economic performance of state-owned enterprises in

TRANSCRIPT

February 2020

Economic performance of state-owned enterprises in emerging economies A cross-country study

The contents of this publication reflect the opinions of the individual authors, Sanja Borkovic and Peter Tabak, and do not necessarily reflect the views of the European Bank for Reconstruction and Development (EBRD).

Sanja Borkovic is an Associate Economist and Peter Tabak is a Regional Lead Economist at the EBRD.

All charts in this report use authors’ calculations based on the Orbis database (published by Bureau van Dijk, a Moody’s Analytics company)

In general, the private sector has been growing as a share of the economy in countries where the European Bank for Reconstruction and Development (EBRD) invests. However, state ownership remains prevalent in many sectors and, in some countries, has even increased (in Hungary, Poland and Turkey, for example). What is more, many larger-scale privatisation plans have stalled, been delayed or been very slow to implement. The share of state ownership was an important measure of economic transition in the 1990s, but is now less closely followed. This study aims to put the metric back on the radar by looking at non-financial state-owned enterprises (SOEs) in 25 of the economies where the EBRD invests. In addition to measuring the size of each country’s state-run sector, it will assess its performance in terms of profitability, liquidity and indebtedness. Our research shows that, almost three decades since the start of transition, there are still quite a few countries with a large state-owned footprint and/or in need of improvement in the state-owned sector in areas from corporate governance to financial management.

Abstract

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 1

2 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

Abstract 1

Introduction 4

Country, time and SOE coverage 5

Data sources 6

Indicators observed 7

Data limitations and cleaning 8

Results 9 Overview of the state sector 9 Sector size 10 Employment 13 Liquidity 14 Profitability 15 Indebtedness 17

SOEs by sector 20

Utilities 20 Transport 22 Manufacturing 24

Potential future work 26

Conclusions 27

References 28

Annex 1 29

Annex 2 30

Acronyms 31

Contents

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 3

0

10

20

30

40

50

60

70

80

100

Mid-2010 Mid-1994

Turk

men

ista

n

Bela

rus

Uzbe

kist

an

Tajik

ista

n

Ukra

ine

Serb

ia

Bosn

ia a

nd H

erz.

Russ

ia

Mon

tene

gro

Mol

dova

Kaza

khst

an

Turk

ey

Slov

enia

Rom

ania

Latv

ia

North

Mac

edon

ia

Croa

tia

Pola

nd

Mon

golia

Lith

uani

a

Kyrg

yz R

epub

lic

Geor

gia

Bulg

aria

Azer

baija

n

Arm

enia

Alba

nia

Slov

ak R

epub

lic

Hung

ary

Esto

nia

Introduction

The share of state ownership was an important measure of economic transition in the 1990s, but is now less closely followed. Although, in general, the private sector has been growing as a share of the economy in countries where the EBRD invests, state ownership remains prevalent in many sectors and has even been increasing in some countries such as Hungary, Poland and Turkey. What is more, many larger-scale privatisation plans have stalled, been delayed or been very slow to implement (for example, in Cyprus, Kazakhstan, Slovenia and Ukraine).

Measuring the size, scope and effectiveness or efficiency of state ownership is still important. EBRD diagnostic studies of Croatia, Serbia and Slovenia, for instance, have uncovered many areas ripe for improvement, from corporate governance to financial management. The large footprint and low efficiency of state-owned enterprises (SOEs) can

also have significant and various negative effects on the private sector. SOEs can have unfair competitive advantage from subsidies, get away with providing low-quality services to private customers, or create financial problems for suppliers by not paying bills on time.

The aim of this study is to provide a much-needed snapshot of state ownership in economies where the EBRD invests and to identify those countries and sectors that most need to improve SOE performance.

Chart 1. Private-sector share of GDP (per cent)

Source: EBRD Transition Report 1994 and Transition Report 2010 - Recovery and Reform.

4 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

The survey sample for our study was limited to 25 of the 38 economies in which the EBRD invests, largely due to the (un)availability of data. While the survey covered Europe quite extensively, the focus in Central Asia and the southern and eastern Mediterranean (SEMED) region was on the largest economies.

• Central Europe and the Baltic states: Croatia, Estonia, Hungary, Latvia, Lithuania, Poland, Slovak Republic, Slovenia

• South-eastern Europe: Albania, Bosnia and Herzegovina, Bulgaria, Cyprus, North Macedonia, Greece, Kosovo, Montenegro, Romania, Serbia

• Eastern Europe and the Caucasus: Belarus, Georgia, Moldova, Ukraine

• SEMED: Egypt

• Central Asia: Kazakhstan

• Turkey

The state-owned sectors of some countries were deemed insufficiently representative, however. Representativeness was judged on the availability of asset data, typically the most widely available indicator. While some countries had a relatively high number of SOEs listed in the Orbis database (published by Bureau van Dijk (BvD), a Moody’s Analytics company), five (Albania, Belarus, Cyprus, Egypt and Georgia) had asset data for fewer than 10 per cent of their SOEs for the period under review. They were consequently deemed insufficiently representative.1 These countries (and others) were omitted from results calculations, effectively reducing the sample to 20 countries (or fewer, depending on the availability of data on a particular indicator).

The study analysed the performance of non-financial companies in which state ownership exceeded 25 per cent. We included minority state ownership (25-50 per cent), as governments can still wield significant influence over the operations of these enterprises, for example, by introducing regulations benefiting the companies in question or blocking certain decisions. Financial companies were not included due to the distortions that could arise from their sizeable leverage (especially banks and insurance companies) compared with non-financial firms and the different nature of their operations.

We included SOEs owned both by the state and sub-sovereign entities (regions, municipalities). Centrally and locally owned SOEs were bundled together, as Orbis’s SOE identification criteria do not facilitate automatic separation. Overall, the sample comprised around 17,600 SOEs.2

Our analysis focused on 2014 to 2016. Data availability analysis for 2008-16 showed significant variation over time in the number of companies for which certain indicator data were available (for most countries, for example, asset data were quite limited for 2008-09, but far more available for 2014-15). This is why, when considering a time-series analysis, attention must be paid to the underlying number of SOEs for which data are available in the years in question. We chose the more recent 2014-16 period for the purposes of this report.

Country, time and SOE coverage

1 Georgia stood out, with around 4,350 SOEs recognised by Orbis,

but no available asset data.

2 The average number of SOEs with data on assets for at least one

year in the 2008-16 period.

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 5

The primary source of the data was the Orbis database (published by BvD, a Moody’s Analytics company), containing firm-level accounting and ownership data for around 300 million companies worldwide, standardised to a “global format” that makes the data comparable across jurisdictions. The primary SOE search strategy was: ownership data; companies owned by an ultimate owner; characteristics of the ultimate owner; and public authorities, states and government of a country. When extracting data, priority was given to unconsolidated accounts based on local registry filings.3

We supplemented the Orbis SOE list with data from other sources. To our knowledge, among service providers the Orbis database has the most comprehensive list of SOEs. However, as Orbis did not recognise all SOEs in the countries studied, the initial list of companies had to be amended. The other sources of information were mainly official national reports (from ministries of finance, fiscal councils or state audit institutions, for example), reports from international financial institutions and government websites.4 Thus, around 600 new SOEs were added to the list.

Additional sources were used to calculate indicators on SOE performance, namely, the International Monetary Fund’s April 2018 World Economic Outlook5 for gross domestic product (GDP) data and the International Labour Organization’s employment statistics for people over the age of 15.6

Data sources

3 We consider unconsolidated data more appropriate, as the

consolidated data of large holding structures would not allow

for proper sectoral analysis.4 In Orbis, manual recognition of SOEs is made more difficult

when some company names are given in the local language and

others in English, the transliteration from the local to the English

alphabet is not done consistently, or abbreviations are used

instead of full names. Such issues were particularly pronounced

for Ukraine, Kazakhstan and Greece.

5 See IMF (2018).6 See ILO (n.d.)

6 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

Indicators observedIndicators observed

SOE size and performance were gauged based on 22 indicators. Definitions of these diverse indicators are available in Annex 1. They can be grouped into six clusters:

1.Overview of the

state sector (number of SOEs, value added

as a percentage of GDP, percentage of listed SOEs)

2.Sector size

(assets, revenues, shareholders’ funds, share of assets of top 10 companies,

five largest SOEs’ share of total SOE assets)

3.Employment

(percentage of total employment, cost of

employees)

4.Liquidity

(ratio, credit days, collection days)

5.Profitability

(profit/loss, return on assets (ROA), return on equity (ROE))

6.Indebtedness

(financial debt, ratio of financial debt to earnings before

interest, tax, depreciation and amortisation (EBITDA), total debt,

ratio of debt to equity, share of long-term liabilities, implied

interest rate)

The financial data of all firms were observed in US dollars.

Indicators observed

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 7

Despite the highly comprehensive nature of the Orbis database, it has several limitations, which can be summarised as follows:

• Some SOEs are not identified as such or missing.

• There is a total absence of data on certain SOEs.

• There is a lack of data on certain indicators:

– no Belarusian or Georgian data on SOE assets; no Turkish data on number of employees; no data on credit periods for SOEs of North Macedonia

– more than half of (the nearly 40,000) SOEs in the database lack data for most indicators in most years

– peculiarities by country: Moldova has 2-3 times more SOEs with asset data in 2012 and 2014 than in other years, while many Egyptian SOEs have data on employees or revenues for only one year.

• There are potential inconsistencies in data for certain indicators:

– in Estonia, the 2011-16 credit period for many companies was cut to 0-1 day

– for some SOEs in the Slovak Republic, the same number of employees was repeated for several years in a row.

• Certain data are suspicious:

– dubious data: negative values for balance- sheet or profit-and-loss account items (such as assets, revenue and financial debt)

– outliers: overly high values for some indicators (for example, data on implied interest rates might show distortions due to large write-downs of financial assets, which were entered as financial expenses alongside interest charges).

• There were changes in SOE ID numbers after initial data downloads, making subsequent updates more challenging, notably in:

– Greece and Kazakhstan.

Data issues were alleviated by quality checks and data-cleaning procedures. Suspicious data were dropped from our calculations, usually by limiting floor or ceiling values, as we note in those sections that delve into the indicators in more detail. In addition, weighted averages were calculated wherever appropriate (mostly for liquidity, profitability and indebtedness ratios) to increase the relative importance of larger companies.

Still, caution is needed when interpreting the results. Complete time series for all indicators over the 2008-16 period were available for just 260 SOEs in eight countries. The remaining SOEs had at least one year of data missing, meaning that the consistency of some time series may be an issue. That was particularly the case with data on value added, the ratio of financial debt to EBITDA, and implied interest costs. Also, as only current owners of companies were listed, the sample may be less representative historically, especially if there were major privatisations in the meantime (for example, Poland in 2008-11). For similar reasons, data on nationalised companies prior to nationalisation (when they were still private) could not be automatically excluded; this had to be done manually when information on nationalisation was obtained (for example, Hungarian MAL Zrt in 2010).

The results in the following section are based on data available as of end November 2018.7

Data limitations and cleaning

7 The cut-off date for data from Orbis was 21 July 2018, except for

60 or so SOEs that were added between then and at the end of

November 2018.

8 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

0 1000 2000 3000 4000 5000 6000 7000 8000

KosovoTurkey

MontenegroMoldova

LithuaniaBosnia and Herz.

GreeceNorth Macedonia

KazakhstanEstonia

HungarySlovak Republic

SloveniaLatvia

CroatiaSerbia

BulgariaRomania

PolandUkraine

(2016)

*With data on assets

0

1

2

3

4

5

6

Pola

nd

Rom

ania

Hung

ary

North

Mac

edon

ia

Bulg

aria

Slov

enia

Serb

ia

Slov

ak R

epub

lic

Croa

tia

Mon

tene

gro

(Percentage of GDP; 2014-16)

Results8

Chart 2. Number of SOEs* Chart 3. Value added

8 Weighted averages are reported for shareholders’ funds,

employee costs, liquidity and profitability indicators, debt to equity,

long-term to total liabilities, implied interest rates and financial

debt to EBITDA. The data are weighted by firm assets. 9 The average number of SOEs with data on assets in 2014-16.

Crimean SOEs were included in Ukrainian SOE listings until 2013.

10 Charts 2-39 in this report use authors’ calculations based on the

Orbis database (published by Bureau van Dijk (BvD), a Moody’s

Analytics company).11 Value added was calculated as the sum of profit/loss and the

cost of employees where both sets of data were available for a

company in a given year.12 For at least 80 per cent of SOEs with data on assets in

2014-16.

Overview of the state sector

The number of SOEs analysed ranged from 20 in Kosovo to around 8,000 in Ukraine.9 As Ukraine is the largest country in the sample, it unsurprisingly boasts the greatest number of SOEs. The majority are sub-sovereign companies, while the rest (around 2,500) are centrally owned. Almost 90 per cent of the SOEs examined for this study are majority owned by the state. The only country where the state predominantly holds minority stakes (two-thirds of the total) is Greece.

SOEs in Montenegro seem to add the most value. However, this should be treated with caution due to the significant lack of data available. Overall, time series on value added11 were some of the least complete series. Data were available for a sufficient share of companies12 in fewer than half of the countries studied. Among those, Montenegrin SOEs created the most value added, at 5.5 per cent of GDP. By way of comparison, the value added of Polish SOEs was 1.5 per cent of GDP.

Source: Authors’ calculations based on the Orbis database.10 Source: Authors’ calculations based on the Orbis database.10

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 9

0

5

10

15

20

25

30

35

40

45

Koso

voLa

tvia

Esto

nia

Bulg

aria

Slov

ak R

epub

licUk

rain

ePo

land

Hung

ary

Turk

eySl

oven

iaKa

zakh

stan

Rom

ania

Gree

ce

North

Mac

edon

iaCr

oatia

Lith

uani

aSe

rbia

Mol

dova

Mon

tene

gro

Bosn

ia a

nd H

erz.

(Percentage of all SOEs, 2016)

Sector size

Based on asset size, the SOE sector is smallest in Turkey and largest in Montenegro and Ukraine. While Turkey’s SOE assets accounted for only 7 per cent of GDP in 2014-16, in Montenegro and Ukraine that figure was around 100 per cent.14 Overall, the average size of the state-owned sector is around 47 per cent of GDP. Two other countries of the former Yugoslavia (Serbia and Croatia) ranked highly in this regard — unsurprising, considering that their transition started later due to the break-up of Yugoslavia and the civil war in the 1990s. In contrast, Turkey abandoned its planned economy and state-dominated corporations in the early 1980s, which may explain the state’s relatively smaller share of GDP. However, the size of the SOE sector in Turkey may have increased considerably since 2016, as the government expropriated a number of companies belonging to businessmen facing terrorism charges after July 2016.

14 Negative values on assets were omitted from calculations.

Results (continued)

Bosnia and Herzegovina has the largest percentage of listed SOEs. Somewhat surprisingly, listed SOEs are not that common in the more developed central and eastern European economies, unlike the relatively less developed and smaller countries. Bosnia and Herzegovina ranks first, with one in three SOEs listed. However, this is mostly the result of a mass privatisation programme in the late-1990s, when two stock exchanges were established to enable citizens to invest in their national enterprises. In reality, the exchanges are illiquid and very few companies use them to raise capital. Furthermore, most of the listed companies are too small to efficiently use the stock exchange to raise capital.13

Chart 4. Listed SOEs

13 See World Bank (2015).

Source: Authors’ calculations based on the Orbis database.10

10 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

0

20

40

60

80

100

120

Turk

eyM

oldo

vaKo

sovo

Rom

ania

Hung

ary

Lith

uani

aBu

lgar

iaPo

land

Kaza

khst

anLa

tvia

North

Mac

edon

iaGr

eece

Esto

nia

Bosn

ia a

nd H

erz.

Slov

enia

Slov

ak R

epub

licCr

oatia

Serb

iaUk

rain

eM

onte

negr

o

(Percentage of GDP)

2016 2014

0

10

20

30

40

50

60

70

80

90

(Percentage of assets; 2016)

Pola

ndRo

man

iaLa

tvia

Slov

enia

Bulg

aria

Mol

dova

Kaza

khst

anSl

ovak

Rep

ublic

Lith

uani

aSe

rbia

Bosn

ia a

nd H

erz.

Hung

ary

Gree

ceCr

oatia

Esto

nia

Mon

tene

gro

Turk

eyNo

rth M

aced

onia

Ukra

ine

Koso

vo

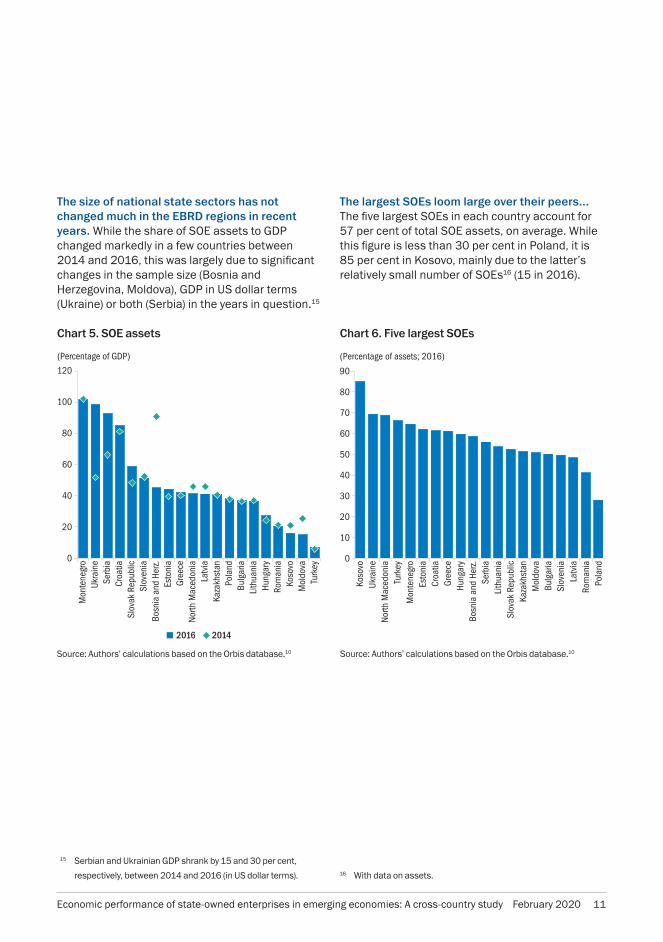

The size of national state sectors has not changed much in the EBRD regions in recent years. While the share of SOE assets to GDP changed markedly in a few countries between 2014 and 2016, this was largely due to significant changes in the sample size (Bosnia and Herzegovina, Moldova), GDP in US dollar terms (Ukraine) or both (Serbia) in the years in question.15

Chart 5. SOE assets

15 Serbian and Ukrainian GDP shrank by 15 and 30 per cent,

respectively, between 2014 and 2016 (in US dollar terms).

The largest SOEs loom large over their peers... The five largest SOEs in each country account for 57 per cent of total SOE assets, on average. While this figure is less than 30 per cent in Poland, it is 85 per cent in Kosovo, mainly due to the latter’s relatively small number of SOEs16 (15 in 2016).

Chart 6. Five largest SOEs

16 With data on assets.

Source: Authors’ calculations based on the Orbis database.10 Source: Authors’ calculations based on the Orbis database.10

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 11

0

10

20

30

40

50

60

70

80

90

Turk

eyM

oldo

vaKo

sovo

Rom

ania

Hung

ary

Gree

ceBu

lgar

iaKa

zakh

stan

Latv

iaPo

land

Esto

nia

North

Mac

edon

iaSl

oven

iaBo

snia

and

Her

z.Li

thua

nia

Slov

ak R

epub

licSe

rbia

Croa

tiaUk

rain

eM

onte

negr

o(Percentage of GDP)

2016 2014

(Percentage of assets; 2016)

0

10

20

30

40

50

60

70

80

90

Turk

eyM

oldo

vaM

onte

negr

oHu

ngar

ySl

ovak

Rep

ublic

Gree

ceBo

snia

and

Her

z.Ko

sovo

Rom

ania

Bulg

aria

North

Mac

edon

iaEs

toni

aSl

oven

iaLi

thua

nia

Serb

iaKa

zakh

stan

Croa

tiaLa

tvia

Ukra

ine

Pola

nd

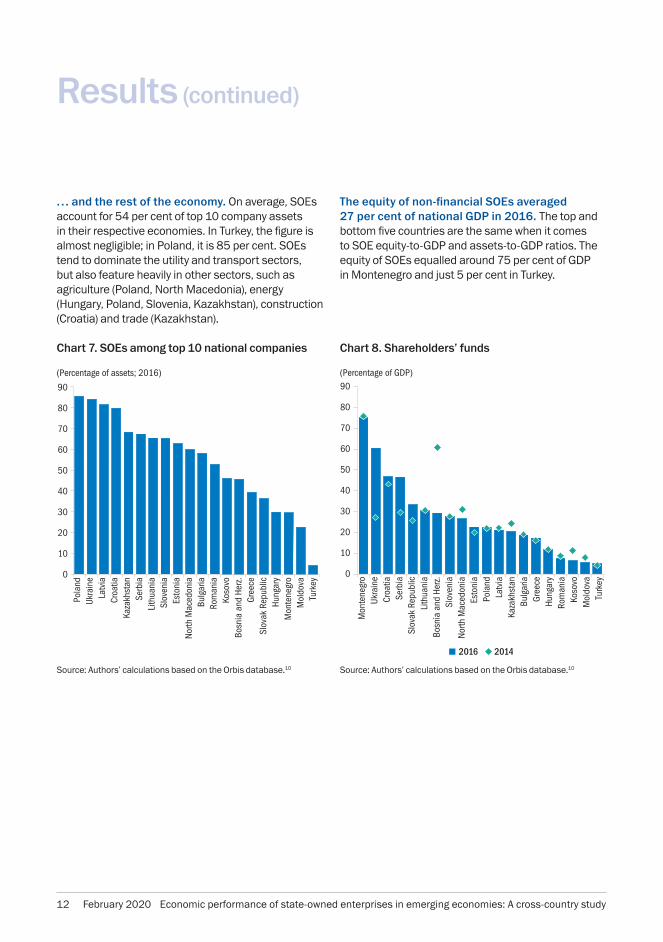

The equity of non-financial SOEs averaged 27 per cent of national GDP in 2016. The top and bottom five countries are the same when it comes to SOE equity-to-GDP and assets-to-GDP ratios. The equity of SOEs equalled around 75 per cent of GDP in Montenegro and just 5 per cent in Turkey.

Chart 8. Shareholders’ fundsChart 7. SOEs among top 10 national companies

… and the rest of the economy. On average, SOEs account for 54 per cent of top 10 company assets in their respective economies. In Turkey, the figure is almost negligible; in Poland, it is 85 per cent. SOEs tend to dominate the utility and transport sectors, but also feature heavily in other sectors, such as agriculture (Poland, North Macedonia), energy (Hungary, Poland, Slovenia, Kazakhstan), construction (Croatia) and trade (Kazakhstan).

Results (continued)

Source: Authors’ calculations based on the Orbis database.10Source: Authors’ calculations based on the Orbis database.10

12 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

0

5

10

15

20

25

30

35

40

Turk

eyKo

sovo

North

Mac

edon

iaRo

man

iaLi

thua

nia

Esto

nia

Mol

dova

Slov

ak R

epub

licKa

zakh

stan

Bulg

aria

Bosn

ia a

nd H

erz.

Gree

ceLa

tvia

Hung

ary

Mon

tene

gro

Serb

iaCr

oatia

Pola

ndUk

rain

eSl

oven

ia

(Percentage of GDP; 2014-16)

0123456789

10111213141516

Gree

ce

Mol

dova

Kaza

khst

an

Rom

ania

Esto

nia

Hung

ary

Slov

ak R

epub

lic

North

Mac

edon

ia

Lith

uani

a

Slov

enia

Croa

tia

Koso

vo

Mon

tene

gro

Serb

ia

Ukra

ine

Latv

ia

Bulg

aria

(Percentage of total national employment)

2016 2014

SOEs generate revenues of around 15 per cent of GDP. The scale of revenues to GDP ranges from 5 per cent in Kosovo to 33 per cent in Slovenia. In general, most revenues come from SOEs in the utility and transport sectors.

Chart 9. Revenues

Employment

Non-financial SOEs account for 5 per cent of total employment, on average. Their contribution varies from 2 per cent in Greece to more than 14 per cent in Bulgaria.17 While some economies (Kosovo, North Macedonia and Moldova, for example) saw this share change significantly between 2014 and 2016, this was primarily down to changes in the number of companies providing employee data.

Chart 10. SOE employment

17 Poland and Bosnia and Herzegovina were excluded from

calculations as significantly fewer SOEs posted employee data

in 2016 than in previous years, while Turkey was omitted due to

lack of data.

Source: Authors’ calculations based on the Orbis database.10 Source: Authors’ calculations based on the Orbis database.10

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 13

0

1

2

3

4

5

Serb

iaM

oldo

vaNo

rth M

aced

onia

Hung

ary

Ukra

ine

Croa

tiaPo

land

Bosn

ia a

nd H

erz.

Slov

enia

Latv

iaBu

lgar

iaGr

eece

Mon

tene

gro

Slov

ak R

epub

licTu

rkey

Lith

uani

aKo

sovo

Rom

ania

Kaza

khst

anEs

toni

a

(2016)

0

5

10

15

20

25

30

35

40

45

Latv

ia

Esto

nia

Hung

ary

Slov

enia

Ukra

ine

Slov

ak R

epub

lic

Pola

nd

Croa

tia

Rom

ania

Bulg

aria

Serb

ia

Bosn

ia a

nd H

erz.

Mon

tene

gro

North

Mac

edon

ia

(Percentage of total revenue; 2014-16)

Liquidity

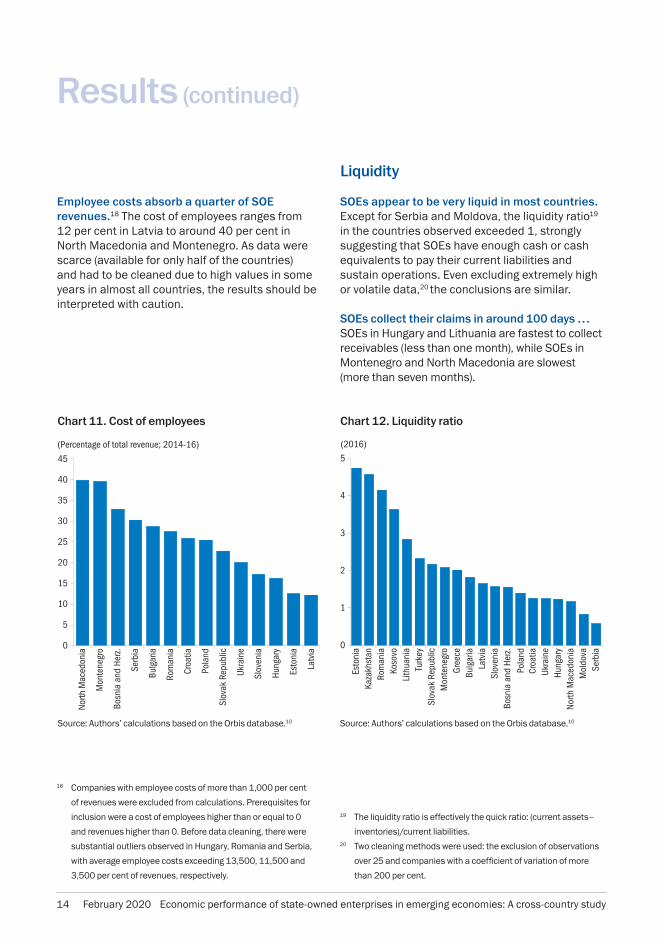

SOEs appear to be very liquid in most countries. Except for Serbia and Moldova, the liquidity ratio19 in the countries observed exceeded 1, strongly suggesting that SOEs have enough cash or cash equivalents to pay their current liabilities and sustain operations. Even excluding extremely high or volatile data,20 the conclusions are similar.

SOEs collect their claims in around 100 days … SOEs in Hungary and Lithuania are fastest to collect receivables (less than one month), while SOEs in Montenegro and North Macedonia are slowest (more than seven months).

Chart 12. Liquidity ratio

19 The liquidity ratio is effectively the quick ratio: (current assets–

inventories)/current liabilities.20 Two cleaning methods were used: the exclusion of observations

over 25 and companies with a coefficient of variation of more

than 200 per cent.

Employee costs absorb a quarter of SOE revenues.18 The cost of employees ranges from 12 per cent in Latvia to around 40 per cent in North Macedonia and Montenegro. As data were scarce (available for only half of the countries) and had to be cleaned due to high values in some years in almost all countries, the results should be interpreted with caution.

Chart 11. Cost of employees

18 Companies with employee costs of more than 1,000 per cent

of revenues were excluded from calculations. Prerequisites for

inclusion were a cost of employees higher than or equal to 0

and revenues higher than 0. Before data cleaning, there were

substantial outliers observed in Hungary, Romania and Serbia,

with average employee costs exceeding 13,500, 11,500 and

3,500 per cent of revenues, respectively.

Source: Authors’ calculations based on the Orbis database.10 Source: Authors’ calculations based on the Orbis database.10

Results (continued)

14 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

0 50 100 150 200 2500

50

100

150

200

250

HRVHUN

HRVLVA

LTUPOL

BGR

SRB

KAZSVK GRC

UKRROU

BIH TUR

KOS

MNE

HRVMDA

SVN

Cred

it pe

riod

Collection period

(Days, 2014-16)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

(Percentage of GDP; 2014-16)

Serb

iaBo

snia

and

Her

z.Bu

lgar

iaGr

eece

Mol

dova

Slov

enia

Mon

tene

gro

Koso

voTu

rkey

Rom

ania

Pola

ndNo

rth M

aced

onia

Lith

uani

aLa

tvia

Hung

ary

Kaza

khst

anCr

oatia

Esto

nia

Slov

ak R

epub

licUk

rain

e

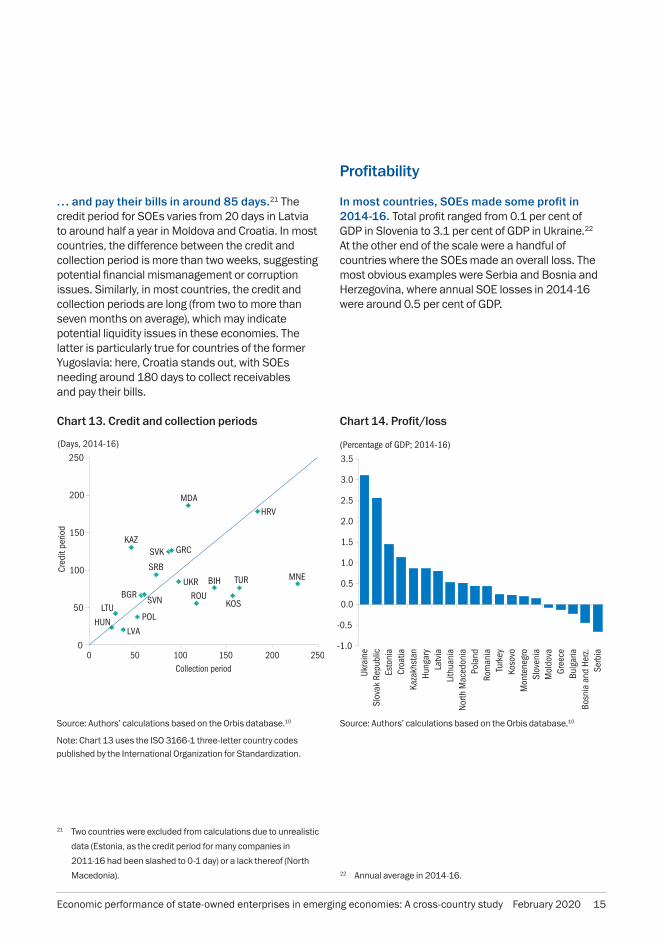

… and pay their bills in around 85 days.21 The credit period for SOEs varies from 20 days in Latvia to around half a year in Moldova and Croatia. In most countries, the difference between the credit and collection period is more than two weeks, suggesting potential financial mismanagement or corruption issues. Similarly, in most countries, the credit and collection periods are long (from two to more than seven months on average), which may indicate potential liquidity issues in these economies. The latter is particularly true for countries of the former Yugoslavia: here, Croatia stands out, with SOEs needing around 180 days to collect receivables and pay their bills.

Chart 13. Credit and collection periods

21 Two countries were excluded from calculations due to unrealistic

data (Estonia, as the credit period for many companies in

2011-16 had been slashed to 0-1 day) or a lack thereof (North

Macedonia).

Source: Authors’ calculations based on the Orbis database.10

Note: Chart 13 uses the ISO 3166-1 three-letter country codes published by the International Organization for Standardization.

Profitability

In most countries, SOEs made some profit in 2014-16. Total profit ranged from 0.1 per cent of GDP in Slovenia to 3.1 per cent of GDP in Ukraine.22 At the other end of the scale were a handful of countries where the SOEs made an overall loss. The most obvious examples were Serbia and Bosnia and Herzegovina, where annual SOE losses in 2014-16 were around 0.5 per cent of GDP.

Chart 14. Profit/loss

22 Annual average in 2014-16.

Source: Authors’ calculations based on the Orbis database.10

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 15

-30

-25

-20

-15

-10

-5

0

5

10

15

Serb

iaGr

eece

Bosn

ia a

nd H

erz.

Mon

tene

gro

Ukra

ine

Slov

enia

Bulg

aria

North

Mac

edon

iaPo

land

Mol

dova

Lith

uani

aCr

oatia

Latv

iaHu

ngar

yKo

sovo

Esto

nia

Rom

ania

Turk

eySl

ovak

Rep

ublic

Kaza

khst

an

(Percentage; 2014-16)

-2

-1

0

1

2

3

4

5

6

7

8

Ukra

ine

Bosn

ia a

nd H

erz.

Bulg

aria

Mol

dova

Gree

ceNo

rth M

aced

onia

Serb

iaM

onte

negr

oSl

oven

iaLi

thua

nia

Koso

voCr

oatia

Pola

ndLa

tvia

Rom

ania

Hung

ary

Esto

nia

Turk

eySl

ovak

Rep

ublic

Kaza

khst

an

(Percentage; 2014-16)

The ROE ranged from 13 per cent in Kazakhstan to -30 per cent in Serbia. The considerable negative ratio in Serbia was a consequence of an outlier (a large SOE had an extremely low 2015 ROE of around -16,500 per cent). Excluding this, Serbian SOEs posted an average ROE of 7.4 per cent, faring much better on this indicator than on overall profitability. However, it could be that the ROE was propped up by the relatively high indebtedness of Serbian SOEs and, consequently, relatively lower equity levels. Hence, individual ROE ratios should be examined in the context of SOE indebtedness.

Chart 16. Return on equity

The ROA23 of SOEs averaged 1.7 per cent in 2014-16. Kazakhstan seems to have had the most profitable firms (with an ROA of more than 6 per cent), but they are likely to have received a significant boost from the currency depreciation of 2015 (of around 50 per cent). This is typical of countries and companies that see (commodity) exports increase in value due to depreciation; wage costs and domestic input prices adjust more slowly, boosting profits. Ukraine, in contrast, experienced even greater depreciation over the same period, but armed conflict meant companies were unable to capitalise on it.

Chart 15. Return on assets

23 ROA and ROE were not automatically taken from Orbis, but

recalculated to increase sample size.

Results (continued)

Source: Authors’ calculations based on the Orbis database.10 Source: Authors’ calculations based on the Orbis database.10

16 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

(Percentage of GDP)

0

5

10

15

20

25

30

Turk

eyM

oldo

vaHu

ngar

yRo

man

iaBu

lgar

iaLi

thua

nia

Bosn

ia a

nd H

erz.

North

Mac

edon

iaPo

land

Koso

voSl

ovak

Rep

ublic

Latv

iaUk

rain

eM

onte

negr

oGr

eece

Kaza

khst

anSl

oven

iaEs

toni

aCr

oatia

Serb

ia

2016 2014

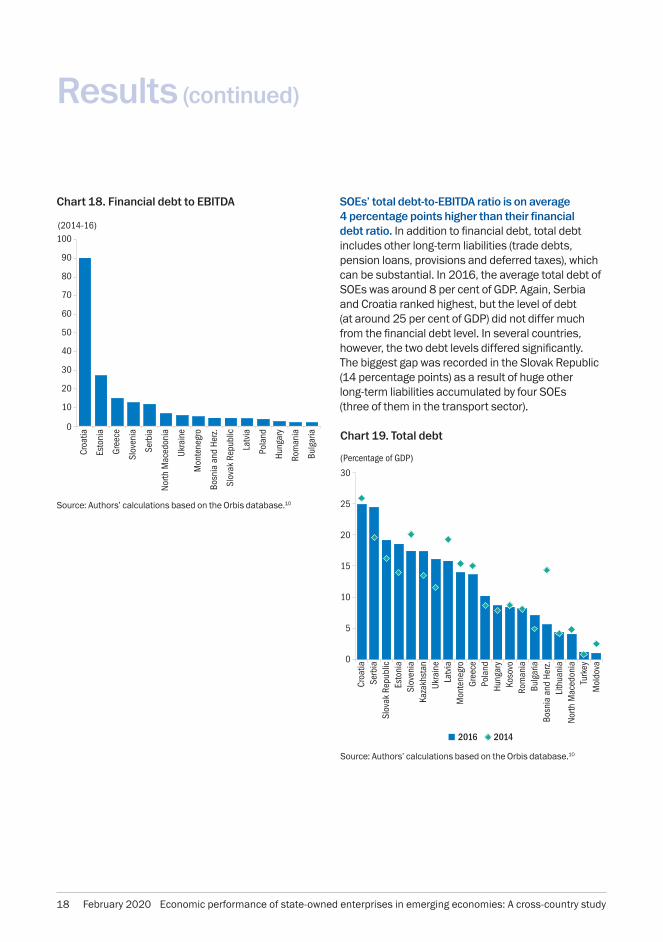

Serbian and Croatian SOEs are the most (financially) indebted, while the opposite is true for Turkish, Moldovan and Hungarian SOEs. The financial debt of SOEs in Serbia and Croatia was 23 per cent of GDP (compared with less than 1 per cent in Turkey, Moldova and Hungary and average financial debt for all countries of 8 per cent of GDP). In Serbia and Croatia, a large amount of debt is held by a handful of firms. In Croatia, three road companies hold US$ 5.6 billion of debt (more than 11 per cent of GDP) amassed during the rapid expansion and modernisation of the country’s road infrastructure. In Serbia, almost 60 per cent of all SOE debt is held by five SOEs; the largest two are in the utilities sector (electricity and gas) and have more than doubled their debt since 2010.

In most countries, the financial debt of SOEs did not change much from 2014 to 2016. Even when there was a more significant change, this was largely a consequence of changes in sample size and/or GDP. Slovenia and Latvia are notable exceptions, with SOEs deleveraging by 25-30 per cent between 2014 and 2016.

Indebtedness

Chart 17. Financial debt

Source: Authors’ calculations based on the Orbis database.10

SOEs in some countries may find it difficult to pay off their debt. Results based on this indicator should be treated with caution, due to the lack of data in certain countries and the calculation requirements, which further shrank the sample.24 That said, Croatian SOEs may be worst off in terms of debt repayment, as the financial debt of SOEs with positive EBITDA is on average 90 times EBITDA.25 In contrast, Bulgarian SOEs seem to be in pretty good shape, with the debt of just 1.5 times EBITDA. Alternative calculations26 suggest that SOEs in Croatia, Greece and Serbia are least able to pay off their debt (with debt-to-EBITDA ratios between 5 and 6), while the opposite is true for SOEs in Bulgaria, Hungary and Romania (with ratios of less than 1). (See Chart 18 on page 18.)

24 The calculation was confined to firms that had financial debt

higher than or equal to 0 (to eliminate unsound data) and positive

non-zero EBITDA. Negative EBITDA was excluded, as it would have

reduced national averages (whereas loss-makers are more likely

to have repayment problems). Zero EBITDA was omitted, as a

denominator cannot have zero value. Data were not available for

Kazakhstan, Kosovo, Lithuania, Moldova or Turkey.25 Values of more than 1,000 were excluded from calculations. The

three Croatian road companies were not among the outliers. Prior

to cleaning, Serbia ranked first, with financial debt of almost 180

times EBITDA due to the extremely high financial debt-to-EBITDA

ratio (18,000) of one relatively large SOE in 2014. 26 The sum of a country’s SOE financial debt was divided by the sum

of its EBITDA. The only condition was that a company had data on

both variables in a given year.

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 17

0

5

10

15

20

25

30

(Percentage of GDP)

Mol

dova

Turk

eyNo

rth M

aced

onia

Lith

uani

aBo

snia

and

Her

z.Bu

lgar

iaRo

man

iaKo

sovo

Hung

ary

Pola

ndGr

eece

Mon

tene

gro

Latv

iaUk

rain

eKa

zakh

stan

Slov

enia

Esto

nia

Slov

ak R

epub

licSe

rbia

Croa

tia

2016 2014

0

10

20

30

40

50

60

70

80

90

100(2014-16)

Bulg

aria

Rom

ania

Hung

ary

Pola

nd

Latv

ia

Slov

ak R

epub

lic

Bosn

ia a

nd H

erz.

Mon

tene

gro

Ukra

ine

North

Mac

edon

ia

Serb

ia

Slov

enia

Gree

ce

Esto

nia

Croa

tia

SOEs’ total debt-to-EBITDA ratio is on average 4 percentage points higher than their financial debt ratio. In addition to financial debt, total debt includes other long-term liabilities (trade debts, pension loans, provisions and deferred taxes), which can be substantial. In 2016, the average total debt of SOEs was around 8 per cent of GDP. Again, Serbia and Croatia ranked highest, but the level of debt (at around 25 per cent of GDP) did not differ much from the financial debt level. In several countries, however, the two debt levels differed significantly. The biggest gap was recorded in the Slovak Republic (14 percentage points) as a result of huge other long-term liabilities accumulated by four SOEs (three of them in the transport sector).

Chart 19. Total debt

Chart 18. Financial debt to EBITDA

Source: Authors’ calculations based on the Orbis database.10

Source: Authors’ calculations based on the Orbis database.10

Results (continued)

18 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

0

20

40

60

80

100

120

140

160

180

Mon

tene

gro

Lith

uani

aM

oldo

vaSe

rbia

Turk

eyUk

rain

eBo

snia

and

Her

z.Ka

zakh

stan

Pola

ndBu

lgar

iaCr

oatia

Slov

enia

Esto

nia

Latv

iaSl

ovak

Rep

ublic

Gree

ceHu

ngar

yRo

man

iaKo

sovo

(Percentage; 2016)

0

10

20

30

40

50

60

70

80

90

(Percentage of total liabilities)

Mol

dova

North

Mac

edon

iaSe

rbia

Bosn

ia a

nd H

erz.

Bulg

aria

Lith

uani

aUk

rain

eTu

rkey

Hung

ary

Pola

ndM

onte

negr

oGr

eece

Kaza

khst

anCr

oatia

Esto

nia

Slov

enia

Rom

ania

Latv

iaSl

ovak

Rep

ublic

Koso

vo

2016 2014

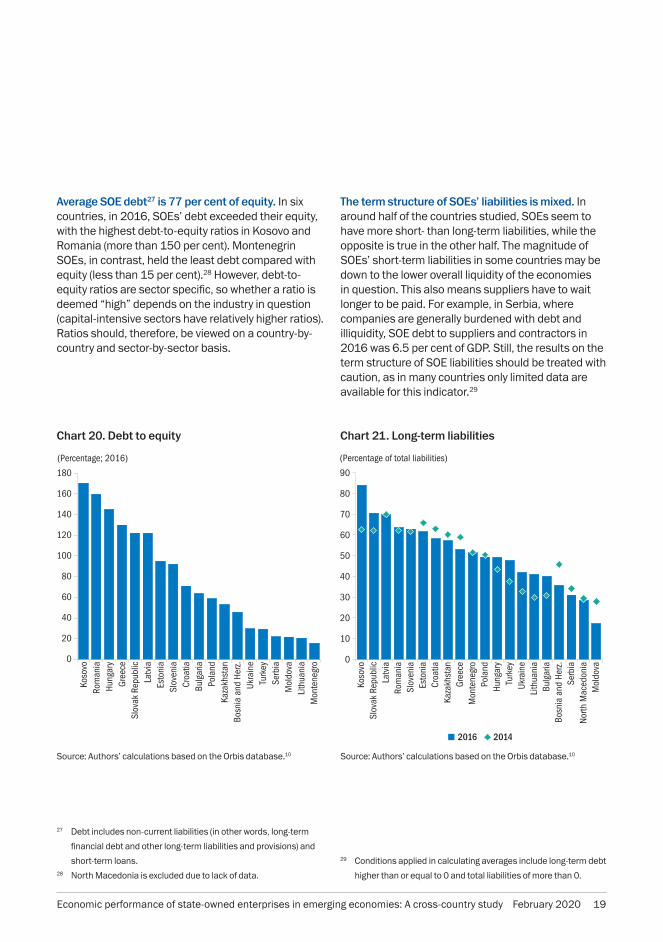

Average SOE debt27 is 77 per cent of equity. In six countries, in 2016, SOEs’ debt exceeded their equity, with the highest debt-to-equity ratios in Kosovo and Romania (more than 150 per cent). Montenegrin SOEs, in contrast, held the least debt compared with equity (less than 15 per cent).28 However, debt-to-equity ratios are sector specific, so whether a ratio is deemed “high” depends on the industry in question (capital-intensive sectors have relatively higher ratios). Ratios should, therefore, be viewed on a country-by-country and sector-by-sector basis.

Chart 20. Debt to equity

27 Debt includes non-current liabilities (in other words, long-term

financial debt and other long-term liabilities and provisions) and

short-term loans. 28 North Macedonia is excluded due to lack of data.

The term structure of SOEs’ liabilities is mixed. In around half of the countries studied, SOEs seem to have more short- than long-term liabilities, while the opposite is true in the other half. The magnitude of SOEs’ short-term liabilities in some countries may be down to the lower overall liquidity of the economies in question. This also means suppliers have to wait longer to be paid. For example, in Serbia, where companies are generally burdened with debt and illiquidity, SOE debt to suppliers and contractors in 2016 was 6.5 per cent of GDP. Still, the results on the term structure of SOE liabilities should be treated with caution, as in many countries only limited data are available for this indicator.29

Chart 21. Long-term liabilities

29 Conditions applied in calculating averages include long-term debt

higher than or equal to 0 and total liabilities of more than 0.

Source: Authors’ calculations based on the Orbis database.10 Source: Authors’ calculations based on the Orbis database.10

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 19

SOEs by sector30

Utilities

Summary

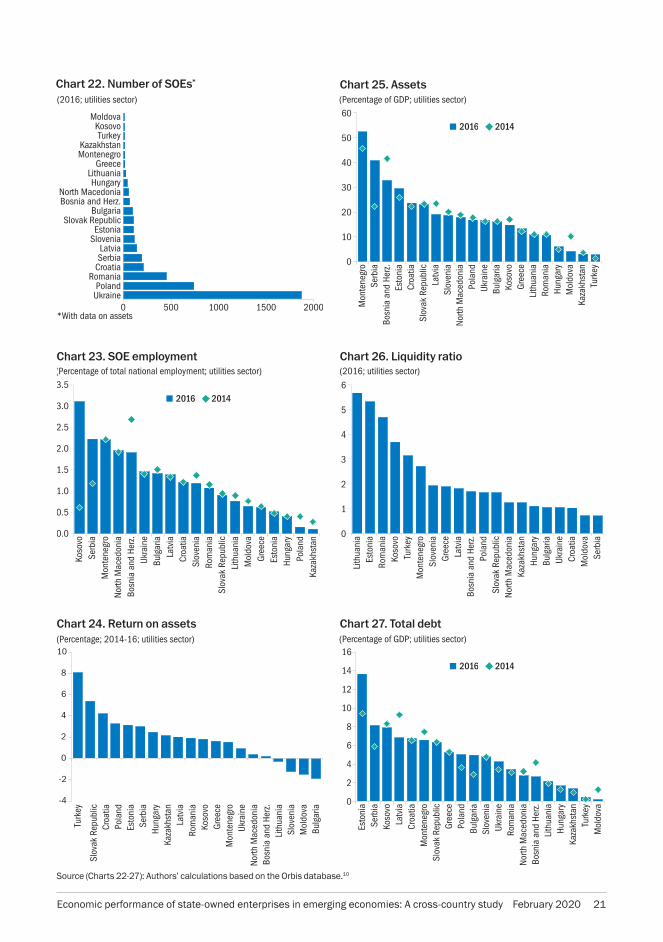

• The number of utility-sector SOEs ranged from 7 in Moldova to 1,870 in Ukraine.

• In terms of assets and equity to GDP, the state-owned utility sector is the largest in Montenegro, Serbia and Bosnia and Herzegovina and smallest in Turkey, Kazakhstan and Moldova. While Turkey’s state-owned utility assets equate to less than 3 per cent of GDP, Montenegro’s figure is more than 50 per cent. Overall, the average size of the state-owned utility sector in asset terms is around 19 per cent of GDP. The equity of state-owned utilities equals 1 per cent of GDP in Moldova and 40 per cent of GDP in Montenegro, compared with an overall average ratio of 11 per cent.

• Slovenian state-owned utilities generate revenues of up to 14 per cent of GDP, while utilities in Kosovo contribute up to 3 per cent of total employment. State-owned utilities in Serbia, Montenegro, North Macedonia and Bosnia and Herzegovina also employ a relatively sizeable slice of their country’s workforce (around 2 per cent). In contrast, Kazakhstan’s state-owned utilities generate the least revenue and contribute least to employment (0.9 per cent of GDP and 0.1 per cent of total employment, respectively).

• Lithuanian and Estonian state-owned utilities are the most liquid (with a liquidity ratio of more than 5), while Serbian and Moldovan utilities are the most illiquid (with a liquidity ratio of less than 1).

• Latvian and Hungarian utilities are fastest to pay their bills and Kazakh utilities are fastest to collect their receivables (it takes them less than a month). State-owned utilities in Montenegro and North Macedonia, in contrast, need around 11 months to collect their receivables, while Greek utilities take more than 4 months to pay their dues.

• While state-owned utilities seem to be most profitable in Turkey and the Slovak Republic (average ROA in 2014-16 of more than 5 per cent), the opposite goes for Bulgaria and Moldova (average ROA equal to or less than –1.5 per cent).

• Estonian state-owned utilities are most indebted (total debt of 14 per cent of GDP); Turkish and Moldovan utilities the least (total debt of less than 1 per cent of GDP).

30 Results by sector should be treated with greater caution and

examined in more detail due to the relatively smaller samples

(sometimes comprising only a few companies) and potentially

more pronounced data issues. The cleaning options applied to

country-level results hold, as do the time periods observed (2016

for stock and 2014-16 for flow variables). Source for all charts:

author’s calculations based on the Orbis database (published by

BvD, a Moody’s Analytics company).

20 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

0 500 1000 1500 2000*With data on assets

MoldovaKosovoTurkey

KazakhstanMontenegro

GreeceLithuaniaHungary

North MacedoniaBosnia and Herz.

BulgariaSlovak Republic

EstoniaSlovenia

LatviaSerbia

CroatiaRomania

PolandUkraine

(2016; utilities sector)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Kaza

khst

anPo

land

Hung

ary

Esto

nia

Gree

ceM

oldo

vaLi

thua

nia

Slov

ak R

epub

licRo

man

iaSl

oven

iaCr

oatia

Latv

iaBu

lgar

iaUk

rain

eBo

snia

and

Her

z.No

rth M

aced

onia

Mon

tene

gro

Serb

iaKo

sovo

(Percentage of total national employment; utilities sector)

2016 2014

-4

-2

0

2

4

6

8

10

Bulg

aria

Mol

dova

Slov

enia

Lith

uani

aBo

snia

and

Her

z.No

rth M

aced

onia

Ukra

ine

Mon

tene

gro

Gree

ceKo

sovo

Rom

ania

Latv

iaKa

zakh

stan

Hung

ary

Serb

iaEs

toni

aPo

land

Croa

tiaSl

ovak

Rep

ublic

Turk

ey

(Percentage; 2014-16; utilities sector)

0

10

20

30

40

50

60

Turk

eyKa

zakh

stan

Mol

dova

Hung

ary

Rom

ania

Lith

uani

aGr

eece

Koso

voBu

lgar

iaUk

rain

ePo

land

North

Mac

edon

iaSl

oven

iaLa

tvia

Slov

ak R

epub

licCr

oatia

Esto

nia

Bosn

ia a

nd H

erz.

Serb

iaM

onte

negr

o

(Percentage of GDP; utilities sector)

2016 2014

0

1

2

3

4

5

6

Serb

iaM

oldo

vaCr

oatia

Ukra

ine

Bulg

aria

Hung

ary

Kaza

khst

anNo

rth M

aced

onia

Slov

ak R

epub

licPo

land

Bosn

ia a

nd H

erz.

Latv

iaGr

eece

Slov

enia

Mon

tene

gro

Turk

eyKo

sovo

Rom

ania

Esto

nia

Lith

uani

a

(2016; utilities sector)

0

2

4

6

8

10

12

14

16

Mol

dova

Turk

eyKa

zakh

stan

Hung

ary

Lith

uani

aBo

snia

and

Her

z.No

rth M

aced

onia

Rom

ania

Ukra

ine

Slov

enia

Bulg

aria

Pola

ndGr

eece

Slov

ak R

epub

licM

onte

negr

oCr

oatia

Latv

iaKo

sovo

Serb

iaEs

toni

a

(Percentage of GDP; utilities sector)

2016 2014

Chart 23. SOE employment

Chart 24. Return on assets

Chart 26. Liquidity ratio

Chart 27. Total debt

Source (Charts 22-27): Authors’ calculations based on the Orbis database.10

Chart 22. Number of SOEs* Chart 25. Assets

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 21

Transport

Summary

• The number of SOEs in the transport sector ranges from 3 in Kosovo and Bosnia and Herzegovina to around 340 in Ukraine.

• In terms of both assets and equity, the state-owned transport sector is largest in Ukraine and smallest in Moldova and Kosovo. While state-owned transport assets in Moldova and Kosovo account for less than 2 per cent of GDP, in Ukraine they make up more than 36 per cent. In asset terms, the average size of the transport sector in the countries studied is 11 per cent of GDP. The equity of state-owned transport companies is less than 0.5 per cent of GDP in Moldova and Kosovo compared with 25 per cent in Ukraine and a country average of 6 per cent.

• Montenegrin state-owned transport firms generate the most revenues (5 per cent of GDP), while Bulgaria’s companies contribute most to total employment (2.8 per cent), both followed closely by Latvian state-owned transport companies. In contrast, transport SOEs in Kosovo produce only 0.3 per cent of GDP in revenues, while Polish state transport firms employ only 0.1 per cent of the country’s workforce.

• Croatia’s transport SOEs are the most liquid (with a liquidity ratio of more than 4.5), while Hungarian and Bosnian firms are the most illiquid (with a liquidity ratio of less than 0.7).31 Liquidity seems to be problematic (with a ratio of less than 1), too, for state-owned transport companies in Greece, Latvia, North Macedonia, Poland and Serbia.

• Latvian transport SOEs are among the fastest ones to pay their bills and collect their receivables (less than 20 days), while Turkish firms are among the slowest (needing around 11 months to collect and almost four months to pay their bills).

• While Estonia’s state-owned transport companies seem to be the most profitable (with an average ROA in 2014-16 of around 4.5 per cent), the opposite is true for transport SOEs in Kosovo (with an average ROA of – 5.5 per cent).

• Slovakian transport firms are most indebted (with total debt of 12 per cent of GDP); Turkish and Kosovan SOEs are the least burdened (0.2-0.3 per cent of GDP).32

31 Moldovan SOEs were excluded, as only one company provided

data on its liquidity ratio.32 Moldovan SOEs were omitted, as data on total debt were only

available for one company.

SOEs by sector (continued)

22 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

(2016; transport sector)

0 50 100 150 200 250 300 350 400

KosovoBosnia and Herz.

MoldovaTurkey

KazakhstanLithuania

North MacedoniaMontenegro

EstoniaGreece

SloveniaSlovak Republic

HungaryCroatia

LatviaBulgaria

SerbiaRomania

PolandUkraine

*With data on assets

(Percentage of total national employment; transport sector)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Pola

ndKo

sovo

Gree

ceBo

snia

and

Her

z.Ka

zakh

stan

Mol

dova

North

Mac

edon

iaRo

man

iaEs

toni

aSl

oven

iaLi

thua

nia

Croa

tiaSe

rbia

Hung

ary

Mon

tene

gro

Slov

ak R

epub

licUk

rain

eLa

tvia

Bulg

aria

2016 2014

(Percentage; 2014-16; transport sector)

-6

-4

-2

0

2

4

6

Koso

voBo

snia

and

Her

z.Gr

eece

Mon

tene

gro

North

Mac

edon

iaBu

lgar

iaUk

rain

eLi

thua

nia

Rom

ania

Pola

ndHu

ngar

yLa

tvia

Serb

iaCr

oatia

Turk

eySl

oven

iaSl

ovak

Rep

ublic

Kaza

khst

anM

oldo

vaEs

toni

a

(Percentage of GDP; transport sector)

0

5

10

15

20

25

30

35

40

Koso

voM

oldo

vaTu

rkey

Bosn

ia a

nd H

erz.

Rom

ania

Pola

ndHu

ngar

yLi

thua

nia

Latv

iaNo

rth M

aced

onia

Esto

nia

Croa

tiaGr

eece

Serb

iaKa

zakh

stan

Bulg

aria

Slov

enia

Slov

ak R

epub

licM

onte

negr

oUk

rain

e

2016 2014

(2016; transport sector)

0

1

2

3

4

5

6

Hung

ary

Bosn

ia a

nd H

erz.

Serb

iaPo

land

North

Mac

edon

iaLa

tvia

Gree

ceUk

rain

eKa

zakh

stan

Slov

enia

Mon

tene

gro

Bulg

aria

Lith

uani

aTu

rkey

Slov

ak R

epub

licRo

man

iaEs

toni

aKo

sovo

Croa

tia

0

2

4

6

8

10

12

Turk

eyKo

sovo

North

Mac

edon

iaLi

thua

nia

Bosn

ia a

nd H

erz.

Bulg

aria

Serb

iaCr

oatia

Pola

ndRo

man

iaGr

eece

Esto

nia

Hung

ary

Latv

iaUk

rain

eKa

zakh

stan

Mon

tene

gro

Slov

enia

Slov

ak R

epub

lic

(Percentage of GDP; transport sector)

2016 2014

Source (Charts 28-33): Authors’ calculations based on the Orbis database.10

Chart 28. Number of SOEs*

Chart 29. SOE employment

Chart 30. Return on assets

Chart 31. Assets

Chart 32 . Liquidity ratio

Chart 33. Total debt

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 23

Manufacturing

Summary

• The number of SOEs in the manufacturing sector ranges between 2 and 4 in Baltic states and Montenegro, and 665 in Ukraine.33

• In terms of assets, the state-owned manufacturing sector is largest in Serbia (at close to 7 per cent of GDP), while in terms of equity, it is largest in Montenegro (at around 3 per cent of GDP). State-owned manufacturing is smallest in Estonia and the Slovak Republic (with assets corresponding to just 0.1 per cent of GDP). Serbian and Ukrainian SOEs have total negative equity of 3.8 and 0.5 per cent of GDP, respectively. Serbian manufacturing SOEs seem to stand out for all the wrong reasons in other respects too.

• Polish manufacturing SOEs generate the most revenue (6 per cent of GDP), while Serbian firms contribute most to total employment (1.2 per cent). In contrast, manufacturing SOEs in most countries make less than 1 per cent of GDP in revenues and employ less than 0.3 per cent of the total workforce.

• Bulgarian manufacturing SOEs are extremely liquid (with a liquidity ratio of 8) and Serbian SOEs are the most illiquid (with a liquidity ratio of less than 0.3). Liquidity seems to be an issue for SOEs in Ukraine, too (where the ratio is less than 1).34

• Hungarian SOEs are the fastest to pay their bills (around 20 days), while Kazakh and Slovakian state manufacturers rush to collect receivables (in around one month).35 Serbian and Greek SOEs, meanwhile, need almost nine months to pay their bills, while Montenegrin, Croatian and Greek SOEs need more than six months to collect receivables.

• Bulgarian and Hungarian manufacturing SOEs seem to be very profitable (with an average ROA in 2014-16 of around 12 per cent), unlike Serbian state-owned manufacturers (with an average ROA in the same period of –12 per cent).36

• While in most countries the debt of state-run manufacturers is fairly low (less than 0.5 per cent of GDP), in Serbia it is quite high (at almost 5 per cent of GDP).

34 Although Latvian and Estonian manufacturing SOEs seem to

score poorly on liquidity, in each case, this is down to one illiquid

company (out of a total of two in the sector with data on assets).35 Latvian and Estonian manufacturing SOEs need only 4 and 14

days, respectively, to collect receivables, but the result is affected

by the small number of companies in the sample (2).36 Again, the result for Estonian state-owned manufacturers was

strongly influenced by developments at just one company.

33 Kosovo was omitted from the assessment, as there were no

data on Kosovan state-owned manufacturers.

SOEs by sector (continued)

24 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

(Percentage; 2014-16; transport sector)

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

Esto

nia

Serb

iaBo

snia

and

Her

z.Uk

rain

eGr

eece

Slov

enia

North

Mac

edon

iaCr

oatia

Slov

ak R

epub

licM

oldo

vaM

onte

negr

oLa

tvia

Pola

ndLi

thua

nia

Kaza

khst

anTu

rkey

Rom

ania

Hung

ary

Bulg

aria

(Percentage of GDP; manufacturing sector)

0

1

2

3

4

5

6

7

8

9

Mol

dova

Lith

uani

aBu

lgar

iaLa

tvia

North

Mac

edon

iaGr

eece

Hung

ary

Kaza

khst

anTu

rkey

Mon

tene

gro

Rom

ania

Slov

enia

Croa

tiaBo

snia

and

Her

z.Po

land

Ukra

ine

Serb

ia

2016 2014

Esto

nia

Slov

ak R

epub

lic

(Percentage of total national employment; manufacturing sector)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Esto

nia

Slov

ak R

epub

lic

Lith

uani

aKa

zakh

stan

Pola

ndGr

eece

Rom

ania

Latv

iaNo

rth M

aced

onia

Bosn

ia a

nd H

erz.

Mol

dova

Bulg

aria

Mon

tene

gro

Hung

ary

Ukra

ine

Croa

tiaSl

oven

iaSe

rbia

2016 2014

(Percentage of GDP; manufacturing sector)

0

1

2

3

4

5

6

7

8

9

Serb

iaLa

tvia

Esto

nia

Ukra

ine

Mon

tene

gro

Pola

ndLi

thua

nia

Slov

enia

Bosn

ia a

nd H

erz.

Gree

ceTu

rkey

Slov

ak R

epub

licM

oldo

vaHu

ngar

yNo

rth M

aced

onia

Kaza

khst

anCr

oatia

Rom

ania

Bulg

aria

(2016; manufacturing sector)

0 100 200 300 400 500 600 700

LatviaEstonia

MontenegroLithuania

Slovak RepublicMoldova

KazakhstanGreeceTurkey

North MacedoniaBosnia and Herz.

SloveniaHungaryCroatia

BulgariaRomania

PolandSerbia

Ukraine

*With data on assets

(Percentage of GDP; manufacturing sector)

0

1

2

3

4

5

6

7

8

Esto

nia

Slov

ak R

epub

licLa

tvia

Lith

uani

aRo

man

iaGr

eece

North

Mac

edon

iaTu

rkey

Kaza

khst

anBu

lgar

iaM

oldo

vaSl

oven

iaBo

snia

and

Her

z.Hu

ngar

yM

onte

negr

oCr

oatia

Pola

ndUk

rain

eSe

rbia

2016 2014

Source (Charts 34-39): Authors’ calculations based on the Orbis database.10

Chart 34. Number of SOEs*

Chart 35. SOE employment

Chart 36. Return on assets

Chart 37. Assets

Chart 38. Liquidity ratio

Chart 39. Total debt

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 25

This study could be deepened and expanded in several ways. First, the sample could be enlarged to include missing SOEs and other economies in which the EBRD invests for which Orbis data are available. Second, more in-depth studies could be conducted, focusing on specific countries or sectors and providing more detail on areas that EBRD interventions could target. Third, SOE performance could be compared with that of national private-sector peers or SOEs in certain developed economies. Lastly, a cross-country analysis of the performance of state-owned financial institutions could be performed.

Potential future work

26 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

Conclusions

Almost three decades on from the start of transition, the non-financial state-owned sector remains substantial. Even though the economies in which the EBRD invests have recorded a significant increase in the private sector’s share of the economy over the past two decades, SOEs are still prevalent and many will continue to play an important role in future. While decisions on whether a public company is fulfilling its goal(s) and whether it should be privatised are political, the operational efficiency of SOEs should remain an economic issue. That is particularly important if public finances are strained or unsustainable.

There is room to improve SOE performance in many of the economies where the EBRD invests. This paper shows considerable differences in the economic variables associated with SOEs in economies from central Europe to Central Asia and SEMED. This suggests that there is significant opportunity in many economies to improve the operational efficiency of SOEs and enhance corporate governance. Ultimately, this would bolster public finances and benefit all citizens and businesses.

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 27

International Labour Organization (n.d.)Employment statistics: https://ilostat.ilo.org/topics/employment/ (last accessed 10 December 2019).

International Monetary Fund (2018)World Economic Outlook, April 2018, Washington, DC (available at: https://www.imf.org/en/Publications/WEO/Issues/2018/03/20/world-economic-outlook-april-2018).

World Bank (2015)Financial Sector Assessment Program: Bosnia and Herzegovina. Capital Markets Technical Note 98305, June 2015, Washington, DC (available at: http://documents.worldbank.org/curated/en/283201468186564489/pdf/98305-WP-P150589-Box393168B.pdf).

References

28 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

Annex 1.

Definition of indicators

Collection period (debtors / operating revenue) * 360

Credit period (creditors / operating revenue) * 360

Debt to equity (gearing) (non-current liabilities + loans) / shareholders’ funds * 100

Financial debt long-term debt + loans

Financial debt to EBITDA financial debt / EBITDA

Implied interest rate (financial expense / financial debt) * 100

Liquidity ratio (current assets - stocks) / current liabilities

Long-term liabilities non-current liabilities / (current + non-current liabilities) * 100

ROA (profit before tax / total assets) * 100

ROE (profit before tax / shareholders’ funds) * 100

Shareholders’ funds(total equity) capital + other shareholders’ funds

Total debt non-current liabilities + loans

Value added profit/loss for period + cost of employees

Source: Orbis database and authors.

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 29

Annex 2.

Translation of NACE Rev. 2* to sectors referred to in this paper

Agriculture A - Agriculture, forestry and fishing

Energy B - Mining and quarrying

Manufacturing C - Manufacturing

UtilitiesD - Electricity, gas, steam and air-conditioning supply

E - Water supply; sewerage, waste management and remediation activities

Construction F - Construction

Trade G - Wholesale and retail trade; repair of motor vehicles and motorcycles

Transport H - Transportation and storage

Tourism I - Accommodation and food services

Other services

J - Information and communication

L - Real estate activities

M - Professional, scientific and technical activities

N - Administrative and support services

O - Public administration and defence; compulsory social security

P - Education

Q - Human health and social work

*Statistical classification of economic activities in the European Union

Source: Authors.

30 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

Acronyms

BvD Bureau van Dijk, a Moody’s Analytics company

EBITDA Earnings before interest, tax, depreciation and amortisation

EBRD European Bank for Reconstruction and Development

GDP Gross domestic product

ILO International Labour Organization

IMF International Monetary Fund

ROA Return on assets

ROE Return on equity

SEMED Southern and eastern Mediterranean

SOE State-owned enterprise

NACE Statistical classification of economic activities in the European Union

US United States

Economic performance of state-owned enterprises in emerging economies: A cross-country study February 2020 31

Notes

32 February 2020 Economic performance of state-owned enterprises in emerging economies: A cross-country study

© European Bank for Reconstruction and Development

All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means, including photocopying and recording, without the written permission of the copyright holder. Such written permission must also be obtained before any part of this publication is stored in a retrieval system of any nature.

Terms and names used in this report to refer to geographical or other territories, political and economic groupings and units, do not constitute and should not be construed as constituting an express or implied position, endorsement, acceptance or expression of opinion by the European Bank for Reconstruction and Development or its members concerning the status of any country, territory, grouping and unit, or delimitation of its borders, or sovereignty.

1228 Economic performance of state-owned enterprises in emerging economies: A cross-country study

European Bank for Reconstruction and DevelopmentOne Exchange SquareLondon EC2A 2JNUnited Kingdomwww.ebrd.com