effects of discretionary fiscal policy in tunisia… · effects of discretionary fiscal policy in...

TRANSCRIPT

1

Vol. 13, September 2011 Topics in Middle Eastern and African Economies

EFFECTS OF DISCRETIONARY FISCAL POLICY IN TUNISIA: A SVAR MODEL INVESTIGATION

Sarra BEN SLIAMNE1 Moez BEN TAHAR2 Zied ESSID3

INTRODUCTION

We attend a renewed interest toward the effectiveness of discretionary fiscal policy to fight against the fluctuations in the economic cycle and in particular against its downward phases. Do the discretionary measures manage to stimulate the economic activity, or conversely are they more harm than good?

Voices were raised calling again public authorities to resort to an active fiscal policy to help the central banks to avoid that the economic activity slows down. Once more, the role that has to play the fiscal policy in the management of the business cycle, been the object of an animated debate and several questions arise: are the discretionary measures useful or they hurt more than of the good? At what moment are they the most effective? When is it preferable to let, simply, the automatic stabilizers play their roles?

The place as fiscal policy must take in the management of the business cycle has made debate for several years and these fundamental questions were the object of vast literature, as well in the field of the public economy as of the macroeconomics and the econometric studies, and that with the recourse to many methods of quantitative studies.

According to the interventionist approach, we can use sensibly the taxes, the transfers and the public spending to face the fluctuations in the economic activity, in particular as far as these fluctuations are, essentially, owed to disequilibrium of markets and not to changes of factors fundamental as the productivity. Others approach affirm that in general discretionary fiscal policy either are ineffective, or deteriorate the situation, because they are taken at unfavorable moments or create harmful distortions. This last point of view having dominated the debate of these last twenty years, the budgetary policy was relegated in the background behind the monetary policy.

Considering these consideration, this paper throws a new glance on the role of fiscal policy to stimulate economic activities. The main things objective are following them: 1) to apprehend

1 DEFI Université de la Méditerranée Aix Marseille II and LEFA, IHEC Carthage. [email protected] 2 CEMAFI, Université de Nice Sophia Antipolis et LEFA, IHEC Carthage [email protected] 3 CEMAFI, University de Nice Sophia [email protected]

2

the consideration of fiscal shocks in the various empirical approaches 2) to identify the channels of transmission of fiscal shocks 3) to analyze the effectiveness of fiscal policy in Tunisia

We propose, so to send all these questions and to clean the respective merits of the diverse empirical approaches and theoretical. We measure in particular the quantitative impact of the public spending and taxes on the economic activity in Tunisia. For this purpose, we use a structural VAR model.

1 SVAR MODEL AND FISCAL SHOCKS

For some years, the literature saw endowed with a new approach of empirical analysis which prints the main works of the modern macroeconomics; it is the approach the VAR. Indeed, since the works of Sims [1980], this methodology was widely applied for problems relating to the effects of the monetary shocks. On the other hand, few works focused on the effects of the budgetary shocks.

Recently, we attend a development of a theoretical and empirical literature which emphasizes the problem of the efficiency of fiscal policy using SVAR. In this respect, we have three approaches:

• Recursive Approach VAR: this approach tries to identify the budgetary shocks on the bass of the decomposition of Cholesky. It is based on specific hypotheses concerning the dynamics of the variables of the model. Some works based themselves on this approach. Fatàs and Mihov [2001], supposes that the level of the public spending is determined according to the production and the tax revenue. The advantage of this model is its simplicity, but the results are strongly sensitive to the various organizations of variables.

• VAR approach with signs restriction: this approach identifies the shocks through limitations of the signs of impulsion functions. This method was introduced by Faust [1998] and Uhlig [1999] to study the effects of the shocks of the monetary policy and was applied to the budgetary policy by Mountford and Uhlig [2002] and Canova and Pappa [2002]. Contrary to the model the recursive VAR, this approach does not impose restrictions on the linear relations between the canonical residues and the structural shocks, but rather restrictions of sign in the functions of impulses. The advantage of this approach is its capacity to feign early fiscal shocks.

• Structural VAR approach: is applied by Blanchard and Perotti [2002]. It based on the estimation of the multivariate autoregressive vector systems. This approach tries to estimate the impact of the fiscal policy under normal times. The identification of the fiscal shocks cannot be based on event approach which emphasizes the exogeneity of the wars as the element release mechanism of the variations of spending and taxes. The methodology SVAR bases on the exploitation of the information relating to the tax regime with the aim of neutralizing any problem of simultaneous feedback between the budgetary policy and the

3

economic activity which could make biased the estimations and expurgate the results of any economic interpretation.

2 STRUCTURAL VAR MODEL FOR TUNISIA

Contrary to the abundant literature on the effects of the monetary policy, the fiscal policy was, until recently, the object of less attention on behalf of the economists. This lack of interest contrasted with the multiplication of public debates on the macroeconomic effects of the public finances. Whereas there is a consensus on the effects of the monetary policy, the thesis according to which fiscal policy is an effective tool of the economic policy does not make the unanimity within the economists.

Blanchard and Perotti [2002], then Perotti [2004], started again the debate on the effectiveness of fiscal policy by proposing an evaluation of its dynamic effects on the macroeconomic variables, in particular on the GDP using structural VAR model. This methodology allows calculating fiscal multipliers and avoiding specifications inherent to the large macro-econometric models.

2.1 Specification of VAR model

The model is represented by the following relation:

ttt uXLAX += −1)( (1)

Where [ ]′= tttttt RPYGTAX ,,,,

and [ ]′= Rt

Pt

Yt

Gt

TAtt uuuuuu ,,,,

Where, tX , A and tu are respectively the vector of endogenous variables, the matrix of the coefficients to be estimated and the vector of innovations.

Three variables are retained to reveal the impact of the budgetary policy on the economic activity. tY represents the real GDP per capita, tG represents the public spending expressed in

real term and per capita. tTA Represent the net fiscal revenues expressed in real term and per capita. These three variables are introduced into the model in first logarithmic difference.

The variable tP represents price level calculated from the informer of the GDP. Finally

tR represent the short-term interest rate and introduced in first difference. The consideration of these two variables allows controlling the impact of the monetary policy.

The data are extracted from databases IFS, WDI and GFS. The series are in quarterly frequency and covering the period 1980: 1-2008:4. The employment of the quarterly data doubtless constitutes a very strong limit of the modeling the VAR applied to the budgetary policy, this one being defined by a law of annual Finance. The construction of the quarter’s series can thus risk recovering from the pure artifact. Nevertheless, because the government

4

can bend the law of initial Finance during the budgetary year, the intra-annual data can also contain information on the orientations discretionary and probably not anticipated by the budgetary policy. The quarterly frequency of the series also allows to model more faithfully the set of the automatic stabilizers supposing that these forcing the immediate effects inside quarter.

2.2 Definition of structural VAR Model

The direct estimation of the model the canonical VAR does not allow an economic interpretation (performance) of the various equations and the coefficients because the definition of the shocks evoked previously, risks to be biased. Innovations from canonical VAR are correlated. Consequently we use a model a structural VAR, which requires an identification of structural shocks where from the imposition of the constraints of identification stemming from the economic theory.

The canonical residual stemming from the model the reduced VAR represent shocks or impulses the distribution of which is translated by fluctuations in the studied dynamic system. So, the obtained innovations cannot be likened to structural shocks; they represent only the not predictable part considering the information resulting from the past realizations of variables endogenous of the system.

So, by noting te the vector of the structural shocks we have then:

[ ]′= Rt

Pt

Yt

Gt

TAtt eeeee ,,,,ε (2)

TAte A shock of tax revenue, G

te a shock of the public spending, Yte a shock of activity, P

te a

shock of inflation and Rte a shock of monetary policy.

Blanchard and Perotti [2002] stipulate that the residues of revenues and public spending of canonical VAR can be interpreted as a linear combination of three types of shocks:

· The immediate responses inside the quarter of the spending and the tax revenue to the innovations of the GDP, the prices and the interest rate; it is the automatic stabilizers.

· The systematic and immediate discretionary answers of the fiscal policy to the evolutions of the GDP, the prices and the interest rate.

· The discretionary shocks of the fiscal policy which do not result from a particular macroeconomic situation; it is these last shocks which we qualify as “structural shock”. The structural VAR methodology consists in transforming the canonical residues in structural shocks which can be economically interpreted. The orthogonalisation is the technique which allows validating this passage given that the structural shocks are independent, thus orthogonal by nature.

5

2.3 Unit roots Tests

The interest of the modeling SVAR does not limit itself to the optimization of the causal relations. It is possible to identify at least two other information sources convenient to the extension of the knowledge. The first one constitutes a preliminary investigation in the modeling, whereas the second lies in a dynamic operation of the results of the model. These two extensions, upstream and downstream to the model the VAR, are generated by the unique constraint which imposes this type of modeling: the stationary of the selected temporal series. The modeling the VAR can highlight linear relations between several variables only if these last ones are still.

Before estimating the autoregressive model, we beforehand have to determine the order of integration of the series and the possible presence of relations of co-integration that is the long-term relations between variables.

The tests of unit roots bring an answer to the question to know what the nature of the present trends is in the studied series. Various tests were establishes by the literature to this end, among which the test of Augmented Dicky Fuller (ADF), the test of Phillips-Perron (PP) and the test Kwiatkowski, Phillips, Schmidt and Shin ( KPSS).

Table 1: Unit Roots Tests in Level

Variable Tests t static 1% 5% 10% LRT

ADF

-0.813153 -4.042819 -3.450807 -3.150766 LG -1.123252 -4.042819 -3.450807 -3.150766 LY -0.940361 -4.042819 -3.450807 -3.150766 P -0.807074 -3.490210 -2.887665 -2.580778 R -0.637198 -3.490210 -2.887665 -2.580778

LRT

KPSS

0.224988 0.216000 0.146000 0.119000 LG 0.224324 0.216000 0.146000 0.119000 LY 0.250345 0.216000 0.146000 0.119000 P 1.226512 0.739000 0.463000 0.347000 R 0.999864 0.739000 0.463000 0.347000

LRT

PP

-1.635081 -4.039797 -3.449365 -3.149922 LG -1.366981 -4.039797 -3.449365 -3.149922 LY -0.429748 -4.039797 -3.449365 -3.149922 P -0.560026 -3.488063 -2.886732 -2.580281 R -0.648987 -3.488063 -2.886732 -2.580281

These tests were applied to the logarithms of the series by including trends and constants. The results are given in table [1] with the number of delay included in the regression for every test. The values observed by the statistics of the tests (ADF) and (PP) of the null hypothesis of presence of unit root are upper to the critical values at the beginning of 1 %, 5 % and 10 %.

6

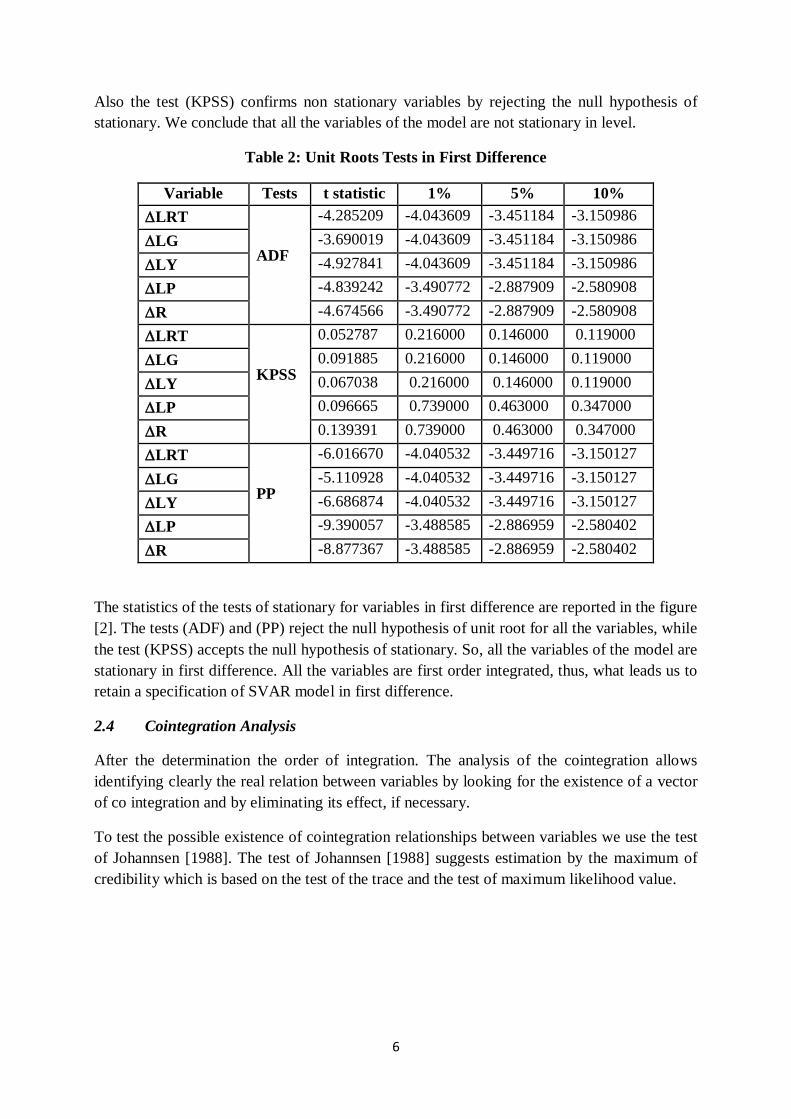

Also the test (KPSS) confirms non stationary variables by rejecting the null hypothesis of stationary. We conclude that all the variables of the model are not stationary in level.

Table 2: Unit Roots Tests in First Difference

Variable Tests t statistic 1% 5% 10% ∆LRT

ADF

-4.285209 -4.043609 -3.451184 -3.150986 ∆LG -3.690019 -4.043609 -3.451184 -3.150986 ∆LY -4.927841 -4.043609 -3.451184 -3.150986 ∆LP -4.839242 -3.490772 -2.887909 -2.580908 ∆R -4.674566 -3.490772 -2.887909 -2.580908 ∆LRT

KPSS

0.052787 0.216000 0.146000 0.119000 ∆LG 0.091885 0.216000 0.146000 0.119000 ∆LY 0.067038 0.216000 0.146000 0.119000 ∆LP 0.096665 0.739000 0.463000 0.347000 ∆R 0.139391 0.739000 0.463000 0.347000 ∆LRT

PP

-6.016670 -4.040532 -3.449716 -3.150127 ∆LG -5.110928 -4.040532 -3.449716 -3.150127 ∆LY -6.686874 -4.040532 -3.449716 -3.150127 ∆LP -9.390057 -3.488585 -2.886959 -2.580402 ∆R -8.877367 -3.488585 -2.886959 -2.580402

The statistics of the tests of stationary for variables in first difference are reported in the figure [2]. The tests (ADF) and (PP) reject the null hypothesis of unit root for all the variables, while the test (KPSS) accepts the null hypothesis of stationary. So, all the variables of the model are stationary in first difference. All the variables are first order integrated, thus, what leads us to retain a specification of SVAR model in first difference.

2.4 Cointegration Analysis

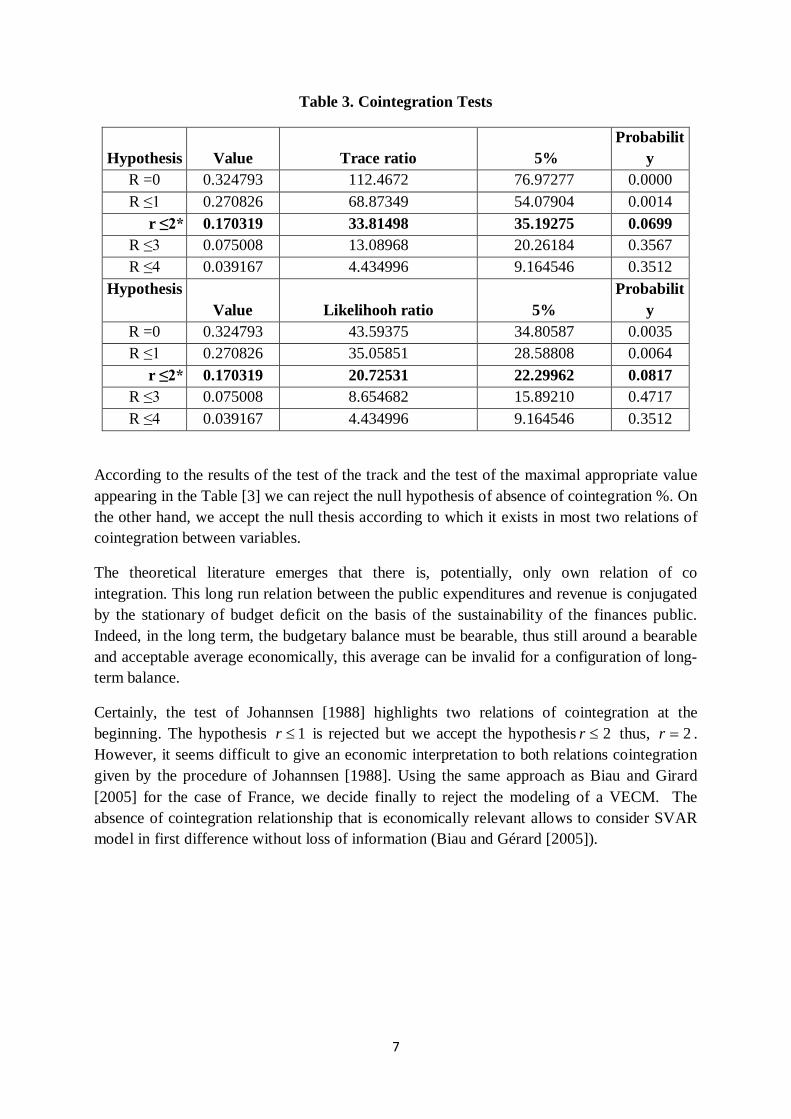

After the determination the order of integration. The analysis of the cointegration allows identifying clearly the real relation between variables by looking for the existence of a vector of co integration and by eliminating its effect, if necessary.

To test the possible existence of cointegration relationships between variables we use the test of Johannsen [1988]. The test of Johannsen [1988] suggests estimation by the maximum of credibility which is based on the test of the trace and the test of maximum likelihood value.

7

Table 3. Cointegration Tests

Hypothesis Value Trace ratio 5% Probabilit

y R =0 0.324793 112.4672 76.97277 0.0000 R ≤1 0.270826 68.87349 54.07904 0.0014

r ≤2* 0.170319 33.81498 35.19275 0.0699 R ≤3 0.075008 13.08968 20.26184 0.3567 R ≤4 0.039167 4.434996 9.164546 0.3512

Hypothesis Value Likelihooh ratio 5%

Probability

R =0 0.324793 43.59375 34.80587 0.0035 R ≤1 0.270826 35.05851 28.58808 0.0064

r ≤2* 0.170319 20.72531 22.29962 0.0817 R ≤3 0.075008 8.654682 15.89210 0.4717 R ≤4 0.039167 4.434996 9.164546 0.3512

According to the results of the test of the track and the test of the maximal appropriate value appearing in the Table [3] we can reject the null hypothesis of absence of cointegration %. On the other hand, we accept the null thesis according to which it exists in most two relations of cointegration between variables.

The theoretical literature emerges that there is, potentially, only own relation of co integration. This long run relation between the public expenditures and revenue is conjugated by the stationary of budget deficit on the basis of the sustainability of the finances public. Indeed, in the long term, the budgetary balance must be bearable, thus still around a bearable and acceptable average economically, this average can be invalid for a configuration of long-term balance.

Certainly, the test of Johannsen [1988] highlights two relations of cointegration at the beginning. The hypothesis 1≤r is rejected but we accept the hypothesis 2≤r thus, 2=r . However, it seems difficult to give an economic interpretation to both relations cointegration given by the procedure of Johannsen [1988]. Using the same approach as Biau and Girard [2005] for the case of France, we decide finally to reject the modeling of a VECM. The absence of cointegration relationship that is economically relevant allows to consider SVAR model in first difference without loss of information (Biau and Gérard [2005]).

8

3 IDENTIFICATION AND SIMULATION of the MODEL

The rejection of the hypothesis of presence of two relations of cointegration which are relevant economically implies the appeal to the VAR modeling as an adequate representation of our dynamic system. We suppose that this model is able to identifying and of measuring the effects of fiscal shocks on the economic activity and on the other aggregates. The VAR model applied to the Tunisian economy is a model with four delays which incorporates five variables in differences

∆∆∆∆∆

=

t

t

t

t

t

t

RPYGTA

X ,

=

5554535251

4544434241

3534333231

2524232221

1514131211

(.)

aaaaaaaaaaaaaaaaaaaaaaaaa

A

=

R

P

Y

G

TA

t

uuuuu

u

3.1 Identification of the model the structural VAR

We chose the method of identification of the structural shocks of Blanchard and Perotti [2002]. This method bases essentially on a matrix of transformation P binding the canonical innovations tu with the shocks structural tε and verifying that tt Pu ε= .

This relation implies the presence of the linear combinations between the canonical innovations and the structural shocks contained in the vector ],,,,[ R

tpt

yt

gt

tatt eeeee=ε . The

representative system of equation of our dynamic system such as presented by Perotti [2002] is sum follows:

Rt

gtRg

tatRta

ptRp

ytRY

Rt

pt

gtpg

tapt

ytpy

pt

yt

gtgy

tatyt

yt

gt

tatgt

RtgR

ptgp

ytgy

gt

tat

gttg

RttR

pttp

ytty

tat

eeeuuu

euuuu

euuu

eeuuuu

eeuuuu

++++=

+++=

++=

++++=

++++=

ββγγ

γγγ

γγ

βααα

βααα

The terms α correspond to elasticity; the terms β correspond to the cross reactions of the variables of the public finances, and the terms γ are the other coefficients to be estimated.

• The first two equations mean that the shocks on fiscal revenues tatu (resp. of

the public spending gtu ) once corrected by the mechanical influence of the economic

activity, the prices and the interest rate (resp. for the spending public: RtgR

ptgp

ytgy uuu ααα ++ ) can result from the structural shock of tax system ta

te (resp. of

the structural shock of spending gte ) but also of the immediate and discretionary

9

answer to the shock of the spending gttgeβ (resp. of the answer to the shock of tax

system tatgteβ ).

• The equation of the canonical residual of the activity ytu supposes that the

unexpected movements of the prices and the interest rate have no immediate effect on the GDP. This shock is exogenous and orthogonal in the other shocks. We suppose that in the quarter when this shock echoes on the innovation of the GDP which affects the budgetary expenditures and revenue which are going to modify then mechanically the dynamics of the income. This equation represents well the game of the automatic stabilizers.

• The fourth equation admits that the unexpected movements of the GDP, receipts and public spending can influence the prices immediately: she supposes only that the extensions of distribution of the movements of interest rate at the prices are superior to the quarter.

• The last equation means that the unexpected movements of the GDP and the prices can have an effect on the interest rate immediately and that the decisions of budgetary policy can possibly provoke fast reactions of the monetary policy (Policy mix).

3.2 Determination of the immediate elasticity

In this first stage we fix not diagonal coefficients of matrices 1M and 2M on the basis of the constraints of economic behavior. If we suppose that an innovation does not influence the other one inside the same quarter, we attribute a zero value to this coefficient. If on the contrary it influences the other one inside quarter we attribute a value.

The values of these coefficients are determined by estimating the immediate elasticity between two innovations on the basis of the institutional information: such as for example the automatic stabilizers. We attribute then the value of this elasticity to the adequate α coefficient. All the coefficientsα in the system are thus immediate elasticity.

The coefficients tyα and gyα get two effects of the economic activity on fiscal receipts and

public spending: on one hand, the effect of the automatic stabilizers and, on the other hand, the automatic discretionary answers which reflect the discretionary adjustment of the budgetary policy in front of shocks of the economic activity inside quarter.

The identification of the structural shocks of the spending (expenses) and the receipts(recipes) requires that residues are expurgated by these two mechanisms with the aim of analyzing the effects of a real discretionary budgetary policy. The key of identification is to recognize that the use of the quarterly data eliminates the automatic discretionary answers.

The experience of the behavior of the budgetary policy in Tunisia incites us, so, to make the hypothesis that the politicians and the legislators need more than a quarter to know the nature

10

of a shock, to decide which budgetary decision to take in answer to this shock and for, possibly, to implement it. So to identify the structural shocks, it is necessary, only to calculate the elasticity in the GDP of the spending and the receipts.

· The elasticity of fiscal receipts with regard to the GDP corresponds to the quarterly elasticity

of the net fiscal receipts of transfers. It is defined as followsPIB

PIBTA

TAty ∂

∂=α . It is interest to

consider that this elasticity is the sum balanced of the elasticity of every type(chap) of tax revenue with regard to the GDP. The elasticity of the income tax is invalid (useless), because of gap between plate and imposition. The elasticity of the national insurance contribution is very low as far as this type of income constitutes only 23 % of income fiscal. Only the elasticity of excise duties is very sensitive (perceptible) especially since he(it) generates 55 % of the tax revenue for Tunisia. Finally, we obtain 73.0=tyα .

· The elasticity of budgetary expenditure with regard to the GDP corresponds to the elasticity

of quarterly of the spending of consumption and investmentPIB

PIBG

Ggy ∂

∂=α it seems difficult

to identify clearly the automatic reactions of the public spending to the economic activity. We thus set 0=gyα .

· The elasticity of the net fiscal receipts at the prices (prizes) is defines as

followsP

PTA

TAtp ∂

∂=α . After calculation, we obtain a coefficient 018.0=tpα . This value is

lower than the average of Blanchard and Perotti [2002] which is close to 1 and that of Biau and Gérard [2005] which is equal to 5.

· The elasticity of budgetary expenditure at the prices is as followsPIB

PIBG

Ggp ∂

∂=α . In our

analysis we suppose that a rise in prices in the quarter decreases budgetary expenditure in real term, given, that this spending (expenses) is fixed in nominal values. We thus hold (retain) a negative elasticity 1−=gpα .

· The coefficient R

RTA

TAtR ∂

∂=α corresponds to the elasticity of fiscal receipts with regard to

the interest rate. An analysis of the structure of the foreign debt in Tunisia shows that this country is weakly displayed to a risk of the interest rate of the fact that 75 % of the debt was contracted in the fixed interest rates. Of this fact a modification of the interest rates in a quarter does not affect immediately and in a substantial way either responsibility of the national debt, or the takings on investments(placements). In these conditions we fix 0=tRα .

11

· The coefficient R

RG

GgR ∂

∂=α does not measure the elasticity of the public spending with regard

to the interest rate .en effect, the public consumption, nor do the public investments react, immediately, to a modification of the interest rate. Thus 0=gRα .

3.3 The MCO and instrumental variables regression

The second stage consists on estimating the other elasticity contained in matrices 1M and 2M . The method consists in estimating the system tt MuM ε21 =

From all the previous elasticity has can build residues corrected by the cycle ccgt

cctat uu ,, , :

gt

tatgt

RtgR

ptgp

ytgy

gt

ccgt

tat

gttg

RttR

pttp

ytty

tat

cctat

eeuuuuu

eeuuuuu

+=++−=

+=++−=

βααα

βααα

)(

)(,

,

To be able to consider this system at two equations, two alternative (alternate) hypotheses are possible. We suppose that the decisions concerning fiscal receipts precedent those of the public spending. It of the other term, the fiscal takings are completely exogenous, whereas the spending (expenses) is determined by the tax revenues. In this budgetary structure the spending (expenses) is a variable of adjustment.

Of this fact 0=tgβ and 0>gtβ .

In that case tat

cctat eu ˆ, = and we estimate by MCO the regression g

ttatgt

ccgt eeu += ˆ, β :

The second hypothesis supposes an alternative budgetary regime in which the decisions of spending precedent the decisions of fiscal receipts. Thus 0=gtβ and 0>tgβ .

It comes then: gt

ccgt eu ˆ, = and we estimate by MCO the regression: ta

tgttg

cctat eeu += ˆ, β .

The coefficients which we estimated are then used as instrumental variables ytγ and ygγ in

the equation of the canonical residue of the GDP. We estimate by the double lesser squares

the following regression: yt

gtyg

tatyt

yt euuu ++= γγ

Afterward we use yt

gt

tat eee ˆ,ˆ,ˆ as instruments to estimate the coefficients pgptapy γγγ ,,

pt

gtpg

tapt

ytpy

pt euuuu +++= γγγ

12

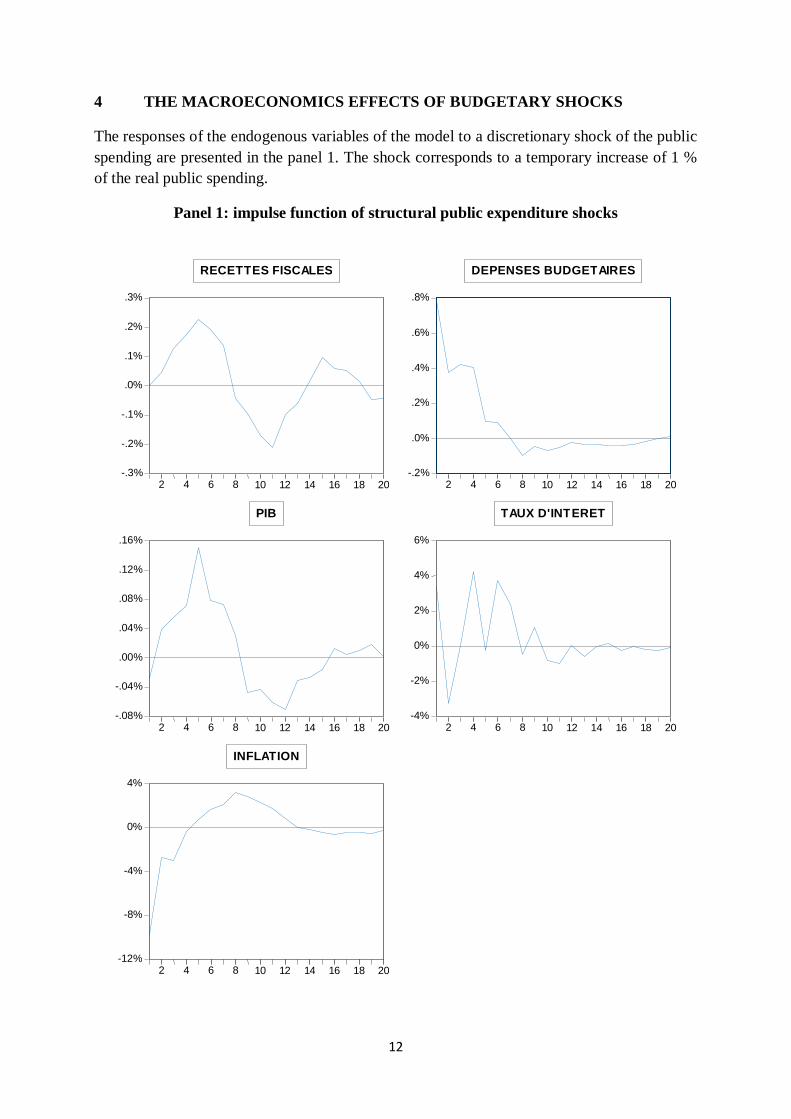

4 THE MACROECONOMICS EFFECTS OF BUDGETARY SHOCKS

The responses of the endogenous variables of the model to a discretionary shock of the public spending are presented in the panel 1. The shock corresponds to a temporary increase of 1 % of the real public spending.

Panel 1: impulse function of structural public expenditure shocks

-.3%

-.2%

-.1%

.0%

.1%

.2%

.3%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

R E C E T T E S F I S C A L E S

-.2%

.0%

.2%

.4%

.6%

.8%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

D E P E N S E S B U D G E T A I R E S

-.08%

-.04%

.00%

.04%

.08%

.12%

.16%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

PIB

-4%

-2%

0%

2%

4%

6%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

T A U X D ' I N T E R E T

-12%

-8%

-4%

0%

4%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

I N F L A T I O N

13

The results of the simulations show that the effects of a structural shock of the public spending on the variation of the real GDP are ambiguous. A discretionary increase of the public spending in Tunisia produces effects very low but which stays of short and medium-term keynesian sign. The extension of transmission is very fast. A quarter after the shock took a place, we attend a low increase of the level of real activity. This variation affects the peak of 0.0015 % a fifth quarter. The positive and significant effect on the GDP does not extend beyond the eighth quarter, it becomes then negative. In the long term, the effect on the economic activity becomes blurred gradually.

To explain the dynamics of the economic activity further to a structural shock of the public spending, we tried to move closer to the dynamics of the real GDP to the evolution of the other aggregates of the model. Our graphic analysis allows us to notice that the dynamics of the inflation and the real GDP are perfectly correlated. We suppose, so, that the evolution of the prices allows to explain a big part the answer of the real GDP to a shock of the public spending

During the first period [T1, T4], the GDP increases gradually further to a structural shock of 1 %, in parallel, this shock produces a deflationary effect which nullifies at the end of this first period. The increase of the real activity is conjugated by the presence of a deflationary effect. During the second period [T5, T14] the economic activity is in decline further to the appearance of the inflationary pressures. For the last period the real activity stabilizes around its initial level of the fact that the inflationary effect became blurred. In summary the answer of the real GDP is, strongly, supervised by the adjustment of the prices.

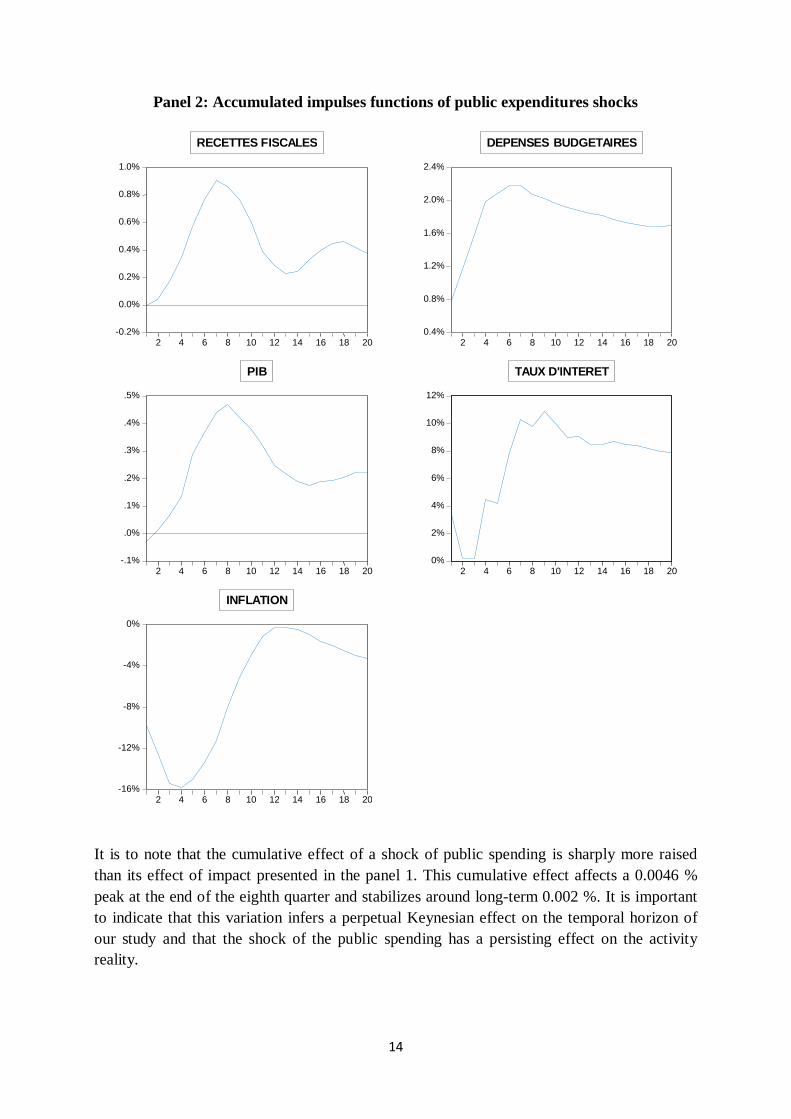

We think that our analysis is more relevant if the analysis and the interpretation of the dynamics of the system is based on cumulative functions of answer. Given that plans of budgetary boost can be implemented as time goes by and given that the reaction of the economy is progressive. The panel 2 presents all the functions of cumulative endogenous answer of the variables of the model further to a 1 % increase of the real public spending.

14

Panel 2: Accumulated impulses functions of public expenditures shocks

It is to note that the cumulative effect of a shock of public spending is sharply more raised than its effect of impact presented in the panel 1. This cumulative effect affects a 0.0046 % peak at the end of the eighth quarter and stabilizes around long-term 0.002 %. It is important to indicate that this variation infers a perpetual Keynesian effect on the temporal horizon of our study and that the shock of the public spending has a persisting effect on the activity reality.

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

2 4 6 8 10 12 14 16 18 20

R E C E T T E S F I S C A L E S

0.4%

0.8%

1.2%

1.6%

2.0%

2.4%

2 4 6 8 10 12 14 16 18 20

D E P E N S E S B U D G E T A I R E S

-.1%

.0%

.1%

.2%

.3%

.4%

.5%

2 4 6 8 10 12 14 16 18 20

PIB

0%

2%

4%

6%

8%

10%

12%

2 4 6 8 10 12 14 16 18 20

T A U X D ' I N T E R E T

-16%

-12%

-8%

-4%

0%

2 4 6 8 10 12 14 16 18 20

I N F L A T I O N

15

From this first investigation, the function of answer of the real GDP informs us that the behavior of an expansionist discretionary policy in Tunisia is capable of stimulating the real activity. However, the quantitative effect of this budgetary impulse brings to light the low scale of this simulation.

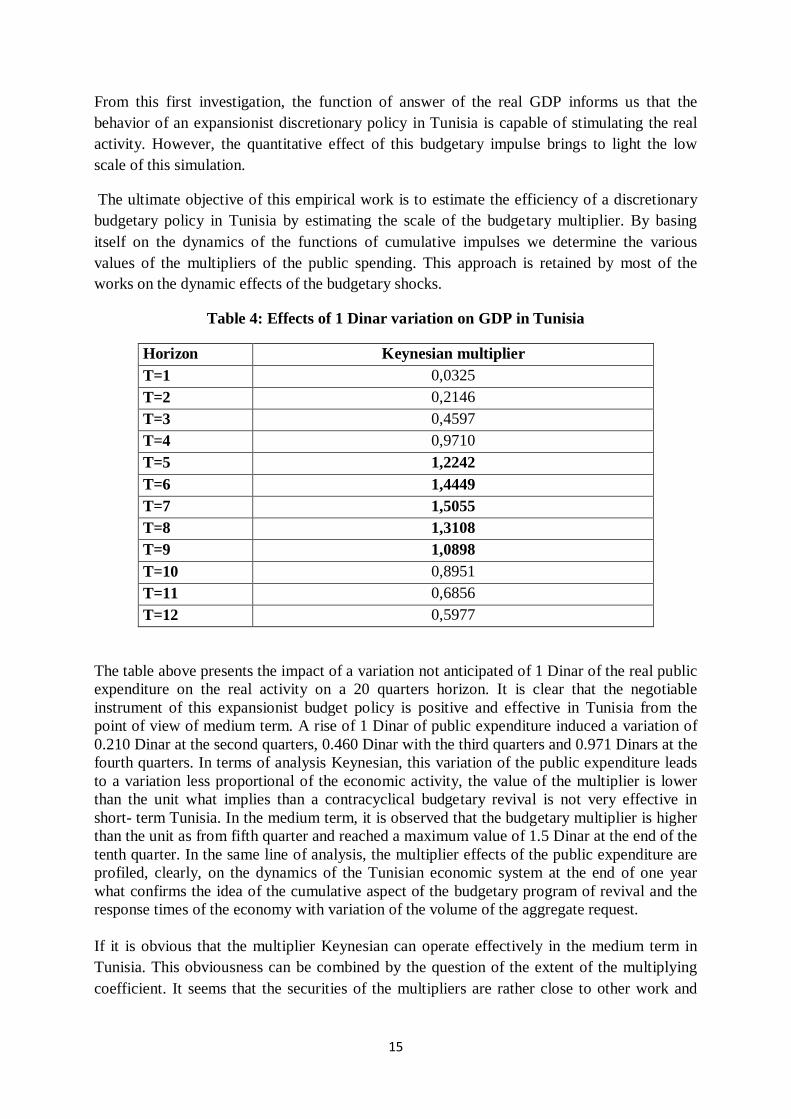

The ultimate objective of this empirical work is to estimate the efficiency of a discretionary budgetary policy in Tunisia by estimating the scale of the budgetary multiplier. By basing itself on the dynamics of the functions of cumulative impulses we determine the various values of the multipliers of the public spending. This approach is retained by most of the works on the dynamic effects of the budgetary shocks.

Table 4: Effects of 1 Dinar variation on GDP in Tunisia

Horizon Keynesian multiplier T=1 0,0325 T=2 0,2146 T=3 0,4597 T=4 0,9710 T=5 1,2242 T=6 1,4449 T=7 1,5055 T=8 1,3108 T=9 1,0898 T=10 0,8951 T=11 0,6856 T=12 0,5977

The table above presents the impact of a variation not anticipated of 1 Dinar of the real public expenditure on the real activity on a 20 quarters horizon. It is clear that the negotiable instrument of this expansionist budget policy is positive and effective in Tunisia from the point of view of medium term. A rise of 1 Dinar of public expenditure induced a variation of 0.210 Dinar at the second quarters, 0.460 Dinar with the third quarters and 0.971 Dinars at the fourth quarters. In terms of analysis Keynesian, this variation of the public expenditure leads to a variation less proportional of the economic activity, the value of the multiplier is lower than the unit what implies than a contracyclical budgetary revival is not very effective in short- term Tunisia. In the medium term, it is observed that the budgetary multiplier is higher than the unit as from fifth quarter and reached a maximum value of 1.5 Dinar at the end of the tenth quarter. In the same line of analysis, the multiplier effects of the public expenditure are profiled, clearly, on the dynamics of the Tunisian economic system at the end of one year what confirms the idea of the cumulative aspect of the budgetary program of revival and the response times of the economy with variation of the volume of the aggregate request. If it is obvious that the multiplier Keynesian can operate effectively in the medium term in Tunisia. This obviousness can be combined by the question of the extent of the multiplying coefficient. It seems that the securities of the multipliers are rather close to other work and

16

approves the empirical report that the budgetary multiplier in the developed nations is higher than that observed in the developing countries.

In addition, the negotiable instrument of the shock structural of public expenditure on the expenditure themselves is cumulative: the variation is positive medium-term. This report implies that an innovation with the expenditure even generates a persistent negotiable instrument on the expenditure they, since the shock is not absorbed quickly. The response of the deflator of the GDP to a shock structural of the public expenditure highlights a negative impact. Panel 2 shows a deflationary negotiable instrument which is combined by a fall of the deflator of the GDP of 1.5% with the third quarters after the date of the shock. This fall of the prices tends to be reduced in the medium term and ended up growing blurred in the long run. The result with which we have succeeds is against intuitive but remains realistic and possible in typical locations. The causes of inflation are numerous and their respective importance is sometimes difficult to appreciate. Two categories emerge, they are the monetary real causes on the one hand, and causes on the other hand. In the first, it is possible to distinguish the demand-pull inflation “” from that called “by the costs”. This category does not exclude the possibility that they all are present, simultaneously, but with different degrees during the same period.

At the real level, inflation is caused by the excess of request of the goods and services in the sense that the request increases in proportions such as the production does not manage to satisfy the request in reasonable delays. The prices then tend to be adjusted upwards, when they are flexible. It is the situation where the total request of the goods becomes higher than the global offer; it is the total excess demand on the global offer. The budget deficit can be financed by the tax, the loan or monetary creation. Indeed, the taking away of taxes or the launching of loan does not create a currency; they reduce, at least in the short run, the national revenue available and the pressures on the total request. However, one can admit that the interests poured at the time of a loan and the settlement of this last can exert pressures with the rise of the prices. But, in all probability, they can be only transitory negotiable instruments. The creation of currency thanks to the various contests of the central bank to the Treasury is the third method of financing of the public deficits. Conform to the quantity theory of money, it is regarded as inflationist. These advances however became extremely reduced in more the share of the developing countries which practically policies of price stability. It is thus allowed to affirm that, for these countries, monetary creation with the profit of the State is not any more one source of inflation. In short, if the level of the total request exceeds that of the offer, so in other words, the offer, because of the paring-iron of the full employment is insufficiently elastic to answer the request, of the inflationary tensions appear. The economy can record a rise in the prices of the goods and services when the request grows quickly and when the offer is insufficiently elastic to answer immediately this increase in request. It is obvious in the case of Tunisia that the increase in the public expenditure is not war a source of inflation by sticking the real approach of the price theory. What we note starting from the function of answer of the deflator of the GDP a fall of the prices following a positive shock structural of the public expenditure. Cavity our analysis is recurring since we introduce

17

theoretical arguments inherent in the dynamics of inflation to explain the deflationary profile of the public expenditure. It is thought that the most realistic explanation is related to the imbalance induced by a rise in the public expenditure on the market of the goods and the services. It proves that the production with reacts more proportionally than the total request follows to a budgetary shock. One explains this reduced variation of the total demand for Tunisia by the presence of the negotiable instruments of ousting. A rise in the budgetary expenditure increases, initially, the total request and the level of production. However, the mechanism of negotiable instrument of ousting is set up at the wire of time and crowd out part of the private sector investments what ends up lowering the level of the total request. In the short run, the level of the production exceeds the request what induces a fall of the prices. Interest rate accepts the innovations of the public expenditure. In this context a budgetary shock of 1% appears by a rise of 0.8% of interest rate. This reaction is the consequence of the deterioration of the budget deficit following an expansionist budget policy. Indeed a rise in the public expenditure involves a digging of budget deficit. This situation of financing need, the State will be directed towards the domestic financial market for raising capital through the issuing of the bonds or the issuing of the goods of treasures. These bonds are placed near the banks and other financial institutions which are held to subscribe to it since part of their deposits should be made up of public bonds. These bond bonds are located within the framework of the ratio of government stock imposed by the monetary authorities on the banks. They `acts of a means of controlling the banking liquidity by the monetary authorities as well as a means making it possible to mobilize a satisfactory request with the bonds issued by the treasure. The recourse of the treasure to this type of lever to finance its financing need results in a taking away of the liquidity and creates a constraint of orientation of the domestic saving towards the Treasury and will finish by the apparition of a negotiable instrument of ousting of the private sector investment consequently of a rise of interest rate. It is to be announced that this rise of interest rate is the result of an increase in total demand, the appearance of the inflationary pressures in the medium term and the deterioration of the budget deficit following an increase in the public expenditure.

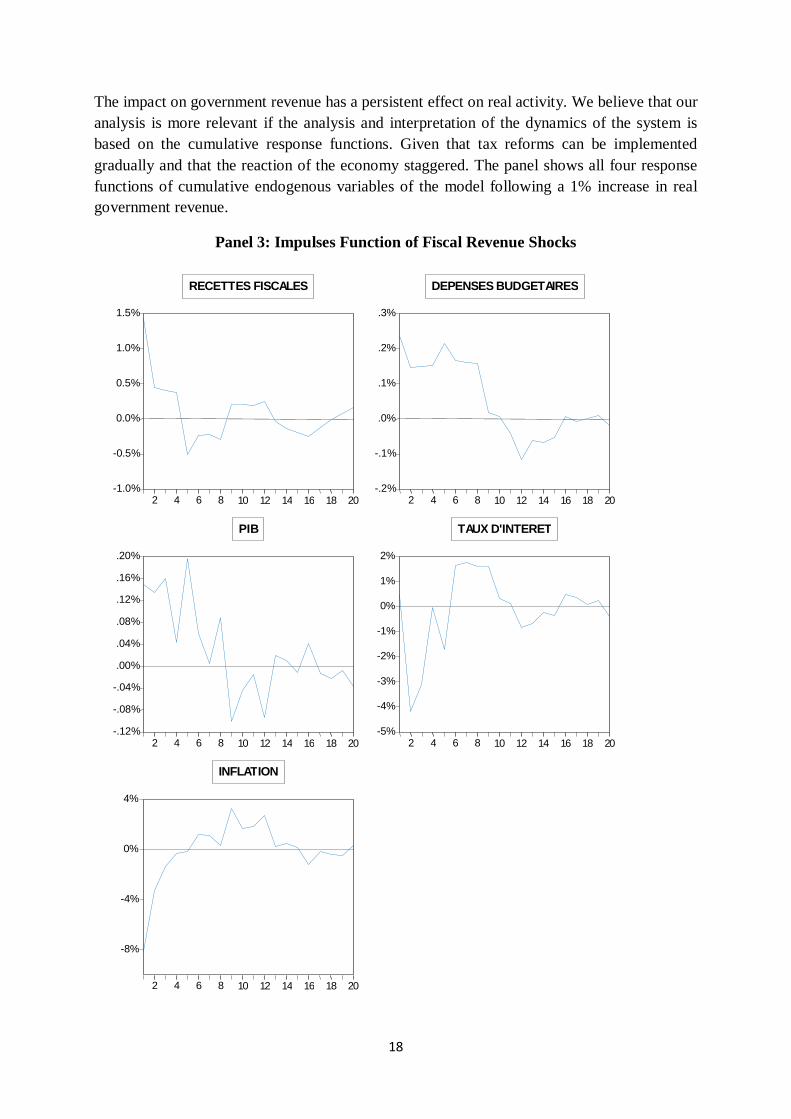

4.2 Effects of structural fiscal revenues shocks The responses of endogenous variables to a discretionary shock of fiscal revenues are presented in panel 3. The shock corresponds to an unanticipated temporary increase of 1% of fiscal revenues. From Panel 3, the results of simulations show that the effects of a structural shock on government revenue in real GDP are ambiguous. An increasing in fiscal revenue in Tunisia produces very small effects. Indeed, there is alternating movements of rise and fall of real GDP, but it remains positive during the forecast period. The presence of a positive effect during the first period [T1, T9] informs the presence of non-Keynesian effects of fiscal revenues on economic activity. In this regard, a tax increasing leads to a slowdown in the IS LM model. This is not the case for Tunisia. To explain this finding we must analyze the dynamics of public expenditure following a discretionary shock of fiscal revenue. The delay of transmission is very fast. A quarter after the shock has occurred; there is a increasing in level of real output. The significant and positive effect on GDP spans eight quarters. In the long term, the effect on the activity gradually fades to no longer be significant.

18

The impact on government revenue has a persistent effect on real activity. We believe that our analysis is more relevant if the analysis and interpretation of the dynamics of the system is based on the cumulative response functions. Given that tax reforms can be implemented gradually and that the reaction of the economy staggered. The panel shows all four response functions of cumulative endogenous variables of the model following a 1% increase in real government revenue.

Panel 3: Impulses Function of Fiscal Revenue Shocks

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

R E C E T T E S F I S C A L E S

-.2%

-.1%

.0%

.1%

.2%

.3%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

D E P E N S E S B U D G E T A I R E S

-.12%

-.08%

-.04%

.00%

.04%

.08%

.12%

.16%

.20%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

PIB

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

T A U X D ' I N T E R E T

-8%

-4%

0%

4%

2 4 6 8 1 0 1 2 1 4 1 6 1 8 2 0

I N F L A T I O N

19

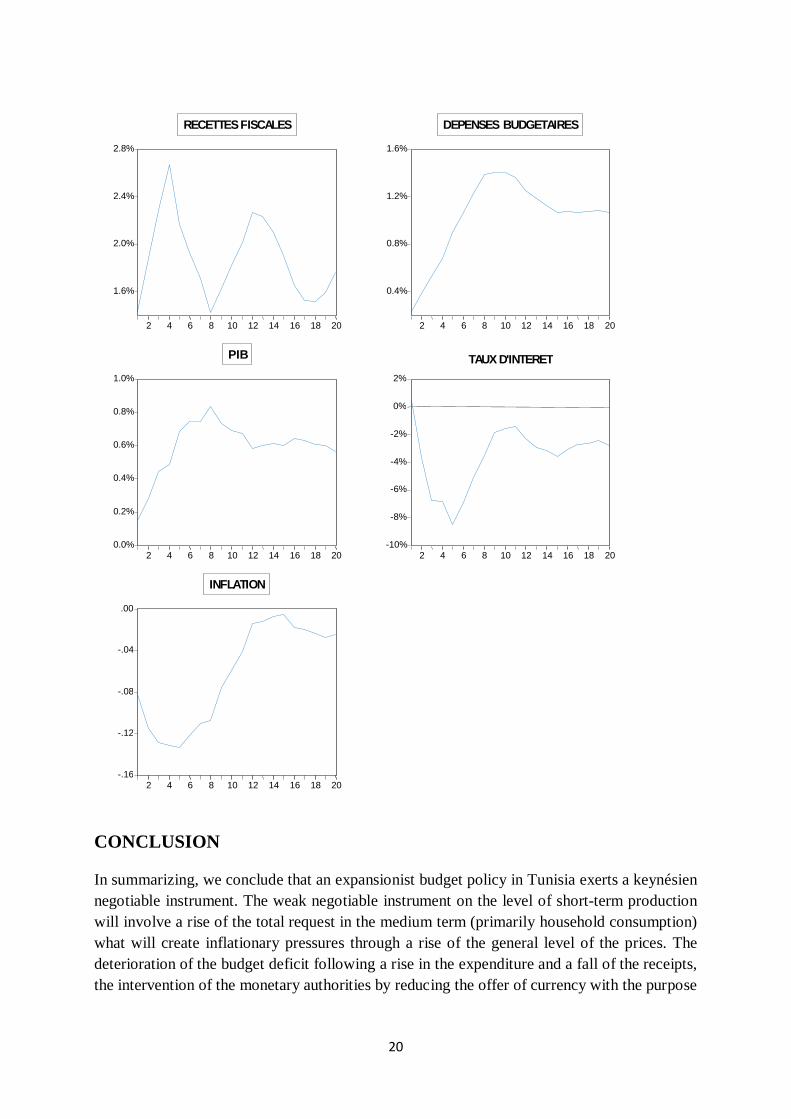

We think that our analysis is more relevant if we interpret of the dynamics based on cumulative impulsions functions. Since the tax reforms can be implemented gradually and that the reaction of the economy is spread out in the time. Panel 4 presents the cumulative impulsions functions of cumulative of the endogenous variables following an increase of 1% of the real fiscal revenue. Panel 4 shows that the cumulative variation is higher than the impact effect. It reaches the peak of 0.075% at the end of eighth period and still significant at 0.05% in the long run. It is important to announce that this variation induces a perpetual non Keynesian effect during forecasting period. To explain these non Keynesian reactions, we focus on the possible adjustment of the public expenditure following a shock of fiscal revenue. SVAR model supposes the presence of a constraint of identification which informs about the presence of adjustment reactions of public expenditure following a variation of fiscal revenues. Following this assumption government can raise its expenditure in answer to an increase in revenues follows to a positive shock of the budget revenue. The impulse function of the public expenditure shows a fast adjustment following a positive shock of the fiscal revenue. Indeed, an unanticipated rise of fiscal revenue results in an increase in public expenditures. This result validates the report of the Keynesians negotiable instruments public receipts. In a countercyclical approach of the fiscal policy, a discretionary shock of fiscal revenue causes a fall of income. To counter this recessive negotiable instrument of the taxes in this model another multiplying mechanism is put in advance. Indeed, this rise of fiscal revenue stimulates public expenditure. The latter, stimulates the level of the economic activities through fiscal multiplier. The effects fiscal revenues rising on inflation is negative. A positive fiscal shock involves a fall of level prices in the short run. This deflationary profile ended up being cancelled in the medium term. In the long run the cumulative effect becomes non significant. One observes also the same reaction for interest rate. In this respect a tax impulse appears by a fall of interest rate by the monetary authorities. The only explanation appears through the will of Central Bank to face the deflationary risk.

20

CONCLUSION In summarizing, we conclude that an expansionist budget policy in Tunisia exerts a keynésien negotiable instrument. The weak negotiable instrument on the level of short-term production will involve a rise of the total request in the medium term (primarily household consumption) what will create inflationary pressures through a rise of the general level of the prices. The deterioration of the budget deficit following a rise in the expenditure and a fall of the receipts, the intervention of the monetary authorities by reducing the offer of currency with the purpose

1.6%

2.0%

2.4%

2.8%

2 4 6 8 10 12 14 16 18 20

R E C E T T E S F I S C A L E S

0.4%

0.8%

1.2%

1.6%

2 4 6 8 10 12 14 16 18 20

D E P E N S E S B U D G E T A I R E S

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

2 4 6 8 10 12 14 16 18 20

PIB

-10%

-8%

-6%

-4%

-2%

0%

2%

2 4 6 8 10 12 14 16 18 20

T A U X D ' I N T E R E T

-.16

-.12

-.08

-.04

.00

2 4 6 8 10 12 14 16 18 20

I N F L A T I O N

21

of lowering inflation, make that interest rate will increase. The rise of this last will reduce request of the firms and thus crowd out e investment deprived consequently, the economic activity will drop for the remainder of the temporal horizon inducing a fall of the revenues from taxes of the State. The weak impact on the economic activity of fiscal impulses comes to more confirm the characteristics of fiscal multiplier in developing countries. In the theoretical and empirical literature, the large body of literature on the fact that the response of the economic activity to an increase in the budgetary expenditure and weaker and less persistent in the developing countries than in the developed nations.