economic opportunity poverty reduction task force 09/04/2013 · economic opportunity poverty...

TRANSCRIPT

FinalSTAFF SUMMARY OF MEETING

ECONOMIC OPPORTUNITY POVERTY REDUCTION TASK FORCE

Date: 09/04/2013 ATTENDANCE

Time: 12:46 PM to 05:07 PM Balmer *Exum X

Place: SCR 356 Hudak XJoshi X

This Meeting was called to order by Marble XSenator Kefalas Pettersen X

Saine XThis Report was prepared by Ulibarri *

Keshia Duncan Fields *Kefalas X

X = Present, E = Excused, A = Absent, * = Present after roll call

Bills Addressed: Action Taken:Breakout into Working GroupsPresentation: PTC Rebate Audit FindingsCDHS on Measuring Economic Well-BeingDebriefing and Suggested Agenda Items for FutureUpdate from Working Groups and Discussion

Witness Testimony and/or Committee Discussion OnlyWitness Testimony and/or Committee Discussion OnlyWitness Testimony and/or Committee Discussion OnlyWitness Testimony and/or Committee Discussion Only-

12:47 PM -- Welcome and Working Group Breakout Session

Senator Kefalas, Chair, welcomed the task force members and stated that the working groups would break out into individual groups to discuss proposed legislation. He requested that the members return by 1:30 pm. The committee recessed.

Economic Opportunity Poverty Reduction Task Force (09/04/2013) Final

2 Final

02:48 PM -- Presentation on PTC Rebate Audit Findings

The committee came back to order. Senator Kefalas asked Trey Stanley and James Taurman from the Office of the State Auditor (OSA) to come to the table and begin their presentation on the audit of the Property Tax/Rent/Heat (PTC) rebate program. Mr. Stanley distributed a copy of the audit (Attachment A) and explained that rebates are divided into two categories: rent and heat. He said that applicants can receive a rebate of up to $700 a year, but most receive less. He reviewed the qualifications and income eligibility requirements, and stated that the Taxpayer Services Division within the Department of Revenue (DOR) oversees the program. He said that the program is funded through General Fund dollars and is not limited by an appropriation, so as long as a person is eligible for the rebate there won't be a cap on the amount they receive. Mr. Stanley said that the objectives of the audit were: to ensure that only eligible applicants were being approved for the rebate; to determine if people were aware of the program; and to examine the efficiency and effectiveness of the program's administration. Senator Kefalas asked Mr. Stanley to discuss the reasons for the decrease the number of rebate recipients. Mr. Stanley stated that the audit did not show any specific reasons, but that program outreach could be responsible for the decrease in numbers. Senator Kefalas asked about eligibility income thresholds and Mr. Stanley answered that this was not within the scope of the audit.

02:59 PM

Mr. Taurman explained the DOR Gen Tax system in terms of processing and payments. Senator Kefalas asked how many applications were denied and how many were approved. Representative Fields asked about underpayments to recipients. Mr. Taurman answered that 45 percent of the recipients surveyed in the audit were not paid the correct amount. He said that when the audit findings were presented, DOR explained that the income thresholds change every year and were not updated in the Gen Tax system. He stated that the audit found that DOR does not have a process in place to notify recipients of payment errors. Senator Kefalas asked why DOR did not update the income thresholds prior to the application deadline. Mr. Taurman responded that DOR said the updates were not made in a timely fashion. Senator Kefalas asked why rebates are paid out in four installments. Mr. Taurman answered that state law requires the rebates to be paid in four installments because of supplemental income requirements.

03:10 PM

Mr. Taurman continued to tell the task force about the issues with the Gen Tax system and the verification process, as well as the relationship between DOR and the Colorado Department of Human Services (CDHS) in regards to the PTC rebate program. Mr. Tuarman told the committee that CDHS provides data from the Colorado Benefits Management System (CBMS) to DOR to input into Gen Tax for verification. Senator Ulibarri asked about the accuracy of the data and how it is determined that a person qualifies for the rebate due to a disability. Mr. Stanley responded that statute requires that someone already be receiving disability assistance in order to qualify for a PTC rebate. The task force discussed reasons why some applications for the rebate were denied and whether the reasons for denial were in line with statutory requirements.

Economic Opportunity Poverty Reduction Task Force (09/04/2013) Final

3 Final

03:18 PM

Mr. Taurman discussed the history of the PTC rebate program, and talked about the need to blend resources and improve program outreach. He stated that per statute, DOR is required to provide PTC rebate forms to the Public Employees' Retirement Association (PERA). The task force discussed ways to improve the program's outreach efforts and statutory changes needed to support improved outreach and cost efficiency. Senator Kefalas asked if the DOR website includes up-to-date information and is user-friendly. Mr. Taurman responded that the information is current but that the audit did not examine whether the website is user-friendly. Senator Kefalas wanted to know if DOR accepted OSA's recommendations pertaining to collaboration with other departments. The task force discussed transferring responsibility for the program from DOR to CDHS, and whether a hybrid model would be more efficient and cost effective.

03:33 PM

Mr. Stanley discussed the benefits of CDHS managing the rebate program since it already administers similar programs. Mr. Stanley continued to review the OSA recommendations, and explained that the Legislative Audit Committee requested that DOR and CDHS report back to the committee in December on their progress implementing the recommendations in the audit. Senator Kefalas thanked Mr. Stanley and Mr. Taurman and pointed out the statutory requirements that the departments have not followed in regards to the PTC rebate program. The task force discussed ways to recover the overpayments made to recipients and the need to continue evaluating the effectiveness of the rebate program.

The following people testified:

03:48 PM -- Herb Homan, representing the Colorado Senior Lobby, came to the table. He distributed a handout (Attachment B). He stated that his views are his own and not representative of the Senior Lobby. Mr. Homan told the committee about difficulties he's faced during retirement, especially since the benefits and income thresholds have not been adjusted for inflation since the 1990s. He talked about the work of the PTC coalition, and specific areas of the PTC rebate program that the OSA audit missed. He told the task force why CDHS should manage the program and discussed other ways to improve the program.

04:05 PM -- Eileen Doherty, representing the Colorado Gerontological Society, came to the table. She suggested auto-enrolling people into the rebate program who are already receiving other benefits. She talked about ways to improve the program and how to increase participation rates.

04:10 PM -- Pat Ratliff, representing Colorado Counties, Inc. (CCI), came to the table. She talked about the importance of the rebate program and stated that CCI should be involved in future discussions about how to improve the program.

Economic Opportunity Poverty Reduction Task Force (09/04/2013) Final

4 Final

04:12 PM -- Presentation on Measuring Economic Well-Being

Julie Kerksick, Deputy Executive Director of the Office of Economic Security, CDHS, introduced herself to the committee and provided a handout (Attachment C). She told the task force about the mission and purpose of the Office of Economic Security. Michael Martinez-Schiferl, Data and Evaluation Analyst, Work Support Strategies, CDHS, introduced himself and gave background information on the Work Support Strategies (WSS) initiative. Ms. Kerksick discussed the WSS initiative and noted that rising caseloads have led to problems administering benefits. She said that her office has made progress in administering food assistance and medical programs and benefits to those in need. She explained that Colorado has one of the lowest participation rates in WSS programs in the country, and that this might be because people are not aware of the program or don't think they are eligible. Senator Kefalas stated that he would like an evaluation of the effectiveness of the tools currently being used for outreach.

04:26 PM

Mr. Martinez-Schiferl told the task force about a survey of organizations done by CDHS examining different ways to measure economic well-being. He said that the survey posed the following questions: how is economic well-being defined; how is economic well-being measured in terms of data and tools used; and what is done with the data once it is collected. He reviewed the types of responses received, and talked about the child well-being index that is based off of U.S. Census data. Mr. Martinez-Schiferl stated that the information CDHS gathered on economic well-being indicators may assist the task force in developing an economic well-being index.

04:36 PM

The task force and presenters continued to discuss ways to measure economic well-being in terms of stability, highest-level of education, and whether basic needs are being met. Mr. Martinez-Schiferl noted that different organizations use different descriptors for the same kind of scale and this creates difficulty when trying to determine qualifying measures for economic well-being. He talked about the importance of uniformity and the ability to share information organization-wide, and explained the collaboration model used by Boulder County and local community organizations. Senator Marble asked if CDHS partners with faith-based groups. Ms. Kerksick stated that they do not at this time, but that they are open to it. Ms. Kerksick answered questions about the composition of the WSS board of directors. Representative Fields asked if any research has been done on how the program would benefit grandparents who are raising their grandchildren or adults who are taking care of aging parents. Ms. Kerksick stated that her office has not focused specifically on problems faced by these populations. Senator Kefalas asked Ms. Kerksick and Mr. Martinez-Schiferl if either of them read the Legislative Council Staff memo on steps to creating an economic well-being index and opened the floor to public comment.

Economic Opportunity Poverty Reduction Task Force (09/04/2013) Final

5 Final

04:54 PM -- Debriefing and Suggested Agenda Items for Future

Senator Kefalas asked each task force member to talk about what he or she learned from the day's meeting and what he or she would like to see included on the agenda for the next meeting. Senator Ulibarri stated the there is a lot more work for the task force to accomplish and that he is unsure where to begin focusing in order to be the most effective. Senator Hudak stated that she was impressed by the level of collaboration by different departments on the issues discussed, and asked what could be done to help fund adult literacy programs. Representative Fields thanked Senator Kefalas for his work on the task force, and stated that she was surprised by how much still needs to be accomplished, especially in regards to adult education. Senator Marble stated that there is a lot of overlap between working groups and talked about the need to identify what gaps have already been filled. Senator Kefalas thanked the task force members for their hard work and said that he recognizes that the work load of the task force is heavy. He explained that at the next meeting on September 18th the task force will focus on recommendations from the working groups that could lead to proposals for specific legislation. He said there will also be a panel discussion on the PTC rebate program. Senator Hudak asked for clarification on the process for proposing and drafting bills. Senator Kefalas responded that bill drafters from the Office of Legislative Legal Services (OLLS) will attend the next meeting and that bill drafts will be voted on at the final meeting of the task force.

05:07 PM

The committee adjourned.

01:36 PM -- Update from Working Groups and Discussion

Senator Kefalas called the meeting back to order. He explained the process and next steps for the working groups to propose legislation, and stated that the task force can suggest administrative or rule changes in addition to legislative changes. He went over the agenda and asked the working groups to provide an update on their progress .

01:39 PM

Senator Hudak provided an update on the Early Childhood Development and Education working group. She said that the group is focusing on two key areas. The first is to make changes to the state Child Care Tax Credit to streamline it to the federal tax credit. She explained that currently, if a person's income is too low to pay federal taxes, he or she will not qualify for the state tax credit. She explained that the working group is planning to propose legislation to separate the federal and state tax credits so that not qualifying for the federal tax credit does not preclude someone from qualifying for the state credit. The legislation will also increase the amount of the tax credit. Senator Hudak told the task force that the working group is also focusing on changes to the Child Care Assistance Program (CCAP). She explained that a number of people who would benefit from CCAP are not being reached, and that the program is under-funded due to program cuts. Senator Hudak said that the working group is focusing on legislation to ensure that all families with young children who are at 130 percent of poverty are able to be served by county CCAP programs.

Economic Opportunity Poverty Reduction Task Force (09/04/2013) Final

6 Final

01:46 PM

Senator Kefalas stated that he would like the state to be more active in allocating county CCAP dollars. Representative Saine provided an update on the Housing Continuum working group. She explained that the group is focusing on issues pertaining to manufactured homes, and that many people who own manufactured homes experience problems financing and refinancing their homes. She said that it is difficult for some people to sell their manufactured home, and that the group is working to identify possible solutions. Senator Ulibarri talked about the National Housing Fund. He explained that $17 million was temporarily invested in the fund, and stated that due to the recession funding to affordable home ownership programs was cut. He stated that Colorado is one of three states that does not have a long-term housing investment program. Senator Ulibarri talked about the tour the task force took of Warren Village, and commended its program model. He explained that Colorado is in a unique position because of restrictions placed by the Taxpayers Bill of Rights (TABOR), and because of this there are only a few housing investment fund models that would be aligned with TABOR restrictions. Representative Fields expressed her support for housing investment fund legislation because it would benefit people in her district. Senator Kefalas stated that he would also support a housing investment fund. He suggested making changes to the laws dealing with Community Development Financial Institutions (CDFI), as well as releasing Deeds of Trust in order to lower restrictions on local community reserve funds. Senator Kefalas talked about making changes to the Mobile Home Park Act to create opportunities for manufactured home owners to purchase the land on which their homes sit if the land owner chooses to sell it.

02:00 PM

Representative Fields updated the task force on the Workforce Readiness working group. She discussed a presentation the group heard from Barbara Kelley, Executive Director of Department of Regulatory Agencies (DORA), about the effects of regulations on small businesses. She stated that the group is interested in proposing legislation to reduce the "red tape" faced by small businesses, as well as legislation focused on funding adult education programs. She stated that Colorado is one of several states that does not provide adequate support for adult education. Senator Marble stated that it has been informative to hear from experts in the field, and talked about issues stemming from a lack of review by agencies on their overlapping, redundant, and conflicting rules. She said that this affects business owners and consumers because it leads to higher costs, and explained that the working group looked at states that have mandatory reviews of rules and regulations in hopes of adopting one of their models. Senator Marble said that the group discussed expanding technology and trade courses for middle school and high school students. Senator Ulibarri asked Senator Marble and Representative Fields to comment on ways the task force can reduce red tape for small businesses. Representative Fields responded that the group discussed reducing the number of applications that businesses must submit by replacing them with a universal application.

02:14 PM

Senator Balmer told the task force about the Career Ready Colorado Certificate which certifies a job seeker's skills and creates common, objective standards for employment readiness. He discussed issues with the current program, as well as the need to pass legislation to make the certificate easier to obtain. Representative Exum told the committee that there is a need for an alternative identification card for individuals who are unable to qualify for a state identification card for a variety of reasons. He explained that a person must show identification in order to receive certain benefits. There was no public testimony.

Economic Opportunity Poverty Reduction Task Force (09/04/2013) Final

7 Final

02:21 PM

Senator Kefalas asked if any of the working groups considered a recommendation to increase the Division of Housing budget line item from the current appropriation of $2.5 million. Senator Ulibarri responded that the Division of Housing has a limited role in housing investment which is why the idea of a housing investment fund was discussed as an alternative. The committee took a brief recess.

OFFICE OF THE STATE AUDITOR

Property Tax, Rent, and Heat Rebate Program

Department of Revenue

Performance Audit August 2013

Attachment A

LEGISLATIVE AUDIT COMMITTEE 2013 MEMBERS

Representative Angela Williams

Chair

Senator Steve King Vice-Chair

Senator Lucia Guzman Representative Su Ryden Senator Owen Hill Representative Jerry Sonnenberg Representative Dan Nordberg Senator Lois Tochtrop

OFFICE OF THE STATE AUDITOR

Dianne E. Ray State Auditor

Monica Bowers Deputy State Auditor

Trey Standley

Legislative Audit Manager

Carleen Armstrong James Taurman Legislative Auditors

The mission of the Office of the State Auditor

is to improve government for the people of Colorado.

Dianne E. Ray, CPA State Auditor

Office of the State Auditor

August 5, 2013 Members of the Legislative Audit Committee: This report contains the results of a performance audit of the Property Tax, Rent, and Heat Rebate Program in the Department of Revenue. The audit was conducted pursuant to Section 2-3-103, C.R.S., which authorizes the State Auditor to conduct audits of all departments, institutions, and agencies of state government. The report presents our findings, conclusions, and recommendations, and the responses of the Department of Revenue and Department of Human Services.

This page intentionally left blank.

i

TABLE OF CONTENTS

PAGE

Glossary of Terms and Abbreviations .................................................................. ii Report Summary ...................................................................................................... 1

Recommendation Locator ....................................................................................... 3 CHAPTER 1: Overview. ........................................................................................ 5

Program Eligibility ........................................................................................ 5

Program Administration ............................................................................... 6

Program Funding and Expenditures ........................................................... 7 Audit Purpose, Scope and Methodology ..................................................... 8

CHAPTER 2: Rebate Processing and Payment. ................................................ 11

Rebate Payment Controls ........................................................................... 13

Disability Verification Controls ................................................................. 19 Improper Denials of Applications .............................................................. 22

CHAPTER 3: Outreach and Program Administration. ................................... 29

Program Outreach ....................................................................................... 30

Program Administration ............................................................................. 36

ii

Glossary of Terms and Abbreviations DHS – Department of Human Services LEAP – Low-Income Energy Assistance Program OAP – Old Age Pension PTC – Property Tax Credit, also known as the Property Tax, Rent, and Heat Rebate Rebate Year – The calendar year during which a PTC Program participant incurs the expenses that qualify them for the rebate SSI – Supplemental Security Income

For further information about this report, contact the Office of the State Auditor 303.869.2800 - www.state.co.us/auditor

Dianne E. Ray, CPA State Auditor

PROPERTY TAX, RENT, AND HEAT REBATE

PROGRAM Performance Audit, August 2013 Report Highlights

Department of Revenue

KEY FACTS AND FINDINGS The Department did not properly update the system it uses to

determine Program eligibility and calculate rebate payments. As a result, about 7,000 (40 percent) of the 17,713 Program participants we reviewed were underpaid, 120 eligible applicants were denied rebates, and 483 ineligible applicants were allowed to participate in the Program.

The Department denied 321 applicants for eligibility reasons that were not support by statute or Program rules. In addition, Department staff responsible for assisting in person applicants erroneously disallowed applicants from claiming rebates for heat sources other than gas (e.g. electricity, propane).

The Department does not have adequate controls to verify that applicants are disabled, as required by statute and Program rules. We found that for eight (29 percent) of 28 sampled participants who qualified based on a disability the Department did not have adequate disability information on file.

The Department does not notify applicants who are approved for the Program of their application’s status prior to paying the rebate. Because rebate payments are made on a quarterly basis, some applicants must wait for over three months to learn the amount of rebate they should expect.

The Department has not provided counties with PTC Program information for distribution to Old Age Pension recipients on an annual basis as required by statute. In addition, there may be opportunities for the Department to improve Program outreach through increased coordination with DHS.

Since its inception, the PTC Program has been expanded to cover a broader segment of the population and now serves a similar population as other benefit programs administered by DHS. As a result, the State may be able to improve outreach and provide better service to participants by moving the PTC Program, in whole or in part, to DHS. However, moving the Program could result in significant initial costs.

AUDIT CONCERN The Department needs to improve its controls to determine Program eligibility and calculate rebate payments and should coordinate with the Department of Human Services to improve Program outreach and administration.

OUR RECOMMENDATIONS The Department should: Properly update its system each year to

ensure accurate payments and eligibility determinations and pay participants who were underpaid and applicants who were improperly denied rebates.

Eliminate system controls that deny applications for reasons not supported by statute.

Ensure that it has adequate information to confirm applicants’ disability status.

The Department and Department of Human Services (DHS) should: Improve Program outreach through

increased coordination between agencies. Consider the benefits and costs of moving

the Program to DHS and work with the General Assembly on legislative change if the determination is made that moving the Program would be beneficial.

The Department and DHS generally agreed with these recommendations.

BACKGROUND The PTC Program provides rebates for

property tax and heat expenses incurred by elderly or disabled Colorado residents whose income falls below Program thresholds.

The Department’s Taxpayer Services Division is responsible for administering the PTC Program, processes rebate applications and conducts outreach to inform the public of Program requirements.

In Fiscal Year 2013 about 21,000 households participated in the Program and received a total of about $6.9 million in rebates or $329 each.

PURPOSE Evaluate the Department of Revenue’s (the Department) administration of the Property Tax, Rent, and Heat Rebate (PTC) Program, including application controls and Program outreach.

-1-

This page intentionally left blank.

-3-

RECOMMENDATION LOCATOR

Rec. No.

Page No.

Recommendation Summary

Agency Addressed

Agency Response

Implementation Date

1

18

Ensure that eligible participants are paid the proper rebate by (a) maintaining a process to update GenTax annually,(b) issuing payments to underpaid participants and recovering payments from overpaid or ineligible participants and (c) notifying approved individuals of their rebate amount.

Department of Revenue

a. Agree b. Agree c. Agree

a. Implemented b. August 2013 c. January 2014

2 21 Establish controls to ensure the Department has sufficient and accurate information to verify applicants’ disability status before approving applications.

Department of Revenue

Agree

January 2014

3 26

Ensure that applicants are only denied based on reasons supported in statute and rules by (a) discontinuing the practice of requiring applicants’ addresses to match the address on file with the Division of Motor Vehicles,(b) discontinuing the practices of subtracting gifts from applicants’ expenses and denying applicants solely because their expenses exceed their income and (c) ensuring that in-person applicants may claim heat rebates for any heat source.

Department of Revenue

Agree January 2014

4 35 Improve outreach by (a) determining the most cost-effective and efficient methods for providing Program information to pension recipients as required by statute, reviewing the requirement, and seeking statutory change, as necessary and (b) working with the Department of Human Services to identify low-cost methods to promote awareness of the Program.

Department of Revenue

Department of

Human Services

Agree

Agree

January 2014

January 2014

-4-

RECOMMENDATION LOCATOR

Rec. No.

Page No.

Recommendation Summary

Agency Addressed

Agency Response

Implementation Date

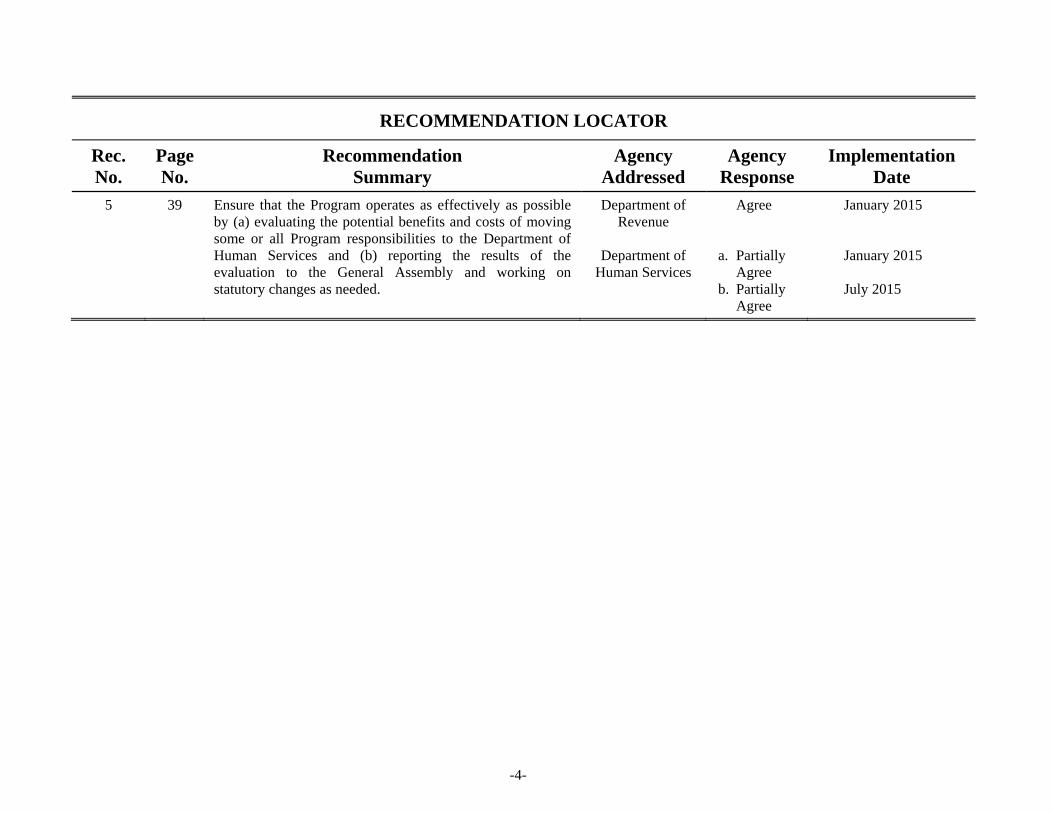

5 39 Ensure that the Program operates as effectively as possible by (a) evaluating the potential benefits and costs of moving some or all Program responsibilities to the Department of Human Services and (b) reporting the results of the evaluation to the General Assembly and working on statutory changes as needed.

Department of Revenue

Department of

Human Services

Agree

a. Partially Agree

b. Partially Agree

January 2015 January 2015 July 2015

5

Overview of the Property Tax, Rent, and Heat Rebate Program

Chapter 1

Statute (Section 39-31-101 et seq., C.R.S) establishes the Property Tax, Rent, and Heat Rebate, also known as the Property Tax Credit (PTC) Program (the Program), to provide financial assistance with property taxes, rent, and home heating expenses to low-income Coloradoans who are either elderly or disabled. Because the PTC Program was created as a grant within the State’s tax laws (Title 39, Articles 1 through 35, C.R.S), it is administered by the Department of Revenue (the Department). During Fiscal Year 2013, about 21,000 individuals and married couples received rebates totaling about $6.9 million. Applicants may apply annually beginning January 1 after the calendar year in which they incurred the property tax, rent, or heating expenses, which is referred to as the “rebate year.” For example, any expense incurred between January 1, 2011 and December 31, 2011 was within Rebate Year 2011. Applicants have up to 2 years to apply for the rebates after the rebate year has ended. Thus, for Rebate Year 2011, individuals and couples could apply for a rebate beginning January 1, 2012, and will be able to apply through December 31, 2013. Statute [Sections 39-31-101(2) and 104(1), C.R.S.] divides the PTC rebate into two categories: (1) property tax or rent and (2) heat. The maximum property tax or rent rebate a Program participant may receive is $600 per year, and the maximum heat rebate is $192 per year, for a maximum total rebate of $792. The actual amount participants receive is determined by their rebate year expenses and income, with the average participant receiving $329 during Fiscal Year 2013.

Program Eligibility Statute provides that both individuals and married couples are eligible for the PTC Program, with married couples required to apply jointly, and establishes the following PTC Program eligibility criteria:

Colorado Residency and Lawful Presence. Statute [Section 39-31-101(1)(a), C.R.S.] requires PTC rebate recipients to be Colorado residents for the full rebate year. Statute [Section 24-76.5-103(4), C.R.S.] also requires recipients to be lawfully present in the United States, produce a

6 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

valid driver’s license or state ID, and sign an affidavit confirming their legal status.

Disability Status. Under statute [Section 39-31-101(1)(c), C.R.S.],

individuals of any age who are unable to work due to a medically determined permanent physical or mental impairment may be eligible to receive a PTC rebate. According to statute, individuals enrolled in disability benefits programs, such as those administered by the Social Security Administration, Veterans Administration, or Department of Human Services (DHS), are considered disabled for the purposes of determining eligibility for the PTC Program.

Age. If not eligible based on a disability, statute [Section 39-31-101(1)(a)

and (b), C.R.S.] requires participants to be 65 years of age or older or a surviving spouse who is 58 years of age or older.

Income. As provided by statute [Section 39-31-101(2), C.R.S.], applicants

whose income is below statutory thresholds, which are adjusted for inflation each year, are eligible for the Program. For Rebate Year 2012, the thresholds were set at $12,481 for individuals and $16,476 for married couples.

In addition, statute [Section 39-31-101(3)(a), C.R.S.] provides that individuals who can be claimed as dependents on another person’s tax return are not eligible for a PTC rebate. Also, statute [Section 39-31-101(4), C.R.S] requires PTC Program participants to reside in a private, non-tax-exempt property. A resident of a facility owned by a tax-exempt organization, such as a nonprofit agency, would only be eligible for a rebate for heating expenses. Further, statute [Sections 39-31-101(4)(b) and 104(1)(a), C.R.S.] prohibits residents of nursing homes from receiving a property tax or rent and heat rebate.

Program Administration Within the Department, the Taxpayer Services Division (the Division) is responsible for administering the PTC Program. Division staff conduct the following activities related to the Program:

Outreach. Staff promote awareness of the Program through outreach efforts, such as mailing applications to prior-year recipients, issuing press releases, and maintaining a Program website.

Report of the Colorado State Auditor 7

Application assistance. The Division assists Program applicants with questions about the Program and helps applicants who choose to apply in person at the Department’s offices to fill out the application form.

Application processing and payment. The Division uses similar procedures for the PTC Program rebate as it does for processing tax returns and relies on GenTax, the Department’s tax database, to automatically determine eligibility and make payments. When GenTax discovers eligibility issues that make an applicant ineligible, it flags the application for Division staff to confirm that GenTax made the proper determination.

In addition to administering the PTC Program, the Division is responsible for processing tax returns and operating a call center to provide taxpayers with assistance.

Program Funding and Expenditures PTC Program rebates are funded entirely with general funds. In Fiscal Year 2013, the Program paid about $6.9 million in rebates. Similar to tax refunds, total rebates for the Program each year are not limited by an appropriation and are paid from revenue held in the statutory income tax refund reserve, meaning all who are eligible and apply for the PTC Program should receive a rebate. No full-time-equivalent (FTE) staff are appropriated to the Division for the PTC Program, and the Division has no staff that are solely assigned to the Program; however, Division management estimates that it uses about 1.9 FTE, primarily tax examiners, data entry staff, and call center staff, to conduct PTC Program activities. The table on the following page provides the number of participants, average rebates, and total amount of rebates paid for Fiscal Years 2009 through 2013. As shown, participation in the PTC Program has declined about 20 percent from Fiscal Year 2009 to Fiscal Year 2013. Although Department staff were not sure why Program participation has declined, increased participation in other benefits programs that provide income to similar populations, such as the Supplemental Security Income Program, may have reduced the number of eligible individuals and the rebate amount participants can receive.

8 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Property Tax, Rent, and Heat Rebate Program Number of Participants, Rebate Amounts Disbursed, and Average Rebates

Fiscal Years 2009 Through 2013

2009 2010 2011 2012 2013

Percentage Change,

2009-2013Number of Participants

26,058 23,595 24,206 21,703 20,878 -20%

Total Rebates Paid

$8,290,629 $7,581,317 $7,373,322 $7,254,389 $6,874,010 -17%

Average Annual Rebate

$318 $321 $305 $334 $329 3%

Source: Department of Revenue Fiscal Year 2012 Annual Report and Fiscal Year 2013 Department of Revenue data.

Audit Purpose, Scope and Methodology This report includes the results of our performance audit of the PTC Program at the Department of Revenue. We conducted this audit pursuant to Section 2-3-103, C.R.S., which authorizes the State Auditor to conduct audits of all departments, institutions and agencies of state government. The audit was prompted by a legislative audit request. Audit work was performed from January through July 2013. We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives The key objectives of the audit were to assess the Department’s:

Controls to ensure only eligible applicants are approved for rebates and

that rebates are paid according to requirements found in statute and rule.

Outreach for the PTC Program to ensure that potentially eligible people are aware of the Program.

Efficiency and effectiveness of Program administration. Because the Department does not administer other public benefits programs, this objective included an assessment of whether moving some or all of the

Report of the Colorado State Auditor 9

Department’s responsibilities for the PTC Program to DHS would better serve participants and improve the efficiency of the Program.

To accomplish our audit objectives, we:

Reviewed relevant state laws, Department promulgated rules, and PTC Program policies and procedures.

Interviewed Department staff to determine how they assist individuals applying for the PTC Program and process Program applications.

Analyzed data on rebate payments for Rebate Year 2011 to determine whether the payment amounts were in accordance with requirements found in statute and rule.

Analyzed data on denied applications for Rebate Year 2011 to determine the reason for the denial and whether the denial decision was in accordance with statute and rule.

Interviewed Department staff about outreach efforts and reviewed outreach materials to determine whether the Program conducted outreach in accordance with requirements found in statute. We also compared the Department’s outreach activities with the efforts of similar programs at DHS.

Compared the participation rate of the Program, which is the percentage of the eligible population in Colorado that participated in the Program, to the participation rate of the Low-Income Energy Assistance Program.

Interviewed management at both the Department and DHS to determine the cost and benefits of moving some or all of the Program responsibilities to DHS. We also compared the cost for DHS to administer similar programs to determine the potential cost-effectiveness of DHS administering the Program.

We relied on sampling techniques to support our audit work as follows:

We selected a nonstatistical random sample of 40 PTC Program participants for Rebate Year 2011. We selected our sample to provide representation of the 17,713 participants for Rebate Year 2011 who received rebates during Calendar Year 2012. We designed our sample based on our audit objectives to test whether the Department paid the correct rebate amount to participants.

10 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

We selected a nonstatistical random sample of 28 disabled PTC participants for Rebate Year 2011. We selected our sample to provide representation of 10,447 disabled participants for Rebate Year 2011 who received rebate payments during Calendar Year 2012. We designed our sample based on our audit objectives to test whether the Department had sufficient information to verify the participants’ disability.

11

Rebate Processing and Payment

Chapter 2

The Department of Revenue (the Department) processes applications for Property Tax, Rent, and Heat Rebate (PTC) Program (the Program) with a process similar to the one used for state tax returns. Beginning on January 1 after the rebate year, applicants either mail a hard-copy application form to the Department or apply in person at the Department’s main office in Denver. The application requires applicants to provide their age; disability status; income; property tax, rent, and heat expenses; and address for each residence they lived in over the rebate year. Staff enter information from each application into GenTax, the Department’s tax processing system. The Department verifies application information, such as income, address, and disability status, using tax data stored in GenTax and data the Department loads into GenTax from other sources, such as federal tax returns, the Division of Motor Vehicles (DMV) database, and data on disability benefits recipients from the Department of Human Services (DHS). GenTax automatically determines whether the individual is eligible for the PTC Program. The flow chart on the following page outlines the application process.

12 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Report of the Colorado State Auditor 13

During the audit, we reviewed the Division’s processing and payment of PTC rebates. As discussed in this chapter, we found three key problems with the Division’s process for determining eligibility and making rebate payments: (1) it lacked procedures to ensure GenTax makes proper eligibility determinations and calculates rebate amounts accurately, (2) it lacked controls in GenTax to verify applicants’ disability status, and (3) it denied rebates for reasons not supported by statute and Program rules and improperly prevented some applicants from applying for heat rebates.

Rebate Payment Controls As previously discussed, the Department relies on GenTax to automatically approve and process PTC rebate payments. GenTax is programmed to calculate and issue payments according to a statutory formula that is based on an applicant’s income along with his or her property tax, rent, and heat expenses. Because the calculation of income and rebate amounts can vary each year based on inflation and on the income participants receive from other public benefits programs, the Department must ensure that it keeps up-to-date information in GenTax so that its rebate payment and eligibility controls work properly. What audit work was performed and what was the purpose? The purpose of the audit work was to determine whether the Department calculated payments correctly, paid PTC Program participants the correct total amount, and notified applicants of the Department’s determination on their application in writing. To do this, we interviewed staff about the application review process and evaluated the Department’s controls for determining rebate amounts. We then tested whether the Department paid the correct amount to participants by comparing payment amounts to information within GenTax, on hardcopy applications, and from other documentation on file at the Department for a random sample of 40 out of the 17,713 PTC participants for Rebate Year 2011. We also interviewed Department staff and management about procedures for notifying individuals of the status of their application. In addition, we reviewed statute, Colorado rules and regulations, and application processing practices for similar programs in Colorado, such as the Low-Income Energy Assistance Program (LEAP) and Old Age Pension (OAP) Program. How were the results of the audit work measured? The Department calculates PTC Program rebates according to a statutory formula that is based on applicants’ income and property tax, rent, and heat expenses. Statute requires the Department to take the following steps to calculate an applicant’s rebate payment:

14 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Determine applicants’ income. Statute [Section 39-31-101(3)(b), C.R.S.] and Program rules require applicants to report income, which includes wages, business income, and income received through certain public assistance programs such as Social Security. In addition, Program rules [Regulation 39-31-101(3)(b)(iii), 1 C.C.R., 201-15] specify that Medicare premiums paid out of the individual’s Social Security benefit are considered income, and the Department uses information from DHS to add these premiums to applicants’ reported income if they fail to do so on the application. Income received as gifts, or from prior year payments from PTC rebates and LEAP, are not considered income for determining PTC rebates. According to statute [Section 39-31-101(2), C.R.S.], the maximum income to receive any rebate in Rebate Year 2011 was $12,313 for individuals and $16,205 for married couples. To account for cost of living increases, statute [Section 39-31-101(2), C.R.S.] requires the Department to adjust the income limits annually based on inflation.

Determine the maximum rebate based on expenses. PTC rebates are

broken down into two categories of expenses: (1) property tax or rent, and (2) heat. According to statute [Sections 39-31-101(2) and 104(2), C.R.S.], the maximum property tax or rent rebate Program participants may receive is their actual expenses or $600 per year, whichever is less, and the maximum heat rebate is their actual expenses or $192 per year, whichever is less. Thus, participants can receive a maximum combined annual rebate of $792. Statute [Section 39-31-101(4)(a), C.R.S.] provides that for participants who pay rent and do not pay property taxes directly, 20 percent of the rent paid will be considered property tax expenses for the purposes of calculating the maximum amount they can receive. For example, if an applicant paid $1,000 for rent during the rebate year, he or she would be eligible for a maximum property tax and rent rebate of $200. Similarly, if a participant’s rent payments include heating expenses, statute [Section 39-31-104(1)(a)(II), C.R.S.] calculates the heating expense amount as 10 percent of the rent paid. Using the previous example, if the applicant paid $1,000 in rent and his or her heat was paid by a landlord as part of a rental agreement, the applicant would be eligible for a maximum heat rebate of $100 in addition to the property tax and rent rebate of $200, for a combined maximum rebate of $300.

Calculate any reductions to the maximum rebate. Statute [Section 39-

31-101(2), C.R.S.] provides a formula to reduce the maximum rebate amount participants receive if their income exceeds certain thresholds. For Rebate Year 2011, the year we tested, the income thresholds were $6,313 for individuals and $10,205 for married couples. Rebate payments are reduced according to the amount of income applicants have above the thresholds, with applicants over the maximum income limits for the Program receiving no rebate. Statute [Section 39-31-101(2), C.R.S.]

Report of the Colorado State Auditor 15

requires the Department to adjust these thresholds each year according to inflation.

Once the total heat and property tax rebate has been calculated, statute [Section 39-31-102(1), C.R.S.] requires the Department to pay the total rebate amount on a quarterly basis, with the amount of all payments equal to the total rebate divided by the number of quarters remaining in the calendar year. For example, if a participant qualifies for a $120 total rebate and applies in January, then the rebate should be paid out in four $30 installments, whereas the same participant applying in April would receive three $40 payments. In addition, we reviewed the payment practices of two other benefits programs in the state that assist elderly and low-income populations. State rules require these other benefit programs to notify applicants of their application status in advance of payment. Specifically, DHS has promulgated rules (Section 3.350-11, 9 C.C.R., 2503-3 and Section 3.756.15, 9 C.C.R., 2503-7) requiring counties to send OAP and LEAP applicants notification of the decision on their application in writing. Because notifying applicants in advance of the agencies’ determination can help applicants plan ahead, we expected that the Department would notify applicants of its determination on their PTC rebate applications in writing and if they are eligible, inform them of the rebate payment they should expect to receive. What problems did the audit work find and why did they occur? We found that the Department did not pay all approved PTC participants the proper amount for Rebate Year 2011. Based on our review of participants’ expenses and income, we found that it underpaid 18 (45 percent) of the 40 Rebate Year 2011 participants in our sample for property tax, rent, and heat rebates. The amount the Department underpaid these 18 participants ranged from $1 to $48 and totaled $387, or 5 percent of the $7,917 that they should have received. According to the Department, the underpayments we identified occurred because GenTax was not updated on time to reflect annual Program changes. Specifically, income thresholds in GenTax were not adjusted on time to account for inflation as required by statute and Medicare premiums paid through applicants’ Social Security benefits, which must be included in applicants’ income when determining eligibility, were also not adjusted on time to reflect annual changes. Both updates were made on February 29, 2012, about two months after the Department began processing applications for Rebate Year 2011. The Department reported that the updates should have occurred before GenTax began determining whether applicants were eligible for the Program and calculating the amount approved applicants should receive for each of their quarterly payments. This

16 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

delay caused GenTax to incorrectly calculate payment amounts and make improper eligibility determinations for applications processed prior to the updates.

In addition to improper payments, we found the Department lacks a consistent process for notifying applicants of its eligibility determinations on their applications. Specifically, the Department only notifies applicants of their application status if they are denied a rebate and does not notify applicants in writing when their applications are approved for payment. Instead, applicants must either call the Department to ask about the status of their application or wait until they receive the first payment to be notified that they were approved and what rebate amount they should expect.

Why does this finding matter? It is important that the Department update GenTax each year, before it begins processing PTC Program applications, to reflect annual changes to ensure that participants receive the correct payment amount and that GenTax makes correct eligibility determinations. This is particularly important for the PTC Program, because rebate payments can represent a significant financial benefit to Program participants. After we informed the Department about the underpayments we identified in our sample, it ran a system check in GenTax to identify the number of individuals that were affected by the update delays and reported that the delays affected a significant number of PTC Program applicants and rebate recipients:

Underpayments to participants. 7,000 (40 percent) of the 17,713 PTC rebate participants who applied for Rebate Year 2011 during Calendar Year 2012 were paid less than the amount provided in statute. The incorrect rebate payments ranged from $1 to $63 and resulted in a total of $165,116 in underpayments. The Department will need to attempt to contact these participants and provide each with a rebate payment equal to the amount they were underpaid.

Incorrect denials of applicants. 120 applicants were denied a rebate

when they should have been approved. These applicants did not receive a total of $44,440 (an average of $370 per applicant) in rebates for which they were eligible. The Department will need to attempt to contact these applicants and provide a rebate payment to each that is equal to the amount the applicant should have been approved for and received.

Incorrect Approvals of Applicants. 483 applicants who should have

been denied were approved and were paid about $200,644 (an average of $415 per applicant). The Department will need to attempt to collect these erroneous rebate payments. Because the population served by the PTC Program has few assets, collecting the money owed may be difficult.

Report of the Colorado State Auditor 17

Thus, the Department may ultimately be unable to collect a significant portion of the overpaid amount.

In addition to affecting Program applicants and participants, the system problems we identified also affected DHS’s calculation of the amount of funding the State must provide to the Supplemental Security Income (SSI) Program in order to meet the State’s federal maintenance of effort requirement. SSI is funded using both state and federal funds, and the State must provide funding equivalent to at least 100 percent of the prior year’s state funding of these programs to meet federal maintenance of effort requirements. PTC Program payments are part of the State’s maintenance of effort funding, and DHS estimates that Program payments comprised about $5 million (18 percent) out of the State’s total funding benchmark of $27.4 million in Calendar Year 2012. According to DHS, it must accurately estimate State expenditures to prevent overpayment and potential fines for underpayment. DHS determined that in Calendar Year 2012 the State had underpaid its benchmark by about $712,000; however, if the Department had properly calculated PTC Program rebates, the amount underpaid would have been as much as $9,000 less, or $703,000. Although this is a small difference, if the Department does not properly update PTC Program information in GenTax each year, there is a risk of larger discrepancies in DHS’s calculation of the State’s maintenance of effort requirement that could increase costs to the State.

The Department reported that it implemented processes for Calendar Year 2013 to ensure all necessary GenTax updates occur before applications are processed and test that payments are correct. However, we were unable to evaluate Calendar Year 2013 payments because they did not begin until April, just before fieldwork on the audit was completed. In addition, after we reported the inaccurate payments from our sample to the Department, it reported that it planned to pay underpaid participants and incorrectly denied applicants the amounts owed and take steps to recover funds paid to individuals who were ineligible. In addition to conducting timely updates in GenTax, providing written notice of the approved rebate amount to applicants can improve customer service and reduce staff time spent answering phone calls from applicants. Under the Department’s current process, approved applicants are not informed of their application status and rebate amount until they receive their first payment, which may be more than three months after they apply. Because PTC rebates can be a significant source of funds for applicants, it would benefit applicants to know the amount of the rebate they will receive in advance so that they can make financial plans. Further, Department staff indicated that PTC applicants frequently call the Department’s customer service line to attempt to determine if their applications were approved and find out when they can expect to receive payments. Thus, by mailing notifications to both approved and denied applicants in a timely manner, the Department may be able to reduce staff time required to answer phone calls.

18 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Recommendation No. 1: The Department of Revenue should ensure that it pays eligible participants the proper Property Tax, Rent, and Heat Rebate by:

a. Maintaining a process for ensuring that GenTax system updates occur and are tested prior to January 1 each year.

b. Attempting to contact and issue payments to underpaid participants for

amounts underpaid or incorrectly denied and attempting to recover payments from participants who were overpaid or who were incorrectly deemed eligible.

c. Creating a process to notify individuals whose applications are approved

of their rebate amount and schedule of payments in writing.

Department of Revenue Response:

a. Agree. Implemented.

The Department of Revenue identified the system issue and made the appropriate change discussed in this recommendation in February 2012. The change was effective for the remainder of the 2011 rebate year. The Department updated its year end processes to ensure that system updates for the PTC Program were identified and properly tested by December 2012 for the 2012 rebate year. The process utilized for the 2012 rebate year will be used for the 2013 and subsequent rebate years.

Auditor’s Addendum: As noted in the report, the Department updated information in GenTax to properly calculate PTC Program rebates and determine eligibility for Rebate Year 2011 in February 2012. This information should have been updated in GenTax before the Department began processing applications in January 2012. In Recommendation No. 1a we recommend that the Department maintain a process to ensure that GenTax system updates occur on time in future years. The Department reports that it implemented this part of the recommendation in December 2012. However, we were unable to evaluate the implementation of this recommendation because Calendar Year 2013 payments did not begin until April, just before fieldwork on the audit was completed.

Report of the Colorado State Auditor 19

b. Agree. Implementation date: August 2013.

The Department of Revenue reevaluated affected applications to determine proper eligibility. The population has been identified and notifications and subsequent payments or bills will be sent to affected applicants in August 2013.

c. Agree. Implementation date: January 2014.

The Department of Revenue will program GenTax to produce notifications regarding the approval of the PTC benefit as part of its year end change process. The notifications will include information regarding the schedule of payments and the amount of each payment.

Disability Verification Controls During Rebate Year 2011 about 59 percent of all PTC Program participants qualified for the Program due to having a disability. To apply on the basis of a disability, applicants must indicate that they are disabled on the application form, but the Department does not require them to provide any documentation to verify their disability. Instead, the Department relies on data provided by DHS and loaded into GenTax to confirm that applicants participated in a state or federal disability program, such as the State’s Aid to the Needy Disabled Program or the federal Supplemental Security Income (SSI) Program. According to the Department, it verifies disability status based on data from DHS instead of requiring documentation from applicants in order to automate the application and approval process and reduce staff time necessary to administer the PTC Program. Additionally, not requiring applicants to provide documentation of their disability benefits is beneficial to applicants because the Social Security Administration charges a fee to individuals to provide disability documentation. What audit work was performed and what was the purpose? The purpose of the audit work was to determine whether the Department has adequate controls to ensure that applicants who claim to be disabled meet the eligibility requirements for the PTC Program. We reviewed electronic data from GenTax for all 17,713 Rebate Year 2011 Program participants. Of these participants, 10,447 were approved based on the applicant being disabled. To perform our testing, we selected a random sample of 28 disabled applicants from Rebate Year 2011. For each application in our sample, we reviewed GenTax data, hard-copy applications, and other documentation on file at the Department to determine whether the Department had sufficient information to verify the

20 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

participants’ disability. In addition, we interviewed Department staff on the process and controls used to determine eligibility and load DHS information into GenTax. How were the results of the audit work measured? Statute [Section 39-31-101(1)(c), C.R.S.] states that a person is eligible for a PTC rebate if they “were disabled during the entire taxable year to a degree sufficient to qualify for the payment to them of full benefits from any bona fide public or private plan or source based solely upon such disability.” To verify that an applicant for the PTC Program had a disability during the entire year for which he or she is applying for a rebate, as is required, the Department needs either the date the individual was declared disabled or the date the individual started receiving monthly disability benefits, and the monthly payment amounts the individual received. In addition, to rely on the disability information from DHS, the Department needs to have controls to ensure the information is complete for use in determining Program eligibility. What did the audit work find? We found that the Department did not obtain sufficient information to verify that some of the PTC Program participants who claimed a disability were in fact disabled. Specifically, for eight (29 percent) of the 28 participants we reviewed, the Department had insufficient disability information on file or in GenTax to confirm their disability during Rebate Year 2011. GenTax determined these participants to be disabled even though the data it had on file from DHS lacked a disability onset date and monthly disability payment amounts that would show the timing and duration of the applicants’ disability. When we brought this issue to the Department’s attention, it requested the individuals’ disability onset date and the amount the individuals received in disability payments from DHS through a manual process outside of GenTax. Based on the additional information the Department obtained, we were able to confirm that seven of the eight applicants were disabled and their income through monthly disability payments qualified them for the PTC Program. For the remaining approved application, GenTax showed that the applicant had received no disability payments. However, DHS provided information showing that, contrary to the information in GenTax, the applicant had received benefit payments of about $1,000 per month that should have been included in their income. Because these payments put the applicant over the PTC Program’s income limits for Rebate Year 2011, the applicant should have been denied a rebate; however, the Department approved the application and paid the applicant $292 in rebates based on the incorrect information in GenTax.

Report of the Colorado State Auditor 21

Why did the finding occur? We found that the Department lacks controls to ensure that GenTax contains sufficient information to confirm PTC applicants are disabled. Based on our review, it appears that the GenTax system considers an applicant to have disability status if the applicant is included in the DHS data it receives, even if the data are insufficient to confirm that the applicant was disabled during the rebate year. Specifically, GenTax automatically accepts the applicant as disabled without requiring the applicant’s disability onset date or the amount of disability payments. Further, the Department does not have a process in place to flag applications in GenTax so that it can obtain additional documentation from DHS or applicants when it lacks sufficient data from DHS to verify that the applicant was disabled and received benefits payments.

Why does this finding matter? The Department needs complete and accurate information to verify the disability status of PTC Program applicants to ensure that only eligible individuals are approved for rebates. The Department paid the seven applicants from our sample a total of $2,091 in rebates without verifying that they were disabled. Although we only identified one instance where an applicant was approved despite being ineligible and was improperly paid $292, a lack of sufficient disability information to verify that applicants are disabled creates a risk that ineligible applicants could be approved and receive rebates. Because 59 percent of the PTC Program participants for Rebate Year 2011 were approved by the Department based on their disability, this risk extends to most PTC Program participants.

Recommendation No. 2: The Department of Revenue should ensure that it has sufficient and accurate information to verify that Property Tax, Rent, and Heat Rebate Program applicants are disabled. This should include establishing controls to ensure that GenTax has information necessary, including applicants’ disability onset date and payment amounts, to confirm applicants’ disability status before approving applications. When applicants do not have sufficient information in GenTax, the Department should obtain additional documentation of disability status from the Department of Human Services or the applicant as necessary to verify the disability.

22 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Department of Revenue Response: Agree. Implementation date: January 2014. The Department of Revenue will modify its business rules to include an applicant’s disability onset and payment amount and will notify the Department of Human Services of the statutory requirements necessary to process PTC applications. The Department of Revenue will update procedures to require that the application has the necessary disability information to be approved, provided either by the Department of Human Services or by the applicant. The Department will develop a process to notify the Department of Human Services when any necessary requirements are missing.

Improper Denials of Applications As discussed, the Department performs numerous checks within GenTax to verify that the information reported on applications is accurate and that applicants are eligible to participate in the PTC Program. These checks include comparing the applicant-reported information to other data, such as the Department’s motor vehicle and income tax data, the Internal Revenue Service’s income tax data, and disability benefits data from DHS, which are all periodically loaded into GenTax. If an applicant provides information that indicates that they are ineligible for a rebate or GenTax cannot verify key information in the application, such as income, age, disability, or legal presence, it denies the application. Once GenTax denies the application, it is forwarded to Department staff for review. Staff check other systems, such as the motor vehicle and DHS databases, to verify that the applicant is not eligible and that data in the other systems haven’t been updated since they were last loaded into GenTax. Once Department staff verify that the applicant is ineligible, a denial letter explaining the reason for denial is mailed to the applicant. When they receive denial letters, applicants have the opportunity to address the reasons for denial by providing additional documentation to the Department and can later be approved for a rebate if the reasons for the initial denial are resolved. What audit work was performed and what was the purpose? The purpose of the audit work was to determine whether the reasons that the Department denied PTC applications complied with statutes and rules pertaining to the PTC Program. We reviewed electronic data from GenTax for the 4,998 applications that were denied for Rebate Year 2011. We also selected a random sample of 15 out of the 4,998 denied applications and compared the sample to

Report of the Colorado State Auditor 23

GenTax, hard-copy applications, and other documentation on file at the Department. Using electronic data and our sample, we assessed whether the Department had made denial determinations in accordance with statute and Program rules. We also interviewed Department staff responsible for assisting applicants who apply in person at the Department’s offices to determine whether they are appropriately applying the requirements found in statute and rule. How were the results of the audit work measured? Statute (Section 39-31-101 et seq., C.R.S) provides eligibility requirements for the PTC Program. Additionally, rebate payments made under the PTC Program are considered a public benefit, and statute [Section 24-76.5-103(9), C.R.S.] prohibits the payment of a public benefit to individuals who are not lawfully present in the United States. In order to comply with these two sections of statute, an applicant must:

Have less than the maximum income, which for Rebate Year 2012 was $12,481 for single applicants or $16,476 for couples.

Pay property taxes, rent or heat. Apply for a rebate within 2 years of the end of the rebate year. Be disabled, 65 years of age or older, or 58 years of age or older if a

surviving spouse. Live in Colorado for the entire rebate year. Not be claimed as a dependent on another individual’s tax return. Sign an affidavit stating that he or she is legally present in the United

States and verify lawful presence by providing a valid social security number and a driver’s license or state identification card number on the application.

What did the audit work find? We found that the Department has denied some applicants for reasons that could prevent eligible applicants from receiving benefits and are not supported by statute. According to the GenTax data we reviewed, the Department utilizes 35 different reasons to deny applications. Most of the reasons for denial are related to Program requirements, such as age or income, but we found that two reasons resulted in the Department denying applicants who met the statutory criteria for the PTC Program. Based on our review of the 4,998 applications that the Department denied for Rebate Year 2011, we identified the following problems:

321 (6 percent) were denied rebates solely because the address on their application did not match the address in the Department’s motor vehicles database. According to the Department, applicants frequently change addresses and do not update their address with the

24 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Department’s DMV, making address discrepancies between the PTC application and the motor vehicle database a common reason for denial. However, statute does not require recipients of the PTC Program or other public benefits to have an updated address with the DMV to receive benefits.

460 (9 percent) were denied rebates in part because the expenses they

listed on their application exceeded their income. However, there is no statutory provision or Program rule that indicates that an applicant’s income must exceed the amount claimed in expenses. Applicants may be using funds, such as gifts, that statute [Section 39-31-101(3)(b)(I), C.R.S.] expressly excludes from being considered income for the purpose of determining eligibility for the Program. In addition, when an applicant provides documentation of receiving gift funds, the Department’s practice is to subtract the gift amount from applicant’s reported expenses and reprocess the application. This practice is also not supported by statute or rule.

In addition, we found that in person applicants were denied the opportunity to apply for heat rebates solely because of their heating source. PTC Program statutes and rules allow an applicant to receive heat rebates regardless of his or her heating source (e.g., natural gas, electricity, propane, or wood), as long as the applicant is otherwise eligible. However, some Department staff who are responsible for assisting applicants who apply in person reported that heating rebates are only available to applicants whose heating source is natural gas. According to these staff, when applicants apply in person at the Department’s main office, Department staff review applicants’ documentation of heating expenses and only permit applicants to claim heat expenses if their heating source is natural gas. Applicants who apply in person and disclose a heating source such as electric heat or propane have effectively been denied a heat expense rebate. In contrast, when applicants mail in their applications, the Department does not review the source of heat expenses and allows rebates based on any heat source. Because the Department does not track the number of in person applicants who attempted to claim a heat source other than natural gas, we were unable to determine how many applicants were improperly denied heat rebates due to this practice. Why did the finding occur? According to the Department, comparing the address on the application with the address on file in the motor vehicle database provides a reasonability check on the applicant’s identity and legal presence in the United States. Therefore, the Department denies applicants whose application address does not match the address on file in the Department’s motor vehicle database because the

Report of the Colorado State Auditor 25

Department concludes that the applicants’ identity and legal presence have not been verified. However, the Department has other controls to verify identity, such as matching the applicants’ names, driver’s license numbers and social security numbers. Further, the Department can confirm applicants’ residency in Colorado and property tax status using just the addresses provided on their applications, regardless of whether they match the address on file with the DMV. The Department denies applications if the reported expenses exceed income because it is concerned that applicants may have other sources of income that were not disclosed on the application. Although an applicant having expenses that exceed income may be a valid reason to request more information from the applicant to determine whether they reported all sources of income, without more information indicating that the applicant had unreported income, denying the application or subtracting gift amounts from the applicant’s reported expenses are practices not supported by Statute (Section 39-31-101 et seq. C.R.S.) or Program rules (1 C.C.R. 201-15). In addition, Department staff told us that their understanding was that applicants with heating sources other than natural gas are ineligible for the heat rebate because of the difficulty in determining the portion of an electric utility bill due to heating and the portion unrelated to heating. However, Department management stated that any heat source is acceptable for reimbursement and that staff should have allowed applicants to claim expenses for heat sources other than natural gas. We reviewed written training materials provided to staff responsible for assisting PTC Program applicants and found the materials did not specifically address which heat sources are allowable. Why does this finding matter? Denial reasons that are not supported in statute or rule can create a barrier to legitimate participation in the PTC Program, which is intended to assist low-income disabled and elderly Colorado residents. Based on our review, 321 otherwise eligible applicants were denied benefits based on address mismatches. Although the Department allows applicants to provide additional information once they receive a denial letter, and some initially denied applicants may eventually be approved for a rebate, this process can result in significant delays for the applicant. For example, under the Department’s current process, an applicant to whom the Department denies a rebate in March would likely have to wait until at least July for his or her first rebate payment. In addition, because Department staff improperly disallowed participants who claimed heat sources other than gas from applying, some applicants may not have applied for up to $192 in heat rebates they could have received and may not apply for heating rebates in future years because of the incorrect information they received.

26 Property Tax, Rent and Heat Rebate Program Performance Audit - August 2013

Recommendation No. 3: The Department of Revenue should ensure that Property Tax, Rent, and Heat Rebate (PTC) Program applications are only denied based on reasons supported in statute and rules by:

a. Discontinuing the practice of requiring that applicants’ addresses match the address on file in the Division of Motor Vehicles’ database to be eligible for the PTC Program.

b. Discontinuing the practices of subtracting gifts from applicants’ expenses

and denying applicants solely because their expenses exceed their income. c. Ensuring that in person applicants may claim the heat rebate for any heat

source. This should include training staff to ensure that they allow applicants to claim expenses from all heat sources.

Department of Revenue Response: a. Agree. Implementation date: January 2014.

The Department of Revenue reviewed the statutory requirements and rules and regulations governing the PTC Program, and determined that the only requirement is that the applicant’s identification is valid, not that the identification’s address match the application, when determining eligibility for this population. As a result, the Department will change its business rules in GenTax starting with the 2013 application period.

b. Agree. Implementation date: January 2014.

The Department of Revenue will discontinue the practice of subtracting gifts from an applicant’s expenses starting with the 2013 application period and will update its training and procedures to reflect this change. The PTC application form currently directs applicants to not include gifts received as income. The Department will change its practice of denying an application outright solely because the expenses exceed income; rather the Department will seek additional information from the applicant. In the future, the Department will amend its form to let the applicant know that if their expenses exceed income they will be required to submit information explaining why.

Report of the Colorado State Auditor 27

c. Agree. Implementation date: January 2014.

Beginning with the 2013 application process, any form of heat will be eligible for the heat rebate. The Department will update its training and procedures to reflect this change.

This page intentionally left blank.

29

Outreach and Program Administration

Chapter 3