emc global data protection index filepoints awarded based on the maturity of their data protection...

TRANSCRIPT

1 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

EMC GLOBAL DATA PROTECTION INDEX KEY FINDINGS & RESULTS FOR THE UK

2 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

THE DATA PROTECTION LANDSCAPE ARE YOU ON SOLID GROUND?

3 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

GLOBAL KEY FINDINGS GLOBALLY, ENTERPRISES ARE LOSING AS MUCH AS $1.7 TRILLION THROUGH DATA LOSS AND UNPLANNED DOWNTIME

Adopting advanced data protection tools leads to reduced data loss

87% of businesses are behind the curve for data protection maturity and 71% of businesses are not fully confident of restoring their data

62% of respondents said at least one of the following: big data, hybrid cloud, mobile devices, is ‘difficult’ or ‘very difficult’ to protect

4 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

DEMOGRAPHICS

INTERVIEWED 3,300 IT DECISION-MAKERS

IN 3 REGIONS:

Americas (575)

Asia Pacific Japan (1,250)

Europe, Middle East, and Africa (1,475)

Interviewed 200 IT decision-makers in

the UK

INDEPENDENT RESEARCH AND ANALYSIS

BOTH PRIVATE AND PUBLIC ORGANIZATIONS

ORGANIZATIONS OF 250 OR MORE EMPLOYEES

24 COUNTRIES TOTAL

5 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

DATA PROTECTION MATURITY

6 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

MATURITY INDEX

* Exact scoring included in appendix – questions show points used for the original model with a maximum score of 68. All scores multiplied by a factor of 1.47 to create a model of 100 points

Maturity scored between 1–100 points*

Points awarded based on the maturity of their data protection strategy

More points awarded for: • Shorter recovery times • Confidence in backup infrastructure • Modern backup systems • Off-site replication

7 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

Leaders (scored 76-100 points) Adopters (scored 51-75 points)

WHO IS LEADING THE WAY?

Figure 1: Analysis of maturity Base: all respondents (3,300)

AHEAD OF ‘MATURITY’ CURVE

Evaluators (scored 26-50 points) Laggards (scored 1-25 points)

Global Results

UK Results

Figure 2: Analysis of maturity Base: all respondents from the UK (200)

35.5%

51.5%

11.0%

2.0%

Laggards

Evaluators

Adopters

Leaders

36.8%

49.5%

11.3%

2.4%

Laggards

Evaluators

Adopters

Leaders

8 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

Figure 3: Analysis of maturity – showing frequency of points scored Base: all respondents (3300)

AHEAD OF THE CURVE

NU

MBER

OF

CO

MPA

NIE

S

GLOBAL IT MATURITY SHOWING FREQUENCY OF POINTS SCORED

0

100

200

300

400

500

600

700

MATURITY POINTS SCORED 25 50 75 100

Laggards 37% (1,214 Companies)

Evaluators 50% (1,635 Companies)

Adopters 11% (372 Companies)

Leaders 2% (79 Companies)

UK

9 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

PROFILE CHARACTERISTICS

LEADERS

LAGGARDS

ADOPTERS

EVALUATORS

Use archiving application with offsite replication

Backup with deduplication & offsite replication

Recovery time 2 – 5 hours

Moderately confident of ability to restore

Active-active instances are core component of strategy

Archive to tape

Backup to tape

Recovery time more than one day

Not confident in ability to restore

Backup is core component of strategy

Use archiving application with retention policies

Disaster tolerant replication with near-zero RPO/RTO

Recovery time one hour or less

Very confident of ability to restore

Standby or virtualised servers are core component of strategy

Archive to disk

Backup to disk

Recovery time 6 – 24 hours

Doubtful of ability to restore

Replication is core component of strategy

10 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

37.6 34.3

31.0 29.1

37.8 35.6 34.8 33.5

31.8 31.5 31.0 30.9 27.3 27.0

42.5 41.7 39.1 37.8 36.6

32.9 30.7 29.5 29.5

26.9

WHERE ARE THE MOST MATURE ORGANIZATIONS?

Figure 4: Analysis of average maturity score by region and country Base: all respondents (3300)

AMERICAS: 33.7

EMEA: 32.2

APJ: 34.7

AVERAGE SCORE ON THE MATURITY MATRIX

11 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• Businesses in China and Hong Kong most likely to be ahead of the curve

• Outside of Asia, the US and the Netherlands most likely to be ahead of the curve

• UAE, Turkey and Switzerland and least likely to be ahead of maturity curve

MATURITY RANK WHICH MARKETS ARE AHEAD?

RANK COUNTRY % OF BUSINESSES AHEAD OF MATURITY CURVE*

1 China 29.6% 2 Hong Kong 27.2% 3 Netherlands 20.8% 4 Singapore 20.0% 5 USA 19.5% 6 India 19.2% 7 South Africa 18.4% 8 Indonesia 18.4% 9 Mexico 17.6%

10 Germany 15.5% 11 Australia 14.4% 12 UK 13.0% 13 The Philippines 11.2% 14 Thailand 11.2% 15 Canada 9.6% 16 Russia 9.6% 17 Italy 9.6% 18 Brazil 8.8% 19 Japan 8.0% 20 South Korea 8.0% 21 France 6.5% 22 Switzerland 6.4% 23 Turkey 5.6% 24 UAE 0.0%

*Please note that the percentages have been rounded to one decimal place

12 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

THE IMPORTANCE OF DATA PROTECTION

13 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• The majority (53%) of respondents consider data protection to be totally critical to their organization’s success

• The public sector (64%) are most likely to see data protection as totally critical, compared to only 37% from the retail and consumer products sector

THE CRITICALITY OF DATA PROTECTION

Figure 5: “Do you consider data protection to be totally critical to the ongoing success of your organization?” Base: all respondents (200)

DO YOU CONSIDER DATA PROTECTION CRITICAL TO THE SUCCESS OF YOUR ORGANIZATION?

53% 39%

7% 2%

Very Important But Not Critical

Totally critical

Plays no role in our success Not very

important

14 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

SPENDING ON DATA PROTECTION Average company spend: • $197 million on IT • $12 million on data protection

• A significant proportion of revenue is spent on data protection, an average of 5.88% (approx. $12m)

• The IT and technology (7.57%) sector spends the most on data protection, while the manufacturing sector spends the least (4.57%)

Figure 6: Analysis of average spend of revenue on IT, and of IT budget on data protection Base: all respondents (200)

Average percentage of annual IT budget

that is spent on data protection

5.88%

Average percentage of domestic annual

revenue that is spent annually on IT

8.14%

15 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

Figure 7: “Is your data protection infrastructure built on technology from more than one vendor?” Base: all respondents (200)

• 62% have more than one data protection vendor

– Two vendors on average

• 74% of the retail and consumer products sector have more than one vendor. Only 51% of the IT and technology sector do

THE NUMBER OF DATA PROTECTION VENDORS

11% Have no specific

vendor

27% Have one vendor

62% Have more than

one vendor

16 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• The more vendors a business has, the greater proportional spend of IT budget on data protection

• In the UK, those with three or more vendors are spending 6.25% compared to 5.80% with one vendor

THE EFFECT OF NUMBER OF VENDORS ON SPEND

Figure 8: Analysis of average spend of IT budget on data protection, cut by number of data protection vendors Base: all respondents (200)

SHARE OF ANNUAL IT BUDGET SPENT ON DATA PROTECTION

6.25% Three or more data protection

vendors

5.80% One data protection

vendor

5.83% Two data protection vendors

17 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• 67% have suffered disruptions in the last 12 months

– 81% of retail and consumer products – 71% of public sector – 68% of manufacturing

• Average annual loss per company – 0.72TB of data (compared to 353GB in

2011) – Equivalent to around 7 million e-mails – Costs $1.1 million

• 25 hours were lost on average in the last 12 months due to unplanned downtime, costing $0.46m

– Compared to 2 days of downtime in 2011

SUFFERING DISRUPTIONS

Figure 9: “Has your organization suffered from either unplanned systems downtime or data loss in the last 12 months?” Base: all respondents (200)

DISRUPTIONS SUFFERED IN LAST 12 MONTHS

67% Suffered data loss

or unplanned downtime

60% Suffered

unplanned downtime

23% Suffered data loss

17% Suffered data loss

and downtime

18 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• The more vendors a business has, the more likely it is to experience disruption

• Three quarters (75%) of those with three of more vendors have experienced unplanned systems downtime within the last 12 months

THE EFFECT OF THE NUMBER OF VENDORS ON DISRUPTIONS

Figure 10: Analysis of the organizations suffering disruptions, cut by the number of data protection vendors Base: all respondents (200)

DISRUPTIONS SUFFERED (BY NUMBER OF VENDORS)

26% 19% 20%

Three or more data protection vendors

One data protection vendor

Two data protection vendors

Data loss Unplanned systems downtime

75% 52% 53%

19 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

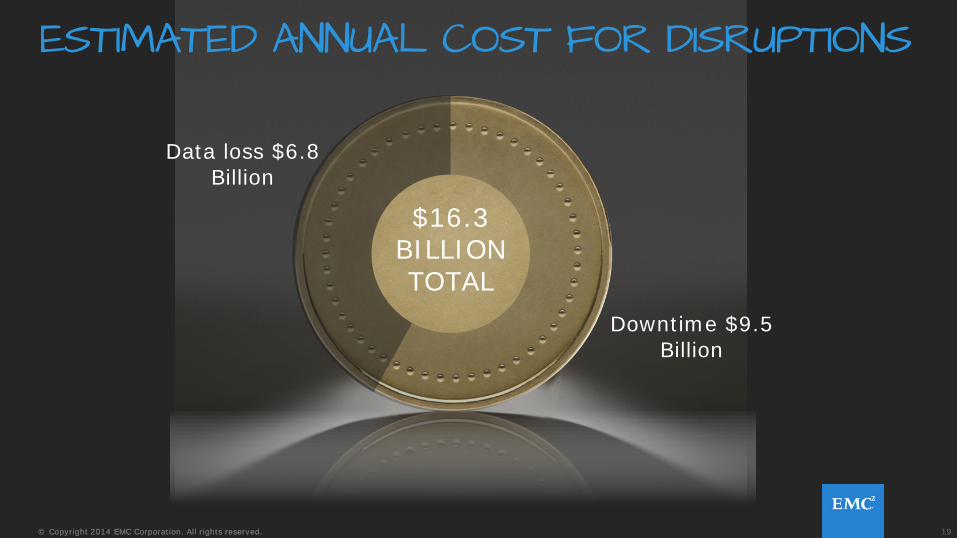

ESTIMATED ANNUAL COST FOR DISRUPTIONS

Downtime $9.5 Billion

Data loss $6.8 Billion

$16.3 BILLION TOTAL

20 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

PERCENTAGE OF DATA BACKED UP CONTINUOUSLY BY BUSINESSES

• On average, around one fifth of data is backed up continuously

• Almost two fifths of organizations do not back up anything continuously & suffer 23 hours downtime

• 85% of those “ahead of the curve” back up some data continuously, compared to 46% of Laggards

FREQUENCY OF CONTINUOUS BACKUP

Figure 11: Analysis of those that backup data continuously Base: all respondents (200)

0% of data backed up continuously

1% - 25% of data backed up continuously

25% - 50% of data backed up continuously

50%- 75% of data backed up continuously

75% - 99% of data backed up continuously

100% of data backed up continuously

38%

40%

13%

6% 3%

2%

21 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

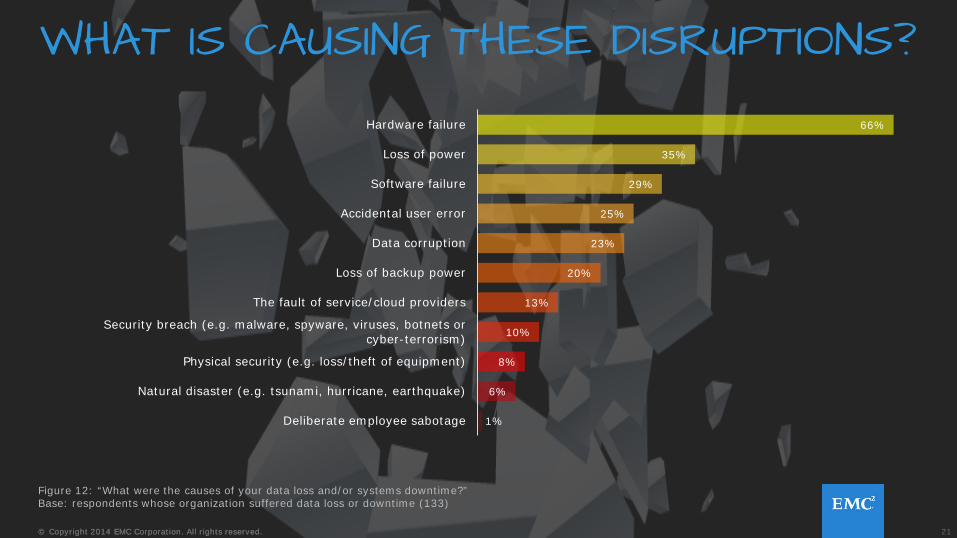

WHAT IS CAUSING THESE DISRUPTIONS?

Figure 12: “What were the causes of your data loss and/or systems downtime?” Base: respondents whose organization suffered data loss or downtime (133)

66%

35%

29%

25%

23%

20%

13%

10%

8%

6%

1%

Hardware failure

Loss of power

Software failure

Accidental user error

Data corruption

Loss of backup power

The fault of service/cloud providers

Security breach (e.g. malware, spyware, viruses, botnets or cyber-terrorism)

Physical security (e.g. loss/theft of equipment)

Natural disaster (e.g. tsunami, hurricane, earthquake)

Deliberate employee sabotage

22 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

THE CONSEQUENCES OF DISRUPTION

Figure 13: “Have any of the above been commercial consequences of the data loss and/or systems downtime you have experienced over the last 12 months?” Base: respondents whose organization suffered data loss or downtime (133)

52%

34%

23%

21%

10%

8%

8%

8%

8%

8%

22%

Loss of employee productivity

Loss of revenue

Loss of customer confidence/loyalty

Delay in product/service development

Loss of a new business opportunity

Delay in getting products/services to market

Loss of business to a competitor

Loss of an incremental business opportunity

Loss of customers

Loss of repeat business

There have been no commercial consequences

23 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• More than three quarters (78%) are not fully confident that they can recover systems/data today from all platforms

• Only 11% in the retail and consumer products sector and 18% in the financial services sector are very confident

ARE ORGANIZATIONS CONFIDENT?

Figure 14: “How confident are you that, in the event of a data loss incident, you can fully recover systems/data today from all platforms, on-premise and off-premise, in order to meet business service level agreements?” Base: all respondents (200) Used for maturity matrix

Very confident

22%

Not very confident

78%

24 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

DATA PROTECTION METHODS

25 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• A significant proportion use backup as the primary protection strategy

• 15% use active-active as a key component

• Those with active-active as the key component suffered less data lost than those with backup

– 14% active-active vs. 19% backup

WHAT STRATEGIES ARE IN PLACE?

Figure 15: “Which of the above best characterises your organization's current data protection environment infrastructure?” Base: all respondents (200) Used for maturity matrix

15%

15%

17%

25%

30%

Active-active instances of applications (including cloud) are key component of

our availability strategy

Virtual servers with restart capabilities (including cloud) are the main

components of our availability strategy

Standby servers on a remote site are the main components of our availability

strategy

Replication is the main component of our availability strategy

Backup is the main component of our availability strategy

26 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

WHAT OTHER STRATEGIES ARE IN PLACE? THERE IS NO CONSENSUS ON THE TECHNOLOGY IN PLACE FOR AVAILABILITY, ALTHOUGH AN AVERAGE OF THREE STRATEGIES SHOWS A VARIED APPROACH ACROSS ALL ORGANISATIONS

Figure 16: “Which technologies/strategies are in place to help you manage the availability of your applications, systems, and data?” Base: all respondents (200) Used for maturity matrix

45%

37%

35%

33%

29%

27%

26%

21%

10%

9%

7%

Disk-based backup and recovery including clones/snaps

Tape backup and tapes are kept off site (on own premises)

Replication of both applications and data (such as virtual machine images)

Tape backup and tapes are kept off site (on 3rd party premises)

WAN-based replication of backup and recovery images to second site

Replication to a second site with restart capabilities (active/passive)

Automatic backup to the cloud

Backup appliance with deduplication

Dynamic mobility of virtual applications between data centres

Disaster tolerant replication (active/active) with near zero RPO and RTO

Tape backup and tapes go home with employees

STRATEGIES TO HELP MANAGE AVAILABILITY OF APPLICATIONS, SYSTEMS & DATA

27 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

DESIRE HAVE VISIBILITY/CONTROL OVER DATA PROTECTION (ON-PREMISE & IN CLOUD)

WHO IS IN CHARGE OF THE CLOUD?

RESPONSIBILITY FOR DATA PROTECTION FOR PUBLIC CLOUD-BASED APPLICATIONS

Figure 17: “For public cloud based applications, which organizations are responsible for data protection?” Base: respondents whose organization is using a type of cloud as a platform for infrastructure (134)

Figure 18: “Do you want to have visibility and/or control over how your data is being protected both on-premise and in the cloud?” Base: respondents whose organization is using a type of cloud as a platform for infrastructure (134)

63%

52%

13%

My IT department as a whole

The cloud service provider

Each department in my organization, dependent on their use of the application in question

60%

47%

9%

Yes – I want to have to visibility of how the organization's on-premise

and off-premise data is being protected

Yes - I want to have to control of how the organization's on-premise

and off-premise data is being protected

No – I only want to manage my local data; the cloud service provider should manage off-

premise data

28 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

WHERE IS DATA STORED? PRIMARY DATA

Figure 19: Analysis of average amount of primary data on different platforms Base: all respondents (200)

32%

30%

10%

9%

8%

5%

5%

2%

On-premise (physical servers)

On-premise (virtualized servers)

Hybrid cloud

On-premise (private cloud)

Mainframe

Desktop/laptop

Public cloud

Mobile devices

29 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

WHAT IS HARDEST TO PROTECT? MAJORITY DO NOT HAVE DISASTER RECOVERY PLAN FOR SOME APPLICATIONS THEY FIND HARDEST TO PROTECT

MOST DIFFICULT APPLICATIONS/PLATFORMS TO PROTECT

APPLICATIONS/PLATFORMS WITHOUT A RECOVERY PLAN

Figure 20: Analysis of applications/platforms that do not have disaster recovery plans Base: all respondents (200)

Figure 21: Analysis of applications/platforms that are difficult to protect Base: all respondents (200)

76%

80%

87%

Big data/data lakes

Mobile devices

Hybrid cloud applications

27%

33%

54%

Hybrid cloud applications

Big data

Mobile devices

30 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

• 28% currently using Backup-as-a-Service; further 29% plan to in the future

• 36% plan to use archive as a service and 33% plan to use data recovery as a service in the future

FUTURE STRATEGIES

Figure 22: “Are you currently, using or looking to adopt, any of the above data protection cloud services in the next 12 months?” Base: all respondents (200)

DATA PROTECTION CLOUD SERVICES

28%

17%

15%

29%

36%

33%

Backup-as-a-Service

Archive-as-a-Service

Data recovery-as-a-Service

Currently using

Plan to adopt at some point

31 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

SUMMARY FOR THE UK

53% consider data protection to be critical to

their organization’s success, still

67% suffered downtime or

data loss in last 12 months

More than one data protection vendor means more spending

on data protection

87% of businesses are

behind the curve for data

protection maturity and

78% of businesses are

not fully confident in their ability to restore

apps/data

ENTERPRISES ARE LOSING AS MUCH AS $16.3 BILLION THROUGH DATA LOSS AND UNPLANNED DOWNTIME

32 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

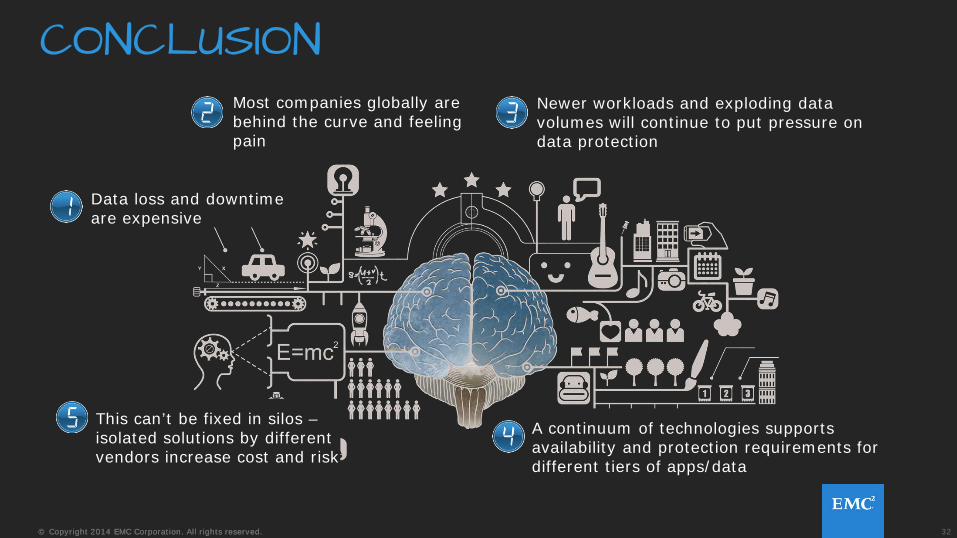

CONCLUSION

Data loss and downtime are expensive

Most companies globally are behind the curve and feeling pain

Newer workloads and exploding data volumes will continue to put pressure on data protection

This can’t be fixed in silos – isolated solutions by different vendors increase cost and risk

A continuum of technologies supports availability and protection requirements for different tiers of apps/data

33 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

EMC RECOMMENDATIONS

Match your data protection approach with the availability and protection requirements for your tiers of applications/data

Evaluate the gaps in your protection strategy that may emerge from disparate vendor solutions

Manage an integrated data protection strategy and maintain a level of visibility and control for application owners

Understand who “owns” data protection – especially in the cloud

Make sure there’s an appropriate data protection solution in place for all of your critical data no matter where it is or how it is generated

34 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

APPENDIX (i) MATURITY SCORING

Which of the following best characterises your organization's current data protection environment infrastructure?

• Backup is the main component of our availability strategy – (1pt.)

• Replication is the main component of our availability strategy – (3pts.)

• Standby servers on a remote site are the main components of our availability strategy – (4pts.)

• Virtual servers with restart capabilities (including cloud) are the main components of our availability strategy - (5pts.)

• Active-active (two or more production data centres that are always on, 24/7 with no downtime) instances of applications (including cloud) are key component of our availability strategy – (6pts.)

What best describes your organization's archiving strategy?

• We don’t have an archiving strategy – (0pt.)

• We use a backup application to archive data onto tape – (1pt.)

• We use an archiving application to archive data online (e.g. onto disk) – (3pts.)

• We use an archiving application to archive data to appliances that provide retention locking, litigation hold etc. – (5pts.)

• We use an archiving application to archive data to appliances that provide retention locking, litigation hold etc. and replicate/keep a copy off site - (7pts.)

35 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

APPENDIX (ii) MATURITY SCORING

• Tape backup and tapes go home with employees – (1pt.)

• Tape backup and tapes are kept off site (on own premises)– (2pts.)

• Tape backup and tapes are kept off site (on 3rd party premises) – (2pts.)

• Automatic backup to the Cloud (2pts.)

• Disk-based backup and recovery including clones/snaps – (3pts.)

• Backup appliance with deduplication – (4pts.)

• WAN-based replication of backup and recovery images to second site – (4pts.)

• Replication of both applications and data (such as virtual machine images) – (5pts.)

• Replication to a second site with restart capabilities (active/passive) – (5pts.)

• Dynamic mobility of virtual applications between data centres – (7pts.)

• Disaster tolerant replication (active/active) with near zero RPO and RTO – (8pts.)

Which technologies/strategies are in place to help you manage the availability of your applications, systems, and data? (Please select all that apply)

36 © Copyright 2014 EMC Corporation. All rights reserved. © Copyright 2014 EMC Corporation. All rights reserved.

APPENDIX (iii) MATURITY SCORING

During an unexpected event causing downtime to our most critical applications, how long is your recovery time?

• Our recovery time is more than one working day (please specify) – (0pt.)

• Our recovery time is 12 - 24hours – (1pt.)

• Our recovery time is 6 -12 hours (2pts)

• Our recovery time is 3 – 6 hours (3pts)

• Our recovery time is 2 – 3 hours (4pts)

• Our recovery time is 1 – 2 hours – (5pts.)

• Our recovery time is less than an hour– (6pts.)

• Our recovery time is zero – (7pts.)

• I do not know – (0pt.)

How confident are you that, in the event of a data loss incident, you can fully recover systems/data today from all platforms, on premise and off premise, in order to meet business service level agreements?

• Very confident – (6pts.)

• Moderately confident – (4pts.)

• Some doubt – (3pts.)

• Not very confident – (1pts.)

• Not at all confident – (0pts.)