economics - nomuradirect.com 2q20_1586343300.pdf · capital nomura securities public company...

TRANSCRIPT

Connecting Markets East & West

© Nomura

A race against time

Capital Nomura Securities Public Company Limited

Investment Research and Investor Services

Economics

2 April 2020

Nuchjarin Panarode (+66 2638 5776)

Capital Nomura Securities Public Company Limited Economics - 1

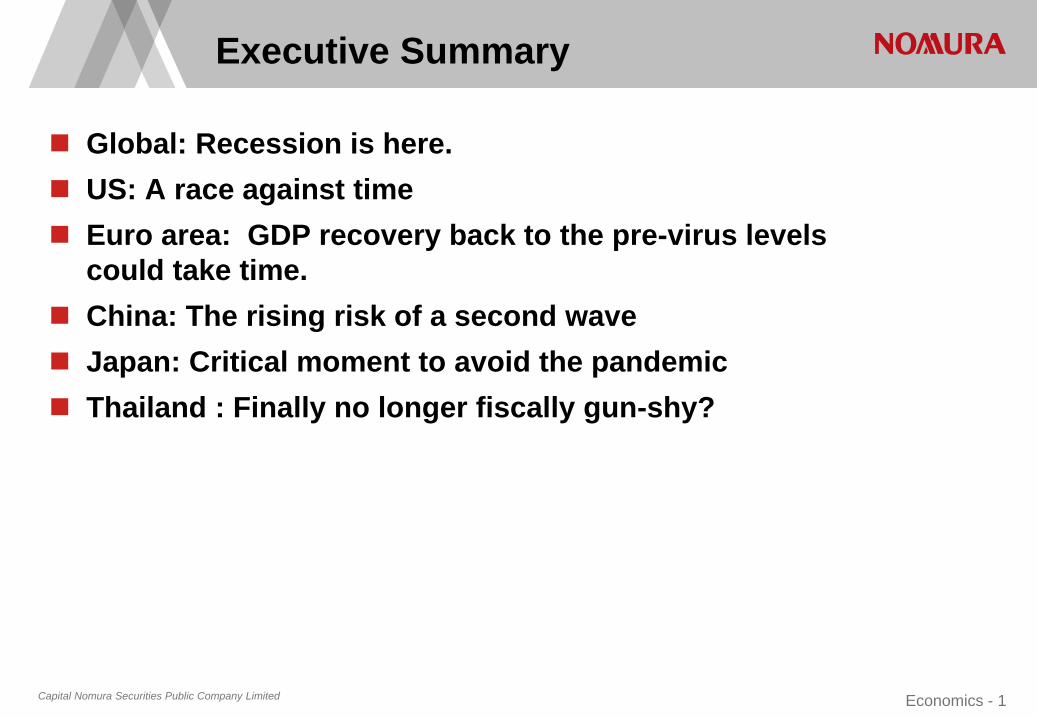

Executive Summary

Global: Recession is here.

US: A race against time

Euro area: GDP recovery back to the pre-virus levels

could take time.

China: The rising risk of a second wave

Japan: Critical moment to avoid the pandemic

Thailand : Finally no longer fiscally gun-shy?

Capital Nomura Securities Public Company Limited Economics - 2

Nomura’s Base case: GDP => Global -4.0%; Thailand -6.3%

Source : Nomura , “Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

การเวนระยะหางทางสงคม (social distancing) ในแหลงทมการระบาดของ COVID-19 จนถงปลายเดอน เม.ย กอนจะเรมผอนปรน

ภาคธรกจและการบรโภคใน Europe และ US จะคอยๆ กลบมาใน Q3

มการใชนโยบายการเงนและการคลงทท าใหรอดพนจากสภาวะสนเชอทตงตวอยางมาก แตตลาดการเงนยงตง มการผดนดช าระหน และ การวางงานเพมขนอยางเหนไดชด

ยงไมมวคซนปองกนโรคระบาดจาก COVID-19 กอน Q4 ท าใหมการระบาดรอบสองใน Q4 ซงเปนฤดหนาวในประเทศใหญๆ แตเปนระบาดทเบาบาง

Capital Nomura Securities Public Company Limited Economics - 3

Source : Nomura , “Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

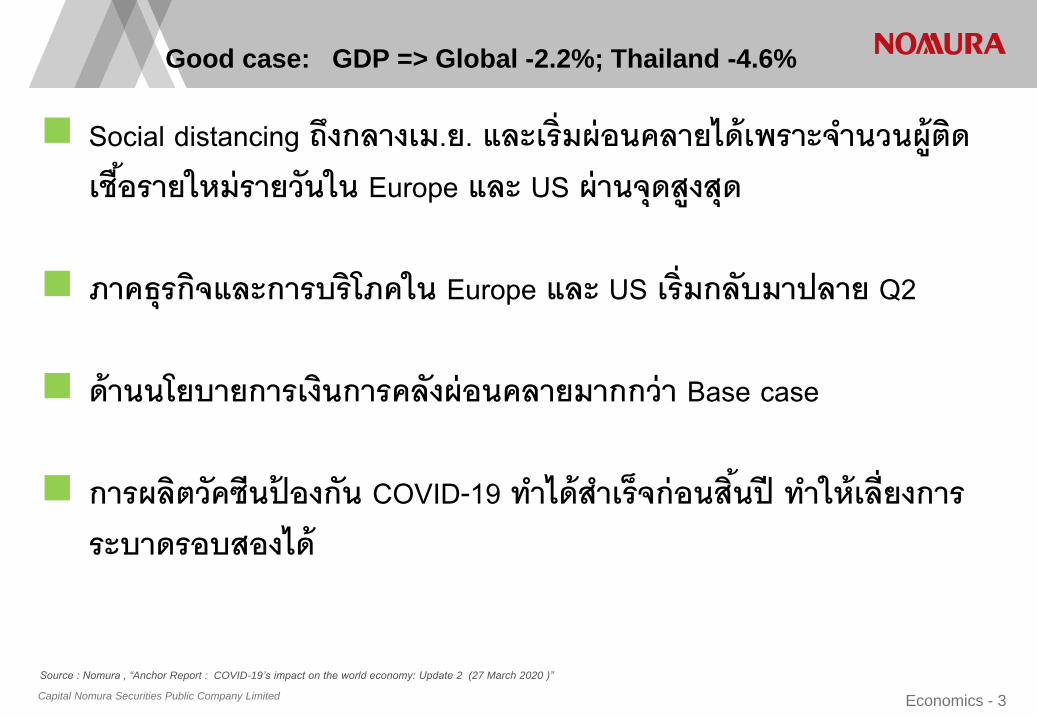

Social distancing ถงกลางเม.ย. และเรมผอนคลายไดเพราะจ านวนผตดเชอรายใหมรายวนใน Europe และ US ผานจดสงสด

ภาคธรกจและการบรโภคใน Europe และ US เรมกลบมาปลาย Q2

ดานนโยบายการเงนการคลงผอนคลายมากกวา Base case

การผลตวคซนปองกน COVID-19 ท าไดส าเรจกอนสนป ท าใหเลยงการระบาดรอบสองได

Good case: GDP => Global -2.2%; Thailand -4.6%

Capital Nomura Securities Public Company Limited Economics - 4

Source : Nomura , “Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

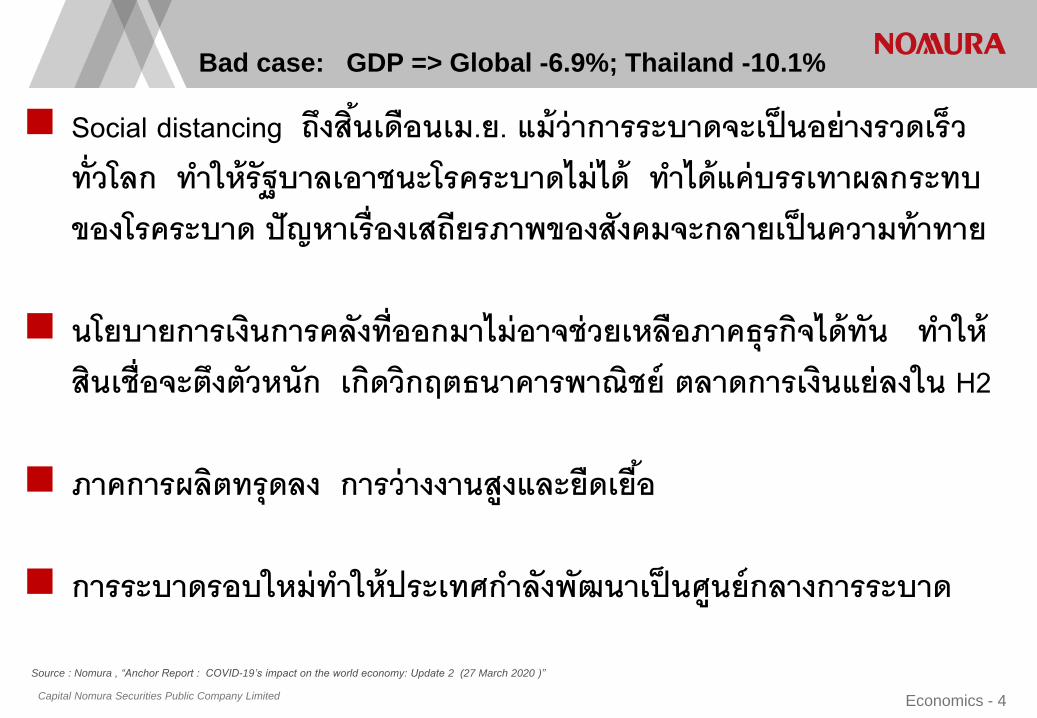

Social distancing ถงสนเดอนเม.ย. แมวาการระบาดจะเปนอยางรวดเรวทวโลก ท าใหรฐบาลเอาชนะโรคระบาดไมได ท าไดแคบรรเทาผลกระทบของโรคระบาด ปญหาเรองเสถยรภาพของสงคมจะกลายเปนความทาทาย

นโยบายการเงนการคลงทออกมาไมอาจชวยเหลอภาคธรกจไดทน ท าใหสนเชอจะตงตวหนก เกดวกฤตธนาคารพาณชย ตลาดการเงนแยลงใน H2

ภาคการผลตทรดลง การวางงานสงและยดเยอ

การระบาดรอบใหมท าใหประเทศก าลงพฒนาเปนศนยกลางการระบาด

Bad case: GDP => Global -6.9%; Thailand -10.1%

Capital Nomura Securities Public Company Limited Economics - 5

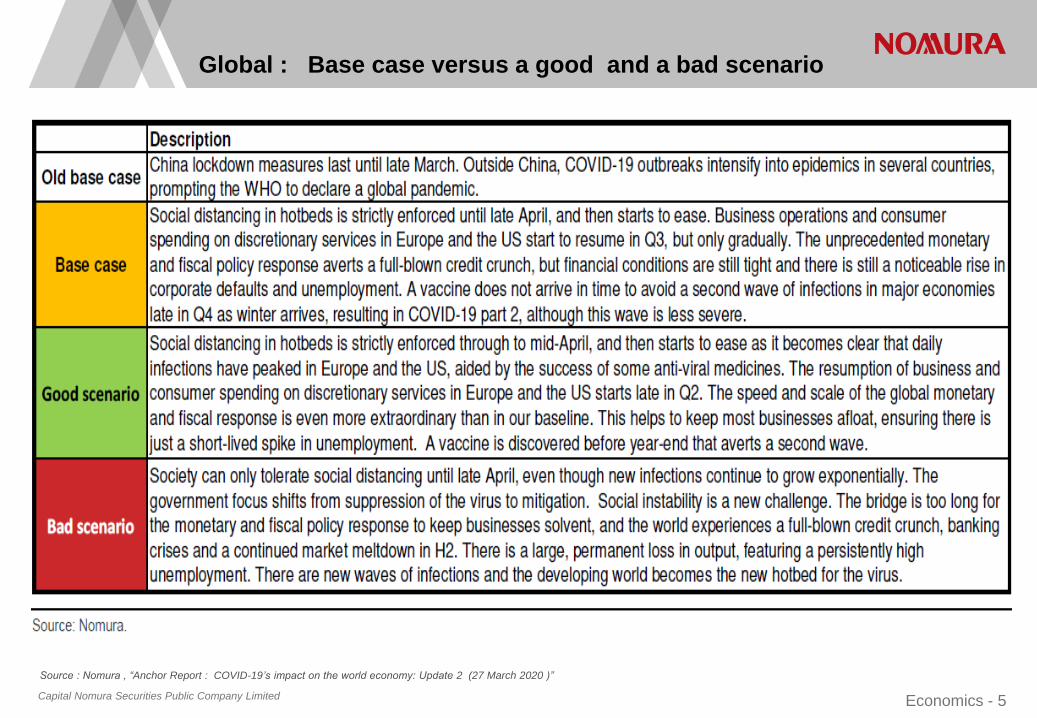

Global : Base case versus a good and a bad scenario

Source : Nomura , “Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 6

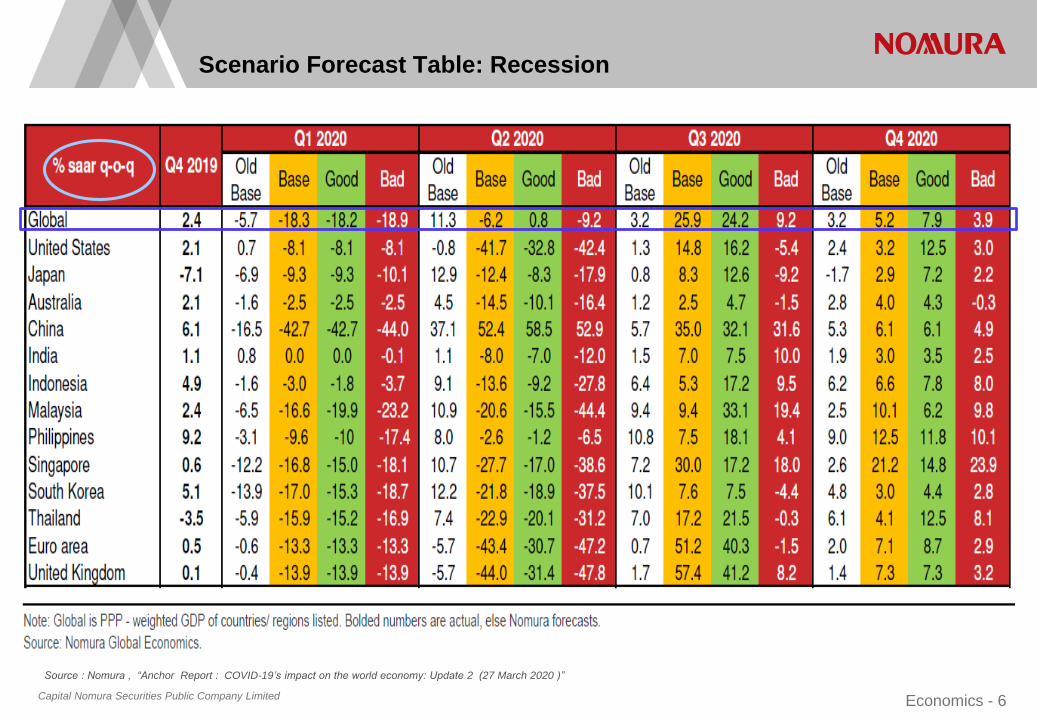

Scenario Forecast Table: Recession

Source : Nomura , “Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 7

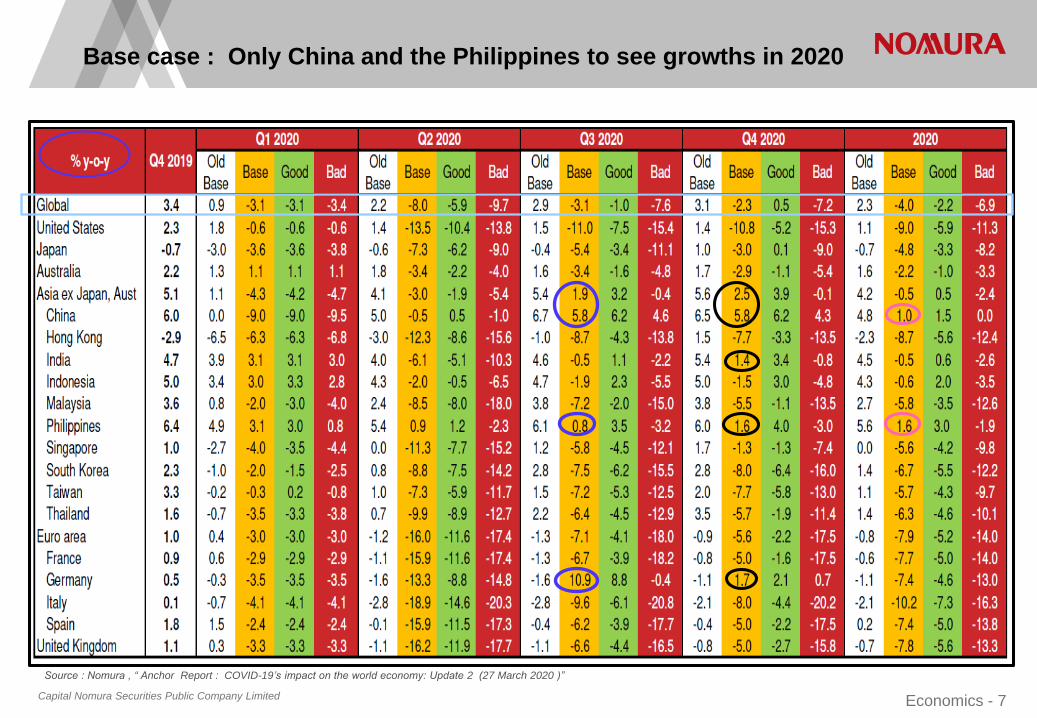

Base case : Only China and the Philippines to see growths in 2020

Source : Nomura , “ Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 8

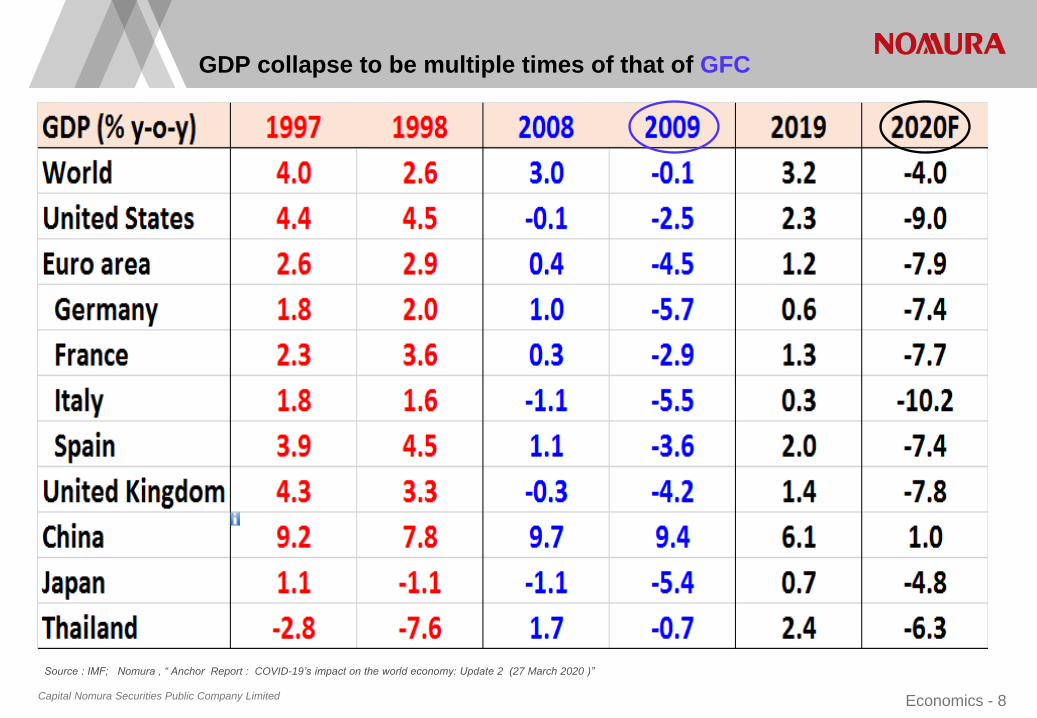

GDP collapse to be multiple times of that of GFC

Source : IMF; Nomura , “ Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 9

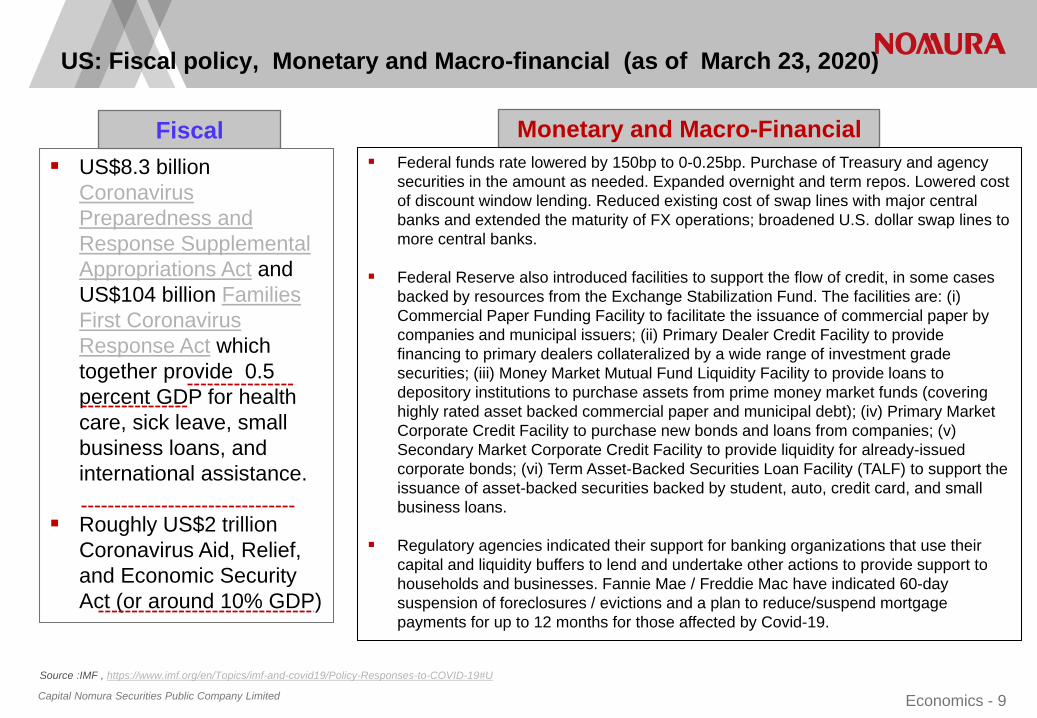

US: Fiscal policy, Monetary and Macro-financial (as of March 23, 2020)

▪ US$8.3 billion

Coronavirus

Preparedness and

Response Supplemental

Appropriations Act and

US$104 billion Families

First Coronavirus

Response Act which

together provide 0.5

percent GDP for health

care, sick leave, small

business loans, and

international assistance.

▪ Roughly US$2 trillion

Coronavirus Aid, Relief,

and Economic Security

Act (or around 10% GDP)

Fiscal Monetary and Macro-Financial

Source :IMF , https://www.imf.org/en/Topics/imf-and-covid19/Policy-Responses-to-COVID-19#U

▪ Federal funds rate lowered by 150bp to 0-0.25bp. Purchase of Treasury and agency

securities in the amount as needed. Expanded overnight and term repos. Lowered cost

of discount window lending. Reduced existing cost of swap lines with major central

banks and extended the maturity of FX operations; broadened U.S. dollar swap lines to

more central banks.

▪ Federal Reserve also introduced facilities to support the flow of credit, in some cases

backed by resources from the Exchange Stabilization Fund. The facilities are: (i)

Commercial Paper Funding Facility to facilitate the issuance of commercial paper by

companies and municipal issuers; (ii) Primary Dealer Credit Facility to provide

financing to primary dealers collateralized by a wide range of investment grade

securities; (iii) Money Market Mutual Fund Liquidity Facility to provide loans to

depository institutions to purchase assets from prime money market funds (covering

highly rated asset backed commercial paper and municipal debt); (iv) Primary Market

Corporate Credit Facility to purchase new bonds and loans from companies; (v)

Secondary Market Corporate Credit Facility to provide liquidity for already-issued

corporate bonds; (vi) Term Asset-Backed Securities Loan Facility (TALF) to support the

issuance of asset-backed securities backed by student, auto, credit card, and small

business loans.

▪ Regulatory agencies indicated their support for banking organizations that use their

capital and liquidity buffers to lend and undertake other actions to provide support to

households and businesses. Fannie Mae / Freddie Mac have indicated 60-day

suspension of foreclosures / evictions and a plan to reduce/suspend mortgage

payments for up to 12 months for those affected by Covid-19.

Capital Nomura Securities Public Company Limited Economics - 10

US: A race against time

Source : Nomura , “ Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 11

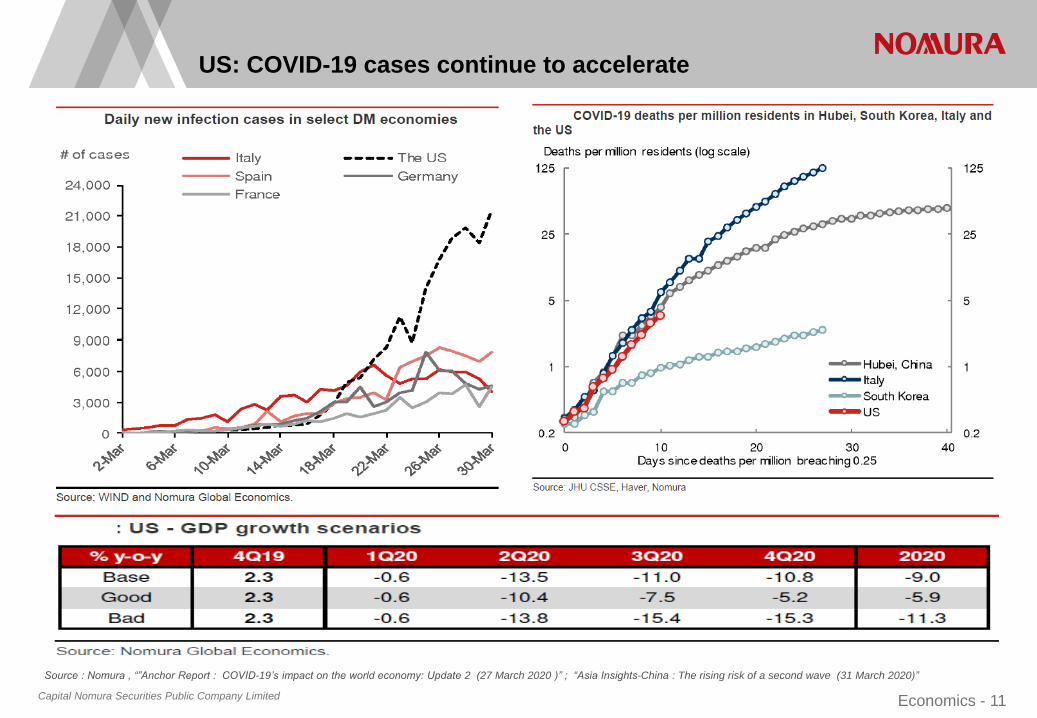

US: COVID-19 cases continue to accelerate

Source : Nomura , “”Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )” ; “Asia Insights-China : The rising risk of a second wave (31 March 2020)”

Capital Nomura Securities Public Company Limited Economics - 12

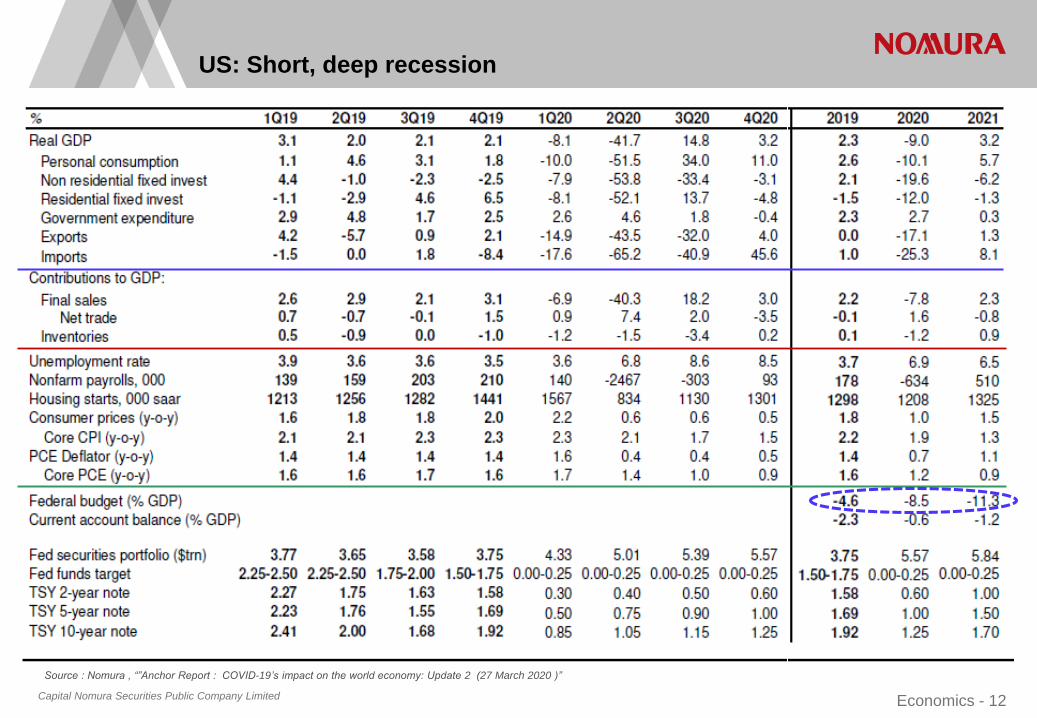

US: Short, deep recession

Source : Nomura , “”Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 13

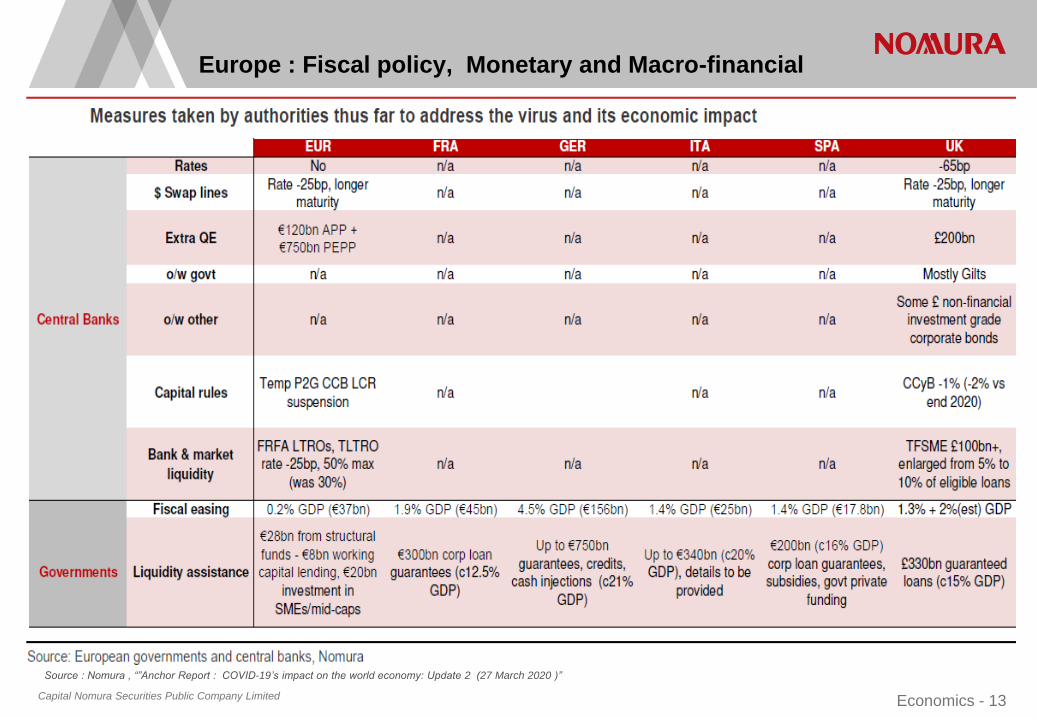

Europe : Fiscal policy, Monetary and Macro-financial

Source : Nomura , “”Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 14

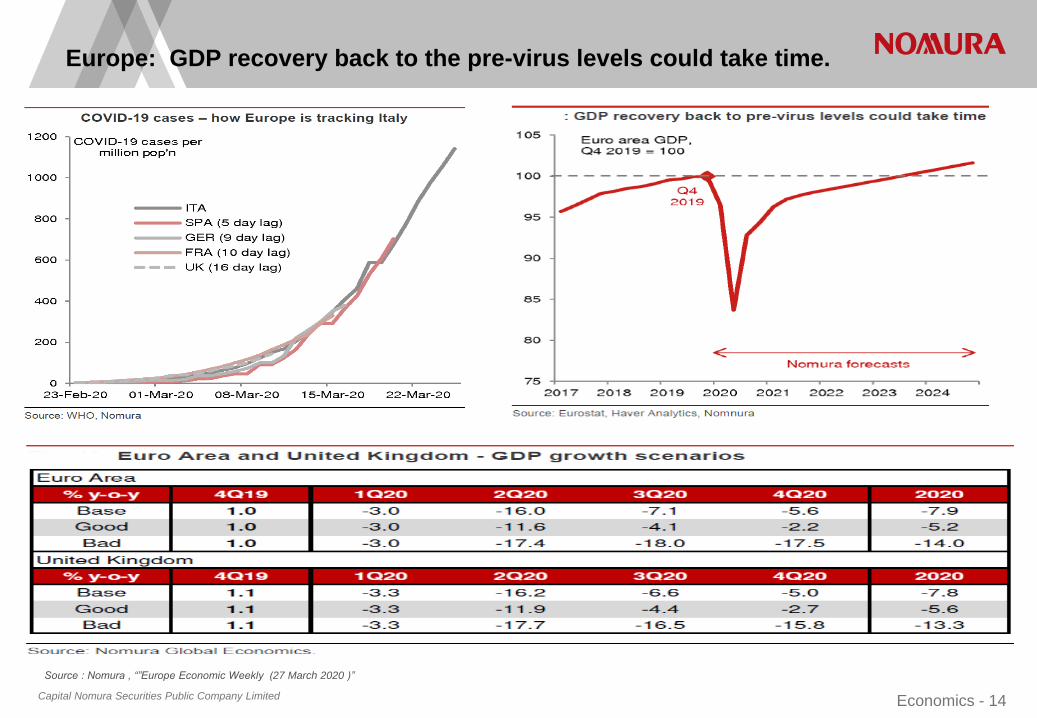

Europe: GDP recovery back to the pre-virus levels could take time.

Source : Nomura , “”Europe Economic Weekly (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 15

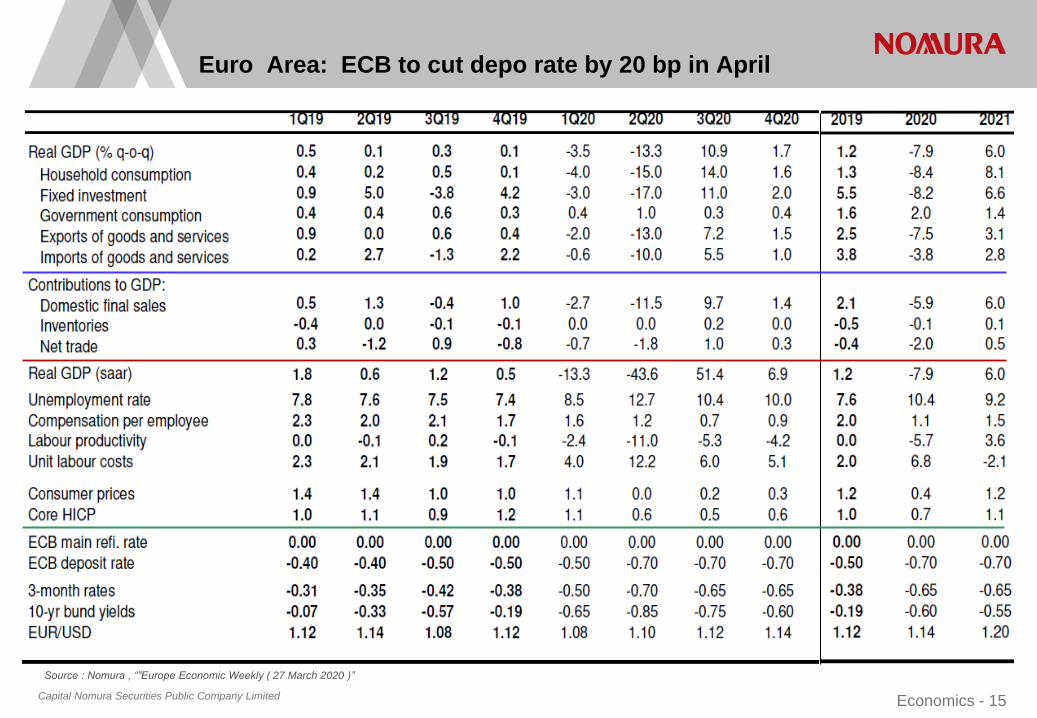

Euro Area: ECB to cut depo rate by 20 bp in April

Source : Nomura , “”Europe Economic Weekly ( 27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 16

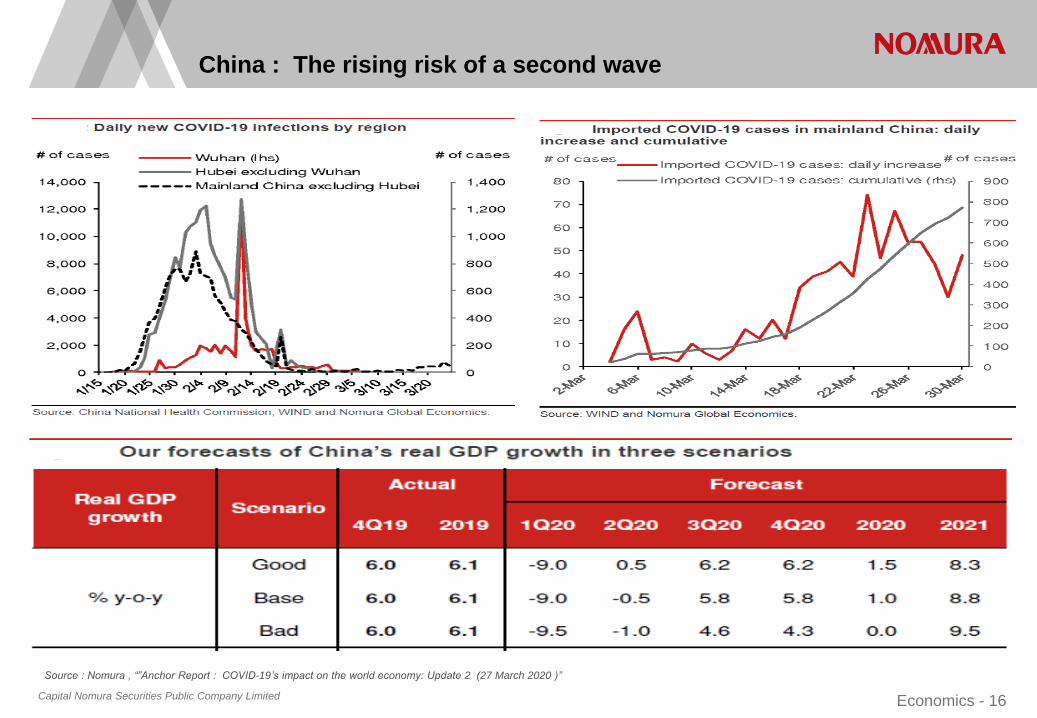

China : The rising risk of a second wave

Source : Nomura , “”Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 17

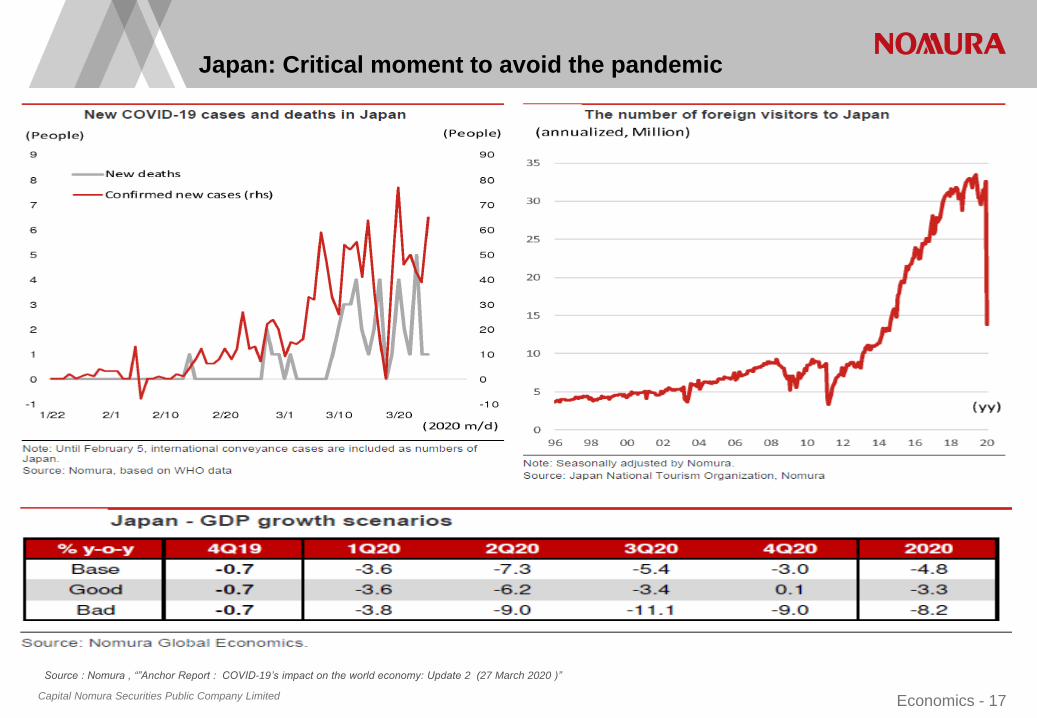

Japan: Critical moment to avoid the pandemic

Source : Nomura , “”Anchor Report : COVID-19’s impact on the world economy: Update 2 (27 March 2020 )”

Capital Nomura Securities Public Company Limited Economics - 18

Thailand : GDP performance in the bad times

Source : NESDC; CNS (IRIS)

% y-o-y

Capital Nomura Securities Public Company Limited Economics - 19

Thailand : GDP performance in the bad times

Source : NESDC; CNS (IRIS)

% y-o-y

Capital Nomura Securities Public Company Limited Economics - 20

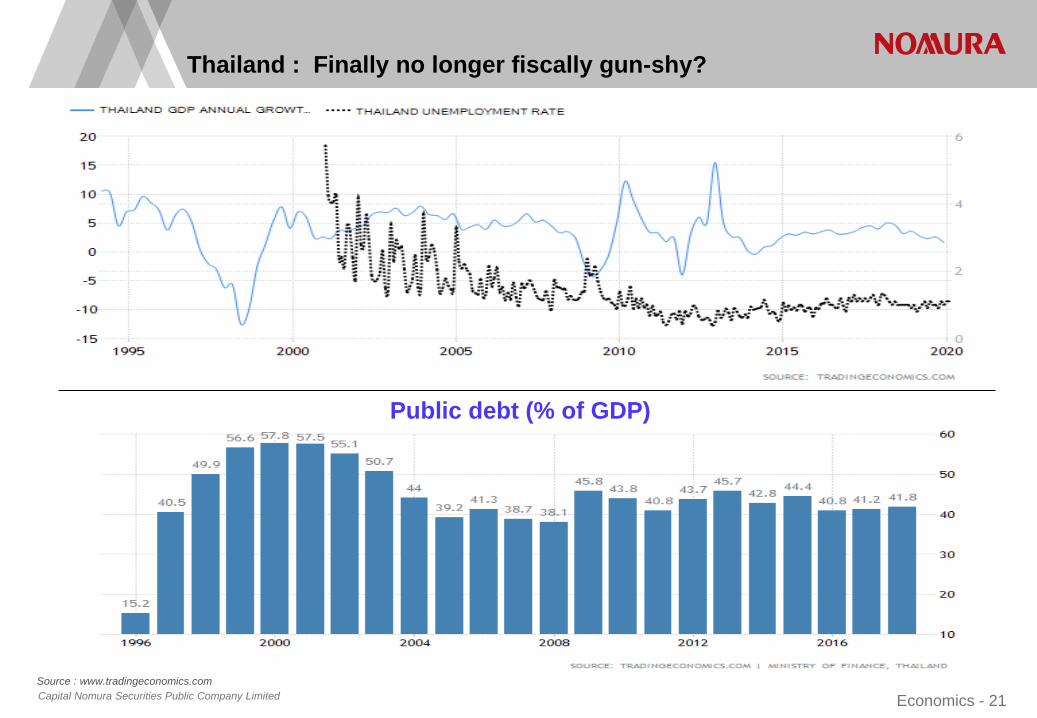

Thailand : Finally no longer fiscally gun-shy?

คาด GDP -6.3% ในป 2020 โดยมภาวะถดถอยทางเทคนค (technical recession) ใน H1 2020 เพราะ

คาดวา GDP จะหดตวในอตรา -15.9% q-o-q saar ใน Q1 และ -22.9% ใน Q2 ตามดวยการฟนตวชาๆ

ใน H2 เพราะคาด GDP + 17.2% ใน Q3 และ +4.1% ใน Q4 เมอเทยบปตอป คาด GDP ลดลง y-o-y ทก

ไตรมาส

คาดวา ธนาคารแหงประเทศไทยจะลดดอกเบยอก 25 bp ในการประชม 20 พ.ค. หรอกอนก าหนด

รฐบาลไดออกมาตรการกระตนทงการคลงและดานสนเชอ 2 รอบวงเงนรวม THB535bn (3.2% ของ GDP)

แตนาจะมการออกมาตรการกระตนเพมอก สงผลใหการขาดดลงบประมาณนาจะขยบขนเปน 3.1% ของ

GDP จากเดมทรฐบาลวางแผนจะขาดดล 2.6% ของ GDP

ตองจบตาดการขาดดลงบประมาณ/ การกเงนเพมเตม

Source : Nomura ,” Anchor Report: How the Coronavirus COVID-19 will impact the world economy (17 February 2020):

Capital Nomura Securities Public Company Limited Economics - 21

Thailand : Finally no longer fiscally gun-shy?

Source : www.tradingeconomics.com

Public debt (% of GDP)

Capital Nomura Securities Public Company Limited Economics - 22

ANALYST CERTIFICATION FOR REGULATION

I, Nuchjarin Panarode , a research analyst employed by Capital Nomura Securities, hereby certify that all of the views expressed in this research report accurately reflect my personal views about any and

all of the subject securities or issuers discussed herein.

In addition, I hereby certify that no part of my compensation was, is, or will be, directly or indirectly related to the specific recommendations or views that I have expressed in this research report, nor is it

tied to any specific investment banking transactions performed by Nomura Securities International, Inc., Nomura International plc or by any other Nomura Group company or affiliate thereof.

Explanation of CNS rating system for Thailand companies under coverage published from 2 March 2009:

Stocks:

Stock recommendations are based on absolute valuation upside (downside), which is defined as (Fair Value - Current Price) / Current Price, subject to limited management discretion. In most cases, the

Fair Value will equal the analyst’s assessment of the current intrinsic fair value of the stock using an appropriate valuation methodology such as Discounted Cash Flow or Multiple analysis etc. However, if

the analyst doesn’t think the market will revalue the stock over the specified time horizon due to a lack of events or catalysts, then the fair value may differ from the intrinsic fair value. In most cases,

therefore, our recommendation is an assessment of the difference between current market price and our estimate of current intrinsic fair value. Recommendations are set with a 6-12 month horizon unless

specified otherwise. Accordingly, within this horizon, price volatility may cause the actual upside or downside based on the prevailing market price to differ from the upside or downside implied by the

recommendation.

• A "Buy” recommendation indicates that potential upside is 15% or more.

• A "Neutral" recommendation indicates that potential upside is less than 15% or downside is less than 5%.

• A "Reduce" recommendation indicates that potential downside is 5% or more.

Sectors:

A "Bullish" rating means most stocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a positive absolute recommendation.

A "Neutral" rating means most stocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a neutral absolute recommendation.

A "Bearish" rating means most stocks in the sector have (or the weighted average recommendation of the stocks under coverage is) a negative absolute recommendation.

DISCLAIMERS:

This publication contains material that has been prepared by Capital Nomura Securities Public Co., Ltd., Bangkok, Thailand. This material is (i) for your private information, and we are not soliciting any

action based upon it; (ii) not to be construed as an offer to sell or a solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal; and (iii) is based upon

information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. Opinions expressed are current opinions as of the date appearing on

this material only and the information, including the opinions contained herein are subject to change without notice. We, or other affiliates and/or subsidiaries of Nomura Holdings, Inc. (collectively referred

to as the “Nomura Group”) may from time to time perform investment banking or other services (including acting as advisor, manager or lender) for, or solicit investment banking or other business from,

companies mentioned herein. We, the Nomura Group, our or any of their officers, directors and employees, including persons involved in the preparation or issuance of this material may, from time to time,

have long or short positions in, and buy or sell (or make a market in), the securities, or derivatives (including options) thereof, of companies mentioned herein. We, or a member of the Nomura Group, our

or any of their officers, directors and employees may, to the extent it is permitted by applicable law, have acted upon or used this material, prior to or immediately following its publication. The securities

described herein may not have been registered under the U.S. Securities Act of 1933, and, in such case, may not be offered or sold in the United States or to U.S. persons unless they have been

registered under such Act, or except in compliance with an exemption from the registration requirements of such Act. Unless governing law permits otherwise, you must contact a Nomura Group entity in

your home jurisdiction if you want to use our services in effecting a transaction in the securities mentioned in this material. This publication is intended for investors who are not private or expert investors

within the meaning of the Rules of the Securities and Futures Authority Limited, and should not, therefore, be redistributed to private or expert investors. No part of this material may be (i) copied,

photocopied, or duplicated in any form, by any means, or (ii) redistributed without CNS’ prior written consent. Further information on any of the securities mentioned herein may be obtained upon request. If

this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost,

destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of this publication, which may arise as a result of electronic

transmission. If verification is required, please request a hard-copy version.