emerging hotspots for commercial vehicles in africa

TRANSCRIPT

Emerging Hotspots for Commercial Vehicles in Emerging Hotspots for Commercial Vehicles in AfricaAfrica

Key Trends in SubKey Trends in Sub--Saharan AfricaSaharan Africa

Derrick Derrick ChikangaChikanga, Research Analyst, Research Analyst

Automotive and TransportationAutomotive and TransportationAutomotive and TransportationAutomotive and Transportation

Africa Africa

© 2012 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

Functional Expertise

� 6 years of research and consulting expertise, which include more than 26 research and 21 consulting projects.

Particular expertise in:

- Research, Data Collection and Analysis

- Report Writing and PowerPoint Presentation

- Contacts Establishment and Project Management

Industry Expertise

� Experience base covering broad range of sectors, leveraging long-standing working relationships with leading industry

participants’ Senior Executives

- Electronic and Security Systems

- Automotive & Transportation Industry

- Water and Wastewater Treatment Technologies; Waste Management and Waste-to-energy

- Renewable Energy Technologies

- Air Pollution Control Technologies; HVAC and Lighting Equipment; Facilities Management

Derrick ChikangaResearch Analyst

Frost & SullivanSouth Africa

Derrick Chikanga

2

- Air Pollution Control Technologies; HVAC and Lighting Equipment; Facilities Management

- Energy Efficiency Technology Analysis (Lighting, HVAC, BMS)

- Sub-Saharan Africa Infrastructure Development Analysis (Transportation, Energy and Power, Telecommunication,

Social and Water Infrastructure)

What I bring to the Team

� Solid Research and Analytical Skills

� Client Relationship Management

� Industry Experience; Broad Network of Industry Contacts

Career Highlights

� Extensive expertise in the Southern African Environmental and Infrastructure Sectors

Education

� MCom Finance (Financial Management) from University of Cape Town, Cape Town, South Africa (On-going)

� BCom (Hons) Financial Analysis & Portfolio Management from University of Cape Town, Cape Town, South Africa

� BCom (Hons) Economics from University of Cape Town, Cape Town, South Africa

� BCom Economics & Finance, Cape Town, South Africa

South AfricaCape Town

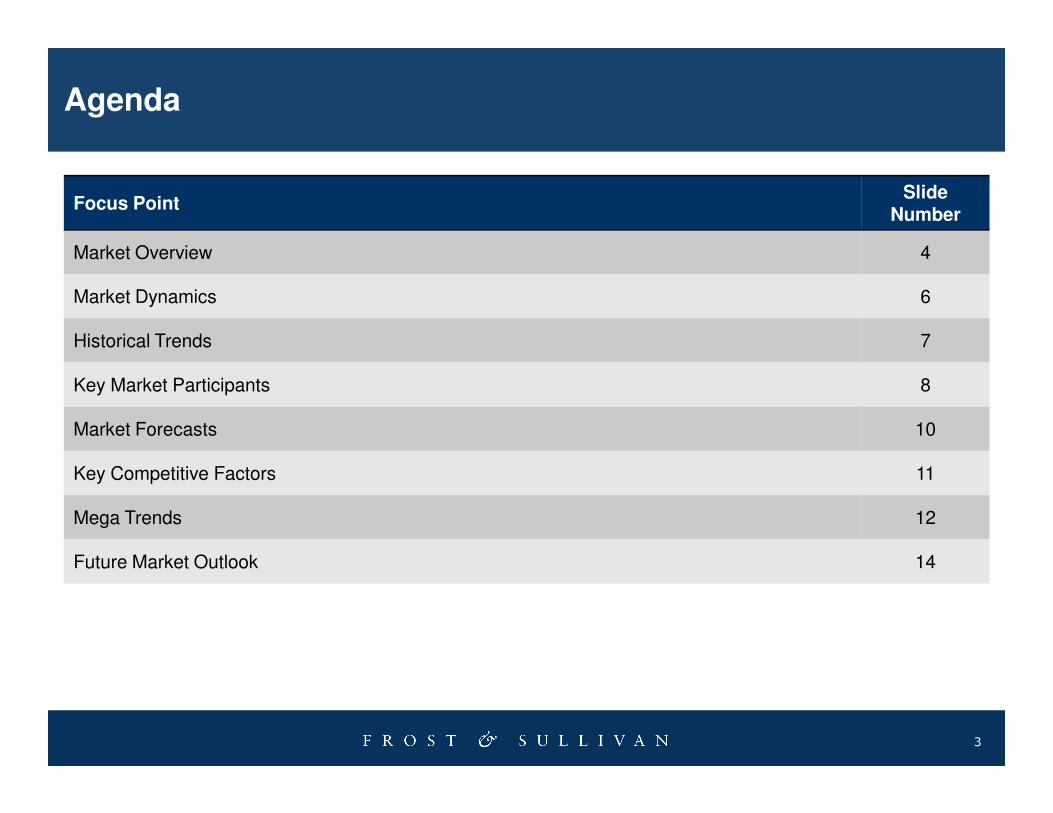

Focus PointSlide

Number

Market Overview 4

Market Dynamics 6

Historical Trends 7

Key Market Participants 8

Agenda

3

Market Forecasts 10

Key Competitive Factors 11

Mega Trends 12

Future Market Outlook 14

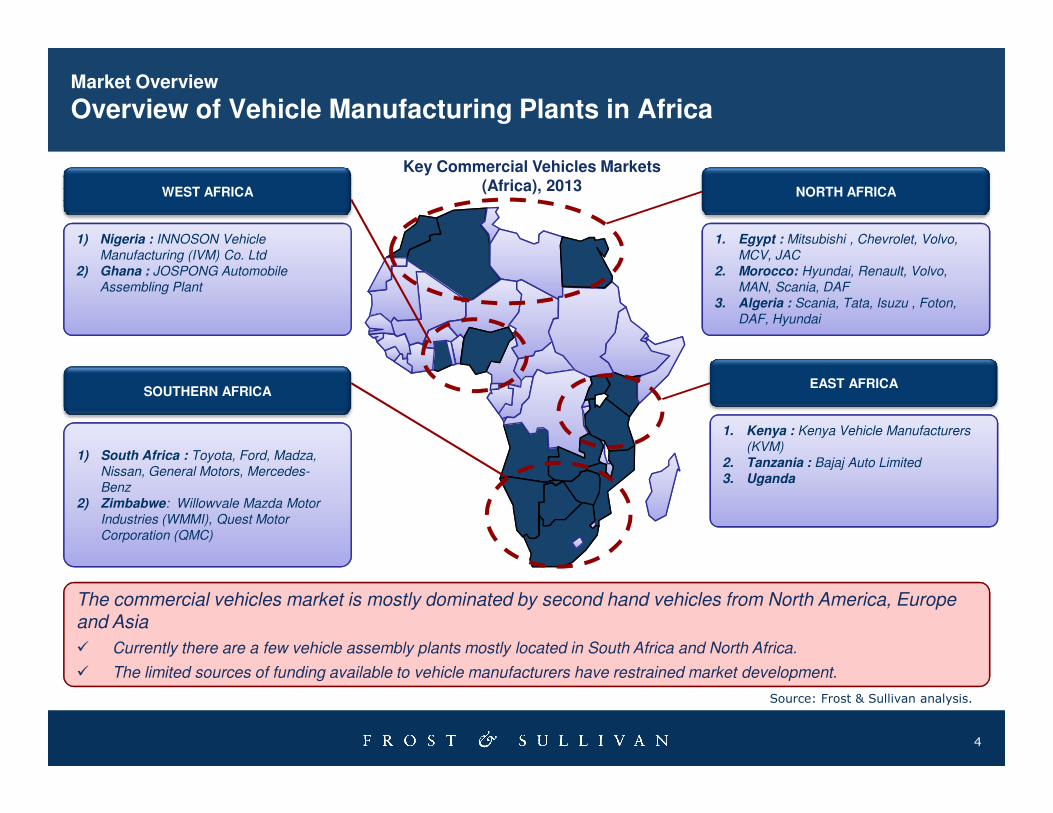

Key Commercial Vehicles Markets (Africa), 2013

1) Nigeria : INNOSON Vehicle

Manufacturing (IVM) Co. Ltd

2) Ghana : JOSPONG Automobile

Assembling Plant

WEST AFRICA

1. Egypt : Mitsubishi , Chevrolet, Volvo,

MCV, JAC

2. Morocco: Hyundai, Renault, Volvo,

MAN, Scania, DAF

3. Algeria : Scania, Tata, Isuzu , Foton,

DAF, Hyundai

NORTH AFRICA

EAST AFRICASOUTHERN AFRICA

Market Overview

Overview of Vehicle Manufacturing Plants in Africa

4

1. Kenya : Kenya Vehicle Manufacturers

(KVM)

2. Tanzania : Bajaj Auto Limited

3. Uganda

1) South Africa : Toyota, Ford, Madza,

Nissan, General Motors, Mercedes-

Benz

2) Zimbabwe: Willowvale Mazda Motor

Industries (WMMI), Quest Motor

Corporation (QMC)

The commercial vehicles market is mostly dominated by second hand vehicles from North America, Europe and Asia

� Currently there are a few vehicle assembly plants mostly located in South Africa and North Africa.

� The limited sources of funding available to vehicle manufacturers have restrained market development.

Source: Frost & Sullivan analysis.

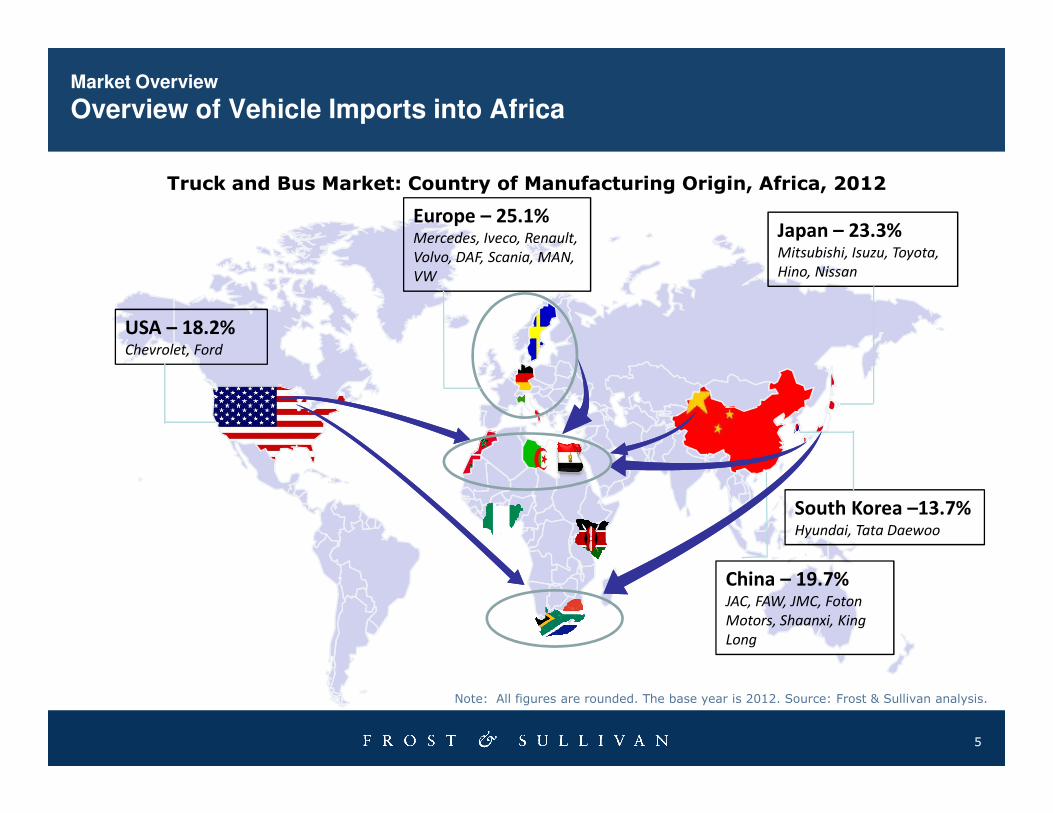

USA – 18.2%Chevrolet, Ford

Japan – 23.3%Mitsubishi, Isuzu, Toyota,

Hino, Nissan

Europe – 25.1%Mercedes, Iveco, Renault,

Volvo, DAF, Scania, MAN,

VW

Truck and Bus Market: Country of Manufacturing Origin, Africa, 2012

Market Overview

Overview of Vehicle Imports into Africa

5

China – 19.7%JAC, FAW, JMC, Foton

Motors, Shaanxi, King

Long

South Korea –13.7%Hyundai, Tata Daewoo

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

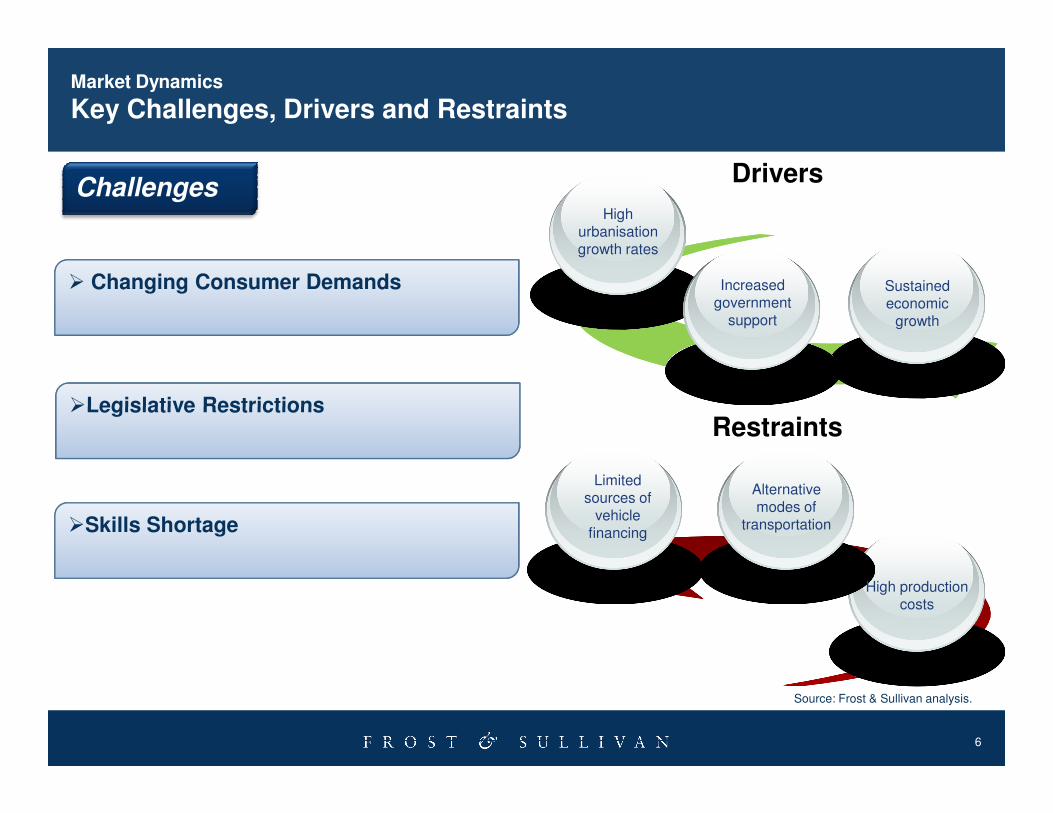

Drivers

High urbanisation growth rates

Sustained economic

growth

Increased government

support

Challenges

� Changing Consumer Demands

�Legislative Restrictions

Market Dynamics

Key Challenges, Drivers and Restraints

6

Restraints

Limited sources of

vehicle financing

Alternative modes of

transportation

High production costs

�Skills Shortage

�Legislative Restrictions

Source: Frost & Sullivan analysis.

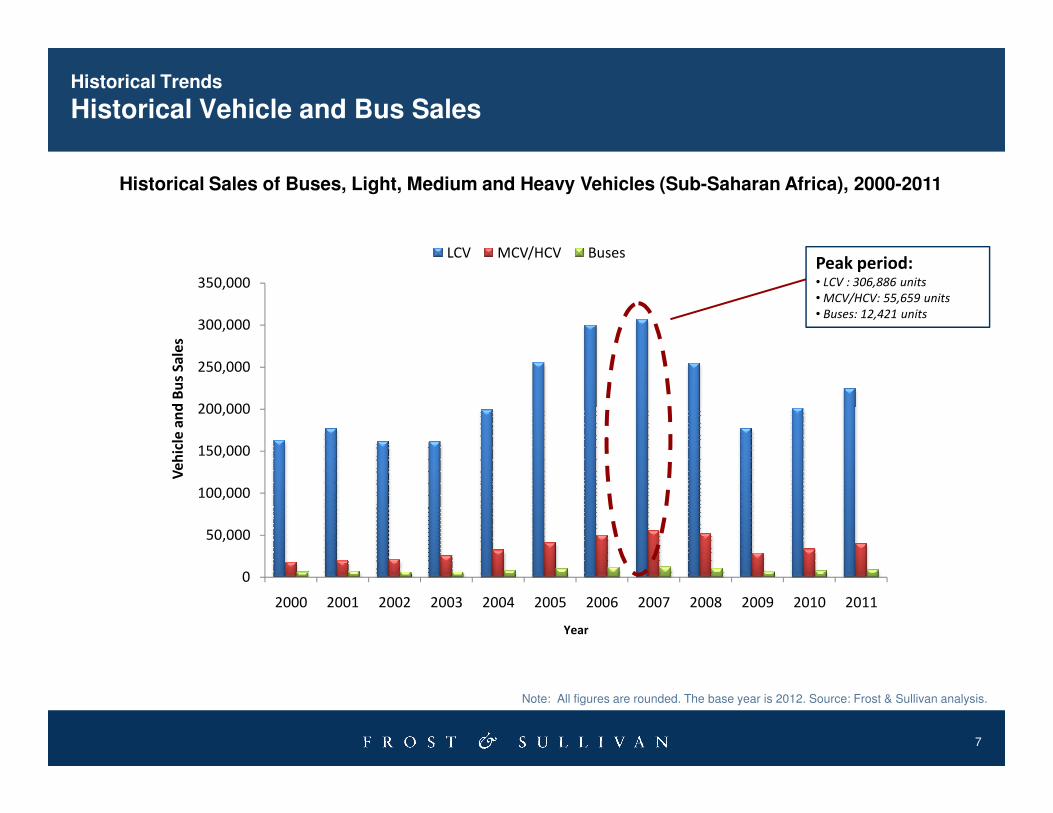

Historical Sales of Buses, Light, Medium and Heavy Vehicles (Sub-Saharan Africa), 2000-2011

200,000

250,000

300,000

350,000

Ve

hic

le a

nd

Bu

s S

ale

s

LCV MCV/HCV Buses

Historical Trends

Historical Vehicle and Bus Sales

Peak period:• LCV : 306,886 units

• MCV/HCV: 55,659 units

• Buses: 12,421 units

7

0

50,000

100,000

150,000

200,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Ve

hic

le a

nd

Bu

s S

ale

s

Year

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

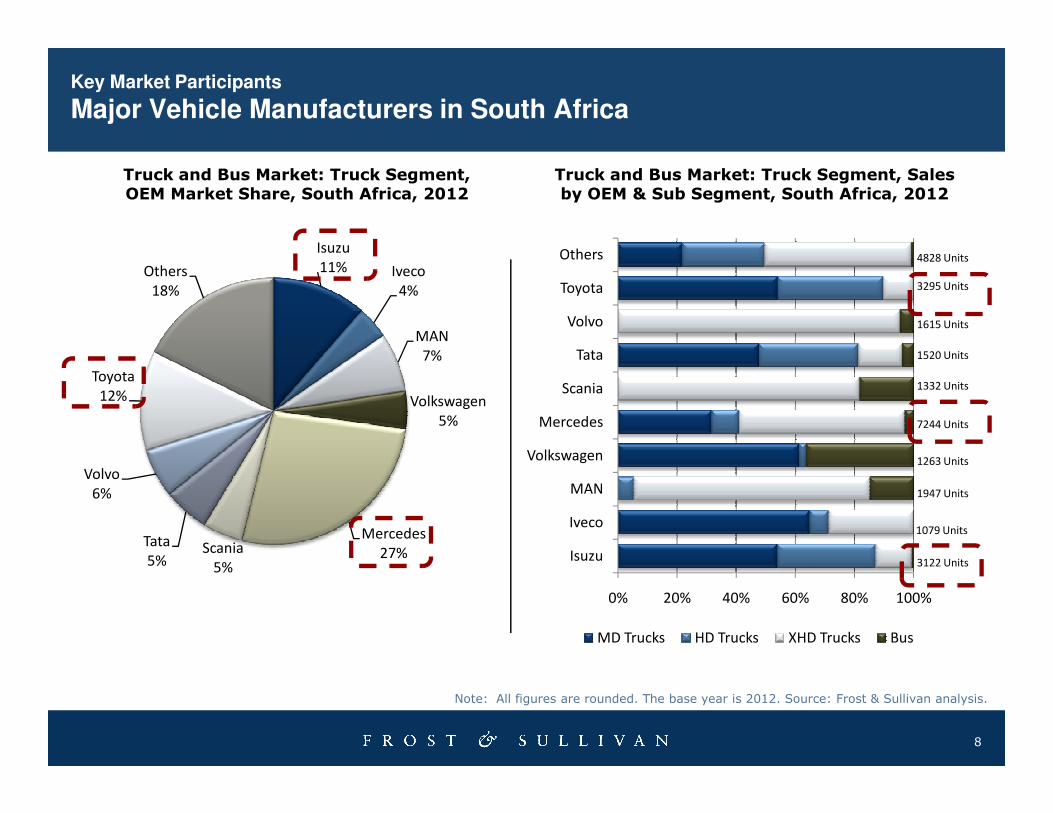

Truck and Bus Market: Truck Segment, OEM Market Share, South Africa, 2012

Truck and Bus Market: Truck Segment, Salesby OEM & Sub Segment, South Africa, 2012

Isuzu

11% Iveco

4%

MAN

7%

Volkswagen

Toyota

12%

Others

18%

Scania

Tata

Volvo

Toyota

Others 4828 Units

3295 Units

1615 Units

1520 Units

1332 Units

Key Market Participants

Major Vehicle Manufacturers in South Africa

8

Volkswagen

5%

Mercedes

27%Scania

5%

Tata

5%

Volvo

6%

0% 20% 40% 60% 80% 100%

Isuzu

Iveco

MAN

Volkswagen

Mercedes

MD Trucks HD Trucks XHD Trucks Bus

7244 Units

1263 Units

1947 Units

3122 Units

1079 Units

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

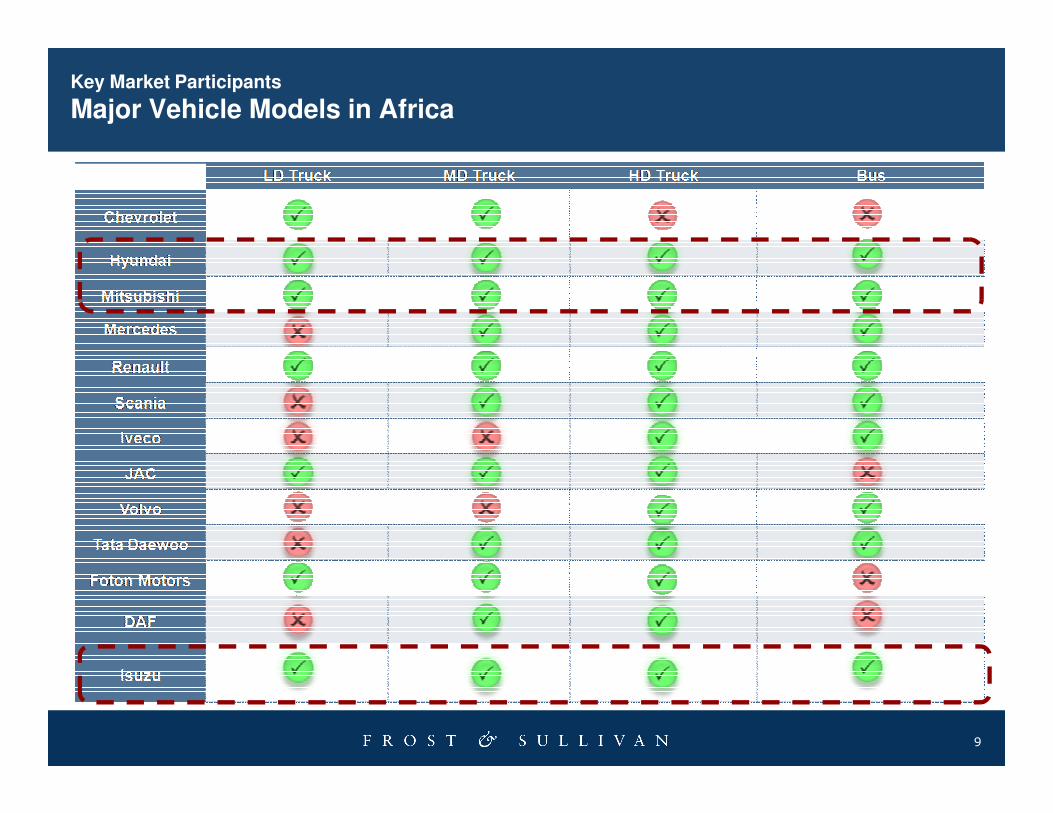

Key Market Participants

Major Vehicle Models in Africa

9

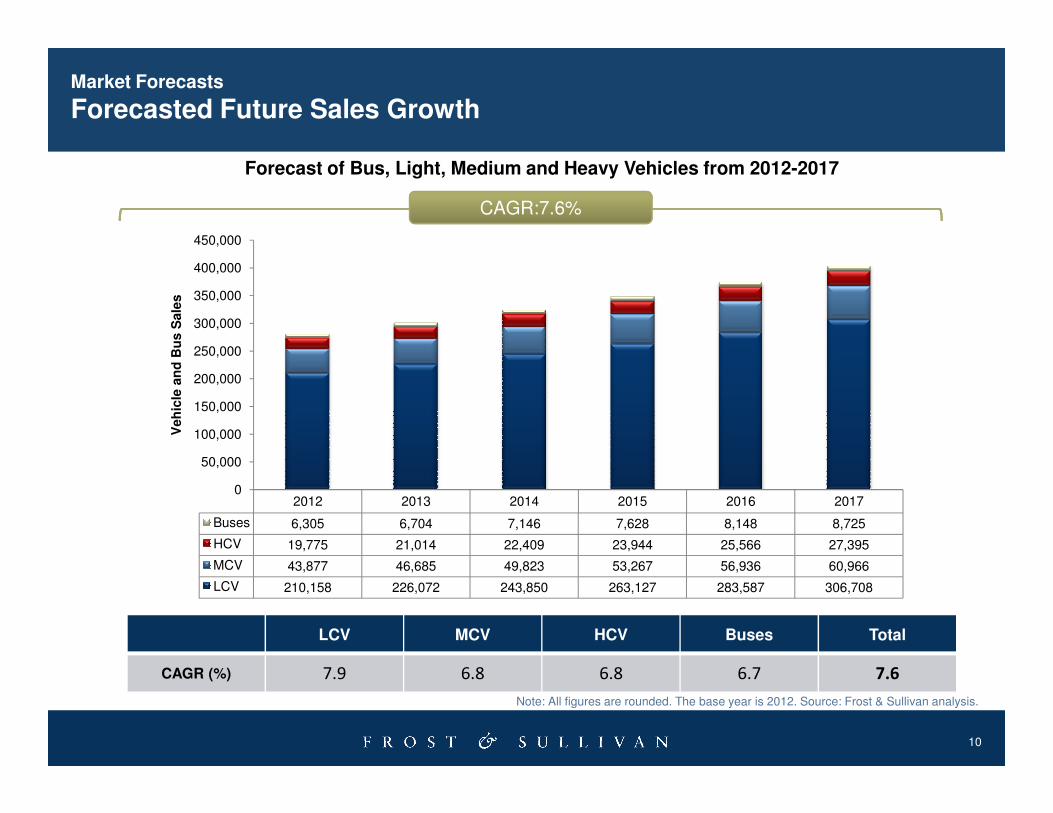

CAGR:7.6%

Forecast of Bus, Light, Medium and Heavy Vehicles from 2012-2017

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Veh

icle

an

d B

us S

ale

s

Market Forecasts

Forecasted Future Sales Growth

10

Note: All figures are rounded. The base year is 2012. Source: Frost & Sullivan analysis.

LCV MCV HCV Buses Total

CAGR (%) 7.9 6.8 6.8 6.7 7.6

2012 2013 2014 2015 2016 2017

Buses 6,305 6,704 7,146 7,628 8,148 8,725

HCV 19,775 21,014 22,409 23,944 25,566 27,395

MCV 43,877 46,685 49,823 53,267 56,936 60,966

LCV 210,158 226,072 243,850 263,127 283,587 306,708

0

50,000

100,000

150,000

Veh

icle

an

d B

us S

ale

s

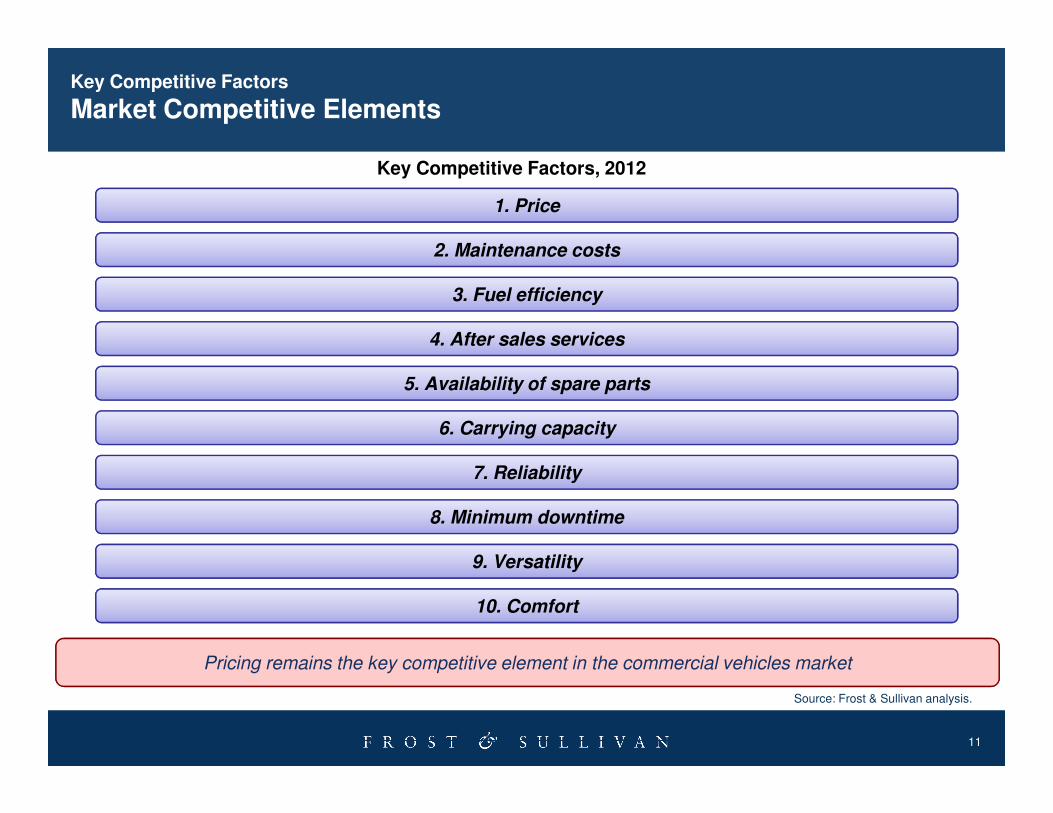

Key Competitive Factors, 2012

1. Price

2. Maintenance costs

3. Fuel efficiency

4. After sales services

5. Availability of spare parts

Key Competitive Factors

Market Competitive Elements

11

6. Carrying capacity

7. Reliability

8. Minimum downtime

9. Versatility

10. Comfort

Pricing remains the key competitive element in the commercial vehicles market

Source: Frost & Sullivan analysis.

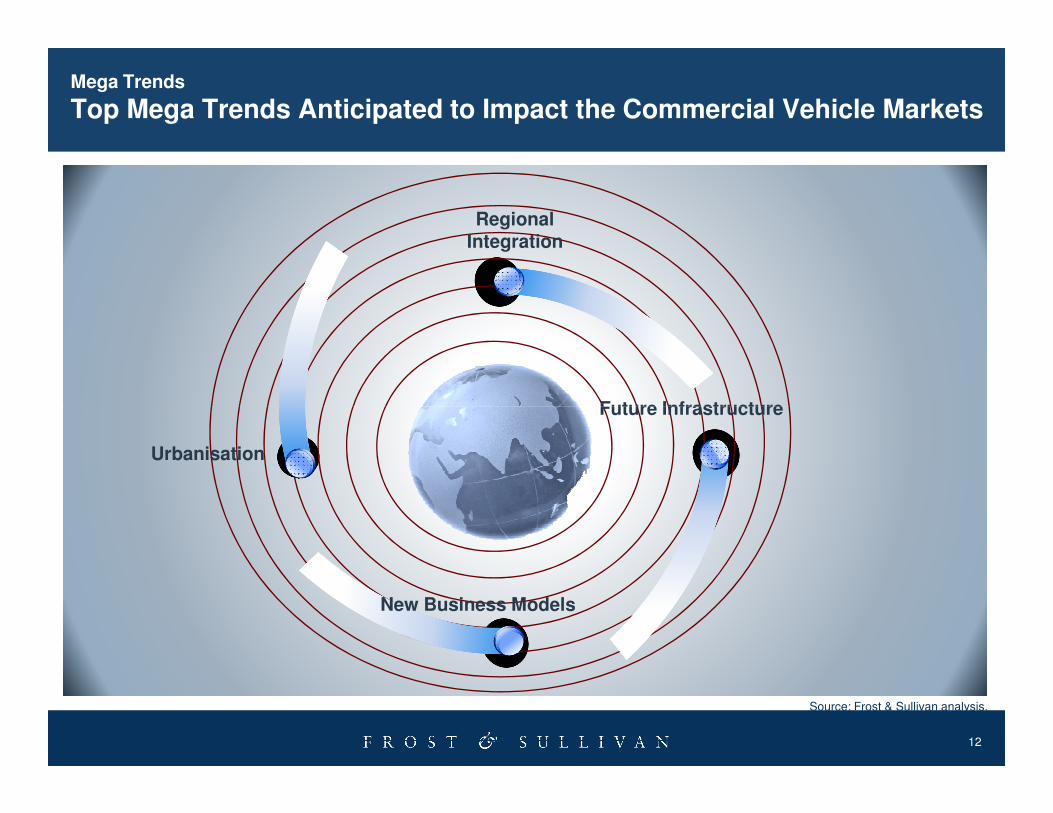

Regional Integration

Future Infrastructure

Mega Trends

Top Mega Trends Anticipated to Impact the Commercial Vehicle Markets

12

Urbanisation

New Business Models

Future Infrastructure

Source: Frost & Sullivan analysis.

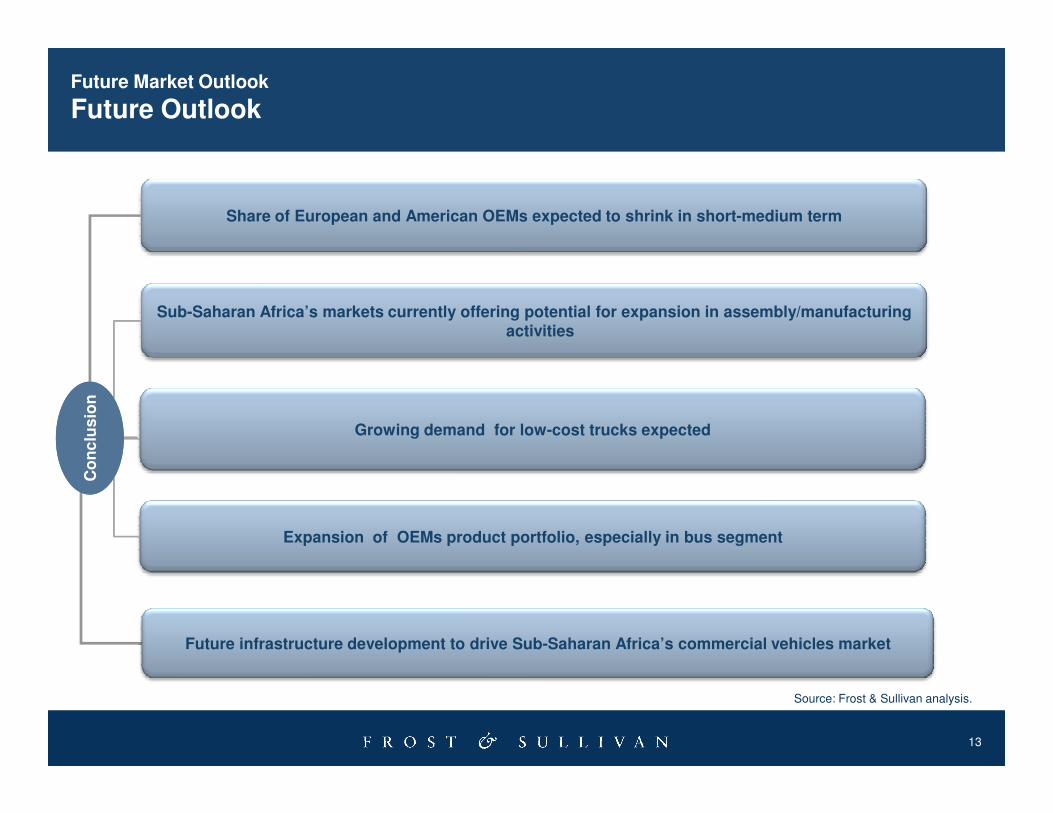

Sub-Saharan Africa’s markets currently offering potential for expansion in assembly/manufacturing activities

Share of European and American OEMs expected to shrink in short-medium term

Co

nc

lus

ion

Future Market Outlook

Future Outlook

13

Source: Frost & Sullivan analysis.

Future infrastructure development to drive Sub-Saharan Africa’s commercial vehicles market

Growing demand for low-cost trucks expected

Expansion of OEMs product portfolio, especially in bus segment

Co

nc

lus

ion

Next Steps

Develop Your Visionary and Innovative Skills Growth Partnership Service

Share your growth thought leadership and ideas or join our GIL Global Community

14

Skills Growth Partnership Service ideas or join our GIL Global Community

Join our GIL Community NewsletterKeep abreast of innovative growth opportunities

Your Feedback is Important to Us

What would you like to see from Frost & Sullivan?

Growth Forecasts?

Competitive Structure?

15

Emerging Trends?

Strategic Recommendations?

Other?

Please inform us by “Rating” this presentation.

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/companies/4506

1616

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

http://twitter.com/FrostsullivanSA

For Additional Information

Samantha James

Corporate Communications

+27 (0)21 680 3574

Derrick Chikanga

Research Analyst – EBT / A&T

+27 (0)21 680 3204

17

Kudzanayi Bangure

Programme Manager – EBT / A&T

+27 (0)21 680 3207

Guillaume de Bassompierre

Director – Business Development

+27 (0)21 680 3203