edelweiss investment research · apart from these, other players are waterbase, bmr group, godrej...

TRANSCRIPT

1 GWM

Edelweiss Investment Research

Long Term Recommendation: Avanti Feeds Ltd.

All set to launch into the next Orbit.

Avanti Feeds (Avanti) is a leading manufacturer of high quality shrimps feed and processor &

exporter of shrimps. The company’s products are synonymous with quality and consistency,

which has helped it establish its credentials among farmers across India. Key growth drivers

envisaged to propel the company’s growth are: i) multiple sector tailwinds; ii) robust growth

in the shrimp feeds space with increasing area under cultivation; iii) healthy capacity

augmentation with aggressive utilization goals; iv) sustenance of leadership in the feeds

space with continued steady market share gains; and v) technical & marketing tie up with

Thai Union to bolster value-added offerings. Hence, we estimate Avanti to clock PAT CAGR of

26% over FY18-20 with healthy RoCE of 56%. Initiate coverage with ‘BUY’ and target price of

INR3,306.

Royalty among shrimp feed produces

Avanti has been in the shrimp feeds business for more than a decade with 43% market share,

which is steadily moving towards 50%. The company has established its credentials among

farmers across India by virtue of its products’ quality and consistency. Avanti has capitalized

on the boom that came in after the introduction of L. vannamei in 2009 and has grown its

feed business 2x every year. The company is running at all most full utilization and has recently

added 1,75,000MT capacity, taking its total capacity to 6,00,000MT.

Augmenting capacity to become largest shrimp processer in India

Since 2009, the company has increased capacity 15x and maintained utilization level above

70% since 2013. Avanti had a processing capacity of 7,000MT and in Q3FY18 it has started a

new 15,000MT facility capable of making high value-added partially or completely cooked

products. Thus, it now boasts of one of the largest processing capacities in India and is slated

to be the largest shrimp exporter in India by FY20. The facitiy has come on stream in Q3FY18

and has already clocked 1.5x (7,749MT) of its 2017 output (5,155MT) with one quarter still to

go. We estimate the company to utilise 100% of its capacity within the next two years.

Tailwinds galore: Industry set to expand 20% in coming years

After Green and White Revolutions in India, it’s time for the Blue Revolution to exploit the huge

potential in the fisheries sector. The government too has sharpened focus on development of

this lucrative industry, in Budget 2019 allocated a dedicated fund of INR10,000cr to develop

fisheries, aquaculture and animal husbandry. Moreover, MPEDA has set an aggressive target

of 10,00,000 MT of shrimp output by 2020 from current 6,00,000 MT. And, industry leaders, in

conjunction with MPEDA and experts, have developed policies, technology and roadmaps

to achieve an export target of USD10bn by FY22. Propelled by these catalysts, we estimate

the industry to clock 20% plus growth in coming years.

Outlook and valuations: Attractive prospects & limited downside; initiate with ‘BUY’

Key drivers envisaged to spur Avanti are: 1) robust growth in shrimp feeds space with

increasing area under cultivation; 2) rising shrimp processing capability with aggressive

capacity utilization goals; 3) maintenance of leadership in the feeds space with sustained

share gains; and 4) target to become India’s largest shrimp exporter. We initiate coverage on

the stock with ‘BUY’ recommendation, valuing it at 20x FY20E P/E and arrive at a target price

of INR3,306.

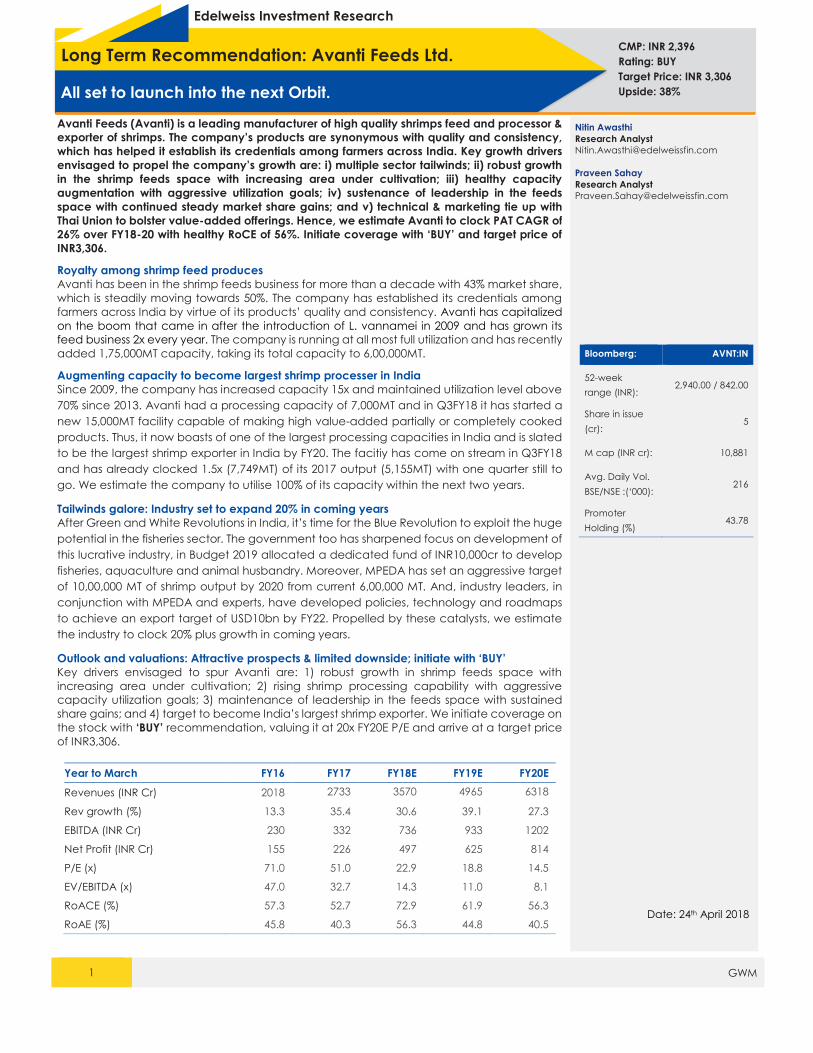

Year to March FY16 FY17 FY18E FY19E FY20E

Revenues (INR Cr) 2018 2733 3570 4965 6318

Rev growth (%) 13.3 35.4 30.6 39.1 27.3

EBITDA (INR Cr) 230 332 736 933 1202

Net Profit (INR Cr) 155 226 497 625 814

P/E (x) 71.0 51.0 22.9 18.8 14.5

EV/EBITDA (x) 47.0 32.7 14.3 11.0 8.1

RoACE (%) 57.3 52.7 72.9 61.9 56.3

RoAE (%) 45.8 40.3 56.3 44.8 40.5

CMP: INR 2,396

Rating: BUY

Target Price: INR 3,306

Upside: 38%

Nitin Awasthi

Research Analyst

Praveen Sahay

Research Analyst

Bloomberg: AVNT:IN

52-week

range (INR): 2,940.00 / 842.00

Share in issue

(cr): 5

M cap (INR cr): 10,881

Avg. Daily Vol.

BSE/NSE :(‘000): 216

Promoter

Holding (%) 43.78

Date: 24th April 2018

Avanti Feeds Ltd.

2 GWM

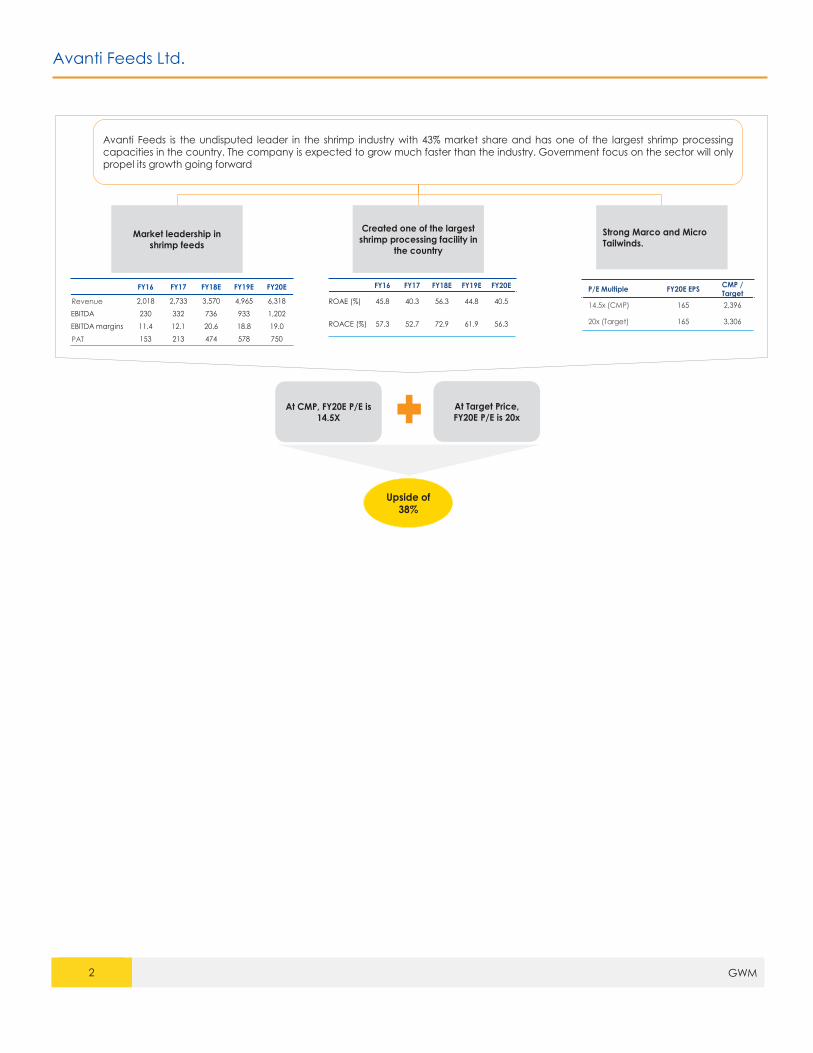

Avanti Feeds is the undisputed leader in the shrimp industry with 43% market share and has one of the largest shrimp processingcapacities in the country. The company is expected to grow much faster than the industry. Government focus on the sector will onlypropel its growth going forward

Market leadership in

shrimp feeds

Created one of the largest

shrimp processing facility in

the country

Strong Marco and Micro

Tailwinds.

FY16 FY17 FY18E FY19E FY20E

Revenue 2,018 2,733 3,570 4,965 6,318

EBITDA 230 332 736 933 1,202

EBITDA margins 11.4 12.1 20.6 18.8 19.0

PAT 153 213 474 578 750

At CMP, FY20E P/E is

14.5X

At Target Price,

FY20E P/E is 20x

Upside of 38%

FY16 FY17 FY18E FY19E FY20E

ROAE (%) 45.8 40.3 56.3 44.8 40.5

ROACE (%) 57.3 52.7 72.9 61.9 56.3

P/E Multiple FY20E EPSCMP / Target

14.5x (CMP) 165 2,396

20x (Target) 165 3,306

Avanti Feeds Ltd.

3 GWM

Risk-reward extremely favourable

Price Target INR 3,306

Assuming 82% utilization in shrimp feed (new capacity) and 105%

utilization in shrimp processing along with margins slightly below previous

peak levels, we arrive at an EPS estimate of INR 165 for FY20. We assign

20x P/E and arrive at target price of INR 3,306.

Bull

22x FY20E EPS INR 4,008

Assuming 82% utilization in shrimp feed (new capacity) and 150%

utilization in shrimp processing (addition of capacity), we arrive at an EPS

estimate of INR182 for FY20. We assign 22x P/E and arrive at target price

of INR4,008.

Base

20x FY20E EPS INR 3,306

Assuming 82% utilization in shrimp feeds (new capacity) and 105%

utilization in shrimp processing along with margin slightly below previous

peak levels, we arrive at EPS estimate of INR165 for FY20. We assign 20x

P/E and arrive at target price of INR3,306.

Bear

18x FY20E EPS INR 2,423

Assuming 77% utilisation in shrimp feed (new capacity) and 105%

utilization in shrimp processing along with margin slightly below previous

peak levels and inability to increase prices of feeds further, we arrive at

EPS estimate of INR135 for FY20. We assign 18x P/E and arrive at target

price of INR2,423.

Avanti Feeds Ltd.

4 GWM

Average Daily Turnover (INR cr) Stock Price (CAGR) Sensex, CAGR (%)

3 months 6 months 1 year 1 year 3 years 5 years 10 years 1 year 3 years 5 years 10 years

21 19 19 176% 90% 160% 81% 16% 9% 12% 7%

Bu

sin

ess

Va

lue

Driv

ers

Nature of

Industry Shrimp feed as well as shrimp processing are directly related to shrimp production in India.

Opportunity Size Avanti has 43% market share within the shrimp feed space, which is estimated at INR8,500cr. The

company is also present within the process space, which is pegged at INR 26,000 cr. Both the segments

are estimated to clock 20% growth in ensuing years.

Capital

Allocation

The company’s 4,25,000MT feed plant is running at full capacity, following which it has added

capacity of 1,75,000 MT for INR50cr. Avanti has also added 15,000MT shrimp processing capacity at a

cost of INR120cr.

Predictability Marine Products Export Development Authority (MPEDA) has an aggressive target of an output of 1

million MT of shrimp by 2020 from the current 0.6 million MT and export target of USD10bn by 2022.

Sustainability Leadership in the domestic market provides high sustainability as it’s a brand built on trust and a framer

rarely shifts his feed, as it risks his crop. Also, he will lose the company’s valuable after-sales service.

Disproportionate

Future An exceptional brand built on trust over the years will propel Avanti going ahead. The company in the

past has shown potential to grow at twice the industry rate.

Business

Strategy &

Planned

Initiatives

Avanti is focusing on processing business by setting up a huge capacity and tying up with Thai Union.

Also, it will continue to focus on profitable growth as reflected in the past as well within the feeds

business.

Near Term

Visibility Healthy industry tailwinds coupled with rising demand for shrimp augur well for the company.

Long Term

Visibility Increase in India’s international market share, along with improvement in value added products and

cost reduction drive will fuel Avanti’s top line and profitability going forward.

Avanti Feeds Ltd.

5 GWM

Focus Charts – Story in a nutshell

Highest ROCE in the industry Largest market share within the feeds business

Largest capacity within feeds One of the Largest capacity with Processing

Growth of 25% CAGR within shrimp feeds Growth of 91% CAGR within shrimp processing

Source: Company, Edelweiss Investment Research

20%23%

35%

25%

50%

0%

10%

20%

30%

40%

50%

60%

Farming Processing Value

Addition

Feeds Avanti

ROCE of various segments

43%

67%

Marketshare

Avanti Feeds Rest

600

300

140 125 110 90 70

Av

an

ti F

ee

ds

Gro

we

ll Fe

ed

s

BM

R G

rou

p

De

vi Se

afo

od

s

Wa

terb

ase

Ca

rgill

Go

dre

j A

gro

ve

t

Feed Capacity of Various Players ‘000 MT

19 20

15

28

17

4

8

23D

ev

i Se

afo

od

s

BM

R g

rou

p

Ap

ex F

roze

n F

oo

ds

Ne

kka

nti S

ea

foo

ds

Sa

nd

hya

Ma

rin

es

Wa

terb

ase

IFB

Ag

ro

Av

an

ti f

ee

ds

Shrimp Processing Capacity ‘000 MT

2346

2880

3626

4614

FY17 FY18E FY19E FY20E

Shrimp Feeds

246

689

1337

1702

FY17 FY18E FY19E FY20E

Shrimps Processing

Avanti Feeds Ltd.

6 GWM

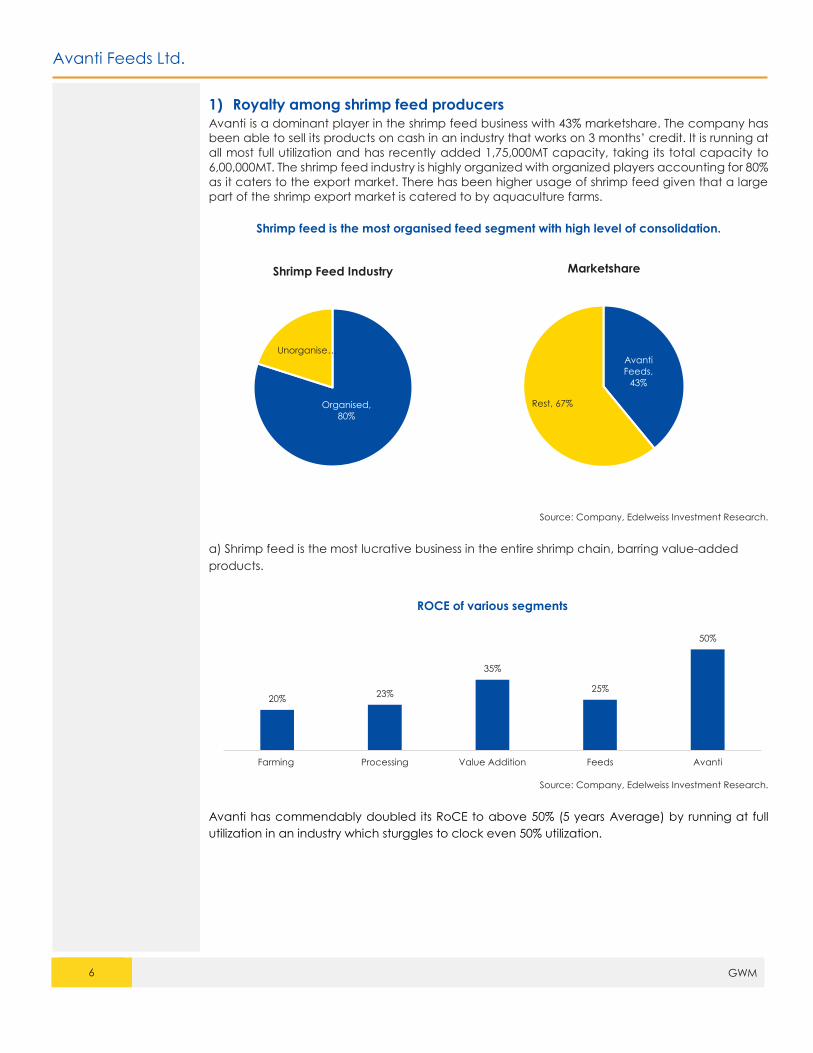

1) Royalty among shrimp feed producers

Avanti is a dominant player in the shrimp feed business with 43% marketshare. The company has

been able to sell its products on cash in an industry that works on 3 months’ credit. It is running at

all most full utilization and has recently added 1,75,000MT capacity, taking its total capacity to

6,00,000MT. The shrimp feed industry is highly organized with organized players accounting for 80%

as it caters to the export market. There has been higher usage of shrimp feed given that a large

part of the shrimp export market is catered to by aquaculture farms.

Shrimp feed is the most organised feed segment with high level of consolidation.

Source: Company, Edelweiss Investment Research.

a) Shrimp feed is the most lucrative business in the entire shrimp chain, barring value-added

products.

Source: Company, Edelweiss Investment Research.

Avanti has commendably doubled its RoCE to above 50% (5 years Average) by running at full

utilization in an industry which sturggles to clock even 50% utilization.

Organised,

80%

Unorganise…

Shrimp Feed Industry

Avanti

Feeds,

43%

Rest, 67%

Marketshare

20%23%

35%

25%

50%

Farming Processing Value Addition Feeds Avanti

ROCE of various segments

Avanti Feeds Ltd.

7 GWM

b) Largest player

The industry is dominated by two giants—Avanti and CP Aqua Feeds, a Thailand-based company.

Apart from these, other players are Waterbase, BMR Group, Godrej Agrovet, Cargill, Growell

Feeds and Devi Seafoods. The total shrimp feed industry was pegged at ~1.2MMT in FY17 with

capacity at about 2.2 MMT.

Source: Company, Edelweiss Investment Research.

c) Lowest FCR

Quality and consistency are key to success of feed manufacture. The base of judging a feed is its

Feed Conversation Ratio (FCR), normal feed has an FCR lower than 1.5x. FCR means how much

of the feed leads to a gram increase in the weight of shrimp; FCR is of prime importance for judging

feed quality; more effective feeds will have a lower FCR. While normal feed has an FCR of less

than 1.5x, Avanti’s is the lowest at 1.2x.

Source: Company, Edelweiss Investment Research.

d) Trusted product

A farmer needs to trust the feed company as wrong or inconsistent feed could lead to death of

shrimp and loss of the entire crop & investment made by the farmer. Once a farmer trusts a feed,

he does not normally shift to another alternative.

Avanti has gained farmers’ trust by engaging with them over time and assisting them in their

farming. The company has set up 12 labs across India, where famers can check their soil and

water samples. It has also set up a special team, Technical Assistance After Sales Service (TASS),

which comprises fisheries graduates. TASS teams visit farmers frequently and extend them

technical assistance; the team’s ultimate objective is best results for farmers. Currently, Avanti has

identified another loophole, which is bad quality seeds. To counter this problem, the company is

setting up a hatchery to provide good quality seeds to farmers.

The company’s products are perceived as premium because of which it has been able to do

cash business in a segment that traditionally works on 3 months’ credit.

600

300

140 125 110 90 70

Avanti Feeds Growell Feeds BMR Group Devi Seafoods Waterbase Cargill Godrej Agrovet

Feed Capacity of Various Players ‘000 MT

1.5

1.2

Normal Feeds

Avanti Feeds

Lowest FCR in the Industry.

Avanti Feeds Ltd.

8 GWM

Source: Company, Edelweiss Investment Research.

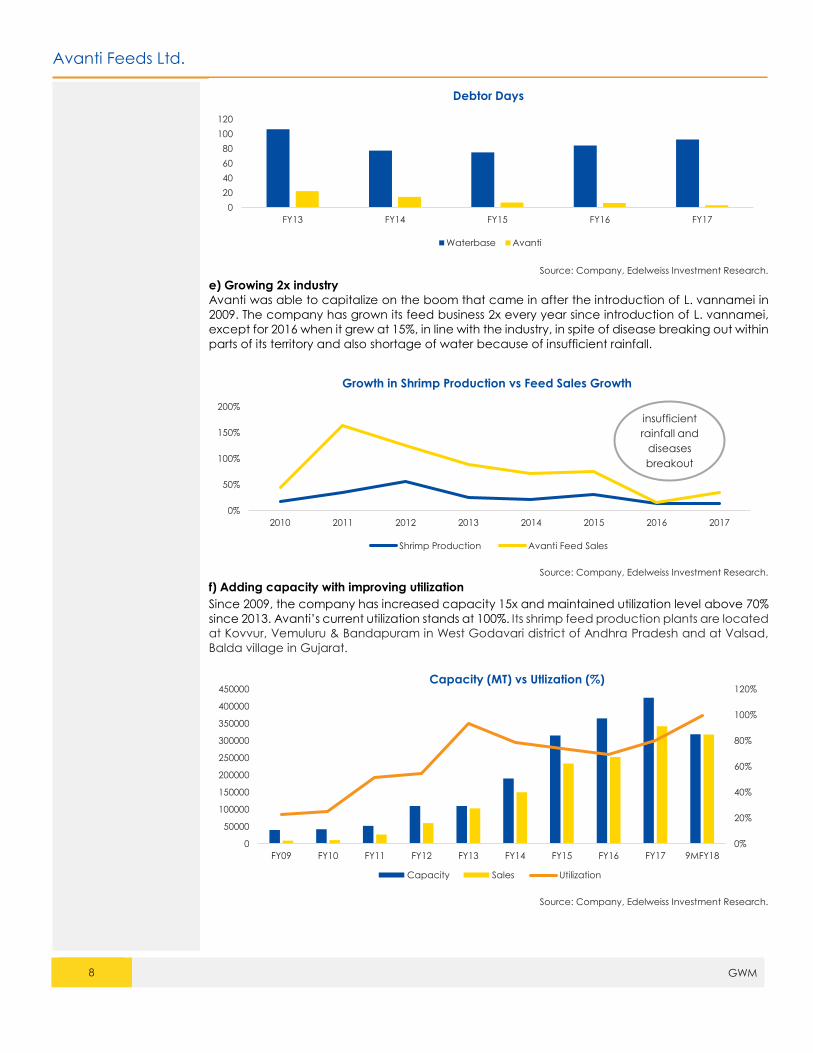

e) Growing 2x industry

Avanti was able to capitalize on the boom that came in after the introduction of L. vannamei in

2009. The company has grown its feed business 2x every year since introduction of L. vannamei,

except for 2016 when it grew at 15%, in line with the industry, in spite of disease breaking out within

parts of its territory and also shortage of water because of insufficient rainfall.

Source: Company, Edelweiss Investment Research.

f) Adding capacity with improving utilization

Since 2009, the company has increased capacity 15x and maintained utilization level above 70%

since 2013. Avanti’s current utilization stands at 100%. Its shrimp feed production plants are located

at Kovvur, Vemuluru & Bandapuram in West Godavari district of Andhra Pradesh and at Valsad,

Balda village in Gujarat.

Source: Company, Edelweiss Investment Research.

0

20

40

60

80

100

120

FY13 FY14 FY15 FY16 FY17

Debtor Days

Waterbase Avanti

0%

50%

100%

150%

200%

2010 2011 2012 2013 2014 2015 2016 2017

Growth in Shrimp Production vs Feed Sales Growth

Shrimp Production Avanti Feed Sales

insufficient

rainfall and

diseases

breakout

0%

20%

40%

60%

80%

100%

120%

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 9MFY18

Capacity (MT) vs Utlization (%)

Capacity Sales Utilization

Avanti Feeds Ltd.

9 GWM

g) Estimated sales

We estimate 25% CAGR in feed sales in coming years with sales touching INR4,614cr in 2020.

Source: Edelweiss Investment Research.

2346

2880

3626

4614

FY17 FY18E FY19E FY20E

Estimated Sales Growth (INR cr)

Avanti Feeds Ltd.

10 GWM

2) Augmenting capacity to become largest shrimp processer in India

Avanti also has a shrimp processing capacity of 7,000MT and in Q3FY18 commissioned a 15,000MT

facility, rendering it one of the largest capacities in the country. In Q3, the company has already

clocked 150% of FY17 volumes with still one quarter to go.

As of 9MFY18, shrimp processing contributed 18% to revenue, which we expect to be 27% by 2020

Source: Company, Edelweiss Investment Research.

a) The industry is led by Devi Fisheries and Devi Seafoods, closely followed by other players, BMR

Group, Apex Frozen Foods, Nekkanti Seafoods, Sandhya Marines, Waterbase, IFB Agro and

now Avanti. Avanti now boasts of one of the largest capacities in the industry.

Source: Company, Edelweiss Investment Research.

85% 86% 91%81% 73% 73%

15% 14% 9%19% 27% 27%

0%

20%

40%

60%

80%

100%

120%

FY15 FY16 FY17 FY18E FY19E FY20E

Revenue Mix

Feeds Processing

19 20

15

28

17

4

8

23

Devi

Seafoods

BMR group Apex Frozen

Foods

Nekkanti

Seafoods

Sandhya

Marines

Waterbase IFB Agro Avanti feeds

Shrimp Processing Capacity ‘000 MT

Avanti Feeds Ltd.

11 GWM

b) Avanti has been in the shrimp processing business for more than a decade and has been

growing steadily. We expect the company’s output to rise significantly riding aggerisve

investments.

Source: Company, Edelweiss Investment Research.

c) Pact with Thai Union: Match made in heaven

Avanti has demergered its processing business into a subsidary Avanti Frozen Foods (AFFPL) in

order to improve business efficacy and establish global brand equity of its shrimp processing

business. Thai Union has taken 40% stake in the company. Thai Union is the largest seafood

company in the world, which operates across the globe and has created dozens of successful

brands. It has the requisite technical expertise to manufacture high value-added products and

the tie up with Avanti gives the latter access to Thai Union’s expertise.

Source: Company, Edelweiss Investment Research.

0

5000

10000

15000

20000

25000

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18E FY19E FY20E

Shrimps processed (MT)

Thai Union Plc ,

40%Avanti Feeds,

60%

Avanti Frozen Foods Private Limited

Avanti Feeds Ltd.

12 GWM

d) Investment in the future

Avanti has invested INR120cr in a separate facility of 15,000 MT which is capable of making high

value-added partially or completely cooked products.

Source: Company, Edelweiss Investment Research.

Avanti Feeds Ltd.

13 GWM

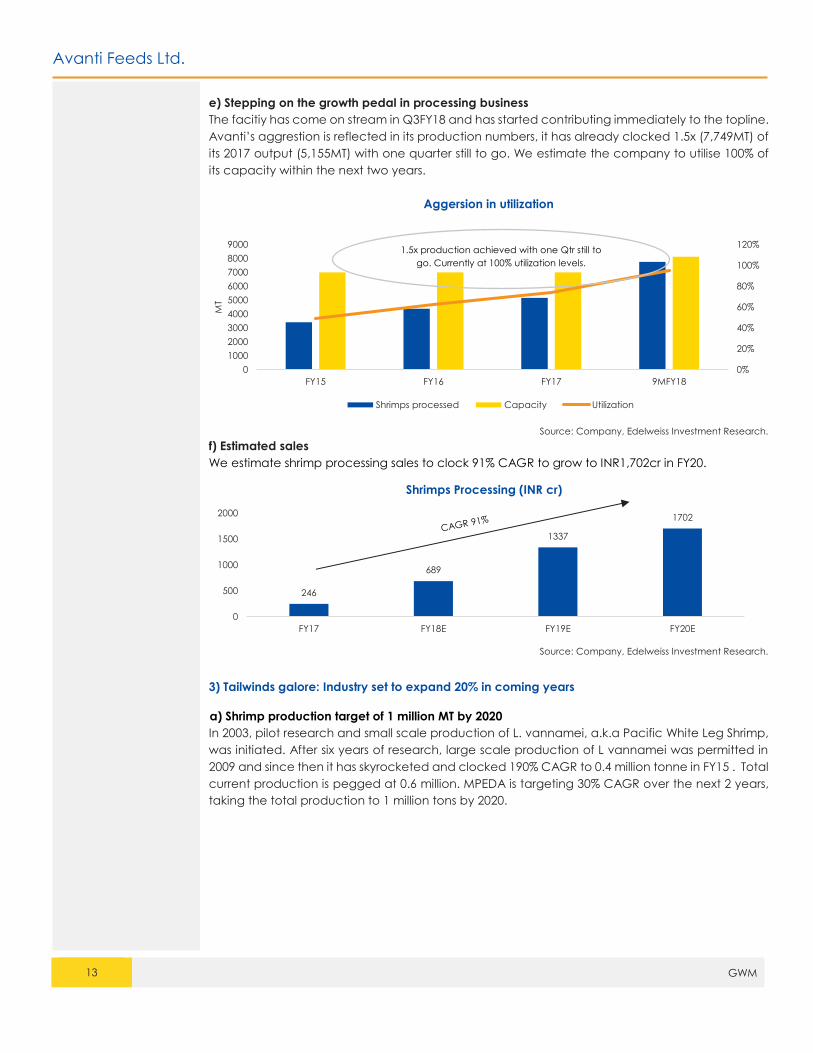

e) Stepping on the growth pedal in processing business

The facitiy has come on stream in Q3FY18 and has started contributing immediately to the topline.

Avanti’s aggrestion is reflected in its production numbers, it has already clocked 1.5x (7,749MT) of

its 2017 output (5,155MT) with one quarter still to go. We estimate the company to utilise 100% of

its capacity within the next two years.

Aggersion in utilization

Source: Company, Edelweiss Investment Research.

f) Estimated sales

We estimate shrimp processing sales to clock 91% CAGR to grow to INR1,702cr in FY20.

Source: Company, Edelweiss Investment Research.

3) Tailwinds galore: Industry set to expand 20% in coming years

a) Shrimp production target of 1 million MT by 2020

In 2003, pilot research and small scale production of L. vannamei, a.k.a Pacific White Leg Shrimp,

was initiated. After six years of research, large scale production of L vannamei was permitted in

2009 and since then it has skyrocketed and clocked 190% CAGR to 0.4 million tonne in FY15 . Total

current production is pegged at 0.6 million. MPEDA is targeting 30% CAGR over the next 2 years,

taking the total production to 1 million tons by 2020.

0%

20%

40%

60%

80%

100%

120%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

FY15 FY16 FY17 9MFY18

MT

Shrimps processed Capacity Utilization

246

689

1337

1702

0

500

1000

1500

2000

FY17 FY18E FY19E FY20E

Shrimps Processing (INR cr)

1.5x production achieved with one Qtr still to

go. Currently at 100% utilization levels.

Avanti Feeds Ltd.

14 GWM

b) Budget allots INR10,000cr potential funds for aquaculture

The government in Budget 2019 has allocated a dedicated fund of INR10,000cr to develop

fisheries, aquaculture and animal husbandry. Investments have started pouring in already with a

decision to set up a world-class aquatic quarantine facility and a brood-stock multiplication

centre at Bangarammapeta in Andhra Pradesh at a cost of INR68cr. The twin projects will help in

supplying superior quality L. vannamei (white-leg shrimp) brood-stock to hatchery operators and

specific pathogen-free seeds, the most significant input for shrimp production.

Currently, hatchery producers import brood-stock and avail the quarantine facility at MPEDA-Rajiv

Gandhi Centre for Aquaculture in Chennai. MPEDA-RGCA unit at Mangamarripeta gets specific

pathogen-free post-larvae from Oceanic Institute, Hawaii, which are quarantined in Chennai and

reared for two months into brood-stock and supplied to hatchery operators. The existing facility at

Mangamarripeta is unable to meet the burgeoning demand for L.vannamei brood-stock of

hatcheries. The Bangarammapeta project will get technical support from MPEDA and RGCA. The

projects will be completed on fast-track mode in an area of 30 acres allotted by the government.

c) Exports

i) Export target of USD10bn by FY22

India’s seafood exports have been growing significantly over the past five years with it exporting

seafood worth USD5.78bn in FY16-17. Provisional export figures during the year have shown an

increase in exports from a year ago. Given the trend, export earnings are estimated to cross

USD6bn during the current fiscal.

Industry leaders led by MPEDA and experts have deliberated on policies, market trends,

technology and roadmaps to achieve an export target of USD10bn by FY22. During the India

International Seafood Show (IISS) in January, MPEDA inked a MoU with Coop, Switzerland—a

supermarket chain with over 2,500 stores—for developing organic seafood supply systems in India

to be marketed through their stores. Around 3,000 delegates and more than 2,000 visitors from

India and abroad, including the US, UK, Spain, Japan, Australia, China, Vietnam, South Korea,

Thailand, Malaysia and the Middle East, participated in the event that had safe and sustainable

seafood from India as its focal theme.

ii) Export market: Shrimps global

The global export market for shrimp stood at USD25.5bn as of FY16 clocking CAGR of 8% over FY09-

16. Japan was the top importer of shrimp and China the top exporter. However, over the past

decade, US has become the top importer, followed by EU, Vietnam and China. Vietnam is a net

exporter of shrimp; it imports raw products and exports them post value addition.

Source: UN.Comtrade, Edelweiss Investment Research.

USA, 26%

Vietnam,

12%

Japan,

10%

China, 8%

EU, 23%

Rest, 21%

Top Shrimp Importing Countries - Marketshare 2017

Avanti Feeds Ltd.

15 GWM

iii) Export market: India

The shrimp export market was pegged at USD3.8bn in FY17 (in value terms), accounting for ~65%

of the overall seafood exports from India; it stood at 434,484MT (in volume terms) in FY17,

accounting for ~38% of the overall seafood export volumes during the year. These figures indicate

the comparatively higher realisations earned by shrimp verses other major Indian seafood export

products.

Source: UN.Comtrade, Edelweiss Investment Research.

Overall, shrimp exports clocked ~17% CAGR between FY09 and FY16. During the corresponding

period, while volumes grew ~10%, realisations grew ~6%. Shrimps account for 1.3% of India’s

exports.

Source: MPEDA, Edelweiss Investment Research.

A major factor which aided India’s growth was the spread of EMS disease in SEA aquaculture

farms, with major shrimp exporters Vietnam and Thailand being impacted the most; this benefited

India. The sudden spurt in demand helped Indian exporters, who had the necessary capability

and capacity to export the requisite quantity, thereby clocking superior realisations. Additionally,

increased adoption of Pacific White Leg Shrimp helped significantly increase production

capacities.

2009 2016

Indian Exports ‘000 MT-USD

USA Vietnam Japan China EU Rest

140 MT-0.8 USD Bn

430 MT-3.6 USD Bn

0

1000

2000

3000

4000

5000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Shrimp Exports US$ Mn

Avanti Feeds Ltd.

16 GWM

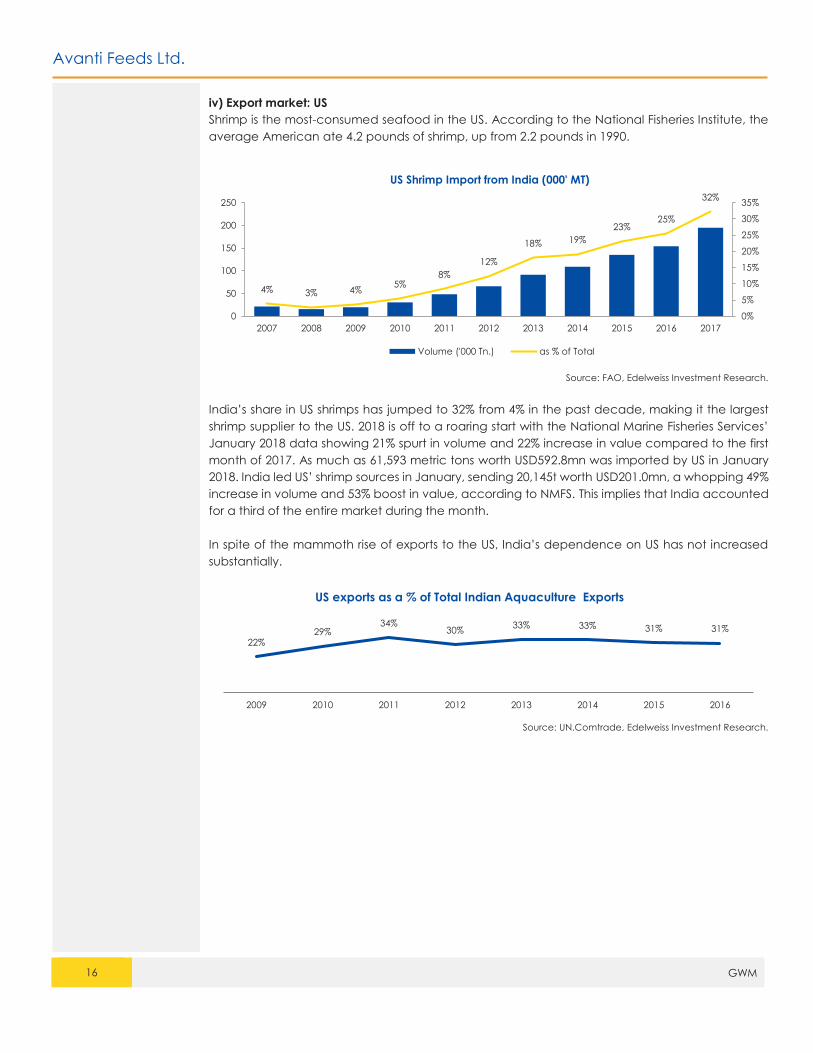

iv) Export market: US

Shrimp is the most-consumed seafood in the US. According to the National Fisheries Institute, the

average American ate 4.2 pounds of shrimp, up from 2.2 pounds in 1990.

Source: FAO, Edelweiss Investment Research.

India’s share in US shrimps has jumped to 32% from 4% in the past decade, making it the largest

shrimp supplier to the US. 2018 is off to a roaring start with the National Marine Fisheries Services’

January 2018 data showing 21% spurt in volume and 22% increase in value compared to the first

month of 2017. As much as 61,593 metric tons worth USD592.8mn was imported by US in January

2018. India led US’ shrimp sources in January, sending 20,145t worth USD201.0mn, a whopping 49%

increase in volume and 53% boost in value, according to NMFS. This implies that India accounted

for a third of the entire market during the month.

In spite of the mammoth rise of exports to the US, India’s dependence on US has not increased

substantially.

Source: UN.Comtrade, Edelweiss Investment Research.

4% 3% 4%5%

8%

12%

18% 19%

23%25%

32%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

US Shrimp Import from India (000' MT)

Volume ('000 Tn.) as % of Total

22%29%

34%30%

33% 33% 31% 31%

2009 2010 2011 2012 2013 2014 2015 2016

US exports as a % of Total Indian Aquaculture Exports

Avanti Feeds Ltd.

17 GWM

v) Export Market- Japan

Japan is the second - largest fish and seafood importer in the world and the top market in Asia. In

the early days of shrimp exports, India was heavily dependent on Japan for its exports. Vietnam is

the largest supplier of shrimp to Japan. Although Japan has fallen in the ranks of top importers of

shrimp, India’s export to the country have been steady and Japan’s dependence on India has

risen to almost a third of there demand.

Source: UN.Comtrade, Edelweiss Investment Research.

While earlier India was dependent on Japan for more than half of its exports, currently the

dependence is down to less than one tenth of the country’s exports.

Source: UN.Comtrade, Edelweiss Investment Research.

16%18% 17%

20%

23%25%

26% 27%

0%

5%

10%

15%

20%

25%

30%

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2010 2011 2012 2013 2014 2015 2016 2017*

Japan Shrimp Import from India ('000 MT)

Volume ('000 M.T) as % of Total Japan imports

21%

23%

19%

14%

11%9% 10%

9%

2009 2010 2011 2012 2013 2014 2015 2016

Japan exports as a % of Total Indian Aquaculture Exports

Avanti Feeds Ltd.

18 GWM

vi) Export market: EU

EU is the second-largest shrimp importer in the world. It was the largest market for sometime, before

being overtaken by US. India was dependent on EU for its exports, but that is not the case

anymore. Vietnam is the largest supplier of shrimp to EU by making full use of the Vietnam-EU Free

Trade Agreement. Although India is not the top exporter to EU, it has been able to steadily increase

volumes as well as share in the market.

Source: UN.Comtrade, Edelweiss Investment Research.

While earlier India was dependent on EU for one third of its trade, currently the dependence is

down to less than half of that.

Source: UN.Comtrade, Edelweiss Investment Research.

10% 10%12%

15% 16% 15%

0%

5%

10%

15%

20%

0

20

40

60

80

100

2010 2011 2012 2014 2015 2016

EU Shrimp Import from India ('000 MT)

Volume ('000 M.T) as % of Total EU imports

33%

25%23% 23%

18% 19% 18%

15%

2009 2010 2011 2012 2013 2014 2015 2016

UK, Netherlands, Belgium, France, Italy, Spain, Portugal and Germany

exports as a % of Total Indian Aquaculture Exports

Avanti Feeds Ltd.

19 GWM

vii) Export market: Vietnam

Vietnam is not as gifted as India with the requirements of shrimp farming, but it is very gifted with

bilateral trade agreements. Although Vietnam is India’s biggest competitor, it is completely

dependent on India for supply of shrimp, about three fourth requirement is met by India. Though

Vietnam was ahead on the learning curve and had mastered value-added products, India is

catching up fast.

Source: UN.Comtrade, Edelweiss Investment Research.

Although India is not the top exporter to EU and Japan, it is the top exporter to its top exporter.

Source: UN.Comtrade, Edelweiss Investment Research.

8%3% 6% 9%

66%74%

0%

20%

40%

60%

80%

0

10

20

30

40

2007 2008 2009 2010 2013 2015

Vietnam Shrimp Import from India ('000 MT)

Volume ('000 Tn.) as % of Total Vietnam imports

1% 1%

6% 6%

14%15% 16%

21%

2009 2010 2011 2012 2013 2014 2015 2016

Vietnam exports as a % of Total Indian Aquaculture Exports

Avanti Feeds Ltd.

20 GWM

vii) Export market: China – Reshaping global shrimp trade

China was once a large exporter of shrimps and has now become a net importer and is set to

take the centre stage in global shrimp trade.

Source: UN.Comtrade, Edelweiss Investment Research.

China has overtaken Japan as the world’s leading seafood consumer, according to a National

Geographic Study. Chinese middle class is a small percentage of ~32% on an average, but the

number is very large at about 400mn due to the sheer size of the overall Chinese population. In

rural areas too, shrimp has become a common site; as farmers are becoming wealthier, shrimp is

now being consumed regularly even in the countryside. There has been a change in eating habits

too, Chinese traditionally bought only live or fresh head-on shrimp, but now accept HOSO frozen

shrimp.

Shrimp exporting companies in China, like the Guangdong Evergreen Group, have started

focusing on the domestic market rather than exports. Domestic wild seafood is no longer enough

to meet the rising demand.

India already has entered this next emerging market.

Source: UN.Comtrade, Edelweiss Investment Research.

0

50000

100000

150000

200000

250000

2009 2010 2011 2012 2013 2014 2015 2016

China Export vs Import MT

Import Export

3% 2% 3%4%

5%

4%

6%

5%

0%

2%

4%

6%

8%

0

5000

10000

15000

2009 2010 2011 2012 2013 2014 2015 2016

China Shrimp Import from India (‘000 M.T)

('000 M.T) as % of Total China imports

Avanti Feeds Ltd.

21 GWM

Valuation and Peers

Avanti is the leader in shrimp aquaculture in India and is expected to surpass industry growth. We

expect the company to benefit from favourable tailwinds in the sector. Key growth drivers are: 1)

robust growth in the shrimp feeds space with increasing area under cultivation; 2) expansion of

shrimp processing facility with aggressive capacity utilization goals; 3) sustenance of leadership in

the feeds space with continued steady share gains; and 4) targeting the crown of largest shrimp

exporter from India in coming years. We initiate coverage on the stock with ‘BUY’

recommendation, valuing it at 20x FY20E P/E and thus arrive at a target price of INR3,306.

Key indicators FY15 FY16 FY17 FY18E FY19E FY20E

Sales growth

Zeal Aqua Ltd 26% (29.2%) 43.9% NA NA NA

Waterbase Ltd 22% 8% 7% NA NA NA

Apex Frozen

Foods Ltd 17% 1% 16% NA NA NA

Avanti Feeds Ltd 57% 13% 35% 31% 39% 27.3%

EBITDA margins

Zeal Aqua Ltd 6% 8% 5% NA NA NA

Waterbase Ltd 11% 3% 9% NA NA NA

Apex Frozen

Foods Ltd 6% 7% 6% NA NA NA

Avanti Feeds Ltd 10% 11% 12% 21% 19% 19%

PAT margins

Zeal Aqua Ltd 2% 2% 1% NA NA NA

Waterbase Ltd 7% 2% 4% NA NA NA

Apex Frozen

Foods Ltd 3% 3% 4% NA NA NA

Avanti Feeds Ltd 7% 8% 8% 13% 12% 12%

Debt Equity

Zeal Aqua Ltd 2.0 1.8 1.3 NA NA NA

Waterbase Ltd 0.1 0.5 0.5 NA NA NA

Apex Frozen

Foods Ltd 3.1 3.2 3.5 NA NA NA

Avanti Feeds Ltd 0.2 0.0 0.0 0.0 0.0 0.0

RoCE

Zeal Aqua Ltd 27% 18% 11% NA NA NA

Waterbase Ltd 28% 4% 14% NA NA NA

Apex Frozen

Foods Ltd 25% 23% 21% NA NA NA

Avanti Feeds Ltd 61% 57% 53% 73% 62% 56%

PE

Zeal Aqua Ltd 52.3 83.9 123.9 NA NA NA

Waterbase Ltd 59.3 214.8 99.7 NA NA NA

Apex Frozen

Foods Ltd 84.9 80.9 63.9 NA NA NA

Avanti Feeds Ltd 93.8 71.0 51.0 22.9 18.8 14.5

Avanti Feeds Ltd.

22 GWM

Major Milestones

1993Avanti Feeds Limited was founded by Mr. Alluri Venkateswara Rao & Mr. Alluri Indra Kumar

2002Mr.Alluri Indra Kumar took over as Managing Director

2008Thai Union PCL invested in a 14.99 %

2009Invested in 50:50 SPV, Avanti Thai Aqua Feeds Pvt Ltd in Gujarat

2014Feed capacity increased to 1,90,000 Mt

2012Amalgamation of Avanti Thai Aqua Feeds with the company Feed capacity increased to 1,10,000 Mt from 52,000 Mt and Shrimp Processing to 7,000 Mt from 2,720 Mt

2016Feed capacity increased to 3,65,000 Mt

2015Feed capacity increased to 3,15,000 Mt

2017Feed capacity increased to 4,25,000 MtSetup subsidiary Avanti Frozen Foods Private Limited

2018Feed capacity increased to 6,00,000 Mt and shrimp processing to 22,000 Mt

Avanti Feeds Ltd.

23 GWM

Business Overview: Well diversified business

Company description

Avanti is a leader in India’s shrimp industry with 43% marketshare in shrimp feed manufacturing. The company is also

present in shrimp processing. Though a minuscule part of the business uptil now, it has expanded its shrimp processing plant

to 23,000MT, making it one of the largest in the country.

Business Model

The company has 2 segments

1) Shrimp feed

2)Shrimp processing

Strategic Positioning Avanti is the largest player in the shrimp feed segment with 43% market share. The company has aggervise plans

for the shrimp processing business and is envisaged to become leading exporter of shrimps in coming years.

Competitive Edge

Trusted Brand,

Technologically superiar product (feeds),

Strong tie-up with Thai Union,

Presence across India.

Financial Structure Completion of capex will result in high free cashflows of about 900 Cr.

As the company moves into value-added products, margins and return ratios will imporve.

Key Competitors

Feeds - C.P.Feeds, Waterbase, BMR Group, Godrej Agrovet, Cargill, Growell Feeds and Devi Seafoods.

Shrimp Processing - Devi Fisheries, Devi Seafoods, BMR Group, Apex Frozen Foods, Nekkanti Seafoods,

Sandhya Marines, Waterbase and IFB Agro.

Industry Revenue

Drivers Continued demand for shrimps globally.

Shareholder Value

Proposition

Avanti is likely to clock 26% earnings CAGR over FY18 -20E, results an EPS of INR 165 in FY20E. A 20x valuation

can give price target of INR 3306 for the company which gives an upside of 38%

Avanti Feeds Ltd.

24 GWM

Financial Outlook

33% revenue CAGR over FY18E-20E

Susuatined growth in feeds business in conjunction with maturing processing business is likely to

drive revenue growth. Avanti has clocked revenue CAGR of 33% over the past 2 years, which we

estimate it to sustain over FY18E-20E.

Source: UN.Comtrade, Edelweiss Investment Research.

Raw marterial prices to catch up

We estiamte rationalisation of EBITDA margin as raw matariel prices rationalize.

Source: UN.Comtrade, Edelweiss Investment Research.

Processing margins to stabilize

We estimate PAT margin to stabilse at ~12% going forward, although raw matariel prices catch up

in the feeds business, Value Added Products with the processing business will push these margins

higher.

Source: UN.Comtrade, Edelweiss Investment Research.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

FY16 FY17 FY18E FY19E FY20E

Revenue Growth

Revenue

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

FY16 FY17 FY18E FY19E FY20E

EBITDA

EBITDA Margins

0%

2%

4%

6%

8%

10%

12%

14%

0

100

200

300

400

500

600

700

800

FY16 FY17 FY18E FY19E FY20E

PAT

PAT Margins

Avanti Feeds Ltd.

25 GWM

Key Management

Name Designation Profile

Mr. Alluri Indra

Kumar

Chairman & Managing

Director

Mr. Kumar was inducted as Executive Director with the responsibility

to look after shrimp feed manufacturing, processing and exporting of

shrimp in 1993. In 2002, he took over as Managing Director. Mr. Kumar,

with his varied experience, has been instrumental in the development

of shrimp culture and processing by bringing in latest technology in

feed manufacture and also development of value- added shrimp

products for exports. He enhanced Avanti's technical and marketing

capabilities by bringing on board Thai Union. He is a B.E. in Chemical

Engineering from the University of Bangalore.

Mr.

C.Ramachandra

Rao

Joint Managing Director,

CFO & CS

Mr. Rao is a qualified Chartered Accountant, Company Secretary &

Law Graduate and has experience of over 25 years in government

and public sector undertakings. He has been instrumental in the

growth of Avanti.

Key Risks

Break out of diesease: The government of India has taken various steps to prevent spread of disease (like in Thailand),

because of which there has never been a wide spread disease in India. Some major steps are: only authorised hatcheries

allowed to import broodstock, broodstock can only be bought from an approved seller, once brought into the country

the broodstock is quarantined in Chennai and checked for diesease, if infected it is destroyed. Apart from these measures,

there has been countinuous education of farmers to prevent diseases.

Dependency on rainfall: Due to India’s vast coastline, chances of entire area under cultivation being affected by lack of

rainfall remains low.

Threat of unfriendly trade polices: Currently, the anti-dumping in US on Indian shrimps is 2.34%, which is low compared to

25.76% on shrimps from Vietnam.

Avanti Feeds Ltd.

26 GWM

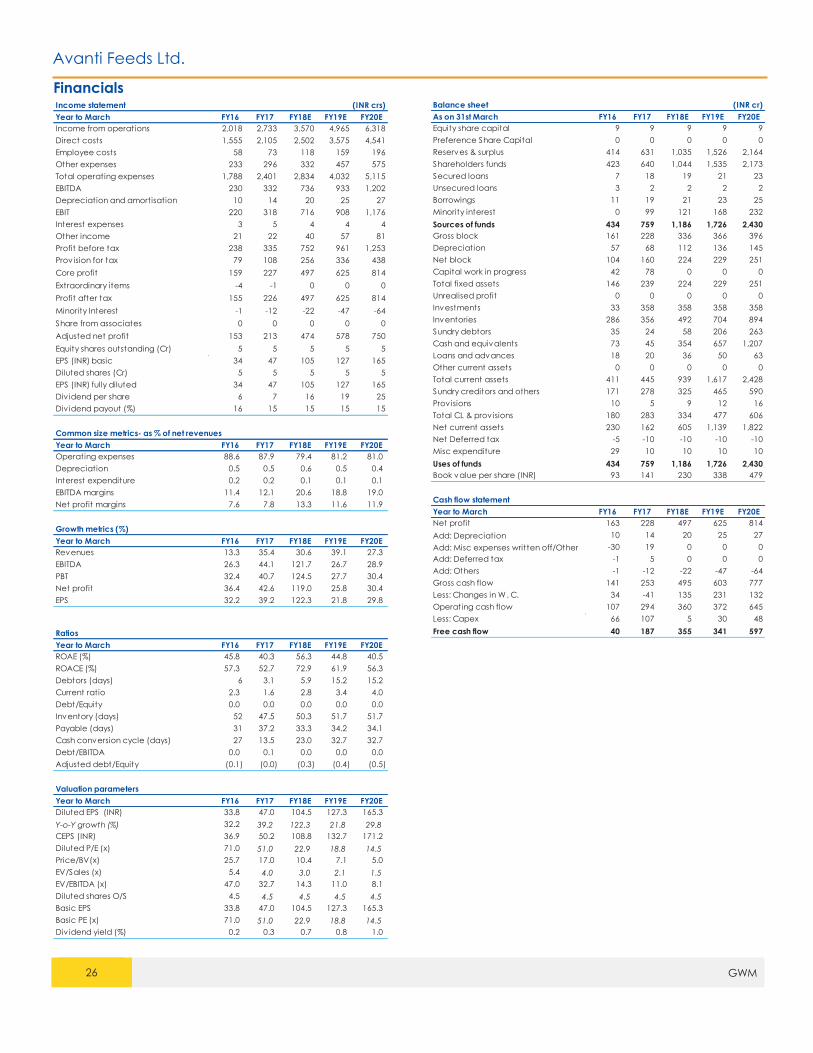

Financials

Income statement (INR crs)

Year to March FY10FY11 FY16 FY17 FY18E FY19E FY20E

Income from operations 2,018 2,733 3,570 4,965 6,318

Direct costs 1,555 2,105 2,502 3,575 4,541

Employee costs 58 73 118 159 196

Other expenses 233 296 332 457 575

Total operating expenses 1,788 2,401 2,834 4,032 5,115

EBITDA 230 332 736 933 1,202

Depreciation and amortisation 10 14 20 25 27

EBIT 220 318 716 908 1,176

Interest expenses 3 5 4 4 4

Other income 21 22 40 57 81

Profit before tax 238 335 752 961 1,253

Provision for tax 79 108 256 336 438

Core profit 159 227 497 625 814

Extraordinary items -4 -1 0 0 0

Profit after tax 155 226 497 625 814

Minority Interest -1 -12 -22 -47 -64

Share from associates 0 0 0 0 0

Adjusted net profit 153 213 474 578 750

Equity shares outstanding (Cr) 5 5 5 5 5

EPS (INR) basic 34 47 105 127 165

Diluted shares (Cr) 5 5 5 5 5

EPS (INR) fully diluted 34 47 105 127 165

Div idend per share 6 7 16 19 25

Div idend payout (%) 16 15 15 15 15

Common size metrics- as % of net revenues

Year to March FY10FY11 FY16 FY17 FY18E FY19E FY20E

Operating expenses 88.6 87.9 79.4 81.2 81.0

Depreciation 0.5 0.5 0.6 0.5 0.4

Interest expenditure 0.2 0.2 0.1 0.1 0.1

EBITDA margins 11.4 12.1 20.6 18.8 19.0

Net profit margins 7.6 7.8 13.3 11.6 11.9

Growth metrics (%)

Year to March FY10FY11 FY16 FY17 FY18E FY19E FY20E

Revenues 13.3 35.4 30.6 39.1 27.3

EBITDA 26.3 44.1 121.7 26.7 28.9

PBT 32.4 40.7 124.5 27.7 30.4

Net profit 36.4 42.6 119.0 25.8 30.4

EPS 32.2 39.2 122.3 21.8 29.8

Ratios

Year to March FY10FY11 FY16 FY17 FY18E FY19E FY20E

ROAE (%) 45.8 40.3 56.3 44.8 40.5

ROACE (%) 57.3 52.7 72.9 61.9 56.3

Debtors (days) 6 3.1 5.9 15.2 15.2

Current ratio 2.3 1.6 2.8 3.4 4.0

Debt/Equity 0.0 0.0 0.0 0.0 0.0

Inventory (days) 52 47.5 50.3 51.7 51.7

Payable (days) 31 37.2 33.3 34.2 34.1

Cash conversion cycle (days) 27 13.5 23.0 32.7 32.7

Debt/EBITDA 0.0 0.1 0.0 0.0 0.0

Adjusted debt/Equity (0.1) (0.0) (0.3) (0.4) (0.5)

Valuation parameters

Year to March FY10FY11 FY16 FY17 FY18E FY19E FY20E

Diluted EPS (INR) 33.8 47.0 104.5 127.3 165.3

Y-o-Y growth (%) 32.2 39.2 122.3 21.8 29.8

CEPS (INR) 36.9 50.2 108.8 132.7 171.2

Diluted P/E (x) 71.0 51.0 22.9 18.8 14.5

Price/BV(x) 25.7 17.0 10.4 7.1 5.0

EV/Sales (x) 5.4 4.0 3.0 2.1 1.5

EV/EBITDA (x) 47.0 32.7 14.3 11.0 8.1

Diluted shares O/S 4.5 4.5 4.5 4.5 4.5

Basic EPS 33.8 47.0 104.5 127.3 165.3

Basic PE (x) 71.0 51.0 22.9 18.8 14.5

Div idend yield (%) 0.2 0.3 0.7 0.8 1.0

Balance sheet (INR cr)

As on 31st March FY10FY11 FY16 FY17 FY18E FY19E FY20E

Equity share capital 9 9 9 9 9

Preference Share Capital 0 0 0 0 0

Reserves & surplus 414 631 1,035 1,526 2,164

Shareholders funds 423 640 1,044 1,535 2,173

Secured loans 7 18 19 21 23

Unsecured loans 3 2 2 2 2

Borrowings 11 19 21 23 25

Minority interest 0 99 121 168 232

Sources of funds 434 759 1,186 1,726 2,430

Gross block 161 228 336 366 396

Depreciation 57 68 112 136 145

Net block 104 160 224 229 251

Capital work in progress 42 78 0 0 0

Total fixed assets 146 239 224 229 251

Unrealised profit 0 0 0 0 0

Investments 33 358 358 358 358

Inventories 286 356 492 704 894

Sundry debtors 35 24 58 206 263

Cash and equivalents 73 45 354 657 1,207

Loans and advances 18 20 36 50 63

Other current assets 0 0 0 0 0

Total current assets 411 445 939 1,617 2,428

Sundry creditors and others 171 278 325 465 590

Provisions 10 5 9 12 16

Total CL & provisions 180 283 334 477 606

Net current assets 230 162 605 1,139 1,822

Net Deferred tax -5 -10 -10 -10 -10

Misc expenditure 29 10 10 10 10

Uses of funds 434 759 1,186 1,726 2,430

Book value per share (INR) 93 141 230 338 479

Cash flow statement

Year to March FY10FY11 FY16 FY17 FY18E FY19E FY20E

Net profit 163 228 497 625 814

Add: Depreciation 10 14 20 25 27

Add: Misc expenses written off/Other -30 19 0 0 0

Add: Deferred tax -1 5 0 0 0

Add: Others -1 -12 -22 -47 -64

Gross cash flow 141 253 495 603 777

Less: Changes in W. C. 34 -41 135 231 132

Operating cash flow 107 294 360 372 645

Less: Capex 66 107 5 30 48

Free cash flow 40 187 355 341 597

27 GWM

Annexure

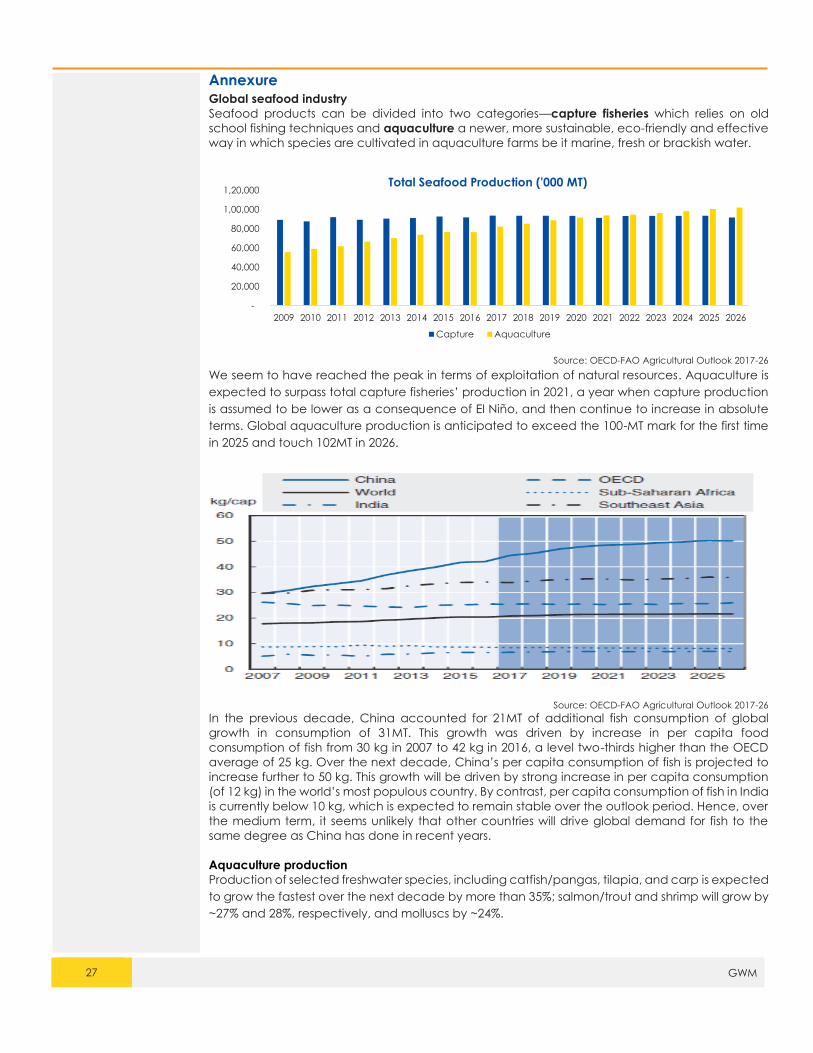

Global seafood industry

Seafood products can be divided into two categories—capture fisheries which relies on old

school fishing techniques and aquaculture a newer, more sustainable, eco-friendly and effective

way in which species are cultivated in aquaculture farms be it marine, fresh or brackish water.

Source: OECD-FAO Agricultural Outlook 2017-26

We seem to have reached the peak in terms of exploitation of natural resources. Aquaculture is

expected to surpass total capture fisheries’ production in 2021, a year when capture production

is assumed to be lower as a consequence of El Niño, and then continue to increase in absolute

terms. Global aquaculture production is anticipated to exceed the 100-MT mark for the first time

in 2025 and touch 102MT in 2026.

Source: OECD-FAO Agricultural Outlook 2017-26

In the previous decade, China accounted for 21MT of additional fish consumption of global

growth in consumption of 31MT. This growth was driven by increase in per capita food

consumption of fish from 30 kg in 2007 to 42 kg in 2016, a level two-thirds higher than the OECD

average of 25 kg. Over the next decade, China’s per capita consumption of fish is projected to

increase further to 50 kg. This growth will be driven by strong increase in per capita consumption

(of 12 kg) in the world’s most populous country. By contrast, per capita consumption of fish in India

is currently below 10 kg, which is expected to remain stable over the outlook period. Hence, over

the medium term, it seems unlikely that other countries will drive global demand for fish to the

same degree as China has done in recent years.

Aquaculture production

Production of selected freshwater species, including catfish/pangas, tilapia, and carp is expected

to grow the fastest over the next decade by more than 35%; salmon/trout and shrimp will grow by

~27% and 28%, respectively, and molluscs by ~24%.

-

20,000

40,000

60,000

80,000

1,00,000

1,20,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Total Seafood Production ('000 MT)

Capture Aquaculture

28 GWM

Indian seafood industry

Fishing in India is a major industry in coastal states, employing over 14mn . According to the Food

and Agriculture Organization (FAO) of the United Nations, fish production has increased more

than 10x since 1947 and doubled between 1990 and 2010.

India has 8,129km of marine coastline, 3,827 fishing villages and 1,914 traditional fish landing

centers. Its fresh water resources consist of 195,210km of rivers & canals, 2.9mn hectares of minor

& major reservoirs, 2.4mn hectares of ponds & lakes, and ~0.8mn hectares of flood

plain wetlands & water bodies.

Fishing in India employs about 14.5mn million people. To harvest the economic benefits from

fishing, India has an exclusive economic zone, stretching 200 nautical miles (370 km) into

the Indian Ocean, encompassing more than 2mn sq km. In addition to this marine zone, it has

~14,000km² of brackish water available for aquaculture, ~16,000km² of freshwater lakes, ponds &

swamps and nearly 64,000km of rivers & streams.

Fish production rose from 800,000tons in FY50 to 4.1mn tons in the early 1990s. From 1990 through

2010, India’s fish industry accelerated, reaching a total marine and freshwater fish production of

~8mn MT.

In 2006, the government initiated a dedicated organization focused on fisheries under its Ministry

of Agriculture. Special efforts have been made to promote extensive and intensive inland fish

farming, modernize coastal fisheries and encourage deep-sea fishing through joint ventures.

These efforts led to a more than 4x increase in coastal fish production from 520,000tons in FY50 to

3.35mn MT in FY13. The increase in inland fish production was even more dramatic, increasing

almost 8x from 218,000 tons in FY50 to 6.10mn tons in FY13. Between 1990 and 2007, fish production

in India has grown at a higher rate than food grains, milk, eggs and other food items.

Fisheries research and training institutions are supported by central and state governments. The

principal fisheries research institutions which operate under the Indian Council of Agricultural

Research are the Fishery Survey of India, Central Marine Fisheries Research Institute at Kochi,

the Central Institute of Fisheries Education at Mumbai, the Central Inland Fisheries Institute

at Barrackpore in West Bengal, Central Fisheries Corporation at Kolkata, the Central Institute of

Coastal Engineering for Fisheries at Bangalore and the Central Institute of Fisheries

Technology at Kochi in Kerala. The Government of India established the National Fisheries

Development Board in 2006 with its headquarters in Hyderabad. The Central Institute of Fisheries

Nautical and Engineering Training with facilities in Chennai, Kochi and Vishakapatnam trains

operators of deep-sea fishing vessels and technicians for shore establishments. Fisheries Institute of

Technology and Training (FITT) was established in Chennai in collaboration Tata Group to improve

the socioeconomic condition of fishermen. The Integrated Fisheries Project was established to

research on processing, popularizing and marketing of unusual fish. At present there are 19

fisheries colleges run by state governments.

Despite rapid growth in total fish production, a fish farmers’ average annual production in India is

only 2 tonnes per person compared to 172 tonnes in Norway, 72 tonnes in Chile and 6 tonnes

in China. India's water and natural resources offer a 10x growth potential in aquaculture from 2010

harvest levels of 3.9mn MT of fish, if India adopts fishing knowledge, regulatory reforms

and sustainability policies.

29 GWM

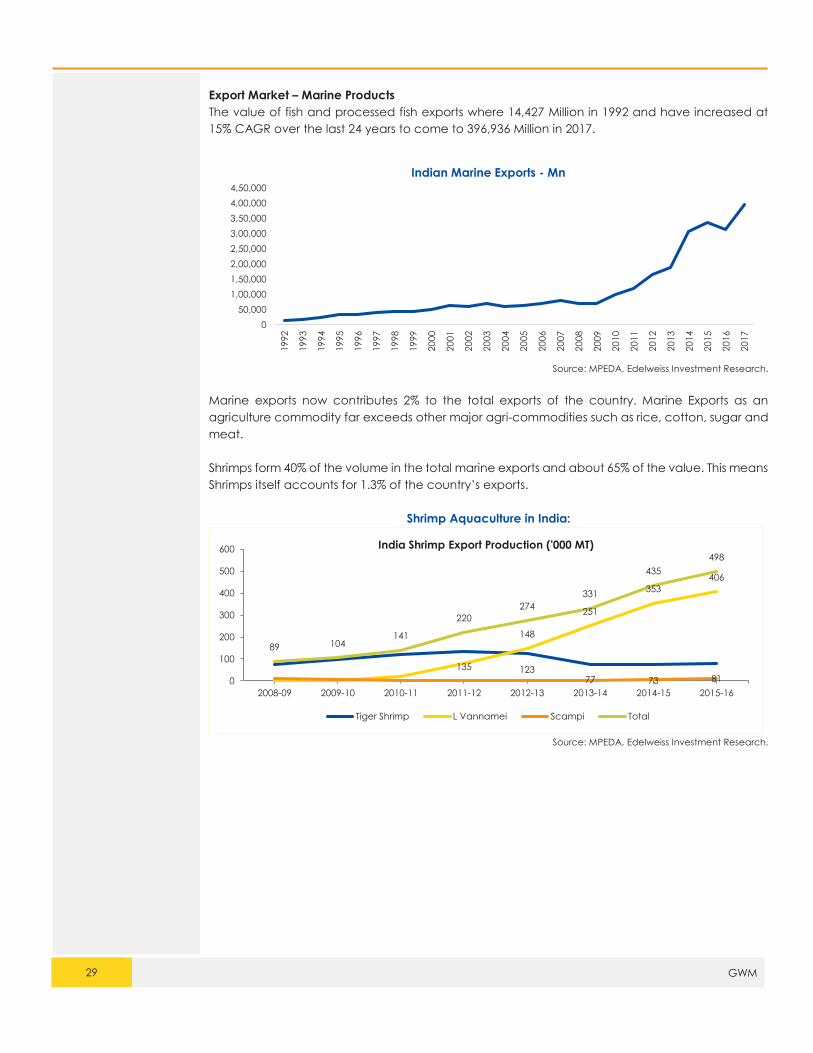

Export Market – Marine Products

The value of fish and processed fish exports where 14,427 Million in 1992 and have increased at

15% CAGR over the last 24 years to come to 396,936 Million in 2017.

Source: MPEDA, Edelweiss Investment Research.

Marine exports now contributes 2% to the total exports of the country. Marine Exports as an

agriculture commodity far exceeds other major agri-commodities such as rice, cotton, sugar and

meat.

Shrimps form 40% of the volume in the total marine exports and about 65% of the value. This means

Shrimps itself accounts for 1.3% of the country’s exports.

Shrimp Aquaculture in India:

Source: MPEDA, Edelweiss Investment Research.

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

3,50,000

4,00,000

4,50,000

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Indian Marine Exports - Mn

135 12377 73 81

148

251

353

406

89 104141

220

274

331

435

498

0

100

200

300

400

500

600

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

India Shrimp Export Production ('000 MT)

Tiger Shrimp L Vannamei Scampi Total

30 GWM

Shrimp is synonymous with prawn, covering stalk-eyed swimming crustaceans with long narrow

muscular tails (abdomens), long whiskers (antennae) and slender legs. Any small crustacean

which resembles a shrimp tends to be called one. They swim forward by paddling with swimmerets

on the underside of their abdomens. Shrimp are widespread and abundant. There are thousands

of species adapted to a wide range of habitats. They can be found feeding near the seafloor on

most coasts and estuaries, as well as in rivers and lakes. The consumption of shrimp is associated

with numerous health benefits as they are high in calcium, iodine, vitamin D, vitamin B3, zinc,

protein and omega-3s but low in saturated fat. In addition, they offer numerous health benefits

such as improved bone and brain health, weight management, lowered risk of cardiovascular

disease, relieved eye fatigue, lowered blood pressure and enhanced overall health.

After Green and White Revolution in India, it is time for Blue Revolution to exploit the huge potential

in fisheries sector. Shrimps are called "Pinkish Gold" of the sea because of their universal appeal,

unique taste, high unit value and increasing demand in the global market. Although there are

thousands of species, commercial production was restricted to a few until early 2000. The

development of brackish water aquaculture was mostly confined to a two species—Penaeus

Monodon, also known as Black Tiger shrimp, the scientific farming of which began only in early

1990s and Macrobrachium rosenbergii also known as scampi. Majority of the shrimps produced

were for exports, which fetched high realizations. However, due to the breakout of white spot

syndrome virus (WSSV) the production of Black Tiger shrimp remained stagnant.

In 2003, pilot research and small scale production of L. vannamei, also known as Pacific white leg

shrimp, was initiated. After six years of research, large scale production of L vannamei was

permitted in 2009 and since then its skyrocketed and grew at a CAGR of 190% to reach 0.4 million

tonne in 2015. The export of Pacific white leg shrimp has fetched hefty export realisations. Its

production is comparatively easier, as they can be reared at high stocking densities up to 150/

square meters and are tolerant to a wide range of salinities.

31 GWM

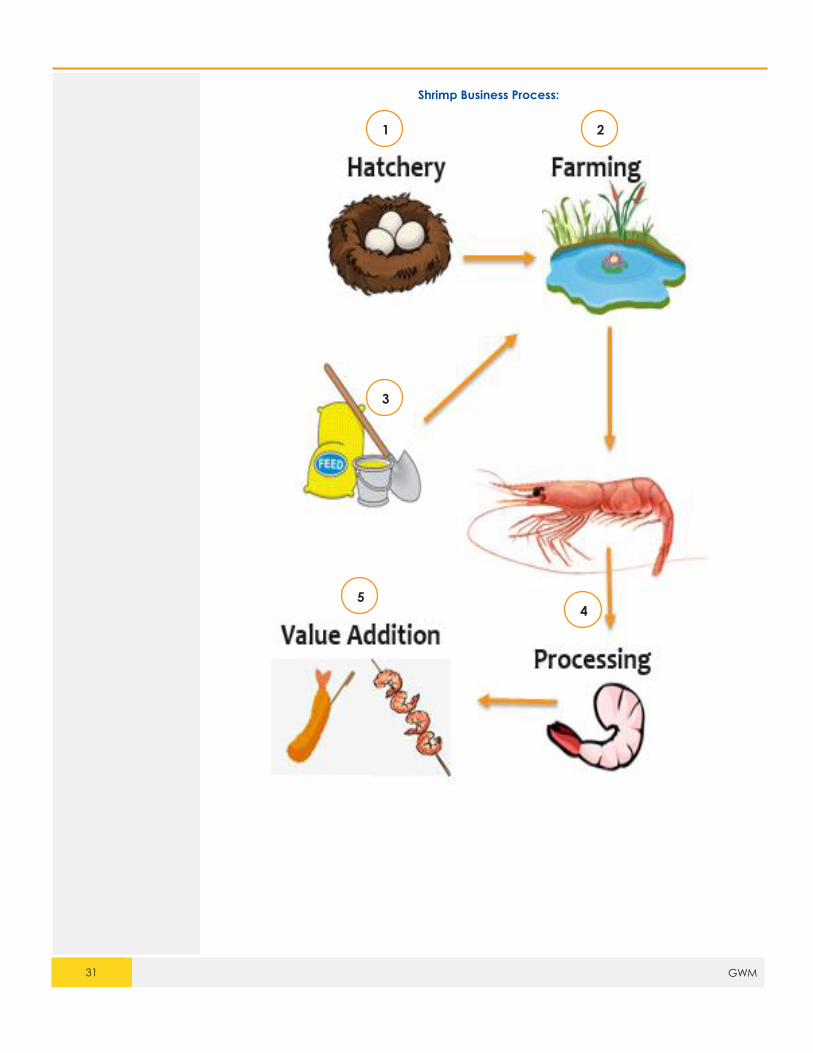

Shrimp Business Process:

1 2

3

4 5

32 GWM

1) Shrimp Hatcheries Industry:

SPF Broodstock

The Broodstock is purchased from

approved vendor in Florida or Hawaii.

Specific pathogen-free (SPF) broodstock is

used to control diseases and maintain

quality across the value chain.

Quarantined

Once brought into the country the

broodstock is quarantined by the Coastal

Aquaculture Authorithy of India. After

being checked for disease it is relased to

licensed Hatcheries.

Maturation

Males start reaching maturity at a weight

of 20g, while females usually grow faster

and bigger and reach this stage from 28g.

The matured male and female brood

stocks are reared for about 20-25 days in

holding tanks to recover from transport

stress & to adopt climate change.

Spawning

The first batch of eggs is discarded. The

female can spawn upto seven times.

Hatching

The females start laying eggs in the

spawning tank around 6 A.M. in the

morning. The eggs will begin to hatch

around 12 P.M. and the entire eggs are

hatched out by 4 P.M. the same day. The

next day all the hatched out young ones

i.e. Nauplii will be transferred to the Larval

Rearing Tanks.

MoltingThe un-segmented body of Nauplius

undergoes six molting’s within 50 hours

and turns into a protozoea. After 4–6 days,

the protozoea finally turn into a mysis. The

mysis remain drifting in the water column

until they transform into post larvae within

10–12 days. The animals grow very fast in

terms of size and are able to swim freely

at a body size of 0.8–1 cm in body length.

33 GWM

2) Shrimp Farming Industry:

Baby shrimp are fed for approximately 20 days before being transferred to open ponds, where

they are reared for 120 to 180 days depending on the size required, before developing into fully

grown shrimp ready for harvest. In 2017 the production of shrimp was about 600 KT.

Types Of Shrimp farmed in India

Penanaeus Monodon ( Black Tiger ) – Black Tiger Shrimp are known for ‘tiger stripes’on their shells

and tails. Shell color can range from brown, black, and grey. Tiger shrimp are most popular for

having a bold, sweet taste. The meat is firm which is described as snappy, meaty texture. Black

Tiger are normally priced higher than White shrimp and grow to a larger size. Black Tiger is available

in abundance in the eastern cost of India. However SPF seeds are not available for this species

making the survival rate lower and also due to the inherit characteristic they can’t be stock in high

density.

Litopenaeus vannamei ( Pacific white shrimp ) - Whiteleg shrimp are native to the eastern Pacific

Ocean, from the Mexican state of Sonora as far south as northern Peru.It is restricted to areas

where the water temperature remains above 20 °C (68 °F) throughout the year. They have a frim

but softer texture with a more delicate flavor. The introduction of L. vannamei during fiscal 2010

triggered massive expansion in farmed shrimp culture in India due to the suitable climatic and

other infrastructural conditions. The average yields rose up to six to eight MT from one to two MT

seen in the regime of black tiger culture. Responding to the increased white shrimp production,

corresponding expansion in processing capacity also took place by way of new players entering

the field while the existing players expanded their processing capacities. Farm yields and

economic viability substantially increased on account of lower susceptibility to disease outbreak

due to favourable climatic conditions, widespread farming area and compliance to best

aquaculture practices. Significant expansion in culture area across all the coastal states also led

to flourishing of feed manufacturing and processing capacities and other supply chain

infrastructure.

34 GWM

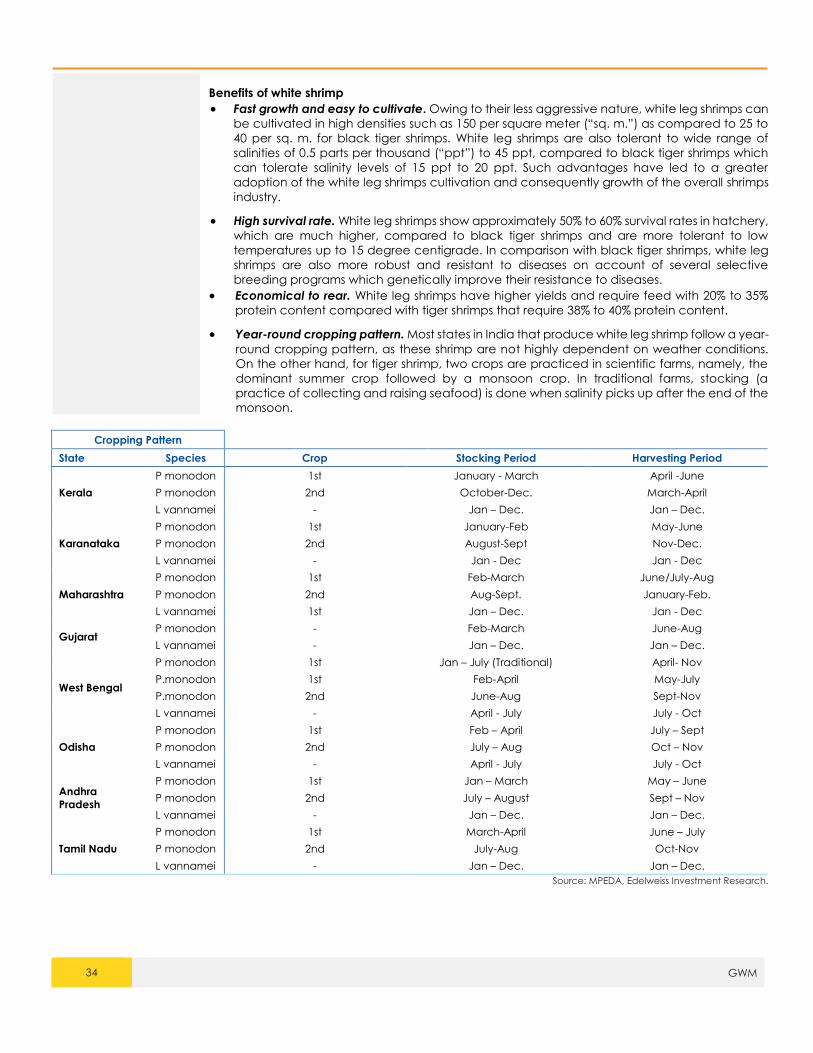

Benefits of white shrimp

Fast growth and easy to cultivate. Owing to their less aggressive nature, white leg shrimps can

be cultivated in high densities such as 150 per square meter (“sq. m.”) as compared to 25 to

40 per sq. m. for black tiger shrimps. White leg shrimps are also tolerant to wide range of

salinities of 0.5 parts per thousand (“ppt”) to 45 ppt, compared to black tiger shrimps which

can tolerate salinity levels of 15 ppt to 20 ppt. Such advantages have led to a greater

adoption of the white leg shrimps cultivation and consequently growth of the overall shrimps

industry.

High survival rate. White leg shrimps show approximately 50% to 60% survival rates in hatchery,

which are much higher, compared to black tiger shrimps and are more tolerant to low

temperatures up to 15 degree centigrade. In comparison with black tiger shrimps, white leg

shrimps are also more robust and resistant to diseases on account of several selective

breeding programs which genetically improve their resistance to diseases.

Economical to rear. White leg shrimps have higher yields and require feed with 20% to 35%

protein content compared with tiger shrimps that require 38% to 40% protein content.

Year-round cropping pattern. Most states in India that produce white leg shrimp follow a year-

round cropping pattern, as these shrimp are not highly dependent on weather conditions.

On the other hand, for tiger shrimp, two crops are practiced in scientific farms, namely, the

dominant summer crop followed by a monsoon crop. In traditional farms, stocking (a

practice of collecting and raising seafood) is done when salinity picks up after the end of the

monsoon.

Cropping Pattern

State Species Crop Stocking Period Harvesting Period

Kerala

P monodon 1st January - March April -June

P monodon 2nd October-Dec. March-April

L vannamei - Jan – Dec. Jan – Dec.

Karanataka

P monodon 1st January-Feb May-June

P monodon 2nd August-Sept Nov-Dec.

L vannamei - Jan - Dec Jan - Dec

Maharashtra

P monodon 1st Feb-March June/July-Aug

P monodon 2nd Aug-Sept. January-Feb.

L vannamei 1st Jan – Dec. Jan - Dec

Gujarat P monodon - Feb-March June-Aug

L vannamei - Jan – Dec. Jan – Dec.

West Bengal

P monodon 1st Jan – July (Traditional) April- Nov

P.monodon 1st Feb-April May-July

P.monodon 2nd June-Aug Sept-Nov

L vannamei - April - July July - Oct

Odisha

P monodon 1st Feb – April July – Sept

P monodon 2nd July – Aug Oct – Nov

L vannamei - April - July July - Oct

Andhra

Pradesh

P monodon 1st Jan – March May – June

P monodon 2nd July – August Sept – Nov

L vannamei - Jan – Dec. Jan – Dec.

Tamil Nadu

P monodon 1st March-April June – July

P monodon 2nd July-Aug Oct-Nov

L vannamei - Jan – Dec. Jan – Dec.

Source: MPEDA, Edelweiss Investment Research.

35 GWM

Currently, 1,40,666 hectare (ha) is the area under cultivation for shrimp with West Bengal leading

with 58,285ha, followed by Andhra Pradesh at 42,462ha. The total area under cultivation only

represents about 12% of the estimated brackish water area of 1.2mn ha, with Gujarat having the

largest potential with 3,76,000ha of brackish water, which is more than double the total area under

cultivation currently.

Source: MPEDA, Edelweiss Investment Research.

Source: MPEDA, Edelweiss Investment Research.

Although the area under cultivation is greater for West Bengal, production remains lower than

Andhra Pradesh as the former is still cultivating Black Tiger, whereas Andhra Pradesh has moved

almost completely to White Leg. Our channel checks indicate that it’s just a matter of time before

West Bengal too shifts to White Leg.

Farming is done by mostly individual farmers. However, some corporates are present in farming,

BMR Group (990 acre), Apex Frozen Foods (1,800 acre), Zeal Aqua (494 acre), Nekkanti Sea

Foods (330 acre), Devi Fisheries (370 acre) and Devi Seafoods (276 acre).

0

80000

160000

240000

320000

400000

480000

W. B

en

ga

l

Oriss

a

An

dh

ra P

rad

esh

Tam

il N

ad

u &

Po

nd

ich

err

y

Ke

rala

Ka

rna

taka

Go

a

Ma

ha

rash

tra

Gu

jara

t

Potential cultivation Hectares

Area Under Cultivation - Hectares Estimated brackish water area

W. Bengal,

58285

Orissa,

10778

Andhra

Pradesh,

42462

Tamil Nadu

&

Pondicherry

, 8263

Kerala,

12622

Karnataka,

2281

Goa, 10

Maharashtra, 1413

Gujarat,

4552

Area Under Cultivation - Hectares

W. Bengal,

73

Orissa, 30

Andhra

Pradesh,

300

Tamil Nadu

&

Pondicherry,

46

Kerala, 4

Karnataka,

2

Maharashtra, 8Gujarat, 35

Export Production ('000 MT)

36 GWM

3) Shrimp Feed Industry

The shrimp feed industry is highly organized as the shrimp industry caters to the export market, with

organized players accounting for 80% of the shrimp feed industry. There has been a higher usage

of shrimp feed given that a large part of the shrimp export market is catered to by aquaculture

farms. While barrier to entry are low in this business, quality and consistence are key to success of

the feed manufacture. The base of judging a feed is its FCR-Feed Conversation Ratio, good feeds

have an FCR lower than 1.3x . FCR means how much of the feed leads to a gram increase in the

weight of the shrimp.

The total market size of the shrimp feed industry was estimated at about 1.2 million MT in fiscal 2017

with capacity at about 2.2 Million MT. The industry is expected to grow at 15%-20% annually for the

next 3 years based on industry experts.

The industry is dominated by two giants Avanti feeds (6,00,000 MT) and CP Aqua feeds an Thailand

based company. Apart from these other players are Waterbase(1,10,000 MT), BMR group(1,40,000

MT), Godrej Agrovet(70,000 MT), Cargill(90,000 MT), Growell feeds(3,00,000 MT) and Devi

Seafoods(1,25,000 MT).

37 GWM

4) Shrimp Processing Industry

India has 536 processing facilities with a combined installed capacity of approximately 26,000 MT

per day (Source: MPEDA statistics). Shrimp processing facilities are largely concentrated in South

India and in particular Andhra Pradesh. Every shrimp processing plant in India is Hazard Analysis

and Critical Control Points ("HACCP") compliant, and all business involved in the shrimp supply

chain from producers to retailers are similarly required to be HACCP-compliant. Additionally, India

has one of the highest number of EU-approved processing plants, with more than two-thirds of

plants being approved.

Post-harvest, fully grown shrimp are transferred to these processing plants for primary processing,

which involves the slicing of shrimp heads and heavy duty washing. Thereafter, these are subject

to a sorting process based on commercially accepted sizes and weights before having their skins

peeled off and being soaked in phosphate chemicals. The phosphate soaking process helps to

maintain the quality and taste of the shrimp, and this process is a prerequisite for almost all export

markets. The raw shrimp is then frozen before packaging. Based on the final desired product,

shrimp can go through a number of processes, including freezing, freeze-drying, chilling, canning,

etc. Different levels of processing include basic processing such as easy-peel type shrimp where

the shell is left on, or where the shell has been removed (head-less, tail-on, tail-off, deveined, etc.).

5) Further value addition can be carried out by partially or completely cooking the shrimp. VAP

processes differ from product to product involving use of skilled workmanship and various

flavouring and breading ingredients etc. The prices of value added shrimp are directly

proportional to the degree and nature of the value addition. Currently, India is a small player

in the prepared shrimps and prawns exports and accounts for around 7% of the global exports

in 2016. Indian exporters are increasingly focused on VAP products, where higher value-add

typically leads to higher price realizations. Examples of value-added shrimp products breaded

and battered shrimp, skewered shrimp, cooked and peeled shrimp and sushi. Larger Indian

exporters are expanding their infrastructure to cater to increasing demand for such VAP

products.

At the final stage of processing, shrimp are frozen either individually (Individual Quick Frozen or

"IQF") or in block form and then pack the shrimp into poly bags or paper cartons of different sizes

specified by the customers. The finished products are kept in cold storage at minus 20 degree

Celsius and are shipped in a refrigerated container on a sea vessel to the customers located in

other countries. The value of India's exports of shrimps prepared has increased at a CAGR of

approximately 49% during the five year period from 2012-2016.

Products

Normal Products-Blockfrozen

Head-Less Shell Off

Head-Less Shell-on Head-On

Easy Peel ShrimpPeeled, Deveined,

Tail-on Shrimp

Peeled, Deveined, Tail-off Shrimp

Value Added Products-IQF

Ready to eat shrimp (cooked)

Ready to cook shrimp (peeled)

Shrimp marinated in different flavors

(marinated)

Shrimp in a particular

presentation form (butterfly shrimp)

Ready for breading shrimp (breaded)

Shrimp skewers (skewered)

Head-Less Devein

38 GWM

Edelweiss Broking Limited, 1st Floor, Tower 3, Wing B, Kohinoor City Mall, Kohinoor City, Kirol Road, Kurla(W)

Board: (91-22) 4272 2200

Vinay Khattar

Head Research

Rating Expected to

Buy appreciate more than 15% over a 12-month period

Hold appreciate between 5-15% over a 12-month period

Reduce Return below 5% over a 12-month period

40

140

240

340

440

540

640

740

Ja

n-1

6

Ap

r-16

Ju

l-16

Oc

t-16

Ja

n-1

7

Ap

r-17

Ju

l-17

Oc

t-17

Ja

n-1

8

Ap

r-18

(In

de

xe

d)

Avanti Sensex

Disclaimer

39 GWM

Edelweiss Broking Limited (“EBL” or “Research Entity”) is regulated by the Securities and Exchange Board of India (“SEBI”) and is licensed to carry on the business of broking, depository

services and related activities. The business of EBL and its Associates (list available on www.edelweissfin.com) are organized around five broad business groups – Credit including Housing

and SME Finance, Commodities, Financial Markets, Asset Management and Life Insurance.

Broking services offered by Edelweiss Broking Limited under SEBI Registration No.: INZ000005231; Name of the Compliance Officer: Mr. Brijmohan Bohra, Email ID:

[email protected] Corporate Office: Edelweiss House, Off CST Road, Kalina, Mumbai - 400098; Tel. 18001023335/022-42722200/022-40094279

This Report has been prepared by Edelweiss Broking Limited in the capacity of a Research Analyst having SEBI Registration No.INH000000172 and distributed as per SEBI (Research Analysts)

Regulations 2014. This report does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. The information

contained herein is from publicly available data or other sources believed to be reliable. This report is provided for assistance only and is not intended to be and must not alone be taken

as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this report should make such investigation as it deems necessary

to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult his own

advisors to determine the merits and risks of such investment. The investment discussed or views expressed may not be suitable for all investors.

This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly

in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a

citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would

subject EBL and associates / group companies to any registration or licensing requirements within such jurisdiction. The distribution of this report in certain jurisdictions may be restricted by

law, and persons in whose possession this report comes, should observe, any such restrictions. The information given in this report is as of the date of this report and there can be no

assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. EBL reserves the right to make modifications and

alterations to this statement as may be required from time to time. EBL or any of its associates / group companies shall not be in any way responsible for any loss or damage that may arise

to any person from any inadvertent error in the information contained in this report. EBL is committed to providing independent and transparent recommendation to its clients. Neither EBL

nor any of its associates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including loss

of revenue or lost profits that may arise from or in connection with the use of the information. Our proprietary trading and investment businesses may make investment decisions that are

inconsistent with the recommendations expressed herein. Past performance is not necessarily a guide to future performance .The disclosures of interest statements incorporated in this

report are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The information provided in these reports remains,

unless otherwise stated, the copyright of EBL. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of EBL and may not be

used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

EBL shall not be liable for any delay or any other interruption which may occur in presenting the data due to any reason including network (Internet) reasons or snags in the system, break

down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the EBL to present the data. In no event shall

EBL be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data presented

by the EBL through this report.

We offer our research services to clients as well as our prospects. Though this report is disseminated to all the customers simultaneously, not all customers may receive this report at the

same time. We will not treat recipients as customers by virtue of their receiving this report.

EBL and its associates, officer, directors, and employees, research analyst (including relatives) worldwide may: (a) from time to time, have long or short positions in, and buy or sell the

securities thereof, of company(ies), mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market

maker in the financial instruments of the subject company/company(ies) discussed herein or act as advisor or lender/borrower to such company(ies) or have other potential/material

conflict of interest with respect to any recommendation and related information and opinions at the time of publication of research report or at the time of public appearance. EBL may

have proprietary long/short position in the above mentioned scrip(s) and therefore should be considered as interested. The views provided herein are general in nature and do not consider

risk appetite or investment objective of any particular investor; readers are requested to take independent professional advice before investing. This should not be construed as invitation

or solicitation to do business with EBL.

EBL or its associates may have received compensation from the subject company in the past 12 months. EBL or its associates may have managed or co-managed public offering of

securities for the subject company in the past 12 months. EBL or its associates may have received compensation for investment banking or merchant banking or brokerage services from