efficient credit & collections management: the way to...

TRANSCRIPT

Efficient Credit & Collections Management:The Way to Optimize Your Working Capital

Nathalie Nolf Stefaan OvaereConsultant PartnerCrion Intensum

SAP Lounge, BrusselsOctober 3-4, 2007

Optimizing Order-to-Cash Management

How SAP FSCM supports the Order-to-Cash Process

Optimizing Order-to-Cash Management - Agenda

I. Working capital• Improving working capital • Impact of managing accounts receivable

II. Order-to-cash management• Analyzing the process from order to cash• How taking control of each phase of the CM process ?• How defining a well designed credit policy ?• Situation nowadays

III. Ingredients of a well designed credit policy

• Optimization of credit risk management• Credit worthiness assessment• Automatic credit control• Business process new & existing customers• Order blocking & deblocking• Centralize credit information

• Optimization of collections management• Optimizing collection methods• Efficient collections management• Feedback

IV. Tool• Reporting• Automation

I. II

III. IV.

III. IV.

I. II.

III.IV.

I. Working capital

III.

I. II

III.IV.

Accounts receivables

Improving working capital

• Critical for the organisation

• Management of working capital = measure of a company’s health

• Financial management :

• Receivables management

treasury receivables payments

Lower DSO

Decrease past due

Reduce bad debt

Mitigate corporate credit risk

Improve sales productivity

Increase cash flow

I. II

III.IV.

Impact of managing accounts receivables

FACT You have a yearly turnover of … million Euro

ACTION You reduce your customers’ credit with 5 days

RESULT You generate … Euro additional working capital

Optimize order-to-cash management

I. II

III.IV.

II. Order-to-cash management

I. II

III.IV.

Analyzing processControl

Defining credit policy

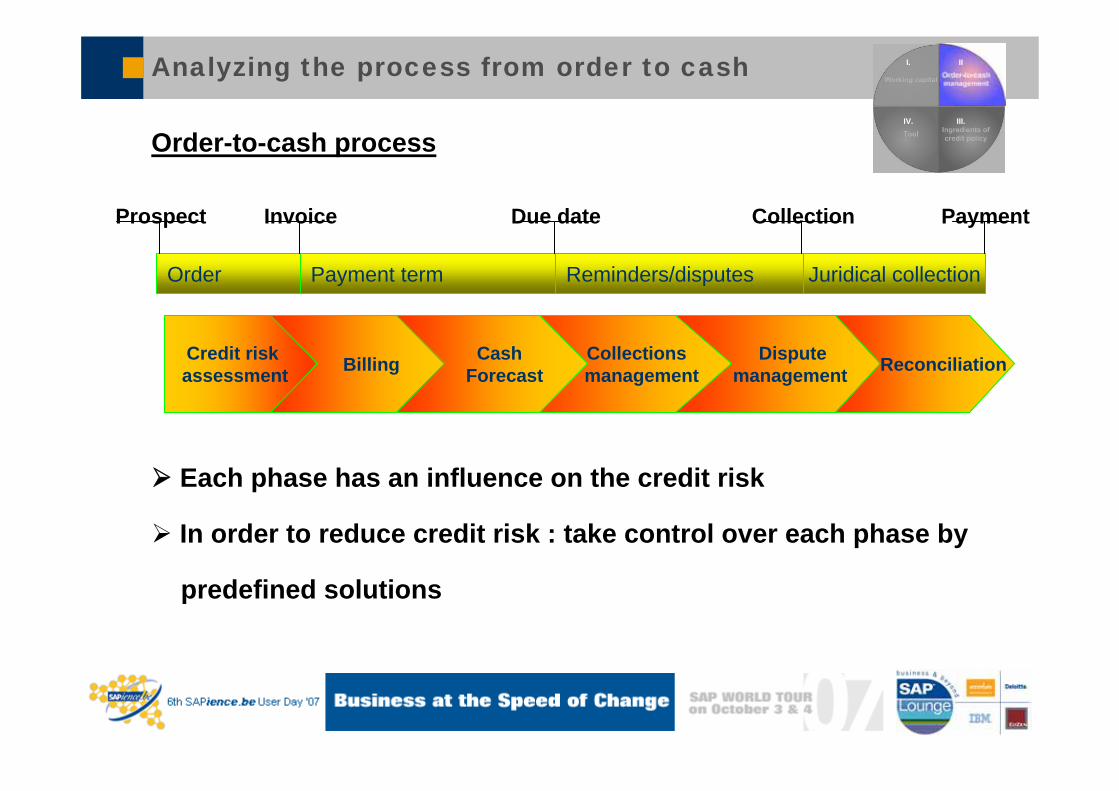

Analyzing the process from order to cash

Order-to-cash process

Each phase has an influence on the credit risk

In order to reduce credit risk : take control over each phase by

predefined solutions

Order Payment term Reminders/disputes Juridical collection

Credit riskassessment Billing Collections

managementDispute

managementCash

Forecast Reconciliation

Invoice Due date Collection PaymentProspect

I. II

III.IV.

How taking control of each phase ?

Setting up a well-designed credit & collection policyclear responsibilities (financial, commercial, …)operational rules

Credit risk management :

* credit approval* order blocking & deblocking

Collections management :* defining pro-active collection

strategies* dunning functionality* handling disputes

Evaluation

Efficient application

Implementing

Defining the policy

I. II

III.IV.

How taking control of each phase ?

Efficient application of policy by automation ofingredients (e.g. automate credit reviews)

Evaluation of the policy reporting adjusting policyEvaluation

Efficient application

Implementing

Defining the policy

I. II

III.IV.

Situation nowadays

•Credit operations have historically been highly inefficient

•Disparate systems and paper based processes

•Lack visibility to accurately measure performance

•No uniform implemented policy

I. II

III.IV.

How defining a well designed credit policy?

Purpose (mission) Why should any business incur the costs of credit & collections ?

GoalsMaximize sales, minimize risk, increase working capital, …

Key success factors (cfr. BSC) defining KPI (e.g. DSO : performance of payment)

Performance monitoring & measurements Do the performance measurements compliment the purpose?

Mission/vision

Strategic goals

Critical performance

Objectives

Actions

Success factors

I. II

III.IV.

III. Ingredients of a well designed credit policy

I. II

III.IV.

Optimization of credit risk management

Optimization of collections management

Optimization of credit risk management

On the pro-active side :

credit worthiness assessment

monitoring existing credit limits : automatic credit control

business process new & existing customers

order blocking & deblocking

centralize credit information

I. II

III.IV.

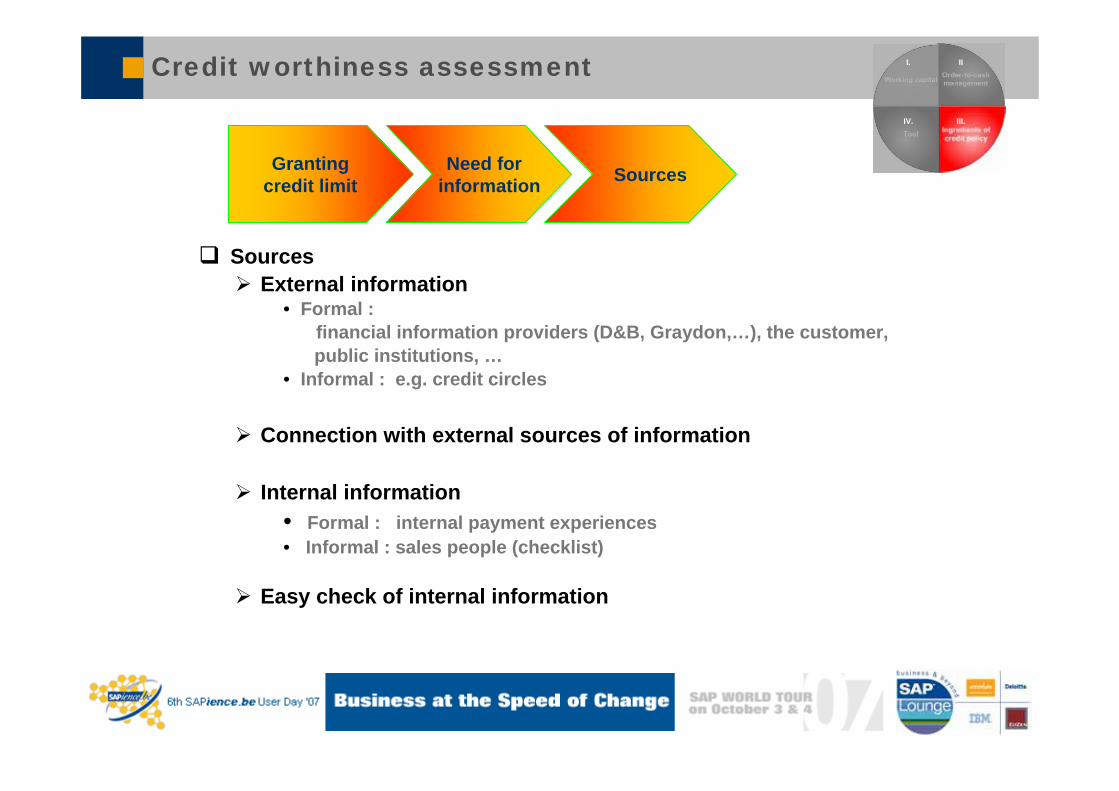

Credit worthiness assessment

For each customer :

File per customerGranting credit limits :

external credit limit of the credit insurerinternal credit limit calculation (basic advanced scoring model with

weighted parameters)risk classes

Need for information in order to fix a credit limit :financials : credit reports (key ratios,…)historic payment behaviourinformal information sales people or visitsnegative signals (judgements, …)

I. II

III.IV.

Grantingcredit limit

Need for information Sources

Credit worthiness assessment

SourcesExternal information

• Formal :financial information providers (D&B, Graydon,…), the customer,public institutions, …

• Informal : e.g. credit circles

Connection with external sources of information

Internal information• Formal : internal payment experiences • Informal : sales people (checklist)

Easy check of internal information

I. II

III.IV.

Grantingcredit limit

Need for information Sources

Automatic credit control

• Permanent monitoring of existing customers and early-warning-system

Top accounts need to be analysed every quarter to ensurethat the credit line is adequate

Input : financial and non-financial information of internal and external sources

Comparison of those information with the existing credit line :

* no change

* automatic change without any direct influenceon the line and operations

* automatic forwarding to the credit manager withrecommandations for action

I. II

III.IV.

Business process new & existing customers

• Credit assessment processes :

* business process new customers :

order inquiry procure information create customer fix credit limit and term of payment

* existing customers :

order inquiry credit limit control

- order within the credit limit determination of credit limit and term of payment automatic approval of the order

- order exceeds credit limit order stop or human resources approval

I. II

III.IV.

Order blocking & deblocking

• Orders can be blocked due to credit limit exceeding, overdues, …

• Release the order Human approval :Authority levels defined in the credit policy :

action for CM, decision management, …

Other solutions defined in the credit policy

Depending on the exceeding amount, overdue, customer (risk class, amount of turnover,…)

I. II

III.IV.

Order blocking and deblocking

•Blocking and deblocking orders needs to happen fast in order to :

improve operational efficiency

alert the right person for action(e.g. alert sales person to collect delivery)

alert the right person for fast decision

speed information delivery

increase customer satisfaction

I. II

III.IV.

Centralize credit information

An efficient credit risk management needs a technological support :• Need for checking credit limits online

Visibility total exposure common customers (decentralisedcompanies) Improve communication between financial and commercial people &facilitate collaboration

• Automate credit decisionsConsistency in credit approvalCredit reviews : a time consuming activity

• Efficient processing of customer dataIncorporate third party data

• Provide credit ratings for other applicationsUsing risk classes for the collection management in order to adjust collection strategies

I. II

III.IV.

III. Ingredients of credit policy

I. II

III.IV.

Optimization of credit risk management

Optimization of collections management

Optimizing collection methods

•Time consuming activity for the collector :• Creating a collection work list• Sending reminders• Calling customers• Preparing customer contacts• Documenting customer contacts

efficient working method and tool

•Using the right collection method is important : • adapted to the culture and the country of the debtor• defining the right actions with the right frequency• adequate content of the reminders and call actions

• Strategically segment customers and apply different collection strategies fordifferent risk classes of customers change of collection method according to riskclass

I. II

III.IV.

Efficient collections management

• Efficient follow-up of overdues : • pro-active collection of outstanding receivables• improve productivity and collection effectiveness by automatically

prioritize activities

• Efficient handling of disputes :

Identify dispute valid solution

invalid continue collection procedure

• Evaluating collection methods through reporting of collection effectiveness

I. II

III.IV.

IV. Tool

I. II

III.IV.

ReportingAutomation

Reporting

Vital for management to monitor risk exposure & track performance :• credit risk warnings/alerts• dispute cycle time• top X customer analysis• collection effectiveness

Management needs ongoing feedback concerning : • order blockings, overdues, aging, reminders, disputes, DSO, losses,…

Management reporting for decision supporttaking action on base of key information

I. II

III.IV.

Automation

• What in case an order is blocked ?

• What in case a customer doesn’t pay nevertheless he made a promise to pay ?

• What if there is a complaint on the invoice : continue sending reminders ? Exceptions

I. II

III.IV.

• Management by exceptions• Need for automation

processes & workflows need to be automated(e.g. credit assessment : automated credit application & decision processes)advantage : more time to concentrate on the exceptions

No efficient credit and collection management without tool. FSCM provides a fully integrated solution.

Optimizing Order-to-Cash Management

How SAP FSCM supports the Order-to-Cash Process

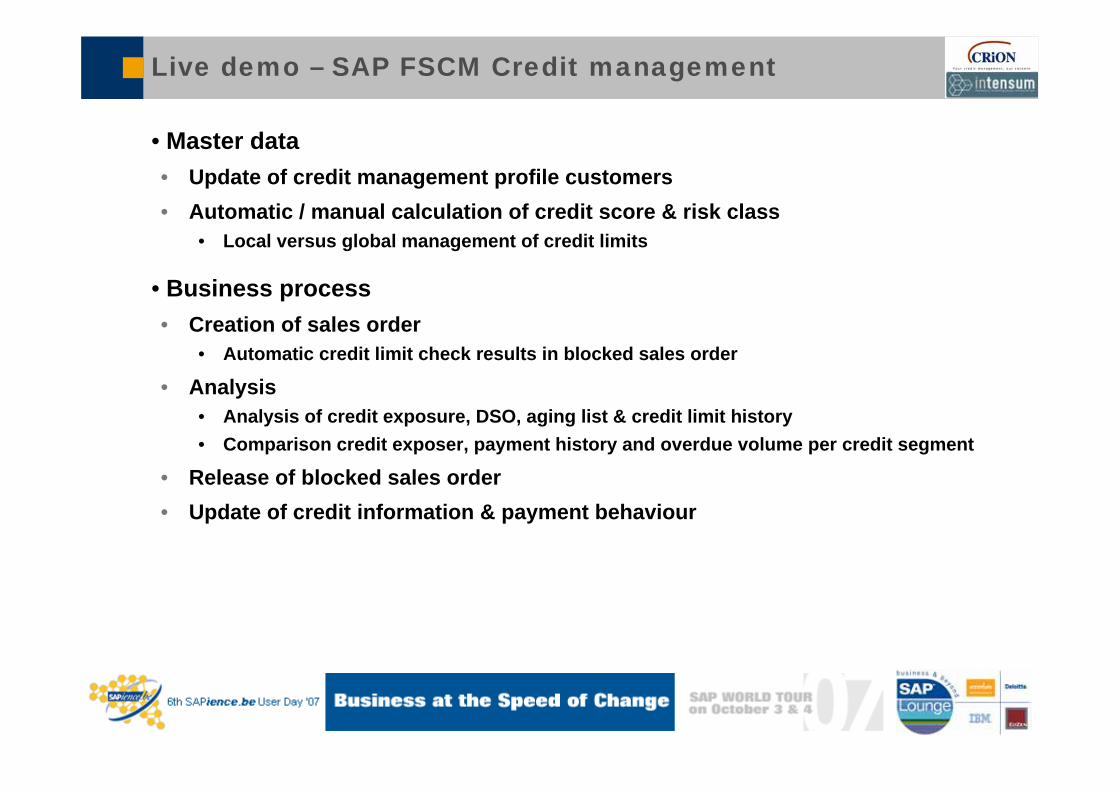

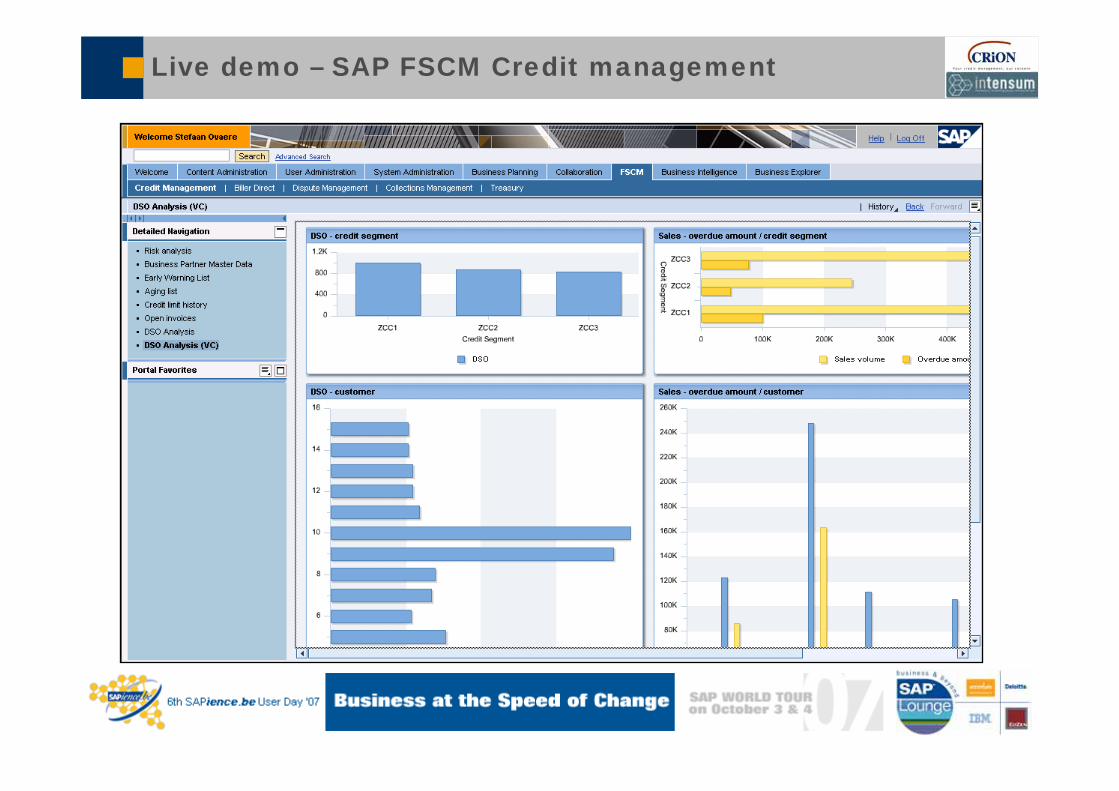

Live demo – SAP FSCM Credit management

• Master data• Update of credit management profile customers• Automatic / manual calculation of credit score & risk class

• Local versus global management of credit limits

• Business process• Creation of sales order

• Automatic credit limit check results in blocked sales order

• Analysis• Analysis of credit exposure, DSO, aging list & credit limit history• Comparison credit exposer, payment history and overdue volume per credit segment

• Release of blocked sales order• Update of credit information & payment behaviour

Live demo – SAP FSCM Credit management

Live demo – SAP FSCM Credit management

Live demo – SAP FSCM Credit management

Live demo – SAP FSCM Credit management

Live demo – SAP FSCM Credit management

Live demo – SAP FSCM Credit management

Live demo – SAP FSCM Collections management

• Master data• Collection management strategy & collection segments• Worklist generation

• Business process• Worklist processing according to priorities

• Online analysis of payment issues• Updating the customer contact history• Creation of promise to pay• Automatic clearing & update of worklist

• Worklist management & follow-up• Reporting and analysis tools

• Effectiveness of collections management• Analysis of customer contacts, resubmissions, dunning, promises to pay, etc.

Live demo – SAP FSCM Collections management

Live demo – SAP FSCM Collections management

Live demo – SAP FSCM Collections management

Live demo – SAP FSCM Collections management

Michel HaesendonckxSolution Advisor for the Office of the CFO SAP Belgium – [email protected]

Questions ? – Contact Info

Stefaan OvaerePartner [email protected]

Nathalie NolfCredit Management Consultant [email protected]