economics, banking and finance in emerging markets

TRANSCRIPT

Economics, Banking and Finance in

Emerging MarketsA collection of my essays focusing

on unique challenges in emerging economies

By Dr Ola Brown, MBBS

Economics, Banking and Finance in Emerging Markets:

A collection of my essays focusing on unique challenges in emerging economies

by Dr Ola Brown, MBBS

Copyright @ 2020 Dr Ola Brown. All Rights Reserved

Cover and Section Illustrations by Caroline Chapple

Layout, Graph & Graphic Design by Iske Conradie

Proofreading by Sarina Cornthwaite

3

DEDICATION I dedicate this book to my youngest sister Busola Orekunrin, who died because of what I thought was a broken, under-funded healthcare system.

Now, I realise that the root cause of her death was a complex interplay of fiscal, structural and other economic factors that continues to contribute to underinvestment in African healthcare systems.

Continue to rest in peace, my Angel forever.

I also dedicate this to my husband, David Brown. My best friend; my inspiration: I love you.

4

FOREWORD

In recent times, literature in economics has been dominated by academics and policymakers. They typically have a somewhat peculiar way of thinking that can sometimes seem a bit abstract to casual readers, including entrepreneurs. It is what makes books by entrepreneurs all the more interesting, and not just to casual readers, but to economists as well. Ola’s book fits the bill as she explains basic concepts and ideas from the perspective of an entrepreneur trying to get things done in a developing country context.

She straddles various topics, from the micro issues affecting firms such as budgeting, savings, and unions, to more “big picture” issues like taxation, monetary policy, and banking; all written in plain English and with easy to follow diagrams that keep things interesting for the casual reader.

Following Ola’s journey, from a mild curiosity about economics to interest enough to start a Masters in Economics & Finance and write a book, has been a joy to behold. This collection of essays is essential reading for those who just want a casual understanding of some key topics in economics, and also worth it for economists who seek a different perspective.

Nonso Obikili, Ph.D

Development Coordination Officer, EconomistUnited Nations

5

ABOUT THE AUTHOR

Dr Ola Brown is the founder of the Flying Doctors Healthcare Investment Group.

The Flying Doctors Healthcare Group invests and operates across the healthcare and wellness value chain in hospital/clinic construction & refurbishment, diagnostics and equipment, health facility management, pharmaceutical retail, drug manufacturing, air ambulance services & logistics, and consulting/healthcare technology.

Academic Background

Dr Ola studied Medicine and Surgery at the Hull York Medical School after which she worked in Acute Medicine in the UK. She was then awarded the Japanese MEXT scholarship which allowed her to further her studies in Tokyo, Japan. The fellowship focused on lab-based research with induced pluripotent stem cells. She is currently completing her Master’s degree in Finance and Economic Policy at the University of London.

Her post-graduate areas of study include Pre-Hospital Emergency care, Healthcare leadership and Healthcare delivery. She has a certificate in Economic Policymaking from IE Business School, Spain, and a certificate in Accounting for Decision Making from the University of Michigan in the United States.

Background in investment and finance

Along with two other directors, Dr Ola runs a leading early stage venture capital firm – Greentree Investment company, which provides growth capital to some of Africa’s most exciting tech start-ups.

Greentree Investment company has invested in start-ups in various sectors including FinTech, media, SaaS, Agri-tech, manufacturing, ecommerce, health tech and Edutech, making it one of West Africa’s leading venture capital firms with a total portfolio value of about $80m.

6

Publications: Books & Articles

She has published four books: EMQ’s in Paediatrics, Pre-Hospital Care for Africa, Fixing Healthcare in Nigeria: a guide to public healthcare policy and Banking, and Finance & Economics in Emerging Markets: an essay collection.

She has also written articles published in the British Medical Journal, the Journal of Emergency Medical Services, the Niger Delta Medical Journal, the New York Times, and the Huffington Post.

Awards, Speaker Engagements and Appointments

She is an international speaker who has spoken at the TED global conference, the European Union, the Swiss Economic Forum, the UN, the World Bank, the World Economic Forum, the World Health Organisation, the Massachusetts Institute of Technology, Cambridge University, and the Aspen Ideas Festival. Dr Ola and her work have also been featured by CNN, the BBC, Forbes and Al-Jazeera.

She has received multiple awards and nominations. These include: The Mouldbreaker’s Award, the THIS Day Award, The Future Award as Entrepreneur of the Year, New Generation Leader for Africa, Ladybrille Personality of the Month, Silverbird Entrepreneurship Award, Nigerian Aviation Personality of the Year award, and Vanguard WOW Awards. She is also a TED fellow (see TEDx talk here), a Dangote Fellow, an Aspen Fellow, and has been honoured by the World Economic Forum as a Young Global Leader.

She is a member of the American College of Emergency Physicians, international editor of the Journal of Emergency Services and a LinkedIn Top Ten Global Healthcare Writer.

International Trade & Investment/Policy Roles

Dr. Ola Brown sits on the board of the Professional Women’s Network (Lagos Chapter). She leads the Health as A Business group at the Nigerian Economics Summit Group (NESG); a think tank. She also facilitates trade between Nigeria, the United Kingdom and the United States through her seats on the committee of the British Business Group (Lagos) and the Nigerian-American Chamber of Commerce (Healthcare Section) respectively.

7

4 57 813 14

20 30 4450

56

64 72 81

86

96 105 110

122 133

Foreword . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .About The Author . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Contents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .How To Read This Book . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Section 1: Microeconomics – Explained . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Chapter 1 (Essay 1 – Microeconomics: traditional vs. behavioural perspectives) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Chapter 2 (Essay 2 – Impact of trade unions on wage structure and work conditions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Section 2: Macroeconomics – Explained . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 3 (Essay 1 – Capital budgeting techniques) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 4 (Essay 2 – Monetary policy: the cost capital channel and the credit channel) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 5 (Essay 3 – Firms’ investment decisions in emerging markets: cost of capital or quantity of finance available?) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 6 (Essay 4 – Assessing fiscal sustainability in emerging economies vs. advanced economies) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Section 3: IMF & Economic Policy - Is The IMF Evil? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 7 (Essay 1 – Mundell-Fleming and Polak Models, IMF’s approach to stabilisation) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 8 (Essay 2 – Nature of crises in emerging markets and how the IMF handled them, the emerging market crisis of 1997 and the global financial crisis) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Section 4: Banking and Capital Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Chapter 9 (Essay 1 – Viability of Nigeria’s bank oriented economy, role of financialisation in emerging markets, corporate governance) . . . . . . . . . . . . . . . . . . . . .Chapter 10 (Essay 2 – Role of deposit insurance/lender of last resort in the stability of financial systems, McKinnon and Pill Model) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

TABLE OF CONTENTS

8

9

INTRODUCTION

For the past seven (7) years since I moved to Nigeria, I have been taking courses in finance, economics, accounting, and banking. After living in countries like the United Kingdom and Japan, I have been fascinated by the myriad of additional considerations that entrepreneurs and policymakers in emerging markets have to think about in comparison to policymakers and entrepreneurs in advanced countries.

My favourite quote from one of my recently published articles is: ‘In advanced countries, there is only one set of forces that can act on your business- the market forces. However, here in Nigeria, there are two sets of forces that can act on your business- the market forces and the evil forces.’

Emerging markets are much more complex and nuanced, which is why business people, entrepreneurs, and policymakers often find them more difficult to work in. I have been studying at the University of London for my Master’s degree in Finance and Economic Policy over the past year, and I’m surprised that even in a city as diverse as London, most of our reading material focuses on developed markets. We read about the US Federal Reserve, the European Central Bank, the Bank of England, and the Bank of Japan, as well as papers and textbooks mostly produced and written by Western scholars.

If it’s true that business and policy management in emerging markets is more nuanced and complex, then why is so much of economics based around just a few rich countries?

Most of what we see in books and the majority of journals and we read about economics are focused on advanced markets. However, most people in the world do not live in developed countries. It is called the G7 group for a reason- there are only seven countries considered to be extremely wealthy on a global basis, out of 195.

Working one’s way out of poverty is serious business. Still, it becomes even more complicated when we do not have enough academic focus on the strategies, policies, data and research that are needed to do this successfully.

10

I have read so much about the Bank of England, the Federal Reserve, the European Central Bank, and even the Bank of Japan. I also want to read just as much about the Central Bank of Nigeria (CBN) in academic literature.

Thus, the purpose of this book is directed towards the dire need to focus on emerging markets. This is because there is very little information on emerging markets, despite their complexities.

From now until the completion of my Master’s degree, I have decided to focus my essays on emerging markets. Either I dwell solely on emerging markets, or I try to contextualise the topics within emerging markets. I hope that this book and similar books written by Nigerians, Kenyans, Bangladeshis and Indians will begin to refocus the world on the complexity of entrepreneurship and policy-making in emerging markets.

I spent a part of my childhood in London in a place called Hackney. At that time, Hackney wasn’t a nice place to live as it wasn’t one of the high-end areas. The bus 38 used to stop outside my house. This bus could take you from Hackney to Piccadilly Circus, one of the nicest parts of London. When I was young, I would get on that bus and ride to Piccadilly Circus. Whenever I was there, I’d begin to wonder why I couldn’t be one of those who lived in that kind of place. I found it difficult to understand why the people in my environment weren’t as affluent as the people just a bus ride away from us. As I moved, I grew up taking my A-levels at a poorly performing public college and thought about it more. How could I compete with the wealthier kids that went to private school when my reality was so different from theirs? When sharing my ideas- I called it the ’38 project’- I tried to get people thinking about questions like: “How do we make our lives better?” “How do we get out of Hackney into Piccadilly Circus?”

This is exactly what emerging markets like Nigeria, Kenya, Congo, and Ethiopia are currently facing. We are trying to play the same game as wealthier countries, but with fewer resources. We want the kind of progress that will get us out of the metaphorical Hackney into our own Piccadilly Circus. We want to have the kind of GDP that can support sustainable growth in our economies. We want to evolve. We want to have our own Google, Facebook, Uber, and Apple. We want to have our own unique forms of innovation.

This book seeks to refocus the world on emerging markets, which are home not only to many of the poorest people, but also to the largest number of people.

11

In the global economy, only half a billion people earn above twenty thousand dollars ($20,000) a year. Two billion people earn between three and twenty thousand dollars ($3,000-$20,000) each year. However, the majority- four billion people- earn three thousand dollars ($3,000) or less per year. Most of these four billion people live in emerging markets.

In spite of these statistics, instead of focusing on the needs, wants and desires of the four billion people that make up most of the world’s population, the whole of economics seems to be focused on 0.5 billion people.

Therefore, the aim of this book, Economics, Banking & Finance in Emerging Markets, is to try to push the needs and desires of those four billion people forward and get us all thinking about how we can improve their lives as well.

Economics is so important because it has an impact on everything. A clear understanding of economics affects the way we vote, the way we spend, the type of business we start, and the kind of things we value. It also affects the way we substitute products for others.

I believe that a little bit of understanding of economics in emerging markets can make a big difference to the world’s poorest and most vulnerable people.

(Source: University of Michigan)

12

This is particularly important to me because I live in Nigeria, which has more poor people than anywhere else in the world. Nigeria is home to over 80 million impoverished people.

Many people think India is a poor country. However, the truth is only 5.5% of India’s population is classified as extremely poor, compared to over 40% of Nigeria’s population.

Entrepreneurs in emerging markets face a number of challenges that would not be faced if they were in developed countries. These challenges are at least, in part, policy driven.

In ‘Africa Rise and Shine’, a book by one of the most successful bankers in Africa, Jim Ovia, he spoke about the condition of the road to his bank being one of the biggest challenges for him, as customers found it difficult to drive on the road without damaging their cars. So he ended up building a road! In advanced countries, it is almost impossible to hear that owners of American or German banks had to engage in road construction or their businesses, as these things have already existed.

Similarly, if you take a brief look at Aliko Dangote - the richest man in Africa - you will discover that he also encountered a similar problem with infrastructure. He has built and is continuing to build roads and helping to develop ports so that he can get cement materials to and from his factories.

The aim of this book, as reiterated earlier, is to refocus the world’s view of economics. It also seeks to ensure that the intricacies and idiosyncrasies of economic, financial, and business policy in emerging markets are projected. In addition, this book attempts to encourage people to think about innovative, policy-based, business-based, and investment-based solutions that can help lift this important, but often ignored demographic of four billion poor people out of poverty and a bit closer to prosperity.

13

HOW TO READ THIS BOOK

This book is divided into four sections- Macroeconomics, Microeconomics, Banking & Capital markets, and the International Monetary Fund (IMF).

Although it is a collection of academic essays, each chapter has an explainer. These explainers are written from a layperson’s perspective.

Some of you reading this book might choose to read the explainers and look at the pretty pictures without going onto the essays... and that’s perfectly fine.

You can pick up the book and say, “You know what? I’m simply going to look at the table of contents, go through the explainers and look at the pretty pictures”.

By doing so, not only have you improved your knowledge of economics and finance, you have also improved your ability to understand the context in which you live, as well as your knowledge of how money, business and investments work in emerging markets- and that could be enough for you.

However, if you feel the need to go further, please note that there are two essays in each chapter. They are my academic work and some of them dig into certain aspects of economics as well as banking and finance. I only focused on a minute area of each, so if you feel the need to dig a little deeper into our world, you are more than welcome to do that. You may want to start with my economic video tutorials on YouTube ; - )

14

SECTION 1

MICROECONOMICS- EXPLAINED

Microeconomics is the branch of economics that studies the economy of consumers, households and individual firms. Basically, Microeconomics looks at the day-to-day decisions of individuals and firms.

To start with, I want to give an illustration centred around Hushpuppi. For those who don’t know the story, Hushpuppi (real name: Ramon Olorunwa Abbas) is a flamboyant social media celebrity who was recently arrested by the FBI after investigations revealed that he was a high-profile internet fraudster.

Before his arrest, Hushpuppi was a spendthrift. If you take a look at his Instagram page, you will see how he spent his money extravagantly. He kept chartering private jets, and buying super-expensive cars like Bentley, Rolls Royce and many others. His clothes and shoes were from world-renowned brands like Louis Vuitton and Gucci. Despite the endless speculations that he financed his opulent lifestyle through fraudulent proceeds, he still audaciously posted all his luxurious spending on the internet. He continued to spend flamboyantly until the day of his arrest.

That is an extreme example of microeconomic decisions- decisions made by an individual that seem bizarre and strange, but still happen.

That’s exactly what microeconomics is all about. It studies why we act the way we act, why we think the way we think, and why we spend the way we spend. It also examines the impact of day-to-day decisions made by households and firms.

One of the most interesting things about microeconomics is the relationship between saving and spending. Microeconomics is concerned about the day-to-day spending- how we spend versus how we save money.

In countries like Japan and Germany, there is a high level of savings. That helps those countries because a high level of savings means that banks have a lot of deposits to invest

15

16

in businesses. However, in a situation where a country has a low level of savings, such as in Nigeria, banks have a relatively low amount of money, which makes it difficult for them to invest in businesses.

Many people in this part of the world spend more than save, and this affects us at a much higher level. Countries with a high marginal propensity to save have much more money in their banks while countries with a higher marginal propensity to consume have less money in their banks.

Saving is something that requires a great deal of discipline and the government can encourage us to do certain things to establish this habit. Occasionally, the government can come up with policies that will allow us to change our behaviour and try to push us towards a specific behaviour, however, several economists say that the government is not supposed to do that.

This raises the question of whether or not the government should implement such policies.

According to neoclassical economists, human beings act naturally. They simply do what will benefit them, and only obey their selfish interests. However, over the years, we have discovered that if you actually study human behaviour, you will see that the government can do a few things to nudge us in the direction they want us to go.

Several questions have risen about this lately. One of them is that is it right for the government to compulsively deduct money from every civil servant’s paycheck and put it in a savings account they are unable to access for five years?

I believe it’s a good thing, because it gives people money on a rainy day. But the question is- is it the place of the government to do?

In my last book, Fixing Health Care in Nigeria, I suggested that if we wanted to fix health care in Nigeria, the federal government should make a deal with all providers of telecommunications services and deduct five thousand naira (₦ 5,000) from every citizen’s phone credit for a year.

However, there was a huge uproar. Some people were of the opinion that the government should not have that much power.

I said to most of them: ‘People can’t pay for their health care, so why don’t we just take it and put it in a fund so that when they have an accident or an emergency, it’s easy for them to be treated, without having to pay?’ Even with this argument, many people still said No.

17

This is one of the key issues I’ve addressed in the essay section. I’ve provided answers to thought-provoking questions such as:

What is the role of the government?

Why do people do what they do?

Do people serve their selfish interests alone, or are they easier to influence than we think?

Let’s assume that people are easier to influence than we think;

Should the government actually do the influence?

Do they have the right?

Should they have the power to influence that kind of thing?

Another issue I’m going to discuss is the environment. It is not in any of the essays, but it’s crucial because environmental economics is part of microeconomics.

Nigeria has suffered some devastating oil spills in the Niger Delta. We generate a lot of wealth from that region as a nation, but at huge costs. Some fishing communities in the Niger Delta can no longer fish because the fish have died as a result of oil spills.

When a company produces something and an unwanted by-product or harmful effect occurs as a result of that production, it is called a negative externality. Nigeria, for example, has suffered greatly from these negative externalities, especially in the oil-producing region.

Since emerging markets like Nigeria desperately need money from natural resources like oil, we haven’t bothered to put policies to preserve our environment in place. As a result, we have had a lot of environmental degradation.

As I go further in this explainer, I would like to talk about corruption- one of Nigeria’s biggest problems.

Research from the Clayton Christensen Institute explains that as people become richer and the economy develops, corruption naturally decreases. According to him, this has been observed in many countries around the world.

There has been much work on market structures and how they are formed in microeconomics. I’m not going to talk about it in the essays, but I think it’s imperative to mention it when giving an overview of microeconomics.

18

Market structures are a crucial part of microeconomics, and the monopoly structure is a market where there is only one influential player with a large market share. They are called price makers because they dictate prices.

In this situation, no matter how expensive a product is, it is almost impossible to substitute.

In emerging markets, corruption tends to bring about some of these monopolies that impoverish people because they provide essential goods at extremely high prices, which has a negative impact on economic development.

Identifying these monopolies, legislating them, and making policies around the formation of monopolies is definitely something that we should look into.

It would not be fair to conclude this explainer without highlighting employment issues. The issue of unemployment would normally be discussed in the macroeconomics explainer. In this microeconomics explainer, I will be talking about employment, although I will be focusing more on why people decide to work as opposed to just resting at home, and what makes them more likely to work.

I mentioned the role of labour unions in my essay on microeconomics. I explained that one of the things that happen in emerging economies is being plagued by low wages. Unions can be a way to raise wages because an average union worker earns more than a non-union worker (references available in the essay).

However, unions may be counterproductive to profitability when they are too strong.

If you look at the trends in union membership, you will see that union membership around the world has decreased significantly in the last ten (10) to twenty (20) years. This is probably due to the impact these unions have on the profitability of companies.

I’m going to talk more about unions in the essay section, however, I want you to understand that while there are good sides to labour unions in terms of actually raising average workers’ wages, they can also be detrimental.

19

Thank you for joining me in exploring the wonderful world of microeconomics. At the end, I’m sure you will know why you have a friend who gets her salary and spends it all right away, and why another one tries to invest as much as she can in land, property, shares, and stocks. You will also know why that other friend of yours likes to keep every penny she has in her savings account.

As I explained earlier, microeconomics simply studies why individuals, as well as firms, do what they do.

Thank you so much for reading.

I hope you enjoy the essay!

20

Chapter 1

MicroeconomicsStandard neo-classical theory argues that saving and spending behaviour is the product of rational financial planning.

Discuss both traditional and behavioural views of such personal financial decision making, highlighting the policy proposals arising from these approaches. Having high rates of saving is important for financial development in countries like Nigeria. But currently, Nigerians save less than many of our African peers. Can government policy interventions to change consumer behaviour ever be legitimised?

IntroductionThis paper will start by examining both the traditional and behavioural views of personal financial decision making. It will go on to explore how personal financial decisions can affect the economy and whether it is therefore the place of government to design policy to attempt to change consumer behaviour.

Microeconomics is concerned with the behaviour of individuals and firms. This behaviour can be studied from different perspectives among which are the traditional perspectives and the behavioural perspective.

Both are discussed on the next page.

21

Figure 1

The traditional view

The origins of the traditional view can be found in the works of philosophers like Aristotle. Aristotle ‘based economics on needs, analyzed their nature and proceeded to isolate the economic goods by which economic needs are satisfied’ (Koumparoulis, 2011).

Views from Aristotle and philosophers like him at the time are called the pre-classical theories.

The pre-classical theory was then superseded by the classical theories. Classical theory was popularised by the world’s most influential economist, Adam Smith. Adam Smith referred to the ‘invisible hand of the market’, explaining that because humans act rationally, there is no need for any central price planning mechanism. This is because the market moves automatically to produce more of what people want. Smith was an ardent proponent of a laissez faire style of governance where demand and supply reigned supreme. He argued that only the free market could bring society into natural harmony (Williams, 1976). To him, government central planning was unnatural and unnecessary (West, 1969).

Introducing ‘Homo Economicus’…

This view dominated the fields of economics, political science, sociology and philosophy for over a century (Anderson, 2000).

22

The term ‘homo economicus’ refers to the archetypal classical description of the way human beings act and make decisions.

According to Doucouliagos (1994), Homo Economicus has three main characteristics:

1. He/She acts to maximise personal benefit or pleasure, maximising behaviour.

2. He/She makes every decision rationally and has the cognitive ability to do so.

3. He/She acts in his/her own self-interest – individualistic behaviour.

Smith argues that the main reason for anyone to engage in exchange is ‘self-love’. Homo economicus is fundamentally self-interested. The quote below from his book ‘The Theory of moral sentiments’ exemplifies this notion:

“Every man is no doubt by nature, first and principally recommended to his own care and as he is fitter to take care of himself than any other person, it is fit and right that it should be so. Every man, therefore, is much more deeply interested in whatever immediately concern himself, than in what concerns any other man.’’

(Smith, 1759)

The central tenet of the subsequent neoclassical theory is similarly built around ‘rational choice theory’. This is the idea that human beings act rationally to maximise utility. However, compared to classical theory, neoclassical theory highlights the roles of marginalism and perception.

Marginalism highlights the pleasure/utility experienced from the consumption of one extra unit of a particular product/service. Classical theory also focuses on the idea that price is determined by the costs required to produce a particular good or service. However, neoclassical theory recognises the role of consumer perception in determining the price or demand for goods and services.

Neoclassical theory would also assume that saving and borrowing decisions are largely rational.

23

The behavioural viewThe behavioural view challenged the notion of the completely rational homo economicus which previously was the dominant perspective on human behaviour in economics. Justin Fox refers to the emergence of the behavioural view in economics as ‘irrationality’s revenge’ in his Harvard Business Review article (Fox, 2015).

Homo economicus has evolved…

After over a century of believing that human beings are rational, many economists began to find out that in many cases, this was not the case. However, Kahneman and Tversky (1979) were the most influential voices in this movement, explaining how psychological phenomena such as bias, context, framing, and heuristics affect decision-making. When these insights from psychology are taken into consideration, it produces a more realistic picture of what people in the real world actually do (Kahneman, 1979).

Borrowing and saving: Neoclassical vs behavioural perspective

Whilst the neoclassical theory would assume that saving and borrowing decisions are largely rational and based on self- interest, the behavioural theory takes a more nuanced approach.

Why do people save?

Savings move income from the present to the future whilst borrowing moves income from the future to the present.

People save because intemporal income (income distribution over different periods of life) doesn’t match consumption needs. So, during early school years, most children in developed countries don’t work but need to consume food, clothing and other expenses such as school fees. When people reach working age, income rises but declines as people move into retirement. However, retirement expenses may increase due to medical bills.

24

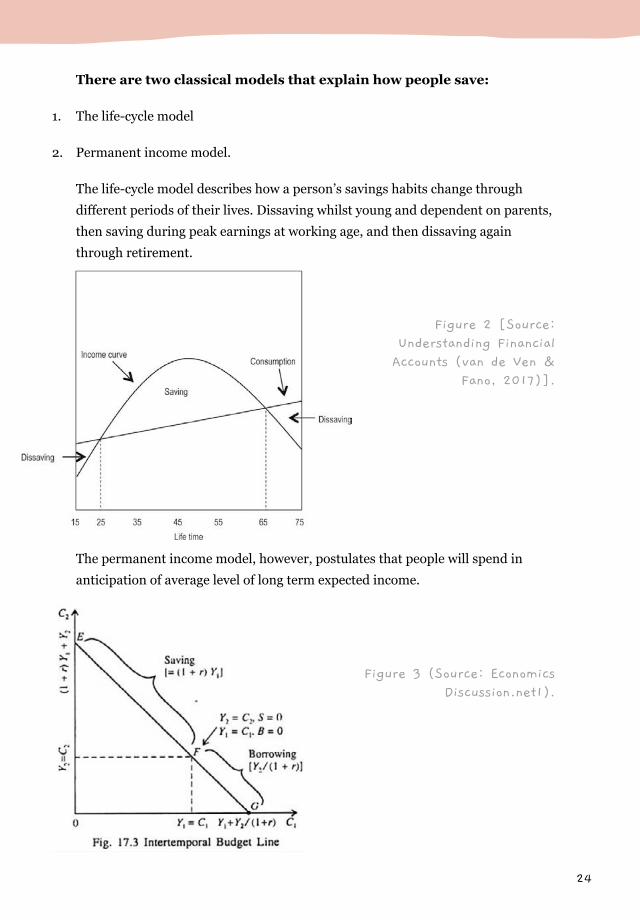

There are two classical models that explain how people save:

1. The life-cycle model

2. Permanent income model.

The life-cycle model describes how a person’s savings habits change through different periods of their lives. Dissaving whilst young and dependent on parents, then saving during peak earnings at working age, and then dissaving again through retirement.

The permanent income model, however, postulates that people will spend in anticipation of average level of long term expected income.

Figure 2 [Source: Understanding Financial Accounts (van de Ven &

Fano, 2017)].

Figure 3 (Source: Economics Discussion.net1).

25

Consumers must decide how much they want to spend in the present and how much they want to save for the future; this is depicted by the intertemporal budget line. This classical model highlights the role of interest rates in both saving and borrowing decisions.

Browning, 1996 acknowledges these models, but also explores the role of behavioural issues that affect how people save and borrow. Some people have more self-control than others. Some people also possess computational ability—the ability to accurately calculate how much to save or borrow to meet their immediate and future needs (Browning, 1996).

The classical models also don’t take into consideration the effect of economic cycle on saving and borrowing behaviour. People borrow more during economic boom periods and save more during down recessions (Nofsinger, 2010).

Furthermore, individuals may engage in precautionary saving if they feel they might experience a drop in income. So they save when the permanent income model predicts they would borrow. The neoclassical model similarly doesn’t take into consideration those extreme low-income earners that have no access to credit markets in the first place (Jones, 2009).

The effect of personal financial decisions for government‘The financial stability of an economy is significantly influenced by the evolution of household financial behavior.’ (Kłopocka, 2017)

Kauffman (1991) explains how a decline in household savings can affect the level of funds needed for investment. Furthermore, Nofsinger explains how household behaviour can actually exacerbate the entire boom/bust economic cycle. This is because during an economic boom, households are influenced by extrapolation bias and groupthink. Extrapolation bias is the tendency to take a recent experience and believe that same pattern will continue forever. Groupthink is a situation where an entire group of people starts thinking in the same way, not questioning the weaknesses, leading to a dysfunctional outcome (Nofsinger, 2010).

26

So since personal financial decisions have such a significant effect on the wider economy, should the government try to influence behaviour through policy?

The role of government policy in changing consumer behaviourAs mentioned earlier, Adam Smith argues that the invisible hand of the market allocates resources in the most effective manner. This therefore negates the need for government intervention. However, Mankiw (2009) argues that the hand of the market is indeed powerful, but by no means all knowing.

Limitations to the hand of the market come in the form of externalities. Externalities are positive or negative consequences of economic output that influences a bystander, who neither pays nor receives any compensation for that effect. An example of a negative externality is pollution. Some industries produce a lot of pollution that affects people in many communities.

Some governments use policy to try to reduce pollution levels and protect citizens from its harmful effects. Economists have argued that private entities are capable of bargaining amongst themselves to counter externalities; this is known as the Coase Theorem, named after the economist who first put this idea forward. Although it sounds logical, it often fails in practice, making a case for some form of government intervention (Mankiw, 2009).

So we have established that in cases like pollution that has widespread effects on our environment, there may be a plausible role for government intervention. In a sense there are already many policy interventions that affect behaviour that are widely accepted. For example, taxation, subsidies, provision of public goods.

In the next section, we consider how and if at all the government should intervene in far more seemingly intrusive matters like our personal finances.

27

Should government get involved in how we spend vs when we save?The Boston Federal Reserve published a paper in 2007 (Benton et al., 2007). It studied low income earners and point out how they are disproportionately affected by under-saving and over-borrowing.

They disagree with the classical perspective that humans act rationally when it comes to financial decisions. They also point out how vulnerable low-income earners are when they do not save due to the possibilities of emergencies. The paper also talks about how damaging low credit scores can be for low income earners that borrow unsustainably and are unable to pay back their loans.

At the centre of their argument is the concept of self-control and how a lack of self-control, closely related to procrastination, is one of the factors responsible for over-borrowing and under-saving.

Four policy suggestions are put forward to help. These include:

1. Commitment devices; vehicles that charge high penalties for withdrawal of saved funds

2. Front loaded devices; instruments that deduct savings from wages at source

3. Default saving clubs that participants must deliberately opt out of

4. Promoting bank account products for the unbanked

(Benton et al., 2007)

However, many economists disagree fundamentally with the idea of libertarian paternalism. This is the idea that it’s possible to deliberately channel people to make decisions which are ‘better’ for them whilst leaving them with freedom of choice.

28

Although some Economists call the term ‘Libertarian paternalism’ an oxymoron, arguing that the freedom of choice and the steering of one’s choice cannot coexist, there is a great deal of support for this idea as well, simply because so many economists now agree that ‘individuals are often not the best judges of their own welfare’ (Schlag, 2003).

Therefore, some method of guiding people towards the correct choices for them without coercion is inevitable (Sunstein & Thaler, 2003).

ConclusionThe history of economic thought is fascinating. From the early work of Aristotle in 384 BC, the question of how and why people make choices and how to predict them has puzzled economists, philosophers and psychologists.

The pre-classical, classical and neoclassical theories view human beings as rational decision makers. However, insights from the field of psychology reveal how a whole host of factors such as framing, anchoring, bias, and heuristics affect how we make decisions. Humans are rarely completely rational.

Libertarian paternalism has been suggested as a solution to help people navigate the increasingly complex array of savings/investment and loan instruments as well as help people with low levels of self-control make better decisions (Carlin, 2013).

29

References• Anderson, E. (2000). Beyond Homo Economicus: New Developments in Theories of Social Norms.

Philosophy & Public Affairs, 29(2), 170–200.

• Benton, M.; Meier, S.; Sprenger, C. (2007). Overborrowing and Undersaving: Lessons and Policy Implications from Research in Behavioral Economics, Federal Reserve Bank of Boston, Community Development Discussion papers, No. 2007-4.

• Browning, M.; Annamaria, L. (1996). Household Saving: Micro Theories and Micro Facts. Open Dartmouth: Faculty Open Access Articles. 2429. https://digitalcommons.dartmouth.edu/facoa/2429

• Carlin, B. I.; Gervais, S.; Manso, G. (2013). Libertarian Paternalism, Information Production, and Financial Decision Making. The Review of Financial Studies, 26(9), 2204–2228.

• Doucouliagos, C. (1994). A Note on the Evolution of Homo Economicus. Journal of Economic Issues, 28(3), 877–883.

• Fox, J. (2015). From economic man to behavioral economics. Harvard Business Review, May 2015 issue, 78–85.

• Kahneman, D.; Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47 (2), 263-291.

• Kauffman, B. (1991). Microeconomics of saving. Economic Papers; Commission of the European communities. Number 89. http://aei.pitt.edu/36996/1/A3031.pdf

• Kłopocka, A.M. (2017). Does Consumer Confidence Forecast Household Saving and Borrowing Behavior? Evidence for Poland. Social Indicators Research, 133, 693–717. https://doi.org/10.1007/s11205-016-1376-4

• Koumparoulis, D. M. (2011). Aristotle’s Economic Thought, Educational Research, 2(13) pp. 1831-1838.

• Nofsinger, J. (2012). Household behavior and boom/bust cycles. Journal of Financial Stability. 8(3), 161-173 https://doi.org/10.1016/j.jfs.2011.05.004

• Schlag, P. (2010). Nudge, choice architecture, and libertarian paternalism. Michigan Law Review, 108(6), 913–924. www.jstor.org/stable/40645851

• Smith, A. (1759). The theory of moral sentiments, ed. DD Raphael & AL Macfie. Liberty Fund (original work published in 1759).

• Sunstein, C.; Thaler, R. (2003). Libertarian Paternalism Is Not an Oxymoron. The University of Chicago Law Review. 70(4), 1159-1202.

• van de Ven, P.; Fano, D. (eds.) (2017). Understanding Financial Accounts, OECD Publishing, Paris, https://doi.org/10.1787/9789264281288-en

• Waters, William R. (1976). Social economics of Adam Smith: introduction. Review of Social Economy, 34(3), 239–243.

• West, E. G. Adam Smith’s Philosophy of Riches. Philosophy, 44(168), 101–115.

• Mankiw, G. (2009). Principles of microeconomics. Fifth edition. Southern Cengage Learning, p. 221-464.

30

Chapter 2

How are wages determined and what role do trade unions play in improving conditions for workers particularly in emerging markets?

Currently, the world is experiencing the first truly global pandemic – an outbreak of the novel coronavirus, COVID-19. This outbreak, along with the chaos and economic strain that has come with it, has left many people asking important questions. Such questions include: Why do we pay footballers and movie stars so much more money than virologists and doctors?

This paper will examine some of the factors that affect the amount people earn and why people work in the first place. Membership of a trade union is one factor that affects how much people earn. Other factors will also be examined before taking a deep dive into the effects of trade unions and trends in trade union membership across the world.

The focus of this paper will be on neoclassical labour theory and the impact of trade unions. Other factors will be touched on briefly towards the end.

1. Demand and Supply

The neoclassical approach to labour views a firm’s decision to hire as a decision based on demand, supply and productivity. It sees workers and firms as completely rational. Firms seek to make the most profit whilst workers seek to maximise utility.

31

Figure 1

Figure 1, above, shows the balance between the neoclassical view of the goals of workers and firms.

Neoclassical theory of labour views the labour market as a ‘place’ where buyers and sellers of labour meet to exchange hours of labour for wages, and based on demand and supply, they reach agreement/equilibrium (Fleetwood, 2014).

Each factor of production earns the value of its marginal contribution to the production of goods/services at equilibrium. Neoclassical theory is widely accepted amongst economists as a starting point when trying to understand why people are paid different wages across industries and professions (Mankiw, 2009).

Neoclassical economics views unemployment effectively as a ‘’choice’’. Unemployment is seen as voluntary leisure, chosen over employment when a worker’s reservation wage is not met (Spencer, 2006).

32

Figure 3 (Prasch, 2000)

The graph above (Figure 2) shows the classical neoclassical representation of the labour market.

However, the curve can be backward bending (as shown below) when a certain level of income is reached as people that are earning large amounts of money at some point stop working so hard. They typically spend more time doing leisure activities after a certain point. In technical languages, the substitution effect becomes more significant than the income effect.

2. Impact of Trade Unions

This section will explore the impact and influence of trade unions as well as some key features/trends.

Figure 2 (Jean, 2014)

33

It’s often assumed that employers have the power to determine wages, but trade unions disrupt this balance by using collective bargaining to negotiate wages on behalf of their members. But there are also less obvious ways that trade unions can influence wages.

Trade unions effect on wages

There are several indirect ways that trade unions can affect wages. Firstly, unions give workers ‘voice’ regarding tenure, training and human development, etc. (Benson, 2009). The threat of unionisation can raise wages in the non-union sector. But also, job losses in the union sector can result in excess labour supply to the non-unionised sector which depresses wages (Bryson, 2014).

The main way trade unions affect wages is directly through their bargaining activities. This can give an estimated wage premium of about 15% according to some research, although there has not been consensus on this (DeFina, 1983 Bargaining activities include strikes (discussed in this section).

Figure 4

34

Unions cause wages to rise partly because unionised workers can withdraw their labour en masse, causing massive disruptions to production if their demands are not met. This is called a strike. However, over the past few decades, the number of union-backed strikes and their effectiveness as regards raising wages have changed, so it’s worth spending a little time below to understand the trends.

a) Strikes

Figure 5 shows the decline in number of strikes over the past few decades (Rosenfield, 2014)

Strikes, previously unions most powerful weapon, has declined gradually over the past few decades, despite a massive growth in the labour force. This has happened despite research that shows that unionised workers that strike obtain higher wages than unionised workers that don’t. Some argue that the decline in strike action is because workers and management understand each other better than they did a few generations ago.

Figure 5

35

However, there is also evidence that strikes simply don’t accomplish what they did in the past. In the 70s, employers began to ‘strike back’ by hiring permanent replacements and moving operations to non-unionised facilities, making union leaders think more carefully about potential repercussions before using this tool (Rosenfield, 2014).

b) Effect on employment/skills

However, it has been found that unions may cause few people to be employed and cause wages for non-unionised workers to fall because the unions’ demands for higher wages often cause fewer people to be employed as firms tend to employ more people when wages are lower. On the other hand, models show that the stronger the union is, the higher the mark-up over the reservation wage (the lowest salary/wage that an employee would be willing to take for any particular type of job) and the lower the resulting wage level (Tito, 2013). Therefore, unions face a trade-off between increased wages for their members and low unemployment (Creedy, 1989).

Oswald (1982) points out that where unions operated, there is a loss of efficiency because the marginal product of labour for a union worker, assuming the labour market is competitive, differs from that of a non-union worker.

He also points out that whilst the union workers are better off, the non-union workers are poorer, and the firm may or may not be negatively affected (Oswald, 1982). But this wage differential between union and non-union workers is highly dependent on skills of the worker. The more skilled the worker is, the less significant the overall difference in wages is between union and non-union workers (Hirsch, 1998).

This issue has led to internal disputes within unions. Many unions base their arguments around wage differential between highly skilled and low skilled workers, pursuing an egalitarian ideal. This potentially diminishes the premium put on additional skills and may alienate highly skilled workers, causing them to leave the union completely. For example, a famous case in Italy called the ‘marcia dei 40,000’ when middle class/highly skilled workers went on strike against the unions (Tito, 2013).

36

c) Income inequality

Most countries strive for higher levels of income equality. A paper by the National Institute for Economic and Social Research explains how income inequality would almost certainly be higher without the bargaining power of unions. Whilst neoclassical theory emphasizes market-driven wages determined by the forces of demand and supply, unions enable workers to extract an above-market premium for their labour.

The influence of unions has decreased over time as indicated in Fig 4; this has led to increased income inequality which is detrimental to workers (Bryson, 2014).

d) Unions as monopolies

Unions do exert some form of monopoly power due to their ‘strike threat system’ described above. They exert some control over the supply of labour; this generates bargaining power which is used to resist downward pressure on wages (Bryson, 2014).

Their actions change both working conditions and wages; this is an evidence of monopoly power, but ‘without coercion’, according to Burkitt (1977). Also, the power that unions wield never becomes all-encompassing like producer monopolies, even when their polices are successful.

Burkitt (1977) argues that “trade unions counter pre-existing market imperfections and eliminate the ‘distortions’ of unorganised labour markets.”

However, Lindbolm (1958) makes an interesting counter-argument. He states that strike action is a form of coercion and that unions can have the same levels of control over the price of labour that private enterprises aren’t allowed over the cost of their products (Lindbolm, 1958).

e) Health and Safety

Unions were at the forefront of pushing for better welfare and health/safety at work. This is particularly relevant in the mining industry where it was worker unions that articulated the link between brown lung disease (a form of respiratory

37

illness) and mining. They went on to bargain for better working conditions that have benefited unionised and non-unionised workers alike (Alejandro, 2012).

f) Political support for unions

In the face of globalisation and decreased political support, the membership and impact of trade unions have decreased (see figure 6 below). Laws have been enacted to decrease the power of trade unions. A large group of air traffic control workers were sacked in the United States under Ronald Reagan when they illegally went on strike (Goodwin, 2019).

g) The future of unions

Unions must evolve to take on non-bargaining with greater levels of collaboration with firms. It is realised that a union cannot offer its members any jobs if the firm is bankrupt (Ratnam, 2007). Ashenfelter and Johnson (1969) support this notion by pointing out the effect of asymmetrical information. They argue that there is often asymmetrical information on the part of the unions, that is, the unions may not be able to accurately determine the financial health of the firm (Ashenfelter, 1969).

Figure 6

38

Figure 6, on the previous page, shows how union membership has declined over the past few decades (Tito, 2013).

This section has highlighted the fact that unions are powerful institutions that can help workers to obtain higher wages through the power of collective bargaining. But it has also pointed out how unions may decrease the actual number of employment opportunities available, disadvantaging non-union workers. The role of skills was also noted; how highly skilled workers don’t need unions as much as lower skilled workers to negotiate higher wages.

Additionally, the reasons why trade union membership is declining, such as globalisation, politics/law/policy and the rise of the service industry, were examined. Unions are also ageing rapidly and finding it hard to attract and recruit younger members (Tito, 2013). Brief comments on the possible future of trade unions – with an expanded scope and collaborative approach – were also made.

To conclude, it’s important to point out just how revolutionary trade unions have been for mainstream policy. Many of the benefits and innovations that have made workplaces easier to navigate, such as flexitime, sick leave and childcare, were born out of trade unions. These are commonplace now but were once very radical. This is a good example of how the hard work of trade unions over decades has ultimately left society better off (Goodwin, 2019).

ConclusionThere are many factors that affect wages and employment that have been analysed in this paper.

It has been shown that the neoclassical approach may have some merit and that has been considered in depth in this paper. Additionally, it has been revealed that demand and supply do affect how much workers are paid in wages and many human beings make trade-offs between the income effect and the substitution effect when considering their work options.

The type of market a worker operates in may also affect wages. In a perfectly competitive market, the labour curve is perfectly inelastic. This means that any attempt to lower wages will result in workers leaving the firm as the market wage is determined by factors beyond the control of the employer.

39

However, in a monopsony, the employer has a lot of control over wages, so therefore, wages can fluctuate and the workers have little power and no alternatives (Manning, 2003).

Neoclassical labour theory teaches us how human beings are rational and the only reason why workers work is to earn a wage to maximise their utility. But there is alternative evidence that this simply isn’t true. A job to many people isn’t just about the money. For many, its central to their identity. Studies by Kaplan (1987) and more recently by Arvey (1996) show that lottery winners don’t typically quit their jobs. Hirschfield (Hirschfeld, 2000) considers this concept of work centrality in his book. He refers to people with a high level of work centrality as “people who consider work as a central life interest, have a strong identification with work in the sense that they believe the work role to be an important and central part of their lives.”

This contrasts directly with the neoclassical approach to the labour market.

Minimum wage legislation, the rise of the gig economy, technology (such as artificial intelligence and robotics) are already affecting wages and will continue to in the future. It is these rapid changes that have fuelled debates around the feasibility of providing everyone with a universal basic income (Downes, 2018). Goodwin (2019) also points out how discrimination based on gender, ethnicity and sexual orientation can also affect wages.

This paper focused on the role of unions, how they influence wages, employment, and how some may view them as monopolies. Although the influence of unions may have declined over the years, their legacy lives on in the form of benefits such as childcare benefits and health that have created happier, safer, more thoughtful workplaces for us all.

40

References• Alejandro, D. (2012). HOW TRADE UNIONS INCREASE WELFARE. The Economic Journal,, 990-

1009.

• Arvey, R. D. (1996). Work Centrality and Post-Award Work. The Journal of Psychology, 2-3.

• Ashenfelter, O. (1969). Bargaining, trade unions and indutrial strike activity. American Economic Review, 45.

• Benson, J. (2009). Employee voice: does union membership matter? Human Resource Management Journal .

• Berle, A. a. (1932). The Modern Corporation and Private Property. New York : Macmilan.

• Bosco, D. (2011, Febuary 10). Why didn’t the IMF predict the financial crisis? Foreign Policy .

• Boughton, J. (2011). “Jacques J. Polak and the Evolution of the International Monetary System. IMF Economic Review, vol. 59, no. 2, pp. 379–399.

• Brett, E. (1983). The World’s View of the IMF.” The Poverty Brokers: IMF and Latin America. London: Latin American Bureau.

• Bryson, A. (2014). Union Wage Effects. IZA world of labour, 1-3.

• Burkitt, B. (1977). Are trade unions monopolies? Industrial relations journal , 16-18.

• Calomiris, C. (1990). Is Deposit Insurance Necessary? A Historical Perspective. The Journal of Economic History , 283-295.

• Carstens, A. (2018). Deposit insurance and financial stability: old and new challenges. 17th IADI Annual General Meeting and Annual Conference on “Deposit insurance and financial stability: recent financial topics”. Basel : Bank for International Settlements.

• Cheffins, B. (2018). The Rise and Fall (?) of the Berle-Means Corporation. Seattle University Law Review.

• Creedy, J. (1989). “Trade Unions, Wages and Taxation. Fiscal Studies, 50-59.

• DeFina, R. (1983). Unions, Relative Wages, and Economic Efficiency. Journal of Labor Economics, 408-429.

• Demirgüç-Kunt, A, E., Feyen, R., & Levine. (2011). The evolving importance of banks and securities markets”. World Bank, Policy Research Working Paper,, no 5805.

• Demirguc-Kunt, A. &. (2001). Deposit Insurance Around The World . The World Bank Economic Review, 481-490.

• Demirguc-Kunt, A. L. (1999). Bank-based and market-based financial systems - cross-country comparisons. Policy Research Working Paper Series 2143, The World Bank.

• Desai, P. (2011). In Financial Crisis Origin. In From Financial Crisis to Global Recovery (pp. pp. 1-20). New York: Columbia University Press.

• Downes, A. (2018). It’s Basic Income: The global debate. Bristol: Bristol University Press.

• Dreher, A. a. (2004). The Causes and Consequences of IMF Conditionality. Emerging Markets Finance & Trade, vol. 40, , pp. 26–54.

• Fischer, S. (1999). On the need for a lender of the last resort. Address to the American Economic Association. New York: American Economic Assciation.

• Fleetwood, S. (2014). Do labour supply and demand curves exist? . Cambridge Journal of Economics, 1087-1113.

41

• Gambacorta, Leonardo, J., & Yang, K. T. (2014). Financial structure and growth. BIS Quarterly Review.

• Goodwin. (2019). Microeconomics in context, 4th Edition . New York : Routledge.

• Hirsch, B. (1998). Unions, Wages, and Skills. The Journal of Human Resources, 201-219 .

• Hirschfeld, R. (2000). Work centrality and work alienation. Journal of Organizational Behavior, 789–800.

• Hogan, T. a. (2016). The Independent Review. Alternatives to the Federal Deposit Insurance Corporation, 433-54.

• IMF. (2015). Ukraine: Letter of Intent, Memorandum of Economic and Financial. Kyiv: IMF.

• Independent Evaluation Office of the International Monetary Fund. (2011). IMF Performance in the Run-Up to the financial and economic crisis. Washington DC: IMF.

• International Monetary Fund. (1998). The Asian Crisis: Causes and Cures. Finance and Development , Volume 35, Number 2.

• Ito, T. (2012). Can Asia Overcome the IMF Stigma? The American Economic Review, 198-202.

• James, B. (2001). Silent Revolution: The IMF 1979-1989. Geneva: IMF Bookstore.

• Jean, V. (2014). The Neoclassical Model of the Labour Market. London: Palgrave Macmillan.

• Joyce, J. (2000). œThe IMF and Global Financial Crises. Challenge, 88.

• Kaplan, H.R. (1987). Lottery winners: The myth and reality. . J Gambling Stud 3, 168-178.

• Kapur, D. (1998). The IMF: A Cure or a Curse? Foreign Policy, no. 111, pp. 114–129.

• King, M. (2001). Who Triggered the Asian Financial Crisis? Review of International Political Economy, 438.

• Krugman, P. (2009). The Return of Depression Economics and the Crisis of 2008. New York : W. W. Norton & Company.

• La Porta, R. L. (1997). Legal Determinants of external finance. Journal of finance, 1131-1139.

• Laeven, L. (2002). Bank Risk and Deposit Insurance. The World Bank Economic Review, 109-137.

• Levy Institute. (2013, April ). The lender of last resort: A critical analysis of the Federal reserves unprecedented intervention after 2007. pp. 1-15.

• Lindblad, J. T. (2010). IMF: The Road from Rescue to Reform.” In The Asia-Europe Meeting: Contributing to a New Global Governance Architecture: The Eighth ASEM Summit in Brussels. Amsterdam: Amsterdam University Press.

• Lindbolm, C. (1958). Are Labor Unions Monopolies? Challenge, 26-31.

• Macey, J. R. (2008). The role of banks and other lenders in corporate governance; corporate governance promise kept, promises broken . Oxford: Princeton University Press.

• Mankiw, G. (2009). Principles of Microeconomics. Boston: South Western Learning.

• Manning, A. (2003). Monopsony in Motion: Imperfect Competition in Labor Markets,. Oxford: Princeton University Press.

• Mc Kinnon, R. &. (1999). Exchange rate regimes for emerging markets: moral hazard and overborrowing. Oxford Review of Economic policy , 19-38.

• McKinnon, R. &. (1997). Credible Economic Liberalizations and Overborrowing. The American Economic Review, 189-193.

42

• Mellor, M. (2010). The Future of Money: From Financial Crisis to Public Resource,. London : Pluto Press.

• Minsky, H. (1992). The Financial Instability Hypothesis. The Levy Economics Institute Working Paper Collection, Working paper 74, 1-10.

• Moschella, M. (2011). The Global Financial Crisis and the Reforms to IMF Lending. St Antony’s International Review , 48-60.

• Mussa, M. a. (1999). The IMF Approach to Economic Stabilization. NBER Macroeconomics Annual, pp. 79–122.

• Nicholas, S. (1998). The IMF as International Lender of Last Resort? A Reappraisal After the ‘Tequila Effec. London: Palgrave Macmillan.

• Nooruddin, I. a. (2006). The Politics of Hard Choices: IMF Programs and Government Spending. International Organization, vol. 60, no. 4, pp. 1001–1033.

• Norrbin, M. M. (2017). International Money and Finance. In S. N. Michael Melvin. Elsevier.

• Nowak, W. (2012). Development of the Polak model . Wroclaw review of law, administration and economics, 28-35.

• Oswald, A. (1982). Trade Unions, Wages and Unemployment: What Can Simple Models Tell Us. Oxford Economic Papers, 526-545.

• Papi, L. P. (2015). IMF Lending and Banking Crises. IMF Economic Review, 644-691.

• Polak, J. (1994). The World Bank and the IMF: A Changing Relationship. Brookings Institution Press.

• Polak, J. J. (1957). Monetary Analysis of Income Formation and Payments Problems. Staff Papers (International Monetary Fund), pp. 1–50.

• Prasch, R. E. (2000). Reassessing the Labor Supply Curve. Journal of Economic Issues, 679–692.

• Prowse, S. (1990). Institutional Investment Patterns and Corporate Financial Behaviour in the United States and Japan. Journal of Financial Economics, 43-66.

• Rajan, R. Z. (2003). The great reversals: the politics of financial development in the twentieth century. Journal of financial economics, 5-50.

• Ratnam, V. (2007). Trade Unions and Wider Society. Indian Journal of Industrial Relations, 620–651.

• Rogoff, K. (2003). The IMF Strikes Back. Foreign Policy , 39-46.

• Rosenfield, J. (2014). Strikes.” What Unions No Longer Do. Boston: Harvard University Press.

• Roubini, N. (2004). Bailouts Or Bail-Ins?: Responding to Financial Crises in Emerging Economies. Peterson Institute for International Economics.

• Shleifer, A. a. (1986). Large Shareholders and Corporate Control. Journal of Political Economy, pp. 461–488.

• Siebert, H. (2005). “The Capital Market and Corporate Governance.” The German Economy: Beyond the Social Market,. Oxford: Princeton University Press.

• Sleet, C. B. (2000). Deposit Insurance and Lender-of-Last-Resort Functions. Journal of Money, Credit and Banking, 518-575.

• Souha, S. B. (2020). Shareholder activism, earnings management and Market performance consequences: French case. International Journal of Law and Management.

• Spencer, D. (2006). “Work for All Those Who Want It? Why the Neoclassical Labour Supply Curve Is an Inappropriate Foundation for the Theory of EEmployment and Unemployment. Cambridge Journal of Economics, 459–472. .

43

• Stone, R. W. (2008). “The Scope of IMF Conditionality. International Organization, vol. 62, no. 4, , pp. 589–620.

• Stuckler, D. a. (2009). THE INTERNATIONAL MONETARY FUND’S EFFECTS ON GLOBAL HEALTH: BEFORE AND AFTER THE 2008 FINANCIAL CRISIS. International Journal of Health Services 39, no. 4 , 771-781.

• Theodor, B. R. (1993). Institutional Investors and Corporate Governance. De Gruyter.

• Tito, B. (2013). Unions and Collective Bargaining- The Economics of Imperfect Labor Markets. Oxford: Princeton University Press.

• Vreeland, J. R. (2003). “Why Do Governments and the IMF Enter into Agreements? Statistically Selected Cases.” . International Political Science Review / Revue Internationale De Science Politique, Vol 24, pp. 321–343.

• Willett, T. (2001). Understanding the IMF Debate. The Independent Review , 593-600.

• Woods, N. (2006). Understanding Pathways Through Financial Crises and the Impact of the IMF: An Introduction. Global Governance, 373-93.

• World Bank. (Accessed 2020). World Bank development indicators. Retrieved from http://datatopics.worldbank.org/world-development-indicators/: http://datatopics.worldbank.org/world-development-indicators/

44

SECTION 2

MACROECONOMICS- EXPLAINED

Macroeconomics, in a broad sense, is the study of what is happening in the economy. It focuses on the aggregate changes in the economy, such as unemployment, growth rate, national income, gross domestic product (GDP), and inflation. In economics, we use the word ‘aggregate’. Although it confuses people, aggregate means total, i.e. an overall picture of what is going on in the economy.

Although macroeconomics studies the economy as a whole, it mainly focuses on the decisions made by governments in two specific areas- tax & expenditure decisions (fiscal policy) and the decisions concerning the control of the banking sector (monetary policy).

Macroeconomics also includes issues related to structural and exchange rate policy. However, in this explainer, I will pay the most attention to fiscal and monetary policies.

The major problem with fiscal policy- a government’s decisions about taxation and expenditure- is poverty.

It is difficult to create an effective tax system in a country like Nigeria. Sixty per cent (60%) of the population is in the informal economy, which means that they do not have a registered business. They also do not have a valid bank account or accurate records of their businesses.

In a complicated situation like this, how would you even know how much they earn? How do you intend to tax people who keep money under their pillows or inside (kolo)? These factors make taxation in Nigeria and other emerging markets complicated.

Taxation is a major source of revenue for governments in advanced countries. Most of the money the government spends comes from taxes. Luckily, here in Nigeria, the government charges a form of tax on the oil sector, which is where we get our oil revenues. However, this is nowhere near the amount of money required to cater for the needs of nearly 200 million people.

45

46

What about countries that do not have as many natural resources like we do? The answer is, most of the time, their government(s) have to rely on their citizens to provide them with money. Obviously, the government needs to spend money on essential things, such as health care, education, roads, security, and so on.

One of the problems in emerging markets is that a significant percentage of the population is too poor to be taxed in most cases. It is even problematic to try to identify them. As a result, the government cannot do much because it does not have enough financial capacity.

In regards to fiscal policy in emerging markets, one of the primary issues to be addressed is innovatively finding out how to identify people. To begin with, the government should help people formalise their businesses and in conjunction with that, institute growth-friendly policies so that they will eventually become rich enough to be able to pay significant taxes.

In Nigeria, there are areas where people spend ninety-five per cent (95%) of their income on food. It is hard to tax people that are starving.

If you take a close look at Nigeria’s poverty rate, you will find that over 40% of the entire population is living in extreme poverty. If over 40% of the population is extremely poor, how do you plan to tax them? Let us assume you devise a strategy; how do you get the money from them? Most of them do not have bank accounts, so do you take the money they owe in cash?

Fiscal policy revolves around the government getting money from citizens and businesses. If the government finds it difficult to get money from the people, it automatically becomes difficult for such a government to spend money on the economy.

It is, however, incomplete to explain fiscal policy without mentioning budgeting.

Have you ever wondered why international banks and financial markets believe in advanced countries enabling them to lend at low rates? It’s not just because of their size or system of government. Rather, this belief is due to the fact that these countries are constantly committed to growth. They keep innovating. They keep building profitable companies. As a result, these banks and financial markets feel comfortable when lending them money, knowing full well that they have the ability and capacity to pay back.

47

In emerging markets, it is much more difficult for these international banks and financial markets to lend, and the reason for this is clear. These financial entities do not have as much confidence in emerging markets compared to advanced countries. Since they do not trust us (emerging markets), they charge us high-interest rates, making us get into debt quickly. Once we start piling on debt, other financial entities will no longer believe in our ability to pay back. This makes it even more difficult for us to fund our budget as advanced countries do.

Regarding monetary policy, it simply has to do with the way the banking system is controlled.In advanced countries, the central bank has subtle ways of controlling the way people spend.When the economy is growing too fast (‘overheating’) and everything seems to be out of control, the central bank knows how to rein it in. They can actually decide that they want people to stop spending much money for the time being. They do this efficiently by using a few techniques to keep banks from loaning money to businesses. As soon as they do that successfully, the economy dries up a little bit and stops overheating.

In a situation where the economy is growing slowly- that is, businesses are not doing well- the central bank has a few tips and tricks to speed things up. They can give banks large amounts of money and encourage them to lend more, thereby boosting the economy. This means that central banks have a relatively good amount of control over the economy in advanced countries. When the economy is growing too fast, they can rein it in; when it is going too slowly, they can speed it up.

However, in emerging markets such as Nigeria, where a large number of people do not have bank accounts, thousands of these tips and tricks by the central bank just don’t work as well. Hence, the central bank resorts to other measures when trying to control the economy.

Another critical point to note is the concept of Gross Domestic Product (GDP).

GDP has to do with the total amount of money generated in a country, usually within a year. The equation for calculating GDP is: private consumption + gross investment + government investment + government spending + (exports- imports).

In advanced countries, if you divide their GDP by the total number of people, you will find that each person has a lot of money- that is called GDP per capita.

48

Take a brief look at rich countries like Luxembourg- if you divide their GDP by their total population to get their GDP per capita, you will see that it’s more than a hundred thousand dollars ($100,000) each. That is massive! If you do the same thing for the U.S., you are going to get more than sixty thousand dollars ($60,000). Do the same for the U.K., and you will get more than forty thousand dollars ($40,000).

On the other hand, emerging economies and developing countries tend to have relatively low GDPs.

In Nigeria, if you divide the GDP by the total population to get the GDP per capita, you will see that it is just under two thousand dollars ($2000).

There are some countries that once had a very low GDP per capita yet have managed to achieve massive growth, raising their extremely low GDP per capita to a much higher level.

Examples of such countries are South Korea, China and Singapore. These countries and countless others have worked their way out of poverty, increasing their GDP per capita from low to much higher levels.

Consequently, the question that begs for an answer is: how do we get more countries to chart the same course?

Above all, it is essential to note that GDP per capita is correlated with many things. It is positively correlated with life expectancy and negatively correlated with infant mortality and inequality. GDP is a relatively good measure of output, but not welfare. Keep in mind that while GDP is not a measure of economic welfare, it is a critical component of economic welfare.

In fact, there are cities in China that no longer use GDP as a measure of economic welfare. They tend to measure the quality of life of their citizens instead. They also measure happiness, as well as personal well-being.

Angola’s GDP, for example, is very high but many Angolans are living in absolute poverty. Identically, Equatorial Guinea’s GDP per capita is almost the same as some Eastern European countries, yet some of their citizens still live in poverty.

49

Another question that every government should ask is: how happy are their people?

Personally, I think that if a country has lower GDP per capita, but the people are doing very well, then that is good.

On a trip to San Francisco- home to the world’s biggest tech companies like Twitter, Uber and Visa- I remember seeing more beggars than I had ever seen in many poorer countries. Being rich does not mean you are a nice person. The fact that a country makes a lot of money does not mean the money will have a positive impact on everyone. This proves that GDP does not necessarily measure welfare. A high GDP per capita does not necessarily mean happiness, although as I said above, a larger GDP per capita is correlated with better outcomes.

This explainer has highlighted a lot, but I am not going to end it without addressing unemployment.

Recent statistics from the National Bureau of Statistics show that our unemployment rate is around 27%. This is a major problem affecting the entire Nigerian economy. When citizens of a country are unemployed or underemployed, GDP is affected. If everyone is productive, the country’s GDP will rise. However if we have low productivity rates, that does not only affect GDP, it also causes poverty.

Over the course of this explainer, I have defined macroeconomics as well as its impact on the economy. I have also explained what fiscal and monetary policy are. I did this effectively by breaking it down in the best way possible so that everyone can understand what both terms mean and how they affect the growth and development of emerging markets, including Nigeria.