effect of technology adoption on underwriting …

TRANSCRIPT

EFFECT OF TECHNOLOGY ADOPTION ON UNDERWRITING

PROCESSES AMONG TOP FIVE INSURANCE COMPANIES IN

NAIROBI COUNTY

BY

NGIRI MUGECHI SUSAN

UNITED STATES INTERNATIONAL UNIVERSITY – AFRICA

SUMMER 2021

EFFECT OF TECHNOLOGY ADOPTION ON UNDERWRITING

PROCESSES AMONG TOP FIVE INSURANCE COMPANIES IN

NAIROBI COUNTY

BY

NGIRI MUGECHI SUSAN

A Research Project Report Submitted to the Chandaria School of Business

in Partial Fulfillment of the Requirement for the Masters of Business

Administration (MBA)

UNITED STATES INTERNATIONAL UNIVERSITY-AFRICA

SUMMER 2021

ii

STUDENT’S DECLARATION

I, the undersigned, declare that this Research Project is my original work and has not been

submitted to any other college, institution or university other than the United States

International University in Nairobi for academic credit.

Signed: ________________________ Date: _____________________________

Ngiri Mugechi Susan (660334)

This research project report has been presented for examination with my approval as the

appointed supervisor.

Signed: ________________________ Date: _______________________________

Dr. Gabriel O. Okello

Sign: __________________________ Date___________________________

Dean, Chandaria School of Business

iii

COPYRIGHT

All rights reserved. No part of this work may be produced or transmitted in any form or by any

means, electronic, mechanical, including photocopying, recording or any information storage

without prior written permission from the author.

© Copyright by MUGECHI NGIRI SUSAN, 2021

iv

ABSTRACT

The purpose of the study was to examine the effect of technology adoption on underwriting

processes among top five insurance companies in Nairobi County. The study was guided by

the following research questions: How does digitization of claims process affect the

underwriting process among the top five insurance firms in Nairobi County? What is the effect

of digital fraud detection on the underwriting process among the top five insurance company

in Nairobi County? Lastly, what is the effect of using customer relationship management

system on the underwriting process among top five insurance firms in Nairobi County?

The study employed survey descriptive design. The target population was 1174 employees of

top 5 insurance companies operating in Nairobi County. The study used stratified sampling to

select 298 employees of the selected insurance firms to participate in the survey. The study

relied on primary data. Data collection was performed through the use of structured

questionnaires. Through SPSS Version 26.0, data analysis entailed the use of descriptive and

inferential statistics techniques. Descriptive statistics techniques to be used include

percentages, mean and standard deviation. Inferential statistics techniques used entailed

Pearson Correlation Coefficient and Simple Linear Regression. Simple linear regression

analysis was used to determine linear relationship and the effect of each technology adoption

variable on the underwriting process. The results and findings were presented in the form of

tables and figures.

The findings on the effect of digital claim processing on the underwriting process among top

five insurers in Nairobi County indicated that most of insurers agreed that automation ensures

that the insured provided accurate information that was verifiable during investigation. The

relationship between digital claim processing and the underwriting process was positive and

weak. The findings further revealed that digital claim processing had positive and significant

effect on the underwriting process among insurers in Nairobi County.

Regarding the effect of digital fraud detection on the underwriting process among top five

insurers in Nairobi County, the findings indicated that most insures agreed that they encounter

the risk of inability to meet claims due to fraudulent claims from policyholders. The

relationship between digital fraud detection and underwriting process was positive and weak.

v

The findings further revealed that digital fraud detection had a positive and significant effect

on the underwriting process among insurers in Nairobi County.

The findings on the effect of customer relationship management system on the underwriting

process among top five insurers in Nairobi County indicated that most insurers agreed that

staff provided service to customers as a priority entry into the company without exceeding.

The relationship between customer relationship management system and underwriting process

was strong and positive. The findings further revealed that customer relationship management

system had a positive and significant effect on process among insurers in Nairobi County.

The study concluded that digitization of claims process, digital fraud detection, and customer

relationship management system factors significantly affected the underwriting among top

insurers. Statistical results (correlation and regression analysis) concluded that all the three

independent variables used in the study namely: Digital claim processing, digital fraud

detection, and customer relationship management system attributes had a significant positive

relationship with the dependent variable, underwriting process. The study recommends that

insurers should always work towards automating their clam’s processes. In addition, the study

recommends that insurers should put in place aspects of building up digital insurance control

mechanisms. The study further recommends that insurers should consider investing in their

customer relationship management programs.

vi

ACKNOWLEDGEMENT

I acknowledge God for guiding me through my academic’s journey, the entire staff of USIU

and my family for the support, sacrifice and encouragement all through. This endeavor would

not have been accomplished without the support of my colleagues in the insurance sector. I

must also thank the Chandaria School of Business for the support offered in this research

project under the invaluable guidance of Dr. Gabriel Okello.

vii

DEDICATION

This project is dedicated to Family. My husband Mr. Joseph K. Mutiga and my children

Natalie, Madeleine and Emmanuel Kimani. for your love, support and sacrifice in all aspects

of my life. To my siblings, mother and to my father Mr. John Ngiri, for encouraging to pursue

further education and his passion for academic excellence. I will forever be indebted to all of

you for molding me to the person I am and the values you instilled in me. Gratias tibi

viii

TABLE OF CONTENTS

STUDENT’S DECLARATION ............................................................................................. ii

COPYRIGHT ......................................................................................................................... iii

ABSTRACT ............................................................................................................................ iv

ACKNOWLEDGEMENT ..................................................................................................... vi

DEDICATION....................................................................................................................... vii

TABLE OF CONTENTS .................................................................................................... viii

LIST OF TABLES ...................................................................................................................x

LIST OF FIGURES .............................................................................................................. xii

LIST OF ACRONYMS ....................................................................................................... xiii

CHAPTER ONE ......................................................................................................................1

1.0 INTRODUCTION.........................................................................................................1

1.1 Background to the Study .............................................................................................1

1.2 Statement of the Problem ............................................................................................5

1.3 Purpose of the Study ...................................................................................................7

1.4 Research Questions .....................................................................................................7

1.5 Significance of the Study ............................................................................................7

1.6 Scope of the Study.......................................................................................................8

1.7 Definition of Terms .....................................................................................................8

1.8 Chapter Summary ........................................................................................................9

CHAPTER TWO ...................................................................................................................10

2.0 LITERATURE REVIEW ..........................................................................................10

2.1 Introduction ...............................................................................................................10

2.2 Effect of Digitization of Claims Process on Underwriting Processes .......................10

2.3 Effect of Digital Fraud Detection on the Underwriting Process ...............................15

2.4 Effect of Using Customer Relationship Management System on the Underwriting

Process ..................................................................................................................................19

2.5 Chapter Summary ......................................................................................................26

CHAPTER THREE ...............................................................................................................27

3.0 RESEARCH METHODOLOGY ..............................................................................27

3.1 Introduction ...............................................................................................................27

ix

3.2 Research Design ........................................................................................................27

3.3 Population and Sampling Design ..............................................................................28

3.4 Data Collection Methods ...........................................................................................31

3.5 Research Procedures .................................................................................................32

3.6 Data Analysis Methods .............................................................................................34

3.7 Chapter Summary ......................................................................................................37

CHAPTER FOUR ..................................................................................................................38

4.0 RESULTS AND FINDINGS ......................................................................................38

4.1 Introduction ...............................................................................................................38

4.2 General Information ..................................................................................................38

4.3 Effect of Digitization of Claims Process on Underwriting Processes .......................43

4.4 Effect of Digital Fraud Detection on the Underwriting Process ...............................50

4.5 Effect of Using Customer Relationship Management System on the Underwriting

Process ..................................................................................................................................56

4.6 Chapter Summary ......................................................................................................63

CHAPTER FIVE ...................................................................................................................64

5.0 DISCUSSION, CONCLUSIONS AND RECOMMENDATIONS ..............................64

5.1 Introduction ...............................................................................................................64

5.2 Summary ...................................................................................................................64

5.3 Discussion .................................................................................................................65

5.4 Conclusions ...............................................................................................................71

5.5 Recommendations .....................................................................................................72

REFERENCES .......................................................................................................................74

APPENDICES

APPENDIX I: INTRODUCTION LETTER

APPENDIX II: QUESTIONNAIRE

APPENDIX III: RESEARCH INFORMED CONSENT

APPENDIX IV: DEBREIF FORM

APPENDIX V: IRB CONFIDENTIALITY FORM

APPENDIX VI: USIU-AFRICA INTRODUCTION LETTER

APPENDIX VII: RESEARCH ETHICAL LETTER

APPENDIX VIII: NACOSTI PERMIT

x

LIST OF TABLES

Table 3.1 : Population Distribution ..........................................................................................28

Table 3.2: Sample Size Distribution ........................................................................................31

Table 3.3: Validity of the Questionnaire..................................................................................33

Table 3.4: Reliability of the Questionnaire ..............................................................................34

Table 4.1: Duration for Handling aspects of Claim Management ...........................................41

Table 4.2: Descriptive Statistics on Digitization of Claims Process .......................................44

Table 4.3: Correlation between Digitization of Claims Process and Underwriting Processes 45

Table 4.4: Tests of Normality for Digitization of Claims Process Variable ............................46

Table 4.5: Linearity Test between Digitization of Claims Process and Underwriting

Process .....................................................................................................................................46

Table 4.6: Multicollinearity Test for Digitization of Claims Process and Underwriting Process

..................................................................................................................................................48

Table 4.7: Regression Model Summary for Linear Relationship between Digitization of Claims

Process and Underwriting Processes .......................................................................................48

Table 4.8: Regression ANOVA for Linear Relationship between Digitization of Claims

Process and Underwriting Processes .......................................................................................49

Table 4.9: Regression Coefficients Values for Linear Relationship between Digitization of

Claims Process and Underwriting Processes ...........................................................................49

Table 4.10: Descriptive Statistics on Digital Fraud Detection ................................................51

Table 4.11: Correlation between Digital Fraud Detection and Underwriting Process ............52

Table 4.12: Normality Test for Digital Fraud Detection Variable ...........................................53

Table 4.13: Linearity Test for Digital Fraud Detection and Underwriting Process .................53

Table 4.14: Multicollinearity Test for Digital Fraud Detection and Underwriting Process ....54

Table 4.15: Regression Model Summary for Linear Relationship between Fraud Detection and

Underwriting Processes ...........................................................................................................55

Table 4.16: Regression ANOVA for Linear Relationship between Digital Fraud Detection and

Underwriting Processes ...........................................................................................................55

Table 4.17: Regression Coefficients Values for Linear Relationship between Digitization of

Claims Process and Underwriting Processes ...........................................................................56

xi

Table 4.18: Descriptive Statistics for Customer Relationship Management System ..............57

Table 4.19: Correlation between Customer Relationship Management System and

Underwriting Process ...............................................................................................................58

Table 4.20: Tests of Normality for Customer Relationship Management System Variable ...59

Table 4.21: Linearity Test for Customer Relationship Management System and Underwriting

Process .....................................................................................................................................60

Table 4.22: Multicollinearity for Customer Relationship Management System and

Underwriting Process ...............................................................................................................61

Table 4.23: Regression Model Summary for Linear Relationship between Customer

Relationship Management System and Underwriting Processes .............................................62

Table 4.24: Regression ANOVA for Linear Relationship between Customer Relationship

Management System and Underwriting Processes ..................................................................62

Table 4.25: Regression Coefficients Values for Linear Relationship between Customer

Relationship Management System and Underwriting Processes .............................................63

xii

LIST OF FIGURES

Figure 4.1: Response Rate .......................................................................................................38

Figure 4.2: Insurance Provider .................................................................................................39

Figure 4.3: Years of Operation in Local Market......................................................................40

Figure 4.4 : Number of Employees ..........................................................................................40

Figure 4.5: Level of Technology Implementation ...................................................................41

Figure 4.6: Incidences of Insurance Fraud ...............................................................................42

Figure 4.7: Profitability of Insurers .........................................................................................43

Figure 4.8: Homoscedasticity Test for Digitization of Claim Process ...................................47

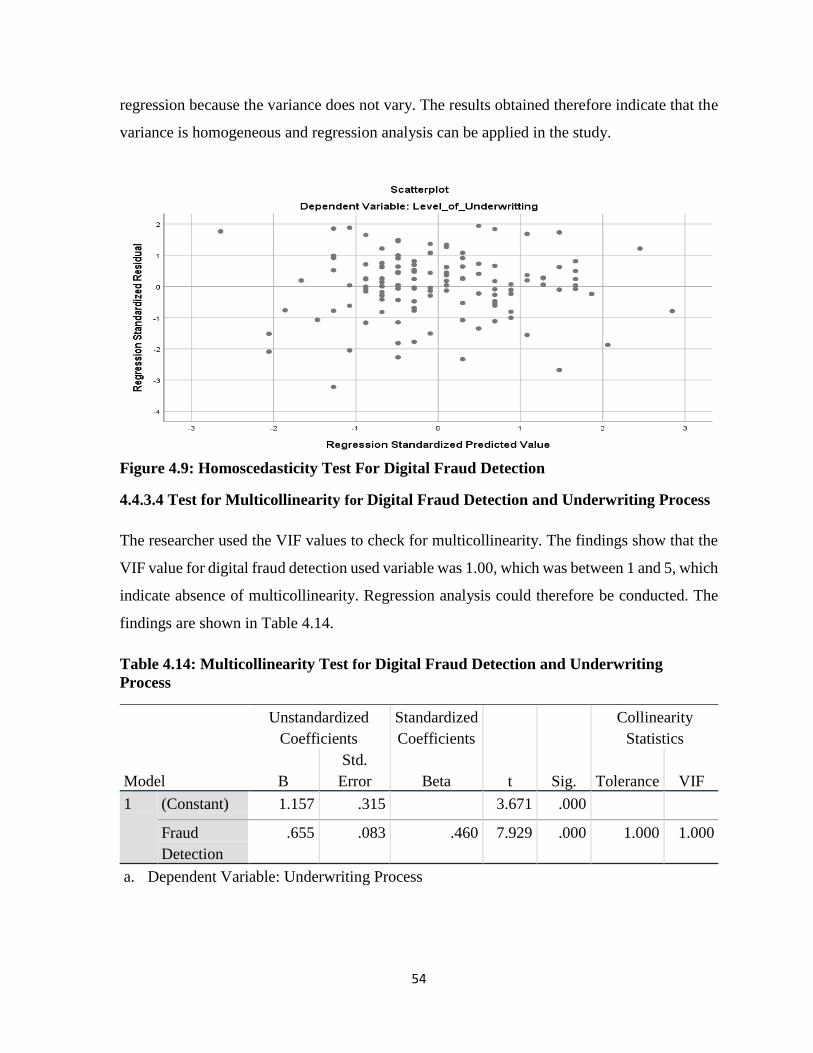

Figure 4.9: Homoscedasticity Test For Digital Fraud Detection .............................................54

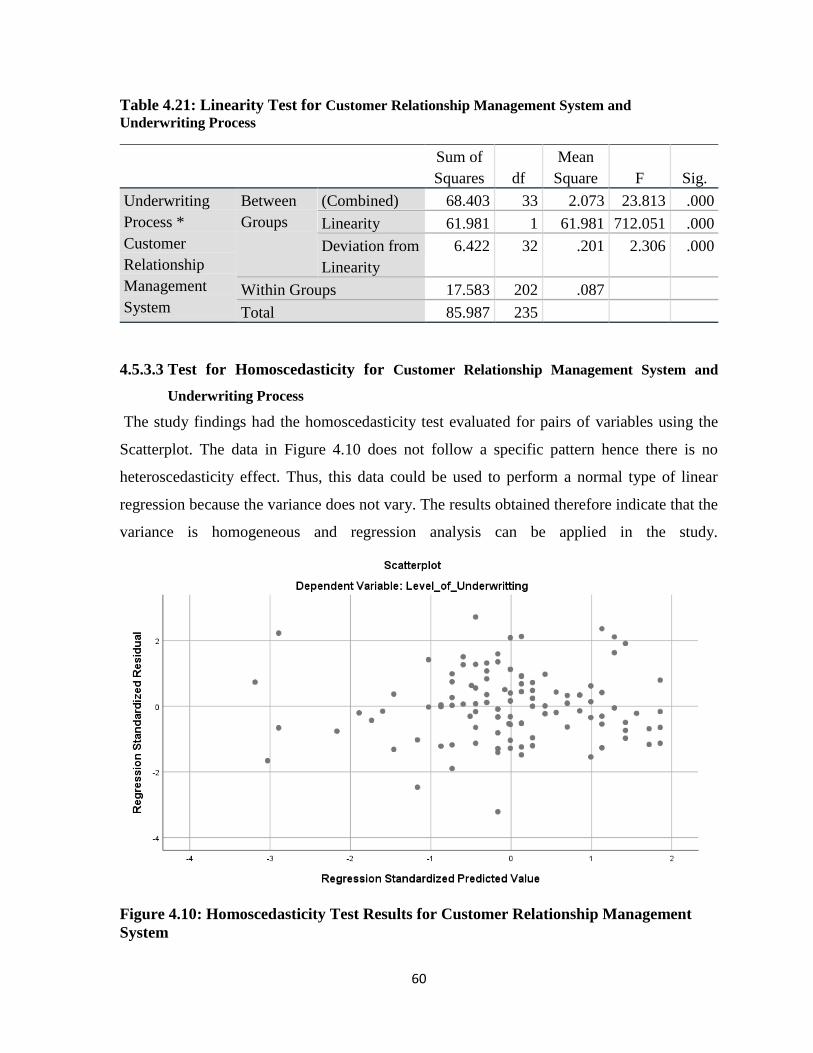

Figure 4.10: Homoscedasticity Test Results for Customer Relationship Management

System ......................................................................................................................................60

xiii

LIST OF ACRONYMS

AKI Association of Kenya Insurer

CRM Customer Relationship Management

CRS Claim Review Support

EIC Earned Income Tax Credit

FTUSA The Tunisian Federation of Insurance Companies

GARCH Generalized Autoregressive Conditional Heteroskedasticity

GWP Gross Written Premium

HIRA Health Insurance Review and Assessment

HMI Health Microinsurance

ICICI Industrial Credit and Investment Corporation

IoT Internet of Things

IRA Insurance Regulatory Authority

IRDA Insurance Regulatory and Development Authority

IT Information Technology

ML Machine Learning

P & C Property and Casualty

PARE Payment Request

RFM Recency, frequency, monetary value

SAS Coalition Statistical Analysis Software

SME Small- to Mid-size Enterprise

SPSS Statistical Package for the Social Sciences

UW Underwriting

VAR Vector Autoregressive

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background to the Study

Over the last decade, a variety of breakthrough technologies have spurred a fundamental

transformation of the insurance industry (Bondurant & White, 2019). The new technologies

such as Cloud computing, the Internet of Things (IoT), advanced analytics, mobile phones,

blockchain, smart contracts, and artificial intelligence (AI) are providing new ways to measure,

control, and price risk, engage with customers, reduce cost, improve efficiency, and expand

insurability (Ferenzy, Silverberg, Van Liebergen, & French, 2016). Fundamentally, one of the

elements of insurance spectrum which has undergone significant revolution is underwriting

process. The emergence of new technology has the potential to change the way insurers

underwrite customers, distribute insurance products, collect data, and change consumer

behaviour in the actual buying of insurance products (Gandhi & Kaul, 2016).

Conventionally, underwriting occurs when an insurer and an insured conclude a contract of

insurance, whereby the insurer undertakes to indemnify the insured against losses due to

specific future risks, while the insured has the obligation to pay periodic premiums to the

insurer in return (Conrad, Mostert, & Mostert, 2015). Underwriting can be categorized into

two major categories; general and life insurance underwriting (Scordis, 2019). There are two

kinds of life insurance underwriting options: Simplified Issue and Fully Underwritten. General

insurance or non-life insurance policies, including automobile and homeowners’ policies,

provide payments depending on the loss from a particular financial event (Neale, Drake, &

Konstantopoulos, 2020).

A report by the Wyman and Zhong (2017) acknowledges wide-scale technology application in

underwriting processes. For instance, Artificial Intelligence applied to past underwriting (UW)

decisions could be used to program next generation underwriting systems (Chester, Ebert,

Kauderer, & McNeill, 2016). Insurers have mandate to respond to growth among consumers

in the use of apps and Internet of things to manage their personal health. Insurers have the

mandate to respond to changing customer demands for convenience, personalisation, and fast

2

execution (Van Dalen, Cusick, & Ferris, 2021). In essence, technology plays a significant role

in underwriting transformation across all segments from SME to mid-market to large

commercial.

According to Schmid (2019) key levers that have a major impact on the underwriting value

chain include automation, data insights and analytics, and underwriting platform-based

solutions. These technologies affect the assessment and proactive monitoring of risks and

hence help in the prevention of the same. Thus, countries with low insurance penetration rates

but with large market and growing middle class are finding great opportunity in tech-insurance.

In Brazil, for instance, the development of information and communication technology in the

country is brightening up the outlook for Brazil’s insurance industry, considering it has the

fourth highest number of internet users in the world (Dimas, 2017).

In developed economies, top insures have led the way in the adoption of modern technology

(Joshi, Pelling, O’Connor, & Wompa, 2020). In 2018, the Germany leading insurer Allianz,

announced a partnership with Microsoft for the digital transformation of the insurance industry

by making the insurance process easier and creating an improved experience for both insurance

companies and customers (Daramola, Oderinde, Anene, Abu, & Akande, 2020). In the same

year, Allianz Insurance launched “Defendant Hub” a new digital proposition that uses artificial

intelligence to enable the company’s injury claims handlers to action Ministry of Justice Stage

3 claims at a single click of a button.

In France, the leading insurer, AXA managed to automate its operations in pursuit of

strengthening its underwriting activities. To reinforce its presence on the strategic SME

business market, AXA developed “OSE”, a corporate underwriting tool that considerably

speeds up and simplifies new contracts through data and automation (Borselli, 2020). To

combat fraud in insurance sector, AXA implemented Sherlock; a data analysis software

solution designed to automate and simplify fraud detection. The tool can help identify and

extract suspicious claims, while more importantly enabling honest claims to be processed more

quickly (Kumar, Srivastava, & Bisht, 2019). In early 2012, AXA made the decision to roll out

the point-of-sale risk assessment and accumulations management software solution,

3

LexisNexis® Map View, globally, to adopt a standardised and consistent approach to risk

management across all its property underwriting divisions worldwide.

In 2020, the China Life Insurance Company Limited pushed forward digital transformation in

all aspects (Shaw & Baumann, 2020). Being customer-centric, the company pushed forward

intelligent upgrade of online services. The “Contactless Services” facilitated customers

accessing insurance services just at home by employing Internet video and intelligent

identification technology. Based on big data and AI technologies, the intelligent claims

settlement model for health insurance, covering 19 key risks in five categories, made claims

settlement services more efficient and convenient (Eckert & Osterrieder, 2020).

In Russia, there has been a growth in digital insurance. The main tasks that a Russian insurer

solves when using IT technologies are the automation of business operations and the formation

of an online system of interaction with customers with the main focus on sales (Kaigorodova,

et al, 2021). Maslova and Ilina (2020) observe that the key advantage of the latter is time saving

and no pressure from insurer or intermediary, whereas the main threat is loss of data access

and leaks. For Russian companies, the prior challenge is to provide the complete service cycle

starting from the pre-sale stage and ending with the settlement of insurance case, as well as to

implement an individual approach to each insurant. Similar shortcomings are observed in the

Mexican insurance market. Kędra, Lyubov, Lyskawa, and Klapkiv (2019) contend that in

Mexico, there is a different tendency in the raising of ICT investments and the values of gross

premiums, claims and expenses.

In order to explore consumers’ preferences, the authors interview 110 Russian policyholders

and study their relations with insurers, their choice of policy acquisition channels, and the

quality of particular digital insurance customized offers. The poll results show the higher

demand for conventional insurance rather than digital one. Nevertheless, there has been a

growth in digital insurance. The key advantage of the latter is time saving and no pressure from

insurer or intermediary, whereas the main threat is loss of data access and leaks. The authors

analyze main drivers of online-insurance in Russia. The general problem is lack of trust

between consumers and insurers. For Russian companies, the prior challenge is to provide the

complete service cycle starting from the pre-sale stage and ending with the settlement of

insurance case, as well as to implement an individual approach to each insurant. That will

4

become the basis for insurance service customization which is considered to be one of the most

promising global trends in this sector.

A substantial portion of insurance companies now are including anti-fraud technology in their

anti-fraud programs. On April 26 2021, The Insurance Fraud Bureau (IFB) commenced

building of a powerful, new fraud detection system on behalf of the UK insurance sector.

Currently one insurance scam takes place each minute in the UK, devastating countless victims

and costing the economy over £3 billion a year (Mohammed, Abdelsalam, Ashraf, & Barake,

2020). In comparison, internal fraud, rate evasion, underwriting fraud, claims fraud,

cybersecurity fraud adds up to more than $80 billion a year in the US (Coalition Against

Insurance Fraud, 2020). Indeed, the Coalition Against Insurance Fraud (2016) surveyed

insurance companies and found that nearly 75 percent had fully integrated technology into

their anti-fraud systems- up from about 50 percent four years ago.

The South Africa’s top insurer, Old Mutual Insure, has developed a laudable reputation for

customer centricity and service quality which are values that form the foundations of its digital

transformation journey (Singh, 2020). The company’s digital transformation is focused on

establishing lean operations that maximise efficiency and improve the customer experience.

Additionally, Sanlam’s understanding of the imperative for cutting-edge digital solutions is

firmly rooted in its desire to offer its customers a seamless and meaningful insurance

experience (Benton, 2020). In Ghana, BIMA agents, the company also utilizes mobile

technology to sign up customers, verify registration, receive premium payments and pay out

claims. BIMA’s registration process is fully paperless and can be completed within two

minutes (Edinger, Adepoj, & Masha, 2017).

The Kenyan insurance life market is characterised by seven main products with ordinary life,

group life and pensions being the key products in the market (Chache, Mwangi, Nyamute, &

Angima, 2020; Kahonga & Kariuki, 2020). Most of the top ten insurers have experienced

reasonable premium growth with an average premium growth of 11% over the year 2018/2019

(Muriuki, & Luo, 2020). In 2019, the number of insurance companies remained 54 similar to

2018. There were 16 Reinsurance brokers in 2019 up two from 14 in 2018. The number of

agents increased from 8,955 in 2018 to 9,262 in 2019. Licensed brokers decreased from 216

in 2018 to 213 in 2019. The number of insurance surveyors and loss adjusters stood at 30 in

5

2019 compared to 28 in 2018. In terms of market capitalization, Britam Life ranks top with

23.59%, Jubilee Insurance came second with 14.48% capitalization, ICEA (13.86%), CIC

(6.95%), and APA (6.59%) (Insurance Regulatory Authority, 2020). Based on market

capitalization and capital investment, the top 10 non-life insurers accounted for more than

56.08% of the fast-growing gross premium income for the year. Squeezed margins in the

sector, continued cases of fraud, and premiums that have grown at a slower rate than the

economic growth, have had a negative impact on shareholders’ returns. Notably, Permanent

Health has not experienced significant growth within the last 4 years (Ngunguni, Misango, &

Onsiro, 2020).

Overall, the Association of Kenya Insurers (2020) reports that Kenya has insurance penetration

of 2.37%. According to Association of Kenyan Insurers (2019), although, the segment is

experiencing growth in terms of premium income, there is persistent recording of underwriting

losses for the past five years. Above all, the insurance sector has quickly recognised the

compelling need for digitalization as a defining and redefining factor to its success and survival

(Kandiri, 2015). There is a particular opportunity for transformation in the underwriting, fraud

detection, customer relationships, and claims functions in the Kenyan market.

1.2 Statement of the Problem

The revolution of Information Technology and internet facilitates the outstanding performance

of the economy in business sector; through the exchanges of information by using internet and

electronic devices facilitate accessibility of doing business between companies globally

(Mgunda, 2019). A study by Genpact (2014) associates technology with significant positive

monetary impact, and that technology is proportionally more applicable to business functions

that address multiple challenges across the enterprise. Cavalcante (2015) argues that

technology platform potentially represents the creation of a new business model for the partner

companies in the consortium. Deloitte (2019) regards digital innovation as a key to unlocking

new markets. The adoption of digital technology enables insurance companies to reduce the

cost of servicing clients, to tailor products to the needs of specific income groups, and to

streamline internal processes (Zahid, 2020).

Insurers are faced with several global challenges ranging from; lack of a centralised view of

its accumulations risk and exposure to perils globally, weak underwriting performance

6

facilitated by inconsistent risk management practices across the underwriting divisions, poor

customer satisfaction levels, and the growing concerns over insurance fraud (Borselli, 2020).

Kumar, Srivastava, and Bisht (2019) categories challenges confronting the insurance sector

into six strategic areas: Opportunity cost, right advice, time consuming, cost, frauds, and bulky

operations.

Locally, as top insurers struggle to absorb the underwriting impacts of large loss associated

with COVID-19, the impact on profitability is still uncertain. Based, on the 2019 market

capitalization, the top 5 leading insurers in Kenya control the larger market share in the

country. According to The Association of Kenya Insurers (2019), approximately 48 percent of

the underwriting markets share is controlled by the top 5 insurance firms. In the financial year

that ended June 2020, General reinsurance business sunk into the loss-making territory after

the reinsurers incurred Sh3.09 billion in claims and Sh1.95 billion in direct expenses (Insurance

Regulatory Authority, 2020). This resulted in an underwriting loss of Sh1.39 billion million,

driven mainly by claim expenses. It appears that the command is simple, insurers digitize or

die. According to Catlin, Deetjen, and Lorenz (2019), digitization can reduce the cost of a

claims journey by as much as 30%.

Studies have been conducted in attempt to establish the linkage between digitization and

performance of underwriting processes. Yıldırım (2019) analysed the prospects of InsurTech

in insurance business. The study did not link on how InsurTech impacted performance of

underwriting process. Owens (2020) analysed The adoption of Big Data Analytics and

algorithms in motor insurance underwriting practice is robust, proving advantageous for

competition in the market. Soye, Adeyemo, and Adeyemo (2018) addressed how underwriting

capacity affected the income of insurance industry in Nigeria. Besides, entirely employing

secondary data from the insurers’ financial records. The study did not incorporate the role of

digitization in underwriting income and asset value. Gakinya (2018) established the influence

of technology as a strategic resource on performance of insurance companies, focusing on

AAR insurance Kenya limited. The study was limited to AAR company hence the need to

survey the top five insurers inorder to make the findings more representative. Mungai (2019)

identified the determinants of the uptake of insurance underwriting of public service vehicles

plying for hire in Kenya.

7

The study focused on government regulations, industry practice, influence of shareholders’

interests but did not assess the extent to which digitization impacted operations of insurance

firms. With the existing scarcity in literature, it is evident that research is conducted in attempt

to establish the effect of technology on underwriting processes within the Kenyan context.

1.3 Purpose of the Study

The purpose of the study was to examine the effect of technology adoption on underwriting

processes among top five insurance companies in Nairobi County.

1.4 Research Questions

1.4.1 How does digitization of claims process affect the underwriting process among the top

five insurance firms in Nairobi County?

1.4.2 What is the effect of digital fraud detection on the underwriting process among the top

five insurance company in Nairobi County?

1.4.3 What is the effect of using customer relationship management system on the

underwriting process among top five insurance firms in Nairobi County?

1.5 Significance of the Study

1.5.1 Management of the Insurance Firms

The management of the insurance firms operating in Nairobi County could find this study

useful in guiding them in the identification critical areas within underwriting that need

technological redress to ensure sustainability of service delivery to the insured.

1.5.2 The Policy Makers

The study findings add value to the leadership of insurance firms in Kenya. The Kenyan

parliament is presented with the opportunity to enact laws that facilitate safe, faster, and

affordable technological adoption within the insurance sector. It also assists the Insurance

Regulatory Authority in the formulation of effective policies that guarantee sound and effective

performance of the insurance sector which can spur the realization of Sustainable Development

Goals and the Vision 2030.

8

1.5.3 The Academia and Researchers

Research on the subject remains scanty within the context of the technology use in the

underwriting procedures. This is part of concerted effort to assess the position of technology

uptake among the insurers with the perspective to recommend certain lines of action through

which existing problems such as low uptake, lengthy claim processing, fraud, and customer

complaints can be managed through proper use of technology. Finally, the study findings

would be of value to the academicians and other researchers as it would provide the base for

further research in the area of techinsurance.

1.6 Scope of the Study

The study concentrates on the digitization of underwriting processes in the Kenyan insurance

market. Specifically, the study was confined to the digitization of claims process, digitization

of fraud detection, and the adoption of customer management system. It covers the top 5

insurance firms operating in Nairobi market. According to the Association of Kenya Insurers

(2019), approximately 48 percent of the underwriting markets share is controlled by the top 5

insurance firms. The target population is 1174 employees of the five underwriters. A sample

of 298 was derived from the staff of: Jubilee, Britam, APA, CIC, and ICEA Lion insurance

companies. The study was conducted between September 2020 and July 2021.

1.7 Definition of Terms

1.7.1 Technology

Technology refers to the technical aspects of the software and hardware required to adopt and

utilize digitization of core business processes to enhance operational efficiency (Carroll, 2017).

1.7.2 Insurance

This is the contractual agreement between two parties, the insured and insurer. At an agreed

fee (premium), the insured transfers their risk to a third party, the insurer/underwriter. The

contract between the two parties is binding. Once the contract is bound, the insured is covered

(indemnified) in the event of a loss (Chartered Insurance Institute, 2016).

1.7.3 Underwriting Processes

Underwriting describes the consideration given to a life or general insurance application, to

determine whether a policy applied for should be issued or there are changes to be made

9

depending on the person’s risk profile (Murphy, Mostert F, & Mostert H, 2014). The process

helps in the selection of risks for the insurance company involved in issuance of an insurance

policy to the person in question.

1.7.4 Digital Claim Processing

This is the automation of some tasks such as: following up with the claimant or third party for

missing documentation and validating that all required claim information has been collected

(Tajudeen, Ajemunigbohunb, & Gbenga, 2017).

1.7.5 Digital Fraud Detection

Digital insurance detection is a set of technological activities undertaken by insurers to prevent

money or property from being obtained through false pretenses or deception (Kalwihura &

Logeswaran, 2020).

1.7.6 Customer Relationship Management System

Customer relationship management (CRM) is the combination of practices, strategies and

technologies that underwriters use to manage and analyze customer interactions and data

throughout the customer lifecycle (Hassan, 2018). The goal is to improve customer service

relationships and assist in customer retention and drive sales growth in insurance companies.

1.8 Chapter Summary

This chapter sets the ground for the study detailing the background information, problem

statement and purpose of this study, its significance, scope and definition of terms. In this

chapter, the study highlights the key role played by digitization in the insurance sector,

stressing the need for technology uptake in addressing matters in consumer relationship

management, fraud prevention, and effective handling of the underwriting operations. Chapter

two presents review and analysis of literature in relation to the effect of technology on the

underwriting processes within the scope of insurance service provision. Chapter three presents

the methodology, which was adopted when accomplishing the study. Chapter four provides

the results and findings while chapter five is about discussion, conclusion and

recommendations based on the research questions.

10

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

The chapter provides review of empirical studies in alignment with the technological adoption

in the underwriting services across global, regional, and local markets. The chapter is

organized based on the research questions under investigation. The first section reviews

literature on digitization of claim processing on the underwriting activities. The section

reviews literature on the effect of fraud detection system on the underwriting processes in

insurance firms. The third section provides analysis of studies concerned with the effect of

using customer relationship management system on the Underwriting process among insurance

firms. The study ends with summary of major themes in the literature.

2.2 Effect of Digitization of Claims Process on Underwriting Processes

Claim is the largest expenses of any insurance company (Olalekan & Sewhenu, 2016). Claims

are filed at the time of maturity or in case of death/disability (Yadav & Mohania, 2015); when

the covered loss or policy event occurs/happens. Therefore, claims management is seen as an

essential tool of image boosting in insurance industry. Excellence in claims handling gives an

insurance company a competitive edge over its competitors. For an insurance company, claims

processing is one of its core activities. It could be said to be the main reason why insurance

companies are established. Investigating, paying and recording claims data is crucial to any

insurance company’s financial stability (Dash, Shakyawar, & Sharma, 2019). Managing it

more effectively and efficiently, aligning it with corporate business objectives, and achieving

real-time operational awareness are high priorities of an insurance company. This is because

claims processing touches all part of the organization, affecting competitive positioning,

customer service, fraud management, risk exposure, cost control and Information Technology

infrastructure (Ogunnubi, 2018). This section reviews literature in connection with claims

investigation, claims processing, and claims settlement with the aid of automation models

within the insurance sector.

2.2.1 Digitized Claim Investigation

Claim is a formal request by a policyholder to an insurance company for cover or compensation

for a specified loss or policy event (Ntwali, Kituyi, & Kengere, 2020). The Claims

11

Investigations process is one in which Insurance Companies, Insurance Examiners, or

Investigators obtain information to evaluate a claim. As a result, it may require perusing

documents, locating witnesses, visiting and interviewing people, inspecting property such as

vehicles, accident sites and physical locations to name a few. The insurance company validates

the claim and, once approved, issues payment to the insured or an approved interested party

on behalf of the insured (Khurramov, 2020).

In some cases, the insurer may not have full facts of the claim and is unable to make a decision

on a claim. The company may therefore appoint an investigator, to carry out investigations and

file a report to the insurer. This is mainly for motor and liability claims. Either for health

insurance, the insured or the injured person might report the claim to the insurer. Once the

insurer opens a file, the insurer will assign it to a claims adjuster. The adjuster is the person

who will investigate the facts of an accident and negotiate a settlement of the claim (Patil &

Abhyankar, 2019). Investigations are also necessary if a claim is suspected to be fraudulent.

The nature of other claims requires an insurer to appoint a loss adjuster, to establish liability

and quantum of the claim. This is especially for property claims, including Fire, Burglary,

Domestic Package, All Risks, and Marine among others (Vanguard, 2017).

Anchan, Jathanna, and Marla (2016) aimed to understand the current claim process of existing

health insurance schemes, to identify the barriers in the claim process at the hospital level and

to study the consumer awareness and satisfaction in health insurance. Method employed was

cross-sectional study with convenient sampling, data included time analysis format and

validated questionnaire. Overall there was a delay in query justification followed by pre-

authorization, preparation and faxing. Policyholders were not fully aware about health

insurance, 50 per cent of policyholders knew what Third Party Administrator (TPA) meant and

consumers were not fully satisfied with health insurance. This study aims to incorporate the

effect of digitization in smoothening claim processing among insurers.

Holtz, Hoffarth, and Desai (2015) demonstrated that analyzing claims data equips

microinsurance (HMI) practitioners with valuable insights to improve the client value and

viability of HMI programmes. The study performed a comparative analysis of three South

Asian HMI programmes - run by VimoSEWA, Uplift Mutuals and Naya Jeevan. Overall

findings illustrated that a relatively small number of common illnesses, such as diarrhoea or

12

fever/malaria, along with trauma and accidents, generate approximately 50 per cent of claims

costs, a pattern that invites closer, focused monitoring and deeper analysis. Park, Yoon, and

Speedie (2012) described the Health Insurance Review and Assessment Service (HIRA)'s

payment request (PARE) system that played the role of the gateway for all health insurance

claims submitted to HIRA, and the claim review support (CRS) system that supports the work

of claim review experts in South Korea. The study found that HIRA's two IT systems had a

critical role in reducing heavy administrative workloads through automatic data processing.

Although the return rate of the problematic claims to providers and the error detection rate by

two systems was low, the actual count of the returned claims was large. However,

interpretation of the study results was confined to the Korean population, paving the way to

replicate the same study in the local context.

2.2.2 Claim Processing

According to Machui (2016), claims process commences at underwriting function which is

guided by structured losses experience data. The first stage starts with the verification of

occurrence of loss. The second stage is the verification of proof of loss to make sure that the

loss occurred accidentally and it was insured. The third process is the negotiation stage to find

out. The funding viewpoints, the volume and allocation of claims are assessed. Whereas, the

operational deals with the operating features of a Claims Settlement Procedure, like processing

capacity, claims quantity and outstanding claims register, are assessed. The helpfulness of this

analysis for efficient and effective organization and management of the claims handling

function is obvious. Claims handling procedures is a tool that allows analysis and predictions

of the handling procedures.

Ashturkar (2015) observed that, in the category of settlement of the claims within 30 days,

private sector companies are more competent compared to public insurers. Hence, Private

companies are more competitive and consumer oriented compared to LIC. Yadav and Mohania

(2015) focused on the claim settlement process of life insurance services of LIC of India and

ICICI prudential life insurance company. The study established that the LIC of India claim

settlement process is very much efficient but not that transparent and approachable as claim

settlement process of ICICI Prudential Life Insurance Company. This study builds on these

findings to incorporate insurance firms engaging in life and non-life insurance claims.

13

Olalekan, Ajemunigbohun, and Alli (2017) investigated claims management among selected

insurance companies in Nigeria. The study was conducted in Lagos metropolis, employed a

descriptive survey design using random sampling technique and thus gathered data through the

use of structured questionnaire. The sample population consisted of 127 respondents made up

of claims managers and other members of staff within the surveyed companies. One sample T-

test was adopted in the analysis of collected data. Empirical assessment revealed that the

various claims handling processing have significant effects in the claims management

processes of insurance companies. The findings from study confirmed the significance of the

various claims handling processing in claims management of insurance companies in Nigeria.

The study suggested that future studies should focus efforts at gathering information from the

larger population as related to customers’ experience of insurance claims.

2.2.3 Claim Settlement

The image and efficiency of any insurance company depends upon the satisfaction of their

policyholders in getting their claims processed and settled in time (Ashturkar, 2015). Payment

of claim is the ultimate objective of life insurance and the policyholder has waited for it for a

quite long time and in some cases for the entire life time literally for the payment (Ntwali,

Kituyi, & Kengere, 2020). It is the final obligation of the insurer in terms of the insurance

contract, as the policyholder has already carried out his/her obligation of paying the premium

regularly as per the conditions mentioned in the schedule of the policy document. Thus, the

settlement of claims within time is very important aspect of service to the policy holders

(Gahigi, 2017).

According to Rendek, Holtz, and Fonseca (2015) large complex claims, especially liability

claims may take long to be concluded. Besides, they may involve a lot of correspondence

between the insurance company and claimant and/or the claimant’s advocate. For such claims,

Capiello (2020) elucidates that there may be a lot of manual intervention, and the IT system

may not be flexible enough to capture all the intricacies of the claims. Further, general

insurance claims are paper-based to a large extent; therefore, automation may be only partial.

In addition, interfaces between insurers and service providers may not be integrated, which

may result to poor claims tracking and lack of management information (Kimura, Saton, Ikeda,

& Noda, 2016).

14

Claims managers need to maximize the use of information technology, in order to reduce

claims processing cycle, thus enhancing efficiency and customer satisfaction. Ineffective IT

governance and control is likely to be the main cause of the negative experiences many

organizations and especially insurance firms have had with the use of IT, including lost

business, damaged reputations, weakened competitive position, inability to meet deadlines,

failed or aborted projects, budget overruns and poor returns on investments (Ostagar, 2018).

Yadav and Mohania (2015) focused on the claim settlement process of life insurance services

of LIC of India and ICICI prudential life insurance company. The study was based on the

secondary data collected from IRDA and research papers from various journals. The study

concluded that in both LIC of India and ICICI prudential life insurance company followed

proper claim settlement process. LIC of India claim settlement process is very much efficient

but not that transparent and approachable as claim settlement process of ICICI Prudential Life

Insurance Company. Yusuf and Ajemunigbohun (2016) assessed the effectiveness, efficiency

and promptness of claims handling process within the Nigerian insurance industry. The study

concluded that claims handling procedures should be managed promptly to evade shortfall in

operational objectives of organization.

Van Jaarsveld, Mostert, and Mostert (2019) paid special attention to the importance of the

claims handling factors of liability insurance, how often the stipulations of liability insurance

policies are adjusted by the short-term insurers to take the claims handling factors into

consideration, as well as the problem areas which short-term insurers may experience during

the claims handling process. Feasible solutions to address the problem areas are also discussed.

De Beer, Mosterst, and Mostert (2015) embodied the improvement of financial decision-

making concerning the claims handling process of engineering insurance. The questionnaire

was sent to the top 10 short-term insurers in South Africa that were providing engineering

insurance. The empirical results focused on the importance of various claims handling factors

when assessing the claims handling process of engineering insurance, the problem areas in the

claims handling process concerned, as well as how often the stipulations of engineering

insurance policies are adjusted to take the claims handling factors into account.

15

Owolabi, Oloyede, Iriyemi and Akinola (2017) investigated the nexus between risk

management and profitability of insurance Company. Findings from regression analysis

disclosed that financial risk management practices, operational risk management practices and

strategic risk management practices have a positive and significant effect on the profitability

of insurance firm. The present study transcends the spectrum of management to focus on digital

strategies in safeguarding insurance firms against fraudulent activities. Anigma and Mwangi

(2017) performed a cross-country on effects of underwriting and claims management practices

on the performance of insurance firms in Kenya, Uganda and Tanzania. Result indicated that

underwriting and claims management practices by non-financial performance are directly and

significantly associated, whereas, the reverse is the case when compared with financial

performance. The model used in the study focused only on underwriting and claims

management practices as a determinant of firm performance of P and C insurance firms in East

Africa. However, there are other insurance risk management practices like pricing and

reinsurance as well as other factors such as liquidity, leverage, investment income among

others, which may have an influence on performance which were not considered and the

inclusion of these variables in future studies would make the findings more robust.

2.3 Effect of Digital Fraud Detection on the Underwriting Process

Insurance fraud is any act committed with the intent to obtain a fraudulent outcome from an

insurance process (Ghorbani & Farzai, (2018). According to the Association of Certified Fraud

Examiners (2018), insurance fraud is the most practiced fraud in the world, and for the third

consecutive time in six years, SAS Coalition (2019) reports that insurers have reported an

increasing amount of suspected fraud. It is hard to reduce the fraud problem as the insurance

business by its very nature is susceptible to fraud. Certified Fraud Examiners (2018) explains

that the large accumulation of reserved funds that are available to pay for loss claims, make

insurance companies attractive for take over and loot schemes. Bodaghi and Teimourpour

(2018) identified that there are two broad types of fraud schemes, namely opportunistic and

professional fraud, alternatively known as soft and hard fraud, respectively. Insurance fraud

falls under the broad category of financial fraud, which consists of other common frauds such

as credit card fraud, money laundering, corporate financial fraud and health-care insurance

fraud. The challenges presented in fraud detection are imbalanced class distribution, lack of

sufficient centralized data and costly black-boxed solutions.

16

2.3.1 Fraud in Insurance Sector

Insurance fraud is a serious and growing problem, and there is widespread recognition that

traditional approaches to tackling fraud are inadequate (Morley, Ball, & Ormerod, 2018).

Insurers are seeing an increase in fraudulent cases and believe awareness and cooperation

between departments is key to stopping this costly problem Insurers indicate that claims (68%)

and underwriting (43%) departments need to be more engaged. Compared to 2016, Callaway,

Kueker, Barker, Dion, Allen, and Kocisak (2019) maintain that there is no change in the

perceived need for fraud engagement in claims departments. However, fraud engagement in

underwriting departments has increased from 30% to 43%. Fighting fraud is still a manual

operation within many organizations, making it a time consuming and error-prone process.

Studies of insurance fraud have typically focused upon identifying characteristics of fraudulent

claims and claimants, and this focus is apparent in the current wave of forensic and data-mining

technologies for fraud detection (Morley, Ball, & Ormerod, 2018). As a result, an alternative

approach is to understand and then optimize existing practices in the detection of fraud. An

ethnographic study by Salim and Hamed (2018) explored the nature of motor insurance fraud-

detection practices in two leading insurance companies. The results of the study suggested that

an occupational focus on the practices of fraud detection can complement and enhance forensic

and data-mining approaches to the detection of potentially fraudulent claims. This necessitates

a study of this nature especially in developing countries such as Kenya.

The Tunisian Federation of Insurance Companies (FTUSA) is currently working in

collaboration with the authorities concerned, to create an agency to fight against fraud in the

sector, particularly in motor insurance, according to the FTUSA president, Mr Habib Ben

Hassine. In July 2020, the Insurance Regulatory Authority of Uganda (2020) added mobile

phone as a new payment platform for Motor Third Party Insurance to supplement walk-ins and

bancassurance. The new digitized mobile payment platform, according to Insurance

Regulatory Authority (IRA) will help curb fraud in the industry as well as promote

convenience (Mukooza, 2020). Wine (2015) postulates that the Kenya’s insurance regulatory

authority is rallying on shared data systems to counter against health insurance fraud in the

sector.

17

2.3.2 Fraud Detection

The machine learning (ML) approach to fraud detection has received a lot of publicity in recent

years and shifted industry interest from rule based fraud detection systems to ML-based

solutions. Insurance fraud investigation is majorly performed using two approaches, the

Machine Learning based solution and the Rule-based approach. In comparison, the rule-based

approach entail using algorithms that perform several fraud detection scenarios, manually

written by fraud analysts. Today, legacy systems apply about 300 different rules on average to

approve a transaction. That is why rule-based systems remain too straightforward. They require

adding/adjusting scenarios manually and can hardly detect implicit correlations. On top of that,

rule-based systems often use legacy software that can hardly process the real-time data streams

that are critical for the digital space; ML-based fraud detection. However, there are also subtle

and hidden events in user behavior that may not be evident, but still signal possible fraud.

Machine learning allows for creating algorithms that process large datasets with many

variables and help find these hidden correlations between user behavior and the likelihood of

fraudulent actions. Another strength of machine learning systems compared to rule-based ones

is faster data processing and less manual work. For example, smart algorithms fit well with

behavior analytics for helping reduce the number of verification steps.

The digital transformation is of increasing relevance for insurance companies’ business

models. It leads to opportunities as well as challenges, especially for IT departments as core

enablers or preventers. Against this background, the aim of this paper is to provide

a comprehensive overview of digital technologies (e.g., artificial intelligence, cloud

computing) and the resulting use cases for the insurance industry. To this end, Eckert and

Osterrieder (2020) conducted a review of academic articles, industry studies and publications

of the supervisory authorities. The study point to the resulting requirements for an insurer’s IT

and find many interdependencies between the digital technologies. The results therefore

emphasize the importance of a holistic digital strategy.

Literature differentiates data mining and machine learning into supervised, unsupervised,

hybrids or semi-supervised methods. As supervised techniques require the data to be labeled

for building a training set, unsupervised techniques will deal with data based on group or

statistical outlying behavior. The unsupervised methods are a piece of technology to identify

18

potentially fraudulent transactions, that additional require the use of expertise to determine the

legitimacy of the claims. Although fraud detection research is a relatively large field, most of

the studies consider outlier detection as the primary tool (Vineela, Swathi, Sritha, & Ashesh,

2020).

2.3.3 Anti-Fraud Solutions for Insurance Claims

Multiple data analytics approaches can mitigate insurance fraud related risks. Wine (2015)

notes that each type of anti-fraud measure has certain advantages and limitations which need

to be carefully considered along with the needs of each individual insurance company before

being implemented. Advanced systems are not limited to finding anomalies but, in many cases,

can recognize existing patterns that signal specific fraud scenarios. There are two types of

machine learning approaches that are commonly used in anti-fraud systems: unsupervised and

supervised machine learning. They can be used independently or be combined to build more

sophisticated anomaly detection algorithms. Supervised learning entails training an algorithm

using labeled historical data. In this case, existing datasets already have target variables

marked, and the goal of training is to make the system predict these variables in future data.

Unsupervised learning models process unlabeled data and classify it into different clusters

detecting hidden relations between variables in data items.

Bogaghi, Modares, and Teimourpour (2017) has put forward a new approach for identification,

representation, and analysis of organized fraudulent groups in automobile insurance through

focusing on structural aspects of networks, and cycles in particular, that demonstrate the

occurrence of potential fraud. Suspicious groups have been detected by applying cycle

detection algorithms (using both DFS, BFS trees), afterward, the probability of being

fraudulent for suspicious components were investigated to reveal fraudulent groups with the

maximum likelihood, and their reviews were prioritized. The actual data of Iran Insurance

Company is used for evaluating the provided approach. As a result, the detection of cycles is

not only more efficient, accurate, but also less time-consuming in comparison with previous

methods for finding such groups.

19

De Zoete, Sjerps, Lagnado, Fenton (2015) have found how the use of a Bayesian Network can

interpret the existing evidence in some linked crimes; in fact, they indicate that how this

method can show the similar dependencies and links between crimes in order to identify the

key people. Kose, Gokturk, and Kilic (2015) studied, implemented and evaluated a new

framework for detecting the fraudulent cases involved in these claims, and developed a

structure for introducing new types of fraud. Moreover, used the well-known methods such as

AHP and EM unsupervised ranking to detect abnormalities and increase the accuracy of the

framework. To sum up, although prevalent fraud detection methods, along with

aforementioned weaknesses, are capable of coping with opportunistic fraudulent activities, and

the least number of them have focused on organized collaboration of perpetrators

(sophisticated fraud), our work is completely different.

Kalwihura and Logeswaran (2020) proposes a data pre-processing technique, particularly a

fraud behavior feature engineering approach, to improve the overall performance of prediction

models. The behavior being assessed is be based on the RFM model along with an additional

behavior analysis related to policy expiration. Furthermore, an ensemble feature selection and

modeling is used to deal with the high dimensionality problems that the feature engineering

approach brings along with it, as well as the class imbalance problems. The proposed approach

shows a 56.2% increase in the F1-meaure, compared against the previous published stat-of-

the-art results.

2.4 Effect of Using Customer Relationship Management System on the Underwriting

Process

According to Nagalakshmi and Subramanian (2016), customer relationship management

becomes more important of market but insurance sector; customer relationship management

cannot be achieved without having an effective procedure for redressing the complaints of

dissatisfied customers. The section reviews literature in line with customer relationship

management, it looks at empirical studies linked to sales and customer service CRM Solutions,

and customer complaint management.

20

2.4.1 Customer Relationship Management

Customer information management is critical to understand the breadth of relationships with

customers, the value of customers, and customer needs and preferences (Srinivasa &

Muramalla, 2020). It is imperative that insurers aggregate their customer information to fulfill

these projects and drive tighter relationships with customers (Assad, 201). Without having this,

insurers are crippled, not being able to make accurate decisions on how to treat customers,

ensure customer value, improve marketing and sales effectiveness, ensure positive customer

experiences, and protect their customer base from churn. Customer intelligence must be in

place, and will be a strategic asset for companies that complete customer data integration and

apply customer analytics to their customer data.

CRM in this industry is one of the factors that can affect the supply and demand for life

insurance. Brofer, Rezaeian, and Shokouhyar (2016) suggested in their research that to

maintain customers in life insurance, the company attempts to transform behavioral loyalty of

these customers to attitudinal loyalty through establishing more communications and

interactions with them; this means managing customer relationships in life insurance industry.

The importance of CRM as a comprehensive and strategic process for maximizing customer

value is emphasized by the organization (Kumar, 2017). Accordingly, studies carried out in

relation to the subject of this research are presented as follows.

In a research titled Implementation of CRM Processes in Life Insurance Sector: A Customers’

Perspective Analysis, Kannan & Vikkraman (2016) stated that CRM processes represent the

stages involved in customer relationship management, with a centralized trend from customer

engagement to customer retention. This research analyzed customers’ perspective on CRM

implementation processes by life insurances. The results also indicated that today, life

insurance companies need to develop CRM processes to attract and maintain customers as well

as profitability.

Using Data Mining Techniques, Brofer, Rezaeian, and Shokouhyar (2016) provided an

appropriate model for customer segmentation based on some of the most important financial

and demographic characteristics as factors affecting indices of customer lifetime value (RFM).

In the proposed process of this research, which was implemented in Saman Insurance

Company, after determining values of indexes of the RFM model, including recency,

21

frequency and monetary in 180000 customers and weighting them using hierarchical analysis,

the optimal number of cluster based on silhouette index and the impact of RFM indexes were

determined using the two-step algorithm. In the next step, customers’ clustering was conducted

using the K-means method. Also, key and valuable customers of the company were identified

by prioritization of clusters based on RFM indexes. Using a case study of Iranian insurance

firms, Ziaeifar & Nazeri (2014) investigated the effect of services quality and customer

relationship management on customer loyalty. For this purpose, 120 customers of Iran

Insurance were selected using convenience sampling. The results indicated that service quality

and customer relationship management are respectively 61% and 47% effective on customer

loyalty.

Brain (2015) used a case study of a UK car insurance company to investigate the relationships

among price aggregator (re-intermediation) purchase channel, purchasing habits, marketing

response models, marketing mix variables, business models, and strategic customer

relationship marketing. A wide range of statistical models and data mining tools were applied

to this research, including vector autoregressive (VAR) modelling, general linear regression,

quantile regression, autoregressive, moving average; autoregressive integrated moving

average, Autoregressive conditional heteroskedasticity (GARCH), logistic regression;

decision trees and neural networks models. These methods allowed the researcher to better

understand the new aggregator enriched environment. The analyses showed that price

aggregator channel significantly interact with other channels in influencing the customer

retention rates and life time values available to the company and hence its future growth and

profitability.

2.4.2 Lead Management and Sales

Customer relationship management (CRM) has been a growing priority among life insurers

during the past 10 years. However, unlike the early days when suites were the primary solution

option, insurers are now opting for targeted solutions to support vertical processes unique to

managing field sales, agent and broker management, and customer service via the call center.

By employing CRM, life insurers can improve the relationships with their sales network,

enhance sales efficiency and improve customer experiences. Buttle and Maklan (2015) assert

that empowering the channels with more customer information (including customer analytics

22

and a whole view of the relationship with the customer) and tools to assist in the sales process,

insurers can drive more profitability in sales and customer service processes.

Knowledge related to leads was investigated by Świeczak and Łukowski (2016), as well as

transaction and activity information that could be tied to leads. Empirical research was

conducted through interviews with sales and marketing management and participant

observation. It was found that to best support sales’ lead management work at Metso, the CRM

system should be configured to support collaboration between different stakeholders.

Collaboration was seen as an important part of being able to manage leads through information.

The scope of this thesis was restricted to concentrate on sales’ part of the lead qualification

process, between the phases of lead generation and opportunity management. Extending the

scope to take into account the full range of activities and processes related to, for example, the

REAN framework, would give a better understanding of all activities related to sales leads.

Assad (2015) examined the factors that affect the customer satisfaction and accordingly

influence the behavior of the customers and what are the perceptions of the customers about

the service quality in the insurance companies in Palestine. The study was quantitative and

qualitative, interviews were conducted with the main key players of PIS, a questionnaire was

designed for insurance companies’ customers. Out of 180 questionnaire distributed, 168

questionnaire returned for analysis representing 93% of the sample. The study found a very

strong relationship between overall customer satisfaction and each of the dimensions:

Reliability, Technical Quality, Image quality, and Price Quality. Also, customer satisfaction

affects customer behavioral intentions such that the customers with lower satisfaction are

thinking to switch to use a better insurance company’s service or unlikely to re-purchase

insurance services of the same insurance company.

In the post-liberalization of insurance market in Kenya; one factor that contributes to the

overall performance of insurance players is Customer Relationship Management (CRM). Due

to the increase in number of insurance players and rising awareness among customers about

different products, companies in the insurance sector realize the importance of CRM (Kumar,

2017). CRM allows insurance companies to enable the marketing departments to identify and

target their best customers, manage marketing campaigns with clear goals and objectives, and

23

generate quality leads for the sales team. In the present study, author attempts to analyze the

effectiveness of CRM practices in underwriting processes.

Accordingly, Moradi (2017) investigated the impact of CRM factors on tendency for life

insurance demand in Dana Insurance. The study population included all Dana Insurance clients

in Tehran. A number of 384 questionnaires were randomly distributed among them. To test the

hypotheses, Spearman correlation coefficient test was applied in SPSS. Based on the results

obtained from testing the hypotheses, all CRM factors, namely creating and maintaining

relationships with key customers, organizing business processes, knowledge management and

technology-based CRM have a significant and positive effect on tendency for life insurance

demand. In general, it can be claimed that with increasing customer relationship management