emerging trends in airport-airline agreements · pdf filenegotiated with airlines ... charges...

TRANSCRIPT

Emerging Trends in Airport-Airline Agreements

AAAE/LeighFisher Rates and Charges Workshop

Phoenix, Arizona November 4, 2016

Sheri Ernico, Director, LeighFisher Jason Snowden, Director, LeighFisher

Discussion Topics

1. Forms of Airport-Airline Business Relationships

2. Airport Rates and Charges and Ratemaking Approaches

3. Negotiation and Planning Process

4. Trends in Airline Lease Negotiations

5. Per-Turn Fees

- Regulatory and Legal Basis

- Implementing and Calculating Fees

Forms of Airport-Airline Business Relationships

3 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Airport-Airline Business Relationship With or Without a Bilateral Agreement

AGREEMENT

Negotiated with airlines

Passenger airlines vs. cargo carriers

Agreements by definition include compromise

RATES BY RESOLUTION

Rates established through consultation

Ordinance and regulations

Permits and regulations

No airline agreement is required, and some airports operate without an agreement, but the vast majority of airports have agreements

Some airports have rates resolution with revenue sharing agreements (e.g., LAX, MCO)

HYBRID

4 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Airport-Airline Business Relationship Relatively Few U.S. Airports Set Rates by Ordinance/Resolution (Less than 20%)

1. Source for enplanements and hub Size: FAA, ACAIS CY 2015, Primary Airports, August 2016. There are 132 large, medium, and small hub airports.

2. On January 1, 2013, a new rate agreement went into effect at Los Angeles (LAX).

Source: Large, medium, and small hub U.S. Airports setting rates by resolution compiled by LeighFisher.

Airport Hub Size CY 2015 e.p.1 Time Under Resolution

Los Angeles International L 36,351,226 Since 19932

Phoenix Sky Harbor International L 21,351,445 > 30 years

Orlando International L 18,759,938 Effective November 20133

Boston Logan International L 16,290,323 > 30 years

Oakland International M 5,506,672 Since 2000

Raleigh-Durham International M 4,954,717 > 30 years

John Wayne Airport-Orange County M 4,945,175 > 20 years

Sacramento International M 4,714,723 Since June 2008

San Juan Luis Munoz Marin International M 4,218,785 > 20 years, but airport privatized March 2013

Omaha Eppley Airfield M 2,046,155 > 30 years

Charleston International S 1,669,960 Since 2001

Grand Rapids Gerald R. Ford International S 1,280,801 > 30 years

Long Beach /Daugherty Field S 1,220,906 At least 10 years

Des Moines International Airport S 1,156,450 Since January 1, 2014

Bill & Hillary Clinton National (Little Rock) S 958,510 Since 2009

Northwest Arkansas Regional S 629,903 Since January 1, 2015

Lexington Blue Grass S 606,977 Since 2001

Asheville Regional N 393,379 Since October 2016

Lehigh Valley International (Allentown, PA) N 320,544 Since 1993

Santa Barbara Municipal N 316,508 Since October 2007

Rapid City Regional N 264,170 Since 2015

5 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Airport-Airline Business Relationship Rates by Resolution

Any unilateral rate methodology must be designed to recover from the air carriers using the airport their fairly allocated share of airport costs in accordance with the U.S. Department of Transportation’s Policy Regarding Airport Rates and Charges, 78 Fed. Reg. 55330 (September 10, 2013), and other applicable law

Without an airline agreement, airline fees set by rate ordinance, resolution, regulation, or tariff

Governed by USDOT Rates and Charges Policy and case law

Key underlying principles and requirements:

― Expressed preference for local resolution

― Endeavor to be self-sustaining

― Rates must be “reasonable” and not “unjustly discriminatory”

― Cost allocation must be “transparent” and comply with USDOT rules

― Justification for significant changes in rate-making approach

― Must consult with airlines

― Compensatory rate-setting permitted without agreement

― Residual rate-setting not permitted without agreement

6 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Airport-Airline Business Relationship Why Have an Airline Agreement?

Specify what airlines can do at airport and what airport is obliged to do for airlines

Provide certainty in airline payments

― Costs in rate base

― Cost center structure

― Rents, fees, and charges

― Calculation methodologies

Prescribe airline role in capital decisions (Majority-In-Interest vs. consultation)

Set term: short unless airlines committing to major investments

Determine control over and use of gates and facilities (exclusive, preferential, common use)

Provide legal protection: indemnification, insurance, environmental, etc.

Primary Negotiation

Airline Payments

Capital Program Control

Facility Control

Airport Rates and Charges and Ratemaking Approaches

8 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Airport Rentals, Fees, and Charges Account for a Small Share of U.S. Scheduled Airline Operating Expenses (vs. labor and fuel)

Note: The figures do not include data for all airlines, such as commuter airlines operating aircraft with fewer than 60 seats. Such carriers are

exempt from filing certain financial information with DOT.

Source: U.S. DOT, Form 41 as compiled by LeighFisher, November 2016.

* Includes data for American, Alaska, JetBlue, Delta, Frontier, Spirit, United, US Airways, Virgin America, and Southwest.

Labor 29.7%

Fuel 19.9% Transport related expenses 13.9%

Outsourcing 8.6%

Maintenance 7.4%

Depreciation, 5.2%

Other 4.9%

Terminal rentals 3.1%

Landing fees 2.0%

Aircraft rentals 2.5%

Food 1.7%

Commissions 1.0%

U.S. Scheduled Passenger Airline Operating Expenses by Category (CY 2015)

9 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Airport Rates and Charges are Also More Predictable than Other U.S. Airline Operating Expenses

Note: The figures do not include data for all airlines, such as commuter airlines operating aircraft with fewer than 60 seats. Such carriers are

exempt from filing certain financial information with DOT. The historical data in the early 1980s is less reliable than the data for more recent years.

Source: U.S. DOT, Form 41 as compiled by LeighFisher, November 2016.

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%1

98

0

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Airport Rates and Charges as Percent of Operating Expenses

Fuel Costs as Percent of Operating Expenses

10 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Some Airlines Pay a Higher Share than Others Due to their Cost Structures and the Airports where they Operate

Source: U.S. DOT, Form 41 as compiled by LeighFisher, November 2016.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Avera

ge

Sp

irit

Delt

a

US

Air

ways

Am

eri

ca

n

Un

ited

Ala

sk

a

JetB

lue

Vir

gin

Am

eri

ca

So

uth

west

Fro

nti

er

Terminal Landing Fees

Airport Rates and Charges as a Percent of Total Operating Expenses: U.S. Scheduled Passenger Airlines

11 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

In Evaluating the Reasonableness of Airport Rates and Charges we Compare them to the Fare Revenues Generated at an Airport

Note: The figures do not include data for all airlines, such as commuter airlines operating aircraft with fewer than 60 seats. Such carriers are

exempt from filing certain financial information with DOT. The historical data in the early 1980s is less reliable than the data for more recent years.

Source: U.S. DOT, Form-41 as compiled by LeighFisher, November 2016.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Airport Rates and Charges as % OperatingExpenses

Airport Rates and Charges as % FareRevenue

12 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

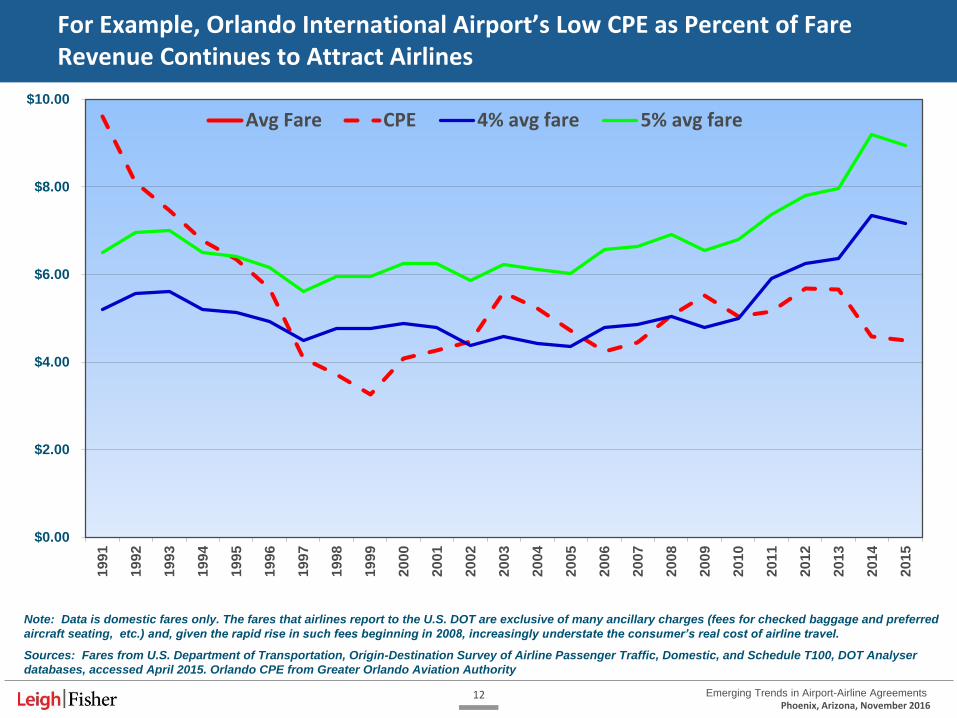

For Example, Orlando International Airport’s Low CPE as Percent of Fare Revenue Continues to Attract Airlines

$0.00

$2.00

$4.00

$6.00

$8.00

$10.001

99

1

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Avg Fare CPE 4% avg fare 5% avg fare

Note: Data is domestic fares only. The fares that airlines report to the U.S. DOT are exclusive of many ancillary charges (fees for checked baggage and preferred

aircraft seating, etc.) and, given the rapid rise in such fees beginning in 2008, increasingly understate the consumer’s real cost of airline travel.

Sources: Fares from U.S. Department of Transportation, Origin-Destination Survey of Airline Passenger Traffic, Domestic, and Schedule T100, DOT Analyser

databases, accessed April 2015. Orlando CPE from Greater Orlando Aviation Authority

13 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airline Business Relationships – Large Hubs

Rank LocidCY 2015

EnplanementsMethod

Airline

Agreement

Rates by

Ordinance or

Agreement

Term

(years)Expiration Airfield Terminal

Revenue

Sharing

1 ATL 49,340,732 Hybrid Yes A 7 6/30/3036 CCR CCR Yes

2 LAX 36,351,226 Compensatory Hybrid* O 10 12/31/2022 CCR CC Yes

3 ORD 36,305,668 Residual Yes A 7 5/11/2018 CCR CCR Yes

4 DFW 31,589,832 Compensatory Yes A 10 9/30/2020 CCR CC Yes

5 JFK 27,717,503 Compensatory Yes A Various Various Unit TBs No

6 DEN 26,280,043 Hybrid Yes A 30 2/28/2025 CCR CC Yes

7 SFO 24,190,549 Residual Yes A 10 6/30/2021 CCR+ CCR Residual

8 CLT 21,913,156 Hybrid Yes A 10 6/30/2026 CCR+ CC Yes

9 LAS 21,824,231 Residual Yes A 5 + 5 6/30/2020 CCR CCR Residual

10 PHX 21,351,445 Compensatory No O n.a. M/M Comp CC No

11 MIA 20,986,341 Residual Yes A 16 4/30/2017 Airport Residual CC Residual

12 IAH 20,595,874 Compensatory Yes A 20 12/31/2017 CCR CC No

13 SEA 20,148,980 Compensatory Yes A 5 12/31/2017 CCR CC Yes

14 MCO 18,759,938 Hybrid Hybrid* O 3 9/30/2019 CCR CC Yes

15 EWR 18,684,765 Compensatory Yes A Various Various Unit TBs No

16 MSP 17,634,252 Hybrid Yes A 10 12/31/2020 CCR CC Yes

17 BOS 16,290,323 Compensatory Yes O n.a. n.a. CCR CC No

18 DTW 16,255,507 Residual Yes A 30 9/30/2032 Airport Residual CC Residual

19 PHL 15,101,318 Residual Yes A 5 6/30/2020 CCR CCR Residual

20 LGA 14,319,924 Compensatory Yes A Various Various Unit TBs No

21 FLL 13,061,607 Residual Yes A 5 9/30/2016 CCR CCR Residual

22 BWI 11,738,828 Compensatory Yes A 5 6/30/2019 CCR Comp No

23 DCA 11,242,375 Hybrid Yes A 10 12/31/2024 Comp CC Yes

24 MDW 10,830,783 Residual Yes A 15 12/31/2027 CCR CC Yes

25 SLC 10,634,519 Hybrid Yes A 10 6/30/2024 CCR Comp Yes

26 IAD 10,363,918 Hybrid Yes A 3 12/31/2017 Comp CC Yes

27 SAN 9,985,739 Compensatory Yes A 5 6/30/2018 CCR CC No

28 HNL 9,479,083 Hybrid Yes A M/M M/M CCR CCR Yes

29 TPA 9,150,414 Hybrid Yes A 5 9/30/2020 CCR CC Yes

30 PDX 8,340,234 Hybrid Yes A 10 9/1/2027 CCR CCR Yes

* LAX and MCO have entered into rate and revenue sharing agreements, not airline use and lease agreements.

Legend: Residual Airport-wide residual calculation, or multi-cost center residual CCR Cost center residual

Compensatory Airport keeps nonairline revenues without sharing Comp Compensatory

Hybrid Compensatory with revenue sharing, and other features CC Commercial compensatory

Summary Methodology Form M/M Month-to-month

Residual 8 Ordinance 4

Compensatory 11 Agreement 26

Hybrid 11 30

30

Source: LeighFisher, November 2016.

14 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airline Business Relationships – Medium Hubs

RankHub

SizeLocid City

CY 2014

Enplaned

Passengers

Former

Hub AirlineMethod

Airline

Agreement

Rates by

Ordinance or

Agreement

Term

(years)Expiration

Revenue

Sharing

31 M DAL Dallas 7,040,921 Hybrid Yes A 20 09/30/2028 Yes

32 M STL St. Louis 6,239,231 TWA/AA Residual Yes A 5 06/30/2016 Residual

33 M HOU Houston 5,937,944 Hybrid Yes A 25 06/30/2040 Yes

34 M AUS Austin 5,797,547 Compensatory Yes A 5 09/30/2014 No

35 M BNA Nashville 5,708,852 AA Hybrid Yes A 7 06/30/2022 Yes

36 M OAK Oakland 5,506,672 Hybrid Yes O m/m m/m Yes

37 M MSY New Orleans 5,329,696 Residual Yes A tbd Residual

38 M MCI Kansas City 5,135,127 BN/F9 Compensatory Yes A 8 03/31/2017 No

39 M RDU Raleigh 4,954,717 AA Compensatory No O n.a. n.a. No

40 M SNA Santa Ana 4,945,175 Compensatory Yes O 5 03/31/2016 No

41 M SJC San Jose 4,814,721 AA Hybrid Yes A 10 6/30/2017 Yes

42 M SMF Sacramento 4,714,723 Compensatory No O n.a. n.a. No

43 M SJU San Juan 4,218,785 AA Compensatory Yes O 15* 4/1/2028 No

44 M RSW Fort Myers 4,159,212 Hybrid Yes A 5 09/30/2018 Yes

45 M SAT San Antonio 4,091,389 Hybrid Yes A 4 09/30/2015 Yes

46 M CLE Cleveland 3,916,914 CO/UA Residual Yes A 35 12/31/2020 Residual

47 M PIT Pittsburgh 3,890,677 US Residual Yes A 30 05/18/2018 Residual

48 M IND Indianapolis 3,889,567 Residual Yes A 5 12/31/2015 Residual

49 M CMH Columbus 3,312,496 HP Hybrid Yes A 10 12/31/2019 Yes

50 M MKE Milwaukee 3,229,876 MW/F9/NW Residual Yes A 5 12/31/2015 Residual

51 M OGG Kahului 3,220,753 Hybrid Yes A m/m m/m Yes

52 M PBI West Palm Beach 3,113,485 Hybrid Yes A 13 09/30/2019 Yes

53 M CVG Cincinnati 3,036,697 DL Hybrid Yes A 5? 12/31/2020 Yes

54 M BDL Hartford 2,926,047 Compensatory Yes A 5 06/30/2020 Yes

55 M JAX Jacksonville 2,716,465 Residual Yes A 5 6/30/2017 Residual

56 M ANC Anchorage 2,525,876 Residual Yes A 10 06/30/2023 Residual

57 M BUF Buffalo 2,331,545 Compensatory Yes A 5 3/31/2019 No

58 M ABQ Albuquerque 2,323,850 Hybrid Yes A 5 06/30/2016 Yes

59 M ONT Ontario 2,089,781 Residual Yes A 25 2024 Residual

60 M OMA Omaha 2,046,155 Compensatory Yes O 1 12/31/2016 No

61 S OKC Oklahoma City 1,803,159 Compensatory Yes A 5 12/31/2018 No

10 Residual Airport-wide residual calculation, or multi-cost center residual Form

9 Compensatory Airport keeps nonairline revenues without sharing Ordinance 6

12 Hybrid Compensatory with revenue sharing, and other features Agreement 25

31 31

Source: LeighFisher, November 2016.

15 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Summary of Airline Business Relationships – Large and Medium Hubs

Source: LeighFisher, November 2016.

Large Hubs Medium Hubs Total

Metric Number Percent Number Percent Number Percent

Methodology

Residual 8 27% 10 32% 18 30%

Compensatory 11 37% 9 29% 20 33%

Hybrid 11 37% 12 39% 23 38%

30 100% 31 100% 61 100%

Form of Agreement

Ordinance 4 13% 6 19% 10 16%

Agreement 26 87% 25 81% 51 84%

30 100% 31 100% 61 100%

Trend away from residual systems as airports operate more like businesses

Blurring of distinctions between traditional rate-making approaches with significant number of hybrid approaches

16 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airline Business Relationships – Small Hubs

RankHub

SizeLocid City

CY 15

EnplanementsAirfield Terminal

Revenue

Shairing

Airline

Agreement

or Rate

Ordinance

61 S BUR Burbank 1,973,869 Airport Residual Fixed (CPI adj) Residual AUA

62 S MEM Memphis 1,873,714 CCR CCR Yes AUA

63 S OKC Oklahoma City 1,803,159 CCR Comp No

64 S PVD Providence 1,763,672 Comp CC No AUA

65 S RIC Richmond 1,740,380

66 S CHS Charleston 1,669,960 Fixed CC No Ordinance

67 S RNO Reno 1,669,863 CCR CC Yes

68 S SDF Louisville 1,640,287 CCR CCR No AUA

69 S TUS Tucson 1,549,114 Airport Residual Fixed (CPI adj) Residual

70 S GEG Spokane 1,515,349 Airport Residual CCR Residual AUA

71 S ORF Norfolk 1,515,198 CCR Comp Yes AUA

72 S BOI Boise 1,487,764 CCR CCR

73 S KOA Kailua Kona 1,485,777 CCR CCR Yes AUA

74 S GUM Tamuning 1,420,500 Airport Residual Comp Residual AUA

75 S LIH Lihue 1,399,528 CCR CCR Yes AUA

76 S ELP El Paso 1,381,367 CCR CCR

77 S TUL Tulsa 1,359,562 CCR CC Yes AUA

78 S BHM Birmingham 1,325,891

79 S GRR Grand Rapids 1,280,801 Comp CC No Ordinance

80 S ALB Albany 1,276,743 CCR CC 50/50 sharing AUA

81 S LGB Long Beach 1,220,906 Ordinance

82 S ROC Rochester 1,177,983 CCR CCR AUA

83 S SFB Sanford 1,174,158

84 S DSM Des Moines 1,156,450 CCR CC No Ordinance

85 S DAY Dayton 1,041,731

86 S MHT Manchester 1,026,342 Comp Comp AUA

87 S SYR Syracuse 987,640

88 S SAV Savannah 980,531

89 S LIT Little Rock 958,510 CCR CC Yes Ordinance

90 S GSP Greenville Spartanburg 955,097

91 S PSP Palm Springs 947,713

92 S MYR Myrtle Beach 899,855

93 S PWM Portland 858,449

94 S TYS Tyson 848,390

95 S GSO Greensboro 848,249 CCR CC Yes AUA

96 S MSN Madison 826,640 Comp CC Yes AUA

97 S PIE Clearwater 819,962

17 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airline Business Relationships – Small Hubs (continued)

RankHub

SizeLocid City

CY 15

EnplanementsAirfield Terminal

Revenue

Shairing

Airline

Agreement

or Rate

Ordinance

98 S CAK Akron 787,901

99 S PNS Pensacola 787,901

100 S ICT Wichita 773,526 CCR Comp Yes AUA

101 S HPN White Plains 757,424

102 S STT Charlotte Amalie 706,098

103 S FAT Fresno 694,994

104 S IWA Mesa 666,168

105 S XNA Bentonville 629,903 CCR CC No Ordinance

106 S ITO Hilo 627,171 CCR CCR Yes AUA

107 S SRQ Sarasota 607,428

108 S LEX Lexington 606,977 CCR CC Yes Ordinance

109 S ISP Islip 603,641

110 S COS Colorado Springs 593,217

111 S ACY Atlantic City 587,967

112 S MDT Harrisburg 587,047 CCR Fixed Yes AUA

113 S BTV Burlington 581,141

114 S CID Cedar Rapids 557,374 Comp Comp No AUA

115 S CAE Columbia 533,575

116 S HSV Huntsville 519,785

117 S MAF Midland 518,496

118 S BZN Bozeman 512,029

119 S JAN Jackson 497,042

120 S FSD Sioux Falls 493,520

121 S FAI Fairbanks 493,443

122 S GSN Saipan 455,232

123 S SGF Springfield 447,843

124 S EUG Eugene 447,803

125 S BLI Bellingham 447,691

126 S LBB Lubbock 443,230

127 S FAR Fargo 437,098

128 S ECP Panama City 428,704

129 S PGD Punta Gorda 421,157

130 S BIL Billings 420,422

131 S GCN Grand Canyon 419,538

132 S FNT Flint 411,763

18 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Examples of Recently Negotiated Airline Agreements 11 of 35 Retained Residual Regime; Shorter Terms

Residual 34%

Hybrid

Compensatory

Residual

Airport City

Hub

Size

AUA/

Reso Ratemaking

Term/

years Effective

MSP Minneapolis L AUA Retained hybrid 10 1/1/2011

DFW Dallas L AUA Full residual to hybrid 10 10/1/2010

LAS Las Vegas L AUA Retained residual 5+5 7/1/2010

SFO San Francisco L AUA Retained residual 10 7/1/2011

FLL Ft. Lauderdale L AUA Retained residual 5 10/1/2012

MDW Chicago-Midway L AUA Retained residual 15 1/1/2013

LAX Los Angeles L Reso Commercial compensatory, revenue sharing agreement 10 1/1/2013

DCA/IAD Washington, DC L AUA Retained hybrid (commercial compensatory w/ rev sharing, ECP) 10 1/1/2015

PHL Philadelphia L AUA Retained residual 2 7/1/2013

SEA Seattle L AUA Retained hybrid, rate resolution threatened 5 11/1/20131

MCO Orlando L Reso Commercial compensatory, revenue sharing agreement 3 11/1/2013

CLT Charlotte L AUA Retained hybrid (includes revenue sharing) 4 7/1/2012

SAN San Diego L AUA Commercial compensatory 5 7/1/2013

BWI Baltimore L AUA Commercial compensatory 5 7/1/2014

PDX Portland L AUA Retained hybrid (includes revenue sharing) 10 1/1/2015

SLC Salt Lake City L AUA Commercial compensatory w/ revenue sharing 10 7/1/2014

IND Indianapolis M AUA Retained residual 5 1/1/2010

JAX Jacksonville M AUA Retained residual 5 7/1/2012

MEM Memphis M AUA Retained residual, airlines can give back space annually 5 11/1/2012

ANC Anchorage M AUA Retained residual 10 7/1/2013

HOU Houston M AUA Commercial compensatory w/ revenue sharing ? 1/1/2013

OKC Oklahoma City M AUA Retained compensatory 5 1/1/2014

SLC Salt Lake City L AUA Retained hybrid 10 1/1/2014

MCI Kansas City M AUA Pure compensatory w/ airline maintenance surcharge 2 4/1/2014

CMH Columbus M AUA Commercial compensatory w/ revenue sharing 5 1/1/2015

BNA Nashville M AUA Full residual to hybrid 7 7/1/2015

TUL Tulsa S AUA Commercial compensatory w/ revenue sharing 5 7/1/2013

ORF Norfolk S AUA Compensatory w/ revenue sharing 5 7/1/2013

TUS Tucson S AUA Retained residual 3 10/1/2013

DSM Des Moines S Reso Hybrid to commercial compensatory 1 1/1/2014

MDT Harrisburg S AUA Fixed terminal rates w/ revenue sharing & ECP 5 1/1/2015

PBI Palm Beach, FL S AUA Commercial compensatory w/ revenue sharing 5 10/1/2014

ERI Erie N AUA Fixed terminal and landing fee rates, with ECP 4 1/1/2013

RAP Rapid City N Reso Compensatory for terminal, residual for airfield w/ revenue sharing 3 1/1/2015

GEG Spokane S AUA Retained residual 2 1/1/2016

Negotiation and Planning Process :

The “90/10” Rule

20 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Execution and Transition Airport Readiness and

Preparations for Agreement Execution of Agreement

“Operationalizing” Airport Obligations and Rights

Airline Engagement

Conceptual Airline Engagement Term Sheet Refinement in

Negotiations Lease Drafting and Refinement

in Negotiations

Planning Structuring, and Refining Airport

Strategies and Goals

Translating Goals into Negotiating Ranges and

Options Developing a Term Sheet

Airline Use and Lease Negotiation Process

21 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Developing a Capital Program is an Iterative Process

22 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Develop a Financial Model to Optimize the CIP Plan of Finance and Airline Ratemaking System

Capital Program Master Plan R&R Infrastructure Noise mitigation

Plan of Finance PFCs AIP/grants Internal funds Third party CFC Bond sizing

Debt Service Existing debt Short-term Long-term PFC-supported Amortization

M&O Expense Existing facilities Incremental/new

projects By cost center

Airline Revenues Terminal rents Baggage fees Landing fees Other

Non-Airline Revenues Parking Rental car Terminal

concessions Cargo Other

Capital Operating Financial Results Key Assumptions

Application of Revenues Cash flow Cash balances P&L by cost center

Debt Service Coverage Senior lien bonds Subordinate line bonds PFC bonds

Financial Targets Airline CPE Airline share of op revenues Debt service coverage Debt per enplanement Cash flow Liquidity (days cash on hand)

Traffic Space Occupancy Borrowing rates Investment rates Term of debt PFC eligibility PFC level CFC level Parking rates Inflation Staff levels Incremental O&M Sensitivity

analyses

Sensitivity Tests to evaluate risk tolerance

23 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Set Financial Targets for Your Airport

Source: Global Infrastructure & Project Finance Peer Study, Fitch Ratings, December 9, 2015.

2.98

1.58 1.541.68

1.93

1.54 1.53

1.89

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

ABC U.S. Hub Regional AA A Medium Small

Overview Traffic Profile Rating Category Hub Size

Debt Service Coverage

$8.40 $8.72

$9.45

$8.08

$9.95

$8.51 $8.99

$7.31

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

ABC U.S. Hub Regional AA A Medium Small

Overview Traffic Profile Rating Category Hub Size

Cost per Enplanement

384

449

683

451

688

451

525

400

0

100

200

300

400

500

600

700

ABC U.S. Hub Regional AA A Medium Small

Overview Traffic Profile Rating Category Hub Size

Days Cash on Hand

$16.25

$78.00

$130.00

$66.00

$113.00

$76.00

$65.00 $68.00

$0

$20

$40

$60

$80

$100

$120

$140

ABC U.S. Hub Regional AA A Medium Small

Overview Traffic Profile Rating Category Hub Size

Debt per Enplaned Passenger

24 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

What Happens When You Don’t Set Targets

25 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

1. Term

2. Signatory Airlines - Affiliates, cargo carriers

- Minimum requirements to become signatory

3. Airline Premises - Exclusive, preferential, joint, and common use

- Preferential use conditions (use it or lose it, sharing, RON parking)

- Equalized gates (a gate is a gate)

4. Cost Centers

5. Rentals, Fees, and Charges - Specific rates and ratemaking methodology

- Rate base (amortization, debt service coverage)

- Common use formula

- Per-turn fees

- Revenue sharing/extraordinary coverage protection

- Non-signatory rates

6. Capital Improvement Consultation (vs. MII)

7. Legal Boilerplate (modernize)

Start With a Term Sheet

Trends in Airline Lease Negotiations

27 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 1. Business Relationship

Increasing number of airports setting rates by resolution

Move away from long-term leases (10 years or longer) -- an area of mutual agreement between both airports and airlines

Airline consortiums to manage airline equipment (e.g., ORD, SFO, DTW, MDW, MIA)

Source: ACI-NA, 2015 Business Terms Survey, October 2015 (based upon 62 responses).

28 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 2. Airport-wide Ratemaking Methodology

Move away from residual cost rate-making toward compensatory and hybrid methods with revenue sharing?

23% 24%

53%

29%

20%

51%

0%

10%

20%

30%

40%

50%

60%

Residual Compensatory Hybrid

U.S. Airport Ratemaking Methodology

2003 2015

Source: ACI-NA, 2015 Business Terms Survey, October 2015 (based upon 96 responses for 2003 and 70 for 2015).

29 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 3. Landing Fee and Terminal Ratemaking Methodology (2015)

Source: ACI-NA, 2015 Business Terms Survey for 2015, October 2015.

30 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 4. Common Use Holdroom and Bag Claim Charges (2015)

Move away from 20/80 common use formulas (per capita/passengers) to no or lower per capita allocation and combination of passengers and operations

Source: ACI-NA, 2015 Business Terms Survey for 2015, October 2015.

31 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 5. Other Common Use Space Charges

Offering of per-turn fees for low frequency airlines that do not want to lease space/gates

Response from FAA to industry requests on per-turn fees

Establishing cost recovery security fees (security checkpoint, bag screening space, etc.)

Source: Fees, Rates, and Charges, Pittsburgh International Airport, January 1, 2016.

32 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 6. MII Clauses

Move away from restrictive Majority-in-Interest (MII) provisions

Move towards less stringent MII clauses

Source: ACI-NA, 2015 Business Terms Survey, October 2015 (based upon 101 responses for 2003 and 62 for 2015).

49% 51%

58%

42%

0%

10%

20%

30%

40%

50%

60%

70%

MII No MII

U.S. Airport MII Clauses

2003 2015

Type of MII (2015)

33 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

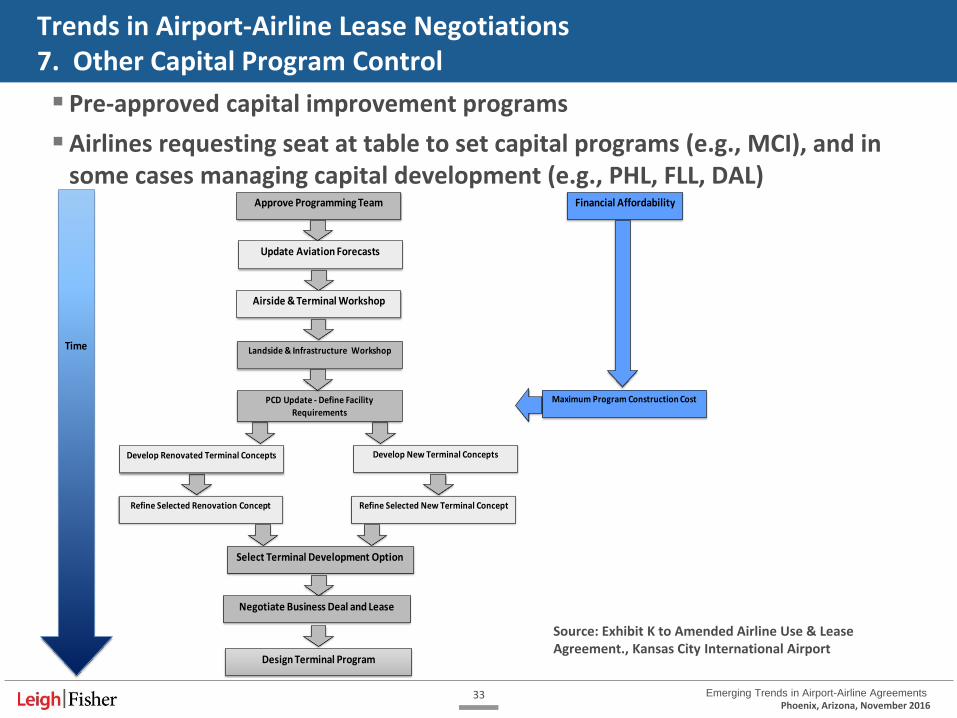

Source: Exhibit K to Amended Airline Use & Lease Agreement., Kansas City International Airport

Approve Programming Team

Update Aviation Forecasts

Airside & Terminal Workshop

Landside & Infrastructure Workshop

Develop Renovated Terminal Concepts Develop New Terminal Concepts

Refine Selected New Terminal ConceptRefine Selected Renovation Concept

Select Terminal Development Option

Negotiate Business Deal and Lease

Design Terminal Program

Financial Affordability

Maximum Program Construction Cost

Time

PCD Update - Define Facility

Requirements

Pre-approved capital improvement programs

Airlines requesting seat at table to set capital programs (e.g., MCI), and in some cases managing capital development (e.g., PHL, FLL, DAL)

Trends in Airport-Airline Lease Negotiations 7. Other Capital Program Control

34 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 8. Facility Control

Move away from exclusive use to preferential and common use space/gates

More common use systems, including outbound baggage systems

Preserving the flexibility to reallocate or reassign exclusive use space to accommodate changing mix of airlines and market shares

Airlines “right-sizing” (returning space after bankruptcies, mergers, lease renewals)

35 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Trends in Airport-Airline Lease Negotiations 9. Other Provisions/Trends

Modernize legal boilerplate (environmental, insurance, indemnification)

Stronger payment and security features (bankruptcy protection)

FAA considering revisions to Rates & Charges Policy

Source: FAA, Feedback from Policy Regarding Airports Rates and Charges Listening Sessions, April 17, 2014.

Per-Turn Fees: Regulatory Basis and Calculations

37 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

The only reference in the Rates and Charges Policy is: – 1.1.3 Airport proprietors should consider the public interest in establishing airport fees, and

aeronautical users should consider the public interest in consulting with airports on setting such fees

USDOT’s statutory responsibilities include: – Ensure… "the availability of a variety of … low-priced services without unreasonable

discrimination or unfair or deceptive practices (49 U.S.C. § 40101(a)(5)) – “Encourage[ing] entry …by new and existing air carriers and …strengthening of small air

carriers to ensure a more …competitive airline industry" (49 U.S.C. § 40101(a)(13))

Under airport competition plans, the USDOT encourages airports to retain common use gates for new entrants and expanding incumbents

Regulatory Basis for Per-Turn Fees

Little guidance under the USDOT Rates and Charges Policy for per-turn fees

“It is the fundamental position of the Department that the issue of rates and charges is best

addressed at the local level by agreement between users and airports…

“Airport proprietors and aeronautical users should consult and make a good-faith effort to reach

agreement. Absent agreement, airport proprietors are free to act in accordance with their

proposals, subject to review by the Secretary or the Administrator on complaint by the user . . ..” - U.S. DOT Policy Concerning Airport Rates and Charges, Introduction and Section 1.1.4

38 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Why is This an Issue?

Due to airline industry consolidation, smaller airports have little negotiating leverage; they need to retain existing and attract new service

Some network airlines are pushing for regimes that price the less-than-daily airlines out of the smaller markets, which is contrary to the “public interest” and the desire to have healthy competition

Low frequency airlines can’t afford to lease full ticket/gate modules

Setting a per-turn fee at a reasonable level, and adjusting as necessary:

― Promotes competition and fosters an encouraging environment for variety of business models and new entrants

― Accomplishes the airport’s obligation to serve the public (both airlines and travelers)

― Provides an airport with the means to remain financially self-sufficient

Alternatively, if the topic is approached from the reverse…

― If an airport does NOT maintain a reasonable per turn fee, it could be considered unjustly discriminatory - a de facto exclusion of low-frequency carriers from the market

Recent/future changes to the US airline structure give smaller communities fewer options

39 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

1. “Arbitrarily” discriminating based on differential rates by concourse 2. Basing per-turn fees on unreasonable usage assumptions - 8 turns per gate per day 3. Offering per-turn fee to some airlines, but not others 4. Disproportionately shifting costs to signatory airlines by not including a fixed fee

component in their common use space allocation methodology 5. Imposing or threatening to impose ordinance rates is not good faith negotiations

What is A4A Saying?

A number of airports have “gone off reservation” – some airports are:

40 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Objectives for Per-Turn Fees

Offer competitive rates to attract and/or retain air service

1. Daily, low-frequency service

2. Less-than-daily service

3. Seasonal service

4. Charters

Avoid giving an incentive to signatory airlines to give back space

Provide a transparent and defensible policy that is reasonable and not unjustly discriminatory

Retain flexibility to apply to all airline business models

― Overflow activity for signatory airlines

― Low volume carriers

41 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Source: Airline Operating and Use Agreement, Des Moines International Airport.

Types of Terminal Space/Per-Turn Fee (ticket, common baggage, gates)

Ticketing/Queue, Baggage Systems, Gates (Holdrooms, Loading Bridges, Aircraft Apron)

Ticket Counters/Queue

Passenger Screening

Baggage Screening Inbound Baggage/ Baggage Claim

Gates = Holdrooms/ Loading Bridges/ Aircraft Parking

42 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Methodologies to Allocate Common / Joint Use Space

Units

― Passengers

― Operations

― Fixed or per capita

― Bags

― Time of use

Formulas

― Passengers / fixed (split equally among users)

80/20, 90/10, 85/15

― 100% passengers

― Passengers / operations – 50/50, 70/30

― Passengers / operations / fixed – 35/55/10

― Bags

Issues

― Turns per day

― Premium for non-signatories

― Limiting per-turn fee option to airlines flying less than [x] flights per week

Carve-outs/exceptions

― Affiliates

― Low volume carriers (e.g., 2% - 5% of passenger market share)

43 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Calculation Methodologies in General

Not all airports have formula-driven methodologies for setting per turn fees

A methodology is preferred, and helps an airport provide reasonable, transparent, and defensible fees; additionally, a fee set according to a methodology can be adjusted over time as other rates and charges are adjusted

Methodologies in the airport industry for setting per turn fees vary widely, but in our experience methods that are reasonable, transparent, and defensible generally fall into two categories

― Method A – Calculated using average cost, size, and operations at a typical gate

― Method B – Calculated using imputed average per turn cost for traditional carriers

The method for charging for joint use space is an important consideration when establishing the per turn fee

― Joint use space can be included in a bundled per turn fee and charged 100% on the basis of operations, or

― Joint use space can be separately charged under established methodology, or

― A separate passenger fee can be calculated to recover joint use costs

44 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Per-Turn Fees at Other Airports

Method A – Calculated using average cost, size, and operations at a typical gate

― TUL, CVG, PHX, LAX, and SEA

― Methods may include an explicit premium (CVG 1.25x) or implicit premium (TUL 3 turns per gate divisor)

― Per-turn fee could be completely “bundled” (inclusive of all terminal fees) or joint use fees could be charged separately (using 100/0 or other methods)

― Per-turn fees could be weighted for aircraft size, especially in situations where a “bundled” rate is charged (LAX fees range from 0.75x to 3.00x; SEA fees range from 0.50x to 2.00x)

Method B – Calculated using imputed average per turn cost for traditional carriers

― LEX determines the average signatory terminal cost per turn and then multiplies the average by a 1.6x premium to calculate the non-signatory per turn fee; the rate is “bundled” and joint use costs are included in the per-turn fee; the 1.6x premium is in recognition of non-signatory status and differences in aircraft size

Method C – Some airports charge a “market rate” per turn, which is annually adjusted for inflation (MDT)

45 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

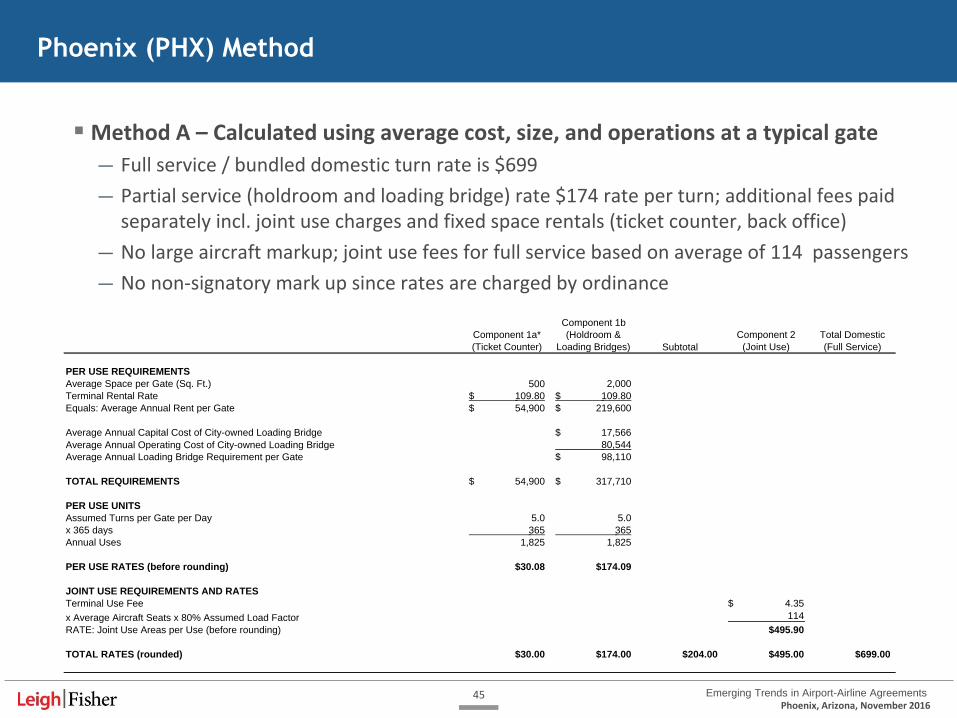

Phoenix (PHX) Method

Component 1b

Component 1a*

(Ticket Counter)

(Holdroom &

Loading Bridges) Subtotal

Component 2

(Joint Use)

Total Domestic

(Full Service)

PER USE REQUIREMENTS

Average Space per Gate (Sq. Ft.) 500 2,000

Terminal Rental Rate 109.80$ 109.80$

Equals: Average Annual Rent per Gate 54,900$ 219,600$

Average Annual Capital Cost of City-owned Loading Bridge 17,566$

Average Annual Operating Cost of City-owned Loading Bridge 80,544

Average Annual Loading Bridge Requirement per Gate 98,110$

TOTAL REQUIREMENTS 54,900$ 317,710$

PER USE UNITS

Assumed Turns per Gate per Day 5.0 5.0

x 365 days 365 365

Annual Uses 1,825 1,825

PER USE RATES (before rounding) $30.08 $174.09

JOINT USE REQUIREMENTS AND RATES

Terminal Use Fee 4.35$

x Average Aircraft Seats x 80% Assumed Load Factor 114

RATE: Joint Use Areas per Use (before rounding) $495.90

TOTAL RATES (rounded) $30.00 $174.00 $204.00 $495.00 $699.00

Method A – Calculated using average cost, size, and operations at a typical gate

― Full service / bundled domestic turn rate is $699

― Partial service (holdroom and loading bridge) rate $174 rate per turn; additional fees paid separately incl. joint use charges and fixed space rentals (ticket counter, back office)

― No large aircraft markup; joint use fees for full service based on average of 114 passengers

― No non-signatory mark up since rates are charged by ordinance

46 Emerging Trends in Airport-Airline Agreements Phoenix, Arizona, November 2016

Lexington (LEX) Method

Method B – Calculated using imputed average per turn cost for traditional carriers ― LEX offers a rate structure where carriers can elect to pay a “Per Turn Fee” or lease space

exclusively/preferentially in the traditional manner

― The Per Turn Fee rate is based on airport-wide average cost per turn with a premium multiplier

― It’s intended to reduce costs for low-frequency operators so as not to discourage even minimal amounts of air service, but yet become disadvantageous once a carrier reaches a certain level so that they move back to paying traditional rentals

Airline Code

Number of

Gates

Excl. and

Pref. Rent

Common Use

Rent Total Rent Annual Turns

Total Rent

per Turn

Reference Exhibit 7.0 Exhibit 7.0 Exhibit 5.0

American AA 1 357,614 378,676 736,290 1,830 402.34

Delta DL 2 608,381 1,113,442 1,721,823 4,553 378.17

United UA 2 186,522 300,824 487,346 1,653 294.82

US Airways US 1 139,496 530,184 669,680 2,928 228.72

Total 6 1,292,013$ 2,323,125$ 3,615,139$ 10,964 329.73$

Average (AA, DL, UA, US) 329.73$

Per Turn Fee Premium 1.50

Calculated Per Turn Fee (rounded) 500.00$

www.leighfisher.com Sheri Ernico LeighFisher 555 Airport Boulevard, Suite 300 Burlingame, CA. 20190 (650) 593-3003 [email protected]