emerging market finance: lecture 13: emerging market debt

DESCRIPTION

Emerging Market Finance: Lecture 13: Emerging Market Debt. The History of Emerging Market Debt. Emerging market Debt at the turn of the Century The EM debt crisis in the 1980’s The 1997-99 EM Financial Crises. 2. The Brady Bond Market. The Brady Plan for Mexico (1990) - PowerPoint PPT PresentationTRANSCRIPT

1

Yale School of Management

Emerging Market Finance:

Lecture 13: Emerging Market Debt

2

Yale School of Management

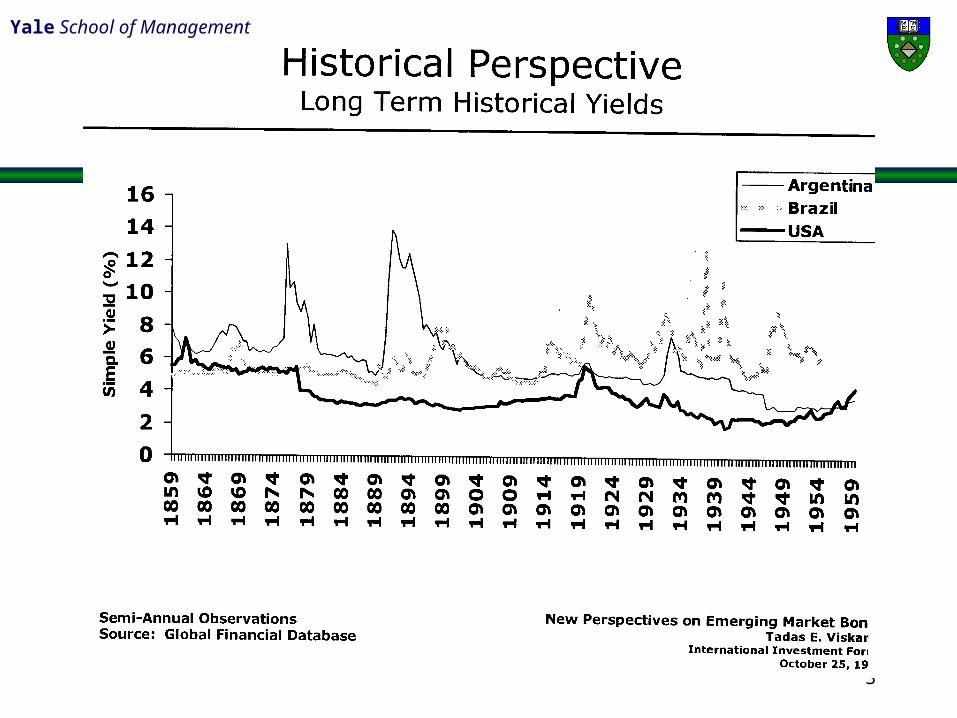

The History of Emerging Market Debt

Emerging market Debt at the turn of the

Century

The EM debt crisis in the 1980’s

The 1997-99 EM Financial Crises

2

3

Yale School of Management

4

Yale School of Management

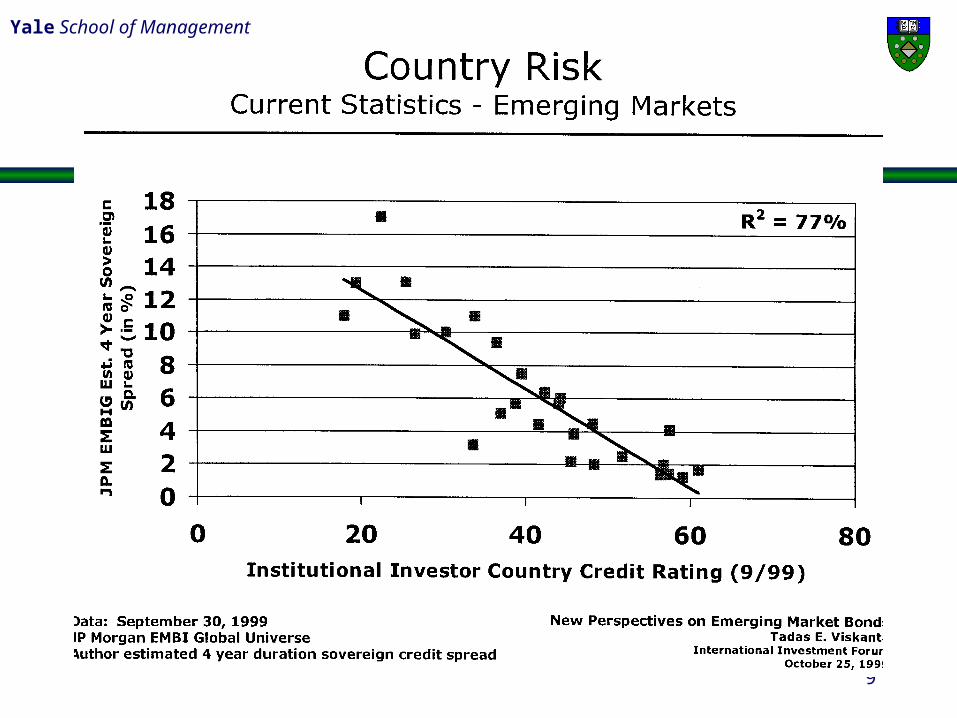

5

Yale School of Management

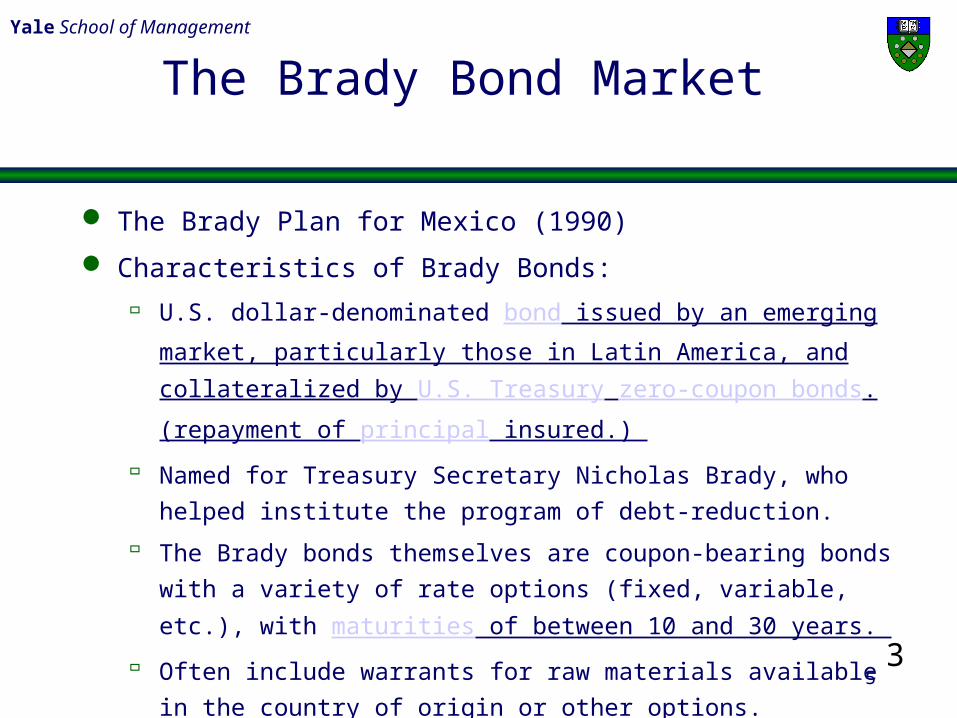

The Brady Bond Market

The Brady Plan for Mexico (1990)

Characteristics of Brady Bonds:

U.S. dollar-denominated bond issued by an emerging market, particularly

those in Latin America, and collateralized by U.S. Treasury

zero-coupon bonds.

(repayment of principal insured.)

Named for Treasury Secretary Nicholas Brady, who helped institute the

program of debt-reduction.

The Brady bonds themselves are coupon-bearing bonds with a variety of rate

options (fixed, variable, etc.), with maturities of between 10 and 30 years.

Often include warrants for raw materials available in the country of origin or

other options. 3

6

Yale School of Management

7

Yale School of Management

FROM 1 -5 -9 4 TO 4 -3 -0 0 WEEKLY INDEXED

1 9 9 4 1 9 9 5 1 9 9 6 1 9 9 7 1 9 9 8 1 9 9 9 2 0 0 06 0

8 0

1 0 0

1 2 0

1 4 0

1 6 0

1 8 0

2 0 0

J .P.M ORGAN EM BI FIXED BRADY - RETURN IND. (OFCL )J .P.M ORGAN EM BI+ COM POSITE - RETURN IND. (OFCL )

So u rc e : DATASTREAM

8

Yale School of Management

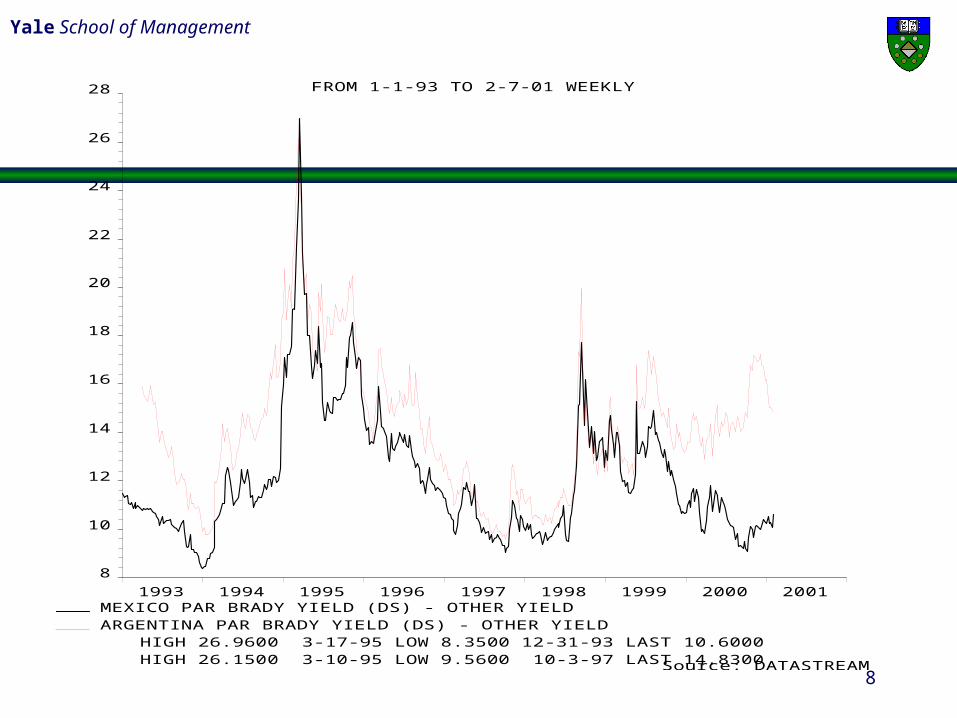

FROM 1-1-93 TO 2-7-01 WEEKLY

1993 1994 1995 1996 1997 1998 1999 2000 20018

10

12

14

16

18

20

22

24

26

28

MEXICO PAR BRADY YIELD (DS) - OTHER YIELDARGENTINA PAR BRADY YIELD (DS) - OTHER YIELD

HIGH 26.9600 3-17-95 LOW 8.3500 12-31-93 LAST 10.6000HIGH 26.1500 3-10-95 LOW 9.5600 10-3-97 LAST 14.8300Source: DATASTREAM

9

Yale School of Management

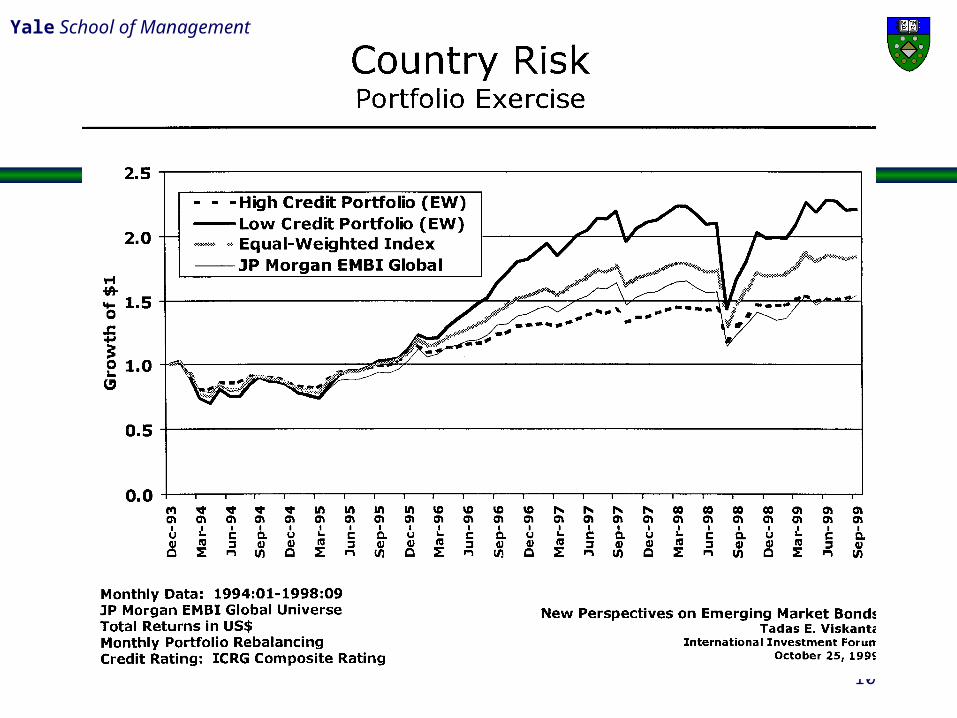

10

Yale School of Management

11

Yale School of Management

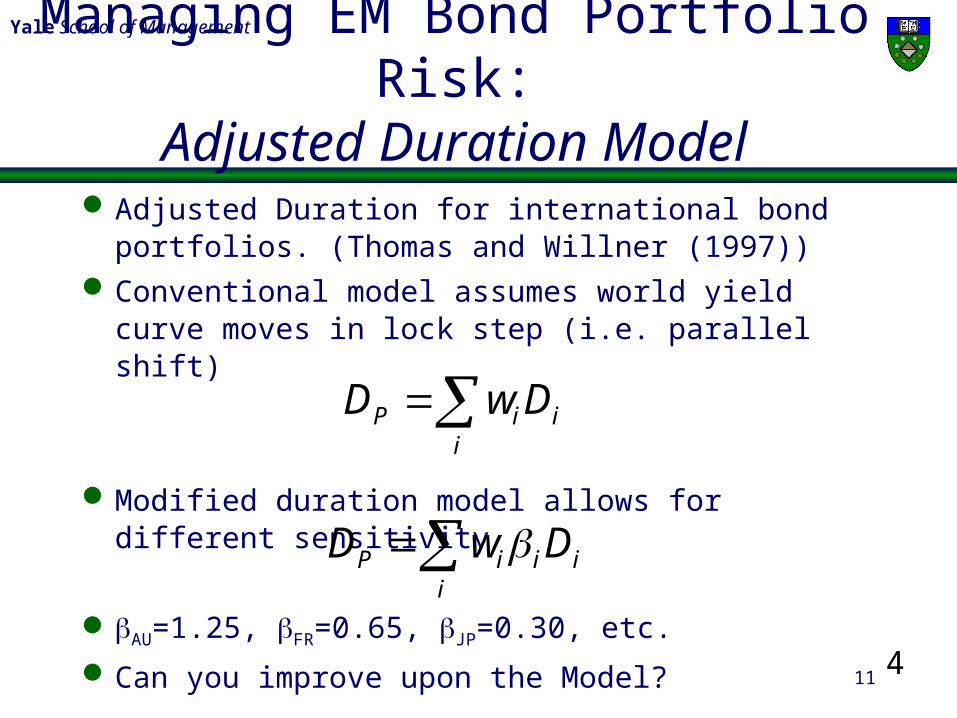

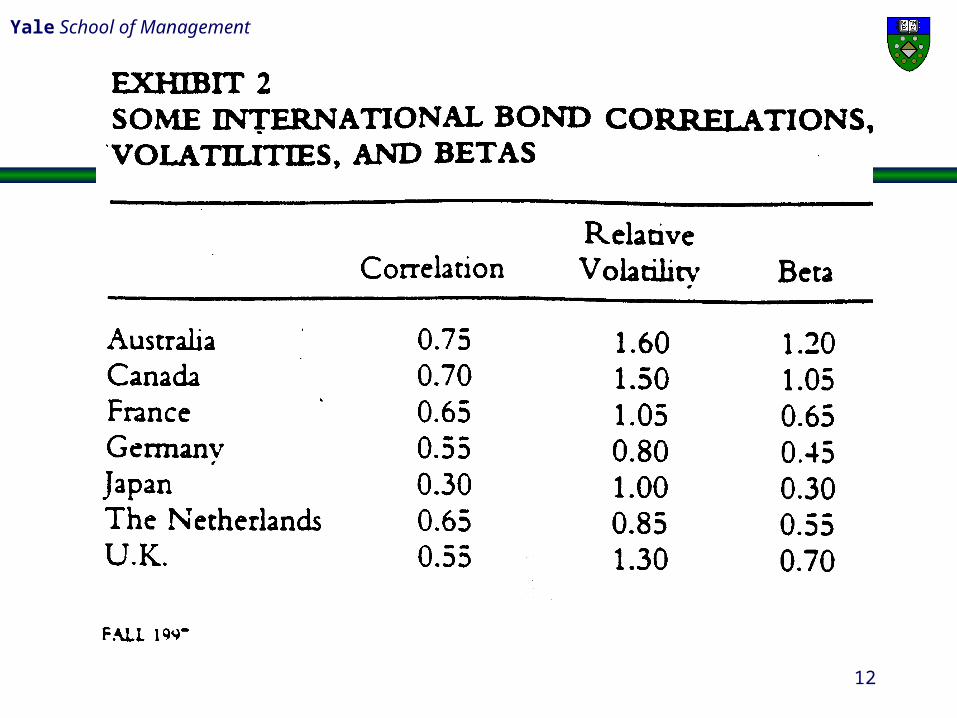

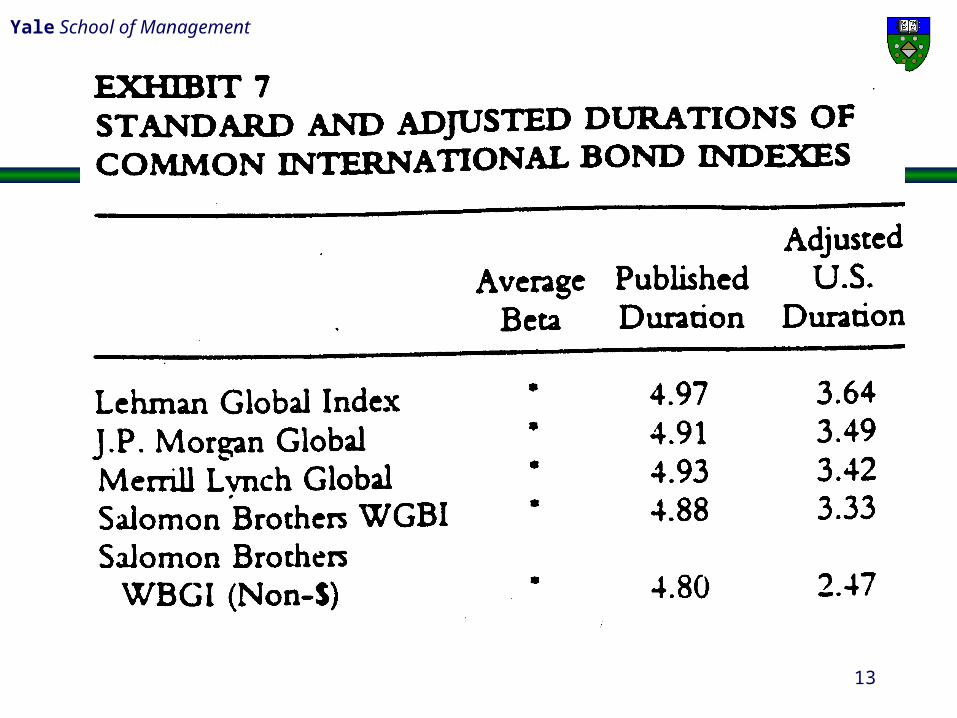

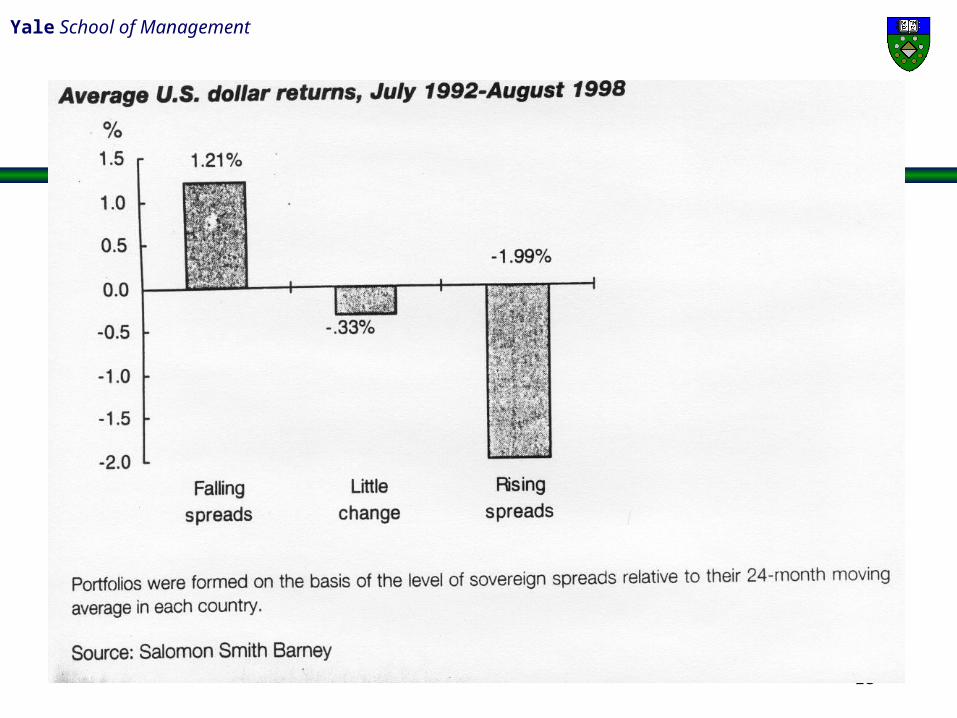

Managing EM Bond Portfolio Risk:Adjusted Duration Model

Adjusted Duration for international bond portfolios. (Thomas and Willner (1997))

Conventional model assumes world yield curve moves in lock step (i.e. parallel shift)

Modified duration model allows for different sensitivity

AU=1.25, FR=0.65, JP=0.30, etc.

Can you improve upon the Model? 4

i

iiP DwD

i

iiiP DwD

12

Yale School of Management

13

Yale School of Management

14

Yale School of Management

15

Yale School of Management

16

Yale School of Management

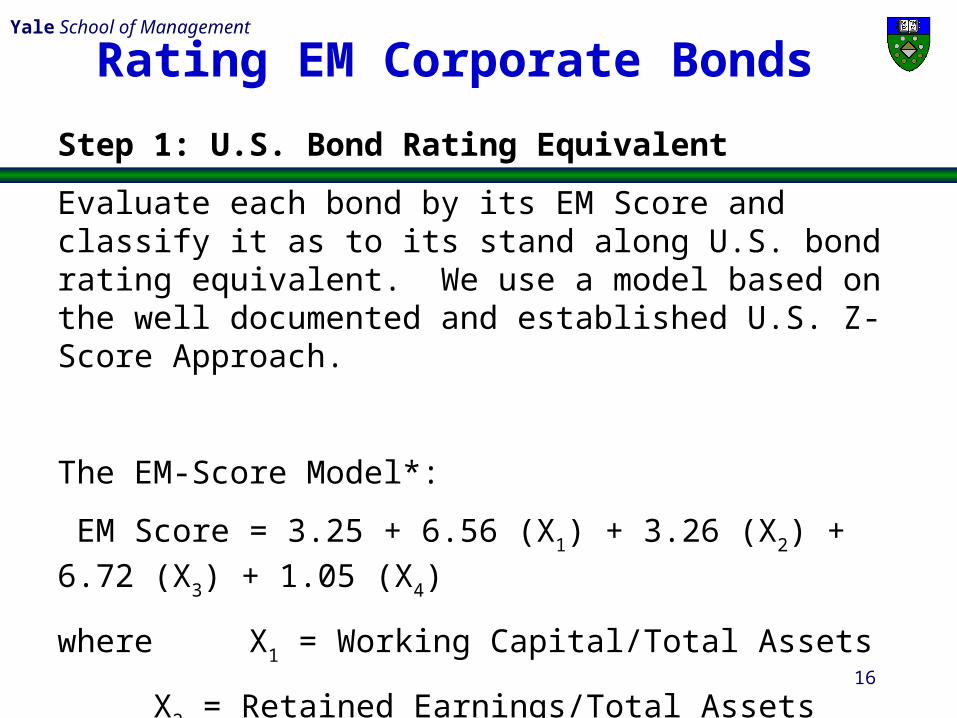

Step 1: U.S. Bond Rating Equivalent

Evaluate each bond by its EM Score and classify it as to its stand along U.S. bond rating equivalent. We use a model based on the well documented and established U.S. Z-Score Approach.

The EM-Score Model*:

EM Score = 3.25 + 6.56 (X1) + 3.26 (X2) + 6.72 (X3) + 1.05 (X4)

where X1 = Working Capital/Total Assets

X2 = Retained Earnings/Total Assets

X3 = EBIT/Total Assets

X4 = Book Value Equity/Total Liabilities

Rating EM Corporate Bonds

17

Yale School of Management

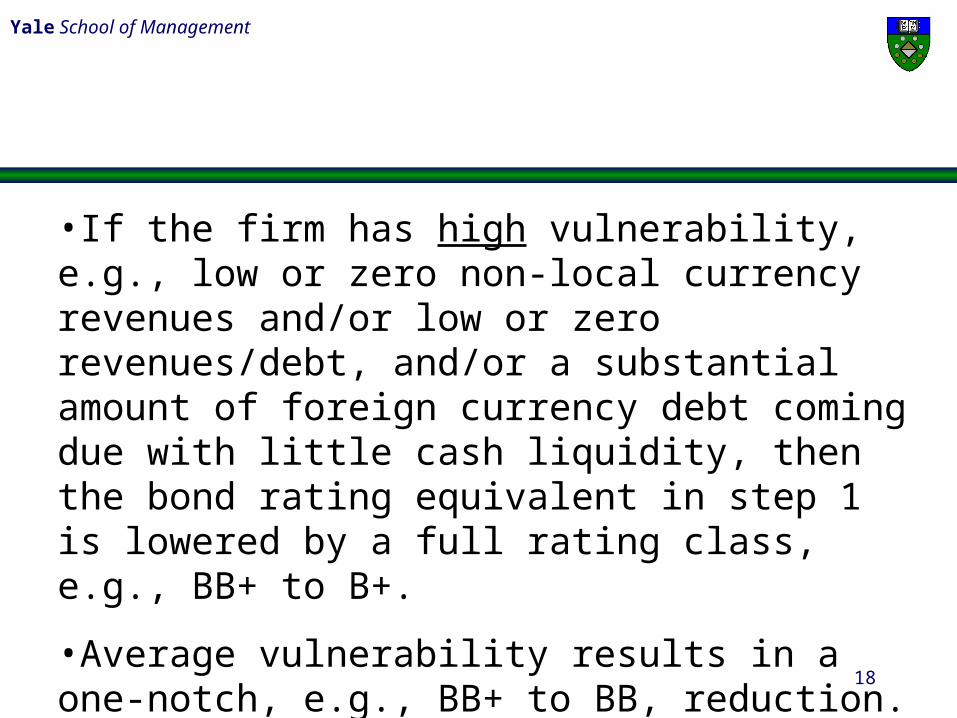

Step 2: Adjusted Bond Rating for Foreign Currency Fluctuation Vulnerability

Each bond is analyzed as to the issuing firm’s vulnerability to problems in servicing its foreign currency denominated debt if the local currency is devalued.

Vulnerability is assessed based on (1) the relationship between non-local currency revenues minus costs compared to non-local currency interest expense and (2) non-local currency revenues vs. non-local currency debt. Finally, (3) the level of cash is compared with the debt coming due in the next year.

18

Yale School of Management

•If the firm has high vulnerability, e.g., low or zero non-local currency revenues and/or low or zero revenues/debt, and/or a substantial amount of foreign currency debt coming due with little cash liquidity, then the bond rating equivalent in step 1 is lowered by a full rating class, e.g., BB+ to B+.

•Average vulnerability results in a one-notch, e.g., BB+ to BB, reduction. There is no upgrade for a good vulnerability assessment.

19

Yale School of Management

Step 3: Adjustment for Industry Risk

The original (step 1) bond rating equivalent is compared to the generic industry bond rating equivalent. For up to one full letter grade difference between the two ratings, step 2’s bond rating equivalent is adjusted up or down by one notch. For example, if the rating from step 1 is BBB and the industry’s rating is BBB-, BB+, or BB, then the adjustment is one notch down. If the difference is more than one full rating class but less than two full ratings, there is a 2-notch adjustment, etc.

20

Yale School of Management

Step 4: Adjustment for Competitive Position

Step 3’s rating is adjusted up (or down) one notch if the firm is a dominant (or not) company in its industry or if it is a domestic power in terms of size, political influence and quality of management. It is possible that the consensus competitive position result is neutral (no change in rating).

21

Yale School of Management

Step 5: Adjustment for Market Value vs. Book Value of Equity

Most Emerging Market Eurobond Issuers have public equity shares outstanding. Since market equity value should reflect expectations and book equity reflects historical values, we adjust the bond rating equivalent (BRE) for the market/book equity ratio. EM Scores and their bond rating equivalents are compared using the two measures of equity value. Where significant differences manifest, a further adjustment is made:

22

Yale School of Management

Adjustment Process:

BRE (Book) vs. BRE (Market)

BRE Difference Adjustment

± 0,1 Notch = None

± 2 Notches = ± 1 Notch

≥ ± 3 Notches = ± 2 Notches

23

Yale School of Management

Step 6: Bond Specific Adjustment

Any unique aspects of the bond, e.g., collateral, guarantees, etc., could impact the final rating and spread.

Step 7: Sovereign Risk Spread Adjustment

The next step in the process is to add the sovereign yield differential vs. comparable duration U.S. Treasury bonds to the yield spread of the bond based on its rating equivalent (BRE) from Step 5.

24

Yale School of Management

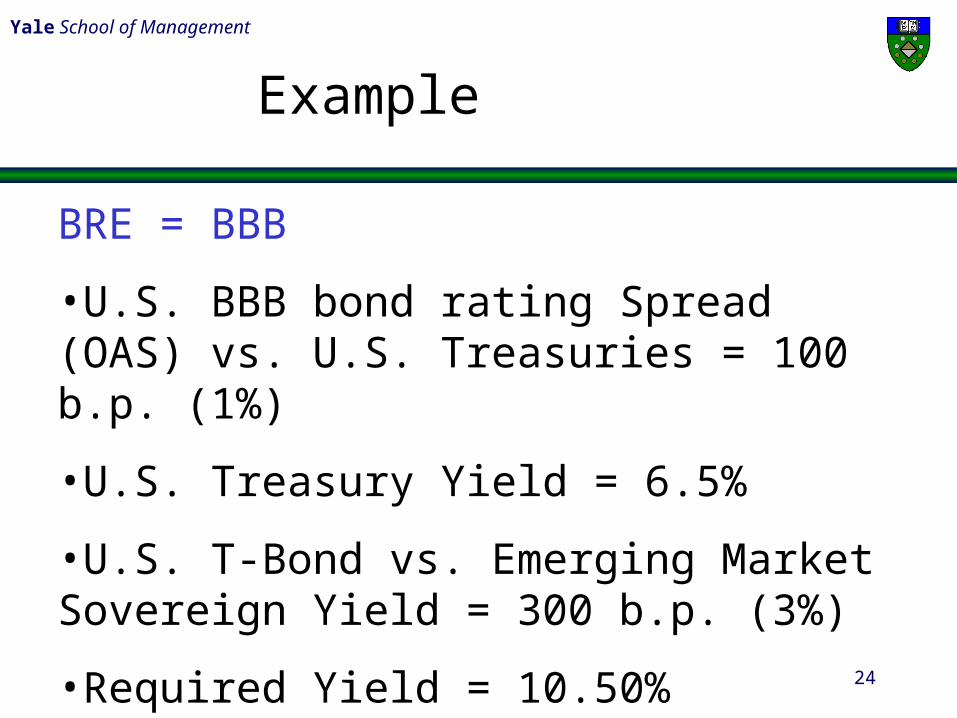

BRE = BBB

•U.S. BBB bond rating Spread (OAS) vs. U.S. Treasuries = 100 b.p. (1%)

•U.S. Treasury Yield = 6.5%

•U.S. T-Bond vs. Emerging Market Sovereign Yield = 300 b.p. (3%)

•Required Yield = 10.50%

Example