efse – supporting our investors 16 economies on their way ...€¦ · translation, reprinting,...

TRANSCRIPT

EFSE – Supporting 16 EconomiES on thEir way to growthAnnuAl report 2013

no. 6armenia stands at 6 in the

ranking of 189 economies on the

ease of starting a business

AM

DisclAiMer

the european Fund for southeast europe is a specialised investment fund governed by luxembourg law

and is reserved for institutional, professional or other well-informed investors as defined by luxembourg

law. the issue document or the assets held in the Fund have, however, not been approved or disapproved

by any authority. the information given herein constitutes neither an offer nor a solicitation of any

action based on it, nor does it constitute a commitment of the Fund to offer its shares to any investor. no

guarantee is given as to the completeness, timeliness or adequacy of the information provided herein.

no investment may be made except upon the basis of the current issue document of the Fund, which is

obtainable free of charge from oppenheim Asset Management services s. à r. l., 4 rue Jean Monnet,

l - 2180 luxembourg.

shares or notes of the Fund are not for distribution in or into the united states of America, canada, Japan

or Australia or to any u. s. person or in any other jurisdiction in which such distribution would be

prohibited by applicable law. All forward-looking statements have been compiled on a best efforts basis,

taking into account multiple variables which may be subject to change, including, without limitation,

exchange rates, general developments in banking markets and regulations, interest rate benchmarks, and

others. Actual developments could differ from the expectations expressed in forward-looking statements.

past performance is not a reliable indicator of future results. prices of shares and the income from them

may fall or rise and investors may not get back the amount originally invested. the Fund is under no

obligation to update or alter its forward-looking statements whether as a result of new information, future

events, or otherwise.

neither the Fund nor any of its shareholders, directors, officers, employees, advisors or agents makes any

representation or warranty or gives any undertaking of any kind, express or implied, or, to the extent

permitted by applicable law, assumes any liability of any kind whatsoever, as to the timeliness, adequacy,

correctness, completeness or suitability for any investor of any opinions, forecasts, projections,

assumptions and any other information contained in, or otherwise in relation to, this document or assumes

any undertaking to supplement any such information as further information becomes available or in

light of changing circumstances. the content of this information is subject to change without prior notice.

this document does not necessarily deal with every important topic or cover every aspect of the topics

with which it deals. the information in this document does not constitute investment, legal, tax or any

other advice. it has been prepared without regard to the individual financial and other circumstances

of persons who receive it.

© european Fund for southeast europe 2014. All rights reserved.

translation, reprinting, transmission, distribution, presentation, use of illustrations and tables or

reproduction or use in any other way is subject to permission of the copyright owner and acknowledgement

of the source.

iMprint

publisher european Fund for southeast europe (eFse)

concept / lAyout Finance in Motion Gmbh (www.finance-in-motion.com)

hilger & boie Design (www.hilger-boie.de)

proDuction Joh. Wagner & söhne KG (www.druckerei-wagner.com)

photoGrAphs peter Grosslaub (www.trendshots.com)

kantver (www.fotolia.de)

pAper recy®satin (www.papyrus.com)

to download or order hardcopies of this Annual report, please go to www.efse.lu

tr

our investors

Donor AGencies

European Investment Fund and KfW as Trustees for theEuropean Commission

internAtionAl FinAnciAl institutions

privAte institutionAl investors

versorgungsfonds des Ministeriums der Finanzen land brandenburg

6armenia stands at 6 in the

ranking of 189 economies on the

ease of starting a business

AM

Al

the FunD’s other privAte investors pArticipAte viA

EFSE – Supporting 16 EconomiES on thEir way to growthAnnuAl report 2013

no. 6armenia stands at 6 in the

ranking of 189 economies on the

ease of starting a business

AM

DisclAiMer

the european Fund for southeast europe is a specialised investment fund governed by luxembourg law

and is reserved for institutional, professional or other well-informed investors as defined by luxembourg

law. the issue document or the assets held in the Fund have, however, not been approved or disapproved

by any authority. the information given herein constitutes neither an offer nor a solicitation of any

action based on it, nor does it constitute a commitment of the Fund to offer its shares to any investor. no

guarantee is given as to the completeness, timeliness or adequacy of the information provided herein.

no investment may be made except upon the basis of the current issue document of the Fund, which is

obtainable free of charge from oppenheim Asset Management services s. à r. l., 4 rue Jean Monnet,

l - 2180 luxembourg.

shares or notes of the Fund are not for distribution in or into the united states of America, canada, Japan

or Australia or to any u. s. person or in any other jurisdiction in which such distribution would be

prohibited by applicable law. All forward-looking statements have been compiled on a best efforts basis,

taking into account multiple variables which may be subject to change, including, without limitation,

exchange rates, general developments in banking markets and regulations, interest rate benchmarks, and

others. Actual developments could differ from the expectations expressed in forward-looking statements.

past performance is not a reliable indicator of future results. prices of shares and the income from them

may fall or rise and investors may not get back the amount originally invested. the Fund is under no

obligation to update or alter its forward-looking statements whether as a result of new information, future

events, or otherwise.

neither the Fund nor any of its shareholders, directors, officers, employees, advisors or agents makes any

representation or warranty or gives any undertaking of any kind, express or implied, or, to the extent

permitted by applicable law, assumes any liability of any kind whatsoever, as to the timeliness, adequacy,

correctness, completeness or suitability for any investor of any opinions, forecasts, projections,

assumptions and any other information contained in, or otherwise in relation to, this document or assumes

any undertaking to supplement any such information as further information becomes available or in

light of changing circumstances. the content of this information is subject to change without prior notice.

this document does not necessarily deal with every important topic or cover every aspect of the topics

with which it deals. the information in this document does not constitute investment, legal, tax or any

other advice. it has been prepared without regard to the individual financial and other circumstances

of persons who receive it.

© european Fund for southeast europe 2014. All rights reserved.

translation, reprinting, transmission, distribution, presentation, use of illustrations and tables or

reproduction or use in any other way is subject to permission of the copyright owner and acknowledgement

of the source.

iMprint

publisher european Fund for southeast europe (eFse)

concept / lAyout Finance in Motion Gmbh (www.finance-in-motion.com)

hilger & boie Design (www.hilger-boie.de)

proDuction Joh. Wagner & söhne KG (www.druckerei-wagner.com)

photoGrAphs peter Grosslaub (www.trendshots.com)

kantver (www.fotolia.de)

pAper recy®satin (www.papyrus.com)

to download or order hardcopies of this Annual report, please go to www.efse.lu

tr

our investors

Donor AGencies

European Investment Fund and KfW as Trustees for theEuropean Commission

internAtionAl FinAnciAl institutions

privAte institutionAl investors

versorgungsfonds des Ministeriums der Finanzen land brandenburg

6armenia stands at 6 in the

ranking of 189 economies on the

ease of starting a business

AM

Al

the FunD’s other privAte investors pArticipAte viA

2 Mission

3 Key Figures 2013

4 letter from the chairperson of the board of Directors

6 Greetings

8 letter from the Fund Manager and Fund Advisor

10 A macro perspective of Mse finance – the european eastern neighbourhood region

14 A macro perspective of Mse finance – southeast europe

18 A Journey throuGh the reGions 20 belarus

21 ukraine

22 Moldova

23 romania

24 serbia

25 croatia

26 bosnia and herzegovina

27 Montenegro

28 Kosovo

29 Albania

30 Fyr Macedonia

31 bulgaria

32 turkey

33 Georgia

34 Azerbaijan

35 Armenia

36 revieW oF investMent AnD DevelopMent FAcility operAtions

36 investment operations

39 eFse Development Facility – highlights 2013

42 operAtionAl results 43 Financial statements

46 investments

49 Funding

51 eFse Development Facility

54 Development impact

58 partner lending institutions

61 AppenDices 62 organisational structure

63 board of Directors and committees

66 contacts

Missioncontents

the eFse aims to foster economic development and prosperity in the southeast europe region * and in the european eastern neighbourhood region ** through the sustainable provision of additional development finance, notably to micro and small enterprises and to private households, via qualified financial institutions.

in pursuing its development goal, the eFse will observe principles of sustainability and additionality, combining development and market orientations.

Mission & contents

* southeast europe in the context on this Annual report comprises Albania, bosnia and herzegovina, bulgaria, croatia, Fyr Macedonia, Kosovo (this designation is without prejudice to positions on status, and is in line with unsc 1244 and the isJ opinion of the Kosovo Declaration of independence), Montenegro, romania, serbia and turkey.

** the european eastern neighbourhood region in the context of this Annual report comprises Armenia, Azerbaijan, belarus, Georgia, the republic of Moldova and ukraine.

AM

67eFse AnnuAl report 2013

AZerbAiJAn, croAtiA, roMAniAFinance in Motion GmbhFund Advisortheodor-stern-Kai 160596 Frankfurt am MainGermanyt: +49 (0)69 977 876 50 0 F: +49 (0)69 977 876 50 10 e: [email protected]

[email protected] [email protected]

bulGAriA, MonteneGroFinance in Motion GmbhFund Advisorbulevar svetog petra cetinjskog 114 81000 podgorica Montenegro t: +382 (0)20 22 83 41 F: +382 (0)20 22 83 40 e: [email protected]

Fyr MAceDoniAFinance in Motion GmbhFund AdvisorMaksim Gorki 20 / 3 1000 skopje Fyr Macedonia t: +389 (0)2 31 32 628 F: +389 (0)2 31 32 627 e: [email protected]

GeorGiAFinance in Motion GmbhFund Advisor 24 rustaveli Avenue, iii Floor 0108 tbilisi Georgia t: +995 (0)322 611 158 F: +995 (0)322 661 158 e: [email protected]

KosovoFinance in Motion GmbhFund AdvisorZija shemsiu 6 (ulpiana) 10000 prishtina Kosovo t: +381 (0)38 54 41 08 F: +381 (0)38 54 41 09 e: [email protected]

MolDovA, belArusFinance in Motion GmbhFund Advisor25, M. banulescu bodoni str., 3rd floor, room 31 MD – 2012 chisinau republic of Moldova t: +373 (0)22 54 46 26 t: +373 (0)22 54 46 26 e: [email protected]

serbiAFinance in Motion Gmbh Fund AdvisorAirport city, omladinskih brigada 90v, building 1700, 8th floor11070 belgradeserbiat: +381 (0)11 22 89 058F: +381 (0)11 22 89 026e: [email protected]

turKeyFinance in Motion Gmbh Fund Advisorbuyukdere caddesi no: 237, noramin is Merkezi A10334398 Maslak, sariyer, istanbulturkeyt: +90 212 286 03 21F: +90 212 286 03 22e: [email protected]

uKrAineFinance in Motion Gmbh Fund Advisorshovkovichna street 21, office 301024 Kyivukrainet: +380 (0)44 451 44 - 51e: [email protected]

2 Mission

3 Key Figures 2013

4 letter from the chairperson of the board of Directors

6 Greetings

8 letter from the Fund Manager and Fund Advisor

10 A macro perspective of Mse finance – the european eastern neighbourhood region

14 A macro perspective of Mse finance – southeast europe

18 A Journey throuGh the reGions 20 belarus

21 ukraine

22 Moldova

23 romania

24 serbia

25 croatia

26 bosnia and herzegovina

27 Montenegro

28 Kosovo

29 Albania

30 Fyr Macedonia

31 bulgaria

32 turkey

33 Georgia

34 Azerbaijan

35 Armenia

36 revieW oF investMent AnD DevelopMent FAcility operAtions

36 investment operations

39 eFse Development Facility – highlights 2013

42 operAtionAl results 43 Financial statements

46 investments

49 Funding

51 eFse Development Facility

54 Development impact

58 partner lending institutions

61 AppenDices 62 organisational structure

63 board of Directors and committees

66 contacts

Missioncontents

the eFse aims to foster economic development and prosperity in the southeast europe region * and in the european eastern neighbourhood region ** through the sustainable provision of additional development finance, notably to micro and small enterprises and to private households, via qualified financial institutions.

in pursuing its development goal, the eFse will observe principles of sustainability and additionality, combining development and market orientations.

Mission & contents

* southeast europe in the context on this Annual report comprises Albania, bosnia and herzegovina, bulgaria, croatia, Fyr Macedonia, Kosovo (this designation is without prejudice to positions on status, and is in line with unsc 1244 and the isJ opinion of the Kosovo Declaration of independence), Montenegro, romania, serbia and turkey.

** the european eastern neighbourhood region in the context of this Annual report comprises Armenia, Azerbaijan, belarus, Georgia, the republic of Moldova and ukraine.

AM

67eFse AnnuAl report 2013

AZerbAiJAn, croAtiA, roMAniAFinance in Motion GmbhFund Advisortheodor-stern-Kai 160596 Frankfurt am MainGermanyt: +49 (0)69 977 876 50 0 F: +49 (0)69 977 876 50 10 e: [email protected]

[email protected] [email protected]

bulGAriA, MonteneGroFinance in Motion GmbhFund Advisorbulevar svetog petra cetinjskog 114 81000 podgorica Montenegro t: +382 (0)20 22 83 41 F: +382 (0)20 22 83 40 e: [email protected]

Fyr MAceDoniAFinance in Motion GmbhFund AdvisorMaksim Gorki 20 / 3 1000 skopje Fyr Macedonia t: +389 (0)2 31 32 628 F: +389 (0)2 31 32 627 e: [email protected]

GeorGiAFinance in Motion GmbhFund Advisor 24 rustaveli Avenue, iii Floor 0108 tbilisi Georgia t: +995 (0)322 611 158 F: +995 (0)322 661 158 e: [email protected]

KosovoFinance in Motion GmbhFund AdvisorZija shemsiu 6 (ulpiana) 10000 prishtina Kosovo t: +381 (0)38 54 41 08 F: +381 (0)38 54 41 09 e: [email protected]

MolDovA, belArusFinance in Motion GmbhFund Advisor25, M. banulescu bodoni str., 3rd floor, room 31 MD – 2012 chisinau republic of Moldova t: +373 (0)22 54 46 26 t: +373 (0)22 54 46 26 e: [email protected]

serbiAFinance in Motion Gmbh Fund AdvisorAirport city, omladinskih brigada 90v, building 1700, 8th floor11070 belgradeserbiat: +381 (0)11 22 89 058F: +381 (0)11 22 89 026e: [email protected]

turKeyFinance in Motion Gmbh Fund Advisorbuyukdere caddesi no: 237, noramin is Merkezi A10334398 Maslak, sariyer, istanbulturkeyt: +90 212 286 03 21F: +90 212 286 03 22e: [email protected]

uKrAineFinance in Motion Gmbh Fund Advisorshovkovichna street 21, office 301024 Kyivukrainet: +380 (0)44 451 44 - 51e: [email protected]

key figures 2013

132,947active sub-borrowers

768.1million euros

outstanding subloans

66per cent

share of private capital

invested in the fund

34per cent

share of public capital

invested in the fund

million euros

9.8volume of efse Development

facility projects for institutional

capacity building, financial sector

support and applied research

472,490number of micro and

small enterprise and home

improvement loans

226number of efse Development

facility projects for institutional

capacity building, financial sector

support and applied research

3.3billion euros

volume of micro and

small enterprise and housing

loans disbursed

billion euros

1.4committed investments

to partner lending institutions

460,000jobs secured or

created through the efse’s

investment activities

961.8million euros

investor commitments

826.2million euros

outstanding investments

71partner lending institutions

since the efse’s inception in December 2005

IntroductIon4 Macro level Journey review operational results appendices

the effects of the worldwide financial crisis may have eased, but they are still felt in some parts of the efse’s target regions where unemployment remains at exceptionally high levels. As micro and small enterprises offer a very high potential for job creation, but are also vulnerable to disruptions, the role of the efse in financing micro and small enterprises is as crucial as ever.

Although demand for additional credit lines in our target countries is growing at a slower pace than pre-crisis, the efse set an annual record volume in 2013 with eur 211.3 million in loans disbursed. since its inception in December 2005, the fund has financed loans to micro and small enterprises and private households in the regions totalling eur 3.3 billion.

the qualitative aspects of the liquidity injected by the efse are just as important. longer tenures and flexible disbursement schedules, combined with subordinated debt to strengthen their capital base, enable partner lending institutions to deepen and broaden the scope of their product offerings to end-borrowers.

the efse Development facility, which operates hand in hand with the fund’s investment management, assisted partner lending institutions in improving credit approval process, helping them to better adjust to new economic realities and to remain on track even in challenging times. this close cooperation between the Development facility and the fund has led to broader and deeper institutional capacities for serving the final target group as well as to a loan portfolio with one of the lowest impairment levels of the industry.

in an effort to further enhance impact and outreach, the efse Development facility launched a comprehensive impact study in

2013 spanning over three years and five sub-projects. We expect to receive first insights, which will undoubtedly inform the fund’s investment strategy, already in 2014. the study is also innovative in that it actively involves all stakeholders and provides a platform for joint discussions and conclusions. in addition, the efse Development facility managed 65 projects totalling eur 3.7 million in 2013 – up from 47 projects with a total volume of eur 2.5 million in 2012. in view of the opportunities it creates for facilitating both access to financial services and lower transaction costs for clients and financial institutions alike, mobile banking remains high on the efse Development facility’s agenda.

in 2013, the efse’s 71 partner lending institutions – a new record – were able to propel the on-lending rate for efse investments to new heights.

the efse aims to further generate impact at the development finance frontier by promoting the local currency agenda in our target markets, by providing risk capital in the form of subordinated loans and equity, and by promoting innovative approaches in mobile banking and agricultural lending.

At the same time, we fully support the resurgence in housing finance. As the only microfinance fund to also finance housing loans, the efse has become one of the main providers of housing finance in the region, having provided more than 30,000 housing loans since its inception in 2005. the efse’s commitment to housing finance is founded on four principles: first, decent shelter is a human right and hence part of the efse’s core mission; second, investments in home construction and improvement create jobs in the local economy; third, creating and preserving

letter from the chAirperson of the boArD of Directors

“the public-private partnership model remains at the core of the efse’s success in

achieving impact and outreach goals.”

5EFSE AnnuAl REpoRt 2013

real estate provides a long-term asset for the households taking out these loans; and fourth, modernization of housing leads to a reduction in energy consumption and co2 emissions, thus helping to counterbalance the effects of climate change.

on the funding side, the efse benefitted from strong growth in private sector contributions – both new and revolving investments – that brought capital commitments to an all-time high of eur 962 million. funding in us dollars especially gained momentum with a 96.6 % rise to close to usD 212 million. the public-private partnership model at the core of the efse consistently proves to be the most effective approach for achieving the fund’s goals, both qualitatively and quantitatively. We remain committed to staying the course whilst maintaining the capability to adapt to new events and meet the multiple expectations of all our stakeholders.

monikA beck

“As micro and small enterprises offer a

very high potential for job creation, but

are also vulnerable to disruptions, the role

of the efse in financing mses is as crucial

as ever.”

IntroductIon6 Macro level Journey review operational results appendices

greetings

the efse lives up to its key role of supporting eu Development goAls

the eu’s enlargement proceeds and continues as underlined most recently by the accession of croatia on 1 July 2013. in the same year, serbia was granted candidate country status and then started accession negotiations, joining other southeast europe countries such as montenegro and turkey.

A successful accession process depends on a number of political and economic factors linked to the accession criteria. one of the necessary preconditions is the existence of a healthy financial sector with firmly anchored institutions to facilitate and guide investment, to prepare and maintain the ground for a sustainable and, more importantly, self-propelling economy.

here, the role of the european fund for southeast europe is evident. since its inception in December 2005, three of the fund’s 16 target countries have joined the eu and accession negotiations with three more are underway. the efse consistently lives up to its role as a

stabilising, supporting and driving force for economic growth built on entrepreneurship, job creation and innovation. efse investments in an expanding target region have grown from eur 68 million at its start eight years ago, to eur 826 million for the benefit of more than 470,000 end-borrowers. this led to the creation of 460,000 jobs covering trade, service, production and the agricultural sector, thus significantly paying in to the economic stability of the region.

the success of the efse has also been confirmed by the eu’s comprehensive results-oriented monitoring system for eu projects, which attested the efse an A rating in all relevant metrics – relevance, efficiency, effectiveness, impact and sustainability.

ŠtefAn füleeuropean commissioner for enlargement and european neighbourhood policy

7EFSE AnnuAl REpoRt 2013

As trusteD AnD cApAble An Ally As ever in the pursuit of A common mission

the year 2013 has again proved that the federal ministry for economic cooperation and Development could not have a better ally in promoting employment creation, providing decent shelter via public-private partnership investments, and enhancing financial sector development in southeast europe and the european eastern neighbourhood regions. the efse more than lives up to its mission of fostering micro and small enterprises – the backbone of local economies – by facilitating ready and reliable access to the credit needed to grow businesses and create jobs.

one of the efse’s great success stories in 2013 has been the partnership with Agricover credit in romania, which benefited from both the funding and the technical assistance provided by the fund. As Agricover not only offers farm equipment and input goods for agricultural production, but also financing via Agricover credit bank, farmers get everything from one source and can be sure that the financing conditions reflect their seasonal cash-flow and payment capacity.

Aligning the components of success in Development finAnce

When we stood by its cradle in 2005, the european fund for southeast europe pioneered the concept of leveraging public funding to attract private capital for development finance. since then, the efse has taken the public-private partnership model to new heights, funding more than 470,000 sub-loans totalling eur 3.3 billion in its target regions since the fund’s inception – with more than 121,000 sub-loans with a total volume of eur 1 billion disbursed in 2013 alone.

Despite continued turbulence in some target countries, the efse remains a source of strength and stability. prudent investment decisions, timely and effective risk monitoring, and targeted technical assistance to partner institutions all contributed to further improving its portfolio quality with a record low level of 0.5 % for the impairment ratio and no realised losses since the start of operations.

the efse’s investment strategy is informed by intensive research. insights into the risks

this also aptly illustrates how the efse consistently practices the responsible finance it preaches, and how it integrates environmental and social guidelines into its strategy. the bmZ supports the efse’s increased focus on rural development, particularly through agricultural lending. in 2013, over 42,000 loans totalling close to eur 200 million were issued to micro and small farming operations, representing 35 % of all the loans granted to enterprises and 20.1 % of total lending – a remarkable

achievement.

the efse and its inclusive approach to development finance, combined with hands-on technical support for partner institutions that channel efse funds, are enabling the bmZ to achieve its goals in support of developing economies more efficiently and more speedily.

associated with foreign currency loans, for instance, led to concrete recommendations for shifting towards local currency lending. While these efforts are already bearing fruit, the efse Development facility is conducting a long-range study to gauge the fund’s development impact and outreach. invaluable guidance also comes from the twice-yearly meetings of the efse Advisory group, which bring together the regions’ central

bank governors and their representatives to exchange views and contribute to shaping the agenda.

kfW sees the efse as a blueprint for successfully interlinking the different components of effective development, and achieving real returns, both financially and in terms of impact, for all stakeholders.

Dr. gerD müllergerman federal minister for economic cooperation and Development

source of picture: bundesregierung / kugler

Dr. norbert kloppenburg member of the executive board of kfW bankengruppe

IntroductIon8 Macro level Journey review operational results appendices

‘Qualitative growth’ probably best captures the focus of fund management activities during 2013. Despite the challenging environment, the efse’s outstanding portfolio, invested in 71 partner lending institutions, grew to close to eur 830 million. even more noteworthy, however, are the dynamics behind these figures. first, around one quarter of the total portfolio was effectively repaid during 2013 and successfully placed again in new investments. the outcome was a record eur 245 million in approved investments. second, the efse welcomed nine new partner lending institutions over the course of the year, clear evidence of our active portfolio management approach to incorporate new clients with diverse institutional profiles who will responsibly provide financing to the fund’s ultimate target group.

furthermore, fund management efforts concentrated, on the one hand, on enhancing development impact whilst controlling portfolio risks on the other. We are particularly proud that all the investments granted to partner lending institutions were almost fully on-lent by year’s end. our partner lending institutions disbursed more than 121,000 sub-loans – averaging slightly more than eur 8,500, they clearly benefited micro and small enterprises – for a total volume of eur 1 billion. the agricultural sector in particular saw a significant uptick this year, accounting for one third of all loans and about 20 % of the total volume disbursed to micro and small enterprises. We see this as the result of well-designed financial products and efficient service delivery mechanisms, to which the efse Development facility contributed significantly through tailored capacity building projects. the efse Development facility closed a record year with 65 projects under management with a total budget of eur 3.7 million.

in addition to enhancing the development impact of our investment and technical assistance activities, the fund management was engaged in intensive risk monitoring and portfolio restructuring. As a consequence of our pro-active and hands-on risk management, the level of impairments in the portfolio dropped by half to only 0.5 % at year-end compared to one year ago – well below the industry average. At the same time, it is worth noting that the fund, completing its eighth year of operations, has never realised any losses.

none of these results and achievements would have been possible without the continuous support and guidance provided by the board of Directors and the various committees, for which we are deeply grateful. finally, we also feel very privileged by the outstanding partnerships that have evolved over the past years with the diverse group of stakeholders of the fund – investors, partner financial institutions, central banks and other financial sector institutions.

We therefore feel very well equipped to continue to provide significant funding and support to further strengthen and expand the fabric of micro and small enterprises in the efse’s target regions in the years to come.

letter from the funD mAnAger AnD funD ADvisor

9EFSE AnnuAl REpoRt 2013

mAX von frAntZius

managing Director,oppenheim Assetmanagement services

sylviA WisniWski

managing Director,finance in motion

thomAs Albert

managing Director,oppenheim Assetmanagement services

elvirA lefting

managing Director,finance in motion

clAuDiA DAmbAX

senior Associate,oppenheim Assetmanagement services

floriAn meister

managing Director,finance in motion

IntroductIon10 Macro level Journey review operational results appendices

micro AnD smAll enterprises: the bAckbone of A mArket economy …it is a common saying that micro and small enterprises (mses) represent the backbone of any market economy. in most countries these businesses usually account for more than 90 % of all enterprises and more than 50 % of employment. moreover, mses are widely regarded as the engine of growth, development and innovation due to their alleged flexibility and entrepreneurial orientation. modern empirical research suggests that most mses start and stay small, i. e. that the traditional view of mses and their contribution to economic growth applies only to a small number of mses – the so-called gazelles. however, a healthy mse sector overall remains a key prerequisite for any successful and stable market economy. given the legacy of state planning in the countries of the european eastern neighbourhood region (enr), i. e. Armenia, Azerbaijan and georgia (the caucasus), as well as belarus, moldova and ukraine, the emergence and development of mses is of even greater importance than in mature market economies. it is against this background that public policies as well as private-public partnerships, such as the european fund for southeast europe, aim at supporting mses, concretely by facilitating mse access to credit.

… yet A mArket economy is WhAt proviDes the bAckgrounD for mse Developmentmses do not operate in a vacuum. rather, as much as they influence growth and development, they, too, are exposed to macroeconomic conditions and outcomes. Whether the economy is growing in real terms at 5 % p. a. or more will decide on the success or failure of mses. strong growth makes it easier to sell

products and services, generate revenues and build up capital. moreover, in good times, banks and other financial service providers are more inclined to engage in providing finance to mses at reasonable terms. conversely, in a recession it is more difficult to ensure an adequate level of retained earnings. in addition, banks and other investors become more risk averse; credit constraints for mses are even more pronounced than in normal times. Access to finance becomes even more impaired if the recession is coupled with a financial crisis, when not only banks, but also bank investors and depositors become more risk-averse – and new funding pressures loom over the banks.

crisis AnD mse Development – tWo vieWsthis being said, there are two opposing views on the impact of a crisis on mse development and subsequent contribution to a dynamic economy. on the one hand there is the view echoing the arguments just made: a crisis puts a special burden on mse development because mses are – given their size – inherently fragile and, due to their often specialised product portfolio and focused regional orientation, more vulnerable to shocks. the other view holds that mses might benefit from tough macroeconomic conditions because – at least in a comparative perspective – they are more nimble and flexible than larger companies, which makes it easier for them to adapt to changing circumstances. some also subscribe to the schumpeterian view of ‘creative destruction’, according to which a recession creates fertile ground and opportunities for small businesses to replace obsolete technologies and products, and effectively take over from the industry dinosaurs represented by large corporations.

A mAcro perspective of mse finAnce – the europeAn eAstern neighbourhooD region

* ADAlbert Winkleris professor of international and Development finance at the frankfurt school of finance & management.

by professor Adalbert Winkler *

11EFSE AnnuAl REpoRt 2013

mAcroeconomic Development in the europeAn eAstern neighbourhooD region – converging to stAgnAtion?Applying this perspective to the enr is not easy, as economic development has been quite heterogeneous. chart 1 shows that Armenia and ukraine experienced a deep post-lehman recession, whilst the downturn was more subdued in belarus, georgia and moldova. in Azerbaijan, reflecting the economy’s reliance on natural resources, notably oil extraction, there effectively was no noticeable decline in output growth in 2009. moreover, the chart also shows that recovery patterns were far from uniform. for example, whilst real gDp per capita in ukraine is still far below pre-crisis levels, Armenia is back to real gDp figures recorded in 2008. Despite facing great turmoil in 2009, georgia’s growth

performance over the whole post-crisis period has been so strong that, in relative terms, the post-2008 growth process has been more dynamic than in Azerbaijan.

however, in 2012, and even more so in 2013, there was a notable convergence of growth patterns across the region, i. e. a decline in the differences. this move towards convergence has been accompanied by a decline in the average growth rate of the countries under review: in 2012 and 2013 real gDp growth was below 3 %, down from around 5 % in 2011 and 2010. Whilst projections made before recent events in ukraine suggested that average growth would pick up slightly in 2014 by about one percentage point, the political turmoil in ukraine is likely to make these projections obsolete.

Chart 1 reAl gDp in the enr per cApitA 2004 – 2013

2008 = 100

source: imf, own calculations

40

50

60

70

80

100

90

110

120

130

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Chart 1

0,3

0,6

0,9

1,2

1,5

Armenia Azerbaijan belarus georgia moldova ukraine

IntroductIon12 Macro level Journey review operational results appendices

the outlook for groWth – Domestic DemAnD AnD privAte sector creDit given the slowdown in growth and stagnating per capita income, domestic demand is not likely to be stimulated by consumption. this holds true even though – until end-2013 – a continuous flow of remittances supported spending by private households. moreover, given rising government debt levels in all countries under review, in particular in Armenia and ukraine, there is barely room for fiscal expansion. thus, within the domestic demand components, investment would have to support growth. however, in contrast to the pre-crisis period, the credit boom is not only

over, but in some countries, i. e. ukraine and belarus, substantial deleveraging has taken place (chart 2). this is also reflected in high non-performing loan ratios for several countries within the region as a legacy of the previous boom-bust cycle and the slow recovery. finally, credit conditions are not likely to improve given the spillovers of monetary tightening in the united states to emerging markets in general. political upheaval in ukraine and its potential implications for the region as a whole have added an exacerbating local component to this aspect.

Chart 2 privAte sector creDit to gDp rAtio in the enr

source: ebrD, World bank (moldova 2004 – 2008), central banks (2013 figures), imf, and own calculations

0

10

20

30

40

60

50

70

80

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Chart 2

01020304050607080 Armenia

Azerbaijan belarus georgia moldova ukraine

in %

13EFSE AnnuAl REpoRt 2013

outlook – Will eXports Drive groWth?given the dismal prospects for domestic demand, countries of the enr might have hoped for a revival of external demand as a source for growth. indeed, Armenia, belarus and ukraine recorded, on average, higher current account deficits in the post-crisis period 2010 – 2013 than in the pre-crisis period (chart 3), a clear indication that the external dimension of regional growth is far from satisfactory. With the end of the recession in europe and the projected further expansion in the united states, the outlook for a pick-up in demand for exports from enr countries seemed promising. however, positive signs from mature economies are counterbalanced by comparatively low growth in emerging market countries, notably russia. the political and economic fallout of recent events in ukraine might even lead to a worsening outlook, reflecting the importance of the russian market to the region, not only with regard to exports but also as a source of remittances.

conclusion: mse Development in A volAtile mAcroeconomic environmentmses are the backbone of any market economy, but macroeconomic developments have a substantial impact on mse activities. in recent years mses in the enr have been facing a diverse macroeconomic environment ranging from deep recessions related to financial crisis to booms reflecting high oil prices, from strong post-crisis recovery to a low growth trajectory. for 2014, early projections indicated a transition towards a somewhat stable but low growth scenario in all countries. the events in ukraine effectively nullify these projections. hence, mses are confronted with yet new challenges that will test their flexibility and expose their vulnerabilities – or strengths.

Chart 3 current Accounts in the enr

in %

source: imf (World economic outlook Database, october 2013), own calculations

– 30

– 20

– 10

0

10

30

20

40

Average 2004 – 2007 Average 2010 – 20132008 2009

Armenia Azerbaijan belarus georgia moldova ukraine

IntroductIon14 Macro level Journey review operational results appendices

Different economic reAlities in the regionsoutheast europe (see) was severely hit by the european economic crisis. the second ‘leg’ of the great recession (2012 / 13) limited external demand and capital inflows after the initial negative shock in late 2008. however, the negative impact was very different across countries.

turkey recorded the highest growth rate since 2011, the size of its economy and long-term growth prospects helping to sustain the investment boom financed by globally more diversified sources of capital inflows in comparison to other see countries. Among other see economies, only kosovo and Albania achieved 2 % or better growth, on average, for 2011 – 2013. the above-average economic growth of these two countries was due to their low starting point and continued financial inflows, which were reflected in current account deficits that remained high at 10 % of gDp. fyr macedonia and montenegro, by contrast, recorded growth rates between 1 % and 2 %. the rest of the region experienced very low growth or prolonged recession (table 1).

stalling capital inflows were most obvious in croatia and bulgaria where no significant deficits of the current account of the balance of payments occurred in the last couple of years. however, this does not suggest that the revival of capital inflows (and associated external deficit) is a necessary ingredient for rekindling economic growth. the experience of bosnia and herzegovina, serbia and

montenegro since 2011 shows large deficits of the current account of the balance of payments (associated with capital inflows) without high rates of economic growth. therefore, the absence of a growth dynamic across most of see should be attributed to fundamental factors other than capital inflows.

inDebteDness, finAnciAl mArket imper fections AnD institutionAl WeAknesses As obstAcles to groWththe three obstacles to economic growth in see discussed here are indebtedness in sectors that had easy access to finance during the cycle’s last boom phase, financial market imperfections, and institutional weaknesses.

first, indebtedness is still relatively high in vital economic segments across the region. the vital segments are governments and large corporations that had easy access to finance during the last boom cycle. government debt to gDp ratios (43.4 % on average) are relatively high for medium income countries (bulgaria being the notable exception). private debt (mainly corporate debt) is also relatively high given the income per capita: bank loan to gDp ratios average 56.7 %. however, there is a relatively small share of lending to households everywhere except croatia. therefore, a reduced capacity to raise additional debt within sectors that had easier access to banks in the past will continue to limit debt-related capital inflows in the future. this, however, does not apply to households in most countries in see.

A mAcro perspective of mse finAnce – southeAst europe

* velimir ŠonJeis Director of Arhivanalitika, a consultancy based in Zagreb, croatia. he worked as a macroeconomic and financial consultant on projects in croatia, bosnia and herzegovina, montenegro, romania and ukraine.

by velimir Šonje *

15EFSE AnnuAl REpoRt 2013

universal commercial banks dominate financial sectors whilst international banking groups dominate local banking systems (turkey is a notable exception, see table 2). given the advanced stage of international banking integration, it is tempting to conclude that banking sector problems in europe led to a sudden stop of capital flows via international banks, which severely slowed down economic growth across the region. following this logic, the recovery of european banks, which will hopefully follow the forthcoming banking union within the eu, will help revive capital inflows via banks and bring credit flows back to former levels. however, this narrative is too simple in terms of providing a complete picture of economic growth and financial development prospects. in gauging these prospects, the imperfect mechanisms of capital allocation in see, which is the second main impediment to economic growth, must be taken into account.

banks and members of international banking groups served the bankable segments of local markets too well before the crisis. for this reason, large debtors facing the prolonged recession or low growth environment have an immediate need for more capital and/or debt restructuring. As far as new capital is concerned, this is where local capital allocation mechanisms proved dysfunctional, reflecting weak capital markets, low venture capital availability (see table 2) and a lack of focus on smaller, healthy businesses on the part of large banks. some segments of the micro and small enterprise (mse) sector and low-income households were financially underserved during the previous boom cycle. the future of banking in the region, therefore, is mainly associated with retail and mse lending, coupled with financial development programmes that should lead to a greater supply of equity. the future also lies in supporting larger companies with a potential for faster growth in international markets.

populA-tion in

million

gDp per cApitA At pps * in %

of eu AverAge

reAl gDp groWth

rAte in %

totAl in-vestment

As % of gDp

gross nA-tionAl sAv-

ings rAte As % of gDp

bop ** current

Account bAlAnce As

% of gDp

gross govern-

ment Debt As % of

gDp

unemploy-ment rAte

in %inflAtion rAte in %

Albania 3.243 30 2.0 24.4 13.7 – 10.7 61.9 13.8 2.5

bosnia and herzegovina 3.884 29 0.4 16.0 6.9 – 9.3 42.3 27.5 2.5

bulgaria 7.285 47 1.0 22.3 22.3 0.0 16.4 12.0 2.4

croatia 4.287 62 – 0.9 20.8 20.6 – 0.2 52.9 15.5 2.9

kosovo n/a n/a 3.4 n/a n/a – 10.6 n/a n/a 4.0

fyr macedonia

2.066 35 1.6 n/a 23.7 – 4.2 32.5 30.9 3.3

montenegro 0.622 41 1.4 20.3 – 1.0 – 17.5 51.1 n/a 3.2

romania 21.339 50 0.3 26.7 23.2 – 3.5 36.9 7.2 4.5

serbia 7.259 36 0.6 20.5 11.4 – 9.1 59.3 24.2 9.0

turkey 75.106 54 4.9 21.2 13.5 – 7.7 37.1 9.5 7.7

SEE average 43 1.5 21.5 14.9 – 7.3 43.4 17.6 4.2

source: imf (World economic outlook Database, october 2013, data for 2013 are imf’s forecasts, eurostat (for gDp at pps per capita)* purchasing power standard** balance of payments

tablE 1 mAin mAcroeconomic inDicAtors for see, 2011 – 2013 AverAges

IntroductIon16 Macro level Journey review operational results appendices

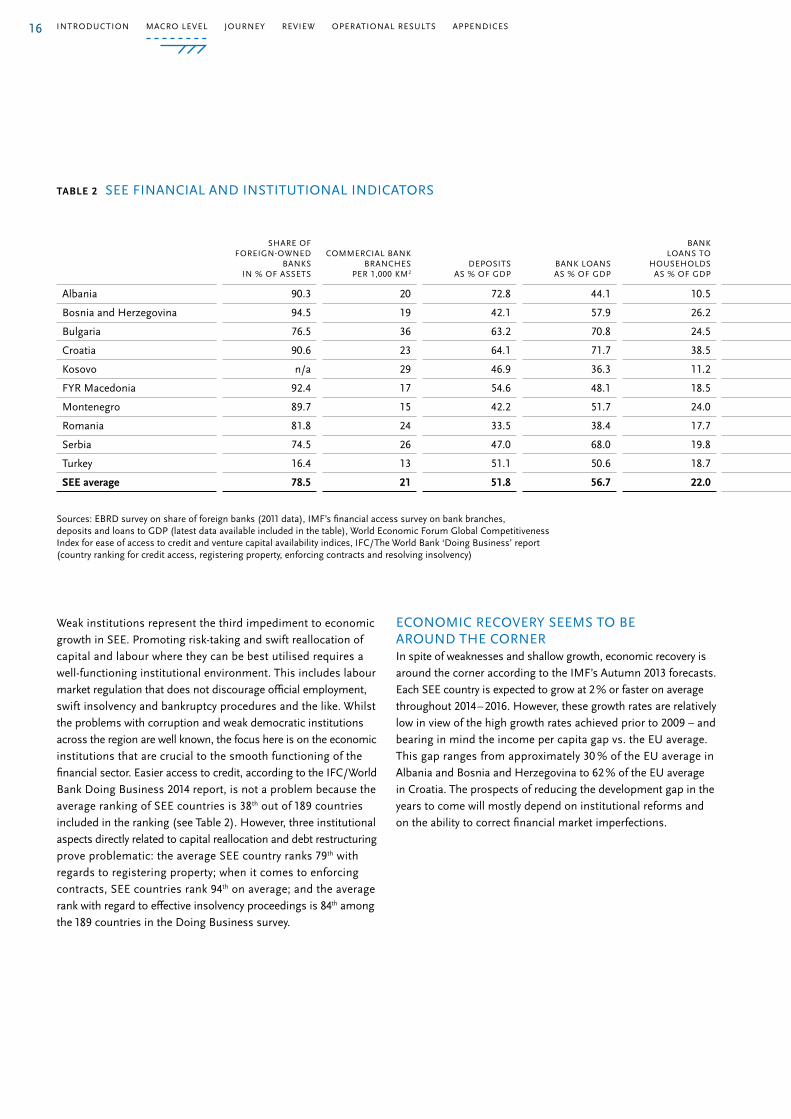

Weak institutions represent the third impediment to economic growth in see. promoting risk-taking and swift reallocation of capital and labour where they can be best utilised requires a well-functioning institutional environment. this includes labour market regulation that does not discourage official employment, swift insolvency and bankruptcy procedures and the like. Whilst the problems with corruption and weak democratic institutions across the region are well known, the focus here is on the economic institutions that are crucial to the smooth functioning of the financial sector. easier access to credit, according to the ifc / World bank Doing business 2014 report, is not a problem because the average ranking of see countries is 38th out of 189 countries included in the ranking (see table 2). however, three institutional aspects directly related to capital reallocation and debt restructuring prove problematic: the average see country ranks 79th with regards to registering property; when it comes to enforcing contracts, see countries rank 94th on average; and the average rank with regard to effective insolvency proceedings is 84th among the 189 countries in the Doing business survey.

economic recovery seems to be ArounD the cornerin spite of weaknesses and shallow growth, economic recovery is around the corner according to the imf’s Autumn 2013 forecasts. each see country is expected to grow at 2 % or faster on average throughout 2014 – 2016. however, these growth rates are relatively low in view of the high growth rates achieved prior to 2009 – and bearing in mind the income per capita gap vs. the eu average. this gap ranges from approximately 30 % of the eu average in Albania and bosnia and herzegovina to 62 % of the eu average in croatia. the prospects of reducing the development gap in the years to come will mostly depend on institutional reforms and on the ability to correct financial market imperfections.

shAre of foreign-oWneD

bAnks in % of Assets

commerciAl bAnk brAnches

per 1,000 km2

Deposits As % of gDp

bAnk loAns As % of gDp

bAnk loAns to

householDs As % of gDp

eAse of Access to

creDit *

venture cApitAl

AvAilAbility *

creDit Access – country rAting **

registering property –

country rAnking **

enforcing contrActs –

country rAnking **

resolving insolvency –

country rAnking **

Albania 90.3 20 72.8 44.1 10.5 1.9 1.9 13 119 124 62

bosnia and herzegovina 94.5 19 42.1 57.9 26.2 2.0 1.9 73 96 115 77

bulgaria 76.5 36 63.2 70.8 24.5 3.3 2.7 28 62 79 92

croatia 90.6 23 64.1 71.7 38.5 2.4 2.2 42 106 49 98

kosovo n/a 29 46.9 36.3 11.2 n/a n/a 28 58 138 83

fyr macedonia 92.4 17 54.6 48.1 18.5 2.9 2.5 3 84 95 52

montenegro 89.7 15 42.2 51.7 24.0 3.3 3.2 3 98 136 45

romania 81.8 24 33.5 38.4 17.7 2.7 2.4 13 70 53 99

serbia 74.5 26 47.0 68.0 19.8 2.2 1.9 42 44 116 103

turkey 16.4 13 51.1 50.6 18.7 3.1 2.5 86 50 38 130

SEE average 78.5 21 51.8 56.7 22.0 2.6 2.4 38 79 94 84

sources: ebrD survey on share of foreign banks (2011 data), imf’s financial access survey on bank branches, deposits and loans to gDp (latest data available included in the table), World economic forum global competitiveness index for ease of access to credit and venture capital availability indices, ifc / the World bank ‘Doing business’ report (country ranking for credit access, registering property, enforcing contracts and resolving insolvency)

* 1 – 7, with 7 being the most desirable outcome** total 189 countries

tablE 2 see finAnciAl AnD institutionAl inDicAtors

17EFSE AnnuAl REpoRt 2013

encourAging risk tAking AnD conDucive policies Are essentiAl for economic Development in conclusion, weak capital markets within a still-developing institutional framework impose high transaction costs and discourage risk taking and capital reallocation. this deficiency is one of the major obstacles to closing the development gap with the eu. some of the well-known recommendations for real convergence by attracting foreign direct investment still have the potential to facilitate economic growth and employment in see, especially when considering the relatively low labour costs in the

region. however, the internal capacities for economic dynamism within see countries must be roused and strengthened. risk taking should be encouraged; capital should be permitted to enter and exit economic activities freely and swiftly in the process of creation and creative destruction. Availability of risk capital should be substantially increased. policies should aim at improving institutions, protecting property rights, reducing bureaucracy and transaction costs, and supporting growth of mses. each and every private venture, no matter how small, is important in this respect. here, access to finance is vital because the future of see, to a not insignificant degree, rests on entrepreneurial spirit.

shAre of foreign-oWneD

bAnks in % of Assets

commerciAl bAnk brAnches

per 1,000 km2

Deposits As % of gDp

bAnk loAns As % of gDp

bAnk loAns to

householDs As % of gDp

eAse of Access to

creDit *

venture cApitAl

AvAilAbility *

creDit Access – country rAting **

registering property –

country rAnking **

enforcing contrActs –

country rAnking **

resolving insolvency –

country rAnking **

Albania 90.3 20 72.8 44.1 10.5 1.9 1.9 13 119 124 62

bosnia and herzegovina 94.5 19 42.1 57.9 26.2 2.0 1.9 73 96 115 77

bulgaria 76.5 36 63.2 70.8 24.5 3.3 2.7 28 62 79 92

croatia 90.6 23 64.1 71.7 38.5 2.4 2.2 42 106 49 98

kosovo n/a 29 46.9 36.3 11.2 n/a n/a 28 58 138 83

fyr macedonia 92.4 17 54.6 48.1 18.5 2.9 2.5 3 84 95 52

montenegro 89.7 15 42.2 51.7 24.0 3.3 3.2 3 98 136 45

romania 81.8 24 33.5 38.4 17.7 2.7 2.4 13 70 53 99

serbia 74.5 26 47.0 68.0 19.8 2.2 1.9 42 44 116 103

turkey 16.4 13 51.1 50.6 18.7 3.1 2.5 86 50 38 130

SEE average 78.5 21 51.8 56.7 22.0 2.6 2.4 38 79 94 84

sources: ebrD survey on share of foreign banks (2011 data), imf’s financial access survey on bank branches, deposits and loans to gDp (latest data available included in the table), World economic forum global competitiveness index for ease of access to credit and venture capital availability indices, ifc / the World bank ‘Doing business’ report (country ranking for credit access, registering property, enforcing contracts and resolving insolvency)

* 1 – 7, with 7 being the most desirable outcome** total 189 countries

FigurE 1 estimAteD AverAge gDp groWth rAtes in see 2014 – 2016

in percent

source: imf’s Autumn 2013 economic forecast

kosovo

1

2

3

4

5

turkey fyr macedonia

bosnia and herzegovina

romania Albania montenegro serbia bulgaria croatia

18

albania 10

kosovo 9

Bulgaria 12

moldova 3

romania 4

croatia 6

bosnia and herzegovina 7

montenegro 8

serbia 5

FYR macedonia 11Al

mD

N

E

S

W

19EFSE AnnuAl REpoRt 2013

turkey 13

georgia 14

azerbaijan 15

armenia 16

Belarus 1

ukraine 2

a jourNEythrough the regions

the efse aims to foster economic development and prosperity in 16 countries in southeast europe and the european eastern neighbourhood region. these countries lie like a string of pearls in the centre of the continent, each with its individual profile. the following pages showcase the key successes of the efse and the efse Development facility in each of these countries throughout 2013.

tr

AZ

20 Journey through the regions

the efse continued to support private micro and small enterprises (mses) in belarus by syndicating with the ebrD to build capacities at its partner lending institution there, belgazprombank, to provide sustainable financial products to the mse market. the eur 30 million credit facility, with the efse’s participation totalling eur 20 million, is the second syndicated loan between the efse and ebrD.

bElaruSefse AnD ebrD Join forces in synDicAtion

“ the european fund for southeast europe is one of the key non-bank participants in the ebrD b loan program in the financial institutions sector, having already participated twice in ebrD b loans in the past, in moldova and belarus. the efse has played an important role for ebrD in its co-financing efforts in countries where attracting foreign private capital from traditional commercial banks is more challenging. the efse brings together private and public sources of financing to provide sustainable funding to micro and small enterprises in southeast europe, and its ability to provide medium-term financing alongside ebrD makes it a very welcome lender for borrowers who are otherwise able to raise only short-term funding from traditional commercial banks.

ebrD’s A / b loan structure is one where ebrD remains the lender of record for the entire commitment, and commercial banks and other institutional investors derive benefit from the ebrD’s preferred creditor status by participating in the b loan. ebrD itself is not part of the syndication and provides finance via the A loan only. the participation agreement will transfer all risks to the participating b lenders who share preferred creditor status.” muZAffAr Zukhurov, principAl bAnker, ebrD loAn synDicAtions DepArtment

muZAffAr Zukhurovprincipal banker, ebrD loan syndications Department

belArus | minsk1

Minsk

populAtion (2013): 9.6 million

currency: belarusian ruble (byr)

gDp (2013, nominAl): eur 50 billion

AreA: 207,595 km2

by

5belarus ranks 5th worldwide by patent activity, indicating a very high scientific and technical potential.

by

21

ukraiNE promoting finAnciAl literAcy in pArtnership With nAbu

the efse Development facility (Df) supported a pertinent initiative of the independent Association of banks in ukraine (nAbu) in 2013. launched in cooperation with kfW Development bank, nAbu’s financial literacy initiative addressed the information gap between financial institutions and the general public. During the course of the project, the efse Df sponsored the development and printing of a brochure on the topic of financial services for elderly people. the brochure was presented to all 80 nAbu member banks and subsequently distributed throughout the ukraine. efse Df funds were also used to co-sponsor a series of trainings, workshops, press conferences and open-house events (mainly at banks) as well as financial education sessions for schoolchildren.

ukrAine | kyiv2

Journey through the regions

kyiv

populAtion (2013 estimAte): 44.6 million

gDp (2013, nominAl): eur 127 billionAreA: 603,628 km2

currency: ukrainian hryvnia (uAh)

uA 1ukraine has the best black soil

in Europe and therefore a strong

agricultural potential.

uA

22 Journey through the regions

given the various challenges the moldovan financial sector has to overcome, the efse emphasised combining investments with targeted technical assistance (tA) to support individual institutions in internal process optimisation and in institutional capacity building. the efse’s partner lending institution microinvest benefitted from a large-scale tA project to enhance its sales management capabilities and to achieve greater efficiency and scale. the dedicated consultancy was accompanied by a senior rural loan facility that enables microinvest to provide financial support to micro and small enterprises (mses) in rural areas, individual farmers and agricultural producers. microinvest is one of the few microfinance institutions in moldova to serve rural mses, ensuring access to finance for entrepreneurs and agricultural businesses countrywide.

the main achievements of the tA project were the successful integration of the sales force effectiveness concept in microinvest’s daily operations and the extensive sales tool training for 70 staff members.

the people at microinvest quickly demonstrated a strong sense of ownership with the tA project; the knowledge transfer is expected to have a sustainable impact on the institution. A new project with microinvest is scheduled for early 2014 with a key focus on financial planning and management capacities, specifically with regard to local currency funding.

MoldovabuilDing microinvest’s cApAcities to ADDress the rurAl mArket

mobile signAture proJect: the moldovan government received the best m-government Award for its mobile signature project at the annual gsmA mobile World congress in 2013.

molDovA | chisinAu

Chisinau

populAtion (2013): 3.6 million

currency: moldovan leu (mDl)

gDp (2013, nominAl): eur 6 billion

AreA: 33,846 km2

7the republic of Moldova is the 7 th

country in the world where citizens

can store an electronic signature

on their mobile phones.

mD

mD

3

23

roMaNia suborDinAteD loAn to bAncA trAnsilvAniA strengthens cApitAl bAse for on-lenDing

romAniA | buchArest

Journey through the regions

bucharest

populAtion (2013): 21.3 million

gDp (2013, nominAl): eur 133 billion

AreA: 238,391 km2

currency: romanian new leu (ron)

in view of the challenging operating environment in romania, which is reflected in the deteriorating asset quality of its financial sector, the efse has focused on the areas where it can achieve the highest possible impact.

one such opportunity in 2013 was to contribute towards strengthening the capital base of one of romania’s leading banks, banca transilvania. An efse partner lending institution since 2006, banca transilvania will leverage a eur 15 million subordinated loan through on-lending to micro and small enterprises (mses) throughout romania.

“over the years, the efse has time and again proved a valuable partner, providing our bank with long-term funding facilities that helped us to offer attractive financing solutions to our customers. our partnership has a long history, having started in 2006 with a eur 10 million housing loan agreement. other notable projects helped to strengthen banca transilvania’s capital base via three subordinated loan agreements.

besides indirect funding to the mse sector in romania, the efse also contributed to enhancing micro and small enterprise business management by preparing an educational booklet on the risks inherent to foreign currency borrowing.

We appreciate the efse’s involvement in and its commitment to our region, and we look forward to continuing our outstanding cooperation.” omer tetik, ceo, bAncA trAnsilvAniA s.A .

3.5 %

romania posted one of the highest gdP growth rates in the Eu in 2013 with 3.5 %.

ro

ro

4

24 Journey through the regions

in serbia, the efse established a new partnership with intesa leasing belgrade through a eur 5 million loan. intesa leasing leverages the nationwide network of its parent, banca intesa belgrade, a long-standing efse partner lending institution, to provide much-needed long-term finance to fuel the growth of micro and small enterprises (mses) as well as agro producers. intesa leasing belgrade is proving very effective at helping these customer segments to overcome the barriers posed by the collateral requirements of traditional commercial bank financing. intesa leasing belgrade was also the first to offer local currency leasing in serbia, thus significantly contributing to the promotion of financial products in local currency.

At first, the company was focused only on financing new passenger and commercial vehicles. by the end of 2006, however, the scope of business was expanded to cover the financing of plant and equipment and in 2013 to the lease of commercial buildings. intesa leasing belgrade also recognised the numerous challenges of the economic crisis, which confronted all the participants in the financial markets, in time, and shifted its financing focus towards production equipment and commercial vehicles. this immediately reduced exposure to the risks and problems that the passenger car industry was facing then and still faces today.

intesa leasing belgrade also places a strong emphasis on the mse segment, i. e. primarily family-owned businesses in manufacturing for exports or services such as domestic and international logistics. it is precisely this client segment, recognised as the healthiest part of the company’s corporate sector, which proved to be the most resilient. these businesses faced the crisis by redoubling their efforts, making new investments and improving their efficiency. the synergies intesa leasing belgrade achieved with these clients, by supporting them financially in the most difficult times, contributed significantly towards establishing long-term cooperation and partnership relations and towards positioning intesa leasing belgrade as a leader in long-term financing for plant and equipment as well as for commercial vehicles.

SErbiaintesA leAsing – groWing the leAsing segment

serbiA | belgrADe

belgrade

populAtion (2013): 7.2 million

currency: serbian dinar (rsD)

gDp (2013, nominAl): eur 32 billion

AreA: 77,474 km2

20.9 %average capital adequacy

of banks in Serbia was 19.9 %

as at Q4 2013.

rs

rs

5

25Journey through the regions

Croatia ZAgrebAckA bAnkA pArticipAtes in the “micro & sme bAnking summer AcADemy”

croAtiA | ZAgreb

Zagreb

populAtion (2013): 4.4 million

gDp (2013, nominAl): eur 43 billionAreA: 56,594 km2

currency: croatian kuna (hrk)

Zagrebacka banka (ZAbA) is the efse’s first partner in croatia and is very much aware of its role in contributing to economic development by supporting entrepreneurship, particularly for micro and small enterprises (mses) in the country. small business clients are served through a close-knit network of 131 branches and 60 entrepreneurial centres with mse-dedicated staff. the efse’s credit line enables ZAbA to further explore new opportunities and create new products in the mse segment. the logical next step was for the efse Development facility to facilitate a training programme for key ZAbA personnel on developing and implementing products specifically destined for the mse segment. upon their return to croatia, the three ZAbA delegates actively shared their know-how throughout the bank’s branch network, enabling relationship managers to in turn present new products to mse clients as well as to better recognise and address the needs of this target group.

47Croatia ranks 47 out of 187 in the uN human development index,

which makes it no. 1 amongst the EFSE target countries.

hr

hr

6

26 Journey through the regions

Despite the difficult economic times and increasingly evident strategic challenges for the microfinance industry in bosnia and herzegovina, the efse continued to facilitate access to finance for micro and small enterprises (mses) in the country through these important socially oriented conduits. the thrust of these efforts was focused on mikrofin group, an efse partner lending institution in bosnia and herzegovina, in the form of both financial and, via the efse Development facility (Df), capacity building support at its two specialised institutions: the microfinance institution mikrofin and the commercial bank mf banka. providing a choice to mses, expanding the financial services to them and leveraging the strength of both institutions, namely the finance company mikrofin and the bank mf banka, was the key objective for the efse. the efse is proud, especially in these difficult economic times, to support an institution that strives to defy the conventional thinking and is consistently making headway in the right direction.

boSNia aNd hErZEgoviNaboosting the strAtegic cooperAtion betWeen An mfi AnD A commerciAl bAnk

“ the idea to integrate the financial support for mses under one roof proved to be exactly what our customers needed. the benefits of such cooperation between the leading microfinance institution and a commercial bank are numerous, both for the two institutions and for their respective clients. this, however, would not have been a success without the understanding and continuous support of the efse, our long-term partner.”

AleksAnDAr kremenovic, chAirmAn of mikrofin group

bosniA AnD herZegovinA | sArAJevo

Sarajevo

populAtion (2013): 3.9 million

currency: convertible mark (bAm)

gDp (2013, nominAl): eur 14 billion

AreA: 51,197 km2

92.6 %

92.6 % of enterprises in bosnia and herzegovina belong

to the MSE sector.

bA

bA

7

27Journey through the regions

me

MoNtENEgro hipotekArnA bAnkA receives technicAl AssistAnce for mse lenDing

in 2013, the efse Development facility provided hipotekarna banka in montenegro with technical assistance (tA) in the area of micro and small enterprise (mse) lending, supporting the bank in addressing this customer segment. the tA covered comprehensive trainings and workshops for management and staff in specific techniques and skills for effectively assessing and selling mse loans as well as managing the associated risks. the project equipped the bank’s staff with the knowledge to implement effective mse lending throughout the entire loan cycle. the ‘training of trainers’ approach will enhance the project’s sustainability, as selected staff will provide future refresher courses within the institution.

montenegro | poDgoricA

Podgorica

populAtion (2013): 0.6 million

gDp (2013, nominAl): eur 4 billion

AreA: 13,812 km2

currency: euro (eur)

rEgioNal: mse brochures on fX risk

A regional financial education project will help the efse partner lending institutions raise financial literacy within their mse client base – this in turn is expected to result in better-informed, and better performing clients. in 2013, the efse Development facility finalised the adaptation of a client educational booklet on foreign exchange lending for mses into eight languages. Distribution of the 150,000 copies to 14 financial institutions in eight countries (Albania, Armenia, Azerbaijan, fyr macedonia, moldova, romania, serbia and ukraine) will be completed in 2014.

1 Eur

the minimum paid-in capital

for establishing a new company in

Montenegro is only one euro.

me

8

28 Journey through the regions

the ‘Agrifinance in kosovo’ study aimed to assess the main supply and demand patterns for financial services in kosovo’s agricultural sector – a topic of particular relevance given the strategic importance of agriculture and its financing gaps. Whilst the study found that there is high demand for agricultural finance in kosovo, it also identified specific barriers. its recommendations cover various aspects ranging from improving the enabling environment, understanding farmer needs and specifics of this important economic segment, a tailored risk assessment and respective agronomic tools, options for advancing in value chain finance, exploring innovative products, improving cost-effectiveness, and the needs for providing technical assistance to overcome these barriers.

koSovoinvestigAting the potentiAl of AgrilenDing

kosovo | prishtinA

Prishtina

populAtion (2011 estimAte): 1.7 million

currency: euro (eur)

gDp (2013, nominAl): eur 5 billion

AreA: 10,908 km2

3 dayS

the time it takes to register a business in kosovo.

ko

ko

9

29Journey through the regions

albaNia nurturing the seeDlings of success

AlbAniA | tirAnA

tirana

populAtion (2013): 3.3 million

gDp (2013, nominAl): eur 9 billion

AreA: 28,748 km2

currency: Albanian lek (All)

“ green beans, that’s the ticket. green beans. it’s strange how a decision like that can make the difference between a good year and a less good one,” muses Ali Dedja, scratching his chin.

“ We get a much better yield than with tomatoes, which is what we grew last year. so switching was actually an easy decision,” Ali adds. With the first loan from noA in 2009, which was for just over eur 8,500, he had erected his first greenhouse on the land behind his house to grow more vegetables, both in terms of quantity and diversity. “good sun exposure and little wind, plus the soil is very healthy. most important, though, is that my wife and i make a very good team,” he says.

growing produce in his greenhouse enabled Ali to substantially increase productivity, and, more importantly, to achieve a more consistent harvest. “A consistent product, especially with consistent quality, that’s really what counts for my customers,” Ali observes. “When it comes to consistency, especially for what we grow, there is really no way around a greenhouse.”

the latest loan from noA, in July 2013, for just over eur 2,000 went towards purchasing new seeds. this investment enabled Ali to better align his cultures with market demand as well as grow a type of produce that was better adapted to the climate and soil conditions. “We thought long and hard about it, but switching from tomatoes to green beans has so far been one of the best decisions we’ve made.”

“ As a grower, you understand that some things take time and that what you get out of something depends on what you put in. it’s the same with business. not only does noA share that philosophy, but they also take pride and pleasure in seeing my little farm grow from a small greenhouse into a robust enterprise.” Ali DeDJA, greenhouse groWer

nAme: Ali Dedja

business: greenhouse grower

bAnk: noA

18 %

agriculture contributes with 18 % to total gdP in albania and is the

only sector that continuously positively contributes to gdP growth.

Al

Al

10

30 Journey through the regions

mAceDoniA | skopJe

Skopje

populAtion (2013): 2.1 million

currency: macedonian denar (mkD)

gDp (2013, nominAl): eur 8 billion

AreA: 25,713 km2

Fyr MaCEdoNiaADApt. innovAte. groW.

“ When i was out of a job in 1991, all i had was my background in engineering and my skills as a welder. i had to adapt. When i decided to start my own business, my family backed me up 100 %,” explains Aleksandar Aleksovski.

speaking of family support, Aleksandar’s two daughters, Angelovska and blagica also work in the business, komont. from a small locksmith’s workshop, Aleksandar leveraged his welding skills into a metal fabrication workshop. eventually, there was enough business to add importing and exporting to komont’s activities.

“ my greatest satisfaction? to be able to build on my experience and my skills and create a business that not only sustains me and my family, but also enables me to create jobs!” exclaims Aleksandar. As the economy developed and consumption increased, so did advertising. komont soon made a name for itself by fabricating aesthetically pleasing yet robust outdoor billboard carriers, especially very large ones. “honestly, i never dreamed i’d be welding frames as tall as a house,” Aleksandar admits.

the eur 50,000 loan from nlb tutunska banka in 2011 enabled komont to stabilise cash flow. “We’re building strong relationships with major media companies. this puts us on a solid footing so we can branch out to larger projects, like hall structures.” Aleksandar adds, “everything one step at a time.”

“ believing in yourself and your skills is good. it can be enough to get you started. but what keeps you going is when others begin to share your vision and join in to help you to make it become reality. i knew i could count on my family. With nlb, i found out i could also count on my bank.” AleksAnDAr Aleksovski, locksmith

nAme: Aleksandar Aleksovski

business: locksmith, metal working

bAnk: nlb tutunska banka AD skopje

25Fyr Macedonia ranks 25 among

189 countries in ease of doing business

according to the Wb / iFC’s

“Ease of doing business” report.

mk

mk

11

31Journey through the regions

Bulgaria | sofia

Sofia

PoPulation (2013): 7.2 million

gDP (2013, nominal): eur 39 billion

area: 110,994 km2

currency: Bulgarian lev (Bgn)

the economic crises in the eurozone have had a strong impact on Bulgarian business and consumption, with the country’s economy slowly recovering from its five-year slump. one of the sectors that suffered the most was construction development, which changed the dynamics of building stock availability in terms of quality and supply. coupled with the increase in private household income instability, this resulted in many banks being more averse to expanding their housing loan portfolios. Providing adequate support to private households for financing home purchases and renovation was becoming an increasingly acute necessity. Despite the difficult environment, efse partner lending institution raiffeisenbank Bulgaria remained committed to supporting this segment.

Bulgaria fostering home imProvement

“ raiffeisenbank (Bulgaria) eaD disbursed more than 600 loans to lower income households with the help of a eur 20 million efse credit line for financing house improvements, renovations, enlargements, and reconstructions, as well as for purchasing homes.

these funds were used for financing housing loans at attractive interest rates with an extended repayment period of 30 years.

the transaction reaffirmed the efse’s commitment to strengthen its presence in Bulgaria’s financial sector and to increase the range of financial products offered to customers from the segments of the economy that are still not well serviced by the banks.” raiffeisenBank

13.5 %

in Bulgaria construction permits for new individual homes in 2013 increased by 13.5 %.

Bg

Bg

12

32 Journey through the regions

nAme: bülent incebayraktar, AZim su ArmAturleri sAn. tic. ltD. sti.

business: kitchen and bathroom fixtures

bAnk: Alternatifbank

turkEytApping the potentiAl for groWth

“ When you’re in business as long as we’ve been – we’re the second generation – you see good times and less good times. And when the going gets tough, you realise the importance of having a strong foundation for business. that and a strong partner like Alternatifbank is what gets you through when the going gets tough.” bülent incebAyrAktA, AZim su ArmAturleri sAn. tic. ltD. sti.

turkey | istAnbul

istanbul

ankara

populAtion (2013): 76.5 million

currency: turkish lira (try)

gDp (2013, nominAl): eur 595 billionAreA: 783,562 km2

7turkey is Europe’s 7th largest economy

tr

tr