emerging from the pandemic

TRANSCRIPT

Updated November 9, 2021Emerging From the Pandemic

“To suggest that the airlines should have better prepared for this environment seems akin to suggesting Pompeii should have invested more heavily in firefighting technology.” (JPMorgan, Mar. 22, 2020)

2

» New ticket sales are rising but demand for corporate and long-haul international air travel continues to lag, leaving revenues depressed.

» Air cargo demand, which reached a record high in 2020, has risen further in 2021.

» As with numerous other industries, airlines are facing inflationary pressures.

» Debt (and interested expense) will remain elevated through at least 2024.

Key Points

3

The Largest U.S. Passenger Airlines Incurred $841 Million in Pre-Tax Losses in YTD 3Q 2021Results Boosted Materially by $19B in Federal Payroll Support Program (PSP) Funds

1. Sale of frequent flyer award miles to airline business partners, transportation of pets, in-sourced aircraft and engine repair, flight simulator rentals, inflight sales, etc.2. Related primarily to ownership of aircraft, ground support equipment, information technology, etc.3. Aircraft rents, professional fees, food/beverage, insurance, commissions, GDS fees, communications, advertising, utilities, office supplies, crew hotels, payments to regional carriers, etc.

Source: Alaska, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit and United

Financial Results (in $ Billions) Jan-Sep 2021 % vs. 2019 % of CategoryPassenger (RPMs down 42%, yield down 8%) 67.8 (47) 83.6Cargo 3.6 53 4.5Other1 9.7 (9) 12.0

Total operating revenues 81.1 (41) 100.0Salaries, wages and benefits* 33.3 (6) 42.7Aircraft fuel and related taxes 17.7 (10) 22.7Maintenance materials and repairs 5.0 (1.5) 6.4Landing fees and airport rentals 7.6 0.6 9.8Depreciation and amortization2 7.1 0 9.2Other3 7.2 (10) 9.2Total operating expenses 77.9 (45) 100.0

Interest and other non-op expenses, net 4.0 2 n/aPre-tax income/(loss) (0.8) n/a n/a

* Includes the benefit of ~$19B in federal PSP funds (Jan. 1-Sept. 30, 2021)

Includes the benefit of ~$19B in federal PSP funds.

4

In 2020, Travel-Sector Profitability Took a Massive Hit; Overall Corporate Profitability Was FlatPre-Tax Profit Margin (% of Operating Revenues)

Source: Company SEC filings

6.3 9.8 13

.8

13.8

14.5

21.5

27.8

28.6

34.6

4.9

(58.

8)

(7.1

)

3.6 14

.5

25.4

(34.

3)

32.0

32.9

Chipotle Airlines Disney Starbucks All USA Apple Hotels McDonald´s Railroads

2019 2020

Note: Airlines = Alaska/Allegiant/American/Delta/Hawaiian/JetBlue/Southwest/Spirit/United; Hotels = Choice/Hilton/Hyatt/Marriott/Wyndham; Railroads = CSX/Norfolk Southern/Union Pacific

5

A Multiyear, Multistage Recovery Is Underway

Traffic Recovery

Revenue Recovery

Financial Recovery

Reduce Cash Burn

Restore Profitability& Rebuild Margins

Repair Balance Sheets

Contain the Virus

Stabilize the Economy

Increase Efficiency

Aviation-Government Collaboration on Health/Facilitation/Safety/Technology

Business Model Adaptation + Cost-Reduction Initiatives + Debt ReductionCost-Reduction Initiatives + Business Model Adaptation + Debt Reduction

6

J.D. Power: North America Airline Customer Satisfaction Climbs to Record HighLatest Results Released May 2021

Source: J.D. Power North America Airline Satisfaction StudySM

Note: The 2021 study is based on responses from 2,309 passengers who flew on a major North American airline between August 2020 and March 2021.

692

687

668

658

673

683

681

695

712

717

726

756

762

773

792

819

0

200

400

600

800

1,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

“The airline industry adapted to a most unusual year by simplifying ticketing processes, waiving change fees and baggage fees which were key to persuading people to fly during the pandemic. Airline personnel rose to meet the challenges of a drastically altered travel environment. Maintaining that level of flexibility and recognition of individual passenger needs will be a strategic advantage for airlines that want to set themselves apart in passenger satisfaction as travel volumes start to recover.” (Michael Taylor, J.D. Power, May 12, 2021)

Aircraft Baggage Boarding Check-in Cost and fees Flight crew ReservationIn-flight services

7

Per Wells Fargo, the Global Economy Will Grow 4.3% in 2022The U.S. Economy Is Projected to Grow 4%

4.3 4.0

4.3 5.1

2.5 4.1

3.6 5.5

8.1 3.0

2.3

WorldUSA

EurozoneUK

JapanCanada

AustraliaChinaIndia

MexicoBrazil

Source: Wells Fargo Securities (Oct. 14, 2021)

“While we remain concerned about COVID’s impact on consumer spending, most individuals seem to be going about their daily routines, albeit perhaps not with the same vigor as they did earlier in the summer when the pandemic appeared to be winding down. In short, significant retrenchment in consumer spending does not appear likely unless the new case count shoots markedly higher…” (Wells Fargo, Oct. 14, 2021)

Projected 2022 Real GDP Growth (%)

$18.7$19.1

$18.4

$19.5

$20.2

2018 2019 2020 2021F 2022F

U.S. Real GDP (Trillions, $2012)

8

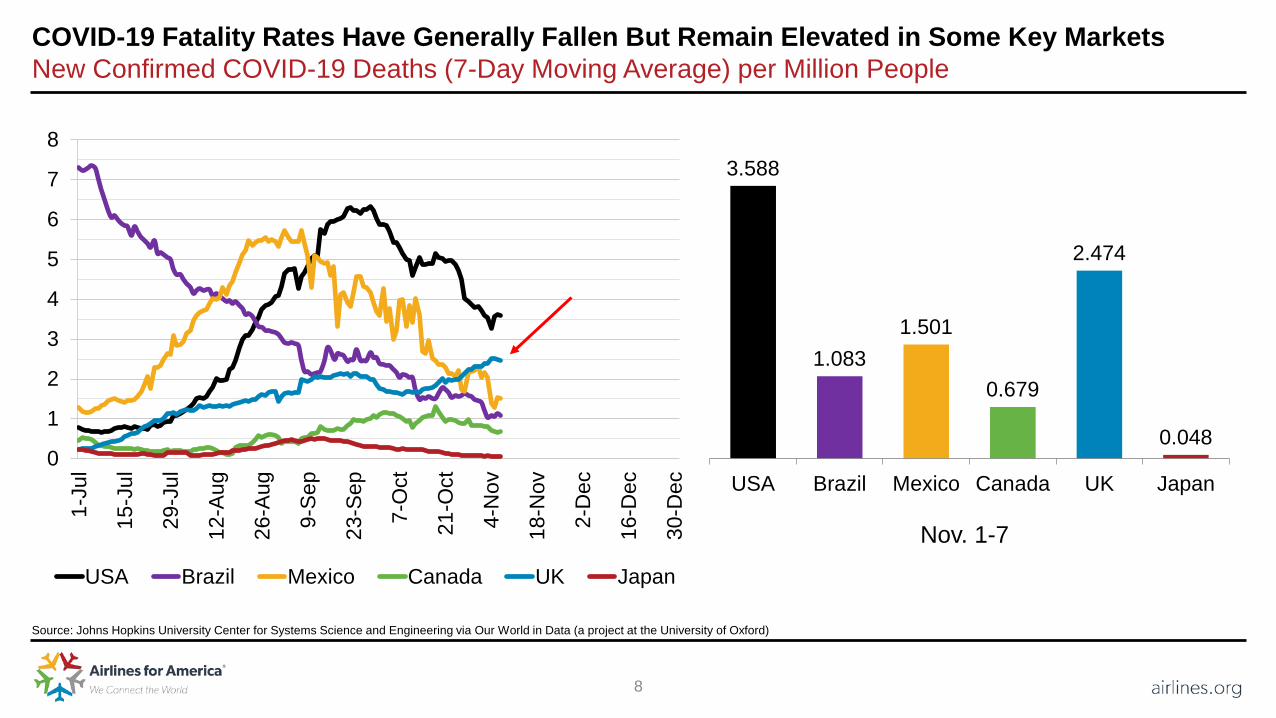

COVID-19 Fatality Rates Have Generally Fallen But Remain Elevated in Some Key MarketsNew Confirmed COVID-19 Deaths (7-Day Moving Average) per Million People

Source: Johns Hopkins University Center for Systems Science and Engineering via Our World in Data (a project at the University of Oxford)

0

1

2

3

4

5

6

7

8

1-Ju

l

15-J

ul

29-J

ul

12-A

ug

26-A

ug

9-Se

p

23-S

ep

7-O

ct

21-O

ct

4-N

ov

18-N

ov

2-D

ec

16-D

ec

30-D

ec

USA Brazil Mexico Canada UK Japan

3.588

1.0831.501

0.679

2.474

0.048

USA Brazil Mexico Canada UK Japan

Nov. 1-7

9

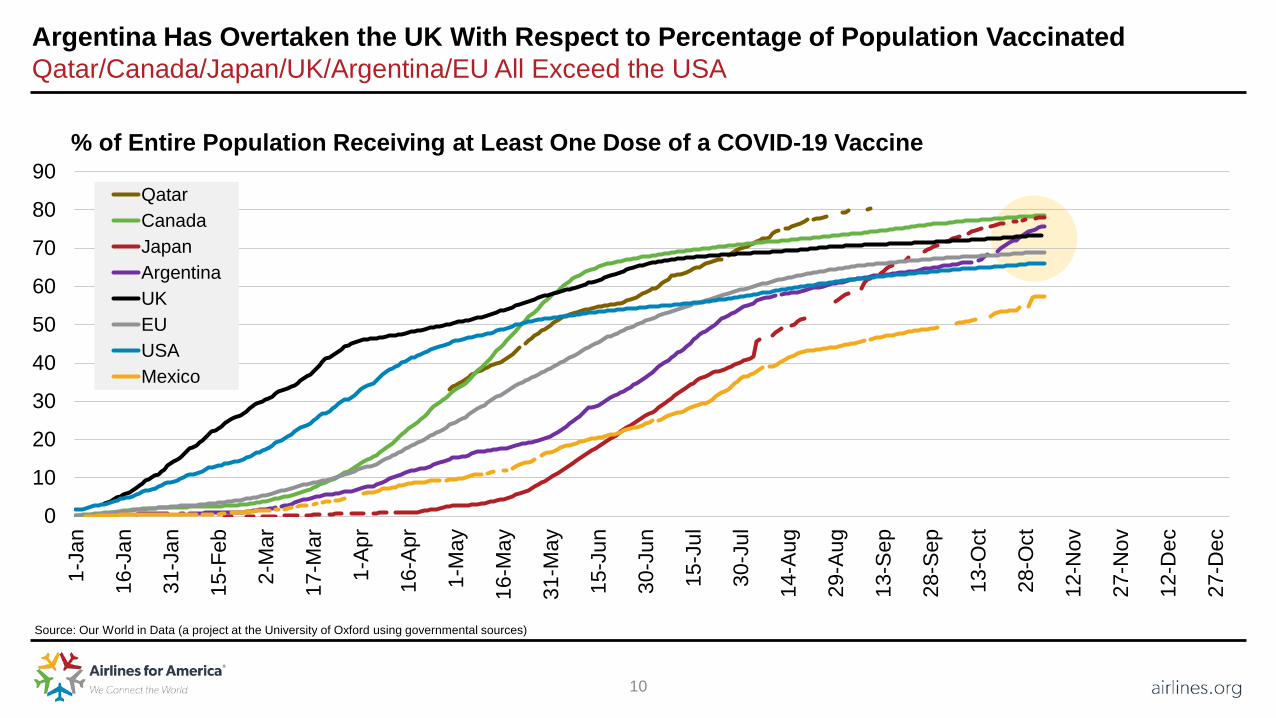

In Several Nations, at Least 70% of the Population Has Received at Least One Dose of a VaccineAruba/Belgium/Canada/China/Ireland/Italy/Japan/S. Korea/Spain Are 70%+ Fully Vaccinated

58 4976 69

5074 67

15

72 69 7755

79

3358

4469 68

25

73 6376 65 76 75

60

910

46

13

43

6

6 86

19

2

4

1818

7 7

29

56

12

5 13

6759

80 7563

7870

21

78 77 8374

81

37

7662

76 75

54

7869

7767

81 7663

0102030405060708090

100

Fully Partially

Source: Our World in Data (a project at the University of Oxford using governmental sources) via The New York Times and DOT Data Bank 1B * Partially = received at least one dose of a vaccine as of Nov. 9, 2021

% of Entire Population Vaccinated* in Selected U.S.-International O&D MarketsSorted left to right by U.S.-carrier O&D passenger volume in 2019

10

Argentina Has Overtaken the UK With Respect to Percentage of Population VaccinatedQatar/Canada/Japan/UK/Argentina/EU All Exceed the USA

0

10

20

30

40

50

60

70

80

90

1-Ja

n

16-J

an

31-J

an

15-F

eb

2-M

ar

17-M

ar

1-Ap

r

16-A

pr

1-M

ay

16-M

ay

31-M

ay

15-J

un

30-J

un

15-J

ul

30-J

ul

14-A

ug

29-A

ug

13-S

ep

28-S

ep

13-O

ct

28-O

ct

12-N

ov

27-N

ov

12-D

ec

27-D

ec

QatarCanadaJapanArgentinaUKEUUSAMexico

% of Entire Population Receiving at Least One Dose of a COVID-19 Vaccine

Source: Our World in Data (a project at the University of Oxford using governmental sources)

11

In Most Recent Week, U.S. Airline Passenger Volumes Were 18% Below Pre-Pandemic LevelsDomestic Air Travel Down 16%, International Air Travel Down 35%

(100)

(80)

(60)

(40)

(20)

0

20

40

7-Ja

n-20

28-J

an-2

0

18-F

eb-2

0

10-M

ar-2

0

31-M

ar-2

0

21-A

pr-2

0

12-M

ay-2

0

2-Ju

n-20

23-J

un-2

0

14-J

ul-2

0

4-Au

g-20

25-A

ug-2

0

15-S

ep-2

0

6-O

ct-2

0

27-O

ct-2

0

17-N

ov-2

0

8-D

ec-2

0

29-D

ec-2

0

19-J

an-2

1

9-Fe

b-21

2-M

ar-2

1

23-M

ar-2

1

13-A

pr-2

1

4-M

ay-2

1

25-M

ay-2

1

15-J

un-2

1

6-Ju

l-21

27-J

ul-2

1

17-A

ug-2

1

7-Se

p-21

28-S

ep-2

1

19-O

ct-2

1

9-N

ov-2

1

30-N

ov-2

1

21-D

ec-2

1

Domestic USA Canada Mexico Atlantic Latin (excl. Mexico) Pacific

7-Day Rolling Change (%) vs. Pre-Pandemic in Onboard Passengers*

* Onboard (“segment”) passengers; “pre-pandemic” precedes March 1, 2020Source: A4A member passenger airlines and branded code share partners

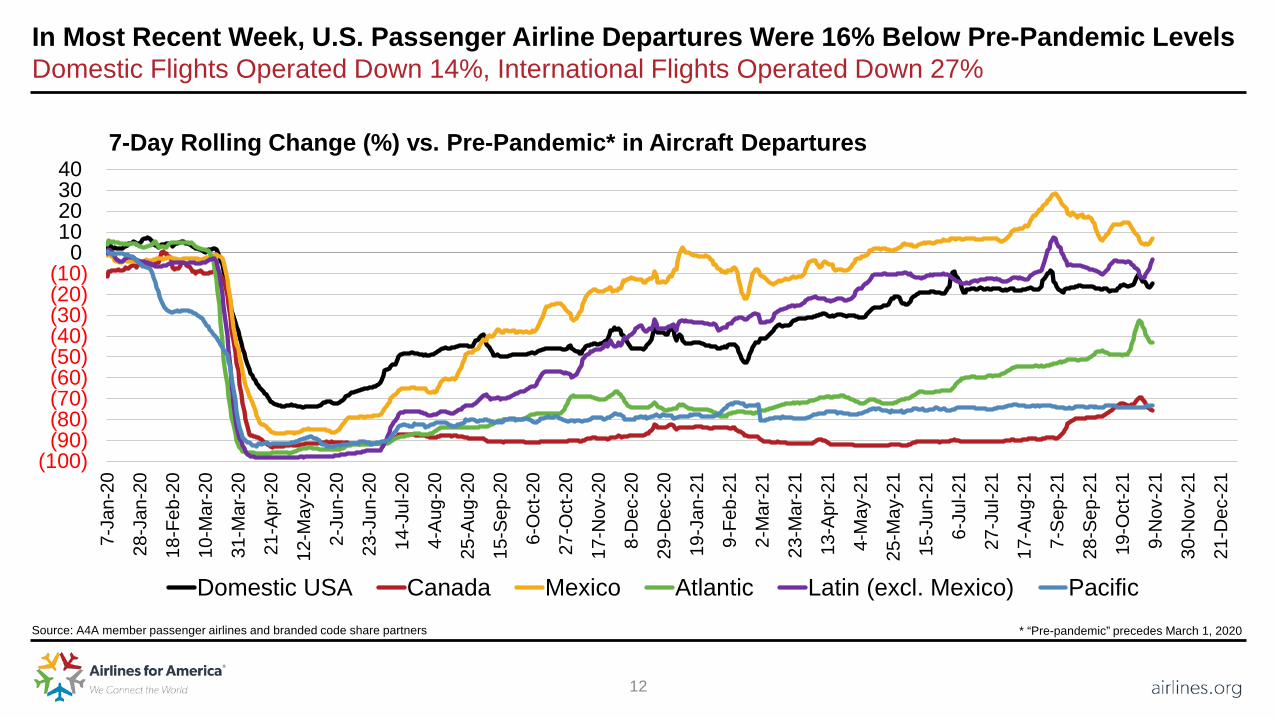

12

In Most Recent Week, U.S. Passenger Airline Departures Were 16% Below Pre-Pandemic LevelsDomestic Flights Operated Down 14%, International Flights Operated Down 27%

Source: A4A member passenger airlines and branded code share partners

(100)(90)(80)(70)(60)(50)(40)(30)(20)(10)

010203040

7-Ja

n-20

28-J

an-2

0

18-F

eb-2

0

10-M

ar-2

0

31-M

ar-2

0

21-A

pr-2

0

12-M

ay-2

0

2-Ju

n-20

23-J

un-2

0

14-J

ul-2

0

4-Au

g-20

25-A

ug-2

0

15-S

ep-2

0

6-O

ct-2

0

27-O

ct-2

0

17-N

ov-2

0

8-D

ec-2

0

29-D

ec-2

0

19-J

an-2

1

9-Fe

b-21

2-M

ar-2

1

23-M

ar-2

1

13-A

pr-2

1

4-M

ay-2

1

25-M

ay-2

1

15-J

un-2

1

6-Ju

l-21

27-J

ul-2

1

17-A

ug-2

1

7-Se

p-21

28-S

ep-2

1

19-O

ct-2

1

9-N

ov-2

1

30-N

ov-2

1

21-D

ec-2

1

Domestic USA Canada Mexico Atlantic Latin (excl. Mexico) Pacific

7-Day Rolling Change (%) vs. Pre-Pandemic* in Aircraft Departures

* “Pre-pandemic” precedes March 1, 2020

13

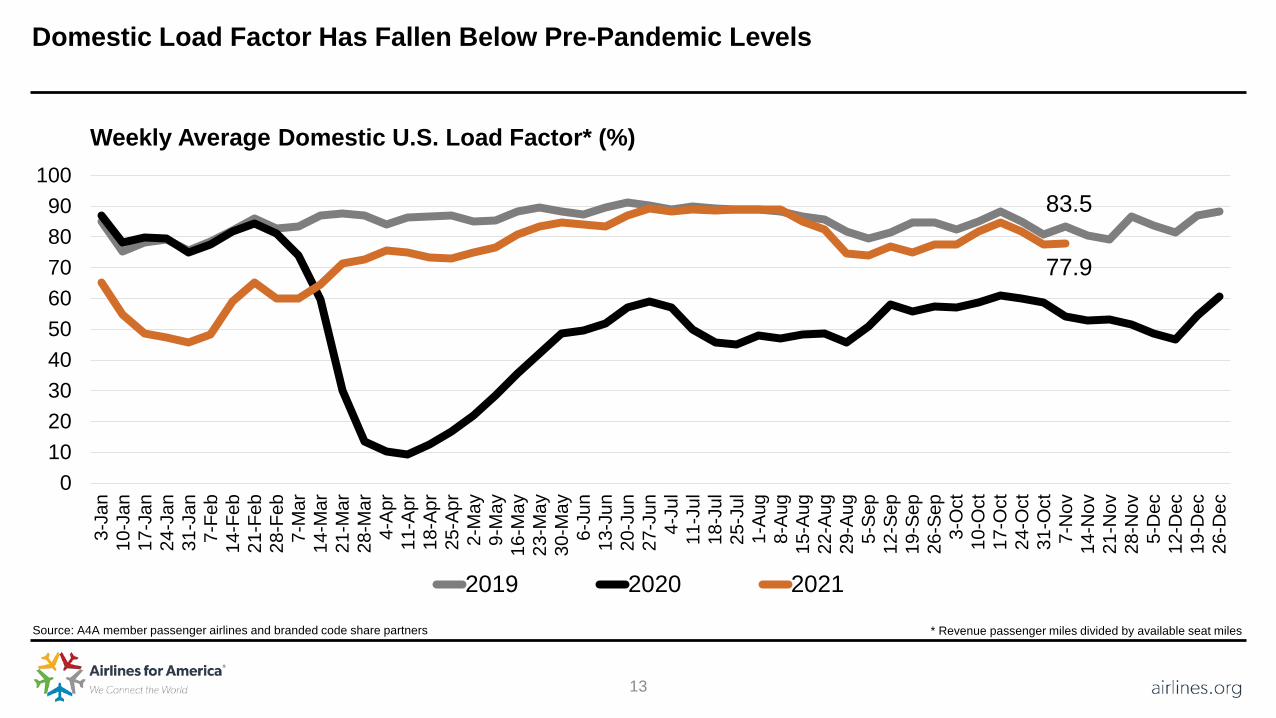

Domestic Load Factor Has Fallen Below Pre-Pandemic Levels

77.9

83.5

0102030405060708090

100

3-Ja

n10

-Jan

17-J

an24

-Jan

31-J

an7-

Feb

14-F

eb21

-Feb

28-F

eb7-

Mar

14-M

ar21

-Mar

28-M

ar4-

Apr

11-A

pr18

-Apr

25-A

pr2-

May

9-M

ay16

-May

23-M

ay30

-May

6-Ju

n13

-Jun

20-J

un27

-Jun

4-Ju

l11

-Jul

18-J

ul25

-Jul

1-Au

g8-

Aug

15-A

ug22

-Aug

29-A

ug5-

Sep

12-S

ep19

-Sep

26-S

ep3-

Oct

10-O

ct17

-Oct

24-O

ct31

-Oct

7-N

ov14

-Nov

21-N

ov28

-Nov

5-D

ec12

-Dec

19-D

ec26

-Dec

2019 2020 2021

Weekly Average Domestic U.S. Load Factor* (%)

Source: A4A member passenger airlines and branded code share partners * Revenue passenger miles divided by available seat miles

14

Average U.S.-Canada Onboard Volumes Notably Improved

Source: A4A member passenger airlines and branded code share partners * Onboard (“segment”) passengers

7-Day Moving Average Onboard Passengers* per Flight

0255075

100125150175200225250

7-Ja

n-19

4-Fe

b-19

4-M

ar-1

91-

Apr-1

929

-Apr

-19

27-M

ay-1

924

-Jun

-19

22-J

ul-1

919

-Aug

-19

16-S

ep-1

914

-Oct

-19

11-N

ov-1

99-

Dec

-19

6-Ja

n-20

3-Fe

b-20

2-M

ar-2

030

-Mar

-20

27-A

pr-2

025

-May

-20

22-J

un-2

020

-Jul

-20

17-A

ug-2

014

-Sep

-20

12-O

ct-2

09-

Nov

-20

7-D

ec-2

04-

Jan-

211-

Feb-

211-

Mar

-21

29-M

ar-2

126

-Apr

-21

24-M

ay-2

121

-Jun

-21

19-J

ul-2

116

-Aug

-21

13-S

ep-2

111

-Oct

-21

8-N

ov-2

16-

Dec

-21

3-Ja

n-22

31-J

an-2

228

-Feb

-22

28-M

ar-2

2

Domestic USA Canada Mexico Atlantic Latin (excl. Mexico) Pacific

15

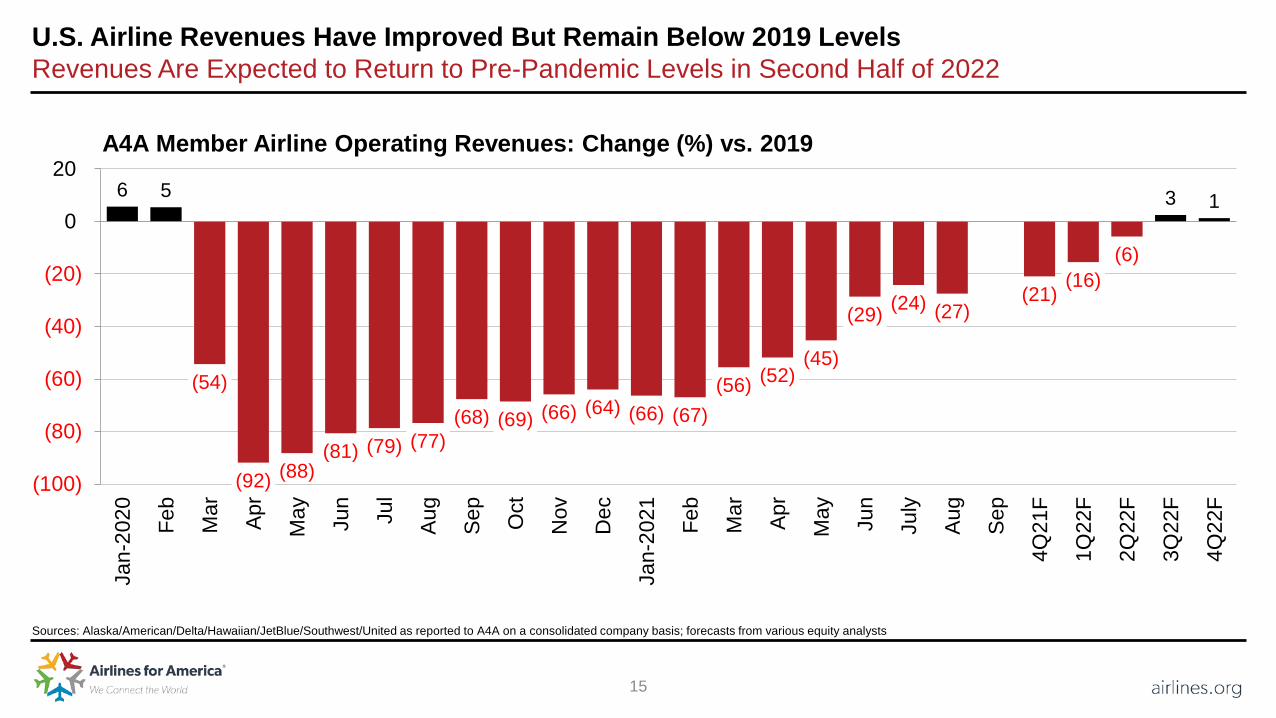

U.S. Airline Revenues Have Improved But Remain Below 2019 LevelsRevenues Are Expected to Return to Pre-Pandemic Levels in Second Half of 2022

Sources: Alaska/American/Delta/Hawaiian/JetBlue/Southwest/United as reported to A4A on a consolidated company basis; forecasts from various equity analysts

A4A Member Airline Operating Revenues: Change (%) vs. 2019

6 5

(54)

(92) (88)(81) (79) (77)

(68) (69) (66) (64) (66) (67)(56) (52)

(45)

(29) (24) (27)(21)

(16)(6)

3 1

(100)

(80)

(60)

(40)

(20)

0

20

Jan-

2020 Fe

b

Mar Ap

r

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan-

2021 Fe

b

Mar Ap

r

May Jun

July

Aug

Sep

4Q21

F

1Q22

F

2Q22

F

3Q22

F

4Q22

F

16

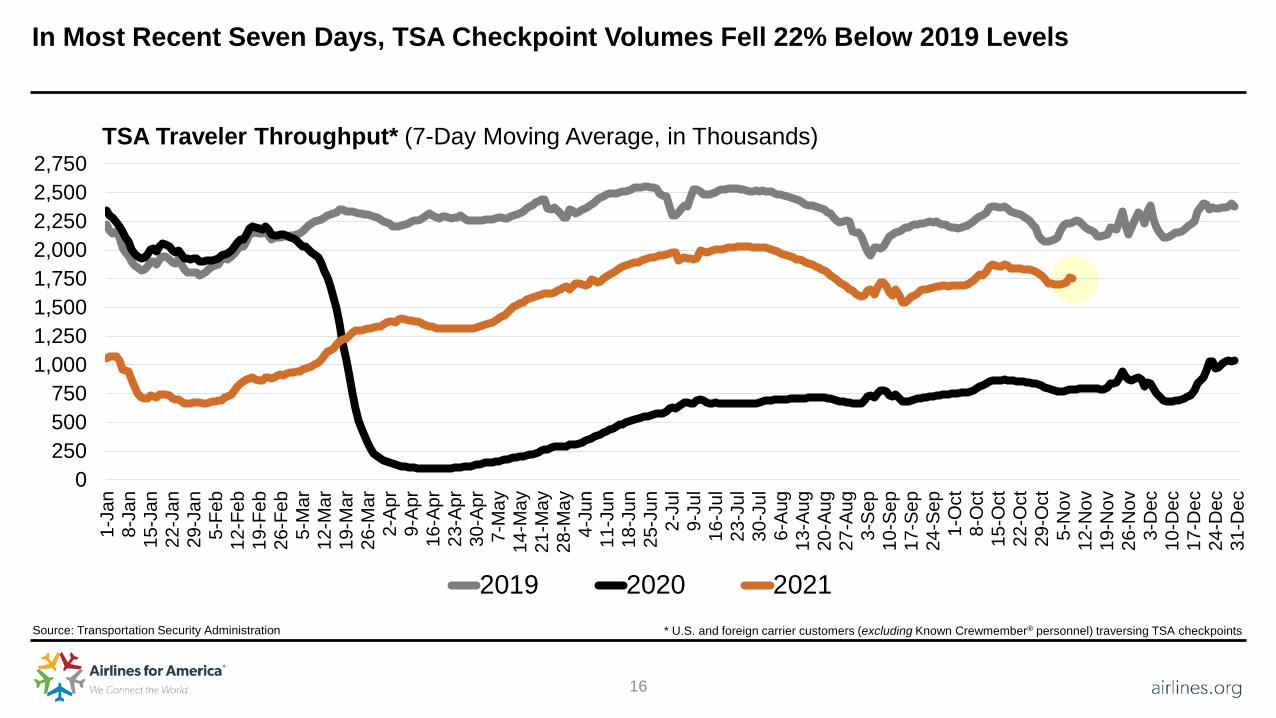

In Most Recent Seven Days, TSA Checkpoint Volumes Fell 22% Below 2019 Levels

Source: Transportation Security Administration

0250500750

1,0001,2501,5001,7502,0002,2502,5002,750

1-Ja

n8-

Jan

15-J

an22

-Jan

29-J

an5-

Feb

12-F

eb19

-Feb

26-F

eb5-

Mar

12-M

ar19

-Mar

26-M

ar2-

Apr

9-Ap

r16

-Apr

23-A

pr30

-Apr

7-M

ay14

-May

21-M

ay28

-May

4-Ju

n11

-Jun

18-J

un25

-Jun

2-Ju

l9-

Jul

16-J

ul23

-Jul

30-J

ul6-

Aug

13-A

ug20

-Aug

27-A

ug3-

Sep

10-S

ep17

-Sep

24-S

ep1-

Oct

8-O

ct15

-Oct

22-O

ct29

-Oct

5-N

ov12

-Nov

19-N

ov26

-Nov

3-D

ec10

-Dec

17-D

ec24

-Dec

31-D

ec

2019 2020 2021* U.S. and foreign carrier customers (excluding Known Crewmember® personnel) traversing TSA checkpoints

TSA Traveler Throughput* (7-Day Moving Average, in Thousands)

17

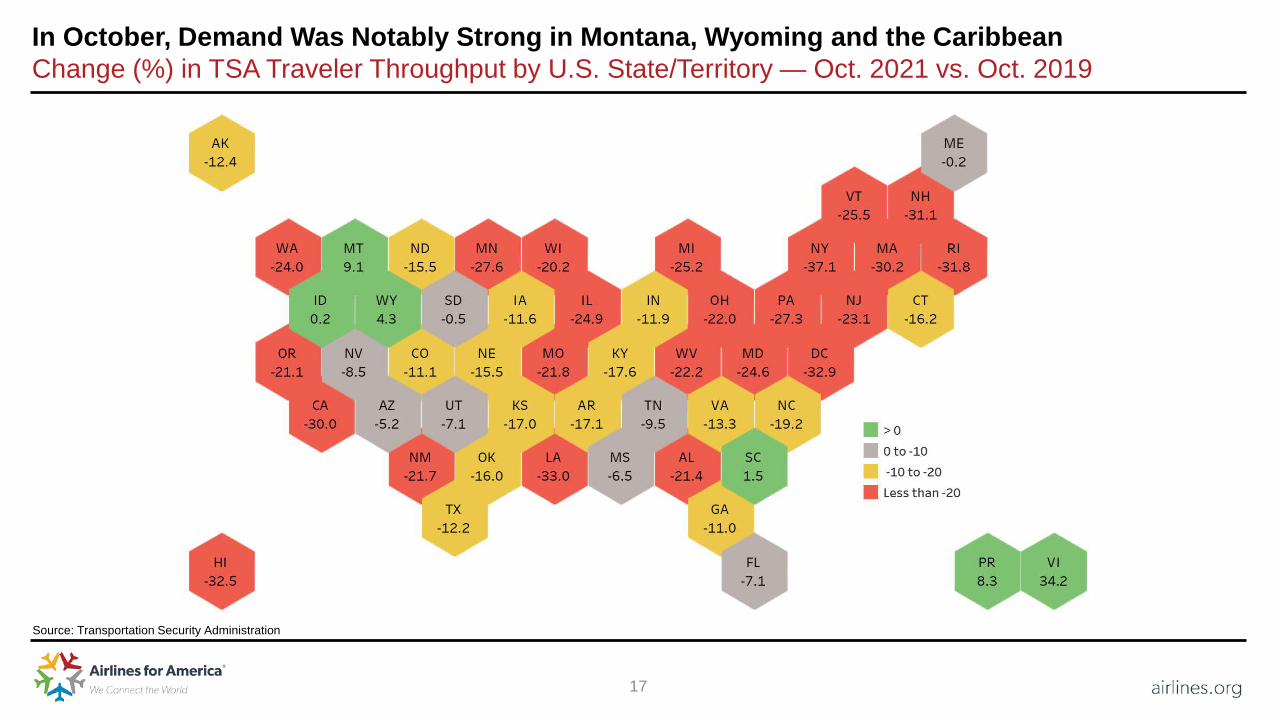

In October, Demand Was Notably Strong in Montana, Wyoming and the CaribbeanChange (%) in TSA Traveler Throughput by U.S. State/Territory — Oct. 2021 vs. Oct. 2019

Source: Transportation Security Administration

18

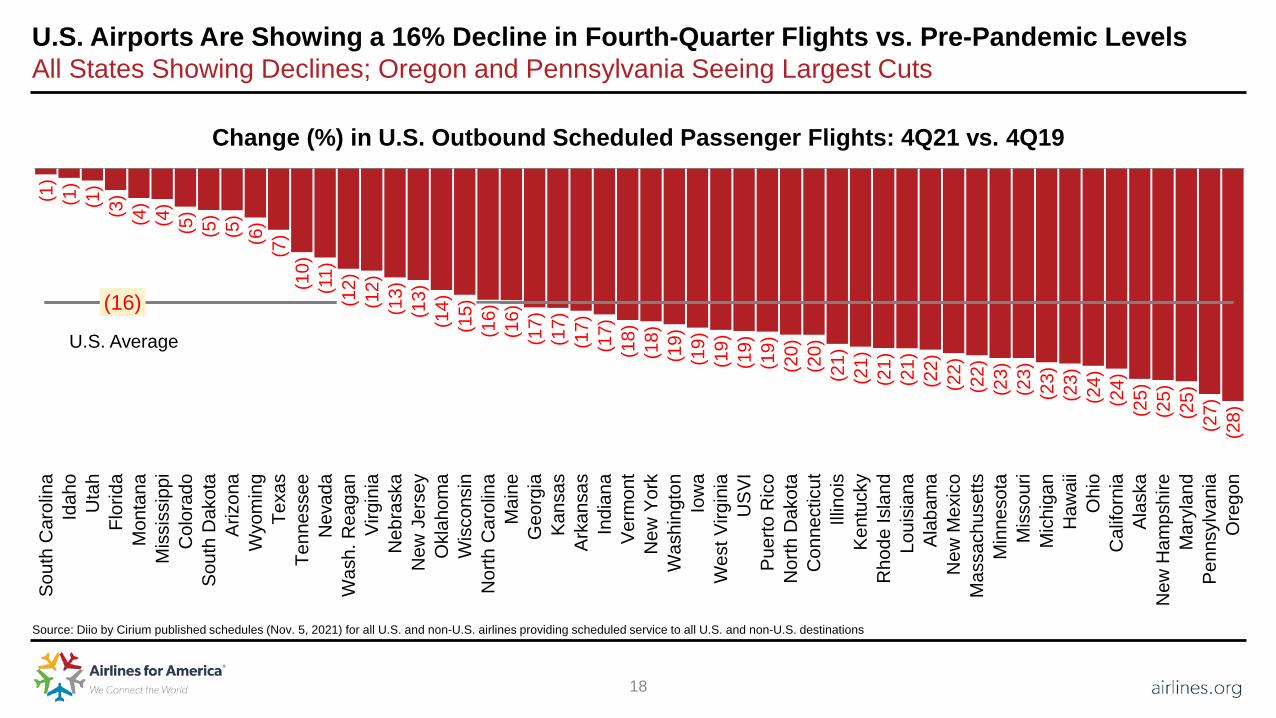

U.S. Airports Are Showing a 16% Decline in Fourth-Quarter Flights vs. Pre-Pandemic LevelsAll States Showing Declines; Oregon and Pennsylvania Seeing Largest Cuts

Source: Diio by Cirium published schedules (Nov. 5, 2021) for all U.S. and non-U.S. airlines providing scheduled service to all U.S. and non-U.S. destinations

(1)

(1)

(1)

(3)

(4)

(4)

(5)

(5)

(5)

(6)

(7)

(10)

(11)

(12)

(12)

(13)

(13)

(14)

(15)

(16)

(16)

(17)

(17)

(17)

(17)

(18)

(18)

(19)

(19)

(19)

(19)

(19)

(20)

(20)

(21)

(21)

(21)

(21)

(22)

(22)

(22)

(23)

(23)

(23)

(23)

(24)

(24)

(25)

(25)

(25)

(27)

(28)

(16)

Sout

h C

arol

ina

Idah

oU

tah

Flor

ida

Mon

tana

Mis

siss

ippi

Col

orad

oSo

uth

Dak

ota

Ariz

ona

Wyo

min

gTe

xas

Tenn

esse

eN

evad

aW

ash.

Rea

gan

Virg

inia

Neb

rask

aN

ew J

erse

yO

klah

oma

Wis

cons

inN

orth

Car

olin

aM

aine

Geo

rgia

Kans

asAr

kans

asIn

dian

aVe

rmon

tN

ew Y

ork

Was

hing

ton

Iow

aW

est V

irgin

iaU

SVI

Puer

to R

ico

Nor

th D

akot

aC

onne

ctic

utIll

inoi

sKe

ntuc

kyR

hode

Isla

ndLo

uisi

ana

Alab

ama

New

Mex

ico

Mas

sach

uset

tsM

inne

sota

Mis

sour

iM

ichi

gan

Haw

aii

Ohi

oC

alifo

rnia

Alas

kaN

ew H

amps

hire

Mar

ylan

dPe

nnsy

lvan

iaO

rego

n

U.S. Average

Change (%) in U.S. Outbound Scheduled Passenger Flights: 4Q21 vs. 4Q19

19

Only Three U.S. Airlines Are Deploying More Capacity in 4Q 2021 Than in 4Q 2019Allegiant and Spirit Growing the Fastest; United and Delta Are Down the Most

Source: Diio by Cirium published schedules (Nov. 5, 2021)

18.4 12.1

3.5

(4.2) (7.7) (12.1) (13.2)(19.8) (20.5) (22.4)

Change (%) in Systemwide Scheduled Available Seat Miles: 4Q21 vs. 4Q19

20

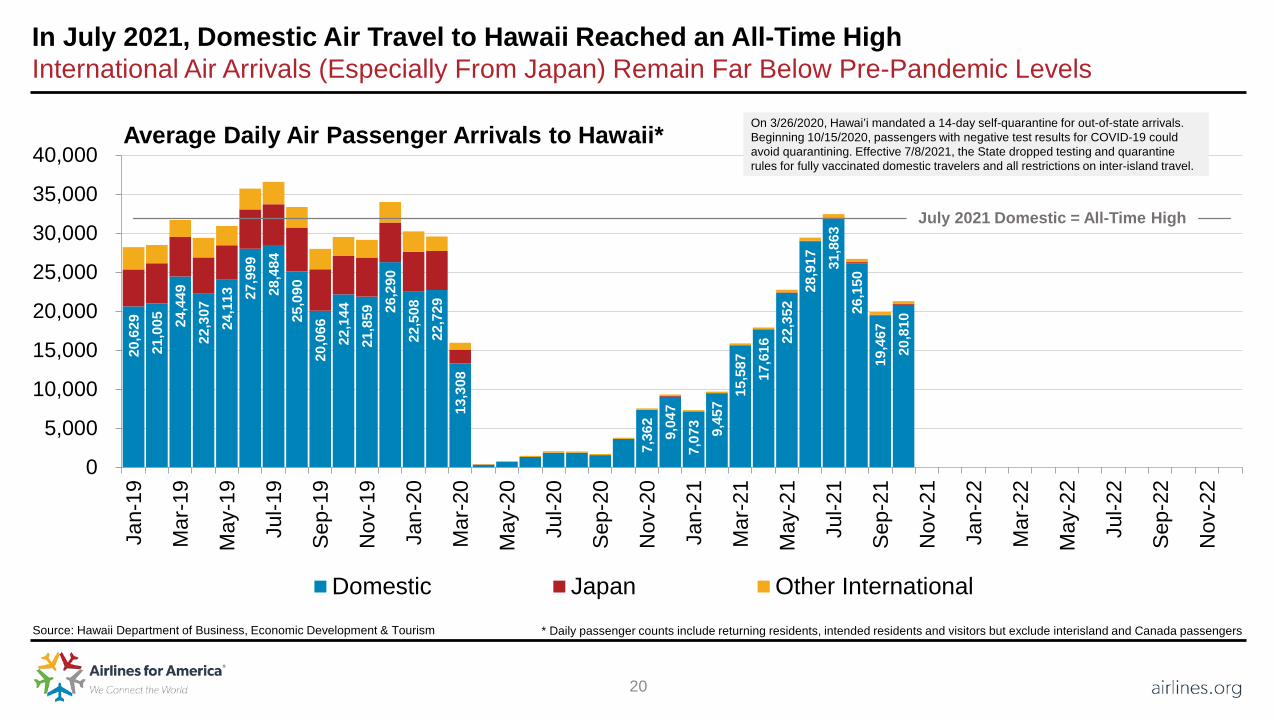

In July 2021, Domestic Air Travel to Hawaii Reached an All-Time HighInternational Air Arrivals (Especially From Japan) Remain Far Below Pre-Pandemic Levels

Source: Hawaii Department of Business, Economic Development & Tourism * Daily passenger counts include returning residents, intended residents and visitors but exclude interisland and Canada passengers

Average Daily Air Passenger Arrivals to Hawaii*20

,629

21

,005

24

,449

22

,307

24

,113

27

,999

28

,484

25

,090

20

,066

22

,144

21

,859

26,2

90

22,5

08

22,7

29

13,3

08

7,36

2 9,

047

7,07

3 9,45

7 15

,587

17

,616

22,3

52 28

,917

31

,863

26

,150

19

,467

20

,810

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000Ja

n-19

Mar

-19

May

-19

Jul-1

9

Sep-

19

Nov

-19

Jan-

20

Mar

-20

May

-20

Jul-2

0

Sep-

20

Nov

-20

Jan-

21

Mar

-21

May

-21

Jul-2

1

Sep-

21

Nov

-21

Jan-

22

Mar

-22

May

-22

Jul-2

2

Sep-

22

Nov

-22

Domestic Japan Other International

On 3/26/2020, Hawai’i mandated a 14-day self-quarantine for out-of-state arrivals. Beginning 10/15/2020, passengers with negative test results for COVID-19 could avoid quarantining. Effective 7/8/2021, the State dropped testing and quarantine rules for fully vaccinated domestic travelers and all restrictions on inter-island travel.

July 2021 Domestic = All-Time High

21

In October 2021, U.S.-International Air Travel* Fell 52% Below 2019 LevelsNon-U.S. Citizen Arrivals Trailed U.S. Citizen Departures by ~23 Percentage Points

(52.4)

(39.6)

(62.8)

(100)

(80)

(60)

(40)

(20)

0

20

Jan-

20

Mar

-20

May

-20

Jul-2

0

Sep-

20

Nov

-20

Jan-

21

Mar

-21

May

-21

Jul-2

1

Sep-

21

Nov

-21

Jan-

22

Mar

-22

May

-22

Jul-2

2

Sep-

22

Nov

-22

Non-U.S. Citizen Arrivals U.S. Citizen Departures Total

Change (%) vs. 2019 in Total* U.S.-International Air Passengers

Source: U.S. Department of Commerce National Travel and Tourism Office using DHS I-92 / APIS data * Gateway-to-gateway passengers on U.S. and foreign scheduled and charter airlines and general aviation

22

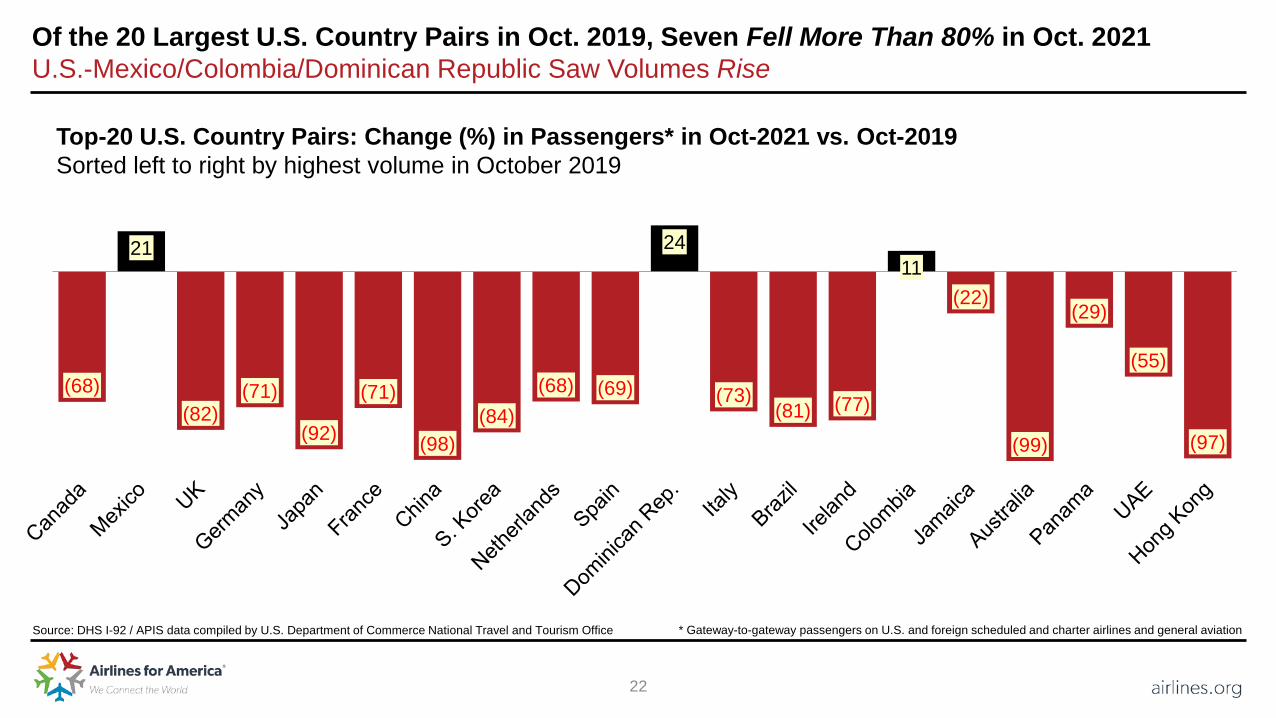

Of the 20 Largest U.S. Country Pairs in Oct. 2019, Seven Fell More Than 80% in Oct. 2021U.S.-Mexico/Colombia/Dominican Republic Saw Volumes Rise

Top-20 U.S. Country Pairs: Change (%) in Passengers* in Oct-2021 vs. Oct-2019Sorted left to right by highest volume in October 2019

(68)

21

(82)(71)

(92)

(71)

(98)(84)

(68) (69)

24

(73)(81) (77)

11 (22)

(99)

(29)

(55)

(97)

* Gateway-to-gateway passengers on U.S. and foreign scheduled and charter airlines and general aviationSource: DHS I-92 / APIS data compiled by U.S. Department of Commerce National Travel and Tourism Office

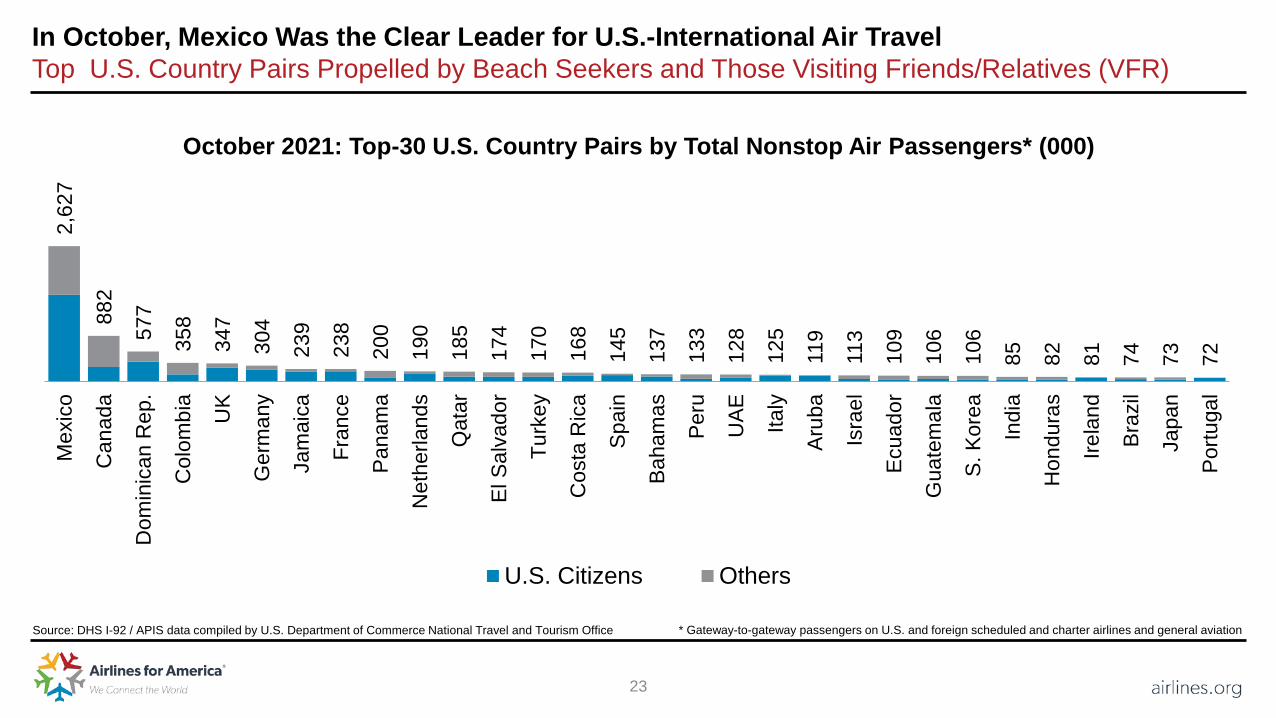

23

In October, Mexico Was the Clear Leader for U.S.-International Air TravelTop U.S. Country Pairs Propelled by Beach Seekers and Those Visiting Friends/Relatives (VFR)

October 2021: Top-30 U.S. Country Pairs by Total Nonstop Air Passengers* (000)

2,62

7

882

577

358

347

304

239

238

200

190

185

174

170

168

145

137

133

128

125

119

113

109

106

106

85

82

81

74

73

72

Mex

ico

Can

ada

Dom

inic

an R

ep.

Col

ombi

a

UK

Ger

man

y

Jam

aica

Fran

ce

Pana

ma

Net

herla

nds

Qat

ar

El S

alva

dor

Turk

ey

Cos

ta R

ica

Spai

n

Baha

mas

Peru

UAE Ita

ly

Arub

a

Isra

el

Ecua

dor

Gua

tem

ala

S. K

orea

Indi

a

Hon

dura

s

Irela

nd

Braz

il

Japa

n

Portu

gal

U.S. Citizens Others

Source: DHS I-92 / APIS data compiled by U.S. Department of Commerce National Travel and Tourism Office * Gateway-to-gateway passengers on U.S. and foreign scheduled and charter airlines and general aviation

24

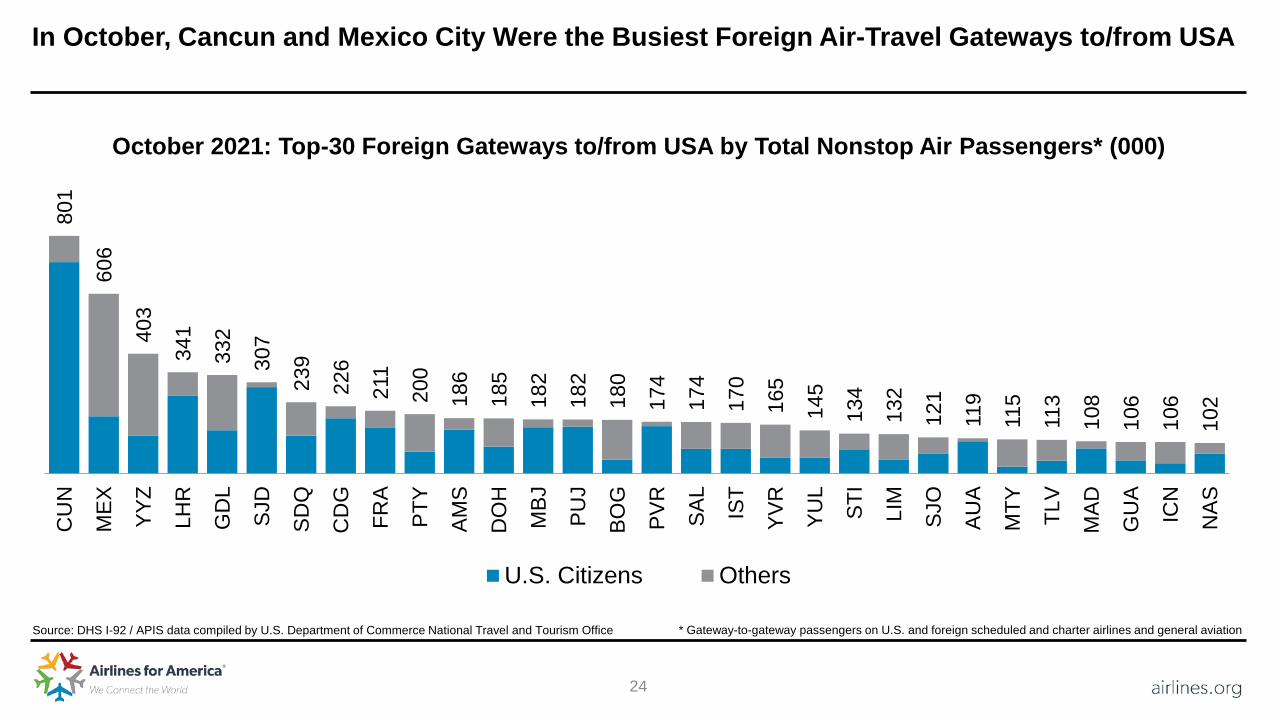

In October, Cancun and Mexico City Were the Busiest Foreign Air-Travel Gateways to/from USA

October 2021: Top-30 Foreign Gateways to/from USA by Total Nonstop Air Passengers* (000)

801

606

403

341

332

307

239

226

211

200

186

185

182

182

180

174

174

170

165

145

134

132

121

119

115

113

108

106

106

102

CU

N

MEX YY

Z

LHR

GD

L

SJD

SDQ

CD

G

FRA

PTY

AMS

DO

H

MBJ

PUJ

BOG

PVR

SAL

IST

YVR

YUL

STI

LIM

SJO

AUA

MTY TL

V

MAD

GU

A

ICN

NAS

U.S. Citizens Others

* Gateway-to-gateway passengers on U.S. and foreign scheduled and charter airlines and general aviationSource: DHS I-92 / APIS data compiled by U.S. Department of Commerce National Travel and Tourism Office

25

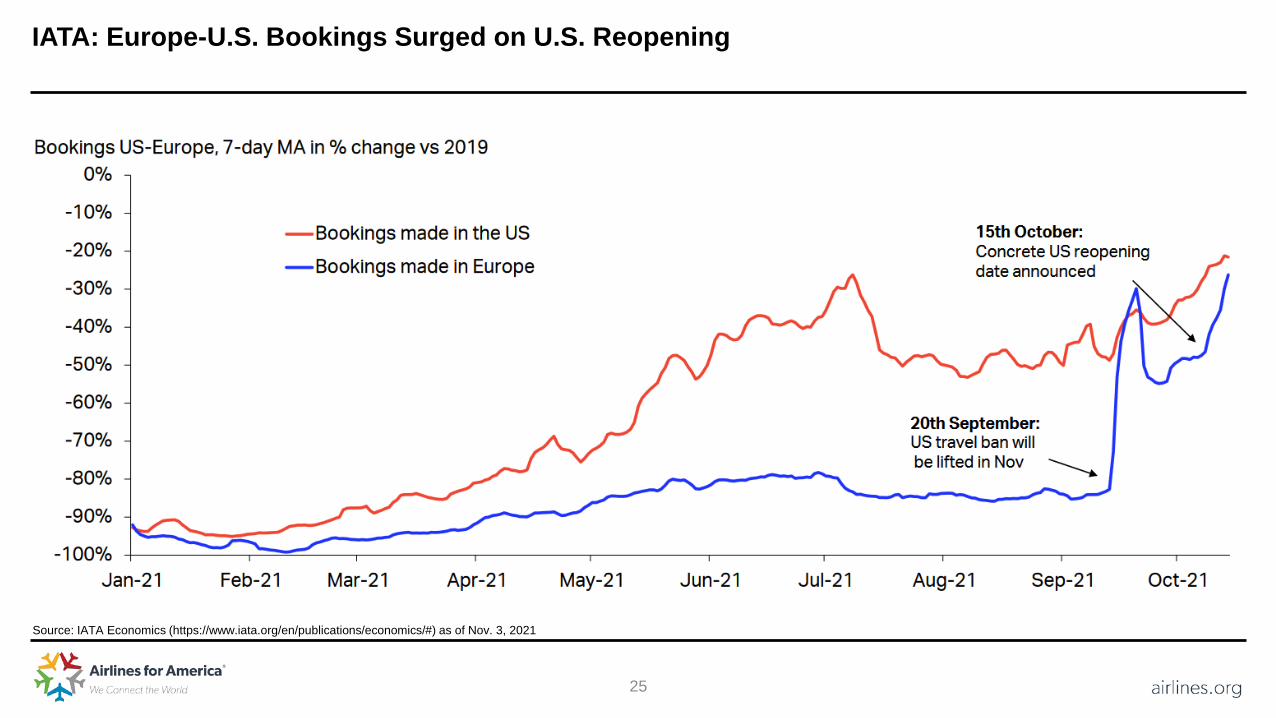

IATA: Europe-U.S. Bookings Surged on U.S. Reopening

Source: IATA Economics (https://www.iata.org/en/publications/economics/#) as of Nov. 3, 2021

26

In Most Recent Week, Average Airfares on Tickets Sold Were 13% Below Pre-Pandemic LevelsFares Down From 2019 Due Primarily to Scarcity of Corporate and Long-Haul International Travel

(13)

(52)

(100)(90)(80)(70)(60)(50)(40)(30)(20)(10)

0

7-Ju

n-20

21-J

un-2

05-

Jul-2

019

-Jul

-20

2-Au

g-20

16-A

ug-2

030

-Aug

-20

13-S

ep-2

027

-Sep

-20

11-O

ct-2

025

-Oct

-20

8-N

ov-2

022

-Nov

-20

6-D

ec-2

020

-Dec

-20

10-J

an-2

124

-Jan

-21

7-Fe

b-21

21-F

eb-2

17-

Mar

-21

21-M

ar-2

14-

Apr-2

118

-Apr

-21

2-M

ay-2

116

-May

-21

30-M

ay-2

113

-Jun

-21

27-J

un-2

111

-Jul

-21

25-J

ul-2

18-

Aug-

2122

-Aug

-21

5-Se

p-21

19-S

ep-2

13-

Oct

-21

17-O

ct-2

131

-Oct

-21

14-N

ov-2

128

-Nov

-21

12-D

ec-2

126

-Dec

-21

Passengers Ticketed (All) Average Fare Passengers Ticketed via Corporate Agency

* Net tickets and fares (gross sales minus refunds) sold in the United States for future travel to/from U.S. airports

Change (%) vs. 2019 in Weekly Ticket Sales*

Source: A4A analysis of data from Airlines Reporting Corporation (ARC)

27

Government Data Shows Average Airfares Remain Lower Than Pre-Pandemic Levels

Source: Bureau of Labor Statistics (CPI series CUSR0000SETG01) and DOT Data Bank 1B (all carriers/cabins/fare basis codes)

$400 $406$418 $421 $423 $419

$387$370

$354 $351$332

$324$340

$356 $364$373 $370

$345$336 $330 $333

$316

$225$200

$250

$300

$350

$400

$450

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Real ($2021) FareNominal Fare

Average 2Q Domestic Round-Trip AirfareSecond quarter of each year

278.

873

314.

655

312.

078

316.

426

306.

111

287.

452

275.

578

267.

277

266.

300

271.

396

203.

594

205.

194

0

50

100

150

200

250

300

350

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

U.S. CPI for Airline Fares (Index: 1982-84 = 100)U.S. city average for Sept. of each year, seasonally adjusted

Down 24% from 2019 and 33% from 2014 Down 36% from 2019 and 47% from 2014

2019

Inde

x: 1

982-

84 =

100

28

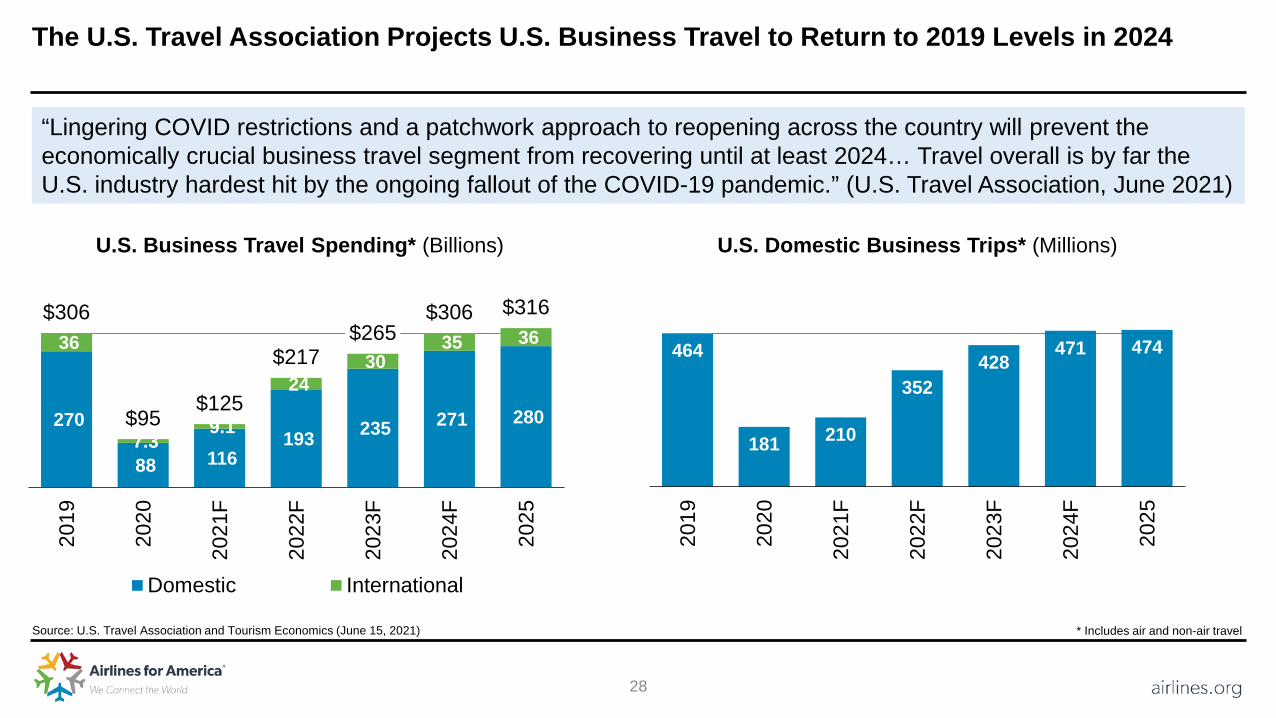

The U.S. Travel Association Projects U.S. Business Travel to Return to 2019 Levels in 2024

Source: U.S. Travel Association and Tourism Economics (June 15, 2021)

270

88 116 193 235 271 280

36

7.3 9.1

24 30

35 36 $306

$95$125

$217$265

$306 $316

2019

2020

2021

F

2022

F

2023

F

2024

F

2025

Domestic International

U.S. Business Travel Spending* (Billions)

“Lingering COVID restrictions and a patchwork approach to reopening across the country will prevent the economically crucial business travel segment from recovering until at least 2024… Travel overall is by far the U.S. industry hardest hit by the ongoing fallout of the COVID-19 pandemic.” (U.S. Travel Association, June 2021)

* Includes air and non-air travel

464

181 210

352428

471 474

2019

2020

2021

F

2022

F

2023

F

2024

F

2025

U.S. Domestic Business Trips* (Millions)

29

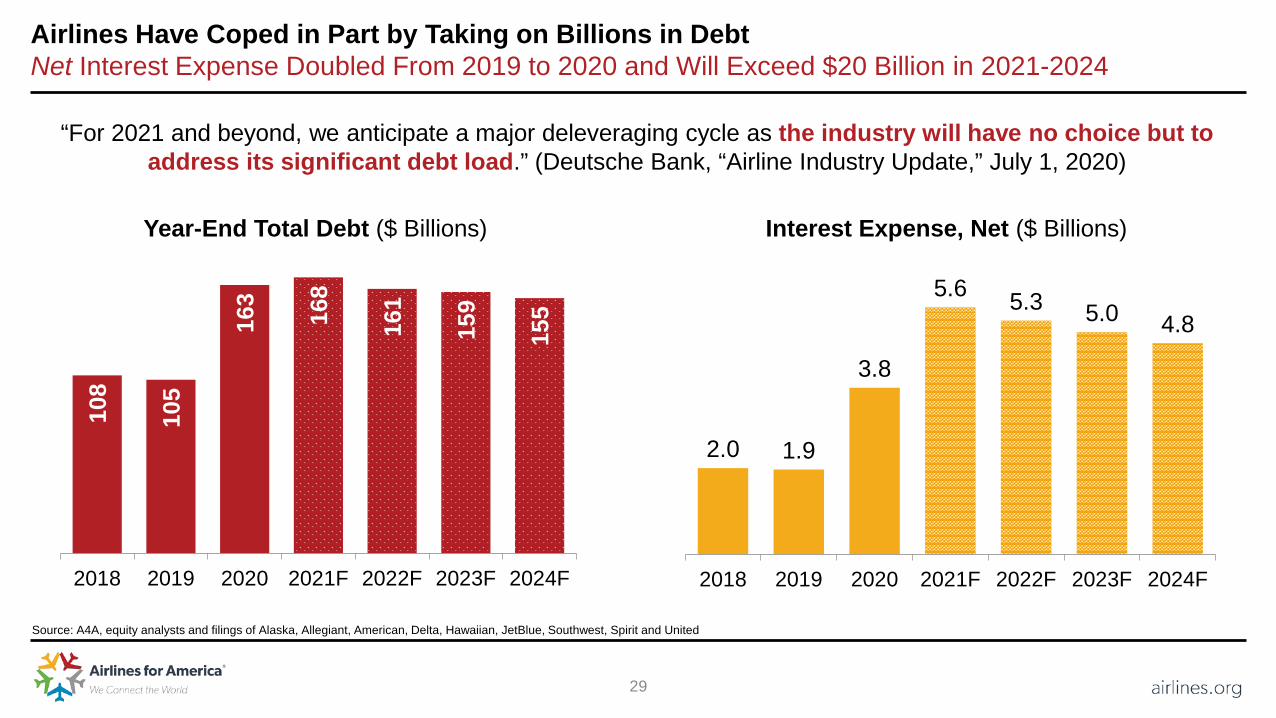

Airlines Have Coped in Part by Taking on Billions in DebtNet Interest Expense Doubled From 2019 to 2020 and Will Exceed $20 Billion in 2021-2024

108

105

163

168

161

159

155

2018 2019 2020 2021F 2022F 2023F 2024F

Year-End Total Debt ($ Billions)

2.0 1.9

3.8

5.6 5.3 5.0 4.8

2018 2019 2020 2021F 2022F 2023F 2024F

Interest Expense, Net ($ Billions)

“For 2021 and beyond, we anticipate a major deleveraging cycle as the industry will have no choice but to address its significant debt load.” (Deutsche Bank, “Airline Industry Update,” July 1, 2020)

Source: A4A, equity analysts and filings of Alaska, Allegiant, American, Delta, Hawaiian, JetBlue, Southwest, Spirit and United

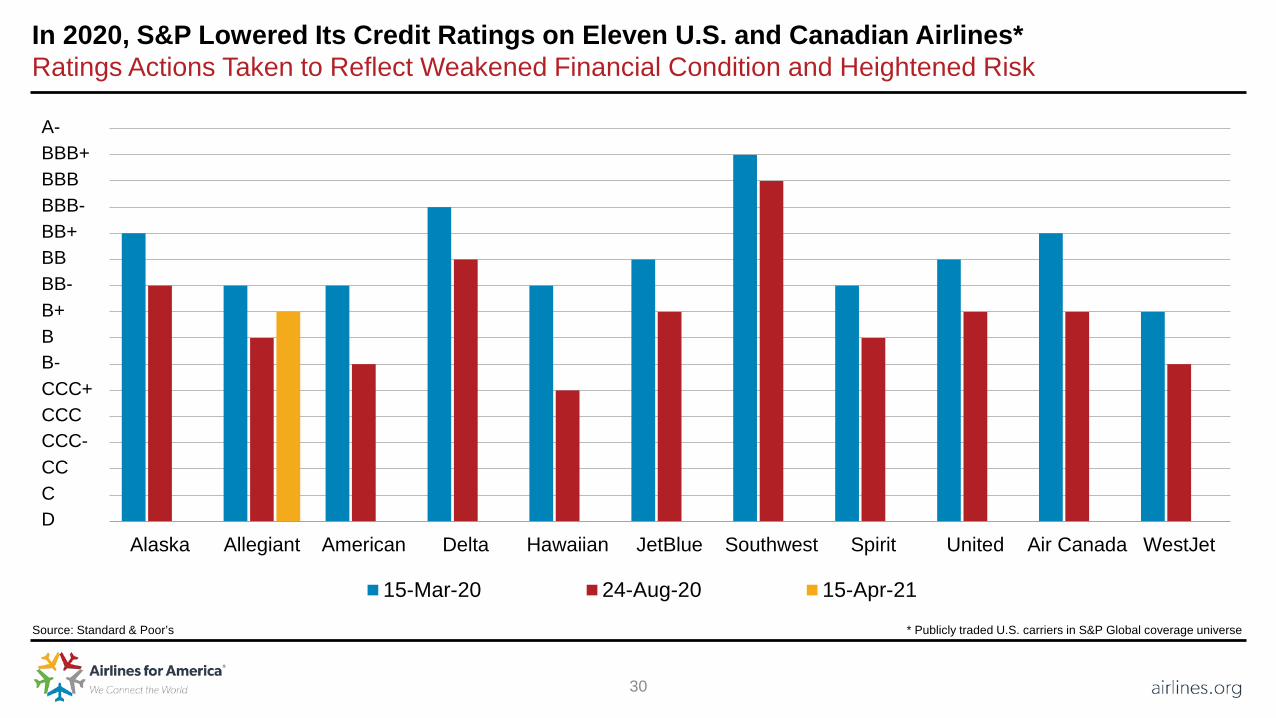

30

In 2020, S&P Lowered Its Credit Ratings on Eleven U.S. and Canadian Airlines*Ratings Actions Taken to Reflect Weakened Financial Condition and Heightened Risk

Source: Standard & Poor’s

Alaska Allegiant American Delta Hawaiian JetBlue Southwest Spirit United Air Canada WestJet

15-Mar-20 24-Aug-20 15-Apr-21

BBB+BBBBBB-BB+BBBB-B+BB-CCC+CCCCCC-CCCD

* Publicly traded U.S. carriers in S&P Global coverage universe

A-

31

Ridership on U.S. Intercity Rail Remains Far Below Pre-Pandemic LevelsJuly 2021 Ridership Fell 39% Below July 2019

Sources: Bureau of Transportation Statistics

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2019 2020 2021

Monthly Ridership (000s) on U.S. Intercity Passenger Rail*

* Passengers transported on Amtrak and Alaska Railroad operations

32

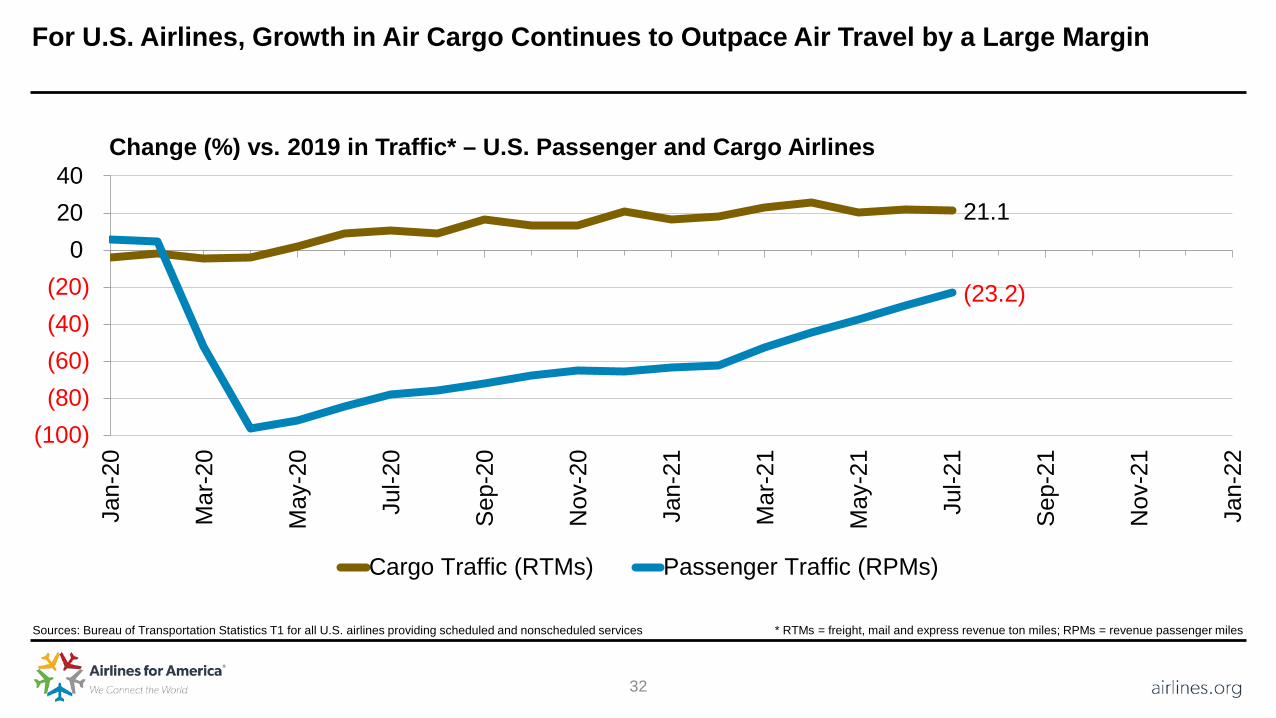

For U.S. Airlines, Growth in Air Cargo Continues to Outpace Air Travel by a Large Margin

Sources: Bureau of Transportation Statistics T1 for all U.S. airlines providing scheduled and nonscheduled services

21.1

(23.2)

(100)(80)(60)(40)(20)

02040

Jan-

20

Mar

-20

May

-20

Jul-2

0

Sep-

20

Nov

-20

Jan-

21

Mar

-21

May

-21

Jul-2

1

Sep-

21

Nov

-21

Jan-

22

Cargo Traffic (RTMs) Passenger Traffic (RPMs)

Change (%) vs. 2019 in Traffic* – U.S. Passenger and Cargo Airlines

* RTMs = freight, mail and express revenue ton miles; RPMs = revenue passenger miles

33

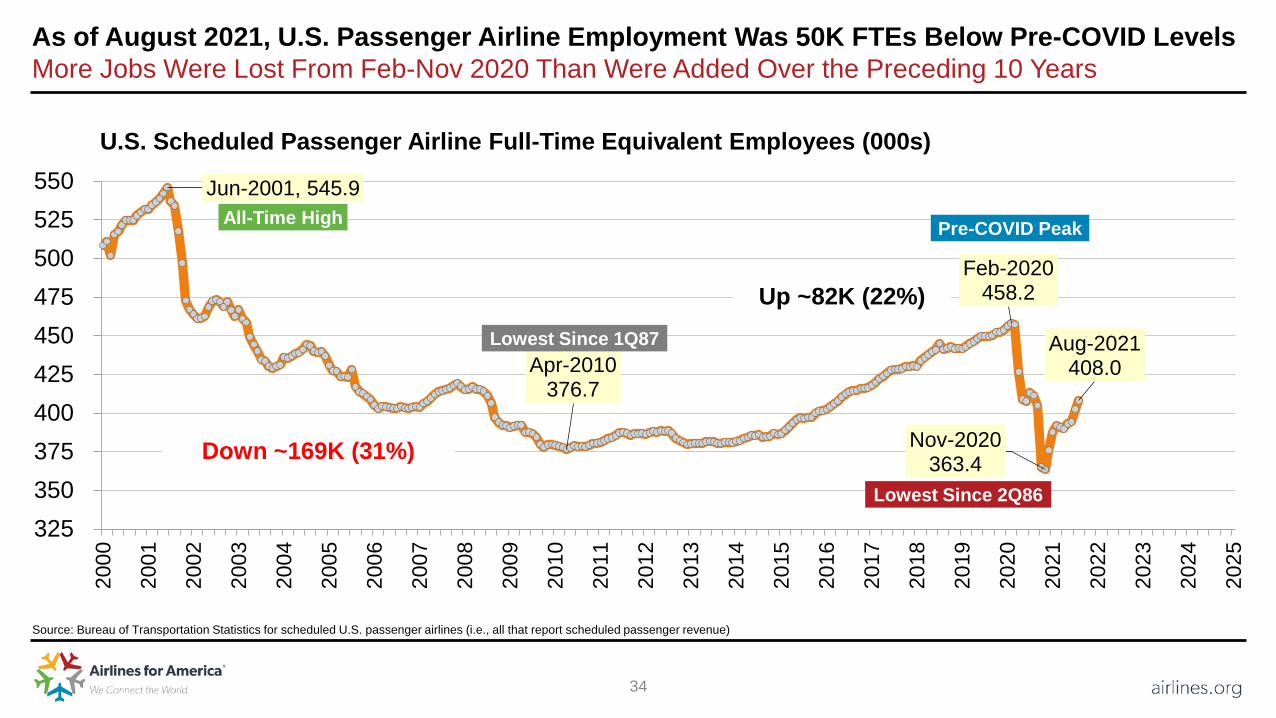

The Pandemic Has Taken a Material Toll on U.S. Airline EmploymentVoluntary Reductions, Retirements, Job Changes, Employer Shutdowns and Other Factors at Play

Source: Bureau of Transportation Statistics based on payroll near the 15th of the month

Carrier Universe Scheduled U.S. Passenger Airlines

All U.S. Passengerand Cargo Airlines

Measure FTEs* (000) Headcount (000)

All-Time High Jun-2001: 545.9 May-2001: 760.8

Post-2000 Low Point Apr-2010: 376.7 Apr-2010: 562.3

Pre-COVID Peak Feb-2020: 458.2 Feb-2020: 753.4

Latest Available Data Point Aug-2021: 408.0 Aug-2021: 719.0

* Full-time equivalents (FTE) = full-time workers plus 0.5 * part-time workers

34

As of August 2021, U.S. Passenger Airline Employment Was 50K FTEs Below Pre-COVID LevelsMore Jobs Were Lost From Feb-Nov 2020 Than Were Added Over the Preceding 10 Years

Source: Bureau of Transportation Statistics for scheduled U.S. passenger airlines (i.e., all that report scheduled passenger revenue)

Jun-2001, 545.9

Apr-2010376.7

Feb-2020458.2

Nov-2020363.4

Aug-2021408.0

325350375400425450475500525550

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

U.S. Scheduled Passenger Airline Full-Time Equivalent Employees (000s)

All-Time High

Lowest Since 1Q87

Pre-COVID Peak

Down ~169K (31%)

Up ~82K (22%)

Lowest Since 2Q86

35

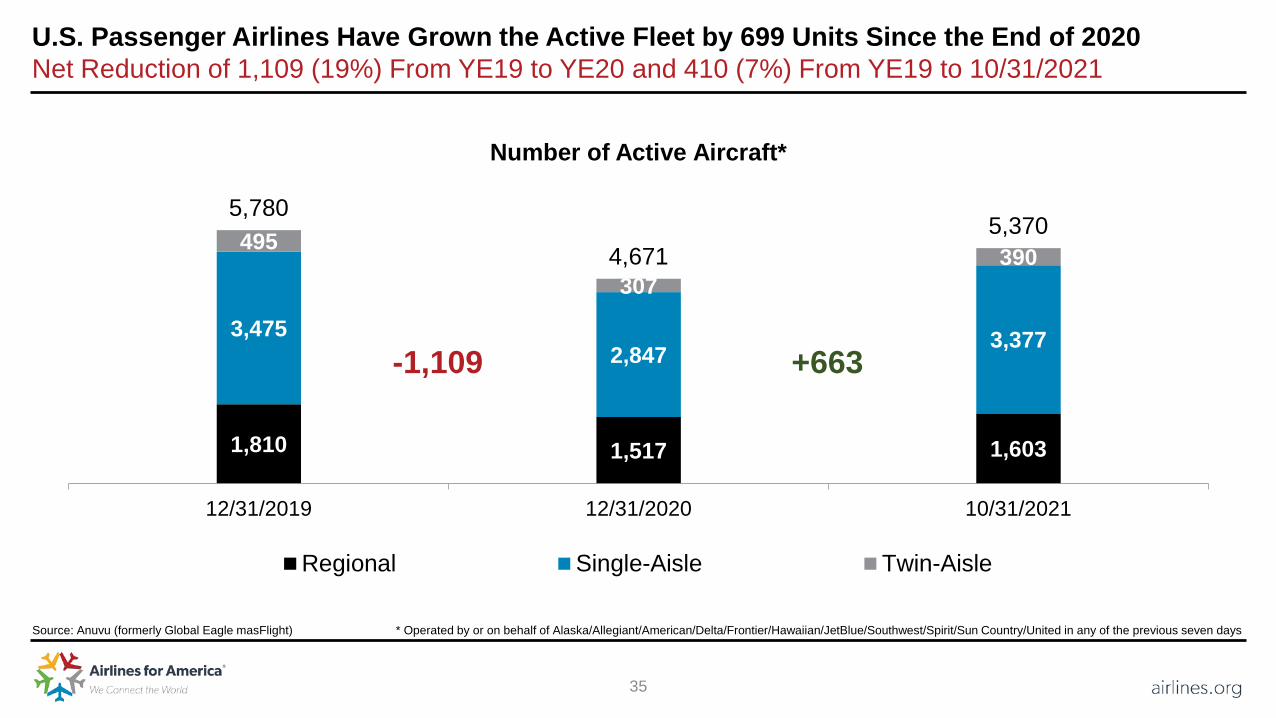

U.S. Passenger Airlines Have Grown the Active Fleet by 699 Units Since the End of 2020Net Reduction of 1,109 (19%) From YE19 to YE20 and 410 (7%) From YE19 to 10/31/2021

Number of Active Aircraft*

1,810 1,517 1,603

3,475 2,847 3,377

495

307 390

5,780

4,671 5,370

12/31/2019 12/31/2020 10/31/2021

Regional Single-Aisle Twin-Aisle

Source: Anuvu (formerly Global Eagle masFlight) * Operated by or on behalf of Alaska/Allegiant/American/Delta/Frontier/Hawaiian/JetBlue/Southwest/Spirit/Sun Country/United in any of the previous seven days

-1,109 +663

36

The Timing of a Return to 2019 Passenger Volumes Depends in Large Part on Business TravelAnother Open Question Is the Degree to Which Leisure and VFR Traffic Remain Robust in 2022-2023

(70)

(60)

(50)

(40)

(30)

(20)

(10)

0

10

20

2019A 2020A 2021F 2022F 2023F 2024F

Pessimistic OptimisticSource: A4A and various airline equity analysts

U.S. Airline Passenger Traffic Change (%) vs. 2019

2019 Passenger Volumes

Note: A = actual; F= forecast

37

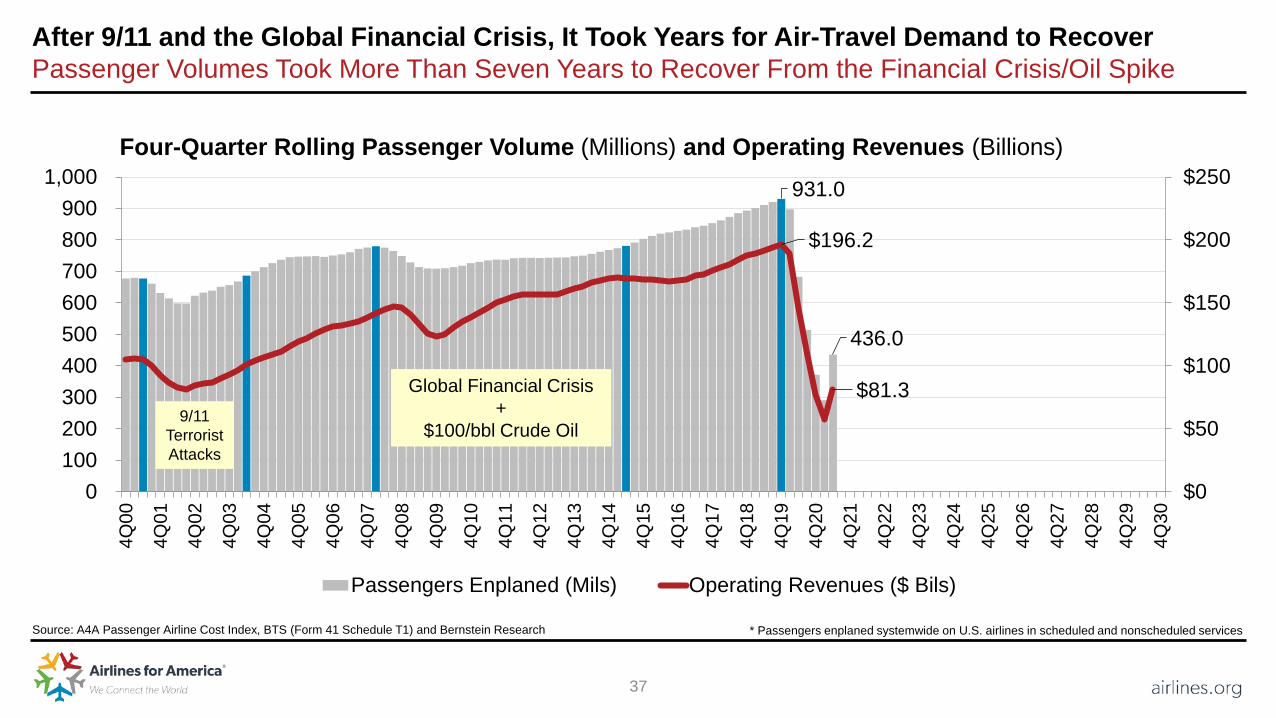

After 9/11 and the Global Financial Crisis, It Took Years for Air-Travel Demand to RecoverPassenger Volumes Took More Than Seven Years to Recover From the Financial Crisis/Oil Spike

Source: A4A Passenger Airline Cost Index, BTS (Form 41 Schedule T1) and Bernstein Research

Four-Quarter Rolling Passenger Volume (Millions) and Operating Revenues (Billions)

931.0

436.0

$196.2

$81.3

$0

$50

$100

$150

$200

$250

0100200300400500600700800900

1,000

4Q00

4Q01

4Q02

4Q03

4Q04

4Q05

4Q06

4Q07

4Q08

4Q09

4Q10

4Q11

4Q12

4Q13

4Q14

4Q15

4Q16

4Q17

4Q18

4Q19

4Q20

4Q21

4Q22

4Q23

4Q24

4Q25

4Q26

4Q27

4Q28

4Q29

4Q30

Passengers Enplaned (Mils) Operating Revenues ($ Bils)

* Passengers enplaned systemwide on U.S. airlines in scheduled and nonscheduled services

9/11 Terrorist Attacks

Global Financial Crisis+

$100/bbl Crude Oil

38

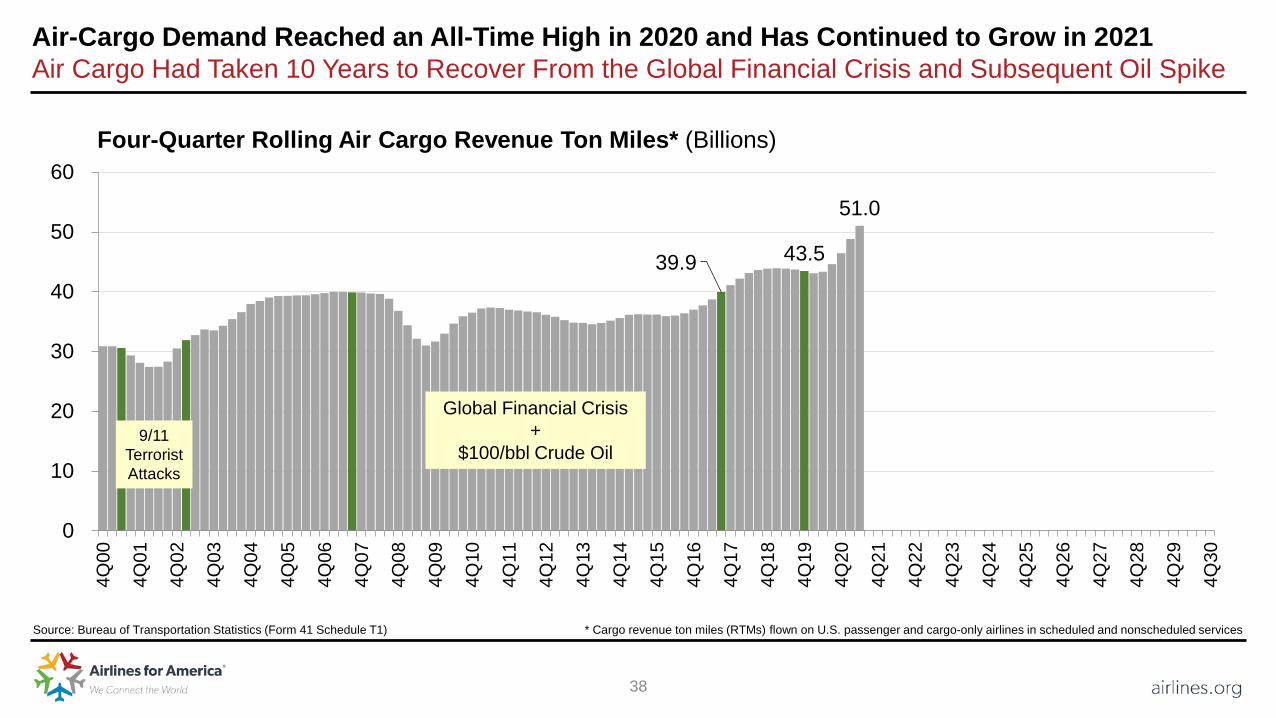

Air-Cargo Demand Reached an All-Time High in 2020 and Has Continued to Grow in 2021Air Cargo Had Taken 10 Years to Recover From the Global Financial Crisis and Subsequent Oil Spike

Source: Bureau of Transportation Statistics (Form 41 Schedule T1)

Four-Quarter Rolling Air Cargo Revenue Ton Miles* (Billions)

39.9 43.5

51.0

0

10

20

30

40

50

60

4Q00

4Q01

4Q02

4Q03

4Q04

4Q05

4Q06

4Q07

4Q08

4Q09

4Q10

4Q11

4Q12

4Q13

4Q14

4Q15

4Q16

4Q17

4Q18

4Q19

4Q20

4Q21

4Q22

4Q23

4Q24

4Q25

4Q26

4Q27

4Q28

4Q29

4Q30

* Cargo revenue ton miles (RTMs) flown on U.S. passenger and cargo-only airlines in scheduled and nonscheduled services

9/11 Terrorist Attacks

Global Financial Crisis+

$100/bbl Crude Oil

39

Pandemic-Driven Technology Acceptance, Digital Competence and Enhanced Cleaning Protocols Will Endure, and Airlines and Airports Will Continue to Invest Accordingly

Source: McKinsey & Company interview with Massachusetts Port Authority CEO Lisa Wieland (Nov. 20, 2020)

“COVID-19 has brought about an acceleration of digital competency across demographic cohorts. We have a lot of different people who fly through the airport. We are constantly thinking about the experience we present to them. And if people have become more technology savvy, more digitally competent, that means we can accelerate and roll out the contactless passenger journey across many platforms—and there will be an acceptance of and a desire for them.”

“Airports and airplanes are cleaner than they’ve ever been and will continue to be that way because it’s important for restoring confidence in air travel. We expect the new hygiene and enhanced-cleaning protocols we’ve implemented to continue. Passengers can expect that from airports and airlines going forward.”

40