC CONSULTING ASSOCIATES LIMITED 41 Lonsdale Road London NW6 6RA UKtel +44 (0)20 7604 4545 / fax +44 (0)20 7604 4547 www.eca-uk.com

1 © 2008 Economic Consulting Associates Ltd

SEE Regional Gasification StudyWorld Bank and KfWStephen Wilson ECA Dr Detlef Edler UGS

Joint Working Group Belgrade, 11 September 2008

2 © 2008 Economic Consulting Associates Ltd

Overview

Underground Gas Storage (UGS) outside original study scope new Task 10 is on storage

Storage in context of EC Ring security of supply synergies with EC Ring

Expected demand for storage projected annual demand seasonality of demand

Existing storage and prospects sites and technical potential SEE storage project case studies

Economics of UGS estimating storage costs opportunity costs, modelling seasonal

prices Results: Economics of storage in

SEE Final Report Gas Forum

3 © 2008 Economic Consulting Associates Ltd

SEE gasification and the EC Ring

4 © 2008 Economic Consulting Associates Ltd

Projected annual gas demand

The pattern is of: generally small and declining indigenous

production, expiry of contracts and growth of demand

Potential incremental demand: 30 Bcm by 2025

Romania and Bulgaria dominate Only ~7 Bcm in the 7 western-most markets

The south-west corner of SEE is ungasified early CCGT anchor demand needed especially in ALB, MTG, MAK, southern CRO - There is some available capacity on

pipelines, although not necessarily in winter - limited pipeline capacity into region

compared with major UKR-ROM-BUL-TUR transit pipeline

BUL

ROM

CROSRB

0

10

20

30

40

2005 2010 2015 2020 2025

BiHALBMKDKSVMTG

bcm/y14 21 29Incremental imports for 9 SEE markets:

7

5 © 2008 Economic Consulting Associates Ltd

Source: Base Map WinGas GmbH. © Verlag Gluckhauf GmbH, Essen 2006

Supply possibilities and EC Ring

Supply possibilities and EC Ring

6 © 2008 Economic Consulting Associates Ltd

Demand for underground gas storage

7 © 2008 Economic Consulting Associates Ltd

Demand for storage

Seasonality of demand can be represented on a load-duration

curve average year, 1-in-20 or 1-in-50

shapes general growth scales up the shape changing the mix changes the shape

Peak demands the more ‘peaky’ the shape, the more

high deliverability storage is required

8 © 2008 Economic Consulting Associates Ltd

UGS in the context of SEE gas

Synergies with the EC Ring Seasonal balancing Additional winter injection points to complement transmission supply

Interaction with neighbouring markets

facilitates future trading SEE – PSV – Baumgarten

Can increase security of supply

UGS

9 © 2008 Economic Consulting Associates Ltd

Existing and prospective UGS

10 © 2008 Economic Consulting Associates Ltd

Source: Base Map WinGas GmbH. © Verlag Gluckhauf GmbH, Essen 2006

Existing and potential UGS sites in SEE

Existing and potential UGS sites in SEE

OkoliOkoli

BenicanciBenicanci

Banatski Banatski DvorDvor

othersothers

DumreaDumrea

DivjakaDivjaka

ChirenChiren

[various][various]

Tuzla-TetimaTuzla-Tetima

11 © 2008 Economic Consulting Associates Ltd

Site Type

Existing Potential Bcm

ALB Divjaka DF - 0.06

Dumrea SC - 0.07 * N

BiH Tuzla-Tetima SC - 0.05

BUL Chiren DF 0.5

Unspecified SC - ?

CRO Okoli DF 0.58 +0.4

Benicanci DF - 0.5 … 2

KSV ~ ~ -

MAK ? SC - ?

MTG ~ ~ - -

ROM Ten sites DF 4.45 1.1

SRB Banatski Dvor

DF 0.03 0.8

Various DF 3 to 5

Total All ~ 5.5 ~ 3 … 8

12 © 2008 Economic Consulting Associates Ltd

Case studies of potential UGS projects

13 © 2008 Economic Consulting Associates Ltd

Prospective new UGS

Croatia: Okoli (depleted field expansion) Benicanci (depleted field)

Bosnia and Herzegovina Tuzla-Tetima (salt structure)

Serbia: Banatski Dvor (depleted field)

Albania Dumrea (salt structure) Divjaka (depleted field)

14 © 2008 Economic Consulting Associates Ltd

Source: Base Map WinGas GmbH. © Verlag Gluckhauf GmbH, Essen 2006

Prospective new UGS sites: study focus

Prospective new UGS sites: study focus

OkoliOkoli

BenicanciBenicanci

Banatski Banatski DvorDvor

DumreaDumrea

DivjakaDivjaka

Chiren

[various]

Tuzla-TetimaTuzla-Tetimaothers

15 © 2008 Economic Consulting Associates Ltd

Economics of storage

16 © 2008 Economic Consulting Associates Ltd

Economics of gas storage

Cost of developing and operating

depleted fields salt caverns

Value of storage: opportunity costs

line pack from larger Ø EC ring peak or seasonal LNG supply pipeline gas supply & capacity electricity sector seasonal dispatch

alternate fuel (secondary or backup)

interruptible (non-firm) customers

17 © 2008 Economic Consulting Associates Ltd

Estimating costs: depleted fields

UGS experts reviewed design of similar wells recently completed

For each potential new facility:

adjust costs for SEE conditions define expected parameters:

working gas volume, MMscm cushion gas, MMscm max withdrawal capacity, MMscm/d number of production wells, # average well depth, m

Taking into account (if known): porosity, % permeability, mDarcy

18 © 2008 Economic Consulting Associates Ltd

Estimating costs: salt caverns

Similar cost estimation approach

For each potential new facility: define expected parameters:

cavern diameter, m cavern height, m cavern net volume, m³ minimum and maximum pressure, bar working gas volume, MMscm cushion gas volume, MMscm number of production wells, # average well depth, m

Taking into account: caverns simultaneously leaching, # water flow rates, m³/h time for cavern creation, months

19 © 2008 Economic Consulting Associates Ltd

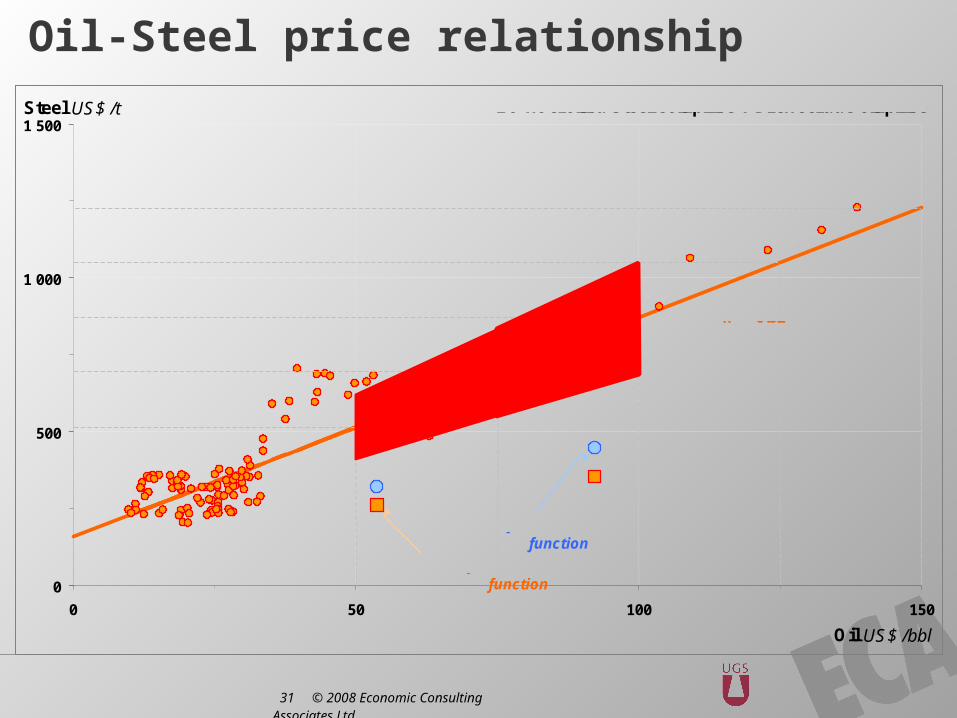

Oil-gas price linkage

Oil-steel price linkage

Handling underlying price uncertainty

20 © 2008 Economic Consulting Associates Ltd

Alternatives to UGS

Dual-firing power plants boilers (cost of backup fuel storage)

Seasonal generation dispatch summer peaking gas-fired plants can complement winter-peaking temperature-sensitive (heating) loads

Interruptible customers industrial customers seasonal shifting, when priced correctly(where capacity is more economic)

LNG LNG

21 © 2008 Economic Consulting Associates Ltd

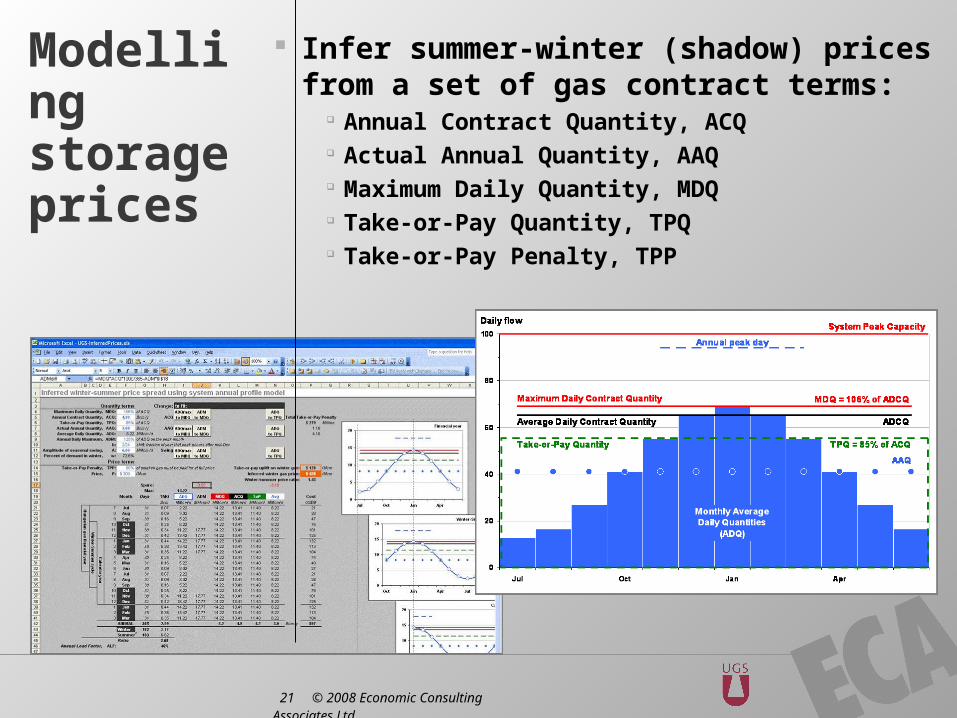

Modelling storage prices

Infer summer-winter (shadow) prices from a set of gas contract terms:

Annual Contract Quantity, ACQ Actual Annual Quantity, AAQ Maximum Daily Quantity, MDQ Take-or-Pay Quantity, TPQ Take-or-Pay Penalty, TPP

22 © 2008 Economic Consulting Associates Ltd

Final report: Gas Forum

23 © 2008 Economic Consulting Associates Ltd

Final report including storage

New sub-sections in existing structure

§2: Demand-side assessments seasonal swing daily variability security of supply

§3: Supply-side options UGS sites geological characteristics development cost estimates cost of alternatives economic analysis updated with

storage §5: Institutional framework

Regulated v market-based storage under national gas markets and cross-border framework

ECONOMIC CONSULTING ASSOCIATES LIMITED 41 Lonsdale Road London NW6 6RA UKtel +44 (0)20 7604 4545 / fax +44 (0)20 7604 4547 www.eca-uk.com

24 © 2008 Economic Consulting Associates Ltd

SEE Regional Gasification StudyWorld Bank and KfWStephen Wilson ECA Dr Detlef Edler UGS

Joint Working Group Belgrade, 11 September 2008

25 © 2008 Economic Consulting Associates Ltd

Estimating economic costs of gas storage worked exampleItem Quantity Price

USD /unit

Cost USD M

Surface facilities and wells

20

Cushion gas 500 MMcm 300 150

TOTAL CAPITAL COST 170

Annualised capital costs 20 years 10 % pa 20.0

Storage cost of carry (6 months)

5% of 500 300 7.5

Annual compression work 2.5% of 500 300 3.8

TOTAL ANNUALISED COSTS

62 31.2

26 © 2008 Economic Consulting Associates Ltd

BUL

ROM

CROSRB

+2.3

0

10

20

30

40

2005 2010 2015 2020 2025

BiHALBMKDKSVMTG

bcm/y14 21 29Incremental imports for 9 SEE markets:

7

3.7

Projected incremental imports for 9 SEE markets

Declining indigenous production and existing import contracts

27 © 2008 Economic Consulting Associates Ltd

28 © 2008 Economic Consulting Associates Ltd

Historical oil and gas prices

$50 oil

$25 oil

$75 oil

$100 oil

0

25

50

75

100

125

150

2000 2001 2002 2003 2004 2005 2006 2007 2008

Brent price US$ / bbl

0

100

200

300

400

Gas price US$ / Mcm

LH axis: Europe Brent spot price FOB$100 oilRH axis: SEE regional gas price estimateRH axis: Baumgarten → AUTRH axis: Baumgarten → ITARH axis: Velke Kapusany

29 © 2008 Economic Consulting Associates Ltd

Oil-Gas price relationship490

410

330

250

170

90

460

385

310

235

160

85

0

100

200

300

400

500

0 25 50 75 100 125 150

Oil US$/bbl

Gas US$/Mcm

30 © 2008 Economic Consulting Associates Ltd

Historical oil and steel prices

0

50

100

150

1990 1995 2000 2005 2010 2015

Oil US$/bbl

100

500

900

1 300

Steel US$/t

Brent crude OIL daily prices

Brent Crude monthly average

Hot rolled STEEL coil (EU)

1997 - 2003 inclusiveOil: $10-35 /bblSteel: $200-400 /t

2004 - mid 2007Oil: $35-75 /bblSteel: $400-700 /t

mid 2007 - … Oil: $75-150 /bbl

Steel: $700-1400 /t

31 © 2008 Economic Consulting Associates Ltd

Oil-Steel price relationship

0

500

1 000

1 500

0 50 100 150

Oil US$ /bbl

Steel US$ /t EU hot rolled steel coil price v Brent crude oil price

Steel = 157.1 + 7.136BrentR² = 0.82

+2σ

-2σ

-1σ

+1σ

inferred EAF cost function

inferred BOF cost function

32 © 2008 Economic Consulting Associates Ltd

AAQ

Annual peak day

0

20

40

60

80

100

Jul Oct Jan Apr

Daily flow

Monthly Average Daily Quantities

(ADQ)

Take-or-Pay Quantity

System Peak Capacity

Maximum Daily Contract Quantity

Average Daily Contract Quantity

MDQ = 106% of ADCQ

ADCQ

TPQ = 85% of ACQ

33 © 2008 Economic Consulting Associates Ltd

34 © 2008 Economic Consulting Associates Ltd

EC Ring offers - diversity - security

- trading

EC Ring offers - diversity - security

- trading

Caspian gas

LNG (backhaul)

Algerian gas

(backhaul)

Croatian gas

mix

SEE

Baum-garten

PSV

Caspian gas

UGS

UGSRussian gas

Russian gas

Source: Base Map WinGas GmbH. © Verlag Gluckhauf GmbH, Essen 2006

35 © 2008 Economic Consulting Associates Ltd

LNG in SEE region Bcm/y of capacityLNG in SEE region Bcm/y of capacity

3.0

Rovigo, ITARovigo, ITA

Adriatic, CROAdriatic, CRO Marmara Marmara Ereglisi, TUREreglisi, TUR

Revithoussa, GRERevithoussa, GRE

Panigaglia, ITAPanigaglia, ITA

3.63.6

8.0

6.3

8.0

36 © 2008 Economic Consulting Associates Ltd