effects of contract farming scheme

TRANSCRIPT

Vol. 20 2011 No.1Author Content -Page

Pippy Fawole andK.AThomas

Effects of Contract Farming Schemeon Cassava Production Enterprise inOyo State. Nigeria

1-7

OduO.O.,V.O. Okoruwa,K.O. Adenegan,A;O. Olajide

Determinants of Rice Farmer's Accessto Credit in Niger State. Nigeria

8-20

Suleiman, A. aridTosan Fregene

Analysis of Costs and Returnsof Artisanal Fish Marketing inKebbi State. Nigeria

21-29

Olatomide Waheed Olowa Remittances and Householdand Timothy T. Awoyemi Expenditure in Rural Nigeria

30-43

Adepoju A. O. andF.Y.Okunmadewa

Households' Vulnerability to Poverty in 44-57Ibadan Metropolis. Oyo State. Nigeria

UNIVERSITY

OF I

BADAN LIBRARY

JOURNAL OF RURAL ECONOMICSAND DEVELOPMENT

Vol. 20 2011 No.1

Author Content Page

Pippy Fawole and Effects of Contract Farming Scheme 1-7K.A Thomas on Cassava Production Enterprise in

Oyo State, Nigeria

Odu 0.0., Determinants of Rice Farmer's Acces &-20V.O. Okoruwa, to Credit in Niger State, NigeriaK.O. Adenegan,A.O. Olajide

Suleiman, A. and Analysis of Costs and Returns 21-29Tosan Fregene of Artisanal Fish Marketing in

Kebbi State, Nigeria

Olatomide Waheed Olowa Remittances and Household 30-43and Timothy T. Awoyemi Expenditure in Rural Nigeria

Adepoju A. O. and Households' Vulnerability to Poverty in 44-57F.Y. Okunmadewa Ibadan Metropolis, Oyo State, Nigeria

III .

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.·1f'

Rural Economics andDevelopment

Determinants of Rice Farmer's Access to Creditin Niger State, Nigeria

Odu O.Ol*.,V.O. Okoruwa', K.O. Adenegarr', A.O. Olajide1

JDepartment of Agricultural Economics University of Ibadan, Ibadan

Abstract

The performance of the agricultural sector has been relatively poor considering the attitude ofexisting financial institutions to the support of the sector. Informal credit supply is limited whileformal credit supply is often inaccessible to smallholder farmers. Therefore, borrower'scharacteristics that determine access to formal and informal sources of credit were examined.Data collected by the Africa Rice Centre from Niger State in 2009 were used. Multi-stagesampling technique was used to obtain a sample of 373 out of 470 rice farmers from whominformation was collected. Descriptive statistics and multinomial logit model were then used toanalyse the data. Results revealed that agricultural credit programmes and village residents in theformal and informal credit sectors respectively were the accessible sources of credit. The resultsalso revealed that access to formal credit was significantly increased by experience in ricefarming, expenses on fertilizer input and rice income while access to informal credit wassignificantly increased by gender, duration of village residency, experience in rice farming andexpenses on fertilizer input. It is recommended that a suitable credit support programme foraccess to formal credit should be introduced.

JEL Classification Code: Q12, Q14

Keywords: Access to credit, Determinants, Rice farmer, Niger State

*Correspondence E-mail: [email protected]; Telephone number: +2348033119504

Introduction meeting operating costs during the cultivationseason (Iqbalet al., 2003). The lack of accessto creditor a given source of credit can bedefined as when the maximum credit limit forthat source of credit is zero and access to

Credit has a significant role to play inincreasing farm productivity because thecultivation of most agricultural products forexample paddy involves a high cash outlay for

8

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No. J

credit exists when the maximum credit limitfor that credit source is positive (Diagne,1999). Access to credit could increase thewillingness of farming households to adoptmore farming technologies resulting inincreased production as well as increasedincome (Li and Zhu, 2007). The two mostcritical periods when credit is needed duringthe season are at pre-planting and harvesting(Akpokodjeet al., 2001), hence, the acutenessof credit needs at different times during thecultivation season. Furthermore, credit is notonly needed for farming purposes, but also forhousehold consumption expenditure,especially during the off-season period. Underthe Structural Adjustment Programme (SAP),the Nigerian Agricultural and CooperativeBank (NACB) set up in 1988 special creditschemes to boost rice production (CBN,2006). Under the scheme, the number ofloans granted for rice production increasedfrom three to five thousand seven hundred andeighty approved loans in 1989 (Akpokodjeetal., 2001). Later on in 1989, the governmentlaunched an agricultural policy for self-sufficiency in rice production for a ten yearsperiod. In 2004, funding for implementing thePresidential Initiative on Rice project wasaugmented from the additional ten percenttariff on imported rice, apart from normalbudgetary provisions for the project (ProgressReport on Presidential Rice Initiative, 2004).The introduction of these policies bysuccessive governments underscores the factthat sustainable economic growth cannot beachieved without putting in place well-focused programmes to increase the access offarmers to factors of production, especiallycredit.

In Nigeria, the performance of theagricultural sector has been relatively poorconsidering the attitude -of the existingfinancial systems to the support of theagricultural sector. Formal credit institutions

are usually not located within the reach ofrural farmers and there is insufficientinformation on the formal agricultural creditsector among the rural farming population.This situation discourages most rural farmersfrom patronising the formal credit sectorwhich has resulted in an over-dependence onthe informal credit sector (Adebayo andAdeola, 2008). In addition, formal creditinstitutions impose credit limits for differentoperations without detailed knowledge of theoperations. These ceilings lead to imbalancesin credit supply during the farming seasonwhich results into farmers being prone tocredit constraint conditions. Smallholder ricefarmers usually have a large household size tocomplement their farm labour needs whichincreases their household dependency ratio asthey have to spend more on familyconsumption. This increased familyconsumption has adverse effect on theiraccess to formal credit facilities because ofthe high risk of default. Coupled with this isthe relatively small size of many rice farms inNigeria, a factor that is also related to thelimited access of farmers to the credit market.Short-term seasonal loans from informalsuppliers of credit which are more readilyavailable to farmers however create uniquelimitations for the level of projects that can beundertaken such that most rice farmersexperience credit constraint early in theplanting season (Adebayo and Adeola, 2008).The willingness of the borrower to payinterest rate and/or collateral still does notplace the right to fix the maximum credit limitin his or her hand. Lenders often fix themaximum credit limit based on theirwillingness to lend and not their ability as

.they put into consideration various criteriasuch as the risk of default and characteristicsof borrowers (Diagne, 1999). Therefore,access to credit is affected by certain variablessuch as availability and eligibility criteria of

9

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

credit programs. In other words, access ismore of a supply-side issue related to thepotential lender's choice of the maximumcredit limit (Diagne, 1999).Furthermore, taking a look at available creditsources in both the formal and informal creditsector, it has been discovered that thoughcredit is important for sustainable agriculturaldevelopment, there still exists a gap betweenits demand and supply as induced by certainfactors. It is therefore the contention of thisstudy that there is insufficient information asto these factors that determine the access offarmers to formal and informal credit. Thecontribution of this study is therefore toprofile the credit sources accessible to andused by rice farmers in the state and todetermine the factors that would influenceaccess to formal and informal credit sources.Again, Niger state has been discovered to

. account for the largest share of creditrecipients from informal credit sources in asurvey conducted by Erenstein et aI., (2003).This study is based on the research need forinformation on financial markets that meet thepeculiar demands of the rural farminghousehold and to provide empirical evidenceon the determinants of access to credit bysmallholder farming populations. The rest ofthe paper has been organized into foursections. Next, it addresses the logic behindthe concept of credit access while thefollowing section would then specify theempirical model and description of data. Adiscussion of the results would then followwith a conclusion.

2. Theoretical frameworkRational choice theory is an approach

used by social scientists to understand humanbehavior and it has been the dominantparadigm in economics. However, in recentdecades it has become widely used in otherdisciplines in the social sciences (Green,

2002). The theory of rational choice considersthe choice behavior of one or more decisionmaking units which could be consumers orfirms (farms). Rational choice theoriesrepresent preferences with a utility function.In this case utility is the ability of a good orservice to satisfy a particular human want.The basic assumption of utility theory is thatthe decision making unit in this case a farmeralways chooses the alternative for which theexpected value of the utility is maximum. Forexample a crop farmer is faced with thedecision of which crop to produce or of howmuch of his farm resources such as land andlabour should be used in cultivating rice asopposed to some other crop like maize. Therational choice approach to this problem isbased on the fundamental premise that thefarmer's choice would be based on thosechoices that would help him or her achieve hisor her objective of maximizing profit andminimizing cost given all other factors thatare beyond control. Therefore the rationalchoice theory is based on the followingaxioms regarding consumer preferences.These are that the consumer faces a known setof alternatives, secondly for any pair ofalternatives (A and B), the consumer eitherprefers A to B, prefers B to A, or is indifferentbetween A and B. Thirdly, if a consumerprefers A to Band B to C, then he or shenecessarily prefers A to C but if he or she isindifferent between A and B and indifferentbetween Band C, then he or she is necessarilyindifferent between A and C. In addition, ifthe consumer is indifferent between two ormore alternatives that are preferred to allothers, he or she will choose one of thosealternatives, with the specific choice fromthem remaining indeterminate. The utilityfunction has certain properties. The first isthat the change in utility associated with asmall increase in the quantity of a goodconsumed i.e. marginal utility is positive. The

10

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

second is that of diminishing marginal utilitywhich states that the positive marginal utilityof each good gets smaller and smaller as moreof the good is being consumed. A simpleexample of a utility function is given aconsumer who purchases two goods. Let xdenote the number of units of good Aconsumed and y denote the number of units ofgood B consumed. The utility function of theconsumer is given by the following equation:U = (x,Y) (1)

where the function U assigns a number to anygiven set of values for x and y.The basic rational choice model assumes alloutcomes are known with certainty. However,this basic model has been extended to accountfor uncertainty. For instance, in the decisionto give a loan to a smallholder farmer, thelender is assumed to consider the likelihood ofthe borrower not being able to repay the loan(pA) or being able to repay based (pH) oncertain factors. These are two possibleoutcomes. There is a 100% chance that eitherA or B would occur. The lender wouldmaximize expected utility which is the sum ofutility in each outcome weighted by theprobability that the outcome would occur.

pA t pH = 1 .......... (2)

Response models have been used in rationaldecision making for which the set ofalternatives must be mutually exclusive andfinite. In these models, decision making unitsare assumed to make decisions based on theobjective of utility maximization (Hausmanand McFadden, 1984). The analytical modelscommonly used include the binary logit andprobit models, nested logit model,

multinomial logit model and multinomialprobitmodel.

3. Methodology

3.1 Study area

The study area, Niger State liesbetween the latitude of 3.20' east andlongitude 8 and 11.3' north. It is bordered tothe north by Sokoto State, west by KebbiState, south by Kogi and south-west by KwaraState. Kaduna and Federal Capital Territoryborder the State to both north-east and south-east respectively. The State has a commonboundary with the Republic of Benin alongNew Bussa, Agwara and Wushishi LocalGovernment Areas. The state capital is Minnaand there are twenty five local governmentareas. 91 per cent of village households inNiger State are engaged in rice production(Erenstein et aI., 2003).Niger State also happens to be in the NorthCentral zone which is the largest producer ofrice in Nigeria accounting for 47 per cent ofthe total rice output in 2000 (Akpokodje et aI.,2001). The state experiences distinct dry andwet seasons with annual rainfall varying from1,100mm in the northern part of the State to1,600 mm in the southern parts. Themaximum temperature is recorded betweenMarch and June, while the minimum isusually between December and January. Therainy season lasts for about 150 days in theNorthern parts of the state and about 120 daysin the Southern parts of the State. Generally,the climate, soil and hydrology of the Statepermit the cultivation of most of Nigeria'sstaple crops and still allows sufficientopportunities for grazing, fresh water fishingand forestry development. With respect toproduction levels, the highest hectarage ofrice under cultivation is that of rain-fedlowland while the lowest is that of mangroveswamp (Akpokodjeet aI., 2001). Rice

11

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

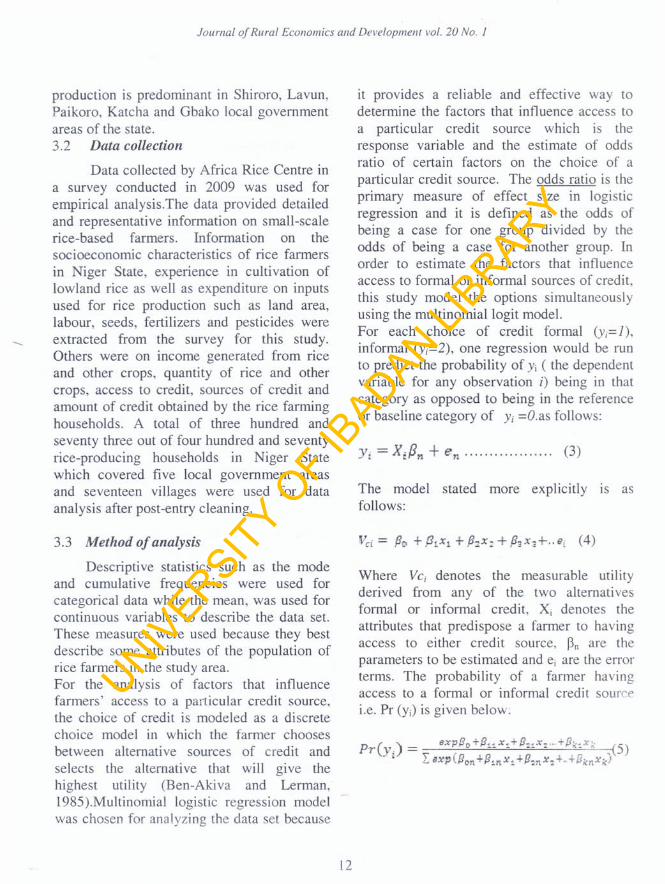

production is predominant in Shiroro, Lavun,Paikoro, Katcha and Gbako local governmentareas of the state.3.2 Data collection

Data collected by Africa Rice Centre ina survey conducted in 2009 was used forempirical analysis.The data provided detailedand representative information on small-scalerice-based farmers. Information on thesocioeconomic characteristics of rice farmersin Niger State, experience in cultivation oflowland rice as well as expenditure on inputsused for rice production such as land arealabour, seeds, fertilizers and pesticides wer~extracted from the survey for this study.Others were on income generated from riceand other crops, quantity of rice and othercrops, access to credit, sources of credit andamount of credit obtained by the rice farminghouseholds. A total of three hundred andseventy three out of four hundred and seventyrice-producing households in Niger Statewhich covered five local government areasand seventeen villages were used for dataanalysis after post-entry cleaning.

3.3 Method of analysis

Descriptive statistics such as the modeand cumulati ve frequencies were used forcategorical data while the mean, was used forcontinuous variables to describe the data set.These measures were used because they bestdescribe some attributes of the population ofrice farmers in the study area.For the analysis of factors that influencefarmers' access to a particular credit source,the choice of credit is modeled as a discretechoice model in which the farmer choosesbetween alternative sources of credit andselects the alternative that will give thehighest utility (Ben-Akiva and Lerman1985).Multinomial logistic regression model -was chosen for analyzing the data set because

it provides a reliable and effective way todetermine the factors that influence access toa particular credit source which is theresponse variable and the estimate of oddsratio of certain factors on the choice of aparticular credit source. The odds ratio is theprimary measure of effect size in logisticregression and it is defined as the odds ofbeing a case for one group divided by theodds of being a case for another group. Inorder to estimate the factors that influenceaccess to formal or informal sources of creditthi.s study mo?el the options simultaneousl;usmg the multmomiallogit model.~or each choice of credit formal (y;=l),mformal (y;=2), one regression would be runto predict the probability of Yi ( the dependentvariable for any observation i) being in thatcategory as opposed to being in the referenceor baseline category of Y; =O.as follows:

}1. =X.D + e (3)t ~jJn n .

The model stated more explicitly is asfollows:

W~ere Vc; denotes the measurable utilitydenved from any of the two alternativesformal or informal credit, Xi denotes theattributes that predispose a farmer to havingaccess to either credit source, Pn are theparameters to be estimated and e, are the errorterms. The probability of a farmer havinzbaccess to a formal or informal credit sourcei.e. Pr (yD is given below.

12

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

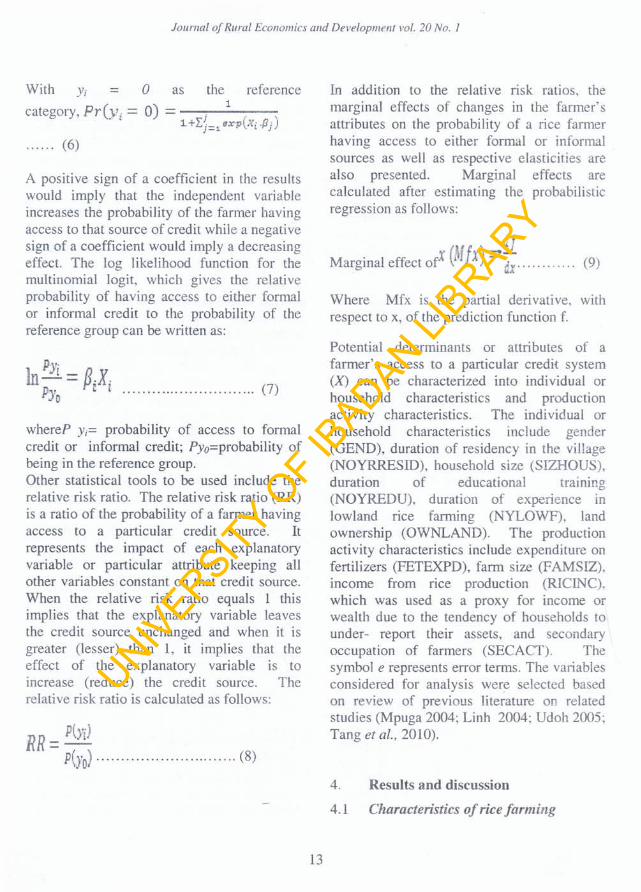

With Yi 0 as the reference1

category, Prt y, = 0) = i ( ,l+Lj=~ exop }fi'P.!)

...... (6)

A positive sign of a coefficient in the resultswould imply that the independent variableincreases the probability of the farmer havingaccess to that source of credit while a negativesign of a coefficient would imply a decreasingeffect. The log likelihood function for themultinomial logit, which gives the relativeprobability of having access to either formalor informal credit to the probability of thereference group can be written as:

J>.v·In...:.L = p.X.p)' f! (7)

-0

whereP Yi= probability of access to formalcredit or informal credit; PYo=probability ofbeing in the reference group.Other statistical tools to be used include therelative risk ratio. The relative risk ratio (RR)is a ratio of the probability of a farmer havingaccess to a particular credit source. Itrepresents the impact of each explanatoryvariable or particular attribute keeping allother variables constant on that credit source.When the relative risk ratio equals 1 thisimplies that the explanatory variable leavesthe credit source unchanged and when it isgreater (lesser) than 1, it implies that theeffect of the explanatory variable is toincrease (reduce) the credit source. Therelative risk ratio is calculated as follows:

RR = NYi)P(YD) (8)

In addition to the relative risk ratios, themarginal effects of changes in the farmer'sattributes on the probability of a rice farmerhaving access to either formal or informalsources as well as respective elasticities arealso presented. Marginal effects arecalculated after estimating the probabilisticregression as follows:

df. X (MIX') ='"-Margmal effect of .,1 ax" .. .. .. . ... (9)

Where Mfx is the partial derivative, withrespect to x, of the prediction function f.

Potential determinants or attributes of afarmer's access to a particular credit system(X) can be characterized into individual orhousehold characteristics and productionactivity characteristics. The individual orhousehold characteristics include gender(GEND), duration of residency in the village(NOYRRESID), household size (SIZHOUS),duration of educational training(NOYREDU), duration of experience inlowland rice farming (NYLOWF), landownership (OWNLAND). The productionactivity characteristics include expenditure onfertilizers (FETEXPD), farm size (FAMSIZ),income from rice production (RICINC),which was used as a proxy for income orwealth due to the tendency of households tounder- report their assets, and secondaryoccupation of farmers (SECACT). Thesymbol e represents error terms. The variablesconsidered for analysis were selected basedon review of previous literature on relatedstudies (Mpuga 2004; Linh 2004; Udoh 2005;Tang et al., 2010).

4. Results and discussion

4.1 Characteristics of rice farming

13

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No. I

households

Table 1 describes the rice farmers thathad access to the two sources of credit. Thetable shows that 21.8% and 7.0% of malefarmers had access to informal and formalsources of credit respectively.

Female farmers that had credit accessused 18.0% and 1.1% of informal and formalcredit respectively which is in agreement withfindings by Udoh (2005). Only 9.5% and15.3% of those that had access to formal andwith the results of Mpuga (2004). Ricefarmers in the area seemed to be experiencedin the different systems of cultivation withthose that had access to credit having thehighest average of 23 years in lowland ricecultivation of which there was a significantdifference in the mean values of experience inlowland rice cultivation. Access to formalcredit facilities, which were of a highervolume than informal credit facilities, mighthave contributed to increasing the purchasingpower of rice farmers such that they were ableto purchase more of inputs such as fertilizer(W23583.87).

4.2 Credit sources and use by rice farmers

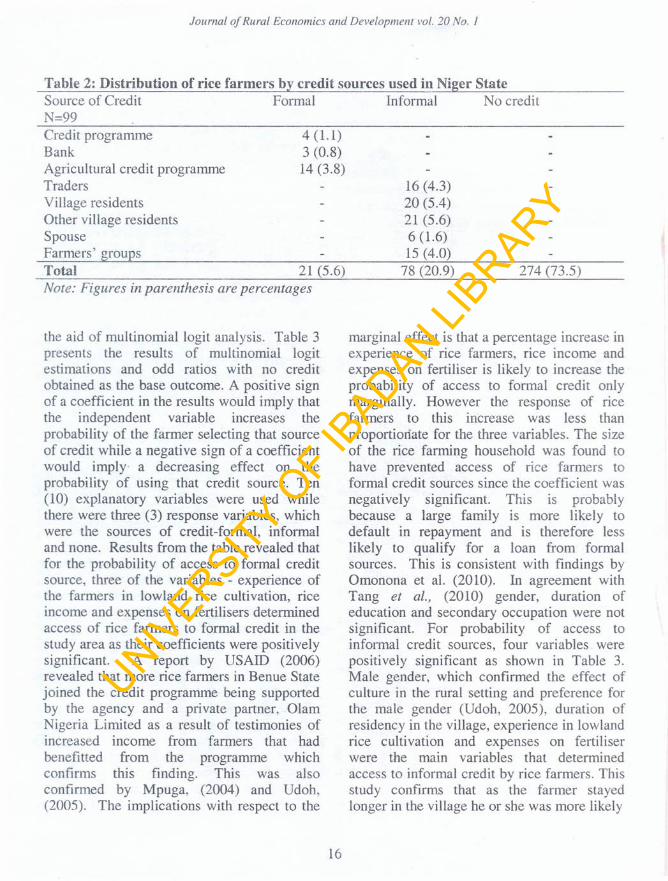

The results presented in this analysisinclude data on the sources of formal andinformal credit used by rice-based farmers,which is highlighted in Table 2. Results fromthe shows only 99 farmers (26.5%) of thesample of 373 farmers had access to creditand of this figure, 21.2% used formal creditsources while 78.8% used informal creditsources. This result is consistent withfindings by Adebayo and Adeola (2008) andTang et al. (2010). The remaining 73.5% ofthe sample of 373 farmers were discoverednot to have had access to any source of credit.The fact that the larger proportion of thesefarmers did not use credit does not mean thatthey had no need for it, rather it is possiblethat the official bottlenecks that formal credit

informal credit respectively were educated upto the secondary school level. The surveyshowed that 80.9% of rice farmers that hadaccess to formal credit and 64.1 % that hadaccess to informal credit however had Islamiceducation. This finding revealed thateducation predisposes farmers to better accessto production credit and high enrolment forIslamic education was probably based on theneed to reduce risk of default as consistent

facilities entailed and the lower volume ofinformal credit facilities must have preventedthese farmers from accessing these creditfacilities. On the supply side of creditservices, farmers lacking sufficient quantityand quality of assets are usually excludedfrom formal credit facilities. Agriculturalcredit programs happened to have been themost preferred source of credit in the formalsector as about 66.7% of farmers using formalcredit subscribe to it. This was followed byother sources such as credit programme(19.0%) and banks(14.3%) in that order ofdescending preference. This is in agreementwith findings from Iqbal et ai., (2003) whoobserved that activities often financed andsupported by banks were agriculturalmarketing rather than production activities. Inthe informal sector, rice farmers preferredresidents from neighbouring villages (26.9%),village residents (25.6%), traders (20.5%),farmers' groups (19.2%) and spouses (7.7%)respectively in descending order ofimportance. This evidence supports theimportant role that communal relationshipshave played in credit support to these small-scale farmers.

4.3 Determinants offarmer's access tocredit

The influence of various variables onthe desired choice of credit compared to thosewho did not obtain credit was determined with

14

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No. 1

Table l:Distribution of rice farmers by socioeconomic and farm characteristicsSocioeconomic characteristics Source of CreditN=373

F-test forequal means

Formal Informal No credit

Proportion of male farmers (%) 7.0 21.8 71.1nl= 284Proportion of female farmers (%) 1.1 18.0 80.9n2= 89Mean Age 46 (4.34) 48 (6.44) 46 (7.40)Mean household size 5 (2.02) 8 (4.35) 9 (4.75)Mean number of years of residence in the 45 (4.55) 48 (6.32) 44 (10.54)villageMean Area of land cultivated to 4.28 (1.41) 2.94 (4.10) 2.98 (4.52)Rice (ha)Education levelsNone (%) 9.5 20.5 48.5Primary (%) 8.9 10.2Secondary (%) 9.5 6.4 10.6Post-secondary (%) 0.7Islamic (%) 80.9 64.1 29.9Mean Years of experience in rice farming 23(7.51) 23 (6.03) 21 (7.69)

Rice productionMean expenses on fertilizer (~ 23583.87

(8662.18)11806.45(6927.71)7277.42(6274.05)10206.67(5228.30)4815.07( 1589.58)306956.50(50612.28)

Mean expenses on herbicide (W1

Mean expenses on seeds(W1

Mean expenses on labour (W1Mean output of rice (kg/ha)

Mean income from rice (W)

1.5510.01 *** '

3.72*

8.67***

4.35**

16675.00 11949.78(9627.48) (8488.26)7591.18 5550.00(7503.02) (5145.61)4301.47 4664.90(3744.86) (4926.99)7136.77 3671.06(4996.39) (4795.62)3692.36 3213.27(1126.42) (2833.24)224605.90 188915.90(101985.6) (94479.78)

29.38***

17.85***

4.48**

2.03**

2.11 *

24.16***

Note: Figures in parentheses are standard deviations;'" 1%" "5%; '10% Significant levels

15UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

Table 2: Distribution of rice farmers by credit sources used in Niger StateSource of Credit Formal Informal No creditN=99Credit programmeBankAgricultural credit programmeTradersVillage residentsOther village residentsSpouseFarmers' groups

4 (1.1)3 (0.8)

14 (3.8)16 (4.3)20 (5.4)21 (5.6)6 (1.6)15 (4.0)

Total 21 (5.6) 274 (73.5)Note: Figures in parenthesis are percentages

the aid of multinomial logit analysis. Table 3presents the results of multinomial logitestimations and odd ratios with no creditobtained as the base outcome. A positive signof a coefficient in the results would imply thatthe independent variable increases theprobability of the farmer selecting that sourceof credit while a negative sign of a coefficientwould imply' a decreasing effect on theprobability of using that credit source. Ten(10) explanatory variables were used whilethere were three (3) response variables, whichwere the sources of credit-formal, informaland none. Results from the table revealed thatfor the probability of access to formal creditsource, three of the variables - experience ofthe farmers in lowland rice cultivation, riceincome and expenses on fertilisers determinedaccess of rice farmers to formal credit in thestudy area as their coefficients were positivelysignificant. A report by US AID (2006)revealed that more rice farmers in Benue Statejoined the credit programme being supportedby the agency and a private partner, OlamNigeria Limited as a result of testimonies ofincreased income from farmers that hadbenefitted from the programme whichconfirms this finding. This was alsoconfirmed by Mpuga, (2004) and Udoh,(2005). The implications with respect to the

78 (20.9)

marginal effect is that a percentage increase inexperience of rice farmers, rice income andexpenses on fertiliser is likely to increase theprobability of access to formal credit onlymarginally. However the response of ricefarmers to this increase was less thanproportionate for the three variables. The sizeof the rice farming household was found tohave prevented access of rice farmers toformal credit sources since the coefficient wasnegatively significant. This is probablybecause a large family is more likely todefault in repayment and is therefore lesslikely to qualify for a loan from formalsources. This is consistent with findings byOmonona et al. (2010). In agreement withTang et aI., (2010) gender, duration ofeducation and secondary occupation were notsignificant. For probability of access toinformal credit sources, four variables werepositively significant as shown in Table 3.Male gender, which confirmed the effect ofculture in the rural setting and preference forthe male gender (Udoh, 2005), duration ofresidency in the village, experience in lowlandrice cultivation and expenses on fertiliserwere the main variables that determinedaccess to informal credit by rice farmers. Thisstudy confirms that as the farmer stayedlonger in the village he or she was more likely

16

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No. I

Table 3: Determinants of farmer's choice of credit sourceExplanatory Variables Formal Credit Source Informal Credit Source

Coefficient RRR Slope Elasticity Coefficient RRR Slope ElasticityEst. Est.(s.e.) (s.e.)

GEND 0.87 2.41 O.OlS 0.03 1.09 2.97 0.123 0.13(1.26) (0.S8)*

NOYRRESID 0.02 1.02 1.22e-04 -3.84e-04 0.06 1.06 0.008 0.01(0.03) (0.02)**

SIZHOUS -0.26 0.77 -0.006 -0.01 -0.11 0.90 -0.014 -0.01(0.09) *,. (0.04)**'

NYLOWF 0.08 1.08 0.002 0.003 0.06 1.07 0.008 0.01(0.03)** (0.03)"

OWNLAND 0.43 1.S4 0.01 0.03 0.03 1.03 0.003 -0.01(0.67) (0.37)

RICINC 7.9Se-06 1.00 1.8Se-07 4. 14e-07 3.36e-06 1.00 S.80e-07 4.3ge-07(4.20e-06)* (2.46e-06)

FAMSIZ 3.28e-OS 1.00 0.001 0.006 -0.2S 0.78 -0.040 -0.04(0.18) 0.12"

NOYREDU -0.07 0.93 -0.002 -0.004 -0.003 1.00 -0.60e-03 0.001(0.10) (0.04)

SECACT 0.22 1.2S 0.006 0.02 -0.11 0.90 -0.016 0.02(0.19) (0.13)

FETEXPD 9.lOe-OS 1.00 2.10e-06 4.62e-06 4.3ge-OS 1.00 S.71e-06 4.03e-06(2.9Se-OS) **. (1.93e-OS)**

Number ofobservations 373Log likelihoodLR chi 2(20) -206.160Pseudo R2 113.83*"

0.216*** Significant at 1% level **Significant at 5% level *Significant at 10% levelNote: The omitted category, (base outcome) in the dependent variables are the farmers who did not have access to credit

17UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

to access informal credit which is factualbecause it was observed that farmers thatborrowed from informal sources had thehighest duration of residence in the villages of48 years. This proved that their familiaritywith the village communities was probably acondition for their using this source of creditas confmned by Diagne (1999) and Udoh(2005). The marginal effects implied that a1% increase in gender, duration of residency,experience and expenses on fertiliser wouldincrease the likelihood of access to informalcredit by 0.12%, 0.01%, and 0.01%respectively. In terms of response, theindications are that the increases lead to lessthan proportionate increase in the probabilityof access to informal credit. Two othervariables however, had a significant butnegative effect on access to informal credit.These include size of rice farming householdand farm size which were found to haveprevented access of rice farmers to informalcredit sources since their coefficients werenegatively significant. These findings inferthat a large farming household would be morelikely to default in loan repayment if care isnot taken due to additional family expenses(Tang et al., 2010) and that the larger the farmsize the more the farmer's likelihood ofhaving access to formal credit sources whichprovide larger loans (USAID, 2006). Resultsfrom this study revealed that access of ricefarmers to formal credit sources was enhancedby higher income from rice farming whichwas considered as assurance that the farmerwould be able to repay the loan on time.Experience in cultivation of lowland rice wasalso shown as being advantageous to securingformal credit facilities as a guarantee that theagricultural project would most likelysucceed. However, accessing informal creditsources was clearly shown to be influenced bygender, with a preference for men andduration of residency in the village. Also, thelevel of familiarity that exists within existing

social groups, family or community settingsfarmers aided access to informal creditsources. This emphasizes the importance ofreliability and openness in all financialtransactions. Expense on fertilizer wasdiscovered to be a key determinant of accessto either of both sources of credit facilities asa major input in rice production. Empiricalfindings revealed that rice farmers in the studypreferred informal sources of creditconfirming the view that banking institutionshave contributed insignificantly to the supplyof credit. Gender considerations in credit usewere found to be biased towards male ricefarmers in the informal sector even though allmale and female farmers were still in theirproductive years.

5. Conclusion

An understanding of the sources ofcredit that are accessible to rice farmers andthe factors influencing their access to formaland informal credit, would help in thepackaging of credit programs targeted at thesefarmers. This paper recognizes the globalimportance of rice and the significantpotential rice market in Nigeria (ProgressReport on Presidential Rice Initiative, 2004).It has therefore provided relevant empiricalevidence in formulating agricultural policiesconcerning agricultural credit access for riceproduction in Nigeria as well as to stimulatesupport for a more conducive businessenabling environment marked by supportivepolicies, and regulations. Information aboutthe factors that influence rice farmer's accessto formal and informal credit would assistgovernment in the formulation of policiestargeted at these farmers. Considering thedynamic nature of the financial servicessector, such policies could offer services thatexpand and complement predominantinformal credit programmes for smallholderfarmers.

18

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No.1

Based on the findings of this study, it isrecommended that credit policies should betargeted at improving access of these farmersto formal credit programmes, which are of alarger volume. Government's efforts shouldbe directed at helping rice farmers increasetheir level of income from rice farming byvalue addition through processing. This wouldincrease the market value of rice resulting inincreased returns from rice production andbetter position these farmers for formal creditfacilities. In addition, necessary intervention

References

Adebayo 0.0. and Adeola RG. (2008).Sources and Uses of Agricultural Creditby Small Farmers in Surulere LGA ofOyo State Anthropologist 10.4: 313-314

Akpokodje G., Lancon F. and Oreinstein Olaf(2001). The Nigerian Rice Economy ina Competitive World: Constraints,Opportunities and Strategic Choices,Nigeria's Rice Economy: State of theArt. WARDA Publication

Ben- Akiva M. and Lerman S.R (1985)Discrete Choice Analysis. The M.I.T. PressCentral Bank of Nigeria. (2006) Microfinance

Policy, Regulatory and SupervisoryFramework for Nigeria: 1-5.

Diagne A. 1999. Determinants of HouseholdAccess to and Participation in Formaland Informal Credit Markets in Malawi.Food Consumption and NutritionDivision. IFPRI.

ErensteinO.F.,Lancon 0., Osiname" andKebbeh M. (2003). Operationalising theStrategic Framework: The NigerianRice Economy in a Competitive World-Constraints, Opportunities and StrategicChoices. WARDA-Africa Rice Centre,Abidjan,

in form of improved access to productioninputs should be implemented as this wouldincrease rice production for better access toformal credit facilities. Formal creditinstitutions need to be readily accessible inorder to contribute more to the developmentof rural farmers. To this end their focusshould be on registering their presence in therural areas with credit programmes that aresuited to the seasonal credit requirements ofthese farmers as a complement to the servicesbeing rendered by the informal sector.

Green S. (2002), Rational Choice Theory: AnOverview: A Presentation at the BaylorUniversity Faculty DevelopmentSeminar on Rational Choice Theory,May 2002

Hausman J. and McFadden D. (1984),Specification Test for the MultinomialLogit Model. Econometrica 52:5 pp1219-40

Iqbal M., Ahmad M. and Abbas K. (2003).The Impact of Institutional Credit onAgricultural Production inPakistan. The Pakistan DevelopmentReview 42.4 Part 1:469-485

Li, Rand Zhu X. (2007). EconometricAnalysis of Credit Constraints of RuralHouseholds and WelfareLoss.Economic Research.2: 146-155

Linh, H. (2004). Effect of Rice FarmingHouseholds in Vietnam: A DEA withBootstrap and Stochastic FrontierApplication. Preliminary Draft,Department of Applied Economics,University of Minnesota

Mpuga P. (2004). Demand for Credit in. Rural Uganda: Who Cares for the Peasants?Paper presentation at the Conference on

Growth, Poverty Reduction and Human

19

UNIVERSITY

OF I

BADAN LIBRARY

Journal of Rural Economics and Development vol. 20 No. I

Development in Africa Centre for theStudy of African Economies

Ogundari K. (2006). Determinants of ProfitEfficiency Among Small Scale RiceFarmers in Nigeria: A Profit FunctionApproach. Poster Paper Presentation atInternational Association ofAgricultural Economists Conference,Gold Coast, Australia, August 12-19,2006

OmononaB.T.,Egbetokun O.A, and AkanbiAT. (2010) Resource Use andTechnical Efficiency in CowpeaProduction in Nigeria. EconomicAnalysis and PolicyAO: 1

Progress Report on Presidential RiceInitiati ve. (2004).

Tang S., Guan Z., Jin S. (2010). Formal andInformal Credit Markets and Rural

Credit Demand in China.Paperpresentation at the Agricultural &Applied Economics Association 2010AAEA,CAES, & WAEA Joint AnnualMeeting, Denver, Colorado.

TiamiyuS.A,Akintola J.O., RahjiM.AY.(201O). Production EfficiencyAmong Growers Of New Rice ForAfrica In The Savanna Zone OfNigeria.AgriculturaTropicaetSubtropica. 43 (2)

Udoh E.J. (2005). Demand and Control ofCredit from Informal Sources by RiceProducing Women of Akwalbom State,Nigeria. Journal of Agriculture andSocial Sciences 1:2 152-155.

US Agency for International Development.2008. Country Report. (2006).

20

UNIVERSITY

OF I

BADAN LIBRARY