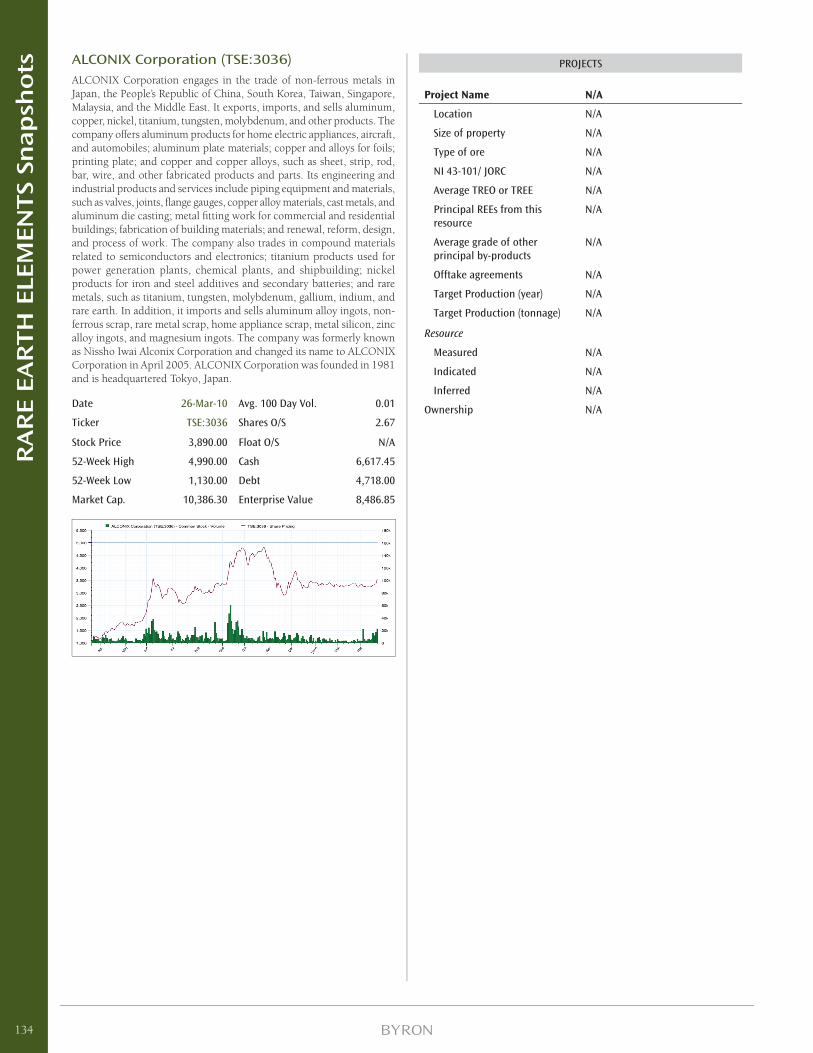

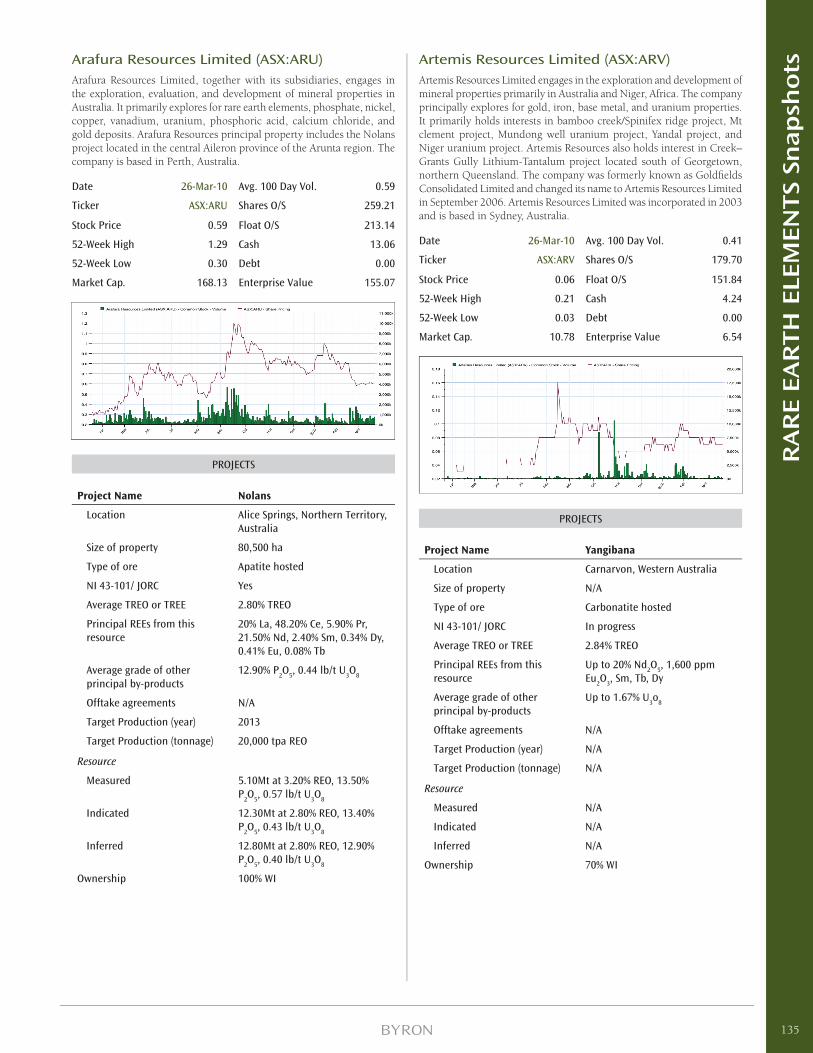

electric metals green book - byron capital markets (april 2010)

TRANSCRIPT

Ele

ctr

ic M

eta

ls |

Gr

ee

n B

oo

k |

Ap

ril 2

01

0

G r e e n B o o k | A p r i l 2 0 1 0

ELECTRIC METALS

4 King Street West, Suite 1100 | Toronto, Ontario | M5H 1B6

t:647 426 1660 | f:647 426 1661 | byroncapitalmarkets.com

Company Directory

Executive

Campbell Becher, President 647-426-1657 [email protected]

Corporate Finance

Cliff Rich, Managing Director – Vancouver 604-805-3606

Robert Orviss, Managing Director – Toronto 647-426-1668 [email protected]

Alex Watson, Associate – Vancouver 604-616-0190

John Rak, Associate 647-426-1663 [email protected]

Russell Mills, Associate647-426-0290 [email protected]

Yeganeh Pakdaman, [email protected]

Research

Guy Gordon, Head – Research, Oil & Gas Analyst647-426-1672 [email protected]

Jon Hykawy, Ph.D., Clean Technologies & Materials Analyst647-426-1656 [email protected]

Drew Clark, Mining Analyst 647-426-1673 [email protected]

Al P. Nagaraj, Special Situations Analyst 647-426-0291 [email protected]

Arun Thomas, Associate 647-426-1674 [email protected]

Gabriela Casasnovas, Associate647-426-0287 [email protected]

Sales & Trading

Main Trading Line 647-426-1670

Cyrus Osena, Head – Institutional Sales 647-426-1675 [email protected]

David Kemp, Head – Institutional Trading 647-426-1666 [email protected]

Kariv Oretsky, Institutional Sales 647-426-1658 [email protected]

Nick Stajduhar, Institutional Sales 647-426-1664 [email protected]

Steve Low, Institutional Sales 647-426-1667 [email protected]

Tom Chudnovsky, Institutional Sales 647-426-1665 [email protected]

Jonathan Samahin, Institutional Sales & Trading 647-426-1670 [email protected]

Nick Perkell, Institutional Trading 647-426-1671 [email protected]

Elisa Chio, Associate 647-426-0288 [email protected]

Operations

Derrick Chiu, Head – Syndication 647-426-1662 [email protected]

Marco Beretta, [email protected]

Robyn [email protected]

Table of Contents

Lithium: The Next Strategic Material ............................................................................................................................1

Western Lithium Canada Corporation – Initiating Coverage .................................................................................... 14

Western Lithium Canada Corporation – Note .......................................................................................................... 25

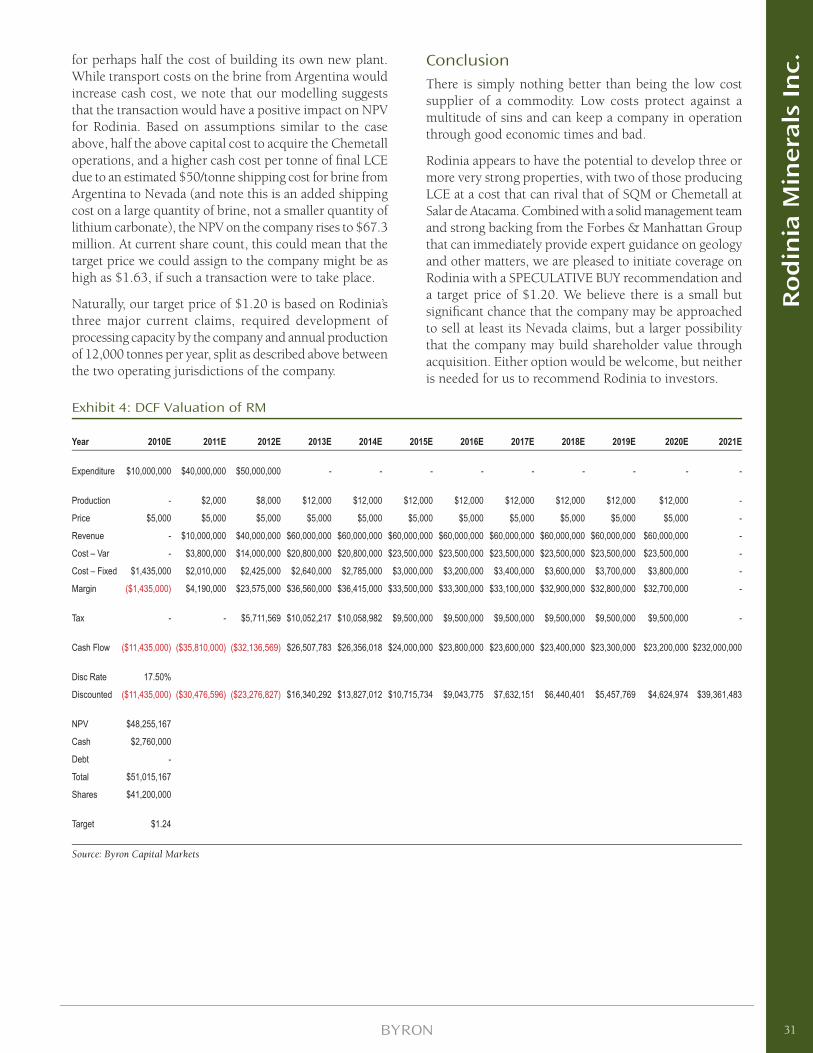

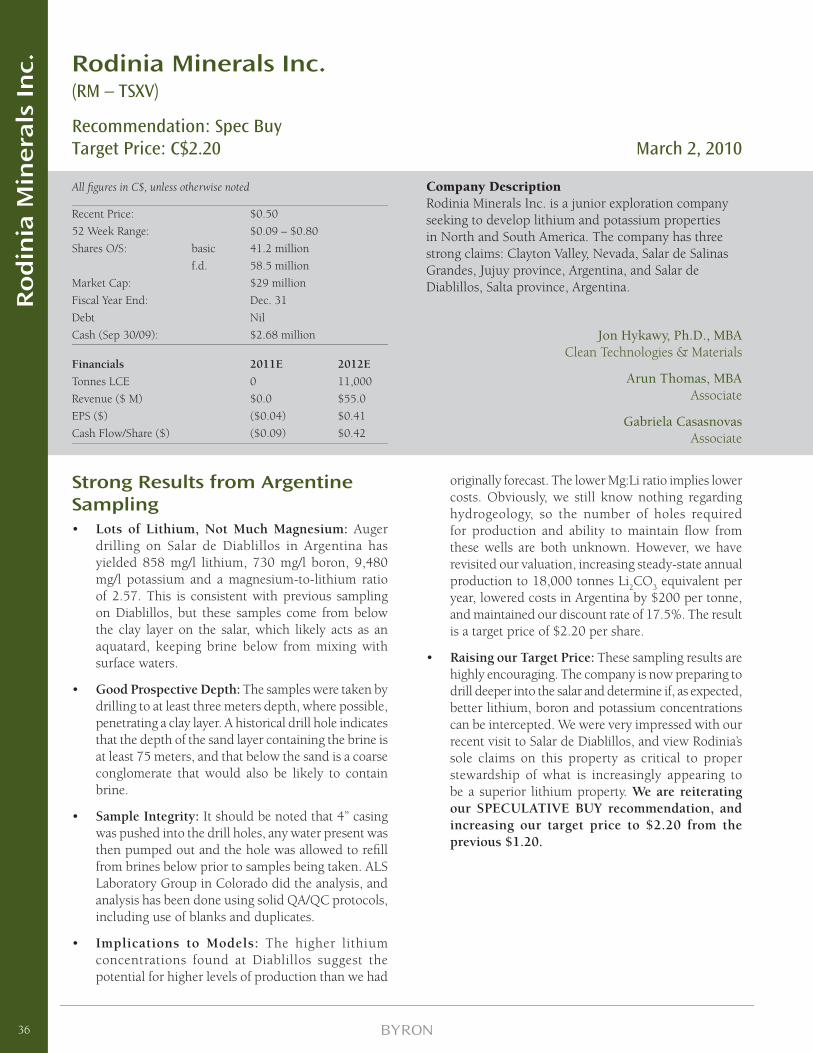

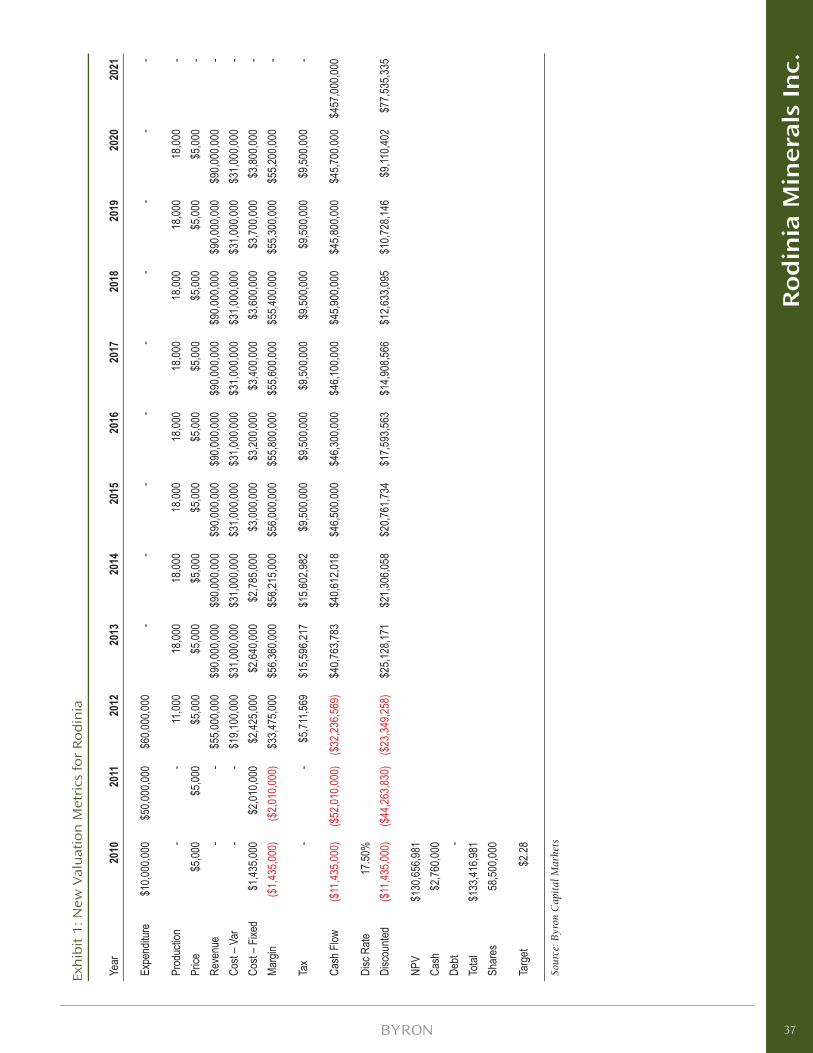

Rodinia Minerals Inc. – Initiating Coverage .............................................................................................................. 27

Rodinia Minerals Inc. – Note ................................................................................................................................... 36

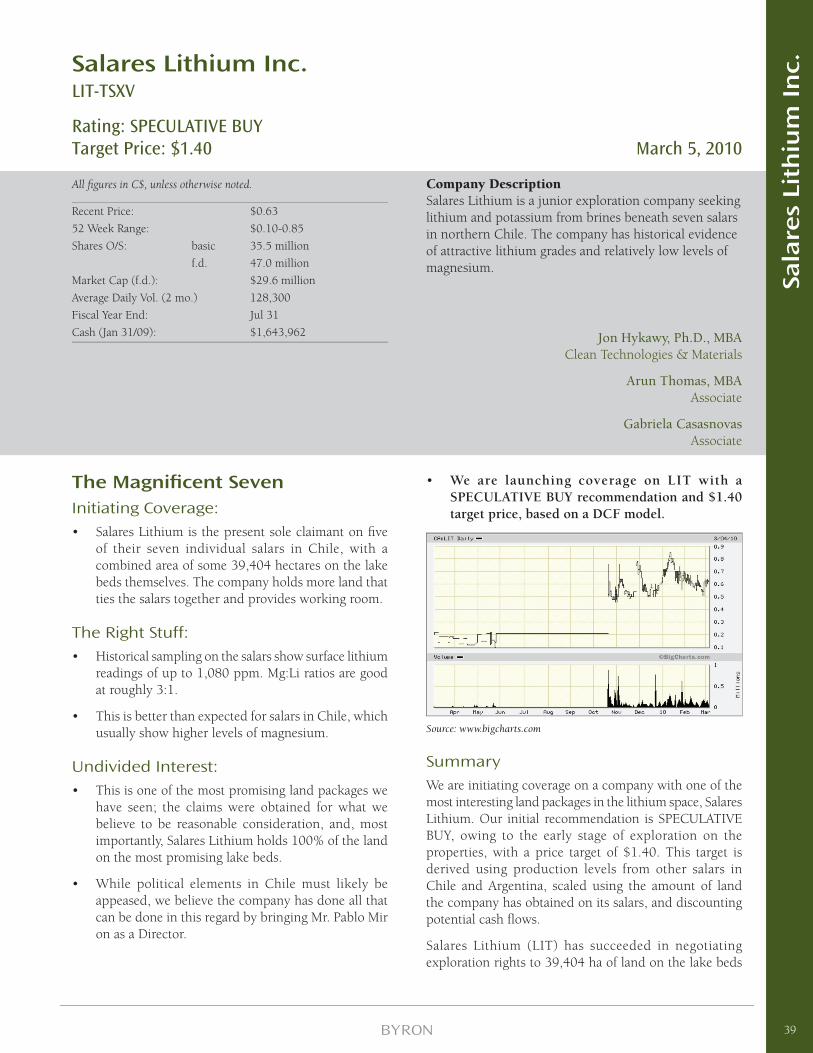

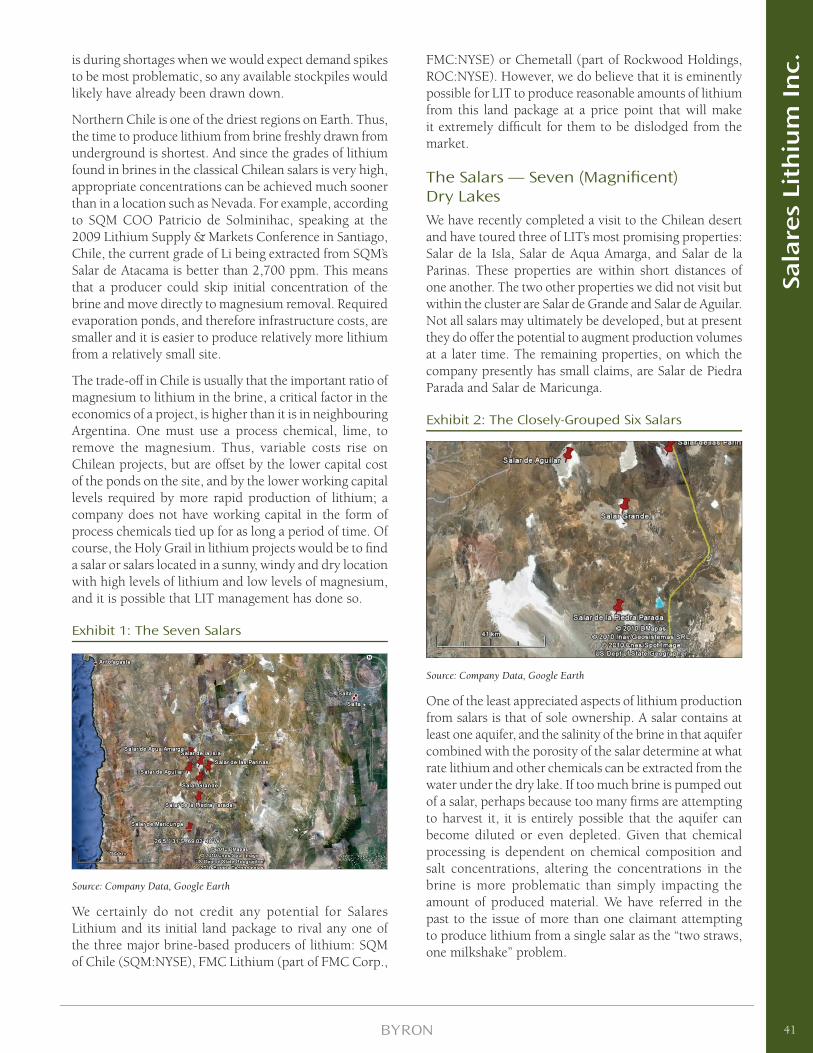

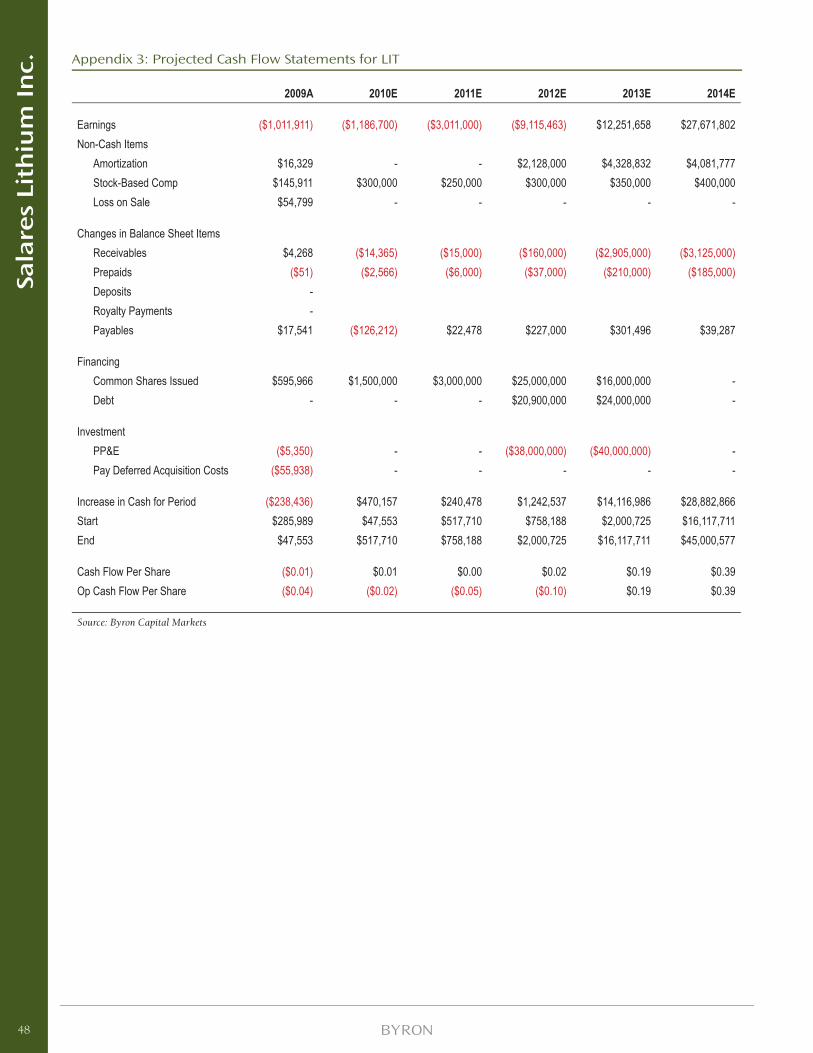

Salares Lithium Inc. – Initiating Coverage ................................................................................................................ 39

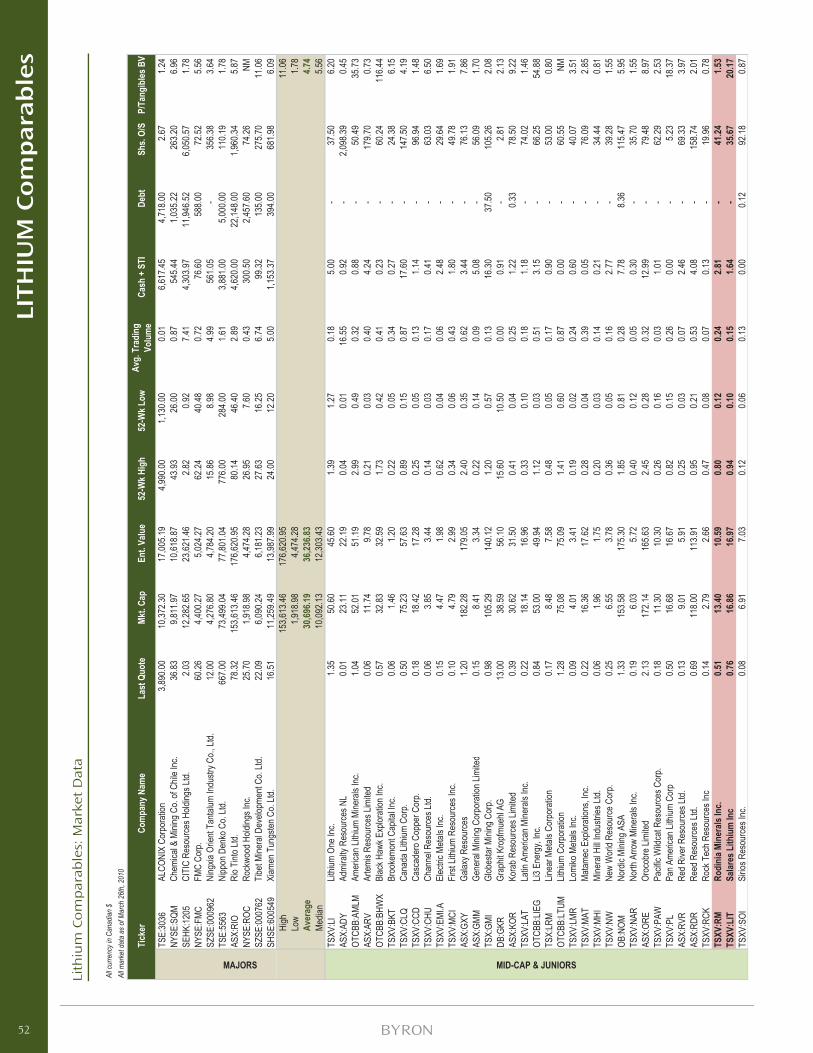

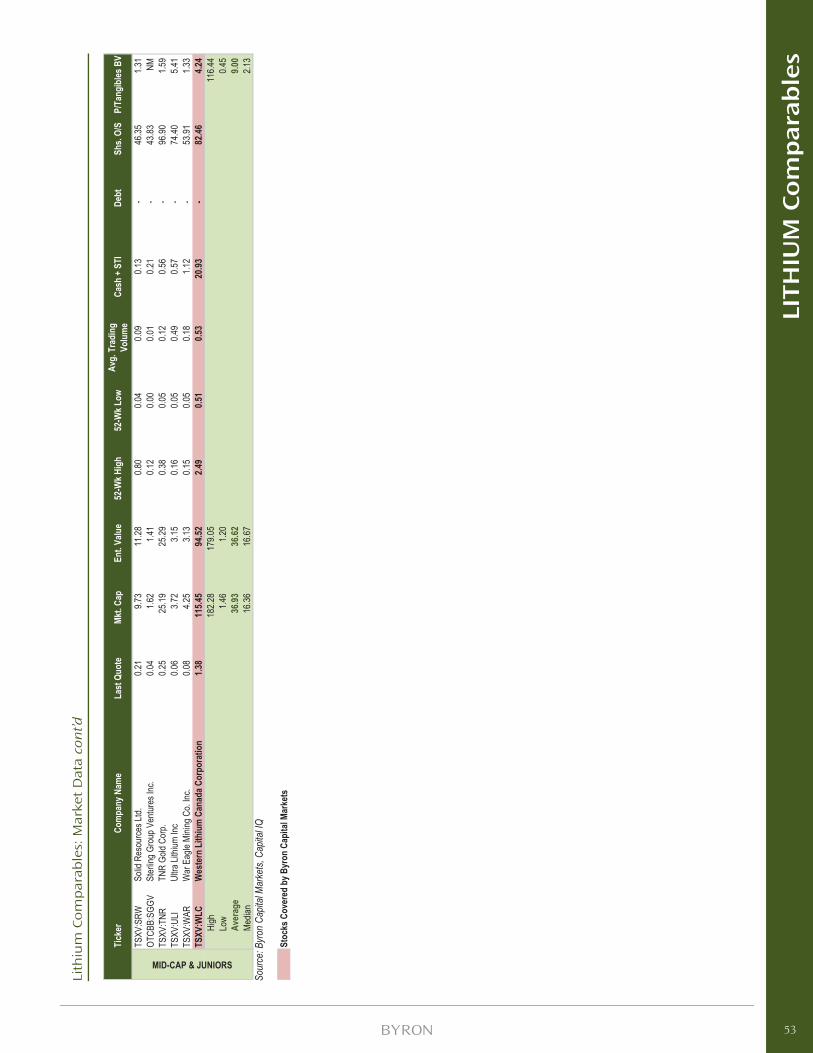

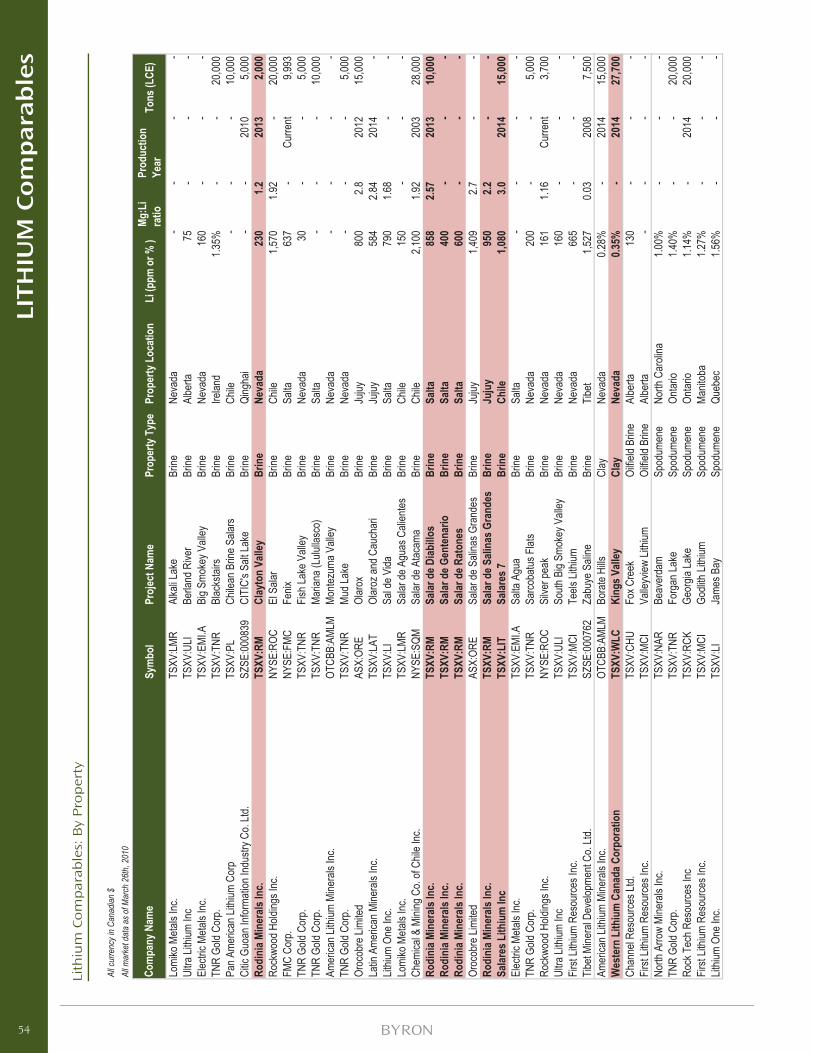

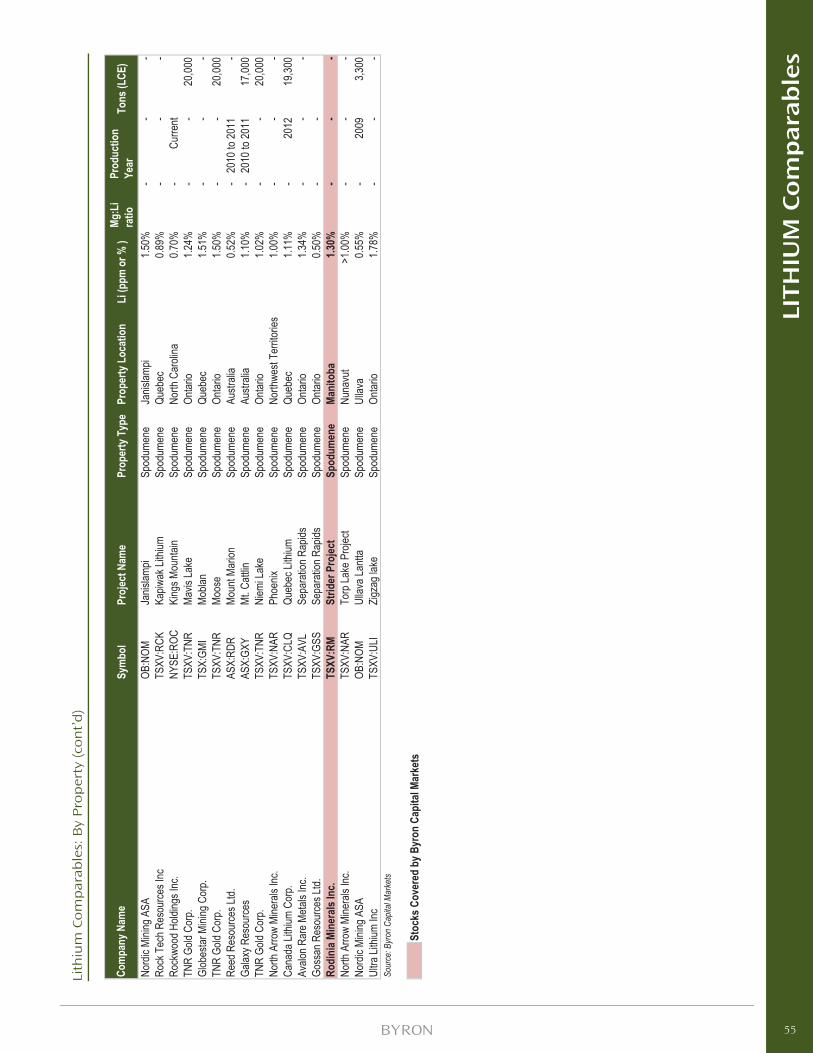

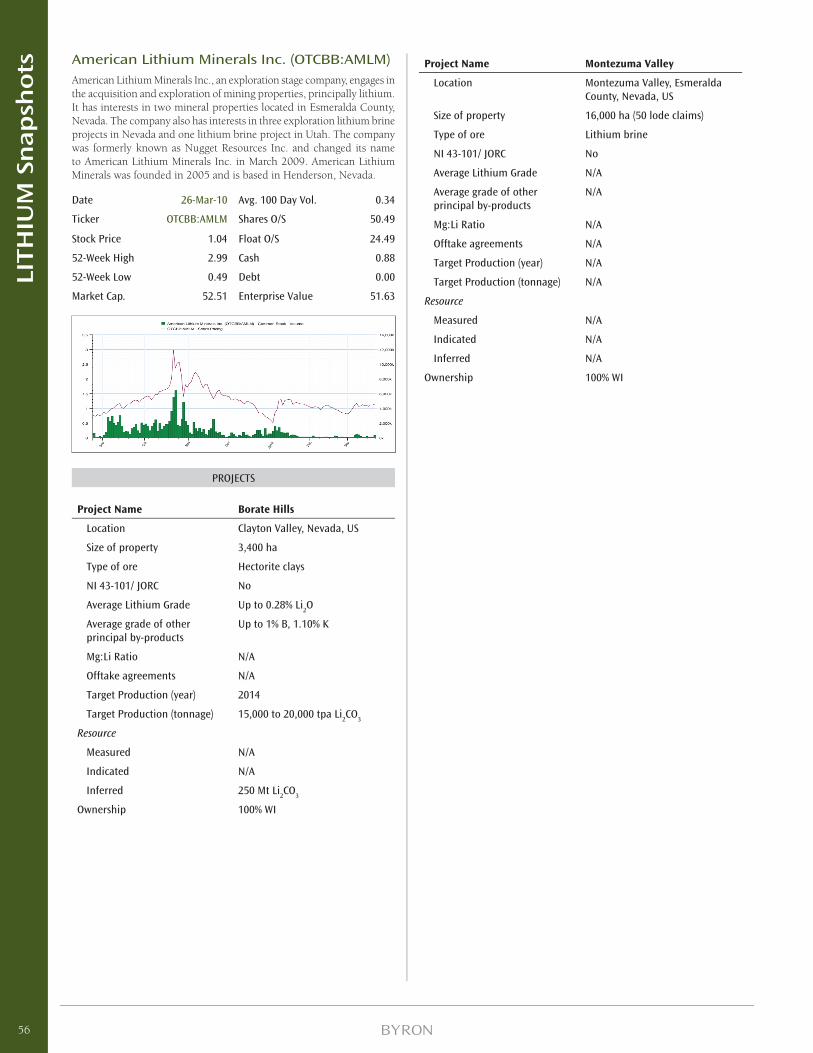

Lithium Comparables Tables .................................................................................................................................... 52

Lithium Snapshots ................................................................................................................................................... 56

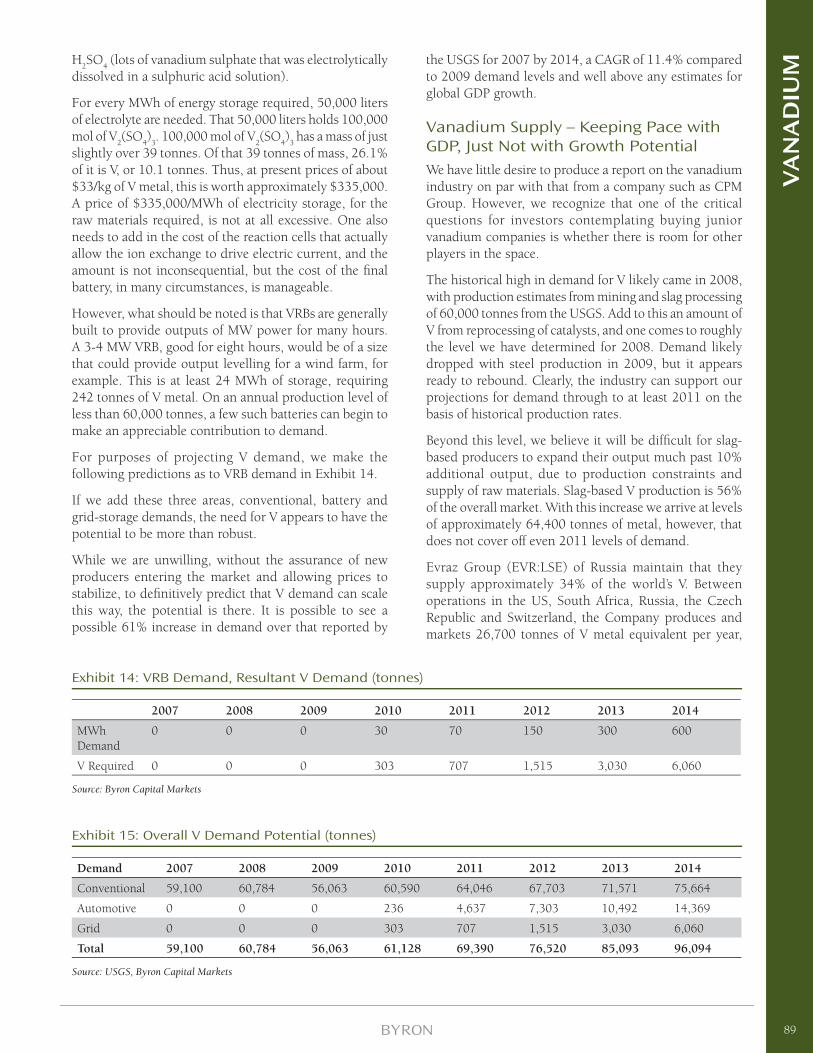

Vanadium: The Supercharger ..................................................................................................................................... 82

Largo Resources Ltd. – Initiating Coverage ............................................................................................................... 93

Vanadium Comparables Table ................................................................................................................................ 104

Vanadium Snapshots .............................................................................................................................................. 105

Rare Earth Elements – Pick Your Spots, Carefully ................................................................................................... 119

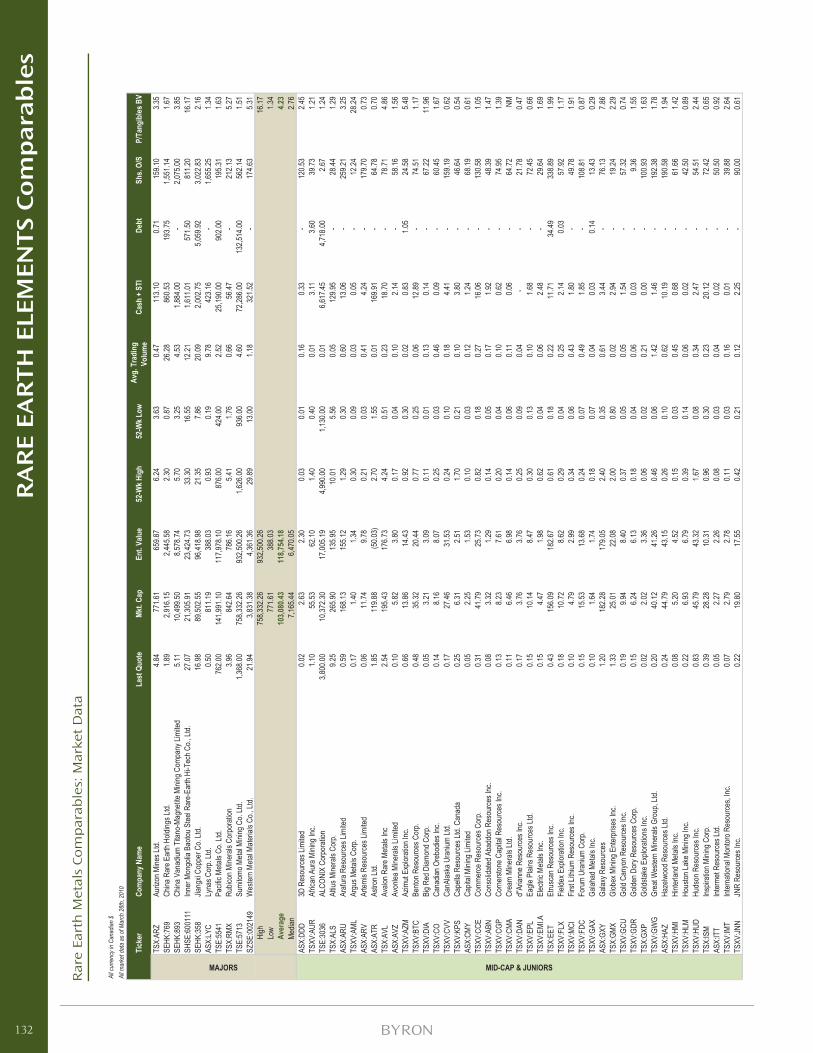

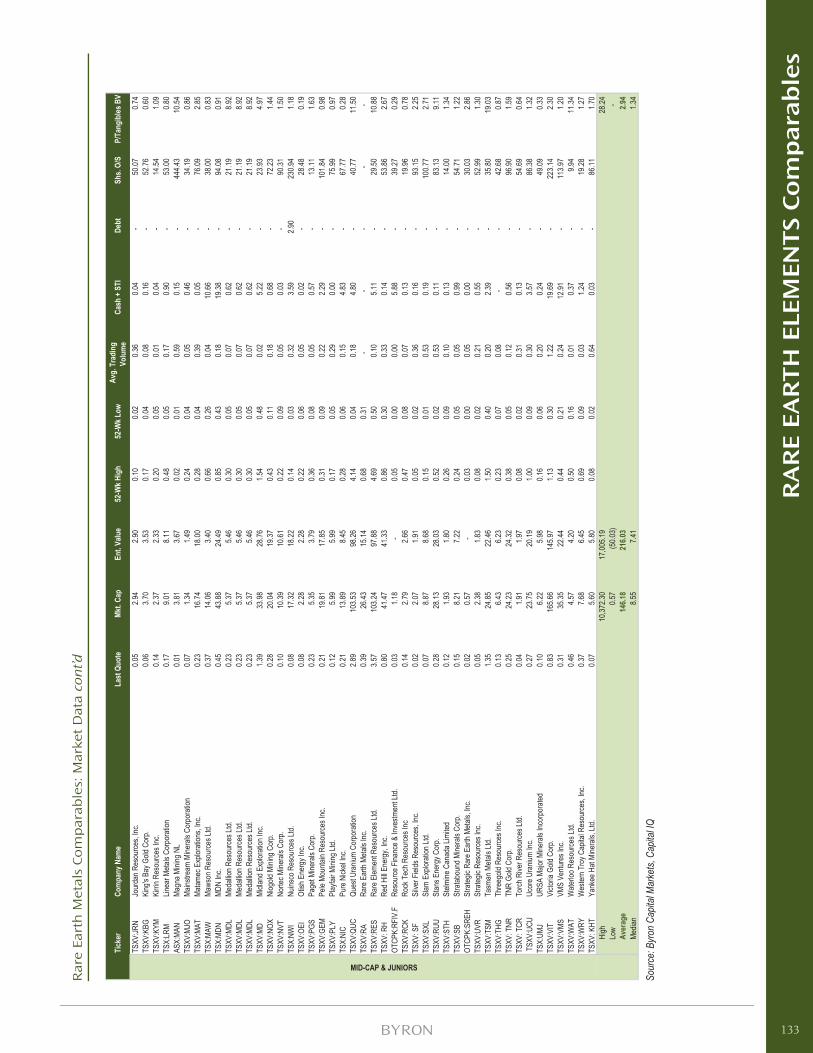

Rare Earth Elements Comparables Table ................................................................................................................ 132

Rare Earth Elements Snapshots .............................................................................................................................. 134

Lithium: The Next Strategic MaterialMarch 31, 2010

Supply is stagnant• Major players in the market produce from brines

through evaporation

• Brines cannot easily respond to spot increases in demand or price

• Brine sources are “living”, dynamic systems, and dramatically increasing production can damage them

• Hard-rock mining is too expensive, and takes too long to establish

• Clays are promising, but under development

Demand is rising• Demand today is in the range of 120,000 tonnes of

lithium carbonate equivalent (LCE) annually

• With GDP levels of growth in some industries, and 10% CAGR in areas such as consumer battery demand, plus automotive use, we foresee demand rising nearly 40% by 2014

Low cost suppliers will win the battle• Lowest cost suppliers are brines. Variable cost of a

brine production is perhaps $1,200 per tonne LCE, ex-labor. Cost may be $2,300 per tonne LCE including amortization, ex-labor. But cost is highly dependent on low magnesium content in the brine.

• Hard rock/spodumene mining has highest costs. Variable costs may be as high as $3,100 per tonne LCE ex-labor, and fully amortized costs may be $6,400 per tonne LCE. If present prices continue to rise, all is well, but varying prices for LCE can spell doom for spodumene-based producers.

• We suggest investors also look at clay-based producers. While variable costs for such an operation may be as high as $2,300 per tonne LCE ex-labor, this is acceptable compared to brines that are higher in magnesium content. Amortized costs are also reasonable at $3,300 per tonne LCE, especially given it appears LCE produced via this route is cleaner than brine-sourced lithium.

Investors can win the war• We believe investors with appropriate risk profi les

are best served by owning a basket of lithium stocks, concentrating on brine-based explorers working in known regions, and some strong speculative plays such as clay-based production.

SummaryLithium has arisen from nothing to represent the great hope for electrifi cation of the light vehicle fl eet. And this is not an unsubstantiated hope. Lithium batteries were relatively unknown in the late 1990s, but have become ubiquitous in portable electronics since. With declining prices and improvements in capabilities, not only have lithium batteries swept close to 100% share in end-use markets such as cellular telephones and laptops, but the batteries are breaking into low-end consumer electronics (game players, music players) and high-performance portable power tools.

Demand is running at levels of roughly 120,000 tonnes of lithium carbonate equivalent (LCE) annually, according to SQM management at the January 2009 Lithium Supply and Markets Conference in Santiago, Chile. We believe that demand is slated to rise dramatically. While roughly 78% of present demand is purely industrial in nature and will increase at rates of global GDP, the remaining 22% of current demand is due solely to the growth in consumer batteries since 2000. This will grow at rates much higher than GDP, and likely much better than the rates of consumer electronic shipments; iSuppli has predicted that consumer electronics shipments will increase by 2% in 2010, 4% in 2011, and then pick up beyond that to the 6-8% per year growth to which we have become accustomed. We believe that with lithium-ion batteries penetrating into new markets due to improving performance and price, and with automotive use beginning in 2010, battery use should accelerate past a 10% CAGR. Based on our estimates, outlined in detail below, we see demand growing to more than 163,000 tonnes annually by 2014.

Demand and supply are tightly balanced today, with the bulk of production coming from SQM (SQM:NYSE) in Chile, at 32,600 tonnes, Talison in Australia at 28,200 tonnes, Chemetall (ROC:NYSE) in Chile at 22,500 tonnes and FMC Lithium (FMC:NYSE) in Argentina at 16,600 tonnes. With the exception of Talison, all the producers are extracting lithium from brines, and most of that brine production is economic at these scales due to production of potash, not lithium. While each of the major producers is likely able to ramp their production, pumping brine from an aquifer at higher rates always runs the risk of diluting, depleting or otherwise damaging the brine. We believe many of the larger producers will be reluctant to pump brine at rates higher than called for by increasing potash demand, due to this risk.

All the above suggests that there will be room in the market for new entrants, but with growth limited over the next fi ve years, the prime candidates to enter the market are those that can do so quickly and inexpensively, both from

1

LITH

IUM

a capital and variable cost point-of-view. Our estimates for cost of various types of production are:

Exhibit 1: Estimated Costs ex-Labor, Lithium Production from Various Sources

Type Brine (Mg:Li of 1:1)

Spodumene Clay

Variable Cost (tonne LCE)

$1,200 $3,120 $2,262

Fully-amortized Cost (tonne LCE)

$2,267 $6,453 $3,262

Source: Byron Capital Markets

We suggest investors concentrate on brine- and clay-based juniors, especially those working in regions with known chemistry and geology.

Lithium: The Next Strategic MaterialLithium, chemical symbol Li, is the lightest of all metals. While not rare, with a concentration in the Earth’s crust roughly that of nickel or lead, its high chemical reactivity causes a problem. While the chemical reactivity of lithium is what makes it attractive to battery manufacturers, as it allows more energy to be stored in a given battery, that same reactivity means that Li reacted to form soluble salts that then spread out in a diffuse layer around the Earth. Thus, the problem is one of fi nding economically viable concentrations of lithium.

As with all basic materials, no one would care about Li without it having a wide variety of applications, and it does. According to the US Geological Survey, a quarter of all Li produced worldwide is used in batteries, both high-power non-rechargeable cells as well as the ubiquitous rechargeable batteries used in cellular phones and laptop computers. Another 18% is used to produce ceramics and glass, 12% goes into production of lithium-based greases, 7% gets used in pharmaceutical compounds, 6% in the air conditioning industry (lithium bromide is a common dessicant, used to reduce humidity of processed air) and 5% to help produce aluminum. A wide variety of other applications consume the remaining 27%.

Most of these industrial uses, surprisingly, are not likely to be impacted by substitutes, even if the price of Li were to multiply. For example, in glass manufacturing, lithium oxide (Li

2O) is added to glass at rates of only 0.10%-

0.17% by weight, and the result is a dramatic reduction in the melting point, viscosity and thermal expansion of a silicon-based glass (all according to information in Ceramic Industry magazine, May 2004). This means that a manufacturer will use perhaps 5-10% less energy, reduce effective emissions including NO

x, and increase capacity.

Admittedly, other chemicals such as sodium and potassium can be used instead of Li, but only at much higher current

cost. Batteries based on chemicals other than lithium can be made, obviously, but do not have the same properties. Perhaps surprising to most, raw lithium makes up only about 1% of the bill of materials for a rechargeable lithium-ion battery. Lubricants based on calcium and aluminum can substitute for lithium, again at higher prices based on current costs. Even if the price of lithium increased substantially, substitution is likely limited, as the content in most applications is either very specifi c to lithium (such as pharmaceuticals or air conditioning) or the fraction of cost from lithium is small enough to simply pass along to the end user. We suspect no more than 400-700 basis points of substitution are practically available, largely due to the lithium grease industry, and we have included appropriate levels of substitution in our demand forecasts.

Lithium Sources – Brine or Spodumene or ClayThere are two major sources for lithium today, brines and minerals, and we believe that the future may bring a strong competitor to hard rock-based suppliers: lithium produced from hectorite clays. Still, in all cases, we believe it is important to understand the potential costs for each of the methods of supply.

Brine – Mother Nature Does the Work

Lithium in brine is in the form of dissolved salts. Typically, the lithium is in concentrations ranging from 200 to as much as 1,500 parts per million, initially. The basic approach is to concentrate the lithium even more by putting brine into evaporation ponds. If lithium were the only salt in the brine, the process would be simple, however, the major problem is that lithium salt is never alone in brine. It is accompanied by many other contaminants, including other salts such as common sodium chloride or potassium chloride, boron, and sulphate compounds. Both boron and the sulphates can contaminate the fi nal lithium carbonate at low levels, and when the lithium carbonate is fi nally processed to very pure lithium in an electrolysis cell, the boron and sulphates can rapidly short circuit the cell and shut down production. The most problematic contaminant is magnesium, usually resulting from the salt MgCl

2 being

present in the brine. Any level of magnesium in the fi nal lithium carbonate will result in magnesium contaminating the lithium metal produced by electrolysis.

According to US Patent Number 4,261,960 awarded to Boryta of the Foote Mineral Company, the process of removal of these contaminants is relatively straightforward. Brine in Clayton Valley, NV, is pumped up to a 300 ha holding pond to bring the initial 250 ppm brine to 400 ppm. The brine then gets pumped to 70 ha pond, until lithium concentration reaches 800 ppm. The brine then gets pumped to a 25 ha pond, and slaked lime (Ca(OH)

2) is

added en route. MgCl2 reacts with lime to make Mg(OH)

2,

2

LITH

IUM

which is barely soluble in water and settles out in the holding pond. As LiCl concentrations increase to 2,000 ppm, MgCl

2 concentrations drop to 2 ppm as the Mg(OH)

2

is formed and precipitates. At this point, Foote Minerals would add hydrochloric acid (HCl) and then calcium chloride (CaCl

2). The result is that both boron and sulphate

compounds react and precipitate out of solution, primarily as gypsum. The resulting “clean” brine is then pumped to a series of 5 ha ponds until LiCl concentration reaches high levels, perhaps 6,000 ppm. At this point, soda ash (Na

2CO

3) is added and the LiCl reacts to form lithium

carbonate, Li2CO

3. Obviously, extraction effi ciency cannot

be 100%, and testing has shown extraction effi ciency of lithium of roughly 50% is reasonable.

The most common salts in brine, sodium and potassium chloride have relatively low solubility, 359 g and 342 g per liter of water at 20 ºC, respectively. Thus, as the brine becomes more concentrated, both sodium and potassium crystallize out of solution. Once carbonates are added, the sodium and potassium are not generally problematic, as both sodium and potassium carbonate have high levels of solubility; 215 g and 1,110 g per liter of water at 20°C, respectively.

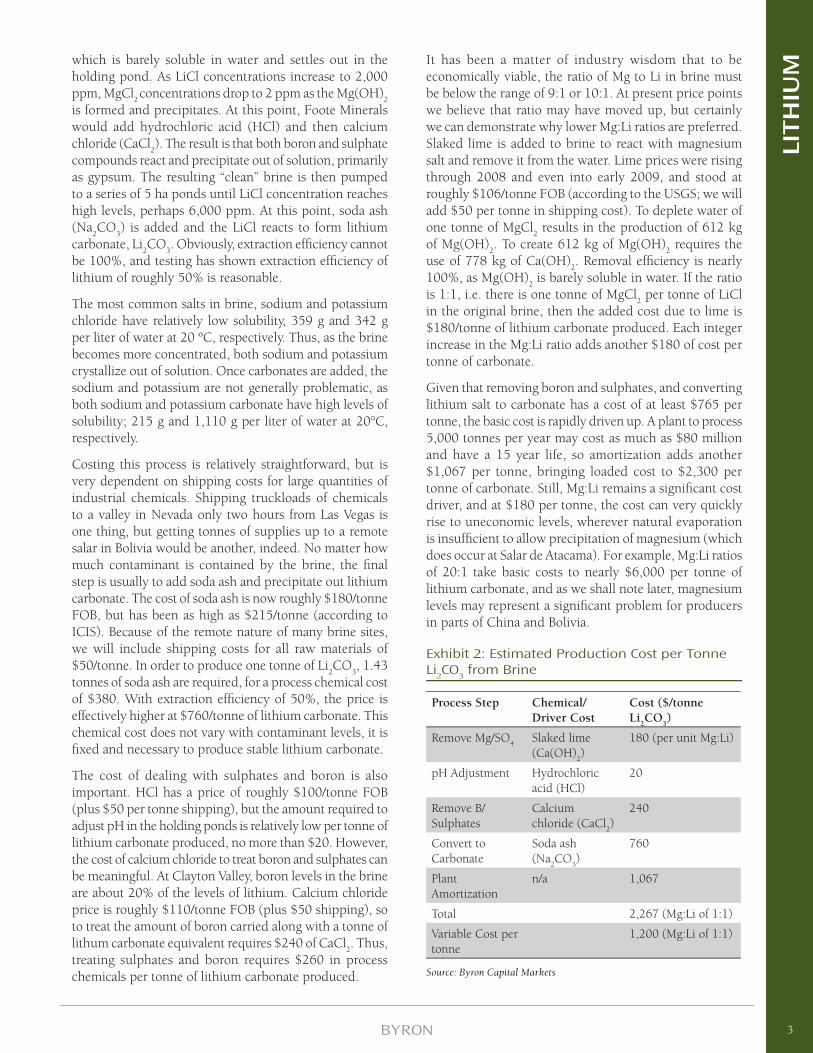

Costing this process is relatively straightforward, but is very dependent on shipping costs for large quantities of industrial chemicals. Shipping truckloads of chemicals to a valley in Nevada only two hours from Las Vegas is one thing, but getting tonnes of supplies up to a remote salar in Bolivia would be another, indeed. No matter how much contaminant is contained by the brine, the fi nal step is usually to add soda ash and precipitate out lithium carbonate. The cost of soda ash is now roughly $180/tonne FOB, but has been as high as $215/tonne (according to ICIS). Because of the remote nature of many brine sites, we will include shipping costs for all raw materials of $50/tonne. In order to produce one tonne of Li

2CO

3, 1.43

tonnes of soda ash are required, for a process chemical cost of $380. With extraction effi ciency of 50%, the price is effectively higher at $760/tonne of lithium carbonate. This chemical cost does not vary with contaminant levels, it is fi xed and necessary to produce stable lithium carbonate.

The cost of dealing with sulphates and boron is also important. HCl has a price of roughly $100/tonne FOB (plus $50 per tonne shipping), but the amount required to adjust pH in the holding ponds is relatively low per tonne of lithium carbonate produced, no more than $20. However, the cost of calcium chloride to treat boron and sulphates can be meaningful. At Clayton Valley, boron levels in the brine are about 20% of the levels of lithium. Calcium chloride price is roughly $110/tonne FOB (plus $50 shipping), so to treat the amount of boron carried along with a tonne of lithum carbonate equivalent requires $240 of CaCl

2. Thus,

treating sulphates and boron requires $260 in process chemicals per tonne of lithium carbonate produced.

It has been a matter of industry wisdom that to be economically viable, the ratio of Mg to Li in brine must be below the range of 9:1 or 10:1. At present price points we believe that ratio may have moved up, but certainly we can demonstrate why lower Mg:Li ratios are preferred. Slaked lime is added to brine to react with magnesium salt and remove it from the water. Lime prices were rising through 2008 and even into early 2009, and stood at roughly $106/tonne FOB (according to the USGS; we will add $50 per tonne in shipping cost). To deplete water of one tonne of MgCl

2 results in the production of 612 kg

of Mg(OH)2. To create 612 kg of Mg(OH)

2 requires the

use of 778 kg of Ca(OH)2. Removal effi ciency is nearly

100%, as Mg(OH)2 is barely soluble in water. If the ratio

is 1:1, i.e. there is one tonne of MgCl2 per tonne of LiCl

in the original brine, then the added cost due to lime is $180/tonne of lithium carbonate produced. Each integer increase in the Mg:Li ratio adds another $180 of cost per tonne of carbonate.

Given that removing boron and sulphates, and converting lithium salt to carbonate has a cost of at least $765 per tonne, the basic cost is rapidly driven up. A plant to process 5,000 tonnes per year may cost as much as $80 million and have a 15 year life, so amortization adds another $1,067 per tonne, bringing loaded cost to $2,300 per tonne of carbonate. Still, Mg:Li remains a signifi cant cost driver, and at $180 per tonne, the cost can very quickly rise to uneconomic levels, wherever natural evaporation is insuffi cient to allow precipitation of magnesium (which does occur at Salar de Atacama). For example, Mg:Li ratios of 20:1 take basic costs to nearly $6,000 per tonne of lithium carbonate, and as we shall note later, magnesium levels may represent a signifi cant problem for producers in parts of China and Bolivia.

Exhibit 2: Estimated Production Cost per Tonne Li2CO3 from Brine

Process Step Chemical/Driver Cost

Cost ($/tonne Li

2CO

3)

Remove Mg/SO4

Slaked lime (Ca(OH)

2)

180 (per unit Mg:Li)

pH Adjustment Hydrochloric acid (HCl)

20

Remove B/Sulphates

Calcium chloride (CaCl

2)

240

Convert to Carbonate

Soda ash (Na

2CO

3)

760

Plant Amortization

n/a 1,067

Total 2,267 (Mg:Li of 1:1)

Variable Cost per tonne

1,200 (Mg:Li of 1:1)

Source: Byron Capital Markets

3

LITH

IUM

Spodumene – Lithium from Granite

The other major source of Li is mineral. In the past, a pegmatic mineral known as spodumene was the major source of Li. Pegmatite is basically coarse-grained granite, an igneous rock with grain sizes of 10 mm or larger. Spodumene is actually lithium aluminum silicate, LiAl(SiO

3)

2. Producers from this type of hard-rock mining

have to contend with lithium concentrations of only 1-2% in this type of deposit (with a theoretical maximum of 8%).

Again, however, the problem and costs come from separating the lithium from everything else in the minerals. Basically, a spodumene concentrate is heated to 1,100°C and then pulverized. The heat is necessary to make the crystalline spodumene amenable to reacting with sulphuric acid, which is now added and heated to 250°C to produce lithium sulphate, which falls out of solution in the acid. The Li

2SO

4 is soluble in water, however, at a level of 348

g per liter of water at 20°C. This allows dissolved Li2SO

4

to react with carbonates and produce Li2CO

3 that will

then fall out of solution to be dried and sold. Obviously, this is a more energy intensive and expensive process than producing lithium from brine, but at the right prices for lithium, it can remain an economically viable process. It should be noted that spodumene-based lithium has historically not been processed to remove contaminants such as boron or sulphates, which are problematic when attempting to produce the highly purifi ed lithium used in batteries. Again, we do not imply that this purifi cation cannot be done, only that it will again increase costs.

And the cost of spodumene-based lithium is, indeed, high. The concentration of spodumene is usually no higher than 1-2% in lithium. In order to create one tonne of lithium carbonate, we require 189 kg of lithium metal. At 2% concentration, a high value for any spodumene deposit, we need to remove 9.4 tonnes of ore. However, this also assumes the processing of spodumene is 100% effi cient at recovery of lithium, and it is not; heap leaching is generally no more than 35% effi cient, so the volume of ore required to make one tonne of lithium carbonate is now 27 tonnes. Moon et al in “Introduction to Mineral Exploration” set broad parameters on the cost of hard rock underground mining, but generally these costs will be from $23-45 per tonne. Therefore, the initial cost of getting ore out of the ground is between $600 and $1,200 per tonne of lithium carbonate.

The spodumene extracted from the ore body must then be concentrated by a factor of between three and six. As per description by Banks et al in the February, 1953 issue of Mining Engineering (mining of spodumene is by no means a new science), the cost of such a separation is roughly $500 per tonne of lithium carbonate.

At this point, the volume of mineral to be treated has been reduced to perhaps nine tonnes. The next step in the process is to heat the mineral to roughly 1,200 °C. This requires a large amount of energy. The specifi c heat of this material will be roughly between granite and mica, quoted as 0.5 kJ/kg K and 0.79 kJ/kg K, respectively. Given we want to heat the material from 20 °C to 1,200 °C, and we have 9,000 kg, the energy required is of order 7.02 GJ. Heating is never 100% effi cient, rough 50% effi ciency would be considered good results, so we need 14 GJ. This requires the lower heating value of 2.3 barrels of oil, perhaps $230 worth of heat per tonne of lithium carbonate.

Pulverizing of the heat-treated material is necessary, to allow reasonable access for chemicals as they extract lithium from the ore. Cost of pulverizing rock is not high per tonne, and we are only dealing with nine tonnes of concentrate at this point, but we can infer from various sources that pulverizing will cost $100 per tonne of lithium carbonate.

Finally we require process chemicals, specifi cally sulphuric acid. Sulphuric acid had been selling for as much as $400 per US ton in the middle of 2008, but prices have retreated to a more reasonable $250 per tonne. To react with 189 kg of lithium metal and produce lithium sulphate, we need at least 1.3 tonnes of sulphuric acid. At the high price, which we regard as being a longer-term level, this is worth $585 per tonne of lithium carbonate produced, including shipping.

There is now a washing step, to put the lithium sulphate produced earlier into solution. We will assign no cost to this stage of the process. Finally, the lithium sulphate must be reacted with soda ash, producing relatively insoluble lithium carbonate. Here the cost of the soda ash, as determined for brines, above, is $505 per tonne of lithium carbonate.

The total variable cost to produce a tonne of lithium carbonate through hard rock mining of spodumene is between $2,500 and $3,100 per tonne of lithium carbonate, explaining why spodumene producers became especially aggressive in late 2000 when lithium carbonate prices topped $4,000 per tonne, and why the same spodumene producers disappeared from the market when pressure from SQM dropped the price to an average $1,400 per tonne in 2001.

Note that the amortization of capital cost on the mine also needs to be included, in order to reach a fi nal cost. The capital cost of the mine and plant for a 10,000 tonne per year annual producer is above $500 million. Based on 15 year life (lower than might be expected owing to the caustic nature of the solutions required during processing), this equates to an additional $3,333 per tonne

4

LITH

IUM

of lithium carbonate. Final cost of the lithium carbonate from spodumene is thus likely now in the range $5,800 to $6,400 per tonne.

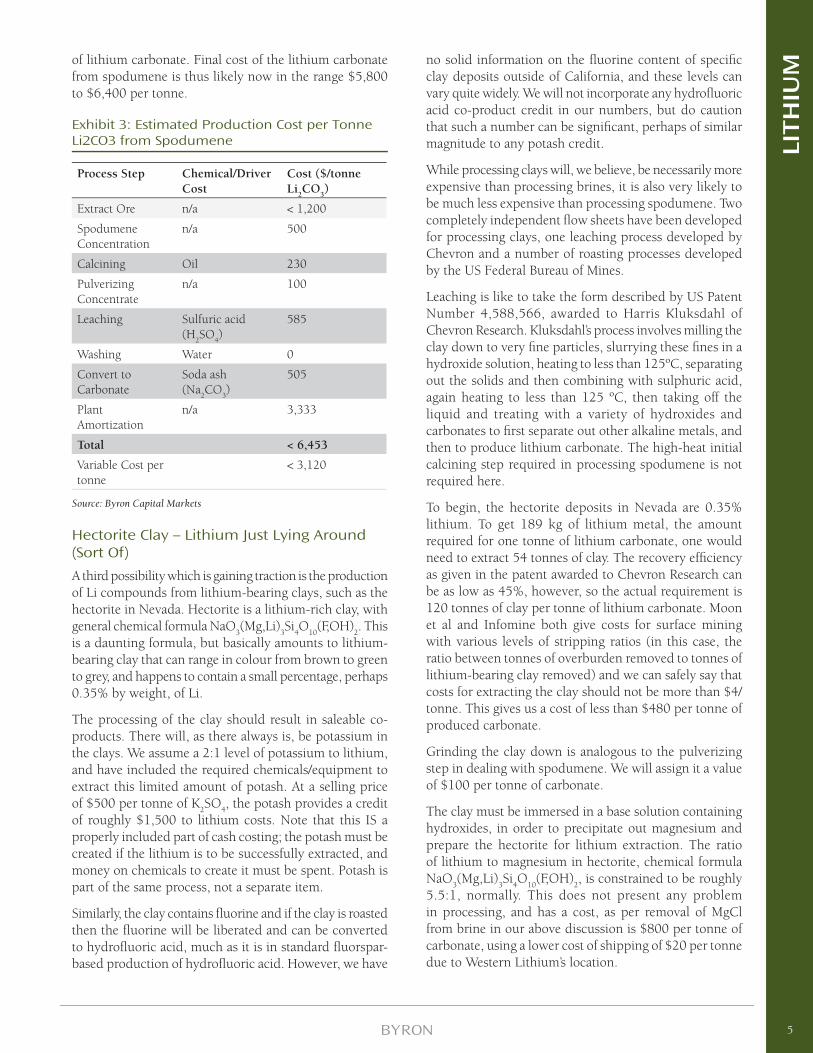

Exhibit 3: Estimated Production Cost per Tonne Li2CO3 from Spodumene

Process Step Chemical/Driver Cost

Cost ($/tonne Li

2CO

3)

Extract Ore n/a < 1,200

Spodumene Concentration

n/a 500

Calcining Oil 230

Pulverizing Concentrate

n/a 100

Leaching Sulfuric acid (H

2SO

4)

585

Washing Water 0

Convert to Carbonate

Soda ash (Na

2CO

3)

505

Plant Amortization

n/a 3,333

Total < 6,453

Variable Cost per tonne

< 3,120

Source: Byron Capital Markets

Hectorite Clay – Lithium Just Lying Around (Sort Of)

A third possibility which is gaining traction is the production of Li compounds from lithium-bearing clays, such as the hectorite in Nevada. Hectorite is a lithium-rich clay, with general chemical formula NaO

3(Mg,Li)

3Si

4O

10(F,OH)

2. This

is a daunting formula, but basically amounts to lithium-bearing clay that can range in colour from brown to green to grey, and happens to contain a small percentage, perhaps 0.35% by weight, of Li.

The processing of the clay should result in saleable co-products. There will, as there always is, be potassium in the clays. We assume a 2:1 level of potassium to lithium, and have included the required chemicals/equipment to extract this limited amount of potash. At a selling price of $500 per tonne of K

2SO

4, the potash provides a credit

of roughly $1,500 to lithium costs. Note that this IS a properly included part of cash costing; the potash must be created if the lithium is to be successfully extracted, and money on chemicals to create it must be spent. Potash is part of the same process, not a separate item.

Similarly, the clay contains fl uorine and if the clay is roasted then the fl uorine will be liberated and can be converted to hydrofl uoric acid, much as it is in standard fl uorspar-based production of hydrofl uoric acid. However, we have

no solid information on the fl uorine content of specifi c clay deposits outside of California, and these levels can vary quite widely. We will not incorporate any hydrofl uoric acid co-product credit in our numbers, but do caution that such a number can be signifi cant, perhaps of similar magnitude to any potash credit.

While processing clays will, we believe, be necessarily more expensive than processing brines, it is also very likely to be much less expensive than processing spodumene. Two completely independent fl ow sheets have been developed for processing clays, one leaching process developed by Chevron and a number of roasting processes developed by the US Federal Bureau of Mines.

Leaching is like to take the form described by US Patent Number 4,588,566, awarded to Harris Kluksdahl of Chevron Research. Kluksdahl’s process involves milling the clay down to very fi ne particles, slurrying these fi nes in a hydroxide solution, heating to less than 125ºC, separating out the solids and then combining with sulphuric acid, again heating to less than 125 ºC, then taking off the liquid and treating with a variety of hydroxides and carbonates to fi rst separate out other alkaline metals, and then to produce lithium carbonate. The high-heat initial calcining step required in processing spodumene is not required here.

To begin, the hectorite deposits in Nevada are 0.35% lithium. To get 189 kg of lithium metal, the amount required for one tonne of lithium carbonate, one would need to extract 54 tonnes of clay. The recovery effi ciency as given in the patent awarded to Chevron Research can be as low as 45%, however, so the actual requirement is 120 tonnes of clay per tonne of lithium carbonate. Moon et al and Infomine both give costs for surface mining with various levels of stripping ratios (in this case, the ratio between tonnes of overburden removed to tonnes of lithium-bearing clay removed) and we can safely say that costs for extracting the clay should not be more than $4/tonne. This gives us a cost of less than $480 per tonne of produced carbonate.

Grinding the clay down is analogous to the pulverizing step in dealing with spodumene. We will assign it a value of $100 per tonne of carbonate.

The clay must be immersed in a base solution containing hydroxides, in order to precipitate out magnesium and prepare the hectorite for lithium extraction. The ratio of lithium to magnesium in hectorite, chemical formula NaO

3(Mg,Li)

3Si

4O

10(F,OH)

2, is constrained to be roughly

5.5:1, normally. This does not present any problem in processing, and has a cost, as per removal of MgCl from brine in our above discussion is $800 per tonne of carbonate, using a lower cost of shipping of $20 per tonne due to Western Lithium’s location.

5

LITH

IUM

We also add in the cost of sulfuric acid, to convert the lithium in the clay to lithium sulfate. As per the above discussion regarding spodumene, the cost of sulfuric acid to properly convert 189 kg of lithium metal to sulfate is $546 per tonne of carbonate, but again using a lower shipping cost.

Finally, soda ash is required to convert the lithium sulfate to lithium carbonate. The fi nal tally here, as per brines and spodumene both but incorporating the lower shipping cost, is $336 per tonne of carbonate.

Hence, the total tally for variable costs is roughly $1,800 per tonne of lithium carbonate. In the specifi c case of hectorite clays in Nevada, we are likely overestimating costs as we are using shipping rates for the bulk chemicals that are more suited to remote locations than sites in the United States.

When the amortized cost of a plant is added to the mix, the situation actually tips more heavily in favor of clays as opposed to spodumene ores. A clay plant does not involve underground mining, it utilizes open pit operations and a vat leaching plant, a much simpler operation than that required for spodumene. Our estimate is that a 20,000 tonne per year carbonate plant based on hectorite clays would cost less than $300 million, and have the same 15 year life of a spodumene facility. Amortization adds $1,000 per tonne to carbonate costs, taking the total to approximately $2,800 per tonne, albeit with higher shipping costs than are likely warranted in the specifi c case of hectorite clays in Nevada.

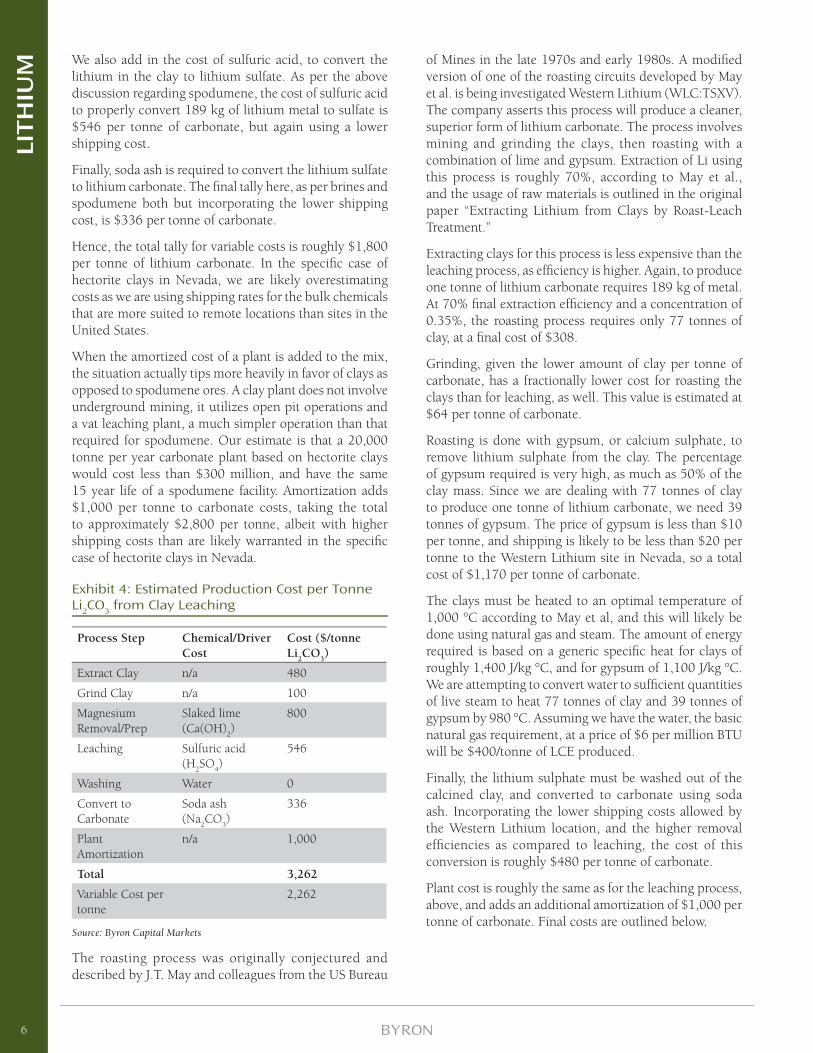

Exhibit 4: Estimated Production Cost per Tonne Li2CO3 from Clay Leaching

Process Step Chemical/Driver Cost

Cost ($/tonne Li

2CO

3)

Extract Clay n/a 480

Grind Clay n/a 100

Magnesium Removal/Prep

Slaked lime (Ca(OH)

2)

800

Leaching Sulfuric acid (H

2SO

4)

546

Washing Water 0

Convert to Carbonate

Soda ash (Na

2CO

3)

336

Plant Amortization

n/a 1,000

Total 3,262

Variable Cost per tonne

2,262

Source: Byron Capital Markets

The roasting process was originally conjectured and described by J.T. May and colleagues from the US Bureau

of Mines in the late 1970s and early 1980s. A modifi ed version of one of the roasting circuits developed by May et al. is being investigated Western Lithium (WLC:TSXV). The company asserts this process will produce a cleaner, superior form of lithium carbonate. The process involves mining and grinding the clays, then roasting with a combination of lime and gypsum. Extraction of Li using this process is roughly 70%, according to May et al., and the usage of raw materials is outlined in the original paper “Extracting Lithium from Clays by Roast-Leach Treatment.”

Extracting clays for this process is less expensive than the leaching process, as effi ciency is higher. Again, to produce one tonne of lithium carbonate requires 189 kg of metal. At 70% fi nal extraction effi ciency and a concentration of 0.35%, the roasting process requires only 77 tonnes of clay, at a fi nal cost of $308.

Grinding, given the lower amount of clay per tonne of carbonate, has a fractionally lower cost for roasting the clays than for leaching, as well. This value is estimated at $64 per tonne of carbonate.

Roasting is done with gypsum, or calcium sulphate, to remove lithium sulphate from the clay. The percentage of gypsum required is very high, as much as 50% of the clay mass. Since we are dealing with 77 tonnes of clay to produce one tonne of lithium carbonate, we need 39 tonnes of gypsum. The price of gypsum is less than $10 per tonne, and shipping is likely to be less than $20 per tonne to the Western Lithium site in Nevada, so a total cost of $1,170 per tonne of carbonate.

The clays must be heated to an optimal temperature of 1,000 °C according to May et al, and this will likely be done using natural gas and steam. The amount of energy required is based on a generic specifi c heat for clays of roughly 1,400 J/kg °C, and for gypsum of 1,100 J/kg °C. We are attempting to convert water to suffi cient quantities of live steam to heat 77 tonnes of clay and 39 tonnes of gypsum by 980 °C. Assuming we have the water, the basic natural gas requirement, at a price of $6 per million BTU will be $400/tonne of LCE produced.

Finally, the lithium sulphate must be washed out of the calcined clay, and converted to carbonate using soda ash. Incorporating the lower shipping costs allowed by the Western Lithium location, and the higher removal effi ciencies as compared to leaching, the cost of this conversion is roughly $480 per tonne of carbonate.

Plant cost is roughly the same as for the leaching process, above, and adds an additional amortization of $1,000 per tonne of carbonate. Final costs are outlined below.

6

LITH

IUM

Exhibit 5: Estimated Production Cost per Tonne Li2CO3 from Clay Roasting

Process Step Chemical/Driver Cost

Cost ($/tonne Li

2CO

3)

Extract Clay n/a 308

Grind Clay n/a 64

Heat for Roasting Steam to 1,000 °C 400

Gypsum Calcium sulphate (CaSO

4)

1,170

Wash Water 0

Convert to Carbonate

Soda ash (Na

2CO

3)

480

Plant Amortization

n/a 1,000

Total 3,422

Variable Cost per tonne

2,422

Source: Byron Capital Markets

The product produced from roasting may be superior to the product produced from leaching. Western Lithium management has asserted that their roasting process improves contaminate levels remaining in the carbonate signifi cantly, making the fi nal electrolytic refi ning step by a battery maker far less expensive. The cost of electrolytic refi ning of most high purity metals, according to Jerry Woodall of Purdue University in a presentation given in September 2008, is about $660/tonne of material. This may, although we are not in a position at present to judge, result in lithium produced from hectorite clays being economically superior to those from brines for battery use.

Current Lithium Pricing and Future SubstitutionWe also note that an increase in lithium carbonate cost is not likely to be catastrophic for any industry relying on lithium. As reported by Evans from the January 2009 Santiago conference on lithium, a benchmark figure recognized in the industry is that 600 grams of LCE is used per kWh of battery storage required (probably slightly low, given the current state of design). Costs for lithium carbonate have been as high as US$6,600 per tonne, so a 1 kWh battery would use roughly $4 of lithium carbonate equivalent. The cost of a 1 kWh battery pack will be no lower than $400, based solely on the cost of the standard 18650 cells used to build it, and excluding any manufacturing costs for the battery module. Clearly, doubling the cost of the lithium required for the battery will have little impact on demand, but not having enough lithium to construct the battery certainly would be disastrous.

Similarly, use of lithium in its oxide form in the glass industry amounts to only 0.03-0.20% by weight, according to articles in Ceramic Industry Magazine (Christine Grahl, May 2004). While offering a signifi cant reduction in energy demand during glass manufacturing, the dollar cost of glass is barely impacted by the cost of lithium. Again, price increases in lithium are unlikely to result in any sort of substitution.

We also note that a trend in the battery industry is a willingness to use more Li in a battery, in order to meet performance specifi cations. This is easily understood, economically; adding $2 of lithium to a battery that can then sell for an additional $5 because of its superior performance is justifi ed.

In short, we believe that potential substitutions to alleviate lithium consumption due to higher lithium prices are unlikely to amount to more than 300-500 basis points of use, and will only occur if Li prices were to increase by factors of three or more. As we do not see this sort of price increase as likely over our fi ve year window, we do not include substitutions in our model.

Lithium Batteries: High Voltage = High Energy and High PowerThe reason Li is so desirable in terms of use in batteries is precisely what makes it available only in low concentrations, its chemical reactivity. Li is a convenient metal that is able to carry large amounts of energy and power in a small and lightweight package. Batteries are built and arranged in individual cells, with the power available from each cell being roughly dependent on the area available for ion exchange across the batteries electrolyte, and the energy it carries dependent more on its volume and its chemistry. Each battery chemistry has different cell voltages, and power is actually directly related to voltage through the equation P = V2/R, where V is battery voltage, R is electrical resistance of the attached load, and P is power. A high voltage from a cell will generally result in higher power being available from the battery, all other things being equal. The cell voltage of a lithium battery is 3.7 V, while the cell voltage of a nickel metal hydride battery is only 1.2 V. Normally, cells are wired together to build fi nal battery packs, but the fewer cells that must be connected, the simpler, cheaper and less failure-prone the fi nal battery will be. The 12 V lead-acid car battery, for example, is typically made up of six lead-acid cells, each one at 2.0 V.

So batteries based on Li chemistry can produce more power and carry more energy than batteries based on other more common materials. For example, typically quoted energy densities for a Li-ion rechargeable battery would be roughly 150 Watt-hours per kilogram of battery mass (abbreviated as Wh/kg; a 100 Wh lithium battery would mass 0.7 kg, and be capable of powering a 100 Watt light

7

LITH

IUM

bulb for one hour, which would be a terrible way to use such a battery, but it can be done). Typical energy density for a nickel metal-hydride (NiMH) rechargeable battery would be roughly 100 Wh/kg, due largely to the heavier mass of the raw materials in a NiMH battery. Li-ion also wins on the basis of energy per volume; Li-ion has energy density of over 300 Wh/l, while NiMH comes in at roughly the same level, perhaps 280 Wh/l. But one must be willing to move a much heavier NiMH battery around, and to settle for the lower peak power that a NiMH battery can generate compared to Li-ion.

Exhibit 6: Tesla Roadster: 52 kWh Battery, $120,000 Price Tag

Source: Tesla Motors

In general, a battery is sized by selecting the smallest cell that can generate the required peak power for the application, and then adding cells to provide the desired run time. In any case that matters, except where power requirements are very small and run time must be very long, Li-ion will beat NiMH. Even in a low-power/long-run-time application, the fact that Li-ion has much lower self-discharge (the undesirable passive loss of energy that can mean a charged battery discharges just by sitting on a shelf) than NiMH may make Li-ion the correct choice. Peak power output from a Li-ion battery can be as high as 2,500 W/kg or 5,300 W/l, according to SAFT, while similar fi gures from NiMH cells do not exceed 1,500 W/kg or 4,500 W/l.

For investors worried about whether a new battery technology will emerge in the next few years to supplant lithium-ion, we can provide a rationale for why this worry is misplaced. There are only so many elements in the periodic table, and so many ways to chemically construct a battery. We already have rechargeable batteries based on NiMH, alkaline and lead-acid chemistries. Li-ion has made all of these other chemistries niche players due to a combination of performance and decreasing cost.

In the automotive space, for example, no one has seriously recommended lead-acid batteries as a feasible technology for use in either hybrid or full-electric vehicles for some

time, although there is a great deal of ongoing research on new variants of lead-acid batteries that are lighter, more powerful, more energetic, etc. While both the current Toyota Prius and Honda Insight are equipped with NiMH battery packs, both Toyota and Honda are investigating the use of Li-ion and Toyota appears ready to move to Li-ion in the Prius for the 2011 model year. Both the Tesla Roadster fully-electric sports car and the upcoming Nissan Leaf and Chevrolet Volt will rely on Li-ion cells (53 kWh, 24 kWh and 16 kWh packs, respectively). There are few indications that any major automotive fi rm is planning on making its long-term battery choice for hybrids and/or electric vehicles anything other than Li-ion.

Exhibit 7: Chevy Volt: 16 kWh Battery Using Roughly 10 kg LCE

Source: General Motors

In terms of novel battery technology, the only current technology that is remotely feasible for automotive use, other than the above-discussed batteries, are known as molten salt batteries. One of the best known versions of this type of cell is called ZEBRA, and is more technically referred to as a sodium-nickel chloride battery. The downside of the ZEBRA is that it operates at 250°C, and must remain molten to be used. The upside is low cost, and (theoretically) very long operating life, but the fact that the battery is fi lled with a molten salt must be taken into account in terms of fi eld reliability (keeping molten salts successfully inside a sealed container for years is easier said than done).

8

LITH

IUM

Exhibit 8: Nissan Leaf: All-Electric, 24 kWh, Announced 21 kg LCE Use

Source: Nissan Motor Co.

Alternative technologies that could become disruptive to the Li-ion battery are likely headed by ultracapacitors. Ultracapacitors are devices that store energy, for lack of a better description, by cramming charge into a device and storing energy in the electric fi eld developed within the device. We should note that ultracaps are probably best thought of as a complementary technology to batteries, because of their extremely low internal resistance. Ultracapacitors can discharge and charge very rapidly, and this allows them to store or produce very large amounts of power; for example, a Maxwell BMOD0094-75V module can produce a maximum power of more than 4,500 Watts, but it only stores 55 Wh of energy (recall a Tesla Roadster’s battery pack stores 53,000 Wh of energy). The Maxwell module could output at its peak rate for only 44 seconds, but this is not to be considered a defi ciency compared to chemical batteries, just a natural difference between the two. The biggest advantage to an ultracapacitor is a very long operating life, perhaps decades in actual operation.

A company making an effort to bridge the gap between ultracapacitors and batteries is eeStor, a secretive fi rm that has made few statements about its technology. However, what the company has stated is that it is working toward modules storing energy of 52 kWh, at a price point well below batteries (less than US$3,000). If this came to pass, aside from the fact that batteries maintain their operating voltage while an ultracapacitor has its voltage drop linearly with energy withdrawn and thus requires DC-DC converters to maintain a reasonably constant voltage output, then batteries would likely be supplanted as quickly as the new ultracapacitors can be produced. We choose to remain sceptical, until solid evidence of performance is made public. We remain wary of factors such as microcracks in the layers of material used in the conjectured devices, of current leakage due to the very high conjectured operating voltages, and a phenomenon known as dielectric saturation, that results in most ultracapacitors being unable to ramp their energy storage linearly with increasing operating voltage.

Supply The fi rst issue is just what sort of supply level we have currently. Lithium is supplied in many different chemical forms, but due to its extreme chemical reactivity it is not shipped as metal. In order to uniformly discuss production, as readers have probably noted we are using units of tonnes of lithium carbonate equivalent, LCE. If one wished to express lithium production or demand in tonnes of metal, for example, then because the molecular mass of lithium carbonate (Li

2CO

3) is 73.9 g/mol, and Li

has a molecular mass of 6.9 g/mol, then one would divide the tonnes of carbonate by 5.3 to arrive at tonnes of metal (and we use 5.3 and not 10.6 as there are two Li atoms in each lithium carbonate molecule).

The US Geological Survey publishes a commodity summary on lithium, and has done so as recently as this year. In it, the USGS suggests current global production is 128,000 tonnes of lithium carbonate equivalent, with 63,600 tonnes or 50% produced in Chile. The four largest producing nations (Chile, Australia, China and Argentina) account for more than 80% of global supply.

Separately, Roskill has estimated that total global lithium production was 121,000 tonnes of carbonate. The lower estimate is probably due to the timing of problems with Chinese brine projects coming to light, as compared to when the USGS estimates were made. We believe the lower Roskill fi gure is a more reasonable estimate.

Supply will grow with new entrants into the market. However, it should be noted that exploration firms investigating brine can be selling lithium in 2-3 years, while fi rms engaged in spodumene exploration are likely 5-6 years from market, owing to the greater time required to establish a new mine versus drilling for water.

We also note that a pair of heavily quoted reports, “The Trouble with Lithium” and “The Trouble with Lithium 2”, both from Meridian Research, have outlined an argument that suggests lithium will come into very short supply, making any reliance on lithium-ion batteries for electric vehicles impossible. The crux of these arguments is that minerals-based sources of lithium are simply unusable for battery production (the actual quote states “Only [a brine lake or salt pan deposit that contains lithium chloride] is economically and energetically viable for Li-ion batteries”), and that rapid increases in lithium demand due to automotive industry use will simply outstrip supply.

The argument made by Meridian is partly true. Spodumene-based lithium is generally contaminated with boron and sulphates that, while working perfectly well for the manufacture of glass or ceramics, makes the electrolytic purification step necessary for battery manufacture extremely diffi cult and expensive. The extra purifi cation required prior to electrolysis would result in dramatic

9

LITH

IUM

price increases in the fi nal product. Given overall demand today, and the fact that roughly 80% of current lithium is produced from brine while less than 25% goes into batteries suggests this is not going to become a problematic situation anytime soon.

It is also true that massive adoption of lithium batteries would wreak havoc on supply. CSM Worldwide has predicted 2009 light vehicle sales worldwide will drop to 52.7 million vehicles. If ALL of these were Chevrolet Volt-like vehicles, each with a 16 kWh battery pack using lithium-ion chemistry, then the total global lithium demand would jump by 455,000 tonnes. This is almost 4x current demand. If the entire global light vehicle fl eet switched to Toyota Prius-like hybrids, however, then global demand for lithium would jump by only 41,000 tonnes. Although this increase would be diffi cult to meet in the near term, it is tractable by 2015 if the demand curve was understood ahead of time.

Some analysts have suggested that lithium supply can grow without bound, and in theory, we believe this to be true. According to the USGS, the prevalence of lithium in the Earth’s mantle is greater than that of nickel or lead, with both of those metals seeing far greater annual demand (nickel metal production is roughly 1.5 million tonnes per year, with no one claiming imminent shortage). But, again the issue with lithium is the relative scarcity of economically viable concentrations. As with most commodities, if one is willing to pay a premium, then more material becomes available for economic extraction. Given current supply and demand, a recent price level is $6,600 per tonne of lithium carbonate, well above cost for both brine- and spodumene-based producers, and likely more than acceptable to clay-based producers in the future, as well. In the near term, then, we are unlikely to experience actual shortages of lithium.

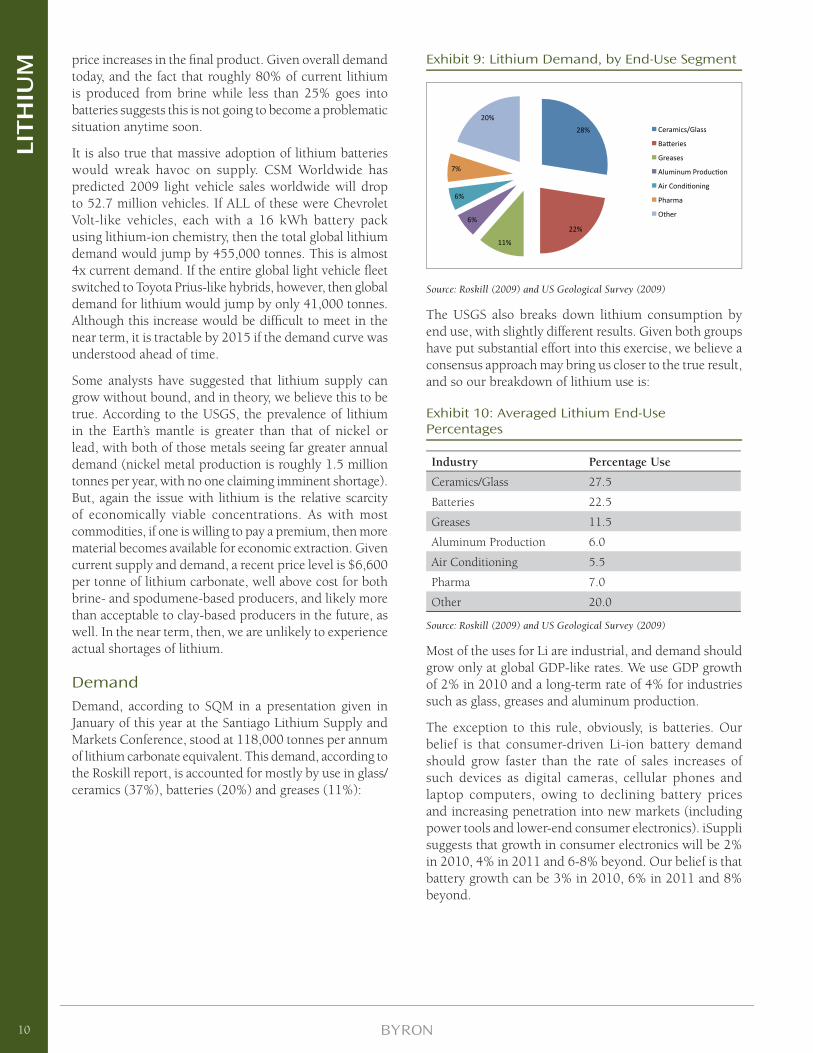

DemandDemand, according to SQM in a presentation given in January of this year at the Santiago Lithium Supply and Markets Conference, stood at 118,000 tonnes per annum of lithium carbonate equivalent. This demand, according to the Roskill report, is accounted for mostly by use in glass/ceramics (37%), batteries (20%) and greases (11%):

Exhibit 9: Lithium Demand, by End-Use Segment

Source: Roskill (2009) and US Geological Survey (2009)

The USGS also breaks down lithium consumption by end use, with slightly different results. Given both groups have put substantial effort into this exercise, we believe a consensus approach may bring us closer to the true result, and so our breakdown of lithium use is:

Exhibit 10: Averaged Lithium End-Use Percentages

Industry Percentage Use

Ceramics/Glass 27.5

Batteries 22.5

Greases 11.5

Aluminum Production 6.0

Air Conditioning 5.5

Pharma 7.0

Other 20.0

Source: Roskill (2009) and US Geological Survey (2009)

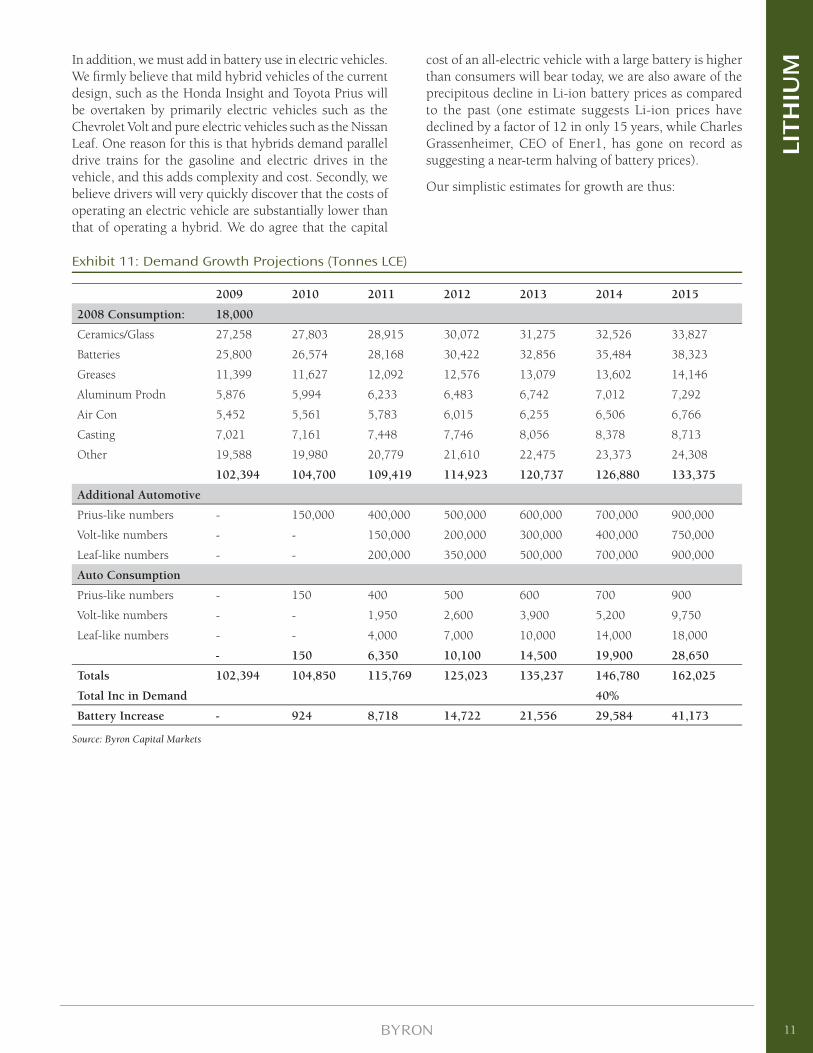

Most of the uses for Li are industrial, and demand should grow only at global GDP-like rates. We use GDP growth of 2% in 2010 and a long-term rate of 4% for industries such as glass, greases and aluminum production.

The exception to this rule, obviously, is batteries. Our belief is that consumer-driven Li-ion battery demand should grow faster than the rate of sales increases of such devices as digital cameras, cellular phones and laptop computers, owing to declining battery prices and increasing penetration into new markets (including power tools and lower-end consumer electronics). iSuppli suggests that growth in consumer electronics will be 2% in 2010, 4% in 2011 and 6-8% beyond. Our belief is that battery growth can be 3% in 2010, 6% in 2011 and 8% beyond.

10

LITH

IUM

Exhibit 11: Demand Growth Projections (Tonnes LCE)

2009 2010 2011 2012 2013 2014 2015

2008 Consumption: 18,000

Ceramics/Glass 27,258 27,803 28,915 30,072 31,275 32,526 33,827

Batteries 25,800 26,574 28,168 30,422 32,856 35,484 38,323

Greases 11,399 11,627 12,092 12,576 13,079 13,602 14,146

Aluminum Prodn 5,876 5,994 6,233 6,483 6,742 7,012 7,292

Air Con 5,452 5,561 5,783 6,015 6,255 6,506 6,766

Casting 7,021 7,161 7,448 7,746 8,056 8,378 8,713

Other 19,588 19,980 20,779 21,610 22,475 23,373 24,308

102,394 104,700 109,419 114,923 120,737 126,880 133,375

Additional Automotive

Prius-like numbers - 150,000 400,000 500,000 600,000 700,000 900,000

Volt-like numbers - - 150,000 200,000 300,000 400,000 750,000

Leaf-like numbers - - 200,000 350,000 500,000 700,000 900,000

Auto Consumption

Prius-like numbers - 150 400 500 600 700 900

Volt-like numbers - - 1,950 2,600 3,900 5,200 9,750

Leaf-like numbers - - 4,000 7,000 10,000 14,000 18,000

- 150 6,350 10,100 14,500 19,900 28,650

Totals 102,394 104,850 115,769 125,023 135,237 146,780 162,025

Total Inc in Demand 40%

Battery Increase - 924 8,718 14,722 21,556 29,584 41,173

Source: Byron Capital Markets

In addition, we must add in battery use in electric vehicles. We fi rmly believe that mild hybrid vehicles of the current design, such as the Honda Insight and Toyota Prius will be overtaken by primarily electric vehicles such as the Chevrolet Volt and pure electric vehicles such as the Nissan Leaf. One reason for this is that hybrids demand parallel drive trains for the gasoline and electric drives in the vehicle, and this adds complexity and cost. Secondly, we believe drivers will very quickly discover that the costs of operating an electric vehicle are substantially lower than that of operating a hybrid. We do agree that the capital

cost of an all-electric vehicle with a large battery is higher than consumers will bear today, we are also aware of the precipitous decline in Li-ion battery prices as compared to the past (one estimate suggests Li-ion prices have declined by a factor of 12 in only 15 years, while Charles Grassenheimer, CEO of Ener1, has gone on record as suggesting a near-term halving of battery prices).

Our simplistic estimates for growth are thus:

11

LITH

IUM

Conclusion – Our Green Thought(s) for the DayWe are now beginning to see the sort of vacillation that has plagued the environmental movement for years be applied to the question of automobiles. As the automotive industry moves toward electric vehicles, some are noting that electric cars may actually be net negative factors for the environment. For example, one argument suggests that since electricity in the United States is at least 50% generated by coal-fi red plants, using electric cars will result in more pollution and greenhouse gas emissions, not less.

We are pleased to be able to refute that concern with some hard data. Recently, Chevrolet touted the effi ciency of the upcoming Volt by widely publicizing a 230 mpg fuel economy rating, the level Chevrolet management believe the new Volt will attain in offi cial testing. But much less widely reported was a more meaningful economy rating; the Volt uses only 25 kWh of energy to travel 100 miles. A very fuel effi cient gasoline-powered car can get 50 mpg on the highway, taking 2 gallons of gasoline to travel 100 miles. Two gallons of gasoline contain roughly 70 kWh of energy. Hence, the primarily electric Volt uses only 36% the energy to travel down the highway as a fuel-effi cient gasoline powered car. This is because the electric car wastes less energy, generated in a gasoline powered car as waste heat from its engine or mechanical losses in the drive train.

The US consumes nine million barrels of motor gasoline per day. This is equivalent to nearly 13 billion kWh of energy per day, simply to drive gasoline powered vehicles around the nation’s roads. If this consumption can be cut to 36% of present levels, the decrease in greenhouse gas emissions would be enormous, regardless of whether the necessary electrical energy comes from burning coal, the fi ssion of uranium, or sunlight falling on solar cells.

Of course, nothing is perfect. While electrical energy consumption to drive a converted US small vehicle fl eet might drop from 13 billion kWh per day to only 5 billion kWh, the entire US generating grid delivered only 11 billion kWh in 2008. Clearly, adding 50% to the generating burden of the United States is a massive undertaking. The problem is actually worse, because if most of those electric vehicles must be recharged overnight, then all those kilowatt hours of energy must be delivered in 12 hours, and we are left, again, with a required doubling of US generating capacity.

Even a reasonably small fraction of the US transportation fl eet converting to electricity would necessitate the use of some sort of technology to prevent blackouts owing to sudden increases in demand from electric vehicle charging,

a “smart grid” of sorts. This, too, would be expensive, but perhaps it holds out the greatest hope of all.

Unreliable forms of power generation, such as wind or solar photovoltaic or solar thermal, can only penetrate into the grid at high rates when some sort of buffer is available. Electric cars can provide that buffer, but not as a form of mass storage. Of nearly equivalent value to a power utility as a storage buffer is a readily variable load. And a smart grid that knows when electric cars are plugged in and can commence charging them or stop charging them at will would allow the demand on the grid to adjust to unreliable (the industry term is “non-dispatchable”) generating technology, such as wind. Wind and solar could then become signifi cant fractions of grid generating capacity.

Now, in the end we do believe that new nuclear generating stations are ultimately required to wean us off fossil fuels and drastically curtail greenhouse gas emissions, but wind makes an interesting stop-gap. Electric vehicles may well turn out to be just what the environment ordered, and electric vehicles are dependent on the lightest metal in the periodic table, lithium.

In order to reap the rewards of increasing lithium demand, we would suggest to investors that they are best served by owning junior exploration companies, the fi rms most heavily levered to increasing lithium demand. We would further suggest owning a basket of these equities, as the exploration and fi nancial risk in any one name is high. We also strongly suggest owning the likely lowest-cost producers, since this protects against fl uctuations in the price of lithium most effectively. We prefer companies basing their exploration on brine, especially brine in known regions where chemistry and hydrogeology are more likely to yield economically viable discoveries.

We are also attracted to those companies exploring the potential of hectorite clays. Since brine producers are limited in terms of having to wait for evaporation to take place, they are largely unable to respond to surges in price or demand. Spodumene-based producers could, but we are concerned about their high operating costs. So we would also suggest that investors reserve part of their portfolio for fi rms researching lithium from clays, such as the deposits of hectorite in Nevada.

It seems to us that there will be no shortage of demand for Li-ion batteries in the future. While we cannot at present predict what particular permutation of chemistry will win the day, or what battery company may be the largest benefi ciary of this demand, we can confi dently predict that there will be more demand for lithium. We can equally confi dently say that those owning shares in strong lithium exploration companies stand to be rewarded.

12

LITH

IUM

Disclosures

Information contained in this Industry report has been drawn from sources believed to be reliable but its accuracy or completeness is not guaranteed, nor in providing it does Byron Capital Markets (a division of Byron Securities Limited) assume any responsibility or liability. From time to time, Byron Capital Markets and its directors, offi cers and other employees may maintain positions in the securities that are directly or indirectly involved in this Industry. The contents of this report cannot be reproduced in whole or in part without the expressed permission of Byron Capital Markets. This information is intended for use by accredited investors only, and is not intended for use by any U.S. investor.

Byron Capital Markets Policies and Procedures Regarding the Dissemination of Research

General policy is to make available a research report to its clients for an exclusive period of up to 30 days. Following that period, the research report will appear on the Byron Capital Markets website at www.byroncapitalmarkets.com.

Analyst Certifi cation

I, Jon Hykawy, certify the views expressed in this report were formed by my review of relevant company data and industry investigation, and accurately refl ect my opinion about the investment merits of the securities mentioned in the report. I also certify that my compensation is not related to specifi c recommendations or views expressed in this report.

Byron Capital Markets publishes research and investment recommendations for the use of its clients. Information regarding our categories of recommendations, quarterly summaries of the percentage of our recommendations that fall into each category and our policies regarding the release of our research reports is available at www.byroncapitalmarkets.com, or may be requested by contacting the analyst.

13

LITH

IUM

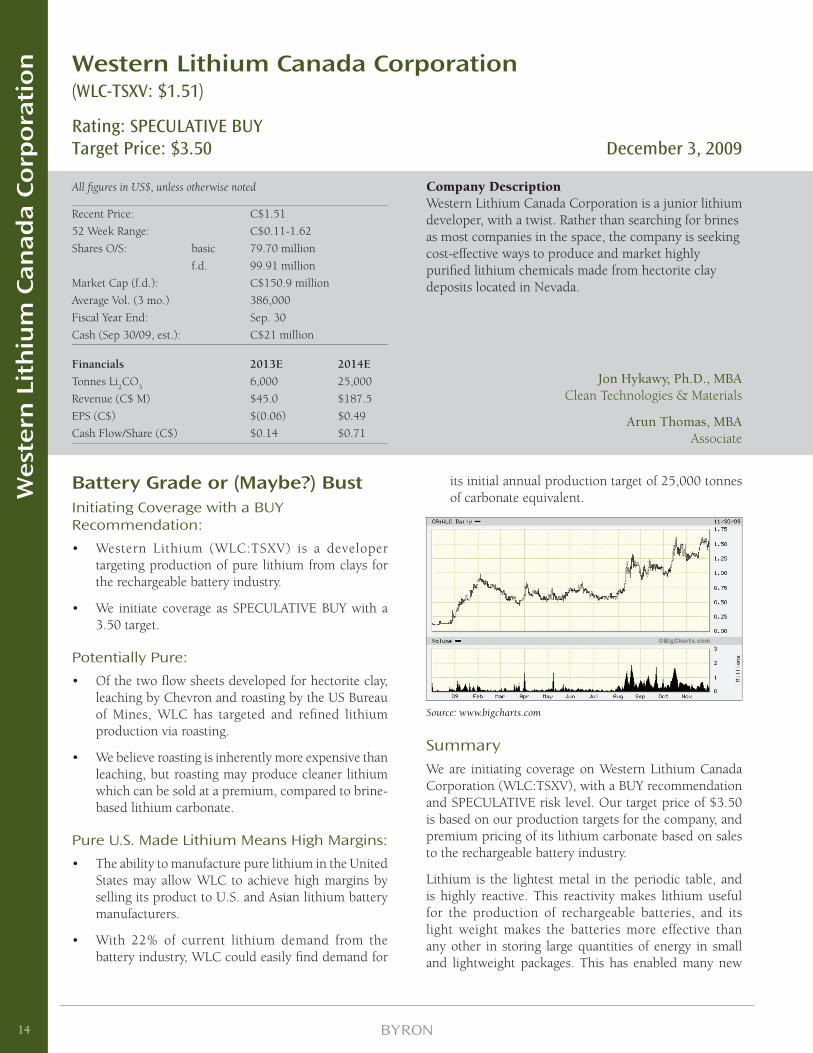

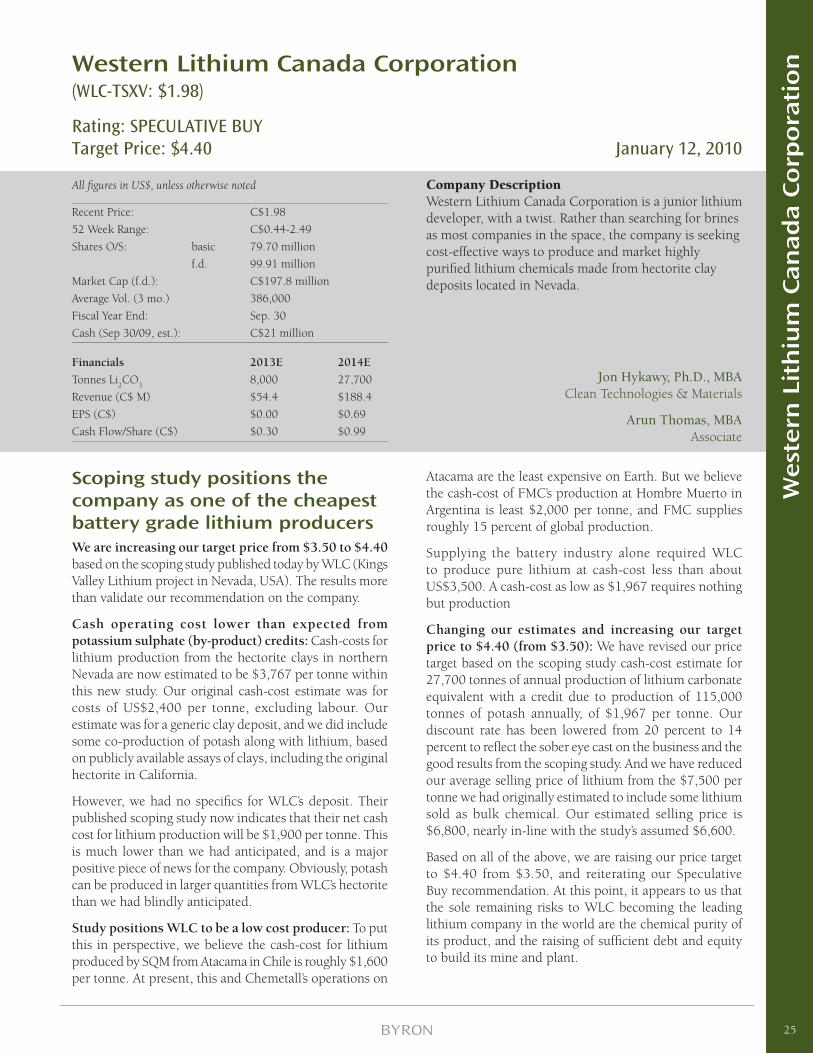

Western Lithium Canada Corporation(WLC-TSXV: $1.51)

Rating: SPECULATIVE BUYTarget Price: $3.50 December 3, 2009

Battery Grade or (Maybe?) BustInitiating Coverage with a BUY Recommendation:

• Western Lithium (WLC:TSXV) is a developer targeting production of pure lithium from clays for the rechargeable battery industry.

• We initiate coverage as SPECULATIVE BUY with a 3.50 target.

Potentially Pure:

• Of the two fl ow sheets developed for hectorite clay, leaching by Chevron and roasting by the US Bureau of Mines, WLC has targeted and refi ned lithium production via roasting.

• We believe roasting is inherently more expensive than leaching, but roasting may produce cleaner lithium which can be sold at a premium, compared to brine-based lithium carbonate.

Pure U.S. Made Lithium Means High Margins:

• The ability to manufacture pure lithium in the United States may allow WLC to achieve high margins by selling its product to U.S. and Asian lithium battery manufacturers.

• With 22% of current lithium demand from the battery industry, WLC could easily fi nd demand for

All fi gures in US$, unless otherwise noted

Recent Price: C$1.51

52 Week Range: C$0.11-1.62

Shares O/S: basic 79.70 million

f.d. 99.91 million

Market Cap (f.d.): C$150.9 million

Average Vol. (3 mo.) 386,000

Fiscal Year End: Sep. 30

Cash (Sep 30/09, est.): C$21 million

Financials 2013E 2014E

Tonnes Li2CO

3 6,000 25,000

Revenue (C$ M) $45.0 $187.5

EPS (C$) $(0.06) $0.49

Cash Flow/Share (C$) $0.14 $0.71

Company DescriptionWestern Lithium Canada Corporation is a junior lithium developer, with a twist. Rather than searching for brines as most companies in the space, the company is seeking cost-effective ways to produce and market highly purifi ed lithium chemicals made from hectorite clay deposits located in Nevada.

its initial annual production target of 25,000 tonnes of carbonate equivalent.

Source: www.bigcharts.com

SummaryWe are initiating coverage on Western Lithium Canada Corporation (WLC:TSXV), with a BUY recommendation and SPECULATIVE risk level. Our target price of $3.50 is based on our production targets for the company, and premium pricing of its lithium carbonate based on sales to the rechargeable battery industry.

Lithium is the lightest metal in the periodic table, and is highly reactive. This reactivity makes lithium useful for the production of rechargeable batteries, and its light weight makes the batteries more effective than any other in storing large quantities of energy in small and lightweight packages. This has enabled many new

Jon Hykawy, Ph.D., MBAClean Technologies & Materials

Arun Thomas, MBAAssociate

14

West

ern

Lit

hiu

m C

an

ad

a C

orp

ora

tio

n

applications over the years, including cellular telephones, laptop computers, power tools and, now, electric vehicles to become commercial successes. Lithium demand from rechargeable batteries is now roughly 20% of a global market of 118,000 tonnes of lithium carbonate equivalent (LCE), or 23,600 tonnes. With continued cost reductions on the batteries, and strong growth in demand for electric vehicles and other electronics, we expect battery demand to grow to 56, 400 tonnes of LCE by 2014.

The argument has been made that major producers of lithium, such as SQM of Chile (SQM:NYSE), Chemetall (part of ROC:NYSE) or FMC Lithium (part of FMC:NYSE), can produce more than enough lithium for all users well into the future. This neglects the fact that most major producers source their lithium through solution mining by pumping brine sourced from dry salt lakes, or salars, to surface and then concentrating and extracting lithium using solar evaporation and process chemicals. The aquifers being used to supply the brines can accommodate only a certain level of annual production before the aquifer becomes diluted or depleted, damaging later production. Concentrating brines takes time, and this means that brine-based producers cannot, without signifi cant stockpiling, alleviate short-term spikes in demand or price. Given the potential critical role played by lithium in the electric vehicle industry, politicians in various jurisdictions (President Evo Morales of Bolivia, Senator Ricardo Nunez of Chile) are openly discussing the nationalization of lithium deposits. All of the above may exacerbate any potential shortages in the supply of LCE.

It is our belief that the well understood mineral source of lithium, spodumene, is too expensive to mine, and new spodumene-based projects are uneconomic unless other minerals (such as the tantalum produced along with lithium by Australia’s Talison Minerals) can help defray total costs. While mineral-based production of lithium would allow producers to meet surges in demand, new projects cannot be constructed on the basis of short price fl uctuations.

The hectorite clay deposits in Nevada offer, we believe, the opportunity to fi nd a stable supply of lithium from a source in the United States. The roasting process developed by the US Bureau of Mines and refi ned by WLC and Kappes, Cassiday & Associates (KCA) in Reno, Nevada, has the potential to produce highly purifi ed LCE, perhaps pure enough to command a substantial price premium over bulk, brine-sourced LCE. And because WLC can produce lithium from clay removed from an open-pit mine, the company has the ability to meet spikes in demand without concern for depletion of its resource.

We believe that WLC represents a world-class company in an industry that is about to undergo explosive demand growth. Investors interested in participating in the trend

toward vehicle electrifi cation should own WLC as one of their lithium suppliers. We have established a target price of $3.50 on WLC, making our initial recommendation a SPECULATIVE BUY.

Lithium From Clay — Why And HowLithium is a critical ingredient in the manufacturing of rechargeable lithium-ion batteries. While certainly not a major factor in fi nal cost of the cell, without lithium there can be no lithium-ion battery. There are other elements that can be used to build other types of rechargeable batteries, but none of them have the ability to produce as much power or store as much energy as a lithium-ion battery.

While the current lithium market is roughly 118,000 tonnes of Li

2CO

3, or lithium carbonate equivalent (LCE),

only about 23,600 tonnes of this demand is currently from rechargeable batteries. Of course, this is up from essentially zero demand from batteries in 1999, so growth has been, and continues to be, robust. Our previous report, Lithium: The Next Strategic Material (Sept. 4, 2009), outlined our projections for supply and demand, and we believe that battery demand alone will grow to 56,400 tonnes of LCE by 2014.

According to TRU Group, some 72% of the lithium produced in the world today comes from brine-based suppliers. This amounts to some 85,000 tonnes LCE per year. Brine-based supply is the least expensive source of lithium (roughly $2,300 per tonne of LCE, versus as much as $6,500 per tonne from spodumene), but supplying lithium from brines demands that the producer respect the aquifer and ensure that its pumping rate does not result in depletion or even excessive dilution of the reservoir.

Production of lithium from brines is done using solar evaporation, the lowest cost method possible. Foote Mineral has previously disclosed, in US Patent Number 4,261,960, the general method of producing lithium carbonate from the brines of Clayton Valley, Nevada. Brine is pumped into a succession of holding ponds until its lithium concentration rises to 800 ppm. At this point, slaked lime is added as the brine is pumped to a new pond, and magnesium (Mg) in the brine reacts with the lime to create Mg(OH)

2, which precipitates out of solution. Mg

is separated out as Li concentration increases to perhaps 2,000 ppm. Acid and calcium chloride are then added to remove boron and sulphate from the brine; the brine is then pumped to the further succession of ponds until Li concentration rises and soda ash is added to precipitate out the lithium as Li

2CO

3, what amounts to lithium-based

chalk.

Necessarily, this process requires time. The speed is determined by the rate of evaporation of water, locally. In Clayton Valley, during the December to March timeframe, the net evaporation rate is negative — more water falls as

15

West

ern

Lit

hiu

m C

an

ad

a C

orp

ora

tio

n

snow than evaporates from ponds. As such, Chemetall does not even attempt to use its ponds during winter months. And even in the best environments on Earth, the time to produce lithium is measured in sizeable fractions of a year, not days or weeks. It is thus impossible, barring stockpiling, for a brine-based producer to respond to sudden spikes in price or demand for lithium. Note that it is during shortages when we would expect demand spikes to be most problematic, so stockpiles would likely have been drawn down.

A mineral-based producer can respond to spikes in demand relatively quickly, compared to a brine-based producer. The problem is that we estimate all-in costs for a spodumene operation producing lithium and no other metals to be as high as $6,500 per tonne LCE. This is due to high costs from the extraction of the ore, and high costs to leach out the lithium. Spodumene operations can be very cost effective if selling to the glass industry, as the glass makers can settle for using concentrates, removing a signifi cant amount of both process chemical and plant costs. But there has not historically been a low-cost mineral-based lithium solution for the chemical or battery industries.

This possibility was originally investigated by Chevron Research. In the 1970s and 1980s, Chevron looked into clay deposits in Nevada that showed anomalously high levels of Li. This clay, known as hectorite after the town of Hector, California, where it was fi rst identifi ed, has a substitution chemistry, with Li atoms taking the place of Mg in the form NaO

3(Mg,Li)

3Si

4O

10(F,OH)

2. Chevron found

that its leaching process (using lime to precipitate out Mg, leaching the clay with sulphuric acid to free lithium and then converting lithium sulphate to carbonate using soda ash) would produce quality lithium but at a price disadvantage to brine production. We believe the cost of lithium produced from clays by leaching is roughly $3,000 per tonne, as opposed to perhaps $2,300 per tonne for very good brine. Given that at the time the lithium market was small and purely industrial, with industrial rates of growth, it is not surprising that Chevron chose to discontinue its work on the Kings Valley hectorite deposit.

The US Bureau of Mines examined an even more expensive method of producing lithium from hectorite, namely roasting. The roasting cycle involves removing and pulverizing the clays, then heating to roughly 1,000°C in the presence of sulphates (such as gypsum) and oxides (such as lime or, in the case of the circuit developed by WLC and its partner KCA, dolomite). Roasting converts lithium in the hectorite to lithium sulphate, which is then washed out of the clay into solution in water, and the presence of hydroxides keep undesirable contaminants such as magnesium from converting to water-soluble form. Once the lithium is dissolved in process water, the conversion to insoluble lithium carbonate is done using soda ash.

Exhibit 1: Lithium Carbonate, Made by WLC and KCA

Source: Byron Capital Markets

We believe the all-in cost for lithium produced via clay roasting (including amortization and labour) is roughly $3,600 per tonne. However, there are two mitigating factors to bear in mind. First, it is possible for WLC to produce some ancillary products, such as potash or potentially even fl uorine compounds. While there are likely additional raw material costs associated with production of these ancillary chemicals, revenue should more than offset costs and result in effectively less expensive lithium.

Exhibit 2: Cost of Lithium from Clay Roasting (Less Labour)

Process Step Chemical/Driver Cost

Cost ($/tonne Li

2CO

3)

Extract Clay n/a 308

Grind Clay n/a 64

Heat for Roasting Steam to 1,000 °C 400

Gypsum Calcium sulphate (CaSO

4)

670

Dolomite CaMg(CO3)

2500

Wash Water 0

Convert to Carbonate

Soda ash (Na

2CO

3)

480

Plant Amortization

n/a 1,000

Total 3,422

Variable Cost per tonne

2,422

Source: Byron Capital Markets

Second, and perhaps even more important, we consider it possible that the lithium produced by WLC may be pure

16

West

ern

Lit

hiu

m C

an

ad

a C

orp

ora

tio

n

enough to either substantially reduce the costs associated with refi ning bulk lithium to battery-grade chemical, or eliminate those costs entirely. Normal bulk-grade lithium carbonate from brine production is at roughly 99% purity, but battery production, depending on the manufacturer, may demand lithium of 99.9% purity or higher, with certain contaminants such as iron or calcium mandated to be below stringent thresholds. If WLC can produce what is essentially battery-grade product at the above cost, the company would likely be extremely successful.

The Deposit — Hectorite Clay in the Desert

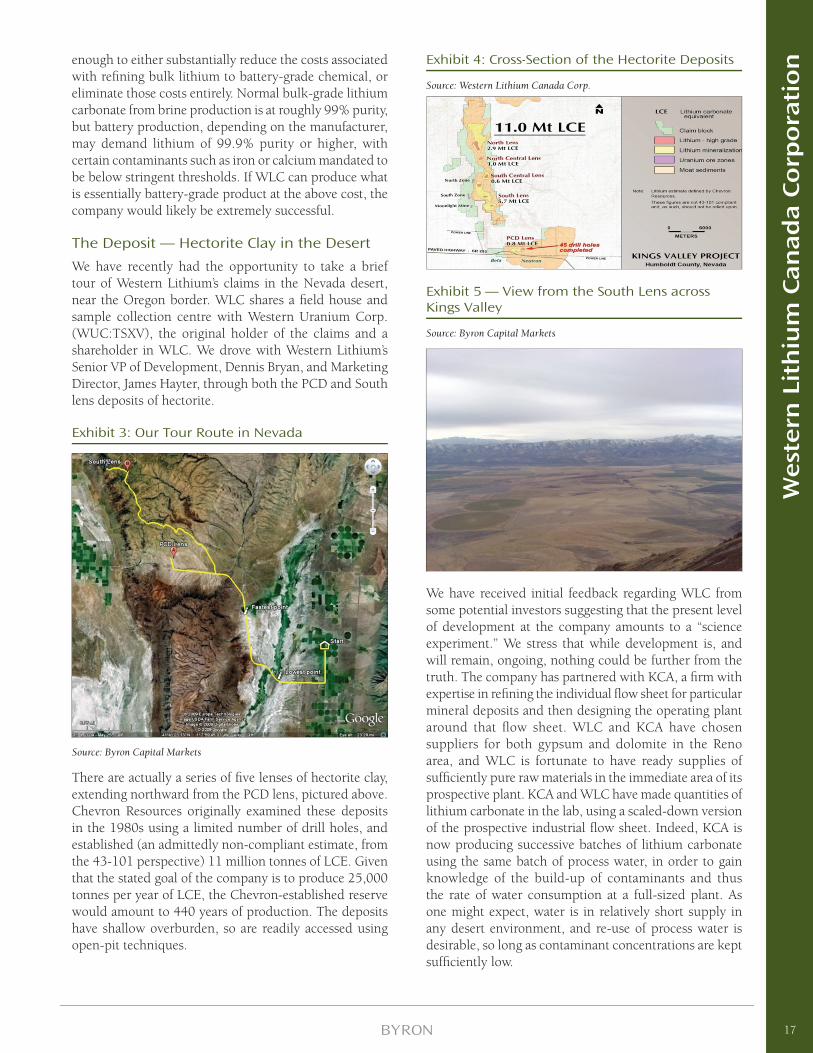

We have recently had the opportunity to take a brief tour of Western Lithium’s claims in the Nevada desert, near the Oregon border. WLC shares a fi eld house and sample collection centre with Western Uranium Corp. (WUC:TSXV), the original holder of the claims and a shareholder in WLC. We drove with Western Lithium’s Senior VP of Development, Dennis Bryan, and Marketing Director, James Hayter, through both the PCD and South lens deposits of hectorite.

Exhibit 3: Our Tour Route in Nevada

Source: Byron Capital Markets

There are actually a series of fi ve lenses of hectorite clay, extending northward from the PCD lens, pictured above. Chevron Resources originally examined these deposits in the 1980s using a limited number of drill holes, and established (an admittedly non-compliant estimate, from the 43-101 perspective) 11 million tonnes of LCE. Given that the stated goal of the company is to produce 25,000 tonnes per year of LCE, the Chevron-established reserve would amount to 440 years of production. The deposits have shallow overburden, so are readily accessed using open-pit techniques.

Exhibit 4: Cross-Section of the Hectorite Deposits

Source: Western Lithium Canada Corp.

Exhibit 5 — View from the South Lens across Kings Valley

Source: Byron Capital Markets